Investigating the Impact of Blockchain Technology on Social Sustainability and the Mediating Role of Ethics and CSR

College of Communication and Media, Al Ain University, Abu Dhabi P.O. Box 112612, United Arab Emirates

Sustainability 2023, 15(21), 15510; https://doi.org/10.3390/su152115510

Submission received: 2 September 2023

/

Revised: 21 October 2023

/

Accepted: 26 October 2023

/

Published: 1 November 2023

(This article belongs to the Section Economic and Business Aspects of Sustainability)

Abstract

:The main aim of this study was to investigate the impact of blockchain technology, business ethics, and corporate social responsibility (CSR) on social sustainability. Additionally, this study sought to explore how CSR and business ethics serve as mediators in shaping these impacts. This study collected data from employees in the banking sector in the United Arab Emirates (UAE), using a purposive sampling technique. A cross-sectional research design was employed, and a questionnaire was developed to gather responses from 416 participants. The usable response rate was 62.67%. This study utilized structural equation modeling (SEM) with SmartPLS as a tool to analyze the data. The results of this study indicate that blockchain technology has a positive influence on CSR, business ethics, and social sustainability. Additionally, CSR and business ethics have a positive effect on social sustainability. This study confirms the mediating role of business ethics and CSR. These findings can be useful for bank officials and academic decisionmakers in developing strategies.

1. Introduction

Currently, numerous data structures are being utilized, and one of these is blockchain technology, which is a distributed and decentralized data structure. This technology allows for data to be shared through open access and peer-to-peer networks. However, transactions executed using blockchain technology must undergo verification and certification by the network’s community [1]. The blockchain was first introduced to the financial industry as a cryptocurrency, with the main goal of replacing manual authentication with digital authentication [2].

The use of blockchain technology can enhance the security, immutability, trust, transparency, and traceability of data, making it a subject of interest for professionals and academicians across various industries [3]. As a result, investments in blockchain solutions from different industries are increasing over time, with an expected investment of around USD 176 billion. Blockchain technology has several capabilities, including promoting environmental, social, and economic sustainability in the manufacturing industry. Given the numerous benefits of utilizing blockchain technology in the manufacturing sector, investments in blockchain solutions for this industry are currently on the rise [4].

Various studies have delved into the concept of business, describing it as a collaborative effort of individuals aimed at organizing the social and ethical aspects of communal life. To comprehend the ethical and social implications of modern organizations, it is crucial to examine their structural, economic, political, and social dimensions [5]. Therefore, conducting business in an ethical manner is vital for organizations. At the micro level, business ethics involves human capabilities, motivations, and needs. The primary goal of an organization is to provide value to its stakeholders, thereby creating value for the organization [6]. While profitability is an important aspect of business, it is not the sole objective. Organizations are expected to engage in social welfare activities that may impact their operational environment. A code of conduct is typically established and enforced within organizations, with business ethics serving as the guiding principle. Although such codes are often developed voluntarily, governments may also impose them through legislation [7]. The practice of business ethics can greatly influence an organization’s public perception and therefore serve as a foundation for its success [8].

In the current dynamic global market, it is imperative for organizations to establish and maintain a positive image while balancing environmental preservation, public welfare, and profits [9]. Adapting strategies to changing societal values and globalization is essential for an organization’s successful operation, and developing partnerships with stakeholders is necessary for long-term sustainable development [10]. Thus, organizations must embrace social responsibility to meet these requirements. Implementation and application of corporate social responsibility (CSR) are highly encouraged in the modern business environment, as they promote transparency in environmental protection and public welfare [11]. Furthermore, following business ethics is also critical to promoting the positive image of banks among stakeholders [12].

Social challenges, in particular, have a significant impact on organizational planning and practices, and addressing them is therefore crucial to achieving sustainability [13]. For the banking sector, social sustainability is one of the major challenges, as it has role to play in engaging the community in which banks operate. Basically, social sustainability is a process of creating sustainable successful places that promote wellbeing by understanding what people need from the places they live and work [14]. In addition, Woodcraft [15] noted that a recent trend in the conversation about sustainable development is social sustainability. It has evolved over a few years in reaction to the predominance of technology and environmental concerns in urban development and the lack of progress in addressing social issues in cities including inequality, eviction, livability, and the growing demand for cheap housing. The social aspects of sustainability have been generally disregarded in discussions, policy, and practice around sustainable urbanism, despite the sustainable communities policy agenda having been adopted in the UK a decade ago. But things are starting to shift. Understanding and assessing the social effects of urban growth and regeneration are becoming more and more important both in the UK and elsewhere. A modest but expanding movement of city planners, architects, builders, housing organizations, and local governments promotes a more “social” method of creating and running cities. This is a part of a growing global interest in social sustainability, which is being used by governments, public institutions, decisionmakers, NGOs, and businesses to frame choices about housing, urban renewal, and development as part of a growing policy discourse on the resilience and sustainability of cities.

Furthermore, meeting society’s ethics and norms is also important for banks. The present study aims to investigate the impact of blockchain technology, corporate social responsibility (CSR), and business ethics on social sustainability in the context of UAE banks, while also examining the mediating role of corporate social responsibility (CSR) and business ethics, as the mediations are rarely tested simultaneously. The importance of sustainability in the success of global organizations cannot be overstated, as it is a critical challenge faced by organizations, encompassing social, environmental, and economic factors. It is important for the banking sector to focus on factors that can improve the social sustainability of banks. Improving the reputation of and trust in banks has long-term impact. Moreover, employee engagement is positively affected on a long-run basis. Therefore, it is key for banks to assess the impact of factors like blockchain technology, corporate social responsibility (CSR), and business ethics on social sustainability.

2. Review of Literature

2.1. Blockchain Technology

Blockchain is an immutable, shared ledger that helps in the facilitation of the process of tracking and recording a transaction’s assets in business networks. There are two types of assets, namely, intangible and tangible assets. Tangible assets include land, cash, cars, property, and many others [16]. Branding copyrights, patents, and intellectual property are examples of intangible assets. Likewise, there are many examples of blockchain technology. One of the famous examples of blockchain technology is bitcoin, which hosts a digital ledger [17]. Like bitcoin, other blockchain technologies also provide a platform to trade, store, and mine digital currency. This process involves a very complex algorithm that is based on a computer and is tied through a network that is distributed. There are many other uses of blockchain technologies aside from usage for transactions. Researchers have mentioned that it can be considered as an inventory and registry for all assets. The transactions that are recorded in one block are considered to take place at the same time. There is linkage among the blocks in the form of chains like a linear as well as chronological order. Regarding this technology, each block has the hash of the previous block [18].

In the literature, the social aspect of blockchain technology has also been discussed. It has role to play in terms of tracking carbon emissions in society [19]. Thus, it can control and mitigate environmental concerns. In terms of trading, it can promote fair trading as well. On the other hand, crisis and humanitarian issues can be handled effectively with the help of blockchain technology [20].

2.2. Business Ethics

Ethics is primarily concerned with promoting good behavior, and scholars have put forth various definitions of this concept. According to Sroka and Szántó [21], ethics can be understood as a developmental concept, whereas morality is concerned with making judgments on what is right and wrong [22]. It is pertinent to mention that morality involves regulations, practices regarding codes, and a list of rules, which include prohibitions against actions that may cause harm to others. In this respect, scholars have noted that ethics are a set of desirable values that aid individuals in performing actions that are deemed good. Cherré, Laarraf [23], therefore, defined ethics as “the study of business situations, activities, and decisions where issues of right and wrong are addressed”. These ethical considerations are critical in ensuring organizational operations are consistent with the law. Stakeholders hold an organization in high esteem if its operations conform to national or local laws [24]. Such a favorable reputation among customers and prospective clients enables the organization to run smoothly [25]. Ethical operations can also aid in the attraction of potential clients and employees. Job seekers are drawn to organizations that demonstrate ethical treatment and care for their employees. Moreover, employee performance can improve in organizations that prioritize ethical conduct towards their workforce [23].

Ethical behavior is essential for fostering trust among employees, clients, and the organization. It is also crucial in building trust between the organization and its stakeholders. When an organization treats its stakeholders ethically, it generates positive word-of-mouth and encourages repeat business, thereby increasing repurchase intention and elevating the quality of the brand [26].

2.3. Corporate Social Responsibility (CSR)

According to research, CSR is a multifaceted construct that comprises four key factors: philanthropic, ethical, legal, and economic. These factors are typically represented as a pyramid, and it is suggested that they should be fulfilled in a parallel manner. CSR involves aligning an organization’s business with the values and behavior expected by stakeholders, including investors, customers, society as a whole, special interest groups, communities, suppliers, and employees [27]. These values are critical to building trust and maintaining positive relationships with stakeholders, which are essential for the long-term success and sustainability of an organization [28].

CSR refers to the responsibility of an organization towards its stakeholders. This concept entails that organizations should adopt and manage activities that have minimal negative impacts on the environment, society, and the economy, while maximizing the benefits. CSR is a business concept that aims to have a positive impact on society over the long term, and as such, it requires a commitment from managers to behave responsibly, fairly, and ethically. Furthermore, CSR also involves contributing to the economic wellbeing of employees, their families, and the community as a whole [29].

2.4. Social Sustainability

Social sustainability involves the management and identification of businesses that have both positive and negative impacts on individuals. Prior research has described social sustainability as a process and condition that can enhance the quality of life in a community. In addition, authors have emphasized the distribution of quality of life both presently and in the future as an important aspect of social sustainability [30]. Scholars have defined social sustainability as the development of a harmonious evolution within civil society that is conducive to compatible cohabitation with the environment and culture. This development should drive groups that encourage social integration and improve the quality of life for all population segments. The previous literature has regarded social infrastructure as a critical link that affects the potential for sustainable social development [31].

The wellbeing and quality of life of a community are dependent on the opinions, objectives, and needs of its members. Objective and subjective assessments, as well as their combination, play a significant role in disclosing the individual perspective of the community’s behavior towards achieving a better life and enhancing social infrastructure. To accurately reflect the current situation, subjective opinions are essential [32].

3. Hypotheses Development

Blockchain Technology and Business Ethics

The utilization of blockchain technology has a significant impact on the way people interact with organizations. The distinctive features of blockchain technology, particularly immutability, play a crucial role in shaping this interaction. Immutability significantly reduces the decision-making power of individuals, leading to better control over business transactions [33]. It also restricts personal use, fraud, distortion, and information theft. Blockchain technology, therefore, ensures transparency in business processes and enforces ethical codes of responsibility, consideration, and honesty, resulting in more accurate tracking of asset valuations and executive services. Moreover, the technology’s transparency and accessibility to information align with the principles of citizenship and human rights [34].

Academics have noted that blockchain technology has an impact on ethical challenges, as it involves the creation of secure networks through data-driven processes. Compliance with community and blockchain regulations and rules is crucial in the context of blockchain technology [35]. Numerous prior studies have examined the relationship between ethics and blockchain technology, with researchers asserting that the accounting and finance sector is particularly susceptible to ethics stemming from blockchain technology [36,37,38]. Therefore, it is essential that all stakeholders possess an understanding of ethical challenges, while also acknowledging the benefits of utilizing blockchain technology [39]. Moreover, ethical values must be taken into consideration by blockchain technology, and applications based on a blockchain must comply with ethical principles. Thus, blockchain applications must conform to ethical regulations. Based on previous research, it has also been observed that the effectiveness of a blockchain can be improved by adopting ethical behaviors and promoting human interaction in business and organizational settings [40]. The studies conducted by [41,42] reported a relationship between blockchain technology and business ethics.

H1.

Use of blockchain technology is positively related to the ethical conduct of a business operation.

4. Blockchain Technology and CSR

Blockchain technology reduces the cost of online transactions while introducing a trust mechanism and rebuilding the incentive mechanism to enhance organizational synergy [43]. Trust within the organization can help individuals and the organization avoid economic losses through knowledge sharing, thereby establishing a synergy relationship through blockchain technology [38]. This relationship is established through constructs and nodes, rules of participation, and the incentive mechanism, thereby realizing the potential of blockchain technology to rethink organizational business processes without the involvement of a central party [44].

Moreover, blockchain technology can increase CSR initiatives by increasing clarity and transparency. CSR initiatives create opportunities for innovation within organizations, and researchers have proposed that the adoption of technology, such as blockchain, can improve CSR practices. Stakeholders must ensure that the organization fulfills its promises regarding CSR performance, and CSR technology can play a crucial role in this regard. By adopting blockchain technology, organizations can easily implement CSR initiatives [43,45]. The research by [46] revealed a positive association between social responsibility, sustainability, and blockchain technology.

H2.

Blockchain technology has a positive impact on CSR.

H3.

Blockchain technology has a positive impact on social sustainability.

4.1. Business Ethics and Social Sustainability

Business ethics provide essential frameworks for evaluating managerial performance, with a focus on sustainable behavior and other related perspectives. Researchers have reported a positive impact of ethics on corporate social responsibility (CSR) activities, with Ferrell, Harrison [12] finding a positive relationship between social responsibility and business ethics across four different scenarios [47]. In this regard, scholars contend that business ethics is crucial to implementing sustainability at the social level [48]. Business ethics play a critical role in engaging policymakers, business decisionmakers, and society, ultimately leading to sustainable outcomes for both business and society. Transparent communication technology and information by organizations can aid in achieving societal sustainability [49].

H4.

Business Ethics have a positive impact on social sustainability.

4.2. CSR and Social Sustainability

Corporate social responsibility (CSR) is commonly defined as an organization’s commitment to promoting social and environmental sustainability. Some organizations prioritize investing in CSR initiatives as a means of enhancing their reputation and ensuring long-term profitability (Reference). Others view CSR as a societal obligation. Importantly, CSR is linked to the mitigation of negative environmental impacts and encompasses sustainability efforts that benefit the organization over the long term [50].

Organizations can leverage CSR as a strategic tool to gain a competitive advantage and achieve long-term financial success. CSR also plays a vital role in improving the lives of local communities by reducing conflict and fostering trust among stakeholders [51]. Moreover, CSR initiatives can facilitate sustainable growth by promoting employment, economic development, social advancement, and profitability [52]. Therefore, organizations should prioritize the use of CSR to enhance their performance and become sustainable entities [53]. The study by [54] reported a positive effect of CSR on social sustainability (see Figure 1). Therefore, we hypothesize that:

H5.

CSR has a positive impact on social sustainability.

H6.

Business ethics mediate the relationship between blockchain technology and social sustainability.

H7.

CSR mediates the relationship between blockchain technology and social sustainability.

5. Methodology

This study adopted a quantitative research approach and cross-sectional research design, keeping the study objectives in view. The model proposed in this study was tested within the banking sector of the UAE using a quantitative methodology to collect data from customers via field surveys. The study respondents were required to be over 18 years old, and the sampling method employed was purposive sampling, a type of nonprobability sampling [55]. Purposive sampling was selected due to its cost effectiveness, simplicity, and ease of data collection, and is commonly used when identifying problems regarding a target market [56]. This sampling approach is similar to that employed in a previous study by Abu Zayyad, Obeidat [57], who also used the purposive sampling technique.

The study items were adapted from previous studies. The items of blockchain technology were adapted from Khan, Godil [58]; the items of business ethics were adapted from Blanco-González, Del-Castillo-Feito [59]; the items of CSR were adapted from Raza, Rather [60]; and the items of social sustainability were adapted from DUONG and HA [61]. These questionnaires were designed on a 5-point Likert scale ranging from 1 to 5. Overall, 416 questionnaires were distributed among employees of banks working in the UAE and 298 questionnaires were returned, with 262 deemed valid for data analysis, resulting in a usable response rate of 62.67%. The gathered data were assessed using SPSS for descriptive analysis and to obtain demographic details of the respondents and using PLS 3.3.9. This tool is more suitable when the proposed model is complex. In the present study, we tested two mediations. Thus, this tool was more suitable for analysis.

The characteristics of the respondents indicated that most of the respondents were male (67%) and married (56.7%). Additionally, 17% of the respondents held degrees below the bachelor’s level, 49% held a bachelor’s degree, and 33% held a master’s degree or higher. To assess common method variance (CMV), VIF was examined, as recommended by Kock [62], and the results are presented in Table 1, with all VIF values being less than 5.

Based on the VIF values in the Table 1, it seems that BE (1.005) and CSR (1.002) have very low multicollinearity with the other variables in the model, while SS (1.460) has a slightly higher but still acceptable level of multicollinearity. This means that the coefficients estimated for BE (2.750) and CSR (2.717) are relatively stable and can be interpreted without much concern for multicollinearity, while some caution might be needed when interpreting the coefficient for SS. If higher VIF values are encountered (typically above 5 or 10), it is a stronger indication of problematic multicollinearity that might require further investigation.

Later, descriptive analysis of this study was conducted. The details are mentioned in Table 2 of this study. Table 2 provides a descriptive analysis of four variables: BCT (3.233), CSR (3.857), BE (2.887), and SS (4.074). This analysis summarizes key statistical characteristics of these variables based on a sample of 262 datapoints. In addition, the Mean (average) column shows the arithmetic mean (average) of each variable. It represents the central tendency of the data, indicating the typical or average value. In addition, Std. Dev (standard deviation) column provides the standard deviation of BCT (0.861), CSR (0.933), BE (1.031), and SS (0.884). The standard deviation is a measure of the spread or variability of the datapoints around the mean. It quantifies how much individual datapoints deviate from the mean.

6. Results and Analysis

To measure the validity and reliability of the instrument and the research framework, partial least squares structural equation modeling (PLS-SEM) was used. However, for the analysis of data, a statistical tool, SmartPLS version 3.2.9, was used. PLS-SEM is a variance-based approach that is used to estimate parameters [63]. This study used PLS-SEM for several reasons, which are consistent with several past studies [64].

On the other hand, the present study adopts a prediction orientation and has the goal of examining the causal relationship between the independent variable and the dependent variable of the model. In the end, the model of the present study is complex, containing a mediating analysis; therefore, this study preferred to use SmartPLS. On the other hand, there are a few benefits to using SmartPLS [65]. It has a high level of statistical power. This means that it is more likely to examine the relationship among variables through PLS-SEM. Moreover, there is no sample size requirement in PLS-SEM [66]. Therefore, this study preferred to use SmartPLS PLS-SEM.

The measurement model was examined using PLS-SEM, which involved assessing the reliability and validity of the data collected, given the use of reflective measurement items. To ensure reliability and validity, item loading was examined, with a threshold of 0.70 or higher, as recommended by Sarstedt, Ringle [67]. In this study, all loadings exceeded the recommended threshold and were thus retained for further analysis.

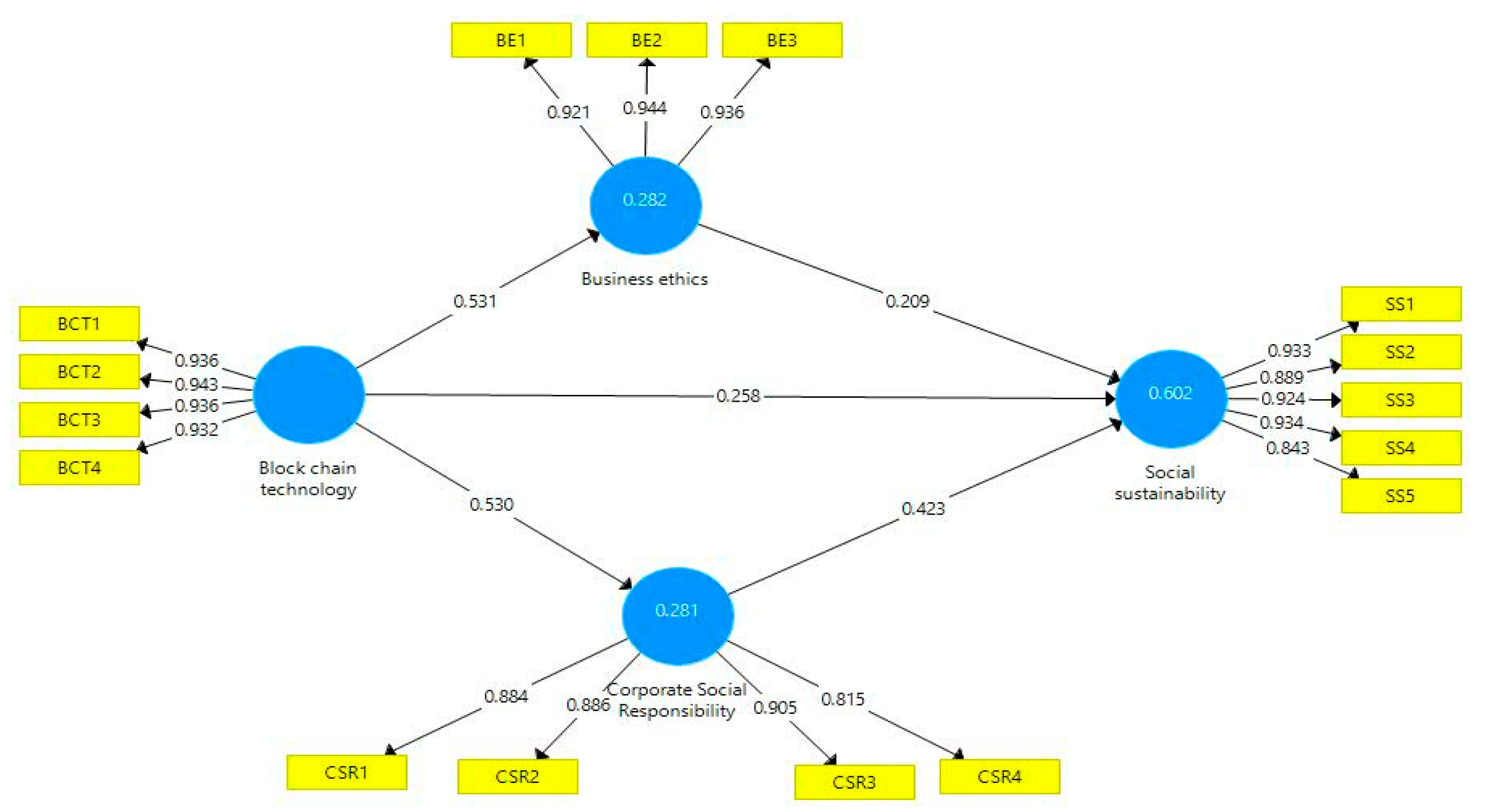

In conducting this study using PLS-SEM, the measurement model was examined, particularly the reflective measurement items. As such, the reliability and validity of the collected data were evaluated based on the loading of items. Sarstedt, Ringle [67] recommended a loading value of at least 0.70 for ensuring reliability and validity. The results, as shown in Figure 2 and Table 3, indicate that all loading values are above 0.70, thus supporting the retention of these items for further analysis. Furthermore, Fornell and Larcker [68] suggested that the average variance extracted (AVE) should be at least 0.50 to explain the variance of a study. The AVE values, as presented in Table 4, all exceed 0.50, further supporting this study’s validity. Finally, composite reliability (CR) was used to examine this study’s reliability, with CR values exceeding 0.70 being deemed acceptable.

The present study also evaluated discriminant validity, which refers to the extent to which one variable exhibits empirical difference from other variables. Two approaches were used to assess discriminant validity: Fornell and Larcker [68] and the HTMT approach. As shown in Table 5, the diagonal values of the matrix, which represent the square root of AVE, are greater than the remaining values, indicating good discriminant validity according to the Fornell and Larcker approach. Furthermore, all values in the matrix are less than 0.90, as per the criteria of the HTMT (see Table 6) approach and criteria suggested by Henseler, Ringle [69], confirming good discriminant validity.

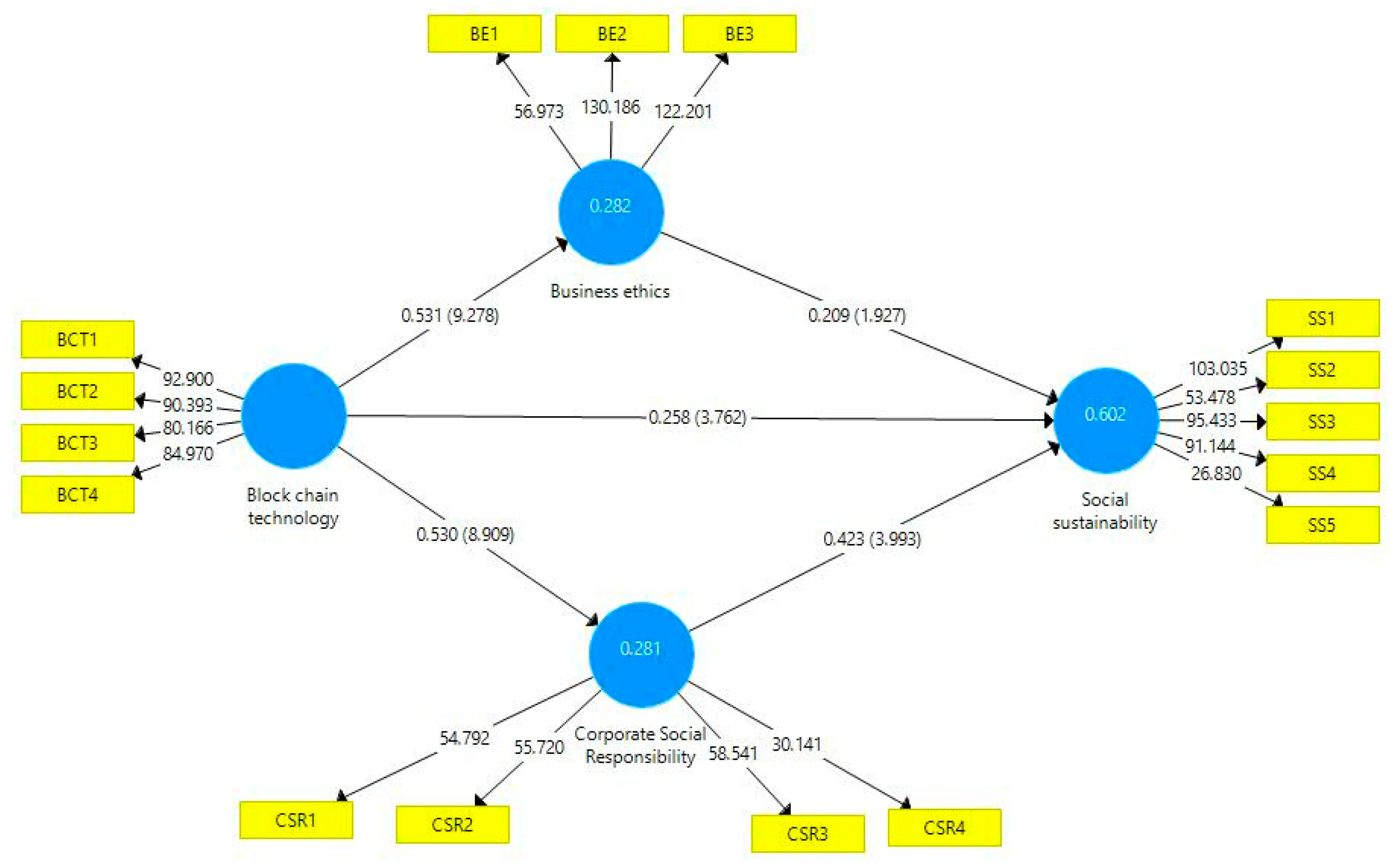

After assessing the discriminant validity, CR, AVE, and factor loading, the measurement model of this study was found to be satisfactory. The next step in using PLS-SEM is to evaluate the structural model [70], which involves testing the relationship between variables in the study. The level of significance for this study was set at 5%. The estimated values of path coefficients were then used to empirically support the direct and indirect hypotheses. The hypotheses of this study were accepted or rejected on the basis of t- (more than 1.67) and p-values.

The findings of this study indicate that H1 is supported (see Table 7), as blockchain technology has a significant effect on business ethics (beta = 0.531, t = 9.278). Similarly, blockchain technology has a significant positive effect on CSR (beta = 0.530, t = 8.909), supporting H2. Furthermore, H3 is supported, as blockchain technology has a significant positive effect on social sustainability (beta = 0.258, t = 3.762). Additionally, H4 is supported, as business ethics have a positive effect on social sustainability (beta = 0.209, t = 1.927). Finally, H5 is significant, as CSR has a positive relationship with social sustainability (beta = 0.423, t = 3.993).

Moreover, this study examined the mediating hypotheses. The results in Table 8 indicate that CSR significantly mediates the relationship between blockchain technology and social sustainability, supporting H6. Furthermore, H7 is also supported, as business ethics significantly mediate the relationship between blockchain technology and social sustainability. Overall, the findings of this study suggest that blockchain technology can have a positive impact on business ethics, CSR, and social sustainability, with business ethics and CSR mediating the relationship between blockchain technology and social sustainability.

This study also examined the value of R square, which measures the amount of variance in the dependent variable explained by the independent variables [71]. Chin [72] suggested that an R square value of 0.19 is considered weak, 0.33 is considered moderate, and 0.67 is considered strong.

The R-squared values used for this study involved four variables: BE (business ethics), CSR (corporate social responsibility), SS (social sustainability), and BCT (blockchain technology). The R-squared value for BE is 0.282 (Figure 3), indicating that approximately 28.2% of the variance in the dependent variable is explained by the independent variable BE (business ethics). The R-squared value for CSR is 0.281, indicating that approximately 28.1% of the variance in the dependent variable is explained by the independent variable CSR (corporate social responsibility). The R-squared value for SS is 0.602, indicating that approximately 60.2% of the variance in the dependent variable is explained by the independent variable SS (social sustainability). R-squared (R2) is a statistical measure that represents the proportion of variance in the dependent variable that is explained by the independent variables in a regression model. It ranges from 0 to 1, where 0 indicates that the model does not explain any of the variance, and 1 indicates that the model explains all of the variance.

7. Discussion

The results of this research were determined using structural equation modeling. The findings of H1 showed that use of blockchain technology is positively related to the ethical conduct of business operations. Moreover, the findings of existing studies support this relationship. Weking, Mandalenakis [73] also highlighted that blockchain technology helps firms in improving the fair working of their business. Meanwhile, Mathivathanan, Mathiyazhagan [74] pointed out that blockchain technology should be integrated in business management for it to work transparently. Demirkan, Demirkan [75] also asserted the use of blockchain technology for the advanced working of firms. The findings of H2 confirmed that blockchain technology has a positive impact on the CSR. Moreover, the findings of existing studies support this relationship. Nuseir [76] highlighted that blockchain technology can be fairly used to advance the fair working of corporations. Schneider, Leyer [77] pointed out that the role of blockchain technology is critical to organizational functioning. Hooper and Holtbrügge [78] also emphasized the use of blockchain technology for the operational improvement of businesses.

The outcomes of H3 showed that blockchain technology has a positive impact on social sustainability. Moreover, the findings of existing studies support this relationship. Wang, Li [79] highlighted that newly emerging of technologies can be fairly used for organizational advancement. In accordance, Nuryyev, Wang [80] pointed out that social sustainability can be achieved with the fair use of technology. Qasim and Kharbat [81] reported that many international firms use blockchain technology for the reliable functioning of organizations. The findings of H4 showed that business ethics has a positive impact on social sustainability. Moreover, the findings of existing studies support this relationship. Bai, Cordeiro [82] asserted that ethical management is required for the improvement in a business’ impact on society. Tönnissen and Teuteberg [83] asserted that only ethically functioning organizations can achieve the goals of CSR. Tan and Sundarakani [84] asserted that employees of firms should be motivated to work ethically.

The findings of H5 confirmed that CSR has a positive impact on social sustainability. Moreover, the findings of existing studies support for this relationship. Rijanto [85] reported that CSR is an important factor in organizational sustainability. Khalil, Khawaja [86] also recommended CSR practices for advancing the work of firms in any market. Mercuri, della Corte [87] pointed out the sustainability of firms can be achieved by their advanced working through social sustainability. The outcomes of H6 showed that business ethics mediate the relationship between blockchain technology and social sustainability. Moreover, the findings of existing studies support this relationship. Jensen, Hedman [88] highlighted that an ethical management body can use technology for organizational sustainability. Liu, Wu [89] reported the importance of technology in the ethical working of organizations to improve the transparency in work. Frizzo-Barker, Chow-White [90] emphasized the use of technology to modernize business practices and improve people’s understanding. The outcomes of H7 showed that CSR mediates the relationship between blockchain technology and social sustainability. Moreover, the findings of existing studies support this relationship. de Villiers, Kuruppu [91] pointed out that blockchain technology is helpful in achieving the goals of CSR. Meanwhile, Ronaghi and Mosakhani [42] pointed out the use of technology in the advancement of working practices.

Enhancing social sustainability is of great significance in improving the quality of society. To this end, this study was undertaken to evaluate diverse factors that can bolster social sustainability. To achieve this objective, data were obtained from bank staff employed in the United Arab Emirates. The research findings suggest that the adoption of blockchain technology by UAE banks plays a pivotal role in enhancing their corporate social responsibility. This is because there are fewer chances of fraud and corruption. Also, all the processes of banks become more transparent. These conclusions are consistent with other work [44]. Furthermore, the results suggest that CSR plays a pivotal role in cultivating a favorable image among stakeholders, which in turn contributes to enhancing social sustainability. One of the plausible reasons is that it promotes the ethical practices of banks. Moreover, effective CSR can engage stakeholders for a longer period. These findings are consistent with those presented in another study [53]. Additionally, it is recommended that banks under investigation adhere to ethical business practices, since such practices have a positive impact on social sustainability. These findings concur with the outcomes of an earlier study [49]. Overall, the results of this study provide evidence of the mediating role of both CSR and business ethics in augmenting social sustainability.

8. Conclusions, Implications, and Limitations

In conclusion, this study explored the factors that play an important role in improving social sustainability. The findings revealed that blockchain technology, CSR, and business ethics are important factors for sustainability. Moreover, our findings also confirm the mediating role of business ethics and CSR. The present research addressed the gap pertaining to the limited number of studies conducted on the implementation of blockchain technology in the context of the banking sector in the UAE. This study also provides guidelines to policymakers of the banking sector in terms of ways they can use blockchain technology to improve social sustainability. By improving social sustainability, banks can develop trust among their stakeholders. Moreover, they can develop a positive image as well. On the other hand, engaging skilled employees also has long-term effects, thus having a positive effect on the profitability of banks. In terms of theoretical implications, this study highlighted the mediating role of CSR and business ethics on blockchain technology and social sustainability. However, this study has certain limitations, as do other empirical investigations. Specifically, this study treats blockchain technology as a composite variable. Future research could explore the impact of different blockchain technologies as distinct variables. Furthermore, the impact of blockchain technology could be examined in conjunction with other technologies, such as mobile learning. Ultimately, the results of this study can be leveraged to inform the strategic development of the banking sector with a view to improving social sustainability. These findings can also be utilized in future research endeavors.

8.1. Implications

8.1.1. Theoretical Contribution

This research has noteworthy implications from a theoretical perspective. The results of this study indicate that blockchain technology, CSR, and company ethics play significant roles in promoting sustainability. Furthermore, the results clearly validate the intermediary function of business ethics and CSR. The current study aimed to fill the research gap by examining the scarcity of studies investigating the adoption of blockchain technology within the banking industry in the United Arab Emirates. This report additionally offers recommendations to authorities in the banking sector regarding the utilization of blockchain technology to enhance social sustainability. The enhancement of social sustainability can facilitate the cultivation of trust among various stakeholders within the banking sector. Additionally, individuals have the potential to cultivate a favorable perception of themselves. Conversely, the long-term engagement of proficient personnel is also subject to influence. Consequently, this has a favorable impact on the financial performance of banking institutions.

8.1.2. Practical, Managerial, and Social Implications

In accordance, this research has practical implications, as it highlighted that fair use of blockchain technology is appropriate for the achievement of organizational success in terms of ethical improvement and CSR. The management of businesses in general can attain appropriate understanding using this research to integrate blockchain technology in their working. This method would be helpful for them to improve their ethical obligations to society regarding the achievement of corporate social responsibility goals. Hence, the findings of this research are reliable for practice by firms to advance the social implications for society. The management of firms is required to integrate the use of new technology in organizational working and to improve practices for better financial performance with ethical standards. Hence, this research is also important from a practical point of view to advance organizational practices in line with CSR and ethical standards.

Funding

This research received no external funding.

Institutional Review Board Statement

This study did not require ethical approval.

Informed Consent Statement

Not applicable.

Data Availability Statement

Data is unavailable due to privacy or ethical restrictions.

Conflicts of Interest

The author declares no conflict of interest.

References

- Pieroni, A.; Scarpato, N.; Felli, L. Blockchain and IoT convergence—A systematic survey on technologies, protocols and security. Appl. Sci. 2020, 10, 6749. [Google Scholar] [CrossRef]

- Ali, S.; Wang, G.; White, B.; Cottrell, R.L. A blockchain-based decentralized data storage and access framework for pinger. In Proceedings of the 2018 17th IEEE International Conference on Trust, Security and Privacy in Computing and Communications/12th IEEE International Conference on Big Data Science and Engineering (TrustCom/BigDataSE), New York, NY, USA, 1–3 August 2018; pp. 1303–1308. [Google Scholar]

- Rejeb, A.; Keogh, J.G.; Zailani, S.; Treiblmaier, H.; Rejeb, K. Blockchain technology in the food industry: A review of potentials, challenges and future research directions. Logistics 2020, 4, 27. [Google Scholar] [CrossRef]

- Holotescu, C. Understanding blockchain opportunities and challenges. In Proceedings of the eLearning and Software for Education, Bucharest, Romania, 19–20 April 2018; pp. 275–283. [Google Scholar]

- Haase, M.; Raufflet, E. Ideologies in markets, organizations, and business ethics: Drafting a map: Introduction to the special issue. J. Bus. Ethics 2017, 142, 629–639. [Google Scholar] [CrossRef]

- López Jiménez, D.; Dittmar, E.C.; Vargas Portillo, J.P. New directions in corporate social responsibility and ethics: Codes of conduct in the digital environment. J. Bus. Ethics 2021, 1–11. [Google Scholar] [CrossRef]

- Tzafestas, S.G. Ethics and law in the internet of things world. Smart Cities 2018, 1, 98–120. [Google Scholar] [CrossRef]

- Gallego-Alvarez, I.; Rodríguez-Domínguez, L.; Martín Vallejo, J. An analysis of business ethics in the cultural contexts of different religions. Bus. Ethics A Eur. Rev. 2020, 29, 570–586. [Google Scholar] [CrossRef]

- Lu, J.; Ren, L.; Qiao, J.; Lin, W.; He, Y. Female executives and corporate social responsibility performance: A dual perspective of differences in institutional environment and heterogeneity of foreign experience. Transform. Bus. Econ. 2019, 18, 174–196. [Google Scholar]

- ElAlfy, A.; Palaschuk, N.; El-Bassiouny, D.; Wilson, J.; Weber, O. Scoping the evolution of corporate social responsibility (CSR) research in the sustainable development goals (SDGs) era. Sustainability 2020, 12, 5544. [Google Scholar] [CrossRef]

- Barauskaite, G.; Streimikiene, D. Corporate social responsibility and financial performance of companies: The puzzle of concepts, definitions and assessment methods. Corp. Soc. Responsib. Environ. Manag. 2021, 28, 278–287. [Google Scholar] [CrossRef]

- Ferrell, O.; Harrison, D.E.; Ferrell, L.; Hair, J.F. Business ethics, corporate social responsibility, and brand attitudes: An exploratory study. J. Bus. Res. 2019, 95, 491–501. [Google Scholar] [CrossRef]

- Eizenberg, E.; Jabareen, Y. Social sustainability: A new conceptual framework. Sustainability 2017, 9, 68. [Google Scholar] [CrossRef]

- Palich, N.; Edmonds, A. Social sustainability: Creating places and participatory processes that perform well for people. Environ. Des. Guide 2013, 1–13. [Google Scholar]

- Woodcraft, S. Understanding and measuring social sustainability. J. Urban Regen. Renew. 2015, 8, 133–144. [Google Scholar]

- Helo, P.; Hao, Y. Blockchains in operations and supply chains: A model and reference implementation. Comput. Ind. Eng. 2019, 136, 242–251. [Google Scholar] [CrossRef]

- Fallucchi, F.; Gerardi, M.; Petito, M.; De Luca, E.W. Blockchain Framework in Digital Government for the Certification of Authenticity, Timestamping and Data Property; ScholarSpace: Honolulu, HI, USA, 2021. [Google Scholar]

- Wang, Y.; Han, J.H.; Beynon-Davies, P. Understanding blockchain technology for future supply chains: A systematic literature review and research agenda. Supply Chain. Manag. Int. J. 2018, 24, 62–84. [Google Scholar] [CrossRef]

- Shojaei, A.; Ketabi, R.; Razkenari, M.; Hakim, H.; Wang, J. Enabling a circular economy in the built environment sector through blockchain technology. J. Clean. Prod. 2021, 294, 126352. [Google Scholar] [CrossRef]

- Hunt, K.; Narayanan, A.; Zhuang, J. Blockchain in humanitarian operations management: A review of research and practice. Socio-Econ. Plan. Sci. 2022, 80, 101175. [Google Scholar] [CrossRef]

- Sroka, W.; Szántó, R. Corporate social responsibility and business ethics in controversial sectors: Analysis of research results. J. Entrep. Manag. Innov. 2018, 14, 111–126. [Google Scholar] [CrossRef]

- Ciulla, J.B.; Ciulla, J.B. Ethics and effectiveness: The nature of good leadership. In The Search for Ethics in Leadership, Business, and Beyond; Springer: Cham, Switzerland, 2020; pp. 3–32. [Google Scholar] [CrossRef]

- Cherré, B.; Laarraf, Z.; Peterson, J. Why is it difficult to be virtuous in business ethics? Hum. Syst. Manag. 2019, 38, 395–409. [Google Scholar] [CrossRef]

- Turyakira, P.K. Ethical practices of small and medium-sized enterprises in developing countries: Literature analysis. S. Afr. J. Econ. Manag. Sci. 2018, 21, 1–7. [Google Scholar] [CrossRef]

- Nadeem, W.; Juntunen, M.; Hajli, N.; Tajvidi, M. The role of ethical perceptions in consumers’ participation and value co-creation on sharing economy platforms. J. Bus. Ethics 2021, 169, 421–441. [Google Scholar] [CrossRef]

- De Cremer, D.; Vandekerckhove, W. Managing unethical behavior in organizations: The need for a behavioral business ethics approach. J. Manag. Organ. 2017, 23, 437–455. [Google Scholar] [CrossRef]

- Mohammed, S. Components, theories and the business case for corporate social responsibility. Int. J. Bus. Manag. Rev. 2020, 8, 37–65. [Google Scholar]

- Aluchna, M. Is corporate social responsibility sustainable? A critical approach. In The Dynamics of Corporate Social Responsibility; Springer: Berlin/Heidelberg, Germany, 2017; pp. 9–25. [Google Scholar]

- Lyon, T.P.; Maxwell, J.W. Corporate social responsibility and the environment: A theoretical perspective. In Review of Environmental Economics and Policy; University of Chicago Press: Chicago, IL, USA, 2020. [Google Scholar]

- Mostafa, M.A.; El-Gohary, N.M. Stakeholder-sensitive social welfare-oriented benefit analysis for sustainable infrastructure project development. J. Constr. Eng. Manag. 2014, 140, 04014038. [Google Scholar] [CrossRef]

- Bojago, E. The Role of Social Sustainability in the Designation of a Sustainable Community: Based on Cumulative Development Patterns in Residential Complexes. Environ. Sci. 2022. [Google Scholar] [CrossRef]

- Grum, B.; Grum, D.K. Concepts of social sustainability based on social infrastructure and quality of life. Facilities 2020, 38, 783–800. [Google Scholar] [CrossRef]

- George, K.; Patatoukas, P.N. The blockchain evolution and revolution of accounting. In Information for Efficient Decision Making: Big Data, Blockchain and Relevance; World Scientific: Singapore, 2021; pp. 157–172. [Google Scholar]

- Hughes, K. Blockchain, the greater good, and human and civil rights. Metaphilosophy 2017, 48, 654–665. [Google Scholar] [CrossRef]

- Tang, Y.; Xiong, J.; Becerril-Arreola, R.; Iyer, L. Ethics of blockchain: A framework of technology, applications, impacts, and research directions. Inf. Technol. People 2020, 33, 602–632. [Google Scholar] [CrossRef]

- Fernando, Y.; Saravannan, R. Blockchain technology: Energy efficiency and ethical compliance. J. Gov. Integr. 2021, 4, 88–95. [Google Scholar] [CrossRef]

- Campbell-Verduyn, M.; Hütten, M. Beyond scandal? Blockchain technologies and the legitimacy of post-2008 finance. Financ. Soc. 2019, 5, 126–144. [Google Scholar] [CrossRef]

- Sharif, M.M.; Ghodoosi, F. The ethics of blockchain in organizations. J. Bus. Ethics 2022, 178, 1009–1025. [Google Scholar] [CrossRef]

- Rahimzadeh, V. Ethics Governance Outside the Box: Reimagining Blockchain as a Policy Tool to Facilitate Single Ethics Review and Data Sharing for the ‘omics’ Sciences. Blockchain Healthc. Today 2018, 1, 1–10. [Google Scholar] [CrossRef]

- Tan, T.M.; Salo, J. Ethical marketing in the blockchain-based sharing economy: Theoretical integration and guiding insights. J. Bus. Ethics 2023, 183, 1113–1140. [Google Scholar] [CrossRef]

- Dierksmeier, C.; Seele, P. Blockchain and business ethics. Bus. Ethics A Eur. Rev. 2020, 29, 348–359. [Google Scholar] [CrossRef]

- Ronaghi, M.H.; Mosakhani, M. The effects of blockchain technology adoption on business ethics and social sustainability: Evidence from the Middle East. Environ. Dev. Sustain. 2022, 24, 6834–6859. [Google Scholar] [CrossRef]

- Funk, E.; Riddell, J.; Ankel, F.; Cabrera, D. Blockchain technology: A data framework to improve validity, trust, and accountability of information exchange in health professions education. Acad. Med. 2018, 93, 1791–1794. [Google Scholar] [CrossRef] [PubMed]

- Fernández-Caramés, T.M.; Fraga-Lamas, P. A Review on the Use of Blockchain for the Internet of Things. IEEE Access 2018, 6, 32979–33001. [Google Scholar] [CrossRef]

- Ezzi, F.; Jarboui, A.; Mouakhar, K. Exploring the Relationship Between Blockchain Technology and Corporate Social Responsibility Performance: Empirical Evidence from European Firms. J. Knowl. Econ. 2022, 14, 1227–1248. [Google Scholar] [CrossRef]

- Upadhyay, A.; Mukhuty, S.; Kumar, V.; Kazancoglu, Y. Blockchain technology and the circular economy: Implications for sustainability and social responsibility. J. Clean. Prod. 2021, 293, 126130. [Google Scholar] [CrossRef]

- Peñaflor-Guerra, R.; Sanagustín-Fons, M.V.; Ramírez-Lozano, J. Business Ethics Crisis and Social Sustainability. The Case of the Product “Pura Vida” in Peru. Sustainability 2020, 12, 3348. [Google Scholar] [CrossRef]

- ElGammal, W.; El-Kassar, A.-N.; Messarra, L.C. Corporate ethics, governance and social responsibility in MENA countries. Manag. Decis. 2018, 56, 273–291. [Google Scholar] [CrossRef]

- Stahl, B.C.; Chatfield, K.; Ten Holter, C.; Brem, A. Ethics in corporate research and development: Can responsible research and innovation approaches aid sustainability? J. Clean. Prod. 2019, 239, 118044. [Google Scholar] [CrossRef]

- Kurnia, A.; Shaura, A.; Raharjo, S.T.; Resnawaty, R. Sustainable Development dan CSR. Pros. Penelit. Dan Pengabdi. Kpd. Masy. 2020, 6, 231–237. [Google Scholar] [CrossRef]

- Ali, S.S.; Kaur, R. Effectiveness of corporate social responsibility (CSR) in implementation of social sustainability in warehousing of developing countries: A hybrid approach. J. Clean. Prod. 2021, 324, 129154. [Google Scholar] [CrossRef]

- Hong, L.; Chao, A. Strategic corporate social responsibility, sustainable growth, and energy policy in China. Energies 2018, 11, 3024. [Google Scholar] [CrossRef]

- Qing, C.; Jin, S. How Does Corporate Social Responsibility Affect Sustainability of Social Enterprises in Korea? Front. Psychol. 2022, 13, 859170. [Google Scholar] [CrossRef]

- Liu, J.-Y. An internal control system that includes corporate social responsibility for social sustainability in the new era. Sustainability 2018, 10, 3382. [Google Scholar] [CrossRef]

- Sekaran, U.; Bougie, R. Research Methods for Business: A Skill Building Approach; John Wiley & Sons: Hoboken, NJ, USA, 2016. [Google Scholar]

- Bagozzi, R.P.; Yi, Y. Specification, evaluation, and interpretation of structural equation models. J. Acad. Mark. Sci. 2012, 40, 8–34. [Google Scholar] [CrossRef]

- Abu Zayyad, H.M.; Obeidat, Z.M.; Alshurideh, M.T.; Abuhashesh, M.; Maqableh, M.; Masa’deh, R.e. Corporate social responsibility and patronage intentions: The mediating effect of brand credibility. J. Mark. Commun. 2021, 27, 510–533. [Google Scholar] [CrossRef]

- Khan, S.A.R.; Godil, D.I.; Jabbour, C.J.C.; Shujaat, S.; Razzaq, A.; Yu, Z. Green data analytics, blockchain technology for sustainable development, and sustainable supply chain practices: Evidence from small and medium enterprises. Ann. Oper. Res. 2021, 1–25. [Google Scholar] [CrossRef]

- Blanco-González, A.; Del-Castillo-Feito, C.; Miotto, G. The influence of business ethics and community outreach on faculty engagement: The mediating effect of legitimacy in higher education. Eur. J. Manag. Bus. Econ. 2021, 30, 281–298. [Google Scholar] [CrossRef]

- Raza, A.; Rather, R.A.; Iqbal, M.K.; Bhutta, U.S. An assessment of corporate social responsibility on customer company identification and loyalty in banking industry: A PLS-SEM analysis. Manag. Res. Rev. 2020, 43, 1337–1370. [Google Scholar] [CrossRef]

- Duong, N.-H.; Ha, Q.-A. The Impacts of Social Sustainability Practices on Supply Chain Performance: Mediating Role of Supply Chain Integration. J. Distrib. Sci. 2021, 19, 37–48. [Google Scholar]

- Kock, N. Common method bias in PLS-SEM: A full collinearity assessment approach. Int. J. e-Collab. 2015, 11, 1–10. [Google Scholar] [CrossRef]

- Hair, J.F.; Harrison, D.; Risher, J.J. Marketing research in the 21st century: Opportunities and challenges. Braz. J. Mark.–Rev. Bras. Mark. Spec. Issue 2018, 17, 5. [Google Scholar] [CrossRef]

- Ali, J.; Azeem, M.; Marri, M.Y.K.; Khurram, S. University Social Responsibility and Self Efficacy as Antecedents of Intention to use E-Learning: Examining Mediating Role of Student Satisfaction. Psychol. Educ. J. 2021, 58, 4219–4230. [Google Scholar]

- Jabeen, S.; Ali, J. Impact of Servant Leadership on the Development of Change-Oriented Citizenship Behavior: Multi-Mediation Analysis of Change Readiness and Psychological Empowerment. In Key Factors and Use Cases of Servant Leadership Driving Organizational Performance; IGI Global: Hershey, PA, USA, 2022; pp. 110–129. [Google Scholar]

- Hair, J.F., Jr.; Sarstedt, M.; Ringle, C.M.; Gudergan, S.P. Advanced Issues in Partial Least Squares Structural Equation Modeling; Sage Publications: Thousand Oaks, CA, USA, 2017. [Google Scholar]

- Sarstedt, M.; Ringle, C.M.; Henseler, J.; Hair, J.F. On the emancipation of PLS-SEM: A commentary on Rigdon (2012). Long Range Plan. 2014, 47, 154–160. [Google Scholar] [CrossRef]

- Fornell, C.; Larcker, D.F. Structural equation models with unobservable variables and measurement error: Algebra and statistics. J. Mark. Res. 1981, 18, 382–388. [Google Scholar] [CrossRef]

- Henseler, J.; Ringle, C.M.; Sarstedt, M. A new criterion for assessing discriminant validity in variance-based structural equation modeling. J. Acad. Mark. Sci. 2015, 43, 115–135. [Google Scholar] [CrossRef]

- Ali, J.; Perumal, S.; Shaari, H. Application of the stimulus-organism-response model in the airline industry: Examining mediating role of airline image in repurchase intention. Int. J. Supply Chain Manag. 2020, 9, 981–989. [Google Scholar]

- Hair, J.F.; Risher, J.J.; Sarstedt, M.; Ringle, C.M. When to use and how to report the results of PLS-SEM. Eur. Bus. Rev. 2019, 31, 2–24. [Google Scholar] [CrossRef]

- Chin, W.W. The partial least squares approach to structural equation modeling. Mod. Methods Bus. Res. 1998, 295, 295–336. [Google Scholar]

- Weking, J.; Mandalenakis, M.; Hein, A.; Hermes, S.; Böhm, M.; Krcmar, H. The impact of blockchain technology on business models—A taxonomy and archetypal patterns. Electron. Mark. 2020, 30, 285–305. [Google Scholar] [CrossRef]

- Mathivathanan, D.; Mathiyazhagan, K.; Rana, N.P.; Khorana, S.; Dwivedi, Y.K. Barriers to the adoption of blockchain technology in business supply chains: A total interpretive structural modelling (TISM) approach. Int. J. Prod. Res. 2021, 59, 3338–3359. [Google Scholar] [CrossRef]

- Demirkan, S.; Demirkan, I.; McKee, A. Blockchain technology in the future of business cyber security and accounting. J. Manag. Anal. 2020, 7, 189–208. [Google Scholar] [CrossRef]

- Nuseir, M.T. Potential impacts of blockchain technology on business practices of bricks and mortar (B&M) grocery stores. Business Process Manag. J. 2021, 27, 1256–1274. [Google Scholar]

- Schneider, S.; Leyer, M.; Tate, M. The transformational impact of blockchain technology on business models and ecosystems: A symbiosis of human and technology agents. IEEE Trans. Eng. Manag. 2020, 67, 1184–1195. [Google Scholar] [CrossRef]

- Hooper, A.; Holtbrügge, D. Blockchain technology in international business: Changing the agenda for global governance. Rev. Int. Bus. Strategy 2020, 30, 183–200. [Google Scholar] [CrossRef]

- Wang, Z.; Li, M.; Lu, J.; Cheng, X. Business Innovation based on artificial intelligence and Blockchain technology. Inf. Process. Manag. 2022, 59, 102759. [Google Scholar] [CrossRef]

- Nuryyev, G.; Wang, Y.-P.; Achyldurdyyeva, J.; Jaw, B.-S.; Yeh, Y.-S.; Lin, H.-T.; Wu, L.-F. Blockchain technology adoption behavior and sustainability of the business in tourism and hospitality SMEs: An empirical study. Sustainability 2020, 12, 1256. [Google Scholar] [CrossRef]

- Qasim, A.; Kharbat, F.F. Blockchain technology, business data analytics, and artificial intelligence: Use in the accounting profession and ideas for inclusion into the accounting curriculum. J. Emerg. Technol. Account. 2020, 17, 107–117. [Google Scholar] [CrossRef]

- Bai, C.A.; Cordeiro, J.; Sarkis, J. Blockchain technology: Business, strategy, the environment, and sustainability. Bus. Strategy Environ. 2020, 29, 321–322. [Google Scholar] [CrossRef]

- Tönnissen, S.; Teuteberg, F. Analysing the impact of blockchain-technology for operations and supply chain management: An explanatory model drawn from multiple case studies. Int. J. Inf. Manag. 2020, 52, 101953. [Google Scholar] [CrossRef]

- Tan, W.K.A.; Sundarakani, B. Assessing Blockchain Technology application for freight booking business: A case study from Technology Acceptance Model perspective. J. Glob. Oper. Strateg. Sourc. 2021, 14, 202–223. [Google Scholar] [CrossRef]

- Rijanto, A. Business financing and blockchain technology adoption in agroindustry. J. Sci. Technol. Policy Manag. 2021, 12, 215–235. [Google Scholar] [CrossRef]

- Khalil, M.; Khawaja, K.F.; Sarfraz, M. The adoption of blockchain technology in the financial sector during the era of fourth industrial revolution: A moderated mediated model. Qual. Quant. 2022, 56, 2435–2452. [Google Scholar] [CrossRef]

- Mercuri, F.; della Corte, G.; Ricci, F. Blockchain technology and sustainable business models: A case study of Devoleum. Sustainability 2021, 13, 5619. [Google Scholar] [CrossRef]

- Jensen, T.; Hedman, J.; Henningsson, S. How tradelens delivers business value with blockchain technology. MIS Q. Exec. 2019, 18, 4. [Google Scholar] [CrossRef]

- Liu, M.; Wu, K.; Xu, J.J. How will blockchain technology impact auditing and accounting: Permissionless versus permissioned blockchain. Curr. Issues Audit. 2019, 13, A19–A29. [Google Scholar] [CrossRef]

- Frizzo-Barker, J.; Chow-White, P.A.; Adams, P.R.; Mentanko, J.; Ha, D.; Green, S. Blockchain as a disruptive technology for business: A systematic review. Int. J. Inf. Manag. 2020, 51, 102029. [Google Scholar] [CrossRef]

- De Villiers, C.; Kuruppu, S.; Dissanayake, D. A (new) role for business–Promoting the United Nations’ Sustainable Development Goals through the internet-of-things and blockchain technology. J. Bus. Res. 2021, 131, 598–609. [Google Scholar] [CrossRef]

Figure 1.

Conceptual framework.

Figure 2.

Measurement model. Note: BCT = blockchain technology; CSR = corporate social responsibility; SS = social sustainability; BE = business ethics.

Figure 2.

Measurement model. Note: BCT = blockchain technology; CSR = corporate social responsibility; SS = social sustainability; BE = business ethics.

Figure 3.

Structural model assessment. Note: BCT = blockchain technology; CSR = corporate social responsibility; SS = social sustainability; BE = business ethics.

Figure 3.

Structural model assessment. Note: BCT = blockchain technology; CSR = corporate social responsibility; SS = social sustainability; BE = business ethics.

Figure 4.

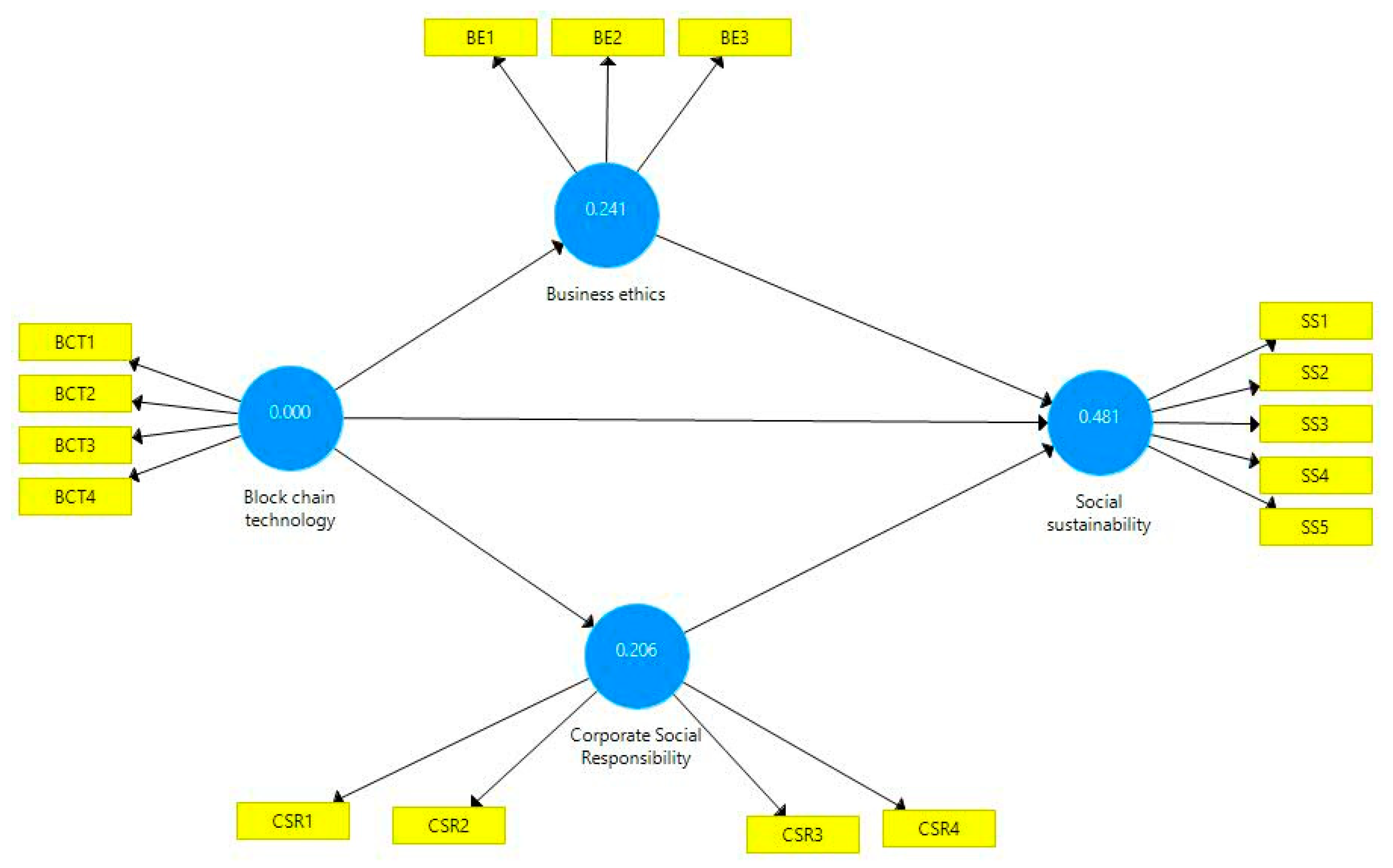

Predictive relevance. Note: BCT = blockchain technology; CSR = corporate social responsibility; SS = social sustainability; BE = business ethics.

Figure 4.

Predictive relevance. Note: BCT = blockchain technology; CSR = corporate social responsibility; SS = social sustainability; BE = business ethics.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Table 1.

Variance inflation factor.

| BE | CSR | SS | |

|---|---|---|---|

| BCT | 1.005 | 1.002 | 1.460 |

| BE | 2.750 | ||

| CSR | 2.717 |

BCT = blockchain technology; CSR = corporate social responsibility; SS = social sustainability; BE = business ethics.

Table 2.

Descriptive analysis.

| Variable | N | Minimum | Maximum | Mean | Std. Dev |

|---|---|---|---|---|---|

| BCT | 262 | 1.00 | 5.00 | 3.233 | 0.861 |

| CSR | 262 | 1.00 | 5.00 | 3.857 | 0.933 |

| BE | 262 | 1.00 | 5.00 | 2.887 | 1.031 |

| SS | 262 | 1.00 | 5.00 | 4.074 | 0.884 |

Table 3.

Individual items related to reliability.

| Items | Instruments | BE |

|---|---|---|

| BCT1 | The use of blockchain technology is effective for an organization. | 0.936 |

| BCT2 | Blockchain technology fulfils an organization’s ethical obligations. | 0.943 |

| BCT3 | The successful implementation of blockchain technology is necessary for CSR. | 0.936 |

| BCT4 | Blockchain technology is effective for this organization. | 0.932 |

| BE1 | There is a clear vision of the objectives that guide my business. | 0.921 |

| BE2 | It is managed with ethics and transparency. | 0.944 |

| BE3 | It takes into consideration its stakeholders in their management decisions. | 0.936 |

| CSR1 | This organization helps to solve social problems. | 0.884 |

| CSR2 | This organization plays a role in society beyond economic benefit generation. | 0.886 |

| CSR3 | This organization is concerned with improving the general wellbeing of society. | 0.905 |

| CSR4 | This organization is concerned with respecting and protecting the natural environment. | 0.815 |

| SS1 | The organization engages in philanthropy. | 0.933 |

| SS2 | The organization is working for the safety of the community. | 0.889 |

| SS3 | The organization is working for health and welfare. | 0.924 |

| SS4 | The organization has equity. | 0.934 |

| SS5 | The organization has ethics. | 0.843 |

Note: BCT = blockchain technology; CSR = corporate social responsibility; SS = social sustainability; BE = business ethics.

Table 4.

Convergent validity.

| CR | AVE | |

|---|---|---|

| BCT | 0.966 | 0.877 |

| BE | 0.953 | 0.872 |

| CSR | 0.928 | 0.763 |

| SS | 0.958 | 0.819 |

Note: BCT = blockchain technology; CSR = corporate social responsibility; SS = social sustainability; BE = business ethics.

Table 5.

Discriminant validity—Fornell and Larker approach.

| BCT | BE | CSR | SS | |

|---|---|---|---|---|

| BCT | 0.937 | |||

| BE | 0.531 | 0.934 | ||

| CSR | 0.530 | 0.786 | 0.873 | |

| SS | 0.594 | 0.679 | 0.725 | 0.905 |

Note: BCT = blockchain technology; CSR = corporate social responsibility; SS = social sustainability, BE = business ethics.

Table 6.

Discriminant validity—HTMT.

| BCT | BE | CSR | SS | |

|---|---|---|---|---|

| BCT | ||||

| BE | 0.562 | |||

| CSR | 0.565 | 0.847 | ||

| SS | 0.623 | 0.722 | 0.781 |

Note: BCT = blockchain technology; CSR = corporate social responsibility; SS = social sustainability; BE = business ethics.

Table 7.

Direct relationships.

| HYP | Relationship | Beta | SD | t Value | p Values |

|---|---|---|---|---|---|

| H1 | BCT → BE | 0.531 | 0.057 | 9.278 | 0.000 |

| H2 | BCT → CSR | 0.530 | 0.059 | 8.909 | 0.000 |

| H3 | BCT → SS | 0.258 | 0.069 | 3.762 | 0.000 |

| H4 | BE → SS | 0.209 | 0.108 | 1.927 | 0.027 |

| H5 | CSR → SS | 0.423 | 0.106 | 3.993 | 0.000 |

Note: BCT = blockchain technology; CSR = corporate social responsibility; SS = social sustainability; BE = business ethics.

Table 8.

Mediating relationships.

| Hypothesis | Relationships | Beta | SD | t Value | p Values |

|---|---|---|---|---|---|

| H6 | BCT → BE → SS | 0.111 | 0.058 | 1.903 | 0.029 |

| H7 | BCT → CSR → SS | 0.224 | 0.059 | 3.801 | 0.000 |

Note: BCT = blockchain technology; CSR = corporate social responsibility; SS = social sustainability; BE = business ethics.

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Aljumah, A.I. Investigating the Impact of Blockchain Technology on Social Sustainability and the Mediating Role of Ethics and CSR. Sustainability 2023, 15, 15510. https://doi.org/10.3390/su152115510

AMA Style

Aljumah AI. Investigating the Impact of Blockchain Technology on Social Sustainability and the Mediating Role of Ethics and CSR. Sustainability. 2023; 15(21):15510. https://doi.org/10.3390/su152115510

Chicago/Turabian StyleAljumah, Ahmad Ibrahim. 2023. "Investigating the Impact of Blockchain Technology on Social Sustainability and the Mediating Role of Ethics and CSR" Sustainability 15, no. 21: 15510. https://doi.org/10.3390/su152115510

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.