The Role of Employee Empowerment in Supporting Accounting Information Systems Outcomes: A Mediated Model

Faculty of Business, Al-Zaytoonah University of Jordan, Amman 11733, Jordan

Sustainability 2023, 15(9), 7155; https://doi.org/10.3390/su15097155

Submission received: 28 December 2022

/

Revised: 24 March 2023

/

Accepted: 12 April 2023

/

Published: 25 April 2023

(This article belongs to the Section Economic and Business Aspects of Sustainability)

Abstract

:The current research study was carried out to explore the mediating influence of management awareness on the relationship between employee empowerment and accounting information systems (AIS) outcomes. A quantitative approach was adopted through the distribution of an online questionnaire to (97) financial managers and accounting managers within banks in Jordan. SPSS was used in order to analyze the primary data, and it was seen that management awareness mediates the relationship between employee empowerment and AIS outcomes, which is attributed to the fact that management needs to be aware of organizational goals and the financial information needed to achieve these goals. This includes an understanding of the latest accounting technology that is available to assist in this process. Additionally, management needs to be aware of the costs associated with the implementation of new systems, and any potential risks that could arise. By being actively involved in the implementation and decision-making process, management can ensure that AIS is efficient and produces the desired results. Finally, management should ensure that appropriate user training is available for all users of the information system. This ensures that the system can be utilized in the most efficient manner possible and produces the desired financial results. This study recommended the need to utilize integrated cloud-based systems to increase the availability of information and reduce the need for manual data entry. Further recommendations were presented in the study.

1. Introduction

According to [1], management awareness and accounting outcomes are closely related in that the decisions made by management have a direct influence on the financial performance of an organization. Management has the responsibility to establish goals, create policies and strategies, determine a budget, and create an environment conducive to successful operations. Having an understanding of the principles of accounting, both current and traditional, is vital to making sound decisions that will positively impact the financial performance of the organization [2]. Ahmad and Al-Shbiel (2019) [3] argued that accounting outcomes are the result of this management decision making, which encompasses all the financial aspects that affect an organization’s future prospects. As such, it is essential that those leading an organization understand the principles of accounting in order to apply them to the organization’s activities, in order to achieve a successful accounting outcome [4].

Based on what was mentioned above, the relationship between empowerment and individual performance is a strong one, as the sense of empowerment can motivate and enable an individual to realize their fullest potential in their work [5]. Empowerment may include activities such as offering support, delegation, providing resources and tools, and allowing autonomy [6]. All of these activities can contribute to an individual’s ability to have greater control over their work and achieve higher performance. Increased motivation can lead to an improved sense of self-confidence in an individual’s ability to succeed, leading to increased self-esteem and higher performance [7].

According to [8,9], employee empowerment and AIS outcomes go hand in hand. AIS are designed to improve productivity, reduce costs, and improve customer service, and these successes are enabled through empowering employees with the tools and information they need to successfully carry out their job roles. Employee empowerment and AIS outcomes must work together to achieve desired goals [10].

Nicholls (2018) [11] added that employee empowerment in accounting helps teams anticipate risks, remain agile in the face of change, reduce costs, and improve accuracy. It helps teams plan for long-term success since empowered employees have the tools, knowledge, and confidence to handle challenges and foster continuous improvement. By cultivating employee ownership of their work, teams can become self-motivated and purposeful in their actions, taking an outcome-based approach to accounting activities. More importantly, refs. [12,13] argued that developing an empowered culture promotes collaboration between departments, which helps ensure accuracy and accountability while creating a sense of community within the accounting team. Additionally, by enabling employees to develop a deeper understanding of the company’s financial data, they can provide greater insights and insights into decision making, driving more reliable outcomes and organizational success [14].

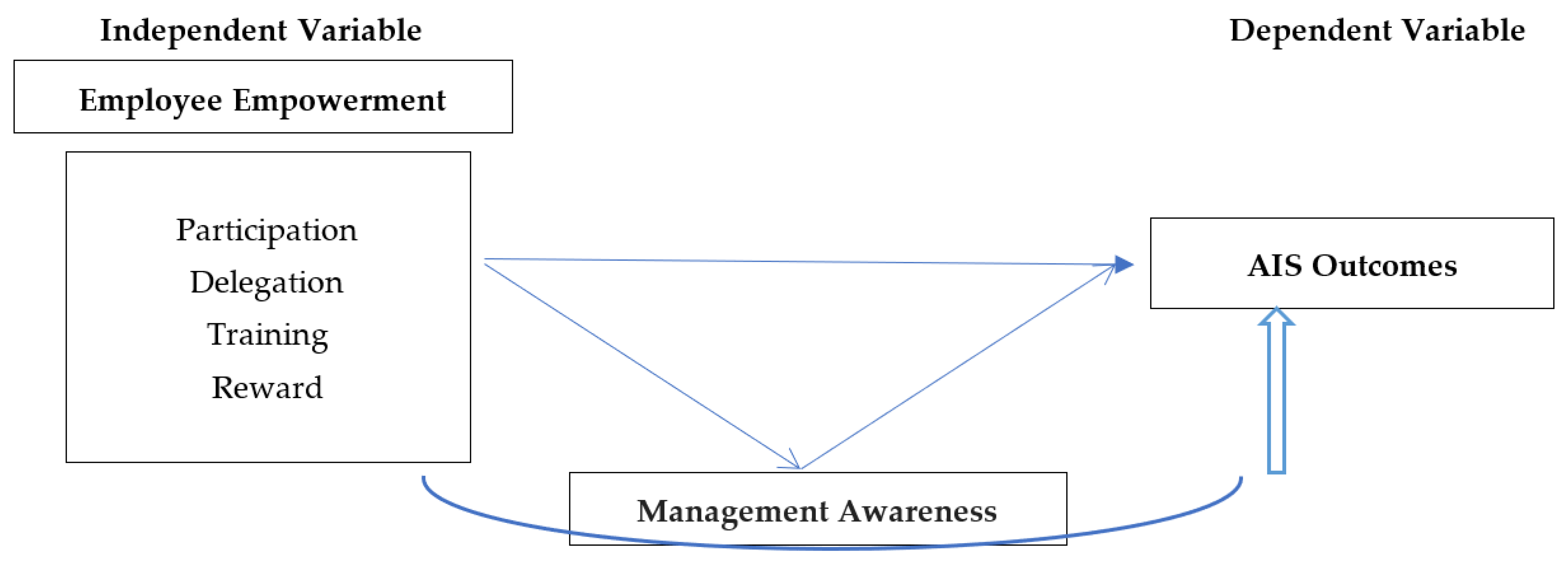

Based on the above argument, this current research aimed at examining the role of employee empowerment (participation, delegation, training, and reward) in supporting better AIS outcomes within the banking sector in Jordan by focusing on the mediating influence of higher management awareness.

The motivation behind examining employee empowerment’s role in supporting AIS outcomes within the banking sector with the mediating influence of higher management awareness is to better understand how employee empowerment and higher management awareness impact the effectiveness of AIS in the banking industry.

Employee empowerment refers to giving employees the autonomy, authority, and resources they need to make decisions and take action to improve organizational performance. Higher management awareness refers to the extent to which senior managers are knowledgeable about the importance of AIS and how they can support its effective implementation.

In addition to that, the motivation behind the current study was to gain a better understanding of how these factors can impact the effectiveness of accounting information systems in the banking sector. This study is motivated by the need to identify ways to improve AIS outcomes in banking organizations, which can lead to increased efficiency, accuracy, and cost savings. By examining the role of employee empowerment, the study seeks to determine how empowering employees can lead to better AIS outcomes and overall organizational performance. Moreover, the study is also motivated by the need to understand how higher management awareness can mediate the relationship between employee empowerment and AIS outcomes. This can help banking organizations to identify the importance of management involvement and support in enhancing the effectiveness of AIS.

By studying the impact of employee empowerment and higher management awareness on AIS outcomes in the banking sector, researchers and practitioners can gain insights into how to improve AIS effectiveness in this industry. Additionally, the mediating influence of higher management awareness on the relationship between employee empowerment and AIS outcomes can help identify specific actions that managers can take to support their employees and ensure that AIS are implemented effectively.

Overall, the motivation for examining employee empowerment and higher management awareness in the context of AIS outcomes in the banking sector is to identify ways to improve organizational performance and maximize the benefits of AIS for banks and their customers.

The literature gap that the current study focuses on stems from the lack of research or knowledge on the specific topic or area that the study aims to investigate. In this particular case, the study aims to examine the role of employee empowerment in enhancing the outcomes of AIS within the banking sector, and how higher management awareness can act as a mediator between employee empowerment and AIS outcomes. The literature gap has arisen due to the limited research available on this particular topic, or the absence of studies that have examined the specific relationship between these variables within the context of the banking sector. This study aims to address this gap by providing insights into the relationship between employee empowerment, higher management awareness, and AIS outcomes within the banking sector, which can help organizations to enhance their accounting information systems and improve overall performance.

Launching from this, the current study seeks to answer the following questions:

- What is the relationship between employee empowerment and AIS outcomes?

- How can management awareness mediate the relationship between employee empowerment and AIS outcomes?

From the above questions, the following set of objectives was reached:

- Identify the impact of employee empowerment on AIS outcomes.

- Realize the role of managerial awareness in enhancing AIS outcomes.

- Highlight the interconnectedness between employee empowerment, AIS outcomes, and managerial awareness.

2. Literature Review

2.1. Employee Empowerment

The concept of employee empowerment has been defined in many facets; according to [15], employee empowerment is giving employees the ability to make decisions, influence outcomes, and take ownership of their work. Refs. [16,17] saw employee empowerment as allowing employees to contribute ideas and opinions freely in the workplace; while [8,9] defined the concept as investing in resources to support employees and helping them gain the knowledge and expertise to meet their job requirements.

From another perspective, employee empowerment is encouraging open lines of communication between employees, managers, and other leaders. It is more about creating an empowering environment that promotes honesty and respect [18]. It involves training staff on problem-solving techniques to enable them to come up with solutions independently, in addition to recognizing and rewarding employees for their hard work and motivation [10]. For [14,19], it was seen that employee empowerment is basically offering flexibilities such as allowing employees to set their own hours, take breaks, and voice their opinions. Reference [20] saw it as soliciting employees’ feedback on decision-making processes and policies. According to [21], employee empowerment is celebrating the contributions and successes of individual team members to build an effective team spirit, and enabling employees to be self-directed and accountable for their work.

2.1.1. Participation

Participation in employee empowerment is a concept that focuses on the empowerment of each individual employee within an organization, allowing them to have a greater say in the decision-making process and allowing them to develop professionally by increasing their responsibilities and autonomy [22]. Participation in employee empowerment is important because it encourages employees to be engaged, allows their skills and talents to be maximized, and helps create a workplace atmosphere that is open to change and innovation [9,23].

2.1.2. Delegation

According to [24,25], delegation in employee empowerment is the practice of handing a degree of decision-making authority down to employees. It allows them to exercise authority, to use their own judgment and skills, and be proactive in resolving conflicts. Delegation of decision making empowers employees and allows them to take ownership of their work and help shape the direction of the organization [26].

2.1.3. Training

Employee empowerment training is designed to educate staff on ways to take ownership of their efforts, develop a sense of personal accountability, and demonstrate initiative [27]. It covers topics such as decision making, communication, problem solving, customer service, and team building [28]. The goal is to create an environment where employee engagement is encouraged and employees feel empowered to take ownership of their work and make meaningful contributions [29].

2.1.4. Reward

According to [30,31], reward in employee empowerment can include financial incentives, recognition from upper management, promotions, flexible work arrangements, special training, or development opportunities, and other non-financial incentives such as flexible work schedules or recognition programs. Moreover, empowering employees through greater job autonomy increases their satisfaction and motivation, which can lead to higher engagement, increased commitment, and improved performance [32].

2.2. AIS Outcomes

According to [33,34], an AIS (AIS) is a type of organizational system that uses software to collect, store, manipulate, and analyze financial and accounting data. [35] defined the AIS as a general ledger that contains a consolidated record of the organization’s assets, liabilities, and equity, as well as all accounts and schedules. According to [36,37], it is the use of accounting information data to identify a company’s most profitable channels and products [38,39,40].

An AIS is based on financial data mining that is launched from the process of collecting, analyzing, and interpreting large amounts of financial data to identify patterns and trends [41,42,43]. It is basically a method used to assign costs to different activities within an organization, or the cycle of activities that record transactional data from source documents to the business database [44,45,46,47,48].

2.3. Management Awareness

According to [49,50], management awareness is an understanding of the impact of decision making on the social and environmental implications of the business. It involves understanding the various stakeholders of a business, such as employees, customers, investors, suppliers, and other entities, and how their perspectives may affect their decisions. It also involves understanding how decisions made in one area of the business may impact other areas [51]. By developing an understanding of how decisions are made, managers are better equipped to make informed decisions that support the business’s strategic objectives and sustainable development goals [52,53].

From another perspective, it can be said that management awareness is about being knowledgeable and informed of the current happenings in the realm of management [54]. Thomas et al. (2019) [55] defined it as the awareness of the specific roles and responsibilities of various management positions, while [56] defined it as knowing the various management strategies, both current and historical. Cao et al. (2021) [57] added that management awareness is the state of understanding the various processes and tools for management success, and having the ability to anticipate and respond to changes in the field of management quickly.

3. Hypotheses Development

According to [13], in order to be competitive in the marketplace, Rural Banks, which are situated near the community and assist the micro, small, and medium enterprises (MSME) sector, need an effective accounting information system (AIS). Thus, to increase the AIS user efficiency in these banks, incentive programs and employee empowerment are important aspects. Research was carried out in 13 Rural Banks in Denpasar with 65 operating section employees, who were chosen by a purposive sampling method. The data collection process combined online questionnaires through Google Forms as well as physical copies. The data analysis was conducted through a Multiple Linear Regression Analysis, which showed a positive and significant impact of incentives and employee empowerment on AIS effectiveness.

Nicholls (2018) [11] research presents the notion of social impact accounting, which is distinct from financial accounting practice in regards to two essential materiality topics: the uncertain nature of its data and the enabling processes for establishing materiality. Data from in-depth empirical analysis are used to present a new theory of social impact accounting and explain how it is effective in allowing service users to be heard and provide precise performance data. This research both advances social impact accounting and furthers the discussion regarding critical approaches to accounting.

Al-Okaily et al. (2020) [33] investigated the effectiveness of accounting information systems (AIS) from an organizational perspective. The research study was based on a survey distributed to accounting professionals in Iran, with a total of 89 valid responses. The study used structural equation modeling (SEM) to analyze the data collected from the survey. The results showed that AIS effectiveness has a substantial impact on organizational effectiveness, both directly and indirectly. Directly, AIS effectiveness impacts on decision maker satisfaction, which then leads to an improvement in organizational effectiveness. Indirectly, AIS effectiveness impacts task integration and decision maker cognition, which in turn contribute positively to organizational effectiveness. The study concluded that the effectiveness of AIS is crucial to the overall effectiveness of an organization. It suggests that organizations should seek to improve the effectiveness of their AIS through measures such as enhancing task integration and decision maker cognition, in order to improve organizational effectiveness. The study also recommends further research in this area to explore the effectiveness of AIS in different organizational contexts.

Al-Okaily (2021) [58] explored the impact of accounting information systems’ (AIS) usage on the effectiveness of these systems in small and medium-sized enterprises (SMEs) in Jordan. The study used a questionnaire-based survey of 398 SMEs to assess the relationship between AIS usage and effectiveness, and also considered the role of firm size in this relationship. The study found that AIS usage has a positive impact on the effectiveness of these systems for both small and large SMEs in Jordan, but the impact is greater for larger firms. Additionally, the study found that larger SMEs tend to use AIS more extensively and are more likely to have dedicated IT departments and trained staff to manage these systems. The study has important practical implications for SMEs in Jordan, as it highlights the importance of investing in AIS to improve the efficiency of financial reporting and decision-making processes. The findings also suggest that larger SMEs may have a competitive advantage over smaller firms when it comes to harnessing the full potential of AIS technology. Overall, the study contributes to the literature on the role of AIS in SMEs and provides insights that could be useful for SMEs in Jordan and other developing countries.

Based on the above literature review and hypotheses development, the researcher was able to formulate the following model—Figure 1—from which hypotheses for this study were extracted:

Based on the above model, the current study hypothesizes the following:

H (1).

Employee empowerment has a significant impact on management awareness.

H (2).

Management awareness has a significant impact on AIS outcomes.

H (3).

Employee empowerment has a significant impact on AIS outcomes.

H (4).

Management awareness mediates the relationship between employee empowerment and AIS outcomes.

4. Methods

4.1. Methodological Approach

Current study adopted the quantitative approach in reaching aim of study and realizes its objectives. Quantitative approach is a research method that uses numerical data or data that can be quantified to answer a research question or measure a phenomenon [60]. It utilizes methods such as surveys, experiments, and statistical analysis to examine relationships between variables, make predictions, and test hypotheses [61]. The quantitative approach is used when the goal of research is to test specific hypotheses, usually with a focus on cause and effect relationships [62]. Epistemology of quantitative approach is based on the belief that quantifiable data provides an objective representation of the phenomena being studied, which can be used to generate reliable, valid, and generalizable conclusions [63]. Quantitative researchers collect numerical data through surveys and experiments and use statistical analysis to identify patterns and trends. This approach often focuses on cause and effect relationships, helping to identify specific factors that influence a particular outcome [64,65].

The philosophy behind a quantitative approach is that we can measure the effectiveness of our decisions by creating a metric-driven approach. This approach relies on mathematical or statistical tools to measure and analyze certain variables and determine the best possible outcome [66]. Quantitative approaches seek to understand the underlying forces that lead to success and failure in different areas, allowing us to make decisions that provide the highest returns and lowest risks [67].

4.2. Study Tool

Current study adopted a questionnaire as a tool of study. The questionnaire is a type of survey used to collect primary data from respondents via a series of written or textual questions [68]. The collected data can be quantitative or qualitative, depending on how the questions are constructed and the types of answers respondents provide [69]; questionnaires are primarily used to measure opinions, perceptions, and attitudes such as demographic characteristics, experiences, beliefs, and opinions [70]. In current study, an online questionnaire was developed on 5-point Likert scale depending on previous studies. The questionnaire consisted of two main sections: the first took into perspective demographics of study sample (age, gender, qualification, and position), while the other section consisted of statements related to study variables including (participation, delegation, training, and reward). In its first copy, the questionnaire was presented before a group of specialists in the field for the sake of arbitration; after that, the researcher modified statements according to arbitrators’ opinions. The questionnaire in its final version consisted of (35) statements as shown in Table 1.

4.3. Population and Sample

Population of current study consisted of financial managers and managers of accounting and financial facilities in the banking sector in Jordan. Study population was defined as the entire set of objects or individuals in a study. In this case, and according to [71], population of current study included banks operating in Jordan, which are (25) banks, including (16) local Jordanian banks, divided into (13) commercial banks and (3) Islamic banks, in addition to (9) foreign banks, including (8) commercial banks, and (1) Islamic bank, according to the Central Bank of Jordan; banks operate through (818) branches and (76) offices.

Study sample is a subset of the population used to represent the population in a study [72]. Researcher chose a convenient sample in current study, which is a non-probability sampling method that involves selecting participants based on their accessibility and willingness to participate in the study. Here are some steps to develop a convenient sample:

Identify the target population: The first step was to identify the population.

Define the inclusion criteria: Define the criteria that participants must meet to be included in the study. This could include age, gender, occupation, location, or any other relevant characteristic.

Determine the sampling location: Convenience sampling involves selecting participants who are easily accessible to the researcher.

Recruit participants: Once identified the sampling location, there is a need to recruit participants. It means approaching people in person, posting an advertisement online, or sending emails to potential participants.

Collect data: After recruiting participants, the data are collected using various methods such as surveys, interviews, or observations.

It is important to note that convenience sampling may not be representative of the entire population and may lead to biased results. Therefore, researchers should carefully consider the limitations of this sampling method and the potential impact on the validity of their findings.

In current study, a convenient sample of (125) financial managers and managers of accounting and financial facilities (5) from each bank was chosen to represent population of study. After application process, researcher was able to retrieve (97) statistically valid questionnaires, indicating that the response rate was (77.6%) and statistically acceptable.

4.4. Data Screening and Analysis

Statistical Package for the Social Sciences (SPSS) was used in order to screen and analyze gathered primary data. SPSS is a statistical analysis program used by researchers in the fields of social science and business [73]. It can be used for surveys, forecasting trends, and analyzing the relationships among data sets. SPSS allows users to analyze data, discover patterns, make predictions, and generate insights that help inform decisions [74]. It can also be used for data visualizations, statistical characterizations of data, research design, and survey management [75]. Cronbach’s Alpha was utilized to determine the study’s dependability. The alpha value of each variable was acceptable since it was greater than the minimum permitted percentage of 0.70 [76]; The Table 2 summarizes the results:

Other statistical tests used in current study included:

- Mean and standard deviation.

- Frequencies and percentages.

5. Results and Discussion

5.1. Demographic Results

As according to Table 3 below, the demographics of respondents were calculated as according to frequencies and percentages; the majority of the sample was made up of males, forming 63.9% of the total sample, who were within the age range 31–36 years old, forming 41.2%. Concerning education, it was found that the majority held a BA degree in a related financial field forming, 79.4%, and were financial facilities managers, forming the majority of 58.8% of the total sample.

5.2. Questionnaire Analysis

According to Table 4, all statements and variables of the questionnaire were positively received as they all scored higher than the mean of the scale 3.00. The highest mean was scored by the variable “participation” with a mean of 3.51/4.00 compared to the lowest mean scored by delegation and training, both scoring a mean of 3.29/5.00. Regarding the statements, it was seen that all statements also scored higher than the mean of the scale 3.00; the highest scoring statement was “Management is aware that empowerment develops the relationship between leadership and employees” scoring 3.60/5.00 compared to the lowest scoring statement with 3.15/5.00, “any errors or mistakes are taken seriously for not being repeated again”.

5.3. Hypotheses Testing

As shown in Table 5, all of the aforementioned indicators fall within the allowed limits, as recommended by the given studies and references; this assures that the researcher may securely utilize the study model’s output and share the study’s findings appropriately.

As Shown in Table 6, Hypotheses testing was performed as follows:

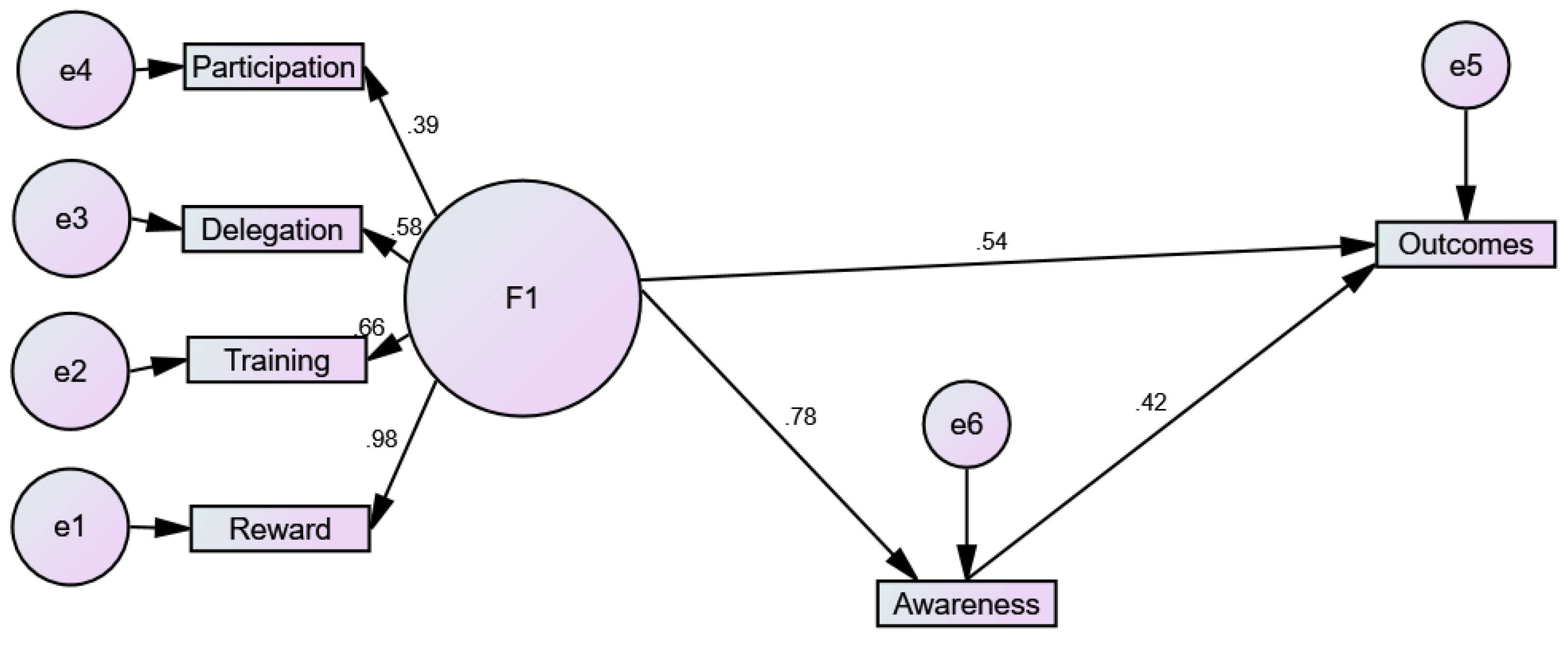

H (1).

Employee empowerment has a significant impact on management awareness.

This hypothesis is accepted (C.R. = 10.184; p < 0.05; = 0.000). This means that employee empowerment has a significant impact on management awareness.

H (2).

Management awareness has a significant impact on AIS outcomes.

This hypothesis is accepted (C.R. = 4.875; p < 0.05; = 0.000). This means that management awareness has a significant impact on AIS outcomes.

H (3).

Employee empowerment has a significant impact on AIS outcomes.

This hypothesis is accepted (C.R. = 5.577; p < 0.05; = 0.000). This means that employee empowerment has a significant impact on AIS outcomes.

H (4).

Management awareness mediates the relationship between employee empowerment and AIS outcomes.

This hypothesis is accepted (indirect impact = 0.33; p < 0.05; = 0.000). This means that management awareness mediates the relationship between employee empowerment and AIS outcomes. Figure 2 below highlighted the analysis of study model.

6. Discussion

This current research was conducted to analyze the impact of employee empowerment, which includes participation, delegation, training, and reward, on the efficiency of AIS within the banking sector in Jordan. Moreover, it aims to highlight how higher management awareness mediates the relationship between employee empowerment and AIS outcomes. The main aim of the study was reached by using a quantitative approach: a questionnaire was utilized as the main study tool and a total of (97) financial managers and managers of accounting and financial facilities in the banking sector in Jordan responded to the online questionnaire. SPSS was used to screen and analyze the gathered primary data. The results of the study indicate the following:

- H (1). Employee empowerment has a significant impact on management awareness.

- H (2). Management awareness has a significant impact on AIS outcomes.

- H (3). Employee empowerment has a significant impact on AIS outcomes.

- H (4). Management awareness mediates the relationship between employee empowerment and AIS outcomes.

6.1. Employee Empowerment Positively Influences AIS Outcomes

This study accepted the first hypothesis, which indicated that employee empowerment is significant for management awareness given that when employees are empowered to take the initiative, speak up, and make decisions, they can—in agreement with [8,9]—help create a more informed, engaged, and productive work environment. This can lead to a better understanding of the company’s goals, objectives, and current operations. By creating an atmosphere of collaboration between management and employees, a company can gain better insight into how to meet their goals and improve their operations. Additionally, by opening up the lines of communication and allowing a mutual exchange of ideas and feedback, both parties can become more aware of the organization’s strengths and weaknesses, leading to improved decision making and increased awareness of the big picture.

6.2. Managerial Awareness Mediates the Relationship between Employee Empowerment and AIS Outcomes

Regarding the relationship between management awareness and AIS outcomes, it was seen through analysis that management awareness significantly affects the outcomes of AIS. Management awareness is important for the implementation and effectiveness of AIS. This agrees with [13], referring to the fact that the role of management is critical in the successful implementation and use of these systems because they influence how these systems are used and what information they provide. When management is aware of AIS, they can make informed decisions, help ensure that the system is up to date, and help to ensure that users and the system fit the operational requirements of the business. Management awareness also ensures that the system is used properly and that decisions are based on accurate information.

As was also seen in the analysis, AIS are of tremendous importance to the banking sector; AIS enable banks to accurately track and document all financial transactions, allowing for full visibility of all financial activities. This helps banks analyze their current financial position and plan for their future. Additionally, AIS enable banks to comply with regulatory obligations and help detect and prevent fraud or other financial criminal activities. By providing timely, organized, and accurate financial information, AIS also enable banks to make informed business decisions with regards to increasing their profits, as shown by the results of [10].

This study was able to achieve results that proved that management awareness can help strengthen the relationship between employee empowerment and AIS outcomes by providing personnel with a better understanding of the necessary processes and tools needed for successful AIS implementation and use. By being aware of the processes and information involved, employees can be better equipped to correctly use AIS, have relevant insights on their specific usage, adjust the system when needed, etc. Effectively utilizing AIS can result in improved AIS outcomes. Additionally, management can provide employees with the necessary tools for success through training sessions and efficient communication channels. A greater understanding of AIS implementation, usage, and expectations can also help ensure employee alignm1ent when it comes to the desired AIS outcomes, as according to the ideas presented by [11,14].

7. Conclusions

Higher management awareness of the relationship between employee empowerment and better AIS outcomes can provide greater support and motivation to staff members. This can include increasing employee autonomy by providing more autonomy and decision-making opportunities, reducing bureaucratic or micro-managing processes, investing in employee training, and recognizing and rewarding successful outcomes. Furthermore, it can provide guidance and a framework that promotes the successful integration of AIS and processes within the organization. By taking advantage of these elements, employers can have an even greater impact on their employees’ ability to successfully implement and use AIS and ultimately achieve better outcomes.

In conclusion, management awareness plays an important role in the successful implementation and use of AIS. Without management involvement, the system may not be used to its fullest potential and may lead to inaccurate decisions or incomplete information. With management engagement, the system can provide accurate, timely information and help the business make well-informed decisions.

8. Theoretical Contribution

The theoretical contribution of examining employee empowerment’s role in supporting AIS outcomes within the banking sector, and the mediating influence of higher management awareness, can be described as follows:

- Employee empowerment: This study contributes to the existing literature on employee empowerment by examining its role in supporting AIS outcomes in the banking sector. It provides empirical evidence on the impact of employee empowerment on AIS outcomes.

- AIS outcomes: The study also contributes to the AIS literature by examining the outcomes of AIS. It identifies the key factors that affect AIS outcomes and provides insights into how employee empowerment can improve these outcomes.

- Mediating influence of higher management awareness: The study also contributes to the literature on the mediating influence of higher management awareness. It provides evidence that higher management awareness plays a critical role in mediating the relationship between employee empowerment and AIS outcomes.

- Banking sector: The study focuses specifically on the banking sector, which is an important industry in most economies; it provides insights into how employee empowerment can be used to improve AIS outcomes in the banking sector.

Overall, the theoretical contribution of this study is significant in terms of enhancing our understanding of the factors that affect AIS outcomes in the banking sector. It highlights the importance of employee empowerment within the financial institution environment, in addition to the vast and undeniable effect of managerial awareness regarding empowerment in general and employee empowerment in particular.

9. Limitations of Study

Some limitations appeared including:

Generalizability: The findings of the study may not be generalizable to other industries or contexts as the study focuses specifically on the banking sector. This may limit the applicability of the findings to other industries or sectors.

Sample size: The sample size of the study may be limited, which may impact the statistical power of the study and the ability to draw robust conclusions.

Self-report bias: The study may rely on self-reported data from employees and managers, which may be subject to biases and inaccuracies. Participants may be reluctant to report negative experiences or provide truthful responses due to social desirability bias.

Time and resource constraints: Conducting a comprehensive study on employee empowerment and accounting information system outcomes within the banking sector may require significant time and resources, which may not be feasible for all researchers.

Overall, while examining the employee empowerment role in supporting AIS outcomes within the banking sector with the mediating influence of higher management awareness can provide valuable insights, researchers should be aware of these limitations and take steps to address them.

10. Recommendations

Based on the results, discussion, and conclusion, the current study recommends the following:

- Utilize integrated cloud-based systems to increase the availability of information and reduce the need for manual data entry.

- Automate key tasks wherever possible to save time and create greater accuracy.

- Balance the security and accessibility of data so that important systems and data are protected but can still be accessed by appropriate staff and systems.

- Take advantage of interactive features for reporting and analysis.

- Implement strong audit trails to help track changes and identify potential problems.

Funding

This research received no external funding.

Informed Consent Statement

Informed consent was obtained from all subjects involved in the study.

Data Availability Statement

Not applicable.

Conflicts of Interest

The author declares no conflict of interest.

References

- Haapamäki, E.; Sihvonen, J. Cybersecurity in accounting research. Manag. Audit. J. 2019, 34, 808–834. [Google Scholar] [CrossRef]

- Nguyen, H.; Nguyen, A. Determinants of accounting information systemsAIS quality: Empirical evidence from Vietnam. Accounting 2020, 6, 185–198. [Google Scholar] [CrossRef]

- Ahmad, M.A.; Al-Shbiel, S.O. The effect of accounting information system on organizational performance in Jordanian industrial SMEs: The mediating role of knowledge management. Int. J. Bus. Soc. Sci. 2019, 10, 99–104. [Google Scholar] [CrossRef]

- Haleem, A.H.; Kevin, L.L.T. Impact of user competency on accounting information system success: Banking sectors in Sri Lanka. Int. J. Econ. Financ. Issues 2018, 8, 167. [Google Scholar] [CrossRef]

- Chen, Y.; Long, X. The Empowerment and Subversion of Information Technology to Accounting Information System. In Proceedings of the 2022 3rd International Conference on E-commerce and Internet Technology (ECIT 2022), Zhangjiajie, China, 4–6 March 2022; pp. 384–392. [Google Scholar] [CrossRef]

- Astuty, W.; Pratama, I.; Basir, I.; Harahap, J.P.R. Does Enterprise Resource Planning Lead to The Quality of The Management Accounting Information System. Pol. J. Manag. Stud. 2022, 25, 93–107. [Google Scholar] [CrossRef]

- Sivagnanasundaram, J.; Goonetillake, J.; Buhary, R.; Dharmawardhana, T.; Weerakkody, R.; Gunapala, R.; Ginige, A. Digitally-Enabled Crop Disorder Management Process Based on Farmer Empowerment for Improved Outcomes: A Case Study from Sri Lanka. Sustainability 2021, 13, 7823. [Google Scholar] [CrossRef]

- Abuzaid, A. Employees’ empowerment and its role in achieving strategic success: A practical study on Jordanian insurance companies. Jordan J. Bus. Adm. 2018, 14, 641–660. [Google Scholar]

- Lassoued, K.; Awad, A.; Guirat, R. The impact of managerial empowerment on problem solving and decision making skills: The case of Abu Dhabi University. Manag. Sci. Lett. 2020, 10, 769–780. [Google Scholar] [CrossRef]

- Andi Kele, A.T. Employee Empowerment in Luxury Hotels in East Malaysia. Ph.D. Thesis, The University of Waikato, Hamilton, New Zealand, 2020. [Google Scholar]

- Nicholls, A. A general theory of social impact accounting: Materiality, uncertainty and empowerment. J. Soc. Entrep. 2018, 9, 132–153. [Google Scholar] [CrossRef]

- Al-Hattami, H.M.; Kabra, J.D. The influence of accounting information system on management control effectiveness: The perspective of SMEs in Yemen. Inf. Dev. 2022. [Google Scholar] [CrossRef]

- Raharjono, M.A.A.; Dharmadiaksa, I.B. The Effect of Incentives and Employee Empowerment on the Effectiveness of Accounting Information SystemsAIS. Am. J. Humanit. Soc. Sci. Res. (AJHSSR) 2021, 5, 149–153. [Google Scholar]

- Al Maani, A.I.; Al Adwan, A.; Areiqat, A.Y.; Zamil, A.M.; Salameh, A.A. Level of administrative empowerment at private institution and its impact on institutional performance: A case study. Entrep. Sustain. Issues 2020, 8, 500. [Google Scholar] [CrossRef] [PubMed]

- Vu, H.M. Employee empowerment and empowering leadership: A literature review. Technium 2020, 2, 20–28. [Google Scholar] [CrossRef]

- Ghasempour Ganji, S.F.; Johnson, L.W.; Babazadeh Sorkhan, V.; Banejad, B. The effect of employee empowerment, organizational support, and ethical climate on turnover intention: The mediating role of job satisfaction. Iran. J. Manag. Stud. 2021, 14, 311–329. [Google Scholar]

- Obiekwe, O.; Zeb-Obipi, I.; Ejo-Orusa, H. Employee involvement in organizations: Benefits, challenges and implications. Manag. Hum. Resour. Res. J. 2019, 8, 1–11. [Google Scholar]

- Zaraket, W.; Garios, R.; Malek, L.A. The impact of employee empowerment on the organizational commitment. Int. J. Hum. Resour. Stud. 2018, 8, 284–299. [Google Scholar] [CrossRef]

- Hewagama, G.; Boxall, P.; Cheung, G.; Hutchison, A. Service recovery through empowerment? HRM, employee performance and job satisfaction in hotels. Int. J. Hosp. Manag. 2019, 81, 73–82. [Google Scholar] [CrossRef]

- Turkmenoglu, M.A. Investigating benefits and drawbacks of employee empowerment in the sector of hospitality: A review. Int. Res. J. Bus. Stud. 2019, 12, 1–13. [Google Scholar] [CrossRef]

- Natrajan, N.S.; Sanjeev, R.; Singh, S.K. Achieving job performance from empowerment through the mediation of employee engagement: An empirical study. Indep. J. Manag. Prod. 2019, 10, 1094–1105. [Google Scholar] [CrossRef]

- Irakoze, E.; David, K.G. Linking Motivation to Employees’ Performance: The Mediation of Commitment and Moderation of Delegation Authority. Int. Bus. Res. 2019, 12. [Google Scholar] [CrossRef]

- Bani-Melhem, S.; Quratulain, S.; Al-Hawari, M.A. Customer incivility and frontline employees’ revenge intentions: Interaction effects of employee empowerment and turnover intentions. J. Hosp. Mark. Manag. 2020, 29, 450–470. [Google Scholar] [CrossRef]

- Philip, K.; Arrowsmith, J. The limits to employee involvement? Employee participation without HRM in a small not-for-profit organisation. Pers. Rev. 2020, 50, 401–419. [Google Scholar] [CrossRef]

- Sandi, H.; Yunita, N.A.; Heikal, M.; Ilham, R.N.; Sinta, I. Relationship Between Budget Participation, Job Characteristics, Emotional Intelligence and Work Motivation As Mediator Variables to Strengthening User Power Performance: An Emperical Evidence From Indonesia Government. Morfai J. 2021, 1, 36–48. [Google Scholar] [CrossRef]

- Baird, K.; Tung, A.; Su, S. Employee empowerment, performance appraisal quality and performance. J. Manag. Control. 2020, 31, 451–474. [Google Scholar] [CrossRef]

- Seaton, F.S. Empowering teachers to implement a growth mindset. Educ. Psychol. Pract. 2018, 34, 41–57. [Google Scholar] [CrossRef]

- Nwachukwu, C.; Chládková, H.; Agboga, R.S.; Vu, H.M. Religiosity, employee empowerment and employee engagement: An empirical analysis. Int. J. Sociol. Soc. Policy 2021, 41, 1195–1209. [Google Scholar] [CrossRef]

- Andika, R.; Darmanto, S. The effect of employee empowerment and intrinsic motivation on organizational commitment and employee performance. J. Apl. Manaj. 2020, 18, 241–251. [Google Scholar] [CrossRef]

- Motamarri, S.; Akter, S.; Yanamandram, V. Frontline employee empowerment: Scale development and validation using Confirmatory Composite Analysis. Int. J. Inf. Manag. 2020, 54, 102177. [Google Scholar] [CrossRef]

- Murray, W.C.; Holmes, M.R. Impacts of employee empowerment and organizational commitment on workforce sustainability. Sustainability 2021, 13, 3163. [Google Scholar] [CrossRef]

- AlKahtani, N.; Iqbal, S.; Sohail, M.; Sheraz, F.; Jahan, S.; Anwar, B.; Haider, S. Impact of employee empowerment on organizational commitment through job satisfaction in four and five stars hotel industry. Manag. Sci. Lett. 2021, 11, 813–822. [Google Scholar] [CrossRef]

- Al-Okaily, A.; Al-Okaily, M.; Shiyyab, F.; Masadah, W. Accounting information system effectiveness from an organizational perspective. Manag. Sci. Lett. 2020, 10, 3991–4000. [Google Scholar] [CrossRef]

- Arif, D.; Yucha, N.; Setiawan, S.; Oktarina, D.; Martah, V. Applications of goods mutation control form in accounting information system: A case study in sumber indah perkasa manufacturing, Indonesia. J. Asian Financ. Econ. Bus. 2020, 7, 419–424. [Google Scholar] [CrossRef]

- Jasim, Y.A.; Raewf, M.B. Information technology’s impact on the accounting system. Cihan Univ.-Erbil J. Humanit. Soc. Sci. 2020, 4, 50–57. [Google Scholar] [CrossRef]

- HA, V.D. Impact of organizational culture on the accounting information system and operational performance of small and medium sized enterprises in Ho Chi Minh City. J. Asian Financ. Econ. Bus. 2020, 7, 301–308. [Google Scholar] [CrossRef]

- Qatawneh, A. The influence of data mining on Accounting Information System Performance: A mediating role of Information Technology Infrastructure. J. Gov. Regul. 2022, 11, 141–151. [Google Scholar] [CrossRef]

- Alshirah, M.; Lutfi, A.; Alshirah, A.; Saad, M.; Ibrahim, N.M.E.S.; Mohammed, F. Influences of the environmental factors on the intention to adopt cloud based accounting information system among SMEs in Jordan. Accounting 2021, 7, 645–654. [Google Scholar] [CrossRef]

- Lutfi, A. Factors Influencing the Continuance Intention to Use Accounting Information System in Jordanian SMEs from the Perspectives of UTAUT: Top Management Support and Self-Efficacy as Predictor Factors. Economies 2022, 10, 75. [Google Scholar] [CrossRef]

- Sarwar, M.I.; Iqbal, M.W.; Alyas, T.; Namoun, A.; Alrehaili, A.; Tufail, A.; Tabassum, N. Data vaults for blockchain-empowered accounting information systems. IEEE Access 2021, 9, 117306–117324. [Google Scholar] [CrossRef]

- Al-Ibbini, O.A. The critical success factors influencing the quality of accounting information systemsAIS and the expected performance. Int. J. Econ. Financ. 2017, 9, 162. [Google Scholar] [CrossRef]

- Amoush, A.; Saleh, I.; Khayata, K.; Al-Shalabi, F. The Impact of Accounting Information SystemsAIS Success on Professional Skepticism Empirical study at Auditing Offices in Jordan. Int. Res. J. Appl. Financ. 2018, 9, 46–66. [Google Scholar]

- Yuan, Z.; Hou, L.; Zhou, Z.; Sun, Y. The impact of accounting information quality on corporate labor investment efficiency: Evidence from China. J. Syst. Sci. Syst. Eng. 2022, 31, 594–618. [Google Scholar] [CrossRef]

- Ahad, T.; Busch, P.; Blount, Y.; Picoto, W. Mobile phone-based information systems for empowerment: Opportunities for ready-made garment industries. J. Glob. Inf. Technol. Manag. 2021, 24, 57–85. [Google Scholar] [CrossRef]

- Al-Okaily, M.; Alkhwaldi, A.F.; Abdulmuhsin, A.A.; Alqudah, H.; Al-Okaily, A. Cloud-based accounting information systemsAIS usage and its impact on Jordanian SMEs’ performance: The post-COVID-19 perspective. J. Financ. Report. Account. 2022; ahead-of-print. [Google Scholar] [CrossRef]

- Khalid, B.; Kot, M. The impact of accounting information systems on performance management in the banking sector. IBIMA Bus. Rev. 2021, 2021, 578902. [Google Scholar] [CrossRef]

- Latifah, L.; Setiawan, D.; Aryani, Y.A.; Rahmawati, R. Business strategy–MSMEs’ performance relationship: Innovation and accounting information system as mediators. J. Small Bus. Enterp. Dev. 2021, 28, 1–21. [Google Scholar] [CrossRef]

- Qatawneh, A.M.; Kasasbeh, H. Role of Accounting Information SystemsAIS (AIS) Applications on Increasing SMES Corporate Social Responsibility (CSR) During COVID-19. In Digital Economy, Business Analytics, and Big Data Analytics Applications; Studies in Computational Intelligence; Yaseen, S.G., Ed.; Springer: Cham, Switzerland, 2022; Volume 1010. [Google Scholar] [CrossRef]

- Elmets, C.A.; Leonardi, C.L.; Davis, D.M.; Gelfand, J.M.; Lichten, J.; Mehta, N.N.; Armstrong, A.; Connor, C.; Cordoro, K.M.; Menter, A. Joint AAD-NPF guidelines of care for the management and treatment of psoriasis with awareness and attention to comorbidities. J. Am. Acad. Dermatol. 2019, 80, 1073–1113. [Google Scholar] [CrossRef]

- Todaro, N.M.; Testa, F.; Daddi, T.; Iraldo, F. The influence of managers’ awareness of climate change, perceived climate risk exposure and risk tolerance on the adoption of corporate responses to climate change. Bus. Strategy Environ. 2021, 30, 1232–1248. [Google Scholar] [CrossRef]

- Wolff, C.E.; Jarodzka, H.; Boshuizen, H. Classroom management scripts: A theoretical model contrasting expert and novice teachers’ knowledge and awareness of classroom events. Educ. Psychol. Rev. 2021, 33, 131–148. [Google Scholar] [CrossRef]

- Saad, A.; Zahid, S.M.; Muhammad, U.B. Role of awareness in strengthening the relationship between stakeholder management and project success in the construction industry of Pakistan. Int. J. Constr. Manag. 2020, 22, 1884–1893. [Google Scholar] [CrossRef]

- Benoit, K.; Watanabe, K.; Wang, H.; Nulty, P.; Obeng, A.; Müller, S.; Matsuo, A. quanteda: An R package for the quantitative analysis of textual data. J. Open Source Softw. 2018, 3, 774. [Google Scholar] [CrossRef]

- Zakrzewska-Bielawska, A. The relationship between managers’ network awareness and the relational strategic orientation of their firms: Findings from interviews with Polish managers. Sustainability 2018, 10, 2691. [Google Scholar] [CrossRef]

- Thomas, G.; van Heinsbergen, M.; van der Heijden, J.; Slooter, G.; Konsten, J.; Maaskant, S. Awareness and management of low anterior resection syndrome: A Dutch national survey among colorectal surgeons and specialized nurses. Eur. J. Surg. Oncol. 2019, 45, 174–179. [Google Scholar] [CrossRef] [PubMed]

- Glezeva, N.; Chisale, M.; McDonald, K.; Ledwidge, M.; Gallagher, J.; Watson, C.J. Diabetes and complications of the heart in Sub-Saharan Africa: An urgent need for improved awareness, diagnostics and management. Diabetes Res. Clin. Pract. 2018, 137, 10–19. [Google Scholar] [CrossRef] [PubMed]

- Cao, C.; Tong, X.; Chen, Y.; Zhang, Y. How top management’s environmental awareness affect corporate green competitive advantage: Evidence from China. Kybernetes 2021, 51, 1250–1279. [Google Scholar] [CrossRef]

- Al-Okaily, M. Assessing the effectiveness of accounting information systems in the era of COVID-19 pandemic. VINE J. Inf. Knowl. Manag. Syst. 2021; ahead-of-print. [Google Scholar] [CrossRef]

- Mohapatra, M.; Mishra, S. The employee empowerment as a key factor defining organizational performance in emerging market. Int. J. Bus. Insights Transform. 2018, 12, 48–52. [Google Scholar]

- Rastogi, R.A.; Sharma, T. Quantitative analysis of drainage basin characteristics. J. Soil Water Conserv. India 2022, 26, 18–25. [Google Scholar]

- Ribeiro, J.P.; Barbosa-Povoa, A. Supply Chain Resilience: Definitions and quantitative modelling approaches–A literature review. Comput. Ind. Eng. 2018, 115, 109–122. [Google Scholar] [CrossRef]

- Jiang, Y.; Liu, J. Definitions of pseudocapacitive materials: A brief review. Energy Environ. Mater. 2019, 2, 30–37. [Google Scholar] [CrossRef]

- Al-Ababneh, M.M. Linking ontology, epistemology and research methodology. Sci. Philos. 2020, 8, 75–91. [Google Scholar]

- Dewaele, J.M. The vital need for ontological, epistemological and methodological diversity in applied linguistics. In Voices and Practices in Applied Linguistics: Diversifying a Discipline; White Rose University Press: New York, NY, USA, 2019; pp. 71–88. [Google Scholar] [CrossRef]

- Lutfi, A.; Al-Okaily, M.; Alsyouf, A.; Alsaad, A.; Taamneh, A. The impact of AIS usage on AIS effectiveness among Jordanian SMEs: A multi-group analysis of the role of firm size. Glob. Bus. Rev. 2020. [Google Scholar] [CrossRef]

- Uher, J. Quantitative data from rating scales: An epistemological and methodological enquiry. Front. Psychol. 2018, 9, 2599. [Google Scholar] [CrossRef]

- Tripp, A.M.; Hughes, M.M. Methods, methodologies and epistemologies in the study of gender and politics. Eur. J. Politics Gend. 2018, 1, 241–257. [Google Scholar] [CrossRef]

- Boparai, J.K.; Singh, S.; Kathuria, P. How to design and validate a questionnaire: A guide. Curr. Clin. Pharmacol. 2018, 13, 210–215. [Google Scholar] [CrossRef] [PubMed]

- Brace, I. Questionnaire Design: How to Plan, Structure and Write Survey Material for Effective Market Research; Kogan Page Publishers: London, UK, 2018. [Google Scholar]

- Krosnick, J.A. Questionnaire design. In The Palgrave Handbook of Survey Research; Palgrave Macmillan: Cham, Switzerland, 2018; pp. 439–455. [Google Scholar] [CrossRef]

- Majid, U. Research fundamentals: Study design, population, and sample size. Undergrad. Res. Nat. Clin. Sci. Technol. J. 2018, 2, 1–7. [Google Scholar] [CrossRef]

- Wang, X.; Cheng, Z. Cross-sectional studies: Strengths, weaknesses, and recommendations. Chest 2020, 158, S65–S71. [Google Scholar] [CrossRef] [PubMed]

- Şahin, M.; Aybek, E. Jamovi: An easy to use statistical software for the social scientists. Int. J. Assess. Tools Educ. 2019, 6, 670–692. [Google Scholar] [CrossRef]

- Jakobsen, T.G.; Mehmetoglu, M. Applied statistics using Stata: A guide for the social sciences. In Applied Statistics Using Stata; Sage: Newcastle upon Tyne, UK, 2022; pp. 1–100. [Google Scholar]

- Vuong, Q.H.; La, V.P.; Vuong, T.T.; Ho, M.T.; Nguyen, H.K.T.; Nguyen, V.H.; Pham, H.H.; Ho, M.T. An open database of productivity in Vietnam’s social sciences and humanities for public use. Sci. Data 2018, 5, 180188. [Google Scholar] [CrossRef]

- Sekaran, U.; Bougie, R. Research Methods for Business: A Skill-Building Approach, 7th ed.; John Wiley & Sons: Haddington, UK, 2016. [Google Scholar]

- Miles, J.; Shevlin, M. Effects of sample size, model specification and factor loadings on the GFI in confirmatory factor analysis. Personal. Individ. Differ. 1998, 25, 85–90. [Google Scholar] [CrossRef]

- Tabachnick, B.G.; Fidell, L.S. Using Multivariate Statistics, 5th ed.; Allyn and Bacon: New York, NY, USA, 2007. [Google Scholar]

- MacCallum, R.C.; Browne, M.W.; Sugawara, H.M. Power Analysis and Determination of Sample Size for Covariance Structure Modeling. Psychol. Methods 1996, 1, 130–149. [Google Scholar] [CrossRef]

- Hu, L.T.; Bentler, P.M. Cutoff Criteria for Fit Indexes in Covariance Structure Analysis: Conventional Criteria Versus New Alternatives. Struct. Equ. Model. 1999, 6, 1–55. [Google Scholar] [CrossRef]

Figure 2.

Model Analysis.

{kind=link}

{kind=link}

Table 1.

Distribution of statements on variables.

| Variable | # of Statements |

|---|---|

| Employee Empowerment | 5 |

| Participation | 5 |

| Delegation | 5 |

| Training | 5 |

| Reward | 4 |

| AIS Outcomes | 5 |

| Management Awareness | 6 |

Table 2.

Reliability test.

| Variable | Alpha |

|---|---|

| Participation | 0.89 |

| Delegation | 0.895 |

| Training | 0.884 |

| Reward | 0.896 |

| Management Awareness | 0.903 |

| AIS Outcomes | 0.897 |

Table 3.

Descriptive statistics of demographics.

| f | % | |

|---|---|---|

| Gender | ||

| Male | 62 | 63.9 |

| Female | 35 | 36.1 |

| Age | ||

| 25–30 | 18 | 18.6 |

| 31–36 | 40 | 41.2 |

| 37–42 | 26 | 26.8 |

| +43 | 13 | 13.4 |

| Education | ||

| BA | 77 | 79.4 |

| MA | 17 | 17.5 |

| PhD | 3 | 3.1 |

| Job | ||

| Financial Manager | 18 | 18.6 |

| Accounting Manager | 22 | 22.7 |

| Financial Facilities Manger | 57 | 58.8 |

| Total | 97 | 100.0 |

Table 4.

Questionnaire descriptive statistics.

| Statement | Mean | Std. Deviation |

|---|---|---|

| employees are engaged in every decision making | 3.59 | 1.37 |

| participation takes place according to job description | 3.54 | 1.26 |

| employees’ recommendations are taken into consideration | 3.46 | 1.16 |

| employees are exposed to all new measures all the time | 3.49 | 1.16 |

| employees are informed in all updates that takes place on AIS | 3.44 | 1.12 |

| Participation | 3.51 | 1.01 |

| All employees are delegated to take decision according to their position | 3.30 | 1.17 |

| leaders delegate a lot of tasks in order to save time and efforts | 3.21 | 0.97 |

| employees are able to access AIS platforms according to their job description | 3.18 | 0.92 |

| delegations are done with clear instructions | 3.30 | 0.94 |

| employees have the ability to take decision based on their | 3.46 | 0.95 |

| Delegation | 3.29 | 0.83 |

| ongoing orientations are done to employees on using AIS | 3.36 | 0.98 |

| Leaders are always available for directions | 3.38 | 0.99 |

| AIS applications are always up to date for employees | 3.40 | 0.96 |

| any errors or mistakes are taken seriously for not being repeated again | 3.15 | 1.18 |

| training courses and seminars on AIS applications are always available | 3.16 | 1.20 |

| Training | 3.29 | 0.89 |

| employees are rewarded based on their performance | 3.54 | 1.16 |

| lack of mistakes and errors make is always appreciated by the management | 3.48 | 1.07 |

| employees are always appreciated and rewarded for their job development | 3.39 | 1.11 |

| Employees’ ability to reach certain goals is always rewarded | 3.36 | 1.01 |

| Reward | 3.44 | 0.95 |

| employees’ empowerment developed the level of AIS outcomes | 3.58 | 0.94 |

| AIS outcomes are always up to date an shared to employees based on their tasks | 3.35 | 0.94 |

| with empowerment employees are more engaged and developed in managing AIS | 3.27 | 1.20 |

| AIS outcomes are more reliable and credible | 3.28 | 1.12 |

| Decision making is more attainable when it comes to AIS outcomes | 3.47 | 1.07 |

| AIS Outcomes | 3.39 | 0.89 |

| the management is aware of empowerment influence on AIS outcomes | 3.23 | 1.02 |

| Management makes sure that all employees get the needed orientation on AIS applications | 3.35 | 0.94 |

| Management supports leadership in empowerment efforts | 3.43 | 1.15 |

| Management appreciate the influence of empowerment on AIS outcomes | 3.41 | 1.09 |

| Management is aware that empowerment develops the relationship between leadership and employees | 3.60 | 1.01 |

| the management makes sure that all employees are aware of their role in AIS applications | 3.35 | 0.98 |

| Management Awareness | 3.40 | 0.85 |

Table 5.

Fit model.

| Indicator | AGFI | GFI | RMSEA | CFI | NFI | |

|---|---|---|---|---|---|---|

| Value Recommended | >0.8 | <5 | >0.90 | ≤0.10 | >0.9 | >0.9 |

| References | [77] | [78] | [77] | [79] | [80] | [80] |

| Value of Model | 0.83 | 4.781 | 0.935 | 0.069 | 0.919 | 0.922 |

Table 6.

Correlation.

| Direct Impact | Indirect Impact | Total Impact | C.R. | p | Result | |||

|---|---|---|---|---|---|---|---|---|

| Awareness | <--- | Employee Empowerment | 0.78 | 0.78 | 10.184 | *** | accept | |

| Outcomes | <--- | Awareness | 0.423 | 0.423 | 4.875 | *** | accept | |

| Outcomes | <--- | Employee Empowerment | 0.54 | 0.33 | 0.87 | 5.577 | *** | accept |

*** p = 0.000.

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Qatawneh, A.M. The Role of Employee Empowerment in Supporting Accounting Information Systems Outcomes: A Mediated Model. Sustainability 2023, 15, 7155. https://doi.org/10.3390/su15097155

AMA Style

Qatawneh AM. The Role of Employee Empowerment in Supporting Accounting Information Systems Outcomes: A Mediated Model. Sustainability. 2023; 15(9):7155. https://doi.org/10.3390/su15097155

Chicago/Turabian StyleQatawneh, Adel M. 2023. "The Role of Employee Empowerment in Supporting Accounting Information Systems Outcomes: A Mediated Model" Sustainability 15, no. 9: 7155. https://doi.org/10.3390/su15097155

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.