Research on the Threshold Effect of Internet Development on Regional Inclusive Finance in China

1

School of Economics and Management, Xianyang Normal University, Xianyang 712000, China

2

School of Economics and Finance, Xi’an Jiaotong University, Xi’an 710061, China

3

Business School, University of Essex, Colchester CO4 3SQ, UK

4

Finance and Data Science School, Xi’an Eurasia University, Xi’an 710199, China

*

Author to whom correspondence should be addressed.

Sustainability 2023, 15(8), 6731; https://doi.org/10.3390/su15086731

Submission received: 4 January 2023

/

Revised: 8 April 2023

/

Accepted: 11 April 2023

/

Published: 16 April 2023

(This article belongs to the Special Issue Sustainable Financing)

Abstract

:The study aims to investigate how the internet has affected China’s financial inclusion from the standpoint of developing internet technologies. Firstly, using the coefficient of variation method and the principal component analysis method, the financial inclusion index (IFI) and the internet development index (INT) were built from multiple dimensions based on the 2006–2016 provincial panel data of China. Then, the fixed-effect panel threshold model, the fixed-effect estimate, and the 2SLS estimate were used to empirically test the impact of internet development on inclusive finance in China. We found that China’s financial inclusion was significantly and positively affected by internet development. Additionally, this effect was nonlinear, and there was a threshold effect on the proportion of internet users. The development of the internet had a significant positive effect on financial inclusion when the internet user proportion (ISP) was higher than 19%, and the effect on IFI became stronger when ISP rose above 53%. This study complements earlier research, in which internet finance is usually perceived as a composite notion, by thoroughly examining the effects of internet information technology on the growth of financial inclusion. Based on our findings, we further put forward policy recommendations for the sustainable development of inclusive finance in terms of the intelligent integration and collaboration of internet communication technologies. Financial inclusion is critical for achieving sustainability because it provides access to affordable financial services to underserved individuals and businesses, and brings them into the formal financial sector, thereby improving their livelihoods while reducing poverty and inequality.

1. Introduction

The idea of financial inclusion was first proposed by the United Nations in 2005 with the goal of offering equal financial services to all societal subjects, especially small and medium-sized enterprises (SMEs), low-income groups, and farmers. China’s idea of financial inclusion was explicitly mentioned in 2013 at The Third Plenary Session of the 18th Central Committee of the Chinese Communist Party. In order to improve the system for financial inclusion, extend the reach of financial services, and promote the growth of the real economy, The State Council of the People’s Republic of China published The Plan for Promoting the Development of Financial Inclusion (2016–2020) in 2016. Mckinnon (1973) and Shaw (1973) argued that the phenomenon of financial repression would split the capital market in a country, which would have a serious negative impact on the quality and quantity of its actual capital accumulation and hinder the development of its finance. In response, the implementation of financial inclusion can realize the deepening and further development of the financial industry and optimize the allocation of financial resources through the establishment of a sound financial system, thus, alleviating financial repression [1,2].

In 1987, Robert Solow observed that despite computers’ widespread use during the 1970s and 1980s, they had little impact on productivity. This is known as the “Solow productivity paradox”, stating that there is a discrepancy between investment in information technology and productivity. Subsequent research on the “Solow productivity paradox” offered various explanations including that it takes a long time for Information and Communication Technology (ICT) and internet technology to affect the economy [3]. Wan (2006)detailed the penetration of modern computer technology into all fields of economic activity, emphasizing the financial industry, which includes banking, insurance, securities, and other sectors [4]. Applications of information technology in the financial industry include electronic payment and electronic financial systems.

At present, economic growth in China, which is in the late stage of industrialization, has slowed down significantly, and internet information technology has been assigned the role of providing a new impetus. Therefore, the promotion of the “Internet+” strategy is considered as an important measure of supply-side structural reform [5]. Internet technology can reduce transaction costs and improve the efficiency of financial transactions through the rapid dissemination of information, sharing features, and network externalities, thereby improving financial transaction platforms, serving more groups, and realizing financial inclusion faster. As a result, the comprehensive integration of internet technology into economic and social sectors, especially the financial sector, will contribute to the growth of the real economy.

For China, a crucial question is to examine how the “Internet+” project and internet development have affected inclusive finance in China. This paper first establishes that there is a significant effect and then focuses on identifying the internal mechanism responsible for this effect. Using the 2006–2016 provincial panel data in China, we found that the internet development index (INT) had a significant positive effect on the financial inclusion index (IFI). Then, we examine three potential venues through which this effect is realized, that is, reducing transaction costs, broadening transaction channels, and controlling risks.

The main contributions of the paper are: (1) In previous literature, internet finance was often regarded as a composite notion in examining its effect on financial development, while this paper focuses on the impact of internet information technology on the development of inclusive finance. (2) Through theoretical analysis and the threshold model using the internet user proportion (ISP), the diffusion effect of network externality on the development of financial inclusion was verified, providing strong evidence in support of government’s promotion of the “Internet+” action.

Financial inclusion can play an important role in achieving sustainability by improving its social aspect. It achieves this by providing underserved individuals and businesses access to affordable financial services, and bringing them into the formal financial sector, thereby reducing extreme poverty and increasing shared wealth [6]. It has been identified as an enabler for 7 out of the 17 Sustainable Development Goals (SDG) by World Bank, including eliminating extreme poverty (SDG 1), reducing hunger and achieving food security (SDG 2), promoting good health and well-being (SDG 3), fostering quality education (SDG 4), achieving gender equality and enhancing women empowerment (SDG 5), promoting shared economic growth (SDG 8) and promoting innovation and sustainable industrialization (SDG 9).

2. Literature Review

2.1. The Concept, Measurement, and Impact Factors of Financial Inclusion

The World Bank and many scholars have defined financial inclusion as the proportion of individuals and companies that have access to formal financial services. The larger this proportion in a society, the more conducive the society is to poverty reduction, to the development of sharing economy and to sustainability [6,7]. The development of financial inclusion is based on micro-finance, emphasizing the fairness and stability of financial development. It can make up for the shortcomings of the existing financial system to a certain extent, thus, better promoting economic development and increasing employment [6]. Currently, there is no unified definition of financial inclusion. A large number of scholars believe that inclusive finance is mainly about poverty alleviation. However, inclusive finance is related to a system that promotes the extensive participation of all financial institutions rather than focusing on an individual poverty alleviation institution. Therefore, it is not a simple poverty alleviation measure, but a way for banks and more financial institutions to jointly provide the financial services required by different groups of people and upgrade themselves to seek the sustainable development of marketization and commercialization. Internationally, more emphasis is placed on the role of inclusive finance in rural remote areas. This is because, compared with urban inclusive finance, rural inclusive finance faces greater challenges, higher transaction costs, and higher risks. Moreover, the financial environment constrains the expansion of financial services and their sustainable development in rural areas [8,9,10]. As an important part of the financial system, financial inclusion can effectively reduce financial service costs from both the supply and demand sides in poor areas and meet the financial needs of the majority [11]. In addition, financial inclusion not only promoted fairness and expanded the coverage of modern financial services but also improved the existing financial system [12]. Li (2018) also pointed out the relatively positive impact of financial inclusion on the improvement of individuals’ income, the optimization of the urban-rural dual structure, and the stimulation of domestic demand, which could promote the transformation of China’s economic growth pattern and sustainable economic development [13].

In the measurement of financial inclusion, Beck et al. (2007) first proposed two dimensions from the perspective of financial service, namely, availability and effectiveness [14]. Based on Beck’s research, Sarma (2008)created a multi-dimensional comprehensive financial inclusion index, which includes three dimensions: geographic penetration, financial service availability, and utility [15]. In China, researchers have constructed diversified financial inclusion index systems from different perspectives such as the density of policy-based financial loans, the density of cooperative financial loans, the basic medical insurance for urban employees, and the number of internet users [16]. For example, the four parameters of financial service penetration, availability, practicability, and affordability were created by Liu et al. (2018) based on Chinese context [17].

Known as the process of offering suitable financial services to low-income and underprivileged populations at a fair price, financial inclusion will be affected by both financial and social factors in terms of its level with the development of a country [18,19]. In other words, it is the process of ensuring that everyone, especially disadvantaged groups, has access to financial services such as deposit, withdrawal, savings, credit, and insurance in a suitable institutional and legal setting. Consequently, the development of financial inclusion will be impacted by the social economy, banking structure, and infrastructure [20,21,22,23]. Senyo and Osabutey (2020) studied the influencing elements of ownership and use of financial services by various global groups to better interpret the development process of financial inclusion [24]. According to the report, financial inclusion may be improved to varied degrees globally by increasing financial access, fostering innovation, and reducing inequality [25].

2.2. The Development of the Internet

Characterized by openness and sharing, the internet is a technological and innovative advancement with wider implications for how the economy functions. The relationship between the internet and economic growth is currently the focus of research on internet development. The widespread use of information technology has significantly contributed to global economic expansion [5,26]. The application of continuously developing information technology and resources is a crucial way to promote economic growth [27]. For one thing, the advancement of internet technology has transformed the way that commodities are traded, removed geographical and geographic distance barriers, lowered the costs of all trading links, and fundamentally increased trading efficiency [26,28]. For another, it has improved the overall economic development of the manufacturing industry and the city by promoting enterprise innovation [5]. Guo and Luo (2016) analyzed this process in detail when computers are interconnected worldwide and form a global network, the development of new technologies, new inventions, and new organizations can be promoted by accelerating information dissemination, and the operating rules of various parts of the economic chain can be changed [26]. Additionally, in light of the network effect of the internet, its effect on the economic system will be magnified instantly after the network scale reaches a critical point.

In addition, few studies have analyzed the impact of the internet on the industry. Shen et al. (2018) suggested that internet technology has changed the traditional mode of production and corporate organization, and the real economy has merged with the internet virtual economy [29]. Mugambi et al. (2014) argued that the internet economy has changed China’s existing demand structure, transformed the production mode, promoted the producer services industry, and upgraded the industrial structure [30].

2.3. The Impact of Internet Development on Financial Inclusion

Ivatury and Mas (2008) pointed out that advanced science and technology can reduce financial transaction costs and meet the financial service needs of the poor [31]. Similarly, Beck and Demirguc-Kuntand (2009) found that the use of high technology had a significant impact on the coverage of financial services in less-developed countries [7]. The internet can effectively optimize the allocation of funds, increase the operating efficiency of the financial system, reduce costs, and enhance the depth and breadth of financial services. In particular, it can provide great convenience for developing countries [32].

Information technology and internet penetration are found to be positively correlated with financial inclusion [33]. This is mainly reflected in three aspects. Firstly, they can expand information channels and enhance the concept of using financial services. Secondly, they can provide financial convenience, especially in internet finance. Thirdly, they can provide technical support for financial business innovation. According to Senyo and Osabutey (2020), internet information and communication technology not only expands the boundaries of financial services but also effectively reduces the cost of financial services, thus contributing to the sustainable commercial development of inclusive finance [24]. In practice, it is found that internet finance can serve groups in third-tier and fourth-tier cities, rural areas, and remote areas. Furthermore, World Bank (2018) proved the positive impact of internet penetration on financial inclusion and pointed out the spiraling upward trend of digital financial inclusion [34]. In areas with high population density and strong financial awareness, the development of digital financial inclusion is better. In addition, the use of the internet can greatly enhance the development capacity of digital financial inclusion, with the influence going far beyond geography and financial awareness.

The diffusion effect of network externality, which is related to information technology, can be demonstrated by Moore’s Law and Metcalfe’s Law. Firstly, according to Moore’s Law, the combination of computing telecommunication indices with the growth of computing power, data storage, data availability, and electronic interconnectivity, which irreversibly changed the way financial markets operate and became a breakthrough in the development of the financial market [35]. Secondly, Shapiro and Varian (1999) indicated that Metcalfe’s law shows the external effect of the network [36]. Generated based on each internet user, the value of the network is proportional to the number of users. The more internet users there are, the greater the value of the network and its impact on the outside world.

3. Theoretical Analysis

In the era of “Internet+”, with the continuous development of technology, the role of the internet has become more than a medium that conveys information. Currently, it is highly integrated with daily life and economic activities [37], which has changed the modern lifestyle and the operation mode of economic sectors.

According to Romer’s endogenous growth theory, internet technology promotes economic growth through innovation processes such as the acceleration of information dissemination [38,39]. Internet broadband infrastructure may be different from other types of infrastructure. The characteristic of the internet in accelerating economic development can be understood as the diffusion effect of the network. When the penetration rate of the internet reaches a certain level, its influence on economic development will be gradually magnified.

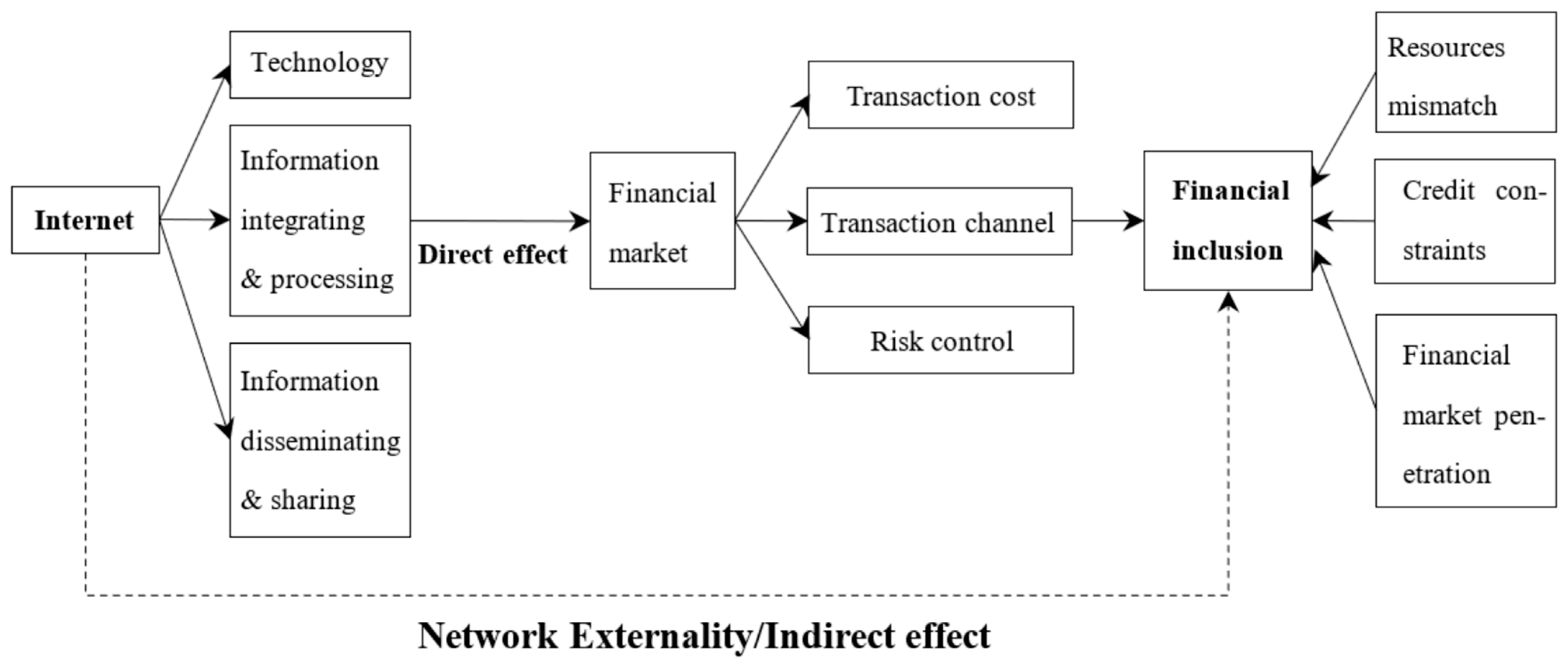

Huang et al., (2019) suggested that the external financial system implanted into the real economy to support rapid economic development is gradually disappearing in China, while the emergence of financial inclusion is inherent in the financial demand of the real economy, which can better serve the real economy sector [5]. With the support of internet technology, transactions between financial organizations have gradually changed. Thus, the financial market has been improved in three aspects: transaction costs, transaction channels, and risk control, with the diffusion effect finally affecting financial inclusion (Figure 1).

3.1. The Impact of the Internet on Financial Transaction Cost

The financial market mainly aims to provide a platform for transactions between buyers and sellers, with a continuous and relatively stable structure [40]. However, the traditional financial market has shortcomings such as basic information asymmetry and high transaction costs, which reduce the market transaction efficiency. Based on transaction cost analysis, Lohrke et al. (2006) studied the extent to which SMEs can use the internet to connect directly with customers and confirmed the significant advantages of internet use in lowering transaction costs of SMEs [41]. As financial inclusion introduced new practices and players to the space of poverty finance [42], the transition of technology-supported financial intermediation was recognized as a key to poverty reduction. The emergence of the internet has prompted the excessive development of the financial market towards a non-intermediary financial market and stimulated it to approach the Walras general equilibrium. There are two ends of the changing financial market. One is the traditional agency market, and the other is the unmediated financial market corresponding to the Walras general equilibrium. The financial transaction and organizational form under the internet are between the two ends. This form of unmediated finance can reduce the additional transaction costs caused by information asymmetry. By sharing information, the internet can greatly reduce the cost of obtaining information, making it possible for financial institutions to achieve disintermediation. This can gradually eliminate the unequal transaction model established by financial intermediaries relying on information asymmetry and special channels in the traditional market environment. In the study of the changes in transaction costs brought about by internet use in inter-enterprise transactions, Garicano and Kaplan (2001) found potential for large process improvements and market gains [43]. One of the significant goals of financial inclusion is to enable financial institutions to serve the real economy by eliminating agencies, thereby reducing transaction costs and maintenance costs and achieving economies of scale and cost control.

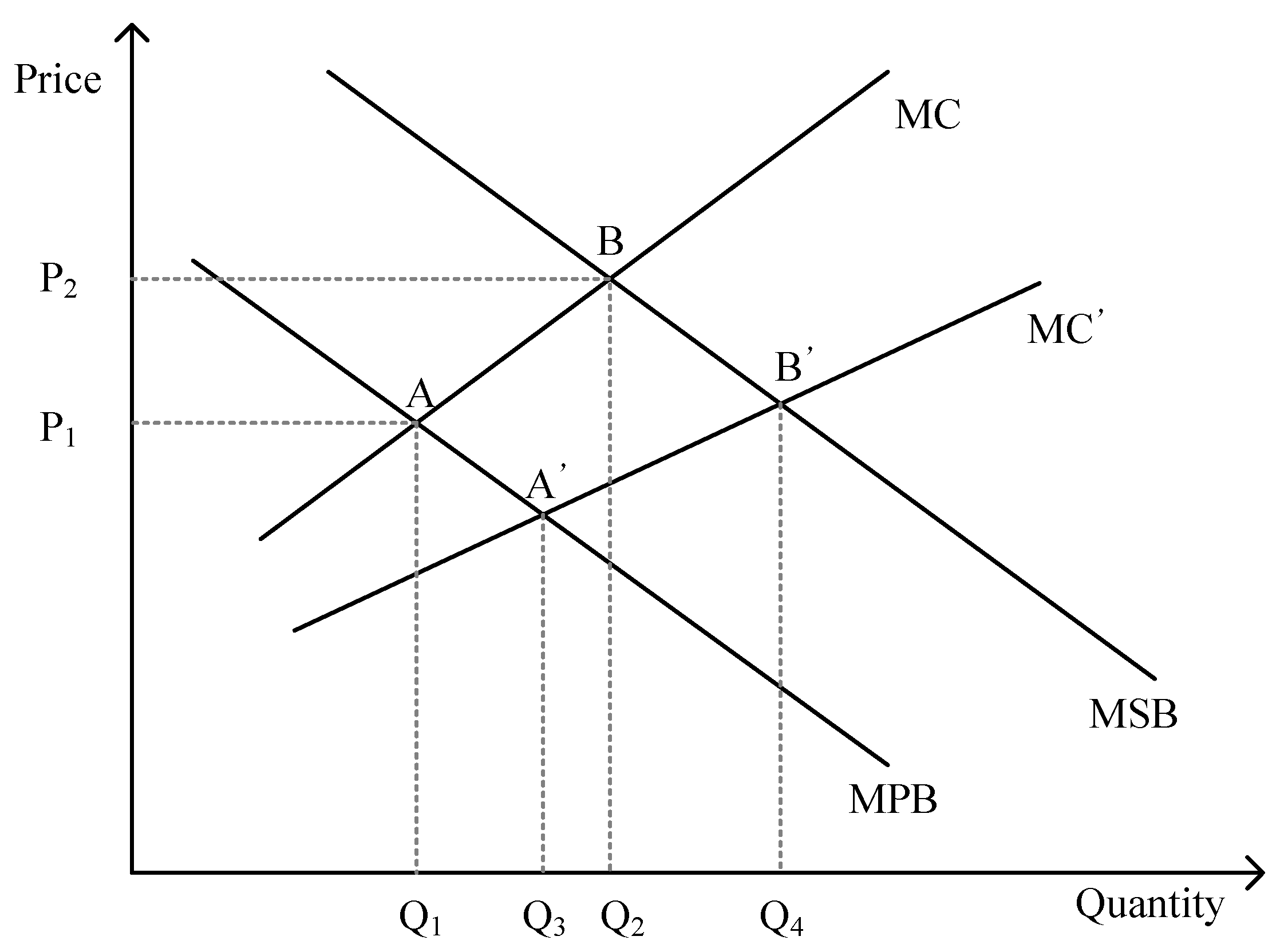

The impact mechanism of internet development can also be explained using the marginal cost and marginal benefit curve. In Figure 2, the line MPB illustrates financial institutions’ private marginal benefit and MSB represents the social marginal benefit. The marginal costs of the private sector and society are the same, illustrated by the line MC under the initial conditions. When considering positive externality, the optimum point for private financial institutions is A, the intersection of MPB and MC, and the corresponding quantity and price is Q1 and P1, respectively. However, for the whole society, the optimum point is B, the intersection of MSB and MC, and the corresponding quantity and price is Q2 and P2, respectively. When the role of internet information technology is added to the overall economic environment, information can be obtained more efficiently and tasks will be performed at a lower cost, which can reduce social and private marginal costs. As a result, the new private and social marginal cost curves will fall to MC’. For society, a reduction in marginal cost curve leads to a new optimum B’ at the intersection of MSB and MC’, which means that the socially optimal supply increases to Q4. Additionally, for the private sector, the new optimal supply increased to Q3. This means that under the influence of the internet, both the private optimal supply and the social optimal supply have been improved to varying degrees. It should also be noted that, in addition to the direct downward shift of the MC curve, due to the economies of scale and network economic effects brought about by internet, the reduction in marginal cost will be greater at higher levels of quantity. That is, the slope of the MC curve will become smaller, causing the difference between private and social optimum to widen as MC decreases. It is clear that the actual impact on the private and social optimum depends on the slope of both the marginal benefit and cost functions.

3.2. The Impact of the Internet on Financial Transaction Channels

The financial market is the source of corporate power, as well as the platform where production, sales, and capital are controlled [44]. Traditional financial market platforms include banks, insurance companies, and securities companies. In the actual operation of these platforms, services for SMEs and poor people are often neglected, which hinders the development of the financial industry. Despite the small amount of funds in a single transaction of these groups, the total amount is considerable. By contrast, internet technology has broadened the financial trading platform, forming a sharing economy and inclusive finance under the new trading platform. Using fully modified ordinary least squares (LM-OLS) and causal analysis, Vincent et al., (2019) examined internet use and mobile subscriptions related to financial inclusion and financial sector development in China, India, Nigeria, and South Africa over the period 2009–2017 [45]. Their empirical findings demonstrate that internet use has greatly promoted the growth of inclusive finance and the financial sector. Evans (2018) and Lenka et al., (2018) investigated the connection and causality between the internet, mobile phones, and inclusive finance in Africa and the South Asian Regional Association, respectively. They found a significant correlation between the use of the internet and mobile devices and inclusive finance [46,47]. Therefore, more people now have access to inclusive finance due to advancements in the internet and mobile technology. In the context of the internet, the current financial market is a platform for matching and exchanging capital endowments with broader access conditions. With the rise of internet finance, some innovative financial services such as P2P online loans and crowdfunding have broken the geographical boundaries. Due to their low thresholds, more people in need of financial support have been served.

3.3. The Impact of the Internet on Financial Risk Control

In the traditional financial industry, the credit risk caused by information asymmetry has always plagued both parties of the transaction. During the credit assessment, the lender needs to conduct due diligence on the borrower. After the funds are lent, follow-up tracking is still required to manage the repayment ability of the borrower. However, traditional risk control is time-consuming and labor-intensive, and may be accompanied by serious management omissions. In addition, it is difficult for SMEs lacking credit records to access credits. If internet information technology is fully popularized, valid information of individuals and enterprises will be stored in internet clients. According to Ozili’s (2021) discussion on big data and financial inclusion, contemporary information technology has improved the efficiency and risk management level of financial services companies [48]. This enables the credit and profitability of individuals and businesses to be assessed accurately and quickly, and solves the problem of credit risk caused by information asymmetry. During credit evaluation, financial institutions can improve processing efficiency and alleviate the credit crisis in the risk control link based on the big data collected through internet cloud computing. After solving these two problems, a win-win situation for both supply and demand sides can be achieved, thereby promoting the development of inclusive finance.

Based on the effect of the internet on the above three points, we propose our first hypothesis:

Hypothesis 1.

The overall development of the internet has a positive impact on China’s financial inclusion.

3.4. The Impact of the Internet on Financial Inclusion through the Diffusion Effect of Network Externality

Financial activities supported by internet technology are more conducive to the prominence and effectiveness of financial substance and financial functions [45]. In terms of access to credit support and credit constraints, financial inclusion under the “Internet+” strategy is also more beneficial to SMEs [49,50]. Katz and Shapiro (1985) highlighted the network technology diffusion effect of the internet [51]. Additionally, the various ways that the diffusion effect of the internet contributes to financial inclusion have been extensively discussed in previous literature [52,53]. Thus, the network utility of the internet may play a role in the development of financial inclusion in China. We then propose our second hypothesis:

Hypothesis 2.

The development of the internet has a network effect on the development of inclusive finance, which is nonlinear and has a threshold.

4. Data and Methods

4.1. Data

The data used in this paper were collected from the Website of the National Bureau of Statistics of China, China’s regional financial operation reports issued by the People’s Bank of China, and the WIND database. Our study spanned from 2006 to 2016. Since some data were missing in the calculation of the IFI, we used interpolation to calculate the index based on the existing data. To increase the robustness of estimates, we also excluded those observations with extreme values, obtaining a balanced panel of 31 provinces, municipalities, and autonomous regions and 341 observations in total.

4.2. Financial Inclusion Index (IFI)

We referred to the indicators of Sarma (2008) to measure IFI and used the coefficient of variation method to determine the weights [15]. It is important to note that the coefficient of variation approach was adopted here as it can assess markers of relative variability and enable accurate comparisons of variables regardless of their correlation [54]. In order to quantify the variability of supply and demand, the coefficient of variation approach was employed in this study to calculate IFI. Our IFI definition includes two dimensions of supply and demand and eight indicators such as business coverage, service availability, and service quality in the financial and insurance industries. Details about the index system are shown in Table 1.

In order to objectively reflect the different contributions of each indicator to the index, the coefficient of variation method was adopted in this study to determine the weight of each indicator. The specific steps are shown below:

(1) Firstly, in order to avoid the differences caused by the inconsistency of the dimension of each indicator, we standardized each indicator based on the following equation:

where the initial value of the jth (j = 1, 2,…, m) index in the ith (i = 1, 2,…, n) sample is , represents the dimensionless indicator after standardization, represents the minimum value of each indicator, and represents the maximum value of each indicator.

(2) Secondly, we calculated the coefficient of variation of each indicator , which can be obtained by dividing the standard deviation by the mean .

Then, we added the coefficient of variation of each indicator together to obtain the weight of each indicator and multiplied the weight of each indicator by the standardized indicator data denoted as .

Finally, using the Euclidean distance method, we calculated the IFI of 31 provinces in China from 2006 to 2016. The formula is as follows:

According to Equation (1), the value range of IFI is between 0 and 1. The larger the value is, the better the development of financial inclusion in the province will be. However, it should be noted that IFI is only a relative index and cannot fully represent the specific development level of financial inclusion in the province.

4.3. Internet Development Index (INT)

Referring to the internet development index developed by Huang et al. (2019) [5], we chose four dimensions of internet output, internet-related practitioners, internet infrastructure, and mobile internet users to measure INT. The details are shown in Table 2.

First of all, it is necessary to determine whether there are significant and positive correlations between the four indicators. The results are shown in Table 3, suggesting that there are significant and positive correlations between the four indicators observed. We normalized the four indicators and performed the Kaiser-Meyer-Olkin (KMO) test and Bartlett’s test of sphericity. Bartlett’s sphericity test provided a significance of 0.000, demonstrating the existence of significant correlations between the variables. Furthermore, the KMO measure was above 0.6, which indicates that the sample is sufficient for the application of principal component analysis (Table 4) [55,56]. The principal components are shown in Table 5. We kept the first two components, which explained about 77% of the variation in the data, as they exceed unity according to Kaiser’s rule. Finally, we calculated the first two principal components and weighted them using their proportions (0.504 and 0.267 in Table 5) to calculate the INT indicator.

In this paper, the proportion of internet users in the region (ISP) was chosen as the threshold variable, which was calculated by dividing the number of internet users in the area by the total population of the area.

4.4. Control Variables

Fiscal Expenditure (Lngov): Yu and Deng, (2021) claimed that the level of regional financial development would be affected by marketization, the environment, and the government system [57]. Fiscal expenditure allows funds to flow from the government to various sectors of society, consequently changing the resource allocation structure and affecting financial allocation. In order to alleviate financial pressure, some local governments will increase their intervention in the allocation of financial resources and strive to allocate credit resources to state-owned enterprises. The logarithm of the total amount of the local government’s financial expenditure was used in this paper to measure the government’s situation.

Urbanization (Urban): The construction and development of urbanization are inseparable from finance, and there is an interdependent relationship between urbanization and financial development. In the process of urbanization, the constant upgrade of infrastructure requires a lot of financial support, driving the development of inclusive finance. When the population continues to flow to cities, the transfer of labor resources from the primary industry to the secondary and tertiary industries will also promote the development of the financial service industry. Therefore, urbanization can affect the development of financial inclusion. We used the proportion of the urban population to the total population in each province to measure the urbanization level of the province.

Industrial Structure (Str): In order to promote economic growth, the upgrading of the industrial structure is inevitable, which affects financial development by transforming labor-intensive products into capital- and technology-intensive products. Goldsmith(1969) found a mutual promotion relationship between financial development, economic growth, and industrial restructuring from a dynamic perspective [58]. Therefore, the ratio of tertiary production to GDP was used in this paper to measure the level of the industrial structure.

Foreign direct investment (LnFDI): Foreign direct investment can reflect international direct investment behavior by the spillover effect. In recent years, “The Belt and Road Initiatives” have promoted the foreign trade of SMEs. Foreign direct investment and commercial banks jointly provide various financing services for enterprises and promote the development of inclusive finance. Therefore, the logarithm of the annual actual balance of foreign direct investment in each province was chosen as an indicator in this paper to measure the level of foreign investment. Since the data provided by the Wind database is in USD, we converted it to RMB according to the annual average exchange rate of U.S. dollars published by the State Administration of Foreign Exchange of the People’s Republic of China.

Financial development (Cre): With the continuous development and improvement of the financial market system, the channels for people to obtain funds continue to increase. As an important part of the entire financial market, financial inclusion will also be affected in terms of its development levels. Credit business, which is one of the main businesses of the financial industry, can effectively reflect the degree of financial development. Therefore, in this paper, the ratio of domestic and foreign currency loan balance to GDP was used to represent the degree of financial development.

4.5. Empirical Strategy

4.5.1. Baseline Model

Based on the theoretical analysis, in order to verify the impact of INT on IFI, we established the baseline model by referring to the equation proposed by Lenka and Barik (2018) [47]:

Among them, i stands for province and t stands for time. IFI is the financial inclusion index, which was calculated from two dimensions of supply and demand with eight indicators. INT represents the provincial development index. refers to a set of control variables. is the time-invariant unobservable within each province, which was used to control the fixed effect in the province. was used to control the time fixed effect. represents the random disturbance term.

4.5.2. Threshold Model

According to the theoretical analysis part, the internet has a network diffusion effect, which may present a non-linear relationship with IFI. Referring to the threshold panel model proposed by Hansen (1999) [59], we further constructed the following threshold model based on Equation (2) to measure the network diffusion effect of INT on IFI:

where is an indicator function (take 1 if the conditions in parentheses are satisfied; take 0 if not), is the threshold variable, the proportion of internet users, and is the specific threshold value. In Equation (3), it is assumed that there is only one threshold. However, there may be multiple thresholds in the estimation, which can be deduced from Equation (3). The double threshold effect model is shown as follows:

4.5.3. Robustness and Endogeneity

To ensure the robustness of model results, we replaced the core explanatory variable with the value of L-INT, which is the one-period lag of INT, to observe whether the empirical results would change.

In order to alleviate the endogeneity problem, we first selected the authoritative database to obtain the data. Secondly, the control variables were added, and the fixed-effect model was adopted. However, due to possible reverse causality and omitted variable bias, we attempted to address the endogeneity problem using two-stage least squares. Referring to the method of Nunn and Qian (2014) [60], we chose two instrumental variables: the fixed telephone penetration rate and the post office coverage rate multiplied by the total number of post and telecommunications services. First of all, according to infrastructure, areas with high levels of landline penetration and a large number of post offices may also have high levels of internet penetration. Secondly, according to the current development situation of the financial industry and the communication industry, the number of landlines and post offices has little impact on IFI and meets the exclusivity requirement.

5. Results

5.1. Descriptive Statistics

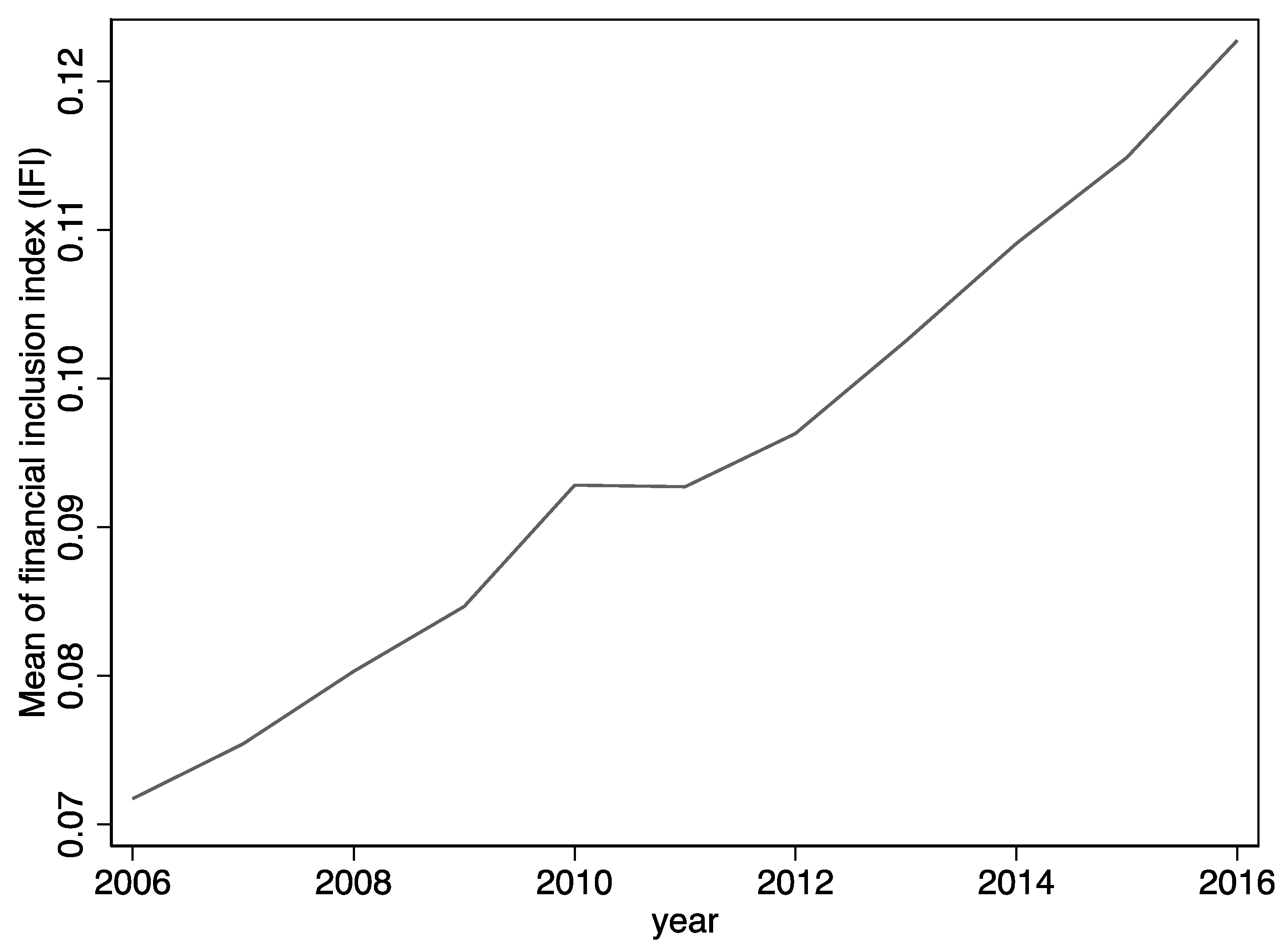

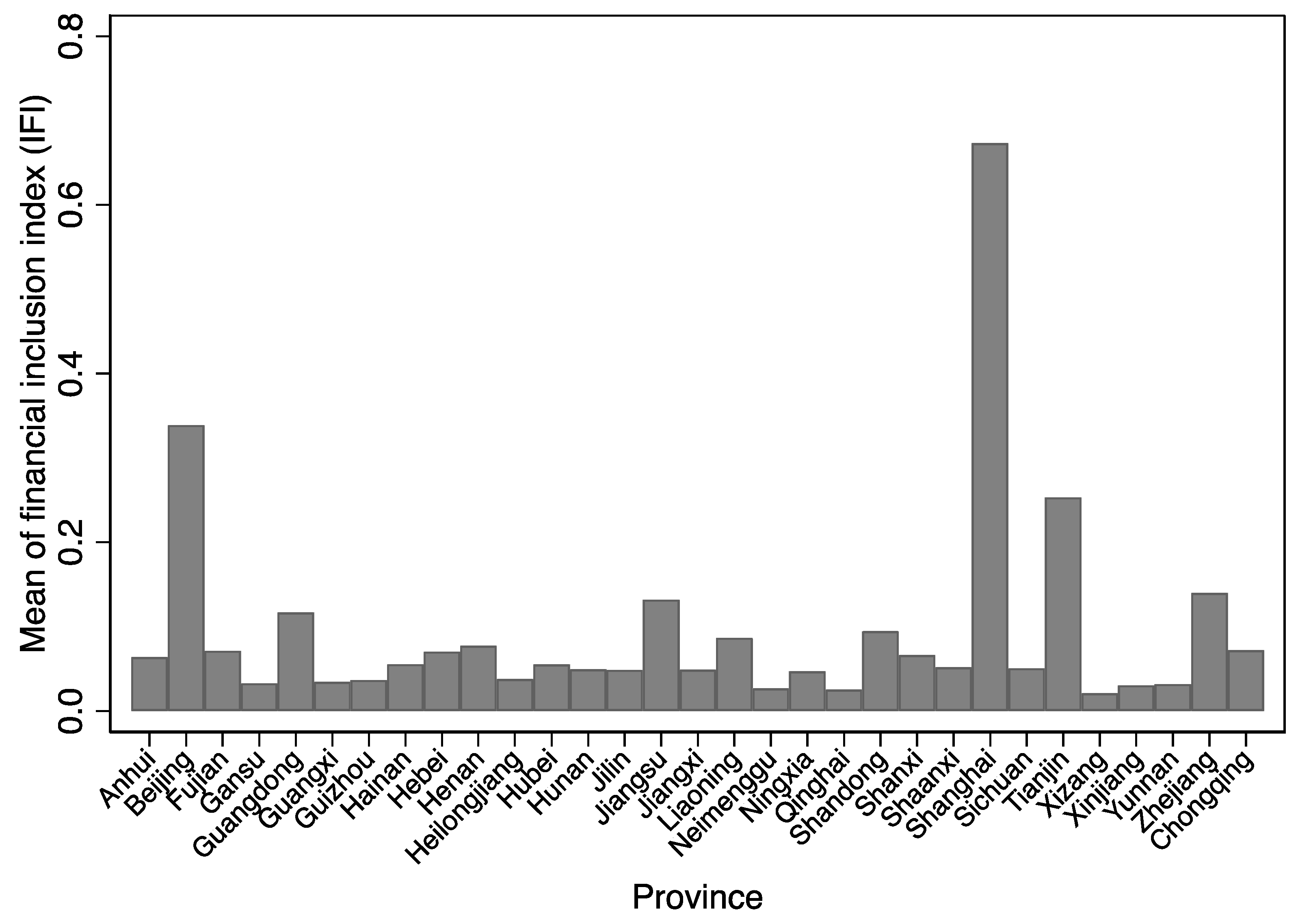

As Figure 3 shows, the average value of IFI kept increasing from 2006 to 2016. Varying greatly across provinces, the average value of INT was particularly high in megacities such as Beijing and Shanghai, indicating that there might be heterogeneity between cities in later analysis (Figure 4). The average logarithm of the total amount of the local government’s financial expenditure was 7.352, and the average logarithm of the annual actual balance of FDI was 3.405. Additionally, on average, the provincial proportion of the urban population, the ratio of tertiary production to GDP, and the ratio of domestic and foreign currency loan balance to GDP were 52.2%, 42.2%, and 116.3%, respectively (Table 6).

5.2. Impact of INT on IFI

Table 7 presents the baseline results, demonstrating a positive and significant impact of INT on IFI (coefficient = 0.025, p < 0.01). Among the control variables, urbanization (Urban) and the degree of financial development (Cre) had an inhibitory effect on IFI at the 1% and 5% significance levels, respectively. Government fiscal expenditure was negatively correlated with IFI, but the correlation was not statistically significant. The urbanization level showed a negative impact on IFI, which may be caused by the unbalanced development of different regions under the dual economic structure of urban and rural areas in China. There was a significant negative correlation between the level of credit business and IFI, which may be due to the large proportion of poor people in China and the incomplete coverage of financial services. Moreover, due to risk considerations, financial institutions dominated by banks hindered this group of people from accessing financial services, thus inhibiting the development of financial inclusion. In addition, the impact of industrial structure (Str) and foreign direct investment (LnFDI) was significantly positive at the 10% and 1% significance levels, which is consistent with the previous analysis. Thus, Hypothesis 1 can be verified, indicating that the overall development of the internet has a positive promotion effect on China’s financial inclusion. Our results are in line with many early findings in this area. The growth of the internet has a tremendous impact on the banking industry. Moreover, macro and micro economies have been influenced by the usage of the internet and mobile devices in varying degrees, and under these influences, the growth effect on inclusive finance emerged [61,62,63,64].

5.3. Threshold Estimation

According to Hansen’s research, ISP was chosen as the threshold variable in this study. We conducted the threshold effect test to determine the optimal number of thresholds. Table 8 shows the F-statistic and p-value obtained from 300 bootstraps under the assumption of a triple threshold. The findings demonstrate the significance of the single threshold and double threshold tests at the 1% and 5% levels, respectively. In order to test the internet threshold effect, the double-threshold model was used.

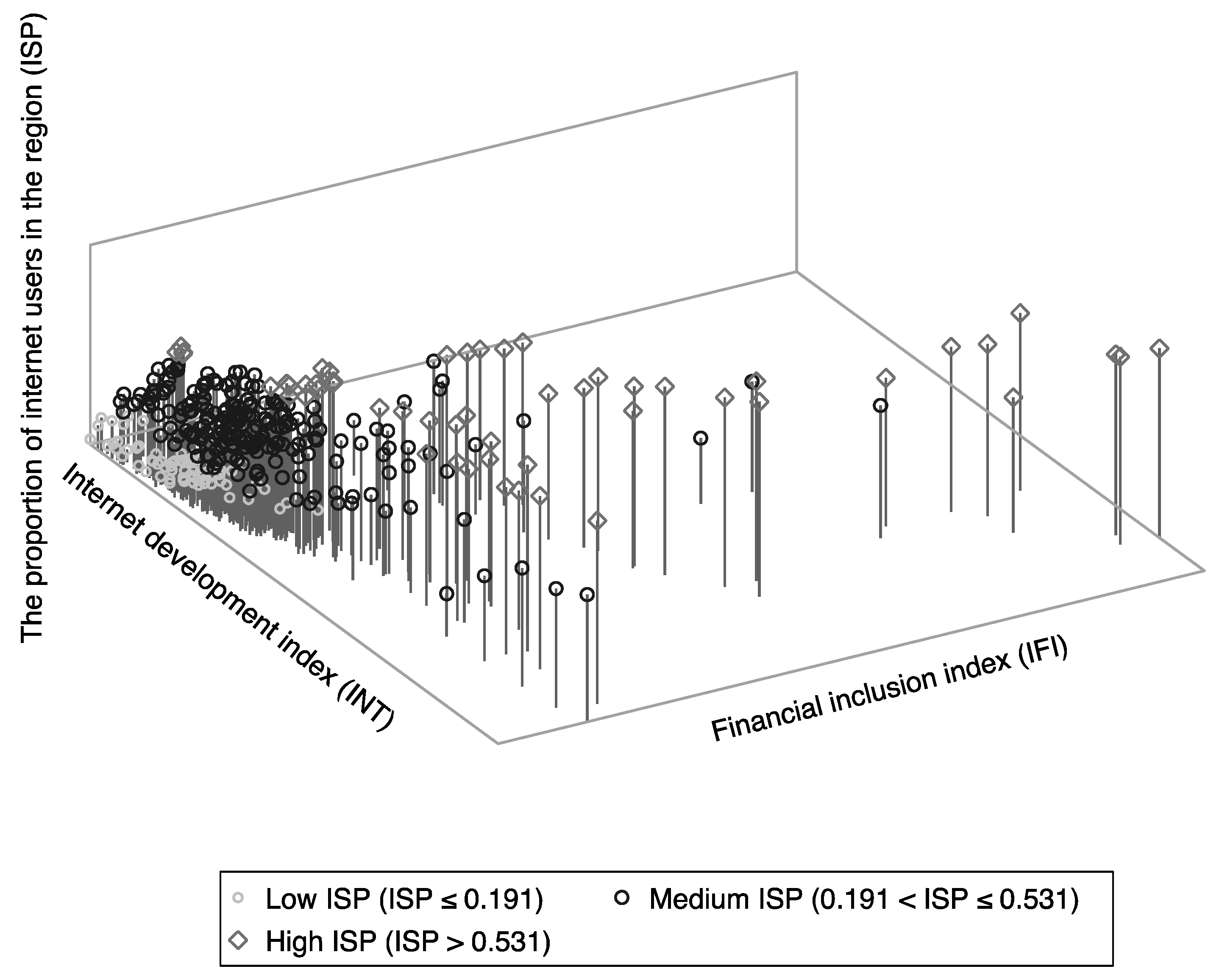

The estimated two threshold values were 0.191 and 0.531, respectively (Table 9). According to the threshold results, the proportion of internet users can be divided into three different intervals: the lower level (ISP ≤ 0.191), the middle level (0.191 < ISP ≤ 0.531), and the higher level (ISP > 0.531). Figure 5 depicts the relationship between INT and IFI under the three intervals. It shows a significant nonlinear relationship, indicating that the threshold regression results obtained above are reliable.

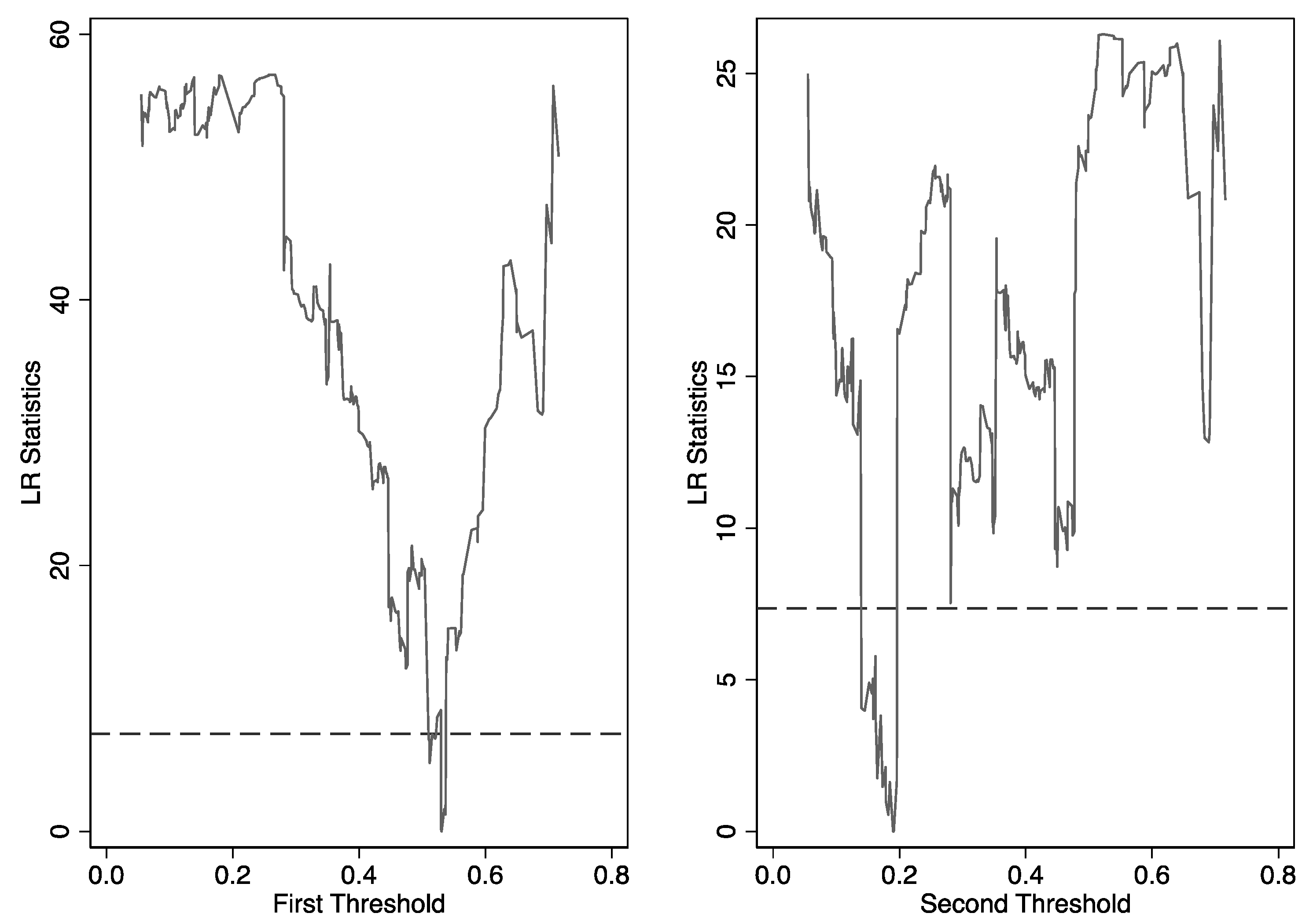

In order to provide more thorough test information, Figure 6 illustrates the LR statistic of two thresholds. The horizontal dashed line indicates the 95% confidence level, and the ordinate corresponding to each point on the curve presents the probability ratio of the threshold value. The curve represents each threshold value’s line of search points. The confidence interval at the 95% confidence level is where the dashed line and the curve intersect. The more accurate the threshold estimate was and the narrower the confidence interval was, the smaller the influence of unobserved factors would be.

We then analyzed the fixed-effect double-threshold model, and the regression results are shown in Table 10. For the control variables, except for the degree of financial development (Cre), all the remaining control variables showed a significant impact on IFI. According to the test and the threshold value, the diffusion effect of the network on IFI can be preliminarily confirmed. When the proportion of internet users was low (ISP ≤ 0.191), the coefficient of INT was 0.002 and insignificant, indicating that the low degree of internet development has no significant promotion effect on IFI. When ISP reached the medium scale (0.191 < ISP ≤ 0.531), the INT coefficient was 0.017 and significantly positive at the 1% level, which means that with the development of information network technology and the improvement of internet popularity, the development degree of the internet has a positive effect on IFI. When ISP reached a high scale level (ISP > 0.531), the INT was significantly positive at the 1% level, with a coefficient of 0.032, which is higher than the medium level, which confirms that with the improvement of the internet penetration rate, the impact of INT on IFI is gradually magnified. The results are consistent with the findings of Li et al. (2022) [65], Liu et al. (2021) [66], and Su et al. (2021) [67] that the popularization of internet technology facilitates trans-regional finance and produces a network spillover effect on inclusive finance. Thus, Hypothesis 2 can be verified, suggesting that the promotion effect of internet development on financial inclusion is nonlinear and has network externality.

5.4. Robustness and Endogeneity Tests

In the robustness test, the core explanatory variable INT in baseline regression was replaced by the one-period lag of INT to verify the reliability of the regression results. The instrumental variables were selected to deal with endogeneity problems through 2SLS regression. The specific results are shown in Table 11. After replacing INT with L-INT, the regression result became consistent with the baseline (coefficient = 0.011, p < 0.01). For the 2SLS estimation, the regression passed the weak instrumental variable test (RKF) and exogenous test, indicating that our instrumental variables are exogenous and effective. The coefficient of INT was still significantly positive for the promotion of IFI (coefficient = 0.012, p < 0.01), which is consistent with our baseline regression and, in turn, verifies our hypothesis.

6. Conclusions

Based on the 2006–2016 provincial panel data, this paper investigated the effect of internet development on financial inclusion. Theoretical analysis suggests that the growth of the internet can raise the level of financial inclusion through three venues: transaction costs, transaction channels, and risk management. In the empirical analysis, we not only measured provincial IFI in China using the coefficient of variation method but also constructed INT through principal component analysis. The results show that INT plays a significant positive role in promoting IFI. Moreover, because of network externality, INT has a threshold effect on IFI. When ISP exceeded the threshold of 0.531, its impact on IFI was found to be accelerated.

The above theoretical analysis and empirical tests lay a factual foundation for China’s internet technology to support the development of financial inclusion. On the basis of the above conclusions, the following policy recommendations are proposed. Firstly, every effort should be made to develop internet communication technology and improve information infrastructure platforms in various regions. Secondly, the integration and collaboration between the internet and the financial industry should be enhanced, and product innovation should be stimulated. Thirdly, the supervision and management system should improve to effectively control and prevent the occurrence of financial risks. More details about the policy proposals are provided as follows.

6.1. To Develop Internet Communication Technology and Expand the Coverage of Communication Infrastructure Platforms Vigorously

The modernization of hardware technology will be necessary for the development of internet communication technology in the future, followed by the development of human resources. Possessing the most advanced internet infrastructure in the world, China attaches great importance to the advancement of internet technology and promotes the construction of its 5G infrastructure steadily. To some extent, mastering 5G technology can influence how the world develops. It was anticipated that this technology would be fully commercialized in 2020, which will raise China’s overall GDP level. Hence, building quality infrastructure is the prerequisite for the development and application of 5G technology. The installation of cables and platforms should completely encircle both urban and rural areas, increase mobile network coverage throughout China, and concentrate on isolated regions with outdated internet infrastructure. The focus should be placed on developing support personnel and service networks, so as to advance China’s internet technology in all areas and help the entire country to step into the “Internet+” age.

6.2. To Promote Intelligent Integration and Collaboration between the Internet and the Financial Industry

The development of inclusiveness is the core of financial inclusion. The issue of insufficient branches and infrastructure in the process of financial development can be resolved through the incorporation of internet technologies. Supporting financial inclusion is essential to the growth of the real economy. The influence of the internet on internet technology financial inclusion is not only reflected through the technological change, but also through the change in the business mode of the whole financial industry. It is also a catalyst for the maintenance of sustainable business development. Therefore, we should first promote the integration of internet technology and the financial industry, combining industrial information automation and internet technology with the financial industry to make the latter more intelligent. Secondly, the government should introduce relevant policies to encourage the professional development of the digital financial industry, improve transaction efficiency, promote innovation in financial products based on internet technology, and broaden the channels of financial services. As outlined in the United Nations SDG, “financial inclusion” refers to the provision of financial services to all segments of society at prices that are affordable using technology [68]. Financial technology is the key driver for financial inclusion, while financial inclusion is the basis for sustainable balanced development [69]. Beyond that, financial inclusion enables people to handle their financial obligations in an effective and sustainable manner, thereby improving the allocation of existing financial resources to support sustainable development and expanding the resources available in the financial system, both of which can, in turn, support the Sustainable Development Goals [70]. Ultimately, with the goals of improving the coverage rate, availability, and satisfaction of financial services, a sustainable and efficient inclusive financial system can be built, with the payment system, credit system and capital market as the infrastructure and the legal system as the institutional assurance.

6.3. To Improve the Supervision and Management System to Prevent Financial Risks

Although internet technology has contributed to new opportunities for the development of financial inclusion, there are many hidden risks. Emerging online finance generally lacks a formal and systematic supervision mechanism due to its low entry threshold, which will increase the possibility of financial risks. Accordingly, the paper gives the following suggestions. Firstly, the relevant government departments should grant licenses to institutions engaged in internet finance to reduce the possibility of risks from the source. Secondly, given the sharing nature of internet information, more attention should be paid to the privacy of institutions and customers. The information supervision and management systems need to be improved, and the information grouping management technology engine should be popularized in financial inclusion. In order to coordinate the development of the internet and financial inclusion, the government must define the framework for integrating the financial sector and create a single security management mechanism. In this way, the inclusiveness of financial services can be expanded under the conditions of sharing information, high efficiency, high convenience, and safe transactions.

On the other hand, this study on the connection between inclusive finance and the internet still has certain limitations. First of all, the research was only undertaken in a single nation, which may be difficult to generalize to other developing countries. Future research could expand to other developing countries and include financial inclusion, digital currencies, and the Internet of Things (IoT). Secondly, due to data limitations, and the fact that there is no unified definition of internet development and inclusive finance, the method and data we used to create indicators in this study may lead to measurement error. Thus, future studies require more appropriate and updated data.

Author Contributions

Conceptualization, M.W.; Methodology, C.Z.; Formal analysis, C.Z.; Resources, C.Z.; Data curation, C.Z.; Writing—original draft, Q.L.; Writing—review & editing, D.M. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Informed consent was obtained from all subjects involved in the study.

Data Availability Statement

The data that support the findings of this study are openly available in OSF at https://osf.io/5ydxc.

Conflicts of Interest

The authors declare no conflict of interest.

References

- McKinnon, R.I. Money and Capital in Economic Development; Brookings Institution: Washington, DC, USA, 1973. [Google Scholar]

- Shaw, E.S. Financial Deepening in Economic Development; Oxford University Press: London, UK, 1973. [Google Scholar]

- Solow, R.M. We’d better watch out. New York Times Book Rev. 1987, 36, 36. [Google Scholar]

- Wan, H.A. Electronic Financial Services: Technology and Management; Chandos: Oxford, UK, 2006. [Google Scholar]

- Huang, Q.H.Y.; Yu, Y.; Zhang, S.L. Internet development and productivity growth in manufacturing industry: Internal mechanism and China experiences. China Ind. Econ. 2019, 8, 5–23. (In Chinese) [Google Scholar]

- World Bank Group. Global Financial Development Report 2014: Financial Inclusion; World Bank Publications: Washington, DC, USA, 2013. [Google Scholar]

- Beck, T.; Demirgüç-Kunt, A. Access to Finance: An Unfinished Agenda. World Bank Res. Obs. 2008, 22, 383–396. [Google Scholar] [CrossRef]

- Conning, J.; Udry, C. Chapter 56 Rural Financial Markets in Developing Countries. In Handbook of Agricultural Economics; Elsevier B.V: Amsterdam, The Netherlands, 2007; Volume 3, pp. 2857–2908. [Google Scholar] [CrossRef]

- Meyer, R.L. Subsidies as an Instrument in Agricultural Development Finance: A Review; World Bank Group: Washington, DC, USA, 2011. [Google Scholar]

- Lopez, T.; Winkler, A. The challenge of rural financial inclusion-evidence from microfinance. Appl. Econ. 2018, 50, 1555–1577. [Google Scholar] [CrossRef]

- Churchill, S.A.; Marisetty, V.B. Financial inclusion and poverty: A tale of forty-five thousand households. Appl. Econ. 2020, 52, 1777–1788. [Google Scholar] [CrossRef]

- Mohan, R.; Ray, P. Indian Financial Sector: Structure, Trends and Turns. IMF Work. Pap. 2017, 17, 1. [Google Scholar] [CrossRef]

- Li, L. Financial inclusion and poverty: The role of relative income. China Econ. Rev. 2018, 52, 165–191. [Google Scholar] [CrossRef]

- Beck, T.; De La Torre, A. The Basic Analytics of Access to Financial Services. Financ. Mark. Inst. Instrum. 2007, 16, 79–117. [Google Scholar] [CrossRef]

- Sarma, M. Index of Financial Inclusion; Finance Working Paper 22259; East Asian Bureau of Economic Research: Canberra, Australia, 2008. [Google Scholar]

- Liang, P.; Guo, S. Social interaction, internet access and stock market participation—An empirical study in China. J. Comp. Econ. 2015, 43, 883–901. [Google Scholar] [CrossRef]

- Liu, Y.; Ding, L.; Li, Y.; Hu, Z. Measurement of China’s inclusive finance development level and economic growth effect. China Soft Sci. 2018, 3, 36–46. (In Chinese) [Google Scholar]

- Lal, T. Impact of financial inclusion on economic development of rural households in northern states of India. Indian J. Econ. 2018, 99, 173–192. [Google Scholar]

- Prasannakumari, K.T. Financial Inclusion through Micro Finance: The way to Rural Development. A Case Study of Rajapalayam Block in Virudhunagar District. KKIMRC Int. J. Res. Financ. Account. 2011, 1, 94–115. [Google Scholar]

- Demirguc-Kunt, A.; Klapper, L.; Singer, D. Financial Inclusion and Legal Discrimination against Women: Evidence from Developing Countries. World Bank Policy Res. Work. Pap. 2013. [Google Scholar] [CrossRef]

- Ozili, P. Theories of Financial Inclusion. SSRN 2020, 89–115. [Google Scholar] [CrossRef]

- Kling, G.; Pesqué-Cela, V.; Tian, L.; Luo, D. A theory of financial inclusion and income inequality. Eur. J. Financ. 2022, 28, 137–157. [Google Scholar] [CrossRef]

- Huang, R.; Kale, S.; Paramati, S.R.; Taghizadeh-Hesary, F. The nexus between financial inclusion and economic development: Comparison of old and new EU member countries. Econ. Anal. Policy 2021, 69, 1–15. [Google Scholar] [CrossRef]

- Senyo, P.K.; Osabutey, E.L.C. Unearthing antecedents to financial inclusion through FinTech innovations. Technovation 2020, 98, 102155. [Google Scholar] [CrossRef]

- Morsy, H. Access to finance-Mind the gender gap. Q. Rev. Econ. Financ. 2020, 78, 12–21. [Google Scholar] [CrossRef]

- Guo, J.T.; Luo, P.L. Does the internet have a positive effect on China’s total factor productivity? Manag. World 2016, 10, 34–49. (In Chinese) [Google Scholar]

- Donovan, K. Mobile money for financial inclusion. Inf. Commun. Dev. 2012, 61, 61–73. [Google Scholar]

- Brynjolfsson, E.; Smith, M.D. Frictionless Commerce? A Comparison of Internet and Conventional Retailers. Manag. Sci. 2000, 46, 563–585. [Google Scholar] [CrossRef]

- Shen, Y.; Hu, W.; Hueng, C.J. The Effects of Financial Literacy, Digital Financial Product Usage and Internet Usage on Financial Inclusion in China. MATEC Web Conf. 2018, 228, 05012. [Google Scholar] [CrossRef]

- Mugambi, A.; Njunge, C.; Yang, S.C. Mobile-Money Benefits and Usage: The Case of M-PESA. IT Prof. 2014, 16, 16–21. [Google Scholar] [CrossRef]

- Ivatury, G.; Mas, I. The Early Experience with Branchless Banking; CGAP Focus Note, No. 46; World Bank Group: Washington, DC, USA, 2008. [Google Scholar]

- Claessens, S.; Glaessner, T.; Klingebiel, D. Developments in global e-finance. J. Financ. Transform. 2001, 2, 53–59. [Google Scholar]

- Diniz, E.; Birochi, R.; Pozzebon, M. Triggers and barriers to financial inclusion: The use of ICT-based branchless banking in an Amazon county. Electron. Commer. Res. Appl. 2012, 11, 484–494. [Google Scholar] [CrossRef]

- World Bank Group. Financial Inclusion on the Rise, but Gaps Remain, Global Findex Database Shows. Available online: https://www.worldbank.org/en/news/press-release/2018/04/19/financial-inclusion-on-the-rise-but-gaps-remain-global-findex-database-shows (accessed on 28 March 2023).

- Kirilenko, A.A.; Lo, A.W. Moore’s Law versus Murphy’s Law: Algorithmic Trading and Its Discontents. J. Econ. Perspect. 2013, 27, 51–72. [Google Scholar] [CrossRef]

- Shapiro, C.; Varian, H.R. Information Rules: A Strategic Guide to the Network Economy; Harvard Business School Press: Boston, MA, USA, 1999. [Google Scholar]

- Klein, M.; Mayer, C. Mobile Banking and Financial Inclusion: The Regulatory Lessons; The World Bank: Washington, DC, USA, 2011. [Google Scholar]

- Romer, M.P. Endogenous Technological Change. J. Political Econ. 1990, 98, 71–102. [Google Scholar] [CrossRef]

- Czernich, N.; Falck, O.; Kretschmer, T.; Woessmann, L. Broadband Infrastructure and Economic Growth. Econ. J. 2011, 121, 505–532. [Google Scholar] [CrossRef]

- Keister, L.A. Financial markets, money, and banking. Annu. Rev. Sociol. 2002, 28, 39–61. [Google Scholar] [CrossRef]

- Lohrke, F.T.; Franklin, G.M.; Frownfelter-Lohrke, C. The internet as an information conduit: A transaction cost analysis model of US SME internet use. Int. Small Bus. J. 2006, 24, 159–178. [Google Scholar] [CrossRef]

- Mader, P. Card crusaders, cash infidels and the Holy Grails of digital financial inclusion. Behemoth-A J. Civilis. 2016, 9, 59–81. [Google Scholar]

- Garicano, L.; Kaplan, S. The Effects of Business-to-Business E-Commerce on Transaction Costs. J. Ind. Econ. 2001, 49, 463–485. [Google Scholar] [CrossRef]

- Mizruchi, M.S.; Stearns, L.B. Getting Deals Done: The Use of Social Networks in Bank Decision-Making. Am. Sociol. Rev. 2001, 66, 647–671. [Google Scholar] [CrossRef]

- Vincent, O.; Evans, O. Can cryptocurrency, mobile phones, and internet herald sustainable financial sector development in emerging markets? J. Transnatl. Manag. 2019, 24, 259–279. [Google Scholar] [CrossRef]

- Evans, O. Connecting the poor: The internet, mobile phones and financial inclusion in Africa. Digit. Policy Regul. Gov. 2018, 20, 568–581. [Google Scholar] [CrossRef]

- Lenka, S.K.; Barik, R. Has expansion of mobile phone and internet use spurred financial inclusion in the SAARC countries? Financ. Innov. 2018, 4, 5. [Google Scholar] [CrossRef]

- Ozili, P. Big Data and Artificial Intelligence for Financial Inclusion: Benefits and Issues. SSRN Electron. J. 2021. [Google Scholar] [CrossRef]

- Bianchi, M. Credit constraints, entrepreneurial talent, and economic development. Small Bus. Econ. 2010, 34, 93–104. [Google Scholar] [CrossRef]

- Karaivanov, A. Financial constraints and occupational choice in Thai villages. J. Dev. Econ. 2012, 97, 201–220. [Google Scholar] [CrossRef]

- Katz, M.L.; Shapiro, C. Network externalities, competition, and compatibility. Am. Econ. Rev. 1985, 75, 424–440. [Google Scholar]

- Chatterjee, A.; Das, S. Information communication technology diffusion and financial inclusion: An inter-state analysis for India. Innov. Dev. 2021, 11. [Google Scholar] [CrossRef]

- McKay, C.; Pickens, M. Branchless Banking 2010: Who’s Served? At What Price? What Next? CGAP focus Note, No. 66; World Bank Group: Washington, DC, USA, 2010. [Google Scholar]

- Bedeian, A.G.; Mossholder, K.W. On the Use of the Coefficient of Variation as a Measure of Diversity. Organ. Res. Methods 2000, 3, 285–297. [Google Scholar] [CrossRef]

- Olawale, F.; Garwe, D. Obstacles to the growth of new SMEs in South Africa: A principal component analysis approach. Afr. J. Bus. Manag. 2009, 4. [Google Scholar]

- Shrestha, N. Factor analysis as a tool for survey analysis. Am. J. Appl. Math. Stat. 2021, 9, 4–11. [Google Scholar] [CrossRef]

- Yu, M.; Deng, X. The Inheritance of Marketization Level and Regional Human Capital Accumulation: Evidence from China. Financ. Res. Lett. 2021, 43, 102268. [Google Scholar] [CrossRef]

- Goldsmith, R.W. Financial Structure and Development; Yale U.P: New Haven, CT, USA; London, UK, 1969. [Google Scholar]

- Hansen, B.E. Threshold effects in non-dynamic panels: Estimation, testing, and inference. J. Econom. 1999, 93, 345–368. [Google Scholar] [CrossRef]

- Nunn, N.; Qian, N. US Food Aid and Civil Conflict. Am. Econ. Rev. 2014, 104, 1630–1666. [Google Scholar] [CrossRef]

- Alderete, M.V. Mobile broadband: A key enabling technology for entrepreneurship? J. Small Bus. Manag. 2017, 55, 254–269. [Google Scholar] [CrossRef]

- Bertschek, I.; Niebel, T. Mobile and more productive? Firm-level evidence on the productivity effects of mobile internet use. Telecommun. Policy 2016, 40, 888–898. [Google Scholar] [CrossRef]

- Kpodar, K.; Andrianaivo, M. ICT, Financial Inclusion, and Growth Evidence from African Countries. IMF Work. Pap. 2011, 11. [Google Scholar] [CrossRef]

- Pathak, A.; Gupta, A. Digitisation and Development: Macro Relation and Micro Experience. In Proceedings of the 10th International Conference on Theory and Practice of Electronic Governance, ICEGOV 2017, New Delhi, India, 7–9 March 2017. [Google Scholar]

- Li, Y.; Wang, M.; Liao, G.; Wang, J. Spatial Spillover Effect and Threshold Effect of Digital Financial Inclusion on Farmers’ Income Growth—Based on Provincial Data of China. Sustainability 2022, 14, 1838. [Google Scholar] [CrossRef]

- Liu, X.; Zhu, J.; Guo, J.; Cui, C. Spatial Association and Explanation of China’s Digital Financial Inclusion Development Based on the Network Analysis Method. Complexity 2021, 2021, 1–13. [Google Scholar] [CrossRef]

- Su, Y.; Li, Z.; Yang, C. Spatial Interaction Spillover Effects between Digital Financial Technology and Urban Ecological Efficiency in China: An Empirical Study Based on Spatial Simultaneous Equations. Int. J. Environ. Res. Public Health 2021, 18, 8535. [Google Scholar] [CrossRef]

- Ahamed, M.M.; Mallick, S.K. Is financial inclusion good for bank stability? International evidence. J. Econ. Behav. Organ. 2019, 157, 403–427. [Google Scholar] [CrossRef]

- Arner, D.W.; Buckley, R.P.; Zetzsche, D.A.; Veidt, R. Sustainability, FinTech and financial inclusion. Eur. Bus. Organ. Law Rev. 2020, 21, 7–35. [Google Scholar] [CrossRef]

- Klapper, L.; Lusardi, A. Financial literacy and financial resilience: Evidence from around the world. Financ. Manag. 2020, 49, 589–614. [Google Scholar] [CrossRef]

Figure 1.

The Underlying Mechanism of Internet Development’s Impact on Financial Inclusion.

Figure 2.

Internet Development, Financial Supply Cost, and Optimal Supply. Note: MPB = marginal private benefit, MSB = marginal social benefit, and MC = marginal cost.

Figure 2.

Internet Development, Financial Supply Cost, and Optimal Supply. Note: MPB = marginal private benefit, MSB = marginal social benefit, and MC = marginal cost.

Figure 3.

Average Value of Financial Inclusion Index (IFI) over Time.

Figure 4.

Average Value of Financial Inclusion Index (IFI) across Provinces.

Figure 5.

Scatter plot of the correlation between IFI and INT.

Figure 6.

Likelihood Ratio (LR) statistic of two thresholds.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Table 1.

Financial Inclusion Index (IFI) in China.

| Dimensions | Indicators | Indicator Nature |

|---|---|---|

| Supply | Number of financial institutions per 10,000 km2 | + |

| Number of employees in financial institutions per 10,000 km2 | + | |

| Number of financial institutions per 10,000 people | + | |

| Number of employees in financial institutions per 10,000 people | + | |

| Demand | Ratio of domestic and foreign currency deposits to GDP | + |

| Ratio of domestic and foreign currency loans to GDP | + | |

| Insurance density (Insured amount per capital) | + | |

| Insurance depth (Insurance income/GDP) | + |

Table 2.

Internet Development Index (INT) System.

| Dimensions | Indicators |

|---|---|

| Internet output | Total telecom services |

| Internet-related employees | Proportions of information transmission, computer services, and software industry employees in the total of employees |

| Internet infrastructure | Length of long-distance optical cable per 10,000 km |

| Mobile internet users | Number of mobile phones per 100 people |

Table 3.

Correlation Matrix.

| Internet Output | Internet-Related Employees | Internet Infrastructure | Mobile Internet Users | |

|---|---|---|---|---|

| Internet output | 1.000 | |||

| Internet-related employees | 0.052 | 1.000 | ||

| Internet infrastructure | 0.408 *** | 0.268 *** | 1.000 | |

| Mobile internet users | 0.202 *** | 0.578 *** | 0.452 *** | 1.000 |

Note: *** p < 0.01.

Table 4.

KMO and Bartlett’s Test.

| Kaiser-Meyer-Olkin (KMO) Measure of Sampling Adequacy | 0.603 | |

|---|---|---|

| Bartlett’s test of sphericity | Approximate chi-square | 278.838 |

| Degree of freedom | 6 | |

| p-value | 0.000 | |

Table 5.

Principal Components.

| Component | Eigenvalue | Proportion | Cumulative |

|---|---|---|---|

| Comp1 | 2.017 | 0.504 | 0.504 |

| Comp2 | 1.068 | 0.267 | 0.771 |

| Comp3 | 0.534 | 0.134 | 0.905 |

| Comp4 | 0.381 | 0.095 | 1.000 |

Table 6.

Descriptive Statistics (2006–2016).

| Variable | Obs. | Mean | S.D. | Min. | Max. |

|---|---|---|---|---|---|

| IFI | 341 | 0.095 | 0.127 | 0.011 | 0.823 |

| INT | 341 | −0.000 | 0.995 | −1.662 | 3.733 |

| Lngov | 341 | 7.352 | 0.352 | 6.242 | 8.129 |

| Urban | 341 | 0.522 | 0.150 | 0.210 | 1.020 |

| Str | 341 | 0.422 | 0.090 | 0.286 | 0.802 |

| LnFDI | 341 | 3.405 | 0.662 | 1.509 | 4.767 |

| Cre | 341 | 1.163 | 0.425 | 0.537 | 2.648 |

Table 7.

Fixed-effect Estimates of INT on IFI in China.

| Variable | Coefficient | Robust S.E. | 95% CI | |

|---|---|---|---|---|

| INT | 0.025 *** | 0.009 | 0.007 | 0.043 |

| Lngov | −0.033 | 0.042 | −0.119 | 0.052 |

| Urban | −0.596 *** | 0.140 | −0.882 | −0.310 |

| Str | 0.141 * | 0.080 | −0.023 | 0.305 |

| LnFDI | 0.040 *** | 0.014 | 0.012 | 0.069 |

| Cre | −0.009 ** | 0.004 | −0.017 | −0.000 |

| R2 | 0.774 | |||

| F | 65.90 *** | |||

| Obs. | 341 | |||

Note: * p < 0.1, ** p < 0.05, *** p < 0.01.

Table 8.

Test for threshold effects: Fixed-effect panel threshold model.

| Threshold | F | p-Value | Critical Value | ||

|---|---|---|---|---|---|

| 10% | 5% | 1% | |||

| Single | 92.57 | 0.000 *** | 26.674 | 34.333 | 51.996 |

| Double | 26.96 | 0.050 ** | 20.846 | 25.469 | 48.976 |

| Triple | 10.90 | 0.690 | 35.053 | 39.842 | 59.023 |

Note: The results obtained after 300 bootstraps. ** p < 0.05, *** p < 0.01.

Table 9.

Threshold estimates: Fixed-effect panel threshold model.

| Internet User Proportion (ISP) | Threshold | 95% CI | |

|---|---|---|---|

| ISP1 | 0.531 | 0.530 | 0.535 |

| ISP2 | 0.191 | 0.164 | 0.196 |

Table 10.

Double threshold estimates of INT on IFI in China.

| Variable | Coefficient | Robust S.E. | 95% CI | |

|---|---|---|---|---|

| Lngov | 0.081 *** | 0.017 | 0.047 | 0.115 |

| Urban | −0.484 *** | 0.145 | −0.780 | −0.187 |

| Str | 0.162 *** | 0.050 | 0.060 | 0.263 |

| LnFDI | 0.041 *** | 0.011 | 0.019 | 0.064 |

| Cre | 0.001 | 0.004 | −0.007 | 0.008 |

| INT | ||||

| ISP ≤ 0.19 | 0.002 | 0.005 | −0.009 | 0.013 |

| 0.19 < ISP ≤ 0.53 | 0.017 *** | 0.006 | 0.006 | 0.029 |

| ISP > 0.53 | 0.032 *** | 0.009 | 0.013 | 0.051 |

| R2 | 0.798 | |||

| F | 80.35 *** | |||

| Obs. | 341 | |||

Note: *** p < 0.01.

Table 11.

Robustness test and 2SLS estimate of INT on IFI in China.

| Variables | FE | 2SLS |

|---|---|---|

| (1) | (2) | |

| L-INT | 0.011 *** | - |

| (0.004) | ||

| INT | - | 0.012 *** |

| (0.004) | ||

| Kleibergen–Paap rk LM p-value | - | 0.0002 |

| Kleibergen–Paap rk Wald F statistic | - | 211.735 |

| Hansen J p-value | - | 0.364 |

| Obs. | 341 | 341 |

Note: Robust standard errors are in parentheses. *** p < 0.01.

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Zhang, C.; Li, Q.; Mao, D.; Wang, M. Research on the Threshold Effect of Internet Development on Regional Inclusive Finance in China. Sustainability 2023, 15, 6731. https://doi.org/10.3390/su15086731

AMA Style

Zhang C, Li Q, Mao D, Wang M. Research on the Threshold Effect of Internet Development on Regional Inclusive Finance in China. Sustainability. 2023; 15(8):6731. https://doi.org/10.3390/su15086731

Chicago/Turabian StyleZhang, Chenjing, Qiaoge Li, Di Mao, and Mancang Wang. 2023. "Research on the Threshold Effect of Internet Development on Regional Inclusive Finance in China" Sustainability 15, no. 8: 6731. https://doi.org/10.3390/su15086731

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.