Why Corporate Sustainability Is Not Yet Measured

1

Rotterdam School of Management, Erasmus University, 3062 PA Rotterdam, The Netherlands

2

D.S. Centre for Economic Policy Research, London EC1V ODX, UK

*

Author to whom correspondence should be addressed.

Sustainability 2023, 15(7), 6275; https://doi.org/10.3390/su15076275

Submission received: 4 March 2023

/

Revised: 20 March 2023

/

Accepted: 28 March 2023

/

Published: 6 April 2023

(This article belongs to the Section Economic and Business Aspects of Sustainability)

Abstract

:Measuring Corporate Sustainability (CS) has been identified as an important enabler for integrating sustainability into corporate practices. Different methodologies and frameworks for measuring CS have been developed in the literature with limited success, as reflected by the lack of application in the real world. Among practitioners, the effort has been on developing frameworks that provide useful indicators of the different items that need to be considered for integrating sustainability. Notwithstanding the increasing attention and progress on the subject, a cohesive and applicable measure of CS across firms, industries and geographies is still missing. This paper provides an examination of the different methodologies for measuring CS, with an analysis of their merits and limitations, as well as guidance for future research focus. The findings show a failure to coherently link the mathematical measurement and data aggregation methodologies to a well-constructed concept where the linkage between the defining features and causal relations are appropriately identified. The proposed models and mathematical techniques are not able to inform on the extent to which a corporation acts sustainably because sustainability is not being measured in its highest extension, making the results narrow, non-referential and non-comparable. Furthermore, there is confusion between developing the indicators of CS, providing their measurement and enabling their integration.

1. Introduction

1.1. Background

Corporate sustainability (CS) is becoming mainstream thinking in business management and performance evaluation. The concept of CS is complex in nature and has a wide scope. Pazienza et al. [1] performed an ontological analysis and a necessary condition analysis to clarify the concept of CS and provide convergence for its definition: Corporate sustainability is a new business model that requires attention to the Environmental, Social and Economic dimensions to provide for current and future generations [1]. Businesses need to move from an outdated sense of fast profits at the expense of the environment to a more mutual interdependence of eco-system innovation. Sustainable development advocates for environmental standards, social integrity and economic well-being, and it should be effective as an organizing criterion for internal business betterment strategies [2]. It is widely accepted that performance measurement is a prerequisite for further improvement of decision making in business management [3,4]. Decision makers are aware of the need for a systematic sustainability evaluation approach for assessing complex systems to replace linear and pre-formatted solutions [5]. Adams et al. [6] stressed that the increasing care in sustainable performance evaluation reflects the pressure on organizations to improve sustainable development. Given that key stakeholders will reward or penalize corporations based on their CS activities and impacts, which may threaten firm survival, managers are increasingly paying attention to CS activities and devoting additional resources to assess and report CS performance [7]. Evaluation of corporate sustainability performance is a significant issue and has strategic importance for every company [8]. The inability of accounting systems to capture sustainability-related information creates a profound disconnect between reporting and current ecological issues [9,10]. Companies use sustainability reports to portray themselves as ‘good’ corporate citizens, even when they do not have strong records [11]. Companies that only report about their financial performance are unlikely to survive in the long term [12]. Even when CS practices are not yet required by law, the stakes of not communicating sustainable progress are too high. The existing performance measurements overlook the economic dimension. Companies still publish two independent reports which give an incomplete and biased picture of CS performance. There is a need to minimize ambiguity and work towards the standardization and consistency of measures. Caiado et al. [13] stated that sustainability must be adopted in the entirety of the company and inform periodically. Sustainability is now seen as the business paradigm of the 21st century. There is increasing pressure from various stakeholder groups to consider the social and environmental consequences of companies’ operations [14,15]. In 2019, Silva et al. [16] conducted a survey on stakeholders’ expectations of sustainability performance measurement and assessment. The study revealed that many stakeholders deem current sustainability performance measurement and assessment insufficient for their needs.

Despite the extensive attention from industrial enterprises, international organizations and researchers, questions remain as to how sustainability should be evaluated. In the process of learning and adapting to a new paradigm of doing business, managers are missing a tested and generally accepted framework to guide decisions towards a sustainable strategy and implementation. Knowledge on which corporate sustainability aspects should be considered to account for performance measurement is still limited [12]. Corporate sustainability evaluation is complex because it deals with a large number of interrelated criteria and many of them are qualitative in nature. Moreover, uncertainties in scoring and weighting criteria always exist [17]. Measuring and improving industrial sustainability are therefore crucial issues [18], as well as foreseeing sustainability as a major competitive factor [19,20]. Despite the progress, standardized methods are still missing [21,22,23], as are complete and simple tools. In order to properly address corporate sustainability, a holistic approach should be adopted that accounts for interrelations among the economic, social and environmental dimensions [24,25,26]. The increasing complexity calls for new approaches and research, and has significant implications for how decision making is framed [27].

1.2. Objectives

In this study, we aim to identify the strengths and weaknesses of the existing methodologies for measuring corporate sustainability. While there is a diversity of inquiries in the literature on measuring corporate sustainability, a study on the merits and limitations of each of the different methodologies brought forward is missing. More specifically, the focus of the existing studies that performed literature reviews of measurement of corporates sustainability in the last ten years, vary between impact on profitability performance, accounting methodologies, characteristics of specific techniques, questions for further research, and so on. Mura et al. [28] performed a bibliometric review, based on citation data, to analyze the evolution of sustainability measurements. The findings suggested the literature is characterized by various research strands, which the authors categorized into eight areas of research and 12 sub-fields. The lack of a comprehensive view has resulted in an incomplete framing of the problem and the proposal of partial solutions. This was further highlighted by Büyükozkan and Karabulut [29], who provided an overview of the current literature on sustainability performance evaluation to analyze trends and highlight gaps. The 128 articles identified between 2007 and 2018 showed the subjectivity of qualitative criteria and the need for a more balanced performance evaluation to adopt well-defined and suitable criteria. This is evidence that the 65 research questions suggested by Searcy [30] to close the gaps in the design and implementation of the sustainability performances measurement had not been addressed. Some of the questions included performing comparative analysis of the available performance measurements, as well as analyzing the worthiness to incorporate standardized indicators that may be used for benchmarking. On this aspect, Antolín-López et al. [12] performed a literature review on the three dimensions of CS to identify which indicators and sub-indicators were included in performance measurement and methodologies. The study concluded that only three papers had used all three dimensions of environment, social and economic to measure CS [31,32,33], and that the lack of agreement impaired progress on the measurement assessment. In 2014, Montiel and Delgado-Ceballos’ [21] literature review concluded that a measure of CS does not exist, and provided a comparison of the most popular methodologies developed at that time: the Global Reporting Index (GRI) and the Dow Jones Sustainability Index (DJSI), mixing what aims to provide a list of indicators for measuring CS versus what aims to qualify whether a corporate is sustainable, by inclusion or exclusion to an index with predefined criteria. In 2021, Pranugrahaning et al. [34] consolidated the corporate sustainability and corporate sustainability assessment literature to develop a CS assessment conceptual framework. The process resulted in the identification of three key elements: 1. Sustainability governance system; 2. Measurement of CS performance; 3. Reporting for corporate sustainability. By providing the conceptual framework for CS assessment, the study aimed at addressing the call for holistic and integrative processes to guide companies adopting sustainable practices into business activities. A major assessment point for integrating CS into corporate practices continues to be the analysis of its impact on the profitability of the corporate. Goyal et al. [35] presented a taxonomy of the available literature on the relation of firm performance and sustainability performance. The results confirmed there is no universally accepted direction of this relationship and that, although there was a pattern of growth in interest, financial performance was the greatest proxy for firm performance. An increasingly adopted methodology for measuring corporate sustainability is the Multi Criteria Decision Making (MCDM) technique, which is a sub-discipline of operation research that explicitly evaluates multiple conflicting criteria in decision making. Chowdhury and Paul [36] performed a systematic literature review and bibliometric analysis approach to analyze the applications of MCDM methods in CS research. The findings showed that single MCDM methods are dominant and that there has been no comparison of results obtained from different MCDM methodologies. More recently, the focus has been shifting to sustainability management accounting. Schaltegger et al. [37] provided a systematic literature review of how sustainability management accounting addresses links with the organization’s contexts and contributions to sustainability transformations beyond organizational boundaries; and Pencle [38] synthesized the existing literature at the intersection of management accounting with corporate sustainability and paradox theory. There is a gap in the research where the limitations of the current methodologies utilized for measuring CS have not been explored in the existing literature.

This paper explores the reasons why a cohesive and comparable measure of CS does not exist yet. It addresses the question by investigating the literature of the past 12 years with the objective of identifying the different methodologies that have been used or developed, together with an analysis of their merits and limitations. Pranugrahaning et al. [34] showed that CS assessment topics grew in importance from 2012 onward, and significantly in 2015 since the adoption of the 2030 Agenda for Sustainability Development by the United Nations (UN 2015) is seen as a milestone year for the wider involvement of stakeholders in cooperating toward achieving the Global Goals (OECD, 2015). The analysis is performed by adopting the guiding principles for measuring concepts in social science developed by Gary Goertz in Social Science Concepts and Measurement (2020) [39].

The findings show that the effort is fragmented and studies do not build on previous results. There is a high degree of confusion between the indicators for measuring CS and how those indicators can be measured and aggregated, which is where the literature is lacking progress. The measurement results focus mostly on categorizing CS within different rankings, establishing order of importance of the different indicators, or on delivering comparative longitudinal analysis. The proposed methodologies do not measure corporate sustainability in its highest extension, which is a pre-requisite for measurement abilities and comparative analysis, and do not link the measurement to a well-constructed concept. Addressing these gaps will create meaningful knowledge crucial for progressing with the measurement of CS, which is of global relevance.

2. Measurements of Corporate Sustainability

2.1. Methodology

This study analyses the merits and shortfalls of the existing measurements of corporate sustainability in the literature of the last 12 years by applying Gary Goertz’s guiding principles of how to measure social science concepts, as outlined in ‘Social Science Concepts and Measurement, Goertz (2020)’. Goertz is the only author who provides a systematic guide to link the development of a concept in social science to its measurement. A concept cannot be measured until it is properly constructed and defined in its constitutive features, and their relationship is established. The questions ‘what counts as a measure of x’ and ‘what is x’ cannot be answered independently of each other. Core to concepts is the problem of aggregation, which involves a degree of substitutability. One of the tensions is the relationship between the definitions and the mathematical operations used in aggregation. For example, it is quite common for the semantics of the concept to invoke an analysis of the necessary and sufficient conditions, while the aggregation operations use sums and means. Mathematical formulations for data aggregation must follow the construct of the concept. Pazienza et al. [1] built the concept of corporate sustainability, through the lenses of Goertz, by performing an ontological analysis of the concept in conjunction with the application of the necessary conditions to identify the constitutive factors of the concept. The findings showed that corporate sustainability has three necessary and jointly sufficient constitutive pillars identified with the economic, social and environmental dimensions. The necessity of the conditions implies the non-substitutability between the factors. Furthermore, based on Goertz’ studies, a concept cannot be measured unless it is defined in its highest extension. In summary, to be able to measure the concepts of corporate sustainability:

- The concept must be properly defined in its constitutive pillars;

- The constitutive pillars are necessary conditions and imply non-substitutability;

- Proposed measures must be properly linked to the identified concept and data aggregation must align;

- The concept must be defined in its highest extension, referred to as the ideal type guideline. For example, in order to know how full a glass is, we need to know the glass’s full capacity, or in order to know how tall a person is, we need to have knowledge of the highest height.

Goertz provides extensive additional guidance of how to measure social science concepts. However, as the measurement of the concept of CS itself is not in the scope of our analysis, we limited the list to those guiding principles that are useful to find the merits and limitations within the existing methodologies.

2.2. Search Strategy

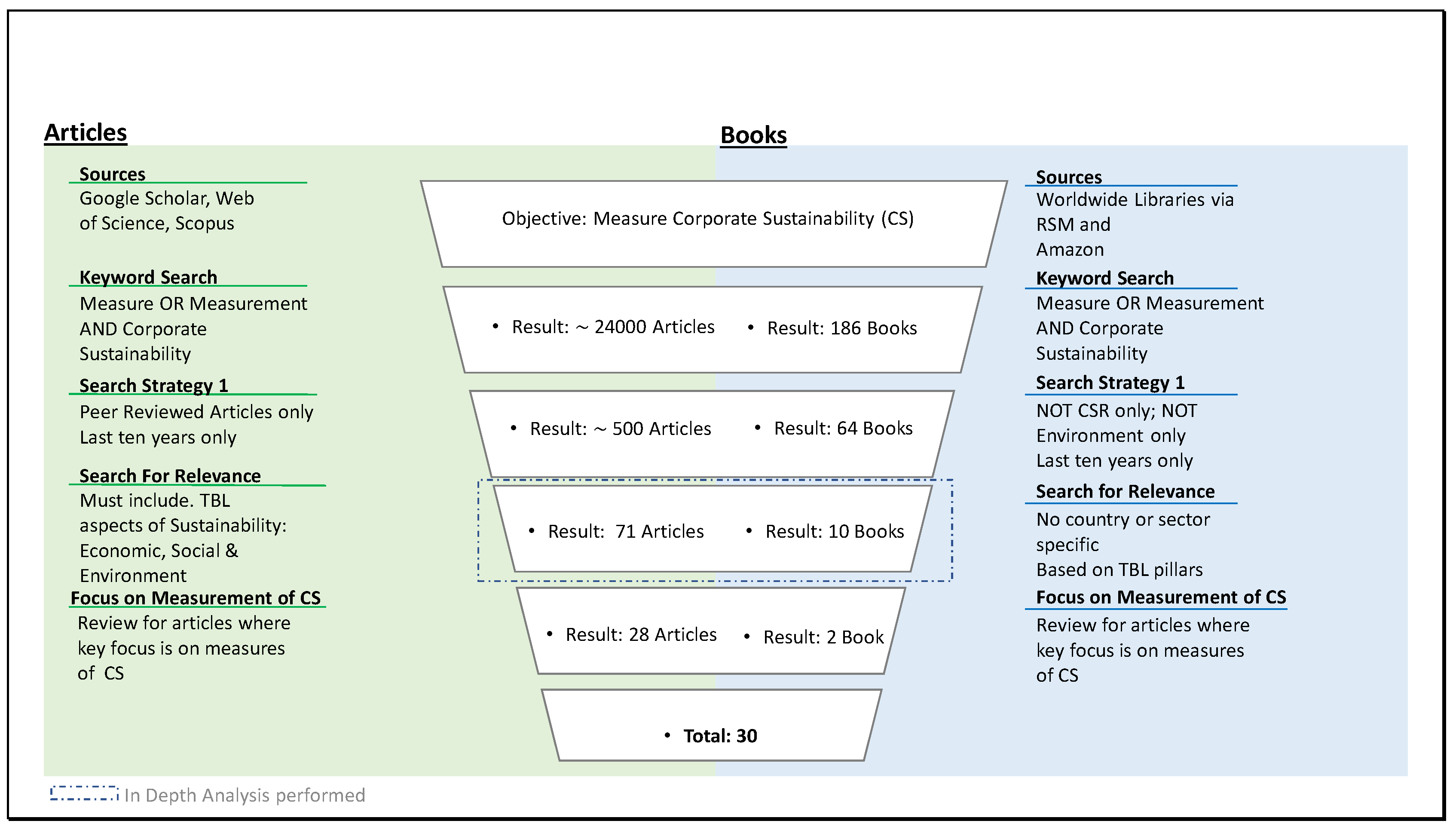

The objective of the literature review was to identify all papers related to the measurement of corporate sustainability. To address this, Google Scholar, Web of Science and Scopus search engines were used to search for peer-reviewed literature, as well as Worldwide Libraries through RSM databases, and Amazon for books and conferences. Results were manually reviewed for relevance to the research objective. The search was restricted to peer-reviewed journal articles. Due to a very high number of results—more than 24,000 results were returned—the search was further narrowed to journal articles for which the measurement of corporate sustainability was a key focus of the paper. The first 50 pages of results were systematically reviewed in all search engines, at which point it seemed as though no new relevant results were occurring. The search was further narrowed to articles published which included the three aspects of corporate sustainability, not CSR only, not environmental only articles. Country or sector-specific articles were excluded and studies published in the last 12+ years—2010 to 2022—were given priority in the analysis. After filtering for relevance, a selection of 71 articles and 10 books were found to be apposite. See Figure 1 for search strategy and results.

3. Findings and Discussion

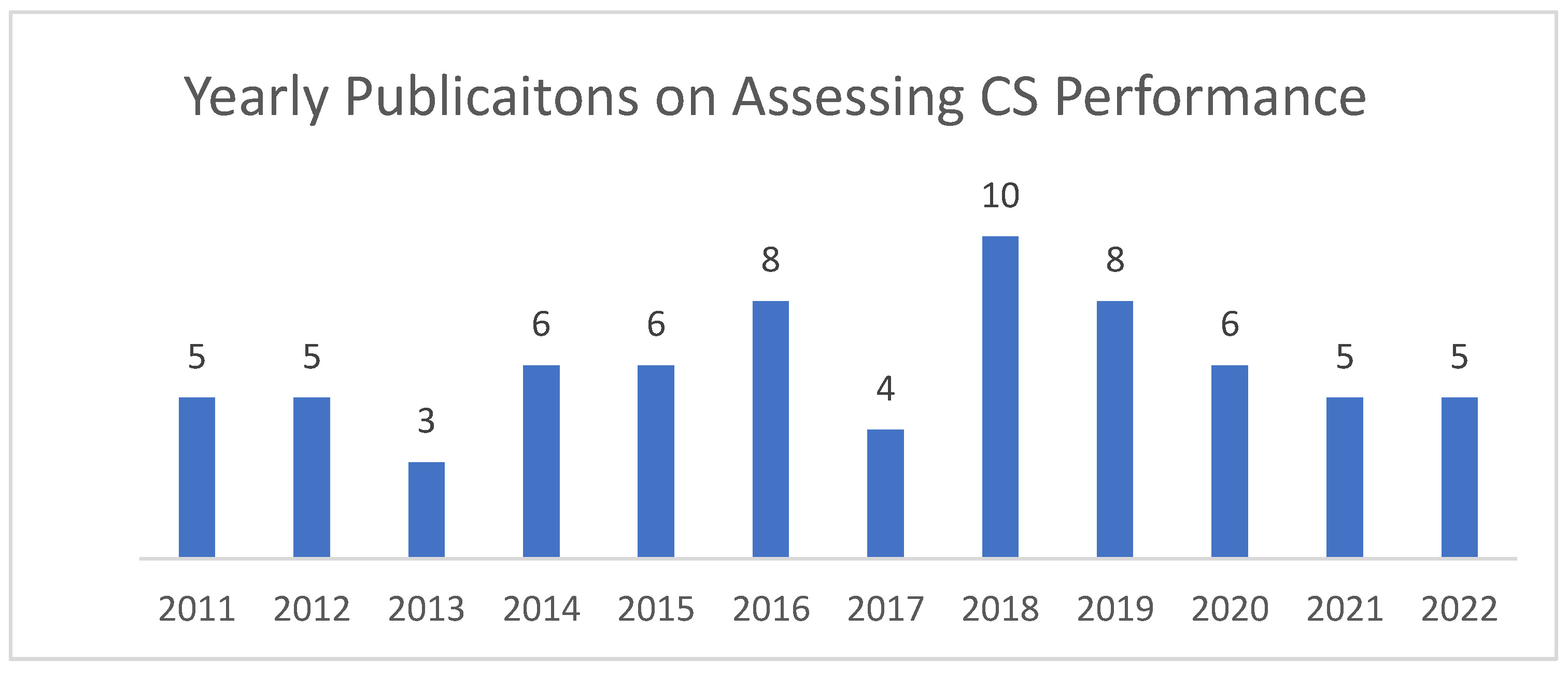

In the last ten years, there has been an increasing number of publications in the literature on measuring corporate sustainability, with a peak in 2018 (See Figure 2).

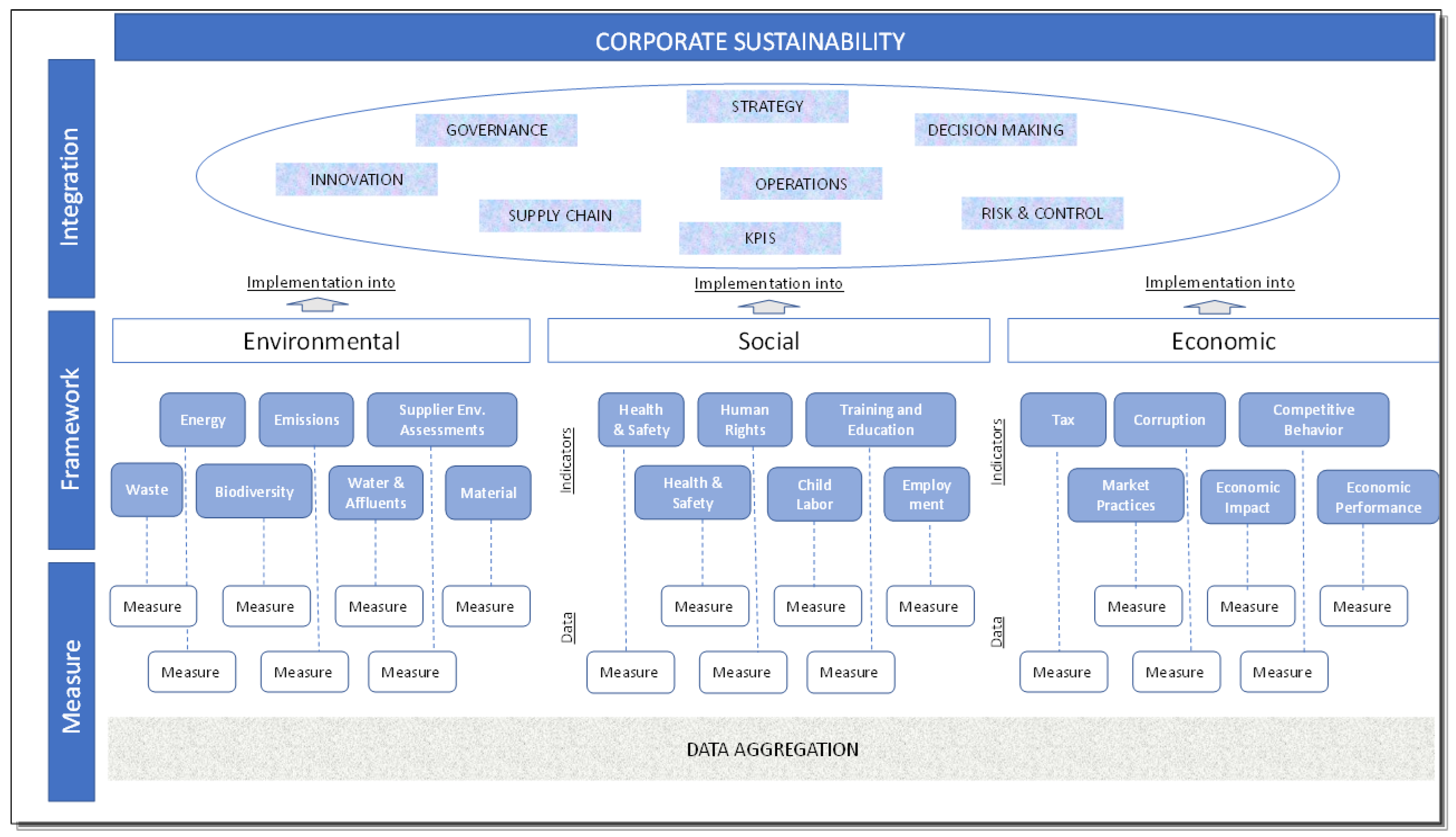

The 71 papers were selected as having the objective of measuring corporate sustainability. However, after analyzing each paper individually, we discover not all of them provide a measure of CS. Among the 71 papers, only 28 provided an indication of a measure or categorization of CS. The remainder focused on other important aspects, which are still relevant to be able to ultimately measure CS, but do not complete the analysis by providing a measure. The findings show a confusion between measuring CS, providing the framework for measuring CS—and therefore their indicators—and integrating CS into corporate practices. By investigating the focus of the publications under analysis, we observe how the selected papers can be classified into five categories: 1. Articles where the focus is to provide a ‘framework’ for guiding corporate sustainability [11 articles and 5 books]. They either provide a selection of indicators for measuring sustainability aspects towards which corporate sustainability should be adopted and measured (a theoretical justification for the choices of the indicators is usually provided), or a framework for promoting and facilitating corporate sustainability; 2. Articles where the focus is the ‘integration’ of corporate sustainability into the corporate practices [5 articles and 1 book]. They suggest models for implementing corporate sustainability in the organization; 3. Articles where the focus is to provide a ‘measure’ of corporate sustainability [28 articles and 2 books]. They ultimately derive a quantified measure or classification of corporate sustainability; 4. Articles where the focus is to provide a ‘literature review’ of one, or all, or a selection of the three subjects mentioned above [10 articles], which have been discussed in the introduction; 5. Articles with a variety of ‘different subjects’ which are mostly enquiring and analyzing on the existing theoretical frameworks and measurements [17 articles and 2 books]. See Figure 3 for different aspects of CS assessment.

3.1. Frameworks

Within the articles that have a focus on ‘frameworks’, new conceptual frameworks and indicators are developed. Most of the emphasis is placed on assessing which area of the corporate should be concerned with sustainability and at what level of the organization it needs to be dealt with. This can take multiple directions. It can, for example, be distinguished between the normative, strategic, and operational domains with the importance of operating at different management levels [40], or it can be assessed within the accounting, control, and reporting frameworks [41]. On a more macro level, strategy, integration, and stakeholders are identified as relevant drivers to guide the promotion and evolution of corporate sustainability [42]. Notwithstanding the different levels, measuring corporate sustainability requires the explicit consideration of a focal firm, its supply chain, and the sustainability context within which the firm operates. Sustainability performance measurement requires a systematic, structured, and integrated approach that considers all aspects of enterprise sustainability, and key requirements need to include supply chain management to encompass the wider ecosystem in which the firm operates [30]. This is how sustainability assessment can be conducted to support decision making in a broad environmental, economic and social context, transcending a purely technical and scientific evaluation [43]. An important component of measuring CS is the identification of the indicators. Defining which aspects of the environmental, social, and economic performance need to be considered is of crucial importance as it has a considerable impact on the results. There has been a proliferation of newly proposed frameworks advocating for certain indicators versus others, as well as systematic reviews trying to consolidate the existing indicators in order to propose new frameworks. Delai and Takahashi [44] suggested a step approach framework for developing sustainability measurement system after studying eight main measurement systems. Goyal et al. [45] identified market value, environmental strategy, R&D, pollution prevention, corporate governance, and investor responsibility as the most important factors in improving CS performance. Prioritization of these factors enhances corporate sustainability. Kocmanová and Sǐmberová [46] determined ESG indicators as a key framework of the measurement of sustainability performance. Among these frameworks there are then different theories as to whether they should be as comprehensive as possible, to be able to fully represent sustainability, or whether they should be minimized, to reduce complexity and facilitate measurement. Moldavska and Welo [47] specified that most of the existing tools tend to include a manageable list of indicators. This resulted in the reductionism of the sustainability concept, which, in turn, fails to cover the whole range of relevant issues. Despite these findings, the literature continues to trend towards reductionism. Cagno et al. [48] proposed three different industrial sustainability performance measurements with a decreasing number of indicators suitable in different contexts of application. Selection mechanisms are conceived and used to reduce the number of indicators while still aiming to provide an adequate coverage of all sustainability pillars. In 2022, Mal et al. [49] assessed and prioritized numerous factors that influence CS performance by using the AHP methodology. Table 1 provides the list of references.

3.2. Integration

The integration of sustainability into corporate activities involves different aspects of the business: innovation, supply chain management, operation management, product development, integrated management systems, product management eco-design and ergonomics; and performance assessment of these areas is directly linked to strategic planning and top-down deployed targets [50]. Corporate sustainability requires integrated measurement and management rather than isolated applications of different tools in different parts of the organization [41]. The problem, though, is that one of the shortcomings of the existing CS assessment methods is that most of them do not distinguish between the extent of the implementation of sustainability-related practice and the actual sustainability performance of the organization [47]. It is time to think more deeply about the integration of different methods and how their interplay can support progress in corporate sustainability. The danger of not achieving an integrated approach was discussed by [51], who investigated the world’s largest corporate reporting on sustainability and concluded that corporations tend to treat sustainable development as given and unproblematic, instead of addressing the fundamental problem of today’s practice, or the dilemma of the concept. Many corporations no longer argue that they are on a ‘journey’ towards sustainability, but that they have already integrated sustainable principles, and that they have worked like this for years. Such arguments inhibit the change in business models that many commentators call for. Different management systems have emerged to integrate different aspects of CS, such as social responsibility, environmental health, quality control, health, and safety. They provide interesting leverage points for integrating sustainability issues into mainstream business processes, but fail to integrate sustainability at all levels, which requires continuous interaction with stakeholders and innovative ways of designing [52]. Baumgartner and Rauter [40] suggested three distinct but complementary dimensions of strategic management from the perspective of integrating sustainability into corporate activities: strategy process, strategy content and strategy context. Table 2 provides the list of references.

3.3. Measure

The studies that focus on measuring corporate sustainability are 28 articles, as well as two books. Among these 30 studies there are 30 different methodologies, models, or constructs for measuring CS. The majority focuses on the creation of composite or single indexes, or on the creation of scorecards. Others utilize a mathematical method or new conceptual models for measuring corporate sustainability. We analyzed the papers based on Goertz’s guidelines and found that, among the 28 articles, four did not provide a definition or concept of corporate sustainability and instead went directly into the merits of the selected methodology; 13 discussed the different definitions and theorizations that have been suggested in the literature through the years, and they indicated either the variety of definitions, or the lack of a harmonized direction, and did not embrace a specific concept. Only 11 studies provided or embraced a definition or a concept of CS. Of those 11, only one links the methodological design and calculation to the identified concept. Some papers, for example, Medel-Gonzalez et al. [53], Kocmanova et al. [54], Docekalova et al. [55], claimed certain constitutive features in the concept and ended up measuring different dimensions. Even though some papers did measure the dimensions they described in the definition, they failed to investigate their relationship and to coherently link the appropriate data aggregation formula. Garcia et al. [27], for example, adopted the Triple Bottom Line and used the average sum of the three pillars, inferring their substitutability. On the contrary, Aras et al. [56] questioned the triple bottom line concept, stating that sustainability is too complex to be confined to three dimensions, and argued for the inclusion of the governance and profitability dimensions. Their mathematical calculation included all five dimensions and correctly summed up the results inferring their non-substitutability; it, however, failed to explain it and to make it explicit. Most of the studies start from the methodology and apply it to the most advantageous concept. Only one article, Ahi et al. [57], was concerned with linking the measurement to the concept. The study adopted the concept of strong sustainability, which relies on the notion that the economy is part of society, which is completely placed inside of the environment. The model considered environmentally related factors when measuring performance, and social and economic related factors are only considered after that foundation has been established. With reference to measuring CS in its highest extension, only one article, Garcia et al. [27], performed the analysis by selecting the best available option. Even though the best selected option may not necessarily be the highest, the authors introduced the concept and the importance of measuring sustainability versus the highest achievable status. In addition, Sari et al. [58] defined various maturity levels, including the highest, but it referred to the level of integration of sustainability into processes. We observe that the lack of identification of the ideal type among indicators resides in the nature of some of the methodologies themselves: complex and single indexes are concerned with minimum thresholds; the multi criteria decision making techniques deal with comparing and ranking different options to facilitate decision making; content analysis is not equipped to establish the highest extension; some models regard sustainability as the difference between the benefits and the costs created. In conclusion, none of the articles provided a cohesive analysis that clearly identifies the concept of CS in its constitutive pillars, aligns the data aggregation to the non-substitutability of the pillars, and highlights the highest achievable measure of the indicators. Table 3 and Table 4 provide the list of references. Table 5 provides an overview of organizations and conferences with focus on Sustainability.

Additionally, conferences and efforts of international organizations were analyzed and findings show that there has been no focus on measuring corporate sustainability.

3.4. Other Subjects

Additionally, there is a diversity of other subjects, across 17 articles and 2 books, which often offer a critical analysis of the merits and shortfalls of the proposed theoretical frameworks and/or of some of the existing measures. Siew [59] provided a review of major reporting tools, including GRI, and concluded that they are important as they inform on a corporate’s progress on sustainability goals, but the rapid growth of different criteria and methodologies has created major complications for stakeholders. Cristofi and Sisaye [60] compared the GRI with the Dow Jones Sustainable Index (DJSI) and finds how the two most widely used reporting instruments/indexes differ in disclosure, practice and method. They recommend further standardization and enforcement, calling for the Securities Exchange Commission (Statutory Authority Body for setting up financial reporting and standards in the USA) and the Financial Accounting Standard Board (Recognized by the US Securities Exchange Commission as the designated accounting standards setter for public companies) to be more actively involved. Searcy and Elkhawas [61] explored the use of the DJSI with reference to Canadian companies, which revealed a range of strategies for gaining and maintaining inclusions in the index, particularly involving a large number of internal stakeholders, in responding to data requests and working with third parties. Other authors offered heuristic models for establishing trade-offs [62,63]. Dočekalová et al. [55] dealt with the inconsistencies of composite indexes. Hansen and Schaltegger [64] performed a literature review of scorecards to find their merits. In 2011, Searcy [4] offered a practical guidance for the evolution of sustainable performance measurement and highlighted the need for further evolution. In 2020, Ye [65] identified a positive relationship between ESG indicators, stock return and sustainable performance. Schneider and Meins [66] identified two shortcomings for corporate sustainability: value creation as a core condition, and failure to credit governance as a key enabler. Mamede and Gomes [67] measured existing practices and observed findings which feature an unbalanced approach towards economic aspects. Nicolăescu et al. [2] explored the contribution of sustainability undertakings towards enhancing corporate performance with a growing need of a culture of sustainability, and the function, as well as challenges, of corporation to accomplish sustainable development. Finally, Caiado et al. [13] tested the perceived importance of factors from practitioners. Results showed that internal organizational factors are the main inductors of sustainable development, and sustainability must be tied to strategic planning, starting from upper management to lower levels. In 2019, Silva et al. [16] explored the gap between the growing number of articles on corporate sustainability and stakeholder satisfaction, and revealed that many stakeholders deem current sustainability performance measurement and assessment approaches insufficient for their needs. In 2022, Delmas [68] investigated the CS disclosure among the biggest US firms and found that, based on the World Economic Forum metrics, the top 300 firms reported less than 49.6% of the metrics. The larger percentage in mean disclosure were in the Governance pillar (72%), followed by Prosperity (54%) and Planet (29%). The low disclosure rate was described as limiting the ability to analyze whether companies are advancing, stagnating, or backsliding across ESG metrics. In his book, ‘Corporate Citizenship & Sustainability. Measuring intangible, physical and assets’, Iyer et al. [69] states that measuring ethical asset usage is crucial for corporates to bring the abstraction into reality: acknowledge value when it is achieved and deconstruct what is valueless. Almost a decade earlier, Ahmed et al. (2012) implied how CSR is the base of sustainability in all realms. In 2021, Diez-Cañamero et al. [70] identified the most common characteristic of the CS system in three typologies: indexes, rankings and ratings. In their conclusions, they highlighted that the CS system is heterogeneous and chaotic, and that, although they have the same objective of measuring, qualifying and quantifying the same thing, companies do not obtain the same results in all the different CS systems in which they participate. They claimed that, even though ESG rating agencies promote the best corporate practice in favor of sustainability development, they are not unbiased. In the previous year, Boiral et al. [71] investigated the rigorousness and reliability of sustainability rating agencies’ evaluation of CS risks, and, by using grounded theory of interviews with practitioners, showed trade-offs and rational myths underlying the evaluation process.

Clarifying the above categorization between integration, creation of frameworks and measurement of CS is important as confusion on the contribution to the different phases and aspects of corporate sustainability may lead users to think that integration of some CS practices, or adherence to the suggested framework, qualifies firms as sustainable. The papers that focus on frameworks and integration provide valuable conceptual guidelines and actionable indications, but fail to measure to what extent a corporate is sustainable. An important observation is that concepts, frameworks, and measures of corporate sustainability do not build on each other. Rather, they are unrelated, pushing towards a diversity of solutions, grounded in justified, theoretical, or practical explanations which, nonetheless, result in the creation of multiple distinct versions. This has generated a proliferation of optionalities which can lead users into confusion, or enable the adoption of easier, but not necessarily more effective or representative, methodology. In the context of self-assessment, the variety of tools allow for the potential misrepresentation of the reality. Furthermore, the utilized approaches for framing, measuring and integrating corporate sustainability are mostly exogenous: they are geared towards finding a model that works in principle and that will ultimately be applied to corporates; instead of an endogenous approach, where a corporate is at the core of the analysis, and models are created around the corporate capabilities of reaching sustainability. The growing interest in the subject, both from scientists and practitioners, testifies that existing accounting practices are no longer sufficient to represent corporate performance holistically. The interest in measuring and framing corporate sustainability seems to result in the unconscious construction of the balance sheet and income statement of corporate sustainability. The activity is growing in its aspiration, but it is still nascent in its development stage. Unity from all stakeholders is needed to eliminate dispersion and ensure clear direction in the effort and actionable results. The lack of a holistic view of sustainability measurement has led to the development of many separate streams, resulting in duplication of efforts, incomplete framing of the problem, and the proposal of partial solutions.

4. Analysis of the Existing Measurement Methodologies of CS

The analysis of the articles that focus on providing a methodology and a measure of corporate sustainability shows a lack of standardization capabilities and intra-companies or intra-sector comparability. As a consequence, a standardized measure of CS that informs on the sustainability magnitude of a corporate, and comparability across firms and industries, is missing.

To streamline the analysis, we can further divide the studies into four categories:

- 1.

- Composite and Single Indexes, and Scorecards;

- 2.

- Performance score based on content analysis;

- 3.

- New methodologies;

- 4.

- New models/tools.

Table 6 provides full references.

4.1. Indexes and Scorecards

Composite and single indexes have grown in popularity. The greatest success of indexes is, perhaps, that a few of them are applied in the real world. The Dow Jones Sustainable Index, FTESE4 Good Index Series, the ECPI Global Developed ESG Best-in-Class Equity Index, and ISS ESG corporate rating are a few examples. They offer a benchmark for companies around the world, and a series of transformations to be able to qualify for the sustainability indexes. In the literature of the last ten years, six composite indexes and three single indexes have been developed. Engida et al. [19] articulated on the benefits of composite indexes as helping firms evaluate their performance against their peers and identify priorities for sustainable improvements. It is also increasingly important for decision making, given the pressure from stakeholders and the need to improve firm image [72]. The composite index can summarize complex multi-dimension concepts while maintaining the underlying information base [73]. They are easier to interpret than a set of individual indicators, and facilitate communication with the general public and other stakeholders. On the opposite side, Nikolaou et al. [74] highlighted that, despite the benefits, they are considered subjective since they utilize unsystematic and unclear ways to introduce and exclude single indicators [75]. Work in data collection and editing is wasted, or hidden, behind a single number of dubious significance [76]. Other drawbacks of composite indexes are the complexity of measurements and the aggregation problem [77], which implies a better overall score of a corporate sustainability index while the performance in one of the three basic aspects of sustainability deteriorates [78]. Other problems are associated with the assignment of weight factors which are necessary to integrate single indicators into the final composite index. According to Büyüközkan and Karabulut [29], indexes can differ greatly in focus, coverage, methodology and objective. Although they are known for their ease of use and generation, the trade-offs and compromise are often poorly considered, leading to distortion in the intended outcome, according to Morrison-Saunders and Pope [79], and significant information can get lost during the aggregation process. Specifically for single based indicators, Nikolaou et al. [74] summarized that they are criticized for (a) the lack of standardization techniques [80]; (b) the measurement of diverse definitions for corporate sustainability and each sustainability aspect; (c) the measurement in mixed output indicators (results) with process indicators (effective operation) [44]; (d) the measurement of a specific firm or sector; (e) the lack of well-defined indicators [81]; and (f) the absence of measurement leading and lacking indicators of sustainability [31].

Maltz et al. [82] attributed the emergence of multidimensional performance tools, including the balanced scorecard (BSC), to the need to overcome the shortcomings of a single-value financial approach to corporate performance. According to Journeault [83], Sustainability Balanced Scorecards are the most promising strategic tools to help organizations face the challenges of developing a sustainability strategy that incorporates environmental and social responsibilities. Some of the research on the Sustainability BSC has argued that this management tool can support the successful implementation of corporate sustainability strategies by developing a hierarchical system of strategic objectives derived from the business strategy. Goals and indicators are then identified for each of these objectives, forming a multidimensional set of sustainability-oriented metrics that are interrelated through cause–and–effect relationships [84]. Epstein and Roy [85] indicated that scorecards help to identify what drives sustainability, what actions would improve it and what consequences are likely to impact the company’s environmental, social and financial performance. Jensen [86], however, criticized the lack of single score: ‘a scorecard that gives no score, that is, no single value measure of how they have performed’. He affirmed that the system can easily have two dozen measures and no information on the trade-offs between them.

4.2. Content Analysis

To assess corporate sustainability properly and to minimize the limitations of the existing methodologies, specifically those of the indexes, in 2019, Molla [87], recommended a content analysis which suggests counting the number of words related to the different indicators of sustainability disclosure in the annual report. The same methodology was utilized by Aras et al. [56]. Content analysis is defined as “a set of procedures to make valid inferences from text” [88]. The methodology is frequently used to determine the number of disclosures in the sustainability reports published by different sectors. Some academicians measure the number of disclosures by the number of pages, while others use the number of words [89], or the number of sentences [90]. Milne and Adler [91] suggested that individual words may lack meaning without a complete sentence. As a result, most researchers favor sentences, although this method omits disclosure in the form of tables and graphs [92]. Page count may be less accurate since different firms may use different margins and font size [90]. Content analysis is a technique of which the merits can be more relevant in studying past performance as the results can be easily manipulated for future analysis as well as be aleatory. Nonetheless, both authors come to the conclusion that a good performance score of corporate sustainability requires a balance of all factors which cannot be compensated for between the different indicators.

4.3. New Methodologies

Lee and Sean [72] and Azadi et al. [8] proposed the Data Envelopment Analysis (DEA) for measuring the performance of corporate sustainability. DEA was introduced by Charnes and Rhodes [93] as a linear programming procedure for a frontier analysis of input and output, which do not require a-priori weights and hence is considered more objective. Engida et al. (2018) highlight that the DEA approach aims to measure relative efficiency, which is based on the comparison with other decision-making units (DMUs) in the sample. DEA identifies inefficient DMUs and efficient DMUs, which are considered as benchmarks. The performance measure therefore is limited to the companies selected in the sample under observation and, as admitted by Lee and Sean [72], the measurement is limited to the performance of the best selected DMU, which may itself be an average indicator of sustainability.

A set of articles applied the Multi Criteria Decision Making (MCDM) methodologies. MCDM is increasing in popularity for assessing CS performance and it is used for evaluating multiple conflicting criteria for decision making. MCDM provides a variety of different methodologies for ranking and ordering decision making. Authors have selected and adopted a few of them to measure CS, arguing for their merits as opposed to others. Bamford et al. [17] proposed a series of mathematical formulations based upon the evidential reasoning (ER) approach, which can be used to aggregate results from qualitative judgments with quantitative measurements under various types of complex and uncertain situations. ER considers belief function, instead of probability, to overcome the degree of incompleteness when evidence is unable to reflect the whole view of the situation precisely. The usefulness of the belief function is, at the same time, its limitation: they are not objectively verifiable and easy to maneuver. Küçükbay and Sürücü [94] proposed the Multimoora Sort as a practical and efficient methodology for measuring CS performance. It ranks the selected companies from best to worst performer according to pre-selected indicators. Bezerra et al. [95] proposed PROMETHEE II as a way to avoid trade-offs among dimensions, offering a non-compensatory method. When compensation occurs, a disadvantage in some criteria can be compensated for by a large advantage in another criteria. The authors identified 9 criteria for measuring CS, that are then aggregated into a single index by using PROMETHEE II. Different MCDM methods produce different assessment results and the application of one methodology only may not be robust [70]. A few authors combined multiple MCDM methodologies. Vivas et al. [96] combined PROMETHEE with the PCA and MLR analysis to analyze the sustainability performance of a specific firm over the years 2009 to 2017. Aktaş and Demirel [97], utilized the Entropy method to weight criteria and then the VIKOR, TOPSIS and MAUT methods were used to define performance ranking of alternative sustainability reports. The Borda count method is finally applied to combine the three rankings into one. Rao [98] selected the most important indicators from CSR reports and designed an expert questionnaire of DEMATEL and IPA according to the key indicators with the highest frequency. Discrete weight of key indicators was found through the application of DANP methodology. The study suggested the priority of the key indicators that a corporate can refer to. DANP methods makes it possible to detect the degree of mutual influence and causality between key indicators as a way to not only predict past performance but also to predict future trends.

Both single and integrated MCDM methods have been used; however single MCDM methods are dominant and there is no comparison of results obtained from the different MCDM methods [36]. MCDM is a methodology used for supporting decision making in problems where a number of alternatives need to be evaluated with respect to a number of criteria. The results can select the best alternative, rank the alternative or sort the alternatives in a number of classes. It is a ranking methodology for facilitating decision making rather than a measurement methodology.

4.4. New Models

Part of the literature is focused on addressing the subject of how much value a firm is creating versus how much resources are being used and whether the differential is positive or negative. New models have been created to address this question. Kocmanová [54] proposed a Sustainable Value-Added model which combined weighted environmental, social and corporate governance indicators with their benchmark determined by DEA analysis. Benchmark values of indicators were set for each company separately to determine the optimal combination of environmental, social and corporate governance inputs to economic outcomes. The value-add of most of the selected companies was negative, with a high probability of resistance among practitioners. Wright and Caudill [99] developed the comprehensive sustainable target model (CSTM) expanding on the Sustainability Target Method (STM), which is a framework for quantitative assessment of environmental burden compared to economic added value by an organization [100]. The expansion included societal and environmental beneficial impacts, as well as the interdependencies between the economic, environmental and societal domains. Based on STM, sustainability is achieved when the economic value added by the company is not lower than the environmental impact created. The share of economic value added by a business is the ratio of its annual value-added generated to the annual level of global economic activity, which can be assumed as the GDP. The share of climate change impact created by the business is the ratio of its total annual greenhouse gas emission to the sustainable level of annual global GHG emission allowable, which is referred to as the Earth’s carrying capacity and varies with time as the concentration level of GHG in the atmosphere changes. Defining the Earth’s carrying capacity in all relevant environmental and social aspects is challenging in nature and, even in case scenarios where they could be reasonably defined, it could incentivize a greater and, to a certain extent, reckless production activity to increase the value add to compensate for the environmental damage. In other words, both the numerator and denominator of the coefficients are moving parts which are, in the former case, subject to managerial choice, but also markets’ dynamics and, in the latter case, can fluctuate based on yearly levels defined independently. Following a similar approach, Ahi et al. [57] proposed a probabilistic model for measuring strong sustainability performance which emphasize the non-substitutability of resources. The model implies that sustainability performance of a company is the probability in which the company’s strength can surpass the challenges imposed, in which case it can be said that the company has progressed towards sustainability. Based on strong sustainability, the model relies on the notion that the economy is part of society, which is completely placed inside of the environment. The proposed model, therefore, considers environmentally related factors only when measuring performance. In a different approach, Sari et al. [58] developed a Corporate Sustainability Maturity Model, which can be used by organizations to conduct self-assessment of maturity levels in order to transition to a mature sustainable organization. It used a systematic literature review and applied content analysis and expert interviews to create a prototype for maturity levels. Through this model firms are meant to be enabled to choose the correct indicators to help improve each sustainability domain in the matrix. It is based on self-assessment and self-selection of the indicators and it doesn’t provide a measure of CS. Still, based on self-assessment, Zenya and Nystad [101] developed the E-SET tool by using indicators from six global sustainability reports. The platform uses self-assigned scores and is therefore more useful as a self-guide tool, rather than as a measurement of sustainable performance. Building on the construct of composite indicators, Docˇekalová and Kocmanová [46] presented a model which integrates the environmental, social, economic and corporate governance performance of the company into a Complex Performance Indicator (CPI). CPI contains seventeen key indicators which were summed up into a single value. The performance is valued against a pre-established benchmark, made of selected KPIs based on experts’ input, which is enabled to quantify the performance gap. The reason it is classified as a new model, rather than composite indicators, is because, unlike other papers that focus on indicators, it sums the complex corporate performance of the 17 indicators used to create the benchmark into a single value. However, it carries the limits of the composite indexes. With the objective to provide a balanced single measure of CS and to facilitate integration into sustainability management, Garcia et al. [27] adopted a multi criteria decision making approach and a stakeholder view, and adapted the Integrated Environmental Evaluation of Water Resources Development model developed by the United National Environmental Programme and United Nations Educational, Scientific and Cultural Organization (UNEP/UNESCO, 1987) to include the three dimensions of TBL. The model provides an overall single measure of sustainability that captures the balance level among TBL dimensions, and performance indices of each of the TBL dimensions, which unfold into multiple levels and various performance indicators. However, the average sum of the dimension is used, inferring their substitutability.

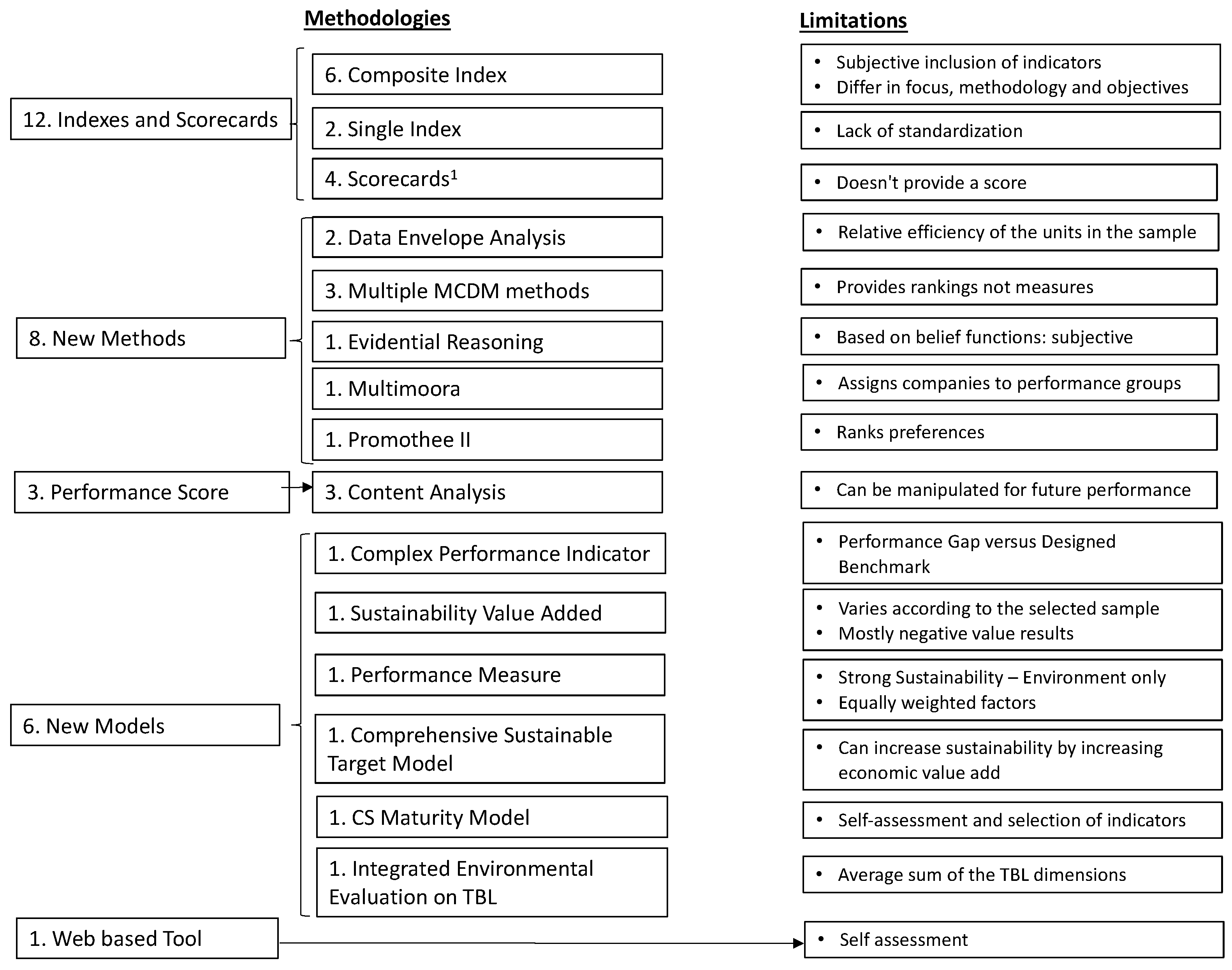

A striking observation is that the proposed methodologies do not encounter application in real life. They logically suffer smaller or larger limitations, but, ultimately, they do not provide a standardized and simple measure of corporate sustainability that can be applied across all sectors, that allow for comparison of performance of companies across industries, or that gauge the company’s sustainable performance in one measure. See Figure 4 for overview of limitations of existing methodologies for assessing CS.

5. Why CS Is Not Yet Measured

The literature has attempted a few approaches for measuring CS. The existing methodologies address important aspects of assessing corporate sustainability. However, they fail to provide a holistic measure which can be applied across firms and sectors consistently. The concept of corporate sustainability is complex in nature and its measurement implies aggregation of qualitative and qualitative indicators whose relationships are not fully explored and understood. The lack of linkage between the ‘how’ to measure and ‘what’ to measure is a primary cause for missing a tested and applicable methodology for measuring corporate sustainability. If the concept of CS is not identified, defined, and constructed in its constitutive features, the identification of the appropriate methodology cannot follow. In the current literature, the effort has been spent on identifying a methodology that can encompass the diversity of the factors under measurement, with little to no regard for their constituency and relationship. As a consequence, the selection of the indicators to measure CS becomes a free-choice and even a differentiating factor to ensure novelty of the research and to provide a unique perspective. The majority of the studies aims at minimizing the indicators to reduce the complexity of the evaluation, which assumes substitutability between factors before establishing they can be compensated with each other. Furthermore, even when a limited number of indicators are selected for measuring CS, the studies fail to explore the highest achievable degree of sustainability, based on which the corporate sustainability of a firm can then be measured. As a consequence, there is a failure to inform of the real sustainability measure of a firm. The analyzed articles negate the basic principles, established by Goertz, for measuring concepts in social science and fail to scientifically identify the constitutive factors of CS, understand the causal relationship of those factors, apply the consequent mathematical technique associated with the identified causal relationship, and to identify the highest extension of all indicators. There are studies that address each, or more than one, of the four above-mentioned categories, but none of them brings it all together to develop a coherent and effective measure of CS. This highlights the scope for future research.

Author Contributions

Conceptualization, methodology, formal analysis, writing, M.P. Supervision, editing and validation, M.d.J. Review and validation, D.S. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Data Availability Statement

All data are reported in the study.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Pazienza, M.; de Jong, M.; Schoenmaker, D. Clarifying the concept of corporate sustainability and providing convergence for its definition. Sustainability 2022, 14, 7838. [Google Scholar] [CrossRef]

- Nicolăescu, E.; Alpopi, C.; Zaharia, C. Measuring corporate sustainability performance. Sustainability 2015, 7, 851–865. [Google Scholar] [CrossRef] [Green Version]

- Neely, A.; Gregory, M.; Platts, K. Performance measurement system design: A literature review and research agenda. Int. J. Oper. Prod. Manag. 2005, 25, 1228–1263. [Google Scholar] [CrossRef]

- Searcy, C. Updating corporate sustainability performance measurement systems. Meas. Bus. Excell. 2011, 15, 44–56. [Google Scholar] [CrossRef]

- Lobos, V.; Partidario, M. Theory versus practice in strategic environmental assessment (SEA). Environ. Impact Assess. Rev. 2014, 48, 34–46. [Google Scholar] [CrossRef]

- Adams, C.A.; Muir, S.; Hoque, Z. Measurement of sustainability performance in the public sector. Sustain. Account. Manag. Policy J. 2014, 5, 46–67. [Google Scholar] [CrossRef]

- Čuček, L.; Klemeš, J.J.; Kravanja, Z. A review of footprint analysis tools for monitoring impacts on sustainability. J. Clean. Prod. 2012, 34, 9–20. [Google Scholar] [CrossRef]

- Azadi, M.; Jafarian, M.; Mirhedayatian, S.M.; Saen, R.F. A novel fuzzy data envelopment analysis for measuring corporate sustainability performance. Int. J. Product. Qual. Manag. 2015, 16, 312–324. [Google Scholar] [CrossRef]

- Milne, M.J.; Gray, R. W(h)ither ecology? The triple bottom line, the global reporting initiative, and corporate sustainability reporting. J. Bus. Ethics 2013, 118, 13–29. [Google Scholar] [CrossRef]

- Tregida, H.; Milne, M.; Kearins, K. (Re)presenting ‘sustainable organizations. Account. Organ. Soc. 2014, 39, 477–494. [Google Scholar] [CrossRef]

- Mahoney, L.S.; Thorne, L.; Cecil, L.; LaGore, W. A research note on standalone corporate social responsibility reports: Signaling or greenwashing? Crit. Perspect. Account. 2013, 24, 350–359. [Google Scholar] [CrossRef]

- Antolín-López, R.; Delgado-Ceballos, J.; Montiel, I. Deconstructing corporate sustainability: A comparison of different stakeholder metrics. J. Clean. Prod. 2016, 136, 5–17. [Google Scholar] [CrossRef]

- Caiado, R.G.G.; Quelhas, O.L.G.; Nascimento, D.L.M.; Anholon, R.; Leal Filho, W. Measurement of sustainability performance in Brazilian organizations. Int. J. Sustain. Dev. World Ecol. 2018, 25, 312–326. [Google Scholar] [CrossRef]

- Haniffa, R.M.; Cooke, T.E. The impact of culture and governance on corporate social reporting. J. Account. Public Policy 2005, 24, 391–430. [Google Scholar] [CrossRef]

- Molina-Azorín, J.F.; Claver-Cortés, E.; López-Gamero, M.D.; Tarí, J.J. Green management and financial performance: A literature review. Manag. Decis. 2009, 47, 1080–1100. [Google Scholar] [CrossRef]

- Silva, S.; Nuzum, A.-K.; Schaltegger, S. Stakeholder expectations on sustainability performance measurement and assessment. A systematic literature review. J. Clean. Prod. 2019, 217, 204–215. [Google Scholar] [CrossRef]

- Bamford, D.; Yang, J.-B.; Sureeyatanapas, P. Evaluation of corporate sustainability. Front. Eng. Manag. 2014, 1, 176–194. [Google Scholar]

- Howard-Grenville, J.; Davis, J.; Dyllick, T.; Joshi, A.; Miller, C.; Thau, S.; Tsui, A.S. Sustainable development for a better world: Contributions of leadership, management and organizations: Submission deadline: July 1 to July 30, 2018. Acad. Manag. Discov. 2017, 3, 107–110. [Google Scholar] [CrossRef] [Green Version]

- Engida, T.G.; Rao, X.; Berentsen, P.B.; Lansink, A.G.O. Measuring corporate sustainability performance–the case of European food and beverage companies. J. Clean. Prod. 2018, 195, 734–743. [Google Scholar] [CrossRef]

- Morioka, S.N.; Iritani, D.R.; Ometto, A.R.; Carvalho, M.M.d. Systematic review of the literature on corporate sustainability performance measurement: A discussion of contributions and gaps. Gestão Produção 2018, 25, 284–303. [Google Scholar] [CrossRef]

- Montiel, I.; Delgado-Ceballos, J. Defining and measuring corporate sustainability: Are we there yet? Organ. Environ. 2014, 27, 113–139. [Google Scholar] [CrossRef]

- Harik, R.; El Hachem, W.; Medini, K.; Bernard, A. Towards a holistic sustainability index for measuring sustainability of manufacturing companies. Int. J. Prod. Res. 2015, 53, 4117–4139. [Google Scholar] [CrossRef]

- Helleno, A.L.; de Moraes, A.J.I.; Simon, A.T. Integrating sustainability indicators and Lean Manufacturing to assess manufacturing processes: Application case studies in Brazilian industry. J. Clean. Prod. 2017, 153, 405–416. [Google Scholar] [CrossRef]

- Gimenez, C.; Sierra, V.; Rodon, J. Sustainable operations: Their impact on the triple bottom line. Int. J. Prod. Econ. 2012, 140, 149–159. [Google Scholar] [CrossRef]

- Pagell, M.; Gobeli, D. How plant managers’ experiences and attitudes toward sustainability relate to operational performance. Prod. Oper. Manag. 2009, 18, 278–299. [Google Scholar] [CrossRef]

- Trianni, A.; Cagno, E.; Neri, A. Modelling barriers to the adoption of industrial sustainability measures. J. Clean. Prod. 2017, 168, 1482–1504. [Google Scholar] [CrossRef]

- Garcia, S.; Cintra, Y.; Rita de Cássia, S.; Lima, F.G. Corporate sustainability management: A proposed multi-criteria model to support balanced decision-making. J. Clean. Prod. 2016, 136, 181–196. [Google Scholar] [CrossRef]

- Mura, M.; Longo, M.; Micheli, P.; Bolzani, D. The evolution of sustainability measurement research. Int. J. Manag. Rev. 2018, 20, 661–695. [Google Scholar] [CrossRef]

- Büyüközkan, G.; Karabulut, Y. Sustainability performance evaluation: Literature review and future directions. J. Environ. Manag. 2018, 217, 253–267. [Google Scholar] [CrossRef]

- Searcy, C. Corporate sustainability performance measurement systems: A review and research agenda. J. Bus. Ethics 2012, 107, 239–253. [Google Scholar] [CrossRef]

- Figge, F.; Hahn, T.; Schaltegger, S.; Wagner, M. The sustainability balanced scorecard–linking sustainability management to business strategy. Bus. Strategy Environ. 2002, 11, 269–284. [Google Scholar] [CrossRef]

- Bansal, P. Evolving sustainably: A longitudinal study of corporate sustainable development. Strateg. Manag. J. 2005, 26, 197–218. [Google Scholar] [CrossRef]

- Kolk, A.; Hong, P.; Van Dolen, W. Corporate social responsibility in China: An analysis of domestic and foreign retailers’ sustainability dimensions. Bus. Strategy Environ. 2010, 19, 289–303. [Google Scholar] [CrossRef] [Green Version]

- Pranugrahaning, A.; Donovan, J.D.; Topple, C.; Masli, E.K. Corporate sustainability assessments: A systematic literature review and conceptual framework. J. Clean. Prod. 2021, 295, 126385. [Google Scholar] [CrossRef]

- Goyal, P.; Rahman, Z.; Kazmi, A.A. Corporate sustainability performance and firm performance research: Literature review and future research agenda. Manag. Decis. 2013, 51, 361–379. [Google Scholar] [CrossRef]

- Chowdhury, P.; Paul, S.K. Applications of MCDM methods in research on corporate sustainability: A systematic literature review. Manag. Environ. Qual. Int. J. 2020, 31, 385–405. [Google Scholar] [CrossRef]

- Schaltegger, S.; Christ, K.L.; Wenzig, J.; Burritt, R.L. Corporate sustainability management accounting and multi-level links for sustainability—A systematic review. Int. J. Manag. Rev. 2022, 24, 480–500. [Google Scholar] [CrossRef]

- Pencle, N. Motivating Corporate Sustainability Research in Management Accounting Through the Lens of Paradox Theory. Account. Perspect. 2022, 21, 663–696. [Google Scholar] [CrossRef]

- Goertz, G. Social Science Concepts and Measurement. Available online: https://press.princeton.edu/books/hardcover/9780691205465/ (accessed on 2 March 2022).

- Baumgartner, R.J. Managing corporate sustainability and CSR: A conceptual framework combining values, strategies and instruments contributing to sustainable development. Corp. Soc. Responsib. Environ. Manag. 2014, 21, 258–271. [Google Scholar] [CrossRef]

- Maas, K.; Schaltegger, S.; Crutzen, N. Reprint of Advancing the integration of corporate sustainability measurement, management and reporting. J. Clean. Prod. 2016, 136, 1–4. [Google Scholar] [CrossRef]

- Pádua, S.I.D.; Jabbour, C.J.C. Promotion and evolution of sustainability performance measurement systems from a perspective of business process management: From a literature review to a pentagonal proposal. Bus. Process Manag. J. 2015, 21, 403–418. [Google Scholar] [CrossRef]

- Sala, S.; Ciuffo, B.; Nijkamp, P. A systemic framework for sustainability assessment. Ecol. Econ. 2015, 119, 314–325. [Google Scholar] [CrossRef]

- Delai, I.; Takahashi, S. Sustainability measurement system: A reference model proposal. Soc. Responsib. J. 2011, 7, 438–471. [Google Scholar] [CrossRef]

- Goyal, P.; Rahman, Z. Corporate sustainability performance assessment: An analytical hierarchy process approach. Int. J. Intercult. Inf. Manag. 2014, 4, 1–14. [Google Scholar] [CrossRef]

- Kocmanová, A.; Šimberová, I. Determination of environmental, social and corporate governance indicators: Framework in the measurement of sustainable performance. J. Bus. Econ. Manag. 2014, 15, 1017–1033. [Google Scholar] [CrossRef] [Green Version]

- Moldavska, A.; Welo, T. A Holistic approach to corporate sustainability assessment: Incorporating sustainable development goals into sustainable manufacturing performance evaluation. J. Manuf. Syst. 2019, 50, 53–68. [Google Scholar] [CrossRef]

- Cagno, E.; Neri, A.; Howard, M.; Brenna, G.; Trianni, A. Industrial sustainability performance measurement systems: A novel framework. J. Clean. Prod. 2019, 230, 1354–1375. [Google Scholar] [CrossRef]

- Mal, H.; Varma, M.; Vishvakarma, N.K. An empirical study to prioritize the determinants of corporate sustainability performance using analytic hierarchy process. Meas. Bus. Excell. 2022. [Google Scholar] [CrossRef]

- Morioka, S.N.; Carvalho, M.M. Measuring sustainability in practice: Exploring the inclusion of sustainability into corporate performance systems in Brazilian case studies. J. Clean. Prod. 2016, 136, 123–133. [Google Scholar] [CrossRef]

- Ihlen, Ø.; Roper, J. Corporate reports on sustainability and sustainable development: ‘We have arrived’. Sustain. Dev. 2014, 22, 42–51. [Google Scholar] [CrossRef]

- Asif, M.; Searcy, C.; Zutshi, A.; Ahmad, N. An integrated management systems approach to corporate sustainability. Eur. Bus. Rev. 2011, 56, 7–17. [Google Scholar]

- Medel-González, F.; García-Ávila, L.F.; Salomon, V.A.P.; Marx-Gómez, J.; Hernández, C.T. Sustainability performance measurement with Analytic Network Process and balanced scorecard: Cuban practical case. Production 2016, 26, 527–539. [Google Scholar] [CrossRef] [Green Version]

- Kocmanová, A.; Pavláková Dočekalová, M.; Škapa, S.; Smolíková, L. Measuring corporate sustainability and environmental, social, and corporate governance value added. Sustainability 2016, 8, 945. [Google Scholar] [CrossRef] [Green Version]

- Dočekalová, M.P.; Kocmanová, A. Composite indicator for measuring corporate sustainability. Ecol. Indic. 2016, 61, 612–623. [Google Scholar] [CrossRef]

- Aras, G.; Tezcan, N.; Furtuna, O.K. Multidimensional comprehensive corporate sustainability performance evaluation model: Evidence from an emerging market banking sector. J. Clean. Prod. 2018, 185, 600–609. [Google Scholar] [CrossRef]

- Ahi, P.; Searcy, C.; Jaber, M.Y. A quantitative approach for assessing sustainability performance of corporations. Ecol. Econ. 2018, 152, 336–346. [Google Scholar] [CrossRef]

- Sari, Y.; Hidayatno, A.; Suzianti, A.; Hartono, M.; Susanto, H. A corporate sustainability maturity model for readiness assessment: A three-step development strategy. Int. J. Product. Perform. Manag. 2021, 70, 1162–1186. [Google Scholar] [CrossRef]

- Siew, R.Y. A review of corporate sustainability reporting tools (SRTs). J. Environ. Manag. 2015, 164, 180–195. [Google Scholar] [CrossRef] [PubMed]

- Christofi, A.; Christofi, P.; Sisaye, S. Corporate sustainability: Historical development and reporting practices. Manag. Res. Rev. 2012, 35, 157–172. [Google Scholar] [CrossRef]

- Searcy, C.; Elkhawas, D. Corporate sustainability ratings: An investigation into how corporations use the Dow Jones Sustainability Index. J. Clean. Prod. 2012, 35, 79–92. [Google Scholar] [CrossRef]

- Delmas, M.; Blass, V.D. Measuring corporate environmental performance: The trade-offs of sustainability ratings. Bus. Strategy Environ. 2010, 19, 245–260. [Google Scholar] [CrossRef]

- Pryshlakivsky, J.; Searcy, C. A heuristic model for establishing trade-offs in corporate sustainability performance measurement systems. J. Bus. Ethics 2017, 144, 323–342. [Google Scholar] [CrossRef]

- Hansen, E.G.; Schaltegger, S. The sustainability balanced scorecard: A systematic review of architectures. J. Bus. Ethics 2016, 133, 193–221. [Google Scholar] [CrossRef]

- Ye, C.; Song, X.; Liang, Y. Corporate sustainability performance, stock returns, and ESG indicators: Fresh insights from EU member states. Environ. Sci. Pollut. Res. 2022, 29, 87680–87691. [Google Scholar] [CrossRef] [PubMed]

- Schneider, A.; Meins, E. Two dimensions of corporate sustainability assessment: Towards a comprehensive framework. Bus. Strategy Environ. 2012, 21, 211–222. [Google Scholar] [CrossRef]

- Mamede, P.; Gomes, C.F. Corporate sustainability measurement in service organizations: A case study from Portugal. Environ. Qual. Manag. 2014, 23, 49–73. [Google Scholar] [CrossRef]

- Delmas, M.A.; Clark, K.; Timmer, T.; McClellan, M. The State of Corporate Sustainability Disclosure. SSRN Electron. J. 2022. [Google Scholar] [CrossRef]

- Iyer, J.R. Corporate Citizenship and Sustainability: Measuring Intangible, Fiscal, and Ethical Assets (Issn) Paperback; Business Expert Press: New York, NY, USA, 2020. [Google Scholar]

- Diez-Cañamero, B.; Bishara, T.; Otegi-Olaso, J.R.; Minguez, R.; Fernández, J.M. Measurement of corporate social responsibility: A review of corporate sustainability indexes, rankings and ratings. Sustainability 2020, 12, 2153. [Google Scholar] [CrossRef] [Green Version]

- Boiral, O.; Talbot, D.; Brotherton, M.C. Measuring sustainability risks: A rational myth? Bus. Strategy Environ. 2020, 29, 2557–2571. [Google Scholar] [CrossRef]

- Lee, K.-H.; Saen, R.F. Measuring corporate sustainability management: A data envelopment analysis approach. Int. J. Prod. Econ. 2012, 140, 219–226. [Google Scholar] [CrossRef]

- Saisana, M.; Tarantola, S. State-of-the-Art Report on Current Methodologies and Practices for Composite Indicator Development; European Commission, Joint Research Centre: Brussels, Belgium, 2002; Volume 214.

- Nikolaou, I.E.; Tsalis, T.A.; Evangelinos, K.I. A framework to measure corporate sustainability performance: A strong sustainability-based view of firm. Sustain. Prod. Consum. 2019, 18, 1–18. [Google Scholar] [CrossRef]

- Singh, R.K.; Murty, H.R.; Gupta, S.K.; Dikshit, A.K. Development of composite sustainability performance index for steel industry. Ecol. Indic. 2007, 7, 565–588. [Google Scholar] [CrossRef]

- Saisana, M.; Saltelli, A.; Tarantola, S. Uncertainty and sensitivity analysis techniques as tools for the quality assessment of composite indicators. J. R. Stat. Soc. Ser. A (Stat. Soc.) 2005, 168, 307–323. [Google Scholar] [CrossRef]

- Sridhar, K.; Jones, G. The three fundamental criticisms of the Triple Bottom Line approach: An empirical study to link sustainability reports in companies based in the Asia-Pacific region and TBL shortcomings. Asian J. Bus. Ethics 2013, 2, 91–111. [Google Scholar] [CrossRef] [Green Version]

- Salvati, L.; Zitti, M. Assessing the impact of ecological and economic factors on land degradation vulnerability through multiway analysis. Ecol. Indic. 2009, 9, 357–363. [Google Scholar] [CrossRef]

- Morrison-Saunders, A.; Pope, J. Conceptualising and managing trade-offs in sustainability assessment. Environ. Impact Assess. Rev. 2013, 38, 54–63. [Google Scholar] [CrossRef] [Green Version]

- Olsthoorn, X.; Tyteca, D.; Wehrmeyer, W.; Wagner, M. Environmental indicators for business: A review of the literature and standardisation methods. J. Clean. Prod. 2001, 9, 453–463. [Google Scholar] [CrossRef]

- Rahdari, A.H.; Rostamy, A.A.A. Designing a general set of sustainability indicators at the corporate level. J. Clean. Prod. 2015, 108, 757–771. [Google Scholar] [CrossRef]

- Maltz, A.C.; Shenhar, A.J.; Reilly, R.R. Beyond the balanced scorecard:: Refining the search for organizational success measures. Long Range Plan. 2003, 36, 187–204. [Google Scholar] [CrossRef]

- Journeault, M. The Integrated Scorecard in support of corporate sustainability strategies. J. Environ. Manag. 2016, 182, 214–229. [Google Scholar] [CrossRef]

- Möller, A.; Schaltegger, S. The sustainability balanced scorecard as a framework for eco-efficiency analysis. J. Ind. Ecol. 2005, 9, 73–83. [Google Scholar] [CrossRef]

- Epstein, M.J.; Roy, M.-J. Sustainability in action: Identifying and measuring the key performance drivers. Long Range Plan. 2001, 34, 585–604. [Google Scholar] [CrossRef]

- Jensen, M.C. Value maximisation, stakeholder theory and the corporate objective function. In Unfolding Stakeholder Thinking; Routledge: Abingdon, UK, 2017; pp. 65–84. [Google Scholar]

- Molla, M.S.; Ibrahim, Y.B.; Ishak, Z.B. Corporate sustainability practices: A review on the measurements, relevant problems and a proposition. Glob. J. Manag. Bus. Res. 2019, 19, 1–8. [Google Scholar]

- Weber, R.P. Measurement models for content analysis. Qual. Quant. 1983, 17, 127–149. [Google Scholar] [CrossRef]

- Ng, L. Social Responsibility Disclosures of Selected New Zealand Companies for 1981, 1982 and 1983, Occasional Paper; Massey University: Palmerston North, New Zealand, 1985; Volume 54. [Google Scholar]

- Hackston, D.; Milne, M.J. Some determinants of social and environmental disclosures in New Zealand companies. Account. Audit. Account. J. 1996, 9, 77–108. [Google Scholar] [CrossRef]

- Milne, M.J.; Adler, R.W. Exploring the reliability of social and environmental disclosures content analysis. Account. Audit. Account. J. 1999, 12, 237–256. [Google Scholar] [CrossRef] [Green Version]

- Al-Tuwaijri, S.A.; Christensen, T.E.; Hughes Ii, K. The relations among environmental disclosure, environmental performance, and economic performance: A simultaneous equations approach. Account. Organ. Soc. 2004, 29, 447–471. [Google Scholar] [CrossRef]

- Charnes, A.; Cooper, W.W.; Rhodes, E. Measuring the efficiency of decision making units. Eur. J. Oper. Res. 1978, 2, 429–444. [Google Scholar] [CrossRef]

- Küçükbay, F.; Sürücü, E. Corporate sustainability performance measurement based on a new multicriteria sorting method. Corp. Soc. Responsib. Environ. Manag. 2019, 26, 664–680. [Google Scholar] [CrossRef]

- Bezerra, P.R.S.; Schramm, F.; Schramm, V.B. A multicriteria model, based on the PROMETHEE II, for assessing corporate sustainability. Clean Technol. Environ. Policy 2021, 23, 2927–2940. [Google Scholar] [CrossRef]

- Vivas, R.; Sant’anna, Â.; Esquerre, K.; Freires, F. Measuring sustainability performance with multi criteria model: A case study. Sustainability 2019, 11, 6113. [Google Scholar] [CrossRef] [Green Version]

- Aktaş, N.; Demirel, N. A hybrid framework for evaluating corporate sustainability using multi-criteria decision making. Environ. Dev. Sustain. 2021, 23, 15591–15618. [Google Scholar] [CrossRef]

- Rao, S.-H. A hybrid MCDM model based on DEMATEL and ANP for improving the measurement of corporate sustainability indicators: A study of Taiwan High Speed Rail. Res. Transp. Bus. Manag. 2021, 41, 100657. [Google Scholar] [CrossRef]

- Wright, J.M.; Caudill, R.J. A more comprehensive and quantitative approach to corporate sustainability. Environ. Impact Assess. Rev. 2020, 83, 106409. [Google Scholar] [CrossRef]

- Dickinson, D. A Proposed Universal Environmental Metric; Lucent Technologies Bell Laboratories Technical Memorandum: Murray Hill, NJ, USA, 1999. [Google Scholar]

- Zenya, A.; Nystad, Ø. Assessing corporate sustainability with the enterprise sustainability evaluation tool (E-SET). Sustainability 2018, 10, 4661. [Google Scholar] [CrossRef] [Green Version]

Figure 1.

Literature search strategy and results.

Figure 2.

Yearly classification of articles on CS assessment, 2010–2022.

Figure 3.

Aspects of corporate sustainability assessment.

Figure 4.

Overview of methodologies for assessing CS and limitations. Note (1): Two articles and 1 Book.

Figure 4.

Overview of methodologies for assessing CS and limitations. Note (1): Two articles and 1 Book.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Table 1.

Overview of the articles with focus on Frameworks.

| Authors | Year | Subject | Journal | |

|---|---|---|---|---|

| 1 | Baumgartner | 2013 | Offers a conceptual framework of the relevance of sustainability aspects of firms | CSR and Environmental Management |

| 2 | Cagno et al. | 2019 | Develops a new framework for the evaluation of industrial sustainability performance | Journal of Cleaner Production |

| 3 | Delai and Takahashi | 2011 | Develops a reference model for measuring | CS Social Responsibility Journal |

| 4 | Goyal et al. | 2013 | Identify the CS practices to improve sustainability performance | Journal of Modelling in Management |

| 5 | Kocmanová and Šimberová | 2014 | Determines CS indicators as a key framework of sustainable performance | Journal of Business Economics and Management |

| 6 | Maas et al. | 2016 | Proposes a comprehensive Framework | Journal of Cleaner Production |

| 7 | Moldavska and Welo | 2018 | Develops a framework to assist companies with identification of improvements to meet GSD goals | Sustainability |

| 8 | Pádua and Jabbour | 2015 | Identifies relevant aspects to guide promotion of CS | Business Process Management Journal |

| 9 | Sala et al. | 2015 | Presents a novel methodological framework for sustainability assessment | Ecological Economics |

| 10 | Searcy | 2014 | Identifies key requirements for measuring enterprise sustainability | Business Strategy & Environment |