Trust, Power, and Tax Risk into the “Slippery Slope”: A Corporate Tax Compliance Model

Department of Fiscal Administration, Faculty of Administrative Sciences, Universitas Indonesia, Depok 16424, Indonesia

*

Author to whom correspondence should be addressed.

Sustainability 2022, 14(22), 14670; https://doi.org/10.3390/su142214670

Submission received: 4 October 2022

/

Revised: 29 October 2022

/

Accepted: 5 November 2022

/

Published: 8 November 2022

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Abstract

:(1) Background: There are still few studies that discuss corporate tax risk, especially those related to tax compliance and the Slippery Slope Framework. Meanwhile, in practice, tax risk, which is tax uncertainty, is essential in corporate tax compliance. Tax risk has not been discussed in the Slippery Slope Framework in previous research, which has become a reference in various tax compliance studies. Therefore, this study aims to analyze the effect of tax risk induced into the slippery slope framework at corporate taxpayer compliance. Dynamic interactions between power, trust, and tax risk (TPR) in one framework are essential to see the tax compliance model’s determinants comprehensively; (2) Methods: We defined our model using a mathematical and economic approach with a Likert scale, as well as geometrical inferences based on the Slippery Slope Framework. (3) Results: This study found that tax risk affects the effort and tendency of corporate taxpayers to comply. The level of tax risk will make it easier or more difficult for corporate taxpayers to comply. Tax risk will affect the level of tax compliance regardless of the quality of trust and existing power; (4) Conclusions: This research’s theoretical contributions are that trust and power are determinants of tax compliance and that tax risk influences companies to be more compliant. This model is to complete the conceptual gap of the determinants of tax compliance from the perspective of the Slippery Slope Framework. The practical implication is that corporate taxpayers should manage tax risk to avoid unexpected tax outcomes in the future and be more compliant. Therefore, the government needs to help companies reduce compliance risks that cannot be controlled by companies but can be influenced by tax authorities.

1. Introduction

Tax is a dynamic fiscal policy instrument. Tax revenue is primarily determined by taxpayer compliance. Tax compliance is one of the challenges that the government must face because it can affect a country’s revenue, which impacts a country’s economic development [1]. The problem of tax non-compliance has become a challenge for the government [2]. The universal problem that all administrators face is tax noncompliance [3,4,5,6,7,8,9]. Taxpayers use various schemes to minimize tax payments to save taxes. The emergence of tax risk is accompanied by a decrease in state tax revenues [10]. Tax risk can cause losses for all parties if not managed properly and can cause a domino effect that affects other risks [10,11]. Tax risk is essential for tax authorities and companies to manage because it will affect the achievement of objectives.

The Slippery Slope Framework (SSF) is used to understand tax compliance [12]. The SSF states that there are two forms of tax compliance: power and trust. Power (of) and trust (in) tax authorities are relevant dimensions for understanding tax compliance [13,14,15]. Research on these two forms of compliance has attracted the attention of tax researchers and has always been a reference in tax compliance research and tax policy. However, studies on tax compliance mainly examine individual behavior [16,17]. There is still little research on tax compliance in corporate taxpayers [16,18,19]. The tax compliance model is being changed into a compliance model within the organization and power and trust in tax authorities are considered to be the main moderators of compliance. Tax authorities can enforce compliance with organizational goals through oversight and penalties or enhance voluntary compliance through the trust dimension [20].

Several previous studies agreed with this view through the results of empirical testing on corporate taxpayers [21,22,23,24,25,26,27,28,29,30,31,32,33,34,35,36,37,38,39,40,41,42,43,44,45,46,47]. From these studies, the dimensions of power and trust and their interaction are essential factors in tax compliance and are concerns of tax authorities in various countries and tax compliance researchers [40,48,49,50,51,52]. Problems arise when obstacles and other factors (distortions) in an equilibrium system make optimal conditions unattainable [53]. The policy requires an investigation of the interaction of existing elements because there are gaps in theory and practice in the real world, so one must look at policy barriers that exist in the real world [54]. Existing compliance research focuses more on the dimensions of power and trust as factors that influence taxpayer compliance behavior [55]. Still, taxpayers will make rational decisions in uncertainty by considering risk factors in making tax decisions [4,56,57,58,59]. Risk analysis can improve the basic approach of compliance risk management in determining rational decisions in carrying out tax compliance [60].

Large businesses play an essential role in the economy because of their significant tax contribution to the state budget [61]. Reducing uncertainty (risk) is important in the compliance strategy because uncertainty can cause a mismatch between the tax burden and the tax paid [62]. Tax risk has a negative effect on company risk [63]. Tax risk is defined from the perspective of tax practitioners and tax authorities as to the uncertainty about future tax outcomes generated by current actions or activities or the failure to take actions or pursue activities from economic risk, tax law uncertainty, and inaccurate information processing [64]. Tax risk is uncertainty relating to corporate taxes, tax payments, and corporate tax burdens in the future [65]. Tax risks will affect the achievement of strategy and business objectives [66]. Saragih & Ali (2021) conducted a literature review of tax risk and stated that few studies discuss it. Research on tax risk examines events from the point of view of tax avoidance as it occurs [67,68,69,70,71,72,73], while other tax risk research focuses on sources and measurements of tax risk [10,64]. Abernathy et al. (2019) tested how external auditors respond to tax risk [74]. Wilde & Wilson (2018) encourage researchers to dig further into the concept of tax risk to gain a deeper understanding of it. So, including the aspect of tax risk is very important to understand the compliance behavior of taxpayers [75].

This study aims to analyze the effect of tax risk induced into the slippery slope framework on corporate taxpayer compliance [13]. The tax risk dimension that is not included in the reference model will be the 3rd variable in the SSF in addition to power and trust, even though the tax risk dimension is essential in understanding corporate behavior on tax compliance because it relates to the uncertainty faced by corporate taxpayers. The level of tax risk seen from this study includes low, moderate, and high tax risks. This study also analyzes the dynamic interaction between power, trust, and tax risk in one framework to see the tax compliance model’s determinants comprehensively.

This study uses a Likert scale approach in the formulation and in-depth explanation of tax compliance with trust, power, and risk dimensions. According to Torgler, (2016), collecting data for research on tax compliance poses difficulties [76]. Therefore, creativity is needed [77]. The existence of tax risk and changes in its values will be so similar that it does not change the way of assessing tax compliance [13]. However, tax compliance will change along with changes in the level of tax risk. Changes will be seen in the visualized model carried out in this study. This study only includes the tax risk variable in the model but does not conduct empirical testing. Nevertheless, this study contributes to completing the conceptual gap regarding tax compliance behavior in corporate taxpayers by including the dimensions of tax risk, power, and trust in one framework and analyzing the effect of these three variables on the company’s efforts to fulfill tax obligations. It is hoped that this study will provide a comprehensive understanding of the behavior of corporate taxpayers in their efforts to comply with taxes and what tax authorities and taxpayers should do to reduce this.

1.1. Tax Compliance Theory in Economic Perspective

Tax compliance research begins with the theory developed by [56]: failure to comply with tax regulations (non-compliance) is a form of criminal behavior. The theory of criminal behavior states that a person exhibits criminal behavior not because of his motivation, but because of the consideration of cost and benefits (benefits are greater than costs). If the benefits of tax cheating or any form of criminal behavior outweigh the risks, people will commit tax fraud or a corresponding crime [78]. Lawbreakers have a risk preference. More severe offenses must be resolved more frequently and punished more severely than lesser offenses. Tax compliance is a decision taken under uncertainty (risk) [56].

Tax compliance research [4,56,79] has determined that taxpayers, in making tax compliance decisions, have the objective of maximizing the utility function and are willing to bear the consequences of tax evasion, if detected and punishment is imposed. This indicates a risk preference over audit probabilities and sanctions. The economic deterrence model of tax compliance assumes risk aversion [58]. This study looks at the economic approach (economic deterrence) by evaluating costs and benefits (cost–benefit analysis) when determining the amount owed, assuming that decisions related to tax reporting (tax declarations) are decisions that are covered by uncertainty (risk) [4]. Taxpayers have rational behavior [4], and seek to maximize the expected utility (expected utility maximizers) in their decisions to report taxes and tax compliance [80,81,82]. We conclude that the Allingham & Sandmo (1972) paradigm is tax compliance behavior as a decision based on risk considerations [4].

Taxpayers are driven to maximize their expected utility by rationally weighing the importance and likelihood of various outcomes in their decisions [4,79]. The rational choice model assumes that everyone knows all decision alternatives, weighs, and chooses the option that produces the highest prospects. Still the taxpayer does not know all alternatives and has bounded rationality (limited cognitive ability). Therefore, it can be said that tax compliance behavior is an individual decision based on risk considerations (as an individual decision under risk) [4,79]. Expected Utility Theory (EUT) is an analysis of risk-based decision-making. The normative theory of rational choice in decision making is often faced with uncertainty. In classical economics, rationality occurs when we are unsure of the outcome resulting from the action to be taken (uncertainty), so the chosen decision gives the highest expected utility. The basic premise in decision-making theory is relevant to explain why taxpayers comply or do not comply with tax regulations. Based on economic rationality, everyone has preferences and has alternatives to obtain the desired results, presented through utility maximization. Therefore, utility theory is considered capable of explaining economic behavior. Rational behavior is described such that the standard economic model would maximize the expected utility [83,84]. The expected utility of each decision alternative will be assessed by identifying the possible outcomes of each choice and looking at the probability (likelihood) of uncertain outcomes.

Prospect Theory research critiques the expected utility theory (EUT), which is considered a descriptive model of decision making under risk, with criticism of decision making that can be seen between prospects or gambles [57]. The choice among risky prospects exhibits some inconsistent pervasive effects based on the basic tenets of utility theory. This study examines the certainty effect, namely risk aversion in choices involving definite gains and risk-seeking in substantial losses options. Prospect theory developed by Kahneman & Tversky is the beginning of the development of modern behavioral economics [57,84]. Any tax paid will be viewed as a loss by taxpayers. Therefore, everyone will pay attention to the risks associated with their tax deductions. Prospect theory is a decision under risk.

1.2. Tax Compliance from a Psychology Perspective

Prospect theory draws criticism. The explanation of the motive for tax compliance due to economic factors shows inconsistencies. Kirchler et al. (2008) said that taxpayers are willing to pay taxes and believe in the applicable taxation system. Hence, the tax compliance model is based on an economic perspective, far from predicting tax evasion behavior compared to the actual situation. Andreoni et al. (1998) show that audit probability has little effect on compliance and conclude that subjective probability can be mediated through psychological variables. The failure of the economic model to predict tax compliance makes researchers aware that other aspects affect compliance from the perspective of psychology. Psychological contract research conducted by Rousseau (1989, 1995) and Osterloh & Frey (2000) contains a formal contract that the parties must obey the agreement. Psychological contracts were later developed by Frey & Feld (2002) and Torgler et al. (2008). According to the agreement, if there is a violation by the parties, there will be sanctions (Frey & Feld, 2002). In the concept of a psychological contract, “taxpayers and the authority treat each other as partners, that is, with mutual respect and honestly” (Feld & Frey, 2007). According to Torgler & Schaltegger (2005), tax compliance will increase if the tax authority treats taxpayers as partners, honest, fair, informative, and mutually beneficial. Trust that is built with respect and good treatment is one of the variables that have an impact on tax compliance. The psychological contract is based on a trust-based relationship between the government, tax authorities, and taxpayers (Alm et al., 2012), believing that tax funds are spent according to tax purposes. Planned behavior (theory of Planned Behavior) was developed by Ajzen (1991). A person’s behavior is driven by three factors: behavioral beliefs, normative beliefs, and control beliefs. James & Alley (2002) concluded that the two approaches (economic and behavioral approaches) should support each other to increase voluntary tax compliance. In their study, Fishbein & Ajzen (2011) use the assumption that individuals are rational and would make judgments based on all available information. Individuals will examine the consequences of their actions before making a choice (Musimenta et al., 2019).

1.3. Slippery Slope Framework–Power and Trust

Research on tax compliance prevention models (deterrence models) developed by Becker (1968), Allingham & Sandmo (1972), and Srinivasan (1973) only looked at the factors that affect tax compliance. This model is considered to fail to see the problem of tax compliance in its entirety. This model cannot explain why taxpayers are willing to pay taxes voluntarily without law enforcement (voluntary compliance tax) (Torgler, 2003b). Feld & Frey (2007) proposed the psychological tax contract, and Torgler et al. (2008) are also considered unable to explain tax compliance fully. Kirchler et al. (2008) then integrate tax compliance from an economic and psychological perspective on tax behavior, which states that the power of tax authorities and taxpayers’ trust in tax authorities are determinants of tax compliance, as stated in the Slippery Slope Framework (Kirchler et al., 2008, 2014). Increased power authority and trust building are used in SSF to obtain tax compliance. Tax compliance will be enforced by power based on control and punishment, but trust building leads to voluntary tax compliance.

The power dimension shows how people think the government can find tax evasion, audit, and punish tax evaders. Power is considered high if audits are frequent and effective, with high fines. Allingham & Sandmo (1972); Slemrod et al. (2001); Kornhauser (2007); McKerchar & Evans (2009); Cummings et al. (2009); Alm et al. (2010); Jackson & Milliron (2002); Braithwaite (2002); Frey & Torgler (2007), Palil & Mustapha (2011), Devos (2014); and Nguyen et al. (2020) found that law enforcement through audits and sanctions will improve tax compliance. The high probability of detection and sanctions will lead to an increase in tax compliance. Taxpayers will report income and pay taxes for fear of audits and fines. However, efforts that rely only on high power encourage negative tax compliance (Olsen et al., 2018).

The psychological determinants of tax compliance are equally important as the probabilities of audits and penalties (Kirchler, 2007). Tax compliance is also based on a trusting relationship between taxpayers and tax authorities (Muehlbacher & Kirchler, 2010). Empirical evidence has found many dimensions of trust in improving overall tax compliance. Scholz & Lubell (1998) and Lisi (2014) found that trust had a positive effect on tax compliance. The trust factor is an important contribution to tax compliance. Trust is obtained through knowledge of tax law, taxpayer attitudes towards government and taxation, personal norms, perceived social norms and justice, and motivation to comply (Hofmann et al., 2008).

Jimenez & Iyer (2016) stated that trust is determined by psychological aspects such as social norms and justice perceptions. Kirchler et al. (2008) and Lisi (2014) state that tax compliance tends to be maximal when trust is maximized (TCmax = Tmax). Trust is an internal variable that depends on the tax climate, namely the relationship between tax authorities and corporate taxpayers (Lisi, 2014). Kirchler et al. (2008) argue that taxpayers’ attitude is essential in the dimensions of power and trust. Power and trust are thought to influence each other. Citizens with high trust will help to increase the authority of the authorities, or vice versa when acts of excessive power (burdensome audits and fines) are seen as signals of distrust. Lisi (2015) found an increase in trust significantly increased tax compliance, while an increase in power had a lower positive impact.

The term slippery slope refers to the mutual influence of power and trust. A decrease in one dimension can reduce another, which results in a significant reduction in tax compliance. At the bottom is a condition of low power and low confidence, in which citizens seek to maximize individual returns by avoiding taxes so that overall compliance is at a minimum. Kirchler et al. (2010) found that trust increases voluntary tax compliance while power decreases voluntary tax compliance. Power will increase enforced obedience, and trust will decrease forced obedience. Strategic behavior was higher in terms of low trust and high power than high trust and high power. Kogler et al. (2013) conducted SSF testing and discovered that conditions of strong trust and power resulted in the highest degree of compliance and the lowest amount of tax evasion. High trust indicates more voluntary compliance, and high-power conditions indicate higher enforced compliance.

Kirchler et al. (2014) stated that trust was good, but control was better. Audits and fines are used to combat tax evasion to prevent illegal behavior, but may have an undesirable effect. The combination of high power and high trust reduces negative feelings, increases intention to comply, and reduces tax avoidance (Olsen et al., 2018). Batrancea (2019) shows that trust and power are not wholly complimentary, as demonstrated by the negative interaction effect. Muehlbacher & Kirchler (2010) and Frey (2003) say that too frequent tax audits and strict penalties can damage the trust of honest taxpayers in tax authorities or communicate distrust to taxpayers. On the one hand, the absence of audits and fines can cast doubt on the authority of tax officials and foster mistrust in their efficacy and integrity. The SSF functions demonstrate that confidence in tax authorities grows with tax authority power until it reaches a maximum, but that subsequent increases in tax authority power have a negative effect on trust, ceteris paribus.

1.4. Tax Risk

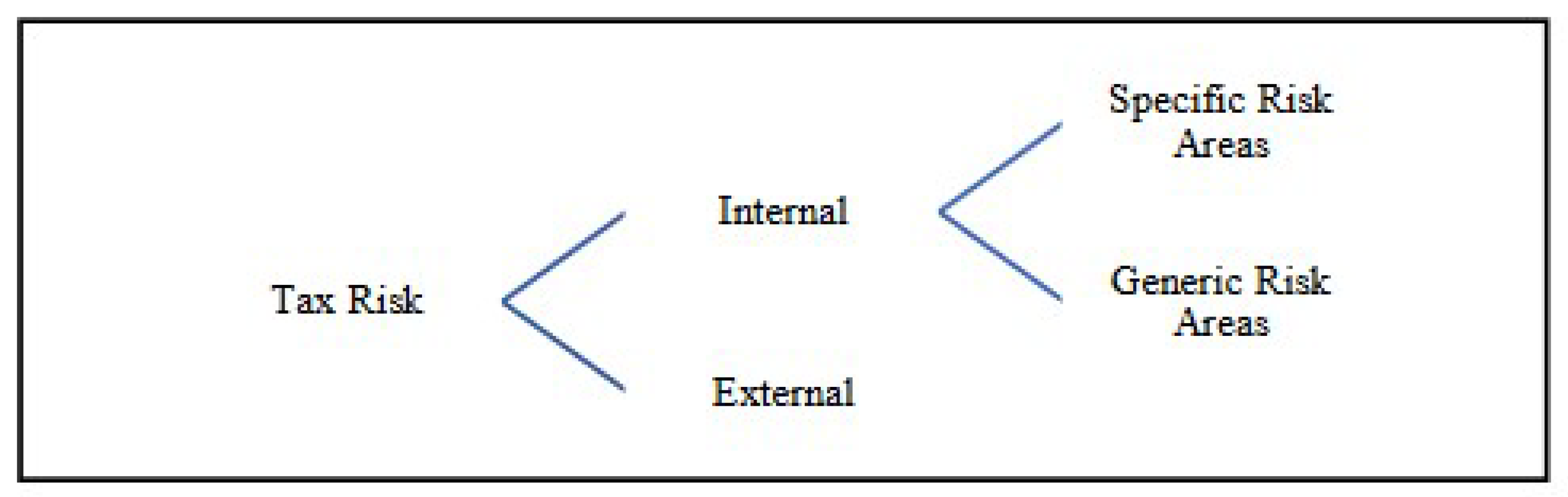

Research on tax compliance, which started from the economics of crime until now, is inseparable from the dimension of Risk. COSO (2017) defined Risk is the possibility that events will occur and affect the achievement of strategy and business objectives. ISO 3100 (2018) states that Risk affects uncertainty on objectives. An effect deviation from the expected can address, create, or result in opportunities and threats. Risk is usually expressed in terms of risk sources, potential events, consequences, and likelihood. PwC (2004) state that tax risk in an organization’s decisions, activities, and operations will cause various uncertainties, one of which is related to taxation. Tax uncertainty is related with the implementation of tax rules and regulations, including how effectively the system performs in determining tax returns for corporate activities and operations, which produces tax risk. Chen (2021a) said that tax risk is the uncertainty of corporate taxes, tax payments, and corporate tax burdens in the future. Lavermicocca (2011) defines tax risk as an event, action, or inaction in taxation strategies, operations, and financial reporting that negatively impacts corporate taxes, business operations, or results in unexpected or unacceptable monetary rates, financial statements, or reputation exposures. Tax risk is defined as a tax gap, the difference between the total amount of tax that must be paid according to the regulations and the amount paid (Vdovychenko & Zubrytskyi, 2013). According to Lin et al. (2019), tax risk refers to unexpected financial losses, negative elements, or unfavorable consequences resulting from the taxation process and issues. Risk is a combination of the likelihood of something happening and the impact that appears as a result. Risk appetite for taxpayers is often an important factor in the theoretical approach to tax compliance. Changes in risk appetite can have an impact on tax risk. Taxpayers may have different risk appetites (van Dijk & Siglé, 2015). Risk appetite reflects the level of uncertainty in the organization and shows a “willingness to accept” risk. If the company can accept more risk, it reflects a high-risk appetite and if the company does not want to take risks, it reflects a low-risk appetite. Tax risks related to tax compliance increase due to fluctuating tax policies (Deloitte, 2014). Risks associated with enforcement by tax authorities and the company’s ability to comply with changes in tax laws (EY, 2014). Eberhartinger & Zieser (2021) and Neuman et al. (2020) use best risk practices published by PwC (2004), Deloitte (2014) and EY (2014). PwC (2004) divides tax risk into two kinds, namely risks from internal and external sources (see Figure 1). Internal risk is the risk from internal sources that can be managed within the company. Meanwhile, the external risk is a risk that originates outside the company and cannot be managed by the company or is beyond the company’s control, such as changes to laws, unexpected court decisions, changes from the government, etc. External risk is as important as internal risk. Internal risk is divided into two areas, namely specific and generic areas.

Specific risk areas include (1) Transactional Risk, the risk and tax exposure of certain transactions carried out by the company. Every transaction may be subject to uncertainty, especially for complex and non-routine transactions. The more unusual or less routine a transaction is, the greater the tax risk on that transaction. Transaction risk usually occurs in non-routine transactions (not routine transactions such as sales of products or services). Tax risks associated with transactions such as acquisitions, dispositions, project restructuring, substantial reorganization, mergers, financing transactions, tax-driven cross-border transactions, and internal reorganizations are often higher risk. (2) Operational risk is the risk of implementing laws, regulations, and tax decisions in the company’s daily business operations. The degree of tax risk varies depending on the type of activity, such as the determination of transfer pricing. Compare sales of third-party products with sales of products across intra-group borders. Cross-border transactions carry greater risk. When a company operates globally, there may be a tax risk of becoming taxable in the country in which it operates. The closer the tax function is to corporate activities, the more effectively it can control risks. The examples of the operational risk area, new business and operating models and the influence of technical advancements are all examples of operational risk. (3) Compliance risk is associated with fulfilling an organization’s tax compliance obligations (Neuman et al., 2020; PwC, 2004). Compliance risks arise from preparing, completing, and processing corporate tax returns for any tax. Compliance risk also encompasses risks inherent in the company’s systems, processes, and procedures for preparing and submitting tax returns and responding to any inquiries or issues raised by the authorities. The integrity of the underlying accounting information and systems is a compliance risk. It has been ascertained that the tax compliance analysis process is based on current knowledge of the most current tax rules and practices and efficient technology. Of course, there is a trade-off between costs and risks taken. What needs to be considered is ensuring that no errors appear on any tax return will almost certainly be prohibitively expensive. The company will engineer the process and reduce costs a little without impacting the risk position. However, the attitude towards tax sanctions must be determined. Low risk means no tolerance for compliance (no error rate), a high risk of receiving a high error rate. The risks associated with the agreement of tax returns, as well as investigations into or audits of submitted tax returns by fiscal authorities, are all part of the tax compliance risk. There is a link between compliance and reputational risk (PwC, 2004). Lack of effective management, poor accounting records or controls, data integrity difficulties, insufficient resources, system changes, legislation changes, revenue investigations, and particular local in-country customs, practices, and compliance emphasis are all common causes of tax compliance risk. Compliance risk includes the inherent risk of the company’s systems, processes, and procedures (inherent risk) in reporting tax returns or other required documents, payment of taxes, or adequate documentation, which may pose financial risks after inspection, including penalties and interest incurred. (4) Financial Accounting Risk is a risk in the field of financial accounting that arises due to changes in legislation, changes in accounting systems, and changes in accounting policies and standards. Some accounting records require estimates. The figures in the account contain uncertainties that exist in the interpretation or application of laws used to calculate tax rates, data quality, and provisions necessary to cover uncertainties and an acceptable level of materiality. Unquantified risk will produce a high risk or low degree of certainty.

Generic risk areas are more about how to manage existing risks. Generic risks include (5) Managerial risks, which are not appropriately managed by specific risks. Managerial risk, among others, is caused by changes in tax personnel and company business personnel. Corporate tax information is often carried in the heads of people in the corporate tax division. When they resign, they will take the tax information they know, which has not been well documented. It could also be because the company does not have experience or new human resources in taxation. (6) Reputational risk involves a broader impact on the company. Risks arise from corporate actions related to taxes that are a matter of public knowledge and impact broader business interests. Businesses must evaluate the impact of litigating a tax problem in a public forum, such as tax authority raids, investigation press releases, and the courts’ information about company activities may influence changing perceptions of consumers, suppliers, and employees. Aggressive tax planning may be detrimental to a business’s reputation. The danger to one’s reputation includes a raid or inquiry by the Internal Revenue Service, press statements, judicial proceedings, or legal action developments in politics. For a business, reputation risk is essential (7) Portfolio risk is the total risk associated with transactional, operational, and compliance risks taken together and the interaction of three different specific risk areas. Certain transactions may be below the risk threshold, but are revealed to represent an unacceptable cumulative risk profile when combined with other risks. The company must consider the worst-case scenario and its impact on the income statement and balance sheet, as well as whether it is acceptable.

Businesses can assess portfolio risk by analyzing the impact and likelihood of certain risks that occur. Ying et al. (2019) add to financial risk in their research on the manufacturing industry. Risks related to tax are financial and reputation risks PwC (2019). Internal risk is managed within the organization (controllable risk), while external risks that cannot be managed by the company but are very important affect the company, such as changes to laws or unexpected court decisions that can cause actual losses for the company. Borrego et al. (2015) and Lavermicocca (2011) assert that the Income Tax Law’s ambiguity and complexity contribute significantly to tax risk, which eventually results in firms failing to comply with the Income Tax Law. According to Kirchler (2007), tax law is too complex to be fully understood. The main tax risk is complex tax laws, regulations and many items that allow ambiguous and controversial interpretations (Artemenko et al., 2017; Tsamis & Liapis, 2014). Changes in tax regulations are one source of tax risk (Artemenko et al., 2017). Therefore, we conclude that tax risk is the possibility of events, current tax action and strategy, tax law, and regulations for fulfilling tax obligation to affect future tax outcomes and impact the achievement of the company’s strategy and objectives.

This study hypothesizes that the level of tax risk affects tax compliance. The interaction between trust, power, and tax risk in a Slippery Slope Framework affects corporate taxpayer compliance.

2. Materials and Methods

This study attempts to provide a mathematical model that illustrates the slippery slope model of Kirchler et al. (2008) by including tax risk as a fourth dimension that changes how sloppy the model would be without violating any of its authenticity. It is to be understood that previously, Kirchler et al. (2008) did not provide a mathematical formulation of their slippery slope model. However, given the limitations it is still possible for the graph itself to reveal various information and criteria that can be inspected; using these, we then can extract underlying statements that form the slippery slope model to create a set of suitable mathematical conditions for modeling the slippery slope.

The stages in forming this mathematical approximation are divided into two parts: the first stage revolves around finding a mathematical notion that can describe the slippery slope regarding the power, trust, and tax compliance dimensions; the second stage will then revolve around the attempt to induce the tax risk variable into the mathematical model that has been built by the first stage (without altering any significant mathematical notion we have built). In other words, the tax risk variable will affect the slippery slope without changing how tax compliance, trust, and power change each other’s value as assessed and described by Kirchler et al. (2008). By choice, we would define our model using functions that revolve around numerical powers.

The essential variables and their notation for this paper in the modeling representing the slippery slope will be P = Power, T = Trust, R = Tax Risk, TC = Tax Compliance. To provide limitation to certain values for the model, an important constant for this model is introduced; that constant would be the upper limit of the Likert scale used to gather data. To show further development and provide an example, we will then show our model when the constant L is changed into 4, an upper limit of a Likert scale we could use to gather data. It is to be understood that in the formulation process later before reaching the final formulation, we would let L act as an important limiting value that is crucial in developing the best formulation possible.

3. Results

The main importance in defining our mathematical model is in such a way that it would fit the SSF geometrically; therefore, we would take geometrical inferences based on the SSF of Kirchler et al. (2008) and also premises developed from the theory and previous research that underly SSF as our main lead. The requirements for the mathematical model in this study are:

- (P, T, TC) = (1, 1, 1) for all values of R such that 1 ≤ R ≤ L

- (T, TC) = (L, L) for all values of R and P such that 1 ≤ R ≤ L and 1 ≤ P ≤ L

- (P, TC) = (L, L) for all values of R and T such that 1 ≤ R ≤ L dan 1 ≤ T ≤ L

- for each value of T, R, and P such that 1 ≤ T ≤ L, 1 ≤ R ≤ L, and 1 ≤ P ≤ L

- for each value of T, R, and P such that 1 ≤ T ≤ L, 1 ≤ R ≤ L, and 1 ≤ P ≤ L

- for each value of T, R, and P such that 1 ≤ T ≤ L, 1 ≤ R ≤ L, and 1 ≤ P ≤ L

- for each value of T, R, and P such that 1 ≤ T ≤ L, 1 ≤ R ≤ L, and 1 ≤ P ≤ L

- for each value of T, R, and P such that 1 ≤ T ≤ L, 1 ≤ R ≤ L, and P = L

- for each value of T, R, and P such that T = L, 1 ≤ R ≤ L, and 1 ≤ P ≤ L

- for each value of T, R, and P such that T = L, 1 ≤ R ≤ L, and 1 ≤ P ≤ L

- for each value of T, R, and P such that 1 ≤ T ≤ L, 1 ≤ R ≤ L, and P = L

The above requirements are obtained from the information taken from the visualization of Kirchler et al.’s SSF. Requirements 1~3 are adopted from the information regarding the “corner points” in the SSF model. Requirements 4~7 are adopted as assumptions to maintain the shape of our model so that it fits the fact that the increase in tax compliance will be in “diminishing returns” as the values of power and trust approach the highest level (Kirchler et al., 2008). Requirements 8~11 are adopted from the information regarding the “edges” in the SSF model, which maintain some similar values along a given condition. This model will then induce tax risk as a variable in the model such that whatever value it holds it still will hold all the given assumptions for the model for any possible values of the other variables.

The modeling in this study is expressed in the form of tax compliance (TC) as a direct function of T, P, R, and L for simplification purposes. The modeling takes an assumption that the change in the values of trust and power will have the same relationship and correspondences to tax compliance values when other variables in the function are considered constant. In other words, the formulation should be made such that it would be equivalent if the variable T is interchanged with the variable P. The first consideration for this modeling starts with the constraints represented by requirements 4~7; the first and second derivatives represent the concept of “diminishing returns” as the power and trust values approach their highest levels, providing a wide selection of “model types” such as models with trigonometric function(s), Euler constant function(s), numerical power function(s), or a combination of some of them. The given function should then help with the mathematical motivation in inserting the tax risk variable in the model. We proceed to define our model using a function revolving around numerical powers.

Without loss of generality, the formation of the “shadow” model will be reviewed first by approximating the TC expression in T when P is ignored. TC must be 1 when T is equal to 1, but TC must be L when T is equal to L. When T increases TC will also increase, but as T approaches L, the increase in TC will decrease following the concept of “diminishing returns”. The formulation will progress through this initial formulation stage:

where (L, T, R) is a function that can be expressed by L, T, and R, which fulfils the following requirements:

These constraints of course do not violate any requirements stated. Through certain inspection, a formulation such as the following is chosen to become the “shadow” of the complete formulation:

h(R) is a function in R (taken from the Likert value) such that when R increases then the tendency of the value of TC to increase decreases; alongside that, h(R) is also induced in such a way that all values of TC cannot be higher when R is higher and the other variables are kept constant; this is to align with our explanation of how tax risk would work with the changes in tax compliance. Due to that, it would be understood that in this formulation, h(R) would increase as R decreases for every value of R taken. On the other hand, the “shadow” model of the expression TC in P when T is not considered directly can be formed from the above equation when the variable T is changed to P:

These two “shadow” models are combined so that for any value and change, it would still be in the constraints of the original requirements. Furthermore, it considers the simplification such that the changes in TC when P is changed on a certain effect and magnitude will be the same when T is changed on the same effect and magnitude. Certain fitting processes are then carried out so that the resulting model maintains Kirchler et al.’s SSF authenticity. The essential coordinates are then maintained as per requirements 1~3. The following is a modified model to include TC, T, P, and R (in h(R)).

If expanded, the model will take the following form:

When we enter the value of L as 4 to match it to a certain Likert scale we would like to use, then the model will take the following form:

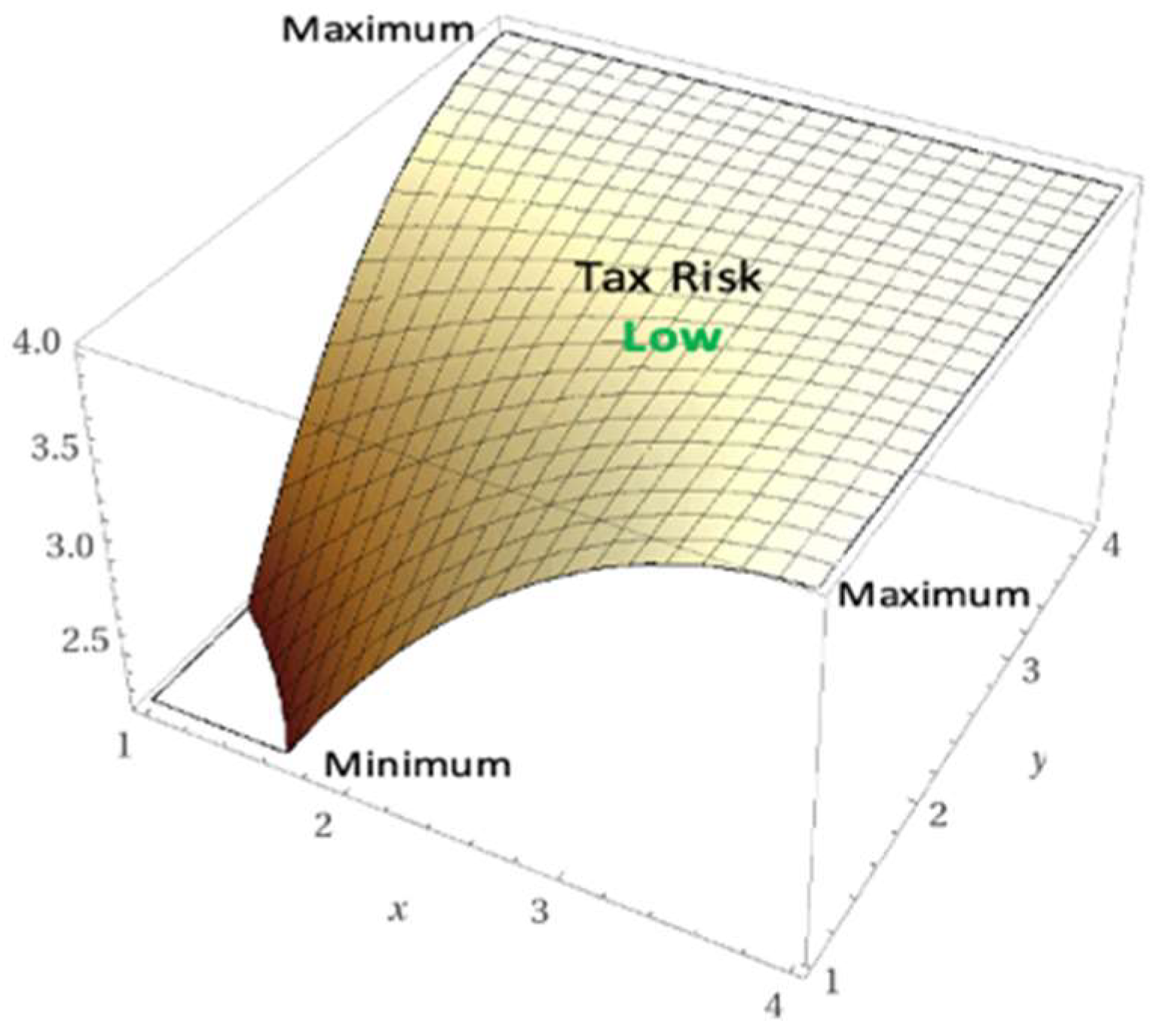

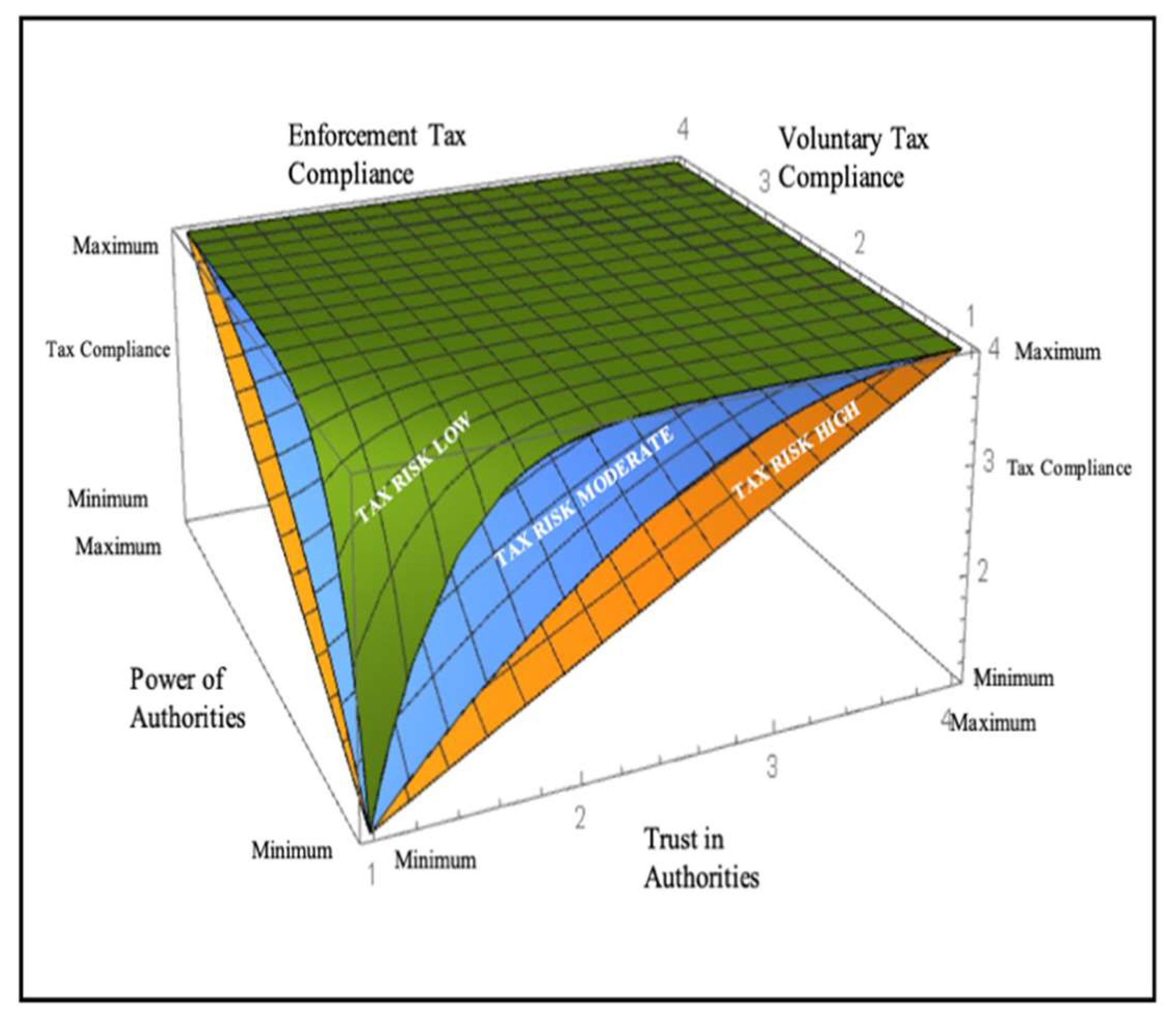

The visualization results that we expect and receive from this model when tax risk changes are as follows:

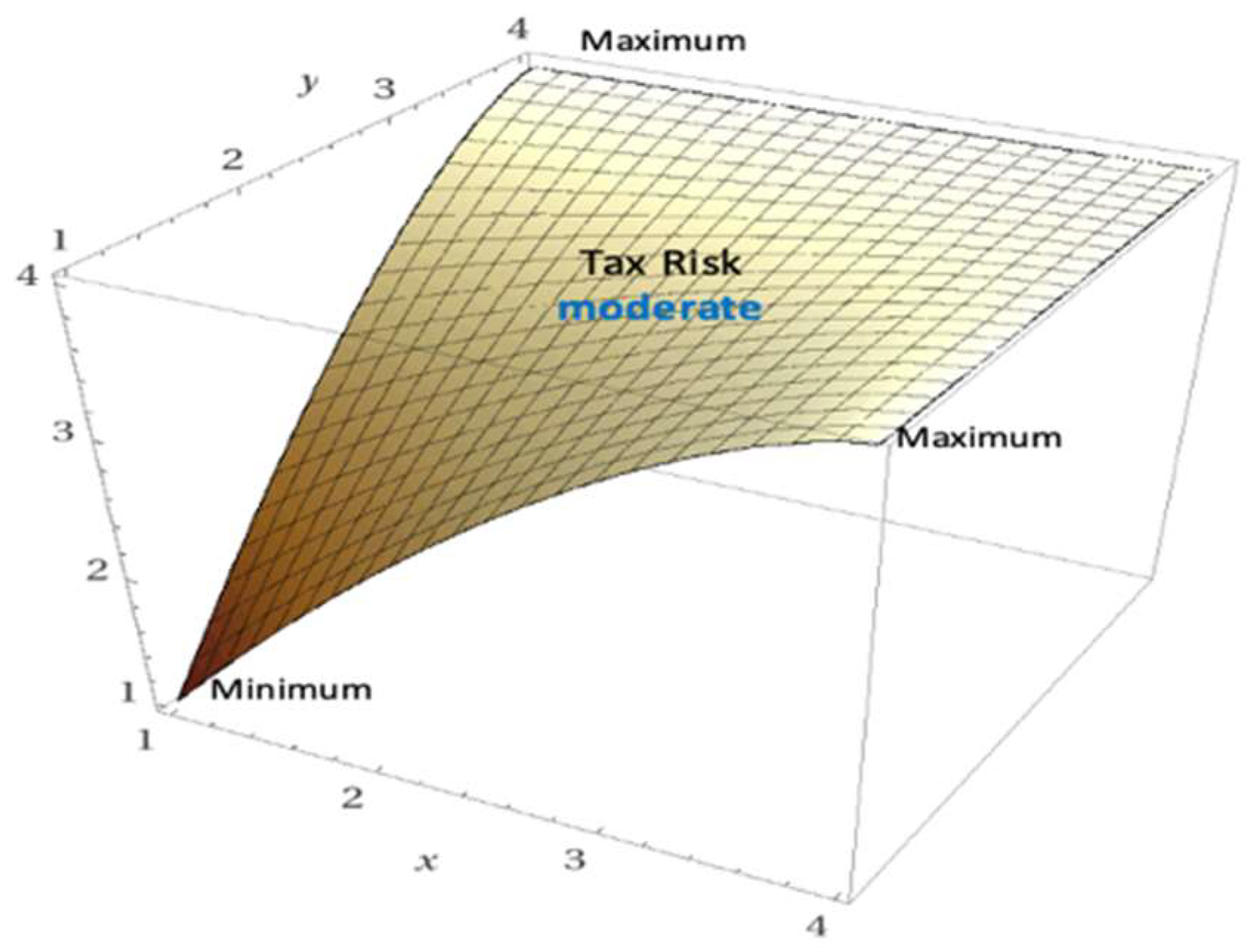

When the tax risk is low, as shown in Figure 2, the curve increases, meaning that a low level of tax risk in corporate taxpayers will make it easier for companies to comply. Lower tax risk does not necessarily guarantee compliance from corporate taxpayers; rather, it makes it easier for the taxpayer to comply. However, if the tax risk level is moderate, it will be seen in Figure 3.

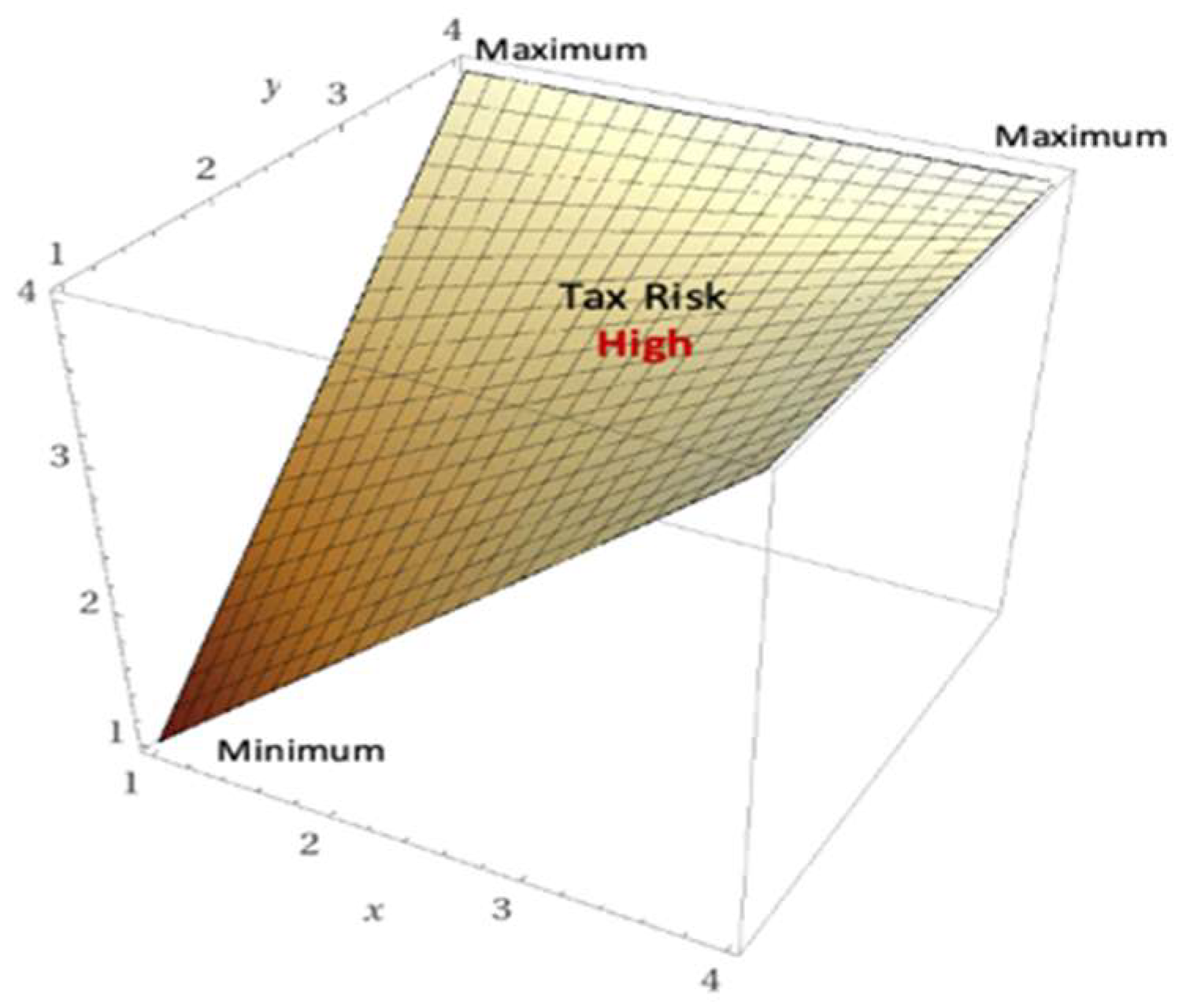

In Figure 3, the increase in the level of risk that the company must face will cause corporate taxpayers to find it increasingly difficult to comply with tax regulations. However, supposing the tax risk level is very high (see Figure 4), corporate internal risk such as a lack of effective accounting, tax controls and documents, data integrity, and changes in systems will increase compliance risk. Therefore, external risk such as legislation changes, complexity and ambiguity of tax regulations will increase compliance risk, effecting tax compliance. It will be increasingly difficult for taxpayers to comply; this does not mean that they do not want to comply, but that tax risk makes it more difficult or hinders companies from complying.

On the theoretical basis that has been described previously, it can be understood visually that as tax risk increases, it becomes increasingly difficult for corporate taxpayers to improve their tax compliance and vice versa. Observe Figure 5. If three graphs with different R levels—low, medium, and high—are to be compared, it can be understood visually that the graph with the lower R value will have their plane “above” the other plane with the higher R value (except for those on the constrained values) as the plane on the graph with the higher R value is sloped, inferring that entities will absolutely comply more to taxes if the given tax risk is lower.

As explained before, it can be further implied from Figure 5 that the level of tax risk will significantly affect the efforts of corporate taxpayers to comply as low tax risk will result in a higher TC value than the medium and high levels of risk. Ultimately, any value for tax risk will provide the same characteristics kept in the SSF; namely, how the “diminishing returns” concept is still being kept.

This study shows that the level of tax risk influences the efforts of corporate taxpayers to comply. When the tax risk is low, the plane becomes steeper, meaning that a low level of tax risk in corporate taxpayers will make it easier for companies to comply when the quality of trust and power increases. It is to be understood that there will be no guarantee that the company will comply if the tax risk is at its lowest; however, as tax risk increases, it would be easier for the company to comply as the quality of trust and power increases. Even companies with low risk levels should not have a level of trust or power of less than two on the Likert scale (less trust or less power). Therefore, the tax authorities must maintain the levels of trust and power at a minimum of two (it should not be less than two). When it is less than two, it will cause a decrease in the slope of tax compliance. As we can see, if the tax risk level had become moderate, it will be more challenging for to increase the tax compliance in value as lower increases in tax compliance are permitted with the same amount of increase in the quality of trust and power increases, which means that the increase in the level of risk faced by the company will cause corporate taxpayers to find it increasingly difficult to comply with taxes. Moreover, suppose the level of tax risk is high.

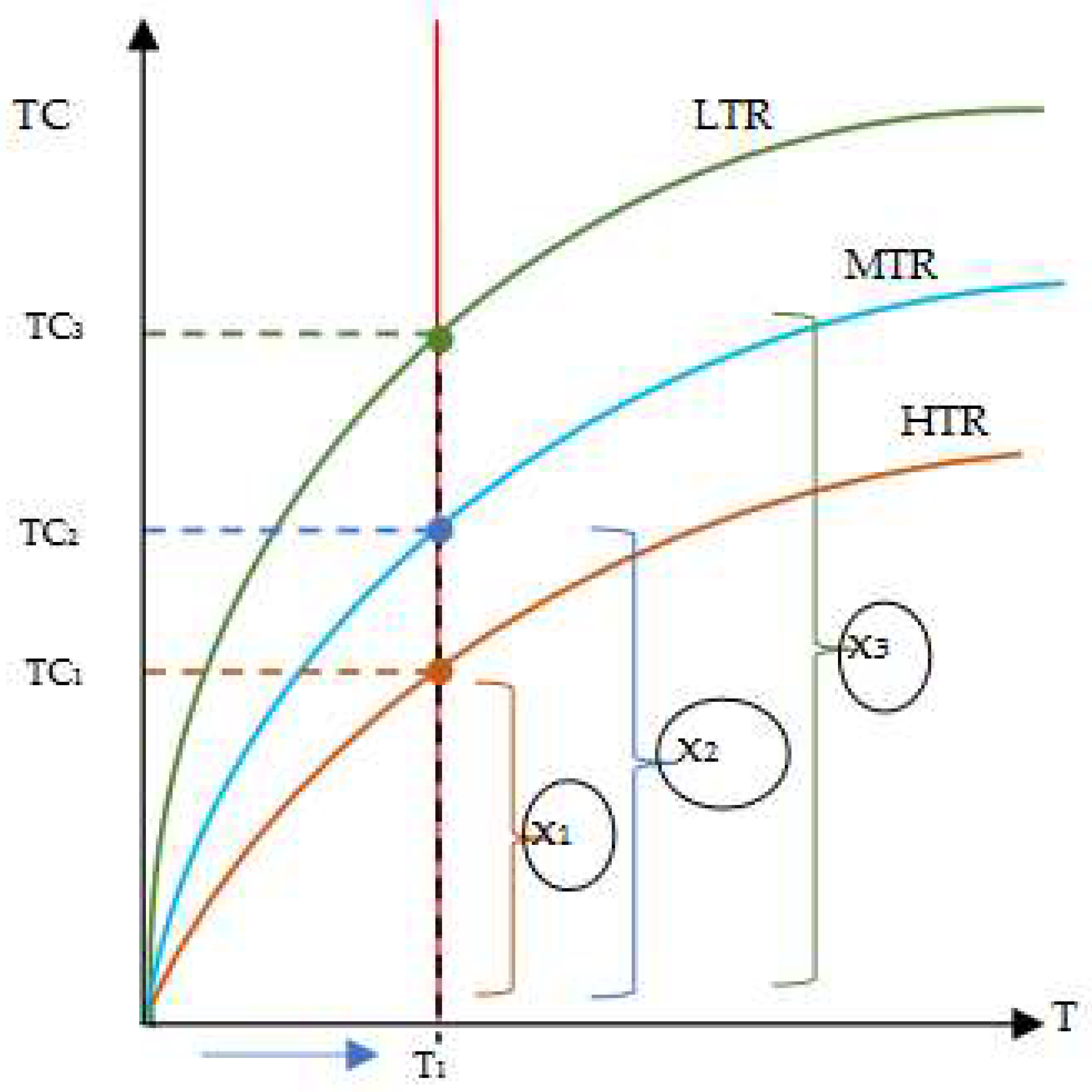

The graph in Figure 6 provides a further explanation regarding the nature of Figure 6 regarding how levels of tax risk would influence the increase in TC as either T or P increases. The chart below shows a 2-dimensional graph that would show how the level of tax risk affects the increase in tax compliance when T increases while P was maintained at a certain value.

When the T value increases to a certain value (e.g., T1 (see Figure 5)), different levels of tax risk will affect the increase in TC differently. Low Tax Risk (LTR) will result in the highest growth in TC compared to Moderate Tax Risk (MTR) and High Tax Risk (HTR). Looking at the increases of the TC between the three curves, namely x1, x2, and x3, it can be understood that x1 < x2 < x3; therefore, the value of the TC increases is lowest at HTR and highest at LTR. This explanation would be similar when we look at the situation when P increases but T was maintained at a certain value.

A simple explanation to conclude this perspective is that a company’s perspective on its TC is much “easier” to increase if its surrounding provides an inference that the tax risk is low. The lower the level of tax risk is on its surroundings, the “easier” it is for a company to comply, as demonstrated by the higher TC values.

In this case, tax risks will be increasingly difficult for taxpayers to comply with. However, it is still to be understood that it does not imply that a high level of tax risk would infer a condition in which taxpayers will ultimately not want to comply; a high level of tax risk would only imply that it would be very difficult for taxpayers to increase their compliance as the quality of trust and power increases because the hindrance to compliance is high. Tax risk will affect the level of tax compliance regardless of the existing quality of trust and power. Tax risk does not guarantee that taxpayers will ultimately comply or not comply with paying taxes at all. Nevertheless, tax risk will help to facilitate or hinder corporate taxpayers in complying; especially in companies that have a high level of complexity with ambiguous and uncertain tax rules.

The four-dimensional formula generated from this study could be specified to any Likert scale, such as maximum values for the Likert scale of 4, 5, or 7. Furthermore, this formulation already meets the theoretical basis of tax compliance. It also meets the original thought proposed by Kirchler et al. (2008) when making the SSF.

Replacing values in R would then add a deeper and more mathematically proven understanding of the tax risk variable as a dimension that effects tax compliance—it does facilitate in telling the differences in compliance between corporate taxpayers, but ultimately does not change the shape and the tendency of its changes in the tax compliance graph. This study provides a basis for the interaction between the variables in a mathematical approach.

4. The Effect of the TPR Model on Tax Compliance on Tax Policy Considerations

The dimensions of power, trust, and tax risk in the framework show the important role of corporate taxpayers and tax authorities in increasing compliance. Tax risk can prevent companies from complying, both as tax risk originating from the company itself (controllable risk) and tax risk arising from external (uncontrollable risk). Corporate taxpayers cannot control power and trust, but both parties can manage tax risk at an acceptable level by increasing tax compliance. If both parties can adequately address the tax risk, then there will be “no tax surprises.” Tax risk that is not appropriately managed can increase and create actual losses for companies and tax authorities’ objectives. Corporate taxpayers must identify tax risk and assess the key tax risk faced by the company correctly and appropriately. Then, they must manage tax risk to an acceptable level. Documented and tested internal controls are needed to reduce existing risks. In addition, a tax control framework is necessary to face this issue and result in minimum tax risk (acceptable tax risk). Companies must also ensure that the resources that will be responsible for managing tax risk have the skills and abilities to do so. The role of corporate tax leaders in managing tax risk is also crucial in determining the level of acceptable risk. Leaders classified as risk averse tend to be conservative in making tax decisions. In contrast, corporate tax leaders who are risk takers tend to be aggressive in managing the level of corporate tax risk, which affects the level of corporate tax compliance. On the other hand, companies that do not manage tax risk well can encounter surprises or worse. Therefore, Tax Risk Management needs to be a priority for the company.

Companies must manage tax risk to an acceptable level to achieve company goals and not harm shareholders through potential disputes or reputational risk. From the perspective of tax administration, risk is considered an event that impacts the objectives of tax administration. Risk-based regulation focuses on the risk, not the law (Black & Baldwin, 2010; OECD, 2010). In conditions of high tax risk caused by regulations and policies of the tax authorities, the mere emphasis on power becomes less relevant. Bronzewsk (2016) stated that to improve tax compliance, and tax authorities should not leave taxpayers to fend for themselves in the tax forest. Reducing the level of risk originating from tax regulations is carried out by providing services (making it easy or assisting in complying) and certainty through cooperative compliance programs and technology. Tax authorities should assist corporate taxpayers with a record of compliant taxpayers or in trying to comply in lowering the level of tax risk to make it easier for companies to fulfill their tax obligations. Power through audits and fines will burden taxpayers and create a cost of compliance on both sides. Cooperative compliance will ultimately increase trust and decrease risk, while trust increases will improve tax compliance and benefit both parties.

5. Conclusions

This study has arguably found a way to include the tax risk variable in the SSF and has shown mathematically and visually how that inclusion affects the relation between the change in the values of TC, T, P, and R. Before the final formulation of our study, the determinants of tax compliance in corporate taxpayers consist of dimensions of power and trust. Inducing tax risk on the determinants could help tax authorities to better understand tax-paying behaviors from taxpayers, giving better insights to adjust tax rulings through policy.

This study found that tax risk produces significant changes and effects on the whole tax compliance issue in which the level of tax risk affects the effort and tendency of a corporate taxpayer to comply. Low levels of tax risk will make it easier for corporate taxpayers to comply when the quality of trust and power increases, while a higher level of tax risk will make it harder for corporate taxpayers to comply when the quality of trust and power increases. However, it is to be understood well that low levels of tax risk do not eventually guarantee that the company will comply; it does however make it easier for the company to comply. It is also to be understood well that tax risk will affect the level of tax compliance, regardless of the existing quality of trust and power. Some types of companies arguably will not need to understand how the tax risk will affect other variables; tax risk would still ease or hinder the increase in compliance with tax paying, even in and especially on companies with a high level of tax-paying complexity and ambiguous tax quantity rulings.

Another conclusion should be accounted for in our formulation processes. The formulation process of our modeling only limits itself with certain accounted simplifications and inspections that would lead to the final formulation. Some of the most prominent of these simplifications and inspections are the fact that we determined that the changes in TC when P is changed with a certain effect and magnitude will be the same when T is changed on the same effect and magnitude; in addition, we directly choose to define our model using a function revolving around numerical powers. It is to be believed that other kinds of models revolving around other mathematical notions could still fit all the requirements; the choice to base the formulation revolving around numerical powers is purely by certain belief that the model would work well in this case. As for the simplification, future research is encouraged to find a way to discover a formulation that would also fit different effects for the change in trust and power, and also how these correspond to each other.

If the final formulation is regarded well, future research can use this model as the basis for fitting the model for approximating the h(R) function using the provided data. However, it is to be understood that some special requirements for h(R) would still need to be fulfilled, which must obey the concept of “diminishing returns” as embraced by Kircler et al.’s SSF and also the theoretical belief that higher tax risk would provide higher hindrance for the increase in the quality of tax compliance. As with the final formulation given in this study, the value of h(R) should not be less than 2; otherwise, the graph’s curve will turn concave and violate the concept of “diminishing return”, which should be embraced. In addition, h(R) should be lower as R gets higher. It is to be understood that the special requirements for h(R) will be different with different formulations; further studies are encouraged to find themselves the requirements that would fit with h(R) or any representation of R in their final formulation. This study, however, did not include any fitting using empirical data. We would expect future research to test or fit this model empirically.

From these findings, it can be inferred that it is in high importance for corporate taxpayers to manage corporate tax risk and build an adequate tax control framework and technology. It is also important for tax authorities to analyze taxpayer risk and then provide a policy approach based on the risk analysis so that they can treat taxpayers according to risk assessment. Furthermore, it is crucial for tax authorities to help corporate taxpayers in reducing tax risk arising from policy or legal uncertainty in order to avoid unnecessary risks that could arise from the company. All in all, everything considered, the accessibility and tendency in helping to reduce tax risk by tax authorities, when done well, could eventually help taxpayers to reach a higher tax paying compliance nature.

Author Contributions

For this research Conceptualization, S.A., H.R. and I.I.; methodology, S.A.; validation, S.A., H.R. and I.I.; Analysis, S.A., H.R. and I.; writing—original draft preparation S.A.; Review, H.R. and I.I.; visualization, S.A.; supervision, H.R. and I.I.; project administration, S.A.; funding acquisition, S.A. All authors have read and agreed to the published version of the manuscript.

Funding

This research was funded by Lembaga Pengelola Dana Pendidikan (Indonesia Endowment Fund for Education). Thank you to LPDI RI for funding my dissertation and research project.

Acknowledgments

We want to thank the editor and the anonymous reviewer for their helpful and valuable comments and recommendations. The authors would like to thank H.M. Susanta for the mathematical economic discussion, the Department of Fiscal Administration Faculty of Administrative Sciences and Vocational Education Program, Universitas Indonesia for supporting this study.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Lozza, E.; Castiglioni, C. Tax climate in the national press: A new tool in tax behaviour research. J. Soc. Political Psychol. 2018, 6, 401–419. [Google Scholar] [CrossRef] [Green Version]

- Rashid, S.F.A.; Ramli, R.; Palil, M.R.; Amir, A.M. Improving Voluntary Compliance Using Power of Tax Administrators: The Mediating Role of Trust. Asian J. Bus. Account. 2021, 14, 101–136. [Google Scholar]

- Allingham, M.G.; Sandmo, A.; Jackson, B.R.; Milliron, V.C.; Small, O.; Brown, L. Tax Compliance Research: Findings, Problems, and Prospects. J. Public Econ. 1986, 5, 125–165. [Google Scholar]

- Allingham, M.G.; Sandmo, A. Income tax evasion: A theoretical analysis. J. Public Econ. 1972, 1, 323–338. [Google Scholar] [CrossRef] [Green Version]

- Eisenhauer, J.G. Ethical preferences, risk aversion, and taxpayer behavior. J. Socio-Econ. 2008, 37, 45–63. [Google Scholar] [CrossRef]

- Franzoni, L.A. Tax Evasion and Tax Compliance. SSRN Electron. J. 1998. [Google Scholar] [CrossRef] [Green Version]

- James, A.; Alley, S. Tax Compliance, Self-Assessment and Tax Administration. 2002. Available online: https://ore.exeter.ac.uk/repository/bitstream/handle/10036/47458/james2.pdf (accessed on 8 July 2022).

- Kirchler, E.; Maciejovsky, B.; Schneider, F. Everyday representations of tax avoidance, tax evasion, and tax flight: Do legal differences matter? J. Econ. Psychol. 2003, 24, 535–553. [Google Scholar] [CrossRef] [Green Version]

- Walpole, M. Ethics and Integrity in Tax Administration; UNSW Law Research Paper 2009-33. 2009. Available online: https://ssrn.com/abstract=1474100 (accessed on 8 July 2022).

- Artemenko, D.A.; Aguzarova, L.A.; Aguzarova, F.S.; Porollo, E.V. Causes of tax risks and ways to reduce them. Eur. Res. Stud. J. 2017, 20, 453–459. [Google Scholar] [CrossRef] [Green Version]

- Cozmei, C.; Şerban, E.C. Risk Management Triggers: From the Tax Risk Pitfalls to Organizational Risk. Procedia Econ. Financ. 2014, 15, 1594–1602. [Google Scholar] [CrossRef] [Green Version]

- Prinz, A.; Muehlbacher, S.; Kirchler, E. The slippery slope framework on tax compliance: An attempt to formalization. J. Econ. Psychol. 2014, 40, 20–34. [Google Scholar] [CrossRef]

- Kirchler, E.; Hoelzl, E.; Wahl, I. Enforced versus voluntary tax compliance: The “slippery slope” framework. J. Econ. Psychol. 2008, 29, 210–225. [Google Scholar] [CrossRef]

- Muehlbacher, S.; Kirchler, E. Tax compliance by trust and power of authorities. Int. Econ. J. 2010, 24, 607–610. [Google Scholar] [CrossRef]

- Muehlbacher, S.; Kirchler, E.; Schwarzenberger, H. Voluntary versus enforced tax compliance: Empirical evidence for the “slippery slope” framework. Eur. J. Law Econ. 2011, 32, 89–97. [Google Scholar] [CrossRef]

- Alon, A.; Hageman, A.M. The Impact of Corruption on Firm Tax Compliance in Transition Economies: Whom Do You Trust? J. Bus. Ethics 2013, 116, 479–494. [Google Scholar] [CrossRef]

- Andreoni, J.; Erard, B.; Feinstein, J. Tax Compliance. J. Econ. Lit. 1998, 36, 818–860. [Google Scholar]

- Bayer, R.; Cowell, F. Tax compliance and firms’ strategic interdependence. J. Public Econ. 2009, 93, 1131–1143. [Google Scholar] [CrossRef]

- Torgler, B. Beyond punishment: A tax compliance experiment with taxpayers in Costa Rica. Rev. De Análisis Económico 2003, 18, 27–56. [Google Scholar]

- Kirchler, E.; Hölzl, E.; Wahl, I. Compliance to authorities: Importing ideas from tax psychology to organizational psychology. In John E. Michaels/Leonardo F. Piraro (Hg.): Small Business. Innovation, Problems and Strategy; Nova Science Publishers: New York, NY, USA, 2009; pp. 7–16. [Google Scholar]

- Nguyen, T.T.D.; Pham, T.M.L.; Le, T.T.; Truong, T.H.L.; Tran, M.D. Determinants influencing tax compliance: The case of Vietnam. J. Asian Financ. Econ. Bus. 2020, 7, 65–73. [Google Scholar] [CrossRef]

- Akhand, Z.; Hubbard, M. Coercion, Persuasion, and Tax Compliance: The Case of Large Corporate Taxpayers. Can. Tax J. 2016, 64, 31–63. [Google Scholar]

- Siglé, M.; Goslinga, S.; Speklé, R.; van der Hel, L.; Veldhuizen, R. Corporate tax compliance: Is a change towards trust-based tax strategies justified? J. Int. Account. Audit. Tax. 2018, 32, 3–16. [Google Scholar] [CrossRef]

- Gobena, L.B.; Van Dijke, M. Fear and caring: Procedural justice, trust, and collective identification as antecedents of voluntary tax compliance. J. Econ. Psychol. 2017, 62, 1–16. [Google Scholar] [CrossRef] [Green Version]

- Akhand, Z. The influence of the corporate sector on the effectiveness of tax compliance instruments. Adv. Tax. 2018, 25, 119–146. [Google Scholar] [CrossRef]

- Lisi, G. The interaction between trust and power: Effects on tax compliance and macroeconomic implications. J. Behav. Exp. Econ. 2014, 53, 24–33. [Google Scholar] [CrossRef]

- Mas’Ud, A.; Manaf, N.A.A.; Saad, N. Trust and power as predictors to tax compliance: Global evidence. Econ. Sociol. 2019, 12, 192–204. [Google Scholar] [CrossRef]

- Mendoza, J.P.; Wielhouwer, J.L. Only the Carrot, Not the Stick: Incorporating Trust into the Enforcement of Regulation. PLoS ONE 2015, 10, e0117212. [Google Scholar] [CrossRef]

- Randlane, K. Tax Compliance as a System: Mapping the Field. Int. J. Public Adm. 2016, 39, 515–525. [Google Scholar] [CrossRef]

- Stam, E.; Verbeeten, F. Tax compliance over the firm life course. Int. Small Bus. J. Res. Entrep. 2015, 35, 99–115. [Google Scholar] [CrossRef]

- Sapiei, N.S.; Kasipilai, J.; Eze, U.C. Determinants of tax compliance behaviour of corporate taxpayers in Malaysia. EJournal Tax Res. 2014, 12, 383–409. [Google Scholar]

- Kastlunger, B.; Lozza, E.; Kirchler, E.; Schabmann, A. Powerful authorities and trusting citizens: The Slippery Slope Framework and tax compliance in Italy. J. Econ. Psychol. 2013, 34, 36–45. [Google Scholar] [CrossRef]

- Lozza, E.; Kastlunger, B.; Tagliabue, S.; Kirchler, E. The relationship between political ideology and attitudes toward tax compliance: The case of Italian taxpayers. J. Soc. Political Psychol. 2013, 1, 51–73. [Google Scholar] [CrossRef]

- Lisi, G. Tax morale, tax compliance and the optimal tax policy. Econ. Anal. Policy 2015, 45, 27–32. [Google Scholar] [CrossRef] [Green Version]

- Kaplanoglou, G.; Rapanos, V.T.; Daskalakis, N. Tax compliance behaviour during the crisis: The case of Greek SMEs. Eur. J. Law Econ. 2016, 42, 405–444. [Google Scholar] [CrossRef]

- Gangl, K.; Hartl, B.; Hofmann, E.; Kirchler, E. The relationship between Austrian tax auditors and self-employed taxpayers: Evidence from a qualitative study. Front. Psychol. 2019, 10, 1034. [Google Scholar] [CrossRef] [Green Version]

- Small, O.; Brown, L. Taxpayer Service Provision and Tax Compliance: Evidence for Large Taxpayers in Jamaica. Public Financ. Rev. 2020, 48, 250–277. [Google Scholar] [CrossRef]

- Nikulin, D. Tax evasion, tax morale, and trade regulations: Company-level evidence from Poland. Entrep. Bus. Econ. Rev. 2020, 8, 111–125. [Google Scholar] [CrossRef]

- Kamasa, K.; Adu, G.; Oteng-Abayie, E.F. Business environment and firms’ decisions to evade taxes: Evidence from Ghana. Afr. J. Bus. Econ. Res. 2019, 14, 135–155. [Google Scholar] [CrossRef]

- Umar, M.A.; Derashid, C.; Ibrahim, I.; Bidin, Z. Public governance quality and tax compliance behavior in developing countries: The mediating role of socioeconomic conditions. Int. J. Soc. Econ. 2019, 46, 338–351. [Google Scholar] [CrossRef]

- Tennant, S.N.; Tracey, M.R. Corporate profitability and effective tax rate: The enforcement effect of large taxpayer units. Account. Bus. Res. 2018, 49, 342–361. [Google Scholar] [CrossRef]

- Almunia, M.; Lopez-Rodriguez, D. Under the radar: The effects of monitoring firms on tax compliance. Am. Econ. J. Econ. Policy 2018, 10, 1–38. [Google Scholar] [CrossRef] [Green Version]

- Bachas, P.; Fattal Jaef, R.N.; Jensen, A. Size-dependent tax enforcement and compliance: Global evidence and aggregate implications. J. Dev. Econ. 2019, 140, 203–222. [Google Scholar] [CrossRef] [Green Version]

- Ya’u, A.; Saad, N.; Mas’ud, A. Effects of economic deterrence variables and royalty rates on petroleum profit tax compliance in Nigeria: An empirical analysis. Int. J. Energy Sect. Manag. 2020, 14, 1275–1296. [Google Scholar] [CrossRef]

- Lee, K. Optimism, pessimism, audit uncertainty, and tax compliance. BE J. Theor. Econ. 2018, 18, 1–13. [Google Scholar] [CrossRef] [Green Version]

- Prihandini, W. Corporate Tax Compliance Based on an Effective Tax Rate and Earnings Management. Int. J. Econ. Perspect. 2017, 11, 312–322. Available online: http://sdl.edu.sa/middleware/Default.aspx?USESDL=true&PublisherID=AllPublishers&BookURL=https://sdl.idm.oclc.org/login?url=http://search.ebscohost.com/login.aspx?direct=true&db=bsu&AN=135858995&site=eds-live (accessed on 12 July 2022).

- Nurwanah, A.; Sutrisno, T.; Rosidi, R.; Roekhudin, R. Determinants of tax compliance: Theory of planned behavior and stakeholder theory perspective. Probl. Perspect. Manag. 2018, 16, 395–407. [Google Scholar] [CrossRef]

- Kirchler, E.; Kogler, C.; Muehlbacher, S. Cooperative Tax Compliance: From Deterrence to Deference. Curr. Dir. Psychol. Sci. 2014, 23, 87–92. [Google Scholar] [CrossRef]

- Larsen, L.B.; Oats, L. Taxing Large Businesses: Cooperative Compliance in Action. Intereconomics 2019, 54, 165–170. [Google Scholar] [CrossRef] [Green Version]

- OECD. Co-Operative Compliance: A Framework; OECD Publishing: Paris, France, 2013. [Google Scholar] [CrossRef]

- Putra, E. A Study of the Indonesia’s Income Tax Reform and the Development of Income Tax Revenues. J. East Asian Stud. 2014, 12, 55–68. [Google Scholar]

- Schön, W. Tax and Corporate Governance: A Legal Approach. Tax Corp. Gov. 2008, 3, 31–61. [Google Scholar] [CrossRef]

- Lipsey, R.G. Reflections on the general theory of second best at its golden jubilee. Int. Tax Public Financ. 2007, 14, 349–364. [Google Scholar] [CrossRef]

- Krelove, R. General equilibrium incidence of taxes. In Tax Policy Handbook; 1995; pp. 39–45. Available online: https://www.elibrary.imf.org/downloadpdf/book/9781557754905/9781557754905.pdf#page=53 (accessed on 10 July 2022).

- Gangl, K.; Hofmann, E.; Kirchler, E. Tax authorities’ interaction with taxpayers: A conception of compliance in social dilemmas by power and trust. New Ideas Psychol. 2015, 37, 13–23. [Google Scholar] [CrossRef] [Green Version]

- Becker, G.S. Crime and Punishment: An Economic Approach. J. Political Econ. 1968, 76, 169–217. [Google Scholar] [CrossRef] [Green Version]

- Kahneman, D.; Tversky, A. Kahneman, D.; Tversky, A. Prospect Theory: An Analysis of Decision under Risk. Econometrica 1979, 47, 263–291. [Google Scholar] [CrossRef] [Green Version]

- Lavermicocca, C. Tax risk management practices and their impact on tax compliance behaviour—The views of tax executives from large Australian companies. EJournal Tax Res. 2011, 9, 89–115. [Google Scholar]

- Newman, W.; Nokhu, M. Evaluating the impact of tax knowledge on tax compliance among small medium enterprises in a developing country. Acad. Account. Financ. Stud. J. 2018, 22. Available online: https://www.abacademies.org/articles/Evaluating-the-Impact-of-Tax-Knowledge-on-Tax-Compliance-Among-Small-Medium-Enterprises-1528-2635-22-6-302.pdf (accessed on 10 July 2022).

- Pijnenburg, M.G.F.; Kowalczyk, W.J.; Dijk, H.-V.; van der Hel-van, D.E. A roadmap for analytics in taxpayer supervision. Electron. J. E-Gov. 2017, 15, 19–32. [Google Scholar]

- van der Hel, L.; Sigle, M. Managing compliance risks of large businesses: A review of the underlying assumptions of co-operative compliance strategies. EJournal Tax Res. 2015, 13, 760–783. [Google Scholar]

- Ftouhi, K.; Ghardallou, W. International tax planning techniques: A review of the literature. J. Appl. Accoun. Res. 2020, 21, 329–343. [Google Scholar] [CrossRef]

- Lin, X.; Liu, M.; So, S.; Yuen, D. Corporate social responsibility, firm performance and tax risk. Manag. Audit. J. 2019, 34, 1101–1130. [Google Scholar] [CrossRef]

- Neuman, S.S.; Omer, T.C.; Schmidt, A.P. Assessing Tax Risk: Practitioner Perspectives. Contemp. Account. Res. 2020, 37, 1788–1827. [Google Scholar] [CrossRef]

- Chen, W. Too far east is west: Tax risk, tax reform and investment timing. Int. J. Manag. Financ. 2021, 17, 303–326. [Google Scholar] [CrossRef]

- COSO. Enterprise Risk Management; Integrating with Strategy and Performance; COSO, 2017; Available online: https://www.coso.org/Shared%20Documents/2017-COSO-ERM-Integrating-with-Strategy-and-Performance-Executive-Summary.pdf (accessed on 10 July 2022).

- Drake, K.D.; Lusch, S.J.; Stekelberg, J. Does Tax Risk Affect Investor Valuation of Tax Avoidance? J. Account. Audit. Financ. 2017, 34, 151–176. [Google Scholar] [CrossRef]

- Guenther, D.A.; Matsunaga, S.R.; Williams, B.M. Is Tax Avoidance Related to Firm Risk? Account. Rev. 2017, 92, 115–136. [Google Scholar] [CrossRef] [Green Version]

- Hamilton, R.; Stekelberg, J. The Effect of High-Quality Information Technology on Corporate Tax Avoidance and Tax Risk. J. Inf. Syst. 2017, 31, 83–106. [Google Scholar] [CrossRef]

- Dyreng, S.; Lewellen, C.; Lindsey, B.P. Tax Planning Gone Awry: Do Tax-Motivated Firms Experience Worse Tax Outcomes from Losses Compared to Other Firms? 2018. Available online: https://ssrn.com/abstract=3291705 (accessed on 10 July 2022).

- Taylor, G.; Richardson, G. Incentives for corporate tax planning and reporting: Empirical evidence from Australia. J. Contemp. Account. Econ. 2014, 10, 1–15. [Google Scholar] [CrossRef] [Green Version]

- Chen, W. Tax risks control and sustainable development: Evidence from China. Meditari Account. Res. 2021, 29, 1381–1400. [Google Scholar] [CrossRef]

- Gallemore, J.; Labro, E. The importance of the internal information environment for tax avoidance. J. Account. Econ. 2015, 60, 149–167. [Google Scholar] [CrossRef]

- Abernathy, J.L.; Finley, A.R.; Rapley, E.T.; Stekelberg, J. External Auditor Responses to Tax Risk. J. Account. Audit. Finance 2019. [Google Scholar] [CrossRef]

- Wilde, J.H.; Wilson, R.J. Perspectives on Corporate Tax Planning: Observations from the Past Decade. J. Am. Tax. Assoc. 2018, 40, 63–81. [Google Scholar] [CrossRef]

- Torgler, B. Tax Compliance and Data: What Is Available and What Is Needed. Aust. Econ. Rev. 2016, 49, 352–364. [Google Scholar] [CrossRef] [Green Version]

- Slemrod, J.; Weber, C. Evidence of the invisible: Toward a credibility revolution in the empirical analysis of tax evasion and the informal economy. Int. Tax Public Financ. 2012, 19, 25–53. [Google Scholar] [CrossRef]

- Carroll, J.S. Compliance with the law: A decision-making approach to taxpaying. Law Hum. Behav. 1987, 11, 319–335. [Google Scholar] [CrossRef]

- Srinivasan, T.N. Tax evasion: A model. J. Public Econ. 1973, 2, 339–346. [Google Scholar] [CrossRef]

- Gahramanov, E. The Theoretical Analysis of Income Tax Evasion Revisited. Econ. Issues 2009, 14, 35–41. [Google Scholar]

- Musimenta, D.; Naigaga, S.; Bananuka, J.; Najjuma, M.S. Tax compliance of financial services firms: A developing economy perspective. J. Money Laund. Control 2019, 22, 14–31. [Google Scholar] [CrossRef]

- Wahl, I.; Kastlunger, B.; Kirchler, E. Trust in authorities and power to enforce tax compliance: An empirical analysis of the “slippery slope framework”. Law Policy 2010, 32, 383–406. [Google Scholar] [CrossRef]

- Kahneman, D.; Slovic, S.P.; Slovic, P.; Tversky, A. Judgment under Uncertainty: Heuristics and Biases; Cambridge University Press: Cambridge, UK, 1982. [Google Scholar]

- Dhami, S. The Foundations of Behavioral Economic Analysis; Oxford University Press: Oxford, UK, 2016. [Google Scholar]

Figure 1.

Source of Corporate Tax Risk.

Figure 2.

Tax Risk Low.

Figure 3.

Tax Risk Moderate.

Figure 4.

Tax Risk High.

Figure 5.

Trust, Power, and Tax Risk (TPR) Model.

Figure 6.

Graph of Relationship of T, R, and TC.

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Aulia, S.; Rosdiana, H.; Inayati, I. Trust, Power, and Tax Risk into the “Slippery Slope”: A Corporate Tax Compliance Model. Sustainability 2022, 14, 14670. https://doi.org/10.3390/su142214670

AMA Style

Aulia S, Rosdiana H, Inayati I. Trust, Power, and Tax Risk into the “Slippery Slope”: A Corporate Tax Compliance Model. Sustainability. 2022; 14(22):14670. https://doi.org/10.3390/su142214670

Chicago/Turabian StyleAulia, Sandra, Haula Rosdiana, and Inayati Inayati. 2022. "Trust, Power, and Tax Risk into the “Slippery Slope”: A Corporate Tax Compliance Model" Sustainability 14, no. 22: 14670. https://doi.org/10.3390/su142214670

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.