1. Introduction

Cloud enterprise resource planning (ERP) is a critical component of a lengthy list of services offered in the cloud that also includes internet data storage for individuals, business services (for example, modules accessible via the cloud), virtual machines for the cloud, and other services built on the cloud computing (CC) structure [

1,

2]. A cloud-based ERP solution allows a company to centralize all of its core business functions in order to increase productivity and preserve a competitive advantage. Cloud ERP is critical for information interchange, product development, and knowledge management between businesses and their clients [

3,

4]. Significant cost savings are one of the primary benefits, particularly for small and medium-sized organizations (SMEs), because cloud vendors assume responsibility for hardware and infrastructure, as well as application maintenance, management, integration, and development [

5,

6,

7]. Additionally, the cloud solution eliminates the need for SMEs to maintain an IT team, and it eliminates the need for upfront costs because it is based on a pay-as-you-go model [

8].

Due to the fact that the majority of cloud ERP clients are small firms, SMEs adopt cloud ERP primarily for its adaptability, ease of control, and, most importantly, its low license, maintenance, and overall investment costs [

9]. Despite the benefits of cloud ERP, its limitations include security, privacy, a lack of trust, a lack of industry-specific standards, and data loss [

10,

11]. Nonetheless, ERP has been widely deployed by organizations of various sizes in a variety of sectors and nations in order to achieve competitive advantages and thus improved performance [

12]. Without successfully integrating a cloud ERP system, the anticipated benefits of increased efficiency and competitive advantage will not materialize [

13,

14]. However, research indicates that using cloud ERP to harness its benefits might be a double-edged sword for firms. For instance, some studies have demonstrated that cloud ERP can have a significant impact on firm performance [

15,

16,

17,

18], whereas others have concluded that cloud ERP has a relatively insignificant impact on firm performance [

8,

19,

20]. However, many of these studies focused exclusively on the direct relationship between cloud ERP implementation and performance, and Gupta et al. [

8] suggested that the relationship between CC services and performance is not simply linear. The aforementioned contradictory findings underscore the importance of considering other reasons for the impact of cloud ERP implementation on firm performance. On the other hand, top management support (TMS) is widely recognized as the most critical success factor in all organizational processes and activities [

21]. From the perspective of cloud ERP, the literature demonstrates that TMS is a significant predictor of cloud ERP implementation [

22,

23,

24].

Additionally, TMS is critical, not only during the implementation phase, but also during the post-implementation (business value realization) phase, when top management is involved in defining IT initiatives, formulating goals, selecting budgets, and allocating human, material, and technical resources [

25]. However, there are few studies examining the role of TMS in the post-implementation period of cloud ERP [

26,

27], and their findings are inconclusive. TMS was proven to be insignificant as a direct predictor of firm performance by Ooi et al. [

26]. One could criticize this study for excluding the CC implementation effect from its model. That is, it considered TMS as a direct predictor of cloud ERP implementation success, a notion dubbed deterministic by Dong [

28]. On the other hand, Shee et al. [

27] explored and discovered the moderating influence of TMS on the link between cloud-enabled supply chain integration and supply chain performance. This study is supply chain centered and does not focus on either the internal or external operations of the firm.

Due to the crucial impact of top leadership throughout the life of an IT project [

29], prior research has demonstrated a limited understanding of the influence of TMS on cloud ERP post-implementation (e.g., [

26,

27]). Thus, this study aims to shed light on the relevance of TMS in the post-implementation phase of cloud ERP by simultaneously examining its mediating and moderating effects in order to gain a better understanding of the cloud ERP implementation–performance relationship that has been beset by inconsistencies. In general, this study is in line with the work of [

30,

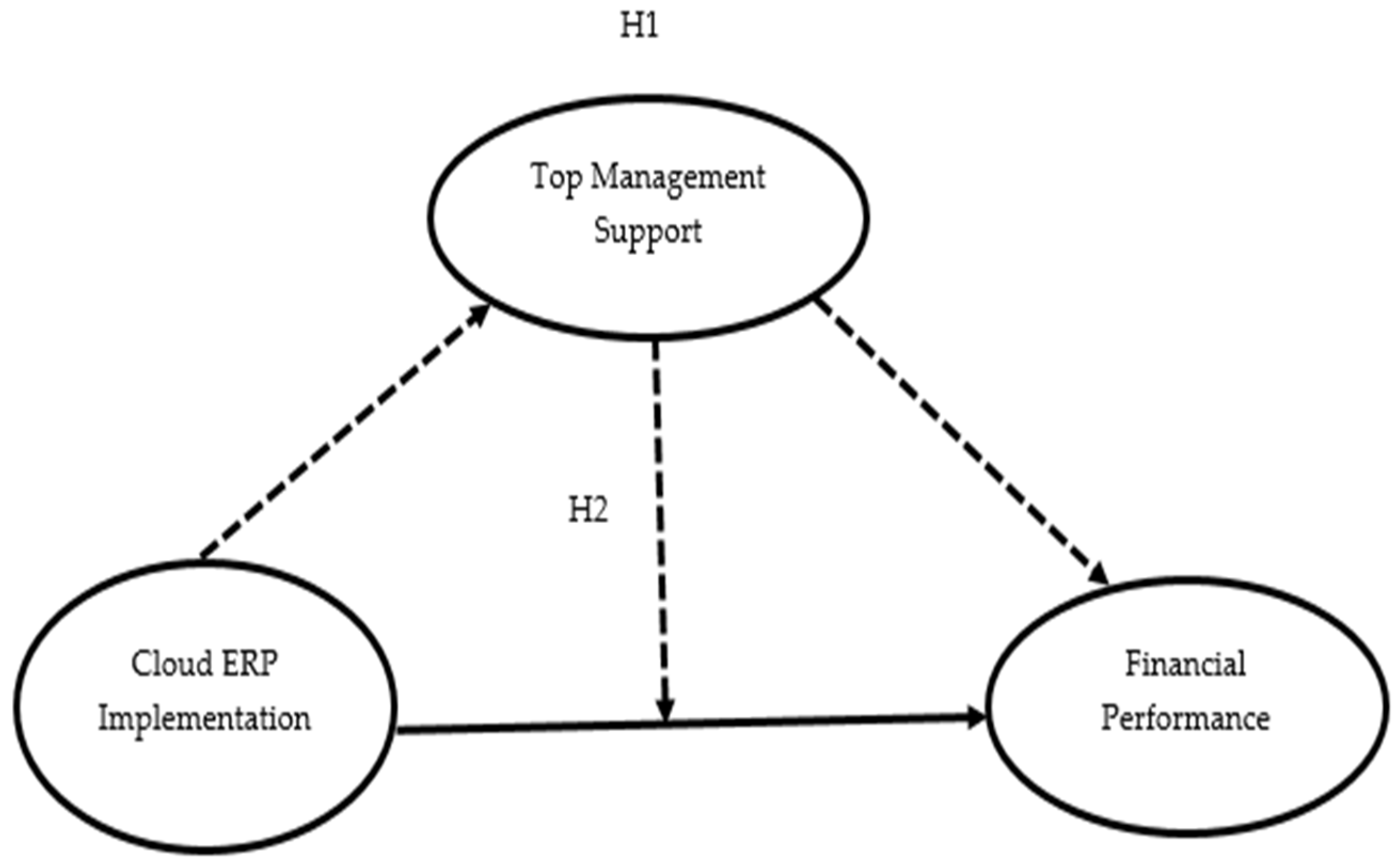

31] on the necessity of investigating mediating and moderating influences to fully grasp the IT innovation and financial performance relationship. The questions this study aims to answer are: Does cloud ERP implementation influence the financial performance of SMEs through TMS? Does TMS help to achieve a stronger relationship between cloud ERP implementation and financial performance of SMEs?

The remainder of the article is structured as follows: a literature review is presented in the next section.

Section 3 reveals the materials and methods used, and

Section 4 summarizes the results.

Section 5 discusses the findings, and

Section 6 presents the conclusions.

5. Discussion

TMS has a direct effect on financial performance, as well as moderating and mediating effects on the cloud ERP implementation–financial performance relationship, according to the results of this research.

First, the findings reveal that TMS partially mediates the relationship between cloud ERP implementation and FP, supporting H1. Considering the total effect, SMEs with an extra unit of cloud ERP implementation are predicted to achieve a 0.446 (45%) unit higher financial performance than other enterprises. Nevertheless, when top management supports the cloud ERP post-implementation, such as by providing usage, training, resources, and incentives, SMEs with an extra unit of cloud ERP implementation are predicted to achieve a 0.257 (26%) unit greater FP, since TMS absorbs part of the effects of cloud ERP implementation on FP. This result typically indicates the significance of TMS as a mediator and confirms previous research conclusions [

54,

56] that TMS is critical in increasing technology integration into business for better overall firm performance. This finding further demonstrates that when TMS fosters a supportive environment for cloud ERP users in SMEs, operational tasks are performed more efficiently, and financial metrics, such as profit, return on investment, and gross earnings, are improved. In addition, because top management minimizes resistance to change by providing essential resources and training their personnel to become more skilled at using cloud ERP [

26], this, in turn, has a favorable impact on the firm’s performance. Top management also acts as a mechanism for enhancing firm performance through the use of cloud ERP by implementing new performance control systems (e.g., offering rewards/incentives) to boost user motivation and change performance targets (e.g., giving assistance, especially during a prolonged period of performance decline) [

58].

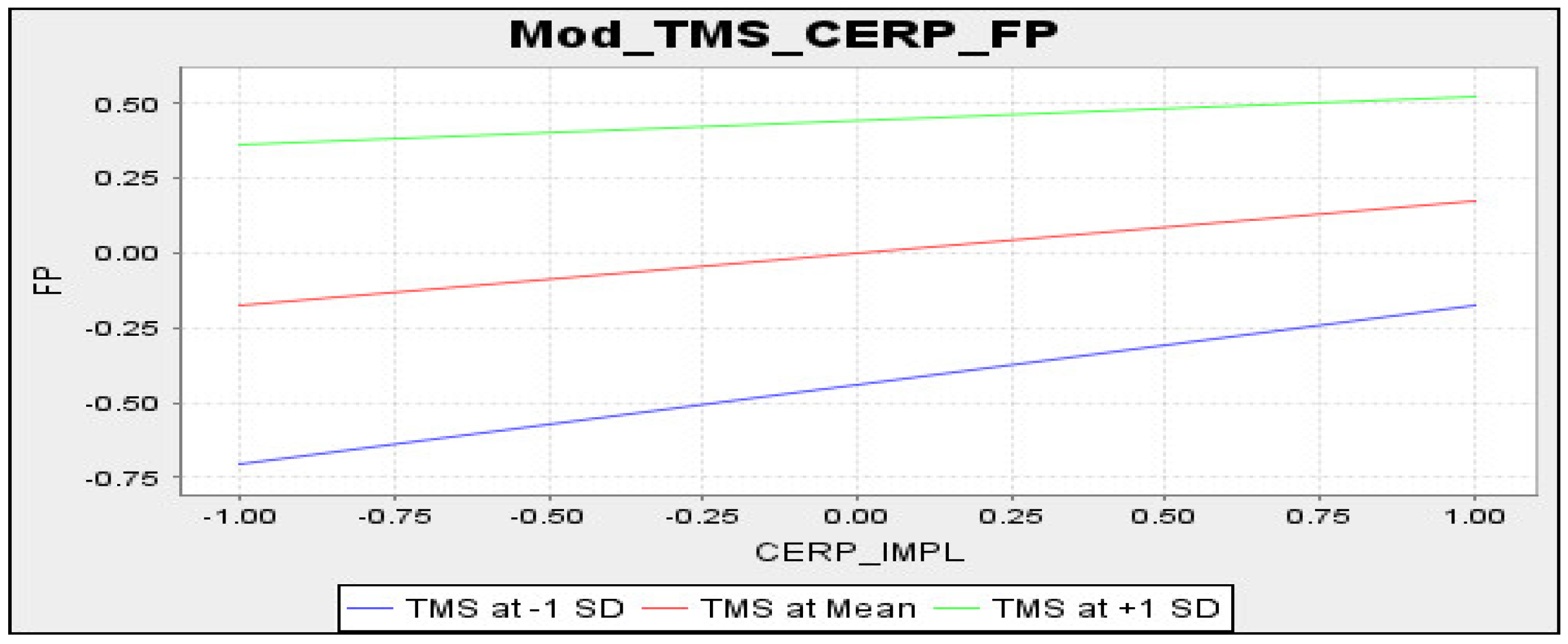

Second, it is found that SMEs with low TMS have a greater impact on the cloud ERP implementation–financial performance link than do enterprises with high TMS, which contradicts our hypothesis and rejects H2. Thus, SME’s with a low TMS are found to benefit more financially from implementing a cloud ERP system. According to scholars, top management should be fully involved in all phases of ERP implementation [

48], including the post-implementation period devoted to achieving economic benefits. However, the finding of the negative moderating effect of TMS in the cloud ERP implementation–FP relationship negates this proposition. On the other hand, our finding supports the proposition that although TMS is frequently advocated as intrinsically beneficial [

96], there is substantial evidence that excessive TMS can be dysfunctional and result in failure [

97]. Furthermore, this finding lends credence to the dynamic perspective of TMS, as advocated by Dong [

28]. The dynamic view of TMS explains that ERP implementation success requires that top management adjust its support level and content based on varying implementation conditions [

28]. In another word, during cloud ERP implementation, TMS is not always static, but dynamic, which means that top management support varies in response to ERP implementation project requirements [

48], and this dynamism will also affect firm performance. For example, Mähring [

96] pointed out that excessive use of TMS can have a negative influence on employee enthusiasm and absorption capacity, as well as interfere with the routine operations of project managers [

56]. Additionally, Somer and Nelson [

98] discovered that following the initial implementation period of ERP, project participants’ evaluations of the importance of TMS continue to decline, which when continued, will dampen firm performance.

6. Conclusions

The goal of this study is to examine whether TMS has a mediating or moderating influence on the relationship between cloud ERP implementation and financial performance. The study establishes that TMS partially mediates the relationship between cloud ERP implementation and financial performance, and that SMEs with a low TMS have a strong positive influence on the cloud ERP implementation–financial performance relationship. Thus, TMS mechanisms, such as resource provision, administrative aid, training, and reward systems, all contribute to the success of cloud ERP implementation. Additionally, an excessive amount of TMS is detrimental and results in failure in terms of negative financial performance. As a result, our study is able to demonstrate the value of TMS while also defining its boundaries in the cloud ERP post-implementation stage.

6.1. Theoretical Contributions

The contingent RBV theory was utilized to explain the impact of cloud ERP on the financial performance of SMEs, with TMS serving as a contextual influencing variable. Theoretically, the findings contribute to the ongoing discourse about how important TMS is in the post-implementation stage of IT implementation by examining the distinctive mediating–moderating effects of TMS on the cloud ERP implementation–financial performance link. For the first time, this study examines the mediating as well as the moderating effects of TMS post-implementation of cloud ERP to better comprehend the subject matter, supporting [

30,

31] viewpoints on the value of investigating mediating–moderating effects concurrently. Thus, our study establishes an indirect influence of TMS on the success (e.g., higher performance) of IT implementation, and provides evidence for the postulations regarding how TMS modifies the effects of CC implementation on various performance dimensions of firms [

27]. Specific to SMEs’ financial performance, our findings provide statistical support for the strong effects of low TMS and the partial mediation role of TMS in the cloud ERP implementation–financial performance relationship, which were previously unknown. Additionally, the study’s findings establish a new mediating–moderating model for enhancing the success of cloud ERP implementations in SMEs via TMS. This study is one of the first to shed light on the contradictory findings regarding cloud ERP implementation and performance, as well as the TMS role in the post-implementation stage, by assessing not only the TMS mediation effect, but also its moderating effect. In conclusion, because businesses must be capable of responding efficiently in the face of a continually changing business environment, the contingent RBV theory was employed to describe the conceptual model in this study. Because the study’s results corroborate the dynamic perspective of TMS [

28], this theory can be used to mitigate the static aspect of the RBV theory, as demonstrated by the findings of the study.

6.2. Practical Contributions

The following section discusses the findings’ managerial implications and practical significance. First, the findings highlight a critical necessity to ensure equilibrium of cloud ERP implementation with TMS in order to optimize the benefits of TMS and achieve a strong cloud ERP–financial performance relationship. Now, more than ever, business organizations, particularly SMEs, are seeking to boost their cost efficiency and overall performance. With the implementation of cloud ERP, a cost-effective method of synchronizing business operations and increasing labor efficiency [

99], the outcomes of this study demonstrate that TMS is a powerful mechanism for achieving improved financial performance. Therefore, SMEs managers, owners, and executives should first be aware of the general benefits of cloud ERP in order to be receptive towards the technology. After successful implementation, top managers should provide administrative assistance in the post-implementation stage of cloud ERP, encourage employees to use cloud ERP, provide adequate resources, train and retrain employees in effectively using the IT, and provide rewards/incentives to bolster the motivation of employees. Additionally, without proper assimilation, adopted IT is incapable of enhancing corporate operations, assisting in strategic decision making, and in ultimately improving firm performance [

100]. SMEs managers should provide a conducive learning environment for users to learn and also encourage employees with fast assimilation to share their knowledge with others to improve the efficiency of the technology, which will subsequently enhance the firm’s financial performance.

Furthermore, the finding that a high level of TMS negatively affects the cloud ERP implementation–financial performance relationship implies that excessive support from top management is a recipe for organizational failure. Therefore, top managers need to be dynamic in order to minimize the detriments of TMS to achieve a strong cloud ERP implementation–financial performance link. Top management should provide support as earlier explicated; however, it should adjust its support level and content based on unfolding conditions and users’ feedback or body language. There should be less meddling from top management during employees’ and other members’ usage of the cloud ERP, which could have a negative impact on the firm’s success. Users should be allowed to be free and creative in order to boost their confidence. Hence, top management needs to control the level of resources, incentives, administrative assistance, and training, and then change the management support it offers after the ERP go-live stage in order to ensure a positive firm performance.

6.3. Limitations and Future Research Directions

While the current study sheds light on an important aspect of cloud ERP implementation and the financial performance of SMEs, it has some shortcomings that can be addressed in future research. First, because we carried out the study in Malaysia, a place where the potential of cloud ERP has not yet been fully realized, our findings may represent both the perceived utility of this technology and the particular circumstances of the country. As a result, caution should be applied when extrapolating the findings to other geographical regions. Second, the sample size is small (204); increasing the sample size in future studies may also result in more significant results. Third, TMS is a multidimensional construct [

21] consisting of top management support for change (TMSC), top management support for vision sharing (TMSV), and top management support for resource allocation (TMSR). Further research should be conducted to determine the mediating and moderating impacts of TMS dimensions in order to fully grasp the dynamics of TMS impact on the cloud ERP implementation–financial performance link. Fourth, additional variables may act as mediators and moderators in the relationship between cloud ERP implementation and financial performance; future research should shed light on this possibility.

,

,

{kind=link}

{kind=link}