The Role of CSR and Ethical Leadership to Shape Employees’ Pro-Environmental Behavior in the Era of Industry 4.0. A Case of the Banking Sector

, ,

, ,  and

and

Abstract

:1. Introduction

2. Literature Review

2.1. CSR and Employees’ Pro-Environmental Behavior

2.2. CSR and Ethical Leadership

2.3. Ethical Leadership and Pro-Environmental Behavior

2.4. Ethical Leadership as a Mediator

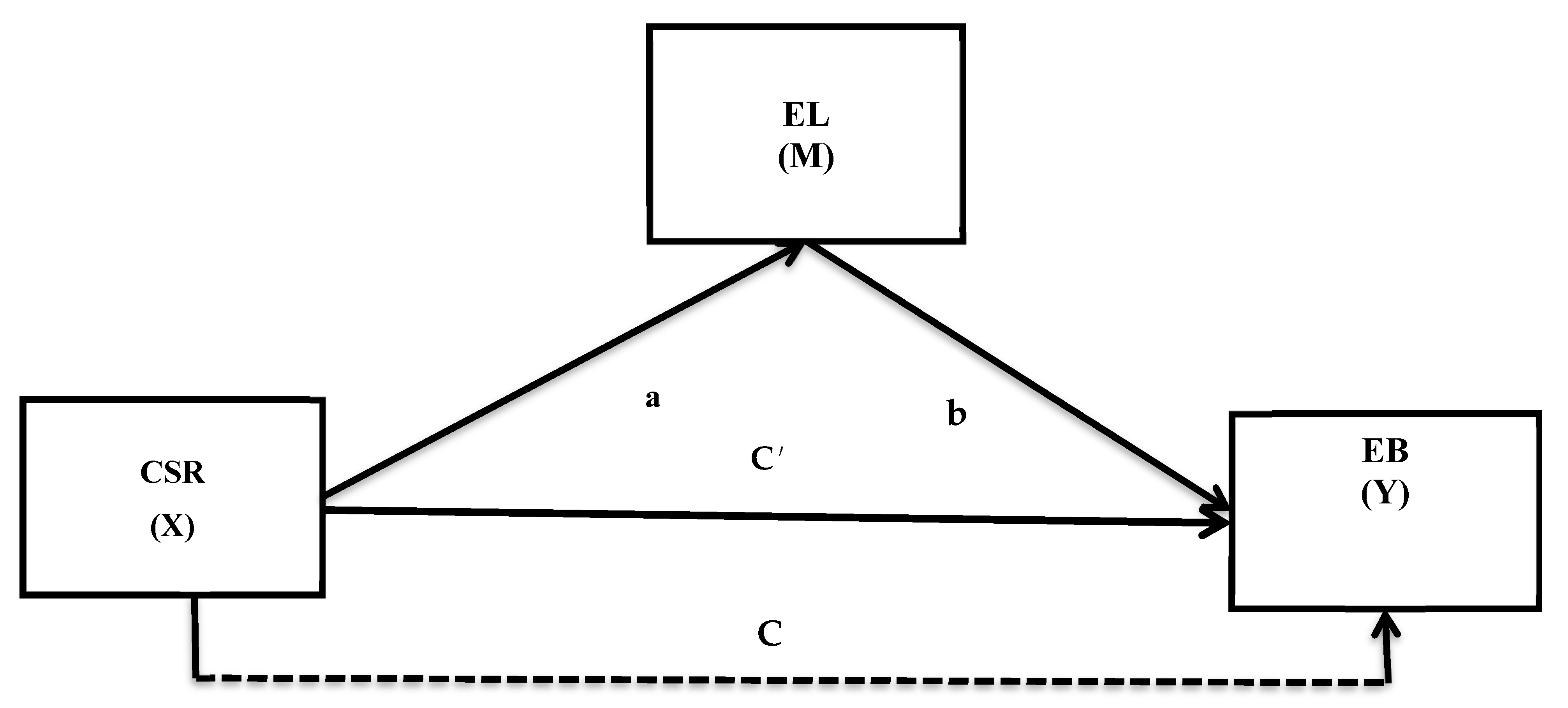

3. Methodology

Measures and Addressing the Issue of Social Desirability

4. Results

4.1. Detecting for Common Method Bias

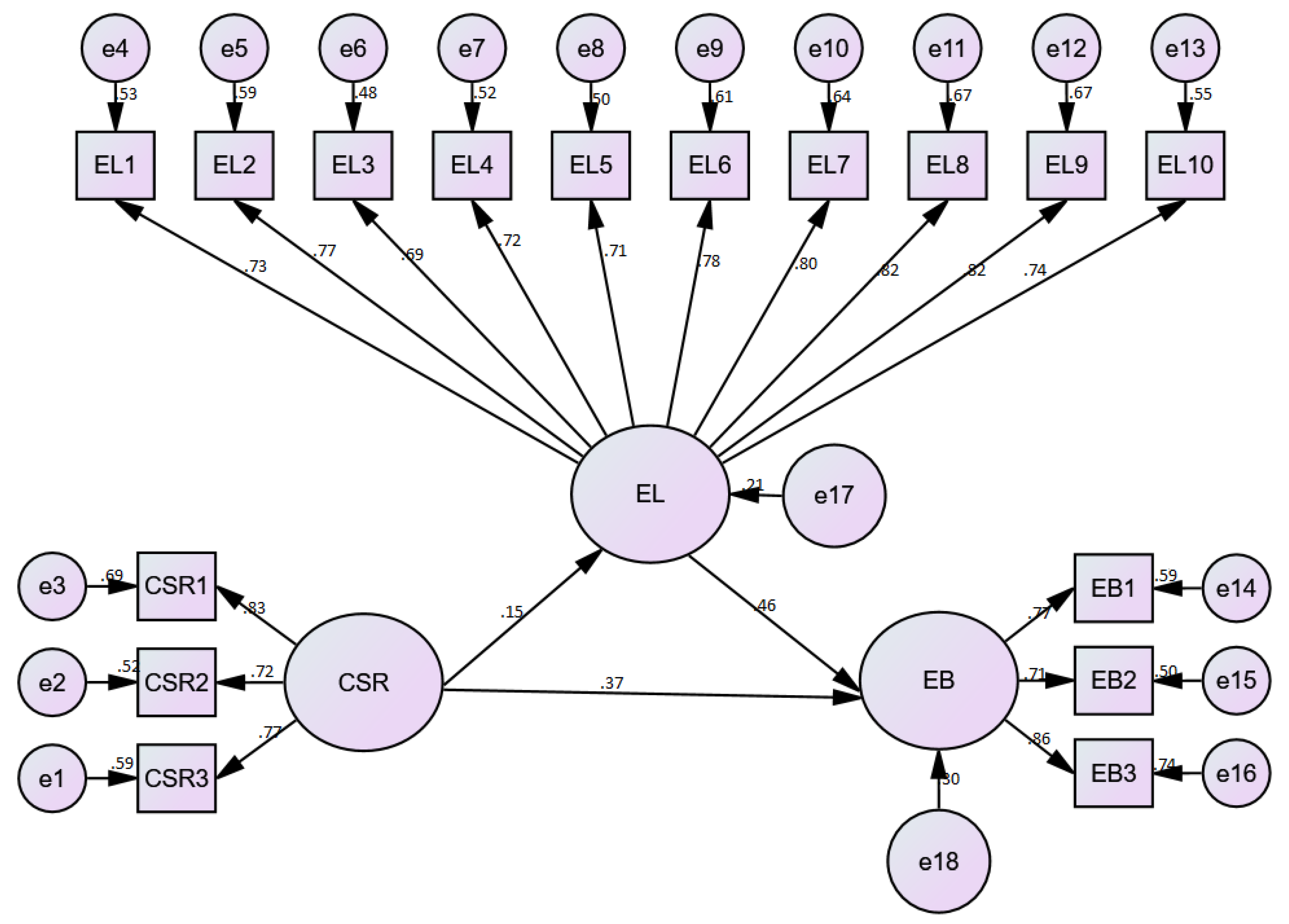

4.2. Convergent Validity, Factor Loadings, and the Reliability Analyses

4.3. Hypotheses Testing

5. Discussion and Implications

5.1. Limitations and Potential Research Directions

5.2. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Glavas, A.; Kelley, K. The effects of perceived corporate social responsibility on employee attitudes. Bus. Ethics Q. 2014, 24, 165–202. [Google Scholar] [CrossRef]

- Afridi, S.A.; Afsar, B.; Shahjehan, A.; Khan, W.; Rehman, Z.U.; Khan, M.A.S. Impact of corporate social responsibility attributions on employee’s extra-role behaviors: Moderating role of ethical corporate identity and interpersonal trust. Corp. Soc. Responsib. Environ. Manag. 2020. [Google Scholar] [CrossRef]

- Molnár, E.; Mahmood, A.; Ahmad, N.; Ikram, A.; Murtaza, S.A. The Interplay between Corporate Social Responsibility at Employee Level, Ethical Leadership, Quality of Work Life and Employee Pro-Environmental Behavior: The Case of Healthcare Organizations. Int. J. Environ. Res. Public Health 2021, 18, 4521. [Google Scholar] [CrossRef] [PubMed]

- Puppim de Oliveira, J.A.; Jabbour, C.J.C. Environmental management, climate change, CSR, and governance in clusters of small firms in developing countries: Toward an integrated analytical framework. Bus. Soc. 2017, 56, 130–151. [Google Scholar] [CrossRef]

- Memon, S.; Sethar, W.; Pitafi, A.; Uddin, W. Impact of CSR on Financial Performance of Banks: A Case Study. J. Account. Financ. Emerg. Econ. 2019, 5, 129–140. [Google Scholar] [CrossRef] [Green Version]

- Fayad, A.A.; Ayoub, R.; Ayoub, M. Causal relationship between CSR and FB in banks. Arab. Econ. Bus. J. 2017, 12, 93–98. [Google Scholar] [CrossRef]

- Boadi, E.A.; He, Z.; Bosompem, J.; Opata, C.N.; Boadi, E.K. Employees’ perception of corporate social responsibility (CSR) and its effects on internal outcomes. Serv. Ind. J. 2020, 40, 611–632. [Google Scholar] [CrossRef]

- Ahmad, N.; Ullah, Z.; Arshad, M.Z.; Kamran, H.W.; Scholz, M.; Han, H. Relationship between corporate social responsibility at the micro-level and environmental performance: The mediating role of employee pro-environmental behavior and the moderating role of gender. Sustain. Prod. Consum. 2021, 27, 1138–1148. [Google Scholar] [CrossRef]

- Dimitrov, R.S. The Paris agreement on climate change: Behind closed doors. Glob. Environ. Politics 2016, 16, 1–11. [Google Scholar] [CrossRef] [Green Version]

- Willuweit, L. Promoting Pro-Environmental Behavior: An Investigation of the Cross-Cultural Environmental Behavior Patterns. The Case of Abu Dhabi; Stockholm University: Stockholm, Sweden, 2009. [Google Scholar]

- Thondhlana, G.; Hlatshwayo, T.N. Pro-environmental behaviour in student residences at Rhodes University, South Africa. Sustainability 2018, 10, 2746. [Google Scholar] [CrossRef] [Green Version]

- Gifford, R.; Nilsson, A. Personal and social factors that influence pro-environmental concern and behaviour: A review. Int. J. Psychol. 2014, 49, 141–157. [Google Scholar] [CrossRef] [PubMed]

- Casaló, L.V.; Escario, J.-J. Heterogeneity in the association between environmental attitudes and pro-environmental behavior: A multilevel regression approach. J. Clean. Prod. 2018, 175, 155–163. [Google Scholar] [CrossRef]

- Bouraoui, K.; Bensemmane, S.; Ohana, M.; Russo, M. Corporate social responsibility and employees’ affective commitment. Manag. Decis. 2019, 57, 152–167. [Google Scholar] [CrossRef]

- Carroll, A.B. Carroll’s pyramid of CSR: Taking another look. Int. J. Corp. Soc. Responsib. 2016, 1, 1–8. [Google Scholar] [CrossRef] [Green Version]

- Carroll, A.B. A three-dimensional conceptual model of corporate performance. Acad. Manag. Rev. 1979, 4, 497–505. [Google Scholar] [CrossRef] [Green Version]

- Kucharska, W.; Kowalczyk, R. How to achieve sustainability?—Employee’s point of view on company’s culture and CSR practice. Corp. Soc. Responsib. Environ. Manag. 2019, 26, 453–467. [Google Scholar] [CrossRef]

- Schaefer, S.D.; Terlutter, R.; Diehl, S. Talking about CSR matters: Employees’ perception of and reaction to their company’s CSR communication in four different CSR domains. Int. J. Advert. 2020, 39, 191–212. [Google Scholar] [CrossRef] [Green Version]

- Tian, Q.; Robertson, J.L. How and when does perceived CSR affect employees’ engagement in voluntary pro-environmental behavior? J. Bus. Ethics 2019, 155, 399–412. [Google Scholar] [CrossRef]

- Sila, I.; Cek, K. The impact of environmental, social and governance dimensions of corporate social responsibility on economic performance: Australian evidence. Procedia Comput. Sci. 2017, 120, 797–804. [Google Scholar] [CrossRef]

- Afsar, B.; Cheema, S.; Javed, F. Activating employee’s pro-environmental behaviors: The role of CSR, organizational identification, and environmentally specific servant leadership. Corp. Soc. Responsib. Environ. Manag. 2018, 25, 904–911. [Google Scholar] [CrossRef]

- Oláh, J.; Aburumman, N.; Popp, J.; Khan, M.A.; Haddad, H.; Kitukutha, N. Impact of Industry 4.0 on environmental sustainability. Sustainability 2020, 12, 4674. [Google Scholar] [CrossRef]

- Khan, M.; Domicián, M.; Abdulahi, M.; Sadaf, R.; Khan, M.; Popp, J.; Oláh, J. Do institutional quality, innovation and technologies promote financial market development. Eur. J. Int. Manag 2020, 14. [Google Scholar] [CrossRef]

- Kong, L.; Sial, M.S.; Ahmad, N.; Sehleanu, M.; Li, Z.; Zia-Ud-Din, M.; Badulescu, D. CSR as a potential motivator to shape employees’ view towards nature for a sustainable workplace environment. Sustainability 2021, 13, 1499. [Google Scholar] [CrossRef]

- Shao, B.; Cardona, P.; Ng, I.; Trau, R.N. Are prosocially motivated employees more committed to their organization? The roles of supervisors’ prosocial motivation and perceived corporate social responsibility. Asia Pac. J. Manag. 2017, 34, 951–974. [Google Scholar] [CrossRef]

- Bauman, C.W.; Skitka, L.J. Corporate social responsibility as a source of employee satisfaction. Res. Organ. Behav. 2012, 32, 63–86. [Google Scholar] [CrossRef] [Green Version]

- Afsar, B.; Umrani, W.A. Corporate social responsibility and pro-environmental behavior at workplace: The role of moral reflectiveness, coworker advocacy, and environmental commitment. Corp. Soc. Responsib. Environ. Manag. 2020, 27, 109–125. [Google Scholar] [CrossRef]

- Islam, T.; Khan, M.M.; Ahmed, I.; Mahmood, K. Promoting in-role and extra-role green behavior through ethical leadership: Mediating role of green HRM and moderating role of individual green values. Int. J. Manpow. 2020, 42, 1102–1123. [Google Scholar] [CrossRef]

- Maqsoom, A.; Arif, U.; Ejaz, A.; Musarat, M.A.; Aslam, I.; Zubair, S. Factors Influencing the Pro-Environmental Behavior of Construction Workers. In Proceedings of the 2020 Second International Sustainability and Resilience Conference: Technology and Innovation in Building Designs (51154), Sakheer, Bahrain, 11–12 November 2020; IEEE: Piscataway, NJ, USA, 2020; pp. 1–5. [Google Scholar]

- Ren, S.; Tang, G.; Jackson, S.E. Effects of Green HRM and CEO ethical leadership on organizations’ environmental performance. Int. J. Manpow. 2020, 42, 961–983. [Google Scholar] [CrossRef]

- Khan, M.A.S.; Jianguo, D.; Ali, M.; Saleem, S.; Usman, M. Interrelations between ethical leadership, green psychological climate, and organizational environmental citizenship behavior: A moderated mediation model. Front. Psychol. 2019, 10, 1977. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Brown, M.E.; Treviño, L.K.; Harrison, D.A. Ethical leadership: A social learning perspective for construct development and testing. Organ. Behav. Hum. Decis. Process. 2005, 97, 117–134. [Google Scholar] [CrossRef]

- Kollmuss, A.; Agyeman, J. Mind the gap: Why do people act environmentally and what are the barriers to pro-environmental behavior? Environ. Educ. Res. 2002, 8, 239–260. [Google Scholar] [CrossRef] [Green Version]

- Keremidchiev, S. The Forth Industrial Revolution and CSR. Econ. Altern. 2019, 2, 169–183. [Google Scholar]

- Scavarda, A.; Daú, G.; Scavarda, L.F.; Caiado, R.G.G. An analysis of the corporate social responsibility and the Industry 4.0 with focus on the youth generation: A sustainable human resource management framework. Sustainability 2019, 11, 5130. [Google Scholar] [CrossRef] [Green Version]

- Potočan, V.; Mulej, M.; Nedelko, Z. Society 5.0: Balancing of Industry 4.0, economic advancement and social problems. Kybernetes 2021, 50, 794–811. [Google Scholar] [CrossRef]

- Julie, C.R. Fourth Industrial Revolution Brings Challenge and Opportunity. Available online: https://hrexecutive.com/fourth-industrial-revolution-brings-challenge-and-opportunity/ (accessed on 23 August 2021).

- Szegedi, K.; Khan, Y.; Lentner, C. Corporate social responsibility and financial performance: Evidence from Pakistani listed banks. Sustainability 2020, 12, 4080. [Google Scholar] [CrossRef]

- Ślusarczyk, B.; Tvaronavičienė, M.; Haque, A.U.; Oláh, J. Predictors of Industry 4.0 technologies affecting logistic enterprises’ performance: International perspective from economic lens. Technol. Econ. Dev. Econ. 2020, 26, 1263–1283. [Google Scholar] [CrossRef]

- Oláh, J.; Kitukutha, N.; Haddad, H.; Pakurár, M.; Máté, D.; Popp, J. Achieving sustainable e-commerce in environmental, social and economic dimensions by taking possible trade-offs. Sustainability 2019, 11, 89. [Google Scholar] [CrossRef] [Green Version]

- Nagy, J.; Oláh, J.; Erdei, E.; Máté, D.; Popp, J. The role and impact of Industry 4.0 and the internet of things on the business strategy of the value chain—the case of Hungary. Sustainability 2018, 10, 3491. [Google Scholar] [CrossRef] [Green Version]

- Meekaewkunchorn, N.; Szczepańska-Woszczyna, K.; Muangmee, C.; Kassakorn, N.; Khalid, B. Entrepreneurial Orientation and Sme Performance: The Mediating Role of Learning Orientation. Econ. Sociol. 2021, 14, 294–312. [Google Scholar]

- Kot, S.; Haque, A.U.; Kozlovski, E. Strategic SCM’s mediating effect on the sustainable operations: Multinational perspective. Organizacija 2019, 52, 219–235. [Google Scholar] [CrossRef] [Green Version]

- Al-Gasawneh, J.A.; Anuar, M.M.; Dacko-Pikiewicz, Z.; Saputra, J. The Impact of Customer Relationship Management Dimensions on Service Quality. Pol. J. Manag. Stud. 2021, 23, 24–44. [Google Scholar]

- Cho, S.J.; Chung, C.Y.; Young, J. Study on the Relationship between CSR and Financial Performance. Sustainability 2019, 11, 343. [Google Scholar] [CrossRef] [Green Version]

- González-Rodríguez, M.R.; Martín-Samper, R.C.; Köseoglu, M.A.; Okumus, F. Hotels’ corporate social responsibility practices, organizational culture, firm reputation, and performance. J. Sustain. Tour. 2019, 27, 398–419. [Google Scholar] [CrossRef]

- Hou, C.-E.; Lu, W.-M.; Hung, S.-W. Does CSR matter? Influence of corporate social responsibility on corporate performance in the creative industry. Ann. Oper. Res. 2019, 278, 255–279. [Google Scholar] [CrossRef]

- Lin, Y.-E.; Li, Y.-W.; Cheng, T.Y.; Lam, K. Corporate social responsibility and investment efficiency: Does business strategy matter? Int. Rev. Financ. Anal. 2021, 73, 101585. [Google Scholar] [CrossRef]

- Gutiérrez-Fernández, M.; Fernández-Torres, Y. Does gender diversity influence business efficiency? An analysis from the social perspective of CSR. Sustainability 2020, 12, 3865. [Google Scholar] [CrossRef]

- Agarwal, J.; Stackhouse, M.; Osiyevskyy, O. I love that company: Look how ethical, prominent, and efficacious it is—A triadic organizational reputation (TOR) Scale. J. Bus. Ethics 2018, 153, 889–910. [Google Scholar] [CrossRef]

- Yuriev, A.; Boiral, O.; Guillaumie, L. Evaluating determinants of employees’ pro-environmental behavioral intentions. Int. J. Manpow. 2020, 41, 1005–1019. [Google Scholar] [CrossRef]

- Robertson, J.L.; Carleton, E. Uncovering how and when environmental leadership affects employees’ voluntary pro-environmental behavior. J. Leadersh. Organ. Stud. 2018, 25, 197–210. [Google Scholar] [CrossRef]

- Elf, P.; Isham, A.; Gatersleben, B. Above and beyond? How businesses can drive sustainable development by promoting lasting pro-environmental behaviour change: An examination of the IKEA Live Lagom project. Bus. Strategy Environ. 2021, 30, 1037–1050. [Google Scholar] [CrossRef]

- Schwartz, S.H. Awareness of consequences and the influence of moral norms on interpersonal behavior. Sociometry 1968, 31, 355–369. [Google Scholar] [CrossRef]

- Fishbein, M.; Ajzen, I. Belief, attitude, intention, and behavior: An introduction to theory and research. Philos. Rhetor. 1977, 10, 130–132. [Google Scholar]

- Ajzen, I. From intentions to actions: A theory of planned behavior. In Action Control; Springer: New York, NY, USA, 1985; pp. 11–39. [Google Scholar]

- Chen, M.-F. Extending the theory of planned behavior model to explain people’s energy savings and carbon reduction behavioral intentions to mitigate climate change in Taiwan–moral obligation matters. J. Clean. Prod. 2016, 112, 1746–1753. [Google Scholar] [CrossRef]

- Wesselink, R.; Blok, V.; Ringersma, J. Pro-environmental behaviour in the workplace and the role of managers and organisation. J. Clean. Prod. 2017, 168, 1679–1687. [Google Scholar] [CrossRef]

- Gatti, L.; Vishwanath, B.; Seele, P.; Cottier, B. Are we moving beyond voluntary CSR? Exploring theoretical and managerial implications of mandatory CSR resulting from the new Indian companies act. J. Bus. Ethics 2019, 160, 961–972. [Google Scholar] [CrossRef]

- Aljarah, A.; Ibrahim, B. The robustness of corporate social responsibility and brand loyalty relation: A meta-analytic examination. J. Promot. Manag. 2020, 26, 1038–1072. [Google Scholar] [CrossRef]

- Moggi, S.; Bonomi, S.; Ricciardi, F. Against food waste: CSR for the social and environmental impact through a network-based organizational model. Sustainability 2018, 10, 3515. [Google Scholar] [CrossRef] [Green Version]

- Ramesh, K.; Saha, R.; Goswami, S.; Dahiya, R. Consumer’s response to CSR activities: Mediating role of brand image and brand attitude. Corp. Soc. Responsib. Environ. Manag. 2019, 26, 377–387. [Google Scholar] [CrossRef]

- Stoyanova, T.; Iliev, I. Employee engagement factor for organizational excellence. Int. J. Bus. Econ. Sci. Appl. Res. (IJBESAR) 2017, 10, 23–29. [Google Scholar] [CrossRef]

- Ghlichlee, B.; Bayat, F. Frontline employees’ engagement and business performance: The mediating role of customer-oriented behaviors. Manag. Res. Rev. 2020, 44, 290–317. [Google Scholar] [CrossRef]

- Nazir, O.; Islam, J.U. Enhancing organizational commitment and employee performance through employee engagement. South Asian J. Bus. Stud. 2017, 6, 98–114. [Google Scholar] [CrossRef]

- Lee, K.; Oh, W.Y.; Kim, N. Social media for socially responsible firms: Analysis of Fortune 500′s Twitter profiles and their CSR/CSIR ratings. J. Bus. Ethics 2013, 118, 791–806. [Google Scholar] [CrossRef]

- Hameed, Z.; Khan, I.U.; Islam, T.; Sheikh, Z.; Khan, S.U. Corporate social responsibility and employee pro-environmental behaviors. South Asian J. Bus. Stud. 2019, 8, 246–265. [Google Scholar] [CrossRef]

- Suganthi, L. Examining the relationship between corporate social responsibility, performance, employees’ pro-environmental behavior at work with green practices as mediator. J. Clean. Prod. 2019, 232, 739–750. [Google Scholar] [CrossRef]

- Bercovici, E.G.; Bercovici, A. Israeli labor market and the Fourth Industrial Revolution. Amfiteatru Econ. 2019, 21, 884–895. [Google Scholar] [CrossRef]

- Arnaud, A.; Sekerka, L.E. Positively ethical: The establishment of innovation in support of sustainability. Int. J. Sustain. Strateg. Manag. 2010, 2, 121–137. [Google Scholar] [CrossRef]

- Norton, T.A.; Zacher, H.; Ashkanasy, N.M. On the importance of pro-environmental organizational climate for employee green behavior. Ind. Organ. Psychol. 2012, 5, 497. [Google Scholar] [CrossRef]

- Rupp, D.E.; Shao, R.; Thornton, M.A.; Skarlicki, D.P. Applicants’ and employees’ reactions to corporate social responsibility: The moderating effects of first-party justice perceptions and moral identity. Pers. Psychol. 2013, 66, 895–933. [Google Scholar] [CrossRef]

- Yuriev, A.; Dahmen, M.; Paillé, P.; Boiral, O.; Guillaumie, L. Pro-environmental behaviors through the lens of the theory of planned behavior: A scoping review. Resour. Conserv. Recycl. 2020, 155, 104660. [Google Scholar] [CrossRef]

- Aziz, F.; Md Rami, A.A.; Zaremohzzabieh, Z.; Ahrari, S. Effects of Emotions and Ethics on Pro-Environmental Behavior of University Employees: A Model Based on the Theory of Planned Behavior. Sustainability 2021, 13, 7062. [Google Scholar] [CrossRef]

- Ateş, H. Merging theory of planned behavior and value identity personal norm model to explain pro-environmental behaviors. Sustain. Prod. Consum. 2020, 24, 169–180. [Google Scholar] [CrossRef]

- Zhu, Y.; Sun, L.-Y.; Leung, A.S.M. Corporate social responsibility, firm reputation, and firm performance: The role of ethical leadership. Asia Pac. J. Manag. 2014, 31, 925–947. [Google Scholar] [CrossRef]

- Lin, C.-P.; Liu, M.-L. Examining the effects of corporate social responsibility and ethical leadership on turnover intention. Pers. Rev. 2017, 46, 526–550. [Google Scholar] [CrossRef]

- Supanti, D.; Butcher, K.; Fredline, L. Enhancing the employer-employee relationship through corporate social responsibility (CSR) engagement. Int. J. Contemp. Hosp. Manag. 2015, 27, 1479–1498. [Google Scholar] [CrossRef]

- Budur, T.; Demir, A. Leadership effects on employee perception about CSR in Kurdistan Region of Iraq. Int. J. Soc. Sci. Educ. Stud. 2019, 5, 184–192. [Google Scholar]

- Pasricha, P.; Singh, B.; Verma, P. Ethical leadership, organic organizational cultures and corporate social responsibility: An empirical study in social enterprises. J. Bus. Ethics 2018, 151, 941–958. [Google Scholar] [CrossRef]

- Glavas, A. Corporate social responsibility and employee engagement: Enabling employees to employ more of their whole selves at work. Front. Psychol. 2016, 7, 796. [Google Scholar] [CrossRef]

- De Roeck, K.; Farooq, O. Corporate social responsibility and ethical leadership: Investigating their interactive effect on employees’ socially responsible behaviors. J. Bus. Ethics 2018, 151, 923–939. [Google Scholar] [CrossRef]

- Kim, M.-S.; Thapa, B. Relationship of ethical leadership, corporate social responsibility and organizational performance. Sustainability 2018, 10, 447. [Google Scholar] [CrossRef] [Green Version]

- Demir, A.; Budur, T. Roles of leadership styles in corporate social responsibility to non-governmental organizations (NGOs). Int. J. Soc. Sci. Educ. Stud. 2019, 5, 174–183. [Google Scholar]

- Sial, M.S.; Chunmei, Z.; Khan, T.; Nguyen, V.K. Corporate social responsibility, firm performance and the moderating effect of earnings management in Chinese firms. Asia-Pac. J. Bus. Adm. 2018, 10, 184–199. [Google Scholar] [CrossRef]

- Sial, M.S.; Chunmei, Z.; Khuong, N.V. Do female and independent directors explain the two-way relationship between corporate social responsibility and earnings management of Chinese listed firms? Int. J. Account. Inf. Manag. 2019, 27, 442–460. [Google Scholar] [CrossRef]

- Guping, C.; Sial, M.S.; Wan, P.; Badulescu, A.; Badulescu, D.; Brugni, T.V. Do Board Gender Diversity and Non-Executive Directors Affect CSR Reporting? Insight from Agency Theory Perspective. Sustainability 2020, 12, 8597. [Google Scholar] [CrossRef]

- Chen, X.; Sial, M.S.; Tran, D.K.; Alhaddad, W.; Hwang, J.; Thu, P.A. Are Socially Responsible Companies Really Ethical? The Moderating Role of State-Owned Enterprises: Evidence from China. Sustainability 2020, 12, 2858. [Google Scholar] [CrossRef] [Green Version]

- Brown, M.E.; Treviño, L.K. Ethical leadership: A review and future directions. Leadersh. Q. 2006, 17, 595–616. [Google Scholar] [CrossRef]

- Knights, D.; O’Leary, M. Leadership, ethics and responsibility to the other. J. Bus. Ethics 2006, 67, 125–137. [Google Scholar] [CrossRef]

- Northouse, P.G. Leadership: Theory and Practice, 5th ed.; SAGE Publications, Incorporated: Kalamazoo, MI, USA, 2021. [Google Scholar]

- Yoon, B.; Chung, Y. The effects of corporate social responsibility on firm performance: A stakeholder approach. J. Hosp. Tour. Manag. 2018, 37, 89–96. [Google Scholar] [CrossRef]

- Akisik, O.; Gal, G. The impact of corporate social responsibility and internal controls on stakeholders’ view of the firm and financial performance. Sustain. Account. Manag. Policy J. 2017, 8, 246–280. [Google Scholar] [CrossRef]

- Hansen, S.D.; Dunford, B.B.; Alge, B.J.; Jackson, C.L. Corporate social responsibility, ethical leadership, and trust propensity: A multi-experience model of perceived ethical climate. J. Bus. Ethics 2016, 137, 649–662. [Google Scholar] [CrossRef]

- Moore, C.; Mayer, D.M.; Chiang, F.F.T.; Crossley, C.; Karlesky, M.J.; Birtch, T.A. Leaders matter morally: The role of ethical leadership in shaping employee moral cognition and misconduct. J. Appl. Psychol. 2019, 104, 123. [Google Scholar] [CrossRef]

- Ahmad, I.; Donia, M.B.L.; Khan, A.; Waris, M. Do as I say and do as I do? The mediating role of psychological contract fulfillment in the relationship between ethical leadership and employee extra-role performance. Pers. Rev. 2019, 48, 98–117. [Google Scholar] [CrossRef] [Green Version]

- Tu, Y.; Lu, X. Do ethical leaders give followers the confidence to go the extra mile? The moderating role of intrinsic motivation. J. Bus. Ethics 2016, 135, 129–144. [Google Scholar] [CrossRef]

- Saleem, M.; Qadeer, F.; Mahmood, F.; Ariza-Montes, A.; Han, H. Ethical leadership and employee green behavior: A multilevel moderated mediation analysis. Sustainability 2020, 12, 3314. [Google Scholar] [CrossRef] [Green Version]

- Nejati, M.; Salamzadeh, Y.; Loke, C.K. Can ethical leaders drive employees’ CSR engagement? Soc. Responsib. J. 2019, 16, 655–669. [Google Scholar] [CrossRef]

- Mostafa, A.M.S.; Shen, J. Ethical leadership, internal CSR, organisational engagement and organisational workplace deviance. Evid.-Based HRM A Glob. Forum Empir. Scholarsh. 2019, 8, 113–127. [Google Scholar] [CrossRef]

- Zhang, Q.; Oo, B.L.; Lim, B.T.H. Drivers, motivations, and barriers to the implementation of corporate social responsibility practices by construction enterprises: A review. J. Clean. Prod. 2019, 210, 563–584. [Google Scholar] [CrossRef]

- Vveinhardt, J.; Andriukaitiene, R. Management culture as part of organizational culture in the context of corporate social responsibility implementation. Econ. Sociol. 2017, 10, 294–320. [Google Scholar] [CrossRef] [Green Version]

- Upadhaya, B.; Munir, R.; Blount, Y.; Su, S.X. Does organizational culture mediate the CSR–strategy relationship? Evidence from a developing country, Nepal. J. Bus. Res. 2018, 91, 108–122. [Google Scholar] [CrossRef]

- Dabija, D.-C.; Postelnicu, C.; Dinu, V. Cross-generational investigation of ethics and sustainability. Insights from Romanian retailing. In Current Issues in Corporate Social Responsibility; Springer: Berlin/Heidelberg, Germany, 2018; pp. 141–163. [Google Scholar]

- Edinger-Schons, L.M.; Lengler-Graiff, L.; Scheidler, S.; Wieseke, J. Frontline employees as corporate social responsibility (CSR) ambassadors: A quasi-field experiment. J. Bus. Ethics 2019, 157, 359–373. [Google Scholar] [CrossRef]

- Engelbrecht, A.S.; Heine, G.; Mahembe, B. Integrity, ethical leadership, trust and work engagement. Leadersh. Organ. Dev. J. 2017, 38, 368–379. [Google Scholar] [CrossRef] [Green Version]

- Ferreira, A.I. Leader and peer ethical behavior influences on job embeddedness. J. Leadersh. Organ. Stud. 2017, 24, 345–356. [Google Scholar] [CrossRef]

- Jamwal, N. Hawala-the invisible financing system of terrorism. Strateg. Anal. 2002, 26, 181–198. [Google Scholar] [CrossRef]

- FATA. The Role of Hawala and Other Similar Service Providers in Money Laundering and Terrorist Financing. 2013. Available online: www.fatf-gafi.org/media/fatf/documents/reports/Role-of-hawala-and-similar-in-ml-tf.pdf (accessed on 15 May 2018).

- Raza, M.S.; Fayyaz, M.; Ijaz, H. The Hawala System in Pakistan: A catalyst for money laundering & terrorist financing. Forensic Res. Criminol. Int. J. 2017, 5, 1–3. [Google Scholar]

- The News. Islamic Banks’ Market Share Up. Available online: https://www.thenews.com.pk/print/746679-islamic-banks-market-share-up#:~:text=The%20market%20share%20of%20Islamic%20banks’%20assets%20stood%20at%2015.3,2020%2C%20primarily%20due%20to%20investments (accessed on 28 April 2021).

- Jafri, R. A Panoramic View of Pakistan’s Banking System. Available online: https://www.globalvillagespace.com/a-panoramic-view-of-pakistans-banking-system/ (accessed on 14 March 2021).

- Habib Bank. Total Assest of Habib Bank. Available online: https://www.hbl.com/about-us (accessed on 12 March 2021).

- National Bank. Financial Statements. Available online: https://www.nbp.com.pk/FinancialStatements/AnnualReports.aspx (accessed on 12 March 2021).

- MCB Bank. Total Assest. Available online: https://www.mcb.com.pk (accessed on 12 March 2021).

- United Bank. Financial Statements. Available online: https://www.ubldirect.com/Corporate/InvestorRelations/FinancialStatement.aspx (accessed on 12 March 2021).

- Allied Bank. Financials. Available online: https://www.abl.com/investor-relations/financials/ (accessed on 12 March 2021).

- IQAir. Air Quality in Pakistan. Available online: https://www.iqair.com/us/pakistan (accessed on 3 January 2020).

- Abuzaid, A.N. The relationship between ethical leadership and organizational commitment in banking sector of Jordan. J. Econ. Adm. Sci. 2018, 34, 187–203. [Google Scholar] [CrossRef]

- Alpkan, L.; Karabay, M.; Şener, İ.; Elçi, M.; Yıldız, B. The mediating role of trust in leader in the relations of ethical leadership and distributive justice on internal whistleblowing: A study on Turkish banking sector. Kybernetes 2020, 50, 2073–2092. [Google Scholar] [CrossRef]

- Bissing-Olson, M.J.; Iyer, A.; Fielding, K.S.; Zacher, H. Relationships between daily affect and pro-environmental behavior at work: The moderating role of pro-environmental attitude. J. Organ. Behav. 2013, 34, 156–175. [Google Scholar] [CrossRef]

- Williams, L.J.; Anderson, S.E. Job satisfaction and organizational commitment as predictors of organizational citizenship and in-role behaviors. J. Manag. 1991, 17, 601–617. [Google Scholar] [CrossRef]

- Fombrun, C.J.; Gardberg, N.A.; Sever, J.M. The Reputation Quotient SM: A multi-stakeholder measure of corporate reputation. J. Brand Manag. 2000, 7, 241–255. [Google Scholar] [CrossRef]

- Ahmad, N.; Ullah, Z.; Mahmood, A.; Ariza-Montes, A.; Vega-Muñoz, A.; Han, H.; Scholz, M. Corporate social responsibility at the micro-level as a “new organizational value” for sustainability: Are females more aligned towards it? Int. J. Environ. Res. Public Health 2021, 18, 2165. [Google Scholar] [CrossRef]

- Sun, H.; Rabbani, M.R.; Ahmad, N.; Sial, M.S.; Cheng, G.; Zia-Ud-Din, M.; Fu, Q. CSR, Co-Creation and Green Consumer Loyalty: Are Green Banking Initiatives Important? A Moderated Mediation Approach from an Emerging Economy. Sustainability 2020, 12, 10688. [Google Scholar] [CrossRef]

- Raza, A.; Saeed, A.; Iqbal, M.K.; Saeed, U.; Sadiq, I.; Faraz, N.A. Linking corporate social responsibility to customer loyalty through co-creation and customer company identification: Exploring sequential mediation mechanism. Sustainability 2020, 12, 2525. [Google Scholar] [CrossRef] [Green Version]

- Harman, H.H. Modern Factor Analysis, 3rd ed.; University of Chicago Press: Chicago, IL, USA, 1976. [Google Scholar]

- Podsakoff, P.M.; MacKenzie, S.B.; Lee, J.-Y.; Podsakoff, N.P. Common method biases in behavioral research: A critical review of the literature and recommended remedies. J. Appl. Psychol. 2003, 88, 879. [Google Scholar] [CrossRef] [PubMed]

- Richter, N.F.; Schubring, S.; Hauff, S.; Ringle, C.M.; Sarstedt, M. When predictors of outcomes are necessary: Guidelines for the combined use of PLS-SEM and NCA. Ind. Manag. Data Syst. 2020, 120, 2243–2267. [Google Scholar] [CrossRef]

- Matthews, L. Applying multigroup analysis in PLS-SEM: A step-by-step process. In Partial Least Squares Path Modeling; Springer: Berlin/Heidelberg, Germany, 2017; pp. 219–243. [Google Scholar]

- Thakkar, J.J. Applications of structural equation modelling with AMOS 21, IBM SPSS. In Structural Equation Modelling; Springer: Singapore, 2020; pp. 35–89. [Google Scholar]

- Baron, R.M.; Kenny, D.A. The moderator–mediator variable distinction in social psychological research: Conceptual, strategic, and statistical considerations. J. Personal. Soc. Psychol. 1986, 51, 1173. [Google Scholar] [CrossRef]

- Hayes, A.F. Beyond Baron and Kenny: Statistical mediation analysis in the new millennium. Commun. Monogr. 2009, 76, 408–420. [Google Scholar] [CrossRef]

- Zhao, X.; Lynch, J.G., Jr.; Chen, Q. Reconsidering Baron and Kenny: Myths and truths about mediation analysis. J. Consum. Res. 2010, 37, 197–206. [Google Scholar] [CrossRef]

- Alzaidi, S.M.; Iyanna, S. Developing a conceptual model for voluntary pro-environmental behavior of employees. Soc. Responsib. J. 2021. [Google Scholar] [CrossRef]

- Bakari, H.; Hunjra, A.I.; Niazi, G.S.K. How does authentic leadership influence planned organizational change? The role of employees’ perceptions: Integration of theory of planned behavior and Lewin’s three step model. J. Chang. Manag. 2017, 17, 155–187. [Google Scholar] [CrossRef]

- Howell, A.P.; Shaw, B.R.; Alvarez, G. Bait shop owners as opinion leaders: A test of the theory of planned behavior to predict pro-environmental outreach behaviors and intentions. Environ. Behav. 2015, 47, 1107–1126. [Google Scholar] [CrossRef]

- Lau, A.K.W.; Lee, S.H.N.; Jung, S. The role of the institutional environment in the relationship between CSR and operational performance: An empirical study in Korean manufacturing industries. Sustainability 2018, 10, 834. [Google Scholar] [CrossRef] [Green Version]

- Ullah, Z.; Ahmad, N.; Nazim, Z.; Ramzan, M. Impact of Csr on Corporate Reputation, Customer Loyalty and Organizational Performance. Gov. Manag. Rev. 2020, 5, 195–210. [Google Scholar]

- Crisan-Mitra, C.; Dinu, V.; Postelnicu, C.; Dabija, D.-C. Corporate Practice of Sustainable Development on an Emerging Market. Transform. Bus. Econ. 2016, 15, 228–243. [Google Scholar]

- Shahzad, M.; Qu, Y.; Javed, S.A.; Zafar, A.U.; Rehman, S.U. Relation of environment sustainability to CSR and green innovation: A case of Pakistani manufacturing industry. J. Clean. Prod. 2020, 253, 119938. [Google Scholar] [CrossRef]

- Ahmad, I.; Umrani, W.A. The impact of ethical leadership style on job satisfaction. Leadersh. Organ. Dev. J. 2019, 40, 534–547. [Google Scholar] [CrossRef]

- Saleem, M.; Qadeer, F.; Mahmood, F.; Han, H.; Giorgi, G.; Ariza-Montes, A. Inculcation of Green Behavior in Employees: A Multilevel Moderated Mediation Approach. Int. J. Environ. Res. Public Health 2021, 18, 331. [Google Scholar] [CrossRef]

- Rezapouraghdam, H.; Akhshik, A.; Ramkissoon, H. Application of machine learning to predict visitors’ green behavior in marine protected areas: Evidence from Cyprus. J. Sustain. Tour. 2021, 1–25. [Google Scholar] [CrossRef]

- Islam, T.; Ali, G.; Asad, H. Environmental CSR and pro-environmental behaviors to reduce environmental dilapidation. Manag. Res. Rev. 2019, 42, 332–351. [Google Scholar] [CrossRef]

- Sial, M.S.; Vo, X.V.; Al-Haddad, L.; Trang, T.N. Impact of female directors on the board and foreign institutional investors on earning manipulation of Chinese listed companies. Asia-Pac. J. Bus. Adm. 2019, 11, 288–300. [Google Scholar] [CrossRef]

- Sial, M.S.; Zheng, C.; Cherian, J.; Gulzar, M.; Thu, P.A.; Khan, T.; Khuong, N.V. Does Corporate Social Responsibility Mediate the Relation between Boardroom Gender Diversity and Firm Performance of Chinese Listed Companies? Sustainability 2018, 10, 3591. [Google Scholar] [CrossRef] [Green Version]

- Guping, C.; Cherian, J.; Sial, M.S.; Mentel, G.; Wan, P.; Álvarez-Otero, S.; Saleem, U. The Relationship between CSR Communication on Social Media, Purchase Intention, and E-WOM in the Banking Sector of an Emerging Economy. J. Theor. Appl. Electron. Commer. Res. 2021, 16, 1025–1041. [Google Scholar]

- Jiang, L.; Cherian, J.; Sial, M.S.; Wan, P.; Filipe, J.A.; Mata, M.N.; Chen, X. The moderating role of CSR in board gender diversity and firm financial performance: Empirical evidence from an emerging economy. Econ. Res.-Ekon. Istraživanja 2020, 34, 2354–2373. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Demographic | Frequency | % |

|---|---|---|

| Gender | ||

| Male | 273 | 59.48 |

| Female | 186 | 40.52 |

| Age-group (Year) | ||

| 22–25 | 56 | 12.20 |

| 26–30 | 109 | 23.75 |

| 31–35 | 139 | 30.28 |

| 36–40 | 92 | 20.04 |

| Above 40 | 63 | 13.72 |

| Experience (Years) | ||

| 1–4 | 76 | 16.56 |

| 5–7 | 173 | 37.69 |

| 8–10 | 114 | 24.84 |

| Above 10 | 96 | 20.70 |

| Category | ||

| Manager | 167 | 36.38 |

| Non-Manager | 292 | 63.62 |

| Total | 459 | 100 |

| Items | Loadings | Square | SS | AVE | CR |

|---|---|---|---|---|---|

| Bank really cares about its employees (CSR1) | 0.83 | 0.69 | |||

| Bank contributes the communities in which it operates (CSR2) | 0.72 | 0.52 | |||

| Bank is environmentally responsible (CSR3) | 0.77 | 0.59 | 1.80 | 0.60 | 0.82 |

| Leader listens to what employees have to say (EL1) | 0.73 | 0.53 | |||

| Leader disciplines employees who violate ethical standards (EL2) | 0.77 | 0.59 | |||

| Leader conducts in an ethical manner (EL3) | 0.69 | 0.48 | |||

| Leader shows interest for employees (EL4) | 0.72 | 0.52 | |||

| Leader makes fair and balanced decisions (ETL5) | 0.71 | 0.50 | |||

| Leader can be trusted (EL6) | 0.78 | 0.61 | |||

| Leader discusses business ethics or values with employees (EL7) | 0.80 | 0.64 | |||

| Leader sets an example to do things ethically (EL8) | 0.82 | 0.67 | |||

| Leader defines success not just by results but also the way that they are obtained (EL9) | 0.82 | 0.67 | |||

| Leader when making decisions, asks employees (EL10) | 0.74 | 0.55 | 5.71 | 0.57 | 0.93 |

| Completion of job tasks in environmentally-friendly manner (EB1) | 0.77 | 0.59 | |||

| Consideration of environment during workplace (EB2) | 0.71 | 0.50 | |||

| Efforts to align with organization to improve the environment (EB3) | 0.86 | 0.74 | 1.84 | 0.61 | 0.82 |

| Construct | Mean | SD | CSR | EL | EB |

|---|---|---|---|---|---|

| CSR | 3.96 | 0.66 | 0.77 | 0.31 ** | 0.38 ** |

| EL | 4.18 | 0.71 | 0.75 | 0.29 ** | |

| EB | 3.98 | 0.59 | 0.88 | ||

| Model fit indices | Range | Obtained | Model fit indices | Range | Obtained |

| χ2/df | 5.00 | 3.681 | IFI | 0.90 | 0.938 |

| RMSEA | 0.08 | 0.063 | TLI | 0.90 | 0.936 |

| NFI | 0.90 | 0.931 | GFI | 0.90 | 0.933 |

| CFI | 0.90 | 0.937 |

| Path | Estimates | SE | CR | p-Value | LLCI | ULCI | Decision |

|---|---|---|---|---|---|---|---|

| CSR→EB (H1) | (β1) 0.37 ** | 0.046 | 8.04 | *** | 0.316 | 0.528 | Accepted |

| CSR→EL (H2) | (β2) 0.15 ** | 0.022 | 6.82 | *** | 0.181 | 0.363 | Accepted |

| ETL→EB (H3) | (β3) 0.46 ** | 0.031 | 10.32 | *** | 0.291 | 0.488 | Accepted |

| Model fit indices | Range | Obtained | Model fit indices | Range | Obtained | ||

| χ2/df | 5.00 | 3.19 | IFI | 0.90 | 0.947 | ||

| RMSEA | 0.08 | 0.053 | TLI | 0.90 | 0.942 | ||

| NFI | 0.90 | 0.938 | GFI | 0.90 | 0.942 | ||

| CFI | 0.90 | 0.943 |

| Path | Estimates | SE | Z-Score | p-Value | LLCI | ULCI | Decision |

|---|---|---|---|---|---|---|---|

| CSR→EL→EB (H4) | (β3) 0.069 ** | 0.021 | 2.28 | *** | 0.036 | 0.183 | Accepted |

| Model fit indices | Range | Obtained | Model fit indices | Range | Obtained | ||

| χ2/df | 5.00 | 2.91 | IFI | 0.90 | 0.948 | ||

| RMSEA | 0.08 | 0.042 | TLI | 0.90 | 0.946 | ||

| NFI | 0.90 | 0.938 | GFI | 0.90 | 0.942 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Wu, Q.; Cherian, J.; Samad, S.; Comite, U.; Hu, H.; Gunnlaugsson, S.B.; Oláh, J.; Sial, M.S. The Role of CSR and Ethical Leadership to Shape Employees’ Pro-Environmental Behavior in the Era of Industry 4.0. A Case of the Banking Sector. Sustainability 2021, 13, 9773. https://doi.org/10.3390/su13179773

Wu Q, Cherian J, Samad S, Comite U, Hu H, Gunnlaugsson SB, Oláh J, Sial MS. The Role of CSR and Ethical Leadership to Shape Employees’ Pro-Environmental Behavior in the Era of Industry 4.0. A Case of the Banking Sector. Sustainability. 2021; 13(17):9773. https://doi.org/10.3390/su13179773

Chicago/Turabian StyleWu, Qiang, Jacob Cherian, Sarminah Samad, Ubaldo Comite, Huajie Hu, Stefan B. Gunnlaugsson, Judit Oláh, and Muhammad Safdar Sial. 2021. "The Role of CSR and Ethical Leadership to Shape Employees’ Pro-Environmental Behavior in the Era of Industry 4.0. A Case of the Banking Sector" Sustainability 13, no. 17: 9773. https://doi.org/10.3390/su13179773