Sustainable Growth in the Agro-Food Cooperatives of Castilla-La Mancha (Spain)

1

Department of Business Administration, University of Castilla-La Mancha, 45071 Toledo, Spain

2

Department of Management, Universidad Loyola Andalucía, 14004 Córdoba, Spain

3

Facultad de Administración y Negocios, Universidad Autónoma de Chile, Santiago 425, Chile

4

Facultad de Economía y Negocios, Universidad Andrés Bello, Santiago de Chile 7591538, Chile

*

Author to whom correspondence should be addressed.

Sustainability 2020, 12(12), 5045; https://doi.org/10.3390/su12125045

Submission received: 15 May 2020

/

Revised: 17 June 2020

/

Accepted: 18 June 2020

/

Published: 20 June 2020

(This article belongs to the Special Issue The Contribution of the Social Economy to the Sustainable Development Goals)

Abstract

:The present study aims at analysing the sustainable growth in the agro-food cooperatives of Castilla-La Mancha (Spain). To this end, the study examines the impact of the corporate social responsibility (hereinafter CSR) on the performance of the agro-food cooperatives. CSR is analysed based on the three dimensions suggested by the triple bottom line approach: Economic dimension, social dimension, and environmental dimension. Results are analysed using a partial least squares regression (PLS-SEM). The main contributions are as follows: (1) The measurement of the CSR through the triple bottom line approach has proven to be appropriate for the agro-food cooperatives of Castilla-la Mancha, as it presents adequate values of reliability and validity; (2) these dimensions make up the CSR, although the environmental dimension is the most relevant one for the agro-food cooperatives of Castilla-La Mancha; and (3) CSR positively and significantly affects the performance of agro-food cooperatives, as it explains 39.2% of their variance, thus confirming a sustainable growth model for the agro-food cooperatives of Castilla-La Mancha.

1. Introduction

The aim of this work is to test the influence of corporate social responsibility (CSR) measures on the performance of agro-food cooperatives. This research is justified because CSR is becoming a priority for companies and their managers [1,2,3]. CSR is also a fundamental aspect for cooperatives because their development model has sustainability values that will allow them, according to the Follow-up Commission of the Luxembourg Declaration [4] or the United Nations [5], to play a relevant role in the future. On the other hand, agro-food cooperatives have a key role to play in achieving sustainable development objectives [5].

The concern about CSR is relatively recent and is motivated by the fact that companies are being encouraged, from different spheres, to carry out CSR activities, due to their impact on economic activities, the environment, and society [6]. In this line, the World Economic Forum held in Davos in 1999 urged companies to be socially responsible and comply with a number of Principles of Conduct. Likewise, the Green Paper of the European Commission promotes a European framework for CSR because of the growing concern about social criteria and the deterioration of the environment [7]. In Spain, there are initiatives that try to promote the application of CSR actions in companies. The Spanish Government establishes that CSR must have a strategic nature for companies, including the design and implementation of CSR strategies in social, labour, environmental, and respect for human rights aspects [8]. Additionally, emphasis is placed on the voluntary nature of CSR actions and the impact of such actions.

In short, CSR has become one of the basic aspects of business activity due to its ability to create shared value [9], both for companies and for society [10]. Moreover, it favours a sustainable development by minimising the negative effects caused by certain unwanted behaviours in companies [6]. CSR is causing a shift in the business palette from an institution with only economic significance to one that also has social implications [11].

Although cooperatives, by their own definition, fall within the scope of the CSR, in this paper, we want to check whether they develop CSR actions. In other words, the first objective of this work is to check that there is no divergence between the formal definition of a cooperative and its reality. Co-operatives must achieve adequate levels of performance in order to meet the needs and interests of their members and of society. Therefore, the second objective of this paper is to analyse the influence of CSR on the performance of co-operatives. In short, in order to meet the objectives indicated above, in this paper, we pose the following research questions:

- Do the Cooperatives carry out CSR actions?

- What dimensions make up the Cooperatives’ CSR?

- Is it feasible to use the Triple Bottom Line to measure CSR in Cooperatives?

- Does CSR influence the performance of the Cooperative?

To carry out this study, a questionnaire was used due to the impossibility of obtaining data from the triple bottom line through sustainability reports. The information was obtained from a questionnaire sent by email to the Presidents of Cooperatives in which the questions have been asked following a Likert scale (1—strongly disagree; 5—strongly agree) of subjective response. Subjective measures have been used for the different items given the difficulty in achieving objective values [12].

There are multiple types of cooperatives that we can find, but in this work, we have focused on the agro-food cooperatives, and especially, on the agro-food cooperatives of Castilla-La Mancha due to their economic and social importance in this region of Spain.

With this work, we want to contribute to deepen the analysis of the CSR in the agro-food cooperatives through the triple bottom line and to verify that the actions in the matter of CSR of this type of cooperatives go beyond their formal definition.

2. Theoretical Framework and Hypothesis

There are different definitions of CSR in academic literature. Carroll [13] states that CSR includes all the economic, legal, ethical, and discretionary expectations that society has of companies at any given time. On the other hand, CSR pursues a sustainable development by involving different stakeholders [14]. The United Nations, through the World Summit Outcome Document (2005), establishes that CSR should count on stakeholders and sustainable development, and emphasises its voluntary nature as a relevant element [15]. According to the European Commission, a company is socially responsible when it considers, on a voluntary basis, social, environmental, and improvement aspects in its daily activity and relationship with stakeholders [7]. Authors such as De Castro [16] and Bigné et al. [17] agree with the definition of CSR given by the European Commission, while authors such as Claver et al. [18] o Fraj et al. [19] insist on the preservation of the environment. Other authors, such as Lozano et al. [2], focus on the voluntary nature of CSR. According to Friedman [20,21], the only social responsibility of a company is to maximise profits while respecting the basic rules of society. Hart [22] states that, for companies to achieve long-term benefits, they must develop resources and capacities that allow them to apply CSR. Based on the above premises and as a consequence of the deep socio-economic transformations our societies are going through, a new business model is emerging, characterised by the relevance of stakeholders and a greater concern for sustainable development [23,24,25].

CSR is not new to cooperatives: The values and principles of CSR have been present in the cooperative model since the very beginning. The cooperative movement is known for pioneering the development and implementation of CSR. Cooperatives have always been characterised by a democratic structure, mutual aid, equity, solidarity, relevance of their members, service to the interests of their workers, their community, and their environment, and all of these values share common elements with CSR [26]. Cooperative values directly connect with CSR values [27,28]. Cooperatives may even be considered as an indicator of the principles of CSR [29,30]. Furthermore, cooperatives are known for their ethical behaviour and the set of social values they represent [31]. When comparing the Davos Principles of Conduct and the Cooperative Principles established by the International Cooperative Alliance, it is easy to see a great similarity between them [25,32]. In this line, the International Cooperative Alliance [33] emphasises that cooperatives are based on values of mutual aid, responsibility, democracy, equality, equity, and solidarity, all of which are included, in one way or another, in their own definition, culture, or nature. The Green Paper of the European Commission is considered the benchmark in CSR in Social Economy [34,35,36]. The Paper states that cooperatives have a long tradition in combining economic viability and social responsibility, thanks to a constant dialogue between stakeholders through a participatory management [7]. Therefore, cooperatives carry out actions that can be framed in the solidarity and social insertion fields, territorial cohesion, etc. [37], as they aim at meeting social demands and improving the quality of life [38]. Therefore, they act as an alternative way to make progress in social transformation [39], since they promote social and economic development by generating employment [40].

Cooperatives are based on democratic and transparent decision-taking while integrating different stakeholders [26,41]. In this respect, the International Cooperative Alliance [33], emphasises that cooperatives are based on values such as mutual aid, responsibility, democracy, equality, equity, and solidarity. In this sense, the Cooperatives Law of Castilla-La Mancha itself, of 10 November 2010, defines cooperatives as “companies that offer goods or services … to achieve the satisfaction of their needs, aspirations and interests … and contribute to the improvement and promotion of their community environment” (Felipe Hernández-Perlines was a member of the Working Group of the Regional Social Economy Council of Castilla-La Mancha that participated in the preparatory work for the drafting of Law 11/2110 of 4 November on Cooperatives of Castilla-La Mancha.) [42]. CSR is an element of the cooperative model, the definition of which is based on a set of inclusive, participatory, extensive, transparent, sustainable, and shared values [6]. Because of their principles, values, and behaviour, cooperatives fall within the scope of CSR [43], to such an extent that they have set a precedent for other types of companies in terms of responsibility actions [25]. Furthermore, the cooperative model has become a guarantee for management models in other companies [44].

The CSR perspectives of cooperatives are very broad and diverse [45], as they cover aspects ranging from achieving economic results to improving their image, prestige and reputation [6]. CSR favours the competitiveness of cooperatives based on their sustainable development and their positioning in the markets as a responsible model. Cooperatives not only operate to generate value, but also consider economic and social aspects of CSR [46], including stakeholders’ needs [47] and integrate a strategic vision that is both internal and external to the company [48]. This strategic CSR management is key to successfully ruling the cooperatives [49] and must take good practices in economic, social, and environmental matters into consideration [41].

Having seen the importance of CSR in companies and, especially, in cooperatives, the present study will now focus on CSR dimensions. Academic literature offers many contributions on this subject. The European Commission’s Green Paper itself establishes two dimensions in CSR: An internal one (linked to human resource management, health and safety of workers, or an environmentally friendly production system) and an external one (linked to different types of interest, local communities, and the environment) [7]. On the other hand, De La Cuesta and Valor [50] distinguish three dimensions in CSR, in line with sustainable development: (1) The economic dimension (the company must generate value); (2) the social dimension (the company must respect legality, customs, and engage in improving the general wellbeing of society); and (3) the environmental dimension (the company must contribute to sustainable development). Finally, Vargas and Vaca [41], following Carroll [13], refer to four dimensions in CSR: (1) The economic one (the company aims to make profits); (2) the legal one (the company must comply with current regulations); (3) the ethical one (business activities must be considered correct by society); and (4) the discretionary dimension (“good practice” always, even when not required by society). In the last few years, the triple bottom line proposal [51] has become popular to measure CSR. This proposal integrates economic, social, and environmental aspects [52]. In addition, it links CSR to sustainable development, which requires the convergence of economic development, social equity, and environmental protection [53] and highlights the company’s externalities [54].

This study has used the latter concept of CSR, motivated by the fact that sustainability reports contain economic, social, and environmental actions that affect the company performance. The literature review in this regard shows research on the theoretical review of this relationship. Preston and O’Bannon [55] highlighted different theoretical possibilities to analyse the influence of CSR on the results. These theoretical possibilities are shown in Table 1.

Alvarado-Herrera et al. [56] reviewed the theoretical approaches to the relationship between CSR and business performance. Likewise, Lu et al. [1] examined 84 research studies published between 2002 and 2011 and concluded that the relationship between CSR and performance is a dynamic one that changes with time and space. Miras-Rodríguez et al. [57] conducted a meta-analysis that highlighted the influence of the country effect on the relationship between CSR and company results.

In this paper, we follow the social impact approach of Perston and O’Bannon [55] as other works have done. However, there are also empirical studies that analyse the relationship between CSR and performance in different types of companies. Gamerschlag et al. [58] studied 130 German-listed companies and established a positive relationship between CSR disclosure and performance in these companies. Campopiano and De Massis [59] focused their research on 98 Italian family businesses and concluded that family businesses spread CSR actions more widely than non-family businesses, and this dissemination is not related to CSR standards, as family businesses are less likely to comply with such standards. Within the field of family businesses, Hernández-Perlines [60] researched 174 Spanish family businesses and concluded that CSR has a positive effect on the performance of these companies. In the same line, Hernández-Perlines and Ibarra-Cisneros [61] examined 140 Mexican family businesses and found that entrepreneurship increases the CSR influence on business outcomes. Martín-Castejón and Aroca-López [62] studied 123 Spanish SMEs, all of which were family businesses, and revealed that gender and level of studies of managers affect the impact of CSR on the performance of their companies. The relationship between CSR and business outcomes can also be found in Chen et al. [63], only in relation to companies in the industrial sector. Specifically, they used a sample of 75 Swedish manufacturing companies and concluded that there is a positive and significant correlation between CSR and business performance. Li et al. [64] stated that CSR activities are value generators for companies. Finally, Bazán et al. [65] described the main topics to be included in a CSR agenda to achieve competitive advantage in large Spanish companies listed on the stock market.

In the field of Social Economy, Server and Villalonga [36] encouraged social economy companies to disclose their CSR actions. Arcas and Briones [6] analysed the way CSR behaviour differs in cooperatives and labour companies in a sample of 70 social economy companies in the Murcia region in Spain. In their introduction to “Monograph no. 75 of CIRIEC-Spain”, a public, social, and cooperative economy journal devoted to Social Business and Social Economy, Monzón and Marcuello [66] pointed out the importance of social companies as a different model to run a company involving stakeholders. On the other hand, Sajardo and Chaves [67] showed that the social economy companies of the Valencia region in Spain are more responsible than any other type of companies. Sanchis and Rodríguez [68] specified the CSR actions carried out in cooperative banking in Spain. In the case of agro-food cooperatives, it is worth stressing the work of Hernández-Perlines [69], who analysed the positive mediating effect of CSR on the relationship between entrepreneurship and performance in 112 Spanish agro-food cooperatives. Pérez-Sanz et al. [25] conducted a case study of agro-food cooperatives in Spain and showed the influence of CSR on their economic outcomes. Finally, López and Zavala [39] analysed the application of CSR in a Mexican agricultural manufacturing cooperative.

From all of the above, the first research question is: Does the CSR affect the performance of agro-food cooperatives?

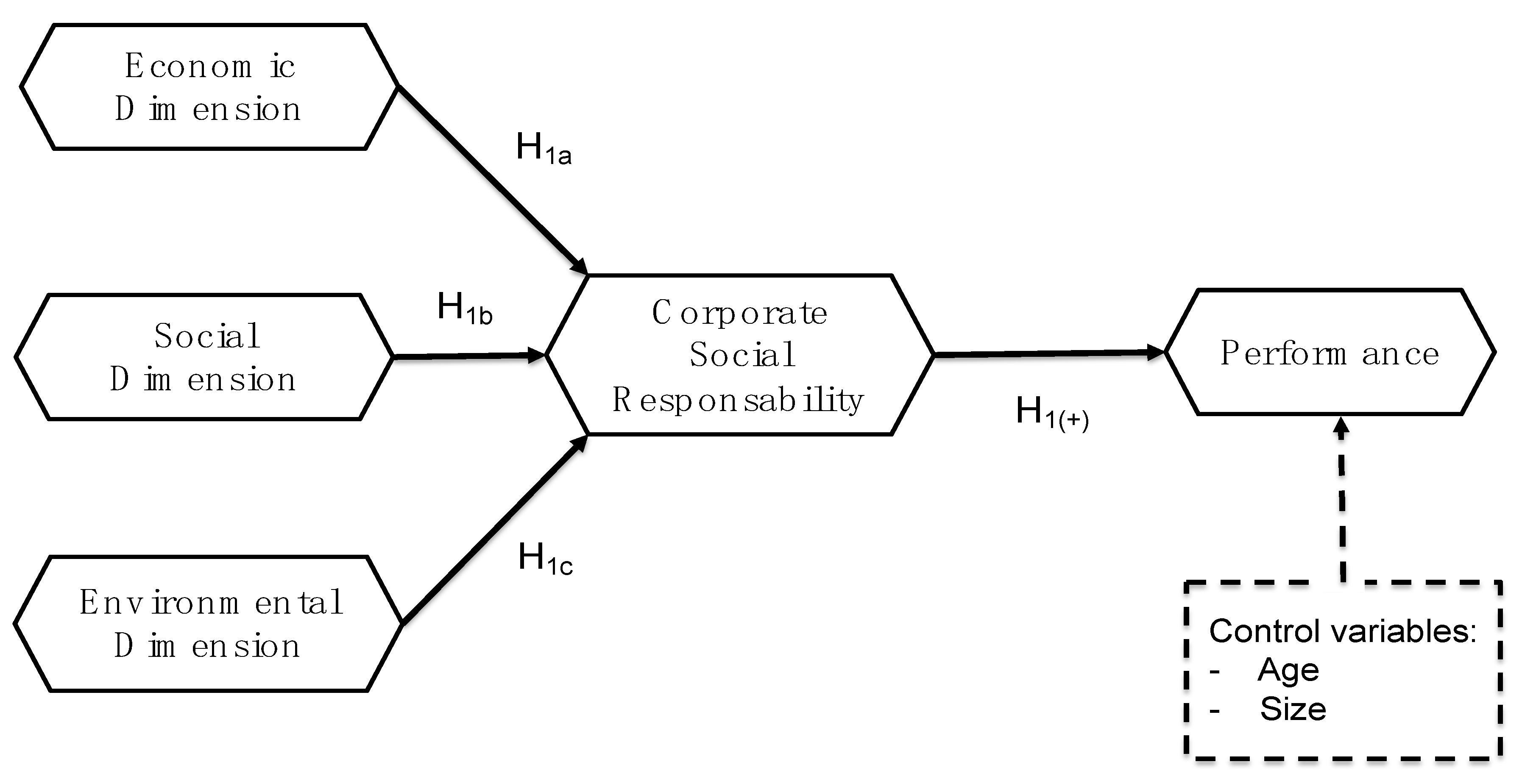

Hypothesis 1.

The CSR, in its triple economic, social, and environmental dimension, positively affects the performance of agro-food cooperatives.

As this research has established CSR to be made up of three dimensions (economic, social, and environmental dimensions), the first hypothesis can be broken down into the following three sub-hypotheses:

Hypothesis 1a.

The economic dimension of the CSR positively affects the performance of agro-food cooperatives.

Hypothesis 1b.

The social dimension of the CSR positively affects the performance of agro-food cooperatives.

Hypothesis 1c.

The environmental dimension of the CSR positively affects the performance of agro-food cooperatives.

3. Materials and Methods

3.1. Model Proposed

Based on the literature review and the specified research objectives, the proposed research model is shown in Figure 1.

3.2. Questionnaire

Given that the majority of agro-food cooperatives in Castilla-La Mancha do not have sustainability reports, it was decided to send a questionnaire to obtain the necessary information to develop and validate the proposed model. The questionnaire contained the following sections: (1) The first block was designed to collect general data on the agri-food cooperatives, (2) the second block contained questions on CSR, with three sub-sections: One for questions on the economic dimension of CRS, another sub-section for questions on the social dimension of CSR, and finally, a third sub-section for questions on the environmental dimension. The questions in this second block are those contained in the GRI-4 document [70]. However, in this case, instead of asking for absolute values of the different dimensions, a reply was requested according to the Likert scale (1—strongly disagree; 5—strongly agree). Finally, the third block was dedicated to questions about the performance of the agro-food cooperative. Also, in this third block, they were asked to answer according to a Likert scale (1—strongly disagree; 5—strongly agree). The use of a Likert scale is based on the fact that it is one of the most widely used scales in social science research [71].

3.3. Data

This study is set to examine if CSR actions carried out by agro-food cooperatives translate into an improvement in their performance. As CSR actions usually translate into value generation, it would be reasonable to think that they also translate into a sustainable growth in agro-food cooperatives. To answer this question, this research will use the CSR data of the agro-food cooperatives associated with “agro-Food cooperatives of Castilla-La Mancha”. This association comprises of 447 agro-food cooperatives from Castilla-La Mancha, with a total of 145,000 members and a turnover of 1500 million euros in 2019. The association brings together agro-food cooperatives from very different sectors such as wine, oil, arable crops, garlic, melon and watermelon, stone fruits, vegetables, mushrooms and fungi, livestock, organic production, credit production, etc.

A questionnaire was sent by email to the Presidents of agro-food cooperatives of Castilla-La Mancha, through Google forms. The email was sent to the Presidents’ e-mails and the responses were followed up. The email was accompanied by a letter with the objectives of the investigation. Once data collection was completed, which took from January to June 2019, valid information was obtained from 92 agro-food cooperatives (see Table 2).

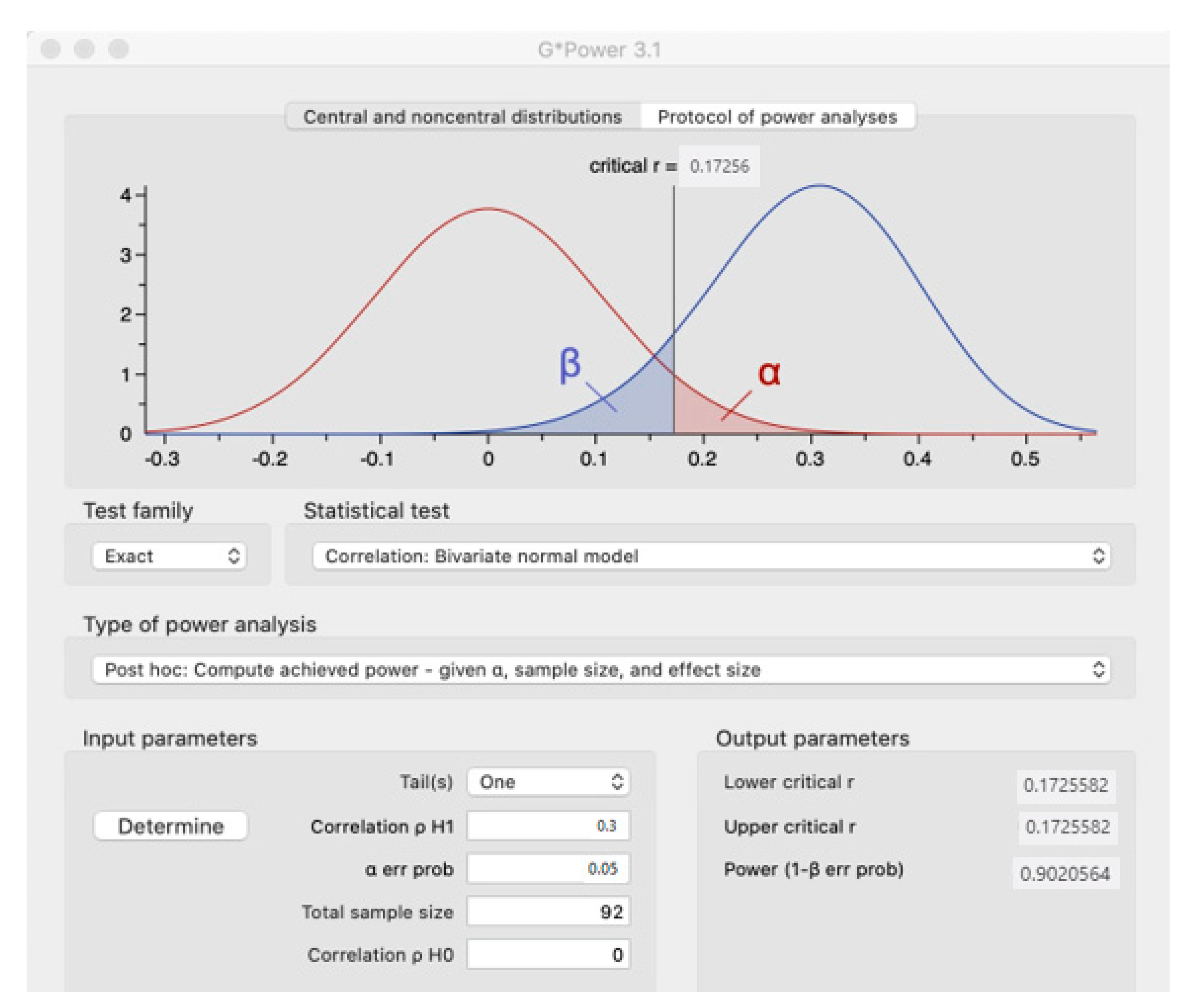

The statistical power of the sample was analysed using a Cohen’s retrospective test [72], through the G* Power 3.1.9.2 programme [73]. In this case, a value of 0.9020 was obtained (see Figure 2), which is higher than the limit of 0.80 established by Cohen [69].

Although some authors recommend samples greater than 100 [74], other authors state that the sample size should be calculated according to the level of relationships between the variables [75] (Marcoulides and Saunders (2006). In our case, there are four relationships and these authors specify that the minimum sample size for optimal results would be 65 [75]. Moreover, this size must be combined with the value of the statistical power, which in our case is 0.9020.

The agro-food cooperatives that have participated in this research have some of the following characteristics:

- (a)

- Age of the agro-food cooperatives—Most of the agro-food cooperatives were constituted in the 1950s, therefore they are more than 70 years old. Only 14.13% have been created in the 21st century (see Table 3).

- (b)

- Number of members of the agro-food cooperatives—most of the agro-food cooperatives in the sample have 300 or fewer members (see Table 4).

- (c)

- Number of employees of the agro-food cooperatives—most of the agro-food cooperatives are small and have less than 9 workers (see Table 5).

- (d)

- Destination of the agro-food cooperatives’ sales—most of the agro-food cooperatives sell their products in Europe (see Table 6).

- (e)

- Gender of the Presidents of the agro-food cooperatives—the vast majority of the Presidents of the agro-food cooperatives in the sample are men, at 93.47%. This is because most of the members of these cooperatives are men (see Table 7).

- (f)

- Age of the Presidents of the agro-food cooperatives—most of the presidents of the agro-food cooperatives in the sample are between 40 and 59 years old (see Table 8).

- (g)

- Level of studies of the Presidents of the agro-food cooperatives—the level of studies of the Presidents of the agro-food cooperatives in the sample is polarized between primary education (majority) and university education (see Table 9)

3.4. Measures of Variables

3.4.1. CSR

It is not easy to establish a measure for CSR. In this paper, we will establish a measure of CSR from the literature review. To do so, we have taken as our starting point the so-called sustainability indices, which both Griffin and Mahon [76] and Margolis and Walsh [77] believe best reflect the company’s responsible performance in relation to its economic and financial results. In this paper, we have opted for the indicators of the GRI (Global Reporting Initiative) Sustainability Reports, which allow the effects of different indexes to be combined with the data from a questionnaire in its Social Report format [78] and which also allows comparisons to be made between different companies. We have considered the CSR as a three-dimensional construct: Economic, social, and environmental. This is what has come to be known as the triple bottom line (TBL) [51,79,80]. This is the model used by the GRI. This type of measure has been used in previous studies such as those by Bansal [81], Epstein et al. [82], Chow and Chen [83], Gallardo-Vázquez et al. [84], Hernández-Perlines, and Rung-Hoch [85]. The difference between this paper and previous ones is that instead of using absolute values of the different indicators in this paper we use subjective measures based on the Likert-type scale (1—strongly disagree; 5—strongly agree).

3.4.2. Performance

In order to measure performance, 4 items were used based on the scale suggested by many authors [86,87,88,89,90]. In particular, a subjective assessment of profit, sales, market share, and return on capital has been used as a measure of performance. This is a subjective Likert-type scale (1—strongly disagree; 5—strongly agree).

3.4.3. Control Variables

Size and age were used as control variables, following recommendations by Chisman et al. [91].

4. Results

In order to test the hypotheses and analyse the results, the study used the multivariate statistical technique of partial least square (PLS) structural equations. This method was selected because it allows to make predictions based on the questions asked [92,93]. It also allows to observe different causal relationships between variables [94], making it unnecessary to make assumptions about the distribution of the sample [95] or its size [96]. Moreover, following Henseler [97], the model of this study is explanatory, as it sets out to examine how performance of agro-food cooperatives can be explained from the CSR actions they take. The software used was ADANCO 2.1 [98].

Before analysing the measurement model, a confirmatory analysis of the items was carried out in order to reduce their number. Such analysis only used items with a factor load greater than 0.7. Results are shown in Table 10.

Before presenting the most important results of the analysis of the measurement model and the structural model, it is convenient to present the values of the descriptive statistics. Table 11 shows the mean and standard deviation values of the economic, social, and environmental dimensions, the CSR, and the performance.

Once the items are “cleaned”, the reliability of the composite is analysed. The analysis involves composite reliability, Cronbach’s alpha, and the average variance extracted (AVE), to check the reliability of the composites. All the composites used in the study (CSR, Economic Dimension, Social Dimension, Environmental Dimension, and Performance) are type A composites.

Hair et al. [99] established the appropriate thresholds for composite reliability, Cronbach’s alpha, and the AVE. Table 12 shows that these values exceed the aforementioned thresholds (0.7 for composite reliability, 0.7 for Cronbach’s alpha, and 0.5 for AVE [99]).

In addition to reliability, discriminant validity was calculated, which measures the difference between the composites. AVE square root values for each composite were contrasted against their correlations [100]. As shown in Table 13, the AVE square root values for all composites were greater than the correlations between them. Therefore, discriminant validity is met according to Fornell and Larcker [101].

According to Henseler et al. [96], another criterion to analyse discriminant validity is the heterotrait–monotrait ratio of correlations (HTMT). This ratio allows calculating the discriminant validity between indicators of the same compound and between indicators of different compounds. Discriminant validity is met if the HTMT value is below 0.85 [96]. This is the case, as shown in Table 14.

Finally, Henseler et al. [96] established a third criterion to analyse discriminant validity. It is known as the HTMTinference and is calculated from a bootstrapping of 5000 subsamples. Discriminant validity is met if the resulting interval values are below 1. As shown in Table 15, this criterion is also useful to meet discriminant validity.

As shown above, the model suggested in this research has composites with adequate values of reliability as well as convergent and discriminant validity, as they exceed the thresholds established in the literature for the different criteria.

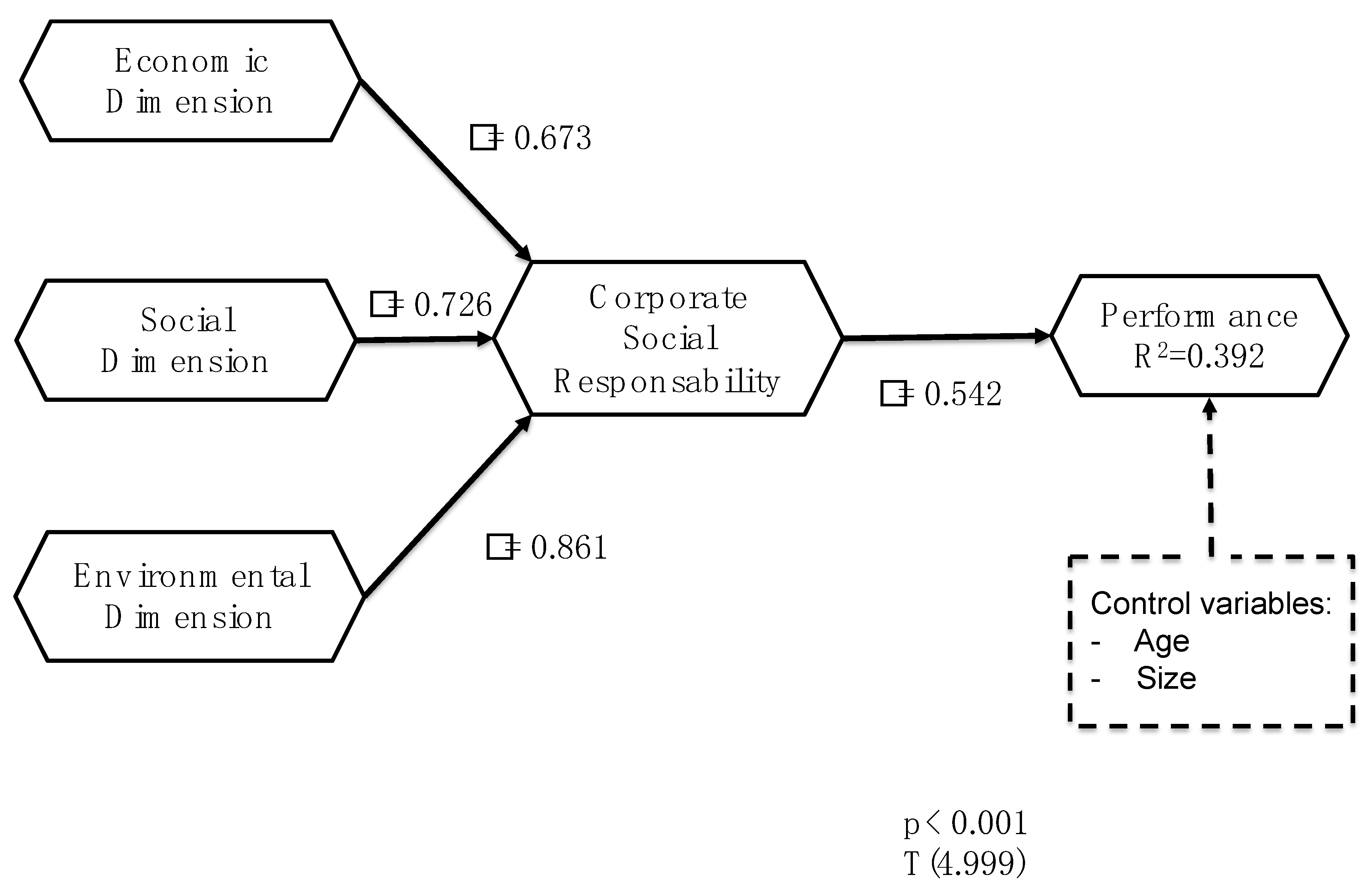

Once the composites have proven to have adequate values of reliability and convergent and discriminant validity, the research hypotheses can be checked. The first hypothesis was that CSR positively affects the performance of agro-food cooperatives. This hypothesis is met, as the path coefficient is 0.542, hence higher than the minimum threshold established by Chin in [102]. Furthermore, the influence is significant for a p < 0.001, since the value of t is 5.431, based on a bootstrapping for a one-tailed t (4.999). CSR can explain 39.2% of the variance in Performance of agro-food cooperatives (see Table 16 and Figure 3).

The three CSR dimensions have positive path coefficients and are above the thresholds established by Chin [102], so they positively affect the performance of agro-food cooperatives. Of the three dimensions, the one with the greatest effect on the performance of agro-food cooperatives is the environmental dimension.

5. Discussion and Conclusions

The aim of this paper is to analyse the influence of CSR on the performance of agro-food cooperatives in Castilla-La Mancha. To do this, we used a questionnaire based on the GRI model [70]. The main difference between the questionnaire used in this research and that of the GRI is that in our case, the questions were asked following a Likert scale (1—strongly disagree; 5—strongly agree) in order to find out the opinion of the Presidents of the Governing Councils of the agri-food cooperatives. The Likert scales have been widely used in social science research work [71]. Precisely, the use of the Likert scale is one of the fundamental differences with respect to previous works, such as that of Hernández-Perlines [69], which also analyses the CSR in agri-food cooperatives (The present paper analyses the direct effect of CSR on the performance of agri-food cooperatives in Castilla-La Mancha, while the paper by Hernández-Perlines [69] analyses the mediating effect of CSR on the influence of entrepreneurial orientation on agri-food cooperatives in Spain. Castilla-La Mancha is a region of Spain).

The choice of the research topic was motivated by the existence of an intense debate on the CSR, which is not unrelated to the Social Economy in general or to agro-food cooperatives in particular. CSR is not new to cooperatives: Cooperative values are largely in line with CSR principles [25,29]. The European Commission’s Green Paper, considered to be the reference for CSR in the Social Economy, states that cooperatives have a long tradition of combining economic viability and CSR, thanks to a constant dialogue between stakeholders through participatory management [34,35,36]. Following this argument, our objective was not only to analyse the CSR itself, but also to check whether the CSR actions adopted by the agro-food cooperatives positively affect their performance and thus verify that they achieve both the CSR objective and the value generation objective.

The cooperative model has become a benchmark that is being replicated by other types of companies [25]. In this sense, the Follow-up Commission of the Luxembourg Declaration [4] and even the United Nations itself have come to affirm that Social Economy entities are called upon to play a fundamental role in the future [6].

One might ask whether CSR is an aspect that falls within the very definition of a cooperative, in our research, agri-food. That is, if the cooperative model, which is made concrete in the cooperative values specified by the International Cooperative Alliance in 2007, among which we highlight mutual aid, responsibility, democracy, equality, equity, and solidarity, falls by its own definition within the scope of the CSR [43]. That is, if by the fact of being a cooperative they are already responsible. Or if, on the contrary, we can analyse the CSR on the basis of the GRI [70] and the triple bottom line [51] model and determine whether agro-food cooperatives are in fact responsible. This choice for measuring CSR is justified for three reasons: (1) It allows the integration of economic, social, and environmental aspects [52]; (2) it links CSR to sustainable development, which requires the convergence of economic development, social equity, and environmental protection [53]; and (3) it highlights the externalities of the company [54]. Moreover, this model makes it possible to focus the analysis of CSR from the perspective of the parties involved [23,24], favouring sustainable development, minimising the negative effects caused by certain undesirable behaviour [6], while improving the immediate environment without forgetting concern for social aspects [7].

In our case, the analysis of the results confirms that agro-food cooperatives in Castilla-La Mancha carry out CSR actions in the three dimensions previously mentioned: The economic dimension, the social dimension, and the environmental dimension. The model proposed in this work presents adequate values of reliability and validity. In addition, the three dimensions of the CSR present positive path coefficient values, higher than 0.2 established by Chin [102], as a minimum value and significant for a p < 0.001 based on a bootstrapping for a one-tailed t (4999). The economic dimension has a ß of 0.673, the social dimension a ß of 0.726, and the environmental dimension a ß of 0.861. In our study, the environmental dimension is the most relevant in the CSR. This result is similar to that obtained by Hernández-Perlines [69] for agro-food cooperatives of different geographical scope and with a different way of measuring the three dimensions of CSR considered. The consideration of the three dimensions as elements that make up the CSR has also been recognized by Hernández-Perlines [60,61] for family businesses in Spain and Mexico. In the latter cases, the effect of each dimension on the CSR changes in relation to the present work. In short, we can say that the cooperative model can be defined as a model of "good practice" when considering economic, social, and environmental aspects [41].

The CSR was operated as a second-order type composite to evaluate the economic, social, and environmental actions carried out by agro-food cooperatives. This way of analysing the CSR has already been used in previous works [54,56] and is also suitable for analysing the CSR in agro-food cooperatives, since it presents adequate reliability and validity values.

Once the CSR and its dimensions have been analysed, the next step was to check whether the CSR has a positive influence on the performance of agro-food cooperatives. The model confirms that CSR has a positive and significant influence on the performance of agri-food cooperatives (ß of 0.542 and a t-value of 5.431 for a bootstrapping of 5000 subsamples and one tail). This result is consistent with previous studies using different forms of performance measurement [71] and for other types of companies [60,61]. This result confirms that agro-food cooperatives have incorporated CSR into their management processes [44,49], improving their competitiveness [6] by taking into account the economic and social [46] stakeholders [47].

With this work, we meet the objectives initially established and it allows us to answer the various research questions raised. Firstly, it has been verified that agro-food cooperatives carry out CSR actions beyond their formal definition of cooperatives, which would already include them within the scope of CSR. In fact, agro-food cooperatives develop CSR actions that result in improved performance, being able to explain 39.2% of their variance. With regard to the type of CSR actions, this study confirms that agro-food cooperatives carry out economic, social, and environmental actions, the latter being the most relevant. All of them have a positive influence on the performance of agri-food cooperatives. We can say that the growth of agro-food cooperatives can be qualified as sustainable growth because it is a consequence of the effect of the CSR.

The first conclusion of this research is that it confirms that the measurement of the CSR from the model proposed by the GRI [70] using, in this case, Likert scales is also suitable for agro-food cooperatives, since all the indicators show adequate values of reliability and validity (convergent and discriminant). The model has adequate levels of goodness of fit [96] for this form of CSR measurement, as has been done in previous studies on agro-food cooperatives [69] and other types of companies [60,61]. Therefore, it is confirmed that the use of different methodologies to measure the CSR generates the same result, which makes it possible to state that the GRI model is suitable for measuring the CSR independently of the values (absolute or Likert scale) used for its measurement.

The second conclusion is that, as the GRI model specifies, in agri-food cooperatives too, CSR is made up of three dimensions: The economic dimension, the social dimension, and the environmental dimension. In addition, the environmental dimension is the most relevant. This conclusion, in its twofold condition, coincides with previous studies for agro-food cooperatives operating in a wider geographical area [69]. This greater concern for the environment in agro-food cooperatives is logical given the strong relationship of this type of enterprise with sustainable development [6].

The third conclusion is that CSR positively affects the performance of agro-food cooperatives. This result confirms that the CSR of agri-food cooperatives is not only in their own definition, as part of their cooperative DNA, but that agri-food cooperatives apply CSR in reality in order to improve their performance. In short, agro-food cooperatives are gradually incorporating CSR into their management processes [44] in order to improve their levels of competitiveness [6] through a combination of economic, social and environmental actions [41].

Author Contributions

All authors have made substantial, direct and intellectual contributions to the work and approval of this article for publication. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Acknowledgments

We are grateful for the collaboration of the agro-food cooperatives of Castilla-La Mancha and their Presidents who have provided us with information for this research.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Lu, W.; Chau, K.W.; Wang, H.; Pan, W. A decade’s debate on the nexus between corporate social and corporate financial performance: A critical review of empirical studies 2002–2011. J. Clean. Prod. 2014, 79, 195–206. [Google Scholar] [CrossRef] [Green Version]

- Lozano, R.; Carpenter, A.; Huisingh, D. A review of ‘theories of the firm’ and their contributions to Corporate Sustainability. J. Clean. Prod. 2015, 106, 430–442. [Google Scholar] [CrossRef]

- Herrera-Madueño, J.; Larrán-Jorge, M.; Martínez-Conesa, I.; Martínez-Martínez, D. Relationship between corporate social responsibility and competitive performance in Spanish SMEs: Empirical evidence from a stakeholders’ perspective. Bus. Res. Q. 2016, 19, 55–72. [Google Scholar] [CrossRef] [Green Version]

- Expansión. Díaz Destaca el Papel de la Economía Social Para la Recuperación Tras el Coronavirus. Available online: https://www.expansion.com/agencia/europa_press/2020/05/28/20200528163616.html (accessed on 28 May 2020).

- Mozas, A. Contribución de las Cooperativas Agrarias al Cumplimiento de los Objetivos de Desarrollo Sostenible; Especial Referencia al Sector Oleícola; Ciriec-España: Valencia, Spain, 2019. [Google Scholar]

- Arcas-Larios, N.; Briones-Peñalver, A.J. Responsabilidad Social Empresarial de las Organizaciones de la Economía Social. Valoración de la misma en las empresas de la Región de Murcia. CIRIEC-España Rev. Econ. Pública Soc. Coop. 2009, 65, 143–161. [Google Scholar]

- Comisión de las Comunidades Europeas. Libro Verde Sobre Responsabilidad Social de las Empresas; Comisión Europea: Bruselas, France, 2001. [Google Scholar]

- Ministerio de Trabajo y Asuntos Sociales. Informe del foro de Expertos en Responsabilidad Social de la Empresas. 2007. Available online: http://www.mtas.es/es/empleo/economiasoc/RespoSocEmpresas/docs/INFORME_FOROEXPERTOS_RSE.pdf (accessed on 4 May 2020).

- Escalonilla-Solano, S.; Plaza-Casado, P.; Ureba, S.F. Análisis de la divulgación de la información sobre la responsabilidad social corporativa en las empresas de transporte público urbano en España. Revista de Contabilidad 2016, 19, 195–203. [Google Scholar] [CrossRef] [Green Version]

- Porter, M.E.; Kramer, M.R. Strategy and Society: The Link between Competitive Advantage and Corporate Social Responsibility. Harv. Bus. Rev. 2006, 84, 78–92. [Google Scholar] [PubMed]

- Boccia, F.; Sarnacchiaro, P. The impact of corporate social responsibility on consumer preference: A structural equation analysis. Corp. Soc. Responsib. Environ. Manag. 2018, 25, 151–163. [Google Scholar] [CrossRef]

- Poon, J.M.; Ainuddin, R.A.; Junit, S.O.H. Effects of self-concept traits and entrepreneurial orientation on firm performance. Int. Small Bus. J. 2006, 24, 61–82. [Google Scholar] [CrossRef]

- Carroll, A.B. A three-dimensional conceptual model of corporate performance. Acad. Manag. Rev. 1979, 4, 497–505. [Google Scholar] [CrossRef] [Green Version]

- World Economic Forum. Global Compact of Shared Values and Principles. 1999. Available online: https://widgets.weforum.org/history/1999.html (accessed on 4 May 2020).

- Naciones Unidas. Documentos Final de la Cumbre Mundial de Nueva York. 2005. Available online: https://www.un.org/spanish/summit2005/fact_sheet.html (accessed on 4 May 2020).

- De Castro, M. La responsabilidad social de la empresa, o un nuevo concepto de empresa. CIRIEC-España Rev. Econ. Pública Soc. Coop. 2005, 53, 29–51. [Google Scholar]

- Bigné, E.; Chumpitaz, R.; Andreu, L.; Swaen, V. Percepción de la responsabilidad social corporativa: Un análisis cross-cultural. Universia Bus. Rev. 2005, 1, 14–26. [Google Scholar]

- Claver, E.; López, M.D.; Molina, J.F.; Zaragoza, P. La integración del capital medioambiental en el capital intelectual de la empresa. Rev. Econ. Empresa 2004, 50, 11–28. [Google Scholar]

- Fraj, E.; Martínez, E. El nivel de conocimiento medioambiental como factor moderador de la relación entre la actitud y el comportamiento ecológico. Investig. Eur. Dir. Econ. Empresa 2005, 11, 223–243. [Google Scholar]

- Friedman, M. Capitalismo y Libertad; University of Chicago Press: Chicago, IL, USA, 1962. [Google Scholar]

- Friedman, M. The Social Responsibility of Business is to Increase its Profits. In Corporate Ethics and Corporate Governance; Springer: Berlin/Heidelberg, Germany, 2007; pp. 173–178. [Google Scholar]

- Hart, S.L. A natural resource based view of the firm. Acad. Manag. Rev. 1995, 20, 874–907. [Google Scholar] [CrossRef] [Green Version]

- Martínez, R.; Martínez, D. Perspectivas de la sustentabilidad: Teoría y campos de análisis. Pensam. Actual 2016, 16, 123–145. [Google Scholar] [CrossRef] [Green Version]

- Vergara, C.A.; Ortíz, D. Desarrollo sostenible: Enfoques desde las ciencias económicas. Apunt. Cene 2016, 35, 15–52. [Google Scholar] [CrossRef] [Green Version]

- Pérez-Sanz, F.J.; Gargallo-Castel, A.F.; Esteban-Salvador, M.L. Prácticas de RSE en cooperativas. Experiencias y resultados mediante el estudio de casos. CIRIEC-España Rev. Econ. Pública Soc. Coop. 2019, 97, 137–178. [Google Scholar]

- Carrasco, I. La ética como eficiencia: La responsabilidad social en las cooperativas de crédito Españolas. CIRIEC-España Rev. Econ. Pública Soc. Coop. 2005, 53, 351–367. [Google Scholar]

- Melián, A. Una Aproximación a los Instrumentos de Medición de la Responsabilidad Social Empresarial (RSE) en las Cooperativas de crédito. In Proceedings of the XI Jornadas de Investigadores de Economía Social y Cooperativa Santiago de Compostela: CIRIEC-España y CECOOP, Santiago de Compostela, Spain, 25–27 October 2006. [Google Scholar]

- Barrera, J.J. Transparencia y reputación como actitud y forma de ser de la empresa. CIRIEC-España Rev. Econ. Pública Soc. Coop. 2016, 87, 327–350. [Google Scholar] [CrossRef]

- Mozas, A.; Puentes, R. La responsabilidad social corporativa y su paralelismo con las sociedades cooperativas. Rev. Estud. Coop. 2010, 103, 75–100. [Google Scholar]

- Aragón, C.; Iturrioz, C.; Narvaiza, L. Cooperatives’ proactive social responsibility in crisis time: How to behave? Rev. Estud. Coop. 2017, 123, 7–36. [Google Scholar]

- Hernández Perlines, F. Análisis estratégico de las cooperativas agrarias de Castilla-La Mancha. CIRIEC-España Rev. Econ. Pública Soc. Coop. 1994, 16, 187–208. [Google Scholar]

- Ceballo Sierra, A.I. Responsabilidad social: Un valor añadido para las empresas, un criterio de discriminación positiva para los consumidores. CIRIEC-España Rev. Econ. Pública Soc. Coop. 2005, 53, 65–77. [Google Scholar]

- International Co-Operative Alliance. Statement on the Co-Operative Identity. 2007. Available online: http://www.ica.coop/coop/principles.html (accessed on 4 May 2020).

- Pérez, F.J.; Gargallo, A. Gestión, desarrollo y aplicación de la responsabilidad social en entidades de economía social: El caso de las cooperativas. CIRIEC-España Rev. Econ. Pública Soc. Coop. 2005, 53, 305–332. [Google Scholar]

- Rodríguez, M. La responsabilidad social empresarial y los consumidores. CIRIEC-España Rev. Econ. Pública Soc. Coop. 2005, 53, 97–109. [Google Scholar]

- Server, R.J.; Villalonga, I. La Responsabilidad Social Corporativa y su gestión integrada. CIRIEC-España Rev. Econ. Pública Soc. Coop. 2005, 53, 137–161. [Google Scholar]

- Server, R.; Capó, J. La responsabilidad empresarial en un contexto de crisis. Repercusión en las sociedades cooperativas. CIRIEC-España Rev. Econ. Pública Soc. Coop. 2009, 65, 7–31. [Google Scholar]

- Chaves, R. La economía social como enfoque metodológico, como objeto de estudio y como disciplina científica. CIRIEC-España Rev. Econ. Pública Soc. Coop. 1999, 33, 115–139. [Google Scholar]

- López, V.; Zavala, B. La responsabilidad social en las dimensiones de la ciudadanía corporativa. Un estudio de caso en la manufactura agrícola. CIRIEC-España Rev. Econ. Pública Soc. Coop. 2019, 97, 179–211. [Google Scholar]

- Mozas, A.; Bernal, E. Desarrollo territorial y economía social. CIRIEC-España Rev. Econ. Pública Soc. Coop. 2006, 55, 125–140. [Google Scholar]

- Vargas, A.; Vaca, R. Responsabilidad social y cooperativismo: Vínculos y potencialidades. CIRIEC-España Rev. Econ. Pública Soc. Coop. 2005, 53, 241–260. [Google Scholar]

- BOE. Ley 11/2010. de 4 de Noviembre, de Cooperativas de Castilla-La Mancha. Available online: https://www.boe.es/buscar/pdf/2011/BOE-A-2011-2707-consolidado.pdf (accessed on 5 May 2020).

- Gallardo, D.; Castilla, F. Modelo de gestión para la responsabilidad social en cooperativas. Econ. Ind. 2015, 396, 139–149. [Google Scholar]

- Morales, A.C. Modas de gestión en el siglo XX y modelo cooperativo: Convergencias implícitas hacia una empresa de alto rendimiento. CIRIEC-España Rev. Econ. Pública Soc. Coop. 2006, 56, 161–186. [Google Scholar]

- Gaytán, M.; Flores, C. Factores determinantes en la adopción de prácticas de responsabilidad social empresarial: Un análisis sectorial en las franquicias mexicanas. AD Minist. 2018, 33, 21–38. [Google Scholar]

- López, A.; Marcuello, C. Agricultural cooperatives and economic efficiency. New Medit. 2006, 3, 119–122. [Google Scholar]

- Grimaldos, M. El impulso de la responsabilidad social de la empresa en las entidades de economía social: Los deberes de los administradores de las sociedades laborales como caso paradigmático. CIRIEC-España Rev. Econ. Pública Soc. Coop. 2018, 33, 1–31. [Google Scholar]

- Domínguez, M. El Aspecto Jurídico-Práctico de la Responsabilidad Social Empresarial: Global (SALCAI-UTINSA) Transportes Interurbano de Gran Canaria. In Proceedings of the XVII Congreso Internacional de Investigadores en Economía Social y Cooperativa de CIRIEC-España, Toledo, España, 4–5 October 2018. [Google Scholar]

- Marín, S.; De La Villa, D.; Calvo-Flores, A. Empresas y auditores ante el medio ambiente: Un reto que afrontar. Rev. Econ. Empresa 2004, 50, 29–60. [Google Scholar]

- De La Cuesta, M.; Valor, C.V. Responsabilidad social de la empresa. Concepto, medición y desarrollo en España. Boletín ICE Económico 2003, 2755, 7–19. [Google Scholar]

- Elkington, J. Towards the Sustainable Corporation: Win-Win-Win Business Strategies for Sustainable Development. Calif. Manag. Rev. 1994, 36, 90–100. [Google Scholar] [CrossRef]

- Portales, L.; García, C.; Yepez, G. Evolución de la responsabilidad social empresarial: Surgimiento, definición y proliferación global. In Responsabilidad, Ética y Sostenibilidad Empresarial; Raufflet, E., Portales, L., García, C., Lozano, J., Barrera, E., Eds.; Pearson: Ciudad de México, México, 2017; pp. 1–14. [Google Scholar]

- Mikušová, M. To be or not to be a business responsible for sustainable development? Survey from small Czech businesses. Econ. Res. Ekon. Istraž. 2017, 30, 1318–1338. [Google Scholar] [CrossRef] [Green Version]

- Hussain, N.; Rigoni, U.; Orij, R. Corporate Governance and Sustainability Performance: Analysis of Triple Bottom Line Performance. J. Bus. Ethics 2018, 149, 411–432. [Google Scholar] [CrossRef]

- Preston, L.E.; O’bannon, D.P. The corporate socialfinancial performance relationship: A typology and analysis. Bus. Soc. 1997, 36, 419–429. [Google Scholar] [CrossRef]

- Alvarado Herrera, A.; Bigné Alcañiz, E.; Currás Pérez, R. Theoretical perspectives for studying corporate social responsibility: A rationality-based classification. Estud. Gerenc. 2011, 27, 115–138. [Google Scholar]

- Miras-Rodríguez, M.; Carrasco-Gallego, A.; Escobar-Pérez, B. Are Socially Responsible Behaviors Paid Off Equally? A Cross-cultural Analysis. Corp. Soc. Responsib. Environ. Manag. 2015, 22, 237–256. [Google Scholar] [CrossRef]

- Gamerschlag, R.; Möller, K.; Verbeeten, F. Determinants of voluntary CSR disclosure: Empirical evidence from Germany. Rev. Manag. Sci. 2011, 5, 233–262. [Google Scholar] [CrossRef] [Green Version]

- Campopiano, G.; De Massis, A. Corporate social responsibility reporting: A content analysis in family and non-family firms. J. Bus. Ethics 2015, 129, 511–534. [Google Scholar] [CrossRef]

- Hernández-Perlines, F. Influencia de la responsabilidad social en el desempeño de las empresas familiares. J. Glob. Compet. Gov./Rev. Glob. Compet. Gob./Rev. Glob. Compet. Gov. 2017, 11, 58–73. [Google Scholar]

- Hernández-Perlines, F.; Ibarra Cisneros, M.A. Analysis of the moderating effect of entrepreneurial orientation on the influence of social responsibility on the performance of Mexican family companies. Cogent Bus. Manag. 2017, 4, 1408209. [Google Scholar] [CrossRef]

- Martín-Castejón, P.J.; Aroca-López, B. Corporate social responsibility in family SMEs: A comparative study. Eur. J. Fam. Bus. 2016, 6, 21–31. [Google Scholar] [CrossRef] [Green Version]

- Chen, L.; Feldmann, A.; Tang, O. The relationship between disclosures of corporate social performance and financial performance: Evidences from GRI reports in manufacturing industry. Int. J. Prod. Econ. 2015, 170, 445–456. [Google Scholar] [CrossRef]

- Li, F.; Li, T.; Minor, D. CEO power, corporate social responsibility, and firm value: A test of agency theory. Int. J. Manag. Financ. 2016, 12, 611–628. [Google Scholar] [CrossRef]

- Bazán, C.; De La Morena, J.; Cortés, H. Evolución y nuevas tendencias de responsabilidad social en las prácticas empresariales. Rev. Responsab. Soc. Empresa 2018, 29, 17–50. [Google Scholar]

- Monzón, J.L.; Marcuello, C. Economía Social y Empresas Sociales. CIRIEC-España Rev. Econ. Pública Soc. Coop. 2012, 35, 151–163. [Google Scholar]

- Sajardo Moreno, A.; Chaves Sajardo, R.J. Responsabilidad Social en las empresas de Economía Social: Un análisis comparativo del tejido productivo de la Comunidad Valenciana. Rev. Estud. Coop. 2017, 125, 213–242. [Google Scholar] [CrossRef] [Green Version]

- Sanchís-Palacio, J.R.; Rodríguez-Pérez, S. Responsabilidad social empresarial en banca. Su aplicación al caso de la banca cooperativa. Rev. Estud. Coop. 2018, 127, 204–227. [Google Scholar] [CrossRef] [Green Version]

- Hernández-Perlines, F. El efecto mediador de la RSE en la relación de la orientación emprendedora y el desempeño de las cooperativas agroalimentarias. CIRIEC-España Rev. Econ. Pública Soc. Coop. 2015, 85, 217–244. [Google Scholar]

- Global Reporting Initiative. Getting Started with the GRI Standards. 2020. Available online: https://www.globalreporting.org/standards/getting-started-with-the-gri-standards/ (accessed on 4 November 2018).

- Matas, A. Diseño del formato de escalas tipo Likert: Un estado de la cuestión. Rev. Electrón. Investig. Educ. 2018, 20, 38–47. [Google Scholar] [CrossRef]

- Cohen, B.; Winn, M.I. Market imperfections, opportunity and sustainable entrepreneurship. J. Bus. Ventur. 2007, 22, 29–49. [Google Scholar] [CrossRef]

- Faul, F.; Erdfelder, E.; Buchner, A.; Lang, A.G. Statistical power analyses using G* power 3.1: Tests for correlation and regression analyses. Behav. Res. Methods 2009, 41, 1149–1160. [Google Scholar] [CrossRef] [Green Version]

- Reinartz, W.; Haenlein, M.; Henseler, J. An empirical comparison of the efficacy of covariance-based and variance-based SEM. Int. J. Res. Mark. 2009, 26, 332–344. [Google Scholar] [CrossRef] [Green Version]

- Marcoulides, G.; Saunders, C. PLS: A silver bullet? Manag. Inf. Syst. Q. 2006, 30, 3–9. [Google Scholar] [CrossRef]

- Griffin, J.J.; Mahon, J.F. The Corporate Social Performance and Corporate Financial Performance Debate. Twentyfive Years Incomparable Res. Bus. Soc. 1997, 36, 5–31. [Google Scholar] [CrossRef]

- Margolis, J.D.; Walsh, J.P. Misery Loves Companies: Rethinking Social Initiatives by Business. Adm. Sci. Q. 2003, 48, 268–305. [Google Scholar] [CrossRef] [Green Version]

- Schadewith, H.; Niskala, M. Communication via Responsibility Reporting and its Effect on Firm Value in Finland. Corp. Soc. Responsib. Environ. Manag. 2010, 17, 96–106. [Google Scholar]

- Elkington, J. Enter the Triple Bottom Line. In The Triple Bottom Line, Does It All Add up? Assessing the Sustainability of Business and CSR; Henriques, A., Richardson, J., Eds.; Earthscan Publications Ltd.: London, UK, 2004; pp. 1–16. [Google Scholar]

- Chang, E.P.; Memili, E.; Chrisman, J.J.; Kellermanns, F.W.; Chua, J.H. Family social capital, venture preparedness, and start-up decisions: A study of Hispanic entrepreneurs in New England. Fam. Firm Rev. 2009, 22, 279–292. [Google Scholar] [CrossRef] [Green Version]

- Bansal, P. Evolving sustainably: A longitudinal study of corporate sustainable development. Strateg. Manag. J. 2005, 26, 197–218. [Google Scholar] [CrossRef]

- Epstein, M.J.; Buhovac, A.R.; Yuthas, K. Managing social, environmental and financial performance simultaneously. Long Range Plan. 2015, 48, 35–45. [Google Scholar] [CrossRef]

- Chow, W.S.; Chen, Y. Corporate sustainable development: Testing a new scale based on the mainland Chinese context. J. Bus. Ethics 2012, 105, 519–533. [Google Scholar] [CrossRef]

- Gallardo-Vázquez, D.; Sánchez-Hernández, M.I.; Corchuelo-Martinez-Azua, M.B. Validación de un instrumento de medida para la relación entre la orientación a la responsabilidad social corporativa y otras variables estratégicas de la empresa. Rev. Contab. 2013, 16, 11–23. [Google Scholar]

- Hernández-Perlines, F.; Rung-Hoch, N. Sustainable entrepreneurial orientation in family firms. Sustainability 2017, 9, 1212. [Google Scholar] [CrossRef] [Green Version]

- Wiklund, J.; Shepherd, D. Entrepreneurial orientation and small business performance: A configurational approach. J. Bus. Ventur. 2005, 20, 71–91. [Google Scholar] [CrossRef]

- Naldi, L.; Nordqvist, M.; Sjöberg, K.; Wiklund, J. Entrepreneurial orientation, risk taking, and performance in family firms. Fam. Firm Rev. 2007, 20, 33–47. [Google Scholar] [CrossRef]

- Chirico, F.; Sirmon, D.G.; Sciascia, S.; Mazzola, P. Resource orchestration in family firms: Investigating how entrepreneurial orientation, generational involvement, and participative strategy affect performance. Strateg. Entrep. J. 2011, 5, 307–326. [Google Scholar] [CrossRef] [Green Version]

- Kellermanns, F.W.; Eddleston, K.A.; Zellweger, T.M. Extending the socioemotional wealth perspective: A look at the dark side. Entrep. Theory Pract. 2012, 36, 1175–1182. [Google Scholar] [CrossRef]

- Kraus, S.; Rigtering, J.C.; Hughes, M.; Hosman, V. Entrepreneurial orientation and the business performance of SMEs: A quantitative study from the Netherlands. Rev. Manag. Sci. 2012, 6, 161–182. [Google Scholar] [CrossRef] [Green Version]

- Chrisman, J.J.; Chua, J.H.; Sharma, P. Trends and directions in the development of a strategic management theory of the family firm. Entrep. Theory Pract. 2005, 29, 555–576. [Google Scholar] [CrossRef]

- Hair, J.F.; Hult, G.T.M.; Ringle, C.M.; Sarstedt, M. A Primer on Partial Least Squares Structural Equation Modeling (PLS-SEM); Sage: Thousand Oaks, CA, USA, 2017. [Google Scholar]

- Sarstedt, M.; Ringle, C.M.; Smith, D.; Reams, R.; Hair, J.F., Jr. Partial least squares structural equation modeling (PLS-SEM): A useful tool for family firm researchers. J. Fam. Bus. Strategy 2014, 5, 105–115. [Google Scholar] [CrossRef]

- Astrachan, C.B.; Patel, V.K.; Wanzenried, G. A comparative study of CB-SEM and PLS-SEM for theory development in family firm research. J. Fam. Bus. Strategy 2014, 5, 116–128. [Google Scholar] [CrossRef]

- Henseler, J.; Ringle, C.M.; Sinkovics, R.R. The use of partial least squares path modeling in international marketing. Adv. Int. Mark. 2009, 20, 277–320. [Google Scholar]

- Henseler, J.; Ringle, C.M.; Sarstedt, M. A new criterion for assessing discriminant validity in variance-based structural equation modeling. J. Acad. Mark. Sci. 2015, 43, 115–135. [Google Scholar] [CrossRef] [Green Version]

- Henseler, J. Partial least squares path modeling: Quo vadis? Qual. Quant. 2018, 52, 1–8. [Google Scholar] [CrossRef] [Green Version]

- Henseler, J.; Dijkstra, T.K. ADANCO 2.1. Kleve: Composite Modeling. 2018. Available online: http://www.compositemodeling.com (accessed on 4 May 2020).

- Hair, J.F.; Risher, J.J.; Sarstedt, M.; Ringle, C.M. When to use and how to report the results of PLS-SEM. Eur. Bus. Rev. 2019, 31, 2–24. [Google Scholar] [CrossRef]

- Hair, J.F.; Hult, G.T.M.; Ringle, C.M.; Sarstedt, M.; Castillo Apraiz, J.; Cepeda Carrión, G.; Roldán, J.L. Manual de Partial Least Squares Structural Equation Modeling (pls-sem); OmniaScience Scholar: Spain, 2019. [Google Scholar]

- Fornell, C.; Larcker, D.F. Evaluating structural equation models with unobservable variables and measurement error. J. Mark. Res. 1981, 18, 39–50. [Google Scholar] [CrossRef]

- Chin, W.W. The partial least squares approach to structural equation modeling. Mod. Methods Bus. Res. 1998, 295, 295–336. [Google Scholar]

- Hu, L.T.; Bentler, P.M. Fit indices in covariance structure modeling: Sensitivity to under parameterized model misspecification. Psychol. Methods 1998, 3, 424. [Google Scholar] [CrossRef]

Figure 1.

Proposed research model.

Figure 2.

Sample statistical power.

Figure 3.

Structural model.

{kind=link}

{kind=link}

{kind=link}

Table 1.

Theoretical models for corporate social responsibility (CSR) analysis.

| Causal Sequence | Relationship Sign | ||

|---|---|---|---|

| Positive | Neutral | Negative | |

| CSR => ER | Social Impact Hypothesis | Moderating and/or mediating variables hypothesis | Trade-off hypothesis |

| ER => CSR | Funding Availability hypothesis | Managers’ Opportunistic hypothesis | |

| CSR <=> ER | Positive Synergy | Negative Synergy | |

Fuente: Preston y O’Bannon (1997). Note: CSR—Corporate Social Responsability; ER—Economic Results.

Table 2.

Fieldwork data sheet.

| Sample size | 447 |

| Scope of application | Castilla-La Mancha |

| Valid answers | 92 |

| Sample processing | Simple random |

| Confidence level | 95%, p = p = 50%; α = 0.05 |

| Response rate | 20.58% |

| Sampling error | 9.12% |

| Fieldwork | January–June 2019 |

Table 3.

Age of the agro-food cooperatives.

| Year of Constitution | Number | (%) |

|---|---|---|

| 1950–1960 | 30 | 32.60 |

| 1960–1970 | 24 | 26.08 |

| 1970–1980 | 6 | 6.52 |

| 1980–1990 | 11 | 11.95 |

| 1990–2000 | 8 | 8.69 |

| 2000– | 13 | 14.13 |

| Total | 92 | 100.00 |

Table 4.

Number of members of the agro-food cooperatives.

| Members | Number | (%) |

|---|---|---|

| 2 1–300 | 51 | 55.43 |

| 301–600 | 19 | 20.65 |

| 601–900 | 1 | 0.010 |

| 901– | 21 | 22.82 |

| Total | 92 | 100.00 |

Note: 1 The minimum number to create a cooperative in Castila-La Mancha is two members.

Table 5.

Number of employees of the agro-food cooperatives.

| Employees | Number | (%) |

|---|---|---|

| 1–9 | 56 | 60.86 |

| 10–49 | 22 | 23.91 |

| 49– | 14 | 15.23 |

| Total | 92 | 100.00 |

Table 6.

Destination of the agro-food cooperatives’ sales.

| Destination | Number | (%) |

|---|---|---|

| National | 35 | 38.04 |

| Europe | 48 | 52.17 |

| Worldwide | 9 | 9.79 |

| Total | 92 | 100.00 |

Table 7.

Gender of the Presidents of the agro-food cooperatives.

| Gender | Number | (%) |

|---|---|---|

| Male | 86 | 93.47 |

| Female | 6 | 6.53 |

| Total | 92 | 100.00 |

Table 8.

Age of the Presidents of the agro-food cooperatives.

| Age | Number | (%) |

|---|---|---|

| 20–39 | 9 | 9.78 |

| 40–59 | 62 | 67.39 |

| 60– | 21 | 22.83 |

| Total | 92 | 100.00 |

Table 9.

Level of studies of the Presidents of the agro-food cooperatives.

| Level of Studies | Number | (%) |

|---|---|---|

| Primary Education | 35 | 38.04 |

| Secondary Education | 24 | 26.08 |

| University Studies | 33 | 35.88 |

| Total | 92 | 100.00 |

Table 10.

Confirmatory item analysis.

| Dimension | Indicators | |

|---|---|---|

| CSR | Social Dimension | Main markets |

| Employees | ||

| Training and personnel expenses | ||

| Purchase value and non-monetary donations | ||

| Certifications and awards | ||

| Stakeholders and External Initiatives | ||

| Economic Dimension | Paid taxes | |

| Financial reserves and balance sheet provisions | ||

| Environmental Dimension | Energy consumption and environmental initiatives | |

| Use of recycled material | ||

| Recycled products |

Table 11.

Descriptive statistics.

| Composite | Mean | Typical Deviation |

|---|---|---|

| Economic Dimension | 3.97 | 0.96 |

| Social Dimension | 4.32 | 1.02 |

| Environmental dimension | 4.25 | 1.05 |

| CSR | 4.18 | 1.03 |

| Performance | 4.20 | 1.08 |

Table 12.

Composites and indicators.

| Composite | Composite Reliability | Cronbach’s Alpha | AVE a |

|---|---|---|---|

| CSR 1 | 0.863 | 0.824 | 0.758 |

| ED 2 | 0.913 | 0.844 | 0.710 |

| SD 3 | 0.885 | 0.863 | 0.747 |

| END 4 | 0.802 | 0.861 | 0.719 |

| P 5 | 0.895 | 0.849 | 0.628 |

Note: 1 Corporate Social Responsibility; 2 Economic Dimension; 3 Social Dimension; 4 Environmental Dimension; 5 Performance; a Average Variance Extracted.

Table 13.

Discriminant validity a.

| CSR 1 | ED 2 | SD 3 | END 4 | P 5 | |

|---|---|---|---|---|---|

| CSR 1 | 0.870 * | ||||

| ED 2 | 0.563 | 0.870 * | |||

| SD 3 | 0.671 | 0.612 | 0.842 * | ||

| END 4 | 0.685 | 0.674 | 0.693 | 0.864 * | |

| P 5 | 0.679 | 0.692 | 0.648 | 0.637 | 0.792 * |

Note: * AVE square roots are shown diagonally (in bold). a The values were calculated for the second- and third-order composites. 1 Corporate Social Responsibility; 2 Economic Dimension; 3 Social Dimension; 4 Environmental Dimension; 5 Performance.

Table 14.

Heterotrait–monotrait ratio of correlations (HTMT).

| CSR 1 | ED 2 | SD 3 | END 4 | P 5 | |

|---|---|---|---|---|---|

| CSR 1 | |||||

| ED 2 | 0.676 | ||||

| SD 3 | 0.784 | 0.743 | |||

| END 4 | 0.687 | 0.712 | 0.693 | ||

| P 5 | 0.610 | 0.636 | 0.702 | 0.698 |

Note: 1 Corporate Social Responsibility; 2 Economic Dimension; 3 Social Dimension; 4 Environmental Dimension; 5 Performance.

Table 15.

HTMTinference.

| Original Data (O) | Mean of Data (M) | 5.0% | 95.0% | Mean of Data (M) | Bias | 5.0% | 95.0% | |

|---|---|---|---|---|---|---|---|---|

| CSR 1 ED 2 | 0.707 | 0.707 | 0.707 | 0.707 | 0.707 | 0.707 | 0.707 | 0.707 |

| CSR 1 SD 3 | 0.726 | 0.726 | 0.726 | 0.726 | 0.726 | 0.726 | 0.726 | 0.726 |

| CSR 1 END 4 | 0.895 | 0.895 | 0.895 | 0.895 | 0.895 | 0.895 | 0.895 | 0.895 |

| CSR 4 P 5 | 0.872 | 0.872 | 0.872 | 0.872 | 0.872 | 0.872 | 0.872 | 0.872 |

Note: 1 Corporate Social Responsibility; 2 Economic Dimension; 3 Social Dimension; 4 Environmental Dimension; 5 Performance.

Table 16.

Structural model.

| Hypothesis | R2 | Β | t-Value | Support |

|---|---|---|---|---|

| CSR 1 P 5 | 0.392 | 0.542 | 5.431 | Yes |

| ED 2 P 5 | 0.673 | 4.974 | Yes | |

| SD 3 P 5 | 0.726 | 5.329 | Yes | |

| END 4 P 5 | 0.861 | 5.248 | Yes |

Note: 1 Corporate Social Responsibility; 2 Economic Dimension; 3 Social Dimension; 4 Environmental Dimension; 5 Performance.

Table 17.

Control variables.

| Variable | ß | t-Value |

|---|---|---|

| Age | 0.061 | 0.061 |

| Size | 0.073 | 0.073 |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Hernández-Perlines, F.; Ariza-Montes, A.; Araya-Castillo, L. Sustainable Growth in the Agro-Food Cooperatives of Castilla-La Mancha (Spain). Sustainability 2020, 12, 5045. https://doi.org/10.3390/su12125045

AMA Style

Hernández-Perlines F, Ariza-Montes A, Araya-Castillo L. Sustainable Growth in the Agro-Food Cooperatives of Castilla-La Mancha (Spain). Sustainability. 2020; 12(12):5045. https://doi.org/10.3390/su12125045

Chicago/Turabian StyleHernández-Perlines, Felipe, Antonio Ariza-Montes, and Luis Araya-Castillo. 2020. "Sustainable Growth in the Agro-Food Cooperatives of Castilla-La Mancha (Spain)" Sustainability 12, no. 12: 5045. https://doi.org/10.3390/su12125045

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.