Government R&D Subsidy and Additionality of Biotechnology Firms: The Case of the South Korean Biotechnology Industry

1

Department of Biomedical Convergence, College of Medicine, Chungbuk National University, 1 Chungdae-ro, Seowin-gu, Cheongju-si 28644, Korea

2

Management Research Center, Seoul National University, 1 Gwanak-ro, Gwanak-gu, Seoul 08826, Korea

3

Division of Data Analysis, Korea Institute of Science and Technology Information (KISTI), 66 Hoegi-ro, Dongdaemun-gu, Seoul 02456, Korea

4

Technology Innovation Group, SK Telecom, 65 Eulji-ro, Jung-gu, Seoul 04539, Korea

*

Author to whom correspondence should be addressed.

Sustainability 2019, 11(6), 1583; https://doi.org/10.3390/su11061583

Submission received: 2 January 2019

/

Revised: 3 March 2019

/

Accepted: 4 March 2019

/

Published: 15 March 2019

(This article belongs to the Section Economic and Business Aspects of Sustainability)

Abstract

:Government research and development (R&D) subsidies are more important in countries that are latecomers to the biotechnology industry, where venture capital has not been developed, and the ratio of start-ups is high. Previous studies have mostly focused on the additionality of the input and output through government R&D subsidies, such as private R&D investment, technological innovation, and financial performance. In addition, some studies have focused on the behavioral additionality (the change in a firm’s behavior) of firms through government R&D subsidies. However, each study is fragmented and does not provide integrated results and implications. Therefore, this study comprehensively investigated the effects of government R&D subsidies on the multifaceted aspects of input, output, and behavioral additionality based on data from South Korean biotechnology companies. This study used the propensity score matching (PSM) method to prevent selection bias. The results showed that firms benefiting from government R&D subsidies had a markedly higher R&D investment in terms of input additionality, and they produced more technological innovation within a shorter period in terms of output additionality, though financial performance was not determined. Moreover, government R&D subsidies have accelerated strategic alliances and suppressed external financing (debt financing) in terms of behavioral additionality.

1. Introduction

The biotechnology industry is considered to be an industry with a high possibility of market failure due to limitations in technological development and commercialization [1]. Guellec and van Pottelsberghe de la Potterie [2] provided justifications for government research and development (R&D) subsidies to biotechnology: (1) imperfect appropriability and (2) risks. In particular, Coriat [3] emphasized that the biotechnology industry is a representative of the science-based industry. Technology, by its nature, is a public good because an abundance of basic science knowledge is required in biotechnology [3], and this hinders the appropriability of technology [4]. With the spread of knowledge, the profit that a company obtains through research and development becomes less than the social profit; hence, the appropriate level of R&D activities required by society has not yet been attained in the biotechnology industry, such that imperfect appropriability causes market failure [5]. In addition, biotechnology R&D has fundamental uncertainty arising from the use of scientific knowledge, risks associated with various stages of the R&D process, the long development period, and money from the discovery of candidate substances in clinical trials. The high uncertainty and risk in biotechnology R&D leads to avoiding behavior by companies towards R&D investment. Therefore, government R&D subsidies in the biotechnology industry are a critical institutional supplement that can mitigate the market failure caused by imperfect appropriability and risks [6].

The effect of government R&D subsidies on firms can be evaluated not only on a company’s performance, but also on its input factors and behavioral (or strategic) changes. In general, the responses in input, output, and behavioral perspectives of a firm, when there is an intervention compared to when there is no intervention, are referred to as the “additionality” of a firm [7]. Therefore, if the intervention is government R&D support, then the input, output, and behavioral changes of the firm through government R&D support are the firm’s additionality through government R&D subsidies. Previous studies have focused on input additionality, such as whether government R&D support has increased firms’ private investment and generated a crowding-out effect, which means that government investment is replaced by private investment. In addition, previous studies also have focused on additionality in terms of the output from government R&D support, which is related to firm’s technological innovation performance or financial performance. Recently, companies’ strategic behaviors have become more important, and scholars have begun to pay attention to behavioral additionality through government R&D support. Behavioral additionality has been studied internally as a strategic renewal of the enterprise, such as functional renewal, internal investment expansion, and externally as strategic actions of the enterprise in cooperation or in competition for resources or capabilities, such as strategic alliances and external funding [8,9]. Nevertheless, previous studies are fragmented, and there is still a lack of research that comprehensively considers input, output, and behavioral additionality.

Therefore, this study examined the input, output, and behavioral additionality of biotechnology firms through government R&D subsidies. Specifically, the context of the study was its focus on: (1) the biotechnology industry and (2) latecomer countries to the industry. In this context, the study investigated the input, output, and behavioral additionality through government R&D support in the South Korean biotechnology industry, which is one of the latecomers to the biotechnology industry. Although the South Korean biotechnology industry has grown, led by the visible achievements of a few companies, the ratio of small companies in the industry with 50 or less employees stands at 58.6% (as of 2012). The government’s support to start-ups or small- and medium-sized enterprises is particularly important [10]. In addition, even among Organization for Economic Cooperation and Development (OECD) countries, South Korea is a leader in providing in government R&D subsidies. Furthermore, starting in 2005, the government announced an agenda targeting development of the biotechnology industry, and it has continuously increased R&D investment in the development of new drugs, stem cells, brain studies, genome studies, and next generation medical infrastructure sectors [11]. In 2013, the share of the biotechnology industry among national R&D projects was 19%, ranking second after the information and communication industry (19.4%). These facts imply that the South Korean biotechnology industry has been government-led in nature [12]. In that sense, we believe that this study has critical implications on government R&D subsidies policy for countries that are latecomers to the biotechnology industry using a government-led industry model, such as South Korea.

This paper is structured as follows. Section 2, the theory and hypothesis verification, where we propose hypotheses on the effect of government R&D subsidies from the view of additionality. Section 3 introduces the data and method for analysis, and it defines the variables to be used in the analysis. Section 4 deduces the results of the analysis and discusses these findings through a comparative analysis with other studies. Section 5 suggests the implications for policies and management based on the analysis results.

2. Theory and Hypotheses

2.1. Additionality by Government R&D Subsidies in the Biotechnology Industry

Additionality is the response by a firm to an intervention [7]. Scholars have been interested in additionality through government R&D subsidies. It appears in three different aspects, which are input, output, and behavioral additionality [13]. Among these, the areas with significant achievements in the studies on additionality through government R&D subsidies are input and output additionality; the influence of government R&D subsidies on promoting a firms’ private investment in R&D activities; and the changes in performance such as technological innovation, revenue, and profit [13,14,15,16]. Input additionality compares the firm when it did not receive government R&D support and how government support has increased the firm’s R&D expenditures, R&D intensity, and the size of the private investment, or alternatively, the extent to which government R&D subsidies to the firm have dampened private investment, called the crowding-out effect [13]. Output additionality relates to the outcomes of government R&D subsidies, and it reveals how much change has occurred in a company’s performance through the support compared to when it did not receive the support [14]. In other words, output additionality is the marginal performance of government R&D subsidies and it represents changes in the number of patents, new products, or services, sales, or profits [15,16].

Behavioral additionality can be defined as changes in the company’s behavior or strategy after it receives government R&D subsidies compared to when it did not receive that support [12,16,17]. This concept helped to develop an extensive and intermediate understanding of the effect of government R&D subsidies from viewpoints which had previously concentrated on input additionality and output additionality [12]. Clarysse and Moray [16] divided the functional types of behavioral additionality into functional additionality and strategic additionality. Functional additionality emphasizes the quality of the level of production and speedup, as well as functional improvements, such as functional expansion of the value chain, growth of the business size, and investment extension. Strategic additionality stresses strategic changes, such as cooperation with external organizations, external financial support, and patent strategy changes. Furthermore, Georghiou and Clarysse [17] classified behavioral additionality into four elements: challenge additionality representing whether a firm participates in risky projects, network additionality indicating if external cooperation has been stimulated, follow-up additionality showing if a firm has conducted a follow-up project, and management additionality identifying the impacts on a firm’s management innovation. Hsu, Horng, and Hsueh [12] argued that behavioral additionality could be revealed through project size expansion, strategic change, increases in cost-effectiveness, and commercialization behavior. Overall, behavioral additionality embraces not only changes in strategies to the R&D level, such as a firm’s range or speed of R&D projects, but also the strategic changes in the firm’s overall management from planning to marketing. It also includes all changes in the internal or external corporate behavior.

Government R&D support to the biotechnology industry plays a very important role in firms’ technological investment and performance. The biotechnology industry is a technology-intensive industry; hence, biotechnology firms should have a higher R&D investment and R&D intensity than companies in other industries [18,19]. This is not a problem that can be solved by a biotechnology company alone. Although it is significant for biotechnology firms to make their own R&D investments, scholars have argued that external financing, such as venture capital and debt financing, as well as public support such as government support, plays an important role. In addition, because of the high risk arising from the long R&D period and the large R&D investment in R&D processes from the discovery of candidate substances to clinical trials, it is also necessary to support a firm’s technological innovation performance through government R&D subsidies. Furthermore, the creation of biotechnology does not necessarily lead to improved firm’s financial performance. Technological commercialization of biotechnology companies is another challenge. This is because even if the new biotechnology is developed, it may incur significant costs to manufacture, and it may not be easy to market through distribution channels. Government R&D support also facilitates this technological commercialization through production and marketing. Therefore, biotechnology firms should manage their financial performance for growth and survival.

In addition, government R&D support is also important in that it facilitates external collaboration or the financing of biotechnology firms. Biotechnology companies need to collaborate with other organizations because of the following characteristics of technology: (1) the uncertainty of technology, (2) the cumulative nature of technology, and (3) the multidisciplinary nature of technology [6]. Biotechnology has a lot of scientific characteristics; therefore, it has fundamentally high uncertainty and there is a limit to the firm’s capability to manage the technological risks. Therefore, biotechnology companies usually do not start their business on various core technologies, but they begin operating with one or two accumulated core technologies. However, in the process of technological development, biotechnology has the characteristic of being able to converge not only with other biotechnologies, but also with the technologies in various areas, such as information and electronic technology, nanotechnology, etc. This means that cooperation with other organizations, such as strategic alliances is necessary in the development of biotechnology [8]. In sum, government R&D support directly contributes to the R&D investment of biotechnology companies, and it can promote R&D investment through self-investment or external financing, promote external cooperation, and ultimately contribute to performance creation (i.e., technological innovation performance, financial performance). This implies that input (R&D investment and R&D intensity), output (technological innovation and financial performance), and behavioral (external collaboration and external financing) additionality exists for the effect of government R&D subsidies in the biotechnology industry.

As one of the latecomers to the biotechnology industry, South Korea should take an integrated look at the effects of government R&D support. The South Korean biotechnology industry was developed through government-led policy in the early 1990s [20]. However, the South Korean biotechnology industry still has a large portion of small-medium enterprises, although some of these companies are producing excellent technological results internationally [11]. In this context, government R&D subsidies have become a valuable source of funding for the early technology investments of companies that lack seed money. However, scholars argue that it is necessary for the development of the biotechnology industry in South Korea that the biotechnology companies nurture self-sustaining power by increasing the firms’ private investment and enhancing their performance [10,11,12,20]. Furthermore, scholars argue that South Korea needs to build an industrial ecosystem to facilitate financing and cooperation in the biotechnology industry. In particular, the role of venture capital, which has become a major factor of growth for the biotechnology industry in developed countries, has been insufficient in South Korea. In the situation of a lack of venture capital, South Korean biotechnology companies have mainly relied on debt financing from banks [12]. In addition, although South Korea’s large conglomerates, known as chaebol, or pharmaceutical incumbents lead the cooperation with biotechnology firms, biotechnology companies are also trying to cooperate with other organizations (other companies, universities, government research institutes, etc.) [20]. Government R&D support in South Korea can be an important policy for the growth of enterprises in these aspects. Therefore, this study examines the effects of government R&D subsidies on R&D investment in terms of input additionality, technological innovation, and financial performance in terms of output additionality; and strategic alliances and external financing (debt financing) in terms of the behavioral additionality in biotechnology firms in the South Korean context.

2.2. Input Additionality: R&D Investment

Input additionality shows how the relative input of a company changes when it receives government R&D subsidies compared to when it did not receive that support [16]. Historically, the additionality concept originates from the debate of whether government R&D subsidies stimulate a company’s private investment in R&D, and many scholars have studied whether government R&D subsidies have a substitutional or complementary aspect to a firm’s R&D expenditure (e.g., References [21,22]). Government R&D subsidies complement the R&D of private firms rather than substituting it [23,24,25]. In a complementary sense, some studies showed that there is a difference in the impact depending on the amount of government R&D subsidies received. A certain level of subsidy induces an increase in private R&D investment, whereas excessive subsidies substitute for private investment in R&D, called the crowding-out effect [2,26].

Branstetter and Sakakibara [27] showed that government R&D subsidies increased firms R&D expenditures. According to the survey conducted by Almus and Czarnitzki [23] on 2,500 manufacturing venture companies in East Germany, companies benefiting from government subsidies showed 4% higher R&D intensity than companies that did not receive subsidies. Firms granted government R&D subsidies made more investments in internal R&D activities than firms that did not receive subsidies [24]. Einio [25] confirmed that government R&D subsidies stimulate the private R&D investment of firms, based on government R&D subsidy data for Finland’s enterprises. Lee [28] found that government R&D support increases the R&D intensity of firms, using company data from Canada, Japan, Korea, Taiwan, India, and China provided by the World Bank. Hong, Feng, Wu, and Fang [29] found that government R&D support increased corporate private R&D investment in high-tech companies in China. Czarnitzki and Hussinger [30] looked at the effects of government subsidies on the full crowding-out effect and the partial crowding-out effect of German companies based on the Mannheim Innovation panel data. They used the total amount of government (public) R&D subsidies and private R&D investment of corporates as a proxy of the full crowding-out effect, and they used a proxy of only the private R&D investment of corporates to investigate the partial crowding-out effect. The results showed that both the total amount and the private R&D investment of the corporation were significantly higher than that of companies that did not receive government R&D support in both cases. Therefore, they demonstrated that the government R&D subsidy is a device to accelerate private R&D investment.

Moreover, Guellec and van Pottelsberghe de la Potterie [2] proved that government R&D subsidies increase a firm’s R&D investment to a certain extent, but if the subsidies exceed 20% of the firm’s R&D investment, a crowding effect occurs, which meant that the firm diverts the government’s R&D investment. Moreover, Görg and Strobl [26] also reported that an appropriate level of government R&D subsidies increased the R&D expenditure of Irish manufacturers, while excessive subsidies causes a crowding-out effect that makes these companies reduce their internal R&D investment. On the other hand, Marino, Lhuillery, Parrotta, and Sala [31] found evidence that there is no input additionality, but rather a substitution effect between government R&D support and private R&D investment in a study of French companies. These results indicated that the government R&D subsidy is a medium that promotes a company’s voluntary private R&D investment; however, adequate government R&D support should consider the volume of the R&D activities of the company. Therefore, the current study proposes the following hypothesis:

Hypothesis 1.

A firm that received government R&D subsidies makes more R&D investments than firms that did not.

2.3. Output Additionality: Technological Innovation and Financial Performance

Government R&D subsidies have a justification with respect to welfare in that they promote a firm’s private investment. However, if they cannot directly guarantee technological innovation performance (output additionality), the impact of the subsidies will be diminished [32]. Government R&D subsidies generally have a positive effect on technological innovation [27,33,34]. Firms participating in an R&D consortium have increased patent performance [27], and a firm with government R&D subsidies has better patent achievement than firms without subsidies [24]. According to Bérubé and Mohnen [33], firms that were given both tax benefits and government R&D subsidies directly generated more technological innovation performance, such as new product development, as compared to firms that only received tax benefits. Cantner and Kösters [34] analyzed the effect of government R&D subsidies on start-ups in East Germany and they confirmed that the number of patents increased in firms to which government R&D subsidies were granted. In addition, Bronzini and Piselli [35] found positive effects of government R&D subsidies on firms’ patent performance (technological innovation performance) in a study of companies in northern Italy. Szczygielski, Grabowski, Pamukcu, and Tandogan [36] also found that government R&D support increases firms’ technological innovation performance in studies of Turkish and Polish machinery and equipment companies. Guo, Guo, and Jiang [37] examined the effects of government R&D support on the patent applications and new product development of firms, in a study of manufacturing firms in China. Czarnitzki and Hussinger [30] demonstrated that in the case of German companies, government R&D support positively influenced both quantitative and qualitative performance of technological innovation performance. These results indicated that government R&D subsidies positively affected the technological innovation performance of firms.

Furthermore, Kang and Park [8] on South Korean biotechnology firms, proved that government R&D subsidies had a direct positive impact and an indirect positive impact through R&D employees and intensity, and R&D alliances on patent performance. Buchmann and Kaiser [38] examined the impact of government R&D support on corporate patent performance in the case of German biotechnology companies. However, government R&D support can have a different impact on the technological innovation performance of firms in the high-tech industry in the short term or the long term. Zhang and Guan [39] found that government R&D support has a positive impact on a company’s technological innovation performance in the short term but has a negative impact in the long term in a study of Chinese high-tech companies. The results showed that the government R&D subsidy had positively influenced the technological innovation performance of the company. Therefore, this study proposes the following hypothesis:

Hypothesis 2a.

A firm that received government R&D subsidies has better technological innovation performance than firms that did not.

Feldman and Kelley [40] found that the possibility of commercialization is critical in the assessment of government R&D subsidies. Moreover, government R&D subsidies increase sales or profits by promoting technology transfer or product commercialization [12,41]. Government R&D subsidies increase the sales of a firm by stimulating technology innovation performance and technology transfer [42]. Audretsch, Link, and Scott [41] argued that the Small Business Innovation Research (SBIR) program, a small and medium-sized business support program of the US government, accelerated the commercialization of technologies already developed, resulting in a positive impact on financial performance. Government subsidies were effective not only in the R&D activities, but also in revenue generation through the commercialization of the technologies because the subsidies activated technology transfer [43]. Government interventions in industries, such as R&D subsidies, provide revenue streams from using the new technology of a firm that can be commercialized through technology transfer [44].

Lerner [45] and Link and Scott [46] analyzed firms participating in the SBIR program of the US and the result showed that the SBIR program vitalized external private investment, which led to the commercial achievement of the firms by promoting productization. Firms that participated in the government’s R&D subsidy program produced more world class products and they were more successful in commercializing their innovation performance, resulting in better financial performance [33]. Hsu, Horng, and Hsueh [12] on the measurement of efficiency of the Taiwanese government’s R&D projects also indicated that government R&D subsidies boosted firms’ technological innovation performance, and it led to a positive impact on the financial performance in a virtuous cycle. Hünermund and Czarnitzki [47] based on European government R&D support data found that although all R&D projects receiving government R&D subsidies could not guarantee financial performance, some high-quality R&D projects increased the likelihood that they would generate corporate financial performance. Therefore, this study proposes the following hypothesis:

Hypothesis 2b.

A firm that received government R&D subsidies has a better financial performance than firms that did not.

2.4. Behavior Additionality: Strategic Alliance and External Financing

Previous studies have demonstrated that the reasons that government R&D subsidies promote a company’s strategic alliance include the increased size of R&D projects, an expanded absorptive capacity, and a reputation effect. First, government R&D subsidies directly expand the volume of R&D activities, and the expansion requires more complementary resources and capabilities. Therefore, the firm makes a larger effort to secure complementary assets and strategic alliances with an external organization. Taking the example of firms that participated in the European framework programs, Bach, Matt, and Wolff [48] argued that firms aimed to obtain the complementary assets they needed by continuously enlarging the size of their network (strategic alliance) to prevent system failure due to insufficient capability and interaction. Furthermore, in the biotechnology industry, where basic science knowledge is crucial, government R&D subsidies can activate connections with basic science research organizations, such as universities. Government R&D subsidies are an opportunity for research institutes, including universities, to express their basic science knowledge and transfer technologies [49,50]. Etzkowitz [51] claimed that government R&D subsidies are an important policy instrument to remove the boundary between universities and firms. Empirically, Liu and Wen [52] studied firms that participated in the Taiwanese government subsidy program and proved that government subsidies had vitalized technology transfer from research organizations and R&D alliances. Greco, Grimaldi, and Cricelli [53] in their study of 43,230 European firms demonstrated that public R&D subsidies increased cooperation with external organizations, which is open innovation, at local, national, and European level.

Second, government R&D subsidies can indirectly strengthen a company’s R&D alliances by reinforcing the company’s absorptive capacity [54]. Government R&D subsidies strengthened the absorptive capacity, making a company’s networking more active [55]. The stronger absorptive capacity of a company through government R&D subsidies heightens the possibility of strategic alliances with various organizations [56]. For example, Kang and Park [8] found that government subsidies have increased vertical alliances between universities and pharmaceutical firms through expanded absorptive capacity as proxies of R&D employees and R&D intensity. In particular, Radas, Anic, Tafro, and Wagner [57] analyzed the small and medium-sized enterprises in Croatia and found that the government R&D subsidy strengthens external cooperation by strengthening the exploitative capacity of external technologies among the firm’s absorptive capacity.

Third, government R&D subsidies imply positive signals to the market, which improves the reputation of a firm, and the halo effect promotes the firm’s strategic alliances. Government R&D subsidies send a positive signal about corporate value to the market because the government does not select a beneficiary company at random [40,58]. Previous studies have investigated whether the size, R&D experiences, or R&D intensity of a firm determines its eligibility as a beneficiary of government R&D subsidies [59,60,61]. The superior technological innovation performance a firm also has a decisive impact on gaining access to government subsidies [34]. Consequently, government subsidies for technological development can certify the firm’s corporate value in the market, as well as a higher reputation given that enhanced corporate value stimulates the firm’s strategic alliances [62,63]. These results imply that government R&D subsidies promote a firm’s strategic alliances. Therefore, this study proposes the following hypothesis:

Hypothesis 3a.

A firm that received government R&D subsidies has more strategic alliances than firms that did not.

Government R&D subsidies provide a justification for external financing by reducing information asymmetry [21]. Owing to the high asymmetry of information between a firm, the entity of technology development, and investors in the high-tech industry, a lemon premium inevitably exists, which means that a firm’s external capital financing for R&D is high [64,65,66]. Investors are more interested in firms conducting projects with a high possibility of commercialization than firms undertaking risky projects [40]. Government R&D subsidies move a firm’s R&D into the commercialization stage and reduce the asymmetry of information between the firm, the entity of technology innovation, and investors, thereby activating a firm’s financing [58]. In addition, government R&D subsidies are not random, so they give positive signals to investors because the fact that a firm receives government subsidies suggests the disclosure of valuable technology to the market or limited information about the firm [45,67,68]. Carboni [69] analyzed 14,911 manufacturing companies in seven European countries and found that the government R&D subsidy increased private investment in the firm. It explained that firms can increase their credit due to government R&D subsidies, and this can be a way to overcome firm’s financial constraints in increasing private investment. In a study of US clean energy start-ups, Islam, Fremeth, and Marcus [70] found that companies receiving R&D grants from the US federal government were 12% more likely to earn subsequent venture capital funds. Interestingly, however, they explained that this effect only appeared for six months after receiving the federal government R&D subsidy and did not appear thereafter. This is a case in which government R&D support serves as a good signal to the market, making it easier for the company to secure funds [71].

In that sense, a firm may facilitate external financing. Better technological innovation performance is expected through government R&D subsidies; thus, a firm’s external financing may increase [72]. Government R&D subsidies mitigate a firm’s financial restrictions, so the firm’s survival can be better guaranteed [73]. In the study by Meuleman and De Maeseneire [58], their analysis of the data of IWT-Flanders (The Institute for the Promotion of Innovation by Science and Technology in Flanders), a government R&D subsidy program in the Flanders region in Belgium, indicated that as a bank gives debt financing, the firms consider future cash flow and the long-term prospects of it. A government R&D subsidy increases the firm’s market value, consequently indicating a positive sign to the market, thereby enabling external financing. These results indicate that government R&D subsidies promote firms’ external financing. Therefore, this study proposes the following hypothesis:

Hypothesis 3b.

A firm that received government R&D subsidies receives more external financing than firms that did not.

3. Methodology

3.1. Data

The data used in this study was from the bio venture database (DB) of the Science and Technology Policy Institute of the Republic of Korea (hereinafter STEPI). This DB was based on the list of companies registered with the Korea Biotechnology Industry Organization (hereinafter Korea BIO) of South Korea, and it was built by gathering financial data, government R&D subsidy data, patent data, and alliance data. First, with regards to bio ventures, Korea BIO confirmed that 2,441 bio ventures existed in South Korea from 1992 to 2012, in the publication “Guide to Biotechnology Companies in Korea”. Among them, 1504 bio ventures were confirmed, excluding foreign firms and firms specialized in importing and sales without technological innovation activities. Moreover, the business areas of biotechnology firms are diverse and include foods, chemical, energy, and fuel and platform companies, as well as pharmaceuticals by bio-industry classification of the Korea BIO. Therefore, for this study, only 736 companies were included: (1) biopharmaceutical firms manufacturing products related to drugs, and diagnostic kits and reagents, and (2) bioplatform firms providing drug analysis supporting services and producing drug analysis equipment to minimize the heterogeneity of the analysis. (Out of the total of 1504 companies, 768 companies in the business fields of foods, chemicals, energy, and fuel were eliminated). The analysis was based on 470 firms in total, for robustness of the analysis, excluding 115 firms with insufficient or unclear information about their finances, government R&D subsidy, patent, and alliance data, and 151 firms that had not generated any sales. (A total of 266 companies were eliminated). The distribution of firms used in these data is shown in Table 1. Among 470 firms in all, there were 311 biopharmaceutical firms (66.2%) and 159 bioplatform firms (33.8%). This was further segmented as 253 biomedicine firms (53.8%), 58 diagnosis and kit firms in biopharmaceutical firms (12.4%), and 118 drug analysis service firms (25.1%), and 41 drug analysis equipment firms (8.7%) in bioplatform firms.

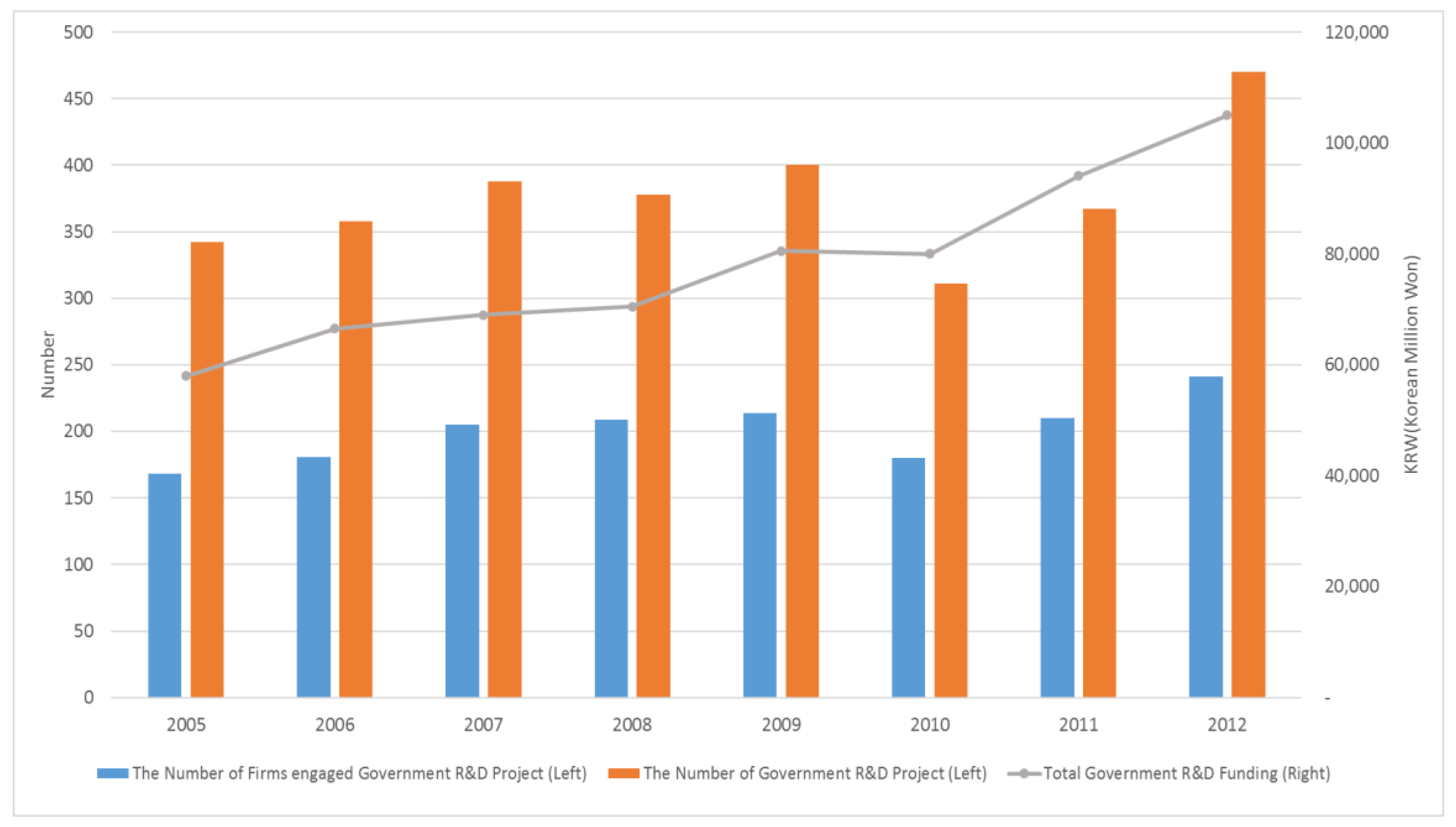

Financial data, government R&D subsidy data, and patent data of the STEPI bio venture DB were based on the Korea Enterprise Data, National Science and Technology Information Service (hereinafter NTIS), and Thomson Reuters, respectively. In particular, government R&D support for Korea’s bio-industry is shown in Figure 1. The number of biotechnology companies receiving government R&D subsidies, as well as government-led projects, have increased since 2005, except for the periods 2010 and 2011. The total amount of government R&D support to the biotechnology industry also increased from 2005 to 2012. Among them, a total of 292 biotechnology companies, including biopharmaceutical firms and bioplatform firms, received government R&D support from 2005 to 2012, while 178 companies that did not receive government R&D subsidies at any one time during the period were included in the analysis. Meanwhile, 714 projects that received government R&D support were also used for the analysis in this study. For alliance data of the STEPI bio venture DB, news related to bio ventures alliances provided by the Biotech Policy Research Center and Biotechnology Industry Organization of South Korea every day or every other day since 2005 was investigated. In the absence of a specialized DB offering strategic alliance information in South Korea, such as Data Monitor in the US and Med Track in the UK, the STEPI built a DB for the strategic alliances of bio ventures based on the information provided by these organizations. This data contains information on 924 alliances from 2005 to 2012, and this study used 463 strategic alliances related to biopharmaceutical and bioplatform firms for analysis. Finally, for analysis of this study, the unbalanced panel data of 470 firms over eight years from 2005 to 2012 with 2980 observations were used.

3.2. Analysis Method

Firms benefiting from government subsidies are highly likely to have better stability, based on the firm’s size and age and better technological innovativeness, compared to firms that have not received subsidies. In this case, in classifying the beneficiary firms and non-beneficiary firms, selection bias from the population occurs. If the policy effect on beneficiary and non-beneficiary firms is assessed without considering the bias, there is a concern of over- and under-estimation of the actual effect [74]. Thus, we used a propensity score matching (PSM) method, which enables a relatively reasonable correction of the selection bias to assess the effect of government subsidies. To compare the performance of the beneficiary firms to their virtual performance if a government subsidy was not granted, this method included a stage for matching beneficiary firms and non-beneficiary firms with the most similar characteristics. By doing so, the performance before and after receiving a government subsidy could be compared to see the difference that developed in the performance through the effect of the government subsidy. In practice, the pure effect of the government subsidy is represented by Equation (1).

The ATT, an abbreviation for the average treatment effect on the treated, is expected to relatively affect the policy support, and Y1 is the output after receiving the benefit of a government R&D subsidy, Y0 is the output without the benefit, and D is an indicator variable indicating if a benefit is given. In addition, X is a characteristic variable that can be observed in each firm.

The problem here is that the most similar pair between firms that are granted subsidies and firms that are not granted subsidies needs to be matched, and this process is divided into two phases. First, the possibility of benefiting from government R&D subsidies is estimated using the observable features of each firm, and it is called the propensity score [75]. Before matching, to compose a group with the same features, the propensity score of a beneficiary firm is calculated using the probit model, and the most similar non-beneficiary firms are extracted using the score. As such, the problem of anti-fact is solved by composing a comparison group with non-beneficiary firms that have similar characteristics to the beneficiary firms. The process assumes that firms with the same propensity score experience the same effect from a government R&D subsidy. The propensity score is represented as Equation (2).

Next is the stage for matching the beneficiary and non-beneficiary firms based on their propensity scores, but it is impossible to match a pair with exactly the same value because the propensity score value is a continuous variable. For this reason, various matching methods for creating a pair with similar calculated propensity scores have been suggested. This study used the nearest neighbor matching method which matches each beneficiary firm with a non-beneficiary firm with the most similar propensity score; thus, all beneficiary firms make a pair [75]. Among those pairs, however, some pairs may have considerably different values of propensity scores, even though they are the closest pair. The output of a beneficiary firm is matched with the average output of some firms with propensity scores that are similar to address this problem. This study used the average output value of four non-beneficiary firms. In the PSM, our analysis had a sufficiently large number of control groups every year from 2005 to 2012 compared with other studies that used PSM, such as Radas, Anić, Tafro, and Wagner [57] and Islam, Fremeth, and Marcus [70]. (The ratio of the average number of companies that received government R&D subsidies during the eight years from 2005 to 2012: The average number of companies that did not receive government R&D subsidies during the eight years from 2005 to 2012 = 89: 381).

3.3. Operational Definition of Variables

In this study, a firm’s size, age, owning of a research center, R&D intensity, and technological innovation performance were used as the independent variables in calculating the propensity score. According to previous studies, a firm’s size is a critical element in deciding whether it will benefit from government R&D subsidies. A firm’s size is proportionate to its size of R&D or willingness (effort) to engage in R&D [60], and it is a decisive factor in receiving government R&D subsidies. In addition, a firm’s age is an indicator representing its experience, so it indicates the accumulation of technical or business capabilities. A firm’s size or age could overcome its financial restrictions [21,59,61]; hence, these variables are critical elements that affect a firm’s R&D expenditure, output, and behavioral additionality. We used sales as a proxy of a firm’s size, and in the analysis, the log-transformed value was used because the values of the variables were skewed. The firm’s age used in this study was the difference between its year of founding and 2012.

Since the objective of a government R&D subsidy is to support firms’ R&D, beneficiary firms need to have the infrastructure and willingness to conduct R&D activities. Therefore, owning a research center or a research task force team, which indicates a firm’s enthusiasm for R&D, significantly affects whether it can be a recipient of government R&D subsidies [76]. In accordance with the principle of “Picking the Winner”, government R&D subsidies inevitably concentrate on firms with excellent R&D capabilities or performance. Shane [77] found that the policy decision method frequently used by policymakers to select a “good firm” for an R&D subsidy involves selecting a firm with excellent technological innovation performance. This is because of a reduction of the crowding-out effect [77], a decreased failure rate of government-sponsored R&D projects [78] and inducing external investment through excellent technological innovation performance [79].

This study controlled the factor of whether a firm was an “initial public offering (hereinafter “IPO”) firm” or a “venture certified firm” because these were the elements that, by providing a good signal of the firm’s valuation or reputation, could affect government R&D support selection. The IPO firms have already received assessments of technological innovation and growth potential for the IPOs [80]. The IPO process itself could have the function of scouting firms that are receiving government R&D subsidies. In addition, the venture certified firm is a firm that has attracted venture investment and has a relatively high technological innovation capability and growth potential compared to other firms, or it is a government-certified firm that has recognition of superiority in technology development. South Korea manages small and medium-sized “venture firms” with a unique certification system. For these reasons, being an IPO firm or venture certified firm positively affects the chances of receiving government R&D subsidies and it is thus a control variable in this study.

Although there is a problem of duplicate benefits of government R&D subsidies, previous studies that applied matching used the indicator of whether a government R&D subsidy is granted as a dependent variable [32,81]. Therefore, this study also used the indicator of whether a government R&D subsidy was granted as an indicator variable.

Previous studies used R&D expenditures and R&D intensity as the proxies of input additionality [23,24,55]. We solved the problem of endogeneity, depending on the size of a firm, by handling the issue of selection bias using a matching method. Absolute values, such as the size of R&D input, rarely show the sustainability of a firm’s R&D investment; therefore, it is hard to measure additionality. In addition, R&D intensity is a value calculated by dividing R&D expenditures by sales [82], so it is unreasonable to apply it to biotechnology firms where initial sales take a long time to mobilize [3]. Therefore, we used the growth rate of R&D investment as the additionality proxy of R&D investment to track the possibility of a sustainable change in input amount.

In terms of output additionality, the number of patents and the sales growth rate were used as proxies of technological innovation performance and financial performance. For biotechnology firms, securing patent rights should be emphasized as a resource for R&D, along with human resources [83]. Unique and unrivalled technological capabilities and the patent rights for them are an important criterion differentiating a firm’s competitiveness. A biotechnology firm’s value can be highly estimated from its patents, even without a clear profit model [84]. However, securing patent rights is insufficient in South Korean biotechnology industry, where the distribution of start-ups is high. Therefore, it means there are many variable values with a “0” value. In variables with a high distribution of “0” values, owning a patent or several patents is more reasonable than the growth rate of patents when observing the relative effect of government R&D subsidies. Therefore, this study used the number of patents for the year as a proxy of the output additionality of a firm’s technological innovation performance.

Moreover, in terms of the growth potential and profitability, sales and profit (or the Return on Assets (ROA) and Return on Equity (ROE)) indices are used as measures for the financial performance of a firm [85]. However, given the characteristics of the biotechnology industry in which the development period is relatively longer than other industries, it takes a significant amount of time to generate sales after starting a business, and it takes even longer to generate a profit. Since the firm’s subject to analysis were start-ups, this study adopted the sales value and the growth rate of sales as the output additionality proxy of financial performance [12,46].

In terms of behavioral additionality, the number of strategic alliances and the growth rate of debt financing are used as proxies of promoting strategic alliances and external financing. Previous studies have used the existence and the number of strategic alliances and their consistency as proxies when measuring the effect of strategic alliances [13,55]. Strategic alliance also has many “0” values due to the features of the South Korean biotechnology industry, where there is a high ratio of start-ups. Therefore, this study used the number of strategic alliances as a quantitative proxy of behavioral additionality regarding the promotion of strategic alliances.

Furthermore, South Korea has built an industrial ecosystem that lacks venture capital, and business founders show the strong characteristic of avoiding managerial intervention [86]. Therefore, the main financing method for South Korean biotechnology firms has been debt financing. Meuleman and De Maeseneire [58] used the size of external financing, such as long-term debt and short-term debt, to identify the effects of investment through government R&D subsidies. Therefore, this study used the growth rate of the total debt as a proxy of behavioral additionality to examine the possibility of sustainable change. Operational definitions of variables are summarized in Table 2.

4. Results and Discussion

In the first stage, a probit analysis was performed to calculate the propensity scores of government R&D subsidies. Elementary statistics and correlations of each variable are shown in Table 3, and the result of the probit analysis is described in Table 4. There was general significance in the correlation, excluding the correlation of the patent and age.

In examining the relation between government R&D subsidies and control variables, IPO had a positive impact on receiving government R&D subsidies, which meant that the government tended to give R&D subsidies to IPO firms in the South Korean biotechnology industry. Venture certification also had a positive impact on receiving government R&D subsidies. The venture certification system in South Korea also assesses the external investment of venture capital and technological capabilities in the certification process; therefore, it positively affects the selection of government R&D subsidy beneficiary firms.

Both the company’s size and age negatively affected the government’s selection of R&D support recipients. A firm’s size and age indirectly represent its technological capabilities and guarantees continuity of the R&D investment based on a stable financial structure, managerial capabilities in the face of risks, and the ability to exclusively possess technological innovation performance. Therefore, these factors may increase the possibility of receiving government R&D subsidies [34,59,60]. However, our study revealed that government R&D subsidies were mostly granted to small and young firms, which implied that government R&D subsidies in the biotechnology industry were concentrated on small-sized start-ups. This result showed that government R&D investment was a critical source of funding for small-sized start-ups in the South Korean biotechnology industry.

The existence of an R&D department, R&D intensity, and the patent performance of a firm in terms of the technological innovativeness of a firm had a positive impact in the selection of beneficiaries of government R&D subsidies. This result supported the arguments of Busom [60], in which government R&D subsidies were granted to firms with excellent R&D capabilities, intensity, and performance. The results contradicted Cantner and Kösters [34], in which a firm’s technological innovativeness did not affect the selection of the beneficiaries of government R&D subsidies. Moreover, it proved that the principle of “Picking the Winner”, i.e., a firm with excellent R&D capabilities and performance benefited from government R&D subsidies, was valid in the South Korean biotechnology industry. In the second stage, the matching results on the effect of government R&D subsidies for three years using a firm’s size, age, existence of an R&D department, R&D intensity, and technological innovation performance as covariates to the propensity score are described in Table 5.

First, in terms of input additionality, the firms receiving government R&D subsidies had a continuously higher growth rate in the firm’s R&D investment over three years relative to when the subsidy was initially granted, as compared to the firms that did not receive the subsidies (Hypothesis 1 was supported). This result suggested that government R&D subsidies promoted a firm’s R&D investment, resulting in a firm’s input additionality for R&D. The results of this study supported the work of Branstetter and Sakakibara [27], Almus and Czarnitzki [23], and Czarnitzki and Hussinger [30]. It meant that government R&D support in the biotechnology industry of South Korea led to an increase in corporate R&D investment. That is, South Korean biotechnology firms have grown their R&D intensity using government subsidies as a foundation for R&D funding. It implied that government R&D subsidies could serve a decisive role in the survival of the firms at the initial stage of business. However, because this study could not strictly know if the firm’s R&D investment was a new private investment or the reassignment of routine R&D expenditure, it could not show whether there was a crowding-out effect as in the study of Czarnitzki and Hussinger [30].

Second, in terms of output additionality, the firms receiving government R&D subsidies had a higher technology innovation performance than the firms that did not, for the first one or two years, but this effect was rarely found after three years. However, the results of this study could not find evidence that firms receiving government R&D support had a higher financial performance than firms that did not. (Hypothesis 2a supported; Hypothesis 2b not supported). With regards to patent performance, biotechnology firms with government R&D subsidies showed better performance over the two years from when the subsidies were initially given, although no significant difference was detected after three years. The result that a firm with a government subsidy had a markedly higher sales growth rate than a firm without support was not verified, which meant that government R&D subsidies could not guarantee the financial performance of a firm, even though it promoted technological innovation performance.

Our results indicated that government R&D subsidies had a positive effect on a firm’s technological innovation performance in the biotechnology industry of South Korea. However, the results of our study in the context of South Korea did not support the study results of Bérubé and Mohnen [33] and Link and Scott [46] who found that government R&D subsidies also had a positive influence on the financial performance of a firm. There is a concern that the effect of the government subsidy is still going up to the R&D stage, but it is not reaching the commercialization stage, thereby weakening the self-sustainability of biotechnology firms in South Korea. In addition, according to this study, only one or two years of short-term technological innovation performance drew a significant result, raising the concern that government R&D subsidies may not have a significant impact on long-term technological innovation performance. This may result from the evaluation system of South Korea on the outcome of government R&D subsidies concentrating on technological innovation performance, such as articles and patents, producing technological innovation performance just for show. This was consistent with the study by Zhang and Guan [39] who found that government R&D support has a positive impact on a firm’s technological innovation performance in the short term, but it does not give significantly positive effects or can even have a negative impact in the long term.

Therefore, the results indicated that South Korean biotechnology companies need more high-quality R&D projects that can be commercialized. Hünermund and Czarnitzki [47] examined the effects of public R&D support on a firm’s revenue, based on the Eurostar’s program R&D support data, supported by EUREKA, a research network of European countries. Although the effect was not significant when viewed on the average of the entire government R&D projects, they proved that only high-quality R&D projects selected through the project evaluation system were effective in increasing firm’s revenue. Therefore, the results of this study suggested that only high-quality government R&D projects that could be commercialized and could guarantee financial performance beyond the firm’s technological innovation performance, were needed in South Korea’s biotechnology industry.

Third, from the perspective of behavioral additionality, government R&D subsidies promoted strategic alliances and reduced a firm’s external financing (Hypothesis 3a supported; Hypothesis 3b not supported). A firm with a government R&D subsidy had more active strategic alliances than non-subsidized firms for the three years after receiving the subsidy. Therefore, it could be argued that government R&D subsidies stimulated a firm’s strategic alliances. To summarize, there are three reasons why government R&D subsidies promote a firm’s strategic alliances. First, government R&D subsidies expand a firm’s scale of R&D activities, so the firm uses the strategic alliance as a corporate strategy to satisfy complementary assets. Second, government subsidies raise a firm’s absorptive capacity; thus, R&D alliances with external organizations are also vitalized. Finally, the positive signal from biotechnology firm valuation by government R&D subsidies facilitates strategic alliances. This was consistent with the results of Shin, Kim, and Park [86]. In the biotechnology industry, where cooperation with other organizations, such as research organizations, other biotechnology venture firms, and pharmaceutical firms, through open innovation is essential, government R&D subsidies resulting in the promotion of strategic alliances are interpreted to have a positive impact on the development of the South Korean biotechnology industry.

Furthermore, from the perspective of behavioral additionality, government R&D subsidies have decreased the growth rate of the debt financing of a beneficiary firm compared to that of firms that are not subsidized, for the three years after subsidization. This result conflicted with Meuleman and De Maeseneire [58] and Szewczyk, Tsetsekos, and Zantout [72], who found that government R&D subsidies vitalized a firm’s external financing. The decrease in the growth rate of total debt due to government R&D subsidies indicated that the beneficiary firm borrowed less money from financial institutions, such as banks. That is, this indicated that government R&D subsidies reduced a firm’s financial leverage. The higher the firm’s financial leverage is, the more favorable it is to improve its profitability, so from a stockholder point of view, increasing financial leverage is advantageous if profitability from the external financing exceeds the financing costs, such as interest expense. This phenomenon has the implication that profits resulting from external financing are insufficient to cover the financing costs in the South Korean biotechnology industry; therefore, firms will reduce debt financing to seek financial stability. Therefore, this study found that government R&D subsidies had the effect of substituting a firm’s debt financing to some extent [77]. This result meant that South Korean biotechnology firms could achieve financial stability through government R&D subsidies in the short term, but these may pose the risks by reducing a firm’s financing scale and may aggravate performance by making the firm’s activities passive in the long term.

5. Conclusions

Government R&D subsidy policy plays a pivotal role in the biotechnology industry because of market failure due to imperfect appropriability and the high risk of technology development and commercialization in the firm, along with other government policies, such as tax reductions or founding of government-funded research institutes [6,87,88]. In particular, government R&D support is important for the growth and survival of biotechnology firms in countries that are latecomers to the biotechnology industry, which lack venture capital and are not well equipped with an industrial ecosystem. In addition, previous studies have presented fragmented results in terms of input, output, and behavioral additionality regarding the effects of government R&D subsidy on firms. Therefore, the impact of government R&D subsidies on biotechnology firms needs to be identified, and this study examined the impact from the perspective of input, output, and behavioral additionality in the context of the biotechnology industry of a latecomer country using the data from South Korea biotechnology companies. Moreover, based on previous studies that found government R&D subsidies are not granted on a random basis, we addressed the issue of selection bias by a comparison of government-subsidized firms and non-subsidized firms using a PSM method.

Government R&D subsidies are mainly given to small and young companies, and technological innovation potential or capability, identified based on whether an R&D department exists, the R&D intensity, and the technological innovation performance, has a positive impact on the recipients of government R&D subsidies in the South Korean biotechnology industry. This study also determined the input, output, and behavioral additionality of firms resulting from government R&D subsidies using matching analysis based on the propensity scores calculated using these factors. In terms of input additionality, biotechnology firms benefiting from government R&D subsidies had markedly higher growth rates in R&D investment than non-subsidized firms. Biotechnology firms benefiting from government R&D subsidies showed better technological innovation performance than non-subsidized firms in the short term; however, a significant result was not found regarding financial performance. In addition, this study inquired about the promotion of strategic alliances and external financing as important features of behavioral additionality in biotechnology firms. The analysis results proved that biotechnology firms benefiting from government R&D subsidies have more strategic alliances than non-subsidized firms and that the growth rate of debt financing has unexpectedly declined.

There are three implications regarding government R&D subsidies for the development of the biotechnology industry. First, policymakers when selecting companies for government R&D subsidies should take into consideration not only the technological aspects but also the size and age of the firm in countries that are latecomers to the biotechnology industry, such as South Korea. The criteria for government R&D subsidies in the South Korean biotechnology industry may be excessively biased towards the technological innovation capability of the firm. Since the justification for government R&D subsidies is based on preventing the reduction of R&D activities due to imperfect appropriability of technology and the risk of technology development and commercialization in the industry, it is natural that government R&D subsidies should be granted to firms with high technological innovation potential or capability. However, this may be an overestimation of the nature of the technology-intensive biotechnology industry in the South Korean context. Previous studies have found that the size and age of the firm have a positive relationship with government R&D support. If government R&D subsidies are mostly granted to young and small-sized enterprises, including start-ups with high technological innovation potential or capability, such firms may find it difficult to overcome the financial constraints of sustainable technological development [79,80,81,82,83,84,85,86,87,88,89,90]. Therefore, in the process of selecting the beneficiary of the subsidy, it is necessary to comprehensively consider the factors related to the size and age of the firm, as well as the technological innovation potential and capability of the firms.

Second, government R&D subsidies should be extended to the commercialization stage in countries that are latecomers to the biotechnology industry, such as South Korea. The results of this study demonstrated that government R&D subsidies in South Korea have promoted technological innovation performance in terms of output additionality, but they have been insignificant in financial performance. Previous studies suggest that government R&D subsidies can positively affect financial performance through technology transfer or product commercialization [43]. Our result failed to support these previous findings, which means that South Korean biotechnology firms need government R&D subsidies to strengthen their commercialization capabilities. There may be a practical debate as to whether government R&D subsidies should be enlarged in scope to the commercialization stage. However, if the scope of government R&D subsidies is considered to be “risk” in technological development and commercialization, they should be extended to the commercialization stage because the high risk in biotechnology development continues to the commercialization stage [91]. The biotechnology development stages of clinical testing, approval, manufacturing, and the marketing process following the initial technological development process, bear high risks [92]. In this context, the biotechnology firm’s performance derived from government R&D subsidies is highly likely to remain at the technological innovation performance stage, thereby failing to continue to commercialization. Therefore, it is necessary to enable policymakers to promote firm’s financial performance through active government R&D support for commercialization.

Third, the government’s supplementary policy for biotechnology firm funding should be executed in countries that are latecomers to the biotechnology industry, such as South Korea. The results of this study proved that a firm that has received government R&D subsidies has a reduced growth rate in debt financing compared to a firm that did not receive subsidies. South Korea has built an industrial ecosystem that lacks venture capital, and business founders or managers show a strong characteristic of avoiding managerial intervention by venture capital [86]. This trait causes biotechnology firms in South Korea to depend on debt financing. However, many biotechnology firms in South Korea cannot afford the cost of debt financing, which leads to the phenomenon that a firm benefiting from government R&D subsidies reduces its debt financing first. Although it is a natural behavior of a firm, attributed to the national character, the government of South Korea should pay attention to the fact that government R&D subsidies can make beneficiary firms’ activities passive by decreasing the level of debt financing. Therefore, policymakers should devise policies to ensure that biotechnology firms do not reduce debt financing after receiving a government R&D subsidy by combining two policies relating to the granting of R&D subsidies and to the lowering of financial costs of debt financing. Furthermore, there is a need for a sustainable financing policy to ensure the active input of equity financing by venture capital to replace the role of debt financing in the biotechnology industry, because the benefit of a government R&D subsidy to the firm can give a good signal to the market [70].

This study demonstrated the various impacts of government R&D subsidies in many aspects by considering them in terms of input, output, and behavioral additionality. However, this study has limitations due to the following reasons and it requires improvement. First, we failed to consider the effect of duplicated or repeated government R&D subsidies. A firm may receive multiple government subsidies in the same year and may repeatedly receive the same subsidy over several years. Therefore, the effect of R&D subsidies may be different due to the redundancy or repeatability. Future studies need to consider redundancy or repeatability to determine the effects of government R&D subsidies. Second, quantitative proxies, the number of patents and strategic alliances, were used instead of the growth rate in the patent and strategic alliances indices. Since events for these variables occur less frequently in the South Korean biotechnology industry, measuring the effects using the growth rate may be relatively inaccurate. Therefore, this study measured the effect of government R&D subsidies based on the absolute numbers instead of the rate of change. These proxies have room to reflect a firm’s endogenous characteristics to some extent. Therefore, these proxies need to be improved to compensate for such limitations. Third, previous studies have found that by promotion of R&D investment through government R&D subsidies, substitution may occur, depending on the amount of the subsidies [26]. However, this study did not consider the amount of government R&D subsidies. Future studies need to investigate the complementation and substitution of subsidies depending on the size of the government R&D subsidies.

Author Contributions

Conceptualization, K.S. and G.P.; methodology, K.S.; validation, K.S. and M.C.; formal analysis, K.S.; data curation, K.S.; writing—original draft preparation, K.S.; writing—review and editing, M.C. and C.L.; project administration, K.S. and G.P.

Funding

This research received no external funding.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Martin, S.; Scott, J.T. The nature of innovation market failure and the design of public support for private innovation. Res. Policy 2000, 29, 437–447. [Google Scholar] [CrossRef] [Green Version]

- Guellec, D.; De La Potterie, B.V.P. The impact of public R&D expenditure on business R&D. Econ. Innov. New Technol. 2003, 12, 225–243. [Google Scholar]

- Coriat, B.; Orsi, F.; Weinstein, O. Does biotech reflect a new science-based innovation regime? Ind. Innov. 2003, 10, 231–253. [Google Scholar] [CrossRef]

- Durand, R.; Bruyaka, O.; Mangematin, V. Do science and money go together? The case of the French biotech industry. Strateg. Manag. J. 2008, 29, 1281–1299. [Google Scholar] [CrossRef] [Green Version]

- Arrow, K. Economic welfare and the allocation of resources for invention. In The Rate and Direction of Inventive Activity: Economic and Social Factors; Nelson, R.R., Ed.; Princeton University Press: Princeton, NJ, USA, 1962; pp. 609–626. [Google Scholar]

- Pisano, G.P. Science Business: The Promise, the Reality, and the Future of Biotech; Harvard Business Press: Brighton, UK, 2006. [Google Scholar]

- Buisseret, T.J.; Cameron, H.M.; Georghiou, L. What difference does it make? Additionality in the public support of R&D in large firms. Int. J. Technol. Manag. 1995, 10, 587–600. [Google Scholar]

- Kang, K.N.; Park, H. Influence of government R&D support and inter-firm collaborations on innovation in Korean biotechnology SMEs. Technovation 2012, 32, 68–78. [Google Scholar]

- Brander, J.A.; Du, Q.; Hellmann, T. The effects of government-sponsored venture capital: International evidence. Rev. Financ. 2015, 19, 571–618. [Google Scholar] [CrossRef]

- OECD. Innovation in Science, Technology and Industry: Key Biotechnology Indicators (Last Updated in October 2018). 2018. Available online: http://www.oecd.org/innovation/inno/keybiotechnologyindicators.htm (accessed on 3 December 2018).

- Biotech Policy Research Center of the Republic of Korea. Biotechnology in Korea 2014. Available online: http://www.bioin.or.kr/board.do?num=247328&cmd=view&bid=w_paper&cPage=1&cate1=all&cate2=all2 (accessed on 30 January 2019).

- Hsu, F.M.; Horng, D.J.; Hsueh, C.C. The effect of government-sponsored R&D programmes on additionality in recipient firms in Taiwan. Technovation 2009, 29, 204–217. [Google Scholar]

- Luukkonen, T. The difficulties in assessing the impact of EU framework programmes. Res. Policy 1998, 27, 599–610. [Google Scholar] [CrossRef]

- Georghiou, L.; Clarysse, B.; Steurs, G.; Bilsen, V.; Larosse, J. Making the difference-the evaluation of behavioural additionality of R&D subsidies. IWT-STUDIES 2004, 48, 7–20. [Google Scholar]

- Roper, S.; Hewitt-Dundas, N.; Love, J.H. An ex ante evaluation framework for the regional benefits of publicly supported R&D projects. Res. Policy 2004, 33, 487–509. [Google Scholar]

- Clarysse, B.; Moray, N. A process study of entrepreneurial team formation: The case of a research-based spin-off. J. Bus. Ventur. 2004, 19, 55–79. [Google Scholar] [CrossRef]

- Georghiou, L.; Clarysse, B. Introduction and synthesis. In Government R&D Funding and Company Behaviour, Measuring Behavioural Additionality; OECD Publishing: Paris, France, 2006; pp. 9–38. [Google Scholar]

- Hall, L.A.; Bagchi-Sen, S. An analysis of R&D, innovation and business performance in the US biotechnology industry. Int. J. Biotechnol. 2001, 3, 267–286. [Google Scholar]

- Hall, L.A.; Bagchi-Sen, S. A study of R&D, innovation, and business performance in the Canadian biotechnology industry. Technovation 2002, 22, 231–244. [Google Scholar]

- Casper, S. Institutional frameworks and public policy towards biotechnology: Can Asia learn from Europe? Asian Bus. Manag. 2009, 8, 363–394. [Google Scholar] [CrossRef]

- David, P.A.; Hall, B.H.; Toole, A.A. Is public R&D a complement or substitute for private R&D? A review of the econometric evidence. Res. Policy 2000, 29, 497–529. [Google Scholar] [Green Version]

- Hayashi, T. Bibliometric analysis on additionality of Japanese R&D programmes. Scientometrics 2003, 56, 301–316. [Google Scholar]

- Almus, M.; Czarnitzki, D. The effects of public R&D subsidies on firms’ innovation activities: The case of Eastern Germany. J. Bus. Econ. Stat. 2003, 21, 226–236. [Google Scholar]

- Czarnitzki, D.; Licht, G. Additionality of public R&D grants in a transition economy. Econ. Transit. 2006, 14, 101–131. [Google Scholar]

- Einio, E. The Effect of Government Subsidies on Private R&D: Evidence from Geographic Variation in Support Program Funding; HECER Discussion Papers No. 263; HECER: Helsinki, Finland, 2009. [Google Scholar]

- Görg, H.; Strobl, E. The effect of R&D subsidies on private R&D. Economica 2007, 74, 215–234. [Google Scholar]

- Branstetter, L.; Sakakibara, M. Japanese research consortia: A microeconometric analysis of industrial policy. J. Ind. Econ. 1998, 46, 207–233. [Google Scholar] [CrossRef]

- Lee, C.Y. The differential effects of public R&D support on firm R&D: Theory and evidence from multi-country data. Technovation 2011, 31, 256–269. [Google Scholar]

- Hong, J.; Feng, B.; Wu, Y.; Wang, L. Do government grants promote innovation efficiency in China’s high-tech industries? Technovation 2016, 57–58, 4–13. [Google Scholar] [CrossRef]

- Czarnitzki, D.; Hussinger, K. Input and output additionality of R&D subsidies. Appl. Econ. 2018, 50, 1324–1341. [Google Scholar]

- Marino, M.; Lhuillery, S.; Parrotta, P.; Sala, D. Additionality or crowding-out? An overall evaluation of public R&D subsidy on private R&D expenditure. Res. Policy 2016, 45, 1715–1730. [Google Scholar]

- Aerts, K.; Schmidt, T. Two for the price of one?: Additionality effects of R&D subsidies: A comparison between Flanders and Germany. Res. Policy 2008, 37, 806–822. [Google Scholar]

- Bérubé, C.; Mohnen, P. Are firms that receive R&D subsidies more innovative? Can. J. Econ. 2009, 42, 206–225. [Google Scholar]

- Cantner, U.; Kösters, S. Picking the winner? Empirical evidence on the targeting of R&D subsidies to start-ups. Small Bus. Econ. 2012, 39, 921–936. [Google Scholar]

- Bronzini, R.; Piselli, P. The impact of R&D subsidies on firm innovation. Res. Policy 2016, 45, 442–457. [Google Scholar]

- Szczygielski, K.; Grabowski, W.; Pamukcu, M.T.; Tandogan, V.S. Does government support for private innovation matter? Firm-level evidence from two catching-up countries. Res. Policy 2017, 46, 219–237. [Google Scholar] [CrossRef]

- Guo, D.; Guo, Y.; Jiang, K. Government-subsidized R&D and firm innovation: Evidence from China. Res. Policy 2016, 45, 1129–1144. [Google Scholar] [Green Version]

- Buchmann, T.; Kaiser, M. The effects of R&D subsidies and network embeddedness on R&D output: Evidence from the German biotech industry. Ind. Innov. 2019, 26, 269–294. [Google Scholar]

- Zhang, J.; Guan, J. The time-varying impacts of government incentives on innovation. Technol. Forecast. Soc. Chang. 2018, 135, 132–144. [Google Scholar] [CrossRef]

- Feldman, M.P.; Kelley, M.R. The ex ante assessment of knowledge spillovers: Government R&D policy, economic incentives and private firm behavior. Res. Policy 2006, 35, 1509–1521. [Google Scholar]

- Audretsch, D.B.; Link, A.N.; Scott, J.T. Public/private technology partnerships: Evaluating SBIR-supported research. Res. Policy 2002, 31, 145–158. [Google Scholar] [CrossRef]

- Eisenberg, R.S. Public research and private development: Patents and technology transfer in government-sponsored research. VA Law Rev. 1996, 82, 1663–1727. [Google Scholar] [CrossRef]

- Hu, A.G.; Jefferson, G.H.; Jinchang, Q. R&D and technology transfer: Firm-level evidence from Chinese industry. Rev. Econ. Stat. 2005, 87, 780–786. [Google Scholar]

- Johnson, W.H. Roles, resources and benefits of intermediate organizations supporting triple helix collaborative R&D: The case of Precarn. Technovation 2008, 28, 495–505. [Google Scholar]

- Lerner, J. When bureaucrats meet entrepreneurs: The design of effective public venture capital programmes. Econ. J. 2002, 112, F73–F84. [Google Scholar] [CrossRef]

- Link, A.N.; Scott, J.T. Private investor participation and commercialization rates for government-sponsored research and development: Would a prediction market improve the performance of the SBIR programme? Economica 2009, 76, 264–281. [Google Scholar] [CrossRef]

- Hünermund, P.; Czarnitzki, D. Estimating the causal effect of R&D subsidies in a pan-European program. Res. Policy 2019, 48, 115–124. [Google Scholar]

- Bach, L.; Matt, M.; Wolff, S. How do firms perceive policy rationales behind the variety of instruments supporting collaborative R&D? Lessons from the European Framework Programs. Technovation 2014, 34, 327–337. [Google Scholar]

- Carayannis, E.G.; Alexander, J.; Ioannidis, A. Leveraging knowledge, learning, and innovation in forming strategic government–university–industry (GUI) R&D partnerships in the US, Germany, and France. Technovation 2000, 20, 477–488. [Google Scholar]

- Cyert, R.M.; Goodman, P.S. Creating effective university-industry alliances: An organizational learning perspective. Organ. Dyn. 1997, 25, 45–57. [Google Scholar] [CrossRef]

- Etzkowitz, H. Innovation in innovation: The triple helix of university-industry-government relations. Soc. Sci. Inf. 2003, 42, 293–337. [Google Scholar] [CrossRef]

- Liu, M.C.; Wen, F.I. Research institutes and R&D subsidies: Taiwan’s national innovation system and policy experiences. Int. J. Technoentrep. 2011, 2, 240–260. [Google Scholar]

- Greco, M.; Grimaldi, M.; Cricelli, L. Hitting the nail on the head: Exploring the relationship between public subsidies and open innovation efficiency. Technol. Forecast. Soc. Chang. 2017, 118, 213–225. [Google Scholar] [CrossRef]

- Lin, C.; Wu, Y.J.; Chang, C.; Wang, W.; Lee, C.Y. The alliance innovation performance of R&D alliances-The absorptive capacity perspective. Technovation 2012, 32, 282–292. [Google Scholar]

- Sakakibara, M. Heterogeneity of firm capabilities and cooperative research and development: An empirical examination of motives. Strateg. Manag. J. 1997, 18, 143–164. [Google Scholar] [CrossRef]