The COVID-19 Impact on Supply Chains, Focusing on the Automotive Segment during the Second and Third Wave of the Pandemic

1

Faculty of Social Sciences, Eötvös Loránd University, 1053 Budapest, Hungary

2

Doctoral School on Safety and Security Sciences, Óbuda University, 1081 Budapest, Hungary

3

Keleti Károly Faculty of Business and Management, Óbuda University, 1081 Budapest, Hungary

*

Author to whom correspondence should be addressed.

Risks 2022, 10(10), 189; https://doi.org/10.3390/risks10100189

Submission received: 17 June 2022

/

Revised: 10 August 2022

/

Accepted: 18 September 2022

/

Published: 28 September 2022

(This article belongs to the Special Issue New Advance of Risk Management Models)

Abstract

:In the last few years, there have been several big changes in the automotive industry, and global automotive supply chains have faced many challenges, mainly due to the COVID-19 epidemic. The virus had several huge impacts on the global market, with different risk management approaches companies and global supply chains needed to adapt to the altered situation. During the second and third wave of the epidemic, several regions and countries were under lockdown for different intervals in order to stop the spread of the virus. Some countries entered lockdown for the first time, and many of them entered lockdown again, as when the first wave occurred. The economy of the Philippines is dependent on electronics-related industries, which faced extraordinary risks from different sources, and these industries suffered severe consequences because of COVID-19. Crucial automotive suppliers outsource their production facilities to the Philippines region, and the dominant semiconductor segments were heavily impaired due to the lockdowns. Electrification in the automotive industry and the spread of electric vehicles is becoming increasingly important due to rapid technological development. The economic shock caused by COVID-19 forced companies in this sector to diversify their supply chain activities in order to stay competitive, minimize the supply chain-related risks and to start recovery processes. The authors analysed the risks, position, opportunities, challenges, difficulties, reactions and solutions of a certain automotive supplier, which was heavily reliant on the Philippines, and Chinese suppliers.

1. Introduction

The global issues caused by COVID-19 spiralled out of control at the beginning of 2020. After the quick spread of the virus, many aspects of economic and social life changed dramatically all around the world. First Asian countries, then the rest of the world, started to introduce several restrictions in order to slow down the pandemic. Many companies and entrepreneurs needed to suspend their production and service activities, certain public institutions were temporarily closed, and as a consequence, many people were forced to stay at home as a primary safety measure. Because of this, many employees lost their jobs and businesses had a very tough time paying their expenses while not being able to earn enough profit. These circumstances and actions drastically changed everyday life almost everywhere in the world (Cramarenco 2020).

As many industries depend on each other, these events made it very difficult to react to uncertainty and risks which had never been experienced before. Previous major economic crises were different, in a way, because during those times the health status of masses of people was not in direct danger because of an epidemic; therefore different factors and aspects need to be considered in order to approach this situation. This virus had an extraordinary impact on the electronics industry in the regions of Southeast Asia, which had, and still has, major effects on the European region as well.

A stable and secure supply of metals and other raw materials is essential to technological, economic, and social development. Value chains that supply raw materials are global, economically complex, and involve hundreds of stakeholders. However, the supply chains of metals can be disrupted by physical barriers, market fluctuations, and geopolitical debates. In 2020, COVID-19 caused huge risks and new kinds of disruptions in raw material supply chains. From early 2020, governments around the world introduced strict measures, the most significant being various forms of quarantine, where the majority of industry, educational institutions, shopping malls, and other non-emergency businesses were closed. COVID-19 also had a decisive impact on the development and strategies of European countries and governments. The economic and social effects of the closure have resulted in a dramatic shock to the supply and the demand for both raw materials and key metals for the economy. In mining areas in 2020, “maintaining good relations with local stakeholders will protect plant closures and associated supply disruptions” may not be an entirely surprising approach, but it has received significantly more attention in response to ensuring production flexibility. The main difference in 2020 compared to the past is that the actors of the supply chain are different. Until then, the lower-end users suffered from different sources of risks and supply chain disruptions, and they had to respond to it, now upper level suppliers and actors are also adapting to maintain flexibility (Habib et al. 2021; Wojtas and Walecka 2020).

Suppliers of traded services reported three times as many jobs as suppliers of traded manufactured goods (20% compared to the 7% employment of the U.S.A). Surprisingly, the supply chain traded services subcategory has the highest wage and STEM intensity in the economy. While most patents are held by manufacturing vendors, vendors of marketed services have the highest incidence of STEM occupations (59% of STEM jobs and only 9% of patents). In the B2C sector, manufacturing employment has also declined, mainly due to growth in local services (health and “Main Street”). The B2C main street subcategory (for example traditional consumer services such as retail stores and restaurants) grew rapidly in terms of employment, but experienced the lowest wage growth. During the Dotcom crisis (2000–2002) and the Great Depression (2007–2009), annual employment growth in the supply chain category declined significantly more than in the B2C category, but the supply chain category grew faster in the pre- and post-recession period than the B2C category. During the Great Recession (2007–2009), average annual employment growth was much lower in the supply chain category than in the B2C category (−4.7% vs. −0.8%). Higher cyclicality in the supply chain category results in wage growth. The economy of the supply chain is bigger, has higher wages, more STEM intensity, and more patents than the B2C industry. By separating commercial suppliers into production and services, the subcategory of services distributed in the supply chain (such as design, engineering, and cloud computing services) is very large and has most STEM occupations but low patentability. Looking at the dynamics of growth in the supply chain economy, employment has moved away from production towards the trade in services (Delgado and Mills 2020; Kilay et al. 2022).

The coronavirus epidemic of 2019 (COVID-19) has brought huge social and economic changes. The risk management and governmental responses around the world have been extraordinary; from financial stimulus packages to unprecedented restrictions on social distance and a ban on international travel. Border control and mobility restrictions have been widely approved to limit the spread of the virus. The crisis has raised questions about the need for business travel, provided a political basis for nativists in favour of greater protectionism and stricter border controls, and disrupted international supply chains. For decades, cheap supply and minimal stocks have been the main part of supply chain management. However, as COVID-19 has demonstrated, in an increasingly volatile world over-reliance on the above factors means vulnerability. The three main drivers of supply chain fragility at the organizational level are consolidated production centres, reduced inventory levels, and a lack of supply chain transparency. COVID-19 is likely to favour long-term flexibility rather than short-term efficiency (planning for quarter year). The growing number of natural disasters, climate crises, epidemics, or other shocks is likely to lead to further risks and greater functional redundancy in supply chains. The challenge is to find the right balance between a lean, efficient supply chain that does not carry a surplus (ideal for a just-in-time stock system) but is sensitive and suited to unexpected shocks. This includes rethinking stock management in a timely manner and computing technologies (Free and Hecimovic 2021; Barbosa et al. 2022; Reyna-Castillo et al. 2022).

COVID-19 negatively affects how companies can identify and assess supply chain risk due to global disruptions that few companies have been able to predict. COVID-19 affected supply chain security/continuity/firmness, with a short-term negative impact (Aday and Aday 2020; Chowdhury et al. 2021). However, supply chain sustainability has not been directly affected by disruptive effects, as most companies believe they have been able (or will be able) to recover and regain the previous performance of their supply chain. It can be seen that the risk identification of the supply chain plays a key role, which requires cooperation with partners at different stages of the supply chain, as well as the sharing of knowledge during the process. (El Baz and Ruel 2021; Shekarian et al. 2022).

The COVID-19 epidemic highlighted the importance of how perceptions of value can change rapidly. COVID-19 has uncovered not only the fragility of the food supply chain, but also its hidden ability and flexibility to adapt and protect the health and safety of consumers and employees in a case of a disruption. The focus on health and safety, as well as the focus on well-being, has also suddenly received significant attention from companies, decision-makers, and consumers equally (Mollenkopf et al. 2020).

“The food supply chain (which would actually be better called a network) is an extremely complex thing that interacts with a wide variety of natural, economic, demographic, cultural and political factors.” (Bőgel 2020). Presumably, as a result of the virus, the actors in the supply chains will work with higher stock levels in the future, thus emphasizing resilience and adaptability. “Where possible, stock levels will be higher, security stocks, alternative sources of supply and distribution channels will increase, and the role of capacities that can be flexibly expanded or reduced will increase. Business plans will give more space to risk analysis and alternative scenarios.” (Bőgel 2020). If companies considering the coverage of food supply from internal sources come to the view that they should reduce risk, supply chains may be shortened and the number of actors may decrease.

Trends in the organization of economic value creation include: regionalization of international value creation, shortening of supply chains, multi-centering of suppliers and increasing the level of security stocks, production of several products instead of one product, creation of coordination centers for the operation of supply chains, digitization, and intensification of automation (Hausmann 2020).

The more significant the adaptability of the BCES (blockchain-enabled circular economy system), the more appropriate the LAD (localization, agility, digitalization) capabilities. Size of the organization and the field of the industry influence the relationship between the BCES and the LAD (Nandi et al. 2021).

Successful store network opportunity management is critical for organizations to guarantee the dynamic flow of their production network (Pitchaiah et al. 2021).

According to some ideas in the post-COVID-19 period, in the event of the next global pandemic, it will not be a transformation of the resilient supply chain which is accepted as the new normal, but an extension of traditional and ongoing efforts (Ishida 2020).

The epidemic highlighted the importance of a coordinated approach to entrepreneurship, supply chain management and strategic management issues for both companies and researchers. For example, as a result of the ban on public gatherings, restaurants were unable to offer their main service, the experience of dining in a restaurant. In addition, they have struggled to obtain basic supplies such as beef and pork, for which there have been no shortages so far. These two supply chain challenges have led restaurants to look for new opportunities to reach customers (so-called entrepreneurship) and steer their business models to new sources of potential competitive advantage (i.e., strategic management). (Ketchen and Craighead 2020).

Electric mobility, self-driving cars, automated factories, and car-sharing are just some of the key disruptions the car industry faced even before the COVID-19 events. Many recent developments of the COVID-19 situation may cause concern. For example, the COVID-19 crisis has forced about 95 percent of all German automotive companies to put their workforce on short-term jobs during downtime, which has led to workers being laid off temporarily and receiving a significant portion of their pay through the government. Prior to the COVID-19 crisis, automotive players were uncertain about the use of digital channels, while companies in other industries made progress aggressively. Industries generally recognize that long-distance selling models will become “normal” in the future, and some players in the industry are already preparing to adopt this model in response to consumer demand. Companies need to focus on specific areas to make their supply chains more resilient after this epidemic. For example, they must carry out strict controls on the health and safety of the workers, and monitor the interactions and the problems. They need to build trust among key stakeholders, relaunch operations based on demand-based data and analysis, and based on transparent supply chains. Overall, organizations should not return to business-as-usual, but should restart with new, faster processes and tools, as well as comprehensive, agile techniques. (Hofstätter et al. 2020).

When automotive production suddenly stopped in March, new vehicles were only produced again in early May. Even then, production progressed rapidly. At the same time, consumers continued to buy vehicles while demand for cars remained surprisingly strong in an uncertain economy, where supply chains faced huge risks in the market. OEM conveyors tried to switch to full production. While suppliers tried to reach the previous level of supply, they were held back by their own planned global supply chains. The situation was complicated by the fact that the parts came from Asia, mainly from China. Trade disputes with China have not helped either. COVID-19 has shown how vulnerable the global supply chain can be in the midst of disruptions, disasters, and crises (Gifford 2020).

Months before the outbreak of COVID-19, global automakers were already thinking about localizing the production of their critical components. The tax war between the United States and China has peaked, causing trade tensions. The intensity of protectionism, through targeted financial trade barriers, has become a real and current threat to multinational car operators that need to pay attention to this threat. Today, most of the leading global automakers source 30–60% of their parts from China (Bhat 2021; Ye and Lau 2022).

An interwired supply network (ISN) is a set of interconnected supply chains (SCs) that, in their integrity, ensure the supply of goods and services to society and the market. The latest example of the COVID-19 epidemic shows that in case of an unexpected global event, the resilience of SCs to disturbances should be considered on a scale of survival or viability to avoid collapse of SCs and the market and to ensure supply of goods and services (Ivanov and Dolgui 2020).

The lean supply chain, which relies on just-in-time and zero stock management strategies, is over-exposed to disruptions caused by the epidemic. Before the epidemic, the efficient long-term inventory strategy was to operate with as low an inventory as possible, only ordering the necessary parts, and using them for production processes as soon as they arrived. Because of the mentioned vulnerability to the uncertainties and risks caused by the global market situation, this may no longer be an efficient way to secure key components and materials. (Balogh et al. 2020).

Building agility is an expensive practice and it would not be appropriate for companies to completely transform their supply chains to deal with “black-swan” events such as the COVID-19 virus. With greater emphasis on excellent communication mechanisms and effective information transfer between suppliers and customers, partnerships are intensifying to respond more quickly to changes in the operating environment. Thus, the focus shifts from cost savings in lean SCM to value creation in an agile SCM. To incorporate greater agility, companies may consider implementing risk management strategies that take into account procurement dependencies and introduce “buffers” to reduce the effects of unexpected events (McMaster et al. 2020).

The advantages of the lean philosophy and agility in supply chain management enables not just different levels of efficiencies, but also security and flexibility, which are crucial to react to market changes, demand-related changes, and enable proactive strategies as well. It also enhances supply chain risk management processes and opportunities, which are essential to mitigate the damages of events such as COVID-19 (Upadhyay et al. 2022).

The pandemic has caused an international economic crisis. “Sectors based on personal interactions (tourism, catering, personal and cultural services) collapsed immediately, but other sectors such as processing industry also suffered great damage. Even those sectors whose demand for their products more or less survived did not have access to the inputs needed for production due to the difficulties of crossing borders, which limited their production. The international production and supply chains that developed in the years before the crisis, which networked the world and became an important component of world production, were suddenly disrupted or stalled.” (Palócz and Matheika 2020). There was a setback in industry (industrial export sales fell by 38% between April and May), construction and services (transport and warehousing fell by more than 20%—due to travel restrictions and curfews, interruptions in foreign trade in goods, etc.). The closure of the border in September did not help the tourism industry either. Forecasts assumed an economic recovery in 2021, but it should not be forgotten that the coronavirus is still present, which will affect and hold back some sectors (such as tourism).

2. Objectives and Methodology

2.1. Case Study Section Review

The authors use the case study methodology, where they focus on certain aspects of the chosen company, which is a multinational automotive supplier. It is globally present in more than 15 countries with a total of more than 50,000 pcs employees with a revenue of more than 1 billion EUR/USD. The authors conducted the interviews and participant observations in 2021.

In general, in case studies the area of research can be a period of time, a group of people, or a company, but the main point is that the target of the study is narrowed down to a certain example. A case study can be descriptive, when the details of a certain example are described, or it can be explanatory, in which case the goal is to understand, for example, the processes, the reactions, or the structure of a firm (Babbie 2003).

In this research, the authors conducted interviews with the experts and leaders of the different analysed areas of the chosen company and, based on the various information that was collected during the interviews and during the participant observation, they created a case study about an automotive supplier, which was affected by COVID-19 challenges. The focus areas of the study were the flexibility and decision-making challenges of the supplier, the different HR difficulties, the demand-related forecast and transportation challenges and, last but not least, the topic of diversification and the related sourcing challenges.

2.2. Interview Section Review

The goal of the authors is to identify, analyse and interpret the COVID-19 related challenges and also the reactions, strategies and solutions of the chosen automotive company to overcome the difficulties. This is a new and relatively uncharted issue, as COVID-19 may only be present for around 3 years, and the authors want to explore the possibilities of how to overcome the different related challenges.

During the research, the authors conducted unstructured, open format interviews as well with several experts in related fields, in order. The interviews took place during September 2021, when the authors had free-form conversations with the relevant experts. The questions were related to the five major areas which are described in the case study in detail. The aim of the interviews was to obtain a better picture of the related challenges and the applied solutions of the company, and to strengthen the participant observation section of the study and uncover further relevant and important information. (Dana et al. 2013). Five interviews were conducted in three major departments, which are relevant for this research: supply chain management, logistics, and human resources, and the summary can be seen below in Table 1. Each of these interviews was about two hours long.

As the participants and the selected company asked for anonymity, further details cannot be shared about the company or about the participants.

3. The Consequences of the Epidemic in the Philippines

In the Southern Asian region, the Philippines is one the key targets for foreign investors to outsource production facilities and processes due to its location and advantages. Because of the cutting edge global competition, multinational companies try to exploit the competitiveness of the countries, and in this case the human resource cost of the Philippines is below average. The other advantage is the quality of the manpower. The second language in the country is considered to be English, enabling the smooth transition of work from other countries, and the English business language overcomes the challenges of language barriers, which can be the decisive factor of the outsource location. As a consequence, there has been a substantial amount of foreign investment starting from the beginning of the 21st century (Intarakumnerd et al. 2010).

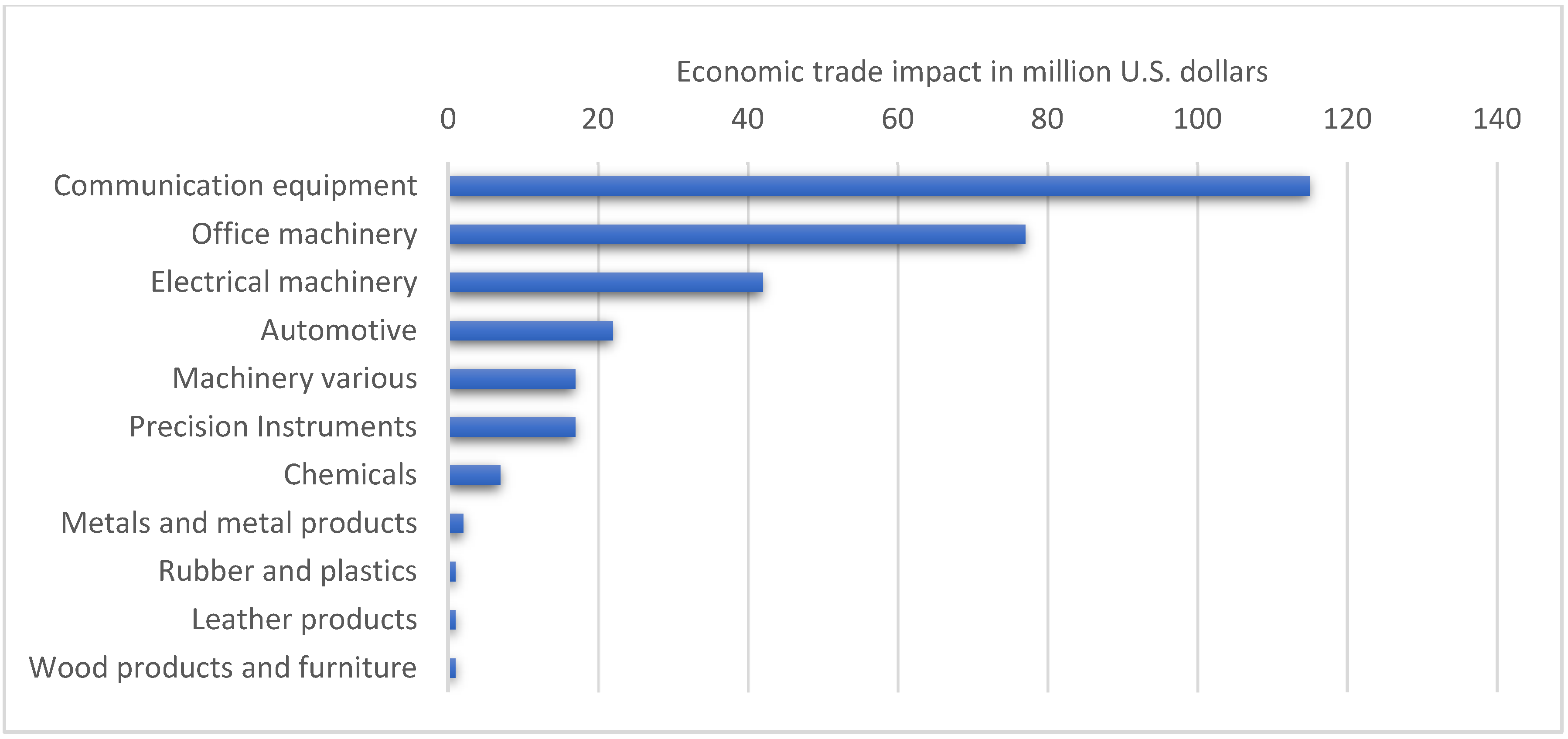

Many major electronics-related, mainly semiconductor, suppliers have been increasing their presence in the Southeast region of Asia, especially in the Philippines. The importance of the Philippines to electronics-related businesses is substantially increasing because of the growing demand for different semiconductor-related products, mainly electronic devices in the field of transportation, computing, communications, healthcare, energy, and in other similar areas. Due to the extraordinary technological development and the electrification in the automotive industry, this region has become one of the strategic locations for sourcing related supply chain activities while minimizing risks. The products of Philippine industries are further processed in supply chains, mainly in China. The Chinese presence in electronics-related industries is becoming more influential because of the increased outsourcing of core production processes, ranging from surface-mounted technology (SMT) production to full box builds to China. Because of all of these factors, the COVID-19 impact on the Philippines caused severe supply issues and risks in global supply chains, especially in the Chinese region (Caldwell et al. 2021). See Figure 1.

During the second wave of COVID-19, there were long lockdowns in the Philippines region, and during the third wave there was also another severe quarantine, which was extended due to infections, heavily impairing the automotive industry as well. The semiconductor industry was highly dependent on this region, and as a consequence, due to the production suspensions, delays, material issues and the lack of transport options, this issue affected the global automotive supply chains as well. Because of the supply chain disruptions and the related risks, the companies that outsourced their production to the Philippines had to find alternative ways to satisfy the customers’ demands in order to avoid major negative consequences. Although this could be considered to be a vis major case, everything still needed to be done in order to avoid global supply chain issues, especially in those cases where the negative effects could be seen in advance. In the automotive market, mainly in electronics, there are several distributor and broker companies, who stockpile different materials, semi-finished and finished products, in order to sell these with a high profit margin. Members of the supply chains can also provide support with their own stock to help their business partners. These stocks located all around the world could be used to mitigate the negative consequences of these situations (Kumar and Sharma 2021).

Diversification could be another alternative solution, which means that a part of the production is sourced to another area. Global allocation between partners could also be a positive approach to keep production running based on different priorities. These practices were actively used during the third wave of the COVID-19 lockdown in the Philippines, and in the Chinese region as well, by members of global automotive supply chains. Despite the fact that these methods were applied in order to minimize the different risks, the transport costs were exceptionally high, as air freight, especially hand carries and NFO services, had to be extensively used in order to supply the customers in time (Lin et al. 2021).

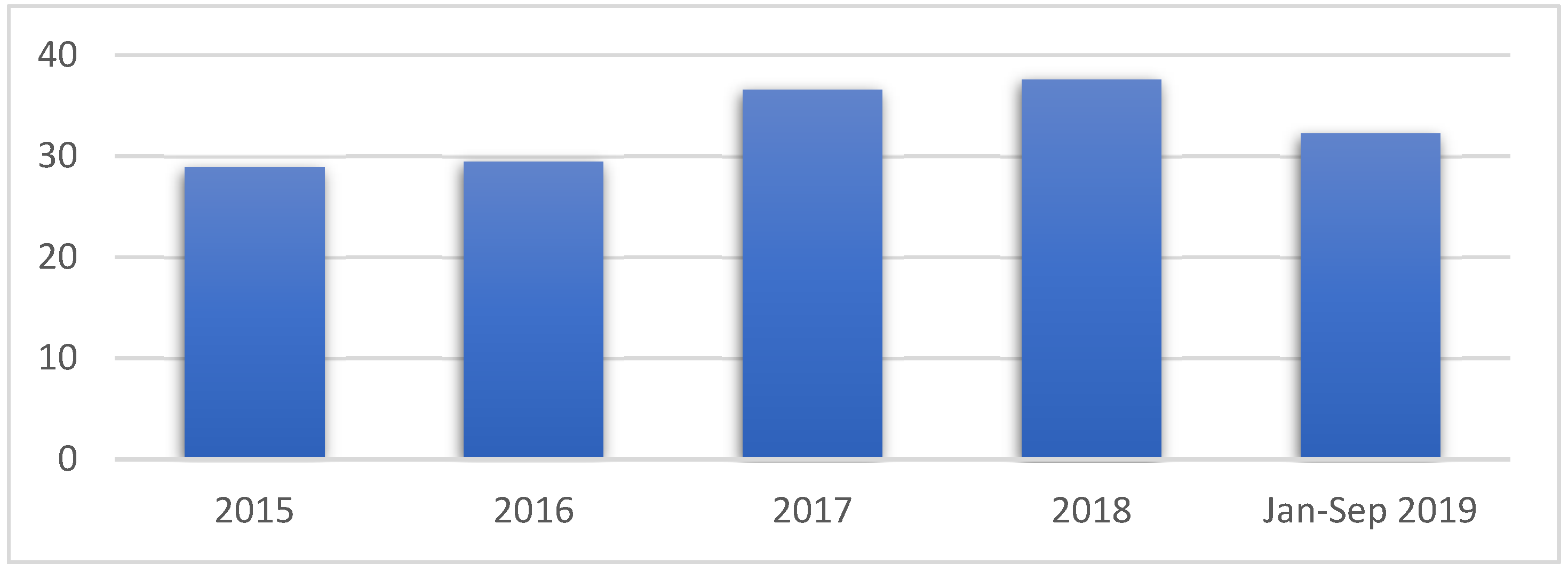

The electronics and semiconductor manufacturing industries are among the most important ones in the Philippines; these contribute the most to economic growth in the country. The ratio of the semiconductor manufacturing firms to electronics manufacturing firms is around 3 to 1. There are more than 3 million direct or indirect employees in this sector. The steady growth of electronics exports can be seen at Figure 2. This segment produces more than 50% of the country’s total exports (Las Marias 2019).

Considering all of these, the negative consequences of COVID-19 affect not only the mentioned global supply chains, the virus presents outstanding challenges to the country in all aspects of life.

4. The Importance of Electrification

Electric car sales started to skyrocket in 2018 and 2019, while the traditional internal combustion engine models kept their popularity. Most of the electric two wheelers are used in China and India and they are also widespread in the ASEAN countries. Electric micro-mobility is also becoming more attractive, mainly in the large cities. The number of electric buses and trucks is also becoming more significant; in this case China is also the biggest market for these vehicles. There are several cities where the whole bus fleet is fully or almost fully electrified. The production of electric buses is also present in Europe, India, Latin America, in addition to the Chinese region. The electrification of shipping and aviation is also in progress (IEA 2021).

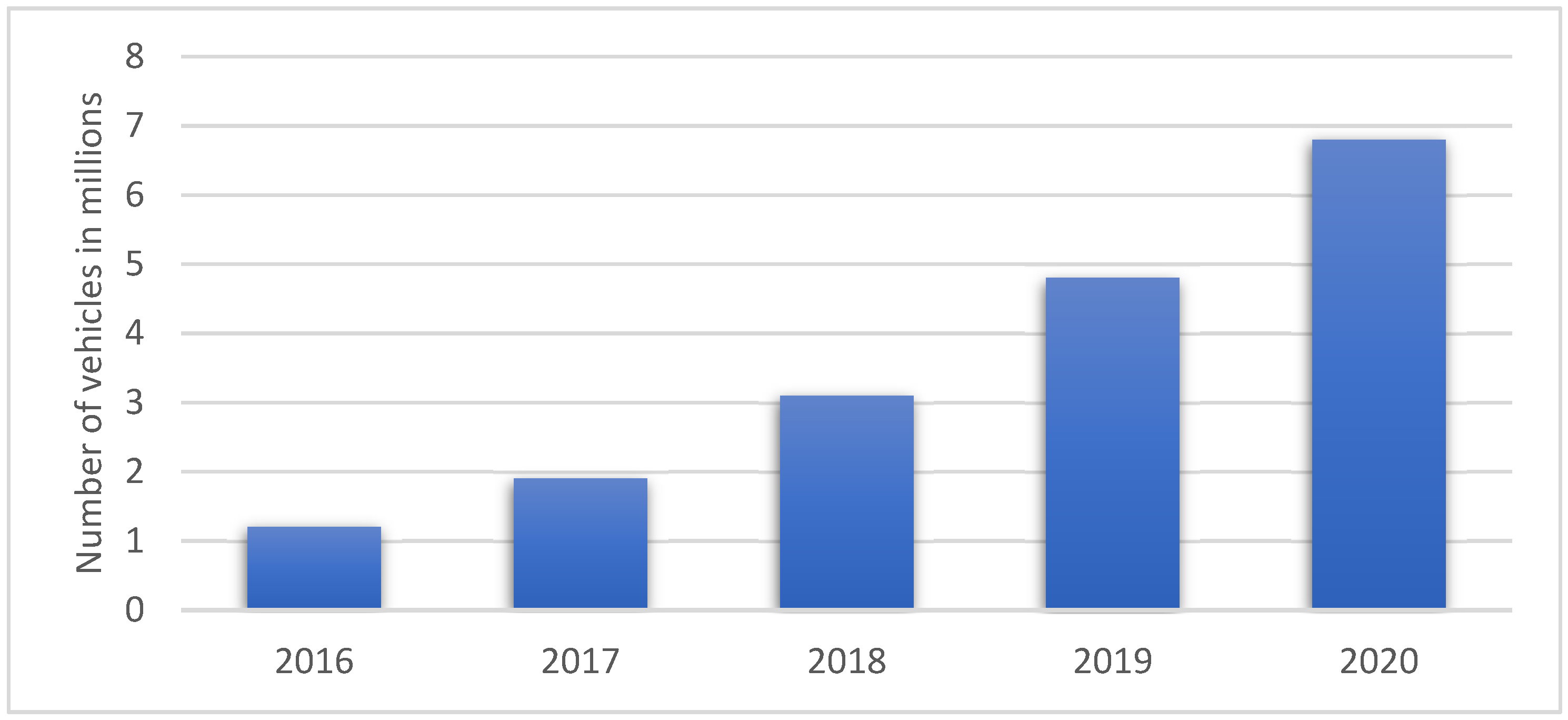

Besides the electrification of vehicles and other modes of transports, the importance of technologies related to robots are also crucial for development. In supply chain and logistics-related processes there are many areas where automation has an essential role. Warehouse and transport electric robots and droids, either semi-autonomous or autonomous, are becoming an essential part of modern processes. They enable efficiency levels that could not have been reached with older technologies or non-electric solutions (Khamis et al. 2021). See Figure 3.

In 2019, there were almost 5 million electric vehicles in use in the world. Compared to that, about 2 million new battery electric vehicles were added to the worldwide fleet in 2020. Because of the electric transmission, these vehicles are gaining recognition and acceptance on a worldwide level; it is the goal of many car maker companies to follow this direction. The electrification process is a new and innovative approach. Tesla is among the leading battery electric vehicle sellers. Tesla took this advantage and followed the path of designing and assembling electric vehicles exclusively. China is the biggest consumer of all-electric vehicles, and this was further empowered by government actions, which include exemptions from tolls or even from parking fees.

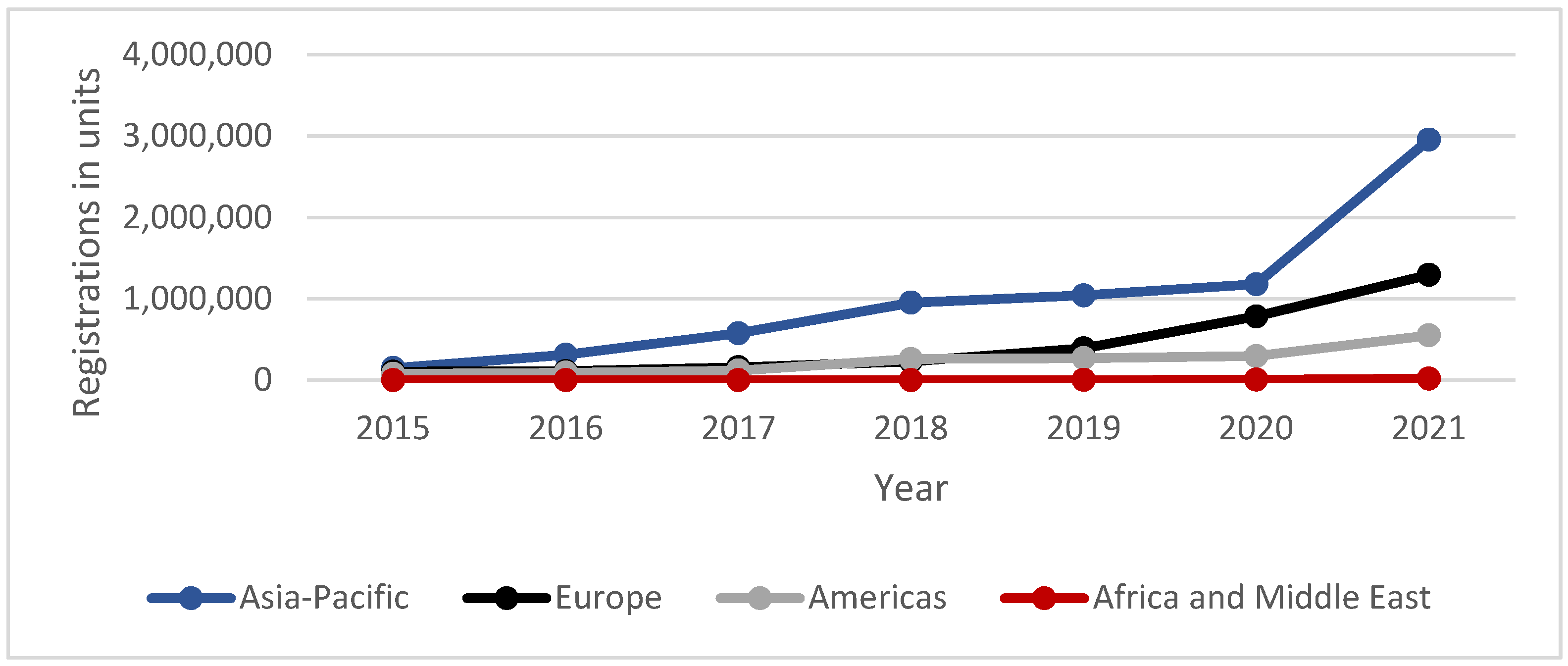

At Figure 4 it can be observed that the majority of the battery electric vehicle registrations are mainly in the Asia-Pacific region, reaching almost 3 million units in 2021, more than doubling the amount compared to 2020. European registrations are also increasing rapidly since 2020; in that year registrations almost reached the level of the Asia-Pacific region. The Americas, Africa, and Middle East regions are showing a growing trend as well, but the rate is not that high compared to the Asia-Pacific and European regions.

5. Case Study—Automotive Supply Chain Difficulties Related to the Lockdowns in the Philippines

The authors analysed the status, challenges, risks, opportunities, and decisions of a key automotive supplier, which is reliant on the Philippines and Chinese supply, during the second and third wave of COVID-19. This company has been facing many difficulties, just like almost all the members of the global automotive supply chains since the beginning of 2020, but the most difficult period proved to be the second and third wave, for several reasons. In this case study, the different supply chain-related challenges of this company are presented.

5.1. Flexibility and Decision-Making Challenges

There has been a huge pressure on car makers and Tier 1 suppliers due to high performance expectations, even before the spread of COVID-19. As a consequence of the virus, there are several factors to be evaluated in order to understand the challenges.

Standardization is an efficient approach on different levels (Gerőcs and Pinkasz 2019) to control and manage the processes, information, and material flow, and almost every aspect of a certain subsidiary. Although it has its advantages in the area of cost efficiency, it also has a disadvantage when dealing with regional or plant-specific challenges and risks. Centralized decision-making can be inflexible when it comes to the unique challenges a certain plant has to face (Bhattacharya et al. 2014).

This inflexibility can lead to many issues, especially in the market situation caused by COVID-19. Validating totally new suppliers or new production facilities of current partners can be a slow and difficult process normally, being proactive with securing the supply is one of the key factors that proved to be efficient during the second and third waves for the company.

5.2. HR-Related Difficulties

The human resources areas of the logistics and supply chain activities were getting more critical due to the consequences and unforeseen risks of COVID-19. The workload of each individual was getting significantly higher, resulting in many hours of overtime.

In addition to the general challenges, motivating the employees and making sure to balance and support their health and welfare were key in order to achieve corporate goals and to keep integrity at all the levels of the organization (Azizi et al. 2021).

As the electronics-related segment of the Philippine economy has strategic importance, the different HR-related issues could have a severe impact. The morale and efficiency of both direct and indirect workers may be reduced due to high corporate pressure.

Sustainability of the operation is key (Yadav et al. 2020) but due to the lockdowns, many people lost their jobs, and when the government gave the green light to restart the production processes, new recruiting waves could be observed. On the other hand, for those who continued to work with exceptionally high loads, burnouts and seeking other opportunities were not uncommon among the employees. The fluctuation rate was rather high, and keeping key employees became harder as companies could not afford to provide sufficient salary increases due to the severe market conditions caused by COVID-19.

Digitalization is another important aspect which gained even more importance during the pandemic. This process enables a lot of opportunities both to employers and to employees as well. The different digital trainings, home office options, and workforce management have started to become a crucial part of overcoming pandemic-related challenges (Veluchamy et al. 2021).

The analysed company managed to solve the HR issues by reallocating the load on the complete supply chain team, while also keeping direct employees by reducing their weekly working days.

5.3. Forecasting Challenges

Another big challenge was related to forecasting. In this volatile market situation, where the workforce could not be fully secured as mentioned previously, and due to the extraordinary risks and dependency on certain governmental decisions, forecasting, and the related inventory and risk management was one of the top critical focuses of companies in global supply chains. Production load and sales commitments had to be aligned, which was a great challenge.

When there are a few critical bottleneck items for production, which has constant supply issues, and the other components keep arriving on time, then as a consequence a huge inventory, which has significant costs, (Yagi and Managi 2021) will be stockpiled, as the rate of the incoming materials is much higher than the production and outbound rate. Because of the uncertainty and risks caused by the virus, the end customer demand fluctuates as well (Gyenge et al. 2021).

As a consequence, the forecast stream coming from the car makers caused huge issues in the supply chains, starting a bullwhip effect. Every member of the supply chains has certain system settings based on their interests, which converts the received forecasts into production orders. Based on these, they drive the material supply, and as the information flow contains a high level of risk, most of the members either ended up with a lot of excess stock, or faced huge material shortages. The load and chase strategy was also used, when companies loaded a certain amount of demand in their system, sometimes ignoring the customer demand in order to avoid gaps in production (Yang et al. 2021).

This was against material management lean principles, such as just-in-time, but in some cases this was the only way of securing the critical items which were either on allocation, or where the suppliers had severe capacity constraints or raw material issues. Aside from this, many other lean management tools and philosophies were still crucial in the production processes. During these difficult times, the value from the customers’ point of view might have also changed. Before COVID-19, the inventory level of a firm added little to no value to customers, but during the second and third waves, having safety stock of certain critical components actually provided major benefits, and this was often acknowledged and requested by customers. In return, to compensate the higher inventory level, the customers financed a portion of the excess materials (Czifra et al. 2019).

Inventory financing is always a sensitive and difficult topic, even when negotiating with the closest customers. The chosen company for the case study successfully initiated this process with its key customers, where the load, commitments, inventory level and sales forecast had to be aligned. See Figure 5.

5.4. Transportation Challenges

The spread of COVID-19 forced governments to act in order to protect people and slow down the virus. The lockdowns started a whole new chapter in cargo transportation. Before 2020, sea and rail freight methods were preferred in the Asian region, while air freight options had huge disadvantages due to high costs and limited capacity. The need to return to normal business processes was clear, but many conditions have changed in the meantime (Budd and Ison 2020).

Lockdowns in many countries, including the Philippines and the Chinese regions, seriously impaired transport opportunities and movement of components (Raj et al. 2022) and, in parallel to this, also generated huge risks. In many cases, no inbound or outbound freight could be transported from different harbours, airports, or even from entire cities; some members of supply chains became isolated. Courier services quickly reached their capacity and much road freight could not reach certain destinations, so the flow of international freight was stunned. In the third wave, this also caused huge issues. Although there were some previous experiences from the previous waves, the members of global supply chains faced similar issues again. Container shortages started to cause even greater disruptions and cost increases in supply chains than before. The heavily increased demand in Asian–European routes, the decrease in the availability of free containers, the overbooking of many transport companies and the lack of capacity at harbours forced many companies to keep regularly using air freight to solve the supply issues. Instead of cost minimization efforts, the trend of securing production with sufficient materials became more dominant.

The chosen company for the analysis also had to conduct negotiations with key Asian suppliers, mostly in the Chinese and Philippines region, to diversify their production, and secure long-term supply options with the most trusted transport companies. See Figure 6.

5.5. Diversification and Sourcing Challenges

When production was shut down in China, new sources and alternatives needed to be found in order to keep production running and to reduce supply chain risks. Asian lockdowns were impacting the majority of global supply chains, as many companies still relied on the supply from China and the Philippines. As an alternative, several firms outsourced some or all of their production facilities to a different location, which could operate independently (Zhu et al. 2020).

In order to achieve the best possible results, the whole activity needed to be analysed with proper risk management approaches in order to achieve a successful transition from one location to another. Without these holistic preparations and planning, major operations could not guarantee success without dealing with different risks (Juhász et al. 2020).

In this case, Mexico was chosen as a target. Splitting the production with Mexico as well from the Philippines meant that even if the situation in the Southeast Asian region grew worse during the current wave, or at a later time, the opportunity to generate revenue elsewhere was created; however, different related risks also needed to be evaluated (Bacsi and Hollósy 2019).

This kind of diversification was unfavourable for the firm in the short run, as this kind of production transfer generates huge costs and risks, which need to be mitigated as much as possible (Mogos et al. 2019); this also means new opportunities for the company in the long run. In many cases, the procurement of a material is based on the mix of the quality, cost, capacity, and efficiency that can be provided by a supplier. There is often only one supplier, which seems to be the best choice for the company; however, there are some cases where the companies share their purchase orders between two or more suppliers. This might not be the best short-term solution, as the costs are usually higher in total, but this kind of multi-sourcing did help a lot during the earlier COVID periods, and it is still very efficient. Even if one supplier had any kind of disruption, the other suppliers could support production processes, so the multi-sourced materials had a much more secure supply overall.

5.6. Results of the Case Study

As a result of the case study, the authors identified the different challenges of the chosen automotive supplier. The validating process of new production sites and suppliers, the reallocation of the workload, inventory financing initiations, negotiations and close cooperation with the trusted partners, and last but not least splitting the sourcing and production have proven to be successful in overcoming pandemic-related challenges. During the analysis of the company, the authors identified key topics and areas which were the most impacted by COVID, did researches in the relevant literature, and in the conclusion section the actions and strategies of the chosen supplier are compared with the literature findings.

6. Conclusions

Reflecting on the literature regarding the standard issues in these areas the authors interpret the strategy and solutions of the analysed company based on participant observation and on conducted interviews with the experts and leaders of the relevant fields in Table 2.

In the literature, the approach of standardization (Gerőcs and Pinkasz 2019; Bhattacharya et al. 2014) is often reinforced by its various advantages, but at the chosen company the standard processes had negative effects on the validations due to the long approval procedures.

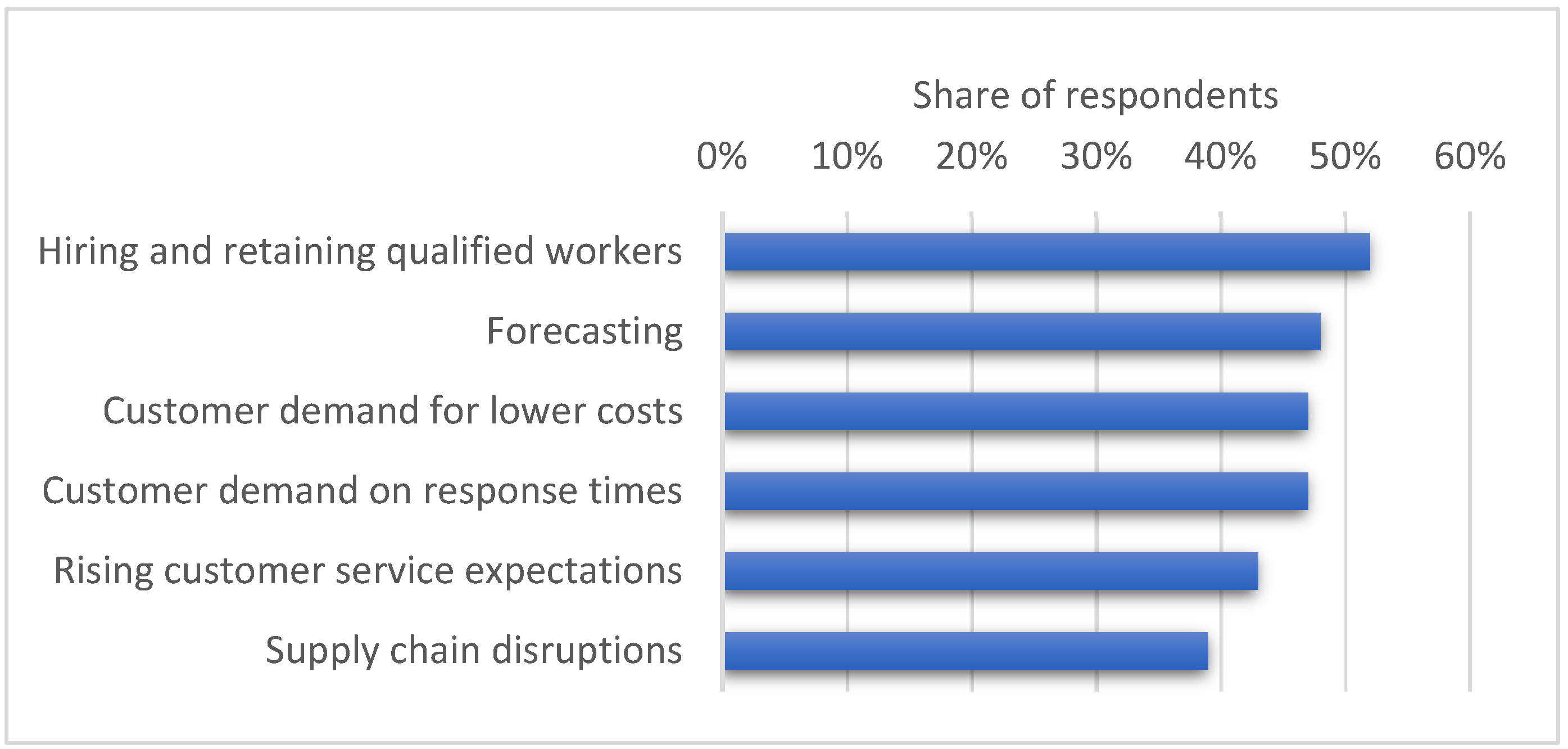

Based on the literature, employee motivation (Azizi et al. 2021), resolving workload issues, sustainability of the operation (Yadav et al. 2020), and digitalization opportunities (Veluchamy et al. 2021) are important topics, and the analysed supplier used a combination of these in addition to reducing the weekly total working hours in order to overcome the HR-related issues caused by the pandemic. In Figure 4, the highest priority issue was also a HR-related one based on that statistic.

The customer demand fluctuations caused by uncertainties and risks (Gyenge et al. 2021) have several effects on supply chains. The increased levels of inventories, and the associated costs (Yagi and Managi 2021) are partially caused by the bullwhip effect (Yang et al. 2021) caused by these forecasting issues. The chosen supplier overcame the negative effects of the huge levels of inventories by negotiating and requesting inventory financing from the customers and also keeping the load versus commit targets, while securing the supply of the critical components. In Figure 6 it can be seen that the negotiations and shortages were among the top issues according to the results of the statistics.

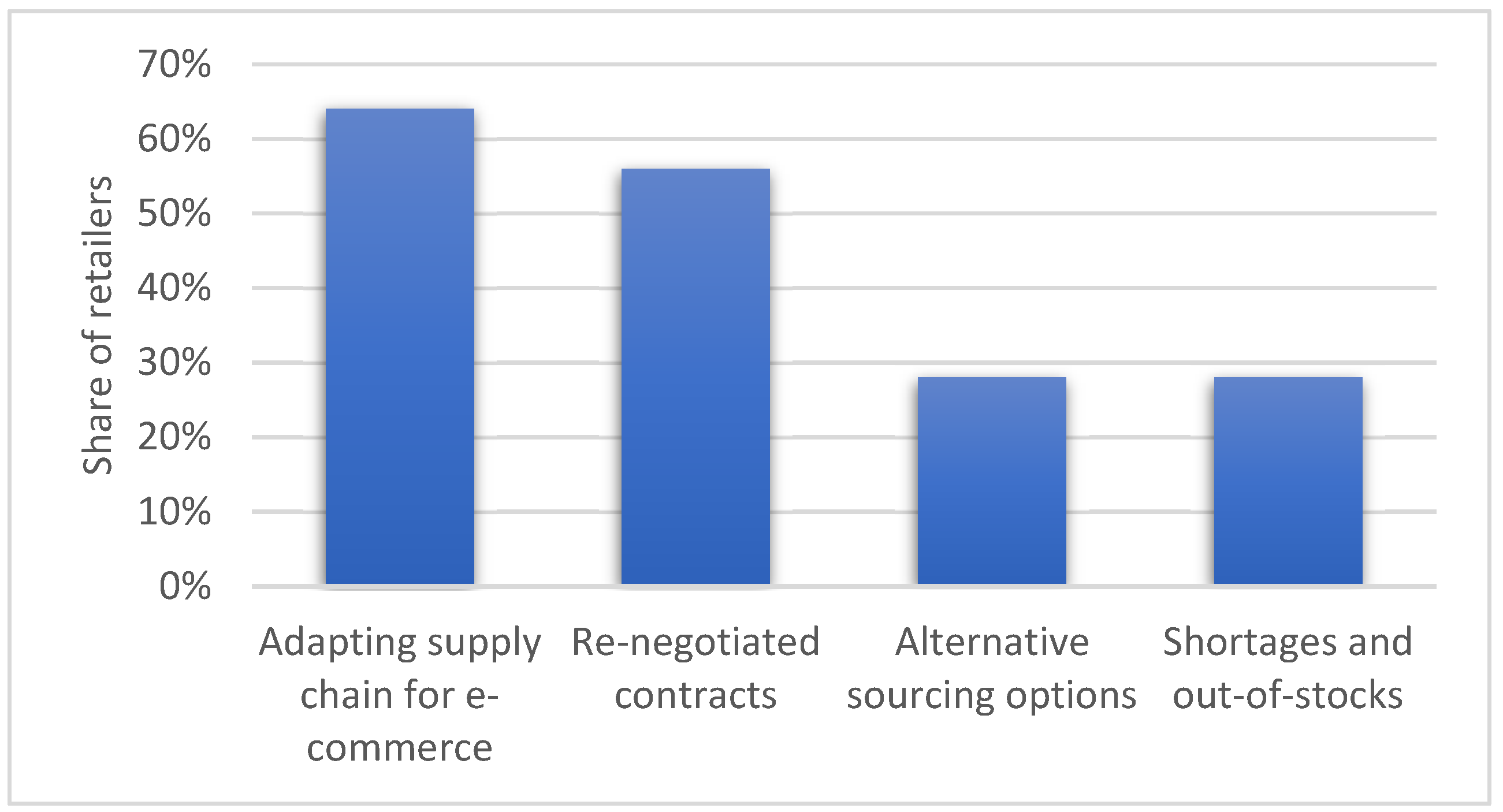

The transport terms and conditions (Budd and Ison 2020) could not be reverted to the 2018 and 2019 state, the related transport costs increased, and the possibilities and methods decreased (Raj et al. 2022); in order to secure the supply of the critical components, the analysed company started negotiations with the key suppliers and transport companies.

In order to successfully plan and execute the outsourcing (Zhu et al. 2020) of certain parts of the production and to secure the operation (Juhász et al. 2020) all the relevant risks had to be evaluated (Juhász et al. 2020) and mitigated (Mogos et al. 2019). The chosen supplier managed to diversify their production by introducing dual sourcing for one of the most critical materials.

As a conclusion, the authors compared the literature with the case study results in the different relevant areas. In some cases, the chosen supplier chose strategies which were suggested in the standard literature in the HR, transportation, diversification, and sourcing areas. In other cases, the supplier had to adapt to the changed market situation, and used different strategies and actions which were not part of the focus or suggestions of the standard literature in the flexibility, decision-making, and forecasting areas. In these areas the chosen supplier used rather uncharted and new strategies due to the changed market situation because of COVID.

All in all, it can be observed that the supplier used strategies that could be related to the standard literature in some of the analysed areas, while in other areas unconventional and new strategies had to be explored and used, reacting to the pandemic-related challenges and market changes in the electronics industry.

In general, due to the pandemic, almost all aspects of life have changed; people, governments, supply chains and companies had to adjust to the new situation and had to deal with the different related risks. The consequences for the Philippines were severe problems with automotive supply chains during the second and third waves of the pandemic. The different members of the supply chains faced many challenges because of the lockdowns. They had to adapt their strategies based on their opportunities and on the changed market situation, and the companies had to closely work together in order to stay competitive in this challenging and growing sector.

Author Contributions

Conceptualization, B.S.G.P., M.H. and Á.C.-K.; methodology, B.S.G.P., M.H. and Á.C.-K.; software, B.S.G.P., M.H. and Á.C.-K.; validation, B.S.G.P., M.H. and Á.C.-K.; writing—original draft preparation, B.S.G.P., M.H. and Á.C.-K.; writing—review and editing, B.S.G.P., M.H. and Á.C.-K. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Not applicable.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Aday, Serpil, and Mehmet Seckin Aday. 2020. Impact of COVID-19 on the food supply chain. Food Quality and Safety 4: 167–80. [Google Scholar] [CrossRef]

- Azizi, Mohammad Reza, Rasha Atlasi, Arash Ziapour, Jaffar Abbas, and Roya Naemi. 2021. Innovative human resource management strategies during the COVID-19 pandemic: A systematic narrative review approach. Heliyon 7: 1–8. [Google Scholar] [CrossRef]

- Babbie, Earl. 2003. A Társadalomtudományi Kutatás Gyakorlata. Budapest: Balassi Kiadó, pp. 324–34. ISBN 963-506-563-9. [Google Scholar]

- Bacsi, Zsuzsanna, and Zsolt Hollósy. 2019. The Yield Stability Index Reloaded—The Assessment of the Stability of Crop Production Technology. Agriculturae Conspectus Scientificus 84: 319–31. [Google Scholar]

- Balogh, Antal, Balázs Gyenge, Ágnes Szeghegyi, and Tímea Kozma. 2020. Advantages of Simulating Logistics Processes. Acta Polytechnica Hungarica 17: 215–19. [Google Scholar] [CrossRef]

- Barbosa, Marcello Werneck, Paulo Renato de Sousa, and Leise Kelli de Oliveira. 2022. The Effects of Barriers and Freight Vehicle Restrictions on Logistics Costs: A Comparison before and during the COVID-19 Pandemic in Brazil. Sustainability 14: 8650. [Google Scholar] [CrossRef]

- Bhat, Rahul. 2021. Multiphysics Simulation of Electric Motor Designs, Et Auto.com From the Economic Times, Live Webinar. Available online: https://auto.economictimes.indiatimes.com/webinar/multiphysics-simulation-of-electric-motor-designs/763?redirect=1 (accessed on 1 June 2022).

- Bhattacharya, Souresh, D. Mukhopadhyay, and Sunil Giri. 2014. Supply Chain Management in Indian Automotive Industry: Complexities, Challenges and Way Ahead. International Journal of Managing Value and Supply Chains 5: 49–59. [Google Scholar] [CrossRef]

- Bőgel, György. 2020. Azonnali reakciók a koronavírus-válságra az élelmezési ellátási láncokban, Logisztikai trendek és legjobb gyakorlatok, A fenntartható ellátási lánc kihívásai. Fókuszban a Teljesítménymérés 4: 21–26. [Google Scholar]

- Budd, Lucy, and Stephen Ison. 2020. Responsible Transport: A post-COVID agenda for transport policy and practice. Transportation Research Interdisciplinary Perspectives 6: 100151. [Google Scholar] [CrossRef]

- Caldwell, Jamie M., Elvira de Lara-Tuprio, Timothy Robin Teng, Maria Regina Justina E. Estuar, Raymond Francis R. Sarmiento, Milinda Abayawardana, Robert Neil F. Leong, Richard T. Gray, James G. Wood, Linh-Vi Le, and et al. 2021. Understanding COVID-19 dynamics and the effects of interventions in the Philippines: A mathematical modelling study. The Lancet Regional Health—Western Pacific 14: 100211. [Google Scholar] [CrossRef]

- Chowdhury, Priyabrata, Sanjoy Kumar Paul, Shahriar Kaisar, and Abdul Moktadir. 2021. COVID-19 pandemic related supply chain studies: A systematic review. Transportation Research, Part E 148: 102271. [Google Scholar] [CrossRef]

- Cramarenco, Romana Emilia. 2020. On migrants and COVID-19 pandemic—An analysis. On-line Journal Modelling the New Europe, 106–115. [Google Scholar] [CrossRef]

- Czifra, György, Peter Szabó, Miroslava Mĺkva, and Jaromíra Vaňová. 2019. Lean Principles Application in the Automotive Industry. Acta Polytechnica Hungarica 16: 43–48. [Google Scholar] [CrossRef]

- Dana, Jason, Robyn Dawes, and Nathanial Peterson. 2013. Belief in the unstructured interview: The persistence of an illusion. Judgment and Decision Making 8: 512–20. [Google Scholar]

- Delgado, Mercedes, and Karen G. Mills. 2020. The supply chain economy: A new industry categorization for understanding innovation in services. Research Policy 49: 104039. [Google Scholar] [CrossRef]

- El Baz, Jamal, and Salomée Ruel. 2021. Can supply chain risk management practices mitigate the disruption impacts on supply chains’ resilience and robustness? Evidence from an empirical survey in a COVID-19 outbreak era. International Journal of Production Economics 233: 107972. [Google Scholar] [CrossRef]

- Free, Clinton, and Angela Hecimovic. 2021. Global supply chains after COVID-19: The end of the road for neoliberal globalisation? Accounting, Auditing & Accountability Journal 34: 58–84. [Google Scholar] [CrossRef]

- Gerőcs, Tamás, and András Pinkasz. 2019. Relocation, standardization and vertical specialization: Core-periphery relations in the european automotive value chain. Society and Economy 41: 171–80. [Google Scholar] [CrossRef]

- Gifford, Daron. 2020. The New Normal in the Automotive Supply Chain, Industry Sectors, Automotive, Team Kentucky Cabinet for Economic Development. Available online: https://www.areadevelopment.com/Automotive/q3-2020-auto-aero-site-guide/the-new-normal-in-the-automotive-supply-chain.shtml (accessed on 1 December 2021).

- Gyenge, Balázs, Ágnes Szeghegyi, Gábor Szalay, and Tímea Kozma. 2021. Consumer Control Supportive Visualization. Acta Polytechnica Hungarica 18: 65–72. [Google Scholar] [CrossRef]

- Habib, Komal, Benjamin Sprecher, and Steven B. Young. 2021. COVID-19 impacts on metal supply: How does 2020 differ from previous supply chain disruptions? Resources, Conservation & Recycling 165: 105229. [Google Scholar] [CrossRef]

- Hausmann, Róbert. 2020. A globális ellátási láncok átalakulása a feldolgozóiparban a koronavírus-járvány következtében. Hitelintézeti Szemle 19: 130–53. [Google Scholar] [CrossRef]

- Hofstätter, Thomas, Melanie Krawina, Bernhard Mühlreiter, Stefan Pöhler, and Andreas Tschiesner. 2020. Reimagining the Auto Industry’s Future: It’s Now or Never. Automotive & Assembly. Atlanta: McKinsey & Company. Available online: https://www.mckinsey.com/industries/automotive-and-assembly/our-insights/reimagining-the-auto-industrys-future-its-now-or-never (accessed on 1 December 2021).

- IEA. 2021. Electric Vehicles. Paris: IEA. Available online: https://www.iea.org/reports/electric-vehicles (accessed on 10 September 2021).

- Intarakumnerd, Patarapong, Sunil Mani, Haryo Aswicahyono, Tomohiro Machikita, Masatsugu Tsuji, Avvari V. Mohan, Mari-Len Macasaquit, Somrote Komolavanij, Truong Chi Binh, and Yasushi Ueki. 2010. Fostering Production and Science & Technology Linkages to Stimulate Innovation in ASEAN. ERIA Research Project Report 2009, No. 7-4. Jakarta: ERIA, pp. 145–57. [Google Scholar]

- Ishida, Shuichi. 2020. Perspectives on Supply Chain Management in a Pandemic and the Post-COVID-19 Era. IEEE Engineering Management Review 48: 146–52. [Google Scholar] [CrossRef]

- Ivanov, Dmitry, and Alexandre Dolgui. 2020. Viability of intertwined supply networks: Extending the supply chain resilience angles towards survivability. A position paper motivated by COVID-19 outbreak. International Journal of Production Research 58: 2904–15. [Google Scholar] [CrossRef]

- Juhász, Zita, Zsolt Hollósy, and Jenifer Márton. 2020. Beruházások és finanszírozásuk kockázatai, kockázatkezelési trendjeik az elmúlt 10 évben. International Journal of Engineering and Management Sciences 5: 184–93. [Google Scholar] [CrossRef]

- Ketchen, David J., Jr., and Christopher W. Craighead. 2020. Research at the Intersection of Entrepreneurship, Supply Chain Management, and Strategic Management: Opportunities Highlighted by COVID-19. Journal of Management 46: 1330–41. [Google Scholar] [CrossRef]

- Khamis, Alaa, Jun Meng, Jin Wang, Ahmad Taher Azar, Edson Prestes, Howard Li, Ibrahim A. Hameed, Árpád Takács, Imre J. Rudas, and Tamás Haidegger. 2021. Robotics and Intelligent Systems Against a Pandemic. Acta Polytechnica Hungarica 18: 13–32. [Google Scholar] [CrossRef]

- Kilay, Aalfonz Lawrenz, Bachtiar H. Simamora, and Danang Pinardi Putra. 2022. The Influence of E-Payment and E-Commerce Services on Supply Chain Performance: Implications of Open Innovation and Solutions for the Digitalization of Micro, Small, and Medium Enterprises (MSMEs) in Indonesia. Journal of Open Innovation: Technology, Market and Complexity 8: 119. [Google Scholar] [CrossRef]

- Kumar, Bipul, and Arun Sharma. 2021. Managing the supply chain during disruptions: Developing a framework for decision-making. Industrial Marketing Management 97: 159–70. [Google Scholar] [CrossRef]

- Las Marias, Stephen. 2019. A Look at the Current Philippine Electronics Manufacturing Landscape (Part 1). Available online: https://www.eetasia.com/a-look-at-the-current-philippine-electronics-manufacturing-landscape-part-1/ (accessed on 29 August 2021).

- Lin, Yongjia, Di Fan, Xuanyi Shi, and Maggie Fu. 2021. The effects of supply chain diversification during the COVID-19 crisis: Evidence from Chinese manufacturers. Transportation Research Part E: Logistics and Transportation Review 155: 102493. [Google Scholar] [CrossRef]

- McMaster, May, Charlie Nettleton, Christeen Tom, Belanda Xu, Cheng Cao, and Ping Qiao. 2020. Risk Management: Rethinking Fashion Supply Chain Management for Multinational Corporations in Light of the COVID-19 Outbreak. Journal of Risk and Financial Management 13: 173. [Google Scholar] [CrossRef]

- Mogos, Maria Flavia, Anna Fredriksson, and Erlend Alfnes. 2019. A production transfer procedure based on risk management principles. Journal of Global Operations and Strategic Sourcing 12: 103–50. [Google Scholar] [CrossRef]

- Mollenkopf, Diane A., Lucie K. Ozanne, and Hannah J. Stolze. 2020. A transformative supply chain response to COVID-19. Journal of Service Management 32: 190–202. [Google Scholar] [CrossRef]

- Nandi, Santosh, Joseph Sarkis, Aref Hervani, and Marilyn Helms. 2021. Do blockchain and circular economy practices improve post COVID-19 supply chains? A resource-based and resource dependence perspective. Industrial Management & Data Systems 121: 333–63. [Google Scholar] [CrossRef]

- Palócz, Éva, and Zoltán Matheika. 2020. Dilemmák a COVID-19-válság magyarországi gazdasági hatásairól. In Társadalmi Riport 2020. Edited by Kolosi Tamás, Szelényi Iván and Tóth István György. Budapest: TÁRKI Társadalomkutatási Intézet Zrt, pp. 573–90. [Google Scholar]

- Pitchaiah, Dusanapudi Sivanagaraju, Manzoor Hussain, N. Sateesh, and D. Govardhan. 2021. Prioritization of supply chain risk by Multi Attribute Decision Making method for manufacturing of automobiles. Materials Today: Proceedings 39: 201–5. [Google Scholar] [CrossRef]

- Raj, Alok, Abheek Aanjan Mukherjee, Ana Beatriz Lopes de Sousa Jabbour, and Samir K. Srivastava. 2022. Supply chain management during and post-COVID-19 pandemic: Mitigation strategies and practical lessons learned. Journal of Business Research 142: 1125–38. [Google Scholar] [CrossRef]

- Reyna-Castillo, Miguel, Alejandro Santiago, Salvador Ibarra Martínez, and José Antonio Castán Rocha. 2022. Social Sustainability and Resilience in Supply Chains of Latin America on COVID-19 Times: Classification Using Evolutionary Fuzzy Knowledge. Mathematics 10: 2371. [Google Scholar] [CrossRef]

- Shekarian, Ehsan, Behrang Ijadi, Amirreza Zare, and Jukka Majava. 2022. Sustainable Supply Chain Management: A Comprehensive Systematic Review of Industrial Practices. Sustainability 14: 7892. [Google Scholar] [CrossRef]

- Statista. 2021. Estimated Economic Trade Impact from Chinese Supply Disruptions Due to the Coronavirus COVID-19 Pandemic in the Philippines in 2020, by Industry. Available online: https://www.statista.com/statistics/1104369/philippines-economic-trade-impact-from-china-due-to-the-coronavirus-covid-19-pandemic-by-industry/ (accessed on 3 December 2021).

- Statista. 2022a. Worldwide Number of Battery Electric Vehicles in Use from 2016 to 2021. Available online: https://www.statista.com/statistics/270603/worldwide-number-of-hybrid-and-electric-vehicles-since-2009 (accessed on 15 June 2022).

- Statista. 2022b. Battery Electric Vehicle Registrations in Selected Regions Worldwide between 2015 and 2021. Available online: https://www.statista.com/statistics/961045/battery-electric-vehicle-registrations-in-selected-countries (accessed on 10 July 2022).

- Statista. 2022c. Supply Chain Challenges in 2021. Available online: https://www.statista.com/statistics/1182057/global-supply-chain-challenges (accessed on 19 April 2022).

- Statista. 2022d. Supply Chain Changes Faced by Retailers Due to the COVID-19 Pandemic Worldwide in 2020. Available online: https://www.statista.com/statistics/1143426/coronavirus-changes-to-supply-chain-retail-worldwide (accessed on 10 February 2022).

- Upadhyay, Arvind, Sumona Mukhuty, Sushma Kumari, Jose Arturo Garza-Reyes, and Vinaya Shukla. 2022. A review of lean and agile management in humanitarian supply chains: Analysing the pre-disaster and post-disaster phases, and future directions. Production Planning & Control: The Management of Operations 33: 641–54. [Google Scholar]

- Veluchamy, Ramar, Komal Sinha, and Karishma Sanghai. 2021. Comparative study on hr practices in automotive companies during COVID-19. Journal of Critical Reviews 8: 359–68. [Google Scholar] [CrossRef]

- Wojtas, Kinga, and Katarzyna Walecka. 2020. The pandemic of COVID-19—A catalyst for changes in the countries of east central Europe. On-line Journal Modelling the New Europe, 184–96. [Google Scholar] [CrossRef]

- Yadav, Gunjan, Sunil Luthra, Suresh Kumar Jakhar, Sachin Kumar Mangla, and Dhiraj P. Rai. 2020. A framework to overcome sustainable supply chain challenges through solution measures of industry 4.0 and circular economy: An automotive case. Journal of Cleaner Production 254: 120112. [Google Scholar] [CrossRef]

- Yagi, Michiyuki, and Shunsuke Managi. 2021. Global supply constraints from the 2008 and COVID-19 crises. Economic Analysis and Policy 69: 514–18. [Google Scholar] [CrossRef]

- Yang, Y., J. Lin, G. Liu, and L. Zhou. 2021. The behavioural causes of bullwhip effect in supply chains: A systematic literature review. International Journal of Production Economics 236: 108120. [Google Scholar] [CrossRef]

- Ye, Ying, and Kwok Hung Lau. 2022. Competitive Green Supply Chain Transformation with Dynamic Capabilities—An Exploratory Case Study of Chinese Electronics Industry. Sustainability 14: 8640. [Google Scholar] [CrossRef]

- Zhu, Guiyang, Mabel C. Chou, and Christina W. Tsai. 2020. Lessons Learned from the COVID-19 Pandemic Exposing the Shortcomings of Current Supply Chain Operations: A Long-Term Prescriptive Offering. Sustainability 12: 5858. [Google Scholar] [CrossRef]

Figure 1.

Estimated economic trade impact from Chinese supply disruptions due to the coronavirus COVID-19 pandemic in the Philippines as of February 2020, by industry (in million U.S. dollars). Source: own compilation, based on Statista (2021), https://www.statista.com/statistics/1104369/philippines-economic-trade-impact-from-china-due-to-the-coronavirus-covid-19-pandemic-by-industry/ (accessed on 1 June 2022).

Figure 1.

Estimated economic trade impact from Chinese supply disruptions due to the coronavirus COVID-19 pandemic in the Philippines as of February 2020, by industry (in million U.S. dollars). Source: own compilation, based on Statista (2021), https://www.statista.com/statistics/1104369/philippines-economic-trade-impact-from-china-due-to-the-coronavirus-covid-19-pandemic-by-industry/ (accessed on 1 June 2022).

Figure 2.

Philippine Electronics Exports ($bn). Source: own compilation based on Las Marias (2019), https://www.eetasia.com/a-look-at-the-current-philippine-electronics-manufacturing-landscape-part-1 (accessed on 1 June 2022).

Figure 2.

Philippine Electronics Exports ($bn). Source: own compilation based on Las Marias (2019), https://www.eetasia.com/a-look-at-the-current-philippine-electronics-manufacturing-landscape-part-1 (accessed on 1 June 2022).

Figure 3.

Worldwide number of battery electric vehicles in use from 2012 to 2020 (in millions). Source: own compilation based on Statista (2022a), https://www.statista.com/statistics/270603/worldwide-number-of-hybrid-and-electric-vehicles-since-2009/ (accessed on 1 June 2022).

Figure 3.

Worldwide number of battery electric vehicles in use from 2012 to 2020 (in millions). Source: own compilation based on Statista (2022a), https://www.statista.com/statistics/270603/worldwide-number-of-hybrid-and-electric-vehicles-since-2009/ (accessed on 1 June 2022).

Figure 4.

Battery electric vehicle registrations in selected regions worldwide between 2015 and 2021 (in units). Source: own compilation based on Statista (2022b), https://www.statista.com/statistics/961045/battery-electric-vehicle-registrations-in-selected-countries/ (accessed on 1 June 2022).

Figure 4.

Battery electric vehicle registrations in selected regions worldwide between 2015 and 2021 (in units). Source: own compilation based on Statista (2022b), https://www.statista.com/statistics/961045/battery-electric-vehicle-registrations-in-selected-countries/ (accessed on 1 June 2022).

Figure 5.

Supply chain challenges in 2020. Source: own compilation based on Statista (2022c), https://www.statista.com/statistics/1182057/global-supply-chain-challenges/ (accessed on 1 June 2022).

Figure 5.

Supply chain challenges in 2020. Source: own compilation based on Statista (2022c), https://www.statista.com/statistics/1182057/global-supply-chain-challenges/ (accessed on 1 June 2022).

Figure 6.

Supply chain changes faced by retailers due to the COVID-19 pandemic worldwide in 2020. Source: own compilation based on Statista (2022d), https://www.statista.com/statistics/1143426/coronavirus-changes-to-supply-chain-retail-worldwide/ (accessed on 1 June 2022).

Figure 6.

Supply chain changes faced by retailers due to the COVID-19 pandemic worldwide in 2020. Source: own compilation based on Statista (2022d), https://www.statista.com/statistics/1143426/coronavirus-changes-to-supply-chain-retail-worldwide/ (accessed on 1 June 2022).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Table 1.

Interview summary.

| Department | Number of Interviewed Subjects |

|---|---|

| Supply chain management | 2 |

| Logistics | 2 |

| Human resources | 1 |

Source: Own compilation.

Table 2.

Results of the case study.

| Key Topics and Areas | Standard Issues in the Literature | Strategy of the Chosen Company to Overcome the Issues |

|---|---|---|

| Flexibility and decision making challenges | Inflexibility due to standardization | Validation of new suppliers and production facilities of an existing supplier |

| HR-related difficulties | Increasing workload and fluctuation, lack of the advanced digitalization options of the direct and indirect workforce | Exploring the opportunities of digitalization, workload reallocation and the reduction of weekly working hours |

| Forecasting challenges | Increasing inventory levels while facing supply issues with the top gating items, inefficiency of JIT in this market situation | Inventory financing of the customers, securing more supply from the allocated components |

| Transportation challenges | Reduced transportation possibilities and increasing freight costs | Securing cargo capacities through negotiations with the key suppliers and transport companies |

| Diversification and sourcing challenges | COVID lockdowns and supply chain constraints | Dual sourcing and splitting the production in order to reduce the supply chain costs in the mid and long term |

Source: Own compilation.

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Pató, B.S.G.; Herczeg, M.; Csiszárik-Kocsir, Á. The COVID-19 Impact on Supply Chains, Focusing on the Automotive Segment during the Second and Third Wave of the Pandemic. Risks 2022, 10, 189. https://doi.org/10.3390/risks10100189

AMA Style

Pató BSG, Herczeg M, Csiszárik-Kocsir Á. The COVID-19 Impact on Supply Chains, Focusing on the Automotive Segment during the Second and Third Wave of the Pandemic. Risks. 2022; 10(10):189. https://doi.org/10.3390/risks10100189

Chicago/Turabian StylePató, Beáta Sz. G., Márk Herczeg, and Ágnes Csiszárik-Kocsir. 2022. "The COVID-19 Impact on Supply Chains, Focusing on the Automotive Segment during the Second and Third Wave of the Pandemic" Risks 10, no. 10: 189. https://doi.org/10.3390/risks10100189

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.