How Digital Financial Inclusion Boosts Tourism: Evidence from Chinese Cities

1

School of Economics, Nanjing University of Posts and Telecommunications, Nanjing 210023, China

2

School of Economics & Management, Southeast University, Nanjing 211189, China

*

Author to whom correspondence should be addressed.

J. Theor. Appl. Electron. Commer. Res. 2023, 18(3), 1619-1636; https://doi.org/10.3390/jtaer18030082

Submission received: 12 July 2023

/

Revised: 2 September 2023

/

Accepted: 11 September 2023

/

Published: 13 September 2023

(This article belongs to the Section Digital Marketing and the Connected Consumer)

Abstract

:It is crucial to explore the impact of digital financial inclusion on tourism for national economic development. This paper utilizes panel data from 256 prefecture-level cities in China between 2011 and 2019 to examine the influence of digital financial inclusion on tourism. The findings demonstrate that digital financial inclusion significantly contributes to the development of the tourism industry. Notably, its coverage breadth, depth of use, and level of digitalization also have positive effects. Mechanism analysis reveals that digital financial inclusion facilitates the growth of tourism by supporting the development of tourism enterprises and enhancing consumer spending. Heterogeneity analysis further reveals regional and urban disparities in the promotion of digital financial inclusion, with the effect being more pronounced in the eastern region and larger cities. In comparison to existing studies, this paper delves into the mechanisms through which digital financial inclusion impacts tourism, as well as investigates regional and city size discrepancies. Consequently, governments should strive to foster the development of digital financial inclusion to attract market players and promote the advancement of residents’ consumption, thereby bolstering tourism development.

1. Introduction

Digital financial inclusion refers to the emerging model of utilizing digital technology and financial innovation to provide financial services to individuals who are excluded from the traditional financial system. With the rapid advancement of internet and mobile payment technology, digital financial inclusion has gained widespread adoption globally [1,2,3]. The tourism industry, being one of the largest service sectors worldwide, has also felt the impact of digital financial inclusion. In China, tourism is rapidly becoming a prominent pillar of the national economy. According to the China National Tourism Administration, the number of domestic tourists in China reached approximately 6.31 billion in 2019, resulting in tourism revenue exceeding CNY 5.7 trillion. The strategic importance of tourism to China’s economy will only continue to grow. Therefore, the Chinese government has set a development goal to transform the tourism industry from its traditional state to a modern and digitally intelligent one. Nonetheless, the tourism industry in China confronts various challenges, such as difficulties in securing financing for enterprises and the limitation of consumption scenarios. The emergence of digital financial inclusion offers a viable solution for the tourism industry in China and presents significant opportunities for its growth and development. Hence, studying the effects of digital financial inclusion on China’s tourism industry carries both theoretical and practical importance.

Tourism is a significant contributor to economic growth and job creation, making it one of the largest service industries globally. However, the tourism industry faces challenges due to limitations in traditional financial systems, which hinder its development. Introducing digital financial inclusion has had a transformative effect on the tourism sector by streamlining various aspects of tourism development, including government processes and the overall visitor experience. Furthermore, expanding the application of tourism finance has enabled tourism companies to enhance both online and offline services for tourists, thereby enriching the demand for tourism supply chain finance and consumer finance markets. Taking Nanjing, the city where all the authors are located, as an example, to cope with the impact of the epidemic, Nanjing has increased financial support to help the tourism industry recover and develop. Additionally, the accommodation and food sectors have improved their service management through the provision of smart travel services, enabling effective risk management. It is evident that digital financial inclusion has the potential to revolutionize the traditional “attraction tourism” model, facilitating the transition towards a more inclusive and comprehensive tourism model while expediting the arrival of an era characterized by mass tourism and self-service travel experiences. Thus, investigating the impact of digital financial inclusion on tourism is crucial for comprehending how it can enhance the financing environment of the tourism sector and promote its sustainable development.

In addition, the development of digital financial inclusion has brought more convenient and efficient payment methods to the tourism industry. Traditional cash payment methods have security risks and problems of portability, while digital financial inclusion provides safer and faster payment methods through mobile payment, electronic payment, and other means, which facilitates tourists’ consumption experience. At the same time, through big data analysis and artificial intelligence technology, an in-depth analysis of tourists’ consumption behavior, preferences, and needs can be conducted to better understand the customer group. These accurate customer positioning and market analysis capabilities enable tourism companies to better formulate marketing strategies, push personalized tourism products and services, and improve customer satisfaction and loyalty. Therefore, studying the impact of digital financial inclusion on tourism clarifies how it can improve the tourism consumption experience and enhance the competitiveness of the industry.

Based on this reality, this paper aims to explore the impact of digital financial inclusion on tourism. Specifically, we investigate its impact on the development of tourism enterprises and tourism consumption. Through an in-depth study of these influences, this paper aims to understand the role and significance of digital financial inclusion on tourism in more detail and provide theoretical and practical guidance for the industry’s development. The contribution of this paper is to conduct in-depth research and analysis on the impact of digital financial inclusion on tourism. It discusses the application and influence of digital financial inclusion in the tourism industry, providing new ideas and methods for it to serve the industry. Specifically, we explore its impact on the development of tourism enterprises, consumer consumption upgrading and innovation, and provide practical guidance and policy recommendations.

The subsequent sections of this paper are structured as follows: Section 2 is a literature review; Section 3 is a theoretical analysis and research hypothesis; Section 4 is variable selection and empirical model construction; Section 5 is an analysis of the empirical results; and Section 6 is a conclusion and policy recommendations. This paper contributes to the research on digital financial inclusion and tourism, shedding light on its impact and proposing policy recommendations for sustainable tourism development.

2. Literature Review

Digital financial inclusion is the result of integrating inclusive finance and digital technology. In comparison to traditional finance, digital financial inclusion offers the advantages of lower cost and wider coverage. Additionally, it expands the scope and depth of traditional finance services, providing diverse financing channels for entities and enriching consumer demand for financial products. Furthermore, digital financial inclusion has also had a profound impact on the tourism industry, which serves as an important sector for meeting people’s aspirations for an improved quality of life. Although limited literature exists on the effects of digital financial inclusion on tourism, there have been numerous studies on the impact of the financial industry or digital technology on the tourism sector. Therefore, this paper aims to review relevant studies from four perspectives: tourism development, the relationship between finance and tourism, the influence of digital technology on tourism, and the impact of digital financial inclusion on tourism.

2.1. Tourism Development

Tourism is a crucial sector that drives economic growth and is influenced by various factors, including infrastructure, economic agglomeration density, and culture [4,5,6]. Financial development plays a significant role in promoting industrial growth and has a profound impact on tourism development. Alternatively, scholars have examined the specific countries to analyze the impact of financial development on tourism. For instance, Karadzova and Dicevska used Macedonia as an example to investigate the link between the financial system and tourism development. Their study revealed the financial intensity of tourism [7]. Additionally, Katircioglu et al. demonstrated the influence of financial markets on tourism expansion in Turkey [8]. In addition to financial development, the impact of financial inclusion on tourism development has also received attention. Gopalan and Khalid analyzed the impact of financial inclusion on tourism demand in 85 emerging markets and developing economies worldwide. They found that higher financial inclusion leads to greater tourism demand [9]. Similarly, Shi et al. examined the effect of financial inclusion on tourism development in 24 developed and 21 emerging economies worldwide. Their study revealed that financial inclusion has a significant positive impact on all aspects of tourism development in different economies, with a more pronounced effect in emerging economies [10].

In recent years, the rapid development of the digital economy has facilitated the integration of digital technology into various industries, including tourism, leading to significant transformation. Digital technologies have the potential to address the information asymmetry between the supply and demand sides of the tourism industry, ensuring a precise matching of tourism preferences with supply information. Moreover, these technologies can enhance the overall tourism experience for travelers. For example, Barros Nunes found that tourism firms can maintain the credibility of their products through social network media, positively influencing consumers’ intentions to make purchases [11]. Adeola and Evans employed a dynamic panel gravity model to analyze African data spanning from 1996 to 2016 [12]. Their study revealed that the growth of information and communication technology (ICT) and infrastructure led to an increase in tourist arrivals. Pedro et al. focused on the influence of ICT accessibility on tourists’ choices of destination, their experiences, and their satisfaction [13]. Natocheeva et al. identified digitalization as a competitive advantage for tourism organizations, as it offers a novel form of communication between tourism service producers and consumers [14]. Tang investigated the spatial effects and impact mechanisms of the digital economy on high-quality tourism development in the Yangtze River Delta Area of China. The study found that the digital economy drives high-quality tourism by enhancing government efficiency and expanding market potential [15].

2.2. The Relationship between the Financial Industry and Tourism

The relationship between the financial industry and tourism is primarily investigated in domestic and foreign studies, focusing on the one-way promotion of the financial industry to tourism. For instance, Perić et al. and Markandya et al. explored the investment of the International Finance Corporation and the World Bank in tourism projects from 1991 to 2009, highlighting the potential contribution of sustainable tourism resource utilization to economic growth [16,17]. Gautam and Bishnu studied tourism finance in Nepal and found that the financial industry not only promoted tourism development but also significantly contributed to the country’s economic growth [18], and the same thing also happened in Bangladesh [19]. Gopalan and Khalid found that financial inclusion can nonlinearly boost tourism demand in emerging and developing countries [20]. In domestic research, Jiang and Hu analyzed the challenges faced by financial support for tourism development in specific locations in China, proposing measures to eliminate financial constraints and increase relevant financial support [21,22]. Song and Xu investigated the impact of financing constraints on the innovation of tourism enterprises and suggested that the government should provide financial support for innovation activities [23]. Wei et al. analyzed dynamic panel data from nine cities in Fujian Province, confirming the supportive role of the financial industry in tourism [24]. Additionally, some studies focus on the integration and development of finance and tourism. For example, Zeng and Shao examined the integration and development of finance and tourism in various regions and proposed measures for their collaboration [25,26]. Gong and Guo conducted an empirical analysis of the coupling development between the two industries in Jiangsu Province and identified a significant coupling relationship, although the financial industry lagged behind [27]. Liao et al. analyzed data from Zhangjiajie, Huangshan, and Sanya, confirming the coupling between the financial industry and the tourism industry [28].

2.3. The Impact of Digital Technology on Tourism

Scholars have also focused on the integration of intelligence into the tourism industry when studying the impact of digital technology. Digital technology brought by Industry 4.0 is constantly changing the tourist experience [29] and the mode of tourism [30]. Wu and Zhou et al. analyzed the theoretical possibility and necessity of integrating and developing tourism and Internet technologies [31,32]. Digital technology not only addresses trust issues arising from information asymmetry but also enhances tourists’ travel experiences. For example, Tom discussed the influence of the proliferation of interactive digital platforms and solutions within tourism practice and behavior [33]. Cenni and Vasquez conducted a rooted theoretical approach by investigating 500 samples of online consumer reviews from 100 different Airbnb online experiences. The study revealed that Airbnb’s online experiences create a sense of belonging and connection for consumers from different countries and regions [34]. Gelb and Guo et al. explored the digital integration of art galleries and museums, creatively meeting customer needs and providing immersive tourism experiences [35,36]. In the future, with the development of the tourism industry, the demand for and reliance on digitalization in the industry will increase. This will lead to a win–win situation for the entire tourism industry chain and consumers through digital empowerment.

2.4. The Impact of Digital Financial Inclusion on the Tourism

The development of digital financial inclusion has integrated the advantages of finance and technology and has become a product that meets the needs of the current era, following the rapid growth of Internet finance. It helps financial entities serve and meet the policy requirements of transitioning from virtual to real [37]. Some domestic scholars have started to focus on the research of digital financial inclusion on the tourism industry. For instance, Ma and Ouyang found that the impact of digital financial inclusion on tourism has provincial spatial heterogeneity [38]. Wang et al. measured the comprehensive index of tourism resources in 30 provinces of China from 2011 to 2018. They used panel data and a fixed-effect model to confirm that digital finance can promote tourism consumption demand and optimize the supply of tourism factors, improving the efficiency of tourism resource allocation [39]. Wang et al. and Huang discussed the positive role of digital financial inclusion in promoting rural tourism and inbound tourism from both empirical and theoretical perspectives [40,41]. Ren et al. conducted theoretical research on the integrated development of digital financial inclusion from the perspectives of shared tourism and provided corresponding policy suggestions [42]. Wu and Chang utilized data from China’s household finance survey to investigate the impact of digital financial inclusion on household tourism consumption. Their findings revealed a significant contribution to such consumption [43]. While these studies form a solid foundation for this paper, there is still room for improvement.

Through a literature review, it is evident that scholars primarily focus on studying the impact of finance and digital technology on tourism while giving less consideration to the effect of digital financial inclusion on the development of tourism. Nonetheless, digital financial inclusion combines the benefits of both finance and digital technology. The aforementioned extensive research demonstrates the positive influence of finance and digital technology on tourism, thereby establishing a solid theoretical foundation for digital financial inclusion to play a constructive role in the tourism sector. Furthermore, the academic community has started to recognize the crucial role of digital financial inclusion in the tourism industry. While a few studies have investigated specific segments within the tourism industry, there has been a lack of comprehensive analysis of its impact on the industry. Moreover, in terms of research samples, most existing domestic literature relies on provincial samples at the macro level and carries out empirical analysis using two primary financial survey databases (China Household Tracking Survey and China Household Financial Survey) at the micro level, neglecting a comprehensive investigation at the prefecture level. Thirdly, there is insufficient research on the internal mechanism of how digital financial inclusion affects residents’ consumption upgrading. In light of these gaps, this paper utilized panel data from 265 prefecture-level cities in China spanning from 2011 to 2019. Firstly, we examined the direct impact of digital financial inclusion on the tourism industry. We then conducted robustness tests by substituting core variables and further investigated the results based on regional and city size differences, as the 265 cities were categorized into east, middle, and west, as well as large, medium-sized, and small cities, to test for heterogeneity in the impact of digital financial inclusion on tourism. Finally, the we explored the dual effects of tourism enterprises and consumption upgrading on tourism from both the supply and demand sides, aiming to provide practical recommendations for digital financial inclusion to promote tourism development.

3. Theoretical Analysis and Research Hypothesis

In recent years, the rapid advancement of digital technology and platforms has facilitated the integration of digital financial inclusion into all aspects of residents’ lives. The significant growth potential generated by the mega market since the 13th Five-Year Plan has provided robust support for China’s economy to achieve high-quality development. As the quality of life improves, residents are increasingly seeking consumer goods that contribute to personal development and enjoyment, such as medical care, insurance, and recreation, which have demonstrated greater market potential. The remarkable surge in tourism revenue, popular attractions, thriving cultural scene, well-organized holiday trips, and efficient food and accommodation arrangements have all been made possible through the utilization of big data and online payment reservation technologies.

Firstly, digital financial inclusion allows for transactions to take place across time and space, facilitating convenient advance reservation of accommodations and food. Transaction vouchers, easily accessible for verification, reduce the likelihood of conflicts arising.

Secondly, the provision of open and transparent information in online transactions enables tourists to plan their attraction reservations and travel routes in advance, thereby improving travel efficiency [44]. Additionally, the volume of online transactions and the feedback received regarding tourism experiences can serve as effective tools in promoting the image of tourism. In the era of “Internet for All,” this extends the travel experience for tourists, allowing them to fully comprehend the nature of the travel service prior to their event, immerse themselves in the travel experience during the event, and evaluate their travel experience afterwards through feedback. Furthermore, this enables travel suppliers to gain comprehensive insights into tourists’ demands and innovate their travel services and products accordingly.

Thirdly, the development of digital insurance provides additional protection for travelers. Insurance products such as hotel cancellation insurance and flight delay insurance, which offer enhanced consumer experiences, are highly favored by consumers. Lastly, the advancement of digital financial inclusion facilitates the provision of efficient financial services for small, medium, and micro-enterprises, thereby promoting the rapid growth of cultural and entertainment enterprises, restaurants, and accommodation [39,45]. Based on these observations, the paper proposes Hypothesis 1.

H1.

Digital financial inclusion improved the tourism economy.

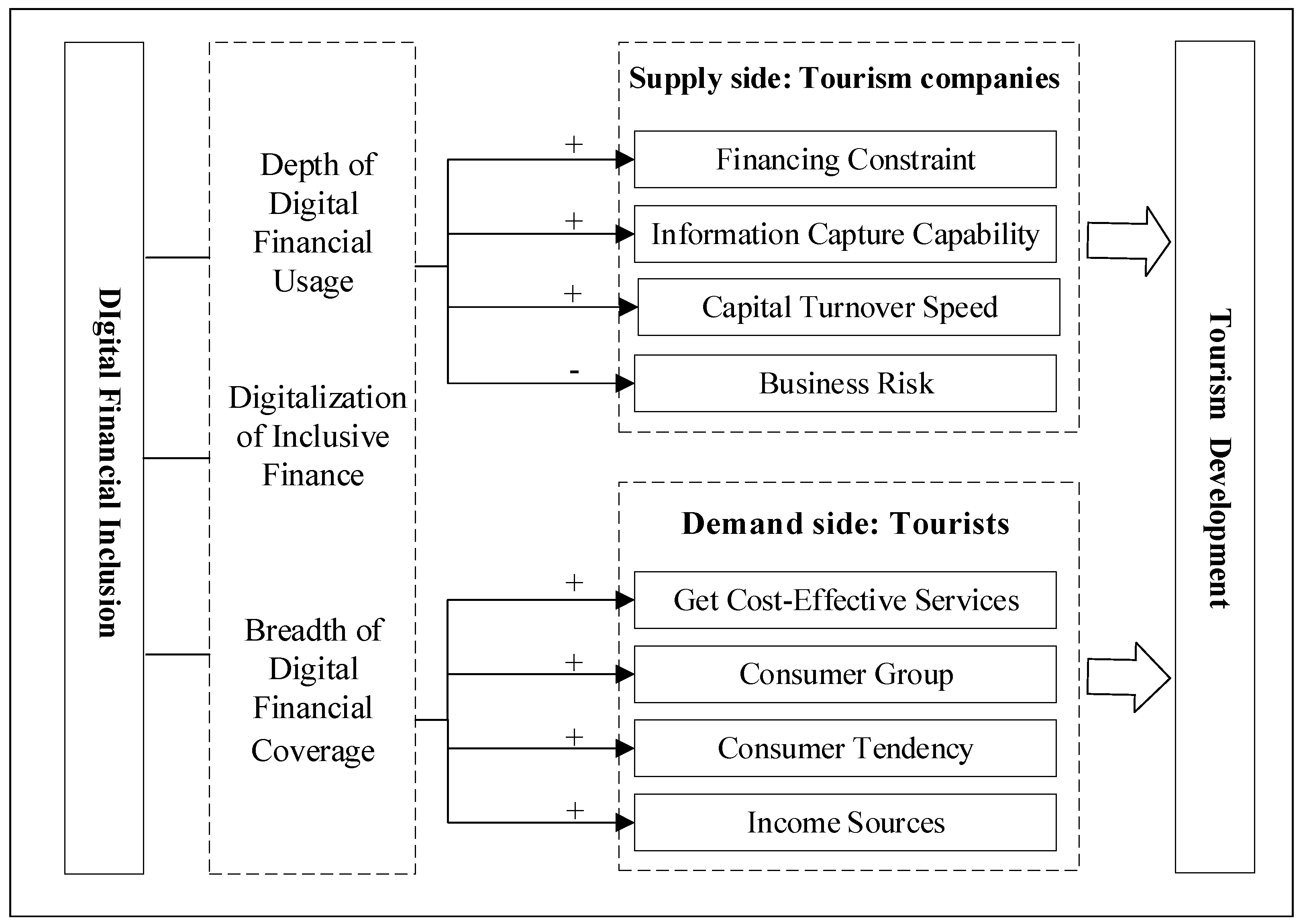

Digital financial inclusion plays a crucial role in the development of the tourism industry through two key mechanisms. Figure 1 illustrates the analysis of the impact of digital financial inclusion on tourism development. Firstly, it enhances the efficiency and quality of tourism services from the supply side. The development of digital financial inclusion has led to changes in consumer habits, enabling them to efficiently plan and book their trips online, thereby making travel more convenient. Moreover, it improves the accessibility of financing for tourism enterprises, expanding their avenues for funding. By reducing information asymmetry and alleviating financing constraints, tourism businesses can secure the necessary funds for research and development (R&D), production, and operational activities, ultimately promoting industry growth.

Secondly, digital financial inclusion facilitates access to information for tourism enterprises, thereby facilitating the dissemination and feedback of dynamic information regarding business, technology, and services. Using big data, tourism service providers can better understand customer needs, develop more personalized products and services, and swiftly adapt their offerings. Additionally, digital finance provides online service channels that facilitate information transmission and social interaction. This, in turn, broadens business cooperation opportunities and strengthens social relations, ultimately boosting the development of the tourism service industry [46].

Furthermore, digital financial inclusion provides digital insurance services for enterprises, enabling them to better mitigate the business risks encountered during the development of the service industry. This improves productivity and mitigates economic volatility through high-quality risk sharing, thereby promoting growth and development in the tourism service industry.

In conclusion, this paper proposes Hypothesis 2, which suggests that digital financial inclusion has a positive impact on the development of the tourism industry. This impact primarily stems from the promotion of tourism from the supply side through improvements in efficiency and quality in tourism services, the facilitation of access to information for tourism enterprises, the generation of online service channels, and the provision of digital insurance services for enterprises.

H2.

Digital financial inclusion can effectively promote the rapid development of tourism service enterprises.

Digital financial inclusion enables a greater number of individuals to access convenient and high-quality financial products and services through digital technology, thereby facilitating increased consumption and promoting consumption upgrading [47]. This includes enhancements to both the level and structure of consumption. The convenience and low cost offered by digital financial inclusion are significant benefits in promoting online consumption [48]. Well-known platforms like WeChat and Alipay provide efficient, inclusive, and convenient online payment systems that reduce shopping times, lower shopping costs, and enhance payment convenience, thereby stimulating consumption [49].

Moreover, digital finance enriches traditional credit services and expands its user base, making credit services more accessible to the public. This not only alleviates liquidity and budget constraints but also creates more opportunities for consumption, thus stimulating consumption and driving the development of related consumer service industries. Digital insurance has emerged as another factor that motivates consumption by offering superior protection for individuals’ lives and property, reducing their propensity to save, and increasing their confidence in the face of future uncertainty [50].

Lastly, the development of digital finance creates more employment opportunities and enhances financial returns, thereby increasing income and further promoting consumption [51]. In the classical macro model, individuals function as both suppliers and consumers, supporting the hypothesis that digital technology can illustrate consumption upgrading. Through the nurturing of numerous digital platforms and relying on the aforementioned factors, digital technology has significantly reduced the cost of travel services while improving their quality. Consequently, residents can transition freely between work and leisure, contributing to consumption upgrading. Thus, this paper proposes Hypothesis 3.

H3.

Digital finance helps to upgrade consumption, which in turn promotes tourism.

4. Variable Selection and Model Design

4.1. Model Design

To discuss the impact of digital finance on the development of tourism, the following effect model is constructed in this paper.

where the subscripts i and t denote city i and period t; DTIit denotes the level of tourism economic development; Digfinit is the level of digital inclusion, specifically containing the overall digital inclusion index (Index_aggregate) and its sub-indicators, Coverage_breadth, Usage_depth and Digitization_level; and Controlsit are a set of control variables. is an unobservable individual fixed effect for province i. is a time fixed effect, and is a random perturbation term.

Subsequently, to examine the mechanism of the impact of digital finance on tourism economic growth, the econometric model was set up as follows.

where represents the mechanism variables, including the number of real businesses in the tourism industry () and consumption escalation (). The meanings of the remaining variables are the same as in model (1). Model (2) is used to examine the effect of digital financial inclusion on the mechanism variables, and model (3) is designed to examine the effect of the mechanism variables on the tourism industry.

4.2. Variable Selection

- (1)

- Explained variables

Depending on the study population and available data, the existing literature differs in the selection of variables to measure tourism outcomes and their determinants. Most studies use tourism revenue and tourist arrivals as indicators of local tourism economic development [52]. In this paper, the domestic tourism revenue of each city was chosen as an indicator of tourism development, and the number of domestic tourist arrivals was measured as a robustness test. The data were obtained from the Wind database and the statistical bulletin of each city. Individual missing values were supplemented using interpolation methods to ensure data completeness.

- (2)

- Core explanatory variables

To examine the impact of digital financial inclusion development on tourism, this paper utilized the latest edition of the China Digital Financial Inclusion Development Index issued by the Digital Finance Research Center of Peking University [53]. This index, jointly compiled by the Digital Finance Research Center of Peking University and Ant Financial Services Group, is based on Ant Financial Services’ transaction account data and is widely used in empirical studies due to its representativeness and reliability. The Digital Financial Inclusion Index includes three sub-indicators: breadth of digital financial coverage, depth of digital financial usage, and digitalization, which comprehensively measure the development of digital financial inclusion.

- (3)

- Mechanism variables

(a) Attracting more market players. The number of tourism enterprises is counted based on the basic information of registered enterprises in the business and industry sectors. This includes the number of registered and surviving enterprises in culture, sports, and entertainment, as well as in accommodation and catering. The development of the tourism industry is closely tied to the presence of accommodation and food enterprises. Meeting the demand for accommodation and food is essential for the modern tourism industry, as the experience of eating and staying has become a central aspect of travel. Therefore, the number of registrations for such businesses is not an appropriate indicator for considering the impact of digital financial inclusion on tourism development from a supply perspective. The number of registrations reflects market prosperity and serves as an important indicator of the market’s economic dynamism, while the number of surviving enterprises proxies the size of the market and the level of tourism enterprise development in each region.

(b) We will upgrade consumer spending. Consumption upgrading includes not only an improvement in consumption level, but also the upgrading of consumption structure. The existing literature on domestic consumption upgrading is divided into two categories. One is from the provincial level, because the provincial level has more direct subdivided consumption categories of residents, consumption upgrading can be measured by simple calculation of subsistence consumption expenditure, enjoyment consumption expenditure and development consumption expenditure, and digital finance has significantly promoted consumption upgrading [54]. The other is from the micro level, with the help of China Household Micro survey data (CFPS) or China Household Finance Survey data (CHFS) research analysis [55]. In this paper, according to Yang et al.’s study on the impact of digital finance on consumption upgrading, consumption upgrading was measured by the consumption expenditure of high-end commodities [47]. In other words, consumption upgrading was measured by excluding the per-capita expenditure on food, tobacco and alcohol in per-capita consumption expenditure and using 1998 as the base period for price index deflating treatment.

- (4)

- Control variables

In this paper, we examined several control variables to better understand the factors influencing the development of tourism by digital finance. These control variables were selected based on their relevance and importance in the context of regional economic development and tourism. The chosen control variables are as follows:

(a) GDP per capita: We used GDP per capita as a measure of the level of regional economic development. The level of economic development is crucial for the growth of tourism and related support industries.

(b) Number of national 5A scenic spots: The number of 5A grade scenic spots, which are designated by the National Bureau of Culture and Tourism, reflects the ability of cities to develop local tourism resources. Compared to other indicators such as world heritage sites and scenic spots of lower grades, the number of 5A scenic spots has better time-varying and accessibility characteristics [52].

(c) Level of urban transportation: The convenience of transportation directly affects the number of tourists visiting a destination. To measure the superiority of urban transportation, we used the ratio of urban road mileage to administrative land area.

(d) Level of public expenditure: Public expenditure indicates the ability of local governments to finance and provide public infrastructure that promotes tourism, as well as organize cultural or sporting events that attract tourists. In this paper, we used fiscal expenditure as a share of GDP to measure the level of public expenditure.

(e) Education level: The share of education expenditure was used in this study as a measure of local investment in education, which indirectly reflects the strength of human capital and its potential impact on tourism development.

(f) Level of service industry development: The ratio of tertiary industry employees is used to gauge the level of service industry development. As the tourism sector is closely related to the service industry, this control variable can provide insights into the overall development of the tourism sector.

(g) Industrial structure: The proportion of tertiary industry output value to total output value was used to measure the industrial structure. A higher proportion of outputs from the tertiary industry indicates a greater emphasis on service-oriented industries, which is conducive to the development of tourism.

(h) Level of openness to the outside world: Cities with a high level of openness tend to have greater cultural inclusiveness and a more diversified economic development. To measure the level of external openness, we used the proportion of real foreign investment to GDP.

These control variables were chosen to ensure a comprehensive analysis of the factors affecting the development of tourism by digital finance. By including these variables, we aimed to control for other factors that may influence the relationship between digital finance and tourism development.

We conducted an empirical study using data from 265 prefecture-level cities in China from 2011 to 2019. The data for the core explanatory variables were derived from the digital financial inclusion Development Index published by the Digital Finance Research Center of Peking University. The mechanism variables were obtained from various sources, including the CnOpenData database, China Statistical Yearbook, China Urban Statistical Yearbook, China Rural Statistical Yearbook, China Social Statistical Yearbook, and statistical bulletins of each province. The data for the explanatory variables and control variables were mainly sourced from the statistical yearbooks of provinces and cities, the Wind database, and statistical bulletins of cities. We addressed any missing values in the sample by employing linear interpolation. The descriptive statistics of specific variables can be found in Table 1.

5. Research Results and Analysis

5.1. Benchmark Model Testing

As detailed in this section, we examined the effects of each level of sub-indicators of digital financial inclusion on the level of urban tourism development separately using benchmark regressions. The regression results, presented in Table 2, show that digital financial inclusion had a positive effect on tourism economic growth at a significant level of 1% in both cases: without and with the addition of control variables. Controlling for other influencing factors, every 1% increase in the level of digital financial inclusion corresponded to an increase of 9.67 percentage points in urban tourism economic development. The economic significance remained significant, although it decreased from 9.67 to 7.28 percentage points. Turning our attention to the sub-indicators of digital financial inclusion, we observe from columns (3) to (5) that breadth of coverage, depth of use, and digitalization all had positive and significant effects on urban tourism economic growth. Furthermore, these sub-indicators had differing impacts on the level of urban tourism economic development. Specifically, depth of use had the most significant positive contribution to tourism economic growth, followed by breadth of coverage, while digitization had the weakest effect. It is worth noting that depth of use encompasses measurements related to payments, insurance, and credit, indicating that these three aspects of digital financial inclusion play a more vital role in tourism development.

In terms of control variables, several factors are expected to have a positive effect on economic growth in tourism. Specifically, variables such as GDP per capita, the share of employees in the tertiary sector, and the level of tourism resource endowment are likely to promote tourism growth. This finding aligns with empirical evidence. Maslow’s hierarchy of needs theory supports the idea that an increase in residents’ income enables them to meet not only their material needs, but also their spiritual needs. As a result, there is an increased demand for leisure time consumer goods, such as tourism experiences. Additionally, a higher proportion of employees in the tertiary sector indicates a more developed service industry in the region, as well as a greater availability of tourism resources. This makes it more appealing for tourists to visit the region and have a more immersive experience of the local customs and culture. On the other hand, factors such as industrial structure, education level, and public expenditure do not significantly contribute to tourism growth. Furthermore, external openness and traffic density do not have a significant impact on the development of local tourism. The lack of impact of external openness can be attributed to the use of domestic tourism revenue as the dependent variable. Additionally, the measure of traffic density may not be capturing the recent increase in high-speed rail travel, as it is solely based on the ratio of road miles to land area.

5.2. Robustness Tests

To ensure rigorous and reliable findings, several robustness tests were conducted in this study to examine the impact of digital financial inclusion on tourism development. Firstly, the extreme values in the sample were excluded to minimize the influence of regions with significantly higher or lower levels of tourism economic development and digital inclusion finance. This was performed by subjecting the explanatory variables and core explanatory variables to a 1% tailoring process prior to regression analysis, as shown in column (1) of Table 3. The results of this tailoring treatment were compared with the baseline model to assess the robustness of the findings.

Secondly, the measure of the level of tourism development was replaced with the measure of the number of domestic tourists to avoid any potential bias associated with using the measure of domestic tourism income exclusively. The regression results, after replacing the explanatory variables, are presented in column (2) of Table 3. It can be observed that the regression coefficient of digital financial inclusion remained significantly positive, which is consistent with the baseline regression results. This indicates the robustness of the conclusions drawn in this paper.

Lastly, a re-estimation was conducted by removing four municipalities from the sample. This was necessary to ensure comparability between ordinary prefecture-level cities and municipalities, as the special administrative status of municipalities can affect the analysis. The re-estimation results were consistent with the benchmark regression, providing further evidence of the robustness of the main conclusions of the previous paper.

5.3. Heterogeneity Analysis

Considering the vast size of China, there are evident convergence characteristics and strong spatial agglomeration in the development of digital financial inclusion across different regions. Some regions demonstrate better development of digital financial inclusion, while others are lagging in this aspect [52,56]. Due to potential regional disparities in the impact of digital financial inclusion on the tourism economy, this study categorized the sample into three regions: east, central, and west, based on the locations of different cities. The corresponding results are presented in columns (1) to (3) of Table 4. The comparison reveals that the influence of digital financial inclusion on tourism economic growth remained consistent across the samples. However, the magnitude of the coefficient shows a decreasing trend from the east to the west and central regions. This divergence can be attributed to several factors. Firstly, the eastern region is more economically developed, with higher rates of technological penetration and progressive consumption concepts. This leads to a preference for tourism services to enhance experiential benefits, thereby increasing the demand for regional tourism products and facilitating the integration of digital financial inclusion into local tourism development. In contrast, the central region is predominantly dominated by heavy industries and boasts high population density, which may hinder the development of ecological environments and tourism. Consequently, the role of digital financial inclusion in promoting tourism is limited in this region. The impact of digital financial inclusion on tourism in the western region falls between the eastern and central regions, potentially because the western region benefits from the overall economic development and higher proportion of tertiary industries. Additionally, the ecological landscapes and local customs in the western region are more attractive to tourists, thereby increasing the likelihood of digital financial inclusion promoting local tourism development. Furthermore, there is notable heterogeneity in city size, and this heterogeneity is more pronounced than that observed in the eastern and western regions. This finding suggests that the development of digital financial inclusion is more likely to facilitate the advancement of tourism in large and medium-sized cities. The promotion of digital financial inclusion in the tourism sector relies heavily on cities with large populations, indicating that digital financial inclusion plays a crucial inclusive role in economic development. Cities with larger populations, more livable environments, and more developed economies tend to be more receptive to digital inclusion, and therefore, more likely to drive tourism growth.

5.4. Mechanism Testing

This paper examined the impact of digital financial inclusion on the development of tourism enterprises and the consumption upgrade of residents. The findings are presented in Table 5, specifically (1) to (4) respectively.

The study shows that the digital financial inclusion index significantly influences the number of registered and surviving tourism enterprises. Additionally, the number of registered and surviving tourism enterprises has a significant impact on domestic tourism revenue. Similarly, (5) to (6) demonstrate the influence path of “digital financial inclusion-consumption upgrading-tourism development level”, thus validating Hypothesis 2 and Hypothesis 3.

Digital financial inclusion effectively addresses the financing needs of micro and small tourism enterprises. The accessibility of capital through inclusive finance benefits real enterprises. The regression coefficient of the number of surviving enterprises is slightly lower than that of the number of registered enterprises, indicating that digital financial inclusion promotes the development of tourism enterprises without blindly directing capital flow. This, in turn, leads to a healthier tourism industry and improved services for consumers.

The development of digital financial inclusion has alleviated capital constraints and increased liquidity. This, along with meeting residents’ quality of life security needs, has promoted consumption upgrading. The tourism industry, which satisfies people’s desires for a high quality of life, is driven by consumption upgrading. Additional tests using the Sobel method and Bootstrap method were conducted to further investigate this relationship. The results, listed in Table 5, indicate that all Sobel test z-values are greater than 1.96, demonstrating significance at the 5% level. Furthermore, the confidence intervals from the Bootstrap test do not contain 0, providing additional evidence for the existence of this mechanism.

6. Conclusions

With the rapid growth of the technology economy and the ever-changing lifestyles of residents, the development of digital financial inclusion has injected new momentum into the real industry [57]. In this paper, we investigate the impact of digital financial inclusion on tourism development using the 2011–2019 Digital Finance Index and analyze the impact mechanism. The paper studies the relationship between digital financial inclusion and tourism development from a new perspective and provides empirical support. Our main findings are as follows:

Digital financial inclusion significantly contributes to tourism development, passing the robustness test. The results of the sub-indicator test demonstrate that the breadth of coverage, depth of use, and digitization of digital financial inclusion all promote tourism development. Digital financial inclusion presents heterogeneity to tourism development. On the one hand, digital financial inclusion shows a significant promotion effect in the east and west, but a weaker promotion effect in the center. On the other hand, its impact also indicates a decreasing promotion effect with the size of cities from large to small. Meanwhile, the impact of city size is much larger than that of regional heterogeneity. Our mechanism analysis reveals that digital financial inclusion not only promotes the development of tourism enterprises from the supply side but also enhances residents’ consumption upgrading from the demand side, promoting tourism development.

Based on our findings, we offer three policy insights. Firstly, it is crucial for the government to establish and implement policies that support the advancement of digital financial inclusion, aiming to enhance its scope, usability, and level of digitalization. This involves incentivizing financial institutions to offer a wider range of digital financial products and services, reducing barriers for accessing digital finance, and fostering the innovation and implementation of digital financial technology. Moreover, the government should reinforce regulations and risk management practices to ensure the sustainable growth of digital financial inclusion. Additionally, particular attention should be given to the inclusive nature of digital financial inclusion, ensuring its benefits reach various groups, especially those in rural areas and individuals with low income.

Secondly, the government should enhance its support and guidance for the tourism industry to maximize the impact of digital financial inclusion on its development. Alongside providing financial aid and tax incentives, the government should devise policies and regulations that facilitate the deep integration of digital financial inclusion and tourism. This can involve establishing programs for digital financial training and consultancy, enabling tourism enterprises to receive guidance and support in their digital transformation efforts. Furthermore, it is essential to strengthen the development of tourism infrastructure and digital tourism at a technological level.

Thirdly, tourism enterprises should actively embrace digital financial inclusion tools to bolster their growth and competitiveness. Collaborating with financial institutions, they can engage in innovative strategies to promote digital financial products, such as offering online payment options, digital marketing, and booking services. Additionally, tourism enterprises should prioritize interaction and communication with consumers, delivering personalized digital financial services to fulfill their needs and enhance their overall tourism experience. Furthermore, the government can incentivize tourism enterprises to adopt digital technologies, providing digital platforms for tourism information and services, and driving the digital transformation of the tourism industry.

Finally, considering the variations across regions and city sizes, it is proposed to support the development of digital payment and electronic transaction infrastructure. This initiative aims to ensure convenient electronic payment options for all regions and to promote tourism consumption. Additionally, offering digital finance training and education to residents in rural and remote areas will enhance their awareness and usage of digital finance. It is also encouraged for digital financial institutions to establish branches in remote areas to provide financial services and support tourism development. In major cities, like Nanjing in Jiangsu Province, the promotion of digital payment and mobile payment will be prioritized to facilitate convenient consumption and payment for tourists. For small cities and rural areas, targeted training on digital financial technologies and services will be provided to help local businesses enhance their financial management and payment capabilities. The ultimate goal is to attract more tourists and investment in those areas.

The present study is constrained in examining the influence of digital financial inclusion on tourism beyond 2020 due to data acquisition difficulties. Therefore, it is imperative to undertake future research that encompasses a more exhaustive and meticulous investigation of this matter. A suggested approach would involve comparing the impact of digital financial inclusion on tourism prior to, during, and following the epidemic. This comparative analysis can furnish researchers with the means to propose more pragmatic policy recommendations.

Although this paper verifies that digital financial inclusion can promote tourism development, some problems still need to be paid attention to in the practical application process. For example, the application of digital financial inclusion in the tourism industry often requires the acquisition and processing of large amounts of personal and sensitive data. Therefore, protecting users’ data privacy and ensuring data security are of paramount importance. Governments and enterprises should develop strict data protection policies and measures to ensure that users’ personal information is not abused or leaked. In addition, the development of digital finance may lead to the deepening of the digital divide. When promoting the use of digital finance in the tourism industry, governments and businesses should ensure the accessibility and inclusion of digital financial inclusion services to ensure that all people can equally enjoy the benefits of digital finance. Finally, the promotion of tourism by the development of digital finance may have a positive or negative impact on society. For example, the popularity of digital payments may improve the convenience of travel consumption, but it may also lead to the decline of the cash economy and the marginalization of some social groups. Therefore, when promoting the development of digital finance, governments and enterprises should consider the overall interests of society, take measures to mitigate negative impacts, and ensure that the development of digital financial inclusion is in line with the principles of social equity and sustainable development. In short, governments, businesses, and all sectors of society should work together to ensure that the development of digital finance and tourism is sustainable and responsible.

Author Contributions

Conceptualization, C.Z. and Z.P.; methodology, Y.L.; software, Y.L.; validation, C.Z., Z.P. and Y.L.; formal analysis, C.Z.; investigation, Y.L.; resources, Y.L.; data curation, Y.L.; writing—original draft preparation, C.Z.; writing—review and editing, C.Z.; visualization, C.Z.; supervision, Z.P.; project administration, Z.P.; funding acquisition, Z.P. All authors have read and agreed to the published version of the manuscript.

Funding

This research work was funded by the National Key R&D Program, China, grant number 2022YFC3802901-04, Jiangsu Social Science Fund, grant number 22EYA003, and Social Science Fund, Nanjing University of Posts and Telecommunications, grant number NYY219004.

Data Availability Statement

The data presented in this study are available on request from the corresponding author.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Ozili, P.K.; Ademiju, A.; Rachid, S. Impact of Financial Inclusion on Economic Growth: Review of Existing Literature and Directions for Future Research. Int. J. Soc. Econ. 2023, 50, 1105–1122. [Google Scholar] [CrossRef]

- Gul, F.; Muhammad, U.; Muhammad, T.M. Financial Inclusion and Economic Growth: A Global Perspective. J. Bus. Econ. 2018, 10, 133–152. [Google Scholar]

- Arnold, B.; Claudio, B.; Luci, E.; Fariborz, M. Systemic Risk, Macroprudential Policy Frameworks, Monitoring Financial Systems and the Evolution of Capital Adequacy. J. Bank. Financ. 2012, 36, 3125–3132. [Google Scholar] [CrossRef]

- Khadaroo, J.; Seetanah, B. Transport Infrastructure and Tourism Development. Ann. Tour. Res. 2007, 34, 1021–1032. [Google Scholar] [CrossRef]

- Smeral, E. The Impact of the Financial and Economic Crisis on European Tourism. J. Travel Res. 2009, 48, 3–13. [Google Scholar] [CrossRef]

- Yang, Y. Agglomeration density and tourism development in China: An empirical research based on dynamic panel data model. Tour. Manag. 2012, 33, 1347–1359. [Google Scholar] [CrossRef]

- Karadzova, V.; Dicevska, S. Interactions between financial system development and tourism development: Conditions in Republic of Macedonia. Sustain. Tour. Socio-Cult. Environ. Econ. Impact 2011, 169–186. Available online: https://www.zbw.eu/econis-archiv/bitstream/11159/162038/1/EBP073918490_0.pdf (accessed on 1 March 2022).

- Katircioglu, S.; Katircioğlu, S.; Altinay, M. Interactions between tourism and financial sector development: Evidence from Turkey. Serv. Ind. J. 2018, 38, 519–542. [Google Scholar] [CrossRef]

- Khalid, U.; Okafor, L.E.; Sanusi, O.I. Exploring diverse sources of linguistic influence on international tourism flows. J. Travel Res. 2022, 61, 696–714. [Google Scholar] [CrossRef]

- Shi, Y.; Swamy, V.; Paramati, S.R. Does financial inclusion promote tourism development in advanced and emerging economies? Appl. Econ. Lett. 2021, 28, 451–458. [Google Scholar] [CrossRef]

- Barros Nunes, N. Consumer Behaviour in the Tourism Industry: A Quantitative Study of Social Media Influencers’ Impact on Brazilian Millennials; Dublin Business School: Dublin, Ireland, 2021. [Google Scholar]

- Adeola, O.; Evans, O. ICT, Infrastructure, and Tourism Development in Africa. Tour. Econ. 2020, 26, 97–114. [Google Scholar] [CrossRef]

- da Costa Liberato, P.M.; Alén-González, E.; de Azevedo Liberato, D.F.V. Digital technology in a smart tourist destination: The case of Porto. J. Urban Technol. 2018, 25, 75–97. [Google Scholar] [CrossRef]

- Natocheeva, N.; Shayakhmetova, L.; Bekkhozhaeva, A.; Khamikhan, N.; Pshembayeva, D. Digital Technologies as a Driver for the Development of the Tourism Industry. In E3S Web of Conferences; EDP Sciences: Paris, France, 2020; p. 04002. [Google Scholar]

- Tang, R. A study of the effects and mechanisms of the digital economy on high-quality tourism development: Evidence from the Yangtze River Delta in China. Asia Pac. J. Tour. Res. 2022, 27, 1217–1232. [Google Scholar] [CrossRef]

- Perić, J.; Mujačević, E.; Šimunić, M. International financial institution investments in tourism and hospitality. J. Int. Bus. Cult. Stud. 2009, 4, 1–17. [Google Scholar]

- Markandya, A.; Taylor, T.; Pedroso, S. Tourism and Sustainable Development: Lessons from Recent World Bank Experience. In The Economics of Tourism and Sustainable Development; Fondazione Eni Enrico Mattei Series on Economics and the Environment; Lanza, A., Markandya, A., Eds.; Edward Elgar Publishing Ltd.: Cheltenham, UK, 2005; pp. 225–251. [Google Scholar]

- Gautam, B.P. Economic Dynamics of Tourism in Nepal: A VECM Approach. Univ. Libr. Munich Ger. 2014, 5, 1–17. [Google Scholar]

- Islam, Y.; Mindia, P.M.; Farzana, N.; Qamruzzaman, M. Nexus between environmental sustainability, good governance, financial inclusion, and tourism development in Bangladesh: Evidence from symmetric and asymmetric investigation. Front. Environ. Sci. 2023, 10, 1056268. [Google Scholar] [CrossRef]

- Gopalan, S.; Khalid, U. How does financial inclusion influence tourism demand? Empirical evidence from emerging markets and developing economies. Tour. Recreat. Res. 2022, 1–15. [Google Scholar] [CrossRef]

- Feng, J. Study on Financial support for the development of Hakka cultural tourism industry—The case of Meizhou, Guangdong Province. China Stat. 2014, 44–46. [Google Scholar]

- Hu, H.; Huang, L.; Luo, H. Path selection of tourism resources development and financial support in Xinjiang: A case study of financial support for the development of Keketuohai Scenic Spot. J. Xinjiang Norm. Univ. (Philos. Soc. Sci. Ed.) 2012, 33, 32–38. [Google Scholar] [CrossRef]

- Song, R.; Xv, Y. Financing conditions and innovation investment intensity of tourism enterprises. Learn. Explor. 2021, 143–149. [Google Scholar]

- Wei, X.H.; Yang, J.Z.; Cao, W. Research on Dynamic Effects of Financial Support to Tourism Industry Development. Soc.Sci. Educ. Hum. Sci. 2017. [Google Scholar] [CrossRef] [PubMed]

- Zeng, H.; Ma, Y.; Chen, Z.; Wang, Y. Research on the integration and innovation development of Finance and tourism under the construction of Free Trade Port. Mark. Field 2021, 26–28. [Google Scholar]

- Shao, Y. Research on the integration degree of Tourism and financial industry in Zhejiang Province: An empirical study based on data from 2001 to 2016. Econ. Res. Guide 2018, 28, 161–163+172. [Google Scholar]

- Gong Yan, G.Z. An empirical analysis on the coupling and coordinated development of tourism and financial industry: A case study of Jiangsu Province. Tour. Forum 2017, 32, 74–84. [Google Scholar]

- Liao, K.C.; Yue, M.Y.; Sun, S.W.; Xue, H.B.; Liu, W.; Tsai, S.B.; Wang, J.T. An Evaluation of Coupling Coordination between Tourism and Finance. Sustainability 2018, 10, 2320. [Google Scholar] [CrossRef]

- Pencarelli, T. The digital revolution in the travel and tourism industry. Inf. Technol. Tour. 2020, 22, 455–476. [Google Scholar] [CrossRef]

- Marques, L.; Borba, C. Co-creating the city: Digital technology and creative tourism. Tour. Manag. Perspect. 2017, 24, 86–93. [Google Scholar] [CrossRef]

- Wu, H. Develop the theory and practice of global tourism from the perspective of smart tourism. Econ. Probl. Explor. 2018, 08, 60–66. [Google Scholar]

- Zhou, L.; Liu, Y. Research on the Integrated development of tourism industry and Internet. Theor. Discuss. 2019, 114–117. [Google Scholar] [CrossRef]

- Van Nuenen, T.; Scarles, C. Advancements in technology and digital media in tourism. Tour. Stud. 2021, 21, 119–132. [Google Scholar] [CrossRef]

- Cenni, I.; Vásquez, C. Early adopters’ responses to a virtual tourism product: Airbnb’s online experiences. Int. J. Cult. Tour. Hosp. Res. 2021. ahead-of-print. [Google Scholar] [CrossRef]

- Gelb, L. Visitor Connection: Digital Integration Strategy for the Art Museum Experience. Ph.D. Thesis, The University of the Arts, Philadelphia, PA, USA, 2015. [Google Scholar]

- Guo, K.; Fan, A.; Lehto, X.; Day, J. Immersive digital tourism: The role of multisensory cues in digital museum experiences. J. Hosp. Tour. Res. 2023, 47, 1017–1039. [Google Scholar] [CrossRef]

- Shen, Y.; Hueng, C.J.; Hu, W. Measurement and spillover effect of digital financial inclusion: A cross-country analysis. Appl. Econ. Lett. 2021, 28, 1738–1743. [Google Scholar] [CrossRef]

- Ma, L.; Ouyang, M. Spatiotemporal heterogeneity of the impact of digital inclusive finance on tourism economic development: Evidence from China. J. Hosp. Tour. Manag. 2023, 56, 519–531. [Google Scholar] [CrossRef]

- Wang, Q.; Yang, L.; Yue, Z. Research on development of digital finance in improving efficiency of tourism resource allocation. Resour. Environ. Sustain. 2022, 8, 100054. [Google Scholar] [CrossRef]

- Wang, Q.; Yue, Z.; Yang, Y. Digital finance and the growth of entrepreneurial enterprises in rural tourism industry. J. Nanjing Univ. Posts Telecommun. (Soc. Sci. Ed.) 2021, 23, 48–61+102. [Google Scholar] [CrossRef]

- Huang, W. The impact of the development of digital inclusive finance on the growth of inbound tourism consumption. Bus. Econ. Res. 2020, 165–168. [Google Scholar]

- Chaowang, R.; Yuna, R. The integrated development of digital finance and shared tourism from the perspective of financial function. J. Hebei Univ. (Philos. Soc. Sci. Ed.) 2021, 46, 128–137. [Google Scholar]

- Wu, X.; Chang, H. Impact of digital inclusive finance on household tourism consumption: Evidence from China. Eur. J. Innov. Manag. 2023. [Google Scholar] [CrossRef]

- Zhong, K.; Liang, P.; Dong, X.; Wang, X. Digital inclusive finance and secondary allocation of commercial credit. China Ind. Econ. 2022, 170–188. [Google Scholar] [CrossRef]

- Cai, Q.; Wang, H.; Li, D. Internet Lending, Labor productivity and enterprise Transformation: A Perspective of Labor Mobility. China Ind. Econ. 2021, 146–165. [Google Scholar] [CrossRef]

- Xie, F.; Shen, Y.; Zhang, H.; Guo, F. Can Digital Finance Promote entrepreneurship?—Evidence from China. China Econ. Q. 2018, 17, 1557–1580. [Google Scholar] [CrossRef]

- Yang, W.; Su, L.; Sun, R.; Yuan, W. Does digital finance promote consumption upgrading?—Evidence based on panel data. Int. Financ. Res. 2021, 13–22. [Google Scholar] [CrossRef]

- Jiang Jinbo, L.F. The impact of tourism e-commerce maturity on online travel booking intention: A case study of Ctrip. Tour. Trib. 2014, 29, 75–83. [Google Scholar]

- Guo, Y.; Li, X. An empirical study on consumers’ willingness to use mobile payment to purchase travel products: Based on the technology acceptance model and the theoretical model of planned behavior. J. Sichuan Univ. (Philos. Soc. Sci. Ed.) 2018, 6, 159–170. [Google Scholar]

- Yi, X.; Zhou, L. Whether the development of digital financial inclusion has significantly affected household consumption—Micro evidence from Chinese households. J. Financ. Res. 2018, 47–67. [Google Scholar]

- Xiang, Y. Study on the impact of Digital inclusive finance on rural residents’ consumption: Based on dynamic effect and threshold effect. Bus. Econ. Res. 2022, 172–176. [Google Scholar]

- Gao, Y.; Nan, Y.; Song, S. High-speed rail and city tourism: Evidence from Tencent migration big data on two Chinese golden weeks. Growth Chang. 2022, 53, 1012–1036. [Google Scholar] [CrossRef]

- Guo, F.; Wang, J.; Wang, F.; Kong, T.; Zhang, X.; Cheng, Z. Measuring the development of digital inclusive finance in China: Index compilation and spatial characteristics. China Econ. Q. 2020, 19, 1401–1418. [Google Scholar] [CrossRef]

- Huang, K.; Hao, X. Does digital finance promote household consumption upgrading? Soc. Sci. Shandong 2021, 117–125. [Google Scholar] [CrossRef]

- Li, X.; Li, T.; Zou, W. Does the Internet promote household consumption upgrading?—Research based on micro survey data in China. J. China Univ. Geosci. (Soc. Sci. Ed.) 2019, 19, 145–160. [Google Scholar] [CrossRef]

- Gao, Y.; Lu, Y.; Wang, J. Does Digital Inclusive Finance Promote Entrepreneurship? Evidence from Chinese Cities. Singap. Econ. Rev. 2022, 1–24. [Google Scholar] [CrossRef]

- Ahmad, M.; Majeed, A.; Khan, M.A.; Sohaib, M.; Shehzad, K. Digital financial inclusion and economic growth: Provincial data analysis of China. China Econ. J. 2021, 14, 291–310. [Google Scholar] [CrossRef]

Figure 1.

Mechanisms of digital financial inclusion affecting tourism growth. Note: “+” indicates a positive promoting effect; “−” indicates a negative inhibiting effect.

Figure 1.

Mechanisms of digital financial inclusion affecting tourism growth. Note: “+” indicates a positive promoting effect; “−” indicates a negative inhibiting effect.

{kind=link}

Table 1.

The descriptive statistics of the variables.

| Variables | Indicators | Definition | Obs | Mean | Std. Dev. | Min | Max |

|---|---|---|---|---|---|---|---|

| Explained variables | DTI | Gross Domestic Tourism Revenue | 2385 | 419.72 | 597.02 | 4.6 | 5866.2 |

| Explanatory variables | Index_aggregate | Digital financial inclusion index | 2385 | 165.87 | 65.61 | 17.02 | 321.65 |

| Coverage_breadth | Coverage breadth index | 2385 | 156.23 | 63.65 | 1.86 | 310.91 | |

| Usage_depth | Depth of use index | 2385 | 163.62 | 68.24 | 4.29 | 331.96 | |

| Digitization_level | Digitization index | 2385 | 201.81 | 82.08 | 3.39 | 581.23 | |

| Mechanism Variables | Zindustry | Number of recreation and restaurant business registration | 2385 | 5923.49 | 7489.09 | 148 | 92148 |

| Cindustry | Number of surviving recreation and restaurant companies | 2385 | 34,488.86 | 48,376.96 | 762 | 740,571 | |

| Consumption | Consumption upgrade | 2385 | 8932.071 | 3084.17 | 2600.16 | 24,354.1 | |

| Control variables | Pergdp | GDP per capita | 2385 | 52,528.21 | 34,334.51 | 6457 | 467,749 |

| Ptieq | Percentage of employees in the tertiary sector | 2385 | 53.29 | 13.57 | 15.39 | 94.82 | |

| Str | Tertiary sector output/GDP | 2385 | 41.80 | 10.51 | 14.36 | 83.52 | |

| Fexp | Fiscal spending/GDP | 2385 | 0.11 | 0.10 | 0.0038 | 1.2905 | |

| Edu | Education spending/GDP | 2385 | 0.01 | 0.02 | 0.0000 | 0.1373 | |

| Open | Real foreign investment/GDP | 2385 | 0.00 | 0.01 | 0 | 0.2484 | |

| Tra | Number of road miles/land area | 2385 | 1.09 | 0.49 | 0.0680 | 2.6279 | |

| Res | Number of 5A-class scenic spots | 2385 | 0.61 | 1.05 | 0 | 9 |

Table 2.

The impact of indicators of digital financial inclusion on tourism.

| Tourism Development DTI | |||||

|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | |

| Index_aggregate | 9.6730 *** (8.393) | 7.2818 *** (6.486) | |||

| Coverage_breadth | 1.9861 * (1.770) | ||||

| Usage_depth | 3.4537 *** (4.844) | ||||

| Digitization_level | 1.3244 *** (4.962) | ||||

| Pergdp1 | 121.4322 *** (3.483) | 173.4626 *** (4.828) | 170.1419 *** (4.885) | 172.9019 *** (4.929) | |

| Ptieq | 4.5070 *** (4.429) | 4.8928 *** (4.714) | 4.4630 *** (4.466) | 4.4274 *** (4.311) | |

| Str | −5.1556 *** (−3.994) | −5.3690 *** (−4.133) | −5.0971 *** (−3.908) | −5.3462 *** (−4.088) | |

| Fexp | −119.9633 * (−1.735) | −156.9529 * (−1.911) | −137.0940 * (−1.864) | −129.3533 * (−1.664) | |

| Edu | −1751.1785 *** (−3.052) | −2427.7734 *** (−3.785) | −1859.4333 *** (−3.149) | −1961.5867 *** (−3.232) | |

| Open | −22.9678 (−0.071) | −13.2869 (−0.040) | −46.5290 (−0.136) | 39.4035 (0.126) | |

| Tra | −79.1524 (−0.875) | −79.5698 (−0.884) | −72.5675 (−0.807) | −82.1855 (−0.919) | |

| Res | 175.3156 *** (5.749) | 183.2928 *** (5.898) | 190.1258 *** (6.205) | 182.1424 *** (5.914) | |

| Constant | −1184.7663 *** (−6.210) | −2055.7279 *** (−4.729) | −1718.0727 *** (−3.900) | −1943.2919 *** (−4.352) | −1649.6115 *** (−3.789) |

| Obs | 2385 | 2385 | 2385 | 2385 | 2385 |

| R-squared | 0.895 | 0.901 | 0.898 | 0.899 | 0.899 |

| City FE | YES | YES | YES | YES | YES |

| Year FE | YES | YES | YES | YES | YES |

Note: *, **, and *** denote 1%, 5%, and 10% significance levels in the two-tailed test, respectively.

Table 3.

Robustness test.

| (1) | (2) | (3) | |

|---|---|---|---|

| Domestic Tourism Revenue-Tailoring | Number of Domestic Tourists | Domestic Tourism Revenue | |

| VARIABLES | DTI_w | DTC | DTI |

| Index_aggregate_w | 4.5950 *** (5.486) | ||

| Index_aggregate | 391.6851 *** (3.697) | 6.6333 *** (6.529) | |

| Controls | YES | YES | YES |

| Obs | 2385 | 2385 | 2349 |

| R-squared | 0.912 | 0.794 | 0.875 |

| City FE | YES | YES | YES |

| Year FE | YES | YES | YES |

Note: *, **, and *** denote 1%, 5%, and 10% significance levels in the two-tailed test, respectively.

Table 4.

Heterogeneity tests.

| East | Middle | West | Large Cities | Medium-Sized Cities | Small Cities | |

|---|---|---|---|---|---|---|

| Index_aggregate | 11.2997 *** (5.209) | 5.2024 *** (3.929) | 6.8641 *** (3.256) | 10.6885 *** (4.033) | 1.7386 ** (2.070) | 0.7766 (1.445) |

| Controls | YES | YES | YES | YES | YES | YES |

| Obs | 954 | 819 | 612 | 774 | 927 | 684 |

| R-squared | 0.936 | 0.899 | 0.832 | 0.911 | 0.832 | 0.843 |

| City FE | YES | YES | YES | YES | YES | YES |

| Year FE | YES | YES | YES | YES | YES | YES |

Note: *, **, and *** denote 1%, 5%, and 10% significance levels in the two-tailed test, respectively.

Table 5.

Impact mechanism test.

| (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| Tourism Business Survival Number | Domestic Tourism Revenue | Number of Tourism Enterprises Registered | Domestic Tourism Revenue | Consumption Upgrade | Domestic Tourism Revenue | |

| VARIABLES | Cindustry1 | DTI | Zindustry1 | DTI | Consumption1 | DTI |

| Cindustry1 | 7.8432 *** (12.124) | |||||

| Zindustry1 | 2.2954 *** (5.344) | |||||

| Consumption1 | 0.0340 *** (6.042) | |||||

| Index_aggregate | 0.8251 *** (9.540) | 0.8073 (0.921) | 0.9215 *** (5.886) | 5.1633 *** (4.593) | 22.9516 *** (4.444) | 6.4975 *** (6.155) |

| Controls | YES | YES | YES | YES | YES | YES |

| Obs | 2385 | 2385 | 2385 | 2385 | 2385 | 2385 |

| R-squared | 0.893 | 0.944 | 0.808 | 0.915 | 0.805 | 0.898 |

| City FE | YES | YES | YES | YES | YES | YES |

| Year FE | YES | YES | YES | YES | YES | YES |

| Sobel method | 0.7045 *** (6.591) | 0.7323 *** (7.618) | 0.2997 *** (6.161) | |||

| Bootstrap method | [0.5209, 0.8881] | [0.5100, 0.9546] | [0.1767, 0.4226] | |||

Note: *, **, and *** denote 1%, 5%, and 10% significance levels in the two-tailed test, respectively. 95% confidence intervals are shown in parentheses.

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Zhang, C.; Liu, Y.; Pu, Z. How Digital Financial Inclusion Boosts Tourism: Evidence from Chinese Cities. J. Theor. Appl. Electron. Commer. Res. 2023, 18, 1619-1636. https://doi.org/10.3390/jtaer18030082

AMA Style

Zhang C, Liu Y, Pu Z. How Digital Financial Inclusion Boosts Tourism: Evidence from Chinese Cities. Journal of Theoretical and Applied Electronic Commerce Research. 2023; 18(3):1619-1636. https://doi.org/10.3390/jtaer18030082

Chicago/Turabian StyleZhang, Chi, Yayu Liu, and Zhengning Pu. 2023. "How Digital Financial Inclusion Boosts Tourism: Evidence from Chinese Cities" Journal of Theoretical and Applied Electronic Commerce Research 18, no. 3: 1619-1636. https://doi.org/10.3390/jtaer18030082