Regulatory Implications of the Supervision and Management of Liquidity Risk: An Analysis of Recent Developments in Spanish Financial Institutions

Abstract

:1. Introduction

- Channeling money from economic agents with a surplus, the savers or investors, to the economic agents demanding this liquidity who need to finance themselves in order to develop their investment projects.

- Transforming maturities, so that customers deposit money with the bank with mostly immediate availability and the bank lends it over the medium to long term.

- The transformation of money in its different forms of financial liabilities, such as deposits or debt securities into multiple and distinct financial assets, such as loans and mortgages.

- Provide the economy with levels of confidence and stability that allow money to flow, transform, and enable payment systems to function normally.

2. An Approach to Liquidity Risk and Liquidity Risk Management Principles

- (a)

- Funding liquidity and market liquidity, given that the concept of liquidity has, initially, two dimensions: funding liquidity, which measures an institution’s ability to meet its payment obligations as agreed; and market liquidity, which measures an institution’s ability to generate or unwind positions in a given market situation.

- (b)

- Timeframes, which commonly consider the short term, about one month, although it could be extended to three months; the medium term, which is usually considered up to one year; or, exceptionally, up to eighteen months, the usual timeframe in which they measure; and the long term above this time dimension.

- (c)

- Liquidity in normal conditions and liquidity in crisis situations. The former considers environments with normal market conditions, and applies going concern criteria to the institution. Liquidity in crisis situations is situated in environments of generalized, structural or systemic market crises.

- Situations arising from the institution’s own daily operations, and/or minor systemic crises.

- Situational crises originating internally or externally to the institution itself, in which liquidity needs arise due to temporary mismatches between cash inflows and outflows arising from normal operations and/or the uneven evolution of asset and liability transactions.

- Severe systemic crises, caused by factors external to the financial institution, including macroeconomic crises, and where liquidity needs are caused by capital market or payment system dysfunction.

- Severe specific or intrinsic crises, with severe liquidity needs caused by factors internal to the financial institution that generate loss of confidence, e.g., negative rumors, a rating downgrade, insufficient capital or a large reduction in earnings.

- Combined crisis, which contains the liquidity needs caused by factors internal and external to the financial institution, being the worst-case scenario.

“A bank is responsible for sound liquidity risk management. A bank should establish a robust liquidity risk management framework that ensures that the bank maintains sufficient liquidity, including a cushion of unencumbered, high-quality liquid assets, to withstand a range of stress events, including those that result in the loss or impairment of both secured and unsecured funding sources. Supervisors should assess the adequacy of a bank’s liquidity risk management framework and liquidity position. Supervisors should take appropriate action if they identify weaknesses in either of these areas in order to protect depositors and limit potential damage to the financial system”.

3. Regulatory Framework and New Instruments: Regulation and Supervision of Liquidity Risk

3.1. Liquidity Coverage Ratio (LCR)

- *

- Factors for which the institution may decrease the ratio below 100%.

- *

- Verify whether a decline is due to a cyclical market situation or to the institution itself.

- *

- Significance of the fall in the stock of liquid assets, as well as its frequency and possible duration.

- *

- Overall assessment of the institution and its risk profile.

- *

- Potential transmission or contagion to the system with the reduction in liquidity in the market.

- *

- Alternative financing measures such as through central banks.

3.2. Net Stable Funding Ratio (NSFR)

4. Methodology

5. Analysis and Discussion of Results

5.1. An Overview of the Banking Sector in Spain in a Globalized Context

- Mergers and acquisitions, with a clear process of concentration in the banking sector, leading to the creation of larger financial groups. This has enabled credit institutions to increase their size and diversify their activity, improving their ability to compete in the market.

- Branch reductions, accelerated by technological developments and changing customer habits, which have led banks to reduce their network. Many banks have opted for digital banking and online services, enabling them to reduce costs and improve efficiency.

- Increased specialization, so that institutions have been evolving towards greater specialization in certain sectors or financial products.

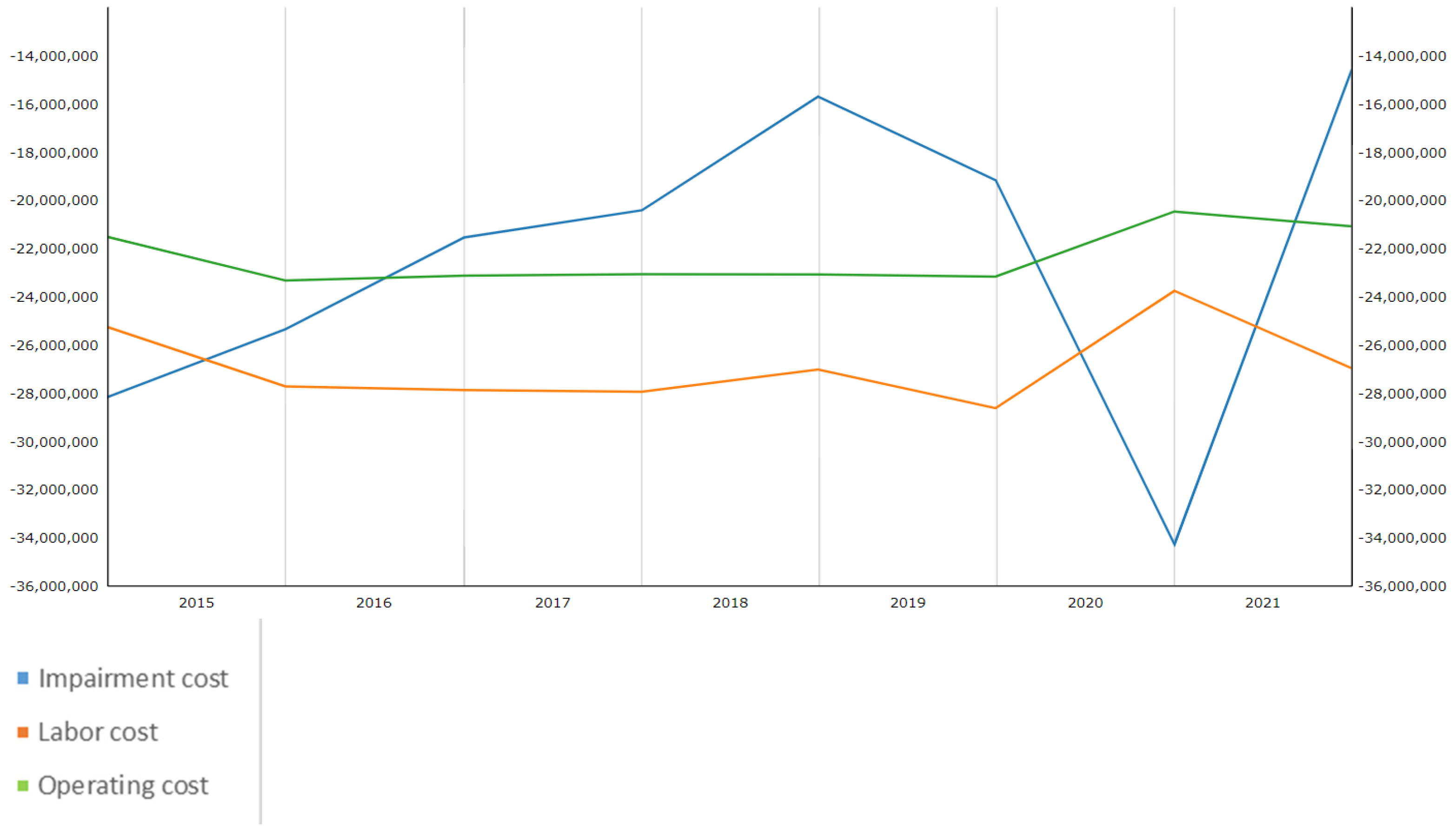

- For the 15-year period under study, it is worth mentioning that, in the baseline year of the study in 2009, Spanish banks were making a profit, while European banks were making a loss.

- From 2009 onwards, the evolution was the opposite: European banks made profits in 2010, tripling their profits in 2012, while in those two years Spanish banks gradually reduced the positive results of their profit and loss accounts.

- Between 2011 and 2013, there was a gradual deterioration in the income statements of both Spanish and European institutions, due to the worsening of the general and Spanish economic situation in particular, which led to record losses for Spanish institutions in 2013.

- From 2014 onwards, the situation, from the point of view of results, improves, although in European banks profits improve year by year until 2020; however, the results of Spanish institutions remain stable between 2014 and 2019, a period that coincides with the process of restructuring, organization, and concentration of Spanish institutions.

- In 2020, Spanish banks will show negative results, significantly reducing the results of European institutions.

- By 2021, there was a V-shaped recovery in both cases, returning to the pre-COVID-19 crisis levels of 2019.

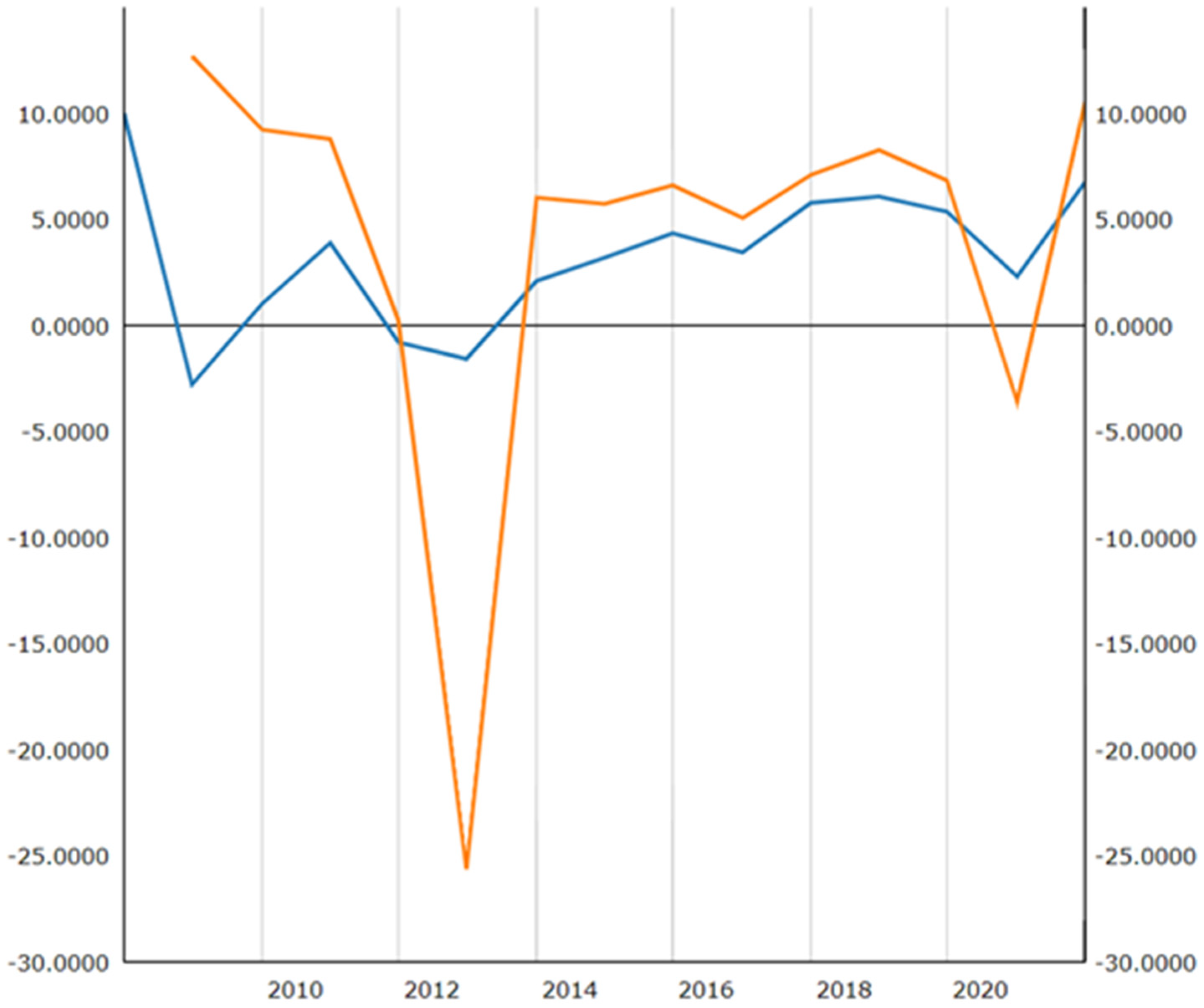

- From 2007 to 2011, profitability experienced a progressive reduction from positions above 12% in 2009 to zero profitability in 2011, reaching an all-time low with a negative profitability of 25.61% in 2012.

- A recovery began in 2013, maintaining a stable performance and with higher yields than the euro area, until 2019.

- Due to the pandemic in 2020, losses in Spanish institutions amount to −3.46% (compared to an EU-wide ROE of 2.30%).

- In 2021, the most pronounced recovery in Spanish institutions was in 2021, with a return of over 10%, which had not been reached in the previous 13 years.

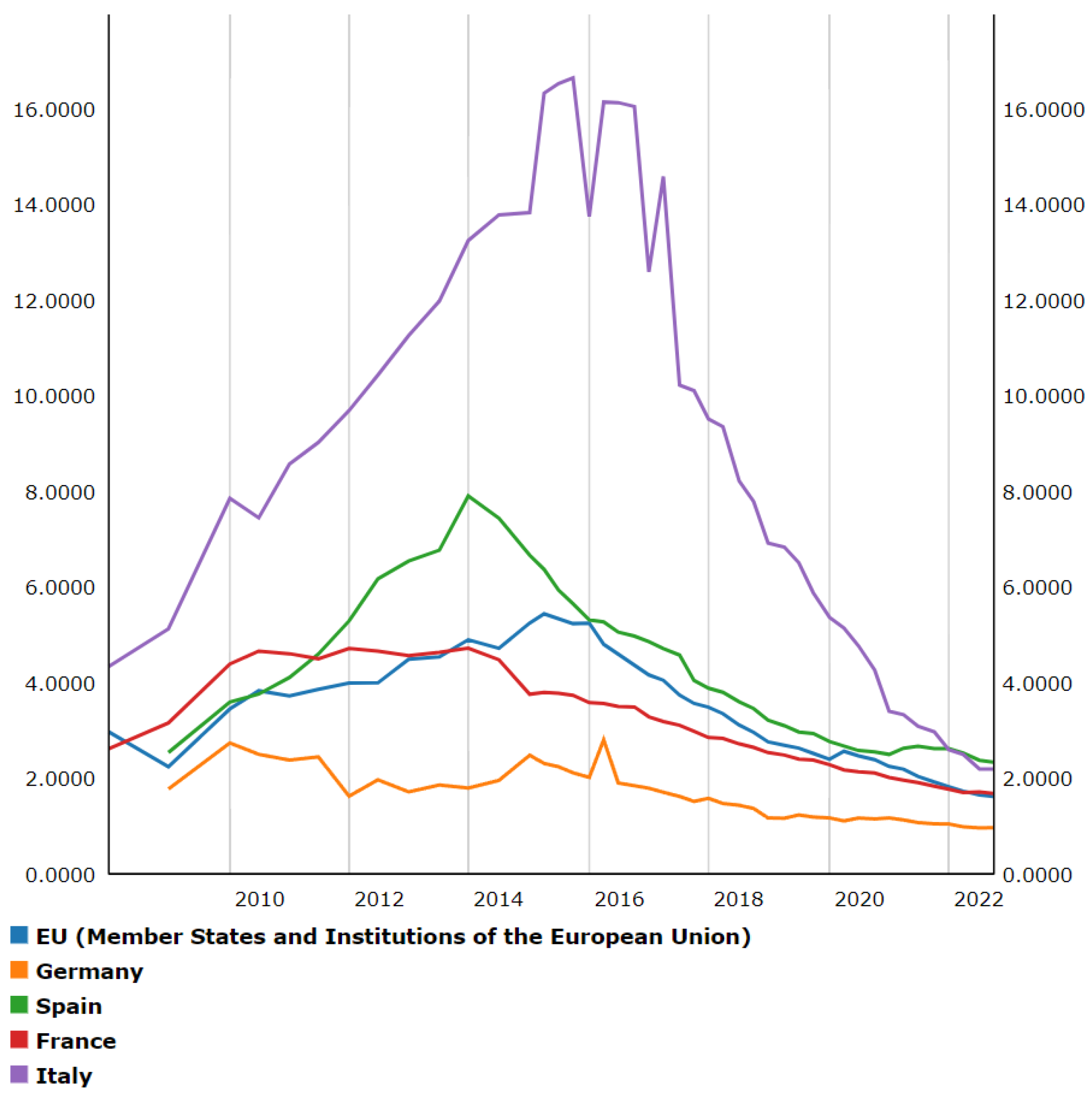

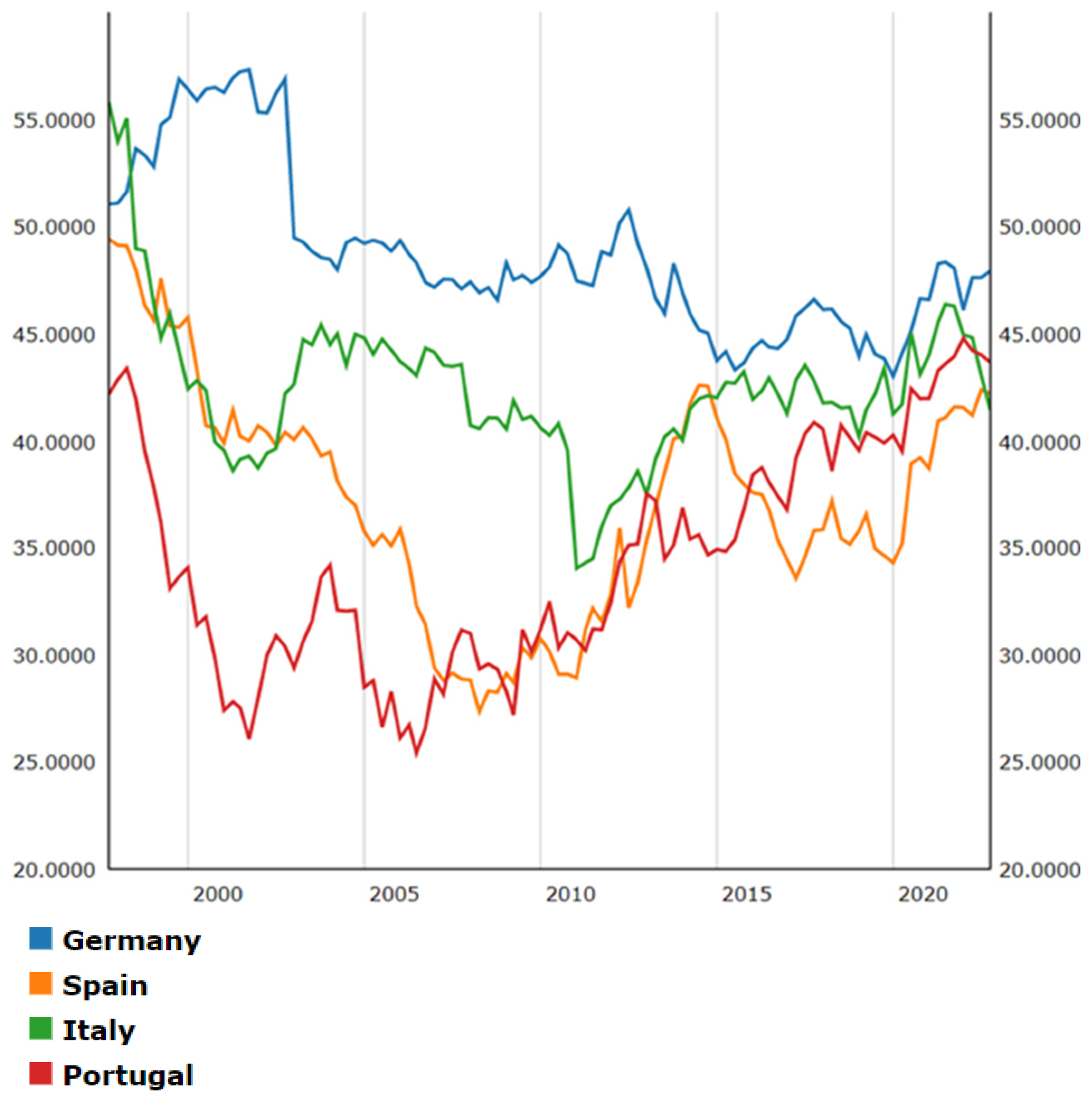

- Since the end of 2007, there has been a progressive deterioration of credit portfolios in almost all euro area banks and at the level of the four major economies, with the exception of Germany.

- The peak in defaults is quite uneven, arriving in France in mid-2010, in Spain in the last quarter of 2013, in the EU area as a whole in mid-2014, and being delayed in Italy until the end of 2015.

- Since 2016, there has been a notable improvement in asset quality, as a result of the ongoing restructuring of banks’ balance sheets, reducing non-performing loans through transfers and sales of non-performing loan portfolios, and thanks to the use of public–private management instruments, as has occurred in the case of Spain, with the transfer of non-performing portfolios to the SAREB.

- The current levels of NPLs are very similar in all these countries and globally, at around 2%.

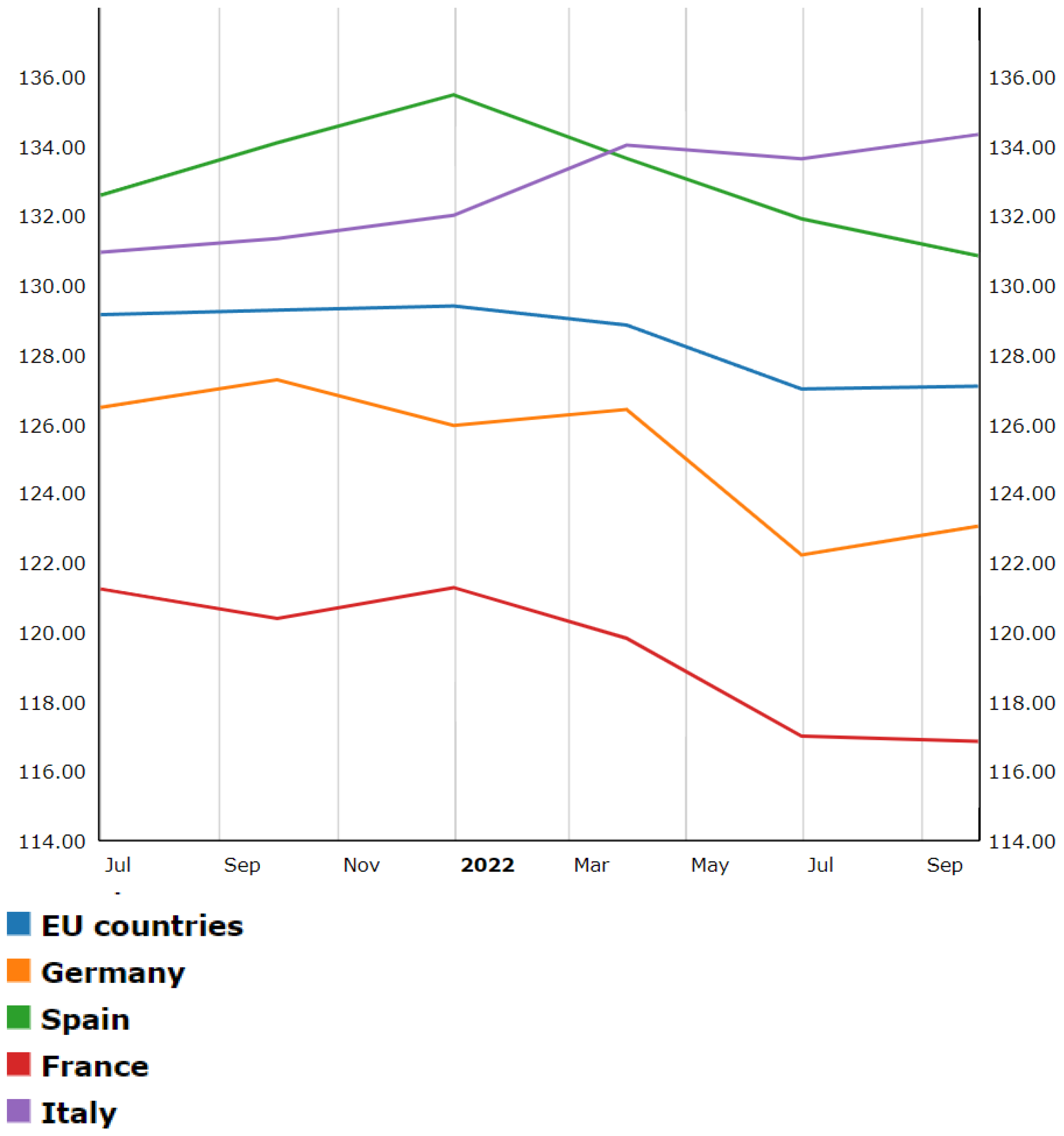

5.2. New Tools for Liquidity Analysis: Evolution of Key Ratios and Indicators

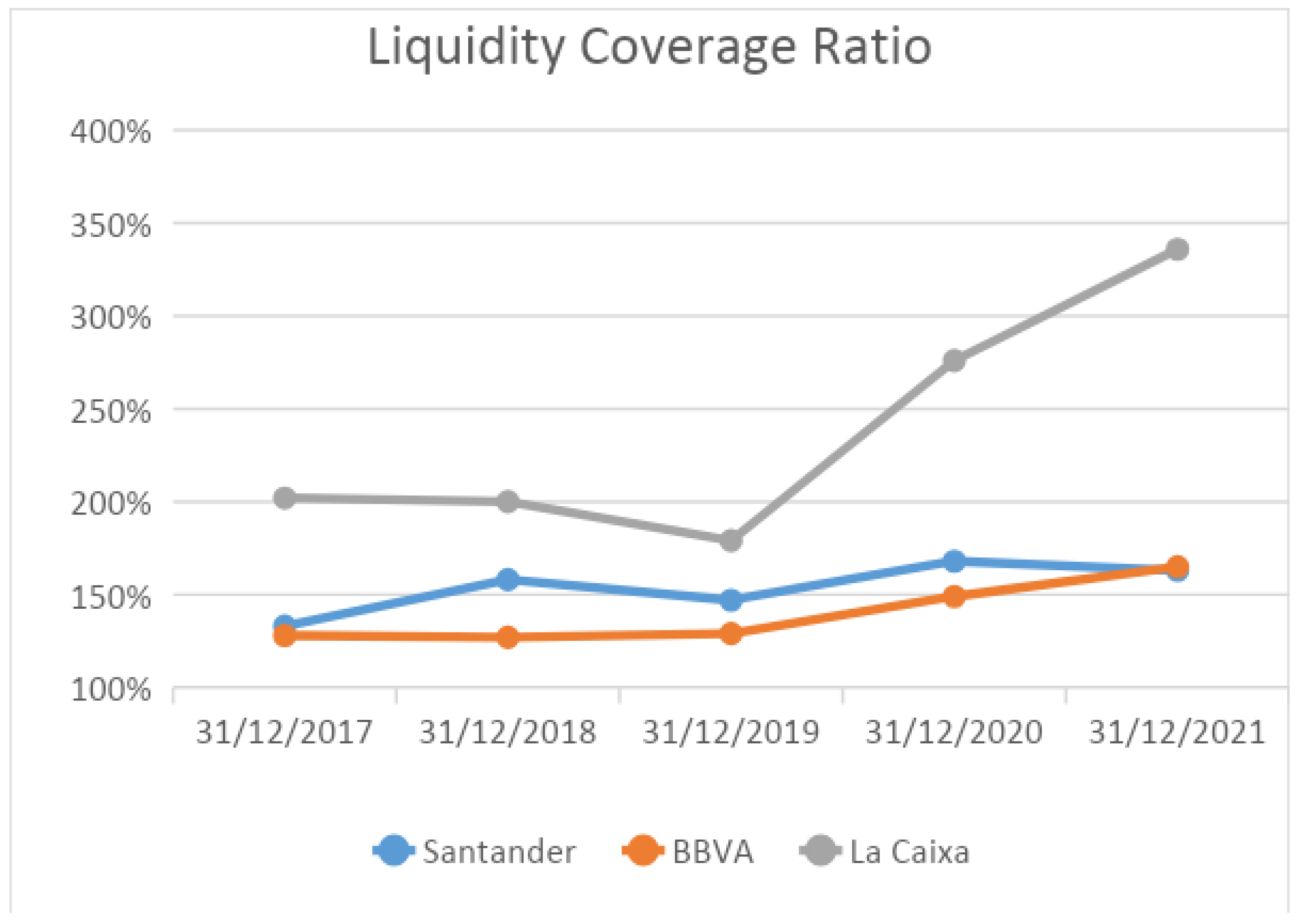

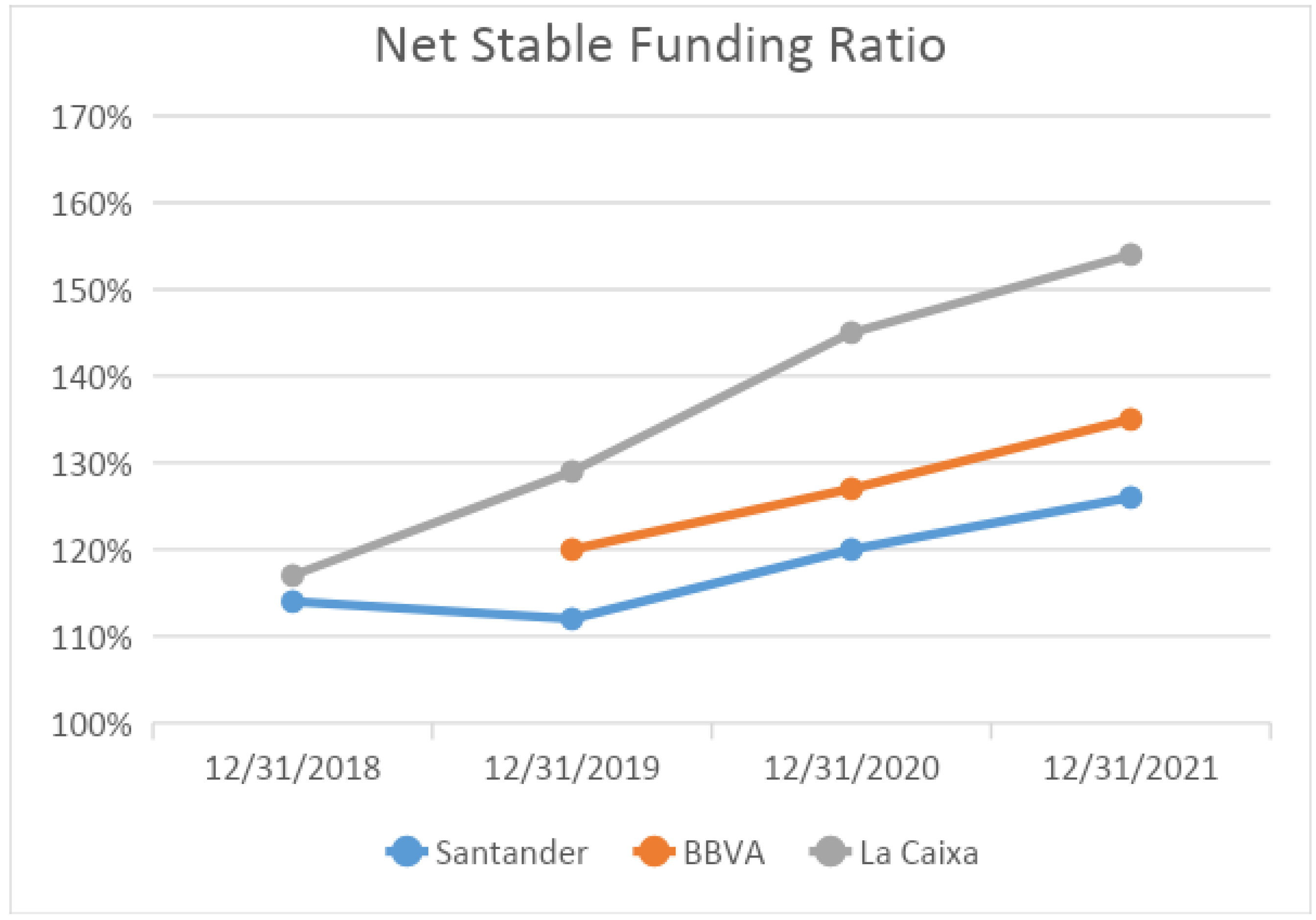

5.3. Special Reference to Liquidity Management at Spanish Credit Institutions

- Banco Santander: one of the world’s largest banks, with a presence in more than 40 countries and assets of approximately EUR 1.4 trillion at the end of 2021. Santander has experienced steady growth in recent years and has strengthened its position through acquisitions and diversification of its financial products and services. In addition, its international expansion and focus on digital banking have enabled it to broaden its customer base (Banco Santander 2018, 2019, 2020, 2021).

- BBVA: the second largest bank in Spain in terms of assets, with a volume of approximately EUR 676 billion at the end of 2021. BBVA also has a strong international presence, with operations in more than 30 countries, and has focused on innovation and digital transformation to improve the customer experience and optimize its operational processes (BBVA 2017, 2018, 2019, 2021, 2022).

- CaixaBank: Spain’s third largest bank in terms of assets, with approximately EUR 415 billion at the end of 2021. CaixaBank merged with Bankia in 2021 to strengthen its market position and improve its ability to compete with other large Spanish and international banks. CaixaBank has also been a leader in the implementation of financial technology and digital solutions, and has expanded its presence in other European markets. (CaixaBank 2018, 2019, 2021)

6. Conclusions, Limitations, Implications, and Future Directions

6.1. Conclusions

6.2. Limitations

- Limitations on the collection of individual financial data. Most supervisory information on credit institutions is subject to regulations and rules that protect the confidentiality of the information, for reasons of sensitivity of the information provided to the market, so that the information is presented in aggregate form, either by country or distinguishing by size of the institutions.

- Information not available or incomplete. In addition to financial information, there is certain information that credit institutions are not obliged to make public, such as commercial strategies, risk models, and internal policies, etc., which has limited in-depth analysis of the institution, mainly in terms of management policies, despite the fact that institutions are becoming increasingly transparent.

- Difficulties in comparing the available information. The lack of granularity in the information available for analysis makes it difficult to establish comparisons between them and therefore to draw general conclusions.

6.3. Guidances for Supervisors and Regulators

- Proactive regulation: Move from a reactive stance to a more proactive approach to regulation. This involves anticipating financial instability and adjusting liquidity requirements in advance, thereby fostering a more resilient banking environment.

- Innovative risk management: Integrate advanced analytical tools and technologies, such as AI and machine learning, into liquidity risk management practices. These innovations can enhance the sector’s ability to predict and manage potential risks more effectively.

- Adapt to fintech and cryptocurrencies: Adapt regulatory frameworks to keep pace with emerging technologies such as fintech and cryptocurrencies. These innovations are rapidly changing the financial landscape and require an adaptive regulatory approach.

- Embrace AI and customer centricity: Recognize the growing importance of artificial intelligence in analyzing financial trends and customer behavior. In addition, adapt to the changing preferences and expectations of new banking customers, which will require a significant cultural shift in the traditional banking sector. This transformation should focus on customer centricity, aligning banking services with the evolving needs and preferences of customers in the digital age.

6.4. Implications and Future Directions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Alonso García, Mercedes. 2019. Credit risk management in Spanish financial institutions. Recent developments and perspectives. Creando redes doctorales: Vol. VII: Investiga y comunica [Recurso electrónico]/coord. por Arturo Chica Pérez, Julieta Mérida García. pp. 407–410. Available online: https://dialnet.unirioja.es/servlet/articulo?codigo=7714654 (accessed on 5 February 2023).

- Ananou, Foly, Dimitris K. Chronopoulos, Amine Tarazi, and John O. S. Wilson. 2021. Liquidity Regulation and Bank Lending. Journal of Corporate Finance 69: 101997. Available online: https://ssrn.com/abstract=3560215 (accessed on 5 February 2023).

- Ávila Ramírez, Carlos Felipe. 2022. Short-Term Liquidity Risk Management in a Private Financial Institution Using an Optimal Model under Basel III Requirements and Financial Impact. Master’s thesis, Universidad Andina Simón Bolívar, Sede Ecuador, Quito, Ecuador. Available online: https://repositorio.uasb.edu.ec/bitstream/10644/8817/1/T3857-MGFARF-Avila-Gestion.pdf (accessed on 5 February 2023).

- Banco de España. 2017. Report on the Financial and Banking Crisis in Spain 2008–2014. Available online: https://www.bde.es/f/webbde/GAP/Secciones/SalaPrensa/InformacionInteres/ReestructuracionSectorFinanciero/Arc/Fic/InformeCrisis_Completo_web.pdf (accessed on 5 February 2023).

- Banco de España. n.d. Supervision—Supervisory Regulations and Criteria Applicable to Supervised Entities—Periodic Information to Be Submitted. Available online: https://www.bde.es/bde/es/areas/supervision/normativa/informacion/Informacion_per_f947c51aafcd821.html (accessed on 5 February 2023).

- Banco Santander. 2018. Financial Statements, Strategic Plans and Other Published Information. Available online: https://www.santander.com/content/dam/santander-com/es/documentos/informe-financiero-anual/2018/IFA-2018-Informe%20Financiero%20Anual%20consolidado-es.pdf (accessed on 5 February 2023).

- Banco Santander. 2019. Financial Statements, Strategic Plans and Other Published Information. Available online: https://www.santander.com/content/dam/santander-com/es/documentos/informe-anual/2019/ia-2019-informe-anual-es.pdf (accessed on 5 February 2023).

- Banco Santander. 2020. Financial Statements, Strategic Plans and Other Published Information. Available online: https://www.santandersostenibilidad.es/recursos/doc/portal/2021/04/22/informe-anual-2020.pdf (accessed on 5 February 2023).

- Banco Santander. 2021. Financial Statements, Strategic Plans and Other Published Information. Available online: https://www.santander.com/content/dam/santander-com/es/documentos/informe-financiero-anual/2021/ifa-2021-informe-financiero-anual-consolidado-es.pdf (accessed on 5 February 2023).

- Bank of England. 2023. Financial Stability Report. London: Bank of England. [Google Scholar]

- Basel Committee on Banking Supervision. 2008a. Management and Supervisory Challenges. February. Available online: https://www.bis.org/publ/bcbs136.pdf (accessed on 5 February 2023).

- Basel Committee on Banking Supervision. 2008b. Principles for Sound Liquidity Risk Management and Supervision. September. Available online: https://www.bis.org/publ/bcbs144.pdf (accessed on 5 February 2023).

- Basel Committee on Banking Supervision. 2013. Liquidity Coverage Ratio and Liquidity Risk Monitoring Tools. December. Available online: https://www.bis.org/publ/bcbs238_es.pdf (accessed on 5 February 2023).

- BBVA. 2017. Financial Statements, Strategic Plans and Other Published Information. Available online: https://accionistaseinversores.bbva.com/microsites/bbvain2017/downloads/bbva-en-2017.pdf (accessed on 5 February 2023).

- BBVA. 2018. Financial Statements, Strategic Plans and Other Published Information. Available online: https://accionistaseinversores.bbva.com/wp-content/uploads/2019/02/5.Cuentas_Anuales_Consolidadas_e_IG_Grupo_BBVA_2018.pdf (accessed on 5 February 2023).

- BBVA. 2019. Financial Statements, Strategic Plans and Other Published Information. Available online: https://accionistaseinversores.bbva.com/wp-content/uploads/2020/03/InformeAnual2019GrupoBBVA_esp-1.pdf (accessed on 5 February 2023).

- BBVA. 2020. Financial Statements, Strategic Plans and Other Published Information. Available online: https://accionistaseinversores.bbva.com/wp-content/uploads/2021/02/Informe-Anual-2020_ESP1.pdf (accessed on 5 February 2023).

- BBVA. 2021. Financial Statements, Strategic Plans and Other Published Information. Available online: https://accionistaseinversores.bbva.com/wp-content/uploads/2022/03/Informe-Anual-2021.pdf (accessed on 5 February 2023).

- BBVA. 2022. What Is Financial Liquidity and Why Is It So Important. BBVA NEWS. October 18. Available online: https://www.bbva.com/es/salud-financiera/que-es-la-liquidez-financiera-y-por-que-es-tan-importante/ (accessed on 5 February 2023).

- Behn, Markus, Claudio Daminato, and Carmelo Salleo. 2019. A Dynamic Model of Bank Behaviour under Multiple Regulatory Constraints. Working Paper Series, No 2233; Frankfurt am Main: ECB, January. [Google Scholar]

- Blinder, Alan S. 2023. Landings, Soft and Hard: The Federal Reserve, 1965–2022. Journal of Economic Perspectives 37: 101–20. [Google Scholar] [CrossRef]

- CaixaBank. 2018. Financial Statements, Strategic Plans and Other Published Information. Available online: https://www.caixabank.com/deployedfiles/caixabank/Estaticos/PDFs/Informacion_accionistas_inversores/Informacion_Economica_Financiera/MEM_GRUPCAIXABANK_30062017-WEB-CAS.pdf (accessed on 5 February 2023).

- CaixaBank. 2019. Financial Statements, Strategic Plans and Other Published Information. Available online: https://www.caixabank.com/deployedfiles/caixabank/Estaticos/PDFs/Informacion_accionistas_inversores/Gobierno_corporativo/Junta_General_Accionistas/2020/Cuentas_Anuales_2019_consolidadas_CAST.pdf (accessed on 5 February 2023).

- CaixaBank. 2020. Financial Statements, Strategic Plans and Other Published Information. Available online: https://www.caixabank.com/deployedfiles/caixabank_com/Estaticos/PDFs/Accionistasinversores/Informacion_General/Cuentas_Anuales_consolidadas_CBK_2020_ES.pdf (accessed on 5 February 2023).

- CaixaBank. 2021. Financial Statements, Strategic Plans and Other Published Information. Available online: https://www.caixabank.com/StaticFiles/pdfs/220225_OIR_CCAA_CaixaBank_2021_es.pdf (accessed on 5 February 2023).

- Calomiris, Charles W., Florian Heider, and Marie Hoerova. 2015. A Theory of Bank Liquidity Requirements (April 15, 2015). Columbia Business School Research Paper No. 14–39. Available online: https://ssrn.com/abstract=2477101 (accessed on 5 February 2023).

- Calvo Bernardino, Antonio, and Irene Martín de Vidales Carrasco. 2014. El rescate bancario: Importancia y efectos sobre algunos sistemas financieros afectados. Revista de Economía Mundial 3: 125–50. Available online: https://repositorioinstitucional.ceu.es/bitstream/10637/6912/1/Rescate_Calvo&MartindeVidales_RevEconMund_2014.pdf (accessed on 5 February 2023). [CrossRef]

- Calvo Bernardino, Antonio, José Alberto Parejo, Luis Rodríguez, Álvaro Cuervo, and A. Alcalde. 2018. Manual of the Spanish Financial System. Available online: https://www.planetadelibros.com/libros_contenido_extra/29/28771_Manual_Sistema_Financiero.pdf (accessed on 5 February 2023).

- Cecchetti, Stephen, and Anil Kashyap. 2018. Inspecting Basel III. Working Paper. Waltham: Brandeis International Business School and Chicago Booth School of Business. [Google Scholar]

- Chami, Ralph, Thomas F. Cosimano, Jun Ma, and Celine Rochon. 2017. What’s Different about Bank Holding Companies? IMF Working Papers, No 17/26, February. Washington, DC: International Monetary Fund. [Google Scholar]

- Cossío, Francisco José, and Enrique Martín. 2001. Market orientation and corporate performance: The case of Spanish banking. Cuadernos de Gestión 1: 33–67. [Google Scholar]

- Directive 2013/36/EU of the European Parliament and of the Council of 26 June 2013 Relating to the Taking up and Pursuit of the Business of Credit Institutions and the Prudential Supervision of Credit Institutions and Investment Firms, Amending Directive 2002/87/EC and Repealing Directives 2006/48/EC and 2006/49/EC. 2013. Available online: https://eur-lex.europa.eu/LexUriServ/LexUriServ.do?uri=OJ:L:2013:176:0338:0436:ES:PDF (accessed on 5 February 2023).

- Domingo Ortuño, Beatriz. 2010. Financial Stability of the Bank of Spain: The New Basel Proposals on Liquidity Risk: From a Qualitative to a Quantitative Approach. Available online: https://repositorio.bde.es/bitstream/123456789/11507/1/ref0418.pdf (accessed on 5 February 2023).

- European Central Bank. 2022a. Banking Union. European Central Bank-Banking Supervision. October 14. Available online: https://www.bankingsupervision.europa.eu/about/bankingunion/html/index.es.html (accessed on 5 February 2023).

- European Central Bank. 2022b. Asset Quality. European Central Bank-Banking Supervision. July 21. Available online: https://www.bankingsupervision.europa.eu/banking/priorities/assetquality/html/index.es.html (accessed on 5 February 2023).

- Federal Reserve. 2023. Recent Developments in Hedge Funds’ Treasury Futures and Repo Positions: Is the Basis Trade ‘Back’? FEDS Notes. Washington, DC: Board of Governors of the Federal Reserve System, August 30. [Google Scholar]

- Fernández, Jesús. 2015. Valuation and Comparative Analysis of Two CoCos Issues: BBVA and Banco Santander. Available online: https://repositorio.comillas.edu/xmlui/bitstream/handle/11531/6333/TFM000184.pdf?sequence=1&isAllowed=y (accessed on 5 February 2023).

- Fernández de Guevara, Juan, Joaquín Maudos, and Francisco Pérez. 2000. Income Structure and Profitability of Firms in the Spanish Banking Sector. Valencia: Instituto Valenciano de Investigaciones Económicas. [Google Scholar]

- Goel, Tirupam, Ulf Lewrick, and Nikola Tarashev. 2017. Bank Capital Allocation under Multiple Constraints. BIS Working Papers, No 666. Basel: Bank for International Settlements. [Google Scholar]

- Guzmán, José Luis. 2019. Analysis of the Financial Risk of the “Kutxabank” Entity in the Period 2014–2018. Available online: https://tauja.ujaen.es/bitstream/10953.1/10768/1/TFG_GUZMN_MANSILLA__BANCA_Y_MERCADOS_FINANCIEROS.pdf (accessed on 5 February 2023).

- Hernández, Ignacio. 2014. Measurement and Supervision of Liquidity Risk in Banks: Basel III Regulatory Framework. Available online: https://repositorio.comillas.edu/xmlui/bitstream/handle/11531/335/TFG000155.pdf?sequence=1&isAllowed=y (accessed on 5 February 2023).

- Hoerova, Marie, Caterina Mendicino, Kalin Nikolov, Glenn Schepens, and Skander Van den Heuvel. 2018. Benefits and Costs of Liquidity Regulation. Working Paper Series, No 2169; Frankfurt am Main: ECB, July. [Google Scholar]

- Ibáñez Sandoval, Jesús P., and Beatriz Domingo Ortuño. n.d. Banco de España, Estabilidad Financiera: La transposición de Basilea III a la legislación europea. Available online: https://repositorio.bde.es/bitstream/123456789/11454/1/ref2013253.pdf (accessed on 5 February 2023).

- Mankart, Jochen, Alexander Michaelides, and Spyros Pagratis. 2018. Bank capital buffers in a dynamic model. Financial Management 49: 473–502. [Google Scholar] [CrossRef]

- Millán, José. Ramón. 2017. Analysis of the Evolution of the Solvency and Profitability of Spanish Deposit Institutions. A State-of-the-Art Approach. Available online: https://analisissolvencia2017.hml (accessed on 5 February 2023).

- Moody’s Investors Service. 2023. Disproportionate LGFV Exposure a Credit Concern for Regional Financial Institutions. New York: Moody’s Investors Service. [Google Scholar]

- Orsikowsky, Bernardo. 2002. Liquidity Risk Monitoring. Financial Stability 2: 139–156. Available online: https://www.bde.es/f/webbde/GAP/Secciones/Publicaciones/InformesBoletinesRevistas/RevistaEstabilidadFinanciera/02/Fic/07_Supervision_liquidez.pdf (accessed on 5 February 2023).

- Pancorbo, Elisabeth. 2017. Analysis of the Financial Risk of the Cajamar Entity through the CAMEL Method (2011–2015). Available online: https://tauja.ujaen.es/bitstream/10953.1/6703/1/TFG_ANLISIS_DEL_RIESGO_FINANCIERO_DE_LA_ENTIDAD_CAJAMAR_A_TRAVS_DEL_MTODO_CAMEL_20112015__ELISABETH_PANCORBO_RICO.pdf (accessed on 5 February 2023).

- Pérez, Daniel. 2006. Impact of accounting circular 4/2004 on the balance sheet and profit and loss account of Spanish deposit institutions. Financial Stability Notes/Banco de España 4. Available online: https://repositorio.bde.es/handle/123456789/11122 (accessed on 5 February 2023).

- Rodríguez de Codes, Elena. 2010. The new Basel III capital measures. Financial Stability 19: 9–19. [Google Scholar]

- Standard & Poor’s Global Ratings. 2023. Satisfying Policyholders Is Becoming Costly for French Life Insurers. New York: Standard & Poor’s. [Google Scholar]

- Sutil, Rafael. 2023. Financial Risk Analysis of (2017–2021). CAMEL Method. Available online: https://tauja.ujaen.es/bitstream/10953.1/19391/1/TFG%20ADE-RAFAEL%20SUTIL%20CONDE%20-%20Rafael%20Sutil%20Conde.pdf (accessed on 5 February 2023).

- Valderrama, Laura, Patrik Gorse, Marina Marinkov, and Petia B. Topalova. 2023. European Housing Markets at a Turning Point: Risks, Household and Bank Vulnerabilities, and Policy Options. IMF Working Paper 23/076. Washington, DC: International Monetary Fund. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Mariscal-Cáceres, J.; Cristófol-Rodríguez, C.; Cerdá-Suárez, L.M. Regulatory Implications of the Supervision and Management of Liquidity Risk: An Analysis of Recent Developments in Spanish Financial Institutions. J. Risk Financial Manag. 2024, 17, 46. https://doi.org/10.3390/jrfm17020046

Mariscal-Cáceres J, Cristófol-Rodríguez C, Cerdá-Suárez LM. Regulatory Implications of the Supervision and Management of Liquidity Risk: An Analysis of Recent Developments in Spanish Financial Institutions. Journal of Risk and Financial Management. 2024; 17(2):46. https://doi.org/10.3390/jrfm17020046

Chicago/Turabian StyleMariscal-Cáceres, Juan, Carmen Cristófol-Rodríguez, and Luis Manuel Cerdá-Suárez. 2024. "Regulatory Implications of the Supervision and Management of Liquidity Risk: An Analysis of Recent Developments in Spanish Financial Institutions" Journal of Risk and Financial Management 17, no. 2: 46. https://doi.org/10.3390/jrfm17020046