The Future of Insurance Intermediation in the Age of the Digital Platform Economy

1

Institute for Risk & Insurance, ZHAW School of Management and Law, Gertrudstrasse 8, 8400 Winterthur, Switzerland

2

Department of Actuarial Science, Faculty of Business and Economics (HEC Lausanne), University of Lausanne, Chamberonne—Extranef, 1015 Lausanne, Switzerland

3

Swiss Finance Institute, University of Lausanne, 1015 Lausanne, Switzerland

*

Author to whom correspondence should be addressed.

J. Risk Financial Manag. 2023, 16(9), 381; https://doi.org/10.3390/jrfm16090381

Submission received: 12 July 2023

/

Revised: 21 August 2023

/

Accepted: 22 August 2023

/

Published: 25 August 2023

(This article belongs to the Special Issue Financial Technologies (Fintech) in Finance and Economics)

Abstract

:Today most insurance is sold by over a million brokers and independent agents acting as intermediaries between the insurance companies and their customers. Digitalization and changing customer behavior have fostered the development of insurtech businesses, and, more recently, multi-sided platforms are emerging as new market forms for insurance intermediation. This paper aims to provide a better understanding of how the emergence of the platform economy, with a market dominated by multi-sided platforms, will potentially impact insurance intermediation in the future. Using inductive content analysis on the results of a systematic literature review of the body of research on insurance intermediation, we identify the key functional roles fulfilled by insurance intermediaries. Applying these roles to a literature review on multi-sided platforms allows us to compare how different market forms and players embody the functional roles of intermediaries. Our findings suggest that multi-sided platforms are better able to perform certain roles in terms of agility, scale and scope, and we discuss the future role of platforms in insurance intermediation.

1. Introduction

Insurance companies function as financial intermediaries, yet insurance is distributed through a variety of marketing channels (Cummins and Doherty 2006). Most insurance is sold by an additional layer of intermediaries, namely by brokers and independent and tied agents. According to IBISWorld (2021), over 1.2 million independent insurance brokers and agents operate worldwide. The existence of financial intermediaries has commonly been attributed to market imperfections (Benston and Smith 1976; Diamond 1984; Gurley and Shaw 1960), while the co-existence of multiple distribution systems, i.e., direct and intermediated, has been explained by the product quality hypothesis (Berger et al. 1997; Eckardt and Räthke-Döppner 2010; Liu et al. 2017) and linked to customer relationships and access channels (Mau et al. 2018; Staudt and Wagner 2018). In more recent research, a functional perspective has been taken that places greater importance on value-adding advisory services, such as risk management and product innovation (Allen and Santomero 1997; Maas 2010; Merton and Bodie 1995; Scholtens and van Wensveen 2000). Against the background of digitization and changing customer behavior, recent articles point out the emergence of new intermediaries, such as insurtech companies (Neale et al. 2020; Stoeckli et al. 2018; Zeier Röschmann et al. 2022). At the same time, the concept of intermediation is very prominent in the literature discussing the development of the platform economy. In the following, we refer to multi-sided platforms (MSPs) in the context of the digital platform economy (DPE), meaning digitally enabled platforms bringing together two or more independent sides of a market. MSPs have become the dominant form of the DPE and are characterized by most authors as intermediaries (Acs et al. 2021; Pousttchi and Gleiss 2019). Given new intermediaries arising in the insurance market and MSPs emerging as intermediaries in the growing platform economy, this paper explores to what extent MSPs can fulfill the roles of insurance intermediation.

While there is a rich body of literature on both insurance intermediation (see, for example, Allen and Santomero 1997; Cummins and Doherty 2006; Eckardt and Räthke-Döppner 2010; Ma et al. 2014a; Scholtens and van Wensveen 2000) and even more on MSPs (Acs et al. 2021; Jia et al. 2019; Sanchez-Cartas and León 2021; Trabucchi and Buganza 2021), there is surprisingly little research available that combines both fields. Pousttchi and Gleiss (2019) provide a well-founded framework on how MSPs impact the insurance industry, Warg et al. (2019) focus on the organizational aspects of insurers evolving towards platform organizations, while Catlin et al. (2018) suggest that insurers must join platform-based ecosystems to stay relevant. However, to the best of our knowledge, no research has investigated the potential dynamics that digital MSPs could unleash in insurance intermediation. We aim to close this gap.

The purpose of this paper is to support research and practice in understanding how the emergence of MSPs potentially impacts insurance intermediation. In doing so, we shed light on the question of how insurance intermediation will be delivered in the future. In particular, we aim to compare how different market forms and players embody the key functional roles of intermediaries.

Our approach is based on a systematic literature review in both the research body on insurance intermediation as well as research focusing on multi-sided platforms. We apply an inductive content analysis to capture the key functional roles fulfilled by insurance intermediaries and identify eight roles. These roles are then applied to the corpus of publications discussing the roles of MSPs in identifying commonalities and differences. The comparison shows that MSPs could perfectly act as insurance intermediaries from a pure functional view of the roles. All the roles described for insurance intermediaries are also present in the literature on MSPs. At the same time, the market dynamic is almost the opposite, with a very fragmented insurance intermediation market opposing the oligopolistic market structure of MSPs. This is because of their “winner-takes-all-or-most” dynamic inherent in the fact that the value of an MSP grows with every participant joining the platform. Given the economic weight of the insurance industry and the broad-based triumph of MSPs over the last decade, further research on understanding this discrepancy will be valuable and could have far-reaching consequences for the insurance industry.

The structure of the paper is as follows: In Section 2, we review the current understanding of MSPs and their role as intermediaries in general. In the following paragraphs, we specifically focus on the insurance industry. In Section 3, we summarize the methodological approach for deriving the functional roles of insurance intermediaries to distill the matching MSP literature. These functional roles that insurance intermediaries fulfill are identified and described in Section 4, and in Section 5, we then provide a review of selected MSP literature through the lens of the functional roles of insurance intermediaries. In Section 6, we integrate the findings from the two separated fields, and in Section 7, we discuss hypotheses on the future of insurance intermediation and potential venues for subsequent research.

2. Review of the Intermediary Role of MSPs

A close connection between intermediation and MSPs is already visible in research in the early years of the 21st century, with references to “free information goods,” “information brokers”, and “intermediation service providers” (Caillaud and Jullien 2003; Parker and Van Alstyne 2000) to describe new phenomena in the information economy where certain goods are given away for free to increase profitability. Reference is also often made to earlier work by Katz and Shapiro (1985) on network externalities that explain some unusual competitive and pricing behavior. Gawer and Cusumano (2002) refer to “platforms” as drivers of innovation through modularity. A common and stable core is surrounded by complementing flexible parts, thereby fostering fast-paced innovation (Baldwin and Woodard 2009). The classical example is Apple’s iPhone operating system as a stable core with millions of smartphone applications as rapidly evolving supplements. In the much-acclaimed work of Rochet and Tirole (2003), the term “platform” is first used in connection with two- or multi-sided markets, eventually resulting in the phrase “multi-sided platforms”. Hagiu (2009a) defines MSPs with functionalities that are at the core of any intermediation when he describes MSPs as providing “a support that facilitates interactions (or transactions) among the two or more constituents (sides) that it serves.” Furthermore, Hagiu (2009a) states that the features or functionalities of MSPs have two fundamental effects, “reducing search costs, incurred by the MSP’s multiple constituents before transacting, and reducing shared costs, incurred during the transactions themselves”. Hagiu (2009a) continues to observe that two- or multi-sided markets have existed for centuries, for instance, the village markets bringing together sellers and buyers of local goods and services. Park et al. (2021) study historical evidence from the U.S. newspaper industry from 1945 to 1963 to find that the reactions to the entry of TV stations already revealed a sophisticated understanding of the multi-sided nature of their businesses. Similarly, research on non-digital markets matching two groups of players, e.g., buyers and sellers, readers and advertisers, or workers and companies, goes back a long time (see Poniatowski et al. 2021). “However, their prominence has soared […] mostly because of information technology, which has tremendously increased the opportunities for building larger, more valuable and powerful platforms” (Hagiu 2009a). Bakos and Katsamakas (2008) summarize the essence of the development by saying that “an increasing number of internet intermediaries provide platforms that are two-sided networks.”

Since the 2010s, the term “platform-based ecosystem” has become prominent (Tiwana et al. 2010). In a platform-based ecosystem, the roles of the platform providers and supplementors of services or goods to the multiple sides of the market and linked to the platform are further differentiated (Gawer 2014). In the following, we refer to MSPs in the context of the DPE, meaning digitally enabled platforms bringing together two or more independent sides of a market, irrespective of whether they are part of broader ecosystems.

Many of the most valuable companies act as MSPs (Acs et al. 2021; Drewel et al. 2021). According to Parker et al. (2016), the disruptive potential and their success stem from two major economic forces, namely network effects and marginal costs. Network effects are indirect when the value of joining the platform is influenced by the number of participants on the other side (also called cross-side effects) and direct when it is influenced by the number of participants on the same side (Eisenmann et al. 2006). Examples of indirect network effects are credit cards and video consoles, and examples of direct ones are social media users (where for advertisers on social media platforms, the network effects are clearly indirect). Network effects can also be adverse, as it is the case with advertisement-driven results on search engine platforms (de Reuver et al. 2018). Similarly, a platform may become congested, or users may face growing search costs once a specific size has been reached, e.g., in a shopping mall (Schmalensee and Evans 2007). Both effects limit the optimal size of the platform. They also trigger the necessity to balance potentially conflicting interests of the multiple sides of markets, making management of an MSP a tricky undertaking as more sides are brought on (Hagiu 2014).

According to Evans (2003), the platform’s role as an intermediary is to internalize some of the externalities that the two or more sides cannot solve directly. Only then can we speak of MSPs. The ability to reap network effects has several far-reaching consequences. Hagiu (2009a) states that “the economic value—as well as the disruptions—created by industry convergence and driven by MSP are at least an order of magnitude larger than what conglomerates operating one-sided businesses across different industries can achieve. Indirect network effects generate powerful demand-side economies of scale and scope, which, combined with technology expand beyond industry boundaries. The nature of network effects provides a distinction between single- and multi-sided platforms. Indeed, in a single-sided platform only direct network effects exist. The occurrence of indirect network effects also leads to unusual pricing effects. Typically, the side gaining more from the presence of the other side is charged higher than the other, which may even be subsidized (Rysman 2009; Schmalensee and Evans 2007).

While network effects are inherent to all (even purely physical) multi-sided markets, the second driving force—marginal cost—has taken off with the development of digital platforms. If designed well, adding a participant to either side of a platform incurs almost no cost. An example is a comparison of Uber and Airbnb to the traditional (franchising) taxi and hotel industry, respectively. Adding capacity to the platform is infinitely less expensive for the former than for the latter (Drewel et al. 2021; Trabucchi and Buganza 2021). The combination of both economic forces creates the “winner-takes-all” dynamic forcing many MSPs to embrace aggressive “get-big-fast” strategies (Cennamo and Santalo 2013; Lee et al. 2006; Schmalensee and Evans 2007). However, Cennamo and Santalo (2013) suggest “that platform competition is shaped by important strategic trade-offs, and that a WTA [winner-takes-all] approach will not be universally successful.”

Schmalensee and Evans (2007) discuss antitrust cases triggered by the potential oligo- or even monopolistic nature of MSPs, stating that “many antitrust cases have […] touched on two-sided issues before economists began to address them formally.” The case “New York v. Marsh” (Spitzer 2004) is particularly insightful for the present research. The complaint focused on the practice of contingent commissions paid by insurers to insurance intermediaries if they placed enough business with them. Translated into the terminology of multi-sided markets, the platform owner (the insurance broker) charged one side of its business (the insurer) an additional access fee on top of the usage fee (the usual commission paid by the insurer as part of the premium charged to the insured). Interestingly, these commissions follow the same logic as pricing structures in MSPs (Hagiu 2014; Rochet and Tirole 2006; Rysman 2009) because insurers are multi-homing, i.e., use several intermediaries, while the insureds tend to “single-home”, i.e., focus on one intermediary. Rochet and Tirole (2003) observe that prices often tend to be higher on the side that is multi-homing as it competes for the single-homing side to join. This somewhat anti-intuitive effect has been confirmed by a study on “paradoxical price effects on insurance markets” (Banyár and Regős 2012). The 2018 U.S. Supreme Court case “Ohio v. American Express” investigating the nature of antitrust law in relation to two-sided markets has led to a surge in the literature on the regulation of MSPs (see, for example, OECD 2018; Wright and Yun 2019). The case for more forceful approaches to antitrust was further exacerbated by the reliance of many MSPs on big data collected about their users (Katz 2019), and many cases arose (see, also, for example, the recent Visa and Mastercard antitrust suit over Square payment fees, Bulusu 2021).

3. Methodology and Systematic Literature Review

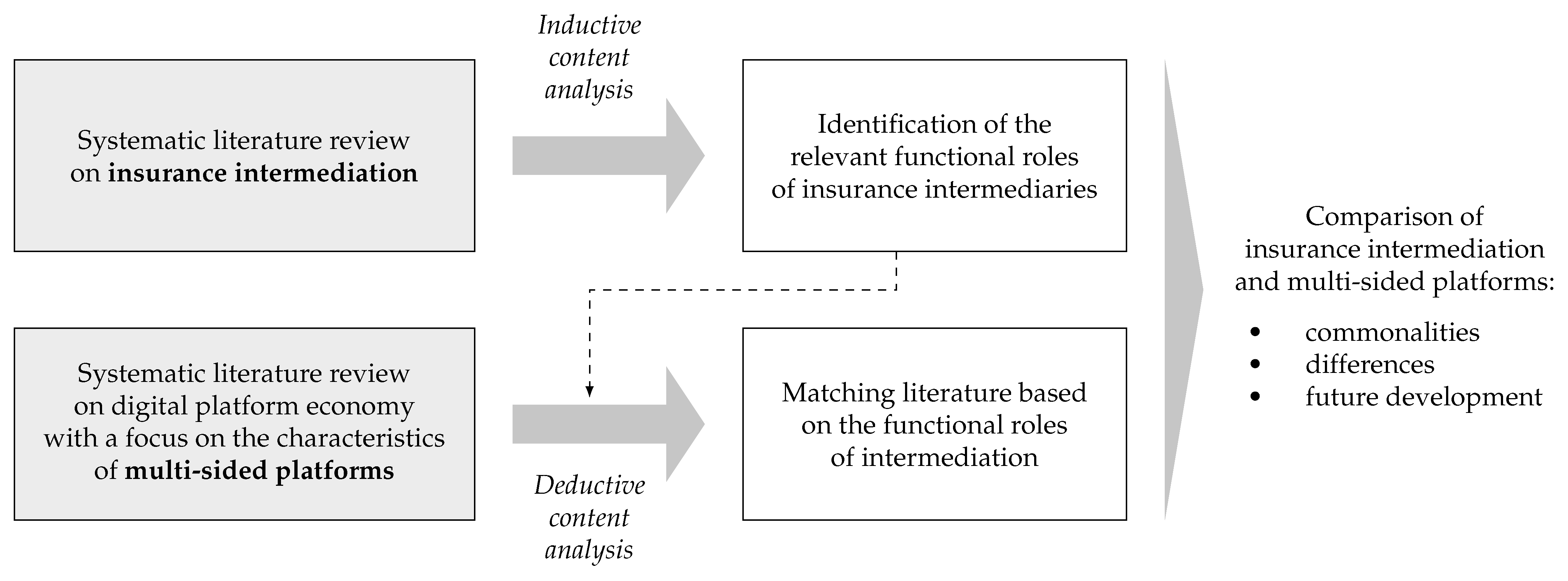

Focusing on the effect on the insurance industry, our methodological approach consists of two steps: First, we carry out a systematic literature review (SLR) on insurance intermediation to evaluate all the relevant functional roles of insurance intermediaries. To do this, we apply an inductive content analysis to the collected body of literature and identify eight functional roles (Section 4). Second, we collect records from the extant literature on MSPs through an SLR. Then, using a deductive content analysis approach, we apply the previously identified functional roles of insurance intermediaries to the corpus of MSP literature (Section 5). Finally, a comparison allows us to identify commonalities and differences and to provide a basis for discussing potential future developments (Section 6). Our methodology is outlined in Figure 1.

We describe the collection of records in both SLRs in Section 3.1, and provide a synthetic overview of the retained body of literature in Section 3.2.

3.1. Review Strategy and Data Collection

To ensure a high degree of reliability for the SLRs, we followed Tranfield et al. (2003) and applied the “preferred reporting items for systematic reviews and meta-analyses” (PRISMA) protocol as a reporting guide (Page et al. 2021). Furthermore, we used the reference manager software Mendeley 2.98.0 to ensure traceability of the entire review process.

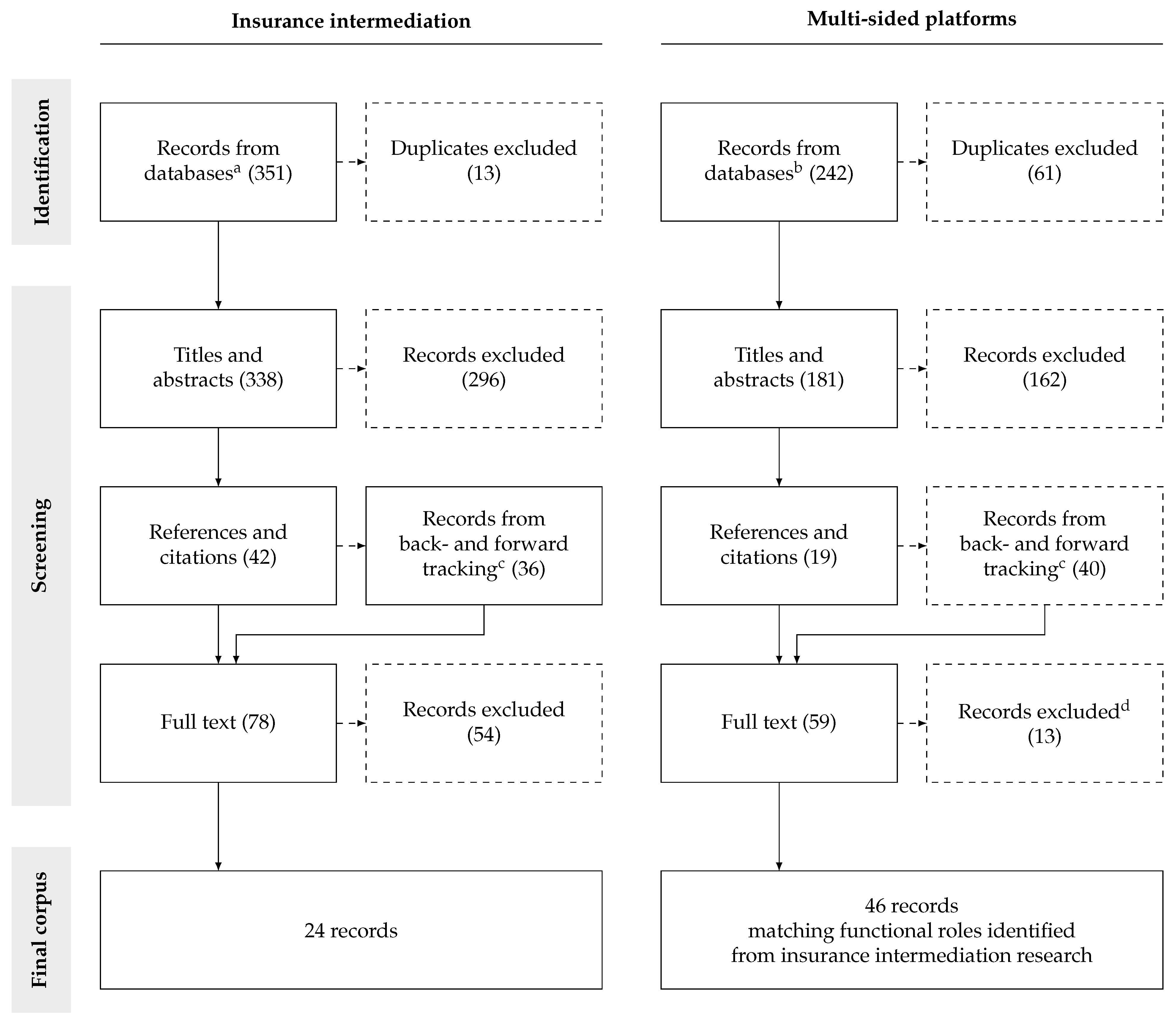

For the SLR on insurance intermediation, we have used the Web of Science and EbscoHost databases. We applied the keywords “insurance” and “intermediation.” The initial search stream AB(“insur*” AND (“intermedia*” OR “broker”)) resulted in 1344 articles from Web of Science and 716 from EbscoHost. We then applied eligibility criteria in terms of the period, i.e., years 2011–2021, as well as language (English only). Given the focus on functional roles, no geographical limitation was applied. Furthermore, we focused on publications from economics, business, and management in Web of Science, and economics, business and economics, and management in EbscoHost. The remaining 320 (Web of Science) and 355 (EbscoHost) records were summarily screened, revealing that more than half of the results discussed the widely researched field of bank runs during credit crunches or phases of market illiquidity. The reason why they appeared in our search stream is twofold. First, banks (and insurers) are often referred to as financial intermediaries, and second, in the context of bank runs, the term deposit insurance often appears, so both keywords were a hit. Consequently, we extended the search stream to exclude the keywords “credit”, “bank run”, and “liquidity”. The final query in the databases was conducted in October 2021 and resulted in 125 records from Web of Science and 179 from EbscoHost.

To ensure we did not miss relevant literature due to our eligibility criteria, we also searched the literature with Google Scholar without restrictions using the search stream “insur*” AND (“intermedia*” OR “broker”) NOT (“deposit insurance” OR “bank run” OR “liquidity” OR “credit” OR “intermediate”). Of the approximately 24,800 results, we included 47 records from the first five search pages, leading to an initial number of 351 records. Eliminating 13 duplicates between the different sources, 338 records formed the pool of literature for manual screening, following the inclusion criteria defined in our review protocol. The main reviewer read the abstracts of the publications and rated their relevance on a scale ranging from 0 (not relevant) to 2 (relevant). The records rated 1 (potentially relevant) were re-rated 0 or 2 by a co-reviewer. Disagreements that arose were discussed and resolved. Only the records that were finally rated 2 were retained: this led to the elimination of 296 records, leaving 42 for further study. By analyzing backward and forward citations, including all years, in those 42 publications using the search tool ResearchRabbit, we added 36 publications. This yielded a body of literature of 78 records from which we reviewed the full text. From these, only 24 publications included a discussion of roles performed by insurance intermediaries. An inductive content analysis of that final corpus resulted in the extraction of eight functional roles described below (see Section 3.2).

For the SLR on MSPs, we also used Web of Science and EbscoHost with the keywords “multi-sided” and “platform”. The initial search stream was AB(“multi sided” OR “multi-sided” OR “multisided”) AND “platform”), resulting in 204 hits from Web of Science and 2307 from EbscoHost. We applied the same eligibility criteria for the period, language, and categories as for the SLR on insurance intermediation (see above). This left us with 124 (Web of Science) and 50 records (EbscoHost). In addition, using the same query without time, language, and category restrictions, the first five pages from Google Scholar added 68 articles. We ran the final query in November 2021, leading to 181 records after the elimination of duplicates. These publications formed the starting point of the manual screening process, which was conducted in the same way as described for the SLR above. The screening process eliminated 162 records, leaving us with 19, which were fed into ResearchRabbit, producing 39 additional records from forward and backward citations. ResearchRabbit also suggested one later item, which was added at the end of November 2021. The corpus of 59 publications underwent a deductive full-text content analysis eliminating another 13 records with no explicit reference to the functional roles derived from the inductive content analysis on the intermediary literature.

The basis for the entire review process of both SLRs was our review protocol jointly developed by the author team. To limit any inappropriate use of the methodology and to counteract the risk of bias, we followed the recommendations of Thomé et al. (2016). Our certainty assessment is based on both the strict application of the review protocol and the fact that cross-checks with both gray literature and SLRs conducted by other authors did not reveal significant gaps. The final corpus of literature consisting of 70 publications—24 from the insurance intermediation and 46 from the MSP SLR—can be found in Table A1 and Table A2 in the Appendix A. In the tables, we report the retained records and include a summary of each publication’s key contents and main results.

3.2. Data Analysis and Synthesis

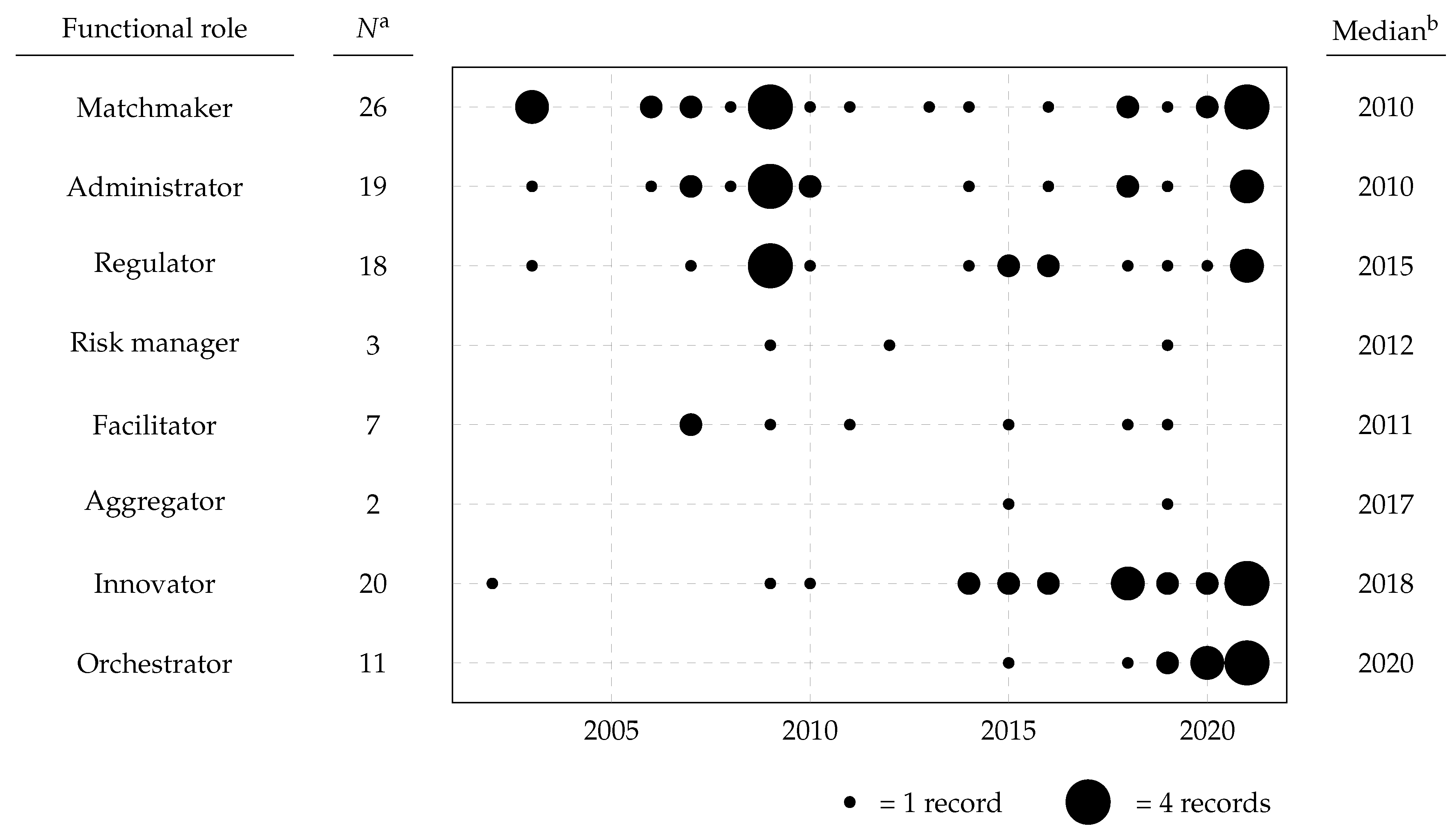

In the inductive content analysis (Mayring 2015) on the intermediary literature, the publications were read randomly to avoid any bias or undue influence. Whenever a functional role emerged, it was registered in a table. The next publication to be screened added to the role already registered and/or prompted the need to add an entirely new role to the table. This procedure was repeated for the first ten records. After ten records, the first categorization was reviewed. Some early categorizations in the process had to be further split as they turned out to be too generic and had been discussed in a more differentiated way in a subsequent publication. This process evolved into a stable categorization of functional roles since, from a certain point on, any additional publication was inserted in the existing categories, thereby confirming the categorization structure. The end result created eight distinct functional roles that insurance intermediaries play, namely matchmakers, administrators, regulators, risk managers, facilitators, aggregators, innovators, and orchestrators (also see Section 4). These functional roles were then deductively applied to the corpus of the MSP literature.

To synthesize the records, we developed two equally structured matrices. Vertically, we listed the final selection of records as shown in Table A1 and Table A2 in the Appendix A, providing information on the publication. We report the author(s), year of publication, and key contents, and main results for each reference. Horizontally, we show the eight functional roles. Thus, for publications related to insurance intermediation and the MSP literature, the matrices indicate which role is discussed in which article. This approach also allowed us to analyze the absolute as well as the temporal distribution of the functional roles in the corpus of literature (see Table 1 in Section 4 and Figure 3 in Section 5 below).

4. Functional Roles of Insurance Intermediaries

A considerable proportion of the research related to insurance intermediation centers on or departs from the notion of imperfections both in terms of the market as well as related to the customer–broker relationship (Berger et al. 1997; Eckardt and Räthke-Döppner 2010; Focht et al. 2013; Ramchander 2016; Schwarcz and Siegelman 2015; Tseng and Kang 2014; Tseng et al. 2016). In contrast, Scholtens and van Wensveen (2000, p. 1249) argue that the theory of financial intermediation “should leave its paradigm of static perfect markets and assume a more dynamic concept in which new markets are developed for new products, where financial institutions do not act as `agents’ who intermediate between savers and investors and thus alleviate `market imperfections’ like asymmetric information and participation costs, but are independent market parties that create financial products and whose value added to their clients is the transformation of financial risk, term, scale, location, and liquidity.” Following the amended theory of financial intermediation (see Scholtens and van Wensveen 2000), we take the dynamic process of financial innovation and market differentiation as a starting point for our analysis. Consequently, we do not concentrate on imperfections and institutional roles but focus on the added value of functional roles. We derive eight distinct but not mutually exclusive functional roles using the systematic literature review and the inductive content analysis described in Section 3. In practice, an insurance intermediary performs one or several of the roles that we discuss in the sequel and summarize in Table 1. The assumed roles will also depend on the geographic scope of the intermediary, the customer segment the intermediary serves, as well as the type of risk involved, e.g., retail versus large commercial customers or managing the risks of family offices versus industrial clients in, say, the oil industry.

4.1. Matchmaker

The role of the matchmaker is to find the best matching supplier for the needs of the customer. In this role, insurance intermediaries match customers with insurers without being an active trading party. They “match the insurance needs of policyholders with insurers who have the capability of meeting those needs” (Cummins and Doherty 2006, p. 359). The main task here is to organize the search and comparison of products and suppliers. Customers need intermediaries because finding the right insurance product is difficult due to its complexity (Cummins and Doherty 2006; Eckardt and Räthke-Döppner 2010; Focht et al. 2013; Köhne and Brömmelmeyer 2018; Ramchander 2016), low financial literacy (Chen 2021; Ramchander 2016), variability, and non-commoditization or because consumer risk profiles and risk attitude are heterogeneous (Schwarcz and Siegelman 2015). The role of matchmakers is generally attributed to the presence of asymmetric information (Eckardt and Räthke-Döppner 2010), which is complicated by the existence of a large number of products and infrequent purchases (Bailey and Bakos 1997). Intermediaries economize on information and transaction costs by repeatedly using the same information (Eckardt 2007, p. 12). They help their customers save time and money (premiums) by improving the efficiency of the search process (Zeier Röschmann 2018). However, the degree to which matchmakers adapt their services to customer-specific circumstances is typically limited as matchmakers focus on executing the insurance deal (Maas 2010). Hence, matchmakers’ lower information and search costs, improve the match, and reduce uncertainty by collecting and using information from both sides (Karaca-Mandic et al. 2018). As efficient searchers, matchmakers will exploit economies of scale by aggregating knowledge on demand and supply and filtering information (Karaca-Mandic et al. 2018; Stoeckli et al. 2018). The role can also extend to providing a marketplace where potential customers and insurers can meet (Benston and Smith 1976).

{kind=link}

{kind=link}

{kind=link}

Table 1.

Description and effect of functional roles in insurance intermediation.

| Functional Role | Role Description | Effect | |

|---|---|---|---|

| Matchmaker “searching efficiently” | Coordinate buyers and sellers, matching the needs between the customer and the supplier by organizing the search and comparison process; efficiently search for the best price, coverage, service, and supplier with the financial strength considering the needs of the customer | Reduce search and information costs | 21 |

| Administrator “facilitating transactions” | Coordinate the exchange of information, documents, or payments between customer and insurer(s) | Reduce transaction and coordination costs | 15 |

| Regulator “guaranteeing the promise” | Authenticate contractual parties, monitor and prevent opportunistic behavior, guarantee service and payment, ensure fulfillment of claims promise, reduce adverse selection and moral hazard problems | Reduce authentication, monitoring and enforcement costs, increase mutual trust and reciprocity | 14 |

| Risk manager “managing risks” | Analyze risk exposure and recommend effective and efficient risk management measures (including but not restricted to insurance) | Optimize the total cost of risk | 10 |

| Facilitator “enabling participation” | Organize access and/or create products to reap benefits from (dynamic, diverse, and fast-changing) markets in which individuals and businesses are or cannot be involved directly due to high learning costs | Reduce learning and participation costs | 6 |

| Aggregator “bundling needs” | Bundle the (similar) needs of many customers to negotiate and organize better solutions and allocate risks more efficiently | Reduce negotiation costs, reduce bargaining asymmetry, increase collective bargaining power | 5 |

| Innovator “closing protection gap” | Develop new or alternative coverage solutions with insurers (and other participants) to close the protection gap or develop better risk management solutions | Increase access to novelty, reduce costs resulting from solutions not fitting individual needs | 5 |

| Orchestrator “optimizing all in one” | Provide or organize complementary services such as financial advice, tax consulting, prevention and recovery | Increase convenience and complementarity, reduce overall costs by using synergies and complementarities | 4 |

Notes: Effect for customers or insurers, not for the market. Number of records discussing the functional role. The underlying 24 publications are reported in Table A1 in the Appendix A. Only risk aggregators and not information or content aggregators.

4.2. Administrator

The role of the administrator is to coordinate the information exchange between customers and insurers by managing contracts, processing documents, or handling payments. In this role, the intermediary facilitates “the exchange of information by coordinating the process and translating the information that is sent between the supplier and the consumer” (Bailey and Bakos 1997). Typical services that insurance intermediaries provide are managing contracts, delivering proof of insurance, changing or updating coverage or customer details, and handling payments. Besides processing documents and payments, intermediaries can service customers and unburden insurers by answering questions about cover (Schwarcz and Siegelman 2015). Overall, the effect of administrating the flow of information between the parties is to reduce transaction and coordination costs for both sides (Bailey and Bakos 1997; Eckardt and Räthke-Döppner 2010; Karaca-Mandic et al. 2018; Schwarcz and Siegelman 2015; Zeier Röschmann 2018). In their analysis of insurtech innovation, Stoeckli et al. (2018) note that novel digital intermediaries reduce the operating costs of private customers by digitizing customer-facing processes and providing, for example, digital claims submission or digital access to policies.

4.3. Regulator

In a regulatory role, the intermediary authenticates the contractual parties, monitors and prevents opportunistic behavior, guarantees service and payment, supports the fulfillment of the claims service promise, and reduces adverse selection and moral hazard problems for the insurer. Trust in the ability and willingness of the supplier to fulfill its pledge in (uncertain) future events is critical for insurance customers (Chen 2021). Intermediaries can advocate, for example, claims service regarding amounts paid or prompt payment (Dominique-Ferreira 2018; Liu et al. 2017; Schwarcz 2021). Likewise, it is vital that insurers receive the correct risk-relevant information to mitigate adverse selection and moral hazard (Cummins and Doherty 2006; Dahlen and Napel 2004; Focht et al. 2013; Yu and Shiu 2014). Since the intermediary has a reciprocal relationship with both parties, the intermediary is better positioned to authenticate transactions between the parties and mitigate potential issues (Dahlen and Napel 2004). Intermediaries encourage market discipline by reducing the “lemons” and adverse selection problems (Chen 2021). Schwarcz (2021, p. 520) further adds that intermediaries can overcome collective action problems and play a role in advancing consumer interests to policy makers.

4.4. Risk Manager

The role of risk managers is to analyze customer risk exposure and suggest practical and efficient risk management measures. While Allen and Santomero (1997) argue that risk management has become the central activity of many financial intermediaries, Scholtens and van Wensveen (2000) maintain that risk management has always been the main “raison d’être.” In his review of broker roles, Maas (2010) notes that the complexity and importance of risk management has increased, especially for businesses. Even multinationals lack the competence and expertise and therefore require selective consulting services from risk management specialists. However, individuals also profit from risk management expertise and services, including debiasing them of over- or under-consumption of insurance and recommending prevention measures (Schwarcz and Siegelman 2015). This role aims to reduce the total cost of risk that results from lowering the frequency and impact of risk by suggesting the most effective and efficient mitigation measures (including but not restricted to insurance).

4.5. Facilitator

The role of the facilitator is to create products for the benefit of (groups of) participants who cannot be fully or directly involved in the respective markets. The need for facilitation is attributed to the existence of complexity and change in demand and supply. Consequently, the costs of directly engaging in such markets are high, and information cannot typically be easily reused in intersectoral and intertemporal dimensions. Being involved on a daily basis, the intermediary learns how to use such markets effectively (Allen and Santomero 1997). Mutual funds, for example, are intermediaries that provide their customers access to market benefits with low participation costs (Allen and Santomero 1997; Scholtens and van Wensveen 2000). Allen and Santomero (1997, p. 1464) note that “the increased size of the financial market has coincided with a dramatic shift away from direct participation by individuals in financial markets towards participation through various kinds of intermediaries.” In markets with complex and changing offers, individuals and businesses incur high learning costs when following market changes; hence, participation costs are also high. Not only buyers but also sellers are subject to high participation costs. Current examples of facilitators in the insurance market are insurtech companies with white labeling solutions or specialized reinsurance brokers that provide access to a market that is otherwise inaccessible to the supplier.

4.6. Aggregator

The aggregator’s role is to bundle customer needs and negotiate optimum terms and conditions with one or several suppliers. Risk aggregators bundle similar needs such as risks that arise from a profession, activity, or ownership. Managing general agents (MGAs) that organize facilities and intermediaries organizing peer-to-peer insurance are examples of intermediaries performing this role. Bundling risk not only increases bargaining power (Bailey and Bakos 1997) but also allows a more efficient allocation of risk (Allen and Santomero 1997). Zeier Röschmann (2018) identifies further potential for positive effects from aggregation, namely the aspect of building communities of interest (e.g., sports activities, vintage cars, starting a business, flat-sharing, family, and travel) that enable customers to share information and recommendations. Furthermore, intermediaries harmonize the needs of searchers and those looking for buyers (Kaur Bawa and Chattha 2017). Stoeckli et al. (2018, p. 300) “identify a variety of intermediaries that exploit digital channels to aggregate insurance needs of potential customers and, then, develop and negotiate policies with specific insurers.” The term “aggregator” is also frequently used for information or content aggregators such as price comparison platforms which establish comparability among suppliers, products, and services by standardizing and bundling information. We exclude these as they are not actively engaged in the transaction process.

4.7. Innovator

The role of innovators is to work with insurers to develop novel products and services for specific customer needs. Maas (2010) identifies a shift toward a problem-solver function among commercial brokers accompanied by a desire from customers for individualized relationships and a high degree of innovation at the content level. As innovators, intermediaries lower protection gaps, for example, by helping customers that do not find capacity (Game-Lopata 2020) or develop tailor-made alternative risk transfer solutions (Maas 2010). Indeed, Scholtens and van Wensveen (2000) see financial innovation at the heart of the financial intermediation theory. Many insurtech companies provide new solutions by leveraging technology (Dominique-Ferreira 2018; Stoeckli et al. 2018). Pousttchi and Gleiss (2019) note that game-changing innovation can stem from intermediaries providing insurers with customer data from different sources.

4.8. Orchestrator

In an orchestrator role, the intermediary facilitates the provision of complementary services across a range of customer needs or customer journeys. In this way, insurance cover is part of the service but not the central value proposition. Rather than mediating between the parties, the intermediary orchestrates services that fulfill the different needs of customers in an all-in-one, customer-centric fashion (Scholtens and van Wensveen 2000). Examples of services are one-stop financial planning, including organizing insurance (Zeier Röschmann 2018), providing security and trust along the transaction process (see, e.g., Stoeckli et al. 2018), and consulting on tax, liability, and pension law (Dahlen and Napel 2004).

4.9. Discussion

Undoubtedly, the matchmaker role is the most prominently discussed in the literature on insurance intermediation, followed by administrating and regulating (see the number of relevant publications reported in Table 1 and the details in Table A1 in the Appendix A). Conversely, the role of risk managers receives surprisingly little attention, and when it does, then mostly in relation to brokers in the commercial segment. This is astonishing, considering that risk is the mainspring of financial intermediaries (see the description above). One potential explanation for this observation is that adding value by optimizing risk exposures (e.g., by saving money) is not easily quantified compared to adding value by lowering search and transaction costs with a focus on executing the insurance deal. In fact, insurance intermediary compensation is often based on the latter, and the considerable body of literature centering on different forms and impacts of compensation schemes (e.g., Browne et al. 2014; Focht et al. 2013; Latorre Guillem 2020; Ma et al. 2014a, 2014b; Puelz 2016; Strümpel et al. 2015) supports our assumption. In addition, aggregating roles have also received little attention. Economizing on collective action and bargaining power seems to have been less of an insurance intermediary role, although, in practice, one would expect that MGAs or large broker houses have the necessary power. Instead, MGAs have offered insurers access to specialist markets (see, e.g., Neale et al. 2020).

The roles of innovating and orchestrating have only recently emerged in the insurance intermediation literature in the wake of research focusing on insurtech development. This is because many insurtech companies are not full-stack insurers but in fact intermediaries. Some have been very successful in digitizing transactions as technology-driven administrators and have developed the capability to complement insurance with additional services such as prevention and recovery (Stoeckli et al. 2018). Pousttchi and Gleiss (2019) note that insurtech companies could be the game changers by providing insurers with customer data from different sources.

This study of functional roles suggests that the principal value that insurance intermediaries add is to reduce the cost of search, information, coordination, transaction, authentication, and monitoring. At the same time, they are (currently) less engaged in exerting bargaining power, optimizing total costs of risk, facilitating participation, developing novelty, or delivering complementary services. Against the background of “platforms” emerging in many industries, the following section explores how MSPs are changing and might fill the roles of the insurance intermediaries described above.

5. Insurance Intermediary Roles in the MSP Literature

This section aims to reveal where insurance intermediary roles match the functionality of MSPs and where not (see the methodology depicted in Figure 1). This allows us to grasp better what role MSPs may play in the further development of insurance intermediation, and, more broadly, in the transformation of the insurance industry towards the DPE.

In Section 4, we inductively derived eight functional roles for insurance intermediaries (see Table 1). After analyzing the 59 records on MSPs retained for full-text screening of content discussing functional roles that match insurance intermediation, we retained 46 publications (see Figure 2). Indeed, we ascertained that 13 of the 59 publications do not discuss any functional roles. Eight articles focus on the specific pricing and competitive strategies triggered by the presence of indirect network effects as well as their consequences in launching an MSP (Armstrong and Wright 2007; Cennamo and Santalo 2013; Chakravorti and Roson 2006; Eisenmann et al. 2006; Evans and Schmalensee 2016; Hagiu and Hałaburda 2014; Park et al. 2021; Parker and Van Alstyne 2000). Three more investigate the specific antitrust concerns triggered by the potential “winner-takes-all” dynamic, or more recently, the extensive employment of user data by MSPs (Evans 2002; Katz 2019; OECD 2018). Beimborn et al. (2011) focus on the specific aspects of the platform-as-a-service business model as part of the cloud economy. Finally, Katz and Shapiro (1985), seen by many authors as one of the originators of research on MSPs, study network externalities. The 46 publications of the final corpus were published between 2002 and 2021 and are distributed as summarized in Figure 3.

5.1. MSPs as Matchmakers

The matchmaking function is the most frequently mentioned role of an MSP. It appears in 26 publications, with a clear dominance in the earlier years of our sample. This is of little surprise, as matchmaking is at the core of both concepts—intermediation and MSPs—bringing two or more sides together to inter-/transact and thus reduce search costs. This overlap is probably the reason why early literature on MSPs, before the term MSP was coined, often referred to “information brokers” or “intermediation service providers” (Caillaud and Jullien 2003; Parker and Van Alstyne 2000). In their book, Evans and Schmalensee (2016) link both terms: “Economists call matchmakers multisided platforms because they provide physical or virtual platforms for multiple groups to get together.” For example, they mention dating sites connecting people, and car-sharing apps matching drivers and passengers. Search costs can turn into a limiting factor, especially but not only for physical MSPs, when a platform becomes congested and users lose oversight (Schmalensee and Evans 2007). Therefore, an effective search function is critical for MSPs to keep indirect network effects positive, as the powerful position of Google demonstrates. Technology advancements help matchmakers become more popular and profitable; those who have understood and implemented the MSP business model are today’s “power brokers” (Evans and Schmalensee 2016).

5.2. MSPs as Administrators

The administrator role is mainly referred to in terms of reducing transaction costs (19 records). Interestingly and unlike research on insurance intermediation, in our sample of the MSP literature, the administrator role seems to go hand in hand with the matchmaker role as it is mostly discussed in combination (18 of the 19 records). Again, the focus on that role was most prominent in the earlier years (before 2010) but remains relevant in later work. Brousseau and Penard (2007) note that “these new [MSP] business models contradict the prediction of a massive disintermediation caused by the strong development of digital technologies and of the Internet.” They claim that both search and transaction costs remain high in the digital age, partly due to increased choice and a lack of interoperability between digital goods.

5.3. MSPs as Regulators

This aspect is directly linked to the discussion on the quality of a platform and is prominently represented in 18 records. Given their modular architecture with many complementors around a stable core (Baldwin and Woodard 2009), MSPs must govern access to and interaction on the platforms. A lack of this led to the much-discussed collapse of one of the first digital MSPs—the Atari game console—and with it, the U.S. video game market in 1983. Boudreau and Hagiu (2009) note: “Atari was unable to prevent the entry of opportunistic developers, who flooded the market with poor quality games. At a time when consumers had few ways to distinguish good from bad games, bad games drove out good ones.” Similar discussions circle around the different strategies of Apple and Microsoft operating systems (Rysman 2009), in which Apple exercises much more control—a strategy some claim almost led to its bankruptcy in the late 1990s (Parker and Van Alstyne 2018). Access control typically involves setting specific standards that a provider of goods and services must adhere to, thus, often unwillingly, assigning the platform owner a regulatory role (Boudreau and Hagiu 2009). This role extends to rules and regulations on interaction as found in numerous examples of MSP industries, for example, the rules against “front-running” in exchanges (Schmalensee and Evans 2007). Hagiu (2009a) points out that the need to introduce standards to maintain quality “may provoke discontent among certain MSP constituents [as it] inherently reduces their ability to differentiate themselves from each other, and thereby lowers the value they derive from being on board the MSP.” The unwillingness of one side to join an MSP is also seen as a significant danger in the critical launch period of an MSP, where it faces the so-called chicken and egg problem (Caillaud and Jullien 2003) where “no one joins until everyone joins” (Veisdal 2020).

5.4. MSPs as Risk Managers

There is no direct match in the MSP literature to the specific role of risk managers. Also, in the more general sense of an MSP acting as an advisor providing specific quality expertise to platform users, there are just a few indirect examples in our sample, with no obvious temporal cluster. There is, however, a broader discussion about the aspect of quality or depth versus breadth of offerings (Hagiu 2009a) or product variety on a platform (Hagiu 2009b). The strategic necessity to get all sides on board quickly when starting an MSP business often means that speed and open access to complementors are more important than quality and depth (Hagiu 2014; Jia et al. 2019). Also, as Cenamor and Frishammar (2021) and others (Boudreau 2010; Ondrus et al. 2015; Parker and Van Alstyne 2018) show, quality control on a platform (e.g., by means of data standards) is in a trade-off relationship with the ability to innovate (limitation of platform providers’ freedom to innovate).

5.5. MSPs as Facilitators

The role of MSPs in facilitating user participation through a reduction of learning costs is infrequently discussed in our sample (seven records with no temporal pattern). Schmalensee and Evans (2007) highlight the significance of reduced learning costs for users of software platforms, while Brousseau and Penard (2007) describe the effect of reduced learning costs enjoyed by users sharing experiences on MSP as a form of “participation in risk reduction”. Evans et al. (2011) use the example of the start of the U.S. credit card industry in the 1970s, where banks launching credit cards suffered high losses. This lead to the creation of dedicated credit card companies in the shape of MSPs to reduce learning costs for participating banks. Helfat and Raubitschek (2018) stress the opportunity for platform owners to learn from complementary asset providers.

5.6. MSPs as Aggregators

The potential role of MSPs as aggregators was much less studied, and from the original 46 records, we only found 2 relevant articles. Hagiu and Wright (2015) mention the role of bundling offers or products on a platform as part of what they call “direct interactions.” Indeed, they suggest a definition of MSPs as a business model based on the ability of platforms to link two or more distinct sides directly, “relative to three traditional alternatives: vertically integrated firms, resellers or input suppliers.” Pousttchi and Gleiss (2019) mention potential MSP roles in risk transformation, which involves balancing individual risks by pooling them over time into collective ones. To do this effectively, the pooling entity needs to act as a customer data aggregator, and given their bridging function, MSPs are well-positioned to perform such tasks.

5.7. MSP as Innovators

The innovation role has been discussed in the MSP literature from the outset, and even more recently—we found reference to it in 20 publications from our sample of 46. Parker and Van Alstyne (2018) use the term “recombinant innovation” to highlight the fact that MSPs, through their modular architecture, boost innovation by recombining complementary parts. This is closely linked to the discussion surrounding the architecture of a platform. The need to control access raises the question of the openness of a platform, which, according to many authors, is a significant design decision (Boudreau 2010; Parker and Van Alstyne 2018; Rysman 2009). Cenamor and Frishammar (2021) comment that the decision on openness also influences the ability to innovate on the platform: “Innovation strategies in complementary product markets come with a dilemma: Platform sponsors must concede third parties’ autonomy to innovate to make a platform successful, but a platform sponsor must also participate in the complementary product market to make the platform grow, thus acting as a competitor to third parties.” Too tight a control can also lead to situations where the platform owner becomes an obstacle to innovation (Boudreau 2010). Gawer and Cusumano (2014) conclude that in contrast to internal product platforms (e.g., used by original equipment manufacturers), external “industry platforms allow firms to manage a division of innovative labor that originates beyond the confines of the firm or its supply chain” using globally distributed capabilities and skills. Thus, industry platforms may enable new ways to create value along technological trajectories. A critical requirement for successfully managing the evolution of such platforms is the ability to make interrelated technological and commercial decisions. The latter finding is confirmed in a case study on the rise of Alibaba conducted by Tan et al. (2015). Trabucchi and Buganza (2020) also highlight the role of big data in platform-based innovation, while architectural decisions about openness and control link to the question of ownership for MSPs. Tiwana et al. (2010) state that in the evolution of ecosystems, “the benefits of technical architectural choices can be reinforced or diminished by how a platform is governed.” Consequently, it is of little surprise to observe various ownership models coexisting for MSPs—from purely commercial and not-for-profit to shared ownership by, for example, a consortium or a society (see also Bakos and Katsamakas 2008).

5.8. MSPs as Orchestrators

The role of MSPs as orchestrators—often referred to in combination with the term ecosystem—has risen in prominence in the last years. We found 11 related publications in the 22 records from our sample published since 2015 but none in the 24 records published before 2015. The ability to expand across industry borders has been discussed much earlier, as have been strategies to add other sides to increase the attractiveness (and the network effects) of the existing sides. However, the MSP literature discussing the orchestrator role presents a more fundamental view, with platforms acting as meta-organizations (Kretschmer et al. 2020). These start to replace the dominant form of organizing economic activities in the 20th century, namely corporations and their management typically owning substantial assets. Trabucchi and Buganza (2021) discuss the fascinating statement that the world’s largest provider of hotel rooms, Airbnb, does not have any rooms of its own. Its function is merely to orchestrate supply and demand, combining all the above roles (matchmaker, aggregator, regulator, risk manager facilitator, and innovator). Poniatowski et al. (2021) state that “new actors establish platforms that act as intermediaries, substituting dyadic interactions among market players” with interchanging connections within networks. Acs et al. (2021) observe that transaction costs have been reduced through economies of scale and scope since markets have been brought within the organization. However, this is achieved at a price, namely “by reducing the need for bureaucracy, the platform organization has been able to reduce costs—search and information costs, bargaining and decision-making costs, and policing and enforcement costs—to almost zero. Moreover, the associated costs of authority and power have also been reduced by substituting networks for bureaucracy”. One pivotal question for the future will be how to regulate such a DPE (Katz 2019).

6. Discussion of the Insurance Intermediation Roles by MSP

To evaluate the potential of the platform economy for insurance intermediation, we compare how MSPs and current insurance market players fulfill the insurance intermediary roles. We consider insurance brokers and emerging insurtech companies (technology-enabled intermediaries) that we compare to digital MSPs shaping a new market form. Hence, at this point, we take an institutional perspective to discuss how different market forms can fulfill the identified key functional roles of insurance intermediation. Our comparison is guided by the context of the macro trend of digitization (Bohnert et al. 2019; Eling and Lehmann 2018) and changing customer behavior (Pugnetti and Seitz 2021). We summarize our labeling in Table 2.

Reducing search and transaction costs by effectively matching buyers and sellers is a critical role that both current market forms and MSPs fulfill. While insurance intermediaries typically perform this role as “relationship managers” based on information and experience collected over time, MSPs match platform users based on the information available on the platform. Against that background, an advantage of MSPs is their greater agility in catching and considering real-time changes on both the buyer and seller sides. MSPs create a “virtual exchange”, and it is therefore no surprise that administration is seen as an enabling function in the MSP literature, while the same role has only emerged recently in insurance intermediation research. As insurance markets become more global, dynamic, and innovative in terms of products (e.g., new pricing factors, shorter contract periods, and embedded preventive services) and suppliers (e.g., insur- and fintech companies, ecosystem orchestrators, and dealers), the agile and more data-driven MSPs and insurtech companies have an advantage over insurance brokers that have grown their business in a static market. As insurtech companies typically focus on revolutionizing a niche segment, we label them “barkers”. Another difference to note regarding the core function of matchmaking is that current brokers are at the core of the matchmaking process. They introduce buyers to sellers but typically have no interest in connecting the two sides but instead manage each side separately. In contrast, the matchmaking role of MSPs is built on networking multiple sides to create direct and indirect effects. MSPs are therefore better positioned to take advantage of scope and scale for matching purposes in an increasingly digitalized and fragmented insurance market. Insurtech companies are well positioned to be part of such an MSP.

Looking at the administrator role, it is evident that seamless digitization with 24/7 access, archiving, and data analysis offer a range of opportunities for insurance intermediation. Many insurtech companies have taken advantage of gaps by digitizing their client interfaces and offering greater convenience and 24/7 access (see Stoeckli et al. 2018). They act as a “digital office” for their customers, and the tasks performed reflect those of insurance brokers. The latter are typically less digitized and we have labeled them “secretary general.” MSPs are well positioned to support documentation, payment processes, and queries efficiently as “digital service providers”. However, achieving inter-operability in a network of multiple sides is still a significant hurdle given the lack of standards in the insurance industry. Defining and regulating standards will be essential for MSPs to thrive, not only as administrators.

Regulating exchanges between the insureds and the insurer is another crucial role that insurance intermediaries play. As customers typically lack the resources to evaluate the quality of a product or a provider, they rely on trusted brokers to guide their decision-making. With a fiduciary duty towards the customer, we have labeled insurance brokers in this role as “consumer guard”, knowing that they also fulfill certain regulatory functions for the benefit of insurers. The need for regulation increases in a fragmented and dynamic market. Although some aspects such as authentication of identity and payment processes can be digitized, for example, by insurtech companies as enablers of a “digital gateway”, monitoring the quality of insurance products is not trivial, requiring inter-temporal monitoring and specialist expertise. On-boarding and monitoring insurance providers and their products is a cumbersome process that might not fit with the agile and open-access approach necessary for MSPs to thrive. Against the background of the critical trade-off between openness and quality, we conclude that MSPs would only unwillingly become the “network inter-operator” that regulates the quality of insurance products and suppliers. Assuming ongoing non-standardization in the insurance industry, regulating exchange remains a crucial role for insurance brokers to add value.

Adding value by managing the total cost of risk is a core function of insurance intermediaries; indeed, providing “risk management expertise” is key in commercial brokerage. At first sight, MSPs are not well-positioned to undertake this advisory role unless they specialize in risk management services. However, the transition of risk financing to risk prevention (Flückiger and Carbone 2021) that accompanies data-driven business models could allow MSPs to take a key role in organizing risk-mitigating solutions. We have, therefore, labeled this potential role of MSPs as “risk mitigators,” providing access to new insurance solutions that are complementary to financing. Insurtech companies are well placed to add value by developing data and technology-driven parametric or sensor-based solutions. Accordingly, we have labeled these “data-driven risk managers.”

As discussed in Section 4, current facilitators in the insurance market are typically reinsurance brokers or insurtech companies with white-labeling solutions; we have labeled them “specialist brokers” or “insurance-as-a-service providers”. Using technology to organize access to specific markets, some insurtech firms can fulfill the role of facilitator, and insurtech can offer insurance products on a white-labeling basis in cooperation with a licensed insurance company. Other than matchmakers (“digital barkers”), facilitators may present themselves as insurers, so we have labeled insurtech intermediaries in this role as “insurance-as-a-service providers”. Where exchange among multiple sides is too complex or dynamic, MPSs could provide insurance content or products themselves, hence acting as facilitators. We have labeled MSPs in this role as “virtual syndicates”.

“Managing general agents” that aggregate customer needs to negotiate better solutions have existed for a long time. However, the question is to what extent can digitization or the platform economy effectively fulfill the role of bundling demand to bargain for better solutions. Peer-to-peer insurance is a recent phenomenon (see Clemente and Marano 2020, for an overview) of a new way to organize better solutions for a group of people. Commonly, such insurance is managed by an intermediary and backed by an insurance company, but the logic can be transferred to any pool of similar risks. We have, therefore, labeled this new type of aggregator an “insurance pooler”. Aggregation is a role that MSPs can also effectively play by offering embedded insurance as a complementary service. Practice shows that “digital dealers”, such as Amazon, already function as insurance intermediaries.

Comparing the role of innovators, we observe a different logic. Innovation by MSPs is often bottom-up in an “open innovation” approach. In contrast, innovation by current insurance intermediaries typically reflects the ability of an “entrepreneur” to develop alternative solutions in cooperation with insurers. In other words, the components necessary for innovation are already part of the platform in the case of MSPs and need to be recombined to satisfy service or protection gaps. The success of innovation by insurance brokers depends on their ability to find a supplier able and willing to close the gap. Hence, the structure of MSPs promotes open innovation with different sides taking the lead while insurance brokers guide the innovation process. In comparison, intermediaries in the form of insurtech companies take a less coordinating role, focusing on innovation driven by technology. We have labeled them “novel solution providers.”

Finally, we consider all market forms able to fulfill an orchestrating role, albeit in different contexts. For example, insurance brokers orchestrate the finance-related needs of their customers as “trusted financial advisors”. Insurtech firms use technology to provide their customers with complementary services, for example, through a comprehensive finance app with banking and insurance services. To distinguish these finance apps from the usual payment transaction apps, and to include the intended broader purpose of covering all major financial risks for individuals and families, such as disability, death, job loss, or sudden increases in interest rates, we call them “financial risk monitors”. “Digital champions” such as Google, Apple, Facebook, Amazon, and Microsoft (GAFAM) can become powerful intermediaries. In their analysis of healthcare roles, Gleiss et al. (2021) outline how GAFAM platforms “edge into existing structures by not only enabling transaction and interaction but also providing content and products themselves”. A prominent example of an insurer that transformed its business model to become a data- and technology-driven platform company is China-based Ping An. Ping An, originally a small unit of a state-owned enterprise, has become the largest P&C insurer in China. With its approach of looking at customers as platform users rather than insurance clients, it outperforms its rivals in cross-selling (The Economist 2020). As such, Ping An is an interesting case study on how to internalize the network effects of a platform (Shi 2021).

In summary, we observe striking commonalities. Both insurance intermediaries and MSPs bring different sides together to interact and transact, reducing a range of costs that neither side would be able to internalize directly. Value is created by efficiently organizing the search process and authenticating and organizing transactions. This begs the question of whether this finding provides evidence for our initial assumption that insurance intermediaries are—in fact—unconsciously functioning as MSPs. However, there are significant differences that lead us to doubt this. First and foremost, insurance intermediaries typically position themselves in the center of dyadic transactions and have no interest in building bridging networks. Value for the insurance intermediary increases with each customer mandate but not necessarily with additional insurers. While an insurance intermediary needs to maintain a good number of relationships with suppliers to provide customers with a choice, at some point, the complexity of managing and maintaining relationships and contracts with various suppliers outweighs the benefits. Eckardt and Räthke-Döppner (2010) found no indication for economies of scale and only some for the existence of economies of scope when an insurance intermediary focuses on specific customer segments (but not insurers). We, therefore, conclude that the potential for direct network effects is limited, and it comes as no surprise that most insurance brokers are small- or medium-sized businesses. Hence, our findings indicate that insurance brokers coordinate relationships between two parties but do not connect multiple sides. The future of insurance intermediation depends on the answer to two questions—first, which roles will be most valuable to customers and required in the future, and second, which market forms are best suited to supplying these services? We expect several channels to continue to coexist for the same reason that brokers still exist (see, e.g., Eckardt and Räthke-Döppner 2010; Liu et al. 2017). However, against the background of continued digital transformation and rising customer use of platforms, we expect more insurance-related business to be transacted via platforms. With matchmaking constituting the core of MSPs, we expect transformation to happen more quickly in those segments in which value can be harnessed by reducing search, information, transaction, coordination and authentication costs by means of data and technology. Intermediation for the benefit of retail customers and small- and medium-sized companies is therefore more prone to change given larger volumes of potential customers and higher degree of product standardization in comparison to the commercial brokerage segment. However, once multiple sides are connected, the potential to provide novelty, to add quality and complementary services emerges by “layering new interactions on top of the core interactions” (Rangaswamy et al. 2020). Analyzing the health care market, Gleiss et al. (2021) outline how platforms change the value network, including the delivery of insurance services. According to them, platforms not only have the potential to coordinate search and transactions and push for shared standards but can also provide value and content in new and more customer- and data-driven ways. In such a scenario, the role of insurance brokers might shift to safeguarding consumer interests and providing complementary consulting services while insurtech firms provide the gateway to novel or niche financing solutions. Insurance companies and other service providers are complementary from the perspective of customers; however, it still could make sense to single-home with an intermediary. As more and more insurance-related business is taken out through platforms, insurance intermediaries will need to adapt their current business models to stay relevant.

7. Conclusions

Our research began with the somewhat surprising assertion that insurance intermediaries seem to be natural MSPs since they bring two or more sides together in a matchmaking role, thereby reducing search, transaction, and participation costs. However, markets dominated by MSPs are concentrated on a few dominant players, while insurance intermediation is highly fragmented. To shed light on the future development of insurance intermediation in the age of the platform economy, we systematically compared the functional roles played by insurance intermediaries with those that MSPs can fulfill.

From the discussion in Section 6, we conclude that the emergence of the platform economy as a manifestation of general digitization will not diminish the need for insurance intermediation, but it will change how those needs could be met in the future. The emergence of insurtech companies is the first indication of a shift of some roles towards more digital and connected market forms. Our analysis leads us to reason that insurtech companies and MSPs can fulfill some roles better (cf. agility, scale, and scope). However, given the lack of standardization in the insurance industry, we do not expect exponential changes. The reason for this is that the lack of standardization inhibits (i) the fundamental architectural platform principle of modularity and prevents distributed development and recombinant innovation (de Reuver et al. 2018) and (ii) the ability to leverage data collected from users in the same way MSPs in other industries do (Lanfranchi and Grassi 2021). Although both effects prevent insurance intermediaries from achieving scale and scope or fully internalizing positive network effects, we recognize the need for change in the currently highly fragmented market. Smaller brokerage firms face the dilemma that they often cannot afford to digitize in terms of investment and capabilities, but they also cannot afford not to digitize in terms of customer expectations and cost effectiveness. It remains to be seen whether new business models from insurtech companies will be able to bridge the gap or whether there will be significant market consolidation.

We chose to study the potential transformation of insurance intermediation by taking a functional perspective and by using findings derived from a systematic literature review. Against that background, the interpretation of our results is prone to some limitations. Our research is exploratory in nature and our findings are short of empirical observation. More research is needed to explore how different roles are fulfilled by current market players (e.g., Stoeckli et al. 2018), how customers take insurance-related decisions in a digital platform context (e.g., Baranauskas and Raišienė 2021), what drives the performance of different market forms in practice (e.g., Comanac et al. 2016), and what impact regulation (e.g., Marano 2021), the choice of pricing and compensation structure (e.g., Tseng and Kang 2014), and the willingness to share data (e.g., Pugnetti and Seitz 2021) have on market development. Considering the significant share of overall expenses currently consumed by insurance intermediation, further research on ways to leverage the dynamics of MSPs in internalizing network effects, triggering recombinant innovation, and enabling scale and scope by minimizing marginal costs will be not only academically interesting but economically relevant. Judging by the sweeping success that MSPs have demonstrated in many industries over the last decade, marginalizing previous operators in those industries, it may now be a question of survival for some established insurance players.

Author Contributions

All authors have contributed to the conceptualization, methodology, investigation, formal analysis and writing. All authors have read and agreed to the published version of the manuscript.

Funding

This project was supported by a grant of Innosuisse—Swiss Innovation Agency, project number 48820.1 (https://www.aramis.admin.ch/Grunddaten/?ProjectID=47765, accessed on 23 August 2023).

Data Availability Statement

Data sharing is not applicable to this article.

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A. Results of the Systematic Literature Reviews

Table A1.

Synopsis of academic research publications on insurance intermediation.

| Reference | Key Contents and Main Results | MM | AD | RE | RM | FA | AG | IN | OR |

|---|---|---|---|---|---|---|---|---|---|

| Allen and Santomero (1997) |

| ✓ | ✓ | ||||||

| Bailey and Bakos (1997) |

| ✓ | ✓ | ✓ | ✓ | ||||

| Banyár and Regős (2012) |

| ✓ | |||||||

| Beloucif et al. (2004) |

| ✓ | ✓ | ||||||

| Benston and Smith (1976) |

| ✓ | ✓ | ✓ | ✓ | ✓ | |||

| Chen (2021) |

| ✓ | ✓ | ||||||

| Cummins and Doherty (2006) |

| ✓ | ✓ | ✓ | |||||

| Dahlen and Napel (2004) |

| ✓ | ✓ | ✓ | ✓ | ||||

| Dominique-Ferreira (2018) |

| ✓ | ✓ | ||||||

| Eckardt (2007) |

| ✓ | ✓ | ✓ | ✓ | ||||

| Eckardt and Räthke-Döppner (2010) |

| ✓ | ✓ | ✓ | ✓ | ||||

| Focht et al. (2013) |

| ✓ | ✓ | ||||||

| Game-Lopata (2020) |

| ✓ | ✓ | ✓ | ✓ | ✓ | |||

| Karaca-Mandic et al. (2018) |

| ✓ | |||||||

| Kaur Bawa and Chattha (2017) |

| ✓ | ✓ | ✓ | |||||

| Latorre Guillem (2020) |

| ✓ | ✓ | ||||||

| Maas (2010) |

| ✓ | ✓ | ✓ | ✓ | ✓ | |||

| Pousttchi and Gleiss (2019) |

| ✓ | ✓ | ✓ | ✓ | ✓ | |||

| Scholtens and van Wensveen (2000) |

| ✓ | ✓ | ✓ | ✓ | ||||

| Schwarcz (2021) |

| ✓ | |||||||

| Schwarcz and Siegelman (2015) |

| ✓ | ✓ | ✓ | ✓ | ||||

| Stoeckli et al. (2018) |

| ✓ | ✓ | ✓ | ✓ | ✓ | |||

| Yu and Shiu (2014) |

| ✓ | ✓ | ✓ | |||||

| Zeier Röschmann (2018) |

| ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ |

Note: The functional roles are coded as follows. “MM” = matchmaker, “AD” = administrator, “RE” = regulator, “RM” = risk manager, “FA” = facilitator, “AG” = aggregator, “IN” = innovator, “OR” = orchestrator.

Table A2.

Synopsis of academic research publications on multi-sided platforms.

| Reference | Key Contents and Main Results | MM | AD | RE | RM | FA | AG | IN | OR |

|---|---|---|---|---|---|---|---|---|---|

| Acs et al. (2021) |

| ✓ | ✓ | ✓ | ✓ | ✓ | |||

| Armstrong (2006) |

| ✓ | |||||||

| Bakos and Katsamakas (2008) |

| ✓ | ✓ | ||||||

| Baldwin and Woodard (2009) |

| ✓ | |||||||

| Boudreau (2010) |

| ✓ | |||||||

| Boudreau and Hagiu (2009) |

| ✓ | ✓ | ||||||

| Brousseau and Penard (2007) |

| ✓ | ✓ | ✓ | |||||

| Caillaud and Jullien (2003) |

| ✓ | ✓ | ||||||

| Catlin et al. (2018) |

| ✓ | |||||||

| Cenamor and Frishammar (2021) |

| ✓ | |||||||

| de Reuver et al. (2018) |

| ✓ | |||||||

| Drewel et al. (2021) |

| ✓ | ✓ | ✓ | |||||

| Evans (2003) |

| ✓ | |||||||

| Evans and Schmalensee (2016) |

| ✓ | ✓ | ✓ | ✓ | ||||

| Evans et al. (2011) |

| ✓ | ✓ | ||||||

| Gawer (2014) |

| ✓ | |||||||

| Gawer and Cusumano (2002) |

| ✓ | |||||||

| Gawer and Cusumano (2014) |

| ✓ | |||||||

| Hagiu (2009a) |

| ✓ | ✓ | ✓ | |||||

| Hagiu (2009b) |

| ✓ | ✓ | ✓ | |||||

| Hagiu (2014) |

| ✓ | ✓ | ✓ | |||||

| Hagiu and Wright (2015) |

| ✓ | ✓ | ✓ | ✓ | ||||

| Helfat and Raubitschek (2018) |

| ✓ | ✓ | ✓ | |||||

| Jia et al. (2019) |

| ✓ | ✓ | ||||||

| Kansu and Parker (2018) |

| ✓ | ✓ | ✓ | ✓ | ||||

| Kretschmer et al. (2020) |

| ✓ | ✓ | ✓ | ✓ | ||||

| O’Reilly and Finnegan (2010) |

| ✓ | |||||||

| Ondrus et al. (2015) |

| ✓ | ✓ | ||||||

| Parker and Van Alstyne (2018) |

| ✓ | |||||||

| Parker et al. (2016) |

| ✓ | ✓ | ||||||

| Poniatowski et al. (2021) |

| ✓ | ✓ | ✓ | ✓ | ✓ | |||

| Pousttchi and Gleiss (2019) |

| ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | |

| Rochet and Tirole (2003) |

| ✓ | ✓ | ||||||

| Rochet and Tirole (2006) |

| ✓ | ✓ | ||||||

| Roson (2005) |

| ✓ | ✓ | ✓ | |||||

| Rysman (2009) |

| ✓ | ✓ | ✓ | |||||

| Sanchez-Cartas and León (2021) |

| ✓ | ✓ | ||||||

| Schmalensee and Evans (2007) |

| ✓ | ✓ | ✓ | ✓ | ||||

| Tan et al. (2015) |

| ✓ | ✓ | ||||||

| Tiwana et al. (2010) |

| ✓ | |||||||

| Trabucchi and Buganza (2020) |

| ✓ | ✓ | ||||||

| Trabucchi and Buganza (2021) |

| ✓ | ✓ | ||||||

| Veisdal (2020) |

| ✓ | ✓ | ||||||

| Weyl (2010) |

| ✓ | ✓ | ||||||

| Wright and Yun (2019) |

| ✓ | |||||||

| Zhu and Iansiti (2012) |

| ✓ |

Note: The functional roles are coded as follows. “MM” = matchmaker, “AD” = administrator, “RE” = regulator, “RM” = risk manager, “FA” = facilitator, “AG” = aggregator, “IN” = innovator, “OR” = orchestrator.

References

- Acs, Zoltan J., Abraham K. Song, László Szerb, David B. Audretsch, and Éva Komlósi. 2021. The evolution of the global digital platform economy: 1971–2021. Small Business Economics 57: 1629–59. [Google Scholar] [CrossRef]

- Allen, Franklin, and Anthony M. Santomero. 1997. The theory of financial intermediation. Journal of Banking & Finance 21: 1461–85. [Google Scholar] [CrossRef]