The Implication of IFRS Financial Instruments Disclosure on Value Relevance

1

Accounting Department, Mutah University, Karak 61710, Jordan

2

School of Business and Management, Liverpool John Moores University, Merseyside L3 5UX, UK

*

Author to whom correspondence should be addressed.

J. Risk Financial Manag. 2022, 15(10), 478; https://doi.org/10.3390/jrfm15100478

Submission received: 25 August 2022

/

Revised: 11 October 2022

/

Accepted: 13 October 2022

/

Published: 19 October 2022

(This article belongs to the Section Sustainability and Finance)

Abstract

:The main objective of this research is to examine the effects of financial instruments declared under IFRSs on value relevance over thirteen years. The research sample included 35 European enterprises that were listed on the main market of the London Stock Exchange from 2007 to 2019. This study focuses on the adoption of IFRS.7 and IAS.32 disclosure standards, in line with previous studies. The Ohlson model (1995) was utilised in the study to evaluate the dependent variable since it is the module used most often in determining value relevance. The findings indicated that financial knowledge about financial instruments (FI) was typically valuable throughout the research. In addition, the significance of financial instruments and other disclosures when examining sub-components were not valued as relevant but rather provided information regarding the kind and level of exposure to FI risks. Furthermore, the earnings and book value of the common equity have a favourable impact on the value relevance. Hence, the key contributions of this study went beyond enriching the body of literature to make recommendations regarding the most influential determinant among financial instrument items that positively enhance value relevance.

1. Introduction

Adopting International Financial Reporting Standards (IFRS) creates a more attractive investment environment. For instance, 166 countries required or allowed IFRS for their listed companies at the end of 2019. These countries can be classified as advanced, emerging, and transitional economies (IASB 2020). The global creation of cohesive financial accounting standards is considered one of the most important priorities by the International Accounting Standards Board (IASB), enhancing international investors’ capability to make wise comparisons between companies’ financial performances in different regions. It, in turn, increases a company’s ability to attract new capital investments (IASB 2018).

In this context, general-purpose financial statements have the objective of providing valuable information to existing and potential investors, lenders and other creditors in order to make decisions relating to providing funds to the entity based on financial information about the reporting entity that is useful, as determined by the IASB (IASB 2018). On the other hand, if the relevant information regarding the financial instruments (FI) was absent, the decision about these instruments could lose usefulness (Givoly and Palmon 1982). Indeed, one of the most vital aims of preparing financial statements is providing adequate and timely data for stakeholders (Shamki and Abdul Rahman 2013).

One of the key characteristics of useful accounting information is value relevance (Francis et al. 2004). It reflects the capability of accounting information to express the status quo of firms that relatively impacts their share prices and related decisions (Francis and Schipper 1999). Accordingly, this study investigates the level of compliance with IFRS concerning FI based on the level of the disclosure practised by companies listed on the London Stock Exchange (LSE) over 13 years and its effect on the value relevance of financial reporting as a measure of earnings quality.

Financial firms are interconnected all over the world. If these firms take uncalculated risks, catastrophic situations can arise due to the large number of funds associated with a negative impact on markets and investors as well as the world economy. This can rapidly affect many nations; the financial crisis that began in 2008 and led to a material economic loss is an appropriate example (Dili 2017).

The foremost causes of the most recent financial crisis were asset securitisations, derivatives and loan loss provisioning. At the time of this crisis, generally accepted accounting principles (GAAP) and IFRS necessitated fair value measurement for certain classes of assets and liabilities, especially FI. The amendments in these values are eventually recognised through profit or loss accounting (Barth and Landsman 2010). In terms of IFRS, the IASB issued IFRS 7 (Financial Instrument Disclosures) in 2005 and applied them to financial reports at the beginning of 2007 (Deloitte 2009). Importantly, this IFRS was connected to IFRS 9 and amended based upon it, as the required disclosure might contribute significantly to resolving or at least mitigating the problem associated with catastrophic situations.

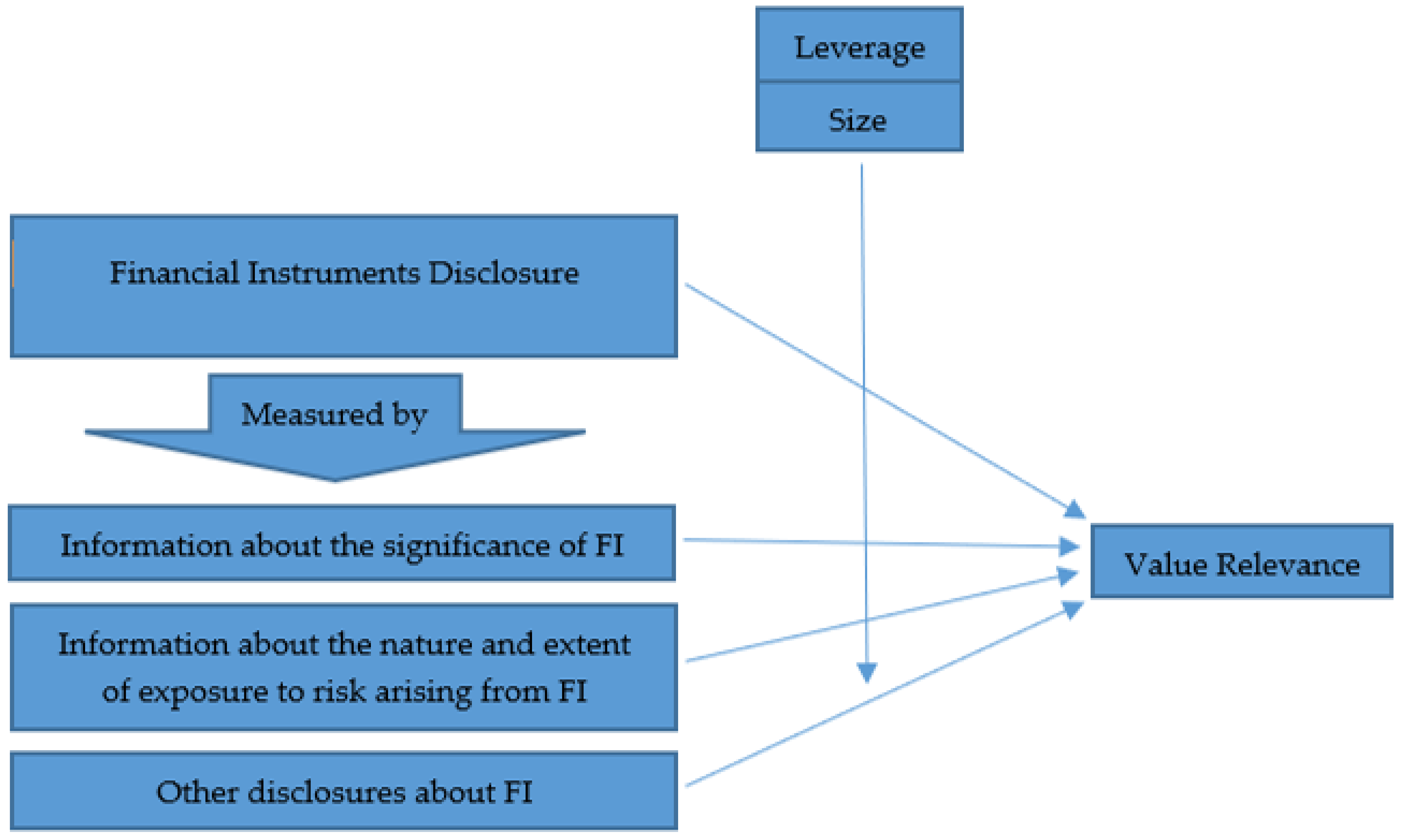

The study’s main objective is to identify the influence of adopting IFRS concerning the disclosure of FI by the companies listed on the LSE on the value relevance of firms in particular and on earnings quality in general. In addition, the study aims to determine the level of disclosure among different LSE sectors. See Figure 1.

Inside Look at IFRS.7

Firms ought to prepare mandatory financial statements pertaining to their economic and financial positions and disclose important events to external users. The weaknesses in the disclosed accounting information are mainly caused by a lack of information on risks encountered by companies (Cabedo and Tirado 2004). Accordingly, if the companies do not consider the quality of disclosed information when preparing general-purpose financial statements, the users of financial reports may face problems concerning presentation and disclosure due to the variety of users’ needs.

The prime focus of the IASB work is creating better communication in financial reporting due to concerns about the quality of disclosures (Deller 2017). These concerns are primarily related to a lack of sufficient relevant information, which may lead to a decreased ability to understand financial information, especially for more sophisticated users such as analysts, and eventually to suboptimal lending or investing decisions and inefficient disclosure (Deller 2017).

In April 2001, the International Accounting Standards Board (Board) adopted IAS 30 Disclosures in the Financial Statements of Banks and Similar Financial Institutions, which the International Accounting Standards Committee had originally issued in August 1990.

The IASB issued IFRS.7 Financial Instruments Disclosures in 2005 as a replacement for IAS.30 Financial Instruments: Disclosure and Presentation. IFRS.7 carried over the disclosure requirements in IAS 32 Financial Instruments: Disclosure and Presentation. Afterwards, IAS.32 was renamed IAS.32 Financial Instruments: Presentation. Moreover, developing and developed and improved disclosures regarding liquidity risk and fair value concerning IFRS.7 in 2005 by the IASB. Table 1 provides an overview of the procedures conducted by the IASB that are related to financial instruments standards or standards associated with financial instruments:

However, some standards were amended based on the amendments made to IFRS.7 over several years since the issuance of IFRS.7, such as IFRS.1, IFRS.10, IFRS.11 and IFRS.16 (IASB 2021).

Derivatives and FI expose companies to several risks that normally include operational, economic and financial risks (Hassan et al. 2008). Therefore, a long debate has been emerging amongst concerned parties about the measurement, disclosure, and presentation of FI, which in turn involves consideration of the hedging contract issues within the relevant standards (Bernhardt et al. 2016). Before adopting fair value measurement, FI were assessed on the historical cost of the financial position (Al-Khadash and Abdullatif 2009).

The IASB and FASB recommend greater use of fair value to account for FI as they recognise that fair value provides users with more relevant information (Johnson 2005). Likewise, the FASB found that fair value is the most appropriate standard to assess FI (Elfaki and Hammad 2015). Furthermore, an important decision was made by FASB that fair value is the most relevant attribute for FI (Bonaci et al. 2008). Similarly, IASB issued IFRS 13 fair value measurement in 2011, effective on 1st January 2013. It involves measuring FI based on fair value inputs determined by the latter standard.

Recently, many accounting academics have been paying attention to the IASB and its issuances of IFRS (Zeff 2012; Dandago and Hassan 2013), especially those linked to FI, such as debt instruments, equity instruments, derivatives and combinations, because FI form a great proportion of many companies’ transactions.

The IASB and previously IASC issued four accounting standards related to FI. The IAS.32 FI presentation and IAS.39 recognition and measurement were issued first. Later, IAS.39 was replaced by the IFRS 9 FI classification and measurement in 2009 (IASB 2021). The main focus of the current study is the IFRS.7 FI disclosure which was issued in 2005 and became effective in 2007. The IASB incorporated all the disclosure requirements regarding FI in a single standard, which is IFRS 7, as a part of its long-term project and, similarly, it was updated accordingly with the changes in other related standards, such as IFRS.9 and IAS.32. The purpose of this project is to cater for user need regarding the risks that might emerge from derivatives and FI that were suggested by the Joint Working Group of Standard Setters in its exposure draft (Joint Working Group of Standard Setters 1999).

IFRS 7 obligates firms to disclose information regarding their FI under particular categories, regardless of whether they relate to derivative or non-derivative instruments (Tahat et al. 2016). Thus, the scope of the disclosure is determined by the range of a company’s use of FI instead of its industrial sector (Gornik-Tomaszewski 2006). IFRS 7 requires a high level of disclosure compared with previous standards (Bischof 2009). IFRS.7 requires disclosure about “the significance of financial instruments” to an entity, including disclosures related to statements of financial position, statements of other comprehensive income, other income statement-related disclosures and other financial position-related disclosures (IFRS 7, Para. 7–29). Secondly, disclosures regarding “the nature and extent of risks arising from financial instruments” include qualitative and quantitative disclosures (IFRS 7, Para. 31–42). A conventional matter in the accounting environment is the value relevance of accounting information (Kouki 2018). The measurement of value relevance is based on the relationships between information presented in financial statements and stock market values (Suadiye 2012). One of the main measures of the usefulness of information is the value relevance of accounting disclosure (Francis et al. 2004). The current study focuses on the value relevance of FI disclosure for a sample of LSE firms.

Barth et al. (1996) mentioned that the reliability of fair value has been widely researched due to debate about the value relevance of fair value accounting for FI. Therefore, fair value accounting has become the favoured tool for measuring FI instead of historical cost (Hassan et al. 2006).

FI disclosures were observed and collected through a disclosure index shown in Table A1 in the Appendix A. This index is adopted from the investigation of Tahat et al. (2016) and amended as appropriate depending on the requirements and developments of IFRS.7 to achieve the objectives of this study. In addition, value relevance is measured using the Ohlson model.

2. Literature Review

Many recent studies have focused on the value relevance of the adoption of IFRS and GAAP; these studies are similar to the current study in some ways and different in others. In this section, studies related to the value relevance resulting from the adoption of standards are reviewed and the key findings are highlighted.

Starting with studies examining the adoption of IFRS, Kouki (2018) compared the value relevance of firms that adopt IFRS and non-IFRS firms across two periods. The first period comprises five years before mandatory IFRS adoption, and the second comprises six years after adoption of IFRS. The sample of this study included companies from three European countries, i.e., France, Germany, and Belgium, from 2000 to 2011. The study employed the Ohlson (1995) model that estimates the correlation between accounting information and the firm’s market value. The findings revealed that the voluntary adoption of IFRS did not boost the value relevance. The study also pointed out that the value relevance of the firms post-adoption was noticeably higher than the value of relevance of the same firms before adopting IFRS. In addition, an increase in the value relevance of equity book value and earnings was observed.

Similarly, Okafor et al. (2016) conducted a study in Canada to investigate whether compulsory adoption of IFRS influenced the value relevance of accounting information disclosed by Canadian firms and if it has higher value relevance than information provided based on local GAAP. The researcher used archival data of firms listed on the Toronto Stock Exchange from 2008 to 2013, whereas the value relevance was measured by price value relevance (using three different models) and returns value relevance. The study used a model similar to the Ohlson (1995) model, and the modified Balachandran and Mohanram (2011) model. The study provided evidence that accounting information prepared previously under local GAAP showed lower price and return value relevance than accounting information prepared and disclosed under IFRS.

Outa et al. (2017) examined the value relevance of accounting information resulting from converged/revised International Accounting Standards (IAS/IFRS). The sample consisted of firms listed in East Africa for the period from 2005 to 2014. The data was divided into two periods at the year of 2009 to reflect the pre- and post-revision and convergence of IAS/IFRS. The researchers applied a model similar to the Ohlson 1995 model, which was utilised to predict the regression of stock prices on both book values and earnings. The findings showed that accounting information prepared from the revised and converged IAS/IFRS was valuable. It also improved after the revision and convergence of IAS/IFRS. The study also found an increase in the relevance of equity book value and earnings.

Equally important, Erin et al. (2017) investigated the value relevance of 52 public entities in Nigeria during pre- and post-IFRS adoption. The researcher investigated the periods four years before IFRS and four years after IFRS adoption. The researchers measured the value relevance using Feltham and Ohlson’s (1995) model. The results revealed that IFRS adoption improved the value relevance of accounting data in Nigeria, such as earnings and book equity value.

Likewise, Agostino et al. (2011) studied the value relevance of accounting information in the European banking industry before and after adopting IFRS. The sample included 221 banks listed in the EU-15 nations from 2000 to 2006, with 2,201 annual observations. To conduct this investigation, the researcher used a model building on the Ohlson (1995) model. The results revealed that adopting IFRS improves the information content regarding the earnings and the book value for more transparent firms. However, less transparent banks do not show any substantial increase in book value’s relevance.

Equally, Turel (2009) examined the relevance of earnings and the book value of equity under IFRS from 2005 to 2006 and Capital Market Board Accounting Standards from 2001 to 2002 for firms listed in Turkey. The sample included 198 companies under Capital Market Board Accounting standards and 406 firms under IFRS. The test of value relevance was performed based on the valuation model of Ohlson (1995). A dramatic rise was found in the value relevance of earnings and book value of equity due to the implementation of IFRS.

Another study by Chebaane and Othman (2014) revealed that the value relevance of earnings per share and book value of equity improved with the mandatory adoption of IFRS in emerging economies of Asia and Africa. In the same way, García et al. (2017) have studied the value relevance of IFRS adoption, and their overall results showed that the value relevance of accounting information has improved in the post-IFRS period.

However, some studies that examined the value relevance of IFRS adoption found different results. For example, Kousenidis et al. (2010) and Alnodel (2018) found that the value relevance of the book value of equity decreased after the IFRS adoption. Kousenidis et al. (2010) attribute this result to the higher fluctuation of the book value of equity, and Alnodel (2018) concluded that the value relevance was positively impacted by firms’ attributes, particularly profitability and size, more than whether the firm adopted IFRS or not. Both studies also revealed an increase in the value relevance of earnings. Another study by Alali and Foote (2012) pointed out that the value relevance of IFRS adoption increased until 2005. In 2005 and 2006, IFRS adoption seemed less relevant due to a bearish market period. On the other hand, Karğın (2013) found that the value relevance of earnings has not been observed while the value relevance of the book value of equity has increased.

Some studies navigate the impact of adopting a single financial instrument standard on the firm value, value relevance or the cost of equity capital. For example, Yamani et al. (2021) studied the impact of financial instrument disclosures on the cost of equity capital, and they revealed that compliance with IFRS 7 disclosures reduces the cost of equity capital. On the other hand, Gómez-Ortega et al. (2022) studied the impact of the first application of IFRS 9 on the financial statements of the credit institutions listed in Spain and found positive and negative impacts of the first adoption of IFRS 9 on the results of the companies.

In terms of the studies that test the impact of FI disclosure on value relevance, Nurudeen et al. (2022) investigated the value relevance of IFRS 7 financial instrument disclosures regarding listed insurance companies in Nigeria. The study used the Ohlson Model (1995) to determine if the accounting information impacts value relevance. The researchers utilised quasi-experimental research methods and revealed that book value is more value relevant than earnings.

Tahat et al. (2016) examined the value relevance of FI disclosure in the financial statements of Jordanian-listed companies under IFRS 7 FI disclosure compared with that provided under IAS 30/32. The study’s sample included 70 Jordanian-listed companies. To measure FI information, the researchers built and used an unweighted disclosure index. In addition, the valuation model of Ohlson (1995) was adopted and used to test the relation between FI disclosure and market value. The study found that the information provided after IFRS 7 implementation was strongly related to market values.

Similarly, Hassan and Mohd-Saleh (2010) tested the value relevance of FI disclosures in the financial statements of Malaysian listed firms on the Main Board of Bursa Malaysia. The researchers used a disclosure index developed based on MASB24 “Financial Instruments: Disclosure and Presentation” requirements to measure disclosure quality. Measurement of the value relevance of fair value information was performed using three models based on Ohlson (1995). The results revealed that the FI disclosure quality was value relevant, and there was a less positive relationship in the period following MASB24 disclosure requirements becoming compulsory. However, other evidence indicated that the disclosure quality of risks causes a less positive relationship.

Based on the discussion above and since compliance with the requirements of IFRS 7, “Financial Instruments Disclosure” seems to be connected with many benefits related to the users of financial reports, the current study posits a correlation between the level of disclosure of FI and value relevance, which forms the following null hypothesis:

Hypothesis H1:

Adopting IFRS concerning the level of disclosures of FI does not impact the value relevance of accounting information.

This main hypothesis is divided into three sub-hypotheses as follows:

Hypothesis H1.1:

The disclosed information about the significance of FI does not impact the value relevance of accounting information.

Hypothesis H1.2:

The disclosed information about the nature and extent of exposure to risks arising from FI does not impact the value relevance of accounting information.

Hypothesis H1.3:

Other FI disclosures do not impact accounting information’s value relevance.

In terms of the structural characteristics of firms such as ownership structure and sector, some studies point toward a direct impact of sector alongside other variables on the level of disclosure. It has been found that the industry type impacts the level of voluntary corporate social responsibility disclosure (Alkayed and Omar 2022). Similarly, the level of disclosure related to integrated reporting was positively correlated with some sectors, particularly firms in manufacturing (Nguyen et al. 2021). Concerning disclosure required by the IAS.38, the level of disclosure was influenced by industry type (Agyei-Mensah 2019). Accordingly, a null hypothesis is formed to test the presumed relationship between sector and level of disclosure, which was used for FI disclosure in the current study.

Hypothesis H2:

There are no significant differences in the level of disclosure concerning FI based on IFRS amongst sectors listed on LSE.

In pursuing the above, each study has pros and cons. For example, Tahat et al. (2016) investigated only the value relevance of the disclosure of FI covering the first year of implementing IFRS 7, 2007, so the results may not be consistent with the following years after 2007, especially as there were many amendments made to this IFRS to reflect the issuance and changes made to either IFRS.9 or IAS.32. In addition, Tahat et al. (2016) investigated companies in a single nation, whereas the current study examined the value relevance of FI over 13 years after IFRS7 adoption in the financial statements for companies listed on LSE, which includes companies from different markets and countries. Tahat et al. (2016) did not include insurance companies and banks listed on the first market because these firms comply with specific regulations prescribed by the Jordanian Insurance Commission and the Central Bank of Jordan. On the other hand, Hassan and Mohd-Saleh (2010) attempted to measure the disclosure quality of FI and its value relevance by relying upon the disclosure index developed according to MASB24, as already mentioned. Consequently, they may have excluded several pieces of voluntarily disclosed information. Moreover, the sample of the latter study was restricted to firms listed on the Main Board of Bursa Malaysia.

Kouki (2018) compared the value relevance of accounting information among IFRS firms and non-IFRS firms. The sample size was slightly reduced, which may bias the results and did not cover a particular topic within the content of IFRS in detail. The current study’s sample is appropriate without excluding companies or choosing a specific sector. Furthermore, to the best of our knowledge, limited studies have compared the level of compliance with IFRS standards in terms of disclosure or measurement among various sectors. They also studied the full IFRS adoption that was either compared with local standards or after the IFRS convergence and revisions.

What Distinguishes the Current Study from the Previous Studies?

To the best of the researchers’ knowledge, the current study is one of only a few studies investigating the value relevance of FI. Moreover, it is conducted in the context of a developed market, contributing to the literature by presenting the LSE as a crucial case study with an efficient market. The sample is not limited to specific sectors as in some recent studies. The present investigation paves the way for future research to test the results of the current study in investigating the value relevance of FI in other developed or developing countries. In addition, the current study differs from several previous studies as it was conducted throughout 13 years to consider longer-term trends. In addition, it examines value relevance during the adoption of IFRS7 from its issuance date in 2007 until 2019, which means that all developments are considered.

The present study has some implications for standard setters and other parties because it highlights how adopting IFRS.7 affects the value relevance of firms in developed markets. The results of this study should encourage markets in other developed countries to recognise the importance of disclosure based on IFRS.7. The findings of this study provide investors with more confidence concerning disclosures related to FI, assisting them to make sound decisions by determining the most influential factors within the discloser lists and indexes about FI.

3. Methodology and Methods

Numerous studies have focused on the value relevance of earnings. Recently, many studies have relied on the model of Ohlson (1995) as the basis for measuring value relevance (Shamki and Abdul Rahman 2013). The model developed by Ohlson (1995) assumes a relationship between accounting information and the market value of the firm (stock price) (Kouki 2018). There are many previous studies examining value relevance (Barth et al. 1996; Hellström 2006; Hassan and Mohd-Saleh 2010; Yu 2013; Shamki and Abdul Rahman 2013; Okafor et al. 2016; Tahat et al. 2016; Erin et al. 2017; Outa et al. 2017; Alnodel 2018; Kouki 2018; Srivastava and Muharam 2021). The present study adopted the valuation model of Ohlson (1995) to measure the value relevance of FI disclosure across 13 years.

The assumptions of Ohlson’s model (Ohlson 1995) are that the fair value of common equity (value relevance) is influenced by several factors (such as adopting standards) alongside the change in both earnings and book value of equity because the change in equity (net assets) is explained through earnings. Other studies measure the value relevance based on the fair value of net assets. The values of equity and earnings were scaled by total assets to exclude the size effect. The impact of the sector was tested in the second hypothesis. Therefore, the model of study does not include control variables.

In the current study, value relevance was measured based on the fair value of common equity. The impact of the level of disclosure of FI was tested within the Ohlson model 1995; in other words, the study tests the impact of earnings, book value of equity, size, leverage and financial instrument disclosure on value relevance in the same model.

The Ohlson model was modified to test the main hypothesis as follows:

The Ohlson model was modified to test the sub-hypothesis as follows:

FI disclosures were observed and collected through a disclosure index shown in Appendix A. This index is adopted from Tahat et al. (2016). The index was slightly amended by deleting some items to achieve the objectives of this study, as shown in Appendix A.

L is zero if the item is not disclosed and one if the item is disclosed. Additionally, n is the number of index items.

Panel regression is used to investigate the study’s hypotheses as the panel regression can explain the relationship between the variables across 13 years, taking into consideration the developments that took place concerning FI standards.

The Population and Sample

The population consists of all EU companies (847 companies) listed in the main market of LSE between 2007 and 2019. These companies comply with IFRS adopted by the European Union and are required by LSE for the firms that prepare consolidated statements.

Several studies were conducted using samples from within banking industries; thus, their results might not be representative or generalizable to other specific industries or jurisdictions, particularly for developing countries that are recently starting to deal with derivatives (Hassan and Mohd-Saleh 2010). The study sample included firms from various industries such as trading, financial, industrial, real estate, and service sectors. Observations were obtained manually from the annual reports of 35 companies over the 13-year period. The researcher used stratified random sampling to select the sample and ensure that the collected data was as representative as possible (see Table 2).

The researcher ensured that the rate within the sample corresponded as closely as possible to the actual rate in the population to ensure the data was representative

4. Results and Discussion

H01: Adopting IFRS concerning the level of disclosures of FI does not impact the value relevance of accounting information.

Sub-Hypothesis.

H01-1: The disclosed information about the significance of FI does not impact the value relevance of accounting information.

H01-2: The disclosed information about the nature and extent of exposure to risks arising from FI does not impact the value relevance of accounting information.

H01-3: Other FI disclosures do not impact accounting information’s value relevance.

The researcher used leverage and size as controller variables to confirm that the financial sector does not bias the model’s specification and findings. Therefore, the researcher retested the sample two times using leverage and size as controller variables with financial sectors.

Additionally, the four Hausman tests assess the consistency of the model’s capabilities and thus choose the optimal model to describe the behaviour of these variables. The results of the four Hausman tests confirmed that the fixed effect model is more appropriate for the data.

The results of the fixed effect model are shown in Table 3. The calculated value of p of the variable “Adopting IFRS concerning the level of disclosures of FI” equals 0.000. As a result, the main hypothesis is rejected because it states that the (fixed effect) is more appropriate with a level of significance less than 0.10, given that the impact was positive, and the model explained 0.5551 of the variation based on the R-sq result.

It is also noticeable that the common equity’s earnings and book value impact the value relevance of accounting information as p values for both are lower than 0.10 before and after excluding financial firms. The same results were found after excluding the financial sector, but it is noticeable that the size and the leverage impacted the value relevance of all FI disclosures after excluding the financial firms. The impact was positive, and the model explained 0.3261 of the variation based on the R-sq result.

As also shown in Table 3, and based on the p values of the three main components of FI disclosures, the first sub-hypothesis (H0.1: The disclosed information about the significance of FI does not impact the value relevance of accounting information) is accepted because it states that the fixed effect is more appropriate with a level of significance higher than 0.10. The second sub-hypothesis (H0.2: The disclosed information about the nature and extent of exposure to risks arising from FI does not impact the value relevance of accounting information) is rejected because it states that the fixed effect is more appropriate with a level of significance less than 0.10. However, the third sub-hypothesis (H0.3: Other disclosures about FI do not impact the value relevance of accounting information) is accepted because it states that the fixed effect is more appropriate with a higher significance level than 0.10. Given that the impact was positive, the model explained 0.5294 of the variation based on the R-sq result. The same results were found after excluding the financial sector, but remarkably, the size and the leverage impacted the value relevance after excluding the financial firms. Given that the impact was positive, the model explained 0.3254 of the variation based on the R-sq result. Additionally, the earnings and the book value of the common equity impact the value relevance of accounting information as p values for both are lower than 0.10 before and after excluding financial firms.

The deeper analysis based on the model showed that disclosures regarding the nature and extent of exposure to risks arising from FI, which includes disclosures concerning qualitative risk, quantitative risk, and liquidity risk, impact the value relevance of accounting information positively. In contrast, the current investigation found that providing information about the significance of FI, which includes disclosures about accounting policies, financial positions, statements of comprehensive income and another income statements, hedging FI, fair value and measurements of FI do not affect the value relevance of accounting information. Similarly, it was found that the other disclosures about FI have did not influence the value relevance across the study period.

The current results confirm the findings of Nurudeen et al. (2022) that disclosures required by IFRS7 increase the value relevance of the examined firms.

The current investigation results are consistent with the findings of the Tahat et al. (2016) study. For instance, both studies found that adopting IFRS7 impacts the value relevance of accounting information. Additionally, both studies revealed that the earnings and book value of the common equity positively affected the value relevance. In addition, both studies agreed that income statement disclosures concerning FI are less crucial for investors as they do not affect the value relevance. The two studies also revealed that risk information played a vital role in FI disclosures after IFRS 7 was introduced.

For the results related to risk disclosures, the current study shows the positive effect of such disclosure on the firm value, and these results partially confirm the findings of Zamzamir et al. (2021) who found a positive influence of derivatives such as risk management strategy on the value of Malaysian firms.

The importance of disclosing information about the nature and extent of exposure to risks arising from FI is extremely clear; the Azevedo et al. (2022) study provides valid explanations for the importance of risk reporting by relying on different accounting theories.

The present examination is partially consistent with other studies that examined the value relevance of pre-IFRS adoption, post-IFRS adoption, IFRS convergence and revisions or only the adoption of IFRS and found improvements in the value relevance of the IFRS adoption, such as Turel (2009); Kousenidis et al. (2010); Agostino et al. (2011); Alali and Foote (2012); Karğın (2013); Chebaane and Othman (2014); Okafor et al. (2016); Outa et al. (2017); García et al. (2017); Erin et al. (2017); Alnodel (2018); and Kouki (2018), as they studied the value relevance of the whole IFRS. This contradiction could be due to the fact that the mentioned studies were conducted in markets other than the LSE. In addition, these studies examined pre-IFRS adoption, post-IFRS adoption, IFRS convergence and revisions or only adopting IFRS. Meanwhile, the results of the current study are consistent with these studies in terms of the relationship of value relevance with book values and earnings. This study showed impact of the book value of equity and earnings on the value relevance of FI disclosure.

As discussed in the previous section, some studies, such as Kousenidis et al. (2010); Alali and Foote (2012); Karğın (2013); and Alnodel (2018), showed different impacts of the IFRS adoption on value relevance. Therefore, the results of the current study are partially inconsistent with these results for the following reasons. The results of the Alnodel (2018) study declared that the value relevance was positively impacted by firms’ attributes, particularly profitability and size, more than whether the firm adopts IFRS or not. Kousenidis et al. (2010) attribute it to the greater fluctuation of the book value of equity, whereas the differences in the results of the Alali and Foote (2012) study were due to a bearish market period.

Regarding the levels of disclosures by IFRS.7 amongst the sectors listed on the LSE, the following hypothesis is tested:

H02: There are no significant differences in the level of disclosure to FI based on IFRS amongst sectors listed on LSE.

A one-way amongst-subjects ANOVA was conducted to compare differences in the level of disclosure for FI based on IFRS between sectors of companies listed on the LSE. As shown in Table 4, Table 5, Table 6, Table 7 and Table 8, there were significant differences in the level of disclosure between the five industries, as F (4, 463) = 207.93, p < 0.01. These results imply a rejection of the null hypothesis.

Based on a post-hoc analysis of the results in Table 6, Table 7 and Table 8 using the Bonferroni, Scheffe, and Sidak methods, it is obvious that the financial sector differed significantly from other sectors. The financial sector had the highest mean score in terms of disclosure level.

Regarding complying with IFRS.7, companies listed on the LSE obey all the requirements of the standard. The current study result provided clear evidence concerning the differences in disclosure levels between different sectors of listed companies. For instance, the financial sector provided a higher level of disclosures on the subject of FI than other sectors, whereas the real estate sector had the lowest level of disclosures about FI, as shown in Table 4. However, the rest of the sectors, such as the services, trading, and industrial sectors, registered almost similar levels of disclosures for FI. These differences in disclosure levels can be attributed to the fact that the scope of the disclosure is determined by the range of a company’s use of FI (Gornik-Tomaszewski 2006).

The following table shows data on the percentage of compliance with FI disclosure requirements each year.

Based on the analysis of the results in Table 9, it is obvious that the companies provided more information concerning FI disclosure as time passed. At the same time, companies disclosed more data on the nature and extent of exposure to risks arising from FI compared with other types of disclosures. These results are consistent with the findings of Mnif and Znazen (2020) for the disclosure levels based on IFRS 7.

Summary of the tested hypothesis results in Table 10.

Summing up the results, it can be concluded that adopting IFRS concerning FI positively correlates with the value relevance of accounting information. In addition, LSE-listed companies in some sectors provided additional significant disclosures, with the financial sector recording the highest levels of disclosed information.

5. Conclusions

The current research examined the influence of IFRS7 disclosure requirements on the value relevance of firms listed on the London Stock Exchange over thirteen years. The research revealed that the information provided over the period was value relevant. For example, disclosures regarding the nature and extent of exposure to risks arising from FI, the earnings and the book value of the common equity impact the value relevance of accounting information. On the other hand, information about the significance of FI and other disclosures about FI do not affect the value and relevance of accounting information.

The results of this research will assist the standard-setters and regulators in focusing on the items that do not affect the value relevance. These items could be made more influential in the future if addressed in a way that affects the value relevance, such as improving the quality of disclosures related to these items. The current results also help the users of financial statements in assessing the significance of FI regarding income statements and financial positions.

6. Recommendations

Based on the results, the current study provides the following recommendations:

- -

- The results of the current study provide insights regarding which components of FI disclosures the LSE Group Board should focus on.

- -

- Collaboration should occur among standards-setting bodies, governments of the European Union countries and the LSE Group Board to discuss possible improvements in the quality of disclosures with a greater focus on the points that affect the value relevance of the disclosed financial information.

- -

- Given the differences in disclosure levels among sectors, it is recommended that the governments of the European Union countries oblige their companies to commit to the highest possible disclosure levels regarding FI to minimise these differences and enhance the relevance and reliability of the disclosed financial information.

- -

- Future research conducted with more resources and time should focus on measuring the differences in disclosures and their relevance for firms with a higher proportion of financial instruments on the balance sheet compared with those with a lower proportion by adding another numerical component to the Ohlson model regression. As a result, this component may serve as a proxy to control for different reporting incentives of firms when providing users with disclosures.

Author Contributions

Investigation, T.A., M.S.A. and A.E.; methodology, T.A., M.S.A. and A.E.; data collection, T.A., M.S.A. and A.E.; formal analysis, T.A., M.S.A. and A.E.; project administration, T.A., M.S.A. and A.E.; writing—original draft, T.A., M.S.A. and A.E.; writing—review and editing, T.A., M.S.A. and A.E. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Not applicable.

Acknowledgments

The authors would like to thank the academic editor and the anonymous referees for their constructive and helpful suggestions on early versions of the paper.

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A

{kind=link}

Table A1.

IFRS.7 “Financial Instruments Disclosure” Index.

| No. | Items | No. | Items |

|---|---|---|---|

| A | Information about the significance of FI which includes: | A.5 | Fair value and measurement disclosure about FI |

| A.1 | Accounting policies | 24 | Measurement methods |

| 1 | The nature, terms and conditions for FI designation | 25 | Comparable carrying amounts |

| 2 | Recognition and measurement of FI | 26 | Information if fair value cannot be measured |

| 3 | Terms and conditions of impairment about FI | B | Nature and extent of exposure to risks arising from FI |

| A.2 | Financial position and other financial position-related disclosures | B.1 | Qualitative risk |

| 4 | FI measured at fair value through profit or loss | 27 | How the risks arise |

| 5 | Financial liabilities measured at amortised cost | 28 | Objectives, policies and processes for managing the methods used to measure the risk |

| 6 | The carrying amounts of each class of FI | 29 | Objectives, policies and processes for managing the changes (in last three items) from previous period |

| 7 | Non-trading equity | B.2 | Quantitative risk: credit risk |

| 8 | FI pledged as collateral | 30 | Maximum exposure to credit risk |

| 9 | Allowances account for credit losses | 31 | Concentration of credit risk |

| 10 | Information on reclassification | 32 | Credit quality of FI that are neither past due nor |

| A.3 | Statement of comprehensive income and other income statement-related disclosures | 33 | Collateral held as security and other credit |

| 11 | Interest income associated with FI | B.3 | Quantitative risk: market risk |

| 12 | Interest expense associated with FI | 34 | Maximum exposure to market risk |

| 13 | Fee income associated with FI | 35 | Concentration of market risk |

| 14 | Net gains/losses associated with FI | 36 | Maturity dates |

| 15 | Interest income on impaired FI | 37 | Sensitivity analysis of market risk |

| 16 | Impairment losses associated with FI | B.4 | Liquidity risk |

| A.4 | Hedge disclosure about FI | 38 | Maximum exposure to liquidity risk |

| 17 | Description of each type of hedge associated with FI | 39 | Maturity analysis |

| 18 | Nature of risks being hedged associated with FI | 40 | Concentration of liquidity risk |

| 19 | Period when cash flow hedges are expected to occur and affect | C | Other disclosures about FI |

| 20 | Forecast transaction for which hedges can be used | 41 | Information on derecognition |

| 21 | Recognised gains/losses on hedge ineffectiveness | 42 | Compound FI |

| 22 | For FV hedge: gains or losses on hedging | 43 | Defaults and breaches |

| 23 | Amount that recognised/removed in/from equity | 44 | FI that either past due or impaired |

References

- Agostino, Mariarosaria, Danilo Drago, and Damiano B. Silipo. 2011. The value relevance of IFRS in the European banking industry. Review of Quantitative Finance and Accounting 36: 437–57. [Google Scholar] [CrossRef]

- Agyei-Mensah, Ben Kwame. 2019. IAS-38 disclosure compliance and corporate governance: Evidence from an emerging market. Corporate Governance 19: 419–37. [Google Scholar] [CrossRef]

- Alali, Fatima A., and Paul Sheldon Foote. 2012. The Value Relevance of International Financial Reporting Standards: Empirical Evidence in an Emerging Market. The International Journal of Accounting 47: 85–108. [Google Scholar] [CrossRef]

- Alkayed, Hani, and Bilal Fayiz Omar. 2022. Determinants of the extent and quality of corporate social responsibility disclosure in the industrial and services sectors: The case of Jordan. Journal of Financial Reporting and Accounting. ahead-of-print. [Google Scholar] [CrossRef]

- Al-Khadash, Husam, and Modar Abdullatif. 2009. Consequences of Fair Value Accounting for Financial Instruments in the Developing Countries: The Case of the Banking Sector in Jordan. Jordan Journal of Business 5: 533–51. [Google Scholar]

- Alnodel, Ali A. 2018. The Impact of IFRS Adoption on the Value Relevance of Accounting Information: Evidence from the Insurance Sector. International Journal of Business and Management 13: 138. [Google Scholar] [CrossRef] [Green Version]

- Azevedo, Graça, Jonas Oliveira, Luiza Sousa, and Maria Fátima Ribeiro Borges. 2022. The determinants of risk reporting during the period of adoption of Basel II Accord: Evidence from the Portuguese commercial banks. Asian Review of Accounting 30: 177–206. [Google Scholar] [CrossRef]

- Balachandran, Sudhakar, and Partha Mohanram. 2011. Is the decline in the value relevance of accounting driven by increased conservatism? Review of Accounting Studies 16: 272–301. [Google Scholar] [CrossRef]

- Barth, Mary E., and Wayne R. Landsman. 2010. How did Financial Reporting Contribute to the Financial Crisis? European Accounting Review 19: 399–423. [Google Scholar] [CrossRef]

- Barth, Mary E., William H. Beaver, and Wayne R. Landsman. 1996. Value-Relevance of Banks Fair Value Disclosures under SFAS No. 107. The Accounting Review 71: 513–37. [Google Scholar]

- Bernhardt, Thomas, Daniel Erlinger, and Lukas Unterrainer. 2016. IFRS 9: The New Rules For Hedge Accounting From The Risk Management’s Prespective. ACRN Oxford Journal of Finance and Risk Perspectives 35: 1–4. [Google Scholar]

- Bischof, Jannis. 2009. The Effects of IFRS 7 Adoption on Bank Disclosure in Europe. Accounting in Europe 6: 167–94. [Google Scholar] [CrossRef]

- Bonaci, Carmen Giorgiana, Dumitru Matiş, and Jiri Strouhal. 2008. Financial reporting paradigms for financial instruments: Empirical study on the Czech and Romanian regulations. Journal of International Trade Law and Policy 7: 101–22. [Google Scholar] [CrossRef]

- Cabedo, J. David, and José Miguel Tirado. 2004. The disclosure of risk in financial statements. Accounting Forum 28: 181–200. [Google Scholar] [CrossRef]

- Chebaane, Sawcen, and Hakim Ben Othman. 2014. The Impact of IFRS Adoption on Value Relevance of Earnings and Book Value of Equity: The Case of Emerging Markets in African and Asian Regions. Procedia—Social and Behavioral Sciences 145: 70–80. [Google Scholar] [CrossRef] [Green Version]

- Dandago, Kabiru Isa, and Nur Isdawani Binti Hassan. 2013. Decision Usefulness Approach to Financial Reporting: A Case for Malaysian Inland Revenue Board. Asian Economic and Financial Review, Asian Economic and Social Society 3: 772–84. [Google Scholar]

- Deller, Adam. 2017. IASB: New Guidance on Disclosures. Available online: https://www.accaglobal.com/africa/en/member/discover/cpd-articles/corporate-reporting/iasb-disclosures0.html (accessed on 2 November 2019).

- Deloitte. 2009. Financial Instruments: Disclosures. Available online: www.iasplus.com/en/standards/ifrs/ifrs7 (accessed on 13 January 2020).

- Dili. 2017. Difference Between Basel 1, 2 and 3. Available online: https://www.differencebetween.com/difference-between-basel-1-and-vs-2-and-vs-3/ (accessed on 6 November 2019).

- Elfaki, Alfatih Alamin Abdalrahim, and Suleiman Musa Elzain Hammad. 2015. The Impact of the Application of Fair Value Accounting on the Quality of Accounting Information. An Empirical Study on a Group of Companies Listed on the Khartoum Stock Exchange. International Journal of Academic Research in Accounting, Finance and Management Sciences 5: 148–60. [Google Scholar] [CrossRef]

- Erin, Olayinka, Paul Olojede, and Olaoye Ogundele. 2017. Value Relevance of Accounting Data in the Pre and Post IFRS Era: Evidence from Nigeria. International Journal of Finance and Accounting 6: 95–103. [Google Scholar]

- Feltham, Gerald A., and James A. Ohlson. 1995. Valuation and Clean Surplus Accounting for Operating and Financial Activities. Contemporary Accounting Research 11: 689–731. [Google Scholar] [CrossRef]

- Francis, Jennifer, and Katherine Schipper. 1999. Have Financial Statements Lost Their Relevance? Journal of Accounting Research 37: 319–52. [Google Scholar] [CrossRef]

- Francis, Jennifer, Ryan LaFond, Per M. Olsson, and Katherine Schipper. 2004. Costs of Equity and Earnings Attributes. The Accounting Review 79: 967–1010. [Google Scholar] [CrossRef] [Green Version]

- García, Martha del Pilar Rodríguez, Klender Aimer Cortez Alejandro, Alma Berenice Méndez Sáenz, and Héctor Horacio Garza Sánchez. 2017. Does an IFRS adoption increase value relevance and earnings timeliness in Latin America? Emerging Markets Review 30: 155–68. [Google Scholar] [CrossRef]

- Givoly, Dan, and Dan Palmon. 1982. Timeliness of annual earnings announcements: Some empirical evidence. The Accounting Review 57: 486–508. [Google Scholar]

- Gómez-Ortega, Alba, Vera Gelashvili, María Luisa Delgado Jalón, and José Ángel Rivero Menéndez. 2022. Impact of the application of IFRS 9 on listed Spanish credit institutions: Implications from the regulatory, supervisory and auditing point of view. The Journal of Risk Finance 23: 437–55. [Google Scholar] [CrossRef]

- Gornik-Tomaszewski, Sylwia. 2006. New international standard for disclosures of financial instruments. Bank Accounting and Finance 19: 43–44. [Google Scholar]

- Hassan, Mohamat Sabri, and Norman Mohd-Saleh. 2010. The value relevance of financial instruments disclosure in Malaysian firms listed in the Main Board of Bursa Malaysia. International Journal of Economics and Management 4: 243–70. [Google Scholar]

- Hassan, Mohamat Sabri, Majella Percy, and Jennifer Stewart. 2006. The transparency of derivative disclosures by Australian firms in the extractive industries. Corporate Ownership and Control 4: 257–70. [Google Scholar] [CrossRef] [Green Version]

- Hassan, Mohamat Sabri, Norman Mohd-Saleh, and Mara Ridhuan Che Abdul Rahman. 2008. Determinants of Financial Instruments Disclosure Quality among Listed Firms in Malaysia. July 2008. SSRN Electronic Journal. [Google Scholar] [CrossRef]

- Hellström, Katerina. 2006. The Value Relevance of Financial Accounting Information in a Transition Economy: The Case of the Czech Republic. European Accounting Review 15: 325–49. [Google Scholar] [CrossRef]

- IASB. 2018. Conceptual Framework for Financial Reporting. Available online: http://eifrs.ifrs.org/eifrs/bnstandards/en/framework.pdf (accessed on 23 December 2019).

- IASB. 2020. Who Uses IFRS Standards? Available online: https://www.ifrs.org/use-around-the-world/use-of-ifrs-standards-by-jurisdiction/#profiles (accessed on 7 February 2020).

- IASB. 2021. IFRS 9 Financial Instruments. From IFRS Foundation. Available online: https://www.ifrs.org/issued-standards/list-of-standards/ifrs-9-financial-instruments.html/content/dam/ifrs/publications/html-standards/english/2022/issued/ifrs9/#about (accessed on 19 September 2020).

- Johnson, L. Todd. 2005. Relevance and Reliability. Available online: http://pds15.egloos.com/pds/200904/21/25/relevance_and_reliability_tfr_feb_2005.pdf (accessed on 3 December 2019).

- Joint Working Group of Standard Setters. 1999. Financial Instruments and Similar Items—Draft Standard and Basis for Conclusions. London: International Accounting Standards Committee. [Google Scholar]

- Karğın, Sibel. 2013. The Impact of IFRS on the Value Relevance of Accounting Information: Evidence from Turkish Firms. International Journal of Economics and Finance 5: 71–80. [Google Scholar] [CrossRef] [Green Version]

- Kouki, Ahmed. 2018. IFRS and value relevance. Journal of Applied Accounting Research 19: 60–80. [Google Scholar] [CrossRef]

- Kousenidis, Dimitrios V., Anestis C. Ladas, and Christos I. Negakis. 2010. Value Relevance of Accounting Information in the Pre- and Post-IFRS Accounting Periods. European Research Studies Journal 13: 143–52. [Google Scholar]

- Mnif, Yosra, and Oumaima Znazen. 2020. Corporate governance and compliance with IFRS 7. Managerial Auditing Journal 35: 448–74. [Google Scholar] [CrossRef]

- Nguyen, Huu Cuong, Phan Minh Hoa Nguyen, Bich Hiep Tran, Thi Thien Nga Nguyen, and Thi Thu Hien Do. 2021. Integrated reporting disclosure alignment levels in annual reports by listed firms in Vietnam and influencing factors. Meditari Accountancy Research. ahead-of-print. [Google Scholar]

- Nurudeen, Sanni Olawale, Dahunsi Olajide David, and Adesina Ayodele Samson. 2022. Value Relevance of IRS 7 Financial Instruments Disclosures for Listed Insurance Firms in Nigeria. International Journal of Economics, Management & Accounting 30: 125–49. [Google Scholar]

- Ohlson, James A. 1995. Earnings, Book Values, and Dividends in Equity Valuation. Contemporary Accounting Research 11: 661–87. [Google Scholar] [CrossRef]

- Okafor, Oliver N., Mark Anderson, and Hussein Warsame. 2016. IFRS and value relevance: Evidence based on Canadian adoption. International Journal of Managerial Finance 12: 136–60. [Google Scholar] [CrossRef]

- Outa, Erick Rading, Peterson Ozili, and Paul Eisenberg. 2017. IFRS convergence and revisions: Value relevance of accounting information from East Africa. Journal of Accounting in Emerging Economies 7: 352–68. [Google Scholar] [CrossRef]

- Shamki, Dhiaa, and Azhar Abdul Rahman. 2013. Does financial disclosure influence the value relevance of accounting information? Education, Business and Society: Contemporary Middle Eastern Issues 6: 216–32. [Google Scholar] [CrossRef]

- Srivastava, Anubha, and Harjum Muharam. 2021. Value relevance of accounting information during IFRS convergence period: Comparative evidence between India and Indonesia. Accounting Research Journal 35: 276–91. [Google Scholar] [CrossRef]

- Suadiye, Gülhan. 2012. Value Relevance of Book Value Earnings Under the Local GAAP and IFRS: Evidence from Turkey. Ege Akademik Bakis (Ege Academic Review) 12: 301–10. [Google Scholar] [CrossRef]

- Tahat, Yasean, T. Dunne, S. Fifield, and D. Power. 2016. Value Relevance of Financial Instruments Disclosure: Evidence from Jordan. Asian Review of Accounting 24: 445–73. [Google Scholar] [CrossRef]

- Turel, Ahmet. 2009. The Value Relevance of IFRS: The Case of Turkey. Œconomica 5: 119–28. [Google Scholar]

- Yamani, Amal, Khaled Hussainey, and Khaldoon Albitar. 2021. The impact of financial instruments disclosures on the cost of equity capital. International Journal of Accounting & Information Management 29: 528–51. [Google Scholar]

- Yu, Kun. 2013. Does Recognition versus Disclosure Affect Value Relevance? Evidence from Pension Accounting. The Accounting Review 88: 1095–127. [Google Scholar] [CrossRef]

- Zamzamir, Zaminor, Razali Haron, and Anwar Hasan Abdullah Othman. 2021. Hedging, managerial ownership and firm value. Journal of Asian Business and Economic Studies 28: 263–80. [Google Scholar] [CrossRef]

- Zeff, Stephen A. 2012. The evolution of the IASC into the IASB, and the challenges it faces. Accounting Review 87: 807–37. [Google Scholar] [CrossRef]

Figure 1.

Depicts the research model. Source: developed by the authors.

Table 1.

IASB Amendments.

| Year | Amendment |

|---|---|

| October 2010 | The IASB amended IFRS.7 by requesting companies to provide disclosures regarding all transferred financial assets that are not derecognised. |

| December 2011 | IFRS.7 was amended by enhancing disclosure of netting arrangements related to financial liabilities and financial assets. |

| September 2019 | Issuing interest rate benchmark reform to meet the hedge accounting requirements in IAS.39 and IFRS.9 as an amendment to IAS.39 and IFRS.9 |

| August 2020 | Phase 2 of issuing Interest Rate Benchmark Reform took place by making amendments to IFRS.16, IFRS.4, IFRS.7, IFRS.9 and IAS.39. These amendments were related to changes regarding the methodology used to identify the contractual cash flows of financial liabilities, financial assets and lease liabilities in addition to Disclosures and hedge accounting. |

Table 2.

Stratified random sampling.

| Main Industry | Sample | The Actual Rate in the Population | Rate within Sample |

|---|---|---|---|

| Trading | 6 | 18% | 17% |

| Service | 8 | 12% | 23% |

| Industrial | 7 | 18% | 20% |

| Real Estate | 5 | 8% | 14% |

| Financial | 9 | 45% | 26% |

| Total | 35 | 100% | 100% |

Table 3.

The results of the fixed effects regression.

| All FI Disclosures without Excluding the Financial Sector | |||

| R-sq: 0.5551 | Observations: 319 | F test that all u_i = 0:F(34, 280) = 35.12 | Prob > F = 0.0 |

| FV of CE | Coefficient | T | P > |T |

| Earnings | 7.622571 | 3.73 | 0.000 |

| BV of CE | 3.865625 | 3.54 | 0.000 |

| All FI disclosures | 110,864.4 | 3.66 | 0.000 |

| Size | −7606.743 | −0.12 | 0.904 |

| Leverage | 511,430.4 | 0.53 | 0.598 |

| All FI after Excluding the Financial Sector | |||

| R-sq: 0.3261 | Observations: 267 | F test that all u_i = 0:F(29, 233) = 60.08 | Prob > F = 0.0 |

| FV of CE | Coefficient | T | P > |T |

| Earnings | 1.151731 | 4.16 | 0.000 |

| BV of CE | 5.464115 | 10.97 | 0.000 |

| All FI disclosures | 17,230.53 | 3.93 | 0.000 |

| Size | −25,326.35 | −2.74 | 0.007 |

| Leverage | 487,954.8 | 2.70 | 0.007 |

| Main Components FI Disclosures without Excluding the Financial Sector | |||

| R-sq: 0.5294 | Observations: 319 | F test that all u_i = 0:F(34, 278) = 34.68 | Prob > F = 0.0 |

| FV of CE | Coefficient | T | P > |T |

| Earnings | 7.600435 | 3.68 | 0.000 |

| BV of CE | 3.954598 | 3.65 | 0.000 |

| Information about the significance of FI | −154,802.4 | −0.80 | 0.423 |

| Information about the nature and extent of exposure to risks arising from FI | 1,533,639 | 2.44 | 0.015 |

| Other disclosures about FI | 120,685.6 | 0.45 | 0.656 |

| Size | −40,920.05 | −0.65 | 0.518 |

| Leverage | 590,231.1 | 0.60 | 0.550 |

| Main Components FI Disclosures after Excluding the Financial Sector | |||

| R-sq: 0.3254 | Observations: 267 | F test that all u_i = 0:F(29, 231) = 60.60 | Prob > F = 0.0 |

| FV of CE | Coefficient | T | P > |T |

| Earnings | 1.111658 | 3.90 | 0.000 |

| BV of CE | 5.318879 | 10.63 | 0.000 |

| Information about the significance of FI | −32,916.27 | −0.83 | 0.406 |

| Information about the nature and extent of exposure to risks arising from FI | 53,742.97 | 3.11 | 0.002 |

| Other disclosures about FI | −61,849.58 | −0.81 | 0.418 |

| Size | −27,089.6 | −2.93 | 0.004 |

| Leverage | 488,085 | 2.68 | 0.007 |

Table 4.

Summary of all FI disclosures.

| Industry | Mean | Std. Dev. | Freq. |

|---|---|---|---|

| Trading | 24.235294 | 3.399375 | 68 |

| Service | 25.533333 | 3.1764902 | 75 |

| Industrial | 25.821429 | 3.9974712 | 84 |

| Real Estate | 25.846154 | 4.3922088 | 39 |

| Financial | 35.950495 | 4.2797132 | 202 |

| Total | 29.918803 | 6.5942215 | 468 |

Table 5.

Analysis of variance.

| Source | SS | df | MS | F | Prob > F |

|---|---|---|---|---|---|

| Between groups | 13,045.1093 | 4 | 3261.27732 | 207.93 | 0.0000 |

| Within groups | 7261.80526 | 344 | 15.6842446 | ||

| Total | 20,306.9145 | 348 | 43.483757 | ||

| Bartlett’s test for equal variances: chi2(4) = 12.4423 Prob > chi2 = 0.014 | |||||

Table 6.

Comparison of all FI disclosures by industries (Bonferroni) row mean.

| Col Mean | Trading | Service | Industrial | Real Estate |

|---|---|---|---|---|

| Service | 1.29804 0.509 | |||

| Industrial | 1.58613 0.144 | 0.288095 1.000 | ||

| Real Estate | 1.61086 0.434 | 0.312821 1.000 | 0.024725 1.000 | |

| Financial | 11.7152 0.000 | 10.4172 0.000 | 10.1291 0.000 | 10.1043 0.000 |

Table 7.

Comparison of all FI disclosures by industries (Scheffe) row mean.

| Col Mean | Trading | Service | Industrial | Real Estate |

|---|---|---|---|---|

| Service | 1.29804 0.430 | |||

| Industrial | 1.58613 0.199 | 0.288095 0.995 | ||

| Real Estate | 1.61086 0.394 | 0.312821 0.997 | 0.024725 1.000 | |

| Financial | 11.7152 0.000 | 10.4172 0.000 | 10.1291 0.000 | 10.1043 0.000 |

Table 8.

Comparison of all FI disclosures by industries (Sidak) row mean.

| Col Mean | Trading | Service | Industrial | Real Estate |

|---|---|---|---|---|

| Service | 1.29804 0.407 | |||

| Industrial | 1.58613 0.135 | 0.288095 1.000 | ||

| Real Estate | 1.61086 0.359 | 0.312821 1.000 | 0.024725 1.000 | |

| Financial | 11.7152 0.000 | 10.4172 0.000 | 10.1291 0.000 | 10.1043 0.000 |

Table 9.

The percentage of compliance with FI disclosure requirements across each year.

| Year | All FI Disclosures | Information about the Significance of FI | Information about the Nature and Extent of Exposure to Risks Arising from FI | Other Disclosures about FI |

|---|---|---|---|---|

| 2007 | 73% | 70% | 83% | 67% |

| 2008 | 75% | 73% | 84% | 67% |

| 2009 | 74% | 74% | 82% | 66% |

| 2010 | 75% | 75% | 83% | 67% |

| 2011 | 75% | 72% | 84% | 69% |

| 2012 | 74% | 70% | 84% | 67% |

| 2013 | 77% | 74% | 84% | 72% |

| 2014 | 77% | 72% | 85% | 73% |

| 2015 | 79% | 74% | 85% | 79% |

| 2016 | 79% | 75% | 85% | 77% |

| 2017 | 79% | 78% | 86% | 74% |

| 2018 | 79% | 76% | 85% | 75% |

| 2019 | 79% | 76% | 85% | 76% |

Table 10.

Hypothesis results.

| Hypothesis | Result |

|---|---|

| H01: Adopting IFRS concerning the level of disclosures of FI does not impact the value relevance of accounting information. | Rejected |

| H01-1: The disclosed information about the significance of FI does not impact the value relevance of accounting information. | Accepted |

| H01-2: The disclosed information about the nature and extent of exposure to risks arising from FI does not impact the value relevance of accounting information. | Rejected |

| H01-3: Other FI disclosures do not impact accounting information’s value relevance. | Accepted |

| H02: There are no significant differences in the level of disclosure concerning FI based on IFRS amongst sectors listed on LSE. | Rejected |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Alsarayreh, T.; Altarawneh, M.S.; Eltweri, A. The Implication of IFRS Financial Instruments Disclosure on Value Relevance. J. Risk Financial Manag. 2022, 15, 478. https://doi.org/10.3390/jrfm15100478

AMA Style

Alsarayreh T, Altarawneh MS, Eltweri A. The Implication of IFRS Financial Instruments Disclosure on Value Relevance. Journal of Risk and Financial Management. 2022; 15(10):478. https://doi.org/10.3390/jrfm15100478

Chicago/Turabian StyleAlsarayreh, Taleb, Mohammad Saleh Altarawneh, and Ahmed Eltweri. 2022. "The Implication of IFRS Financial Instruments Disclosure on Value Relevance" Journal of Risk and Financial Management 15, no. 10: 478. https://doi.org/10.3390/jrfm15100478