An Alternative to Coping with COVID-19—Knowledge Management Applied to the Banking Industry in Taiwan

Abstract

:1. Introduction

2. The Review of the Professional and Academic Literature

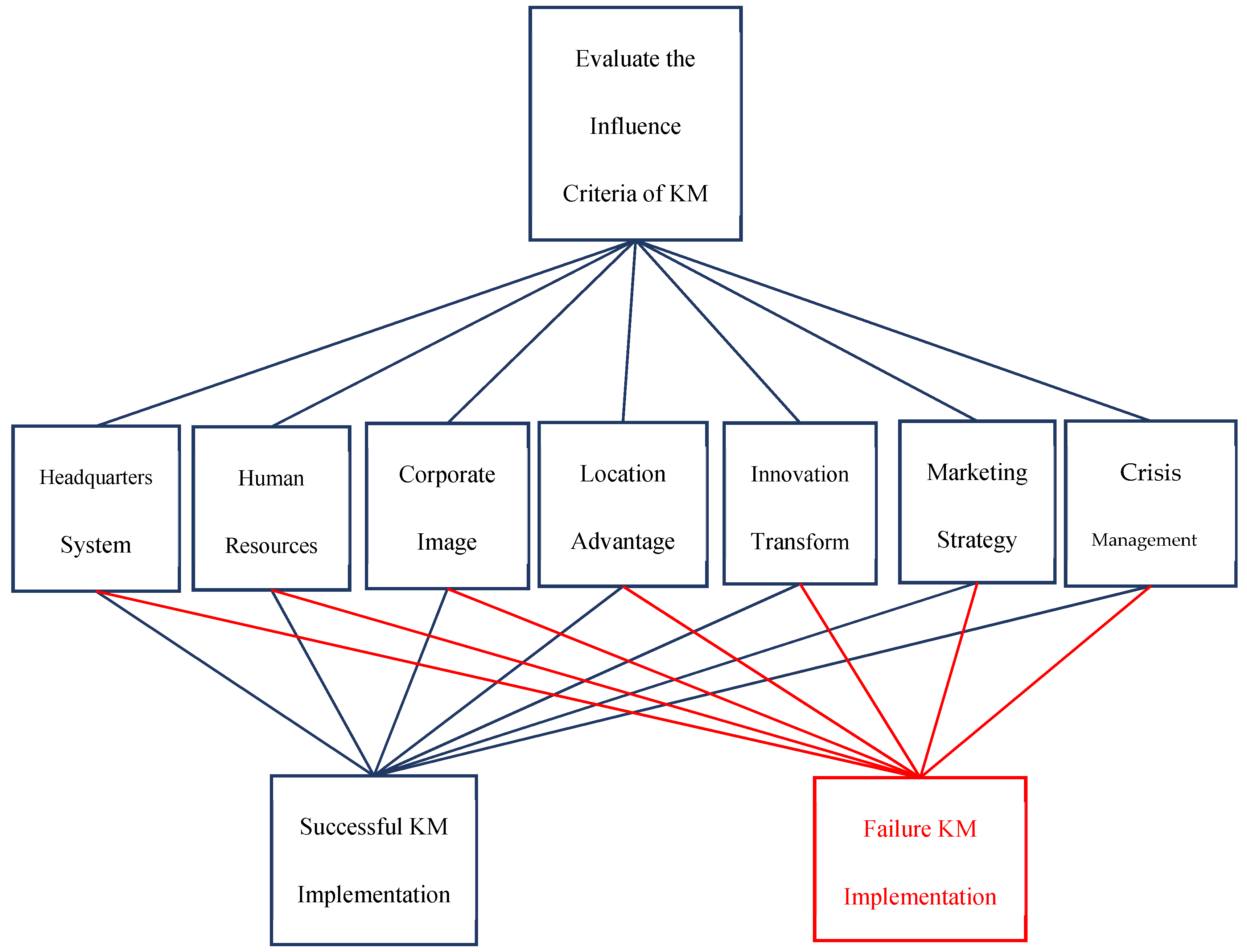

2.1. Headquarters System

2.2. Human Resources

2.3. Corporate Image

2.4. Location Advantage

2.5. Innovation and Transformation

2.6. Marketing Strategy

2.7. Crisis Management

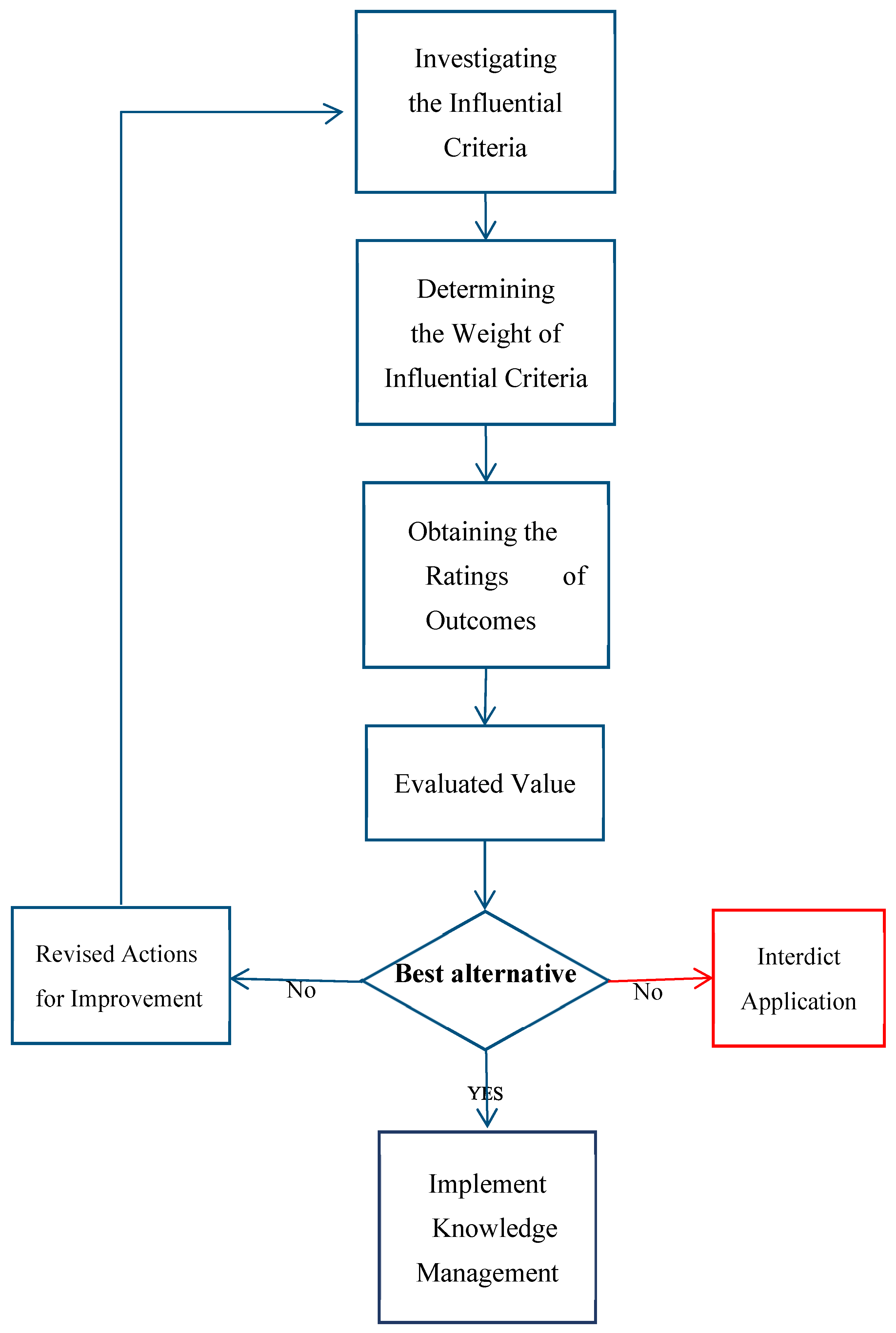

3. The Research Methodology and Design

3.1. Fuzzy Preference Relations

3.2. Consistency of the Fuzzy Preference Relations

3.3. Additive Transitivity Consistency of the Fuzzy Preference Relations

4. Research for KM Implementation

4.1. Evaluated Influential Criteria and Framework of the Evaluation Model

4.2. The Hierarchy Analytical Process for Evaluating Criteria Influence

4.2.1. Linguistic Variables

4.2.2. Defining the Priority Ratings for Possibility of Outcome Compliance with Each Criterion

4.2.3. Acquiring the Priority Weight for Prediction

4.3. Empirical Case for Predicting Possibility of Success of Implementing KM

4.3.1. Weight Calculation of the Influential Criteria

4.3.2. The Influential Criteria were Calculated to Acquire Weights for Possibilities of Outcomes

4.3.3. Determining the Prediction Values of Priority Weight

(0.1307 × 0.6206) + (0.1340 × 0.7008) + (0.1515 × 0.6128) = 0.6534,

(0.1307 × 0.3794) + (0.1340 × 0.2992) + (0.1515 × 0.3872) = 0.3466

5. Discussion and Implications of the Study

5.1. Discussion

5.2. Implications of the Study

6. Conclusions and Limitations

6.1. Conclusions

6.2. Limitations and Future Work

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Abdul-Rahim, Ruzita, Siti Aisah Bohari, Aini Aman, and Zainudin Awang. 2022. Benefit–Risk Perceptions of FinTech Adoption for Sustainability from Bank Consumers’ Perspective: The Moderating Role of Fear of COVID-19. Sustainability 14: 8357. [Google Scholar] [CrossRef]

- Akram, Tayyaba, Shen Lei, Muhammad Jamal Haider, and Syed Talib Hussain. 2018. Exploring the Impact of Knowledge Sharing on the Innovative Work Behavior of Employees: A Study in China. International Business Research 11: 186–94. [Google Scholar] [CrossRef]

- Amir, Khorram-Manesh, Maxim A. Dulebenets, and Krzysztof GoniewiczInt. 2021. Implementing Public Health Strategies-The Need for Educational Initiatives: A Systematic Review. International Journal of Environmental Research and Public Health 18: 5888. [Google Scholar] [CrossRef]

- Ar, Anil Yasin, and Asad Abbas. 2021a. Public-private ICT-based collaboration initiative during the COVID-19 pandemic: The case of Ehsaas Emergency Cash Program in Pakistan. Brazilian Archives of Biology and Technology 64. [Google Scholar] [CrossRef]

- Ar, Anil Yasin, and Asad Abbas. 2021b. Corporate Response Against COVID-19: Manufacturing Shift by Ford-Otosan. Annals of Global Health 87: 60. [Google Scholar] [CrossRef]

- Awan, Hayat M., Sahar Hayat, and Rafia Faiz. 2018. Antecedents and consequences of corporate image: Conventional and islamic banks. Revista de Administração de Empresas 58: 418–32. [Google Scholar] [CrossRef]

- Barnes, Victoria, and Lucy Ann Newton. 2019. Symbolism in bank marketing and architecture: The headquarters of National Provincial Bank of England. Management & Organizational History 14: 1–32. [Google Scholar] [CrossRef]

- Błach, Joanna. 2020. Barriers to Financial Innovation—Corporate Finance Perspective. Journal of Risk and Financial Management 13: 273. [Google Scholar] [CrossRef]

- Broad, Robin. 2007. Knowledge Management: A case study of the World Bank’s research department. Development in Practice 17: 700–8. [Google Scholar] [CrossRef]

- Cebi, Ferhan, Onur Feray Aydin, and Sitki Gozlu. 2010. Benefits of Knowledge Management in Banking. Journal of Transnational Management 15: 308–21. [Google Scholar] [CrossRef]

- Chiclana, Francisco, Francisco Herrera, and Enrique Herrera-Viedma. 2001. Integrating multiplicative preference relations in a multipurpose decision-makingmodel based on fuzzy preference relations. Fuzzy Sets and Systems 122: 277–91. [Google Scholar] [CrossRef]

- Chirilă, Viorica. 2022. Connectedness between Sectors: The Case of the Polish Stock Market before and during COVID-19. Journal of Risk and Financial Management 15: 322. [Google Scholar] [CrossRef]

- Choudhury, Archita Pal, Amit Kundu, Dev Narayan Sarkar, and Arabinda Bhattacharya. 2022. Practitioners’ perspectives on the marketing strategies in Indian banking sector: A framework for strategy formulation. Journal of Financial Services Marketing. [Google Scholar] [CrossRef]

- Corra-Ariass, Manuel Ángel. 2020. Foreign bank location in Spain: An analysis by provinces. UCJC Business and Society Review 2020: 174–221. [Google Scholar] [CrossRef]

- D’Angelo, Chiara, Diletta Gazzaroli, Chiara Corvino, and Caterina Gozzoli. 2022. Changes and Challenges in Human Resources Management: An Analysis of Human Resources Roles in a Bank Context (after COVID-19). Sustainability 14: 4847. [Google Scholar] [CrossRef]

- Drahan, O. O., I. O. Herasymenko, and N. O. Verniuk. 2021. Anti-crisis management of the bank in the conditions of financial market instability. ResearchGate. [Google Scholar] [CrossRef]

- Edeh, Friday Ogbu, Nurul Mohammad Zayed, Vitalii Nitsenko, Olha Brezhnieva-Yermolenko, Julia Negovska, and Maryna Shtan. 2022. Predicting Innovation Capability through Knowledge Management in the Banking Sector. Journal of Risk and Financial Management 15: 312. [Google Scholar] [CrossRef]

- El-Chaarani, Hani, Rebecca Abraham, and Yahya Skaf. 2022. The Impact of Corporate Governance on the Financial Performance of the Banking Sector in the MENA (Middle Eastern and North African) Region: An Immunity Test of Banks for COVID-19. Journal of Risk and Financial Management 15: 82. [Google Scholar] [CrossRef]

- Firdiansyah, Fitra Azkiya. 2021. Optimization of Human Resources Management in Islamic Banking. JPS 2: 150–64. [Google Scholar] [CrossRef]

- Gazi, Funda, Tarık Atan, and Mahmut Kılıç. 2022a. The Assessment of Internal Indicators on The Balanced Scorecard Measures of Sustainability. Sustainability 14: 8595. [Google Scholar] [CrossRef]

- Gazi, Md. Abu Issa, Md Nahiduzzaman, Iman Harymawan, Abdullah Al Masudand, and Bablu Kumar Dhar. 2022b. The Impact of COVID-19 on Financial Performance and Profitability of Banking Sector in Special Reference to Private Commercial Banks: Empirical Evidence from Bangladesh. Sustainability 4: 6260. [Google Scholar] [CrossRef]

- Ghouse, Ghulam, Muhammad Ishaq Bhatti, and Muhammad Hassam Shahid. 2022. Impact of COVID-19, Political, and Financial Events on the Performance of Commercial Banking Sector. Journal of Risk and Financial Management 15: 186. [Google Scholar] [CrossRef]

- Heard, Christopher, Flavio Menezes, and Alicia N. Rambaldi. 2017. The dynamics of bank location decisions in Australia. Australian Journal of Management 43: 031289621771757. [Google Scholar] [CrossRef]

- Herrera, Francisco, Enrique Herrera-Viedma, and Franciisco Chiclana. 2001. Theory and Methodology Multiperson decision-making based on multiplicative preference relations. European Journal of Operational Research 129: 372–85. [Google Scholar] [CrossRef]

- Herrera-Viedma, Enrique, Francisco Herrera, Francisco Chiclana, and Maria Luque. 2004. Some issues on consistency of fuzzy preference relations. European Journal of Operational Research 154: 98–109. [Google Scholar] [CrossRef]

- Herrera-Viedma, Enrique, Sergio Alonso, Francisco Chiclana, and Francisco Herrera. 2007. A Consensus Model for Group Decision Making with Incomplete Fuzzy Preference Relations. IEEE Transactions on Fuzzy Systems 15: 863–77. [Google Scholar] [CrossRef]

- Van Hoa, Vu, Hoang Dung, Ha Thi Thu Phuong, and Pham Van Hieu. 2022. Human Resources Development of Vietnam Commercial Banking System. Cross Current International Journal of Economics, Management and Media Studies 4: 19–27. [Google Scholar] [CrossRef]

- Hsieh, Hsiu-Chin, Xuan Huynh Nguyen, Tien-Chih Wang, and Jen-Yao Lee. 2020. Prediction of Knowledge Management for Success of Franchise Hospitality in a post-Pandemic Economy. Sustainability 12: 8755. [Google Scholar] [CrossRef]

- Islam, Asraful, Abdullah Almamun, and Mijanur Rahman Molla. 2022. Analyzing the Uses of Event Marketing Strategy as the Experiential Marketing Stategy of Bank: A Study on a Commericial Bank Limited. International Journal of Marketing Research Innovation 6. [Google Scholar] [CrossRef]

- Jovanovic, Dijana, Milos Antonijevic, Milos Stankovic, Miodrag Zivkovic, Marko Tanaskovic, and Nebojsa Bacanin. 2022. Tuning Machine Learning Models Using a Group Search Firefly Algorithm for Credit Card Fraud Detection. Mathematics 10: 2272. [Google Scholar] [CrossRef]

- Kabbani, Samira, Silva Karkoulian, Puzant Balozian, and Sandra Rizk. 2022. The Impact of Ethical Leadership, Commitment and Healthy/Safe Workplace Practices toward Employee Attitude to COVID-19 Vaccination/Implantation in the Banking Sector in Lebanon. Vaccines 10: 416. [Google Scholar] [CrossRef] [PubMed]

- Kien, Cao Dinh, and Nguyen Huu That. 2022. Innovation Capabilities in the Banking Sector Post-COVID-19 Period: The Moderating Role of Corporate Governance in an Emerging Country. International Journal of Financial Studies 10: 42. [Google Scholar] [CrossRef]

- Kopylyuk, Okcaha Ibahibha, Onekcahopa Mupohibha Muzychka, and Oneha Isopibha Lozynska. 2019. The Strategic Approach to Crisis Management in Banks of Ukraine. Business Inform 10: 226–32. [Google Scholar] [CrossRef]

- Kuchciak, Iwa, and Izabela Warwas. 2021. Designing a Roadmap for Human Resource Management in the Banking 4.0. Journal of Risk and Financial Management 14: 615. [Google Scholar] [CrossRef]

- Kuś, Agnieszka, and Dorota Grego-Planer. 2021. A Model of Innovation Activity in Small Enterprises in the Context of Selected Financial Factors: The Example of the Renewable Energy Sector. Energies 14: 2926. [Google Scholar] [CrossRef]

- Laidroo, Laivi, and Urmas Ööbik. 2013. Banks’ CSR disclosures-headquarters versus subsidiaries. Baltic Journal of Management 9: 47–70. [Google Scholar] [CrossRef]

- Li, Dan, Hongwei Guo, Xianzhi Wang, Ze Liu, Cheng Li, and Wuhong Wang. 2016. Analyzing the Effectiveness of Policy Instruments on New Energy Vehicle Industry using Consistent Fuzzy Preference Relations. International Review for Spatial Planning and Sustainable Development 4: 45–57. [Google Scholar] [CrossRef]

- Liu, Li Xian, Fuming Jiang, Milind Sathye, and Hongbo Liu. 2021. Are Foreign Banks Disadvantaged Vis-À-Vis Domestic Banks in China? Journal of Risk and Financial Management 14: 404. [Google Scholar] [CrossRef]

- Mila, Kavalić, Milan Nikolić, Dragica Radosav, Sanja Stanisavljev, and Mladen Pečujlija. 2021. Influencing Factors on Knowledge Management for Organizational Sustainability. Sustainability 13: 1497. [Google Scholar]

- Mohamed, Beraich, and El Main Salah Eddin. 2022. Volatility Spillover Effects in the Moroccan Interbank Sector before and during the COVID-19 Crisis. Risks 10: 125. [Google Scholar] [CrossRef]

- Mohamed, Pateh Bah, Ezekiel Kalvin Duramany-Lakkoh, and Ernest Udeh. 2022. Assessing the Effect of Human Resource Information Systems on the Human Resource Strategies of Commercial Banks. European Journal of Business Management and Research 7: 304–12. [Google Scholar]

- Mustafa, Raza Rabbani, Mahmood Asad, Mohd Ali, Habeeb Ur Rahiman, Mohd Atif, Zehra Zulfikar, and Yusra Naseem. 2021. The Response of Islamic Financial Service to the COVID-19 Pandemic: The Open Social Innovation of the Financial System. Journal of Open Innovation: Technology, Market, and Complexity 7: 85. [Google Scholar]

- Ndegwa, Rose. 2022. The Influence of Electronic Marketing Strategies on the Performance of Equity Bank Limited in Kenya. European Journal of Economic and Financial Research 5. [Google Scholar] [CrossRef]

- Nedelchev, Miroslav Colev. 2002. Corporate Image of Commercial Banks (1996–1997). SSRN Electronic Journal, Discussion Papers. [Google Scholar] [CrossRef]

- Nedelchev, Miroslav Colev. 2003. Management of the Corporate Image of Commercial Banks. SSRN Electronic Journal, Discussion Papers. [Google Scholar] [CrossRef]

- Nguru, Fracier, Kepha Ombui, and Mike A. Iravo. 2017. Effects of Marketing Strategies on the Performance of Equity Bank. International Journal of Scientific and Research Publications 6: 569–76. [Google Scholar] [CrossRef]

- Ologbenla, Patrick. 2021. Corporate Image Management and Bank Performance in Nigeria. Journal of Economics, Finance and Management Study 4. [Google Scholar] [CrossRef]

- Ordonez-Ponce, Eduardo, Truzaar Dordi, David Talbot, and Olaf Weber. 2022. Canadian banks and their responses to COVID-19—Stakeholder-oriented crisis management. Journal of Sustainable Finance & Investment 12: 423–30. [Google Scholar] [CrossRef]

- Osman, Ismah, Sharifah Faigah Syed Alwi, Imani Mokhtar, Husniyati Ali, Fatimah Setapa, Ruhaini Muda, and Abdul Rahman Abdul Rahim. 2015. Integrating Institutional Theory in Determining Corporate Image of Islamic Banks. Procedia-Social and Behavioral Sciences 211: 560–67. [Google Scholar] [CrossRef]

- Özkaynar, Kürşad. 2022. Marketing Strategies of Banks in the Period of Metaverse, Blockchain and Crypiocurrency in the Context of Consummer Behavior Theories. International Journal of Insurance and Finance, 1–12. [Google Scholar] [CrossRef]

- Rushchyshyn, Nadiia M., Tetyana V. Medynska, and Serhii M. Klymenko. 2022. Application of Anti-Crisis Management by Ukrainian Banks in the Face of Modern Challenges. Business Inform 1: 314–22. [Google Scholar] [CrossRef]

- Sakas, Damianos P., Ioannis Dimitrios G. Kamperos, Dimitrios P. Reklitis, Nikolaos T. Giannakopoulos, Dimitrios K. Nasiopoulos, Marina C. Terzi, and Nikos Kanellos. 2022. The Effectiveness of Centralized Payment Network Advertisements on Digital Branding during the COVID-19 Crisis. Sustainability 14: 3616. [Google Scholar] [CrossRef]

- Singh, Ravi Kumar. 2018. The Role of Central Bank in Crisis Management. SSRN Electronic Journal, Conference Paper. [Google Scholar] [CrossRef]

- Sinyagovsky, Yu. 2021. Object Field of Crisis Management at the Bank. Visnyk of Sumy State University, 228–35. [Google Scholar] [CrossRef]

- Soemitra, Andri, and Tri Inda Fadhila Rahma. 2022. The Role of Micro Waqf Bank in Women’s Micro-Business Empowerment through Islamic Social Finance: Mixed-Method Evidence from Mawaridussalam Indonesia. Economies 10: 157. [Google Scholar] [CrossRef]

- Stefanovic, Nikola, Lidija Barjaktarovic, and Alexey Bataev. 2021. Digitainability and Financial Performance: Evidence from the Serbian Banking Sector. Sustainability 13: 13461. [Google Scholar] [CrossRef]

- Supari, Supari, and Hendranata Anton. 2022. The Impact of the National Economic Recovery Program and Digitalization on MSME Resilience during the COVID-19 Pandemic: A Case Study of Bank Rakyat Indonesia. Economies 10: 160. [Google Scholar] [CrossRef]

- Szili, Dóra, Tibor Guzsvinecz, and Judit Szűcs. 2022. How Banks Were Chosen and Rated in Hungary before and during the COVID-19 Pandemic. Sustainability 14: 6720. [Google Scholar] [CrossRef]

- Szwajca, Danuta. 2018. Relationship between corporate image and corporate reputation in Polish banking sector. Oeconomia Copernicana 9: 493–509. [Google Scholar] [CrossRef]

- Talatahari, Siamak, Abolfazl Ranjbar, Mohammad Tolouei, and Iman Rahimi. 2022. 6-Multiobjective Charged System Search for Optimum Location of Bank Branch. In Multi-Objective Combinatorial Optimization Problems and Solution Methods. Amsterdam: Elsevier Science, pp. 119–33. [Google Scholar] [CrossRef]

- Tomescu-Dumitrescu, Cornelia. 2020. Management of Human Resources in the Financial-Banking System. Annals-Economy Series 4: 71–76. [Google Scholar]

- Uksumenko, Alena Anatolia, Irina Kuzmicheva, and Olga Yurievna Vorozhbit. 2017. Effective marketing strategy for regional banks. European Research Studies Journal 20: 558–67. [Google Scholar]

- Ünlü, Ulaş, Neşe Yalçın, and Nuri Avşarlıgil. 2022. Analysis of Efficiency and Productivity of Commercial Banks in Turkey Pre- and during COVID-19 with an Integrated MCDM Approach. Mathematics 10: 2300. [Google Scholar] [CrossRef]

- Wang, Tien-Chin, and Tsung-Han Chang. 2007. Application of consistent fuzzy preference relations in predicting the success of knowledge management implementation. European Journal of Operation Research 182: 1313–29. [Google Scholar] [CrossRef]

- Wang, Tien-Chin, Chia-Nan Wang, and Xuan Huynh Nguyen. 2016a. Evaluating the Influence of Criteria to Attract Foreign Direct Investment (FDI) to Develop Supporting Industries in Vietnam by Utilizing Fuzzy Preference Relations. Sustainability 8: 447. [Google Scholar] [CrossRef] [Green Version]

- Wang, Tien-Chin, Hsiu-Chin Hsieh, and Shu-Chen Hsu. 2016b. Predicting the Success of Promoting a Decision-maker’s Judgment by InLinPreRa. Paper presented at 2016 International Conference on Business and Management, Shenzhen, China, 30 June. [Google Scholar]

- Wu, You, Shengqi Wang, Xing Wang, and Zheng Wang. 2022. Application Research of Particle Swarm Algorithm in Bank Human Resource Management. Security and Communication Networks 2022: 8788894. [Google Scholar] [CrossRef]

- Yeung, Ruth, Mureen Brookes, and Levent Altinay. 2016. The hospitality franchise purchase decision-making process. International Journal of Contemporary Hospitality Management 28: 1–20. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Criteria | Objective | Methods | Findings |

|---|---|---|---|

| Headquarters system | Being the first criteria of knowledge management, it was proven by the studies that banks’ headquarters play an important initiative on coping with the financial crisis and pandemic. | Document analysis combined with qualitative and quantitative analysis was applied to the studies, to prevent any bias from either of analyses. |

|

| Human Resources | Through the studies related to human resource management, knowledge management can be strengthened to overcome the problems from COVID-19. | Document analysis combined with qualitative and quantitative analysis was applied to the studies, to prevent any bias from either of analyses. |

|

| Corporate image | Because the importance of the corporate image is indisputable in any organizations, these studies confirmed the positive relationship between knowledge management and the corporate image. | Document analysis combined with qualitative and quantitative analysis was applied to the studies, to prevent any bias from either of analyses. |

|

| Location advantage | Based on the studies associated with the location of banks, it was proven that the location decisions have an influence on the implementation of knowledge management. | Document analysis combined with qualitative and quantitative analysis was applied to the studies, to prevent any bias from either of analyses. |

|

| Innovation and transformation | Exploring these studies involving in innovation, the objective is to construct the relationship between knowledge management and innovation, and the results proved that there were casual relationships between them. | Document analysis combined with qualitative and quantitative analysis was applied to the studies, to prevent any bias from either of analyses. |

|

| Marketing strategy | According to these studies on marketing strategies, combining knowledge management, it’s more probable for banking sector to respond to the impact of COVID-19. | Document analysis combined with qualitative and quantitative analysis was applied to the studies, to prevent any bias from either of analyses. |

|

| Crisis management | Facing the impact of COVID-19, banks needed to pay more attention to the crisis management. Either crisis management or anti-crisis management achieved knowledge management to solve the problems derived from the pandemic. | Document analysis combined with qualitative and quantitative analysis was applied to the studies, to prevent any bias from either of analyses. |

|

| Definition | Intensity of Importance |

|---|---|

| Equally important (EQ) | 1 |

| Weakly important (WK) | 3 |

| Strongly important (ST) | 5 |

| Very strongly important (VS) | 7 |

| Absolutely important (AB) | 9 |

| Intermediate values used to represent a compromise | 2,4,6,8 |

| Definition | Intensity of Importance |

|---|---|

| Fair (F) | 1 |

| High (H) | 3 |

| Very High (VH) | 5 |

| Intermediate values used to represent a compromise | 2,4 |

| C1 | LSLV | LVLA | VS | VS | SW | LVS | ST | VS | EQ | VS | ST | VS | AB | VS | VS | C2 |

| C2 | LST | AV | LVLA | ST | ST | VS | ST | VT | VS | LVS | WK | VT | VS | SW | ST | C3 |

| C3 | VS | AV | AV | EQ | SW | EQ | VS | SW | EQ | VS | ST | ST | WE | LVS | WK | C4 |

| C4 | LVS | LVLA | LSLV | LST | SW | LVLA | WK | LVS | VS | LVS | LVS | LSLV | SW | EQ | LVS | C5 |

| C5 | ELW | AV | LVS | LST | SW | SW | LST | LVS | EQ | LVS | EQ | VT | LVS | EQ | SW | C6 |

| C6 | LSLV | LVLA | LST | LST | LSLV | LAB | WK | VT | LAB | LVS | ST | LVS | ST | WK | LVS | C7 |

| 1.0000 | LSLV | ||||||

| 1.0000 | LST | ||||||

| 1.0000 | VS | ||||||

| 1.0000 | LVS | ||||||

| 1.0000 | ELW | ||||||

| 1.0000 | LSLV | ||||||

| 1.0000 |

| 1.0000 | 1/6 | × | × | × | × | × | |

| × | 1.0000 | 1/5 | × | × | × | × | |

| × | × | 1.0000 | 7 | × | × | × | |

| × | × | × | 1.0000 | 1/7 | × | × | |

| × | × | × | × | 1.0000 | 1/2 | × | |

| × | × | × | × | × | 1.0000 | 1/6 | |

| × | × | × | × | × | × | 1.0000 |

| 0.5000 | 0.0923 | −0.2740 | 0.1688 | −0.2740 | −0.4317 | −0.8394 | |

| 0.9077 | 0.5000 | 0.1338 | 0.5766 | 0.1338 | −0.0240 | −0.4317 | |

| 1.2740 | 0.8662 | 0.5000 | 0.9428 | 0.5000 | 0.3423 | −0.0655 | |

| 0.8312 | 0.4234 | 0.0572 | 0.5000 | 0.0572 | −0.1005 | −0.5083 | |

| 1.2740 | 0.8662 | 0.5000 | 0.9428 | 0.5000 | 0.3423 | −0.0655 | |

| 1.4317 | 1.0240 | 0.6577 | 1.1005 | 0.6577 | 0.5000 | 0.0923 | |

| 1.8394 | 1.4317 | 1.0655 | 1.5083 | 1.0655 | 0.9077 | 0.5000 |

| 0.5000 | 0.3478 | 0.2111 | 0.3764 | 0.2111 | 0.1522 | 0.0000 | |

| 0.6522 | 0.5000 | 0.3633 | 0.5286 | 0.3633 | 0.3044 | 0.1522 | |

| 0.7889 | 0.6367 | 0.5000 | 0.6653 | 0.5000 | 0.4411 | 0.2889 | |

| 0.6236 | 0.4714 | 0.3347 | 0.5000 | 0.3347 | 0.2758 | 0.1236 | |

| 0.7889 | 0.6367 | 0.5000 | 0.6653 | 0.5000 | 0.4411 | 0.2889 | |

| 0.8478 | 0.6956 | 0.5589 | 0.7242 | 0.5589 | 0.5000 | 0.3478 | |

| 1.0000 | 0.8478 | 0.7111 | 0.8764 | 0.7111 | 0.6522 | 0.5000 |

| E | |||||||

|---|---|---|---|---|---|---|---|

| 0.5000 | 0.5896 | 0.7114 | 0.8127 | 0.7108 | 0.6999 | 0.6411 | |

| 0.4104 | 0.5000 | 0.6219 | 0.7231 | 0.6212 | 0.6103 | 0.5515 | |

| 0.2886 | 0.3781 | 0.5000 | 0.6013 | 0.4993 | 0.4885 | 0.4297 | |

| 0.1873 | 0.2769 | 0.3987 | 0.5000 | 0.3981 | 0.3872 | 0.3284 | |

| 0.2892 | 0.3788 | 0.5007 | 0.6019 | 0.5000 | 0.4891 | 0.4303 | |

| 0.3001 | 0.3897 | 0.5115 | 0.6128 | 0.5109 | 0.5000 | 0.4412 | |

| 0.3589 | 0.4485 | 0.5703 | 0.6716 | 0.5697 | 0.5588 | 0.5000 | |

| Total | 2.3345 | 2.9614 | 3.8146 | 4.5234 | 3.8100 | 3.7338 | 3.3222 |

| E | Total | Weight | Ranking | |||||||

|---|---|---|---|---|---|---|---|---|---|---|

| 0.2142 | 0.1991 | 0.1865 | 0.1797 | 0.1866 | 0.1874 | 0.1930 | 1.3464 | 0.1861 | 1 | |

| 0.1758 | 0.1688 | 0.2100 | 0.1599 | 0.1631 | 0.1635 | 0.1660 | 1.2070 | 0.1668 | 2 | |

| 0.1236 | 0.1277 | 0.1688 | 0.1329 | 0.1311 | 0.1308 | 0.1293 | 0.9442 | 0.1305 | 6 | |

| 0.0802 | 0.0935 | 0.1346 | 0.1105 | 0.1045 | 0.1037 | 0.0988 | 0.7259 | 0.1003 | 7 | |

| 0.1239 | 0.1279 | 0.1691 | 0.1331 | 0.1312 | 0.1310 | 0.1295 | 0.9457 | 0.1307 | 5 | |

| 0.1285 | 0.1316 | 0.1727 | 0.1355 | 0.1341 | 0.1339 | 0.1328 | 0.9691 | 0.1340 | 4 | |

| 0.1537 | 0.1514 | 0.1926 | 0.1485 | 0.1495 | 0.1497 | 0.1505 | 1.0959 | 0.1515 | 3 | |

| Total | 1.0000 | 1.0000 | 1.0000 | 1.0000 | 1.0000 | 1.0000 | 1.0000 | 7.2344 | 1.0000 |

| F | F | F | F | F | F | F | F | F | F | F | F | F | F | F | ||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| C1 | s | HF | VHG | VH | H | H | H | H | H | F | VHG | H | VHG | VH | VHG | VHG |

| C2 | s | VHG | VHG | H | F | H | VHG | VHG | H | VHG | HF | LHF | VHG | VH | H | VHG |

| C3 | s | H | VHG | VH | LH | H | LHF | H | HF | LVH | VHG | H | H | H | H | H |

| C4 | s | F | VHG | HF | VHG | VHG | F | F | H | VHG | F | LHF | H | VHG | LH | H |

| C5 | s | VHG | LHF | H | F | LHF | H | H | VHG | HF | F | VHG | VHG | H | HF | H |

| C6 | s | VHG | H | H | H | H | F | VHG | VHG | VHG | VHG | VHG | H | VHG | HF | H |

| C7 | s | VH | H | VHG | F | HF | H | H | HF | LVHG | VHG | H | VH | F | LVHG | VHG |

| F | F | F | F | F | F | F | F | F | F | F | F | F | F | F | Total | Average | ||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| C1 | s | 0.7153 | 0.9307 | 1.0000 | 0.8413 | 0.8413 | 0.8413 | 0.8413 | 0.8413 | 0.5000 | 0.9307 | 0.8413 | 0.9307 | 1.0000 | 0.9307 | 0.9307 | 12.9165 | 0.8611 |

| C2 | s | 0.9307 | 0.9307 | 0.8413 | 0.5000 | 0.8413 | 0.9307 | 0.9307 | 0.8413 | 0.9307 | 0.7153 | 0.2847 | 0.9307 | 1.0000 | 0.8413 | 0.9307 | 12.3799 | 0.8253 |

| C3 | s | 0.8413 | 0.9307 | 1.0000 | 0.1587 | 0.8413 | 0.2847 | 0.8413 | 0.7153 | 0.0000 | 0.9307 | 0.8413 | 0.8413 | 0.8413 | 0.8413 | 0.8413 | 10.7505 | 0.7167 |

| C4 | s | 0.5000 | 0.9307 | 0.7153 | 0.9307 | 0.9307 | 0.5000 | 0.5000 | 0.8413 | 0.9307 | 0.5000 | 0.2847 | 0.8413 | 0.9307 | 0.1587 | 0.8413 | 10.3360 | 0.6891 |

| C5 | s | 0.9307 | 0.2847 | 0.8413 | 0.5000 | 0.2847 | 0.8413 | 0.8413 | 0.9307 | 0.7153 | 0.5000 | 0.9307 | 0.9307 | 0.8413 | 0.7153 | 0.8413 | 10.9292 | 0.7286 |

| C6 | s | 0.9307 | 0.8413 | 0.8413 | 0.8413 | 0.8413 | 0.5000 | 0.9307 | 0.9307 | 0.9307 | 0.9307 | 0.9307 | 0.8413 | 0.9307 | 0.7153 | 0.8413 | 12.7779 | 0.8519 |

| C7 | s | 1.0000 | 0.8413 | 0.9307 | 0.5000 | 0.7153 | 0.8413 | 0.8413 | 0.7153 | 0.0693 | 0.9307 | 0.8413 | 1.0000 | 0.5000 | 0.0693 | 0.9307 | 10.7266 | 0.7151 |

| s | s | s | s | s | s | s | s | s | s | s | s | s | s | s | Total | Average | ||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| C1 | F | 0.2847 | 0.0693 | 0.0000 | 0.1587 | 0.1587 | 0.1587 | 0.1587 | 0.1587 | 0.5000 | 0.0693 | 0.1587 | 0.0693 | 0.0000 | 0.0693 | 0.0693 | 2.0835 | 0.1389 |

| C2 | F | 0.0693 | 0.0693 | 0.1587 | 0.5000 | 0.1587 | 0.0693 | 0.0693 | 0.1587 | 0.0693 | 0.2847 | 0.7153 | 0.0693 | 0.0000 | 0.1587 | 0.0693 | 2.6201 | 0.1747 |

| C3 | F | 0.1587 | 0.0693 | 0.0000 | 0.8413 | 0.1587 | 0.7153 | 0.1587 | 0.2847 | 1.0000 | 0.0693 | 0.1587 | 0.1587 | 0.1587 | 0.1587 | 0.1587 | 4.2495 | 0.2833 |

| C4 | F | 0.5000 | 0.0693 | 0.2847 | 0.0693 | 0.0693 | 0.5000 | 0.5000 | 0.1587 | 0.0693 | 0.5000 | 0.7153 | 0.1587 | 0.0693 | 0.8413 | 0.1587 | 4.6640 | 0.3109 |

| C5 | F | 0.0693 | 0.7153 | 0.1587 | 0.5000 | 0.7153 | 0.1587 | 0.1587 | 0.0693 | 0.2847 | 0.5000 | 0.0693 | 0.0693 | 0.1587 | 0.2847 | 0.1587 | 4.0708 | 0.2714 |

| C6 | F | 0.0693 | 0.1587 | 0.1587 | 0.1587 | 0.1587 | 0.5000 | 0.0693 | 0.0693 | 0.0693 | 0.0693 | 0.0693 | 0.1587 | 0.0693 | 0.2847 | 0.1587 | 2.2221 | 0.1481 |

| C7 | F | 0.0000 | 0.1587 | 0.0693 | 0.5000 | 0.2847 | 0.1587 | 0.1587 | 0.2847 | 0.9307 | 0.0693 | 0.1587 | 0.0000 | 0.5000 | 0.9307 | 0.0693 | 4.2734 | 0.2849 |

| Success | Failure | Total | Average | ||

|---|---|---|---|---|---|

| Success | 0.7826 | 0.6327 | 1.4152 | 0.7076 | |

| Failure | 0.2174 | 0.3673 | 0.5848 | 0.2924 | |

| Success | 0.7411 | 0.6227 | 1.3638 | 0.6819 | |

| Failure | 0.2589 | 0.3773 | 0.6362 | 0.3181 | |

| Success | 0.6383 | 0.5891 | 1.2274 | 0.6137 | |

| Failure | 0.3617 | 0.4109 | 0.7726 | 0.3863 | |

| Success | 0.6166 | 0.5795 | 1.1961 | 0.5980 | |

| Failure | 0.3834 | 0.4205 | 0.8039 | 0.4020 | |

| Success | 0.6482 | 0.5930 | 1.2412 | 0.6206 | |

| Failure | 0.3518 | 0.4070 | 0.7588 | 0.3794 | |

| Success | 0.7714 | 0.6301 | 1.4016 | 0.7008 | |

| Failure | 0.2286 | 0.3699 | 0.5984 | 0.2992 | |

| Success | 0.6370 | 0.5885 | 1.2255 | 0.6128 | |

| Failure | 0.3630 | 0.4115 | 0.7745 | 0.3872 |

| Prediction Probability | ||||||||

|---|---|---|---|---|---|---|---|---|

| Rank | 1 | 2 | 6 | 7 | 5 | 4 | 3 | |

| priority Weight | 0.1861 | 0.1668 | 0.1305 | 0.1003 | 0.1307 | 0.1340 | 0.1515 | 1.0000 |

| Success | 0.7076 | 0.6819 | 0.6137 | 0.5980 | 0.6206 | 0.7008 | 0.6128 | 0.6534 |

| Failure | 0.2924 | 0.3181 | 0.3863 | 0.4020 | 0.3794 | 0.2992 | 0.3872 | 0.3466 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Chang, C.-H.; Chang, W.-H.; Hsieh, H.-C.; Shih, Y.-Y. An Alternative to Coping with COVID-19—Knowledge Management Applied to the Banking Industry in Taiwan. J. Risk Financial Manag. 2022, 15, 405. https://doi.org/10.3390/jrfm15090405

Chang C-H, Chang W-H, Hsieh H-C, Shih Y-Y. An Alternative to Coping with COVID-19—Knowledge Management Applied to the Banking Industry in Taiwan. Journal of Risk and Financial Management. 2022; 15(9):405. https://doi.org/10.3390/jrfm15090405

Chicago/Turabian StyleChang, Chih-Hsiung, Wu-Hua Chang, Hsiu-Chin Hsieh, and Yi-Yu Shih. 2022. "An Alternative to Coping with COVID-19—Knowledge Management Applied to the Banking Industry in Taiwan" Journal of Risk and Financial Management 15, no. 9: 405. https://doi.org/10.3390/jrfm15090405