1. Introduction

Scale-driven economic growth has led to excessive energy consumption and pollution emissions [

1,

2]. Problems, such as over-exploitation of resources, environmental pollution, and abnormal climate, have become huge obstacles to sustainable economic development [

3,

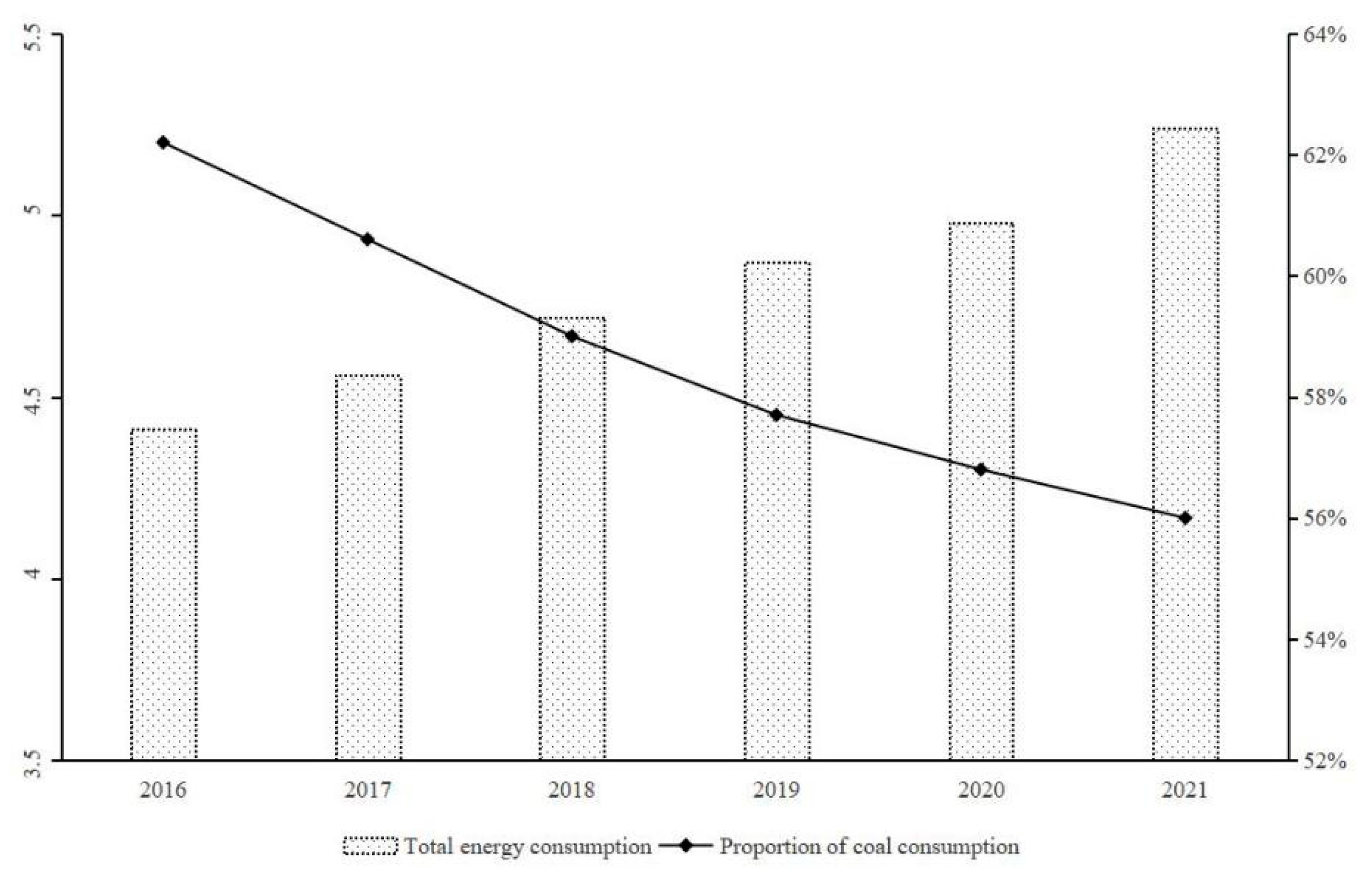

4]. According to the statistics released by the National Bureau of Statistics of China, in 2021, China’s total energy consumption was 5.24 billion tons of standard coal, an increase of 5.2% over the previous year (

Figure 1). Coal consumption accounted for 56.0% of the total energy consumption. China is still the world’s largest coal consumer and greenhouse gas emitter. According to calculations based on China Emission Accounts and Datasets (CEADs,

https://www.ceads.net.cn (accessed on 10 September 2022)), in 2021, China’s total carbon emissions exceeded 10.3 billion tons, accounting for about 27% of the total global carbon emissions, close to the sum of the United States, the European Union, and Japan. The task of achieving carbon neutrality by 2060 is extremely arduous. In recent years, China has rapidly developed green finance with carbon reduction, environmental protection, and sustainable development. According to the statistical data of the People’s Bank of China, by the end of 2021, the balance of China’s green loans was CNY 15.9 trillion, an increase of 33%, ranking first in the world. As an important policy tool of modern environmental governance, green finance not only has the characteristics of market-oriented environmental regulation but also has the function of resource allocation of the financial sector. Promoting the development of green finance can reduce the credit rationing of ‘two high industries’ (high energy-consuming and high-emissions), improve the industrial structure, and accelerate the transformation of production mode to cleaner production [

5,

6]. The goal of environmental governance is to change the behavior choice of enterprises. Only when more enterprises take the initiative and are willing to undertake ESG can carbon neutrality be finally achieved.

As the primary green financial tool, green credit has gradually attracted the attention of Chinese government departments. In 2012, the China Banking Regulatory Commission issued the “notice on printing and distributing green credit guidelines”, which put forward more explicit and specific requirements for the banking industry, from green credit organization management, process management, internal control, and information disclosure. It emphasized that financial institutions should take energy conservation, emission reduction, environmental protection, and other factors as important bases for credit decisions, not grant credit to customers that may bring risks to the environment and society, and increase credit support for pollution control and resource conservation projects. This policy provides an excellent opportunity to identify the policy effect of green finance. The main reason is that data availability makes it difficult to accurately measure green bonds and stocks. With green credit gradually becoming China’s most important green financial tool, it is reasonable to use it as a proxy variable of green finance.

Under the traditional financial framework, there is a contradiction between the corporate ESG and the profit maximization goal [

7]. Enterprises that do not undertake or rarely undertake ESG may achieve better market performance [

8,

9]. Due to the lack of assessment of the enterprise’s environmental level and supervision of the investment flow, the advantages of green enterprises in the traditional credit market are not obvious. The green finance policy requires enterprises to provide environmental information, which can alleviate the adverse selection and moral hazard caused by information asymmetry [

10]. When there are no external constraints, enterprises mainly consider using limited resources to maximize profits and generally not be motivated to fulfill ESG. The implementation of the green finance policy enables the financial sector to incorporate environmental factors into enterprise credit granting and project management and grant more credit resources to green projects. However, due to the asymmetry of information in the capital market, it is difficult to observe the actual green level of enterprises. Therefore, enterprises must send signals to financial institutions through their green behaviors to ensure that they have an advantage in credit activities. Among them, the most convenient way is to undertake ESG or carry out environmental information disclosure [

11,

12] and send “green signals” to financial institutions in exchange for favorable conditions in the credit market, thus green finance can more effectively encourage financial institutions and enterprises to assume more social responsibilities. However, some studies believe that the effectiveness of green finance depends on environmental regulation and the response of enterprises to policies, and the willingness of enterprises to assume social responsibility directly impacts the implementation effect of policies [

13]. Therefore, it is important evidence to evaluate the micro effect of green finance to explore whether green finance can have a practical impact on corporate behavior, analyze the regulatory effect of corporate behavior on green finance policy, and clarify the specific ways of green finance affecting corporate ESG behavior [

14].

3. Materials and Research Design

3.1. Materials

This paper takes China’s A-share listed companies from 2006 to 2020 as the sample. The data sources mainly include the following parts: data of listed companies, the basic information, financial statements, and other data of all listed companies are obtained from the Chinese Research Data Services Platform (CNRDS), and relevant indicators such as control variables and financing costs are calculated and eliminate the data with missing severe financial indicators. Data of industrial pollution emission is obtained from China Environmental Statistics Yearbook over the years. After matching the above data, the data of 1196 listed companies were finally obtained.

3.2. Modeling and Variable Definition

Under the modern environmental governance system, the behavior choice of enterprises can directly change the industrial structure and production mode and ultimately determine the implementation effect of environmental regulation. Green credit can encourage enterprises to reduce pollution emissions and improve environmental and social governance. For example, in 2014, China formulated “The Key Assessment Indicators for the Implementation of Green Credit,” which divided the production and operation activities and industry scope of enterprises that pollute the environment, providing a basis for the banking industry to carry out the customer selection and risk management of green credit. The policy impact of green credit runs through the whole process of enterprise production. In the financing stage, the credit quota is inclined to green enterprises. In the production process, financial institutions can carry out post-loan management according to the green credit policy to promote the green production of enterprises. After the production is completed, the green audit can be carried out further. Therefore, compared with traditional environmental regulation, green credit policy has a more significant structural effect and a more complete environmental and social governance cycle.

This paper uses the ‘notice on printing and distributing green credit guidelines’ issued in 2012 as a quasi-natural experiment. A continuous difference-in-differences (DID) method has been used to investigate the impact of green finance, especially green credit policies, on corporate ESG [

48]. The definition of treatment group and control group in existing research mainly divides enterprises into high-pollution enterprises and low-pollution enterprises. It compares the differences between groups, which is insufficient to identify treatment groups. This study uses the restrictive industries of green credit policy to define the setting method of experimental groups.

On the one hand, it excludes the non-restrictive industries from being defined as experimental groups. On the other hand, it also depicts the size of the experimental groups affected by the policy. The basic idea of the DID model is to identify the average processing effect of the policy by using the difference in the intensity of the impact of the policy between the experimental group and the control group. The model is as follows:

where

means enterprise,

means industry, and

means year. The dependent variable

represents the corporate ESG behavior, and

is the main independent variables to measure the extent to which the experimental group is affected by the green finance policy.

is a virtual variable that distinguishes whether the green finance policy restricts the industry, and

represents other control variables. In addition, the fixed effect of individual enterprise, industry effect, and time effect are added to the model, and

represents the interference term which is assumed to be normally distributed at zero mean value [

49,

50,

51] nd constant variance [

52,

53,

54].

3.2.1. The Dependent Variable

This paper mainly investigates the impact of green finance, represented by green credit policy, on two kinds of corporate ESG behaviors. Green technology (GT) is measured by the indicator ‘whether the enterprise develops or applies innovative products or technologies beneficial to the environment. If this variable takes 1, it indicates that the enterprise has allocated corresponding funds for purchasing environmentally beneficial technologies and product R&D. Pollution emission (PE) is measured by the indicator “whether the enterprise has taken measures to reduce the emission of industrial solid waste, industrial waste gas, industrial smoke, and dust discharge and industrial wastewater discharge”, which reflects the treatment of pollutant emissions by the enterprise.

3.2.2. Main Independent Variable

Industry is a sub item of traditional DID. If the enterprise is a green credit-restricted industry and the sample year is 2012 or later, take 1. is the cross-term of and the extent to which the green credit policy affects the enterprise. Its estimated coefficient is the policy effect. > 0 indicates that green credit policies promote the improvement of corporate environmental and social governance, < 0 means that policies inhibit the improvement of corporate environmental and social governance, and = 0 indicates that the policy effect is not obvious. It mainly measures the degree of impact by the green credit policy. It uses the weighted average of pollutant emission reduction levels of various industries to measure the intensity of the industry affected by the policy. This paper selects four kinds of pollutants: industrial solid waste, industrial waste gas, industrial smoke, and dust discharge and industrial wastewater discharge, and the overall change of pollutant discharge in each industry is determined by standardized methods. The main sources of industrial pollutant data are the ‘China Environmental Statistics Yearbook’ and ‘China Statistical Yearbook’ over the years. The industries restricted by green credit policies match those of listed companies.

3.2.3. The Control Variable

This paper introduces a series of control variables to control other characteristics that affect corporate ESG. The size of the enterprise (Size) is measured by the natural logarithm of total annual assets. The asset liability ratio (Lev) is the total liabilities divided by total assets at the end of the year. ROA is the net profit divided by the average balance of total assets. The cash flow ratio (Cashflow) is the cash flow generated from operating activities divided by total assets. The increase rate of primary business revenue (Growth) is the ratio of this year’s operating revenue to the previous year’s operating revenue minus 1. The enterprise nature (SOE) is the ownership nature of the enterprise; the state-owned enterprise takes 1.

3.3. Descriptive Statistics

Table 1 shows the descriptive statistical results for the above variables. To avoid the heteroscedastic problem and narrow the intra-group and inter-group differences of variables, the variable of enterprise size is processed by logarithmic transformation.

{kind=link}

{kind=link}