How to Promote Low-Carbon Economic Development? A Comprehensive Assessment of Carbon Tax Policy in China

Abstract

:1. Introduction

2. Literature Review

2.1. Research on Influencing Factors of Carbon Emissions

2.2. Research on Carbon Emission Mechanism

2.3. Research on CGE Model of Carbon Tax

3. Methodology and Data

3.1. Description of the CGE Model

3.2. Data Sources

3.2.1. Source of Basic Data

3.2.2. Parameter Calibration

4. Scenarios Setting

4.1. Carbon Tax Design

4.2. Simulation Scenario Design

4.2.1. Carbon Emission and Energy Simulation Analysis

4.2.2. Carbon Tax Recycling Simulation Analysis

5. Results

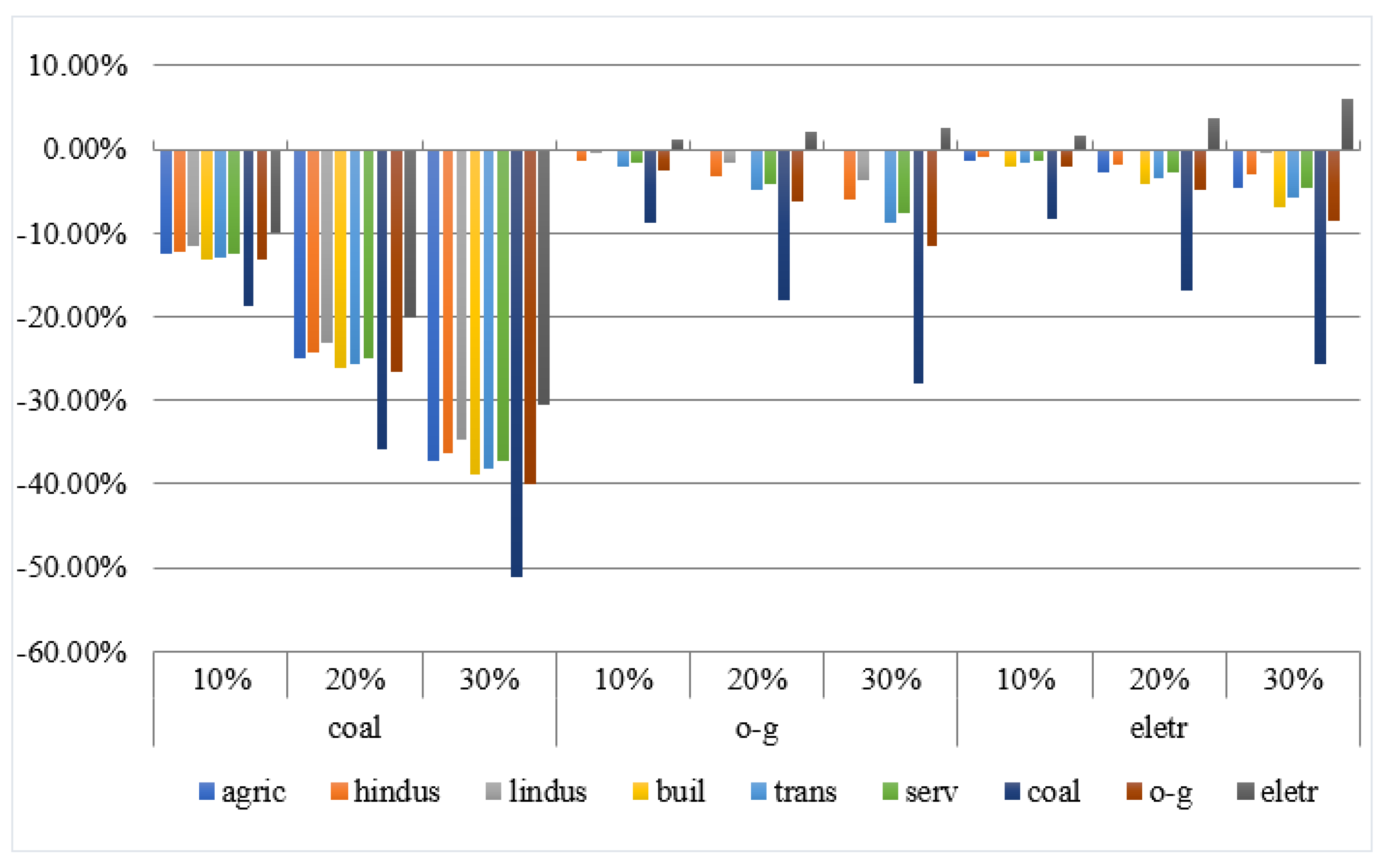

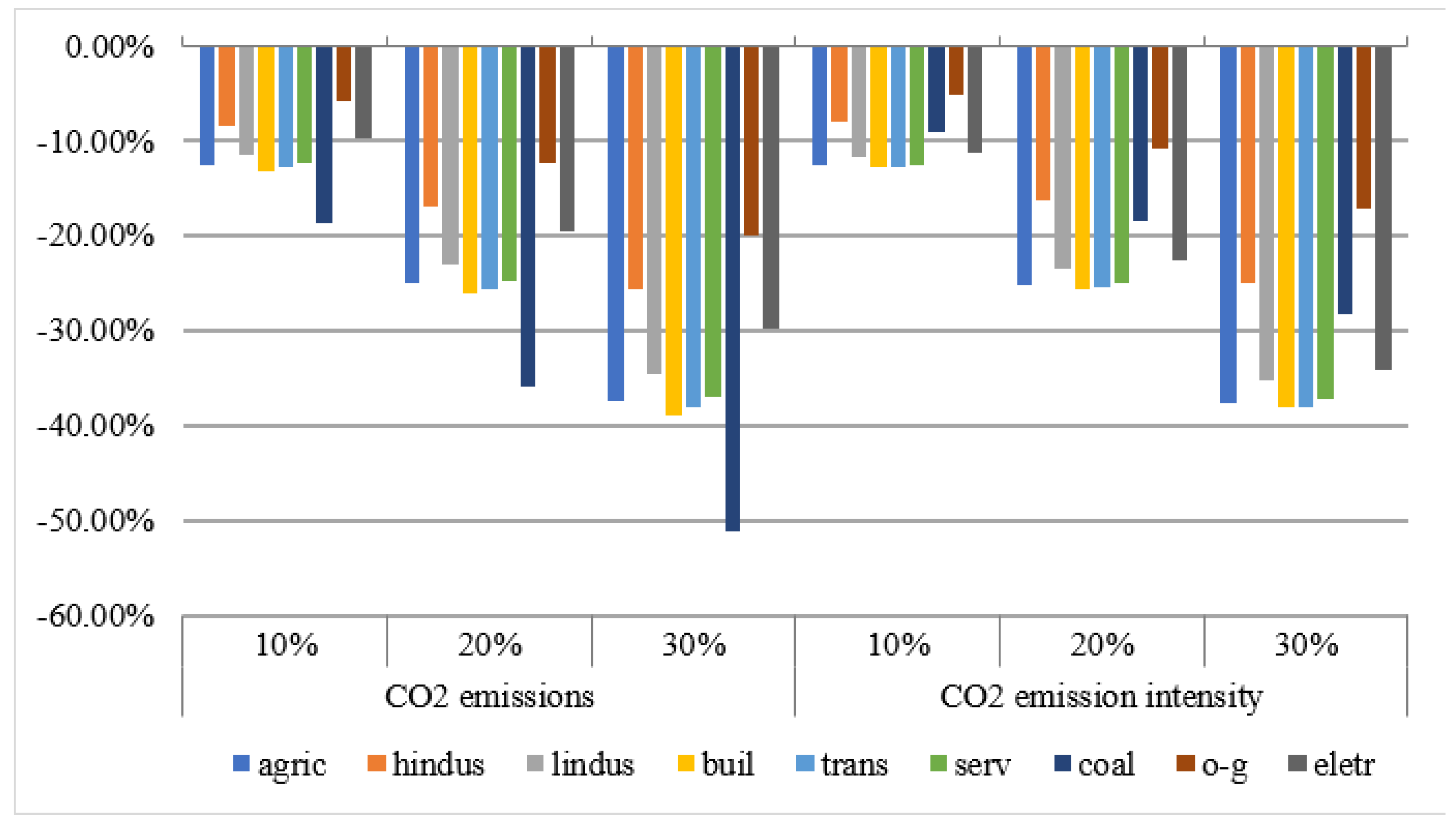

5.1. Energy and Carbon Emissions Simulation Results

5.1.1. Energy Effect

5.1.2. Sectoral Effects

5.1.3. Macroeconomic Variables Effects

5.2. Carbon Tax Recycle Simulation Results

5.2.1. The Impact on Institutions

5.2.2. The Impact on the Economy

5.2.3. The Impact on Carbon Emissions

6. Discussion and Conclusions

6.1. Discussion

6.2. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Xiao, J.; Zhen, Z.; Tian, L.; Su, B.; Chen, H.; Zhu, A. Green Behavior towards Low-Carbon Society: Theory, Measurement and Action. J. Clean. Prod. 2020, 278, 123765. [Google Scholar] [CrossRef]

- Bao, J.-Q.; Miao, Y.; Chen, F. Low Carbon Economy: Revolution in the Way of Human Economic Development. China Ind. Econ. 2008, 4, 017. [Google Scholar]

- Ji, X.; Zhang, Y.; Mirza, N.; Umar, M.; Rizvi, S.K.A. The impact of carbon neutrality on the investment performance: Evidence from the equity mutual funds in BRICS. J. Environ. Manag. 2021, 297, 113228. [Google Scholar] [CrossRef] [PubMed]

- Shi, Y.; Han, B.; Zafar, M.W.; Wei, Z. Uncovering the driving forces of carbon dioxide emissions in Chinese manufacturing industry: An intersectoral analysis. Environ. Sci. Pollut. Res. 2019, 26, 31434–31448. [Google Scholar] [CrossRef]

- Bouscayrol, A.; Chevallier, L.; Cimetiere, X.; Clenet, S.; Lemaire-Semail, B. EPE’13 ECCE Europe, a carbon-neutral conference. EPE J. 2018, 28, 43–48. [Google Scholar] [CrossRef]

- Usama, A.; Kraslawski, A.; Huiskonen, J. Governing interfirm relationships for social sustainability: The relationship between governance mechanisms, sustainable collaboration, and cultural intelligence. Sustainability 2018, 10, 4473. [Google Scholar]

- Sun, C.; Ma, T.; Ouyang, X.; Wang, R. Does service trade globalization promote trade and low-carbon globalization? Evidence from 30 countries. Emerg. Mark. Financ. Trade. 2021, 57, 1455–1473. [Google Scholar] [CrossRef]

- Ulucak, R.; Kassouri, Y. An assessment of the environmental sustainability corridor: Investigating the non-linear effects of environmental taxation on CO2 emissions. Sustain. Dev. 2020, 28, 1010–1018. [Google Scholar] [CrossRef]

- Wang, H.; Chen, Z.; Wu, X.; Nie, X. Can a carbon trading system promote the transformation of a low-carbon economy under the framework of the porter hypothesis? Empirical analysis based on the PSM-DID method. Energy Policy 2019, 129, 930–938. [Google Scholar] [CrossRef]

- Bruvoll, A.; Larsen, B.M. Greenhouse gas emissions in Norway: Do carbon taxes work? Energy Policy 2004, 32, 493–505. [Google Scholar] [CrossRef] [Green Version]

- Floros, N.; Vlachou, A. Energy demand and energy-related CO2 emissions in Greek manufacturing: Assessing the impact of a carbon tax. Energy Econ. 2005, 27, 387–413. [Google Scholar] [CrossRef]

- Jia, L.; Jinyu, B.; Yi, D.; Xiaohong, C.; Xiang, L. Impact of energy structure on carbon emission and economy of China in the scenario of carbon taxation. Sci. Total Environ. 2020, 762, 143093. [Google Scholar]

- Metcalf, G.E. On the economics of a carbon tax for the United States. Brook. Pap. Econ. Act. 2019, 2019, 405–484. [Google Scholar] [CrossRef]

- Burtraw, D.; Krupnick, A.; Palmer, K.; Paul, A.; Toman, M.; Bloyd, C. Ancillary benefits of reduced air pollution in the U.S. from moderate greenhouse gas mitigation policies in the electricity sector. J. Environ. Econ. Manag. 2003, 45, 650–673. [Google Scholar] [CrossRef]

- Meng, S.; Siriwardana, M.; McNeill, J. The environmental and economic impact of the carbon tax in Australia. Environ. Resour. Econ. 2013, 54, 313–332. [Google Scholar] [CrossRef]

- Tietenberg, T.H. Reflections—Carbon pricing in practice. Rev. Environ. Econ. Policy 2013, 7, 313–329. [Google Scholar] [CrossRef]

- Wang, W.; You, X.; Liu, K.; Wu, Y.J.; You, D. Implementation of a Multi-Agent Carbon Emission Reduction Strategy under the Chinese Dual Governance System: An Evolutionary Game Theoretical Approach. Int. J. Environ. Res. Public Health 2020, 17, 8463. [Google Scholar] [CrossRef] [PubMed]

- Yamazaki, A. Jobs and climate policy: Evidence from British Columbia’s revenue-neutral carbon tax. J. Environ. Econ. Manag. 2017, 83, 197–216. [Google Scholar] [CrossRef]

- Meng, X. Will Australian carbon tax affect the resources boom? Results from a CGE model. Nat. Resour. Res. 2012, 21, 495–507. [Google Scholar] [CrossRef]

- Mohammed, T. A CGE analysis of the macroeconomic effects of carbon dioxide emission reduction on the Algerian economy. Springer Proc. Bus. Econ. 2017, 1–20. [Google Scholar] [CrossRef]

- Xu, X.; Xu, X.F.; Chen, Q.; Che, Y. The impact on regional “resource curse” by coal resource tax reform in China—A dynamic CGE appraisal. Resour. Policy 2015, 45, 277–289. [Google Scholar] [CrossRef]

- Sofia, D.; Gioiella, F.; Lotrecchiano, N.; Giuliano, A. Mitigation strategies for reducing air pollution. Environ. Sci. Pollut. Res. 2020, 27, 19226–19235. [Google Scholar] [CrossRef]

- Jakeman, G.; Hester, S.; Woffenden, K.; Fisher, B.S. Kyoto protocol: The first commitment period and beyond. Aust. Commod. 2002, 9, 176–197. [Google Scholar]

- Kutlu, L. Greenhouse Gas Emission Efficiencies of World Countries. Int. J. Environ. Res. Public Health 2020, 17, 8771. [Google Scholar] [CrossRef] [PubMed]

- Settimo, G.; Avino, P. The Dichotomy between Indoor Air Quality and Energy Efficiency in light of the Onset of the COVID-19 Pandemic. Atmosphere 2021, 12, 791. [Google Scholar] [CrossRef]

- Pearce, D. The Role of Carbon Taxes in Adjusting to Global Warming. The Economic Journal. 1991, 101(407), 938. [Google Scholar] [CrossRef]

- Chikaire, J.; Nwakwasi, R.N.; Anyoha, N.O.; Nnadi, F.N. Short note potential impacts of climate change on African agriculture. Int. J. Nat. Appl. Sci. 2010, 6, 493–496. [Google Scholar]

- Hao, F.; van Brown, B.L. An analysis of environmental and economic impacts of fossil fuel production in the U.S. from 2001 to 2015. Soc. Nat. Resour. 2018, 32, 693–708. [Google Scholar] [CrossRef]

- Pearce, A.; Stilwell, F. ‘Green-collar’ jobs: Employment impacts of climate change policies. J. Aust. Political Econ. 2008, 62, 120–138. [Google Scholar]

- Awan, U.; Kraslawski, A.; Huiskonen, J. Progress from Blue to the Green World: Multilevel Governance for Pollution Prevention Planning and Sustainability. Semant. Sch. 2019. [Google Scholar]

- Zhao, Y.; Zhang, Z.; Wang, S.; Wang, S. CO2 emissions embodied in China’s foreign trade: An investigation from the perspective of global vertical specialization. China World Econ. 2014, 22, 102–120. [Google Scholar] [CrossRef]

- Yoichi, K. Impact of Carbon Dioxide Emission on GNP Growth: Interpretation of Proposed Scenarios; Presentation to the Energy and Industry Subgroup, Response Strategies Working Group; IPCC: Paris, France, 1989. [Google Scholar]

- Ang, B.W.; Liu, F.L. A new energy decomposition method: Perfect in decomposition and consistent in aggregation. Energy 2001, 26, 537–548. [Google Scholar] [CrossRef]

- Liaskas, K.; Mavrotas, G.; Mandaraka, M.; Diakoulaki, D. Decomposition of industrial CO2 emissions: The Case of European Union. Energy Econ. 2000, 22, 383–394. [Google Scholar] [CrossRef]

- Zhang, M.; Mu, H.; Ning, Y. Accounting for energy-related CO2 emission in China, 1991–2006. Energy Policy 2009, 37, 767–773. [Google Scholar] [CrossRef]

- Schipper, L.; Murtishaw, S.; Khrushch, M.; Ting, M.; Karbuz, S.; Unander, F. Carbon emissions from manufacturing energy use in 13 IEA countries: Long-term trends through 1995. Energy Policy 2001, 29, 667–688. [Google Scholar] [CrossRef]

- Davis, W.B.; Sanstad, A.H.; Koomey, J.G. Contributions of weather and fuel mix to recent declines in U.S. energy and carbon intensity. Energy Econ. 2003, 25, 375–396. [Google Scholar] [CrossRef] [Green Version]

- Haites, E. Carbon taxes and greenhouse gas emissions trading systems: What have we learned? Clim. Policy 2018, 18, 955–966. [Google Scholar] [CrossRef] [Green Version]

- Lee, C.F.; Lin, S.J.; Lewis, C.; Chang, Y.F. Effects of carbon taxes on different industries by fuzzy goal programming: A case study of the petrochemical-related industries, Taiwan. Energy Policy 2007, 35, 4051–4058. [Google Scholar] [CrossRef]

- Newell, R.G.; Pizer, W.A. Regulating stock externalities under uncertainty. J. Environ. Econ. Manag. 2003, 45, 416–432. [Google Scholar] [CrossRef] [Green Version]

- Avi-Yonah, R.S.; Uhlmann, D.M. Combating global climate change: Why a carbon tax is a better response to global warming than cap and trade. Stanf. Environ. Law J. 2009, 28, 3–50. [Google Scholar] [CrossRef] [Green Version]

- Stram, B.N. A new strategic plan for a carbon tax. Energy Policy 2014, 73, 519–523. [Google Scholar] [CrossRef] [Green Version]

- Orlov, A.; Grethe, H.; McDonald, S. Carbon taxation in Russia: Prospects for a double dividend and improved energy efficiency. Energy Econ. 2013, 37, 128–140. [Google Scholar] [CrossRef] [Green Version]

- Dissou, Y.; Karnizova, L. Emissions cap or emissions tax? A multi-sector business cycle analysis. J. Environ. Econ. Manag. 2016, 79, 169–188. [Google Scholar] [CrossRef] [Green Version]

- Wittneben, B.B.F. Exxon is right: Let us re-examine our choice for a cap-and-trade system over a carbon tax. Energy Policy 2009, 37, 2462–2464. [Google Scholar] [CrossRef]

- Timilsina, G.R.; Shrestha, R.M. General equilibrium analysis of economic and environmental effects of carbon tax in a developing country: Case of Thailand. Environ. Econ. Policy Stud. 2002, 5, 179–211. [Google Scholar] [CrossRef]

- Garbaccio, R.F.; Ho, M.S.; Jorgenson, D.W. Why Has the Energy-Output Ratio Fallen in China? Energy J. 1999, 20, 63–91. [Google Scholar] [CrossRef] [Green Version]

- Shrestha, R.M.; Marpaung, C.O.P. Supply- and demand-side effects of carbon tax in the Indonesian power sector: An integrated resource planning analysis. Energy Policy 1999, 27, 185–194. [Google Scholar] [CrossRef]

- Wissema, W.; Dellink, R. AGE analysis of the impact of a carbon energy tax on the Irish economy. Ecol. Econ. 2007, 61, 671–683. [Google Scholar] [CrossRef]

- Allan, G.; Lecca, P.; McGregor, P.; Swales, K. The economic and environmental impact of a carbon tax for Scotland: A computable general equilibrium analysis. Ecol. Econ. 2014, 100, 40–50. [Google Scholar] [CrossRef] [Green Version]

- Lin, B.; Jia, Z. The energy, environmental and economic impacts of carbon tax rate and taxation industry: A CGE based study in China. Energy 2018, 159, 558–568. [Google Scholar] [CrossRef]

- Fu, Y.; Huang, G.; Liu, L.; Zhai, M. A factorial CGE model for analyzing the impacts of stepped carbon tax on Chinese economy and carbon emission. Sci. Total Environ. 2021, 759, 143512. [Google Scholar] [CrossRef]

- Paroussos, L.; Fragkos, P.; Capros, P.; Fragkiadakis, K. Assessment of carbon leakage through the industry channel: The E.U. perspective. Technol. Forecast. Soc. Chang. 2015, 90, 204–219. [Google Scholar] [CrossRef]

- Lu, Y.; Liu, Y.; Zhou, M. Rebound effect of improved energy efficiency for different energy types: A general equilibrium analysis for China. Energy Econ. 2017, 62, 248–256. [Google Scholar] [CrossRef] [Green Version]

- Zhao, Y.; Li, H.; Xiao, Y.; Liu, Y.; Cao, Y.; Zhang, Z.; Wang, S.; Zhang, Y.; Ahmad, A. Scenario analysis of the carbon pricing policy in China’s power sector through 2050: Based on an improved CGE model. Ecol. Indic. 2018, 85, 352–366. [Google Scholar] [CrossRef]

- Pui, K.L.; Othman, J. Economics and environmental implicationsof fuel efficiency improvement in Malaysia: A computable general equilibriumapproach. J. Clean. Prod. 2017, 156, 459–469. [Google Scholar] [CrossRef]

- Li, W.; Zhang, Y.; Lu, C. The impact on electric power industryunder the implementation of national carbon trading market in China: Adynamic CGE analysis. J. Clean. Prod. 2018, 200, 511–523. [Google Scholar] [CrossRef]

- Tran, T.M.; Siriwardana, M.; Meng, S.; Nong, D. Impactof an emissions trading scheme on Australian households: A computable general equilibrium analysis. J. Clean. Prod. 2019, 221, 439–456. [Google Scholar] [CrossRef]

- Lin, B.; Jia, Z. Economic, energy and environmental impact of coal-to-electricity policy in China: A dynamic recursive CGE study. Sci. Total Environ. 2019, 698, 134241. [Google Scholar] [CrossRef] [PubMed]

- Li, N.; Zhang, X.; Shi, M.; Hewings, G.J.D. Does China’s air pollution abatement policy matter? An assessment of the Beijing-Tianjin-Hebei region based on a multi-regional CGE model. Energy Policy 2019, 127, 213–227. [Google Scholar] [CrossRef]

- Zhou, Y.; Fang, W.; Li, M.; Liu, W. Exploring the impacts of a low-carbon policyinstrument: A case of carbon tax on transportation in China. Resour. Conserv. Recycl. 2018, 139, 307–314. [Google Scholar] [CrossRef]

- Zhao, Y.; Zhang, Y.; Wei, W. Analysis of the energy-environment-economysystem in China based on the dynamic CGE model. J. Syst. Eng. 2014, 29, 581–591. [Google Scholar]

- Zhao, Y.; Zhang, Y.; Wei, W. Quantifying international oil price shocks on renewable energy development in China. Appl. Econ. 2020, 53, 329–344. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| Design Exploration | Scenarios | Description |

|---|---|---|

| Carbon tax policy | Business as Usual (BaU) | A carbon tax is levied on the intermediate input of energy in the production sector, and no carbon tax is levied on the final demand sector. |

| Carbon tax cycle | Scenario 1 | Based on the BaU scenario, reduce the resident income tax rate and maintain government revenue neutrality. |

| Scenario 2 | Based on the BaU scenario, reduce the enterprise income tax rate and maintain government revenue neutrality. | |

| Scenario 3 | Based on the BaU scenario, reduce the enterprise indirect tax rate and maintain government revenue neutrality 1. |

| Scenarios | Energy | 10% | 20% | 30% |

|---|---|---|---|---|

| Carbon tax (yuan/ton) | 30.50 | 71.35 | 128.20 | |

| Fossil energy tax rate | Coal | 0.11 | 0.24 | 0.42 |

| O-G | 0.03 | 0.06 | 0.11 | |

| Fossil energy reduction contribution | Coal | 97.46% | 96.87% | 96.10% |

| O-G | 2.54% | 3.13% | 3.90% | |

| Energy consumption change | Coal | −12.22% | −24.29% | −36.14% |

| O-G | −1.26% | −3.10% | −5.78% | |

| Electricity | −0.44% | −0.92% | −1.46% | |

| Scenarios | 10% | 20% | 30% |

|---|---|---|---|

| Nominal GDP | −0.09% | −0.20% | −0.33% |

| Real GDP | −0.11% | −0.28% | −0.52% |

| Household income | 0.03% | 0.06% | 0.08% |

| Household demand | −0.25% | −0.55% | −0.92% |

| Household saving | 0.03% | 0.06% | 0.08% |

| Enterprise income | −0.20% | −0.43% | −0.70% |

| Enterprise saving | −0.20% | −0.42% | −0.70% |

| Government income | 1.65% | 3.43% | 5.40% |

| Government saving | 1.65% | 3.43% | 5.40% |

| CO2 emission intensity | −9.91% | −19.84% | −29.77% |

| Social welfare | −802.06 | −1767.84 | −2953.36 |

| Heading | Heading | Scenarios | |||

|---|---|---|---|---|---|

| BaU | Scenario 1 | Scenario 2 | Scenario 3 | ||

| Households | Social welfare | −1767.84 | 3276.83 | −2203.59 | −337.08 |

| Labor income | 0.00% | 0.00% | 0.00% | 0.00% | |

| Capital income | −0.43% | −0.54% | −0.42% | −0.28% | |

| Total income | 0.06% | −0.08% | −0.06% | −0.04% | |

| Demand | −0.55% | 1.02% | −0.69% | −0.11% | |

| Savings | 0.06% | −0.08% | −0.06% | −0.04% | |

| Enterprises | Total income | −0.43% | −0.54% | −0.42% | −0.28% |

| Savings | −0.42% | −0.54% | 2.48% | −0.28% | |

| Government | Total income | 3.43% | 0.00% | 0.00% | 0.00% |

| Demand | 3.18% | −0.20% | −0.26% | 0.29% | |

| Heading | Scenarios | |||

|---|---|---|---|---|

| BaU | Scenario 1 | Scenario 2 | Scenario 3 | |

| Nominal GDP change | −0.20% | −0.25% | −0.17% | −0.86% |

| Real GDP change | −0.28% | −0.28% | −0.26% | −0.23% |

| Total investment change | −0.19% | −0.48% | 1.21% | −0.24% |

| CO2 emission intensity change | −19.84% | −19.80% | −19.86% | −19.30% |

| Carbon tax (yuan/ton) | 71.35 | 71.88 | 73.44 | 76.97 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Liu, W.; Li, Y.; Liu, T.; Liu, M.; Wei, H. How to Promote Low-Carbon Economic Development? A Comprehensive Assessment of Carbon Tax Policy in China. Int. J. Environ. Res. Public Health 2021, 18, 10699. https://doi.org/10.3390/ijerph182010699

Liu W, Li Y, Liu T, Liu M, Wei H. How to Promote Low-Carbon Economic Development? A Comprehensive Assessment of Carbon Tax Policy in China. International Journal of Environmental Research and Public Health. 2021; 18(20):10699. https://doi.org/10.3390/ijerph182010699

Chicago/Turabian StyleLiu, Weijiang, Yangyang Li, Tingting Liu, Min Liu, and Hai Wei. 2021. "How to Promote Low-Carbon Economic Development? A Comprehensive Assessment of Carbon Tax Policy in China" International Journal of Environmental Research and Public Health 18, no. 20: 10699. https://doi.org/10.3390/ijerph182010699