Linkage Analysis between Finance and Environmental Protection Sectors in China: An Approach to Evaluating Green Finance

Abstract

:1. Introduction

2. Literature Review

2.1. Green Finance

2.2. Industrial Linkage

3. Methods and Data

3.1. Methods: Linkage Analysis Based on the Input–Output Model

3.1.1. General Framework of the Input–Output Model

3.1.2. Linkage Measures

Measurement of Backward Linkage

Measurement of Forward Linkage

3.2. Data Sources

4. Results

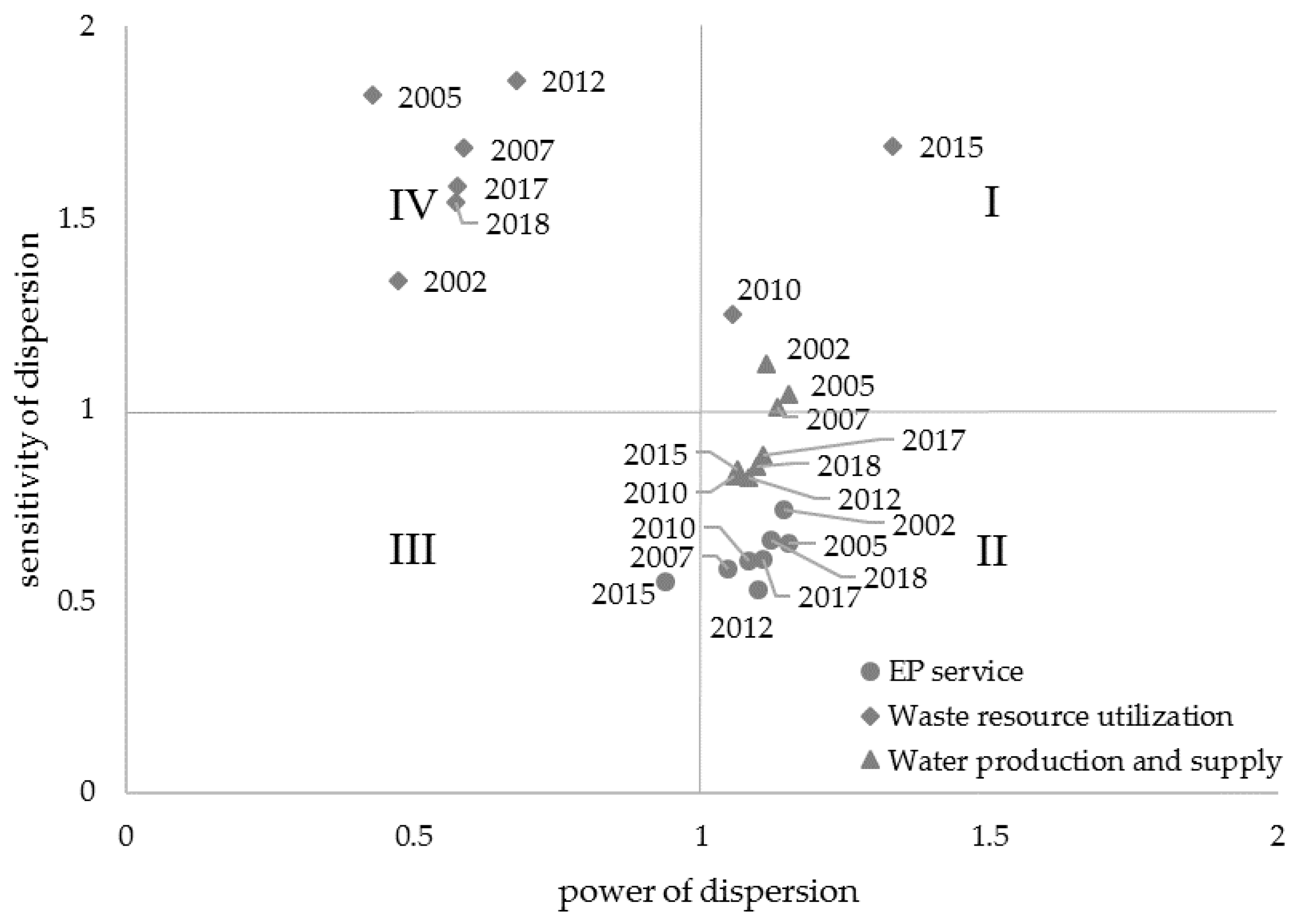

4.1. Industrial Linkage Effects and Temporal Variations of the EPS

4.2. Industrial Linkage between the EPS and Finance Sectors

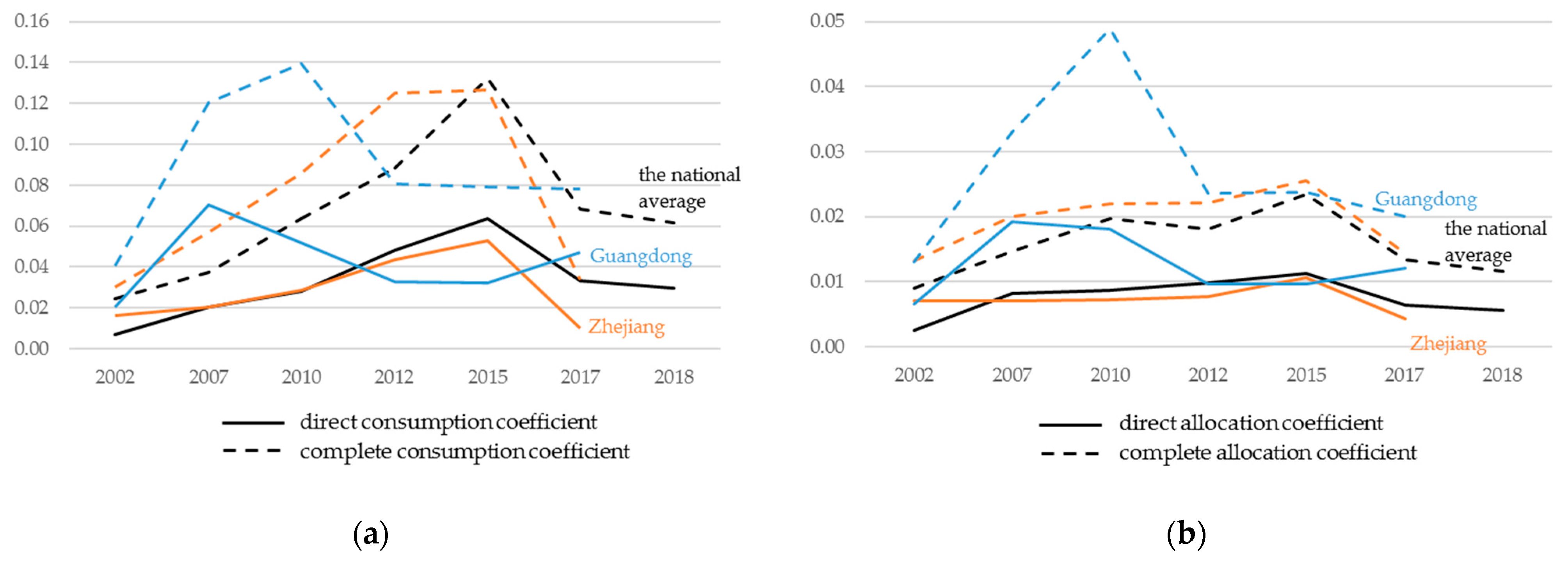

4.2.1. Backward Linkage Analysis

4.2.2. Forward Linkage Analysis

5. Discussion and Policy Implications

5.1. On the Support of the Finance Sector to the EPS

5.2. On the Development of the EPS

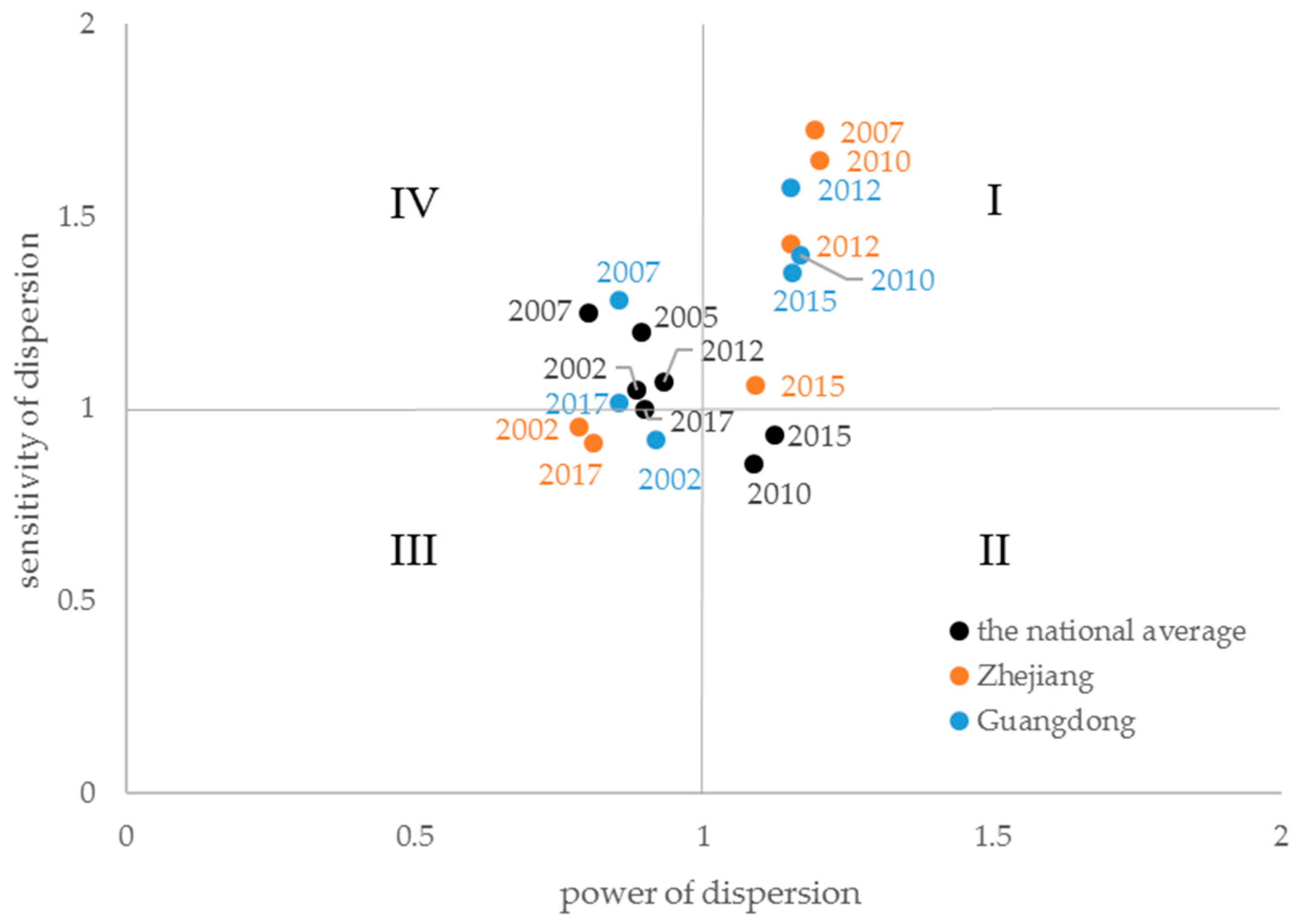

5.3. On the Development of Green Finance at the Provincial Level

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

| Sector | Dispersion Coefficient | 2002 | 2005 | 2007 | 2010 | 2012 | 2015 | 2017 | 2018 |

|---|---|---|---|---|---|---|---|---|---|

| Waste resource utilization | Power | 0.472 | 0.428 | 0.588 | 1.052 | 0.678 | 1.332 | 0.576 | 0.573 |

| Sensitivity | 1.336 | 1.821 | 1.682 | 1.249 | 1.861 | 1.688 | 1.582 | 1.539 | |

| Water production and supply | Power | 1.141 | 1.150 | 1.044 | 1.082 | 1.097 | 0.938 | 1.105 | 1.121 |

| Sensitivity | 1.117 | 1.040 | 1.005 | 0.828 | 0.822 | 0.844 | 0.880 | 0.850 | |

| EP service | Power | 1.141 | 1.150 | 1.044 | 1.082 | 1.097 | 0.938 | 1.105 | 1.121 |

| Sensitivity | 0.739 | 0.649 | 0.582 | 0.606 | 0.531 | 0.550 | 0.611 | 0.659 |

References

- OECD; Eurostat. The Environmental Goods & Servcies Industry-Manual for Data Collection and Anlaysis; OECD Publications Service: Paris, France, 1999. [Google Scholar]

- Bucher, H.; Drake-Brockman, J.; Kasterine, A.; Sugathan, M. Trade in Environmental Goods and Services: Opportunities and Challenges; ITC: Geneva, Switzerland, 2014. [Google Scholar]

- China Environmental Protection Industry Association. Report on the Development of China’s Environmental Protection Industry; China Environmental Protection Industry Association: Beijing, China, 2020. [Google Scholar]

- Akomea-Frimpong, I.; Adeabah, D.; Ofosu, D.; Tenakwah, E.J. A review of studies on green finance of banks, research gaps and future directions. J. Sustain. Financ. Invest. 2021, 1–24. [Google Scholar] [CrossRef]

- Research Bureau of People’s Bank of China. China Green Finance Progress Report 2019; China Finance Press: Beijing, China, 2020. [Google Scholar]

- Devas, H. Green Finance. Eur. Energy Environ. Law Rev. 1994, 8, 220–222. [Google Scholar]

- Salazar, J. Environmental Finance: Linking Two World; Financial Innovations for Biodiversity: Bratislava, Slovakia, 1998. [Google Scholar]

- G20 Green Finance Study Group. G20 Green Finance Synthesis Report; G20 Green Finance Study Group: Sanya, China, 2016. [Google Scholar]

- Berensmann, K.; Volz, U.; Alloisio, I.; Bak, C.; Bhattacharya, A.; Leipold, G.; Schindler, H.; MacDonald, L.; Tian, H.; Yang, Q. Fostering Sustainable Global Growth through Green Finance—What Role for the G20. 2017. Available online: https://www.g20-insights.org/policy_briefs/fostering-sustainable-global-growth-green-finance-role-g20/ (accessed on 5 January 2021).

- Li, C.; Liu, X.; Bai, X.; Umar, M. Financial Development and Environmental Regulations: The Two Pillars of Green Transformation in China. Int. J. Environ. Res. Public Health 2020, 17, 9242. [Google Scholar] [CrossRef] [PubMed]

- Zhang, D.; Zhang, Z.; Managi, S. A bibliometric analysis on green finance: Current status, development, and future directions. Financ. Res. Lett. 2019, 29, 425–430. [Google Scholar] [CrossRef]

- Scholtens, B. Finance as a driver of corporate social responsibility. J. Bus. Ethics 2006, 1, 19–33. [Google Scholar] [CrossRef]

- Taghizadeh-Hesary, F.; Yoshino, N. The way to induce private participation in green finance and investment. Financ. Res. Lett. 2019, 31, 98–103. [Google Scholar] [CrossRef]

- D’Orazio, P.; Popoyan, L. Fostering green investments and tackling climate-related financial risks: Which role for macroprudential policies? Ecol. Econ. 2019, 160, 25–37. [Google Scholar] [CrossRef] [Green Version]

- Secinaro, S.; Brescia, V.; Calandra, D.; Saiti, B. Impact of climate change mitigation policies on corporate financial performance: Evidence-based on European publicly listed firms. Corp. Soc. Responsib. Environ. Manag. 2020, 27, 2491–2501. [Google Scholar] [CrossRef]

- Wang, W.; He, T.; Wu, H.; Shi, Y. Study on Comprehensive Evaluation and Influencing Factors of Green Finance Development in Beijing, Tianjin and Hebei. North China Financ. 2021, 1, 28–41. (In Chinese) [Google Scholar]

- Ren, D. Policy-driven or Market-driven?—Calculation of Green Finance Development Index and Analysis of Influencing Factors Based on Text Mining Technology. Southwest Financ. 2020, 4, 78–89. (In Chinese) [Google Scholar]

- Zhang, L.; Xiao, L.; Gao, J. Measurement and Comparison of Green Financial Development Level and Efficiency in China:Based on Data of 1040 Public Companies. Forum Sci. Technol. China 2018, 9, 100–112. (In Chinese) [Google Scholar]

- Jeucken, M. Sustainable Finance and Banking: The Financial Sector and the Future of the Planet; Earthscan: London, UK, 2010. [Google Scholar]

- OECD. Trends in Environmental Finance in Eastern Europe, Caucasus, and Central Asia (EECCA); OECD: Paris, France, 2007; Volume 7, pp. 41–90. [Google Scholar]

- Ling, L.; Dong, Z.; Lin, L.; Pan, X.; Liu, H.; Yu, C. Research on Industrial Linkage between China’s Environmental Protection and Finance Industries:Analysis Based on Multi-Year Input-Output Tables. Ecol. Econ 2020, 36, 51–58. (In Chinese) [Google Scholar]

- Miller, R.E.; Blair, P.D. Input-Output Analysis: Foundations and Extensions; Cambridge University Press: Cambridge, UK, 2009. [Google Scholar]

- Hirschman, A. The Strategy of Economic Development; Yale University Press: New Haven, CT, USA, 1958. [Google Scholar]

- Rasmussen, P.N. Studies in Inter-Sectoral Relations; WorldCat: Amsterdam, The Netherlands, 1956. [Google Scholar]

- Wen, W.; Wang, Q. Identification of key sectors and key provinces at the view of CO2 reduction and economic growth in China: Linkage analyses based on the MRIO model. Ecol. Indic. 2019, 96, 1–15. [Google Scholar] [CrossRef]

- Cai, J.; Leung, P. Linkage Measures: A Revisit and a Suggested Alternative. Technol. Anal. Strateg. Manag. 2004, 16, 63–83. [Google Scholar] [CrossRef]

- Song, Y.; Liu, C.; Langston, C. Exploring intersectoral linkages between real estate and construction. Int. J. Constr. Manag. 2008, 8, 73–85. [Google Scholar] [CrossRef]

- Forni, M.; Paba, S. Spillovers and the growth of local industries. J. Ind. Econ. 2002, 50, 151–171. [Google Scholar] [CrossRef]

- He, H.; Reynolds, C.J.; Li, L.; Boland, J. Assessing net energy consumption of Australian economy from 2004–05 to 2014–15: Environmentally-extended input-output analysis, structural decomposition analysis, and linkage analysis. Appl. Energy 2019, 240, 766–777. [Google Scholar] [CrossRef]

- Lenzen, M. Environmentally important paths, linkages and key sectors in the Australian economy. Struct. Chang. Econ. Dyn. 2003, 14, 1–34. [Google Scholar] [CrossRef]

- Chan, S.; Han, G.; Zhang, W. How strong are the linkages between real estate and other sectors in China? Res. Int. Bus. Financ. 2016, 36, 52–72. [Google Scholar] [CrossRef]

- Freytag, A.; Fricke, S. Sectoral linkages of financial services as channels of economic development—An input–output analysis of the Nigerian and Kenyan economies. Rev. Dev. Financ. 2017, 7, 36–44. [Google Scholar] [CrossRef]

- Shi, Q.; Deng, X.; Shi, C.; Chen, S. Exploration of the intersectoral relations based on input-output tables in the Inland River Basin of China. Sustainability-Basel 2015, 7, 4323–4340. [Google Scholar] [CrossRef] [Green Version]

- Zhu, R.; Hu, X.; Liu, C. Structural analysis of inter-industrial linkages: An application to the Australian construction industry. Constr. Manag. Econ. 2020, 38, 934–946. [Google Scholar] [CrossRef]

- Fan, Y.; Wu, S.; Lu, Y.; Zhao, Y. Study on the effect of the environmental protection industry and investment for the national economy: An input-output perspective. J. Clean. Prod. 2019, 227, 1093–1106. [Google Scholar] [CrossRef]

- Midmore, P.; Munday, M.; Roberts, A. Assessing industry linkages using regional input–output tables. Reg. Stud. 2006, 40, 329–343. [Google Scholar] [CrossRef]

- Yi, S.; Xie, J. A study on the dynamic comparison of logistics industry’s correlation effects in China. China Financ. Econ. Rev. 2017, 5, 15. [Google Scholar] [CrossRef] [Green Version]

- Sauian, M.S.; Kamarudin, N.; Rani, R.M. Analyzing the importance of transportation and financial services sectors using economic linkages analysis. In Proceedings of the 2012 International Conference on Statistics in Science, Business and Engineering (ICSSBE), Kedah, Malaysia, 10–12 September 2012; pp. 1–4. [Google Scholar]

- Ali, Y.; Bilal, M.; Sabir, M. Impacts of transport strike on Pakistan economy: An inoperability Input-Output model (IIOM) approach. Res. Transp. Econ. 2020, 100860. [Google Scholar] [CrossRef]

- Han, S.; Yoo, S.; Kwak, S. The role of the four electric power sectors in the Korean national economy: An input–output analysis. Energy Policy 2004, 32, 1531–1543. [Google Scholar] [CrossRef]

- Wang, Y.; Tian, Y.; Wu, Y. Input-output Analysis on the Correlation Effect of Environmental Industry in China. Chin. J. Environ. Manag. 2017, 4, 39–45. (In Chinese) [Google Scholar]

| Industrial Linkage | Direct Linkages | Total Linkages | Normalized Linkages |

|---|---|---|---|

| Backward linkages | Equation (1) | Equation (2) | Equation (3) 1 |

| Forward linkages | Equation (4) | Equation (5) | Equation (6) 2 |

| Classification Value | Sensitivity of Dispersion < 1 | Sensitivity of Dispersion > 1 |

|---|---|---|

| Power of dispersion <1 | Generally independent (LL) | Dependent on inter-sectoral demand (LH) |

| Power of dispersion >1 | Dependent on inter-sectoral supply (HL) | Generally dependent (HH) |

| Sectors in the Original I–O Table | Sectors in the Established I–O Table | |

|---|---|---|

| 42-Sector I–O Table | More Than 100-Sector I–O Table | |

| Waste resource utilization (in the secondary industry) | Environmental protection sector (EPS) | |

| Water production and supply (in the secondary industry) | ||

| Water conservancy and environmental and public facility management (in the tertiary industry) 1 | Water conservancy management | |

| Ecological protection and environmental management | ||

| Public facility management | ||

| Finance (in the tertiary industry) | Monetary finance service | Finance sector |

| Capital market service | ||

| Insurance service | ||

| Industry | 2002 | 2005 | 2007 | 2010 | 2012 | 2015 | 2017 | 2018 |

|---|---|---|---|---|---|---|---|---|

| EPS | 0.885 | 0.892 | 0.802 | 1.087 | 0.931 | 1.124 | 0.897 | 0.876 |

| Finance | 1.049 | 1.198 | 1.250 | 0.858 | 1.068 | 0.932 | 0.998 | 1.045 |

| Primary | 0.840 | 0.832 | 0.750 | 0.722 | 0.809 | 0.708 | 0.855 | 0.873 |

| Secondary | 1.168 | 1.003 | 0.988 | 1.087 | 1.079 | 1.086 | 1.061 | 1.035 |

| Tertiary | 0.917 | 0.873 | 0.925 | 0.864 | 0.896 | 0.867 | 0.899 | 0.882 |

| Industry | 2002 | 2005 | 2007 | 2010 | 2012 | 2015 | 2017 | 2018 |

|---|---|---|---|---|---|---|---|---|

| EPS | 1.049 | 1.198 | 1.250 | 0.858 | 1.068 | 0.932 | 0.998 | 1.045 |

| Finance | 0.840 | 0.832 | 0.750 | 0.722 | 0.809 | 0.708 | 0.855 | 0.873 |

| Primary | 1.168 | 1.003 | 0.988 | 1.087 | 1.079 | 1.086 | 1.061 | 1.035 |

| Secondary | 0.917 | 0.873 | 0.925 | 0.864 | 0.896 | 0.867 | 0.899 | 0.882 |

| Tertiary | 0.934 | 1.001 | 1.004 | 1.157 | 1.055 | 1.148 | 1.119 | 1.093 |

| Province | Dispersion Coefficient | 2002 | 2007 | 2010 | 2012 | 2015 | 2017 |

|---|---|---|---|---|---|---|---|

| Zhejiang | Power | 0.784 | 1.192 | 1.201 | 1.150 | 1.090 | 0.808 |

| Sensitivity | 0.951 | 1.725 | 1.648 | 1.428 | 1.062 | 0.911 | |

| Guangdong | Power | 0.916 | 0.855 | 1.168 | 1.152 | 1.155 | 0.854 |

| Sensitivity | 0.918 | 1.282 | 1.398 | 1.574 | 1.356 | 1.017 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Li, L.; Wu, W.; Zhang, M.; Lin, L. Linkage Analysis between Finance and Environmental Protection Sectors in China: An Approach to Evaluating Green Finance. Int. J. Environ. Res. Public Health 2021, 18, 2634. https://doi.org/10.3390/ijerph18052634

Li L, Wu W, Zhang M, Lin L. Linkage Analysis between Finance and Environmental Protection Sectors in China: An Approach to Evaluating Green Finance. International Journal of Environmental Research and Public Health. 2021; 18(5):2634. https://doi.org/10.3390/ijerph18052634

Chicago/Turabian StyleLi, Libo, Wenbing Wu, Mingyu Zhang, and Lu Lin. 2021. "Linkage Analysis between Finance and Environmental Protection Sectors in China: An Approach to Evaluating Green Finance" International Journal of Environmental Research and Public Health 18, no. 5: 2634. https://doi.org/10.3390/ijerph18052634