Mind the Gap—A Socio-Economic Analysis on Price Developments of Green Hydrogen, Synthetic Fuels, and Conventional Energy Carriers in Germany

Abstract

:1. Introduction

- (1)

- If conventional fuels increase in price and renewable energy carriers also feature high price levels in the future, what should be an adequate benchmark price for both types of energy supply?

- (2)

- To what extent do the recent as well as the expected future price developments lead to an intensified financial burden for customers?

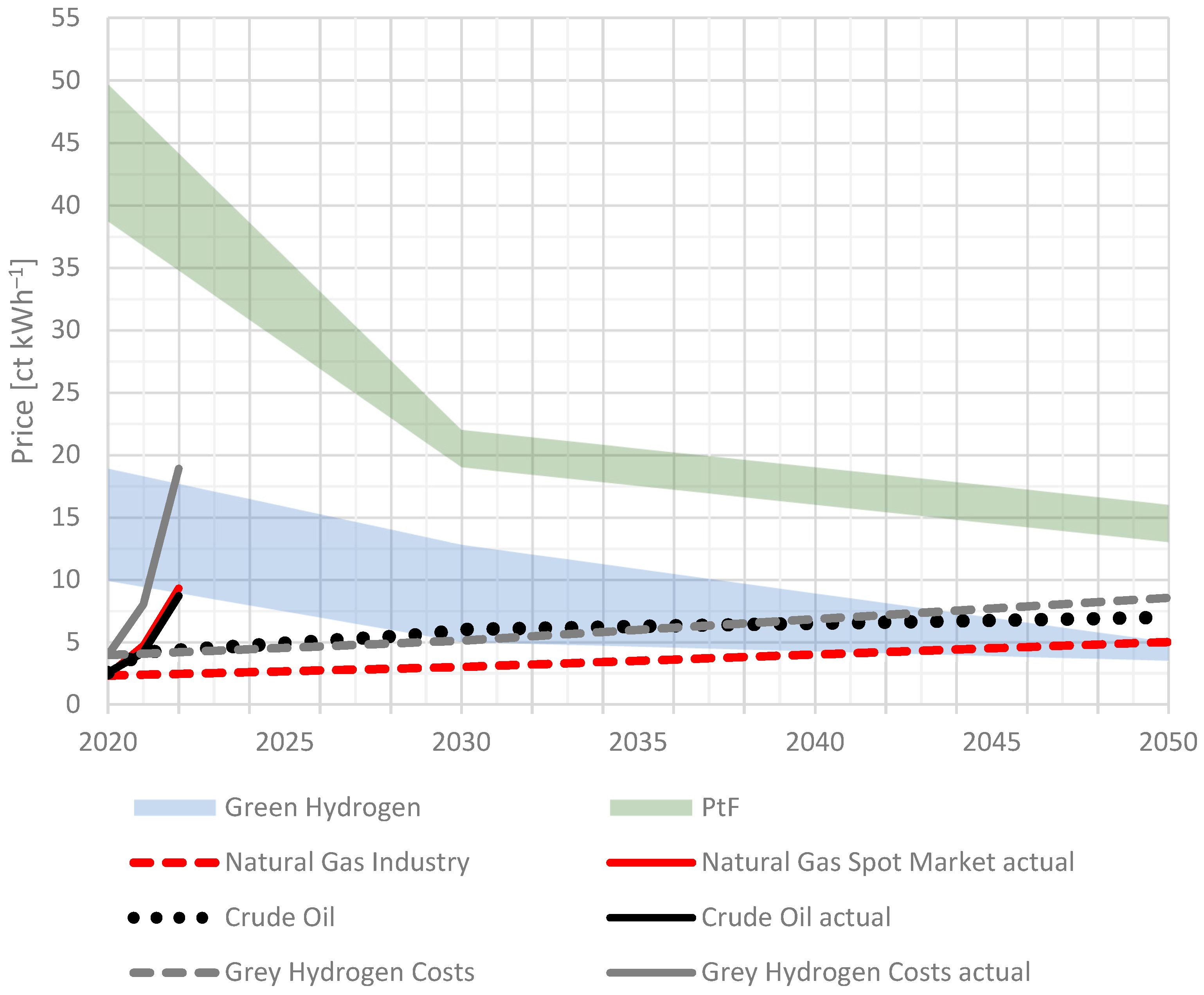

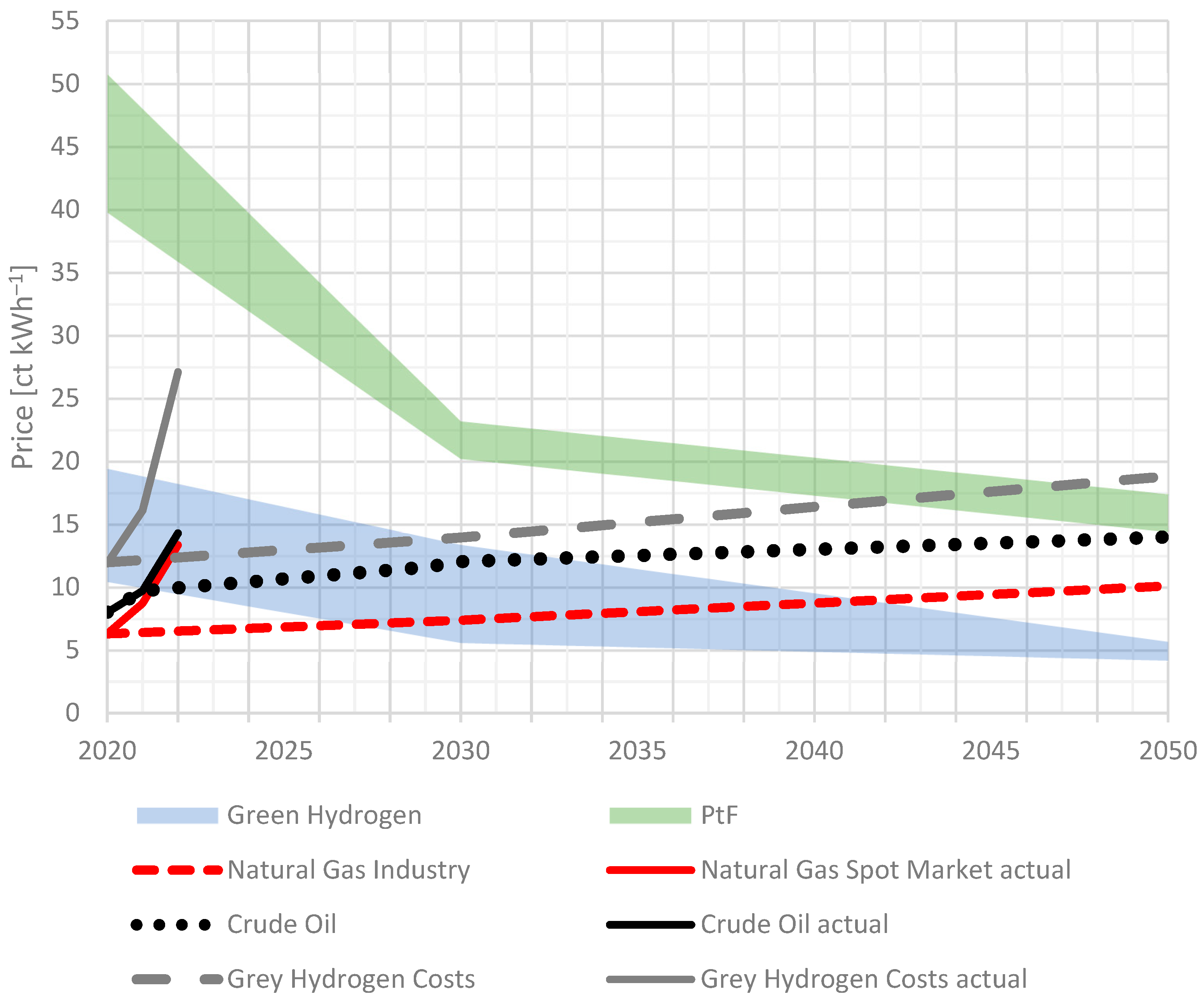

2. Price Projections and Consideration of Greenhouse Gas-Induced Environmental Impact Costs

2.1. State-of-the-Art and Prospective Price Developments of Renewable and Conventional Energy Carriers in Germany

2.2. Consideration of Greenhouse Gas-Induced Environmental Impact Costs

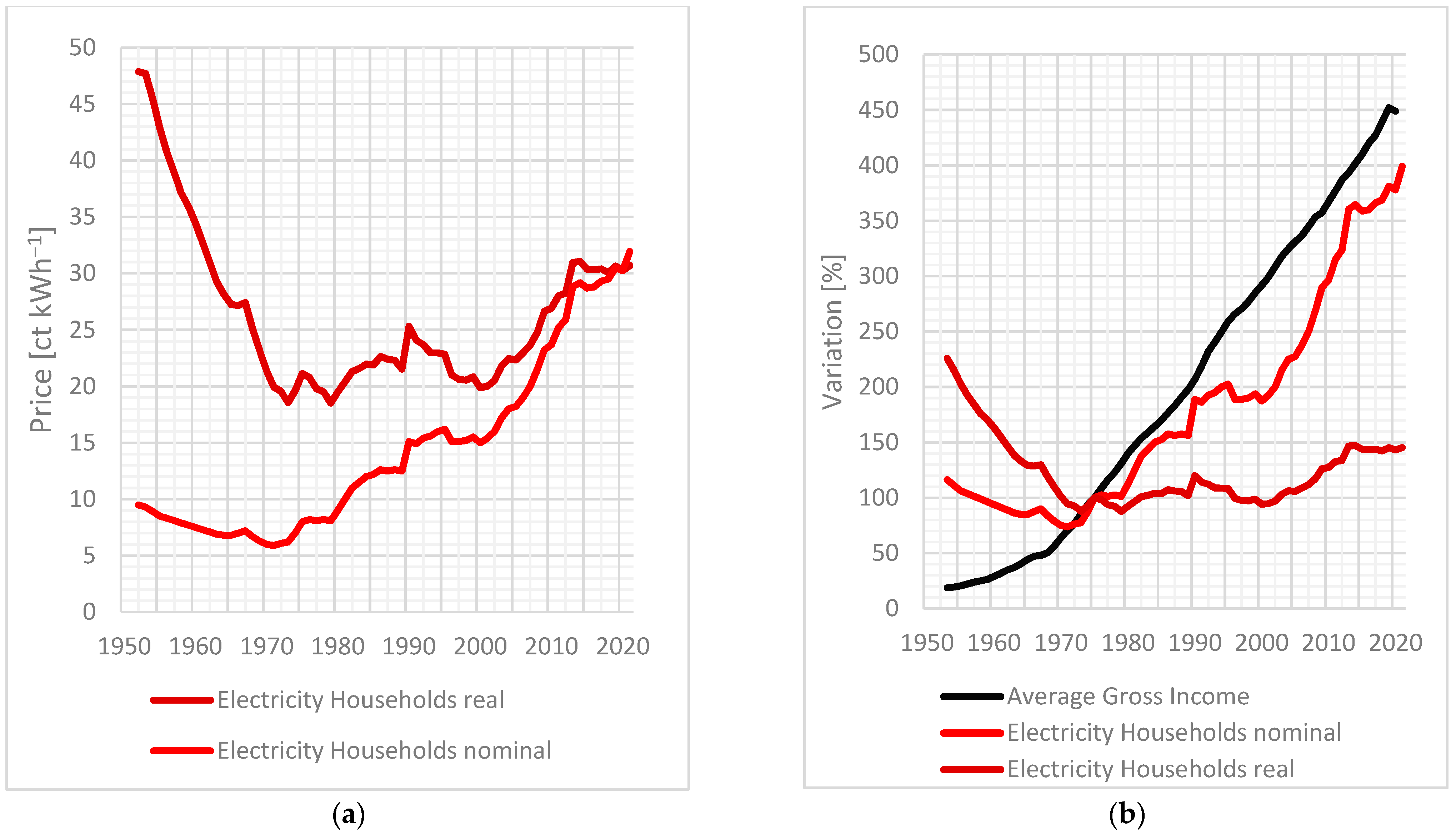

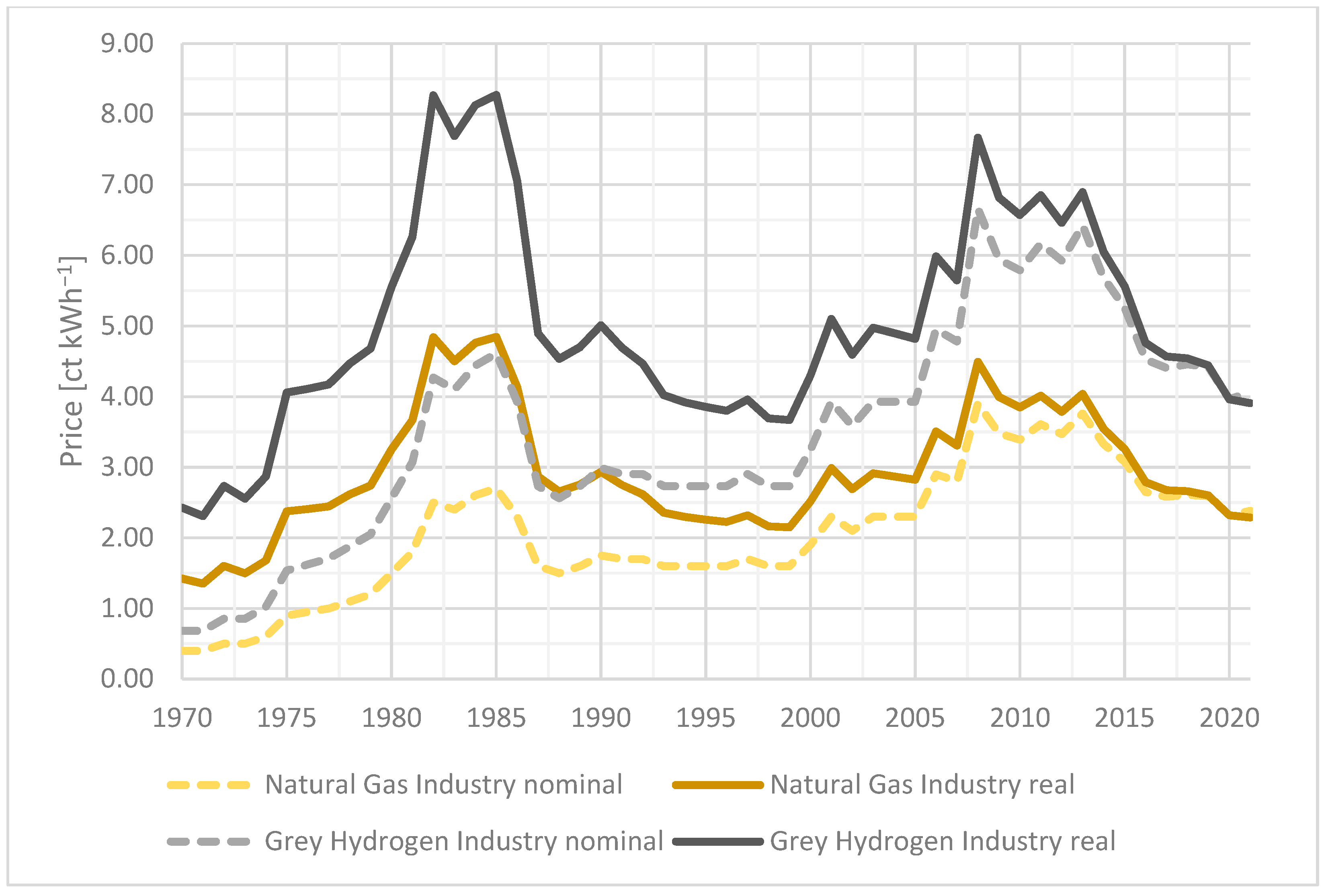

3. Discussion of Price Developments from a Socio-Economic Perspective

4. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Fraunhofer ISE. Jährlicher Anteil erneuerbarer Energien an der Stromerzeugung in Deutschland, Energy Charts. 2021. Available online: https://energy-charts.info/charts/renewable_share/chart.htm?l=de&c=DE&interval=year (accessed on 11 October 2021).

- Umweltbundesamt. Zeitreihen zur Entwicklung der Erneuerbaren Energien in Deutschland, Dessau-Roßlau. 2021. Available online: https://www.umweltbundesamt.de/themen/klima-energie/erneuerbare-energien/erneuerbare-energien-in-zahlen#uberblick (accessed on 11 October 2021).

- Ueckerdt, F.; Pfluger, B.; Odenweller, A.; Günther, C.; Knodt, M. Durchstarten trotz Unsicherheiten: Eckpunkte einer Anpassungsfähigen Wasserstoffstrategie; Ariadne-Kurzdossier: Potsdam, Germany, 2021. [Google Scholar]

- Wuppertal Institut. Verkehrswende für Deutschland: Der Weg zu CO2-Freier Mobilität bis 2035; Greenpeace: Hamburg, Germany, 2017. [Google Scholar]

- European Commission. Communication from the Commission to the European Parliament, the Council, the European Economic and Social Committee and the Committee of the Regions-A hydrogen Strategy for a Climate-Neutral Europe, Brussels. 2020. Available online: https://ec.europa.eu/energy/sites/ener/files/hydrogen_strategy.pdf (accessed on 20 April 2022).

- Sozialdemokratische Partei Deutschlands (SPD), Bündnis 90/Die Grünen, Freie Demokratische Partei (FDP). Mehr Fortschritt wagen-Bündnis für Freiheit, Gerechtigkeit und Nachhaltigkeit. Koalitionsvertrag 2021–2025, Berlin. 2021. Available online: https://www.spd.de/fileadmin/Dokumente/Koalitionsvertrag/Koalitionsvertrag_2021-2025.pdf (accessed on 20 April 2022).

- Schnuelle, C.; Kisjes, K.; Stuehrmann, T.; Thier, P.; Nikolic, I.; von Gleich, A.; Goessling-Reisemann, S. From Niche to Market—An Agent-Based Modeling Approach for the Economic Uptake of Electro-Fuels (Power-to-Fuel) in the German Energy System. Energies 2020, 13, 5522. [Google Scholar] [CrossRef]

- Energiewende, A.; Verkehrswende, A.; Frontier Economics Ltd. Die Zukünftigen Kosten Strombasierter Synthetischer Brennstoffe. 2018. Available online: https://www.agora-energiewende.de/fileadmin/Projekte/2017/SynKost_2050/Agora_SynCost-Studie_WEB.pdf (accessed on 18 November 2021).

- Rudolph, F. Der Beitrag von synthetischen Kraftstoffen zur Verkehrswende: Optionen und Prioritäten. 2019. Available online: https://www.greenpeace.de/publikationen/kurzstudie_kraftstoffe_verkehrswende.pdf (accessed on 18 November 2021).

- Decker, M.; Schorn, F.; Can, R.; Peters, R.; Stolten, D. Off-grid power-to-fuel systems for a market launch scenario—A techno-economic assessment. Appl. Energy 2019, 250, 1099–1109. [Google Scholar] [CrossRef]

- Verband der Chemischen Industrie. Energiepreise Explodieren. 2021. Available online: https://www.vci.de/themen/energie-klima/energiepolitik/strom-und-erdgas-werden-immer-teurer-energiepreise-explodieren.jsp (accessed on 19 November 2021).

- Bockenheimer, J.C. Energiepreise Explodieren! Regierung Lässt uns mit TEUER-SCHOCK Allein, Bild Zeitung. 2021. Available online: https://www.bild.de/geld/wirtschaft/wirtschaft/energiepreise-explodieren-regierung-laesst-uns-mit-teuer-schock-allein-78059692.bild.html (accessed on 19 November 2021).

- Müller, K. Wer soll das noch Bezahlen? Beim Heizen droht uns der Teuerste Winter aller Zeiten. Focus Online. 2021. Available online: https://www.focus.de/finanzen/news/verrueckte-energiepreise-wer-soll-das-noch-bezahlen-beim-heizen-droht-uns-der-teuerste-winter-aller-zeiten_id_24306345.html (accessed on 20 November 2021).

- Agora Energiewende and Guidehouse. Making Renewable Hydrogen Cost-Competitive: Policy Instruments for Supporting Green H2. 2021. Available online: https://static.agora-energiewende.de/fileadmin/Projekte/2020/2020_11_EU_H2-Instruments/A-EW_223_H2-Instruments_WEB.pdf (accessed on 15 March 2022).

- Dovan, D.J.; Dolanc, G. Can Green Hydrogen Production Be Economically Viable under Current Market Conditions. Energies 2020, 13, 6599. [Google Scholar] [CrossRef]

- Aditiya, H.; Aziz, M. Prospect of hydrogen energy in Asia-Pacific: A perspective review on techno-socio-economy nexus. Int. J. Hydrogen Energy 2021, 46, 35027–35056. [Google Scholar] [CrossRef]

- Bleischwitz, R.; Bader, N.; Trümper, S. The socio-economic transition towards a hydrogen economy. Energy Policy 2010, 38, 5297–5300. [Google Scholar] [CrossRef]

- Maack, M.; Skulason, J. Implementing the Hydrogen Economy. J. Clean. Prod. 2006, 14, 52–64. [Google Scholar] [CrossRef]

- König, D.H.; Freiberg, M.; Dietrich, R.-U.; Wörner, A. Techno-economic study of the storage of fluctuating renewable energy in liquid hydrocarbons. Fuel 2015, 159, 289–297. [Google Scholar] [CrossRef] [Green Version]

- Dieterich, V.; Buttler, A.; Hanel, A.; Spliethoff, H.; Fendt, S. Power-to-liquid via synthesis of methanol, DME or Fischer–Tropsch-fuels: A review. Energy Environ. Sci. 2020, 13, 3207–3252. [Google Scholar] [CrossRef]

- Brynolf, S.; Taljegard, M.; Grahn, M.; Hansson, J. Electrofuels for the transport sector: A review of production costs. Renew. Sustain. Energy Rev. 2018, 81, 1887–1905. [Google Scholar] [CrossRef]

- Tenhumberg, N.; Büker, K. Ecological and Economic Evaluation of Hydrogen Production by Different Water Electrolysis Technologies. Chem. Ing. Tech. 2020, 92, 1586–1595. [Google Scholar] [CrossRef]

- Weimann, L.; Gabrielli, P.; Boldrini, A.; Kramer, G.J.; Gazzani, M. Optimal hydrogen production in a wind-dominated zero-emission energy system. Adv. Appl. Energy. 2021, 3, 100032. [Google Scholar] [CrossRef]

- Schnuelle, C.; Wassermann, T.; Fuhrlaender, D.; Zondervan, E. Dynamic Hydrogen Production from PV & Wind Direct Electricity Supply—Modeling and Techno-Economic Assessment. Int. J. Hydrogen Energy 2020, 45, 29938–29952. [Google Scholar] [CrossRef]

- Pfennig, M.; Gerhardt, N.; Pape, C.; Böttger, D. Mittel- und Langfristige Potentiale von PTL- und H2-Importen aus Internationalen EE-Vorzugsregionen-Teilbericht, Kassel; Fraunhofer IWES: Hamburg, Germany, 2017. [Google Scholar]

- International Energy Agency. The Future of Hydrogen-Seizing Today’s Opportunities. 2019. Available online: https://iea.blob.core.windows.net/assets/9e3a3493-b9a6-4b7d-b499-7ca48e357561/The_Future_of_Hydrogen.pdf (accessed on 18 December 2021).

- Joas, F.; Witecka, W.; Lenck, T.; Peter, F.; Seiler, F.; Samadi, S.; Schneider, C.; Holtz, G.; Kobiela, G.; Lechtenböhmer, S.; et al. Klimaneutrale Industrie: Schlüsseltechnologien und Politikoptionen für Stahl, Chemie und Zement; Agora Energiewende: Berlin, Germany, 2020. [Google Scholar]

- IRENA. Hydrogen: A Renewable Energy Perspective; International Renewable Energy Agency: Abu Dhabi, United Arab Emirates, 2019; ISBN 978-92-9260-151-5. [Google Scholar]

- EEX Group. EEX Natural Gas Reference Prices. 2022. Available online: https://www.eex.com/fileadmin/EEX/Downloads/Trading/Indices/20220404_EEX_Gas_Reference_Price_EGIX.pdf (accessed on 20 April 2022).

- Destatis. Daten zur Energiepreisentwicklung-Lange Reihen von Januar 2005 bis Mai 2021; Destatis: Wiesbaden, Germany, 2021. [Google Scholar]

- Verivox. Die Gaspreisentwicklung für bundesdeutsche Haushalte. 2022. Available online: https://www.verivox.de/gas/verbraucherpreisindex/ (accessed on 26 March 2022).

- e-Bridge. Kompetenz in Energie, Wasserstoff-Preisindex (Hydex). 2022. Available online: https://www.e-bridge.de/#hydexmodal (accessed on 26 March 2022).

- International Energy Agency. World Energy Outlook 2019; International Energy Agency: Paris, France, 2019; Available online: https://www.iea.org/reports/world-energy-outlook-2019 (accessed on 20 March 2022).

- Hauser, P.; Heinrichs, H.U.; Gillessen, B.; Müller, T. Implications of diversification strategies in the European natural gas market for the German energy system. Energy 2018, 151, 442–454. [Google Scholar] [CrossRef]

- Kemmler, A.; Kirchner, A.; der Maur, A.A.; Ess, F.; Kreidelmeyer, S. Energiewirtschaftliche Projektionen und Folgeabschätzungen 2030/2050. 2020. Available online: https://www.bmwi.de/Redaktion/DE/Publikationen/Wirtschaft/klimagutachten.html (accessed on 15 February 2022).

- Ökoinstitut e.V. Rahmendaten für das Impact Assessment der Ziele im Klimaschutzplan 2050. 2017. Available online: https://www.oeko.de/fileadmin/oekodoc/Folgenabschaetzung-Klimaschutzplan-2050-Endbericht.pdf (accessed on 16 February 2022).

- European Union. Recommended Parameters for Reporting on GHG Projections in 2017; European Union: Brussels, Belgium, 2016. [Google Scholar]

- Trading Economics. EU Carbon Permits. 2022. Available online: https://tradingeconomics.com/commodity/carbon (accessed on 11 April 2022).

- Matthey, B.; Bünger, A. Methodenkonvention 3.1 zur Ermittlung von Umweltkosten; Umweltbundesamt: Dessau-Roßlau, Germany, 2020. [Google Scholar]

- Greenpeace Energy EG. Blauer Wasserstoff-Lösung oder Problem der Energiewende? Hamburg, Germany. 2020. Available online: https://green-planet-energy.de/fileadmin/user_upload/broschuere-wasserstoff.pdf (accessed on 15 November 2021).

- Agora Verkehrswende. Klimabilanz von strombasierten Antrieben und Kraftstoffen. 2019. Available online: https://www.agora-verkehrswende.de/fileadmin/Projekte/2019/Klimabilanz_Batteriefahrzeugen/32_Klimabilanz_strombasierten_Antrieben_Kraftstoffen_WEB.pdf (accessed on 15 November 2021).

- Hauser, J. Der Strompreis steigt und steigt, Frankfurter Allg. Zeitung. 2021. Available online: https://www.faz.net/aktuell/wirtschaft/der-strompreis-steigt-groessere-huerden-fuer-den-klimaschutz-17575274.html (accessed on 19 December 2021).

- Jahberg, H. Warum steigt der Strompreis ständig? Der Tagesspiegel. 2021. Available online: https://www.tagesspiegel.de/themen/strom/strompreis-warum-steigt-der-strompreis-staendig/8413202.html (accessed on 19 December 2021).

- Schultz, S. Deutsche Zahlen Global Fast die Höchsten Strompreise, Spiegel Online. 2021. Available online: https://www.spiegel.de/wirtschaft/service/strompreis-deutsche-zahlen-weltweit-fast-die-hoechsten-preise-a-efd023db-3036-4f02-9948-ed6ae5c5bdfe (accessed on 19 December 2021).

- Wetzel, D. Die Deutschen Zahlen Jetzt die Mit Abstand Höchsten Strompreise der Welt, Welt. 2021. Available online: https://www.welt.de/wirtschaft/plus224386200/Energiewende-Deutsche-zahlen-die-weltweit-hoechsten-Strompreise.html (accessed on 18 December 2021).

- Göpfert, A. Deutsche Zahlen Immer Mehr für Strom, Tagesschau. 2021. Available online: https://www.tagesschau.de/wirtschaft/verbraucher/strompreise-deutschland-vergleich-rekordhoch-eeg-101.html (accessed on 21 December 2021).

- Rahlf, T. Deutschland in Daten-Zeitreihen zur historischen Statistik; Bundeszentrale für Politische Bildung: Bonn, Germany, 2015. [Google Scholar]

- Energieagentur NRW. Energiepreise-Entwicklung in Deutschland; Bundesministerium für Wirtschaft und Energie: Berlin, Germany, 2021. [Google Scholar]

- Destatis. Verbraucherpreisindizes für Deutschland-Lange Reihen ab 1948. 2021. Available online: https://www.destatis.de/DE/Themen/Wirtschaft/Preise/Verbraucherpreisindex/Publikationen/Downloads-Verbraucherpreise/verbraucherpreisindex-lange-reihen-pdf-5611103.pdf?__blob=publicationFile (accessed on 14 February 2022).

- Emele, L. Entwicklung der Strompreise im Verhältnis zur Kaufkraft und Abhängigkeit der Strompreise von den Primärenergiekosten im Untersuchungszeitraum 1950 bis heute. 2009. Available online: https://www.lukas-emele.de/cms/wp-content/uploads/2009/05/Projekt1.pdf (accessed on 28 October 2021).

- Destatis. Verdienste und Verdienstunterschiede-durchschnittliche Bruttomonatsverdienste, Zeitreihe. 2021. Available online: https://www.destatis.de/DE/Themen/Arbeit/Verdienste/Verdienste-Verdienstunterschiede/_inhalt.html (accessed on 14 January 2022).

- Europäische Zentralbank. EZB-Rat Verabschiedet Neue Geldpolitische Strategie, Pressemitteilung. 2021. Available online: https://www.ecb.europa.eu/press/pr/date/2021/html/ecb.pr210708~dc78cc4b0d.de.html (accessed on 9 January 2021).

- Bundesministerium für Wirtschaft und Klimaschutz, Fossile Inflation–Treibt die Energiewende Aktuell Wirklich die Preise? Nein, Sagen Fachleute und Sehen in Ihr vor Allem einen Teil der Lösung, Schlaglichter April 2022, Berlin. Available online: https://www.bmwk.de/Redaktion/DE/Infografiken/Schlaglichter/2022/04/04-im-fokus-download.pdf?__blob=publicationFile&v=4 (accessed on 28 April 2022).

- Schnuelle, C.; Thoeming, J.; Wassermann, T.; Thier, P.; von Gleich, A.; Goessling-Reisemann, S. Socio-technical-economic assessment of power-to-X: Potentials and limitations for an integration into the German energy system. Energy Res. Soc. Sci. 2019, 51, 187–197. [Google Scholar] [CrossRef]

- Bach, S.; Isaak, N.; Kemfert, C.; Kunert, U.; Schill, W.-P.; Wägner, N.; Zaklan, A. Für eine sozialverträgliche CO2-Bepreisung, Deutsches Institut für Wirtschaftsforschung (DIW). 2019. Available online: https://www.diw.de/documents/publikationen/73/diw_01.c.635193.de/diwkompakt_2019-138.pdf (accessed on 24 April 2022).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Energy Carrier | Specific CO2 Equivalents g kWh−1 | Benchmark Price ct2020 kWh−1 | Price in 2020 ct2020 kWh−1 |

|---|---|---|---|

| Grey hydrogen | 403 | 12 | 4 |

| Green hydrogen | 26 | - | - |

| Natural gas | 200 | 6.3 | 2.34 |

| Petrol | 275 | 9.9 | 4.7 |

| Synthetic fuels | 54 | - | - |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Schnuelle, C.; Wassermann, T.; Stuehrmann, T. Mind the Gap—A Socio-Economic Analysis on Price Developments of Green Hydrogen, Synthetic Fuels, and Conventional Energy Carriers in Germany. Energies 2022, 15, 3541. https://doi.org/10.3390/en15103541

Schnuelle C, Wassermann T, Stuehrmann T. Mind the Gap—A Socio-Economic Analysis on Price Developments of Green Hydrogen, Synthetic Fuels, and Conventional Energy Carriers in Germany. Energies. 2022; 15(10):3541. https://doi.org/10.3390/en15103541

Chicago/Turabian StyleSchnuelle, Christian, Timo Wassermann, and Torben Stuehrmann. 2022. "Mind the Gap—A Socio-Economic Analysis on Price Developments of Green Hydrogen, Synthetic Fuels, and Conventional Energy Carriers in Germany" Energies 15, no. 10: 3541. https://doi.org/10.3390/en15103541