1. Introduction

Changes in global energy policy are already a fact. They have been confirmed by successive climate conferences, including the last one in 2021 in Glasgow. More and more countries are adopting and implementing those policies in the form of new laws regulating the activities of the energy sector in line with new, green economy standards. In all Western European countries, this sector is one of the most regulated, with significant state interference. Despite attempts to regulate the market and a competitive economy within it, policy has not been radically changed in recent years. Therefore, more and more energy companies, within their resources and legal possibilities, have changed their strategies toward the use of renewable energy sources [

1]. This way they diversify their energy production. As changes in the energy sector must occur very quickly, many enterprises decide to develop externally, preferring mergers and acquisitions (M&A) [

2,

3] as faster ways to comply with the requirements of declarations formulated at climate conferences. Those M&A transactions are most often takeovers of photovoltaic companies, wind farms, hydropower, and other producers of energy from renewable sources. This is often done through the acquisition of start-ups [

4]. Many of such mergers and acquisitions take place especially in Western Europe. This is due not only to pressure from governments, but also to the high awareness of societies that do not accept the “brown economy”. If it turns out that the main motives for mergers and acquisitions in the energy sector are related to the diversification of activities toward the production of energy from renewable sources, it will confirm that political decisions can influence the companies’ behaviors and thus influence the economy. At the same time, it will expand the knowledge related to strategic analysis and the strategies of enterprises in the regulated sectors.

Therefore, the aim of the research, the results of which are presented in this publication, was to identify the motives for mergers and acquisitions in the energy sector after the introduction of green economy elements in Western Europe. The mentioned region is the group of countries where changes related to moving to green energy are most visible (in addition to some countries from different regions, such as Singapore, New Zealand, or countries of the Arabian Peninsula).

The research assumed the hypothesis that over the years since the Paris Conference [

5] the themes of mergers and acquisitions changed from motives close to the views related to energy generation in traditional systems (black energy in large monopolistic systems) to motives close to green energy (the research hypothesis). In addition to emphasizing the direction of changes in M&A motives, the authors of this study decided to check whether since 2015 (when the Paris Conference was organized) the motives behind the M&A transactions conducted by companies operating in the electrical energy generation sector have changed, making their motives close to the green energy dominant in Western Europe. The research used a critical analysis of the literature on the subject, a study that used desk research based on openly available sources and our own analytical tool developed for the needs of this analysis, which is a transformation of the concept of analysis of the M&A motives proposed in K. Borowski’s research entitled, “The strategic development of the technology companies. The mergers and acquisitions perspective” [

6].

The article’s structure consists of a theoretical part, which presents the results of literature studies on changes in the energy sector, but also in the entire economy, resulting from the fundamentals of the green economy. One of those fundamentals is to move away from coal and oil as energy sources and to switch to renewable sources. The result of the literature research is also a review of the motives behind mergers and acquisitions, including motives in the energy sector. They will be used as the basis for the analysis carried out in the next, empirical part of the article.

The second, empirical part presents the results of research on the identification of the motives behind M&A transactions in the energy sector after the introduction of green economy elements in Western Europe. The authors selected 95 M&A transactions that were announced by energy companies from 2015–2021. The acquiring companies come from nine countries. Most of them come from France. This was a result of the high activity of enterprises from these countries in M&A in the energy sector. The whole work ends with a summary that discusses the results.

2. Green Economy as the Main Reason for Mergers and Acquisitions in the Energy Sector

The “green economy” is a term that was first used in a report commissioned for development by the British government in 1989. That report, entitled Blueprint for a Green Economy [

7] (p. 192), was prepared primarily to determine whether there was a consensus definition of the term “sustainable development” and to identify the relationship between sustainable development and the measurement of economic progress [

8]. Indeed, the word “green” appears only in the title of this document, and there are no further references to environmental issues throughout the study. Follow-up reports issued in 1991 and 1994, entitled Blueprint 2: Greening the World Economy and Blueprint 3: Measuring Sustainable Development, respectively, deal with global issues in the context of ecology, highlighting climate change, the shrinking ozone layer, tropical deforestation, and the loss of natural resources. These led to the development of so-called green stimulus packages by the United Nations Environment Program (UNEP). UNEP has developed one of the priority definitions of green economy, identifying it is a set of activities aimed at improving human well-being and the realization of social equality, while at the same time meeting the postulate of reducing the risk of environmental hazards and the ecological shortages of natural resources [

8]. The green economy at its most basic level is a clean energy economy reflected in renewable energies (e.g., solar, wind, geothermal), green building and energy-efficiency technologies, energy-efficient infrastructure and transportation, and recycling and converting waste to energy [

9]. The green economy is not just about clean energy generation opportunities, but more significantly about new markets, new products that are created using new technologies, and the associated new processes that reduce an organization’s negative impact on the environment. Oceans, fresh air, and diversity of life are essential conditions for human life and well-being. If the public goods system is to avoid a tragedy of the goods that belong to everyone, it must coordinate norms of behavior that protect and enhance this common good [

10,

11,

12]. This is in opposition to the brown economy, which assumes unlimited economic growth, intensive use of natural resources, damage to biodiversity, over-consumption, and a lack of responsibility for the environment and future generations [

13,

14]. The key moment for the development of this trend in global economies was the economic crisis of 2008–2010, considered the biggest crash since the crisis of the 1930s. The European Economic Recovery Plan was based on two main grounds, one of which concerned the increase in the competitiveness of the European Union economy in the long term as a result of dynamic growth in innovative, green, and energy-efficient solutions. This point became critical in the process of sustainable development, one of the ways of which was the green economy. The green economy ensures growth through the creation of an adequate number of jobs, eliminating the impoverishment of society through investments in the protection of natural capital, which is a low-carbon economy, resource-efficient, and socially inclusive [

15].

Green economy applies to [

16]:

Green products and services, i.e., those that throughout their life cycles have little impact on the environment because of the use of harmless components and are easily recycled after use [

17];

Green investments—related to the construction of self-sufficient facilities in terms of energy, or to the use in production processes of machinery and equipment that are efficient in terms of energy or raw materials [

18]. A company’s strategy to focus on green investment is to gain and maintain stakeholders’ acceptance and support. In this way, a company manages the negative environmental impacts of its operations by reducing energy consumption and carbon emissions [

19,

20];

Green economy sectors, i.e., such production that is environmentally friendly, commonly associated with agriculture, forestry, and animal husbandry, but also and primarily related to renewable energy and its widespread use in global economies;

Green public procurement [

21], i.e., a policy under which public entities integrate ecological criteria and/or requirements into the purchasing process (public procurement procedures) and look for solutions that minimize the negative impact of products/services on the environment and take into account the entire life cycle of the products; by doing so, they influence the development and dissemination of environmental technologies [

22]. The aim of green public procurement is to integrate environmental considerations into tender procedures, which is reflected in the tender criteria; in particular, it draws attention to their quality, functionality, technical parameters, and the use of the best technologies in terms of environmental impact [

23];

Green jobs, which are created as part of projects aimed at reducing the environmental pressure of the economy and consumption, are created in every sector of the economy and the only condition they must meet is to prevent harmful effects on the environment [

24]; green jobs are directly related to the concept of sustainable development, i.e., economic growth associated with environmental protection and respect for human dignity—people become the subjects of such development, and the level of environmental degradation depends on their activity in terms of using natural resources in a sustainable way [

25]. The European Commission (2018) specifies that “a green job is one that directly deals with information, technologies, or materials that preserves or restores environmental quality. This requires specialized skills, knowledge, training, or experience (e.g., verifying compliance with environmental legislation, monitoring resource efficiency within the company, promoting and selling green products and services)” [

26].

Green economy is most often identified with sectors (e.g., energy), general issues (e.g., pollution), and principles and policies in which economic instruments affecting the degree of socio-economic development in the context of the role of the environment are of key importance. The priorities in terms of creating a green economy are (a) the development of renewable energy sources, (b) increasing energy efficiency in individual sectors of the economy, production, and service facilities, as well as households, (c) restructuring industry (especially traditional industry), and (d) creating new, environmentally friendly branches of the economy [

27] (p. 122). Furthermore, activities related to the development of the environmental goods and services sector (EGSS) are also highlighted, as are the already mentioned green jobs. In the discussed area, innovation, in particular eco-innovation, that aims to reduce pollution is of great importance in the microeconomic aspect, the enterprise, as well as in the macroeconomic aspect, the whole economy [

28].

Green economy is oriented toward renewable energy sources, the so-called green energy sources [

29], which are the subject of many climate conferences and symposiums. Such a turning point for the development of the renewable energy sector was the 2015 conference in Paris (COP21), which resulted in the signing of the Paris Agreement and the cooperation of countries from around the world. The long-term goal of the agreement is to stop the global average temperature from rising to below 2 °C compared to pre-industrial times and to take measures to keep it below 1.5 °C. The agreement came into force on 4 November 2016, when at least 55 countries responsible for at least 55% of global greenhouse gas emissions ratified the agreement’s findings, and it has since been ratified by all European Union countries [

30]. The Paris Agreement set a major challenge for Europe, according to which the continent is to become the world’s first climate-neutral geographic area by 2050. The green transition is described by a set of mechanisms and associated actions, outlined in the European Green Deal on 11 December 2019. The document outlines energy strategies for a safe, sustainable, and low-carbon economy [

31], and its effects are already being seen in the rise of renewable energy deals as consolidations in the value chain and increased deal activity in the energy industry. It turns out that 144 of the 174 M&A deals since December 2020 involved renewable energy assets or companies [

32].

These transactions represent a response from the market to the necessity of transformation from a brown to a green economy. It is a path that requires active environmental management (risk management, investment in natural capital), realization of environmental sustainability (eco-efficiency), and the decoupling of economic growth from increasing resource consumption through innovation and demand shift [

33]. Accordingly, the aim of the research, which was to identify the motives for mergers and acquisitions in the energy sector after the introduction of green economy elements in Western Europe, was identified. We assume that there is a high probability that these market transactions were triggered by a change in environmental policy worldwide.

3. Review of Selected Research Results on the Motives of Mergers and Acquisitions in the Energy Sector

Business acquisitions are undertaken based on several motives of a different nature and arising from different sources. It should also be remembered that it is rare for such processes to be determined by single motives. Such complex processes are most often the result of bundled motives, in which profit and development are the dominant ones in this case.

The motives for concluding M&A transactions can also be divided into offensive and defensive ones. The former direct the buyer to take over a significant number of entities from various market segments in a not too-long period. They are used by entities with good financial conditions and strong market positions in which the managerial staff is characterized by a relatively high appetite for risk. The latter, defensive ones, are to help defend the company’s position in the face of increasing competition, protect the buyer’s export markets, and help avoid trade barriers [

34] (pp. 110–112).

The motives for the implementation of M&A processes can be divided, for example, into those that are external to a given entity, i.e., generated by the environment in which a given entity operates, and those that are internal, most often related to the pursuit of improving the functioning of the enterprise, generating new market opportunities, and gaining new competitive advantages. It is worth noting here that international mergers and acquisitions as methods of implementing the strategy of increasing the company’s international competitiveness are widely used in the energy sector. To confirm this fact, it is worth citing the data according to which the share of M&A in the energy sector amounted to 13.7% of all transactions in terms of value and 7.2% of the number of the most expensive transactions that took place in the years 1985–2015 in the world economy. The largest M&A transactions in the analyzed period took place in the United States, Great Britain, France, Canada, and Spain. For example, the largest deals in recent years were made between such market giants as Exxon Corp. and Mobil Corp. in 1998, Dutch Petroleum Co. and Shell Transport & Trading Co. in 2004, Royal Dutch Shell PLC and BG Group PLC in 2015, and General Electric Co. and Baker Hughes Inc. in 2016. This trend not only covers the broadly understood traditional energy sector but increasingly continues to apply to actors in the field of renewable energy, especially solar and wind energy [

3,

35]. It is worth noting that there are fundamentally different motives that drive the actions of buyers—this is what we will focus on in this article—while other motives are behind the actions of sellers [

36,

37].

When analyzing M&A motives of an external nature, it should be remembered that the energy market is created by both domestic, macro-regional energy systems, industry markets, and the actions of global players both in terms of supply and demand [

38]. Therefore, on the list of external motives of M&A processes, determining the “buy” answer to a typical question about the ways of company development, “Make or buy?”, the following should be mentioned first of all [

2,

3,

39,

40,

41,

42,

43]:

Globalization of sales markets, related to the uniformization and californiation of needs;

Technological globalization, especially in the most expansive industries; implementation of the Smart Grid concept in energy systems, significantly affecting the cost side of energy production;

A massive increase in energy demand and, at the same time, a special development, also with the support of the state, of some energy sources (shale gas, liquefied natural gas, nuclear, and renewable energy) with a simultaneous decrease in the use of coal;

Denationalization, demonopolization, and privatization in the energy sector and a striving to diversify the sources of energy supplies;

Striving to maximize the scale and scope of production to be able to compete in global markets;

Emphasis on ecology and, hence, stringent environmental requirements and emission obligations in the energy supplier sector, including subsequent international agreements, such as the Paris Climate Agreement of 22 April 2016 on the regulation of activities aimed at reducing carbon dioxide emissions, or the program adopted in New York in September 2015 for ensuring a sustainable future and sustainable development goals—significantly increasing the interest in markets with access to “clean energy”, but also significantly increasing the costs of energy companies;

Growing economic and political unrest: oil and currency crises, high business cycle volatility, shortening of product life cycles, and COVID-19.

Internal motives for which the buyer undertakes M&A activities can be divided into several groups. First of all, these are technical and operational motives, among which special attention should be paid to increasing the efficiency of management, which may take place because of various restructuring activities undertaken in the combined entity as part of post-trade integration. This may be, for example, the introduction of new products to the portfolio, technology transfer and capability [

4,

44], abandoning activities of marginal importance, or changing strategic priorities. Another particularly important motive from this group is the pursuit of benefits related to operational synergy [

45]. This can happen, for example, because of the economies of scale—when the acquisition takes place horizontally and concerns competitors [

46] or because of technical integration within processes carried out in a vertical system. It is worth noting that the motives related to the pursuit of synergy effects and, thus, the reduction of operating costs were the dominant motives in the energy sector in the case of transactions concluded in 1995–2010 [

2,

47,

48].

The second large group of motives for the implementation of M&A processes are market and marketing motives. They are primarily a manifestation of the desire to increase the potential [

49,

50] for building a dominant position for the future, so that in the conditions of global competition they use what globalization provides and do not lose by it. This position can be built by increasing market share, eliminating competition, increasing added value, increasing originality, filling gaps in the product portfolio, and even entering completely new areas of activity [

51]. It is this group of motives that in the last decade has become the main driver of companies from the energy sector toward concluding M&A transactions. Transactions of this type are now providing entities in this sector with greater development opportunities, ensuring supply in the face of the significantly increasing demand for green energy and the progressive transformation of the energy sector toward renewable sources [

2].

Another important group of M&A motives are financial. Within this group of motives, it is worth distinguishing two in a special way. The first is to make a better valuation of the value of the acquired company in relation to that made by the market. An entity whose value is underestimated by the market is, thus, particularly attractive to a potential buyer, the purchase of which is, in a way, a market opportunity worth exploiting. In the second case, it is about tax savings—the acquisition of a company incurring a loss can be used to reduce the taxation of profit after the acquisition. Other reasons for this type of transaction of a financial nature include, for example, an increase in the possibility of incurring liabilities in the case of merged entities, or the possibility of using cheaper sources of financing because the transaction lowers the risk for lenders [

52]. What is characteristic of transactions concluded based on financial motives is that the intended effects of these transactions can be achieved even in the absence of other benefits from the M&A process. Their fulfillment does not require difficult, costly, and, importantly, often unsuccessful post-transaction integration. Although this group of motives often becomes the basis for concluding M&A transactions in other sectors, it seems to be of less importance in the energy sector [

53,

54].

The last group of motives driving buyers in M&A processes are managerial. Among other motives, the latter, although they are not of great importance for the shareholders themselves, often do not provide greater chances for the company’s success in the future, but they are a particularly important element of the global puzzle that determines the choice of this form of company development. Importantly, in the case of this type of process, there may also be problems described in the framework of the agency theory, consisting of a significant difference between the motives of the owners of the entity and the motives of the managers they employ [

55].

The abovementioned classification of the M&A motives was prepared based on the work of M. Lewandowski [

56]. These motives include, for example, an increase in the prestige and power of management associated with sitting on the management board of a much larger entity, which is growing at an exponential pace, and thus a significant increase in remuneration, as well as a lowering of the level of management risk and an increase of the freedom to act in the face of potentially diluting shareholding [

56,

57] (pp. 80–81). The problem is smaller, if these motives fulfill a complementary function, in which case they may even be desirable, as they may constitute an additional bonus, building the involvement of the managerial staff in the implementation of the process. Such a situation may occur, for example, as part of an MBO management buyout transaction [

58]. What is worse is when these motives become dominant, in the absence of other justifications of the sensibility of the transaction. Such cases can most often be dealt with at times of significant increases of the occurrence of this type of process within successive M&A waves when emotional motives begin to dominate rational analysis. As economic history teaches, this usually ends in a deplorable manner.

4. Research Procedure

The research procedure proposed in this paper was prepared based on the proprietary model of identifying M&A motives. The model used in this work was designed and developed as part of the research method used in the research, “The development of the technology companies. The M&A perspective” [

6]. This qualitative research method derives from various data sources, maximizing chance to accurately identify the leading motives behind each M&A transaction. The main goal is to verify the hypothesis provided in the previous part of this paper. First, the authors aim to identify the leading M&A motives behind M&A transactions conducted by Western European companies from the electrical energy generation sector and identify how those motives have been changing within the last 7 years as a result of the Paris Agreement on climate change, accepted by the world leaders during the 2015 United Nations Climate Change Conference. This will allow us to verify the hypothesis that the themes of mergers and acquisitions have changed from motives close to the views related to energy generation in traditional systems (black energy in large monopolistic systems) to motives close to green energy, and to understand how the companies operating in the electrical energy generation sector reacted to the agreement and how it changed their overall, long-term strategies. Moreover, by analyzing the leading motives behind the M&A transactions, the authors aim to identify the key M&A motive changes in particular Western European countries.

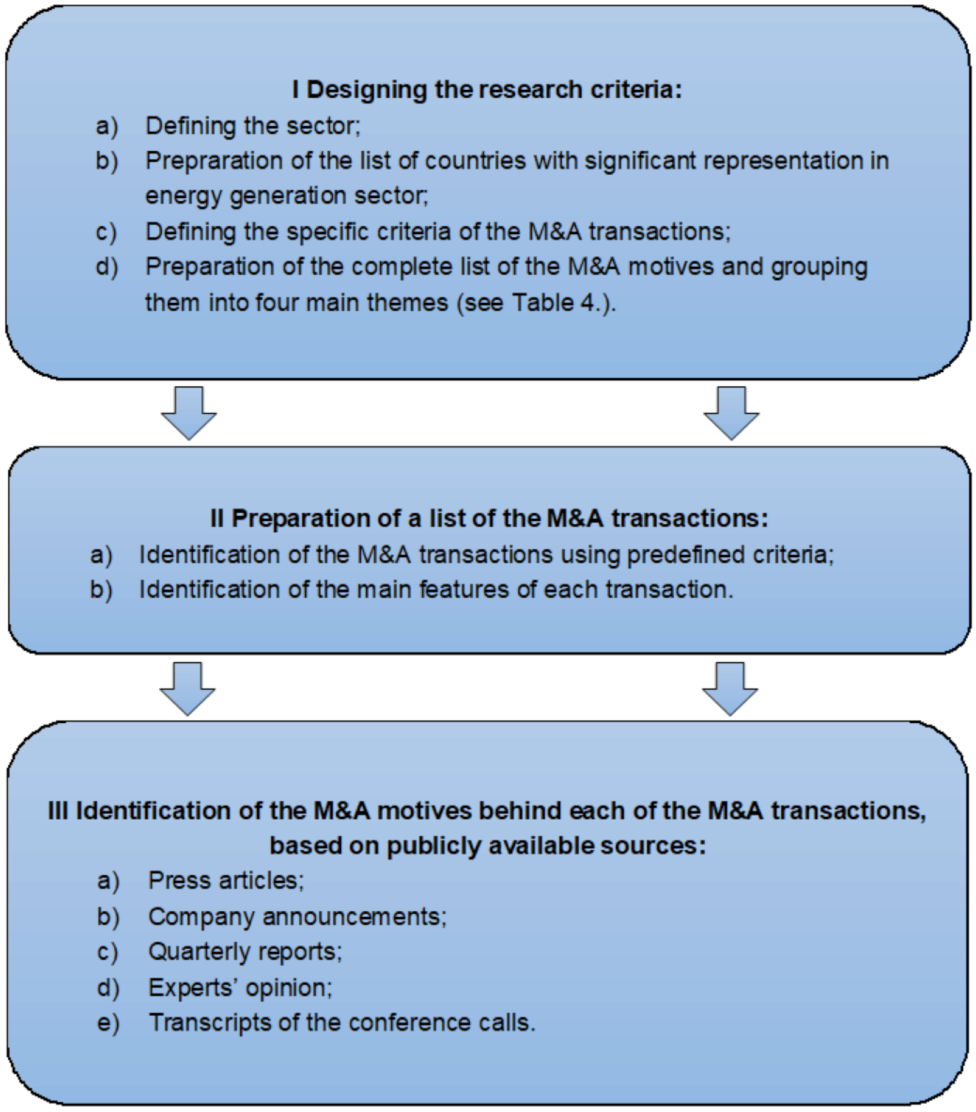

To achieve those goals the authors proposed the research procedure described in

Figure 1 below. The research procedure was divided into three main stages: designing the research criteria, preparing the list of M&A transactions, and identifying the motives behind the M&A transactions.

In the first part, the authors defined the clear boundaries of the sector. Many companies are operating in energy-related sectors; however, their main source of revenue varies from electricity distribution or transmission to oil, gas, or coal exploration. For the purpose of this research, the authors focused on companies making revenues predominantly from electrical energy generation utilities. As defined above, only companies from Western European countries were included in the scope of this research. The authors focused on the biggest economies in the region, based on the country populations (including the most populated countries) and the strategically significant roles of the companies from the sector (the number of companies, their market value and revenues). Representatives from the following countries were included in the scope of this research: Germany, France, the United Kingdom, Italy, Spain, Switzerland, Denmark, Norway, and Luxembourg. Due to data limitation, the authors focused on M&A transactions conducted by public companies only because of various regulatory obligations around transparency and disclosure to all shareholders of the rationale behind strategic decisions. Such an approach will significantly increase a chance for accurate identification of the strategic rationale behind each M&A transaction and help to understand the true M&A motives. The last step of the first stage of the research procedure was to prepare the comprehensive list of the possible motives behind M&A transactions, which were then grouped into four main themes: operational, market, financial, and managerial motives.

The second part of the research procedure related to the list of M&A transactions was research sample. Using publicly available data sourced through a search engine (Google Search) from news articles, press releases, and companies’ reports, the authors identified a list of the M&A transactions announced from 1 January 2015 to 19 November 2021 by the Western European companies operating in the electrical energy generation sector. For the purpose of this paper, an M&A transaction was defined as an investment in a target company or strategic asset, after which the acquirer will procure at least a 51% shareholding in the target company or strategic asset. Then, using various publicly available data sources, the authors harvested the data (such as the value of the transaction and the country of the target company/asset) about each transaction.

Last, using various similar publicly available data sources, each transaction was analyzed to identify the M&A motives. For each transaction, the authors identified two M&A motives: one leading and one secondary. To maximize the chances of accurately identifying the M&A motives, the following data sources were analyzed:

News articles;

Press releases;

Companies’ quarterly reports;

Transcripts of the calls from the press conferences held because of an M&A transaction announcement;

Experts’ opinions—the study enabled the expansion of knowledge in the field of M&A motives of the companies from the electricity generation sector, helping to verify the hypothesis, and it included information about:

The most common M&A motives in the electrical energy generation sector;

How those motives have been changing over the last 6 years, since the Paris Agreement on climate change;

The differences between M&A motives in transactions conducted by companies from different Western European countries.

5. Results of Our Own Research of the M&A Motives Identified in the M&A Transactions Conducted by Companies from the Electrical Energy Generation Sector

The authors analyzed 95 announced M&A transactions conducted by public Western European companies during the period from 1 January 2015 to 19 November 2021.

Table 1 below presents the key information about the research sample: the number of transactions, the biggest transaction (based on the value of the M&A transaction), the number of transactions announced by representatives of each Western European country, and the number of M&A transactions announced every year. The research sample was dominated by three holding companies: Electricite de France SA and Engie SA from France, and the Drax Group from the United Kingdom. Together they were responsible for conducting 52 M&A transactions in a given period. Electricite de France SA, French-state-owned, is one of world’s top electric utilities producing, transmitting, distributing, importing, and exporting electricity. Engie SA produces, transports, stores, and distributes natural gas. It also offers energy management and engineering services. The Drax Group is a UK renewable energy company.

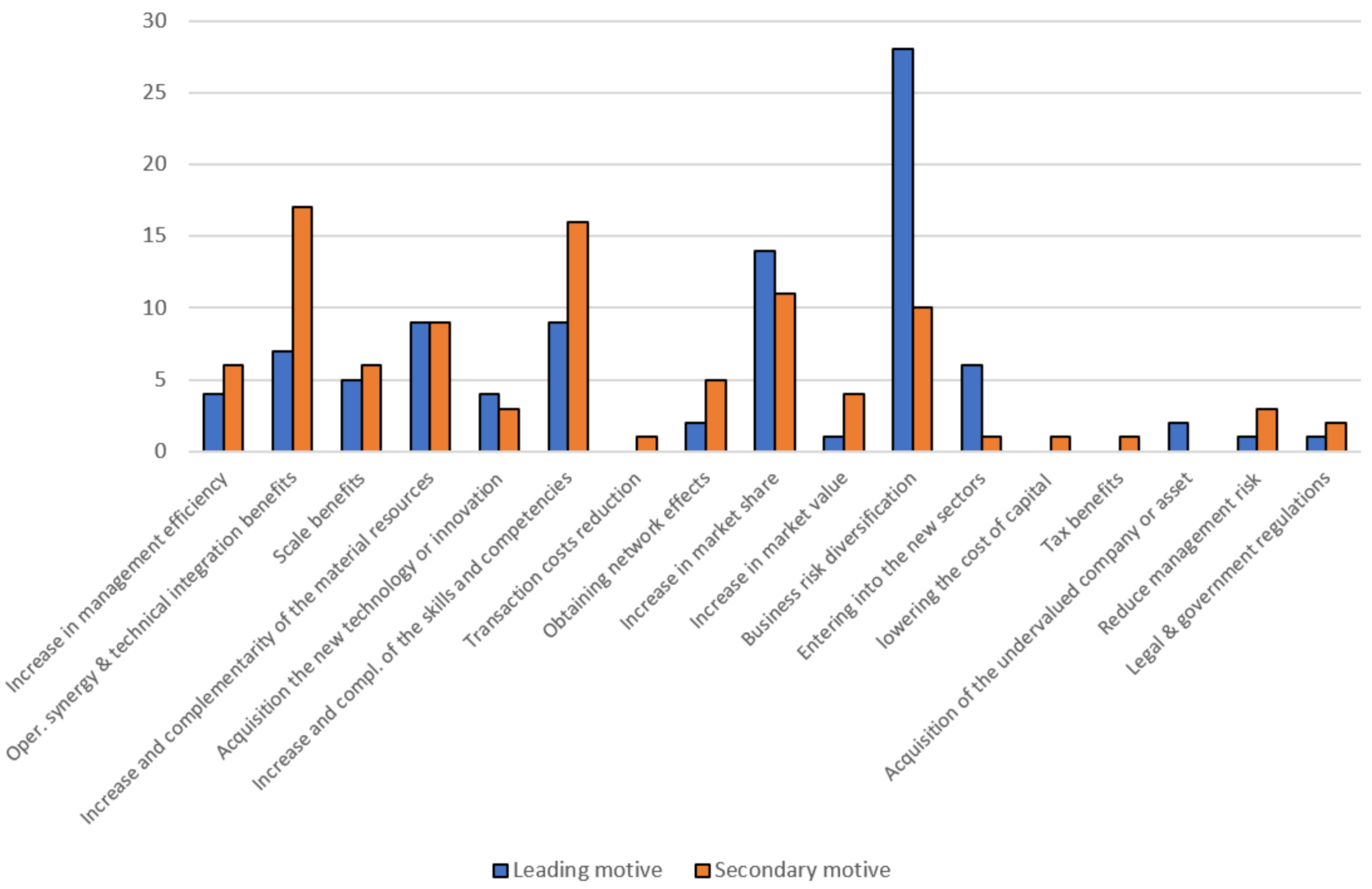

The identified motives were divided into two categories: leading and secondary. The results of the analysis are presented in

Figure 2 below. The most popular M&A motive, identified as the leading motive of 28 M&A transactions and as a secondary motive of 10, was “business risk diversification”. This motive was observed predominantly in the M&A transactions in which the acquirer was purchasing another company or strategic assets operating in green energy, i.e., wind or solar panel farms. Very often, companies decided to conduct an M&A transaction to acquire new electrical energy generation assets, to strengthen production capacity, diversify the source of the energy (wind farms, solar panels, etc.), and spread the business across different jurisdictions to diversify the risk in relation to weather conditions. Another popular motive refers to an increase in market share, usually while entering new, geographical markets or consolidating the market through the acquisition of small energy-generating companies. Operational synergy and technical integration benefits were the most popular secondary M&A motives. Companies from the electrical energy generation sector quite often acquire companies that provide services from earlier parts of the sector value chain, so as to reduce the risk related to relying on suppliers or to combine the technical knowledge from the synergy. Another popular secondary motive was the “increase and complementarity of the skills and competencies”.

The 2015 United Nations Climate Change Conference was held at the end of that year. The authors analyzed the motives behind the M&A transactions in the years 2015–2021 to identify changes in the most important motives driving the transactions. The calculations were made based on how often the specific motives were identified as leading or as secondary in all M&A transactions announced in a given year. For most of the analyzed period, business risk diversification was the most important motive, as presented in

Table 2. Companies usually tried to diversify their energy production capacities by acquiring other plants and farms, and use their renewable energy sources. This slightly changed during the years 2019 and 2020 when it was classified (respectively) as the third and second most important motives. Another motive, which has been gaining significance in the last 4 years, is the increase in market share, proving the ongoing consolidation across the sector.

As discussed earlier, the research samples were dominated by the French and United Kingdom companies, but also by those from Germany, Spain, and Italy. M&A transactions conducted by companies from those countries accounted for 87% of the M&A transactions included in the research sample.

Table 3 below presents the most important M&A motives identified in transactions conducted by companies from a given country. Business risk diversification was the dominant motive in M&A conducted by Spanish, British, and Italian companies. French companies were usually driven by the increase and complementarity of skills and competencies and German ones by operational synergy and the technical integration benefits. In some of the countries taken into consideration, it is possible to identify differences in the indication of M&A motives. They may result from the specific features of the current energy economies conducted in these countries. France is such an example because the energy sector is dominated by a few companies, which are historically used and owned by the government. Moreover, nuclear energy still has a high share in the sector. Most of the analyzed M&A transactions of the French companies allude to the use of the possessed competences to develop the economies of scale of the already possessed potential, mainly hydropower, and only recently of the purchase of wind farms. That is why the “business risk diversification” motive is the second most important M&A motive. In Spain (similarly to South America), the M&A transactions are predominantly purchases of solar and wind farms. Again, this is determined by the current development directions of the energy sector, which is mainly in the geographical dimension (increases in the market shares in Spain and South America). The ban on the development of nuclear energy and compulsory decommissioning of nuclear power plants introduced in 2002 had a decisive influence on the development of the energy sector in Germany [

59]. Hence, the motives of M&A mainly come back to operational and technological changes in the sector. In the United Kingdom and Italy, the main motives are in line with the overall results for the entire analyzed group of transactions. This is due to the lack of fossil fuels in these countries (except the gas from the North Sea) and the need to comply with green-energy directives without any historical or geographic restrictions.

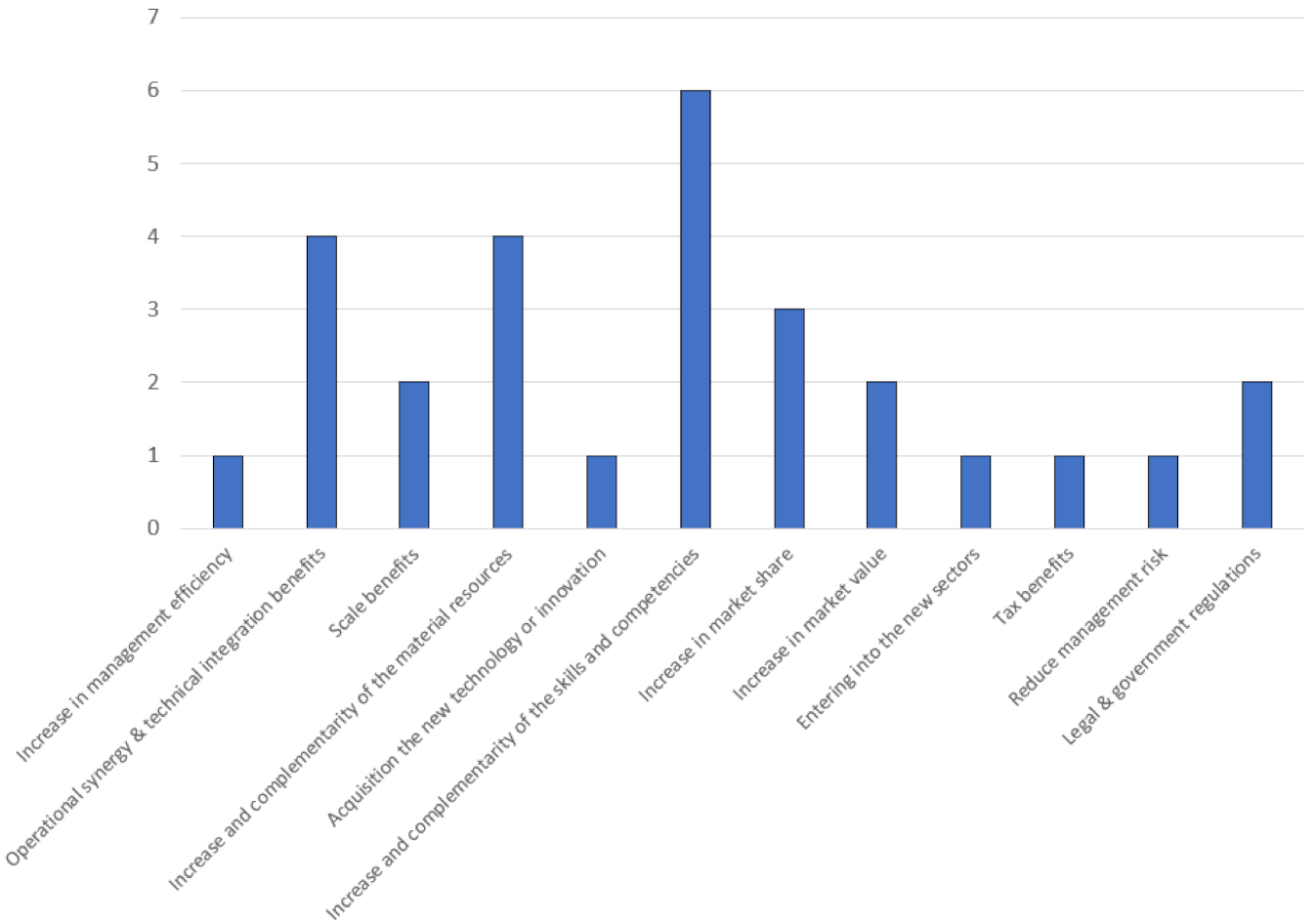

As presented above, business risk diversification was the most popular M&A motive identified in a research sample. The authors analyzed what secondary motives usually accompanied those transactions. The results presented in

Figure 3 below show that the following three motives were identified the most often: the increase and complementarity of skills and competencies, operational synergy and the technical integration benefits, and the increase and complementarity of the material resources.

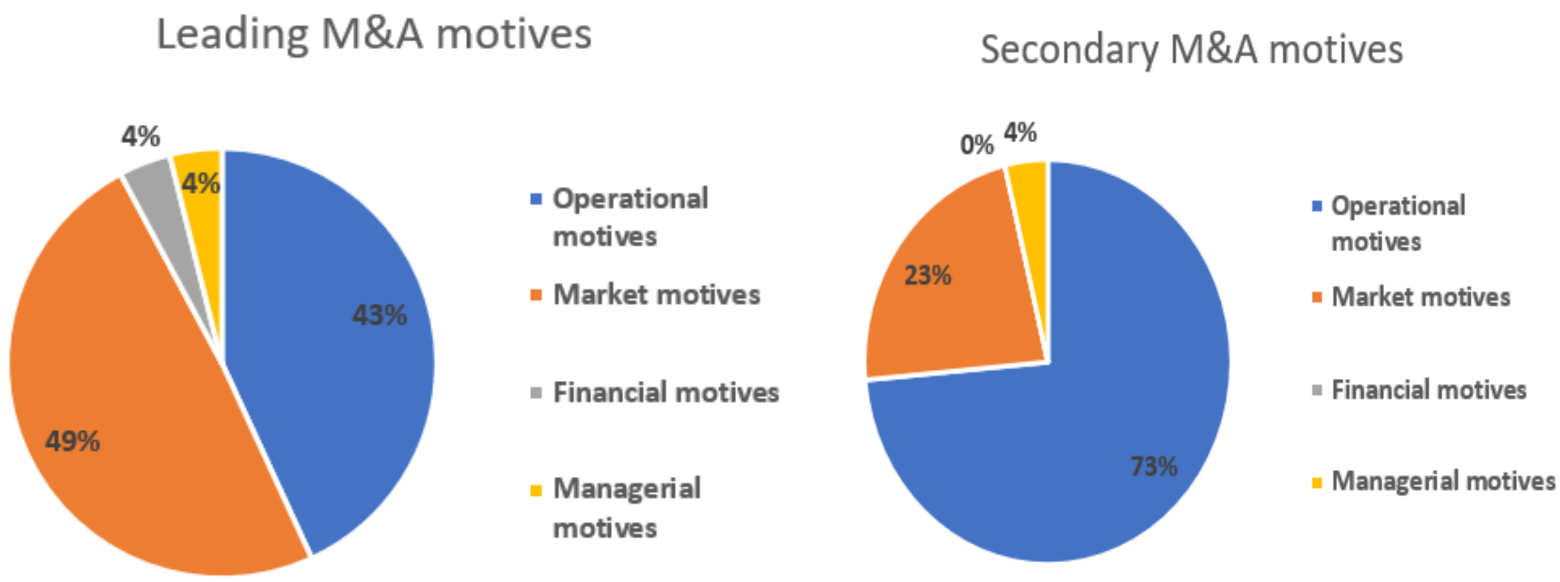

The M&A motives presented in the previous part of this paper were classified into specific M&A motive categories, as presented in

Section 3. The operational motives refer to operational activities conducted by the company. Market motives are related to the competitive position of the company in the sector. Financial motives include taking advantage of the current, good financial position of the company, and the opportunity to acquire undervalued assets or to get bargain power in relation to getting funding with better conditions. Managerial motives usually refer to the personal motives of the senior management of the acquiring company.

Finally, all the motives behind M&A transactions, grouped in line with the categories described above, were analyzed from the perspective of being the leading or secondary motives. The results are presented in

Figure 4 below. The frequency of market and operational motives being the leading M&A motives was similar (49% vs. 43%); however, a significant difference was observed in relation to secondary M&A motives, as 73% of those motives were classified as operational M&A motives.

6. Discussion and Conclusions

6.1. Discussion of the Results

Pursuing the goal set out at the beginning of the article, which was to define the main motives for the implementation of M&A processes in the energy sector in Western Europe after the introduction of green economy elements, by looking at the results of the empirical research presented in the article, we can conclude that entities in this sector undertake such activities mainly for the purpose of achieving a stabilization of activities based on the diversification of business risk. This may be related to the fact that this risk undergoes numerous changes resulting from the transformation of this sector toward increasing the use of renewable energy sources and reducing greenhouse gas emissions. Government regulations and the influence of political factors make the environment of energy enterprises less and less stable. Entering a new sector or increasing market share, which have emerged as the leading premises for mergers and acquisitions, are, from the point of view of strategic decisions, expressions of a striving to strengthen one’s position and, indirectly, to reduce risk. Thus, market motives overtook operational motives, which were considered more significant in the period from 1995 to 2010 [

2]. In this way, the authors verified the hypothesis with regards to the change of strategic priorities—from those related to development within the so-called black energy toward building the potential of entities in the area of green methods of production. It should be remembered, however, that the competitiveness of energy entities in Europe is embedded in the fabric of international agreements related to energy exchange, in which the largest market players have the best negotiating positions. Therefore, some operational motives remained important, as the use of economies of scale or targeting the use of network effects contribute to a certain extent, though not as much as they once did, to achieving greater efficiency while increasing the value of the enterprise [

2]. To summarize, the tendency toward mergers and acquisitions in the energy sector is significant and well-grounded in market conditions. Building a market position indirectly translates into operational efficiency grounded in access to complementary technical resources, including a limited transmission network. A large entity that builds a synergy of cooperation with other entities through acquisition and integration may obtain much better rates and operational capacities in energy exchange. Due to an inability to store energy from renewable energy sources, access to the transport layer is becoming one of the most important factors in building operational efficiency. It should also be emphasized that modern technologies, e.g., smart grids, IoT, or asset management systems, which allow us to solve many operational problems faced by energy companies undergoing transformation, are of increasing importance. Excess employment, the requirement of dispersed supervision, and the modernization of assets, or the need to cope with modern methods of energy exchange, are difficult challenges for the majority of large state-owned energy entities. The acquisitions dictated by technological considerations are therefore a natural response to this situation.

The generally low level of interest rates in European countries that lasted from 2015 to 2020 and the related availability of capital were conducive to mergers and acquisitions in the energy market. Therefore, financial motives appeared in a significant minority and were more a use of market opportunities than of efforts to improve the financial condition of enterprises. However, their importance cannot be ignored because M&A transactions in the pure energy sector are characterized by high value, so the premises related to financial optimization in the field of taxes, cash surplus, or the lowering of the cost of capital take place here. When taking over smaller technological entities, in connection with increasing operational efficiency, we deal with smaller transactions with operational motives that are more visible than the financial motives, which is also reflected in the presented research results.

The last group of analyzed motives were the managerial motives, which, although in a minority, held a stable position in both groups of primary and secondary M&A motives. This is dictated by the fact that the government has a fundamental influence on energy companies and the managers of these companies. In this case, one can observe the tendency to increase the scope of the power, remuneration, and general prestige of the company, while maintaining compliance with all regulations resulting from the laws of a given country.

6.2. Conclusions

Summarizing the obtained results, we can state that they emphasize the importance of mergers and acquisitions in the energy sector. They are becoming an important element of the energy companies’ responses to changes in the environment. This variability is a derivative of government decisions resulting from international agreements. In response to these changes, over which enterprises have little influence, decisions are made on a market basis to increase the competitiveness and efficiency of the entities’ operations. Market motives are now becoming key. The most important M&A theme, however, is related primarily to the pursuit of diversification of business risk, which is conditioned by the need to maintain the energy security of economies, as well as a response to the changing environmental conditions related to the transformation of the energy sector. Therefore, the most important practical conclusion from the research is the confirmation of the changes taking place in the energy sector related to the departure from coal-based energy toward changes initiated at the conference in Paris in 2015. The identified M&A motives clearly indicate this direction of change. Since the analysis concerned mergers and acquisitions in highly developed countries, it should be expected that these changes will take place in other countries as well. However, this should be the subject of further research. The presented conclusions are the most important practical contributions. They are all the more important in a situation where the importance of the energy sector in the world and its impact on other sectors of the economy is growing.

In the conducted research, the analysis of the available documentation was used and the evaluations of the transactions were carried out on its basis, taking into account the dominant motives for conducting them. The proposed methodological approach allows us to confirm the adopted hypothesis for the analyzed group of transactions.

The most valuable, theoretical part of the research is the analysis of the factors influencing the choice of the M&A motives. The research analyzed the impact of changes resulting from radical changes in the world’s energy policy. The results obtained from a well-defined group of analyzed mergers and acquisitions (key countries, key companies, and significant transaction value) allowed the credibility of the study to increase. Therefore, it is worth emphasizing the selection of the sample. This is a significant contribution to this work.

In the literature on the subject, there is little research aimed at identifying the motives for transforming economic sectors. Most often, the subject of research are entire sectors, but without indicating specific contexts. The proposed research fills this gap. It indicates the need to analyze M&A motives in the context of the impact of specific factors that may trigger such changes. In this way, we obtain results that allow us to evaluate the effectiveness of the impact of selected factors. This is also a significant value of this research from the perspective of the theory of scientific research.

The conducted research also proves the usefulness of the proposed method of examining the use of open-source intelligence elements, in this case the analysis of press documents and financial results published in accordance with the rules of public markets. Public companies have to be transparent. In addition, their stock exchange indicators minimize the influence of many market and internal factors. Thanks to these features, we obtain certainty about the assessments of statements and opinions contained in these documents. Of course, this mainly applies to public companies, not to private companies. The energy sector in many countries is (and, in many, was) state-owned. This need and the usefulness of this type of research constitute other contributions of the research results contained in this work.

In the case of the energy sector analysis, this research it is worth continuing even for other groups of countries, continents, or countries selected according to the degree of their development, or for other countries, especially those that dominate the global economy in generating CO2, i.e., the USA and China. Moreover, it is worthwhile to continue this research to more precisely define the pace of internalization of macroeconomic factors by the energy sector. It is also worth indicating in subsequent studies which methods of exerting influence are the most effective. Were these changes determined, for example, by legal solutions or financial instruments in the form of CO2 certificates, or by the pressure of public opinion or of the media of social communication?

In the coming years, the energy sector will be a key sector of the world economy, where breakthrough innovations will take place, forced by the pressure of public opinion on environmental activities. This is also the sector in which completely new business models of energy generation, transmission, and consumption will be created. It is here that the key decision will finally have to be made about whether the energy sector must still be a regulated or a market sector. At the same time, marketization does not have to be pejorative. In modern economies, the market character can mean sustainable development, the development of alignment with ecosystem strategies, and development positively influencing the development of other sectors. Treating the energy sector as a sector in the service of other sectors unnecessarily destroys the reputation of the sector as a sector that can be a vehicle for development and progress. In the opinion of the authors, the above-mentioned challenges can and should be the subject of further research.

,

,

{kind=link}

{kind=link}

{kind=link}

{kind=link}