Assessment of the Target Model Implementation in the Wholesale Electricity Market of Greece

1

School of Economics, Aristotle University of Thessaloniki, 54124 Thessaloniki, Greece

2

School of Management, Audencia Business School, 44300 Nantes, France

3

School of Informatics, Aristotle University of Thessaloniki, 54124 Thessaloniki, Greece

*

Author to whom correspondence should be addressed.

Energies 2021, 14(19), 6397; https://doi.org/10.3390/en14196397

Submission received: 29 July 2021

/

Revised: 13 September 2021

/

Accepted: 27 September 2021

/

Published: 6 October 2021

(This article belongs to the Special Issue Emerging Trends in Energy Economics)

Abstract

:The European Union Target Model aims to integrate European energy market by removing barriers to trade and align markets. The most important goals of the Target Model are to provide consistent prices, enhance liquidity, support cross boarder trading, facilitate interconnections, and coordinate the use of transmission system capacity. In that context, the smooth operation of both forward and spot markets is a core development that directly affects the good operation of the wholesale market. This paper examines the application of the Target Model in the wholesale electricity market of Greece and its impact on electricity prices. The study explores the time period before the implementation of the Target Model, which took place on November 2020, and the first nine months of its execution. Based on the feedback received by the rest of the European countries, which are already part of the European Single Market, this crucial period of time is considered transitional, when many distortions and unethical behaviors take place. Empirical findings indicate a relatively successful implementation of the Target Model in Greece, with price disorders mostly met in the Balancing Market.

1. Introduction

Since 1996, the European Union (EU) aims to harmonize and liberalize the internal energy market, by adopting a list of measures to eventually create the “Single European Energy Market”. The need to strengthen competition for the benefit of final consumers via reliable prices, transparency, and reliability are some of the key factors that have pushed Europe to support cross-border electricity trade among Member States. The Target Model is the official tool that Member States need to implement towards the completion of the Single Market. Prior to that, most of the countries operated their wholesale electricity markets according to the guidelines of a Mandatory Pool model.

The EU Target Model is based on two broad principles: (i) the development of integrated regional wholesale markets, preferably established on a zonal basis, in which prices provide important signals for generators’ operational and investment decisions; and (ii) market coupling based on the so-called ‘flow-based’ capacity calculation, a method that takes into account that electricity can flow via different paths and optimize the representation of available capacities in meshed electricity grids. More information on the Target Model are available online: https://eur-lex.europa.eu/legalcontent/bg/TXT/?uri=CELEX:52017SC0383 (accessed on 13 September 2021), In general, Market Coupling, which is a crucial component of the Target Model refers to the interconnected cross-border electricity market among the Member States of the European Union. Through the physical interconnection among them, the flow of electricity takes place based on the optimal and shortest route from various production sources towards the final consumer. According to [1], discrepancies between regulatory policies and market designs could distort the normal functioning of the neighboring markets and security of supply. Market Coupling is based on Price Coupling of Regions (PCR), Flow-Based Market Coupling, and the Cross-Border Intraday (XBID) Project. In line with [2], by maximizing the use of cross-border interconnection capacity, market coupling increases the level of market integration and facilitates the access to low-cost generation by consumers located in high-cost generation countries. Thus, it is expected that a high-priced area could greatly benefit from the introduction of this mechanism. Existing literature supports the above argument [3,4].

To achieve market coupling, and for the benefit of all participants, the Mandatory pool was gradually replaced across Europe by the Target model (the Commission pursues the vision of a ‘Target Model’ using a European governance process (Third package, Directive 2009/72/EC.)). The ultimate goal of the Target Model is to enable the energy produced in one country to be delivered to another Member State participating in this Model. The Member States of the European Union are committed to complying with the fundamental principles which ensure a level playing field. Cross-border electricity trade initially takes place at a regional level and aims to achieve pan-European market coupling and consequently convergence to a single electricity price for the whole of Europe [5]. A prerequisite for the smooth operation of the model is the coordination of national actions between neighboring countries, and the optimal exploitation of cross-border electricity transactions. The implementation of the Target model envisages the creation of four new electricity markets that operate on an energy exchange. Given the above, the purpose of the Target model is to promote competition, convergence of energy prices with the prices of neighboring countries and increase of the overall welfare in the economy. However, considering the case of Greece, the implementation of the Target Model, that took place on the 1 November 2020, provides mixed results [6]. In theory, the goal of a Single European Energy Market is to favor end consumers. However, wholesale electricity prices in Greece have more than doubled since the beginning of November 2020. This sharp rise is partially attributed to the peculiarities of the introduced model, since both marker participants and regulators broadly accept that the market was not completely prepared for that fundamental shift [7,8,9].

This paper examines the application of the Target Model in the wholesale electricity market of Greece and its impact on electricity prices. To our knowledge, this is the first study to analyze and evaluate this application. The study explores the time period before the implementation of the Target Model and the first nine months of its execution. Based on the feedback received by the rest of the European countries, which are already part of the European Single Market, this transitional period of time is considered crucial, when many distortions and unethical behaviors take place. Empirical findings indicate a relatively successful implementation of the Target Model in Greece, with price disorders mostly met in the Balancing Market. However, those increased prices have caused great market turmoil and unbearable pressure on businesses and small suppliers who are unable to cope financially with the unprecedented situation.

A plethora of academic papers have reviewed the efficiency of Target Model implementation in various counties across Europe. As a starting point, Ref. [10] provides an overall estimation considering the benefits of Target Model implementation across Europe. The authors highlight that additional improvements are feasible by reducing unscheduled flows and preventing the curtailment of renewables with improved market design. In general, the study underlines the necessity to assist interconnections and cross-border trading, given that the final outcome, via the provision of balancing services, leads to increased gains for the overall economy. Based on the challenge to achieve a common electricity market design in a multi-regional context, Ref. [11] analyzed how diverse design approaches, such as cross-border congestion management and capacity mechanisms, affect generation adequacy and welfare in Europe. Their findings confirm the benefits of market coupling in terms of welfare as well as generation adequacy. Earlier investigations of the effectiveness of a common electricity market design suggested a partial successful [12,13,14,15]. However, recent studies are clearly in favor of the effectiveness of a Single Electricity Market across Europe [16,17,18]. For instance, Ref. [19] argue that investment in interconnection reduces wholesale electricity prices in France and Ireland as well as the net revenues of thermal generators.

Considering country-by-country analysis, Ref. [2] evaluated the impact of the Target Model in the Italian electricity market and estimated the welfare benefits using various scenarios. The study concludes that a welfare increase is apparent when market fundamentals are tight. Next, Ref. [20] examined the evolution of the Irish Single Electricity Market under the European Target Model for electricity. The authors focused on the theoretical and practical circumstances under which derivatives markets stimulate competition in the spot and retail markets. In addition, the authors examined the impact of market concentration on the new capacity payment mechanism, and, eventually, provided specific proposals towards the regulatory authorities to enhance the overall performance of the wholesale market. The authors conclude that regulators should promote competition in the forward market and at the same time extend regulation to the price and quantity that the dominant firm bids.

Another study, considering the case of Britain, [21], investigates the EU Target Electricity Model and its effectiveness before and after 2015. The paper provides theoretical and empirical implications of delivering capacity, energy, and quality of supply, by paying special attention to the trilemma problem of the country and considers potential solutions. Ref. [22] provides an exploratory analysis of the price spikes both in the Day-Ahead and Imbalance markets following the implementation of the Electricity Act of 1998 in the Netherlands. The authors argue that market participants gain from more stable economic environment in which they can better forecast future prices and evaluate investment plans. Finally, a recent study considering the case of Spain compares the regulatory framework and the cost of electrical energy among European countries [23]. The limited electricity interconnection capacity of Spain leads to higher energy bill costs and, eventually, lower competition of electricity intense industries.

Prior studies have analyzed the wholesale electricity market of Greece [24]. For instance, Ref. [25] provided a detailed analysis of recent developments in the electricity market of Greece and described the structure of the Hellenic Energy Exchange and the markets that will be formed in the future. The authors presented the basic design variables and respective options for the integration of the Greek wholesale electricity market with the other European markets under the Target. Finally, a recent study by [26] highlights the recent attempt to liberalize the electricity market, which was hindered for a long time by socio-economic forces that favored the monopolistic system of the market. Overall, the authors argue that the road towards a Single European Energy Market is an opportunity for the country to move forward and in parallel to maintain the pace of “coupling” with the most developed energy economies of Europe.

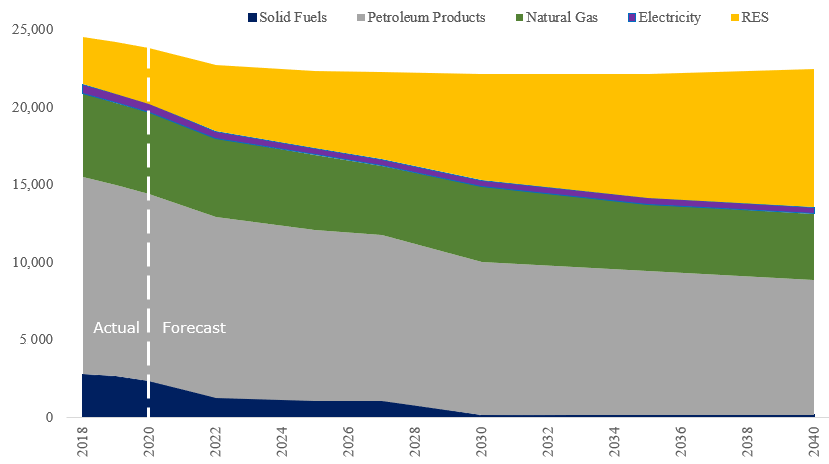

Over the past decade, national authorities demonstrated a strong commitment on energy policy goals and are constantly in line with the EU’s overall goal to achieve climate neutrality by 2050. Greece aims to achieve a 62–65% share of renewable energy in the electricity mix by 2030. To accomplish the above objective, the Greek government announced various packages of financial incentives, tax cuts, exemptions, and funding programs. In parallel, ambitious incentives for private companies were introduced, to invest in Renewable Energy Sources (RES) and contribute to the gradual decarbonization of the country. In 2020, the renewed National Energy and Climate Plan and the introduction of the Green Legislative Framework played a key role by continuing to support RES penetration in the energy mix of Greece. It is estimated that gross energy consumption in Greece is expected to fall below 22,000 ktoe by the year 2040, while the share of RES will gradually exceed petroleum products. In line with Figure 1, between 2020 and 2040, RES are expected to play a dominant role in the country’s energy production, increasing their share by up to 36%. Currently, Greece has exceeded the 2020 targets for the production of energy from RES. At the same time, Greece faces the highest wholesale energy price in Europe and in parallel one of the lowest retail prices in the EU. In that context, according to Eurostat (2019), the electricity market is considered as a key sector in Greece, since generation, transportation, distribution, supply, and trade of electricity produce 2% of national Gross Added Value of the total economy. Gross electricity generation in 2019 remained relatively steady compared to 2018 levels, reaching 53.3 TWh, while COVID-19 affected the total electricity consumption in Greece, an index which continued to decline for a third consecutive year.

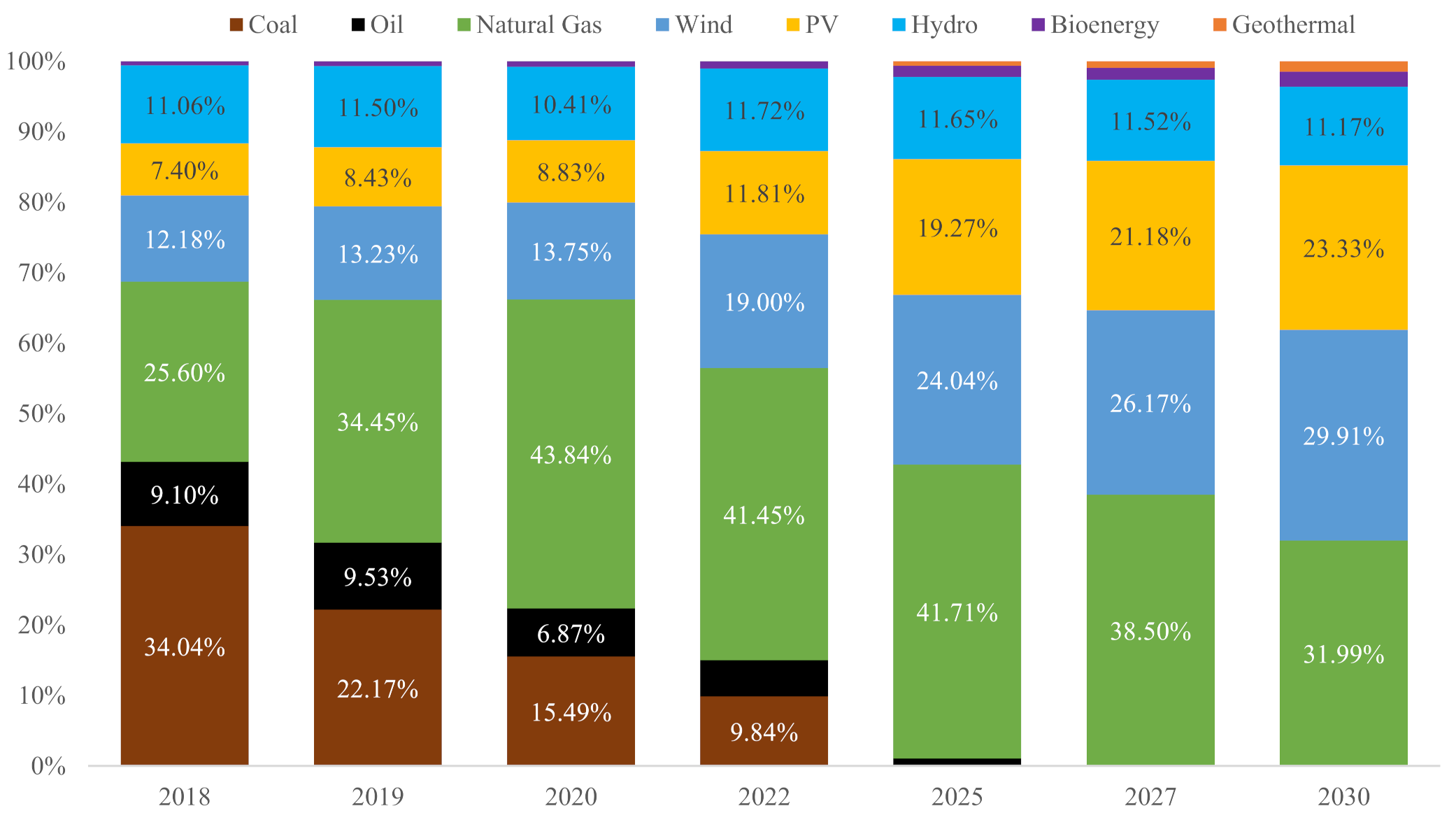

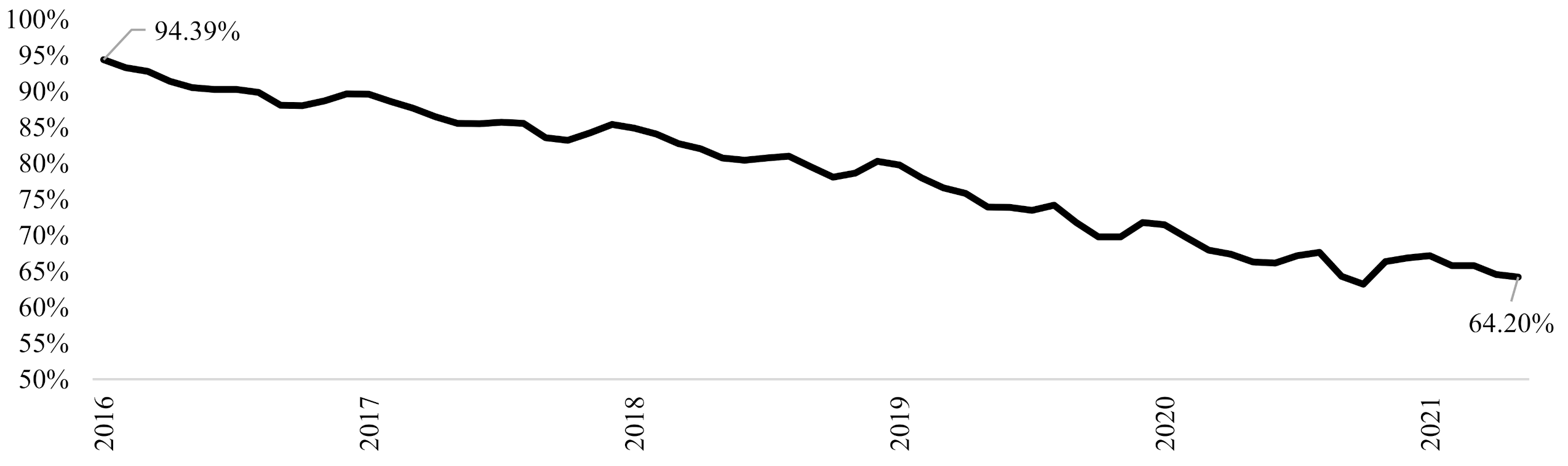

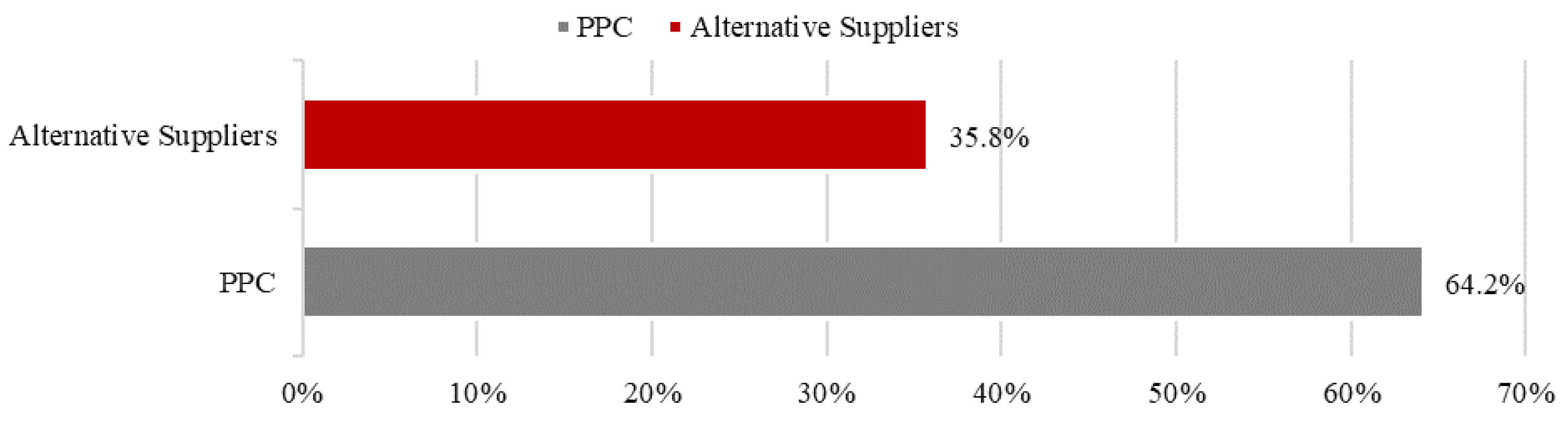

In line with Figure 2, the further decarbonization process of the electricity generation in Greece continues, with the lignite share plummeting to 15.4% in 2020. The share of RES recorded the most significant growth in the electricity mix, increasing by 9.7% during the period December 2019–October 2020. In addition, April 2020 was characterized as a “Snapshot from the Future” when natural gas and RES prevailed in the electricity mix. At the same time, the price of CO2 emission allowances directly affects electricity prices and contribute to emissions reduction through Europe. Beyond lignite-fired units, natural gas-fired units are also affected by the increasing cost of CO2 emissions, however, at a lower magnitude. In 2020, RES and Hydro together represented a greater share of total capacity (53%) compared to coal and natural gas combined (47%). According to Figure 3, the incumbent, Public Power Cooperation (PPC), retained a dominant share in electricity generation. PPC’s share in the retail market continues the downward trend, reaching 64.2% in May 2020 from 94.3% in January 2016 (Figure 4).

Considering alternative suppliers, three energy groups are active generators in the Greek energy market (Mytilineos, Heron, Elpedison). The oligopoly that prevails due to the small number of thermal producers has distorted competition in the wholesale market. In recent years, NOME-type auctions have played a key role in the electricity market, mainly towards the reduction of PPC retails’ market share. Essentially, alternative suppliers entered the market, exploiting cheap energy from NOME and achieving increasing their shares without substantial risk. Energy suppliers that are not vertically integrated into the market are forced to buy energy at high prices with the impact of either losing market share, raising their tariffs, or presenting losses on their balance sheets.

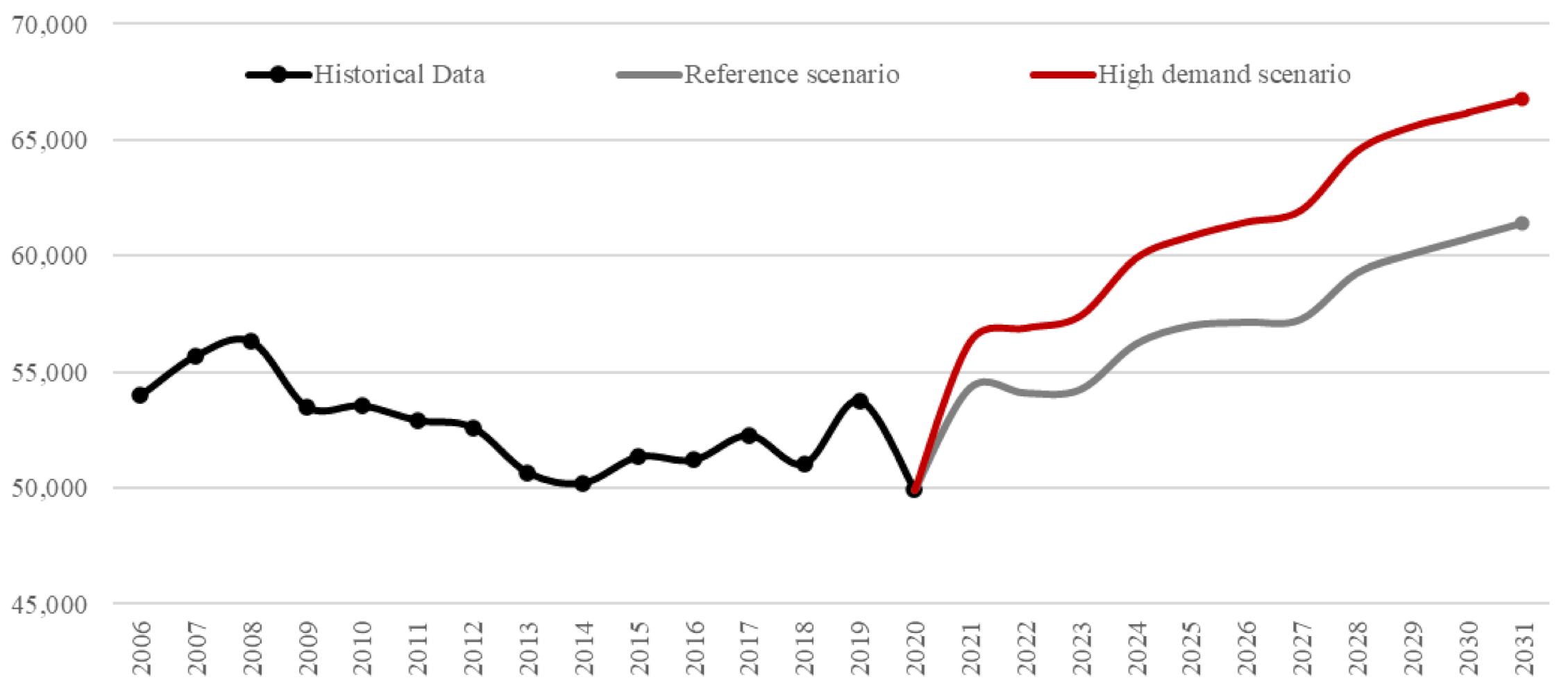

Figure 5 shows that, since the financial crisis of 2008, energy demand decreased exponentially and, in 2014, it reached 50,000 GWh. Then, a slight increase occurred, and it reached 50,217.4 GWh in 2019. The appearance of the pandemic stopped the upward trend of demand and, according to the “Reference Scenario” of the Hellenic Transmission System Operator (HTSO), electricity demand will regain its prior level in 2022. In April 2020, when COVID-19 restrictive measures were firstly introduced, a decrease of 9.8% in energy demand was recorded compared to April of 2019. Overall, the first four months of 2020 recorded a decrease in demand of 3.8% compared to the first four months of 2019. The pandemic heavily impacted oil and electricity demand, while natural gas consumption remained stable.

According to prior literature, an efficient design for real-time markets should address the special challenges of electricity system operation and support the intended economic outcomes by providing a spot market basis for development of and reliance on forward contracts [27,28]. Hellenic Energy Exchange S.A., (HEnEx) is the entity responsible for the operation of Spot and Derivatives markets in Greece. HEnEx has established the EnEx Clearing House S.A. (EnEx Clear) as the market Clearing House, in order to undertake the responsibilities of clearing, risk management, and settlement of the transactions. Under the Target Model, HEnEx Members are able to participate in the following markets: Day-Ahead Market (DAM), Intra-Day Market (IDM), Balancing Market (BM), and Forward Market (FWM).

2. The Application of the Target Model in Greece

A key energy market improvement was accomplished as the Target Model, a specific commitment of Greece, was implemented on 1 November 2020. This is considered as an important phase in the direction of Greece to fulfill the requirements of the EU energy policy. The innovative structure of the market which include the Day-Ahead Market, the Intra-day Market, the Balancing Market, and Forward Market is anticipated to provide improved price information and broader involvement and market entree of various services. The scheme “produce and forget” that used to be the case for Greece is transforming into a flexible and dynamic one. The novel market design is well-suited with all EU Members, permitting for the quick Day-Ahead and Intraday coupling with the neighboring countries. Considering the case of Greece, coupling with Italy and Bulgaria has already been achieved, which in turn is anticipated to boost energy security, assist the ongoing growth of RES, and promote competition in the wholesale market.

The latest market formation entails the collaboration of several entities like ADMIE, which is the Transmission System Operator, the Hellenic Energy Exchange, the Clearing House, and the Athex Clear for the Derivatives Market. Moreover, the Regulatory Authority for Energy (RAE) and the Hellenic Capital Market Commission collaborate for the efficient supervision of the legal structure that oversees the daily function of the markets. The recently formed clearing house, EnEx Clear, is in charge for the financial settlement, the invoicing of participants, and eventually the risk management of the system. Financial institutions, such as banks, are already listed as official General Clearing Members to provide their services for both the spot and derivatives market.

The intense unpredictability of electricity prices has constantly concerned academics, generators, retail suppliers, and traders [29,30]. Those variations could be attributed to several factors that may be either easily predicted or not. Namely, reasons that crucially affect electricity prices are unexpected modifications in demand, unit availability, established interconnections with neighboring countries, fuel price such as natural gas, coal or oil, CO2 prices, the stochastic generation of RES, macroeconomic conditions, and broader socioeconomic disorders like the pandemic. Consequently, members are able to exploit the hedging opportunities of the Derivatives Market. However, despite the fact that the Derivatives Market has been available to market participants in Greece since March 2020, it is not utilized by them, and liquidity persists at minimum levels, even after 15 months of official operation.

The Market Clearing Price of the Day-Ahead Market is formed at the point where the aggregate supply and aggregate demand curves intersect. Next, the energy exchange is responsible for submitting priority price taking orders by representing previous transactions as submitted on the Forward Market or the unregulated bilateral Over-The-Counter (OTC) market. In that framework, the recently established energy exchange aims to be a vital component in the growth, of the domestic and regional economy over the utilization of the Target Model. Regardless of the COVID-19 outbreak, the market layout of a totally functional gas exchange is presently under formation. In the wake of the electricity market, a natural gas trading platform will be available to participants at a later stage. Hence, including a gas marketplace in the framework of HEnEx is expected to function as a key step for the overall market, along with the recent developments in Northern Greece with the Trans Adriatic Pipeline, and other pivotal projects being supported by the EU [31].

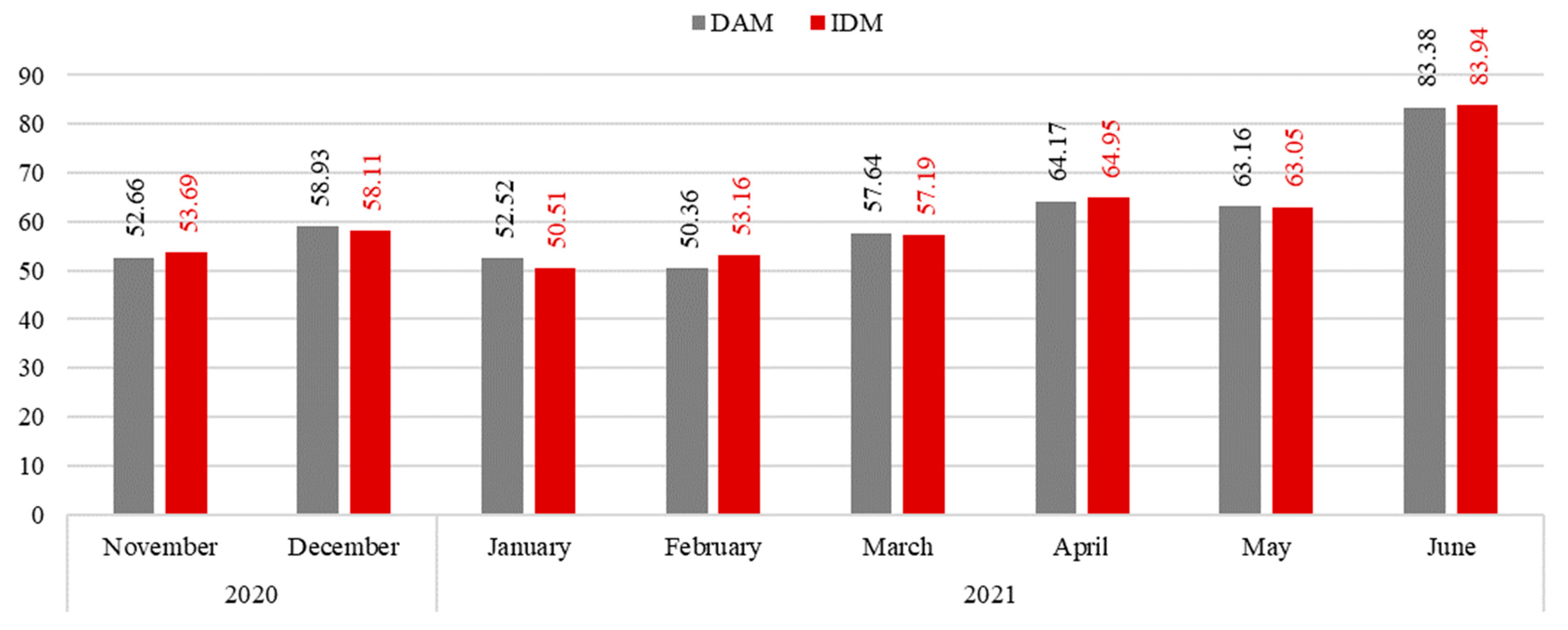

According to Table 1 which depicts the most recent available data provided by the HEnEx, Day-Ahead Market accounts for more than 98.5% (or 3972 GWh) of the total volume traded during May 2021. Hence, the biggest share of market value derives from DAM (€254.7 Million), since the Intraday Market accounts for 1.5% (54.1 GWh) of the total volume by taking into consideration the three Intraday Auctions (LIDA 1, LIDA 2, & LIDA 3). Next, we identify small discrepancies between the Day-Ahead Market Price and the Intraday Prices. Figure 6 shows that, in May 2021, DAM price was equal to 63.16 €/MWh, while the average Intraday price was slightly lower at 63 €/MWh (LIDA 1 (62.53 €/MWh), LIDA 2 (63.12 €/MWh) and LIDA 3 (63.52 €/MWh)). The analysis that follows provides detailed information considering the comparison between DAM and IDM prices and shows that prices between the two markets were almost identical from November 2020 until June 2021.

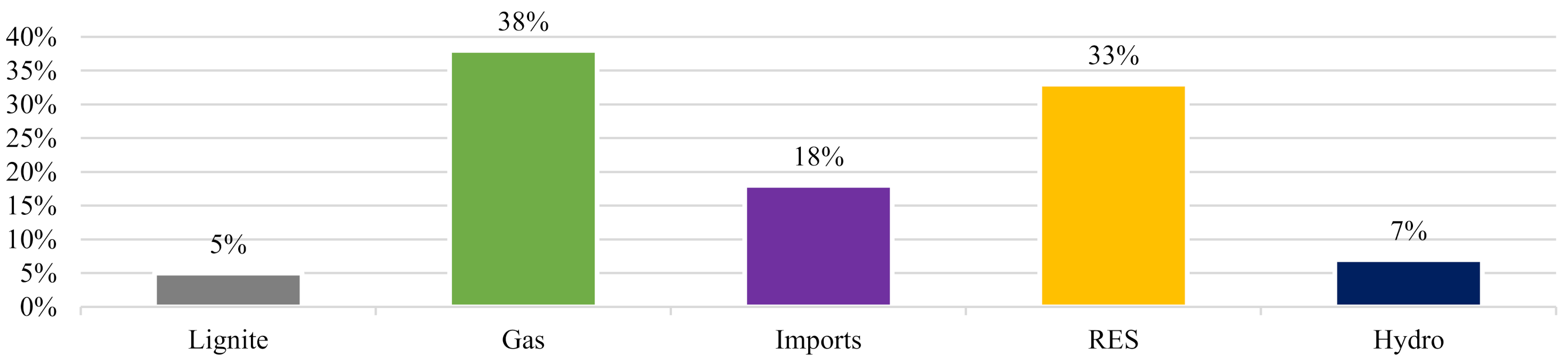

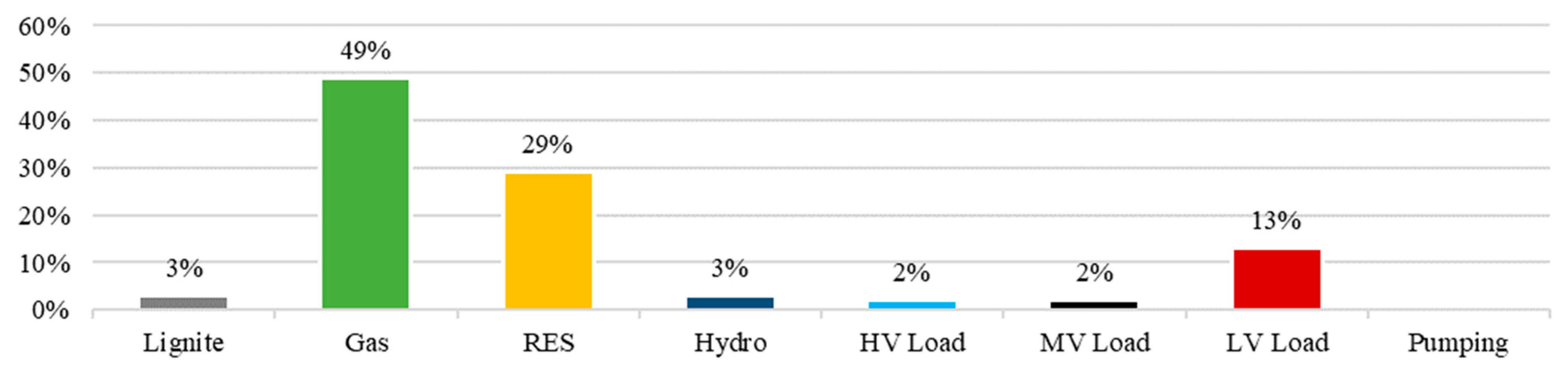

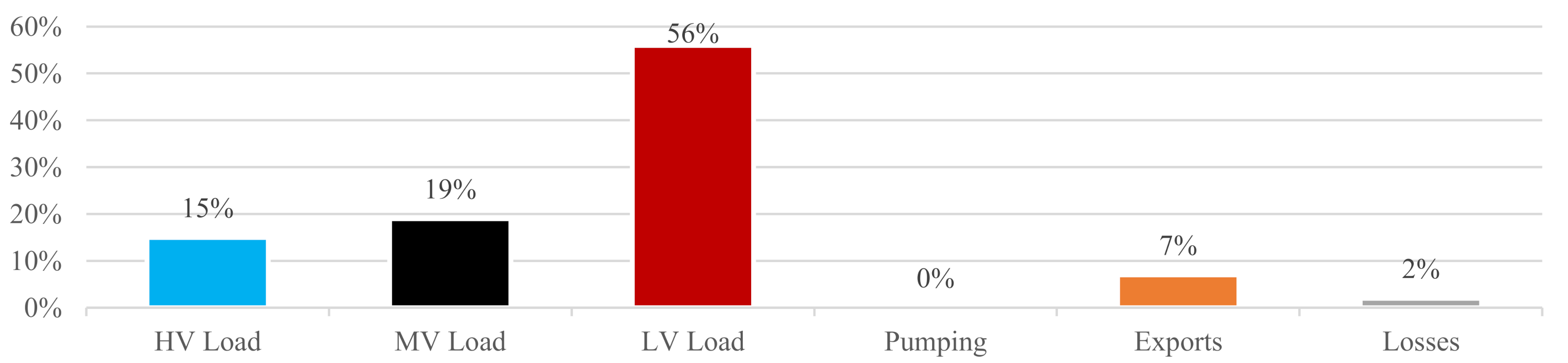

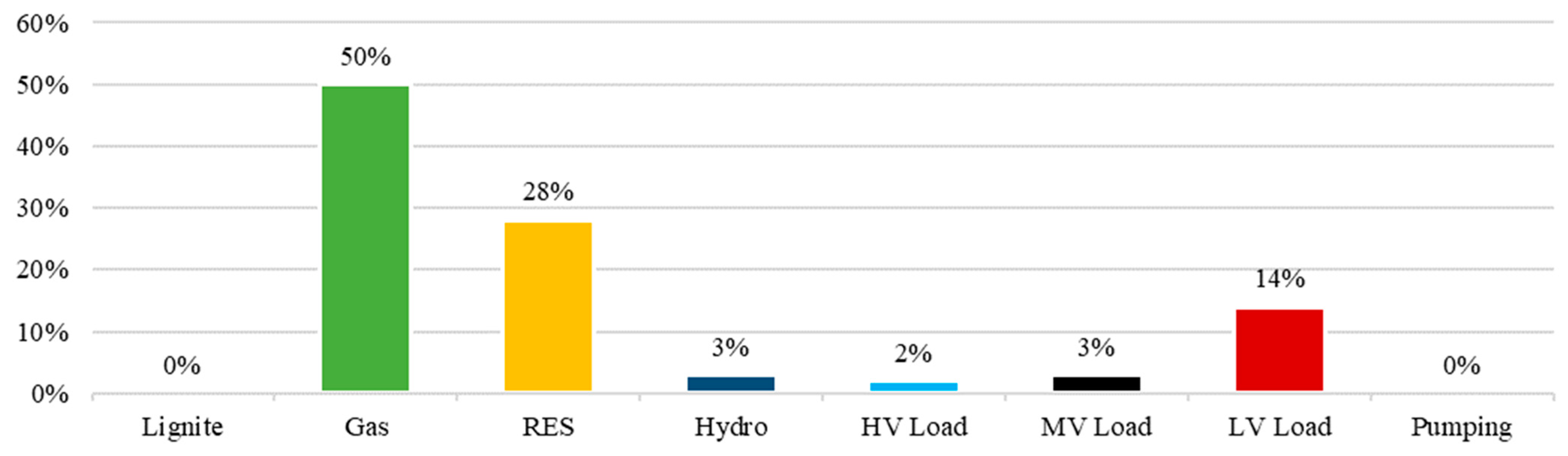

Next, in terms of the electricity mix for May 2021, the sell volume of the Day-Ahead Market is dominated by the natural gas (38%) and RES (33%), while imports (18%), hydro (7%), and lignite (5%) account for the remaining share of generation (Figure 7). Considering the Intraday Market, again, natural gas (49%) and RES (29%) account for 78% of the total generation (Figure 8). Moreover, on the buy side of the Day-Ahead Market, considering again May 2021, the majority of the volume directed to Low Voltage (LV) Load (56%), Medium Voltage (MV) Load (19%) and High Voltage (HV) Load (15%) (Figure 9). In the Intraday market, we identify natural gas-fired units absorbing 50%, RES aggregators 28%, and LV load 14% (Figure 10).

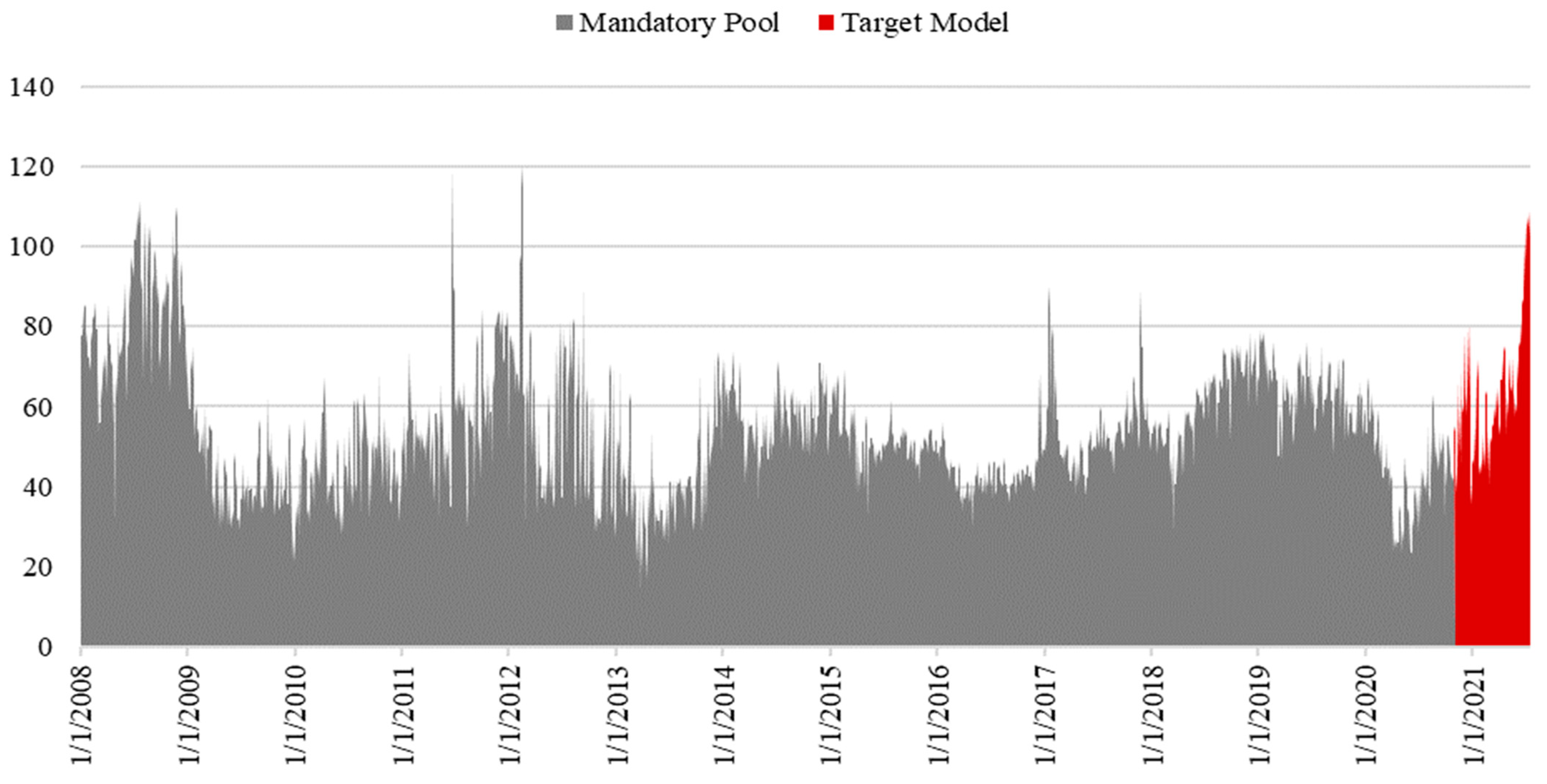

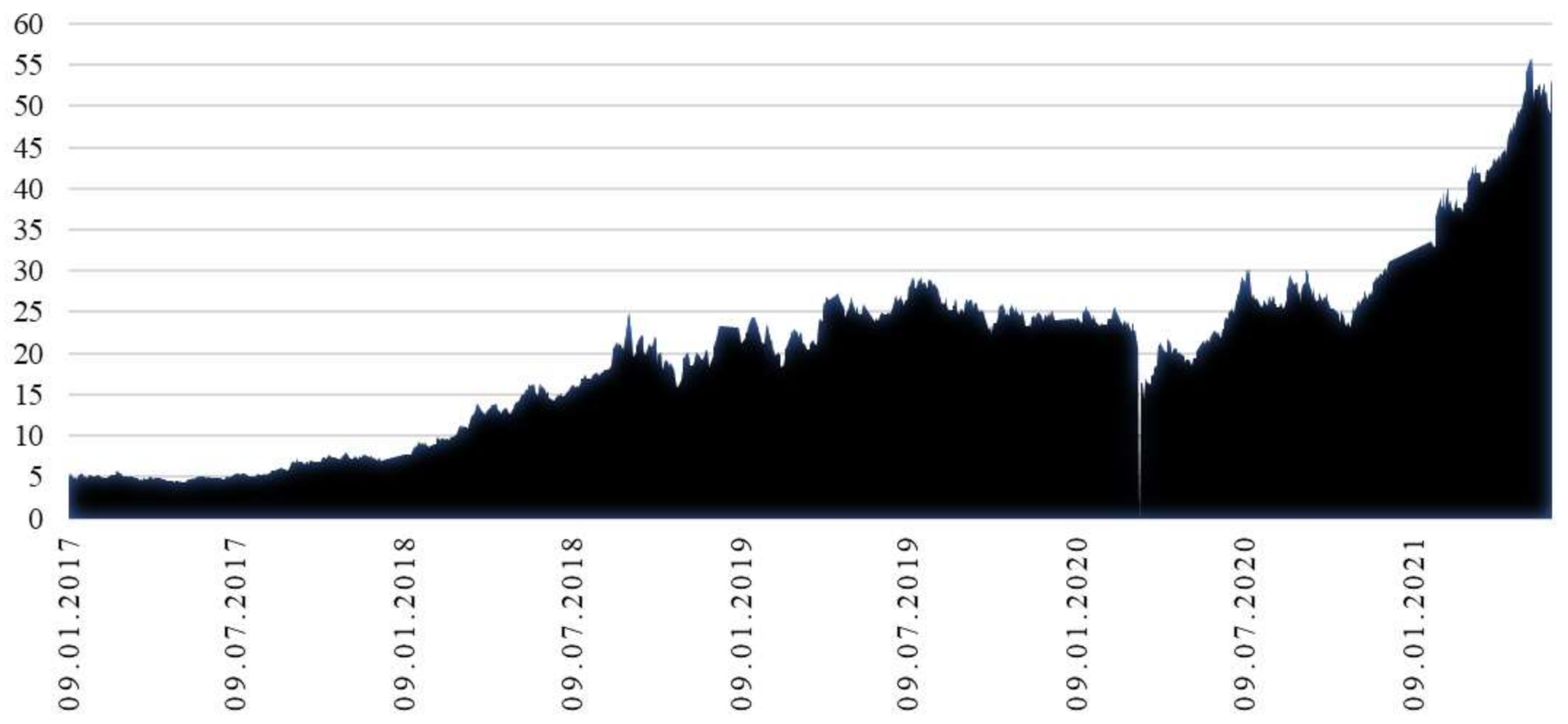

As Figure 11 illustrates, since 2008, the daily average market clearing price in Greece fluctuated from 10 €/MWh to 123 €/MWh, with an average price considering the period 1 January 2008 until 1 June 2021 at 54.1 €/MWh. In terms of the overall fluctuation, and prior to the implementation of the Target Model, we identify spikes in electricity prices (values higher than 100 €/MWh) only four times in a period of a 13.5 year period. Specifically, the first spike is identified by the end of 2008, the second at the beginning of 2012, the third in mid-2014, and the fourth in early 2017. However, only following the implementation of the Target Model, the average daily Market Clearing Price skyrocketed to 128 €/MWh. Prior to the launch of the Target Model, a significant drop occurred in wholesale electricity prices during the 1st period of COVID-19 lockdown (March 2020–April 2020), reaching 28.5 €/MWh in April 2020.

3. Empirical Findings

3.1. Day-Ahead Market and Intraday Market

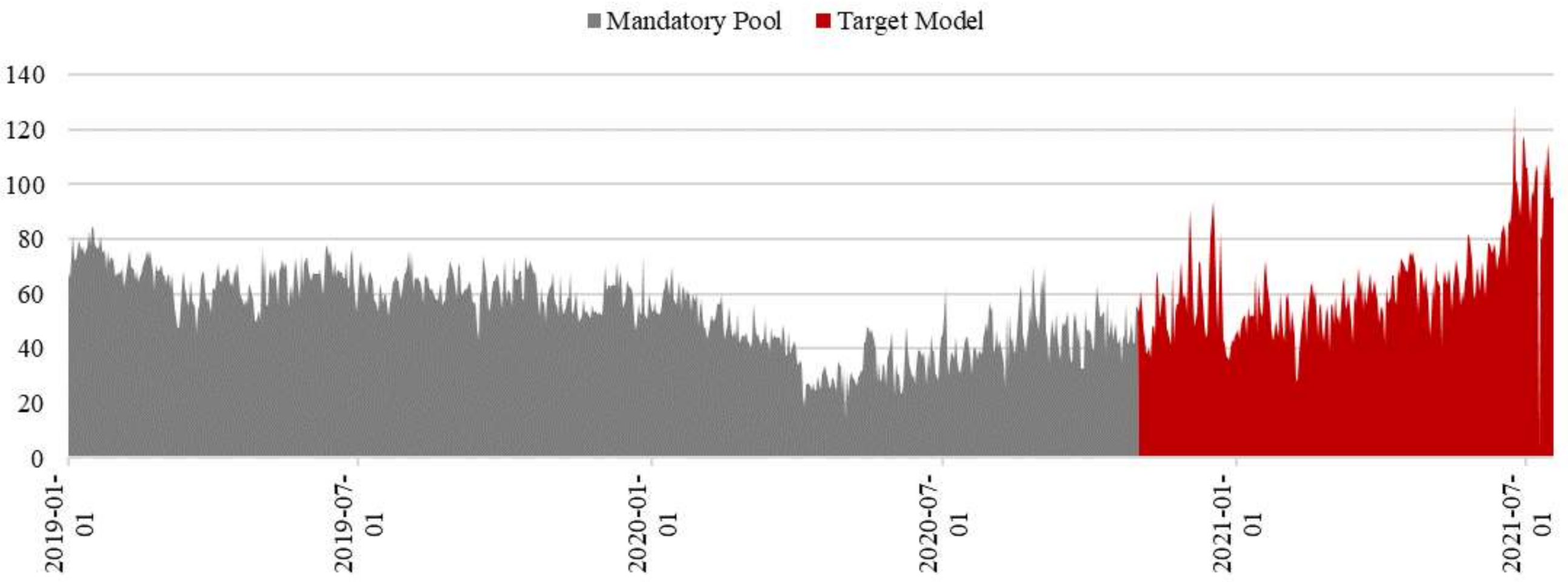

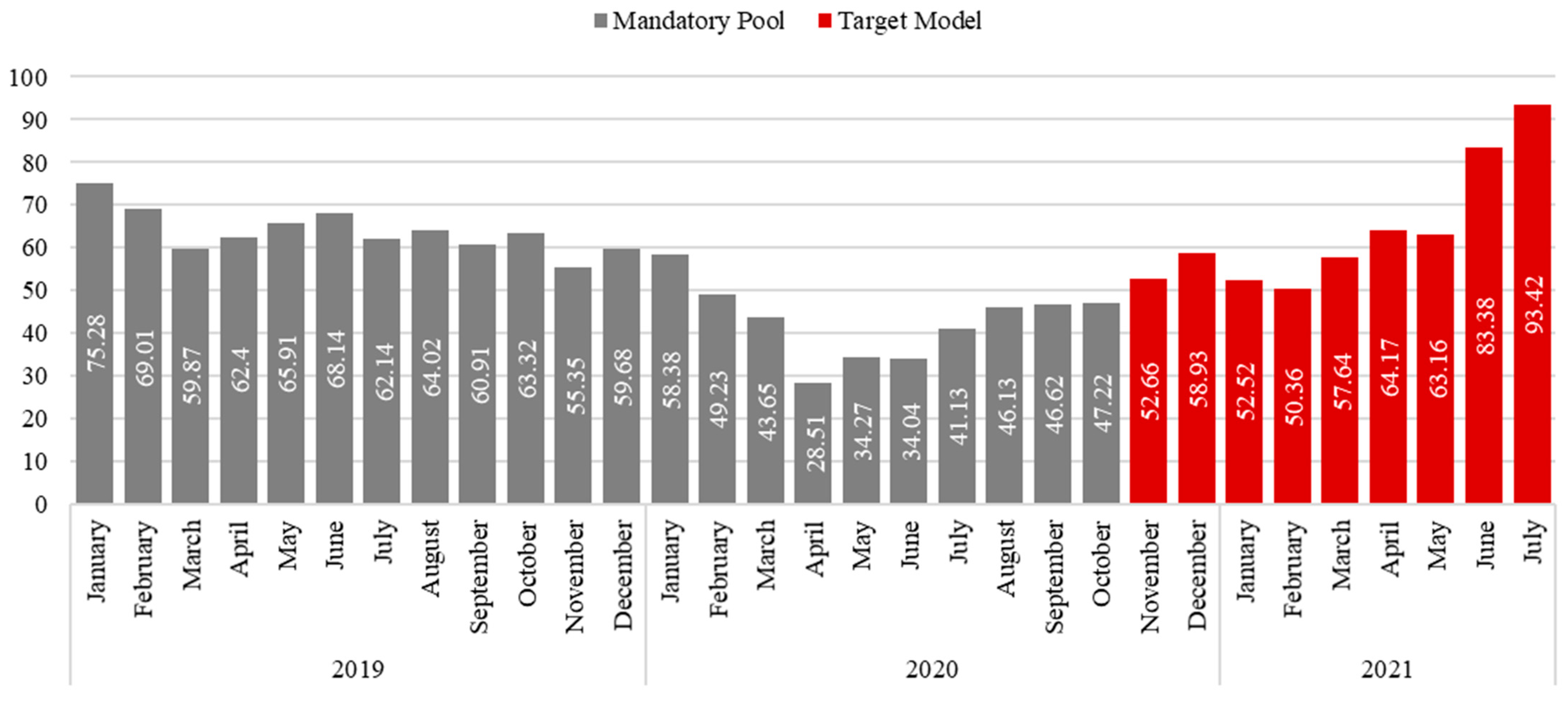

A price increase in the Day-Ahead Market causes intense concern, which, during the first nine months of Target Model operation, recorded an increase of 97.8%, since the average price soared from 47.2 €/MWh in October 2020 to 93.4 €/MWh in July 2021. Interestingly, despite the fact that the total electricity consumption reduced by almost 10% from March 2021 to April 2021, the price followed an upward trend from 57.64 €/MWh in March to 64.17 €/MWh in April (an increase of 11.3%). On a year-to-year comparison, the price levels during April 2020 were equal to 28.51 €/MWh, thus the price increase was more than 125%. Based on Figure 12, the upward trend of Day-Ahead Market price continued until July 2021. In detail, during June 2021, the price at DAM was set at 83.38 €/MWh, an increase of 32% compared to May 2021 when the price was recorded at 63.16 € MWh. On an annual basis, during June 2020, the DAM price was 34.04 €/MWh, meaning that the growth was equal to 144% (see Figure 13 for Day-Ahead Market prices and Table 2 for Intraday Market prices).

The aforementioned developments are not entirely attributed to the implementation of the Target Model. The overall demand increase due to high temperatures is one of the main reasons that led to a spectacular rise in the price of electricity, which, on 25 June 2021, reached 128.15 €/MWh. In line with the prices recorded during June 2021 and July 2021, with prices exceeding the benchmark of 100 €/MWh, it is anticipated that the increase in price levels will be maintained during the following period. At the same time, the constantly increasing natural gas prices crucially affect electricity cost in Greece, since natural gas accounts for 38% of electricity generation in the DAM. The natural gas import price since June 2020 follows an upward trend, while consumption hits an all-time high record during 2020. Precisely, natural gas import price in Greece during the COVID-19 outbreak dropped to 5.4 €/MWh in March 2020 yet recovered to 13.4 €/MWh by December 2020.

Market coupling systems exist both in Day-ahead trading and in Intraday markets, and this interconnection among markets ensures efficient electricity trading. Furthermore, the participation in short-term markets, the initiation of bilateral contracts, and the removal of prior restrictions on trading are expected to boost liquidity, with a positive impact on the balancing market. In this direction, a significant change that is taking place is the implementation of continuous trading in the Intraday market within the first quarter of 2022. At the same time, during October 2021, the wholesale gas market will be activated. Initially, spot transactions will be available to market participants and, in the second stage, futures products as well, thus acting as a starting point for the establishment of a regional energy hub.

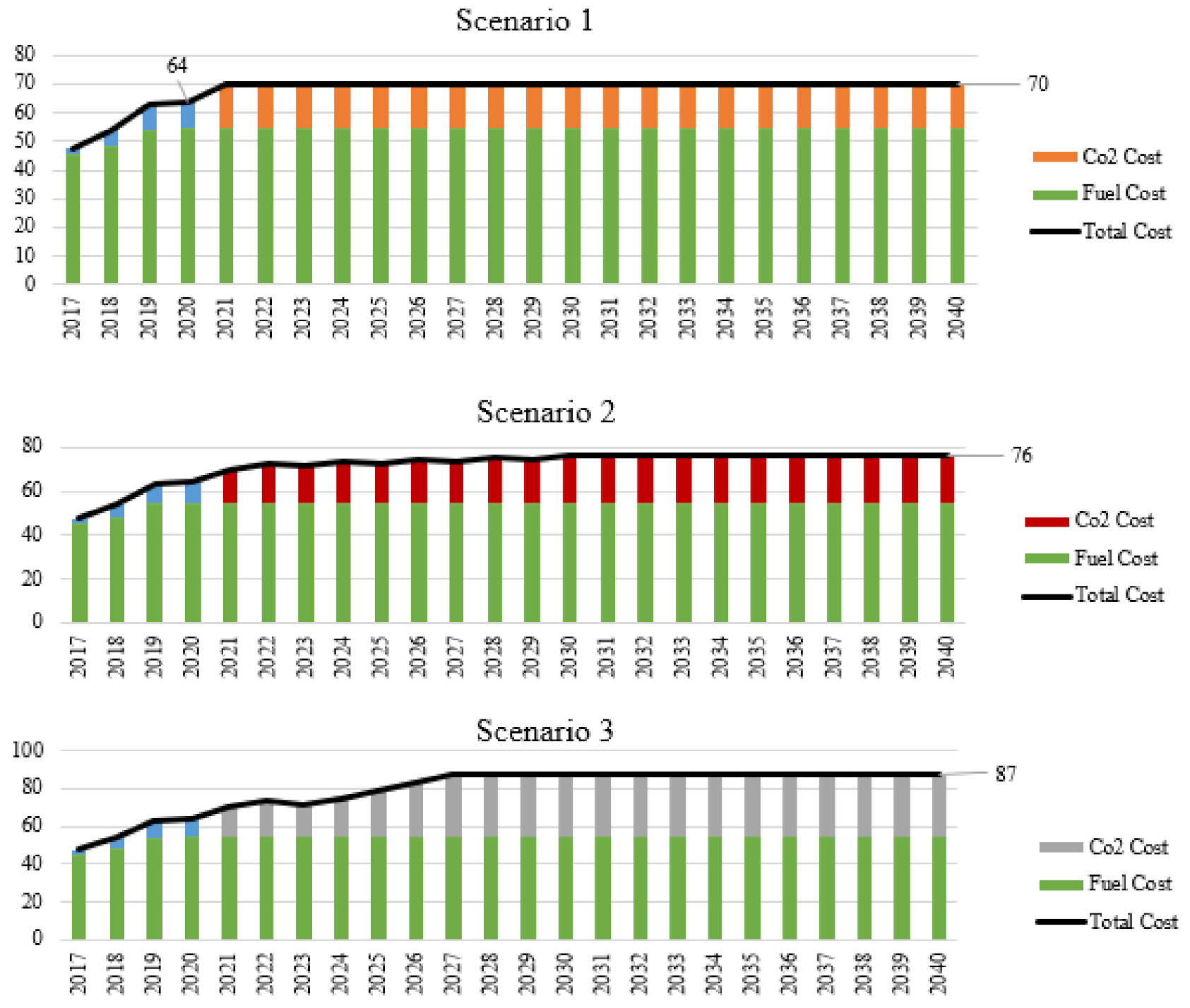

Figure 14 illustrates that, the impact of Co2 prices is already apparent on coal-fired units since their total operational cost today is more than 75 €/MWh (35 €/MWh fuel cost + 40 €/MWh CO2 cost). In addition, the increased CO2 prices will generate additional pressure to the daily operation of natural gas-fired plants and eventually lead to higher electricity prices. The corresponding levels of total operational cost for natural gas-fired units is more than 65 €/MWh (55 €/MWh fuel cost + 10 €/MWh co2 cost). Even though the emissions from natural gas (117 pounds of CO2 emitted /btu) are lower compared to coal (215 pounds of CO2 emitted /btu), given the current and projected prices of CO2 emissions, natural gas-fired units are anticipated to drive electricity prices at increased levels in all three Scenarios (see Figure A1 and Figure A2 in Appendix A for more details. Main assumptions: auction price €/t CO2 not to drop at lower than 50 €/t CO2, fuel cost remains steady in all three Scenarios at 55 €/MWh)).

In 2022, the Target Model is expected to incorporate the optimization algorithm, EUPHEMIA. The EUPHEMIA algorithm is a key tool for calculating and linking individual electricity prices across Europe as well as for optimal cross-border capacity allocation. It offers transparency in the calculation of energy price and its distribution. The procedure of the algorithm is as follows: first, the participants submit their orders to the respective energy exchange; the algorithm accumulates the orders and, according to specific criteria, those orders are accepted or rejected. The criteria on the basis of which it operates are the maximum prevalence of social welfare (according to the consumer surplus, the producer surplus and the congestion rent in the area) and the flow of capacity so that no congestion is caused. The following table provides illustrative information considering imports and exports of electricity for both explicit and implicit allocation. Greece is a net importer of electricity to cover the domestic demand. According to Table 3, the main countries from which Greece imports electricity are Albania (235 GWh), North Macedonia (166 GWh), and Bulgaria (125 GWh from Explicit Allocation and 135 GWh from Implicit Allocation). On the contrary, Greece exported electricity towards Italy via Implicit Allocation (152 GWh) and towards North Macedonia via Explicit Allocation (75 GWh).

3.2. Balancing Market

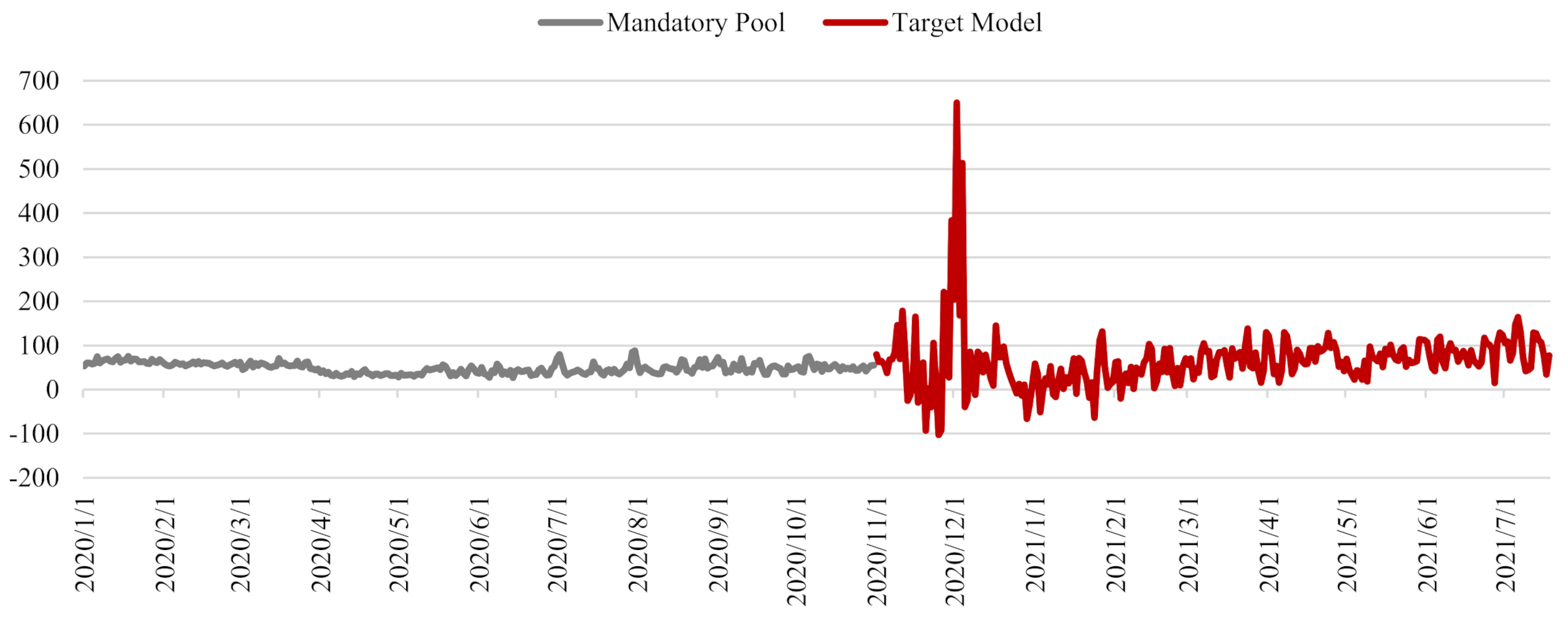

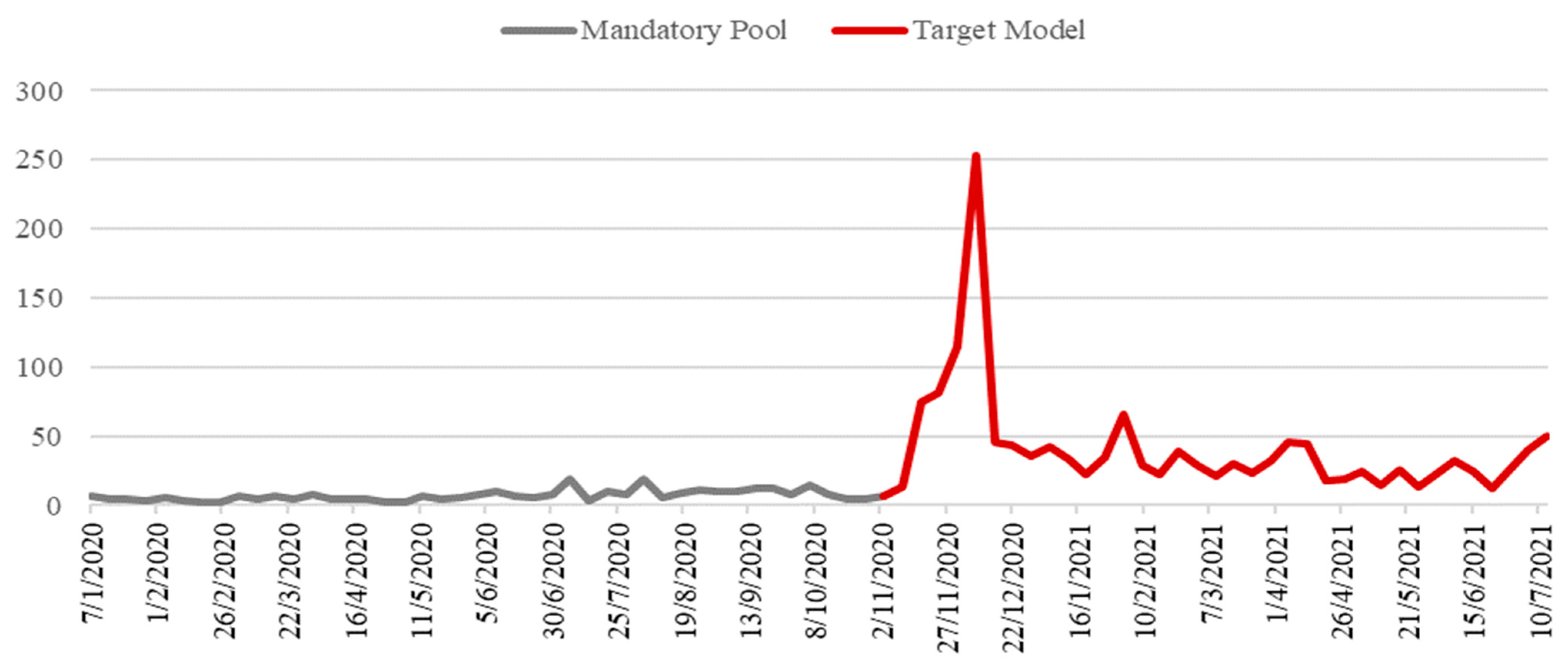

The Balancing Market, which is the market responsible for the smooth operation of the system as electricity approaches the actual delivery, was the one that presented the biggest problems as its cost multiplied compared to the corresponding cost from the previous model of mandatory pool. In November 2020, the balancing market quadrupled compared to the previous model (Figure 15 and Figure 16). Only during the last two months of 2020, when the Target Model was initiated, the burden on the Balancing Market was estimated at €135 million euros while the total annual burden of 2020 at €200 million. Based on the liquidation of the Balancing Market for the period from November 30 to December 6, the cost amounted to 43.37 euros per megawatt hour. For the same period, the corresponding weighted average price of the Day-Ahead Market (DAM) was 66.18 euros per megawatt hour. This means that the cost of the Balancing Market amounted to 66% of the market value. The prices formed in the Balancing Market force the companies to increase the tariffs by 15% to 20% even in the low voltage (households). Medium increases are already being borne by similar increases (large commercial companies). The cost of energy is close to 70 euros per megawatt hour, while in the same period there were contracts on the market with 55–60 euros per megawatt hour. The surge in the price of electricity caused a great upheaval in the market in December 2020 with consumers massively terminating electricity contracts.

4. The Response of the Regulator

Due to the deteriorating situation resulting from the implementation of the Target Model, the regulator was aware of the potential impact of this situation and, in order to curb the rise in wholesale energy costs, on 13 February 2021 (Figure 17), made the Decision (54/2021) to impose a threshold on the bids of the producers regarding the downward balancing action (The Decision was taken in cooperation with the European Commission and the Ministry of Environment and Energy). RAE also modified the Integrated Scheduling Process (ISP) algorithm. The ISP refers to an action performed by the System Administrator in order to configure the unit allocation program and the distribution of balancing power to the entities that provide it. The exercise is executed three times: once immediately after the resolution of the Day-Ahead Market and twice more after the resolution of each of the two intraday auctions held within the framework of the Intraday Market. It can additionally be performed at the request of the TSO, in case any serious changes occur during the operation of the System, such as serious damage related to loss of unit, loss of interface, and forecast failures.

Based on the above decision, RAE modified the ISP algorithm in such a way as to eliminate the submission of tenders for quantities of energy that are lower than the technical minimum production quantity. In the explanatory memorandum, RAE notes that it recognizes that there is an issue of abusive behavior in the balancing market and states that the measures it promotes aim to balance the market by keeping it essentially able to operate, and, secondly, the restoration of conditions of good operation and competition. In particular, the adoption of these measures strengthened the operational framework of the Balancing Market, by discouraging the occurrence of abusive behaviors and preventing the avoidance of standard rules in order to benefit, to the detriment of the system’s economy and a healthy competition. Another action of RAE regarding the inconsistent operation of the Target model was the imposition of a penalty of five million euros on the TSO, due to the failure of completing the Western Corridor in the Peloponnese. Although the above arrangements prevented the continuous rise in balancing costs, the situation does not remain viable, and more adjustments are needed for the smooth operation of the energy exchange:

- ▪

- The causes of the malfunction—Improper operation of the Target model in Greece

- ▪

- Price liberalization given that producers providing balancing services were able to provide prices up to 100 times their actual variable unit costs.

- ▪

- Oligopoly on the producers of thermal units.

- ▪

- Inability of the system administrator algorithm to prevent unethical bids.

- ▪

- Congestion of the high voltage network in the Peloponnese due to overload.

- ▪

- Low interconnection power transmission of electricity from other countries

- ▪

- Low liquidity in the Forward and Intraday market. Both the number of participants and the volume of transactions should increase, aiming to reduce the need for balancing energy and, consequently, the corresponding costs.

Measures to Be Taken

Demand response: The expected development of RES has considerable impacts on the average daily pattern of electricity generation in the current decade. Demand Response concerns the storage of energy that comes from RES during peak hours so that it can be stored and used when demand is increased. According to the TSO, it is estimated that in 2025 the thermal units will only cover the remaining quantities apart from the generation from RES. Nowadays, Demand Response is not available to support the wholesale electricity market in Greece, yet it is crucial for smoothing the typical load curve in the future. In addition, the use of batteries as a means of energy storage is anticipated to provide long-term profits for the overall economy. Hence, the authorities need to establish concrete steps to allow participation of Demand Response and Storage in all stages including in the Balancing Market.

Central scheduling: The Balancing Market is governed by the principle of Central Dispatching per unit. The Marker Operator considers the generation offers and, according to an algorithm optimization solution, provides the most efficient nominations to each to the entity providing balancing services. These entities submit bids in the market area per unit, per load zone, and per interconnection border. This model is applied to Greece, Poland, Italy, and Ireland, while the model of Self-Scheduling is selected in other European countries. In countries where the Self-Scheduling model is applied, first the backup auction process takes place, then follows the Day-Ahead Market, the Intraday Market, and finally the self-scheduling nomination. In this way, the simultaneous action of upward and downward balancing is prevented, a fact that is usually observed in the Greek electricity market. The imposition of a penalty for the simultaneous action of upward and downward balancing is one of the best measures to minimize this phenomenon.

5. Next Steps

- ▪

- Power Purchase Agreements (PPAs)—Several GWs of merchant driven projects are expected to come online by 2030 and a supportive framework for PPAs is key for their deployment. In that context, the national authorities are seeking to establish a subsidy support-scheme by supporting renewable electricity absorbed by energy-intensive industries and other enterprises. Balancing costs are an important part of the equation, and the scheme is anticipated to subsidize balancing market costs by using recovery fund money as part of the effort. According to the plan, the support mechanism will be made available to energy consumers whose energy cost exceeds 20% of operating costs. Besides industrial producers, the mechanism’s availability could be expanded to also cover hotels in the tourism sector, retail food chains, and other enterprises operating on a mass scale. RES investors opting to establish bilateral PPAs with industrial consumers are expected to be given licensing priority for the projects over peers planning to secure tariffs via RES auctions. The licensing priority for PPAs is a measure to counteract the fact that projects that have been awarded a contract via the auction system (Auction prices have decreased significantly in the previous auctions, especially in the last common auction, where the weighted average price dropped by 30% compared to the Starting Price. For more details on auction results, see Table A1 in Appendix A) are likely to enjoy more favorable treatment for project financing. The scheme needs to be endorsed by the European Directorate for Competition. For the moment, there is only one PPA signed in Greece—Mytilineos has signed a PPA with Egnatia group for 200 MW solar at 33 €/MWh (It is worth noting that Mytilineos acquired over 1 GW of assets in the late stage of development by Egnatia group, which suggests that the pricing might not necessarily show a representative fair value of a PPA).

- ▪

- Capacity Remuneration Mechanism (CRM)—Greece aims to create a new permanent CRM following the temporary CRM from 2020. Additionally, Greece is pushing for a strategic reserve scheme in order to compensate lignite units which need to stay on the system for capacity adequacy purposes despite being unprofitable. At the moment, Greece has submitted a proposal highlighting the need and operation details of a strategic reserve scheme along with a set of answers posed by the EU commission in June 2021. The new CRM needs to be aligned with EU regulations. Greece submitted in June 2021 a draft of the Market Reform Plan for the national Day-ahead, Intraday and Balancing markets that were launched in November 2020. In July 2021, DG Comp is set to start consultations which will take four months before the final Market Reform Plan can be published. In parallel with the consultations of the Market Reform Plan, a new capacity adequacy report from the Greek TSO will be prepared for the EU commission as a supplement to the Greek energy ministry’s proposal for the strategic reserve scheme—a final Market Reform Plan by the last quarter of 2021 that can be legally implemented as early as the first quarter of 2022. The setup of a strategic reserve scheme could be activated in the first quarter of 2022 together with the updates from the Market Reform Plan. The legislation of the new CRM would be activated after the strategic reserve scheme ends and will include, among others, Demand Response.

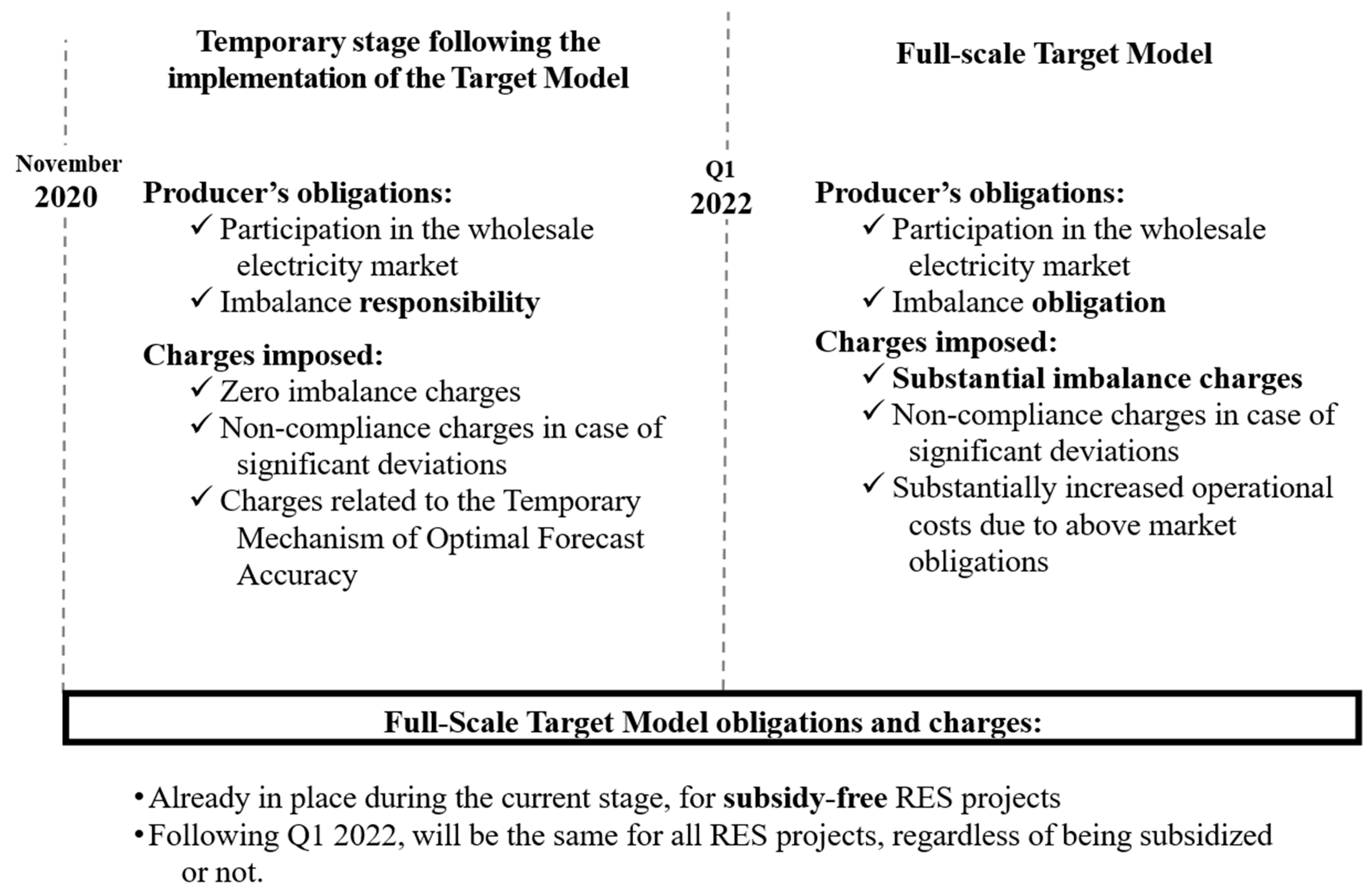

The Transition to Full-Scale Target Model for RES

Existing literature provides illustrative information considering the impact of the Target Model on RES [32] and the role of RES Aggregators [33]. Figure 18 depicts the upcoming scheme in Greece, which contains substantial operational charges such as clearing, imbalance, and non-compliance costs. Under the introduced scheme, it is mandatory for generators with a capacity bigger than 500 KW to sell their production in wholesale market, either by utilizing own resources or via the existing aggregators. Apart from their aforementioned obligation, RES producers need to also be considered for accurate forecast projections. As long as the interim phase of the Target Model is available, and until the introduction of the full-scale Target Model, participants will be credited with 1 €/MWh, which corresponds to a Fixed Management Premium. During this phase, RES producers are burdened by the Temporary Mechanism of Optimal Forecast Accuracy that equals 12.98 €/MWh for 2021. Overall, RES producers under the Sliding FiP framework receive a premium which is the difference between the Reference Price (or Auction Price) with the monthly Reference Market Price (RMP) per technology.

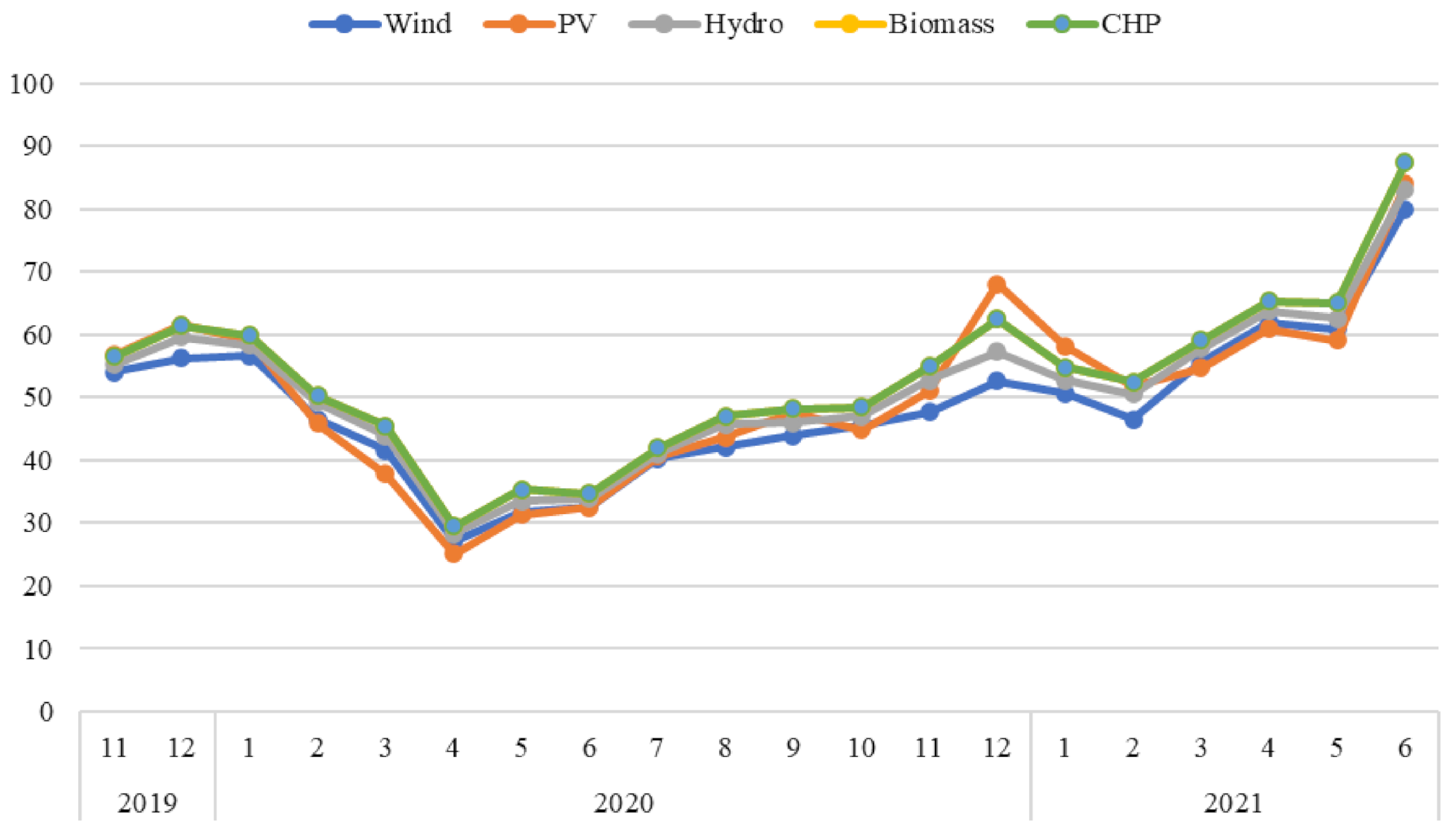

For the Greek wholesale electricity Market, the RMP is derived from the hourly generation that corresponds to each RES technology. The calculation considers the aggregate production coming from the total number of identical technologies. RMP is part of an exercise that yields the “Sliding Premium” which is the same for every producer per RES technology. Therefore, this process guarantees that total revenues in terms of each technology are resulting from the multiplication of the Reference Price (or Auction Price) with the total production for the specific time unit. Historical data of Reference Market Price by month reveal that, on average, compensation prices for all RES technologies are 48.8 €/MWh. The COVID-19 effect is apparent in this figure as well since prices for all RES technologies dropped around 33 €/MWh. However, as Figure 19 illustrates, a sharp increase in prices followed along with the gradual withdrawal of mobility restrictions. Even during the 2nd wave of lock down of lockdown restrictions in Greece (November 2020 until May 2021), RES compensation prices remained at increased levels (around 55 €/MWh). Average Reference Market Price of all RES Technologies from November 2019 until May 2021 (excluding COVID-19 effect) equals 52.2 €/MWh

6. Conclusions

This paper investigated the implementation of the Target Model in the wholesale electricity market of Greece and its impact on electricity prices. The study explores the time period before the implementation of the Target Model and the first nine months of its execution. In countries like Greece, where a monopoly or oligopoly of producers prevails in the wholesale electricity market, in combination with low capacity in connectivity with other neighboring countries, an upward trend on electricity prices is mostly anticipated. The above, combined with the lack of supervision in order to prevent manipulative behavior, could partially lead to the postponement of energy related investment plans. Energy producers are the only ones who benefit from the price increase and the overall market turmoil since those companies are able to exploit the legislative and technical gaps and implement unethical strategies in order to achieve extremely high profitability.

The peculiarity in this case is that the market itself provides room for the above exploitation since the submitting bids are within the limits set by the European Union. Especially in times of high demand, where there is a low supply from the producers, it is necessary to check by the competent regulator in order to determine whether they meet the reality or whether they use the regulations of the Target model to achieve profit maximization through the Balancing Market. As market participants understand better the dynamics of the new market and RAE monitors competition and costs, the Target Model is expected to become more fluent and efficient eventually increasing competition and reducing costs. In addition, RES seems to be responsible for a large share of the cost of the Balancing Market. This fact is due to the inability of accurately predicting their production, due to their stochastic nature. In addition, in line with [34], the increase of RES to an electricity market has an ambiguous effect on wholesale prices. The merit order effect has a downward pressure on prices while, with market power, higher inframarginal rents will tend to increase prices. Considering the case of Greece, we observe simultaneous increase in RES share and higher prices which yields to the existence of market power. This could be mainly attributed to the increased share of one RES aggregator in the market, which is equal to 54%. It is apparent that the aforementioned finding has important consequences for the domestic wholesale prices.

Part of prior studies found that Target Model implementation was accompanied by welfare increase, which is not yet the case of the Greek wholesale market. Some benefits that are anticipated to be evident on the wholesale market of Greece are the consumers benefit from lower prices as a buyer will be automatically matched with the cheapest generation in Europe, and the fact that balancing markets will be integrated so that consumers benefit from lower balancing costs and improved security of supply across the EU. However, a study from the United Kingdom (UK) illustrates how market design solutions characterized by good intentions could have adverse effects, depending on the details of how they are implemented in practice [35]. The author lists some drawbacks in the case of UK such as the increased cost of relieving congestions, increased risk of discrimination by system operators, increase in the potential scope for abuse of market power by generators, and failure to capture positive externalities and perverse incentives. We observe that our findings are in line with the case of Spain, where the limited electricity interconnection capacity of the country led to higher energy bill costs and, eventually, lower competition of electricity intense industries [23].

At the same time, our research is in line with prior empirical findings towards the direction of extended regulation to the price and quantity of the dominant firm bids. As can be seen from the countries of the European Union where the Target model has been implemented, it takes a period of one and a half years for the market to function properly and for healthy competition to prevail. One of the main limitations of the study is that the study explores only the first nine months of its execution; thus, future research should utilize new data and reevaluate the effectiveness of Target Model implementation in the wholesale market of Greece. This study documents in detail all the developments that took place up to this point, but this is yet to be seen in the future if the Target model achieves functioning properly and effectively in Greece and eventually benefiting the final consumers.

Author Contributions

Conceptualization, F.I., K.K. and K.A.; Data curation, F.I. and A.E.; Formal analysis, F.I.; Investigation, F.I. and K.K.; Methodology, F.I., K.K. and K.A.; Project administration, F.I., K.K., K.A. and A.E.; Software, F.I.; Supervision, K.K. and K.A.; Validation, K.K. and K.A.; Visualization, A.E.; Writing—original draft, F.I. and A.E.; Writing— review & editing, F.I., K.K. and K.A. funding acquisition, F.I. All authors have read and agreed to the published version of the manuscript.

Funding

This research was partially funded through a Ph.D. scholarship by Hellenic Petroleum, via A.U.TH. Research Committee, grant number 98665.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Data are publicly available in the following link: https://www.enexgroup.gr/web/guest/markets-publications-el-day-ahead-market (accessed on 7 June 2021).

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A

Figure A1.

Projection of CO2 Price evolution €/t, Source: Authors’ projections.

Figure A2.

Estimation of average annual total cost of Natural Gas-fired Units (€/ΜWh), (2017–2040), Source: Authors’ projections.

Figure A2.

Estimation of average annual total cost of Natural Gas-fired Units (€/ΜWh), (2017–2040), Source: Authors’ projections.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Table A1.

RES Auctions Results (PV & Technology Neutral), Source: Regulatory Authority for Energy (RAE).

Table A1.

RES Auctions Results (PV & Technology Neutral), Source: Regulatory Authority for Energy (RAE).

| Participation/Applications (MW) | Final Auctioned Capacity (MW) | Starting Price (€/MWh) | Highest Bid (€/MWh) | Lowest Bid (€/MWh) | Weighted Price (€/MWh) | |

|---|---|---|---|---|---|---|

| July 2018 | ||||||

| Category Ι (PV < 1 MWp) | 94.07 | 53.52 | 85.00 | 80.00 | 75.87 | 78.42 |

| Category ΙI (1 MWp < PV < 20 MWp) | 93.44 | 53.40 | 80.00 | 71.00 | 62.97 | 63.81 |

| December 2018 | ||||||

| Category Ι (PV < 1 MWp) | 108.40 | 61.95 | 81.71 | 68.99 | 63.00 | 66.66 |

| Category ΙI (1 MWp < PV < 20 MWp) | 151.32 | 86.47 | 71.91 | 71.91 | 63.00 | 70.39 |

| April 2019 | ||||||

| Category ΙV (technology neutral) (Technology Neutral: Common Auction for PV > 20MW & Wind > 50MW) | 637.78 | 437.78 | 64.72 | 64.72 | 53.00 | 57.03 |

| July 2019 | ||||||

| Category Ι (PV < 20 MWp) | 200.26 | 142.8 | 69.26 | 67.7 | 61.95 | 62.78 |

| December 2019 | ||||||

| Category Ι (PV<20 MWp) | 147.65 | 105.00 | 66.02 | 65.99 | 53.82 | 59.98 |

| April 2020 | ||||||

| Category ΙV (technology neutral) * | 712 | 502.94 | 61.32 | 54.82 | 49.11 | 51.59 |

| July 2020 | ||||||

| Category Ι (PV < 20 MWp) | 94.07 | 141.93 | 63.00 | 62.45 | 45.84 | 49.80 |

| May 2021 | ||||||

| Category V (technology neutral) (Technology Neutral: Common Auction for PV < 20MW & Wind < 50MW) | 1090.27 | 350 | 53.86 | 41 | 32.97 | 37.60 |

* Technology Neutral: Common Auction for PV > 20MW & Wind > 50MW.

References

- Cepeda, M.; Finon, D. Generation capacity adequacy in interdependent electricity markets. Energy Policy 2011, 39, 3128–3143. [Google Scholar] [CrossRef]

- Pellini, E. Measuring the impact of market coupling on the Italian electricity market. Energy Policy 2012, 48, 322–333. [Google Scholar] [CrossRef]

- Böckers, V.; Heimeshoff, U. The extent of European power markets. Energy Econ. 2014, 46, 102–111. [Google Scholar] [CrossRef]

- Keles, D.; Bublitz, A.; Zimmermann, F.; Genoese, M.; Fichtner, W. Analysis of design options for the electricity market: The German case. Appl. Energy 2016, 183, 884–901. [Google Scholar] [CrossRef]

- Hyland, M. Restructuring European electricity markets—A panel data analysis. Util. Policy 2016, 38, 33–42. [Google Scholar] [CrossRef] [Green Version]

- Metaxas, A.; Mathioulakis, M.; Lykidi, M. Implementation of the Target Model: Regulatory reforms and obstacles for the regional market. Eur. Energy J. 2019, 8, 28–43. [Google Scholar]

- Koltsaklis, N.; Dagoumas, A. Policy implications of power exchanges on operational scheduling: Evaluating EUPHEMIA’s market products in case of Greece. Energies 2018, 11, 2715. [Google Scholar] [CrossRef] [Green Version]

- Papaioannou, G.P.; Dikaiakos, C.; Dagoumas, A.S.; Dramountanis, A.; Papaioannou, P.G. Detecting the impact of fundamentals and regulatory reforms on the Greek wholesale electricity market using a SARMAX / GARCH model. Energy 2018, 142, 1083–1103. [Google Scholar] [CrossRef]

- Dagoumas, A. Impact of bilateral contracts on wholesale electricity markets: In a case where a market participant has dominant position. Appl. Sci. 2019, 9, 382. [Google Scholar] [CrossRef] [Green Version]

- Newbery, D.; Strbac, G.; Viehoff, I. The benefits of integrating European electricity markets. Energy Policy 2016, 94, 253–263. [Google Scholar] [CrossRef] [Green Version]

- Ringler, P.; Keles, D.; Fichtner, W. How to benefit from a common European electricity market design. Energy Policy 2017, 101, 629–643. [Google Scholar] [CrossRef]

- Zachmann, G. Electricity wholesale market prices in Europe: Convergence? Energy Econ. 2008, 30, 1659–1671. [Google Scholar] [CrossRef]

- Weidlich, A.; Veit, D. A critical survey of agent-based wholesale electricity market models. Energy Econ. 2008, 30, 1728–1759. [Google Scholar] [CrossRef]

- Weigt, H.; von Hirschhausen, C. Price formation and market power in the German wholesale electricity market in 2006. Energy Policy 2008, 36, 4227–4234. [Google Scholar] [CrossRef] [Green Version]

- Biskas, P.N.; Chatzigiannis, D.I.; Bakirtzis, A.G. European Electricity Market Integration with Mixed Market Designs Part II: Solution Algorithm and Case Studies. IEEE Trans. Power Syst. 2014, 29, 466–475. [Google Scholar] [CrossRef]

- Newbery, D.; Pollitt, M.G.; Ritz, R.A.; Strielkowski, W. Market design for a high-renewables European electricity system. Renew. Sustain. Energy Rev. 2018, 91, 695–707. [Google Scholar] [CrossRef] [Green Version]

- Peng, D.; Poudineh, R. Electricity market design under increasing renewable energy penetration: Misalignments observed in the European Union. Util. Policy 2019, 61, 100970. [Google Scholar] [CrossRef]

- Biskas, P.; Chatzigiannis, D.; Bakirtzis, A. European Electricity Market Integration with Mixed Market Designs Part I: Formulation. IEEE Trans. Power Syst. 2014, 29, 458–465. [Google Scholar] [CrossRef]

- Di Cosmo, V.; Collins, S.; Deane, P. Welfare analysis of increased interconnection between France and Ireland. Energy Syst. 2020, 11, 1047–1073. [Google Scholar] [CrossRef]

- Di Cosmo, V.; Lynch, M. Competition and the single electricity market: Which lessons for Ireland? Util. Policy 2016, 41, 40–47. [Google Scholar] [CrossRef] [Green Version]

- Newbery, D. Tales of two islands—Lessons for EU energy policy from electricity market reforms in Britain and Ireland. Energy Policy 2017, 105, 597–607. [Google Scholar] [CrossRef]

- Tanrisever, F.; Derinkuyu, K.; Jongen, G. Organization and functioning of liberalized electricity markets: An overview of the Dutch market. Renew. Sustain. Energy Rev. 2015, 51, 1363–1374. [Google Scholar] [CrossRef]

- González, J.S.; Alonso, C.Á. Industrial electricity prices in Spain: A discussion in the context of the European internal energy market. Energy Policy 2021, 148, 111930. [Google Scholar] [CrossRef]

- Biskas, P.; Simoglou, C.; Zoumas, C.; Bakirtzis, A. Evaluation of the impact of IPPS on the Greek wholesale and retail electricity markets. In Proceedings of the IASTED International Conference on Power and Energy Systems, EuroPES 2012, Napoli, Italy, 25–27 June 2012; pp. 208–215. [Google Scholar] [CrossRef]

- Ioannidis, F.; Kosmidou, K.; Makridou, G.; Andriosopoulos, K. Market Design of an Energy Exchange: The Case of Greece. Energy Policy 2019, 133, 110887. [Google Scholar] [CrossRef]

- Vlados, C.; Chatzinikolaou, D.; Kapaltzoglou, F. Energy market liberalisation in Greece: Structures, policy and prospects. Int. J. Energy Econ. Policy 2021, 11, 115–126. [Google Scholar] [CrossRef]

- Hogan, W.W. Electricity market restructuring: Reforms of reforms. J. Regul. Econ. 2002, 21, 103–132. [Google Scholar] [CrossRef]

- Hogan, W.W. Virtual bidding and electricity market design. Electr. J. 2016, 29, 33–47. [Google Scholar] [CrossRef]

- Ioannidis, F.; Kosmidou, K.; Savva, C.; Theodossiou, P. Electricity pricing using a periodic GARCH model with conditional skewness and kurtosis components. Energy Econ. 2021, 95, 105110. [Google Scholar] [CrossRef]

- Stathakis, E.; Papadimitriou, T.; Gogas, P. Forecasting price spikes in electricity markets. Rev. Econ. Anal. 2020, 12, 1–24. [Google Scholar]

- HAEE. Greek Energy Market Report 2020; Hellenic Association for Energy Economics (2020). Available online: https://www.haee.gr (accessed on 11 June 2021).

- Stavrakas, V.; Kleanthis, N.; Flamos, A. An ex-post assessment of RES-E support in Greece by investigating the monetary flows and the causal relationships in the electricity market. Energies 2020, 13, 4575. [Google Scholar] [CrossRef]

- Faia, R.; Pinto, T.; Vale, Z.; Corchado, J.M. Prosumer Community Portfolio Optimization via Aggregator: The Case of the Iberian Electricity Market and Portuguese Retail Market. Energies 2021, 14, 3747. [Google Scholar] [CrossRef]

- Bahn, O.; Samano, M.; Sarkis, P. Market power and renewables: The effects of ownership transfers. Energy J. 2021, 42, 195–225. [Google Scholar] [CrossRef]

- Mautino, L. The EU Electricity Target Model: The Devil Is in the Details? 2013. Available online: https://www.oxera.com. (accessed on 13 September 2021).

Figure 1.

Evolution of Gross Energy Consumption in Greece (ktoe), (2018–2040), Source: National Energy and Climate Plan (2020) and Authors’ estimations.

Figure 1.

Evolution of Gross Energy Consumption in Greece (ktoe), (2018–2040), Source: National Energy and Climate Plan (2020) and Authors’ estimations.

Figure 2.

Evolution of Electricity Generation by Source in Greece (%), (2018–2030), Source: National Energy and Climate Plan (2020) and Authors’ estimations.

Figure 2.

Evolution of Electricity Generation by Source in Greece (%), (2018–2030), Source: National Energy and Climate Plan (2020) and Authors’ estimations.

Figure 3.

PPC’s Market Share (%), (2016–May 2021), Source: Hellenic Energy Exchange and Authors’ estimations.

Figure 3.

PPC’s Market Share (%), (2016–May 2021), Source: Hellenic Energy Exchange and Authors’ estimations.

Figure 4.

Retail Market Share (%), (2016–May 2021), Source: Hellenic Energy Exchange and Authors’ estimations.

Figure 4.

Retail Market Share (%), (2016–May 2021), Source: Hellenic Energy Exchange and Authors’ estimations.

Figure 5.

Historical Data and Forecast of Total Annual Demand for Electricity in Greece (GWh), (2006–2031), Source: Hellenic Transmission System Operator and Authors’ estimations.

Figure 5.

Historical Data and Forecast of Total Annual Demand for Electricity in Greece (GWh), (2006–2031), Source: Hellenic Transmission System Operator and Authors’ estimations.

Figure 6.

Day-Ahead & Intraday Prices (€/MWh) (November 2020–June 2021), Source: Hellenic Energy Exchange and Authors’ estimations.

Figure 6.

Day-Ahead & Intraday Prices (€/MWh) (November 2020–June 2021), Source: Hellenic Energy Exchange and Authors’ estimations.

Figure 7.

Day-Ahead Market, Sell Volume mix (%), (May 2021), Source: Hellenic Energy Exchange and Authors’ estimations.

Figure 7.

Day-Ahead Market, Sell Volume mix (%), (May 2021), Source: Hellenic Energy Exchange and Authors’ estimations.

Figure 8.

Intraday Volume—Sell Volume mix (%), (May 2021), Source: Hellenic Energy Exchange and Authors’ estimations.

Figure 8.

Intraday Volume—Sell Volume mix (%), (May 2021), Source: Hellenic Energy Exchange and Authors’ estimations.

Figure 9.

Day-Ahead Market—Buy Volume mix (%), (May 2021), Source: Hellenic Energy Exchange and Authors’ estimations.

Figure 9.

Day-Ahead Market—Buy Volume mix (%), (May 2021), Source: Hellenic Energy Exchange and Authors’ estimations.

Figure 10.

Intraday—Buy Volume mix (%), (May 2021), Source: Hellenic Energy Exchange and Authors’ estimations.

Figure 10.

Intraday—Buy Volume mix (%), (May 2021), Source: Hellenic Energy Exchange and Authors’ estimations.

Figure 11.

Daily Average Market Clearing Price in Greece (€/ΜWh), (2008–July 2021), Source: Hellenic Energy Exchange and Authors’ estimations.

Figure 11.

Daily Average Market Clearing Price in Greece (€/ΜWh), (2008–July 2021), Source: Hellenic Energy Exchange and Authors’ estimations.

Figure 12.

Daily Average Market Clearing Price in Greece (€/ΜWh), (2018–July 2021), Source: Hellenic Energy Exchange and Authors’ estimations.

Figure 12.

Daily Average Market Clearing Price in Greece (€/ΜWh), (2018–July 2021), Source: Hellenic Energy Exchange and Authors’ estimations.

Figure 13.

Monthly Average Market Clearing Price (€/ΜWh), (2019–July 2021), Source: Hellenic Energy Exchange and Authors’ estimations.

Figure 13.

Monthly Average Market Clearing Price (€/ΜWh), (2019–July 2021), Source: Hellenic Energy Exchange and Authors’ estimations.

Figure 14.

CO2 European Emission Allowances (€/ton), (2017–May 2021), Source: EEX and Authors’ estimations.

Figure 14.

CO2 European Emission Allowances (€/ton), (2017–May 2021), Source: EEX and Authors’ estimations.

Figure 15.

Daily Imbalance Price in Greece (€/ΜWh), (January 2020–July 2021), Source: Hellenic Transmission System Operator and Authors’ estimations.

Figure 15.

Daily Imbalance Price in Greece (€/ΜWh), (January 2020–July 2021), Source: Hellenic Transmission System Operator and Authors’ estimations.

Figure 16.

Weekly Standard Deviation of imbalance prices in Greece, (January 2020–July 2021), Source: Hellenic Transmission System Operator and Authors’ estimations.

Figure 16.

Weekly Standard Deviation of imbalance prices in Greece, (January 2020–July 2021), Source: Hellenic Transmission System Operator and Authors’ estimations.

Figure 17.

Timeline of important developments following the Target Model implementation in Greece.

Figure 18.

New RES Framework under the Target Model in Greece, Source: Hellenic Energy Exchange and Authors’ estimations.

Figure 18.

New RES Framework under the Target Model in Greece, Source: Hellenic Energy Exchange and Authors’ estimations.

Figure 19.

Reference Market Price in Greece (€/MWh), (November 2019–June 2021), Source: Hellenic Energy Exchange and Authors’ estimations.

Figure 19.

Reference Market Price in Greece (€/MWh), (November 2019–June 2021), Source: Hellenic Energy Exchange and Authors’ estimations.

Table 1.

Summary of the main figures from DAM & LIDAs (April & May 2021), Source: Hellenic Energy Exchange and Authors’ estimations.

Table 1.

Summary of the main figures from DAM & LIDAs (April & May 2021), Source: Hellenic Energy Exchange and Authors’ estimations.

| May 2021 April 2021 | DAM | LIDA 1 | LIDA 2 | LIDA 2 |

|---|---|---|---|---|

| Price (€/MWh) | 63.16 | 62.53 | 63.12 | 63.52 |

| 64.17 | 63.17 | 64.88 | 66.80 | |

| Volume (GWh) | 3972 | 28.2 | 14.6 | 11.3 |

| 4176 | 37.8 | 17.0 | 9.7 | |

| Value (MM€) | 254.7 | 1.91 | 0.98 | 0.78 |

| 271.1 | 2.28 | 1.08 | 0.64 |

Table 2.

Monthly average Intraday prices (€/ΜWh), (November 2020–June 2021), Source: Hellenic Energy Exchange and Authors’ estimations.

Table 2.

Monthly average Intraday prices (€/ΜWh), (November 2020–June 2021), Source: Hellenic Energy Exchange and Authors’ estimations.

| LIDA 1 | LIDA 2 | LIDA 3 | Average IDM | |

|---|---|---|---|---|

| Nov-20 | 53.21 | 51.84 | 56.03 | 53.69 |

| Dec-20 | 60.26 | 59.09 | 54.98 | 58.11 |

| Jan-21 | 53.57 | 49.9 | 48.07 | 50.51 |

| Feb-21 | 50.67 | 54.31 | 54.52 | 53.16 |

| Mar-21 | 55.66 | 56.82 | 59.11 | 57.19 |

| Apr-21 | 63.17 | 64.88 | 66.8 | 64.95 |

| May-21 | 62.53 | 63.12 | 63.51 | 63.05 |

| June 2021 | 82.96 | 83.12 | 85.75 | 83.94 |

Table 3.

Imports/Exports at Day-Ahead Market, May 2021 (GWh), Source: Hellenic Energy Exchange and Authors’ estimations.

Table 3.

Imports/Exports at Day-Ahead Market, May 2021 (GWh), Source: Hellenic Energy Exchange and Authors’ estimations.

| Exports—Explicit Allocation | Imports—Explicit Allocation | Exports—Implicit Allocation | Imports—Implicit Allocation | |

|---|---|---|---|---|

| Albania | 17 | 235 | 0 | 0 |

| North Macedonia | 75 | 166 | 0 | 0 |

| Bulgaria | 12 | 125 | 7 | 135 |

| Italy | 0 | 0 | 152 | 25 |

| Turkey | 6 | 37 | 0 | 0 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Ioannidis, F.; Kosmidou, K.; Andriosopoulos, K.; Everkiadi, A. Assessment of the Target Model Implementation in the Wholesale Electricity Market of Greece. Energies 2021, 14, 6397. https://doi.org/10.3390/en14196397

AMA Style

Ioannidis F, Kosmidou K, Andriosopoulos K, Everkiadi A. Assessment of the Target Model Implementation in the Wholesale Electricity Market of Greece. Energies. 2021; 14(19):6397. https://doi.org/10.3390/en14196397

Chicago/Turabian StyleIoannidis, Filippos, Kyriaki Kosmidou, Kostas Andriosopoulos, and Antigoni Everkiadi. 2021. "Assessment of the Target Model Implementation in the Wholesale Electricity Market of Greece" Energies 14, no. 19: 6397. https://doi.org/10.3390/en14196397

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.