New Circular Challenges in the Development of Take-Away Food Packaging in the COVID-19 Period

1

Research and Innovation Centre Pro-Akademia, 9/11 Innowacyjna Street, 95-050 Konstantynów Łódzki, Poland

2

National Laboratory for Energy and Geology (LNEG, I. P.), Bioenergy and Biorefineries Unit, Estrada do Paço do Lumiar 22, 1649-038 Lisbon, Portugal

3

Faculty of Economics and Management, University of Zielona Góra, Licealna Street 9, 65-417 Zielona Góra, Poland

*

Author to whom correspondence should be addressed.

Energies 2021, 14(15), 4705; https://doi.org/10.3390/en14154705

Submission received: 14 June 2021

/

Revised: 21 July 2021

/

Accepted: 30 July 2021

/

Published: 3 August 2021

(This article belongs to the Special Issue Economic Aspects of Low Carbon Development)

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Abstract

:The COVID-19 pandemic has set new challenges for the HoReCa industry. Lockdowns have coincided with and strongly impacted the industrial transformation processes that have been taking place for a decade. Among the most important HoReCa transition processes are those related to the rapid growth of the delivery-food market and ordering meals via internet platforms. The new delivery-food market requires not only the development of specific distribution channels, but also the introduction of appropriate, very specific food packaging. Food packaging and its functionality are defined by the administrative requirements and standards applicable to materials that have contact with food and principally through the prism of the ecological disaster caused by enormous amounts of plastic waste, mainly attributed to the food packaging. To meet environmental and administrative requirements, new technologies to produce food packaging materials are emerging, ensuring product functionality, low environmental impact, biodegradability, and potential for composting of the final product. However, predominantly, the obtained product should keep the nutritional value of food and protect it against changes in color or shape. Current social transformation has a significant impact on the food packaging sector, on one hand creating a new lifestyle for society all over the world, and on the other, a growing awareness of the negative impact of humans on the environment and increasing responsibility for the planet. The COVID-19 pandemic has highlighted the need to develop a circular economy based on the paradigm of shortening distribution channels, using local raw materials, limiting the consumption of raw materials, energy, water, and above all, minimizing waste production throughout the life cycle of products, all of which are in line with the idea of low-carbon development.

1. Introduction

The coronavirus pandemic has changed the entire world. However, it has had different impacts on diverse sectors of socio-economic life. For example, in 2020, the global gross domestic product (GDP) decreased by 3.4% [1]. Furthermore, many rules and principles have changed, as the effectiveness and durability of many economic systems have been verified. Due to the pandemic, entrepreneurs from the SME sector incurred additional costs of up to 25% of companies’ expenses. A study conducted in Poland on a group of 357 companies from the SME sector, including micro (employing 3–9 people), small (10–49), and medium-sized enterprises (50–249) showed that 82% of SMEs consider their economic situation as worse and have no plans to invest or increase employment in the near-future, i.e., three months [2].

However, the circular economy paradigm is one of the few to have been validated, confirmed and strengthened during the pandemic. A circular economy is defined by the European Parliament as a model for extending the life cycle of products through both production and consumption methods for as long as possible. The circularity of the products and material indicates recycling, reusing, sharing, leasing, etc. In practice, this means reducing waste to a minimum and the saving natural resources, water and energy to a maximum. As a consequence, the implementation of the circular economy concept leads to a change in the traditional, linear economic model, which is based on the system: “raw material-production-product–waste” in favour of: waste (used product) as a raw material (feed-stock) for the production of new, sometimes better products [1], as shown in Figure 1. The circular economy paradigm is closely related to sustainable development. The implementation of the circular economy widely will contribute to the achievement of the Sustainable Development Goals of the United Nations 2030 Agenda. The sanitary and hygienic regimes enforced during the Coronavirus period contribute to the achievement of Sustainable Development Goals too, e.g., goal 3: good health and well-being, goal 6: clean water and sanitation, as well as goals 14 and 15: life below water and life on land. However, the pandemic situation contributes most towards achievement of the 12th SDG regarding responsible consumption and production implementation.

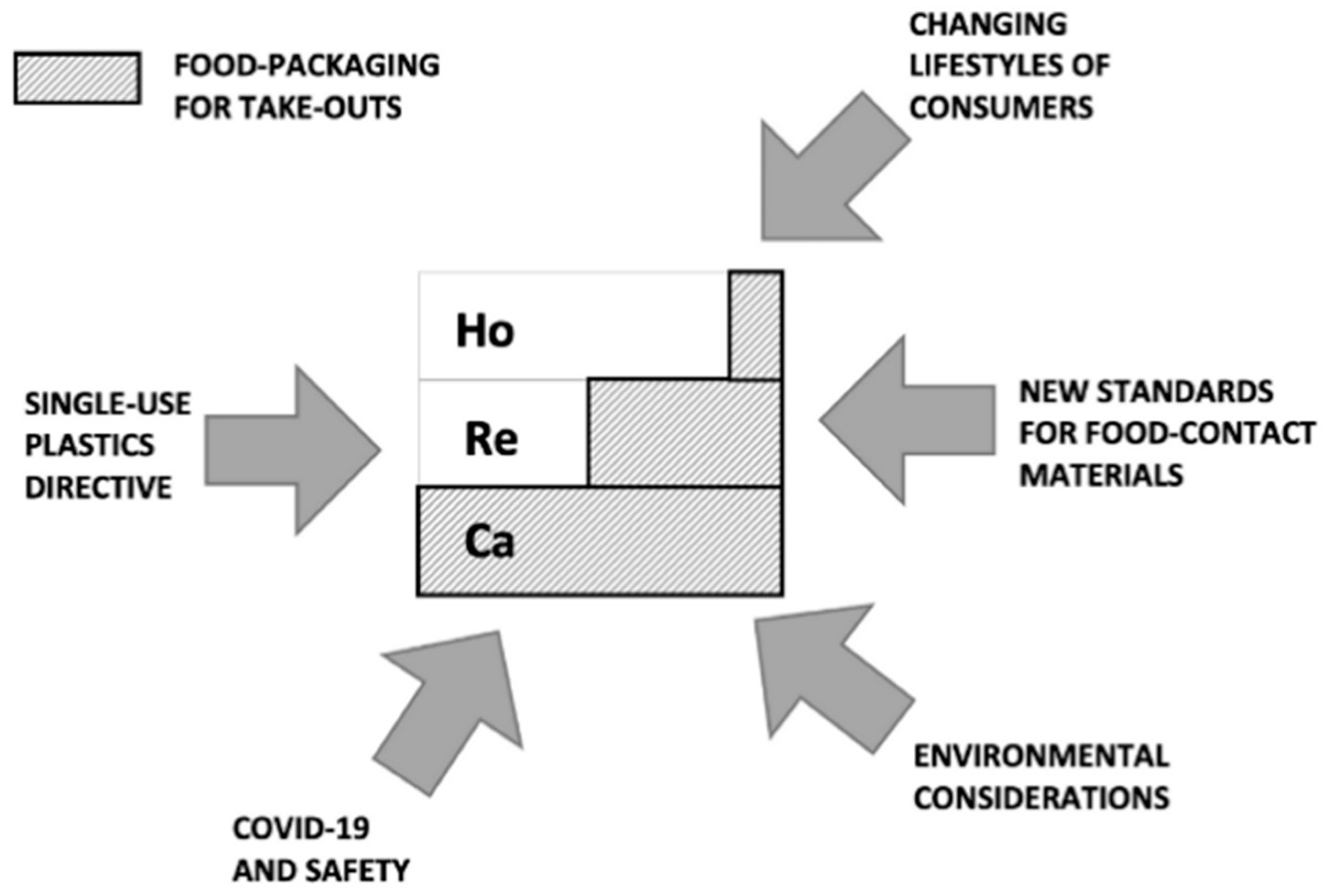

The importance of the basic principles of the circular economy were shown with full force during the lockdown period, and in particular the care for use of all resources effectively, e.g., raw materials, water, energy, working time, and others. Intelligent and smart waste management and closing technology cycles using waste as a wholesome raw material for production have become more important than ever. The results of our study, dedicated to new perspectives for take-away packaging show the impact the 12th SDG implementation. The following specific but associated factors have the greatest importance for the 12th SDG achievement: changing lifestyle of food consumers, new standards for food-contacts material together with the single-use plastics directive, together with environmental considerations and the sanitary safety caused by COVID-19 requirements (Figure 2).

The main idea of the study is to present the impact of the pandemic situation on the food packaging material development under the condition of circular economy paradigm. We focus our attention on the specific questions of how food packaging, responding especially to the needs of the HoReCa (hotels, restaurants, catering) sector, addresses the mutually exclusive requirements caused by circular economy rules and the pandemic regime simultaneously.

The challenges related to the pandemic have clashed with such global trends in the development of a circular economy, especially in the concept of digitalization, new organization of decentralized and remote work in sustainable growing cities, and green, environmentally friendly technology implemented in industries, etc. During the pandemic, changes in social behavior are observed, favoring solutions such as “from owning to sharing”, online shopping, etc. Within the HoReCa sector, new “pandemic” trends, e.g., increasing of ordering meals with home delivery, the use of single-use packaging on a large scale, and request for sanitary and hygienic safety, have been observed [3]. Within the sector of single-use packaging for food production, the trends of the circular economy are seen in the following dimensions:

- management of natural resources to produce packaging, efficient use of water, energy and fuels, including reduction of transport costs, both in terms of the supply of raw materials and of employees, as well as shortening the distance between the producer of ready, processed food, and the end-user/final consumer, which create new challenges on food packaging system;

- waste minimization and intelligent waste management;

- limitation of people’s work through flexible organization of working time and, if possible, home-office;

- digitalization of the sector either on the production and distribution side.

The review of the literature indicates that little research has investigated the food packaging for HoReCa sector in the context of circular economy development, taking into consideration environmental, energy, and climate problems.

Simultaneously, we hardly identified scientific research where these problems have been addressed jointly, in multi-dimensional combination. Therefore, we based our study on the specific and available sources of information, mostly statistical reports, internet papers, and professional journals articles.

This study has therefore addressed the following specific research questions:

- What is the association between rising HoRECa market expectations (end-users and consumers) of the functionality of food packaging in context of the environmental, energy, and climate requirements in the light of pandemic situation?

- What is the association between the trends of replacing the plastic food packaging by the food packaging made by biopastic and the circular economy development catalyzed by the COVID-19?

- What is the impact of sanitary and hygienic regimes caused by pandemic situations on the development of the food packaging market?

We structured the study as follows:

- The methodology of the research is presented in Section 2.

- The results of our study, with consideration of the specific research questions and presentation multi-dimensional associations between new consumer trends in take-away food packaging, circular economy development, environmental requirements, and impact of the sanitary and hygienic regimes on replacing plastic take-away packaging by bioplastics, are presented in Section 3.

- Conclusions are presented in Section 4.

- References with 59 literary positions are provided at the end of the study (Section 5).

2. Method of Research

The research conducted in this work is a part of the research areas of positive economics. This work aims to predict the effects of the COVID-19 pandemic on the implementation of the circular economy paradigm in selected economic sectors, i.e., HoReCa and the production of packaging for food. These industries share common areas of interest, such as food packaging. To assess the impact of the SARS-CoV-2 pandemic on the development of the HoReCa sector in connection with the food packaging sector, 57 source materials (references) were analyzed and most of them are reports and current statistics.

On the basis of analyses of the Scopus and Web of Science databases, it is not possible to conduct a literature review that would cross-analyze HoReCa, the packaging sector, both in line with the circular economy paradigm. Therefore, the source material that was used for the extrapolation was (i) current information from the market, (ii) opinions of specialists and practitioners, (iii) interviews, and (iv) scarce literature data. In line with the assumptions of the positive economy, the core elements of the methodology were observations of the market and analyses of the observed phenomena, drawing conclusions for the future, although without formulating them in the form of socio-economic or political recommendations. Positive economics deal with decidable (empirically or logically) facts and the search for cause–effect relationships for explaining the occurring economic and social phenomena and their impact for future.

The results presented in this work were assessed by expert interpretation methods based on the available statistical data, generalized results, and finally drawn conclusions and forecasts. The main interests are focused on the multifaceted impact of the implementation of the circular economy paradigm and the currently observed social changes on the development of the food packaging sector.

The geographic area of the study was mainly the European Union with an especial focus on Poland, with references to the global situation. The global dimension is necessary especially with regard to the contamination of soil and water with plastic, which is observed all over the world, and also concerning new trends in take-away food packaging, which, although mainly created outside Europe, are promoted and widely disseminated in Europe. In order to effectively achieve the research goals, the following research methods were also used in the work:

- Analysis of source documents.

- Tabular and descriptive methods and charts.

- Analysis of the literature on the subject.

- Descriptive and mathematical statistics methods.

- Deductive method.

The research methods used in the study are appropriate for a positive economic approach and they are based on an objective, devoid of our individual assessment or emotion analysis of past and present facts within the scope of the topic of our research [2]. On such a basis, we are drawing conclusions for the future of bioplastics application to the HoReCa food packaging and for the association of pandemic requirements with the circular economy development.

We have gathered facts, statistics, and valuable opinions of practitioners, which set the basis for predicting the impact of COVID19 restrictions on the development of a circular economy in relation to biodegradable food packaging.

A positive economy and its methodology are tangible. It deals with “what is” rather than “what should be” and is based on facts, which are discussed almost exactly at the time of their formation. Because of that, the methodology of a positive economy is similar to methods typical for physical and technical sciences. Of course, the methods of our study relate to multidimensional economic and social issues, so they cannot be as objective as in the physical sciences. The effect of relativism is disturbed by, inter alia, market regulations, unpredictability of technology development, mutual relations between people, etc. Nevertheless, the collected evidence (statistics, expert statements, market analysis, etc.) was used at two stages: at the phase of the research questions and hypotheses preparations, as well as at the stage of drawing objective conclusions.

The proposed methodology allowed a complete and comprehensive analysis of the actual data in order to define an association between the restrictions introduced during the pandemic period and boosting the implementation of the circular economy concept in the area of biodegradable packaging for the HoReCa industry. The conclusions resulting from the study do not contradict our experiences or observations.

3. Results

The COVID-19 pandemic has had a negative impact on each of the HoReCa market segment, although the sector of catering and ordering food with delivery, the so-called “take-away meals” have suffered the least [4]. The study “Coronavirus and change in consumer behavior in Poland 2020” confirms that 65% of respondents plan to resign or limit visits to classic restaurants in favor of ordering food with delivery [5]. However, the pos- COVID-19 reality in Europe demonstrates that after re-opening, reservation of tables in restaurants hit numbers never seen in the past [6]. Regardless of this and despite the sanitary restrictions or even economic lockdowns, the take-away meals sector is dynamically developing, together with on-line portals for food ordering and with more and more interesting offers from companies specializing in delivering meals to consumers [7].

Ever since Pizza Hut launched the first-ever internet pizza ordering system in 1994, online food delivery has become a billion-dollar business. The food delivery market is divided into two main types: platform-to-customer and restaurant-to-customer. Platform-to-consumer delivery platforms, such as Takeaway.com, DeliveryHero.com, and Polish Pyszne.pl (part of Takeaway.com Central Core B.V.) have developed around the world due to the sale of consistent logistics and infrastructure solutions and attractive commission rates for restaurants. Platform-to-consumer delivery companies, such as Deliveroo, DoorDash, GrubHub or Uber Eats handle all food-delivery logistics. These companies have also grown in importance in the recent months of the pandemic, especially in densely populated urban regions.

The food delivery market continues to grow worldwide. Revenues in the on-line food delivery segment are expected to reach USD 151,526 million in 2021 and the annual growth rate (CAGR 2021–2024) will hit 6.36% [8]. Forecasted market volume is expected to increase to USD 182,327 million by 2024. The largest segment of the market is Platform-to-Consumer Delivery, with a forecast global market volume of USD 79,608 million in 2021, and the largest market growth expected in China at USD 56,936 million in 2021 [9]. In Europe, e.g., the CAGR of Germany is forecast to be around 20.6%. According to the latest Stava Report on the food delivery market [10], 20% of Polish restaurants used to deliver their meals to their customers and developed platform-to-consumer delivery.

Within 12 months (February 2020–January 2021), the number of restaurants and bars offering take-away meals in Poland has more than doubled. Profits of delivery-food businesses are growing faster than costs. In the analyzed period, revenues increased by an average of 20%, while costs increased by an average of 10%. After a preliminary analysis of the impact of the pandemic on food-delivery business, the growth was revised to 52.2% CAGR for the next seven years [11].

The development of the ready-made delivery-food market results in a growing demand for appropriate food-packaging characterized by its functionality, low price, and environmentally friendly and ecological character. The rising social understanding of environmental issues and acceptance of the urgent elimination of plastic single-use food packaging from everyday life are in contradiction to the established model of societies in most countries, where consumers are more and more willing to get food and meals prepared away (in restaurants or bars) or to get delivery-food. This means enlarged expectations and requirements of single-use functional food packaging, especially used on a large scale.

The period of the pandemic coincided with the entry into force of the Directive of the European Parliament and of the Council (EU) on the reduction of the impact of certain plastic products on the environment [12]. The directive obliges EU Member States to eliminate single-use plastic products and packaging, such as cutlery (forks, knives, spoons and chopsticks), plates and other dishes, drinking straws, and food containers already from 1 July 2021. On the other hand, the pandemic and administrative regulations created a pressure on the production sector and on the use in everyday life of safe food packaging. The pandemic has forced the use of sanitary and hygienic security measures on an unprecedented scale, and the Directive has forced the replacement of plastic food packaging with new, environmentally friendly packaging. As a result of this multiplied pressure, biodegradable packaging of high quality, with the functional features of packaging made using fossil fuel resources, began to appear on the market. notwithstanding which of these factors had a greater impact on the development of the technology to produce biodegradable single-use food packaging, their combined pressure doubtless contributed significantly to the practical implementation of the principles of circular economy in this economic sector.

Eliminating plastic packaging for food from everyday life and replacing it with biodegradable eco-packaging is not only consistent with the paradigm of a circular economy, but is also a response to the growing worldwide withdrawal from plastic in food packaging (plastic bottles, cups, trays, drinking straws, cutlery, etc.) in the name of environmental protection and widespread global perception of the ecological disaster caused by plastics.

Pollution by plastic waste is recognized by The United Nations Environment Program (UNEP) as a major global environmental problem and has reached epidemic proportions [13,14]. It is estimated that there are currently 100 million tons of plastic in the oceans, 80–90% of which comes from land-based sources. Microplastic is particularly dangerous. According to the CSIRO, Australia’s national science agency research, the bottom of the oceans pollutes about 14 million tons of microplastics, and more than twice as many micro-plastic contaminants are found on the ocean’s surface [15].

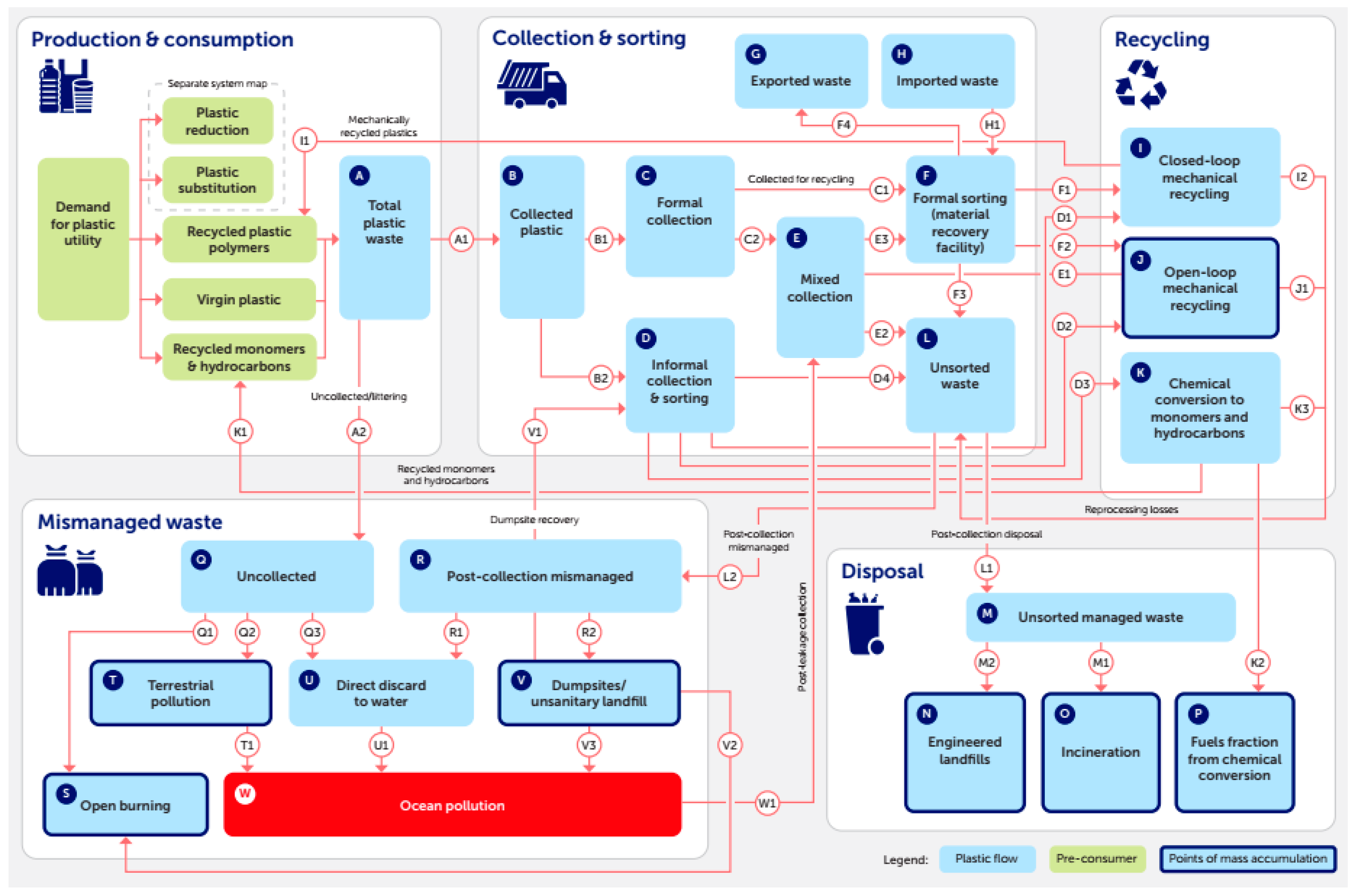

According to the last report of the Ellen MacArthur Foundation, a comprehensive circular economy approach has the potential to reduce the annual volume of plastics entering our oceans by over 80%, generate savings of USD 200 billion per year, providing a 25% reduction of greenhouse gas emissions as well as over 700,000 net jobs by 2040 [16]. However, to achieve this remains challenging, taking into consideration the complexity of the plastic flows in the economy, as depicted in Figure 3.

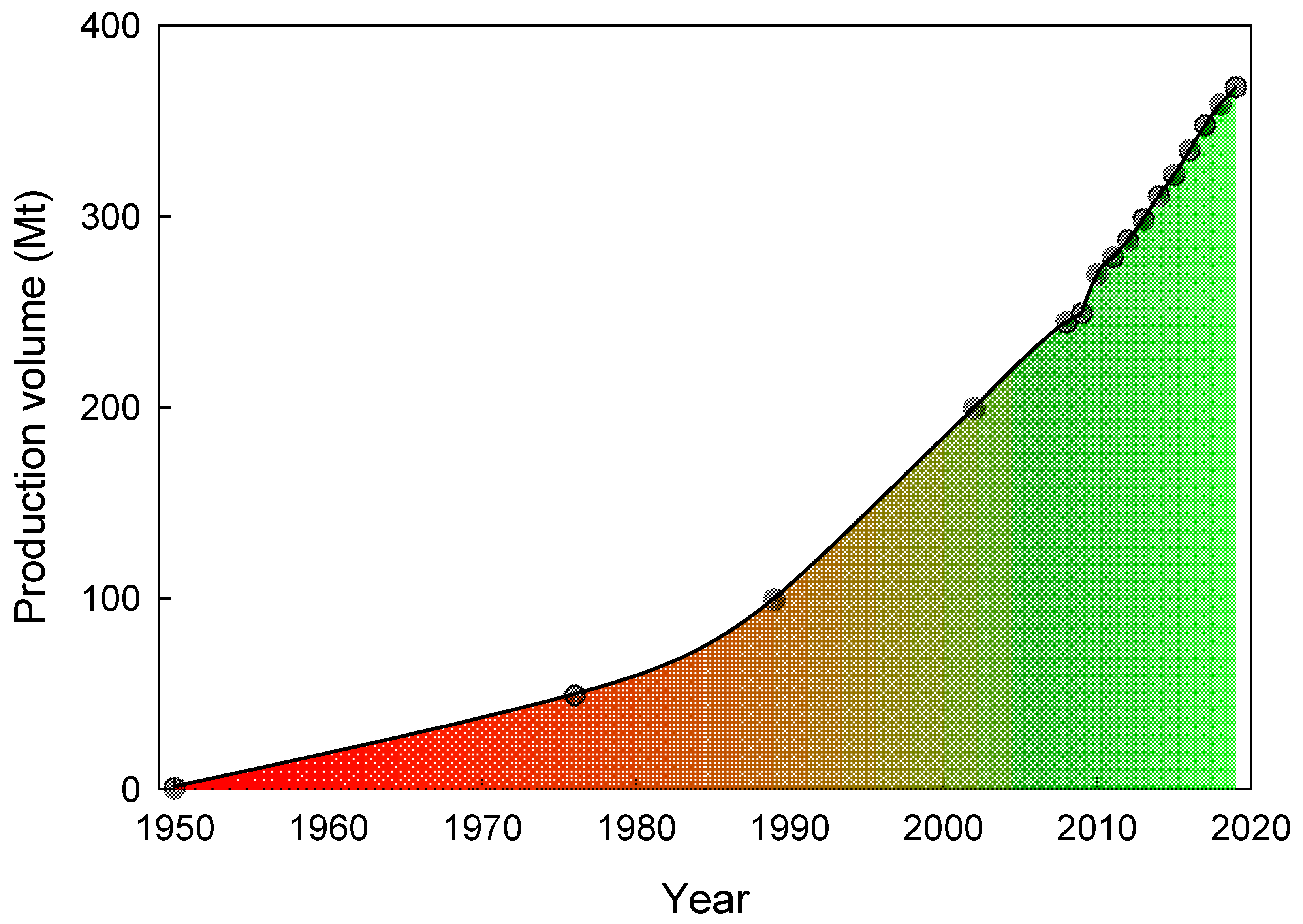

It is even more complex bearing in mind that, in 2019, the production of plastics worldwide was approximately 368 million tons, as depicted in Figure 4, and the incredible flexibility, versatility, and usefulness of this group of materials result in a steady increase in production from year to year [18].

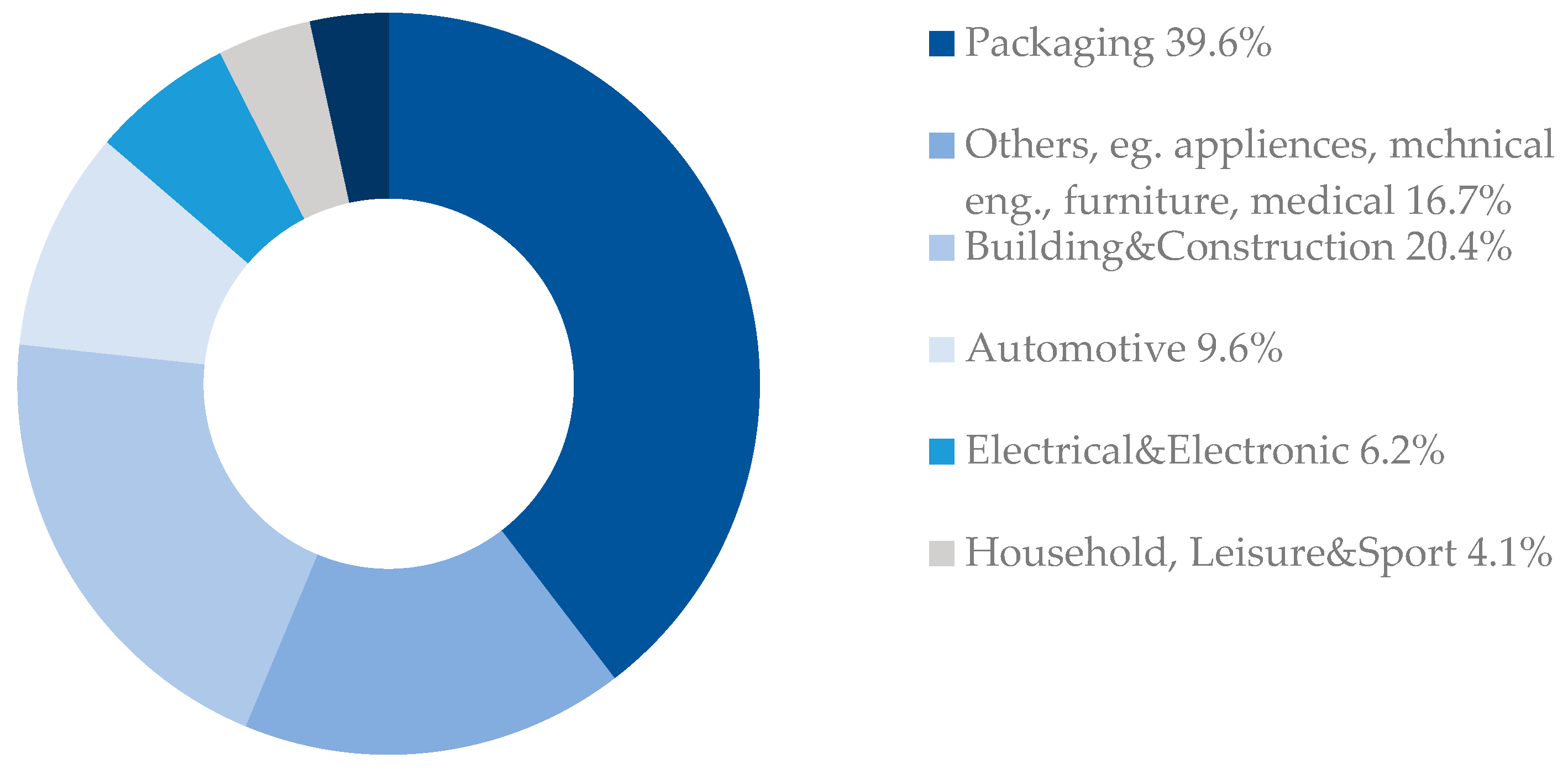

In 2019, the European plastics industry had a turnover of more than 350 billion euros [19]. Along with the increase in production, the market value of plastics is also growing steadily, especially given that they are used in many different products among which the largest end-user of plastics is the packaging industry, as shown in Figure 4 and Figure 5.

In Poland, the demand for plastics is 3.5 million tons per year, with the largest user of plastics, similarly to the whole EU, being the packaging industry with a share of 33%. Plastic is mainly used for the production of packaging, foil, and single-use products: plastic plates, cups, cutlery, drink tubes, and shopping bags [20]. At the same time, as stated already above, the level of pollution of the planet with used plastic packaging is increasing dramatically. In 2018, packaging waste generated per statistic inhabitant in the EU was estimated at 174 kg (varying from 67.8 kg per inhabitant in Croatia and 227.5 kg per inhabitant in Germany) [21]. The Directive of the European Parliament and of the Council of Europe [12] is to be successively implemented into national legal orders of each EU country starting in mid-2021. The Directive is going to significantly impact the life of every EU citizen, because it promotes the circular economy approach and gives preference to sustainable reusable products together with re-use systems instead of single-use products. This is therefore of the greatest importance for producers of disposable, single-use plastic products dedicated to contact with food and for the greatest end-user of such products, the HoReCa industry. Administrative requirements governing the growing awareness of the society all over the world about the urgent need to limit the use of plastic as a material for food packaging puts a pressure on seeking for a material that would have the functional features of plastics, traditionally produced from petroleum, but would be biodegradable and compostable. The demand for biodegradable and compostable packaging with the functional parameters of plastic, but manufactured in accordance with the assumptions of the circular economy, is growing, mainly due to the HoReCa industry demands.

The recent months of sanitary regimes caused by COVID-19 have revealed the failure of complex and overly complicated supply chain systems and long economic value chains. The catering suppliers and producers of “take-away food” focused on the use of locally available vegetables, fruits, dairy products, or meat fight to shorten the path of food “from farm to fork” [22], following the circular economy patterns, but at the same time burdening and littering the environment with increasing amounts of plastic food packaging. In the global structure of plastics trash, waste of packaging, especially food and drink packaging, is responsible of 64.8% of them [23].

Plastic used for the packing and transporting of food products, made of various materials, can be considered as a self-introduced market product or as a product inherently associated with the packaged food. Such a vision of the packaging material for food in the future is presented in “A Review of Contemporary Development from Conventional Plastics to Polylactic Acid Based Materials” [24].

The degree of market saturation with food packaging of biodegradable and compostable products is currently low as it is equal to only several percentage points. For example, in Poland, according to the estimation of the Polish Chamber of Packaging (PIO), in 2018, in the structure of the packaging market, biodegradable packaging products represent only approx. 2%, while in 2019 their share slightly increased to 2.3%. Although in 2021 an increase is expected, it will still be small, no higher than 3% [25]. Global production of biodegradable plastics for food packaging is expected to increase to 1.33 million in 2024, especially due to the significant growth rate of PLA and PHA [26].

In parallel with development of bioplastic production technology and the growing EU goal to limit and finally terminate disposable plastic packaging, the share of biodegradable packaging of organic origin in the overall market structure will systematically grow. It is expected that, by 2026, the European market of biodegradable plastics will take over 50% of all plastics packaging [27], while the share of all fossil fuel-based plastic packaging will decrease to 37.5%. However, taking into consideration that, in 2021, as stated above, the share of bioplastics remains at the level of a few percentage points, it will be challenging to achieve the challenging targets for 2026, i.e., half of the plastic packaging accounts for a bioplastic. Indeed, this would require a significant change in the social behavior as well as dramatic adjustments in the technological development to satisfy a dramatic increase in the demand for bioplastics to the market. Regardless, it is very likely that many new entities and new technologies for the production of disposable food packaging, with features imposed jointly by sanitary and hygienic considerations (the impact of the Coronavirus pandemic), new models of life (the impact of social changes), legal and administrative considerations (Directive 2019/904 [12]), and economic considerations (implementation of a circular economy) will appear in the near future [28].

Currently, biodegradable food packaging, made of, e.g., paper, bran, or palm leaves, is already available on the European market, but their properties are far from expected by the market. Packaging made only of paper/cardboard, bran or palm leaves has a limited use in contact with food, because their features related to, e.g., water absorption, i.e., the level of absorption and retention of a significant amount of liquid by the internal structures of the base material, de facto exclude them from the market for liquid food products. The functional features of paper or palm leaf packaging and tableware could be provided by plastic coatings, and therefore their degradation in the natural environment lasts as long as the plastics decomposes. Hence, again, the alternative for plastic packaging for food is bioplastic. Forecasts indicate that, by the end of 2020, the global bioplastic material market has reached even USD 5.5 billion, while the European biodegradable polymers market is currently worth USD 403 million and is growing at a rate of 15.5% [29]. Among biodegradable polymers are, e.g., poly(butylene succinate) (PBS), poly(lactic acid) (PLA), poly(butylene adipate terephthalate) (PBAT), poly(butylene succinate-co-adipate) (PBSA), cellulose, cellulose acetate, poly(hydroxybutyrate) (PHB) and its co-polymers, starch, and other natural polymers. All these polymers are readily biodegradable within relatively short time, and the kinetics of degradation depends on the environment, i.e., marine, fresh water, soil, home or industrial composting, landfill, and anaerobic digestion [30]. As some of them are so quickly biodegradable, their practical use in the packaging material is limited. Thus, the most popular bioplastic, especially in the context of packaging material, is PLA. Currently 70% of the PLA use is dedicated to the food packaging [19] and the largest global bioplastics producers are currently Bio-On (Italy), NatureWorks LLC (USA), Total Corbion PLA (Thailand), Mitsubishi Chemical (Japan), Biome Bioplastics (UK), Toray Industries (Japan), and Plantic Technologies (Australia). However, the main drawback in the PLA production is the feedstock. For this purpose, mostly food crops, e.g., beet and corn are used. Hence, an increasing demand for PLA and, on the other hand, a competition between food and bioplastic production is in the near future going to have a negative effect on food prices. It looks that bioplastic will follow the same pathway as observed in the case of biofuels [31]. At the beginning, the main feedstock for biofuels were food crops. This introduced a huge distortion on the food market resulting in a famous food vs. fuel dilemma. Only some years later did legislative changes impose a significant reduction in the use of food product for biofuel production, introducing, e.g., indirect land use change for the assessment of biofuel sustainability criteria [32] and finally implementing the celling for 1st generation biofuel [33]. Therefore, it can be expected that similar limitations will be imposed in the near future on the bioplastic market, forcing the search for alternative sources of sugars used for bioplastic production. As always, research and development is increasing and there are already numerous studies in the production of bioplastics and strictly PLA from alternative feedstocks including, e.g., food waste. The interesting examples of this direction of scientific approach can be the “RESources from URban BIo-waSte” project, implemented under the H2020 and coordinated by the Research Centre for Protection of Environment and Cultural Heritage, University of Rome “La Sapienza” [34], or the project executed in Poland by the Research and Innovation Center Pro-Akademia about the production PLA from agriculture and forest by-products [35].

The current pandemic situation also revealed how the long supply chains of the EU and the rest of the world are flawed and that the production of any good should be based on the local supply chain. Thus, the production of material for biodegradable food packaging in a circular business model should rely on technology based on local sources including organic wastes.

The HoReCa market, the largest consumer of disposable packaging and single-use tableware used for contact with food, was doing well before the COVID-19 pandemic. In 2019, in Poland, it increased by 6% year-on-year and reached the value of PLN 32 billion. The new model of life of Europeans resulted in an increase of the value of this market. Far below half of the households in Poland declare that they cook meals every day, and the most common reason for visiting restaurants and ordering take-out food is not only the lack of time, but also willingness to try new tastes, to meet with friends, and to spend time outside homes (reference). Europeans are more and more willing to use the service of food delivery in disposable packaging. Indeed, 34% of Poles like such service and order a food at least once a week. Another 37.8% of Poles do the same sometimes, however at least once a month. As much as 73.2% of the respondents of the market research prepared for the food-delivery portal pyszne.pl, agree with the statement that “Eating and shopping with delivery is the future on the Polish market”. According to the forecasts of experts from the HoReCa industry, the market for food deliveries in disposable packaging will double by 2025, and the online food ordering market will be 4.5 times larger [36,37,38]. Thus, the following main trends in the HoReCa industry can be noticed, which cross and mutually impact on circular economy development:

- 1.

- Demand for food supplies, made from locally available products, is growing rapidly because of the increase of the number of individual households across Europe.

- 2.

- While visits to restaurants are still important as a part of consumer habits and remain not only as places to satisfy hunger, but a kind of attractive leisure activity, take-out food is becoming more and more popular all over the world.

- 3.

- Food portals and external meal delivery companies are progressively gaining HoReCa market share and engaging in this aggressive competition.

- 4.

- The importance of veganism and vegetarianism continue to grow, and healthy menu options are a decisive factor for many restaurant visitors or food delivery customers. This trend is also reflected in the current popularity of novel foods, e.g., a vegetable meat. There is an increasing cooperation of vege-food producers and large restaurants-for example, Burger King’s Impossible Burger, and Beyond Meat’s. Veganism and vegetarianism impact not only on type of food but it is rather a broader philosophy of life in harmony with nature. Thus, it impacts economy, environment, and ethical and sustainable development.

- 5.

- The ability to order and pay for food online has guaranteed that restaurants stay afloat during the pandemic storm. Market research shows that consumers are ready to spend more money when ordering food online or through an app than when visiting a restaurant [39].

- 6.

- Dark kitchens, also known as virtual kitchens, cloud kitchens, ghost kitchens, or delivery-only restaurants, selling meals exclusively through delivery, are popping up all over Europe. VC-funded start-ups are opening one kitchen after another, food delivery companies, such as Bolt and Deliveroo, are also following this trend and starting their own kitchens, winning the benefits of cost savings in producing meals, ordering, and transporting.

- 7.

- Packaging is an important component of food supplies, to fulfill not only functional tasks in relation to food safety, the health of consumers, and aesthetic value, but also to inform about the attitude of the food producer towards the protection of the natural environment.

The above trends in the take-away food sector impact the development of a circular economy and environmental protection. Relying on local products and substrates mean (i) shorter transport, i.e., saving transport fuels, and (ii) reduction of CO2 and smog emissions, and (iii) less food waste. An important determinant for the implementation of the circularity paradigm in the HoReCa industry regarding packaging is the growing public awareness that it is urgent to limit the use of fossil plastic single-use packaging and replace it with bioplastic. The search for a technology for the production of bioplastic for food packaging from organic waste, such as table scraps, bakery, and confectionery waste, e.g., straw and beet pulp, will contribute to the development of the circular economy.

The analysis of HoReCa markets and plastic production, in particular Q2–Q4 2020 in European Union, leads to the conclusion that, in general, the growth rate of both these sectors has clearly decreased, with a clear increase in the sales of single-use plastic box and bag products that guarantee hygiene, as well as antiviral and antibacterial protection for food. Together with gloves, masks and helmets, sales of single-use food packaging, as well as food trays, plates, cutlery, and cups increased [40]. During the pandemic, the consumption of packaged food and food with delivery increased significantly too [19].

In Poland, catering orders, including dietary catering, increased by 30% compared to 2019. Catering companies that had a delivery and take-away infrastructure before the pandemic have found new niches in the market. The growing popularity of box diets and dietary catering have been used by catering companies to supply offices and-due to the posting or outplacement of many employees to on-line work-to deliver food to the special, “pandemic office” at home. Since the outbreak of the COVID-19 pandemic, remote working has become the norm for millions of workers in the EU and worldwide. Early estimates by Eurofound suggests that close to 40% of people currently working in the EU have started full-time remote working as a result of the pandemic [41]. On the other hand, employees prefer remote work. Even if research results regarding the advantages for employees of remote work are not available today, a survey of 1400 Flexjobs.com users shows that it makes working life more flexible, and in most cases increased personal satisfaction and even improved health. Moreover, 89% of survey responders believed that remote work decrease their levels of stress and 94% thought it would have a positive impact on their personal life [42]. According to the Nationale Nederlanden research and reports entitled “Employee Benefits” and “Family of the Future”, in the time of the pandemic, as much as 43% of people working in Poland perform their professional tasks outside the company’s premises. In this group, one fifth of the survey respondents declare that it is a new mode of work for them, while 14% admit that they have already worked in this way before. Every tenth Poles work in the office only as part of the assigned duty [43,44].

The most visible consumer trend related to remote work is the dynamic growth of online purchases. For example, online food sales in Poland in 2020 increased compared to 2019 by nearly 100% month by month. According to the data presented in the latest Market & Product Research Experts report [5], e-commerce in the food industry will grow at a double-digit rate for the next three years. The development of food sales via the Internet demands of providing an appropriate packaging that should meet the requirements as to functional parameters, compliance with national and EU law and the growing social awareness to avoid plastic littering the environment. Public striving and determination to move away from plastics and the veto of the usage of disposable plastic products in the EU on one hand, and on the other hand, remote work system development and new environmentally friendly models of everyday life of society, forced producers to meet the above-mentioned conditions. However, there are a lot of problems and difficulties which have to be resolved as soon as possible, either in legal terms or technological challenges and associated economic profitability or corresponding to them emerging social environmentally friendly models of life [39,45].

The HoReCa industry around the world draws conclusions from the growing on-line food delivery markets and the double restrictions imposed on disposable food packaging, i.e., the ban on the use of disposable plastic products for packaging, transportation and serving food, and equally important, sanitary and hygienic restrictions caused by the COVID-19 pandemic. Development trends in the HoReCa industry are generated by the most important purchasing group for HoReCa, i.e., residents of large urban centers, including, in particular young people classified in sociology and marketing as the Millennials, generation Y, or the “next generation” as well as “Digital generation”. The representatives of this group are considered to have been born in the period 1983–1999 [46]. Millennials, that is, today’s 20-, 30-, and 40-year-olds, account for more than half of the world’s population in reproductive age, i.e., ca. 1.7 billion people. In Poland, the group of Millennials is estimated at over 11 million consumers who create the mass market and represent a huge business potential [47]. This consumer segment has a decisive impact on the development of the “green economy” and circular economy, as well as pro-ecological market trends. Moreover, it is a group of consumers that has significant purchasing power to increase the sales volume [48]. This group experienced a prolonged, good economic situation, which has been accompanied by the dynamic development of modern technologies and the deepening of globalization, which influenced the emergence of new needs, determining purchasing and consumption choices. This generation differs from its predecessors in terms of, among others, culture, lifestyle, and aspirations. Millennials are distinguished by better education, the ability to easily use digital tools, but also a high sensitivity to environmental issues, including knowledge about the negative impact of disposable plastic products on the planet and on one’s own health.

All over the world, Millennials, regardless of their country of origin, have similar characteristics. This is a group of consumers who freely shop online, paying particular attention to ecological and pro-health products, a convenient offer. They are conscious, well-informed, and active, appreciating the added value of the product. Much more often than older consumer groups, Millennials are willing to pay more for a product they consider iconic, and in buying them, they can support noble, moral aims which are close to them. Millennials appreciate the combination of functional and emotional benefits.

According to surveys conducted in Poland, Germany, the Czech Republic, and Slovakia, on a sample of over 1000 people from this group [49], their preferences and requirements in regard to new food products, methods of serving, packaging, distribution, and transport methods, and the manner of consumption with respect to searching for new products are as follows:

- 1.

- Hedonistic values, new sensations, and experiences in all aspects of life, but in harmony with nature;

- 2.

- Comfort combined with aesthetics;

- 3.

- Pro-environmental values;

- 4.

- Compliance with the experiences and values of the buyer, which are not only environmental issues, but also present a sense of social responsibility for the future of the next generations;

- 5.

- Low complexity, simplicity, reliance on natural resources, obtained locally, without the need to transport for long distances;

- 6.

- Safety in all aspects of the impact of the product on human health;

- 7.

- The possibility to demonstrate the system of values via attributes essential for the image of the buyer, especially environmental friendliness, biodegradability, and compostability of the packaging. These features are relevant for other generations too and they are often subject to verification during purchasing. One of the most important is the conformity of the supplier/producer with the principles of environmental responsibility of business.

In Poland, the following market trends are conducive to the development of technology for the environmentally friendly food packaging production and the development of a circular economy within this industry:

- 1.

- Only one thid of households in Poland declare that they prepare meals at home every day, 19% cook occasionally or very rarely, and 11% are singles. This means that the take-away food market increases and volume of disposable packaging escalates [50];

- 2.

- More and more people order food online, and the popularity of catering is one of the most important trends of the decade [51];

- 3.

- The popularity of the so-called box diet (five meals) and lunch boxes (three meals) is growing [50];

- 4.

- 26% of Millennials are vegetarians and 10% of the world’s population follows some kind of vegetarian-diet. For example, in Poland, the take-away food market for these groups increased in 2019 by 50% compared to 2018 and by 100% in 2020 compared to 2019 [52].

- 5.

- The development of a new business model for the HoReCa industry, considering the growing trend of selling food in disposable packaging via portals such as pizzaportal and UberEATS with contactless payments and deliveries by specialized food-delivery companies like Glovo.

- 6.

- The locality of food products is important for the HoReCa industry and for end-consumers as well. In this sense, questions concerning, e.g., where the food and packing comes from or if the product and technology of production are environmentally friendly are being asked much often.

- 7.

- Functionality and price are the most important.

- 8.

- Novelty and variety: 72% of take-away buyers want to have a new experience, including novelty in food packaging.

4. Discussion

Changes in the approach to food packaging and the accelerated replacement of plastic packaging with bioplastic address the following four environmental problems:

(1) An increasing amount of plastic food packaging made of fossil fuels is a huge burden for the natural environment, especially the oceans.

In 2017, 172.6 kg of packaging waste was generated per capita in the EU-27. This amount ranged from 64.1 kg per inhabitant in Bulgaria to 230.9 kg per inhabitant in Luxembourg [21]. In Poland, the demand for plastics is 3.5 million tons per year. The largest recipient of plastics is the packaging sector, which receives an average of 39.9% of plastic in the EU and 33% in Poland, mainly for the production of reusable shopping bags, foil, and plastic cutlery, drink tubes, and food packaging. However, there are significant differences in the recovery of plastics in European countries. On average in the EU, 32.5% of packaging plastic is recycled, 42.6% is used for energy purposes and 24.9% is landfilled [19]. In Poland, 30–50% of plastic packaging is landfilled, and the recycling rate is ca. 40%. It is worth stressing that it is not known what is happening to over 406,000 tons of plastic every year in Poland [53].

Nowadays, more than 99% of plastics are made of chemicals derived from the fossil oil and gas. The fossil fuel industry and the plastics industry are closely related. About 8–9% of the fossil fuels consumed in the EU are used as a raw material in industrial processes and about a half of this is used in the production of polymers. This means that, in 2018, 223,715 million tons of crude oil were allocated to the production of plastics, including 89.5 million tons for the production of plastic packaging (Source: own calculations based on [54]).

(2) The need to reduce CO2 emissions and protect the climate by consistently implementing the circular economy paradigm.

Plastic refining is one of the most carbon-intensive industries, and emissions related to plastics production are estimated at an average of 1.9 tons of CO2 per ton of product, which in the case of plastics production, 400 million tons of packaging annually, is responsible for 760 million tons of emissions. Half of these emissions are related to energy consumption, while the other half comes from the so-called process emissions resulting from manufacturing technology. So, even if the energy supply for the production of packaging plastic was 100% renewable, this would only reduce CO2 emissions by half. The development of a technology for the production of bioplastics for food packaging and the replacement of fossil fuels with, e.g., food waste in the production processes will avoid the emission of a significant part of greenhouse gases into the atmosphere. Simultaneously, the circular economy will be implemented in the packaging industry and will be developed step by step in the HoReCa sector as well.

(3) The problem of food waste and growing amounts of heterogeneous organic waste, such as, e.g., confectionery and bakery waste, beetroot pulp, or by-products of agricultural production (straw, chaff), can be valorized in a technologically and economically more efficient way using biotechnological processes than with current traditional biogas or composting technologies.

The UNEP Food Waste Index Report 2021 shows that 17% of total global food production is wasted (11% in households, 5% in food service and 2% in retail) [55]. So, there is a significant potential as this kind of wastes can be transformed into a valuable raw material for the production of bioplastics. It also opens room for reduction of the amount of food waste going to landfills or to be incinerated inefficiently, in line with the circular economy paradigm.

(5) The necessity of economical, pro-environmental management of food products, taking into account sanitary regimes and safeguards against the spread of coronavirus.

The restrictions and lockdowns related to the pandemic COVID-19 will end, sooner or later, and the containment and restriction measures will be gradually lifted and finally removed. However, the world economy after COVID-19 will no longer be the same. The overall supply and demand for HoReCa will not recover from the crisis unscathed. For example, the sector’s turnover is permanently reduced, because the industry’s profitability is significantly impacted by its openness to direct contact with the consumer. The HoReCa sector’s costs caused by sanitary regulations, long-term full lockdowns, and months of maintaining social distance in restaurants or bars impact on the loss of income. There are many new challenges for the recovery and development of the industry. The pandemic crises and the completely new economic situation could create a positive impact on the in HoReCa sector. The best perspectives for the take-away food delivery and food portal development can be observed. These sectors are some of the few in the world economy, apart from the industries directly related to health care and antivirus protection, which, in response to the requirements of the pandemic period, significantly improved the quality and technology of the services provided.

5. Conclusions

Increased take-away food deliveries during the COVID-19 period are at the same time linked to tighter food packaging requirements. Food packaging should be functional, i.e., effectively protect food, first of all against infection or spreading the virus, but also to maintain resistance against the loss of nutritional and aesthetic values. The material for food packaging should therefore at least have the characteristics of plastic, but without any negative environmental impact. Currently, the food packaging material substitutable for petroleum-based plastic is bioplastics, a material with the features of plastic, but biodegradable and biocompostable, produced on the basis of a lactic acid polymer (PLA).

Technologies to produce bioplastics on an industrial scale are mainly based on the 1st generation sugars obtained from corn, wheat, or sugar beet, based on large-scale corn or sugar beet plantations. This approach is questionable for two reasons:

- 1.

- World agriculture, especially agriculture in the EU, has no freely available land for production other than food or feed, especially in the face of increasing negative climate change, water shortage, and progressing urbanization [56].

- 2.

- In line with the EU agricultural policy, corn and sugar beet products should be used as food or feed only [57].

Therefore, the challenge for the scientific community is to answer the question about how to effectively produce bioplastics without draining food resources. The answer is the circular economy paradigm and the use of food waste as an effective raw material to produce food packaging material. The material sought should meet the new requirements that have been revealed during the last months of the coronavirus pandemic. The technology for producing bioplastics using food waste can be a significant stimulus for transformations in the production of petroleum-derived plastics, accelerating the shift of the plastics industry from a wasteful linear economy to a circular economy [58,59]. The importance of changes as we can observe in the food packaging sector is a positive prognosis for the entire industry. The effect of the transition of packaging industry from mass, disposable, environmentally harmful production towards bioplastic packaging production may have a fundamental technological and economic impact. The impact of such a transition can be socially noticeable because a new circular post-COVID and pro-environmental era has just begun.

Author Contributions

Conceptualization, E.K., R.M.Ł. and M.D.; methodology, E.K., R.M.Ł. and M.D.; formal analysis, E.K. and R.M.Ł.; investigation E.K. and R.M.Ł.; resources, E.K., R.M.Ł. and M.D.; data curation, E.K., R.M.Ł. and M.D.; writing—original draft preparation, E.K., R.M.Ł. and M.D.; writing—review and editing, E.K. and R.M.Ł.; visualization, E.K. and R.M.Ł.; supervision, E.K., R.M.Ł. and M.D.; project administration, E.K. and M.D.; funding acquisition, E.K. and M.D. All authors have read and agreed to the published version of the manuscript.

Funding

This research was funded by the National Science Centre, Poland. Program OPUS, grant No. 2018/31/B/HS4/00485.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

The datasets used and analysed during the current study are available from the corresponding author on reasonable request.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Statista. Coronavirus: Impact on the Global Economy. 2021. Available online: https://www.statista.com/study/71343/economic-impact-of-the-coronavirus-covid-19-pandemic/ (accessed on 3 June 2021).

- IMAS. International, KoronaBilans MŚP. 2020. Available online: https://www.imas.pl/ (accessed on 5 June 2021).

- Blériot, J. The Covid-19 Recovery Requires a Resilient Circular Economy, European Circular Economy Stakeholder Platform. 2021. Available online: https://medium.com/circulatenews/the-covid-19-recovery-requires-a-resilient-circular-economy-e385a3690037 (accessed on 8 June 2021).

- Singh, S. The Soon to Be $200B Online Food Delivery Is Rapidly Changing the Global Food Industry. Available online: https://www.forbes.com/sites/sarwantsingh/2019/09/09/the-soon-to-be-200b-online-food-delivery-is-rapidly-changing-the-global-food-industry/ (accessed on 23 May 2021).

- Market Experts. Koronawirus a zmiana zachowań konsumentów w Polsce 2020. Scenariusze i prognozy rozwoju na lata 2020–2021 (Coronavirus and Change in Consumer Behaviour in Poland 2020. Scenarios and Development Forecasts for 2020–2021); Market &Product Research (PMR): Cracow, Poland, 2021. (In Polish) [Google Scholar]

- Gonçalves, M. Disparam as reservas nos restaurantes para o fim-de-semana. 2021. Available online: https://www.publico.pt/2021/04/30/fugas/noticia/disparam-reservas-restaurantes-fimdesemana-1960682 (accessed on 3 June 2021). (In Portuguese).

- Research&Markets. Online Food Delivery Services Global Market Report 2020-30: COVID-19 Growth and Change; The Business Research Company: Hyderabad, India, 2020. [Google Scholar]

- Market Watch. Online Food Delivery Services Market 2021 CAGR Value, Share, Trends, Industry Size, Top Key Players, Type and Application and Forecast to 2026. Available online: https://www.marketwatch.com/press-release/cyclopentanone-market-size-2021-cagr-status-analysis-growth-opportunities-industry-share-top-manufacturers-future-trends-with-covid-19-impact-till-2026-2021-05-06 (accessed on 13 June 2021).

- Statista. On-line Food Delivery Worldwide. 2021. Available online: https://www.statista.com/outlook/dmo/eservices/online-food-delivery/worldwide?currency=eur (accessed on 13 June 2021).

- Stava. Raport o rynku dowozów jedzenia. 2020. Available online: https://app.hubspot.com/documents/7739611/view/122857523?accessId=6330df (accessed on 11 June 2021). (In Polish).

- Cision US Inc. Online On-Demand Food Delivery Services Market by Business Model and Geography—Forecast and Analysis 2020–2024. 2021. Available online: https://www.technavio.com/report/online-on-demand-food-delivery-services-market-size-industry-analysis (accessed on 3 June 2021).

- European Parliament; The Council of the European Union. Directive (EU) 2019/904 of 5 June 2019 on the Reduction of the Impact of Certain Plastic Products on the Environment; European Parliament; The Council of the European Union: Brussels, Belgium, 2019. [Google Scholar]

- The United Nations Environment Programme (UNEP). Global Commitment to the New Plastics Economy. 2020. Available online: https://www.unep.org/ar/node/29048 (accessed on 13 June 2021).

- Ellen MacArthur Foundation. The Circular Economy Solution to Plastic Pollution. 2020. Available online: https://www.ellenmacarthurfoundation.org/assets/downloads/The_circular_economy_solution_to_plastic_pollution_July_2020.pdf (accessed on 1 June 2021).

- Harvard University. 14 Million Tons of Microplastic Are on the Ocean Floor. 2020. Available online: https://sitn.hms.harvard.edu/flash/2020/14-million-tons-of-microplastic-are-on-the-ocean-floor/ (accessed on 19 May 2021).

- Perspective on “Breaking the Plastic Wave” Study. The Circular Economy Solution to Plastic Pollution. 2021. Available online: https://www.ellenmacarthurfoundation.org/news/new-study-confirms-need-for-urgent-transition-to-a-circular-economy-for-plastic (accessed on 2 June 2021).

- One Planet. Breaking the Plastic Wave—A Comprehensive Assessment of Pathways Towards Stopping Ocean Plastic Pollution. 2020. Available online: https://www.oneplanetnetwork.org/breaking-plastic-wave-comprehensive-assessment-pathways-towards-stopping-ocean-plastic-pollution (accessed on 28 May 2021).

- Statista. Production of Plastics Worldwide from 1950 to 2019. 2021. Available online: https://www.statista.com/statistics/282732/global-production-of-plastics-since-1950/ (accessed on 30 May 2021).

- PlasticsEurope. Plastics—The Facts. 2020. Available online: https://www.plasticseurope.org/application/files/9715/7129/9584/FINAL_web_version_Plastics_the_facts2019_14102019.pdf (accessed on 17 May 2021).

- Kozera-Szałkowska, A. Rynek tworzyw sztucznych—Produkcja, zapotrzebowanie, zagospodarowanie odpadów. Plast. Mark. Prod. Demand Waste Manag. Polim. 2019, 64, 751–758. (In Polish) [Google Scholar] [CrossRef]

- EuroStat. Packaging Waste Statistics. 2020. Available online: https://ec.europa.eu/eurostat/statistics-explained/index.php?title=Packaging_waste_statistics (accessed on 21 May 2021).

- Mowlds, S. The EU’s farm to fork strategy: Missing links for transformation. Acta Innov. 2020, 36, 17–30. [Google Scholar] [CrossRef]

- Bednarczyk, M.; Borkowski, K. Środowiskowe aspekty projektowania opakowań. Krajowa Izba Gospodarcza Warszawa 2020 (Environmental Aspects of Packaging Design); The Polish Chamber of Commerce: Warsaw, Poland; pp. 61–62. (In Polish)

- Ncube, L.K.; Ude, L.K.; Ogunmuyiwa, E.N.; Zulkifli, Z.; Beas, I.N. Environmental Impact of Food Packaging Materials: A Review of Contemporary Development from Conventional Plastics to Polylactic Acid Based Materials. Materials 2020, 13, 4994. [Google Scholar] [CrossRef]

- Polska Izba Opakowań. Rynek opakowań biodegradowalnych w latach 2019, 2020 i 2025, 25 (Polish Chamber of Packaging, Biodegradable Packaging Market in 2019, 2020 and 2025). Available online: http://www.pakowanie.info/uploads/1/0/2/5/10250887/newsletter_2019-7.pdf (accessed on 23 May 2021). (In Polish).

- Bhargava, N.; Sharanagat, V.S.; Mor, R.S.; Kumar, K. Active and intelligent biodegradable packaging films using food and food waste-derived bioactive compounds: A review. Trends Food Sci. Technol. 2020, 105, 385–401. [Google Scholar] [CrossRef]

- Allied Market Research. Bioplastic Market Outlook—2027. 2020. Available online: https://www.alliedmarketresearch.com/bioplastics-market (accessed on 13 June 2021).

- Jõgi, K.; Bhat, R. Valorization of food processing wastes and by-products for bioplastic production. Sustain. Chem. Pharm. 2020, 18, 100326. [Google Scholar] [CrossRef]

- Allied Market Research. Market Research Report, Polylactic Acid (PLA) Market in Packaging, Textile, Agriculture, Transportation, Bio-Medical, Electronics and Others, 2012–2020. 2020. Available online: https://renewable-carbon.eu/news/polylactic-acid-pla-market-in-packaging-textile-agriculture-transportation-bio-medical-electronics-and-others/ (accessed on 13 June 2021).

- Wu, F.; Misra, M.; Mohanty, A.K. Challenges and new opportunities on barrier performance of biodegradable polymers for sustainable packaging. Prog. Polym. Sci. 2021, 117, 101395. [Google Scholar] [CrossRef]

- European Commission. Directive 2009/28/EC of the European Parliament and of the Council of 23 April 2009 on the Promotion of the Use of Energy from Renewable Sources and Amending and Subsequently Repealing Directives 2001/77/EC and 2003/30/EC; European Commission: Brussels, Belgium, 2009. [Google Scholar]

- EC. Directive (EU) 2015/1513 of the European Parliament and of the Council of 9 September 2015 Amending Directive 98/70/EC Relating to the Quality of Petrol and Diesel Fuels and Amending Directive 2009/28/EC on the Promotion of the Use of Energy from Renewable Sources; European Commission: Brussels, Belgium, 2015. [Google Scholar]

- Directive (EU) 2018/2001 Directive (EU) 2018/2001 of the European Parliament and of the Council of 11 December 2018 on the Promotion of the Use of Energy from Renewable Sources. PE/48/2018/REV/1 2018. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A32018L2001 (accessed on 25 June 2021).

- RESources from URban BIo-waSte. 2020. Available online: https://www.resurbis.eu (accessed on 18 May 2021).

- Kochanska, E.; Lukasik, R. Opracowanie roślinnych opakowań do żywności wytwarzanych w kaskadowych procesach biorafineryjnych, Centrum Badań i Innowacji Pro-Akademia (Development of Vegetable Food Packaging Produced in Cascade Biorefinery Processes); Research and Innovation Center Pro-Akademia: Konstantynow Lodzki, Poland, 2020. (In Polish) [Google Scholar]

- Jungowska, J.; Kulczyński, B.; Sidor, A.; Gramza-Michałowska, A. Assessment of Factors Affecting the Amount of Food Waste in Households Run by Polish Women Aware of Well-Being. Sustainability 2021, 13, 976. [Google Scholar] [CrossRef]

- Skotnicka, M.; Karwowska, K.; Kłobukowski, F.; Wasilewska, E.; Małgorzewicz, S. Dietary Habits before and during the COVID-19 Epidemic in Selected European Countries. Nutrients 2021, 13, 1690. [Google Scholar] [CrossRef]

- Malak-Rawlikowska, A.; Majewski, E.; Wąs, A.; Borgen, S.O.; Csillag, P.; Donati, M.; Freeman, R.; Hoàng, V.; Lecoeur, J.-L.; Mancini, M.C.; et al. Measuring the Economic, Environmental, and Social Sustainability of Short Food Supply Chains. Sustainability 2019, 11, 4004. [Google Scholar] [CrossRef] [Green Version]

- PosBistro. Badania Gastronomii w Polsce w Trakcie Pandemii (Reseach of Gastronomy Sector during the Pandemic). 2020. Available online: https://posbistro.com/blog/pl/pandemia-zwiekszyla-zapotrzebowanie-na-dowozy-jedzenia-ktore-trwa-do-teraz/ (accessed on 21 May 2021). (In Polish).

- Eurostat. Waste Generation by Packaging Material. 2020. Available online: https://ec.europa.eu/eurostat/statistics-explained/index.php?title=Packaging_waste_statistics#Waste_generation_by_packaging_material (accessed on 27 May 2021).

- Ahrendt, D.; Cabrita, J.; Clerici, E.; Hurley, J.; Leončikas, T.; Mascherini, M.; Riso, S.; Sándor, E. Living, Working and COVID-19; Publications Office of the European Union: Luxembourg, 2020. [Google Scholar]

- Bulińska-Stangrecka, H.; Bagieńska, A. The Role of Employee Relations in Shaping Job Satisfaction as an Element Promoting Positive Mental Health at Work in the Era of COVID-19. Int. J. Environ. Res. Public Health 2021, 18, 1903. [Google Scholar] [CrossRef]

- Vishnubhotla, S.D.; Mendes, E.; Lundberg, L. Investigating the relationship between personalities and agile team climate of software professionals in a telecom company. Inf. Softw. Technol. 2020, 126, 106335. [Google Scholar] [CrossRef]

- Rovelli, P.; Ferasso, M.; De Massis, A.; Kraus, S. Thirty years of research in family business journals: Status quo and future directions. J. Fam. Bus. Strategy 2021, 100422, in press. [Google Scholar] [CrossRef]

- Conesa, J.A.; Nuñez, S.S.; Ortuño, N.; Moltó, J. PAH and POP Presence in Plastic Waste and Recyclates: State of the Art. Energies 2021, 14, 3451. [Google Scholar] [CrossRef]

- Zhang, K.; Zhao, D.; Feng, L.; Cao, L. Cycling Trajectory-Based Navigation Independent of Road Network Data Support. ISPRS Int. J. Geo-Inf. 2021, 10, 398. [Google Scholar] [CrossRef]

- Calín-Sánchez, Á.; Carbonell-Barrachina, Á.A. Flavor and Aroma Analysis as a Tool for Quality Control of Foods. Foods 2021, 10, 224. [Google Scholar] [CrossRef] [PubMed]

- Chalyi, I.; Levykin, S.; Guryev, I. Model and technology for prioritizing the implementation end-to-end business processes components of the green economy. Acta Innov. 2020, 35, 65–80. [Google Scholar] [CrossRef]

- Skawińska, E.; Barska, A. Konsumenci pokolenia Milenium na rynku innowacyjnych produktów żywnościowych na obszarach przygranicznych Polski, Niemiec, Czech i Słowacji (Millennium generation consumers in the market of innovative food products in the border areas of Poland, Germany, the Czech Republic and Slovakia, Zagadnienia Ekon). Rolnej. Probl. Agric. Econ. 2020, 364, 204–209. (In Polish) [Google Scholar]

- Wierzbiński, B.; Surmacz, T.; Kuźniar, W.; Witek, L. The Role of the Ecological Awareness and the Influence on Food Preferences in Shaping Pro-Ecological Behavior of Young Consumers. Agriculture 2021, 11, 345. [Google Scholar] [CrossRef]

- Wondirad, A.; Kebete, Y.; Li, Y. Culinary tourism as a driver of regional economic development and socio-cultural revitalization: Evidence from Amhara National Regional State, Ethiopia. J. Destin. Mark. Manag. 2021, 19, 100482. [Google Scholar] [CrossRef]

- Jacimovic, D. 20 Remarkable Vegetarian Statistics. 2021. Available online: https://dealsonhealth.net/vegetarian-statistics/ (accessed on 29 May 2021).

- Statistics Poland. Gospodarka Materiałowa w 2019, Materials Management in 2019; Główny Urząd Statystyczny (Statistics Poland): Warszawa, Poland, 2021. (In Polish) [Google Scholar]

- Statistical Review of World Energy, 69th ed.; Hydrocarbon Engineering, 2020; Available online: https://www.hydrocarbonengineering.com/special-reports/17062020/bp-releases-its-statistical-review-of-world-energy-2020/ (accessed on 27 June 2021).

- UNEP. Food Waste Index Report. 2021. Available online: https://www.unep.org/resources/report/unep-food-waste-index-report-2021 (accessed on 7 June 2021).

- Szarek-Iwaniuk, P.A. Comparative Analysis of Spatial Data and Land Use/Land Cover Classification in Urbanized Areas and Areas Subjected to Anthropogenic Pressure for the Example of Poland. Sustainability 2021, 13, 3070. [Google Scholar] [CrossRef]

- Ben Allen, J.W.; Bas-Defossez, F. Feeding Europe: Agriculture and Sustainable Food Systems. 2018. Available online: https://ieep.eu/uploads/articles/attachments/64e06bc1-6c2e-4b94-bc93-9150725093ac/Think%202030%20Feeding%20Europe.pdf?v=63710011359 (accessed on 12 June 2021).

- Morone, P.; Yilan, G.A. paradigm shift in sustainability: From lines to circles. Acta Innov. 2020, 36, 5–16. [Google Scholar] [CrossRef]

- Distaso, M. Potential contribution of nanotechnolgy to the circular economy of plastic materials. Acta Innov. 2020, 37, 57–66. [Google Scholar] [CrossRef]

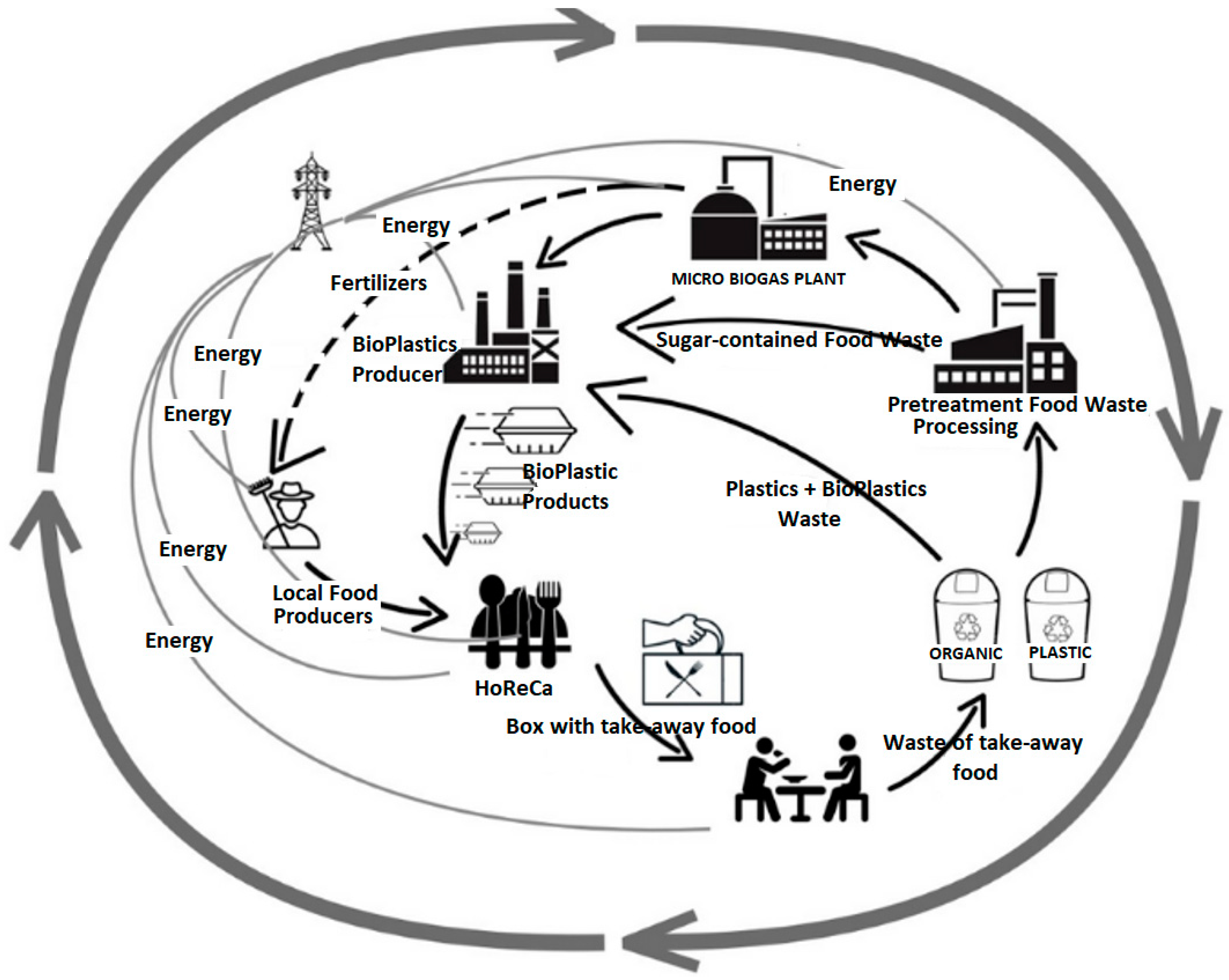

Figure 1.

Circularity in the life cycle of take-away food packaging. Source: Authors’.

Figure 2.

Factors of impact on development of take-away food packaging in COVID-19 period. Source: Authors’.

Figure 2.

Factors of impact on development of take-away food packaging in COVID-19 period. Source: Authors’.

Figure 3.

The microplastic system map depicts the five major components of the global plastic system: production and consumption; collection and sorting; recycling; disposal; and mismanaged. The boxes labelled with letters (A to W) represent mass aggregation points in the model, and the arrows represent mass flows. Boxes outlined in solid lines represent places where plastic mass leaves the system, including where it leaks into the ocean (see Box W). The boxes to the left of Box A reflect plastic demand. Copyright © 2020 The Pew Charitable Trusts licensed under a Creative Commons License Attribution-Noncommercial 4.0 International (CCBY-NC 4.0) [17].

Figure 3.

The microplastic system map depicts the five major components of the global plastic system: production and consumption; collection and sorting; recycling; disposal; and mismanaged. The boxes labelled with letters (A to W) represent mass aggregation points in the model, and the arrows represent mass flows. Boxes outlined in solid lines represent places where plastic mass leaves the system, including where it leaks into the ocean (see Box W). The boxes to the left of Box A reflect plastic demand. Copyright © 2020 The Pew Charitable Trusts licensed under a Creative Commons License Attribution-Noncommercial 4.0 International (CCBY-NC 4.0) [17].

Figure 4.

Production volume of plastics worldwide from 1950 to 2019 [18].

Figure 4.

Production volume of plastics worldwide from 1950 to 2019 [18].

Figure 5.

Plastics demand by segment 2019 in EU [19].

Figure 5.

Plastics demand by segment 2019 in EU [19].

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Kochańska, E.; Łukasik, R.M.; Dzikuć, M. New Circular Challenges in the Development of Take-Away Food Packaging in the COVID-19 Period. Energies 2021, 14, 4705. https://doi.org/10.3390/en14154705

AMA Style

Kochańska E, Łukasik RM, Dzikuć M. New Circular Challenges in the Development of Take-Away Food Packaging in the COVID-19 Period. Energies. 2021; 14(15):4705. https://doi.org/10.3390/en14154705

Chicago/Turabian StyleKochańska, Ewa, Rafał M. Łukasik, and Maciej Dzikuć. 2021. "New Circular Challenges in the Development of Take-Away Food Packaging in the COVID-19 Period" Energies 14, no. 15: 4705. https://doi.org/10.3390/en14154705

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.