The Impact of the Measure Used to Calculate the Distance between Exchange Rate Time Series on the Topological Structure of the Currency Network

, , and

, , and

Abstract

:1. Introduction

- −

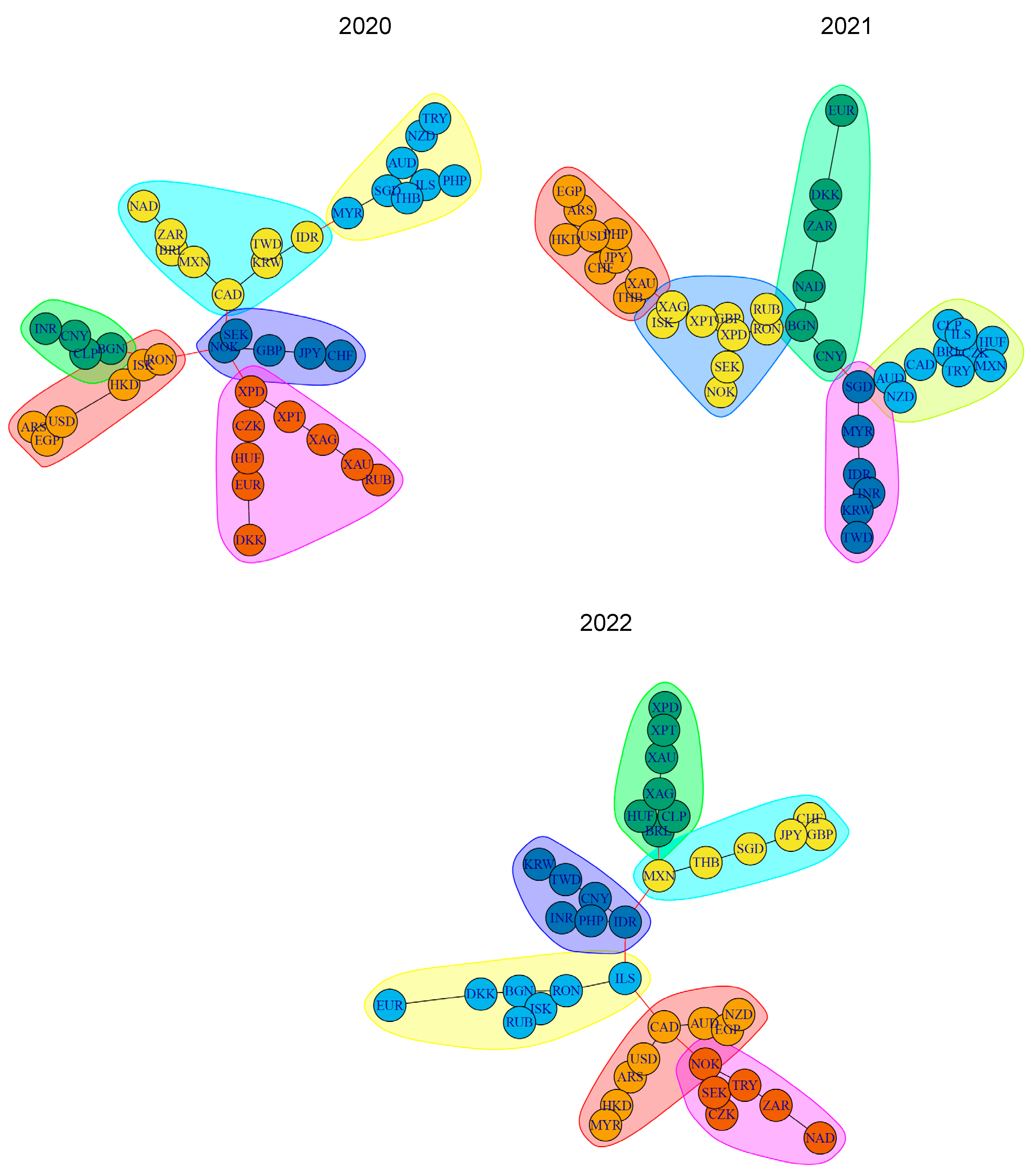

- in the year of the COVID-19 pandemic outbreak (from 1 January to 31 December 2020);

- −

- in the next year of the pandemic (from 1 January to 31 December 2021);

- −

- in the year of Russia’s invasion of Ukraine (from 1 January to 31 December 2022).

- What is the impact of the distance measure used on the topological structure of the currency network?

- Are different measures equally sensitive to the choice of numeraire currency?

- Does the topological structure of the currency network during the periods of the pandemic crisis and the crisis caused by Russia’s invasion of Ukraine differ from the structure of the network in the period in between?

2. Literature Review

3. Description of Data

4. Description of the Research Method

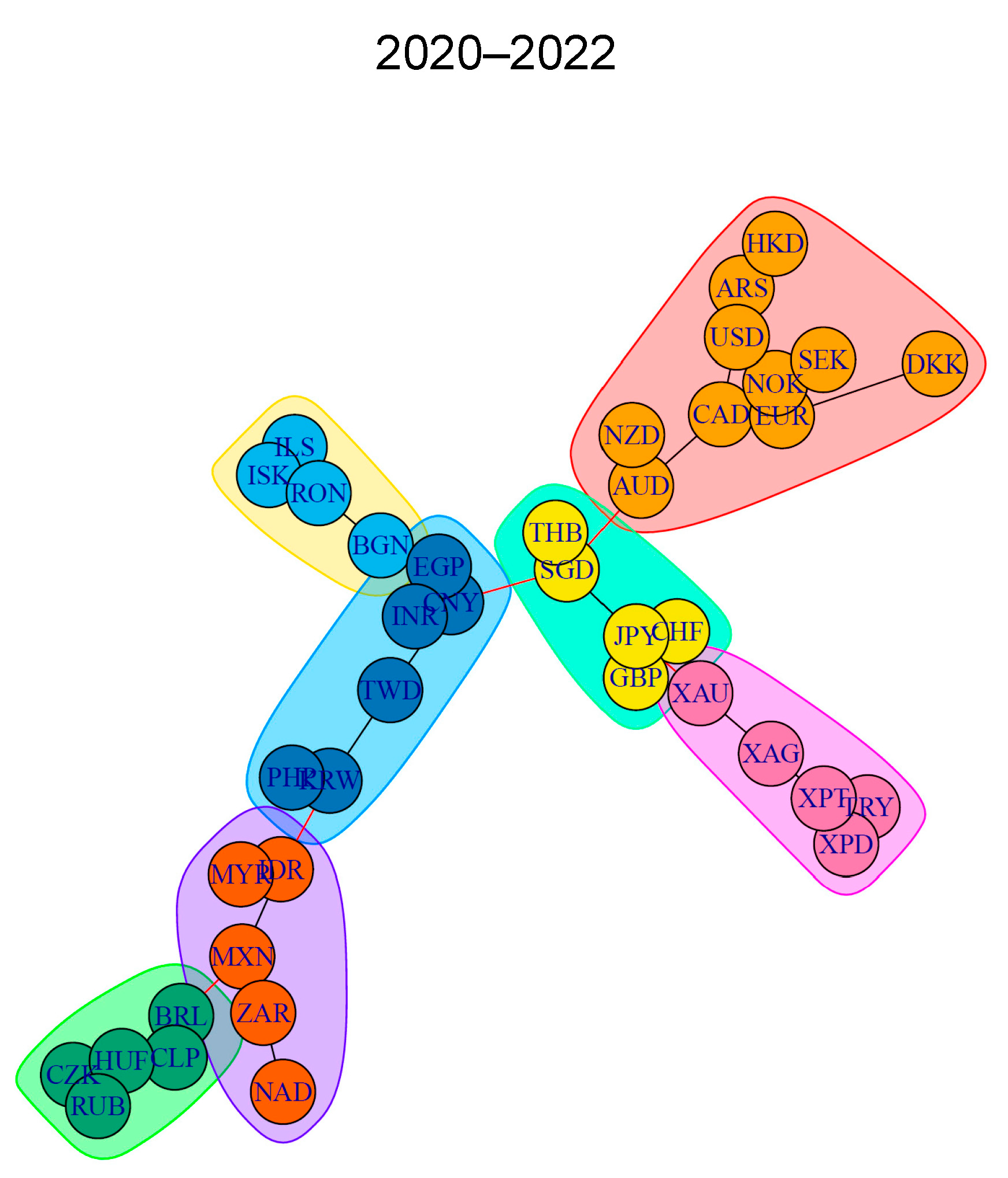

4.1. Minimum Spanning Trees

4.2. Determining the Distance between Currency Nodes

- Euclidean distance :

- Distance based on Pearson’s correlation coefficient :where and are the average values of the series examined.

- Distance based on Spearman’s correlation coefficient (rank-based correlation coefficient):where is the difference in the ranks given to the two variables values.

- Distance based on Kendall’s correlation coefficient , which measures the correspondence between the rankings of two variables:where —number of concordant pairs, —number of discordant pairs. A pair is concordant if the observation that ranks higher for variable is also higher for variable . A pair is discordant if the observation that ranks higher for is lower for .

- Distance based on the partial correlation coefficient , which measures the degree of association between variables, with the influence of a set of controlling variables removed:where —partial correlation between Xi and Xj given all others, are the elements of the precision matrix defined as (the inverse of the joint covariance matrix).

- DTW distance , which is suitable when comparing series with similar structures but shifted in time [52,53,54]. The DTW algorithm finds the smallest distance between two time series, allowing their time transformation. A local cost function , is defined, and the optimal series matching involves finding a sequence of points (path) that minimizes the total cost C. A matching path w (warping path) is sought that runs through low-cost areas and avoids high costs [55,56]. The optimal warping path w* has minimum matching cost, and the distance between and is then given bywhere is the set of all possible warping paths.

- Kullback–Leibler divergence (also named relative entropy) , which is a metric that quantifies the difference between two probability distributions [57]. For two continuous distributions P and Q,where and denote the probability densities of and . The nonparametric estimators for and were obtained in this work through kernel density estimation aswhere is a symmetric, positive kernel function that integrates to one, and is the bandwidth. We used a common biweight (quadratic) kernel function, the bandwidth vector was computed by Scott’s rule of thumb, and the output was calculated over a grid of 400 points from to .

4.3. Topological Characteristics of Networks

- −

- average path length (mean distance)—the mean of the lengths of the shortest paths , between all pairs of vertices in the network (Wang et al., 2014) [29]

- −

- diameter—length of the longest shortest path between any pair of nodes

- −

- degree centrality—indicator relating to the number of links of nodes (it measures the risk of nodes capturing all that flows through the network). The formula for degree centrality is

- −

- closeness centrality—measure based on the average shortest path from that node to all other nodes in the network. It is defined aswhere is the shortest path length between node and . Closeness centrality ranges between 0 and 1; the higher value indicates that the node is closer to all other nodes in the network on average.

- −

- eigenvector centrality—measure of influence of a node in the network. The centrality score of a node is proportional to the sum of the centrality scores of its neighbors, with each neighbor’s score weighted by its own centrality. This means that many connections of a node are important, but also if these connections come from other important nodes. The formula for eigenvector centrality iswhere λ is the dominant eigenvalue of the adjacency matrix , is the element of the adjacency matrix, indicating whether there is a connection between nodes and , is the centrality score of a node , and is the number of nodes in the network.

- −

- assortativity—the tendency of vertices to connect or ‘attach’ to vertices with similar properties in a graph [61]. This is a measure of homophily in a graph, which is based on some vertex labeling or values assigned to vertices (if the coefficient is high, then the connected vertices tend to have the same labels). The assortativity coefficient of a graph ranges between −1 and 1; values close to 1 indicate a very high likelihood of two vertices with the same property being connected; values close to −1 indicate a very low likelihood of two vertices with the same property being connected. Negative assortativity indicates the structure of the star network, positive—the connections of high degree nodes to high degree nodes. Assortativity describes how the vertices are connected to each other and informs on network resilience to the spread of crises.

- −

- betweenness—shows how many times a node plays the role of a bridge on the shortest path between two other nodes; it points out the most critical vertices of the network.

5. Results of the Study

6. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Górski, A.Z.; Drożdż, S.; Kwapień, J.; Oświęcimka, P. Minimal Spanning Tree graphs and power like scaling in FOREX networks. Acta Phys. Pol. A 2008, 114, 531–538. [Google Scholar] [CrossRef]

- Basnarkov, L.; Stojkoski, V.; Utkovski, Z.; Kocarev, L. Correlation Patterns in Foreign Exchange Markets. Phys. A Stat. Mech. Its Appl. 2019, 525, 1026–1037. [Google Scholar] [CrossRef]

- Boccara, N. Modeling Complex Systems; Springer: New York, NY, USA, 2003. [Google Scholar]

- Albert, R.; Barabási, A.L. Statistical mechanics of complex networks. Rev. Mod. Phys. 2002, 74, 47–97. [Google Scholar] [CrossRef]

- Newman, M.E.J. Networks: An Introduction; Oxford University Press: Oxford, UK, 2010. [Google Scholar]

- Erdős, P.; Rényi, A. On Random Graphs. Publ. Math. 1959, 6, 290–297. [Google Scholar] [CrossRef]

- Watts, D.; Strogatz, S. Collective dynamics of ‘small-world’ networks. Nature 1998, 393, 440–442. [Google Scholar] [CrossRef]

- Barabasi, A.-L.; Albert, R. Emergence of scaling in random networks. Science 1999, 286, 509–512. [Google Scholar] [CrossRef]

- Milgram, S. The Small World Problem. Psychol. Today 1967, 1, 61–67. [Google Scholar]

- Albert, R.; Jeong, H.; Barabási, A.-L. Error and attack tolerance of complex networks. Nature 2000, 406, 378–382. [Google Scholar] [CrossRef]

- Cohen, R.; Erez, K.; ben-Avraham, D.; Havlin, S. Resilience of the Internet to Random Breakdowns. Phys. Rev. Lett. 2000, 85, 4626–4628. [Google Scholar] [CrossRef]

- Liu, Z.; Lai, Y.-C.; Ye, N. Propagation and immunization of infection on general networks with both homogeneous and heterogeneous components. Phys. Rev. E—Stat. Phys. Plasmas Fluids Relat. Interdiscip. Top. 2003, 67, 031911. [Google Scholar] [CrossRef]

- Fortunato, S. Community detection in graphs. Phys. Rep. 2010, 486, 75–174. [Google Scholar] [CrossRef]

- Porter, M.A.; Onnela, J.-P.; Mucha, P.J. Communities in Networks. Not. Am. Math. Soc. 2009, 56, 1082–1097,1164–1166. [Google Scholar]

- Fenn, D. Network Communities and the Foreign Exchange Market; University of Oxford: Oxford, UK, 2010. [Google Scholar]

- Kruskal, J.B. On the shortest spanning subtree of a graph and the traveling salesman problem. Proc. Am. Math. Soc. 1956, 7, 48–50. [Google Scholar] [CrossRef]

- Palla, G.; Barabási, A.; Vicsek, T. Quantifying social group evolution. Nature 2007, 446, 664–667. [Google Scholar] [CrossRef] [PubMed]

- Mantegna, R. Hierarchical structure in financial markets. Eur. Phys. J. B–Condens. Matter Complex Syst. 1999, 11, 193–197. [Google Scholar] [CrossRef]

- Mantegna, R.N.; Stanley, H.E. Introduction to Econophysics: Correlations and Complexity in Finance; Cambridge University Press: Cambridge, UK, 1999. [Google Scholar]

- Onnela, J.-P.; Chakraborti, A.; Kaski, K.; Kertész, J.; Kanto, A. Dynamics of market correlations: Taxonomy and portfolio analysis. Phys. Rev. E 2003, 68, 056110. [Google Scholar] [CrossRef]

- McDonald, M.; Suleman, O.; Williams, S.; Howison, S.; Johnson, N. Detecting a Currency’s Dominance or Dependence using Foreign Exchange Network Trees. Phys. Rev. E 2005, 72, 046106. [Google Scholar] [CrossRef]

- Ortega, G.J.; Matesanz, D. Cross-country hierarchical structure and currency crises. Int. J. Mod. Phys. C 2006, 17, 333–341. [Google Scholar] [CrossRef]

- Naylor, M.J.; Rose, L.C.; Moyle, B.J. Topology of foreign exchange markets using hierarchical structure methods. Phys. A Stat. Mech. Its Appl. 2007, 382, 199–208. [Google Scholar] [CrossRef]

- Kwapień, J.; Gworek, S.; Drożdż, S. Structure and evolution of the foreign exchange networks. Acta Phys. Pol. B 2009, 40, 175–194. [Google Scholar]

- Jang, W.; Lee, J.; Chang, W. Currency crises and the evolution of foreign exchange market: Evidence from minimum spanning tree. Phys. A Stat. Mech. Its Appl. 2011, 390, 707–718. [Google Scholar] [CrossRef]

- Feng, X.; Wang, X. Evolutionary topology of a currency network in Asia. Int. J. Mod. Phys. C 2010, 21, 471–480. [Google Scholar] [CrossRef]

- Wang, G.J.; Xie, C.; Chen, Y.-J.; Chen, S. Statistical properties of the foreign exchange network at different time scales: Evidence from detrended cross-correlation coefficient and minimum spanning tree. Entropy 2013, 15, 1643–1662. [Google Scholar] [CrossRef]

- Wang, G.J.; Xie, C.; Han, F.; Sun, B. Similarity measure and topology evolution of foreign exchange markets using dynamic time warping method: Evidence from minimal spanning tree. Phys. A Stat. Mech. Its Appl. 2012, 391, 4136–4146. [Google Scholar] [CrossRef]

- Wang, G.J.; Xie, C.; Zhang, P.; Han, F.; Chen, S. Dynamics of Foreign Exchange Networks: A Time-Varying Copula Approach. Discret. Dyn. Nat. Soc. 2014, 170921, 1–11. [Google Scholar] [CrossRef]

- Kazemilari, M.; Mohamadi, A. Topological Network Analysis Based on Dissimilarity Measure of Multivariate Time Series Evolution in the Subprime Crisis. Int. J. Financ. Stud. 2018, 6, 47. [Google Scholar] [CrossRef]

- Rešovský, M.; Horváth, D.; Gazda, V.; Siničáková, M. Minimum Spanning Tree Application in the Currency Market. Biatec 2013, 21, 21–23. [Google Scholar]

- Limas, E. An application of minimal spanning trees and hierarchical trees to the study of Latin American exchange rates. J. Dyn. Games 2019, 6, 131–148. [Google Scholar] [CrossRef]

- Cao, H.; Guo, Z.; Li, Y.; Ran, Z. The Relationship Structure of Global Exchange Rate Based on Network Analysis. J. Math. Financ. 2020, 10, 58–76. [Google Scholar] [CrossRef]

- Miśkiewicz, J. Network Analysis of Cross-Correlations on Forex Market during Crises. Globalisation on Forex Market. Entropy 2021, 23, 352. [Google Scholar] [CrossRef]

- Iyke, B.N. The disease outbreak channel of exchange rate return predictability: Evidence from COVID-19. Emerg. Mark. Financ. Trade 2020, 56, 2277–2297. [Google Scholar] [CrossRef]

- Narayan, P.K. Has COVID-19 changed exchange rate resistance to shocks? Asian Econ. Lett. 2020, 1, 1–4. [Google Scholar] [CrossRef]

- Narayan, P.K.; Devpura, N.; Wang, H. Japanese currency and stock market-What happened during the COVID-19 pandemic? Econ. Anal. Policy 2020, 68, 191–198. [Google Scholar] [CrossRef] [PubMed]

- Gupta, K.; Chatterjee, N. Examining Lead-Lag Relationships In-Depth, with Focus on FX Market as COVID-19 Crises Unfolds. arXiv 2020, arXiv:2004.10560. [Google Scholar]

- Hossain, A.T.; Masum, A.-A.; Saadi, S. The impact of geopolitical risks on foreign exchange markets: Evidence from the Russia–Ukraine war. Financ. Res. Lett. 2024, 59, 104750. [Google Scholar] [CrossRef]

- Aliu, F.; Kučera, J.; Horák, J. Exchange rate instabilities during the Russia-Ukraine war: Evidence from V4 countries. Heliyon 2024, 10, e25476. [Google Scholar] [CrossRef] [PubMed]

- Zaheer, K.; Aslam, F.; Mohmand, Y.T.; Ferreira, P. On the Dynamic Changes in the Global Stock Markets’ Network during the Russia–Ukraine War. Economies 2024, 12, 41. [Google Scholar] [CrossRef]

- Marti, G.; Nielsen, F.; Bińkowski, M.; Donnat, P. A Review of Two Decades of Correlations, Hierarchies, Networks and Clustering in Financial Markets. In Progress in Information Geometry. Signals and Communication Technology; Nielsen, F., Ed.; Springer: Cham, Switzerland, 2021. [Google Scholar]

- Mizuno, T.; Takayasu, H.; Takayasu, M. Correlation networks among currencies. Phys. A Stat. Mech. Its Appl. 2006, 364, 336–342. [Google Scholar] [CrossRef]

- Aghabozorgi, S.; Shirkhorshidi, A.S.; Wah, T.Y. Time-series clustering—A decade review. Inf. Syst. 2015, 53, 16–38. [Google Scholar] [CrossRef]

- Kenett, D.Y.; Tumminello, M.; Madi, A.; Gur-Gershgoren, G.; Mantegna, R.N.; Ben-Jacob, E. Dominating clasp of the financial sector revealed by partial correlation analysis of the stock market. PLoS ONE 2010, 5, e15032. [Google Scholar] [CrossRef]

- Marti, G.; Nielsen, F.; Donnat, P. Optimal copula transport for clustering multivariate time series. In Proceedings of the 2016 IEEE International Conference on Acoustics, Speech and Signal Processing (ICASSP), Shanghai, China, 20–25 March 2016; IEEE: Piscataway, NJ, USA, 2016; pp. 2379–2383. [Google Scholar]

- Billio, M.; Getmansky, M.; Lo, A.W.; Pelizzon, L. Econometric measures of connectedness and systemic risk in the finance and insurance sectors. J. Financ. Econ. 2012, 104, 535–559. [Google Scholar] [CrossRef]

- Shternshis, A.; Mazzarisi, P.; Marmi, S. Efficiency of the Moscow Stock Exchange before 2022. Entropy 2022, 24, 1184. [Google Scholar] [CrossRef]

- Chakraborty, A.; Easwaran, S.; Sinha, S. Uncovering hierarchical structure of international FOREX market by using similarity metric between fluctuation distributions of currencies. Acta Phys. Pol. A 2020, 138, 105–115. [Google Scholar] [CrossRef]

- Keskin, M.; Deviren, B.; Kocakaplan, Y. Topology of the Correlation Networks among Major Currencies Using Hierarchical Structure Methods. Phys. A Stat. Mech. Its Appl. 2011, 390, 719–730. [Google Scholar] [CrossRef]

- Prim, R. Shortest connection networks and some generalizations. Bell Syst. Tech. J. 1957, 36, 1389–1401. [Google Scholar] [CrossRef]

- Bellman, R.; Kalaba, R. On adaptive control processes. IRE Trans. Autom. Control 1959, 4, 1–9. [Google Scholar] [CrossRef]

- Sakoe, H.; Chiba, S. Dynamic programming algorithm optimization for spoken word recognition. IEEE Trans. Acoust. Speech Signal Process. 1978, 26, 43–49. [Google Scholar] [CrossRef]

- Rabiner, L.; Rosenberg, A.; Levinson, S. Considerations in dynamic time warping algorithms for discrete word recognition. IEEE Trans. Acoust. Speech Signal Process. 1978, 26, 575–582. [Google Scholar] [CrossRef]

- Keogh, E.; Ratanamahatana, C.A. Exact indexing of dynamic time warping. Knowl. Inf. Syst. 2005, 7, 358–386. [Google Scholar] [CrossRef]

- Stübinger, J.; Schneider, L. Epidemiology of coronavirus COVID-19: Forecasting the future incidence in different countries. Healthcare 2020, 8, 99. [Google Scholar] [CrossRef] [PubMed]

- Kullback, S.; Leibler, R.A. On information and sufficiency. Ann. Math. Stat. 1951, 22, 79–86. [Google Scholar] [CrossRef]

- Denkowska, A.; Wanat, S. Dynamic Time Warping Algorithm in Modeling Systemic Risk in the European Insurance Sector. Entropy 2021, 23, 1022. [Google Scholar] [CrossRef] [PubMed]

- Li, W.; Hommel, U.; Paterlini, S. Network topology and systemic risk: Evidence from the Euro Stoxx market. Financ. Res. Lett. 2018, 27, 105–112. [Google Scholar] [CrossRef]

- Freeman, L.C. Centrality in social networks conceptual clarification. Soc. Netw. 1979, 1, 215–239. [Google Scholar] [CrossRef]

- Newman, M.E.J. Assortative mixing in networks. Phys. Rev. Lett. 2002, 89, 208701. [Google Scholar] [CrossRef]

- Newman, M.E.J.; Girvan, M. Finding and evaluating community structure in networks. Phys. Rev. E 2004, 69, 026113. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| ARS | Argentinian Peso | HUF | Hungarian Forint | RON | Romanian New Leo |

| AUD | Australian Dollar | IDR | Indonesian Rupiah | RUB | Russian Rubles |

| BGN | Bulgarian Lev | ILS | Israeli New Shekel | SEK | Swedish Krona |

| BRL | Brazilian Real | INR | Indian Rupee | SGD | Singaporean Dollar |

| CAD | Canadian Dollar | ISK | Icelandic Krona | THB | Thai Baht |

| CHF | Swiss Franc | JPY | Japanese Yen | TRY | Turkish Lira |

| CLP | Chilean Pesos | KRW | South Korean Won | TWD | Taiwan Dollar |

| CNY | Chinese Yuan | MXN | Mexican Peso | USD | U.S. Dollar |

| CZK | Czech Koruna | MYR | Malaysian Ringgit | XAG | Silver (ozt) |

| DKK | Danish Krone | NAD | Namibian Dollar | XAU | Gold (ozt) |

| EGP | Egyptian Pound | NOK | Norwegian Krone | XPD | Palladium (ozt) |

| EUR | Euro | NZD | New Zealand Dollar | XPT | Platinum (ozt) |

| GBP | UK Pound Sterling | PHP | Philippines Peso | ZAR | South Africa Rand |

| HKD | Hong Kong Dollar | PLN | Polish Zloty |

| Currency | Mean | Std. Dev. | CV | Currency | Mean | Std. Dev. | CV | Currency | Mean | Std. Dev. | CV |

|---|---|---|---|---|---|---|---|---|---|---|---|

| ARS | 0.044 | 0.010 | 0.230 | HUF | 0.012 | 0.000 | 0.036 | RON | 0.932 | 0.021 | 0.022 |

| AUD | 2.892 | 0.189 | 0.066 | IDR | 0.000 | 0.000 | 0.067 | RUB | 0.058 | 0.010 | 0.180 |

| BGN | 2.334 | 0.066 | 0.028 | ILS | 1.219 | 0.094 | 0.077 | SEK | 0.438 | 0.014 | 0.033 |

| BRL | 0.781 | 0.086 | 0.109 | INR | 0.054 | 0.003 | 0.051 | SGD | 2.977 | 0.209 | 0.070 |

| CAD | 3.137 | 0.242 | 0.077 | ISK | 0.031 | 0.002 | 0.065 | THB | 0.124 | 0.004 | 0.033 |

| CHF | 4.348 | 0.272 | 0.063 | JPY | 0.035 | 0.002 | 0.043 | TRY | 0.426 | 0.130 | 0.305 |

| CLP | 0.005 | 0.000 | 0.036 | KRW | 0.003 | 0.000 | 0.030 | TWD | 0.140 | 0.009 | 0.061 |

| CNY | 0.608 | 0.046 | 0.075 | MXN | 0.198 | 0.021 | 0.104 | USD | 4.073 | 0.339 | 0.083 |

| CZK | 0.179 | 0.010 | 0.055 | MYR | 0.957 | 0.048 | 0.051 | XAG | 91.001 | 12.552 | 0.138 |

| DKK | 0.613 | 0.018 | 0.029 | NAD | 0.257 | 0.018 | 0.071 | XAU | 7284.903 | 630.602 | 0.087 |

| EGP | 0.243 | 0.018 | 0.073 | NOK | 0.442 | 0.024 | 0.055 | XPD | 9057.949 | 1094.614 | 0.121 |

| EUR | 4.564 | 0.128 | 0.028 | NZD | 2.695 | 0.142 | 0.053 | XPT | 3976.287 | 462.726 | 0.116 |

| GBP | 5.268 | 0.235 | 0.045 | PHP | 0.080 | 0.003 | 0.034 | ZAR | 0.257 | 0.018 | 0.071 |

| HKD | 0.523 | 0.041 | 0.079 |

| Characteristics | |||||||

|---|---|---|---|---|---|---|---|

| 2020–2022 | |||||||

| Mean Values | |||||||

| apl | 162.277 | 5.833 | 6.385 | 8.436 | 14.575 | 2.292 | 1.443 |

| diameter | 439.147 | 15.785 | 17.500 | 21.688 | 34.392 | 5.767 | 12.253 |

| centr_degree | 0.098 | 0.098 | 0.116 | 0.125 | 0.075 | 0.233 | 0.047 |

| centr_clo | 0.241 | 0.241 | 0.233 | 0.242 | 0.181 | 0.284 | 0.098 |

| centr_eigen | 0.814 | 0.814 | 0.832 | 0.839 | 0.810 | 0.871 | 0.812 |

| assortativity | −0.195 | −0.195 | −0.250 | −0.236 | −0.282 | −0.321 | −0.293 |

| Coefficient of Variation (CV) Values | |||||||

| apl | 0.378 | 0.378 | 0.352 | 0.269 | 0.058 | 0.305 | 0.549 |

| diameter | 0.319 | 0.319 | 0.306 | 0.258 | 0.086 | 0.297 | 0.410 |

| centr_degree | 0.137 | 0.137 | 0.258 | 0.242 | 0.113 | 0.431 | 0.287 |

| centr_clo | 0.172 | 0.172 | 0.238 | 0.258 | 0.124 | 0.320 | 0.229 |

| centr_eigen | 0.031 | 0.031 | 0.037 | 0.038 | 0.019 | 0.033 | 0.075 |

| assortativity | −0.445 | −0.445 | −0.304 | −0.369 | −0.172 | −0.278 | −0.409 |

| Characteristics | |||||||

|---|---|---|---|---|---|---|---|

| 2020 | |||||||

| Mean Values | |||||||

| apl | 102.936 | 6.421 | 6.638 | 8.715 | 13.499 | 2.673 | 0.800 |

| diameter | 276.695 | 17.260 | 18.157 | 22.358 | 30.765 | 6.527 | 3.410 |

| centr_degree | 0.080 | 0.080 | 0.110 | 0.110 | 0.075 | 0.130 | 0.050 |

| centr_clo | 0.213 | 0.213 | 0.220 | 0.225 | 0.222 | 0.239 | 0.110 |

| centr_eigen | 0.815 | 0.815 | 0.831 | 0.830 | 0.840 | 0.839 | 0.790 |

| assortativity | −0.145 | −0.145 | −0.256 | −0.262 | −0.102 | −0.295 | −0.290 |

| Coefficient of Variation (CV) Values | |||||||

| apl | 0.403 | 0.403 | 0.366 | 0.274 | 0.079 | 0.305 | 0.340 |

| diameter | 0.319 | 0.319 | 0.310 | 0.244 | 0.104 | 0.266 | 0.270 |

| centr_degree | 0.299 | 0.299 | 0.294 | 0.298 | 0.113 | 0.263 | 0.320 |

| centr_clo | 0.211 | 0.211 | 0.258 | 0.235 | 0.121 | 0.240 | 0.220 |

| centr_eigen | 0.041 | 0.041 | 0.046 | 0.043 | 0.019 | 0.050 | 0.080 |

| assortativity | −0.686 | −0.686 | −0.392 | −0.322 | −0.769 | −0.265 | −0.370 |

| 2021 | |||||||

| Mean Values | |||||||

| apl | 97.806 | 6.089 | 6.490 | 8.632 | 15.788 | 3.125 | 0.580 |

| diameter | 271.857 | 16.925 | 18.024 | 22.531 | 38.599 | 8.000 | 4.520 |

| centr_degree | 0.131 | 0.131 | 0.122 | 0.129 | 0.075 | 0.112 | 0.060 |

| centr_clo | 0.239 | 0.239 | 0.230 | 0.232 | 0.142 | 0.215 | 0.120 |

| centr_eigen | 0.841 | 0.841 | 0.836 | 0.843 | 0.801 | 0.835 | 0.810 |

| assortativity | −0.312 | −0.312 | −0.302 | −0.284 | −0.366 | −0.299 | −0.300 |

| Coefficient of Variation (CV) Values | |||||||

| apl | 0.395 | 0.395 | 0.376 | 0.285 | 0.063 | 0.358 | 0.250 |

| diameter | 0.311 | 0.311 | 0.323 | 0.275 | 0.101 | 0.336 | 0.270 |

| centr_degree | 0.241 | 0.241 | 0.279 | 0.254 | 0.113 | 0.248 | 0.300 |

| centr_clo | 0.241 | 0.241 | 0.236 | 0.259 | 0.170 | 0.291 | 0.220 |

| centr_eigen | 0.040 | 0.040 | 0.043 | 0.044 | 0.056 | 0.052 | 0.060 |

| assortativity | −0.233 | −0.233 | −0.286 | −0.274 | −0.160 | −0.351 | −0.430 |

| 2022 | |||||||

| Mean Values | |||||||

| apl | 92.492 | 5.769 | 6.042 | 8.088 | 13.122 | 2.743 | 0.920 |

| diameter | 254.037 | 15.846 | 16.317 | 20.270 | 27.875 | 6.442 | 8.120 |

| centr_degree | 0.119 | 0.119 | 0.119 | 0.123 | 0.057 | 0.124 | 0.060 |

| centr_clo | 0.250 | 0.250 | 0.255 | 0.264 | 0.211 | 0.242 | 0.110 |

| centr_eigen | 0.838 | 0.838 | 0.840 | 0.842 | 0.764 | 0.835 | 0.810 |

| assortativity | −0.299 | −0.299 | −0.214 | −0.214 | 0.008 | −0.327 | −0.330 |

| Coefficient of Variation (CV) Values | |||||||

| apl | 0.387 | 0.387 | 0.339 | 0.245 | 0.042 | 0.335 | 0.490 |

| diameter | 0.367 | 0.367 | 0.300 | 0.237 | 0.101 | 0.329 | 0.440 |

| centr_degree | 0.239 | 0.239 | 0.264 | 0.248 | 0.172 | 0.257 | 0.240 |

| centr_clo | 0.242 | 0.242 | 0.211 | 0.176 | 0.058 | 0.240 | 0.220 |

| centr_eigen | 0.044 | 0.044 | 0.036 | 0.027 | 0.035 | 0.053 | 0.070 |

| assortativity | −0.224 | −0.224 | −0.465 | −0.391 | 9.087 | −0.266 | −0.320 |

| Time Period | ||||

|---|---|---|---|---|

| Mean | CV | Mean | CV | |

| 2020–2022 | 0.481 | 0.397 | 0.077 | 0.007 |

| 2021 | 0.484 | 0.369 | 0.101 | 0.006 |

| 2022 | 0.480 | 0.392 | 0.093 | 0.007 |

| 2023 | 0.487 | 0.374 | 0.095 | 0.006 |

| Base PLN | 2020–2022 | 2020 | 2021 | 2022 |

|---|---|---|---|---|

| apl | 14.183 | 13.405 | 16.077 | 12.934 |

| diameter | 32.420 | 30.344 | 38.505 | 27.305 |

| centr_degree | 0.078 | 0.078 | 0.078 | 0.053 |

| centr_clo | 0.186 | 0.221 | 0.135 | 0.217 |

| centr_eigen | 0.804 | 0.846 | 0.782 | 0.756 |

| assortativity | −0.311 | −0.072 | −0.419 | 0.006 |

| Base USD | 2020–2022 | 2020 | 2021 | 2022 |

| apl | 14.432 | 13.649 | 15.912 | 13.184 |

| diameter | 34.519 | 30.344 | 40.760 | 27.305 |

| centr_degree | 0.078 | 0.078 | 0.078 | 0.078 |

| centr_clo | 0.186 | 0.221 | 0.141 | 0.220 |

| centr_eigen | 0.827 | 0.845 | 0.787 | 0.824 |

| assortativity | −0.202 | −0.109 | −0.357 | −0.082 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Andrzejak, J.; Chmielewski, L.J.; Landmesser-Rusek, J.; Orłowski, A. The Impact of the Measure Used to Calculate the Distance between Exchange Rate Time Series on the Topological Structure of the Currency Network. Entropy 2024, 26, 279. https://doi.org/10.3390/e26040279

Andrzejak J, Chmielewski LJ, Landmesser-Rusek J, Orłowski A. The Impact of the Measure Used to Calculate the Distance between Exchange Rate Time Series on the Topological Structure of the Currency Network. Entropy. 2024; 26(4):279. https://doi.org/10.3390/e26040279

Chicago/Turabian StyleAndrzejak, Joanna, Leszek J. Chmielewski, Joanna Landmesser-Rusek, and Arkadiusz Orłowski. 2024. "The Impact of the Measure Used to Calculate the Distance between Exchange Rate Time Series on the Topological Structure of the Currency Network" Entropy 26, no. 4: 279. https://doi.org/10.3390/e26040279