Quantum Bohmian-Inspired Potential to Model Non–Gaussian Time Series and Its Application in Financial Markets

,

,  and

and

{kind=link}

{kind=link}

{kind=link}

Abstract

:1. Introduction

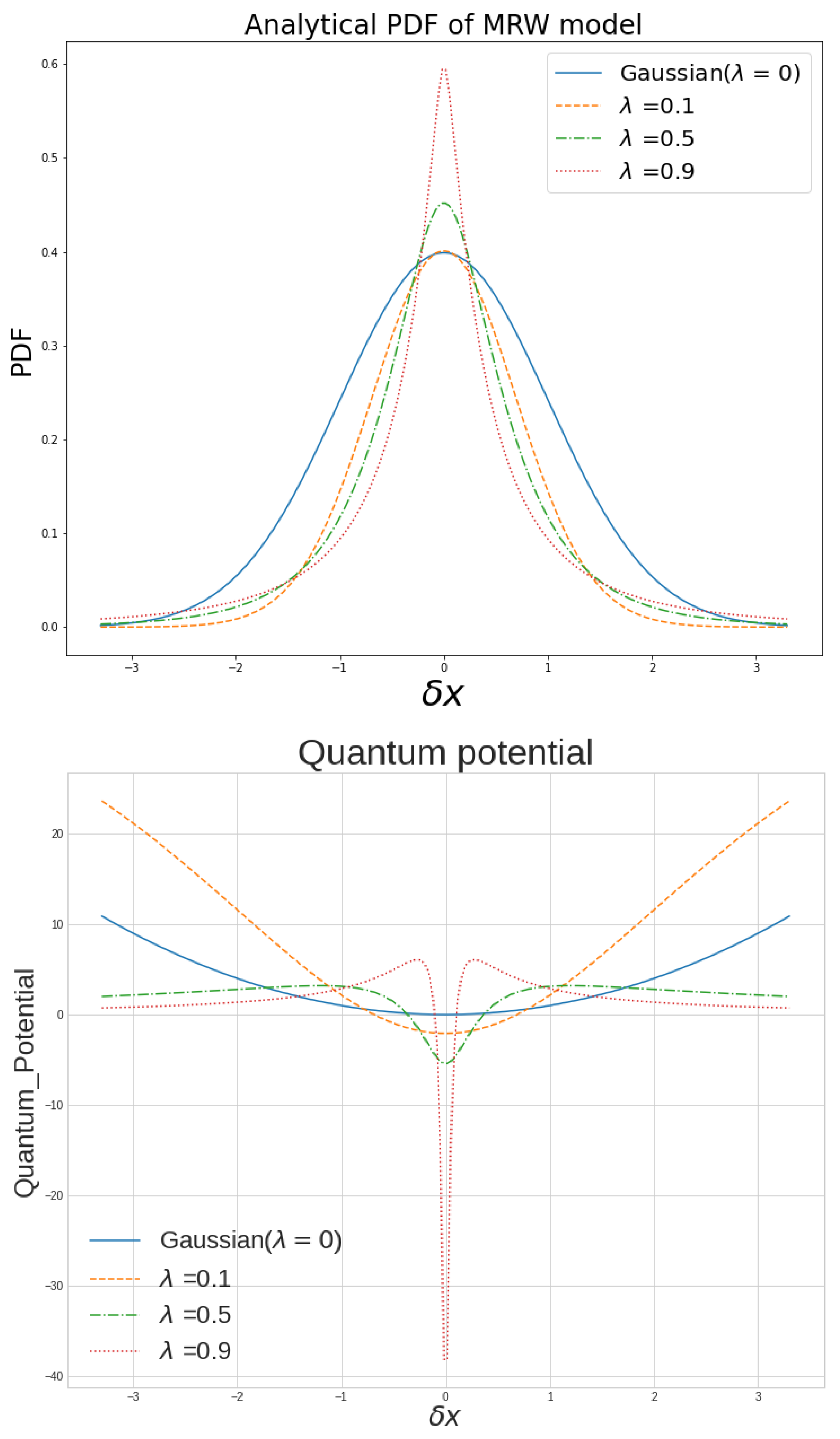

2. Bohmian Mechanics and the Quantum Potential Inspired Method

3. Multifractal Formalism

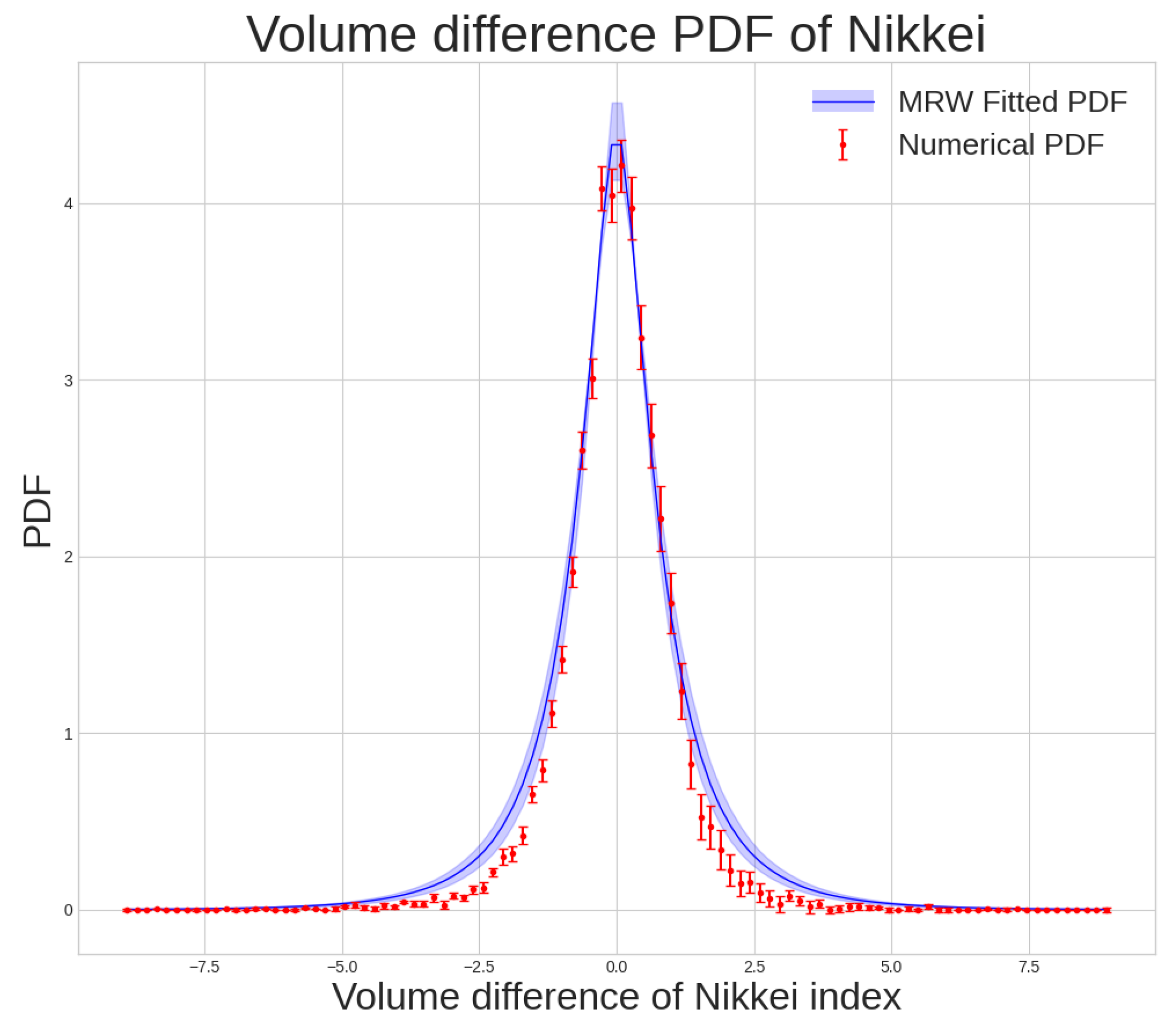

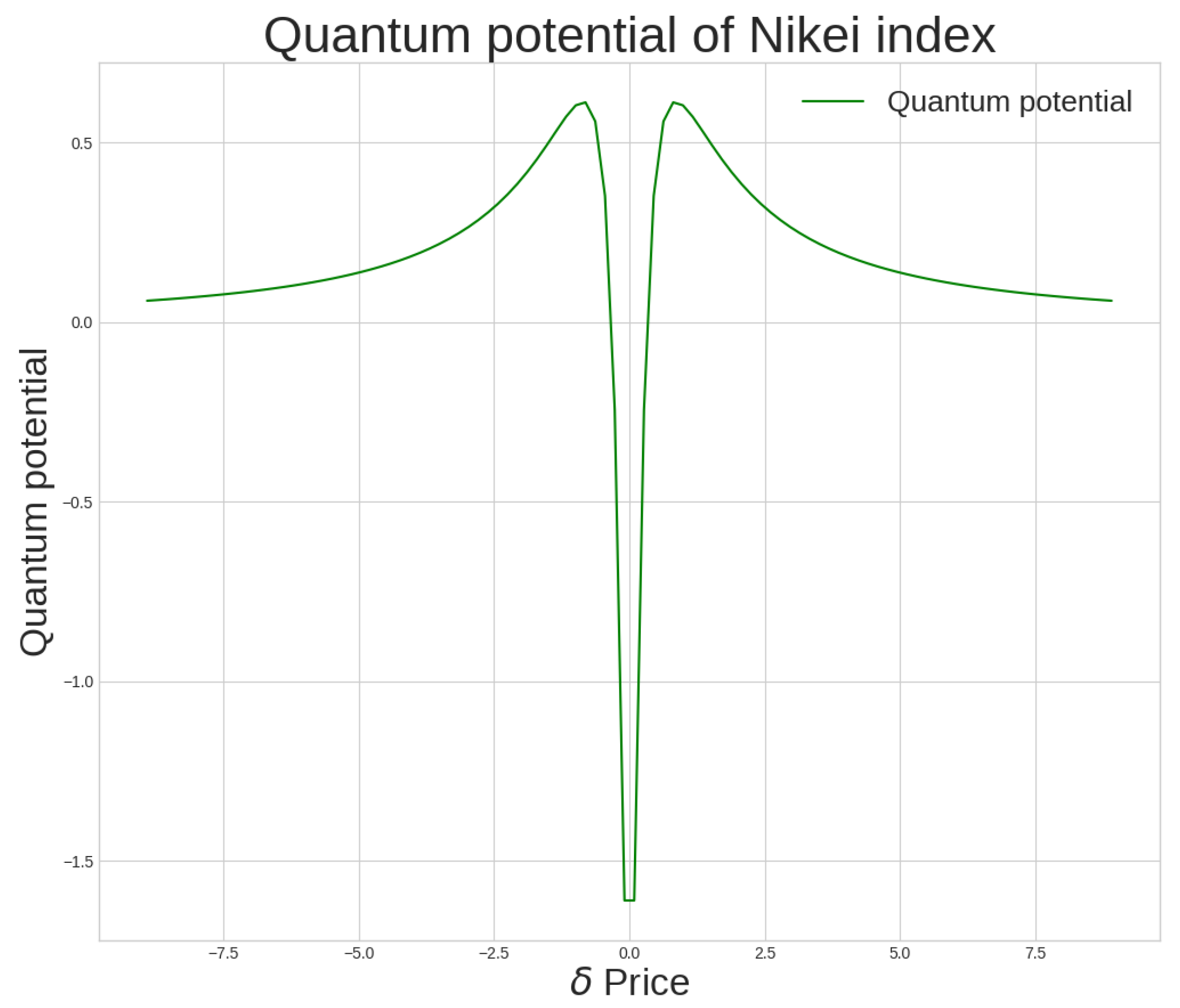

4. Results for Computing Quantum Potential and Real Data Fit

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Baaquie, B.E. Quantum Finance: Path Integrals and Hamiltonians for Options and Interest Rates; Cambridge University Press: Cambridge, UK, 2007. [Google Scholar]

- Bohm, D.; Hiley, B.; Holland, P. Book-Review-the Undivided Universe-an Ontological Interpretation of Quantum Theory. Nature 1993, 366, 420. [Google Scholar]

- Orus, R.; Mugel, S.; Lizaso, E. Quantum computing for finance: Overview and prospects. Rev. Phys. 2019, 4, 100028. [Google Scholar] [CrossRef]

- Khrennikov, A. Ubiquitous Quantum Structure; Springer: Berlin/Heidelberg, Germany, 2010. [Google Scholar]

- Khaksar, H.; Haven, E.; Nasiri, S.; Jafari, G. Using the Quantum Potential in Elementary Portfolio Management: Some Initial Ideas. Entropy 2021, 23, 180. [Google Scholar] [CrossRef] [PubMed]

- Lee, R.S. Future Trends in Quantum Finance. In Quantum Finance; Springer: Berlin/Heidelberg, Germany, 2020; pp. 399–405. [Google Scholar]

- Bagarello, F. Quantum Dynamics for Classical Systems: With Applications of the Number Operator; John Wiley & Sons: Hoboken, NJ, USA, 2012. [Google Scholar]

- Mugel, S.; Abad, M.; Bermejo, M.; Sánchez, J.; Lizaso, E.; Orús, R. Hybrid quantum investment optimization with minimal holding period. Sci. Rep. 2021, 11, 19587. [Google Scholar] [CrossRef]

- Woerner, S.; Egger, D.J. Quantum risk analysis. Npj Quantum Inf. 2019, 5, 15. [Google Scholar] [CrossRef] [Green Version]

- Tahmasebi, F.; Meskinimood, S.; Namaki, A.; Farahani, S.V.; Jalalzadeh, S.; Jafari, G. Financial market images: A practical approach owing to the secret quantum potential. EPL 2015, 109, 30001. [Google Scholar] [CrossRef]

- Choustova, O. Quantum probability and financial market. Inf. Sci. 2009, 179, 478–484. [Google Scholar] [CrossRef]

- Chabaud, B.; Naert, A.; Peinke, J.; Chilla, F.; Castaing, B.; Hebral, B. Transition toward developed turbulence. Phys. Rev. Lett. 1994, 73, 3227. [Google Scholar] [CrossRef]

- Haven, E. An ‘h-Brownian motion’of stochastic option prices. Phys. A 2003, 344, 151–155. [Google Scholar]

- Nasiri, S.; Bektas, E.; Jafari, G.R. The impact of trading volume on the stock market credibility: Bohmian quantum potential approach. Phys. A Stat. Mech. Its Appl. 2018, 512, 1104–1112. [Google Scholar] [CrossRef]

- Haven, E.; Khrennikov, A. Quantum Social Science; Cambridge University Press: Cambridge, UK, 2013. [Google Scholar]

- Mikhaylov, A.N.; Guseinov, D.V.; Belov, A.I.; Korolev, D.S.; Shishmakova, V.A.; Koryazhkina, M.N.; Filatov, D.O.; Gorshkov, O.N.; Maldonado, D.; Alonso, F.J.; et al. Stochastic resonance in metal-oxide memristive device. Chaos Solitons Fractals 2021, 144, 110723. [Google Scholar] [CrossRef]

- Guarcello, C.; Valenti, D.; Spagnolo, B.; Pierro, V.; Filatrella, G. Josephson-based Threshold Detector for Lévy-Distributed Current Fluctuations. Phys. Rev. Appl. 2019, 11, 044078. [Google Scholar] [CrossRef] [Green Version]

- Lisowski, B.; Valenti, D.; Spagnolo, B.; Bier, M.; Gudowska-Nowak, E. Stepping molecular motor amid Lévy white noise. Phys. Rev. E 2015, 91, 042713. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Bonanno, G.; Spagnolo, B. Escape times in stock markets. Fluct. Noise Lett. 2005, 5, L325–L330. [Google Scholar] [CrossRef]

- Valenti, D.; Fazio, G.; Spagnolo, B. Stabilizing effect of volatility in financial markets. Phys. Rev. E 2018, 97, 062307. [Google Scholar] [CrossRef] [Green Version]

- Bonanno, G.; Valenti, D.; Spagnolo, B. Role of noise in a market model with stochastic volatility. Eur. Phys. J. B 2006, 53, 405–409. [Google Scholar] [CrossRef]

- Valenti, D.; Spagnolo, B.; Bonanno, G. Hitting time distributions in financial markets. Phys. A 2007, 382, 311–320. [Google Scholar] [CrossRef] [Green Version]

- Fényes, I. A Deduction of Schrödinger Equation. Acta Bolyaiana 1946, 1, 5. [Google Scholar]

- Fényes, I. Eine wahrscheinlichkeitstheoretische Begründung und Interpretation der Quantenmechanik. Z. Für Phys. 2006, 132, 81–106. [Google Scholar] [CrossRef]

- de Broglie, L. La réinterpretation de la mécanique ondulatoire. Phys. Bull. 2006, 19, 133. [Google Scholar] [CrossRef]

- Nelson, E. Dynamical Theories of Brownian Motion; Princeton University Press: Princeton, NJ, USA, 1966. [Google Scholar]

- Nelson, E. Quantum Fluctuations; Princeton University Press: Princeton, NJ, USA, 1985. [Google Scholar]

- Nelson, E. Field Theory and the Future of Stochastic Mechanics. In Stochastic Processes in Classical and Quantum Systems, Proceedings of the 1st Ascona-Como International Conference, Ascona, Ticino (Switzerland), 24–29 June 1985; Springer: Berlin/Heidelberg, Germany, 1986; pp. 438–469. [Google Scholar]

- Bohm, D. A suggested interpretation of the quantum theory in terms of “hidden” variables. I. Phys. Rev. 1952, 85, 166. [Google Scholar] [CrossRef]

- Choustova, O. Quantum modeling of nonlinear dynamics of stock prices: Bohmian approach. Theor. Math. Phys. 2007, 152, 1213–1222. [Google Scholar] [CrossRef]

- Haven, E.; Khrennikov, A. Applications of quantum mechanical techniques to areas outside of quantum mechanics. Front. Phys. 2017, 5, 60. [Google Scholar] [CrossRef]

- Shen, C.; Haven, E. Using empirical data to estimate potential functions in commodity markets: Some initial results. Int. J. Theor. Phys. 2017, 56, 4092–4104. [Google Scholar] [CrossRef] [Green Version]

- Lai, Z.K.; Farahani, S.V.; Movahed, S.; Jafari, G. Coupled uncertainty provided by a multifractal random walker. Phys. Lett. A 2015, 379, 2284–2290. [Google Scholar]

- Ausloos, M. Generalized Hurst exponent and multifractal function of original and translated texts mapped into frequency and length time series. Phys. Rev. E 2012, 86, 031108. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Jafari, G.R.; Sadegh Movahed, M.; Norouzzadeh, P.; Bahraminasab, A.; Sahimi, M.; Ghasemi, F.; Rahimi Tabar, M.R. Uncertainty in the fluctuations of the price of stocks. Int. J. Mod. Phys. C 2007, 18, 1689. [Google Scholar] [CrossRef] [Green Version]

- Saakian, D.B.; Martirosyan, A.; Hu, C.K.; Struzik, Z. Exact probability distribution function for multifractal random walk models of stocks. EPL 2011, 95, 28007. [Google Scholar] [CrossRef] [Green Version]

- Muzy, J.F.; Sornette, D.; Delour, J.; Arneodo, A. Multifractal Returns and Hierarchical Portfolio Theory. Quant. Financ. 2001, 1, 131–148. [Google Scholar] [CrossRef]

- Muzy, J.F.; Delour, J.; Bacry, E. Modelling fluctuations of financial time series: From cascade process to stochastic volatility model. Eur. Phys. J. B-Condens. Matter Complex Syst. 2000, 17, 537–548. [Google Scholar] [CrossRef] [Green Version]

- Ghashghaie, S.; Breymann, W.; Peinke, J.; Talkner, P.; Dodge, Y. Turbulent cascades in foreign exchange markets. Nature 1996, 381, 767–770. [Google Scholar] [CrossRef]

- Bacry, E.; Delour, J.; Muzy, J.F. Multifractal random walk. Phys. Rev. E 2001, 64, 026103. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Kiyono, K.; Struzik, Z.R.; Yamamoto, Y. Criticality and phase transition in stock-price fluctuations. Phys. Rev. Lett. 2006, 96, 068701. [Google Scholar] [CrossRef] [Green Version]

- Manshour, P.; Saberi, S.; Sahimi, M.; Peinke, J.; Pacheco, A.F.; Tabar, M.R.R. Turbulence like behavior of seismic time series. Phys. Rev. Lett. 2009, 102, 014101. [Google Scholar] [CrossRef] [PubMed]

- Shayeganfar, F.; Jabbari-Farouji, S.; Movahed, M.S.; Jafari, G.; Tabar, M.R.R. Multifractal analysis of light scattering-intensity fluctuations. Phys. Rev. E 2009, 80, 061126. [Google Scholar] [CrossRef] [Green Version]

- Koohi Lai, Z.; Namaki, A.; Hosseiny, A.; Jafari, G.; Ausloos, M. Coupled criticality analysis of inflation and unemployment. Entropy 2021, 23, 42. [Google Scholar] [CrossRef] [PubMed]

- Shayeganfar, F.; Jabbari-Farouji, S.; Movahed, M.S.; Jafari, G.R.; Tabar, M.R.R. Stochastic qualifier of gel and glass transitions in laponite suspensions. Phys. Rev. E 2010, 81, 061404. [Google Scholar] [CrossRef] [Green Version]

- Castaing, B.; Gagne, Y.; Hopfinger, E. Velocity probability density functions of high Reynolds number turbulence. Phys. D Nonlinear Phenom. 1990, 46, 177–200. [Google Scholar] [CrossRef]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Hosseini, R.; Tajik, S.; Koohi Lai, Z.; Jamali, T.; Haven, E.; Jafari, R. Quantum Bohmian-Inspired Potential to Model Non–Gaussian Time Series and Its Application in Financial Markets. Entropy 2023, 25, 1061. https://doi.org/10.3390/e25071061

Hosseini R, Tajik S, Koohi Lai Z, Jamali T, Haven E, Jafari R. Quantum Bohmian-Inspired Potential to Model Non–Gaussian Time Series and Its Application in Financial Markets. Entropy. 2023; 25(7):1061. https://doi.org/10.3390/e25071061

Chicago/Turabian StyleHosseini, Reza, Samin Tajik, Zahra Koohi Lai, Tayeb Jamali, Emmanuel Haven, and Reza Jafari. 2023. "Quantum Bohmian-Inspired Potential to Model Non–Gaussian Time Series and Its Application in Financial Markets" Entropy 25, no. 7: 1061. https://doi.org/10.3390/e25071061