Global Existence and Fixed-Time Synchronization of a Hyperchaotic Financial System Governed by Semi-Linear Parabolic Partial Differential Equations Equipped with the Homogeneous Neumann Boundary Condition

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Abstract

:1. Introduction

- We introduce diffusion terms to the hyperchaotic financial system (2) to stress that the aftereffect (or memory) in economy and regional disparities of economic development cannot always be neglected, and equip these semi-linear parabolic partial differential equations with the homogeneous boundary condition, thus obtaining the principal research object of this paper, i.e., (3). To the best of our knowledge, the research object of Reference [11] is most closely related to our research object in this paper, and the research aims of References [9,12,13,14] are most closely related to our aims in this paper. However, as remarked above, the systems concerned in References [9,12,13,14] are hyperchaotic financial systems (1) incorporating diffusion terms. The inclusion of diffusion terms in the hyperchaotic financial system (2), and the coefficients of the diffusion terms as functions in , facilitate our application of theoretical results concerning the system (3) obtained in this paper to coming up with suggestions for decision-making in real-world finance or economics.

- We prove rigorously that the initial-boundary value problem (3)–(7) is globally well posed in lower regularity space in Hadamard’s sense: for every initial datum in , the initial-boundary value problem (3)–(7) admits a unique global solution; in addition, the data-to-solution map is continuous. As alluded in Reference [11], the initial-boundary value problem (3)–(7) admits mild solutions; we find in this paper that mild solutions coincide with weak solutions to the initial-boundary value problem (3)–(7). We provide this assertion a complete rigorous proof via Galerkin’s method and by establishing two a priori estimates, and prove via utilizing the aforementioned a priori estimates that all solutions to the initial-boundary value problem (3)–(7) exist globally in time. Furthermore, we prove, via exploiting semigroup theory, two new assertions (which have not been claimed in Reference [11] or any other published paper): there exists a unique global weak (or equivalently, mild) solution in the Fréchet space corresponding to every initial datum in , thus defining a mapping of the Hilbert space into the Fréchet space ; the aforementioned mapping is continuous.

- We come up with a synchronization control for the response system corresponding to the drive financial system (3), and provide two criteria ensuring that the drive system (3) and its response system with the proposed control implemented achieve fixed-time synchronization. To the authors’ knowledge, among the results in the vast references concerning synchronization problems for (hyper)chaotic financial systems, only the results in References [30,31,32], whose main contributions were introduced briefly above, are highly close to our fixed-time synchronization results in this paper. The results in Reference [30] are concerned with finite-time synchronizability of the time-fractional-order (in the Grünwald–Letnikov sense) counterpart of the financial system (2). The results in Reference [31] are concerned with the fixed-time synchronizability of the financial system (1). The results in Reference [32] are concerned with the fixed-time synchronizability of the time-fractional-order (in Caputo’s sense) counterpart of the financial system (1). In view of these summaries, we conclude that our fixed-time synchronization results in this paper are indeed new.

2. Global Well-Posedness of the Initial-Boundary Value Problem (3)–(7)

2.1. Preliminaries

2.2. Two Useful a Priori Inequalities

2.3. The Global Well-Posedness

3. Existence Result of (5)–(8)–(48) and the Fixed-Time Synchronizability of the Drive-Response Systems (3) and (5) Controlled by (48)

3.1. Design of the Synchronization Control

3.2. Global Existence of the Problems (51) and (5)–(48)

3.3. The Fixed-Time Synchronizability of the Drive-Response Systems (3) and (5) Controlled by (48)

- In the control law (48), it depends not only on the structure of the drive-response financial system (3)–(5), but also on the information of the trajectory of the drive financial system (3). More precisely, in the control law (48), the control includesthe control includesand the control includesFrom the point of view of system or control theory, it is flawed to incorporate trajectory information in the synchronization control. The flaw in the control law (48) arises due to the nonlinearity of the financial system (3). This flaw could be eliminated by restricting the trajectory quadruple of the financial system (3) to be bounded in .

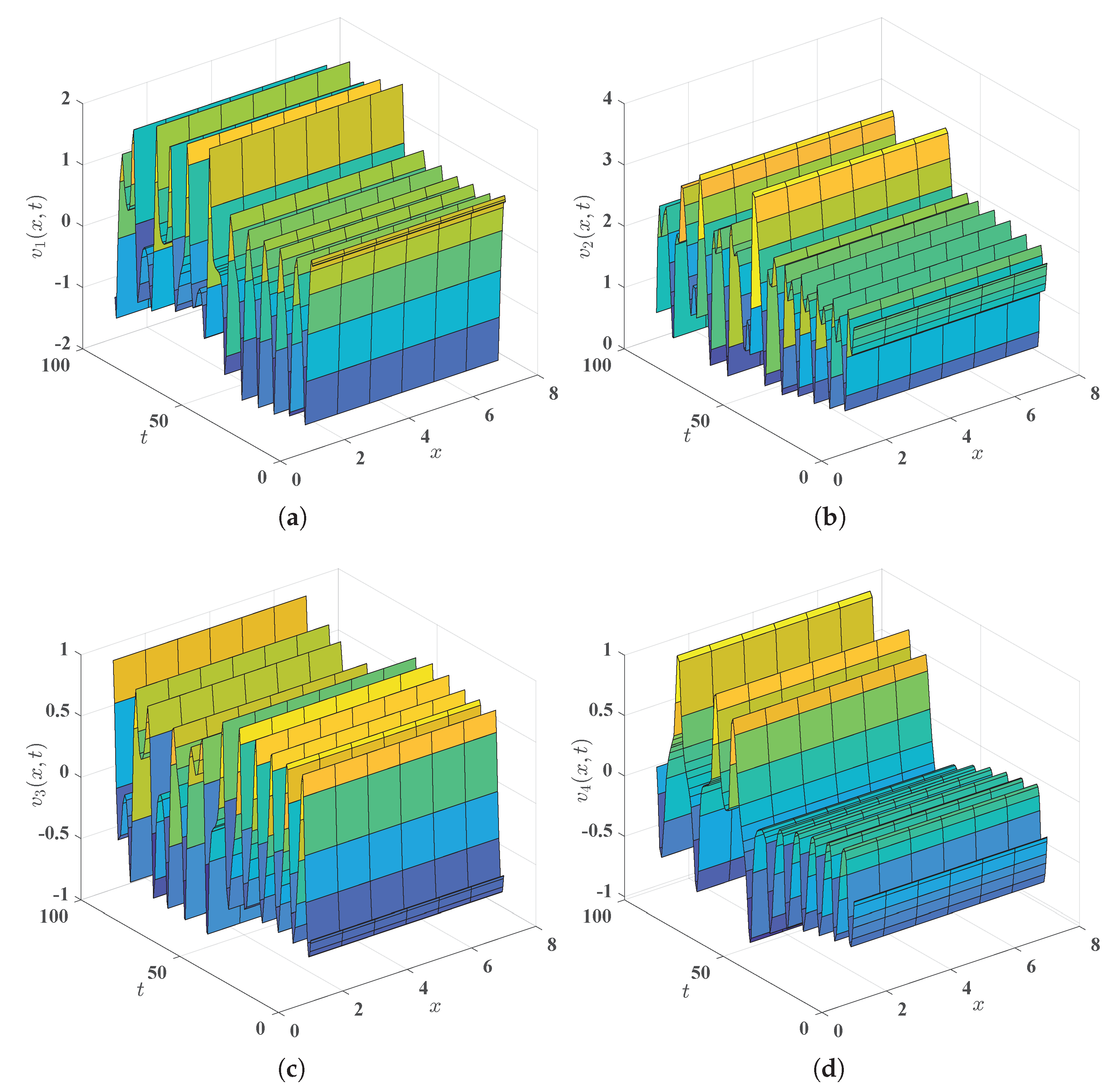

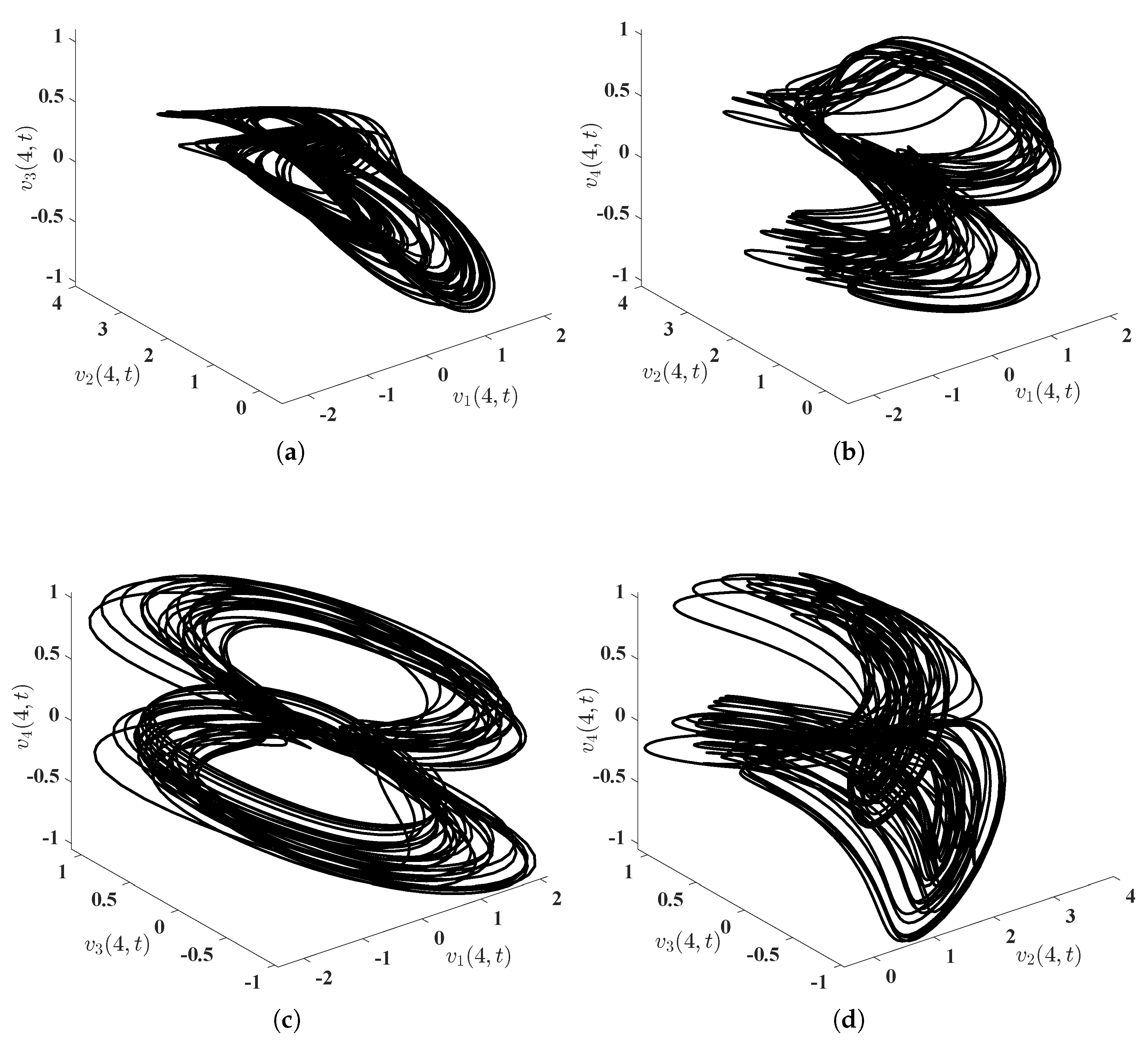

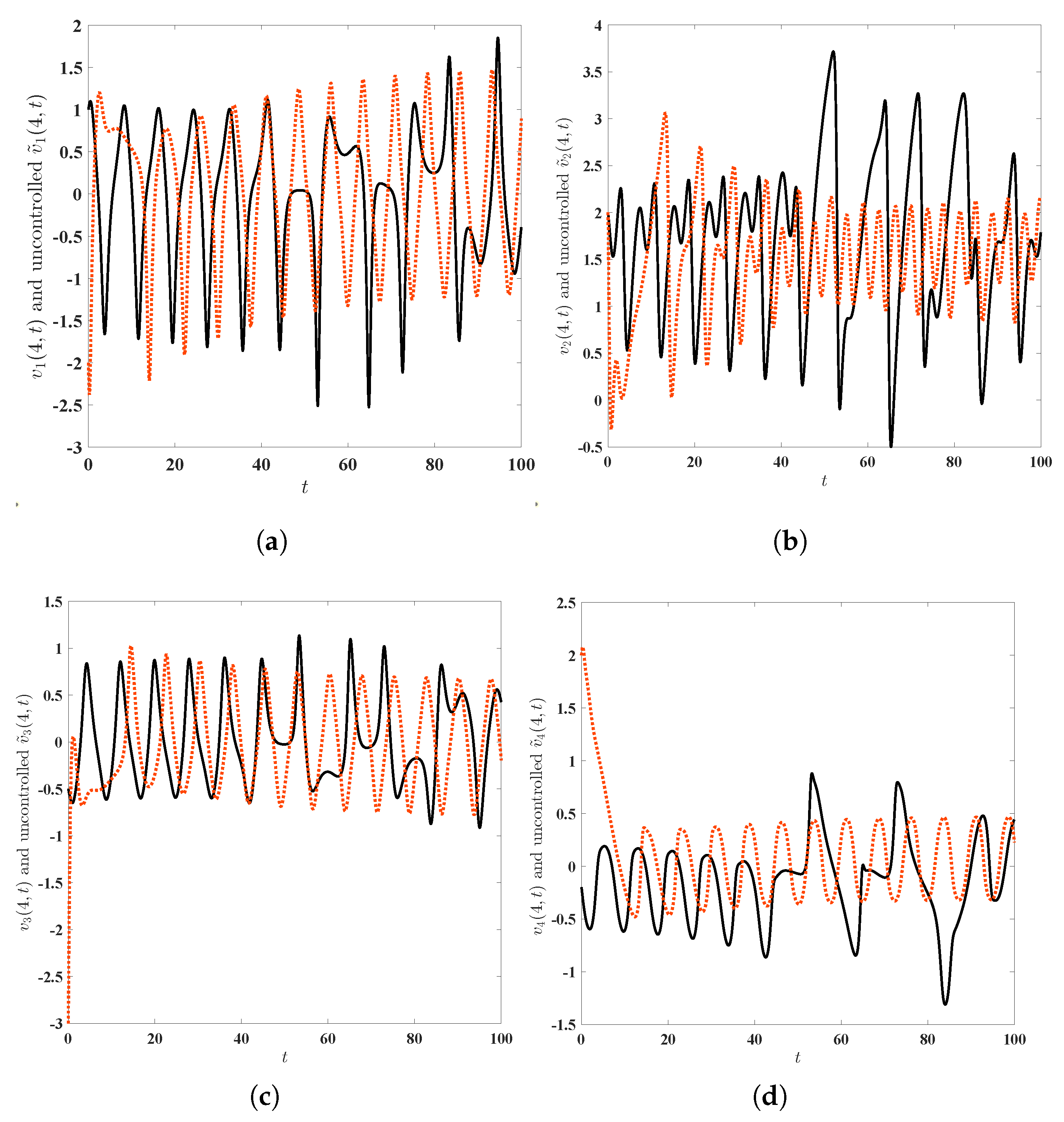

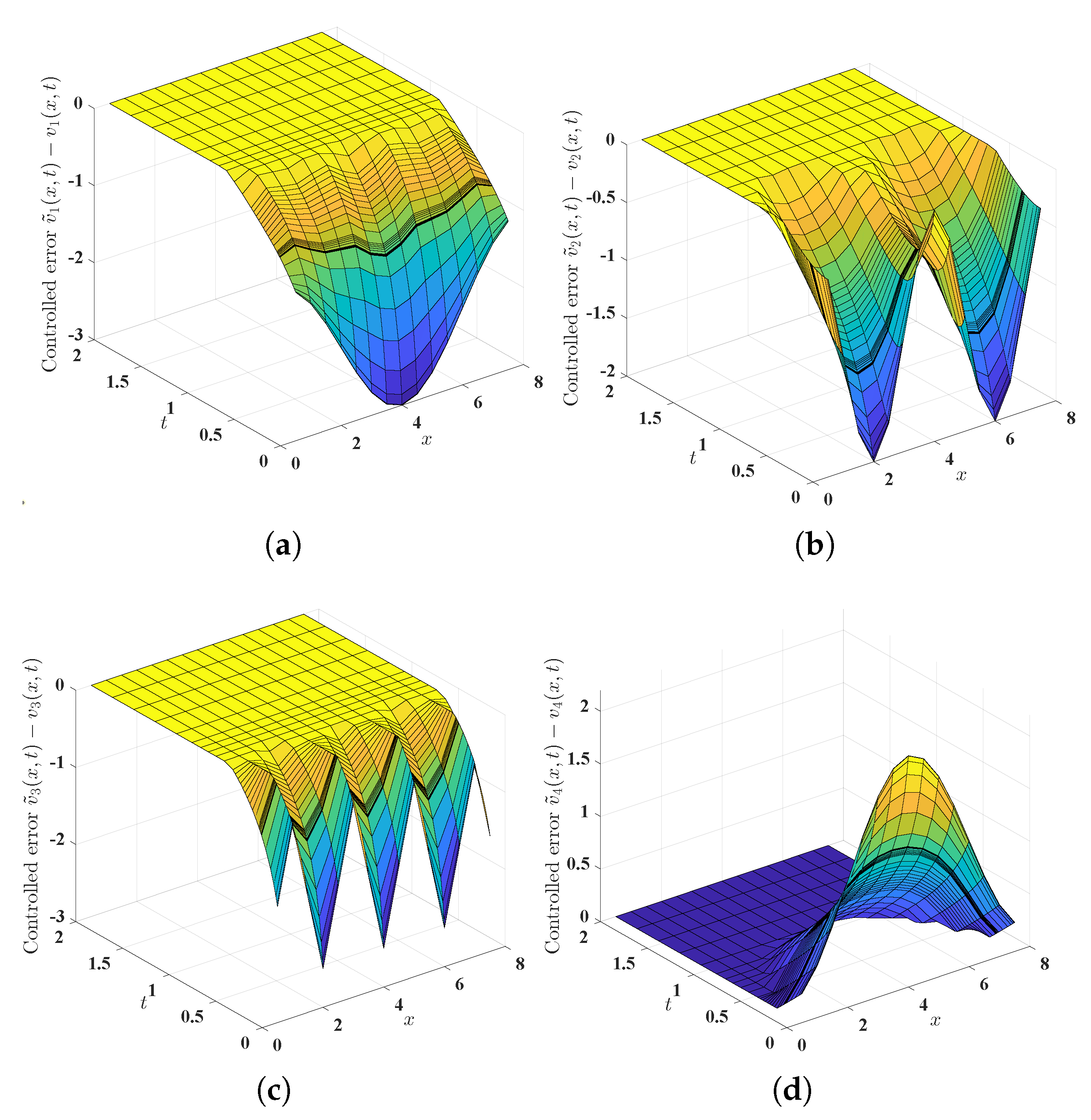

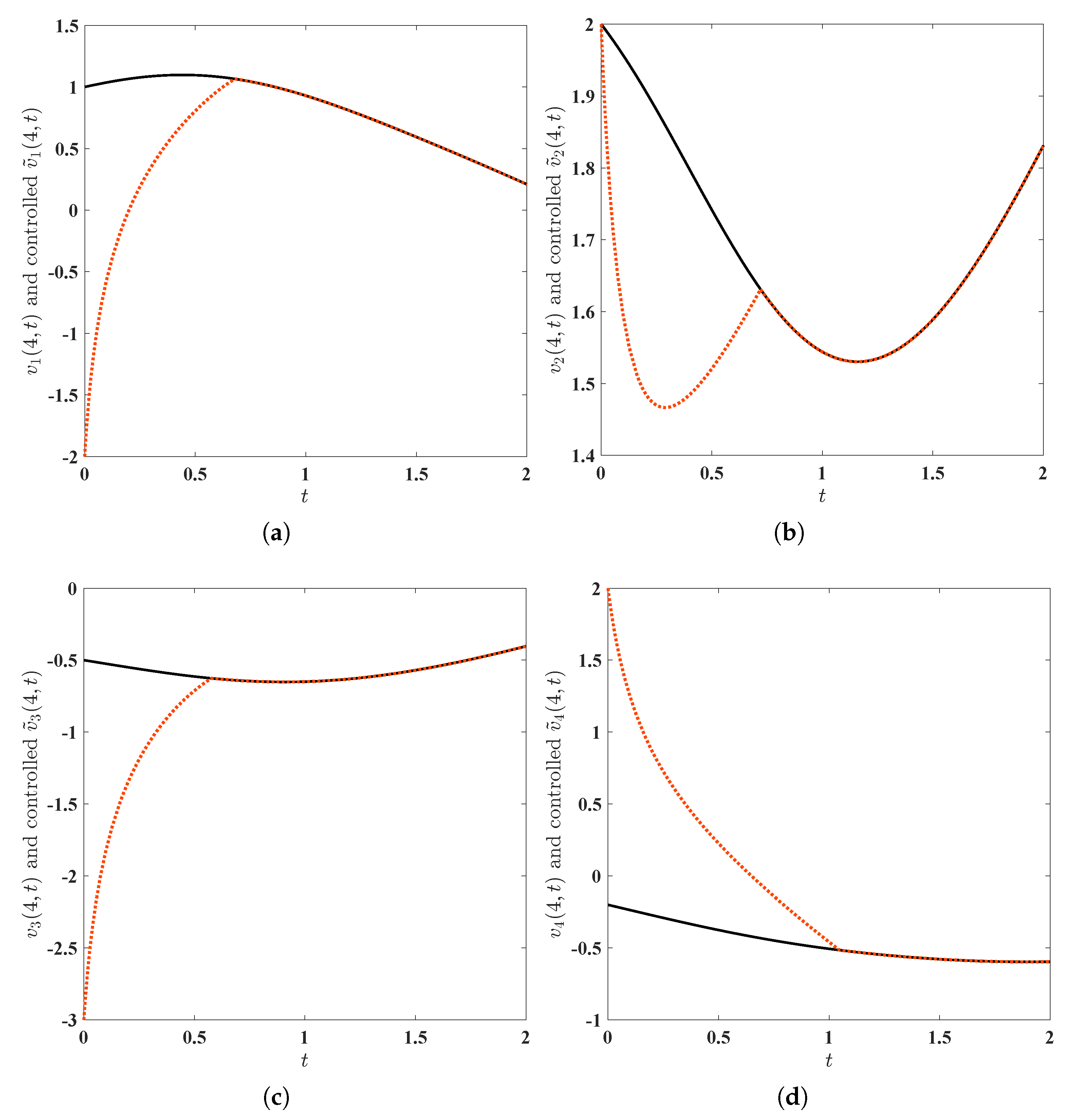

4. Numerical Simulations

5. Conclusions

Author Contributions

Funding

Conflicts of Interest

Appendix A. Proof of the Continuous Dependence and Uniqueness Parts of Theorem 1

References

- Huang, D.S.; Li, H.Q. Theory and Method of Nonlinear Economics; Sichuan University Press: Chengdu, China, 1993. (In Chinese) [Google Scholar]

- Chian, A.L.; Rempel, E.L.; Rogers, C. Complex economic dynamics: Chaotic saddle, crisis and intermittency. Chaos Solitons Fractals 2006, 29, 1194–1218. [Google Scholar] [CrossRef]

- Chen, W.C. Dynamics and control of a financial system with time-delayed feedbacks. Chaos Solitons Fractals 2008, 37, 1198–1207. [Google Scholar] [CrossRef]

- Chen, W.C. Nonlinear dynamics and chaos in a fractional-order financial system. Chaos Solitons Fractals 2008, 36, 1305–1314. [Google Scholar] [CrossRef]

- Yu, H.; Cai, G.; Li, Y. Dynamic analysis and control of a new hyperchaotic finance system. Nonlinear Dyn. 2012, 67, 2171–2182. [Google Scholar] [CrossRef]

- Cavalli, F.; Naimzada, A. Complex dynamics and multistability with increasing rationality in market games. Chaos Solitons Fractals 2016, 93, 151–161. [Google Scholar] [CrossRef]

- Tarasova, V.V.; Tarasov, V.E. Logistic map with memory from economic model. Chaos Solitons Fractals 2017, 95, 84–91. [Google Scholar] [CrossRef] [Green Version]

- Jajarmi, A.; Hajipour, M.; Baleanu, D. New aspects of the adaptive synchronization and hyperchaos suppression of a financial model. Chaos Solitons Fractals 2017, 99, 285–296. [Google Scholar] [CrossRef]

- Rao, R.F.; Zhong, S.M. Input-to-state stability and no-inputs stabilization of delayed feedback chaotic financial system involved in open and closed economy. Discrete Contin. Dyn. Syst. Ser. S 2021, 14, 1375–1393. [Google Scholar] [CrossRef] [Green Version]

- Almutairi, B.N.; Abouelregal, A.E.; Bin-Mohsin, B.; Alsulami, M.D.; Thounthong, P. Numerical solution of the multiterm time-fractional model for heat conductivity by local meshless technique. Complexity 2021, 2021, 9952562. [Google Scholar] [CrossRef]

- Li, X.G.; Rao, R.F.; Yang, X.S. Impulsive stabilization on hyper-chaotic financial system under neumann boundary. Mathematics 2022, 10, 1866. [Google Scholar] [CrossRef]

- Rao, R.F. Global stability of a markovian jumping chaotic financial system with partially unknown transition rates under impulsive control involved in the positive interest rate. Mathematics 2019, 7, 579. [Google Scholar] [CrossRef] [Green Version]

- Rao, R.F.; Zhu, Q.X. Exponential synchronization and stabilization of delayed feedback hyperchaotic financial system. Adv. Diff. Equ. 2021, 2021, 216. [Google Scholar] [CrossRef]

- Rao, R.F.; Li, X.D. Input-to-state stability in the meaning of switching for delayed feedback switched stochastic financial system. AIMS Math. 2021, 6, 1040–1064. [Google Scholar] [CrossRef]

- Wang, F.Z.; Ahmad, I.; Ahmad, H.; Alsulami, M.D.; Alimgeer, K.S.; Cesarano, C.; Nofal, T.A. Meshless method based on RBFs for solving three-dimensional multi-term time fractional PDEs arising in engineering phenomenons. J. King Saud Univ.-Sci. 2021, 33, 101604. [Google Scholar] [CrossRef]

- Khennaoui, A.A.; Ouannas, A.; Bekiros, S.; Aly, A.A.; Alotaibi, A.; Jahanshahi, H.; Alsubaie, H. Hidden homogeneous extreme multistability of a fractional-order hyperchaotic discrete-time system: Chaos, initial offset boosting, amplitude control, control, and synchronization. Symmetry 2023, 15, 139. [Google Scholar] [CrossRef]

- Medio, A.; Pireddu, M.; Zanolin, F. Chaotic dynamics for maps in one and two dimensions: A geometrical method and applications to economics. Internat. J. Bifur. Chaos Appl. Sci. Engrg. 2009, 19, 3283–3309. [Google Scholar] [CrossRef] [Green Version]

- Jahanshahi, H.; Yousefpour, A.; Wei, Z.C.; Alcaraz, R.; Bekiros, S. A financial hyperchaotic system with coexisting attractors: Dynamic investigation, entropy analysis, control and synchronization. Chaos Solitons Fractals 2019, 126, 66–77. [Google Scholar] [CrossRef]

- Almalki, S.J.; Abushal, T.A.; Alsulami, M.D.; Abd-Elmougod, G.A. Analysis of type-II censored competing risks’ data under reduced new modified Weibull distribution. Complexity 2021, 2021, 9932840. [Google Scholar] [CrossRef]

- Liu, C.Y.; Ding, L.; Ding, Q. Research about the characteristics of chaotic systems based on multi-scale entropy. Entropy 2021, 21, 663. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Alsulami, M.D.; Abu-Zinadah, H.; Ibrahim, A.H. Machine learning model and statistical methods for COVID-19 evolution prediction. Wirel. Commun. Mob. Comput. 2021, 2021, 4840488. [Google Scholar] [CrossRef]

- Jahanshahi, H.; Shahriari-Kahkeshi, M.; Alcaraz, R.; Wang, X.; Singh, V.; Pham, V.T. Entropy analysis and neural network-based adaptive control of a non-equilibrium four-dimensional chaotic system with hidden attractors. Entropy 2019, 21, 156. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Alsulami, M.D. Computational mathematical techniques model for investment strategies. Appl. Math. Sci. 2021, 15, 47–55. [Google Scholar] [CrossRef]

- Chen, L.; Chen, G.R. Controlling chaos in an economic model. Phys. A Stat. Mech. Its Appl. 2007, 374, 349–358. [Google Scholar] [CrossRef]

- Wang, Y.L.; Ma, J.H.; Xu, Y.H. Finite-time chaos control of the chaotic financial system based on control Lyapunov function. Appl. Mech. Mater. 2011, 55–57, 203–208. [Google Scholar] [CrossRef]

- Zheng, S. Impulsive stabilization and synchronization of uncertain financial hyperchaotic systems. Kybernetika 2016, 52, 241–257. [Google Scholar] [CrossRef] [Green Version]

- Ahmad, I.; Ouannas, A.; Shafiq, M.; Pham, V.T.; Baleanu, D. Finite-time stabilization of a perturbed chaotic finance model. J. Adv. Res. 2021, 32, 1–14. [Google Scholar] [CrossRef]

- Zhao, X.S.; Li, Z.B.; Li, S. Synchronization of a chaotic finance system. Appl. Math. Comput. 2011, 217, 6031–6039. [Google Scholar] [CrossRef]

- Xu, Y.H.; Xie, C.R.; Wang, Y.L.; Zhou, W.N.; Fang, J.A. Chaos projective synchronization of the chaotic finance system with parameter switching perturbation and input time-varying delay. Math. Methods Appl. Sci. 2015, 38, 4279–4288. [Google Scholar] [CrossRef]

- Yousefpour, A.; Jahanshahi, H.; Munoz-Pacheco, J.M.; Bekiros, S.; Wei, Z.C. A fractional-order hyper-chaotic economic system with transient chaos. Chaos Solitons Fractals 2020, 130, 109400. [Google Scholar] [CrossRef]

- Yao, Q.J.; Jahanshahi, H.; Batrancea, L.M.; Alotaibi, N.D.; Rus, M.-I. Fixed-time output-constrained synchronization of unknown chaotic financial systems using neural learning. Mathematics 2022, 10, 3682. [Google Scholar] [CrossRef]

- He, Y.J.; Peng, J.; Zheng, S. Fractional-order financial system and fixed-time synchronization. Fractal Fract. 2022, 6, 507. [Google Scholar] [CrossRef]

- Li, X.G.; Rao, R.F.; Zhong, S.M.; Yang, X.S.; Li, H.; Zhang, Y.L. Impulsive control and synchronization for fractional-order hyper-chaotic financial system. Mathematics 2022, 10, 2737. [Google Scholar] [CrossRef]

- Yang, X.S.; Cao, J.D.; Yang, Z.C. Synchronization of coupled reaction-diffusion neural networks with time-varying delays via pinning-impulsive controller. SIAM J. Control. Optim. 2013, 51, 3486–3510. [Google Scholar] [CrossRef]

- Yang, X.S.; Lam, J.; Ho, D.W.C.; Feng, Z.G. Fixed-time synchronization of complex networks with impulsive effects via nonchattering control. IEEE Trans. Autom. Control 2017, 62, 5511–5521. [Google Scholar] [CrossRef]

- Hu, J.T.; Sui, G.X.; Li, X.D. Fixed-time synchronization of complex networks with time-varying delays. Chaos Solitons Fractals 2020, 140, 110216. [Google Scholar] [CrossRef]

- Wang, C.Q.; Zhao, X.Q.; Wang, Y. Finite-time stochastic synchronization of fuzzy bi-directional associative memory neural networks with Markovian switching and mixed time delays via intermittent quantized control. AIMS Math. 2023, 8, 4098–4125. [Google Scholar] [CrossRef]

- Pazy, A. Semigroups of Linear Operators and Applications to Partial Differential Equations, 2nd ed.; Springer: New York, NY, USA, 1983. [Google Scholar] [CrossRef]

- Arendt, W. Semigroups and evolution equations: Functional calculus, regularity and kernel estimates. In Handbook of Differential Equations: Evolutionary Equations; Dafermos, C.M., Feireisl, E., Eds.; Elsevier B.V.: Amsterdam, The Netherlands, 2002; pp. 1–85. [Google Scholar] [CrossRef]

- Evans, L. Partial Differential Equations, 2nd ed.; American Mathematical Society: Providence, RI, USA, 2010. [Google Scholar] [CrossRef] [Green Version]

- Polyakov, A. Nonlinear feedback design for fixed-time stabilization of linear control systems. IEEE Trans. Autom. Control 2012, 57, 2106–2110. [Google Scholar] [CrossRef]

- Bhat, S.; Bernstein, D. Finite-time stability of continuous autonomous systems. SIAM J. Control Optim. 2000, 38, 751–766. [Google Scholar] [CrossRef]

- Ye, H.P.; Gao, J.M.; Ding, Y.S. A generalized Gronwall inequality and its application to a fractional differential equation. J. Math. Anal. Appl. 2007, 328, 1075–1081. [Google Scholar] [CrossRef]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Wang, C.; Zhao, X.; Zhang, Y.; Lv, Z. Global Existence and Fixed-Time Synchronization of a Hyperchaotic Financial System Governed by Semi-Linear Parabolic Partial Differential Equations Equipped with the Homogeneous Neumann Boundary Condition. Entropy 2023, 25, 359. https://doi.org/10.3390/e25020359

Wang C, Zhao X, Zhang Y, Lv Z. Global Existence and Fixed-Time Synchronization of a Hyperchaotic Financial System Governed by Semi-Linear Parabolic Partial Differential Equations Equipped with the Homogeneous Neumann Boundary Condition. Entropy. 2023; 25(2):359. https://doi.org/10.3390/e25020359

Chicago/Turabian StyleWang, Chengqiang, Xiangqing Zhao, Yulin Zhang, and Zhiwei Lv. 2023. "Global Existence and Fixed-Time Synchronization of a Hyperchaotic Financial System Governed by Semi-Linear Parabolic Partial Differential Equations Equipped with the Homogeneous Neumann Boundary Condition" Entropy 25, no. 2: 359. https://doi.org/10.3390/e25020359