Project Risk in the Context of Construction Schedules—Combined Monte Carlo Simulation and Time at Risk (TaR) Approach: Insights from the Fort Bema Housing Estate Complex

Abstract

:1. Introduction

2. Literature Review

3. Materials and Methods

3.1. Fort Bema Housing Estate Complex (Parkowo-Leśne Housing Estate)

3.2. Construction Process Model and Time Schedules

3.3. Research Method

3.3.1. Relationships between Individual Stages of the Project

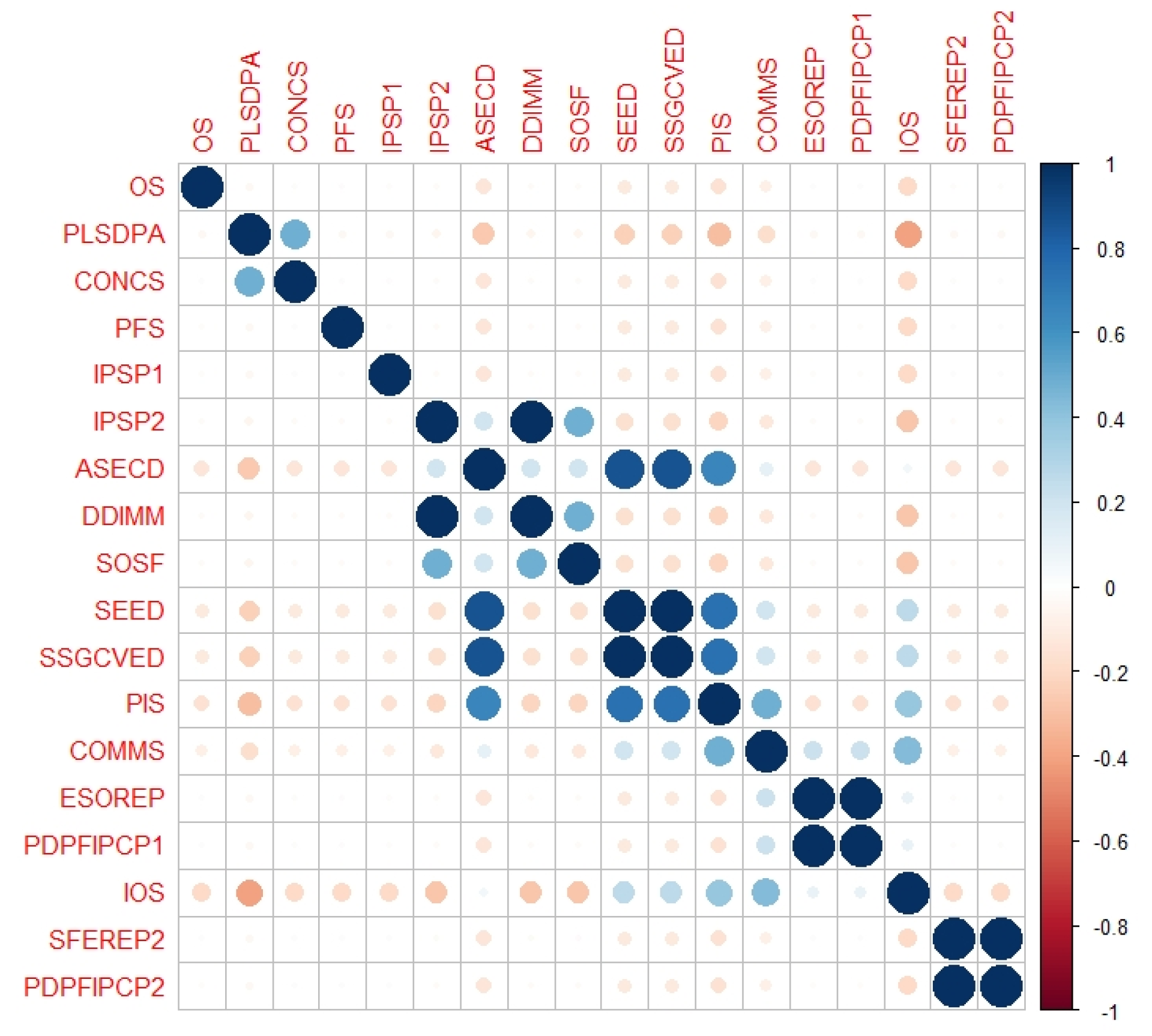

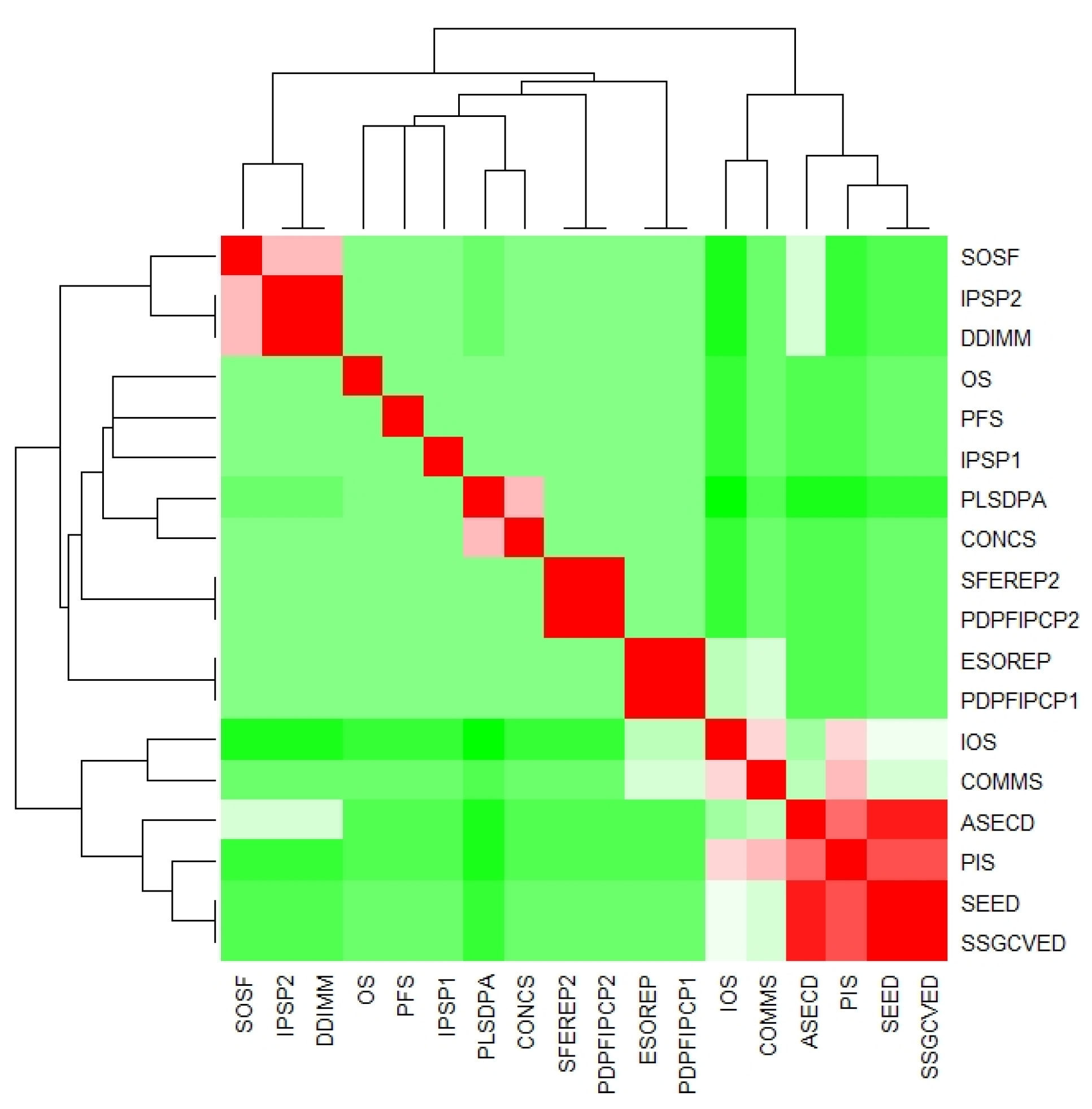

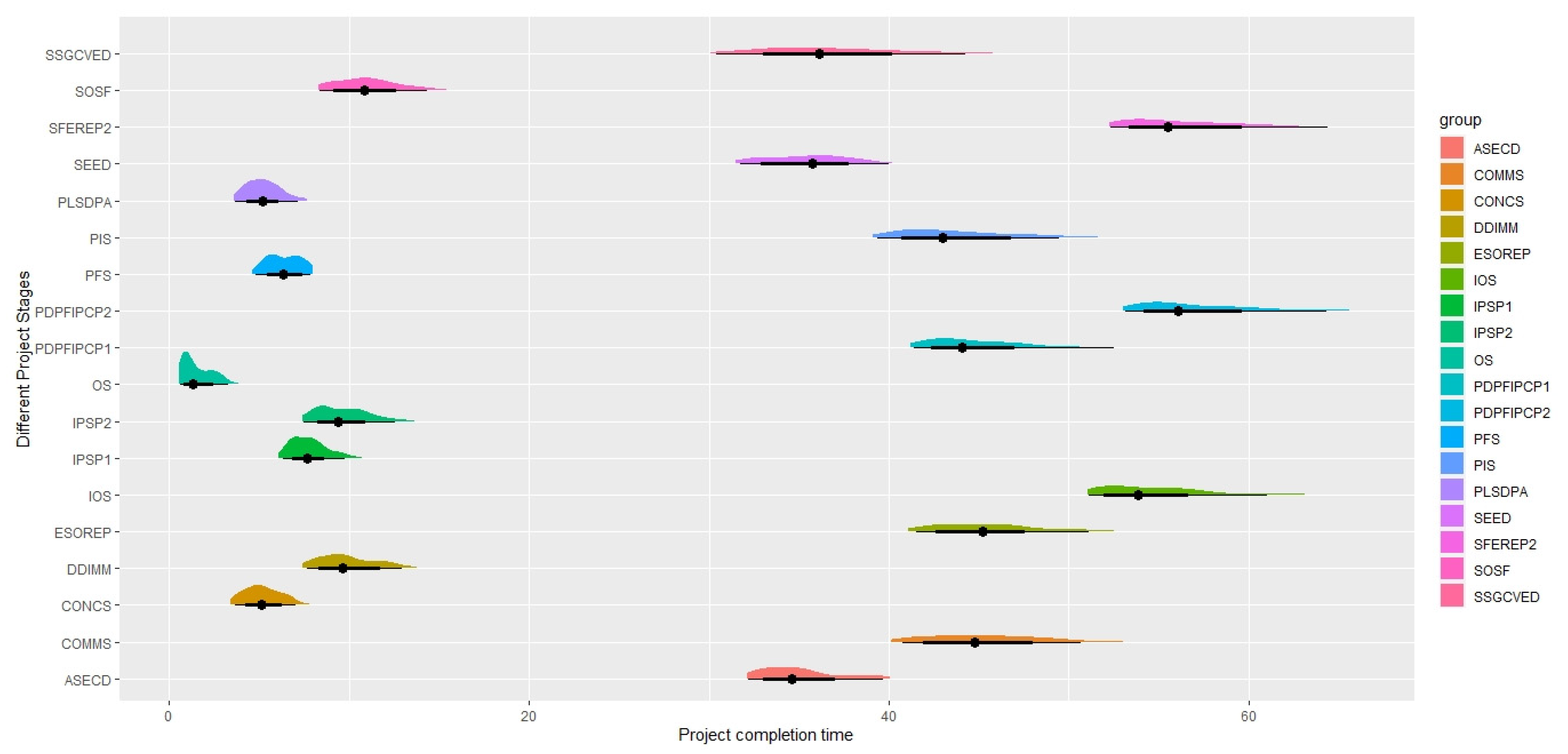

3.3.2. Correlation Matrix

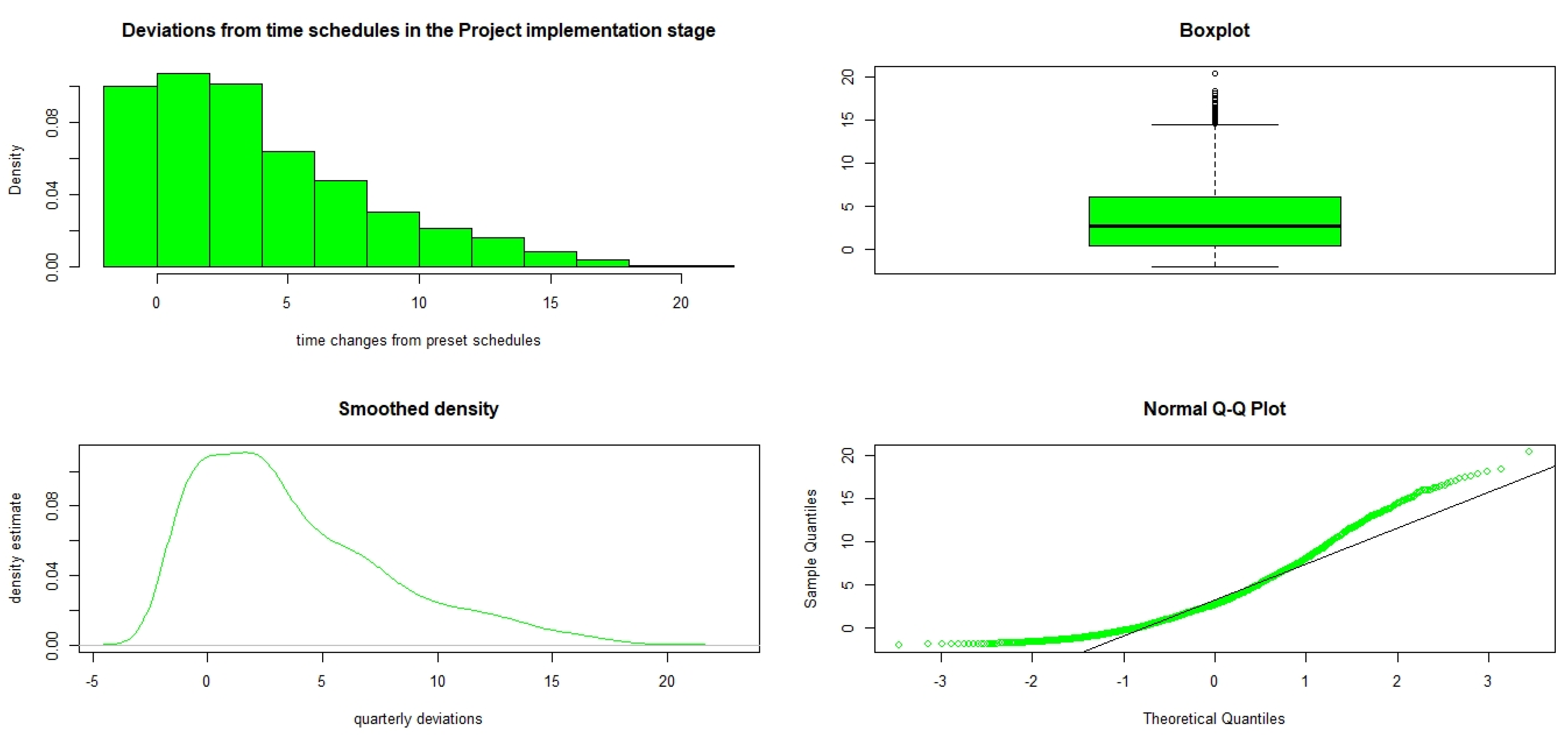

3.3.3. Time-at-Risk (TaR) and Monte Carlo Simulation

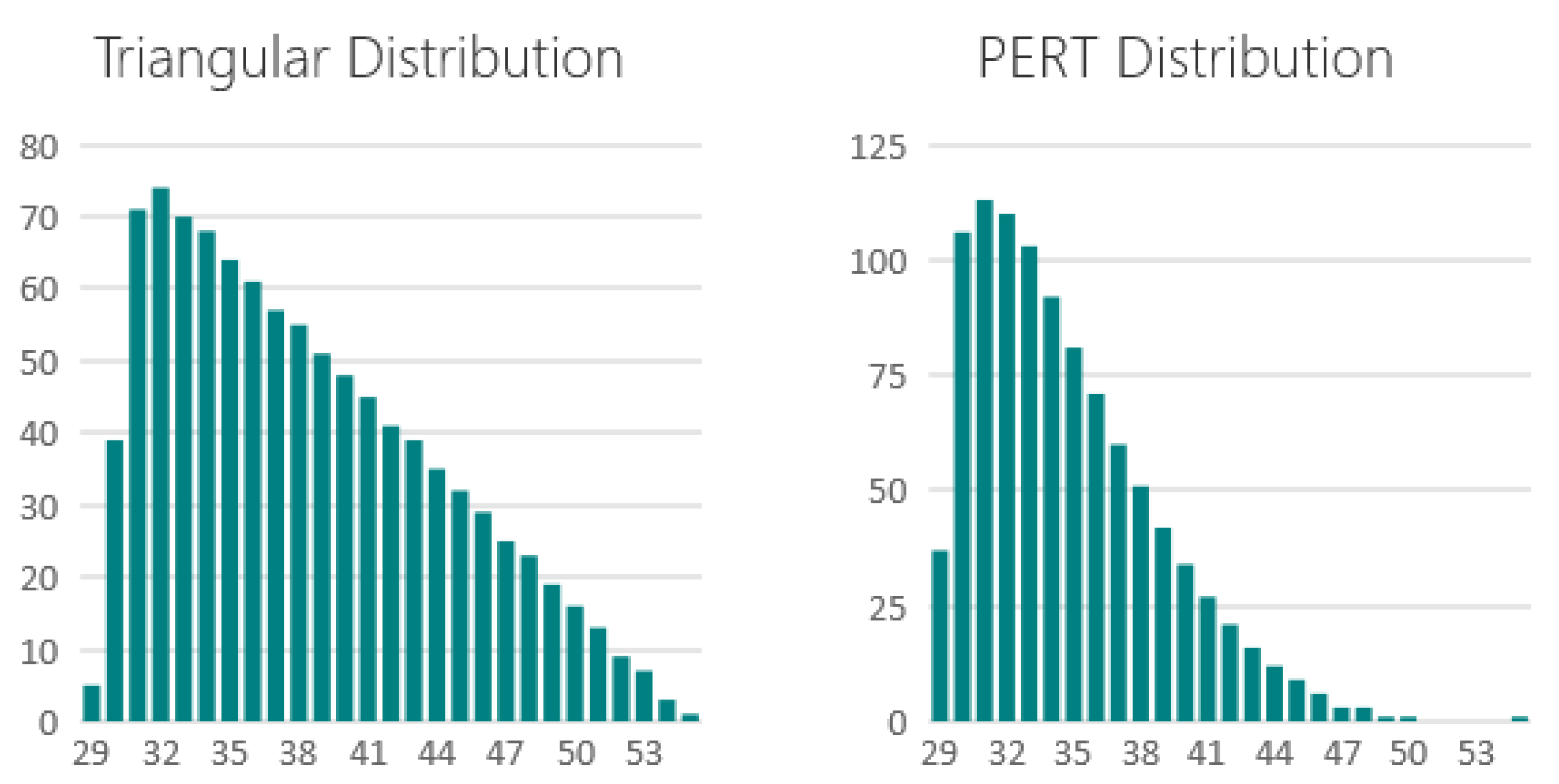

- Time deviations from the expected project stages’ completion times, simulated with different type of a distribution, e.g., PERT, triangular or Weibull.

- Covariance matrix reflecting the relationship between different project stages.

- Monte Carlo simulation with a certain number of repetitions (e.g., 10,000).

- A given confidence level of , and quantile of the distribution, for which the TaR value is determined.

4. Results

5. Discussion

6. Conclusions

7. Patents

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

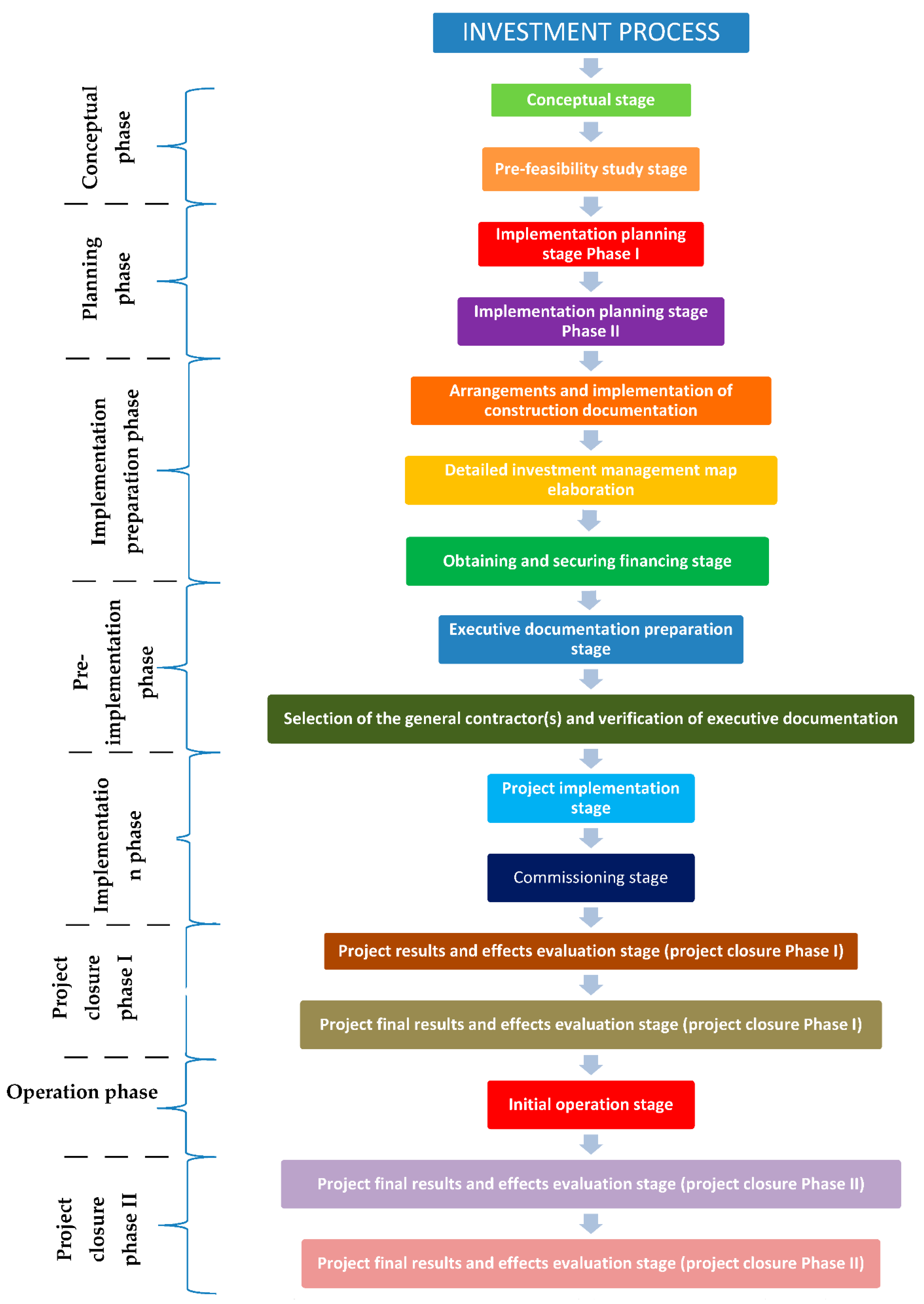

| Phases/Stages of the Investment Project | Description | Cited by Authors |

|---|---|---|

| Opportunity study | First, an investment opportunity study and a preliminary economic assessment must be carried out, considering various investment opportunities and project proposals, which will then be pursued in further steps. An opportunity study is carried out at the earliest stage of a project. The scope of the study includes an initial exploration of a project idea or identification of opportunities. Project ideas in a specific region, for a specific industry or based on available raw materials are explored. | Behrens and Hawranek [101]; Armaneri [102]; Tamošiūnienė and Angelov [103]. |

| Participation in local spatial development plan approvals | As part of this stage, the possibilities of preparing, approving and adopting a local spatial development plan are examined. It is considered that the adoption of a local spatial development plan should be the starting point for further investment activities. The next step is to elaborate a number of urban and architectural concepts, preliminary conceptual studies, as well as provisional, alternative media requirements for the entire area and for individual investment tasks. | Leśniak et al. [104]; Sobieraj [9,10,48] |

| Conceptual stage | The conceptual stage is about conceptualising and institutionalising the project’s design processes. It boils down to the following activities:

| Tizani [105]; Biliński [45]; Obolewicz [46], Sobieraj [9,10] |

| Pre-feasibility study | For each project, a pre-feasibility study must be carried out specifying how the project will be implemented, which allows the selection of the final version of the project. The study ends with the formulation of the final version of the project feasibility study, covering all technical, economic, commercial and financial aspects of the investment process. The final version of the project (feasibility study) is then submitted to banks, potential foreign contractors, developers and investors to assure them of the future success and expediency of the intended project. When acquiring the information necessary to prepare both the feasibility study and the prefeasibility study, particular attention should be paid to its reliability, timeliness, completeness and usefulness. At this stage the experience and assistance of the most reputable experts is used, relying on their specialist knowledge. Therefore, in this phase of the investment process, the following activities should be carried out:

| Escobar-García et al. [106]; Sobieraj [48]; Kim et al. [107] |

| Implementation planning stage—phase I | Investment planning is such an important element of each investment process that mistakes made at this stage/phase determine the final project costs (those that will be known retrospectively when the project is completed) to a greater extent than those made during project implementation [45,46]. Therefore, each project should include a separate planning phase, preferably consisting of two stages, each of which should integrate a number of different activities that significantly facilitate the implementation of the preparation phase, followed by the pre-implementation, implementation and investment closure phases [9,10]. The implementation planning stage (phase I) entails:

| Biliński [45]; Ebi [108] Obolewicz [46]; Sobieraj [9,10,48] |

| Implementation planning stage—phase II | The implementation planning stage (phase II) entails:

| Biliński [45]; Obolewicz [46]; Sobieraj [9,10,48] |

| Arrangements stage and execution of construction documentation | In the realisation of every project, a strong emphasis should be placed on the design and execution of construction documentation including a description, calculations and construction drawings [9,109]. The list of individual tasks to be completed during this stage is as follows:

| Elnagar and Yates [98]; Roy et al. [110]; Adriańczyk [109]; Levy [111]; Sobieraj [9,10] |

| Developing a detailed investment management map | The list of individual tasks to be completed during this stage is as follows:

| Yakura [55]; Kim et al. [112]; Maya [113]; Houston [114]; Sobieraj [9,10] |

| Obtaining and securing financing (feasibility study) | The obtaining and securing financing stage entails:

| Strzelecka et al. [81]; Sobieraj [48] |

| Executing executive documentation |

| Biliński [45]; Sobieraj [9,10] |

| Selecting of general contractor(s) and verification of executive documentation | This stage involves:

| Sobieraj [9,10] |

| Project implementation stage | At this stage, the efficiency of project (contract) management directly influences the smooth implementation of each objective [115,116]. Project implementation stage includes:

| Zhao-xia [115]; Yan and Chen [116]; Sobieraj [9,10] |

| Commissioning stage | Many projects go well until they enter the commissioning phase and then even comparatively minor problems can cause a disproportionate amount of trouble and delay [117]. This stage involves the following steps:

| Barnes [118]; Covey et al. [117]; Połoński [82]; Baryłka and Baryłka [83]; Sobieraj [9,10] |

| Evaluation stage of obtaining results and effects of the project (1st phase of project closing) | This stage addresses the following activities:

| Trocki and Wyrozębski [119]; Sobieraj [9,10] |

| Phase of drawing up proposals for future implementation after Project Closure Phase I | This project closure (Phase I) involves:

| Trocki and Wyrozębski [119]; Sobieraj [9,10] |

| Initial operation stage (usually 3 years of warranty and guarantee) | The initial operation stage requires:

| Biliński [45]; Zabielski [79]; Grzywiński [78]; Sobieraj [9,10] |

| The stage of final evaluation of the results and effects of the project (II stage of project closing) | This stage involves the following activities:

| Trocki and Wyrozębski [119]; Sobieraj [9,10] |

| Phase of drawing up proposals for future implementation after Phase II of the project closure | This stage involves:

| Trocki and Wyrozębski [119]; Sobieraj [9,10] |

| Method | Descriptions | Authors |

|---|---|---|

| Critical Path Method (CPM) | The planning method most commonly used in large construction projects is the critical path method (CPM). CPM is based on the assumption that the completion of each activity depends on a few critical resources or constraints. Because of the critical importance of boundary conditions, project managers study CPM as part of their project management certification (PMP). For this reason, it is also the legal standard for measuring delays when project-related disputes arise. CPM creates a graphical view of a project and calculates how much time and resources are needed to complete each activity. It also determines the critical activities that need attention to ensure the project is completed on time. | Yamin and Harmelink [11]; East [12]; Galloway [120] |

| Program Evaluation and Review Technique (PERT) | PERT is one of the most accessible tools for building design and scheduling. It provides a visual representation of the key project activities and the order in which they must be completed. Each of these steps represents the commitment of time or resources. The diagram can be thought of as a roadmap for the completion of the project; only when all milestones have been reached has the building project reached its final phase. PERT Diagrams are often built from back to front, as many projects have a pre-determined deadline, but contractors have some flexibility in the early phases and stages of the project [9,10]. | Kirytopoulos et al. [93]; Liu [121]; Sobieraj [9,10]; Galloway [120] |

| Critical Chain Project Management (CCPM) | Critical Chain Project Management (CCPM) was developed by Goldratt [122]. This method emphasises the appropriate use of resources required to complete project tasks, i.e., people, equipment and physical space. In contrast to more traditional methods such as CPM or PERT (which take into account task sequencing and rigid scheduling), the CCPM method relies on resource alignment, which of course involves some flexibility in their allocation (as well as in start times). In other words, the appropriate use of resources plays a key role in the CCPM method. With the critical chain method (CCM), one can perform an analysis of the scheduling network, addressing dependencies between tasks, resource availability and appropriate buffers. Thus, the CCM allows for better (more efficient) planning (scheduling) when the execution of project tasks is accompanied by some uncertainty related to resource management, namely to their availability or constraints. | Goldratt [122] |

| Line of Balance (LOB) | LOB is a construction scheduling tool that relies on thoughtful planning of projects through repeated iterations. It is a management control process where the project contains blocks of repetitive work activities. LOB collects, measures and presents information in terms of time, cost and completion and compares it to a specific plan. It helps identify where projects are going off track by identifying the specific moments when deviations occur. It reflects project objectives as a single line on a chart in terms of completed activities/time that teams are expected to adhere to in order to stay on track. | Arditi and Albulak [22]; Arditi et al. [24]; Soini et al. [26]; Tokdemir et al. [23]; Damci et al. [25] |

| Q Scheduling | Q Scheduling Quantitative scheduling is a planning approach that uses a bar chart to indicate the quantities of materials that will be used at different locations and times during the project. This type of scheduling allows companies to clearly see the amount and type of material needed at different times and places. It also includes a hierarchical component so that staff and managers can see what materials they need at what time, order them accordingly, carry out the activities/tasks in the right order and not disrupt the work of others—all while controlling costs. | Sulbaran and Ahmed [28]; Majumder et al. [27] |

| Resource Oriented Scheduling | Resource Oriented Scheduling method focuses on project resources, prioritising the most efficient use of those resources. As limited resources increase the likelihood of delays due to different teams fighting over them. Without a smart approach to determine who gets them and when, a construction company may be powerless to prioritise. A resource-driven schedule takes into account everyone who needs the resources in advance and then assigns them to an orderly use throughout the project. | Trimble [29]; Venkatesh et al. [30] |

| Last Planner System | The Last Planner system is a short-term collaborative planning process, and in this sense, it is not a typical construction scheduling tool compared to other techniques. Even though it is not a stand-alone tool, it can be used well with planning techniques such as CPM. LPS brings together those who will do the work (the team) to plan when and how the work will be done through a series of conversational processes. This allows teams to assess and remove likely obstacles in advance, promoting the timely completion of each task. | AlSehaimi et al. [31]; |

| Gantt Chart | A Gantt Chart is a type of bar chart that encourages stakeholders to structure the project with several levels of detail and consider dependencies between tasks [32]. Gant Charts help them estimate the duration of the project and identify the critical path to take during construction. A Gantt chart is a bar chart used to illustrate a project schedule, that includes some milestones, and it is not as detailed as a full CPM. It normally includes start/end dates of activities and a summary of activities of a project. However, it lacks the complexity of more comprehensive approaches and doesn’t include the resources or materials needed to complete it. Gantt Charts are excellent for creating a hierarchy among projects, showing which ones require immediate attention and which must be completed before other, dependent projects can follow. | Maylor [33]; Geraldi and Lechter [32]; |

References

- Poh, P.; Lam, Y.M. Confidence based scheduling procedure (CBSP): A pragmatic approach to manage project schedule uncertainty. Int. J. Constr. Proj. Manag. 2014, 6, 119. [Google Scholar]

- Sobieraj, J.; Metelski, D. Identification of the key investment project management factors in the housing construction sector in Poland. Int. J. Constr. Manag. 2020, 1–12. [Google Scholar] [CrossRef]

- Sobieraj, J.; Metelski, D. Quantifying Critical Success Factors (CSFs) in Management of Investment-Construction Projects: Insights from Bayesian Model Averaging. Buildings 2021, 11, 360. [Google Scholar] [CrossRef]

- Pinto, J.K.; Slevin, D.P. Critical factors in successful project implementation. IEEE Trans. Eng. Manag. 1987, 34, 22–27. [Google Scholar] [CrossRef]

- Cleland, D.I.; King, W.R. Project Management Handbook, 3rd ed.; REI: New York, NY, USA, 1983. [Google Scholar]

- Sobieraj, J.; Metelski, D.; Nowak, P. The View of Construction Companies’ Managers on the Impact of Economic, Environmental and Legal Policies on Investment Process Management. Arch. Civ. Eng. 2021, 67, 111–129. [Google Scholar]

- Herroelen, W.; Leus, R. Project scheduling under uncertainty: Survey and research potentials. Eur. J. Oper. Res. 2005, 165, 289–306. [Google Scholar] [CrossRef] [Green Version]

- Bruni, M.E.; Beraldi, P.; Guerriero, F.; Pinto, E. A scheduling methodology for dealing with uncertainty in construction projects. Eng. Comput. 2011, 28, 1064–1078. [Google Scholar] [CrossRef]

- Sobieraj, J. Wpływ Polityki Gospodarczej, Srodowiskowej i Prawnej na Zarządzanie Procesem Inwestycyjnym w Budownictwie Przemysłowym; ITE-PIB: Radom, Poland, 2019. [Google Scholar]

- Sobieraj, J. Investment Project Management on the Housing Construction Market; Aurum Universitas Grupo Hespérides: Madrid, Spain, 2020. [Google Scholar]

- Yamin, R.A.; Harmelink, D.J. Comparison of linear scheduling model (LSM) and critical path method (CPM). J. Constr. Eng. Manag. 2001, 127, 374–381. [Google Scholar] [CrossRef] [Green Version]

- East, E. Critical Path Method (CPM) Tutor for Construction Planning and Scheduling; McGraw-Hill Education: New York, NY, USA, 2015. [Google Scholar]

- Mohamed, Y. A Framework for Systematic Improvement of Construction Systems. Ph.D. Thesis, University of Alberta, Edmonton, AB, Canada, 2002. [Google Scholar]

- Koskela, L. An Exploration Towards a Production Theory and Its Application to Construction; VTT Technical Research Centre of Finland: Espoo, Finland, 2000. [Google Scholar]

- Howell, G.; Ballard, G. Lean production theory: Moving beyond “Can-Do”. Lean Constr. 1997, 17–23. [Google Scholar]

- Kong, Z.; Zhang, J.; Li, C.; Zheng, X.; Guan, Q. Risk assessment of plan schedule by Monte Carlo simulation. In Proceedings of the 4th International Conference on Information Technology and Management Innovation (ICITMI), Shenzhen, China, 12–13 September 2015; pp. 509–513. [Google Scholar]

- Frein, J. Handbook of Construction Management and Organization; Springer Science & Business Media: Berlin, Germany, 2012. [Google Scholar]

- Hulett, D. Practical Schedule Risk Analysis; Routledge: London, UK, 2016. [Google Scholar]

- Ruogang, L.; Guoxiang, W.; Yue, L.; Jialin, R. Study on uncertainty of activity duration in PERT. Syst. Eng. Electron. 1997, 19, 40–45. [Google Scholar]

- Petroutsatou, K. A proposal of project management practices in public institutions through a comparative analyses of critical path method and critical chain. Int. J. Constr. Manag. 2019, 1–10. [Google Scholar] [CrossRef]

- Gonçalves-Dosantos, J.C.; García-Jurado, I.; Costa, J. ProjectManagement: An R Package for Managing Projects. R J. 2020, 12, 419–436. [Google Scholar] [CrossRef]

- Arditi, D.; Albulak, M.Z. Line-of-balance scheduling in pavement construction. J. Constr. Eng. Manag. 1986, 112, 411–424. [Google Scholar] [CrossRef]

- Tokdemir, O.B.; Erol, H.; Dikmen, I. Delay Risk Assessment of Repetitive Construction Projects Using Line-of-Balance Scheduling and Monte Carlo Simulation. J. Constr. Eng. Manag. 2019, 145, 1–19. [Google Scholar] [CrossRef]

- Arditi, D.; Tokdemir, O.B.; Suh, K. Challenges in line-of-balance scheduling. J. Constr. Eng. Manag. 2002, 128, 545–556. [Google Scholar] [CrossRef]

- Damci, A.; Arditi, D.; Polat, G. Resource leveling in line-of-balance scheduling. Comput. -Aided Civ. Infrastruct. Eng. 2013, 28, 679–692. [Google Scholar] [CrossRef]

- Soini, M.; Leskelä, I.; Seppänen, O. Implementation of line-of-balance based scheduling and project control system in a large construction company. In Proceedings of the 12th Annual Conference of the International Group for Lean Construction, Helsingor, Denmark, 3–5 August 2004. [Google Scholar]

- Majumder, S.; Majumder, S.; Biswas, D. Impact of effective construction planning in project performance improvement. Qual. Quant. 2021, 1–12. [Google Scholar] [CrossRef]

- Sulbaran, T.; Ahmed, F. Expert System for Construction Scheduling Decision Support Based on Travelling Salesman Problem. In Proceedings of the 53rd ASC Annual International Conference Proceedings, Seattle, WA, USA, 5–8 April 2017. [Google Scholar]

- Trimble, G. Resource-oriented scheduling. Int. J. Proj. Manag. 1984, 2, 70–74. [Google Scholar] [CrossRef]

- Venkatesh, M.P.; Malathi, B.; Umarani, C. Factors Affecting Implementation of Resource Scheduling in Indian Construction Projects. Appl. Mech. Mater. 2012, 174, 2782–2786. [Google Scholar] [CrossRef]

- AlSehaimi, A.O.; Fazenda, P.T.; Koskela, L. Improving construction management practice with the Last Planner System: A case study. Eng. Constr. Archit. Manag. 2014, 21, 51–64. [Google Scholar] [CrossRef] [Green Version]

- Geraldi, J.; Lechter, T. Gantt charts revisited: A critical analysis of its roots and implications to the management of projects today. Int. J. Manag. Proj. Bus. 2012, 5, 578–594. [Google Scholar] [CrossRef]

- Maylor, H. Beyond the Gantt chart: Project management moving on. Eur. Manag. J. 2001, 19, 92–100. [Google Scholar] [CrossRef]

- Khodakarami, V.; Fenton, N.; Neil, M. Project Scheduling: Improved approach to incorporate uncertainty using Bayesian Networks. Proj. Manag. J. 2007, 38, 39–49. [Google Scholar] [CrossRef]

- Khodakarami, V.; Abdi, A. Project cost risk analysis: A Bayesian networks approach for modeling dependencies between cost items. Int. J. Proj. Manag. 2014, 32, 1233–1245. [Google Scholar] [CrossRef]

- Gondia, A.; Siam, A.; El-Dakhakhni, W.; Nassar, A.H. Machine learning algorithms for construction projects delay risk prediction. J. Constr. Eng. Manag. 2020, 146, 04019085. [Google Scholar] [CrossRef]

- Kim, S.Y.; Van Tuan, N.; Ogunlana, S.O. Quantifying schedule risk in construction projects using Bayesian belief networks. Int. J. Proj. Manag. 2009, 27, 39–50. [Google Scholar]

- Anastasopoulos, P.C.; Labi, S.; Bhargava, A.; Mannering, F.L. Empirical assessment of the likelihood and duration of highway project time delays. J. Constr. Eng. Manag. 2012, 138, 390–398. [Google Scholar] [CrossRef]

- Azaron, A.; Ghomi, S.F. Lower bound for the mean project completion time in dynamic PERT networks. Eur. J. Oper. Res. 2008, 186, 120–127. [Google Scholar] [CrossRef]

- Sobieraj, J.; Metelski, D.; Mihi Ramírez, A. Pivotal project management factors in the context of polish residential construction projects. In Proceedings of the International Conference on Industry, Business and Social Sciences (IBSS), Osaka, Japan, 28–30 August 2019. [Google Scholar]

- Bolgorian, M.; Raei, R. A quantile-based Time at Risk: A new approach for assessing risk in financial markets. Phys. A Stat. Mech. Appl. 2013, 392, 5673–5677. [Google Scholar] [CrossRef]

- Kovalenko, T.; Sornette, D. Dynamical Diagnosis and Solutions for Resilient Natural and Social Systems. arXiv 2012, arXiv:1211.1949. [Google Scholar]

- Sobieraj, J.; Metelski, D.; Mihi Ramírez, A. The view of SME construction companies’ managers on the impact of economic, environmental and legal policies on investment process management. Case of Polish Companies. In In Proceedings of the XXVIII AEDEM International Conference, Tokyo, Japan, 3–4 September 2019; pp. 1046–1069. [Google Scholar]

- Cooper, K.G. The $2000 hour: How managers influence project performance through the rework cycle. Proj. Manag. J. 1994, 25, 11–24. [Google Scholar]

- Biliński, T. Struktura i uwarunkowania współczesnego procesu inwestycyjno-budowlanego. Przegląd Bud. 2010, 81, 46–52. [Google Scholar]

- Obolewicz, J. Koordynacja budowlanego procesu inwestycyjnego. Bud. I Inżynieria Sr. 2016, 7, 153–163. [Google Scholar]

- Laufer, A.; Howell, G.A. Construction Planning: Revising the Paradigm; Project Management Institute: Newtown Square, PA, USA, 1993. [Google Scholar]

- Sobieraj, J. Impact of spatial planning on the pre-investment phase of the development process in the residential construction field. Arch. Civ. Eng. 2017, 63, 113–130. [Google Scholar] [CrossRef] [Green Version]

- Project Management Institute. A Guide to the Project Management Body of Knowledge; Project Management Institute: Newtown Square, PA, USA, 2004. [Google Scholar]

- Basu, A. Practical Risk Analysis in Scheduling; AACE International Transactions: Morgantown, WV, USA, 1998. [Google Scholar]

- Rubinstein, R.Y.; Kroese, D.P. Simulation and the Monte Carlo Method; John Wiley & Sons: New York, NY, USA, 2016. [Google Scholar]

- Sarma, M.; Thomas, S.; Shah, A. Selection of Value-at-Risk models. J. Forecast. 2003, 22, 337–358. [Google Scholar] [CrossRef]

- Lindkvist, L.; Soderlund, J. Managing product development projects: On the significance of fountains and deadlines. Organ. Stud. 1998, 19, 931–951. [Google Scholar] [CrossRef] [Green Version]

- Dille, T.; Söderlund, J. Managing inter-institutional projects: The significance of isochronism, timing norms and temporal misfits. Int. J. Proj. Manag. 2011, 29, 480–490. [Google Scholar] [CrossRef]

- Yakura, E.K. Charting time: Timelines as temporal boundary objects. Acad. Manag. J. 2002, 45, 956–970. [Google Scholar]

- Vaughan, D. The Challenger Launch Decision: Risky Technology, Culture, and Deviance at Nasa; University of Chicago Press: Chicago, IL, USA, 1996. [Google Scholar]

- Sobieraj, J. Review of Knowledge on Strategy Development, Strategic Management and Strategic Analysis; Wydawnictwo ITEE: Radom, Poland, 2017. [Google Scholar]

- Jugdev, K.; Müller, R. A retrospective look at our evolving understanding of project success. Proj. Manag. J. 2005, 36, 19–31. [Google Scholar] [CrossRef]

- Flyvbjerg, B.; Garbuio, M.; Lovallo, D. Delusion and deception in large infrastructure projects: Two models for explaining and preventing executive disaster. Calif. Manag. Rev. 2009, 51, 170–194. [Google Scholar] [CrossRef] [Green Version]

- Flyvbjerg, B.; Garbuio, M.; Lovallo, D. Delusion and deception in large infrastructure projects: Two models for explaining and preventing executive disaster. Def. AR J. 2017, 24, 583–585. [Google Scholar] [CrossRef] [Green Version]

- Beckers, F.; Chiara, N.; Flesch, A.; Maly, J.; Silva, E.; Stegemann, U. A risk-management approach to a successful infrastructure project. Mckinsey Work. Pap. Risk 2013, 52, 18. [Google Scholar]

- Bertsimas, D.; Sim, M. The price of robustness. Oper. Res. 2004, 52, 35–53. [Google Scholar] [CrossRef] [Green Version]

- Jaśkowski, P. Methodology for enhancing reliability of predictive project schedules in construction. Eksploat. I Niezawodn. 2015, 17, 470–479. [Google Scholar] [CrossRef]

- Al-Fawzan, M.A.; Haouari, M. A bi-objective model for robust resource-constrained project scheduling. Int. J. Prod. Econ. 2005, 96, 175–187. [Google Scholar] [CrossRef]

- Van de Vonder, S.; Demeulemeester, E.; Herroelen, W.; Leus, R. The use of buffers in project management: The trade-off between stability and makespan. Int. J. Prod. Econ. 2005, 97, 227–240. [Google Scholar] [CrossRef] [Green Version]

- Namazian, A.; Yakhchali, S.H.; Yousefi, V.; Tamošaitienė, J. Combining Monte Carlo simulation and Bayesian networks methods for assessing completion time of projects under risk. Int. J. Environ. Res. Public Health 2019, 16, 5024. [Google Scholar] [CrossRef] [Green Version]

- Fitzsimmons, J.; Hong, Y.; Brilakis, I. Improving Construction Project Schedules before Execution. In Proceedings of the 37th International Symposium on Automation and Robotics in Construction (ISARC), Aarhus, Denmark, 27–28 October 2020. [Google Scholar]

- Ökmen, Ö.; Öztaş, A. Construction project network evaluation with correlated schedule risk analysis model. J. Constr. Eng. Manag. 2008, 134, 49–63. [Google Scholar] [CrossRef]

- Levin, J. Relational incentive contracts. Am. Econ. Rev. 2003, 93, 835–857. [Google Scholar] [CrossRef] [Green Version]

- Mitkus, S.; Mitkus, T. Causes of conflicts in a construction industry: A communicational approach. Procedia-Soc. Behav. Sci. 2014, 110, 777–786. [Google Scholar] [CrossRef] [Green Version]

- Kaming, P.F.; Olomolaiye, P.O.; Holt, G.D.; Harris, F.C. Factors influencing construction time and cost overruns on high-rise projects in Indonesia. Constr. Manag. Econ. 1997, 15, 83–94. [Google Scholar] [CrossRef]

- Moselhi, O.; Gong, D.; El-Rayes, K. Estimating weather impact on the duration of construction activities. Can. J. Civ. Eng. 1997, 24, 359–366. [Google Scholar] [CrossRef]

- Honek, K.; Azar, E.; Menassa, C.C. Recession effects in United States public sector construction contracting: Focus on the American Recovery and Reinvestment Act of 2009. J. Manag. Eng. 2012, 28, 354–361. [Google Scholar] [CrossRef]

- Bragadin, M.A.; Kähkönen, K. Safety, space and structure quality requirements in construction scheduling. Procedia Econ. Financ. 2015, 21, 407–414. [Google Scholar] [CrossRef] [Green Version]

- ElZomor, M.; Burke, R.; Parrish, K.; Gibson, G.E., Jr. Front-end planning for large and small infrastructure projects: Comparison of project definition rating index tools. J. Manag. Eng. 2018, 34, 04018022. [Google Scholar] [CrossRef]

- Ortiz-González, J.I.; Pellicer, E.; Howell, G. Contingency management in construction projects: A survey of Spanish contractors. In Proceedings of the IGLC-22, Oslo, Norway, 25–27 June 2014; pp. 195–206. [Google Scholar]

- Mubarak, S.A. Construction Project Scheduling and Control; John Wiley & Sons: Hoboken, NJ, USA, 2015. [Google Scholar]

- Grzywiński, J. Proces Inwestycyjny Zgodnie z Polskim Prawem Budowlanym; Wyd. Kancelarii Furtek Komosa Aleksandrowicz: Warsaw, Poland, 2015. [Google Scholar]

- Zabielski, J. Proces Inwestycyjno-Budowlany. Materiały Dydaktyczne Wydziału Prawa i Administracji UW; Wyd. CRE Edukacja: Warsaw, Poland, 2014. [Google Scholar]

- Dzierżewicz, Z.; Dylewski, J. Proces Budowlany w Świetle Ustawy Prawo Budowlane; Wyd. Grupa APEXnet: Lublin, Poland, 2011. [Google Scholar]

- Strzelecka, E.; Glinkowska, B.; Maciejewska, M.; Wiażel-Sasin, B. Zarządzanie Przedsięwzięciami Budowlanymi. Podstawy, Procedury, Przykłady; Wyd. Politechniki Łódzkiej: Łódź, Poland, 2014. [Google Scholar]

- Połoński, M. Kierowanie Budowlanym Procesem Inwestycyjnym; Wyd. SGGW: Warsaw, Poland, 2009. [Google Scholar]

- Baryłka, A.; Baryłka, J. Funkcje Techniczne w Budownictwie. Przewodnik Po Inwestycyjnym i Eksploatacyjnym Procesie Budowlanym; Polcen: Warsaw, Poland, 2015. [Google Scholar]

- Liu, Y.; Li, Y. Risk management of construction schedule by PERT with Monte Carlo simulation. Appl. Mech. Mater. 2014, 548, 1646–1650. [Google Scholar] [CrossRef]

- Hendradewa, A.P. Schedule Risk Analysis by Different Phases of Construction Project Using CPM-PERT and Monte-Carlo Simulation. In Proceedings of the 11th International Seminar on Industrial Engineering & Management (ISIEM), Technology and Innovation Challenges towards Industry 4.0 Era, Makasar, Indonesia, 27–29 November 2018. [Google Scholar]

- Abdelkader, Y.H. Evaluating project completion times when activity times are Weibull distributed. Eur. J. Oper. Res. 2004, 157, 704–715. [Google Scholar] [CrossRef]

- Clark, C.E. Letter to the editor—The PERT model for the distribution of an activity time. Oper. Res. 1962, 10, 405–406. [Google Scholar] [CrossRef] [Green Version]

- Johnson, N.L.; Kotz, S.; Balakrishnan, N. Continuous Univariate Distributions; John Wiley & Sons: New York, NY, USA, 1995. [Google Scholar]

- Kay, M. ggdist: Visualizations of Distributions and Uncertainty. R Package Version 3.0.1. Available online: https://mjskay.github.io/ggdist/ (accessed on 18 January 2022).

- Vose, D. Risk Analysis: A Quantitative Guide; John Wiley & Sons: New York, NY, USA, 2008. [Google Scholar]

- Buchsbaum, P. Modified PERT Simulation; Great Solutions: Rio de Janeiro, Brazil, 2012. [Google Scholar]

- Barraza, G.A.; Bueno, R.A. Probabilistic control of project performance using control limit curves. J. Constr. Eng. Manag. 2007, 133, 957–965. [Google Scholar] [CrossRef]

- Kirytopoulos, K.A.; Leopoulos, V.N.; Diamantas, V.K. PERT vs. Monte Carlo Simulation along with the suitable distribution effect. Int. J. Proj. Organ. Manag. 2008, 1, 24–46. [Google Scholar] [CrossRef]

- Vanhoucke, M. Measuring the efficiency of project control using fictitious and empirical project data. Int. J. Proj. Manag. 2012, 30, 252–263. [Google Scholar] [CrossRef]

- Koulinas, G.K.; Xanthopoulos, A.S.; Tsilipiras, T.T.; Koulouriotis, D.E. Schedule delay risk analysis in construction projects with a simulation-based expert system. Buildings 2020, 10, 134. [Google Scholar] [CrossRef]

- Rumelt, R.P. Good Strategy/Bad Strategy: The Difference and Why It Matters. Strateg. Dir. 2012, 28, 8. [Google Scholar] [CrossRef]

- Metelski, D.; Mihi-Ramirez, A.; Arteaga-Ortiz, J. Research and development projects upon real options view. Eng. Econ. 2014, 25, 283–293. [Google Scholar] [CrossRef]

- Elnagar, H.; Yates, J.K. Construction documentation used as indicators of delays. Cost Eng. 1997, 39, 31. [Google Scholar]

- Sobieraj, J.; Metelski, D.; Nowak, P. PMBoK vs. PRINCE2 in the context of Polish construction projects: Structural Equation Modelling approach. Arch. Civil Eng. 2021, 67, 551–579. [Google Scholar]

- Kapliński, O.; Dziadosz, A.; Zioberski, J.L. Próba standaryzacji procesu zarządzania na etapie planowania i realizacji przedsięwzięć budowlanych. Zesz. Nauk. Politech. Rzesz. Bud. I Inżynieria Sr. 2011, 58, 11. [Google Scholar]

- Behrens, W.; Hawranek, P.M. Manual for the Preparation of Industrial Feasibility Studies; United Nations Industrial Development Organization: Vienna, Austria, 1991; pp. 176–181. [Google Scholar]

- Armaneri, Ö. An Integrated Multi-Criteria Decision Making Methodology for Risky Investment Projects Evaluation. Ph.D. Thesis, DEÜ Fen Bilimleri Enstitüsü, Buca/İZMİR, Turkey, 2009. [Google Scholar]

- Tamošiūnienė, R.; Angelov, K. Project and Programme Management and Evaluation; Publishing House of Technical University–Sofia: Sofia, Bulgraria, 2011. [Google Scholar]

- Leśniak, A.; Plebankiewicz, E.; Kozik, R.; Amanowicz-Marcinkowska, K. Impact of the current local spatial development plans on the activity of investor on the Polish residential real estate market. Earth Environ. Sci. 2021, 656, 012004. [Google Scholar] [CrossRef]

- Tizani, W. Collaborative Design in Virtual Environments at Conceptual Stage. In Collaborative Design in Virtual Environments, 2nd ed.; Wang, X., Tsai, J., Eds.; Springer: Dordrecht, The Netherlands, 2011; pp. 67–76. [Google Scholar]

- Escobar-García, D.A.; Younes-Velosa, C.; Moncada-Aristizábal, C.A. Application of a prefeasibility study methodology in the selection of road infrastructure projects: The case of Manizales (Colombia). Dyna 2015, 82, 204–213. [Google Scholar] [CrossRef]

- Kim, H.Y.; Shin, Y.H.; An, J.H.; Vinh, B.T.; Dung, T.Q. Prefeasibility Study on the Construction and the Operation of the Underground Cold Storage in Lam Dong Province, Vietnam. Tunn. Undergr. Space 2021, 31, 184–197. [Google Scholar]

- Ebi, U. Implementation of projects in the housing sector: A view of world bank assisted low income housing project in Aba and umuahia in retrospect. Sch. J. Sci. Res. Essay 2015, 6, 90–95. [Google Scholar]

- Adriańczyk, A.K. The Project Fire Water Storage Tank with a Capacity of 6000 m3. Ph.D. Thesis, Insitute of Civil Engineering, Warsaw University of Technology, Warsaw, Poland, 2016. [Google Scholar]

- Roy, R.; Low, M.; Waller, J. Documentation, standardization and improvement of the construction process in house building. Constr. Manag. Econ. 2005, 23, 57–67. [Google Scholar] [CrossRef]

- Levy, S.M. Project Management in Construction; McGraw-Hill Education: New York, NY, USA, 2018. [Google Scholar]

- Kim, N.; Park, M.; Lee, H.S.; Roh, S. Performance management method for construction companies. In Proceedings of the 24th International Symposium on Automation and Robotics in Construction Companies, Kochi, India, 19–21 September 2007; pp. 523–529. [Google Scholar]

- Maya, R.A. Performance management for Syrian construction projects. Int. J. Constr. Eng. Manag. 2016, 5, 65–78. [Google Scholar]

- Houston, D.A. Knowledge Management and Positive Deviance: A Study of Construction Project Outcomes. Ph.D. Thesis, Capella University, Minneapolis, MN, USA, 2019. [Google Scholar]

- Zhao-xia, M.A. Research on Contract Management in Project Implementation Stage. Nonferrous Met. Des. 2010, 2, 70–77. [Google Scholar]

- Yan, W.Z.; Chen, P. Based on the System Dynamics construction phase of the project cost control Study. Appl. Mech. Mater. 2014, 501, 2691–2694. [Google Scholar] [CrossRef]

- Covey, G.; Shore, D.; Harvey, R.; Faber, G. Preparing for commissioning. Appita Technol. Innov. Manuf. Environ. 2011, 64, 314–322. [Google Scholar]

- Barnes, M. Construction project management. Int. J. Proj. Manag. 1988, 6, 69–79. [Google Scholar] [CrossRef]

- Trocki, M.; Wyrozębski, P. Planowanie Przebiegu Projektów; Oficyna Wydawnicza SGH: Warsaw, Poland, 2015. [Google Scholar]

- Galloway, P.D. Survey of the construction industry relative to the use of CPM scheduling for construction projects. J. Constr. Eng. Manag. 2006, 132, 697–711. [Google Scholar] [CrossRef]

- Liu, M. Program evaluation and review technique (PERT) in construction risk analysis. Appl. Mech. Mater. 2013, 357, 2334–2337. [Google Scholar] [CrossRef]

- Goldratt, E.M. Critical Chain; The North River Press: Great Barrington, MA, USA, 1997. [Google Scholar]

| Method | Authors | Contribution |

|---|---|---|

| Naïve Bayesian; machine learning models; decision tree and naive Bayesian classification algorithms | Gondia [36] | Machine learning models facilitate accurate analysis and prediction of project delay risks (time overruns). In the case of Gondia’s [36] study, the evaluation results show that the naïve Bayesian model provides better predictive performance for the data studied. |

| Bayesian networks | Khodakarami et al. [34]; Khodakarami and Abdi [35] | Khodakarami et al. [34] used Bayesian network modelling for project scheduling. They reflect the causal relationship between these sources of uncertainty and project parameters. This method has the advantage (over other methods) of considering both uncertainty and causality. Khodakarami and Abdi [35] studied project-related uncertainties by modelling different factors affecting project performance. In their study, they quantified different types of uncertainty by relying on a modelling method for complex project dependencies such as common causal factors, formal use of expert opinion, and learning from data to update prior beliefs and probabilities. |

| Bayesian Belief Network (BBNs) | Kim et al. [37] | Kim et al. [37] used BBNs as a tool for predicting the probability of schedule delays. It is a method that offers great flexibility in accepting inputs and providing outputs. In addition, BBNs have the ability to treat the value of a variable as a known input or to evaluate its probability as an output of the system. It is a very useful technique for calculating the probability of events before and after the entry of evidence and for making predictions with the use of expert opinions (BBNs do not necessarily require historical data). Kim et al. [37] quantified the probability of delays in construction projects using Bayesian belief networks. The top main causes of changes in time schedule construction projects turned out to be the owner’s financial difficulties, inadequate experience and financial difficulties of contractors, shortage of materials, slow site handover, inappropriate construction methods, defective works and reworks and a lack of management capacity by owners/project managers. |

| Logistic regression | Anastasopoulos et al. [38] | The probability of a project having a time delay can be modelled as a binary outcome variable (1 if there was a time delay and 0 otherwise). Statistical approaches for such a model include the standard probit and logit models. To investigate the probability of a project delay, Anastasopoulos et al. [38] used a binary logit model with random parameters. The results of the model estimation show that the probability and duration of project delays are significantly influenced by factors such as project cost (bid amount), project type, planned project duration and the probability of bad weather. |

| Combination of Bayesian networks, support vector machines and Monte Carlo simulation to simulate project outcomes | Fitzsimmons et al. [67] | To improve the performance of critical path (pre-project) activity scheduling, Fitzsimmons et al. [67] proposed a method that integrates Bayesian networks to estimate the conditional delay probability of an activity based on its predecessor. It yields much better results than the traditional Monte Carlo simulations (by 52%). The Fitzsimmons et al. [67] method relies on data that originates from 302 completed infrastructure construction projects; Fitzsimmons et al.’s [67] model was appropriately trained/calibrated and validated on a large infrastructure road construction project. It works well in predicting project delays. |

| Monte Carlo simulation and Bayesian network | Namazian et al. [66] | Namazian et al. [66] brought together the Bayesian network and Monte Carlo simulation methods and presented the timing of a construction project in the context of a framework for assessing the overall impact of risks in such a project. |

| Confidence based scheduling procedure (CBSP) | Poh and Lam [1] | Poh and Lam [1] propose a method to determine the probability distribution of project completion times by estimating the duration of individual tasks/activities using confidence-based estimation. |

| Robustness | Bertsimas and Sim [62]; Al-Fawzan and Haouari [64]; Van de Vonder et al. [65]; Jaśkowski [63] | As one of the methods, Van de Vonder et al. [65] presented robustness, and more precisely, proactive heuristic methods for robust project scheduling. According to Al-Fawzan and Haouari [64], robustness of a schedule means that its validity is maintained despite small changes in the duration of processes (activities) and these changes are due to risks. The development of robust methods is described by Bertsimas and Sim [62]. Predictive scheduling with a proactive approach is about creating schedules that are robust to disturbances (hence the name—robust schedules). |

| Markov Dynamic PERT Model | Azaron and Ghomi [39] | Refinement of project time duration uncertainty bounds; this approach estimates the influence of factors such as war, strikes and inflation that make activity durations non-static over time. This is an untested model, but it combines externalities, deterministic CPM, PERT and correlation in an interesting way. |

| Correlated Schedule Risk Analysis Model (CSRAM) | Ökmen and Öztaş [68] | CSRAM accounts for covariance and correlation effects with PERT and CPM; it uses simple subjective inputs for a number of project risks, including weather factors, soil conditions, labour productivity and material/resource availability. However, CSRAM does not address the key problem of subjectivity and opinion-based analysis, a factor commonly associated with contract disputes [69,70]. Furthermore, there is a lack of empirical evidence that this technique is scalable and works across different types of projects. |

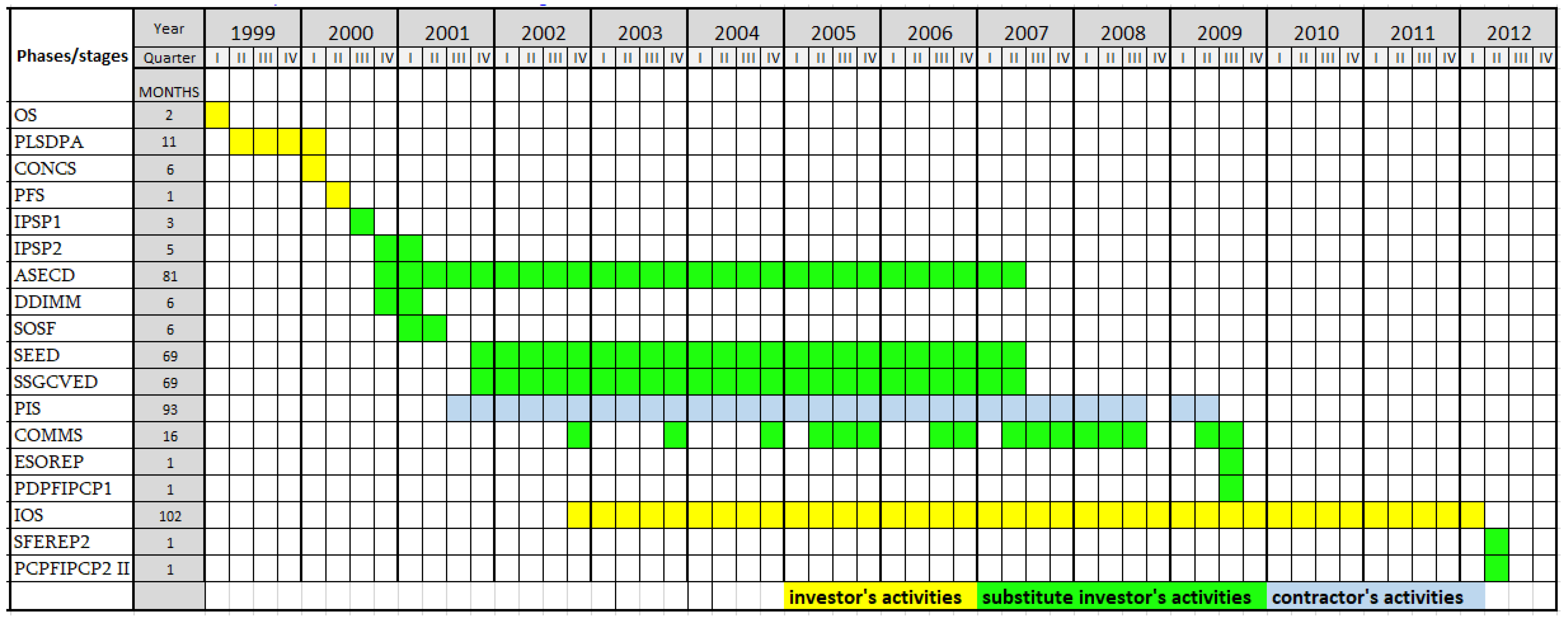

| Activities/Phases/Stages | Abbreviation | Execution Time in Months |

|---|---|---|

| Opportunity study | OS | 2 |

| Participation in local spatial development plan approvals | PLSDPA | 11 |

| Conceptual stage | CONCS | 6 |

| Pre-feasibility study | PFS | 1 |

| Implementation planning stage—phase I | IPSP1 | 3 |

| Implementation planning stage—phase II | IPSP2 | 5 |

| Arrangements stage and execution of construction documentation | ASECD | 81 |

| Developing a detailed investment management map | DDIMM | 6 |

| The stage of obtaining and securing financing (feasibility study) | SOSF | 6 |

| The stage of executing executive documentation | SEED | 69 |

| Stage of selecting general contractor(s) and verification of executive documentation | SSGCVED | 69 |

| Project implementation stage | PIS | 93 |

| Commissioning stage | COMMS | 16 |

| Evaluation stage of obtaining results and effects of the project (1st phase of project closing) | ESOREP | 1 |

| Phase of drawing up proposals for future implementation after Project Closure Phase I | PDPFIPCP1 | 1 |

| Initial operation stage (usually 3 years of warranty and guarantee) | IOS | 102 |

| The stage of final evaluation of the results and effects of the project (II stage of project closing) | SFEREP2 | 1 |

| Phase of drawing up proposals for future implementation after Phase II of the project closure | PCPFIPCP2 II | 1 |

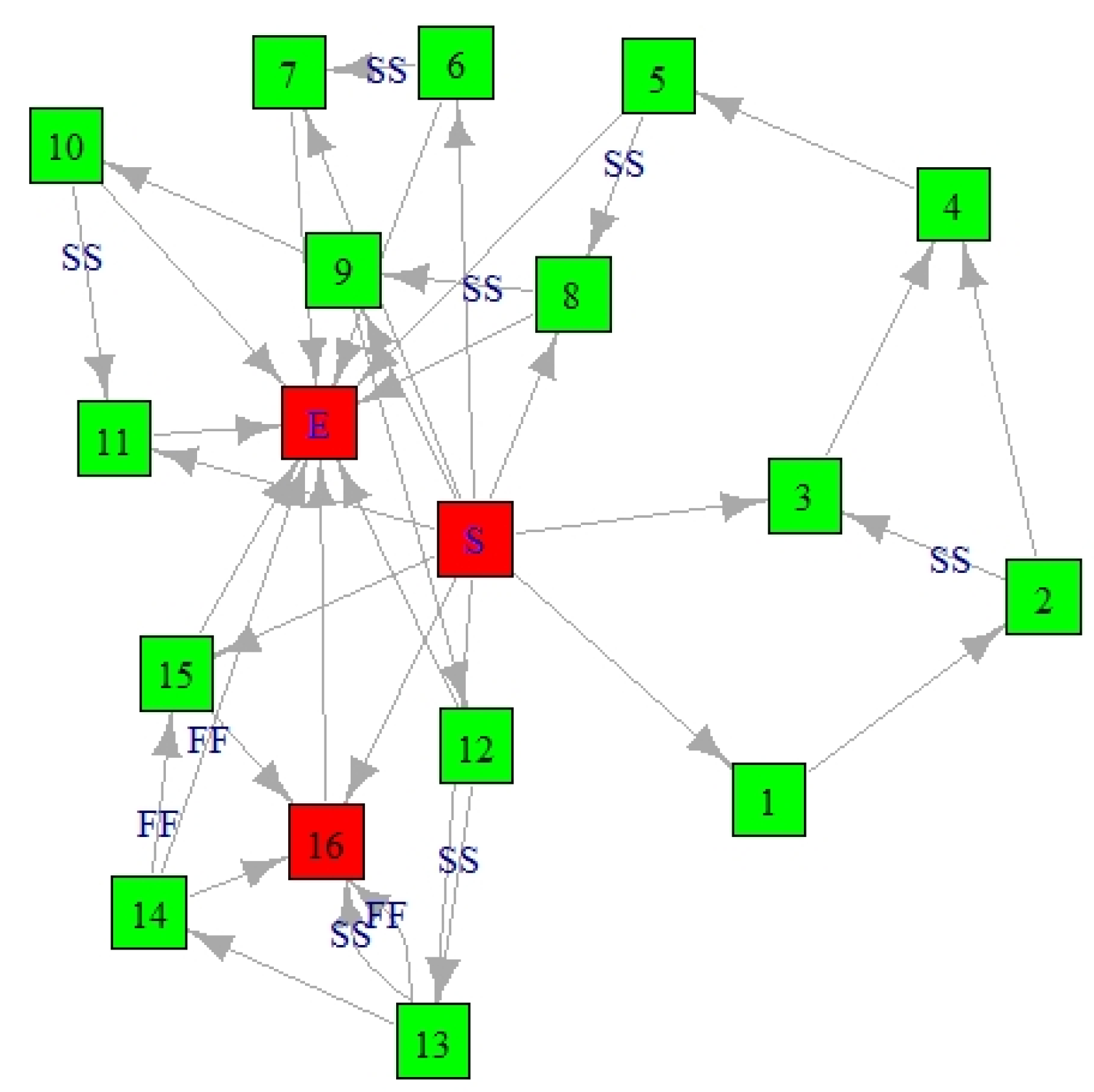

| N | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | 13 | 14 | 15 | 16 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Finish–start (FS) type of precedence | NA | 1 | NA | 2, 3 | 4 | 5 | NA | NA | NA | 9 | NA | 9 | NA | 12 | NA | NA |

| Start–start (SS) type of precedence | NA | NA | 2 | NA | NA | NA | 6 | 6,7 | 8 | NA | 10 | NA | 12 | NA | 14 | 13 |

| Finish–finish (FF) type of precedence | NA | NA | NA | NA | NA | NA | NA | NA | NA | NA | NA | NA | NA | NA | NA | 15 |

| Start–finish (SF) type of precedence | NA | NA | NA | NA | NA | NA | NA | NA | NA | NA | NA | NA | NA | NA | NA | NA |

| Durations | 2 | 11 | 6 | 1 | 3 | 5 | 81 | 6 | 6 | 69 | 69 | 93 | 16 | 1 | 1 | 102 |

| Time-at-Risk (TaR) (in Quantiles) | Scenario A | Scenario B 1 | Scenario C 2 |

|---|---|---|---|

| 99% quantile | 6.35866 | 6.77638 | 6.15269 |

| 95% quantile | 4.47752 | 5.12026 | 4.40843 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Sobieraj, J.; Metelski, D. Project Risk in the Context of Construction Schedules—Combined Monte Carlo Simulation and Time at Risk (TaR) Approach: Insights from the Fort Bema Housing Estate Complex. Appl. Sci. 2022, 12, 1044. https://doi.org/10.3390/app12031044

Sobieraj J, Metelski D. Project Risk in the Context of Construction Schedules—Combined Monte Carlo Simulation and Time at Risk (TaR) Approach: Insights from the Fort Bema Housing Estate Complex. Applied Sciences. 2022; 12(3):1044. https://doi.org/10.3390/app12031044

Chicago/Turabian StyleSobieraj, Janusz, and Dominik Metelski. 2022. "Project Risk in the Context of Construction Schedules—Combined Monte Carlo Simulation and Time at Risk (TaR) Approach: Insights from the Fort Bema Housing Estate Complex" Applied Sciences 12, no. 3: 1044. https://doi.org/10.3390/app12031044