Impact of El Niño on Oil Palm Yield in Malaysia

by

,

,

Jen Feng Khor

1,

Lloyd Ling

1,*,

Zulkifli Yusop

2,

Wei Lun Tan

3,

Joan Lucille Ling

4 and

Eugene Zhen Xiang Soo

1 1

Centre of Disaster Risk Reduction (CDRR), Lee Kong Chian Faculty of Engineering & Science, Civil Engineering Department, Universiti Tunku Abdul Rahman, Jalan Sungai Long, Kajang 43000, Malaysia

2

Centre for Environmental Sustainability and Water Security, Universiti Teknologi Malaysia, Skudai 81310, Malaysia

3

Centre for Mathematical Sciences (CMS), Lee Kong Chian Faculty of Engineering & Science, Department of Mathematical and Actuarial Sciences, Universiti Tunku Abdul Rahman, Jalan Sungai Long, Kajang 43000, Malaysia

4

Department of Liberal Arts and Sciences, American Degree Programme, Taylor’s University, No. 1, Jalan Taylors, Subang Jaya 47500, Malaysia

*

Author to whom correspondence should be addressed.

Agronomy 2021, 11(11), 2189; https://doi.org/10.3390/agronomy11112189

Submission received: 6 October 2021

/

Revised: 26 October 2021

/

Accepted: 26 October 2021

/

Published: 29 October 2021

(This article belongs to the Special Issue Crop Yield Prediction in Precision Agriculture)

Abstract

:Oil palm crop yield is sensitive to heat and drought. Therefore, El Niño events affect oil palm production, resulting in price fluctuations of crude palm oil due to global supply shortage. This study developed a new Fresh Fruit Bunch Index (FFBI) model based on the monthly oil palm fresh fruit bunch (FFB) yield data, which correlates directly with the Oceanic Niño Index (ONI) to model the impact of past El Niño events in Malaysia in terms of production and economic losses. FFBI is derived from Malaysian monthly FFB yields from January 1986 to July 2021 in the same way ONI is derived from monthly sea surface temperatures (SST). With FFBI model, the Malaysian oil palm yields are better correlated with ONI and have higher predictive ability. The descriptive and inferential statistical assessments show that the newly proposed FFBI time series model (adjusted R-squared = 0.9312 and residual median = 0.0051) has a better monthly oil palm yield predictive ability than the FFB model (adjusted R-squared = 0.8274 and residual median = 0.0077). The FFBI model also revealed an oil palm under yield concern of the Malaysian oil palm industry in the next thirty-month forecasted period from July 2021 to December 2023.

1. Introduction

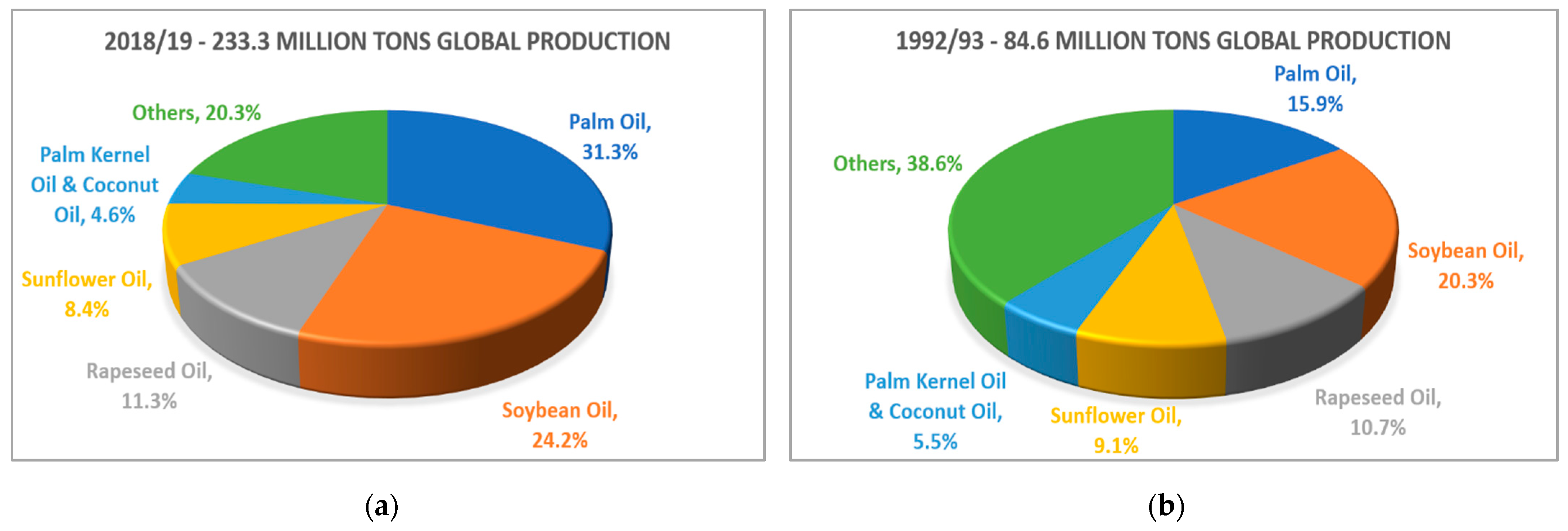

The edible oil and fat sectors consist of 17 varieties of oils and fats that can be categorized into vegetable oils and animal fats. As seen in Figure 1, global edible oil and fat output increased by around 176% in the span of 26 years, from 84.6 million tons (Mt) in 1992/93 to 233.3 Mt in 2018/19. That equates to a mean annual increment of 5.7 Mt [1].

Palm oil made a significant 40% rise in demand, which was an increase of about 2.3 Mt per year in the whole edible oil and fat sectors within the aforementioned period [1]. The said increase was a consequence of the growing demand for palm oil consumption within the food sector, specifically household consumable oil, the cosmetics sector and biodiesel fuel. Typically, vegetable oils are regarded to be an effective replacement for fossil fuels that can lead to a renewable energy source [2].

Palm oil is by far the most manufactured oil relative to many other edible oils and fats, accounting for nearly 31.3% of total edible oils and fats manufactured [1]. As presented in Table 1, oil palm is the most efficient in terms of edible oil yield per hectare with yields of about 4.27 tons per hectare per year (t/ha/yr) (combined palm and palm kernel oil) and at least six times more productive than any other oilseed [3,4]. This claim is supported by the national oil yield of 4.02 t/ha/yr in Malaysia (Appendix A: 3.66 t/ha/yr for palm oil and 0.36 t/ha/yr for palm kernel oil) [5,6,7]. Its input-output ratio is greater than that of other edible oils and fats. As a result, a smaller plantation area is required for oil palms to produce the same quantity of edible oil than other crops. Oil palm cultivation is also extremely alluring given the limited land resources available globally. In addition, the production cost for palm oil is about 700 USD per ton (USD/t), much cheaper compared to other vegetable oils. The next lowest cost is 850 USD/t for rapeseed oil [8,9,10].

Oil palm crop is a crucial income resource in Malaysia, as the revenue from palm oil exports amounted to 5.16% of the country’s Gross Domestic Product (GDP) in 2020 [11,12,13]. Situated between the Indian and Pacific Oceans, Malaysia, being the second largest exporter (after Indonesia) of palm oil in the world [14] is susceptible to El Niño and La Niña occurrences. El Niño (warm phase) and La Niña (cool phase) are phases of a larger phenomenon called the El Niño-Southern Oscillation (ENSO). During non-El Niño conditions (ENSO neutral), trade winds blow westwards across the tropical Pacific Ocean, pushing warm surface water towards the western Pacific (Asia and Australia). During an El Niño event, trade winds which normally blow westwards weaken or reverse direction, now blowing eastwards across the tropical Pacific Ocean, bringing warm water towards the coasts of South America. As warm water accumulates at the coasts of South America, convection above the warm surface water causes warm air to rise and precipitation happens. As a result, drastically increased rainfall would be seen in Ecuador and northern Peru. On the other side of the tropical Pacific Ocean, El Niño brings droughts to Malaysia, Indonesia and Australia [15,16,17].

Scientists use the Oceanic Niño Index (ONI) to measure deviations from normal sea surface temperatures [17]. This study uses ONI to classify El Niño events from January 1986 to June 2021 as shown in Table 2. The ONI is the running three-month mean SST anomaly for the Niño 3.4 region (5° N–5° S, 120° W–170° W). El Niño events are characterized by five consecutive overlapping three-month periods at or above +0.5 °C anomaly [18,19]. In general, El Niño causes lower rainfall, higher temperatures and abnormally dry conditions in Malaysia [20,21,22]. This study analysed the impact of past El Niño events on the oil palm production in Malaysia.

Yield of fresh fruit bundles (FFB) and crude palm oil (CPO) are affected by El Niño as oil palm crop is sensitive to prolonged drought periods like other oil crops [22,23,24]. During the occurrence of El Niño, a high level of water stress is generated for the palm trees due to reduced rainfall and increased temperature [2].

Many researchers have looked into the relationship between rainfall, temperature and oil palm production in Malaysia [2,20,22,25,26,27,28,29]. However, the direct correlation between ENSO index and oil palm production has yet to be analysed. Furthermore, past studies lack the quantification study of actual financial losses due to the impact of El Niño on the Malaysian oil palm industry. Therefore, this study investigated the direct relationship between ONI and the monthly oil palm FFB yield. The objective of this study is to model the impact of El Niño on the palm oil production in Malaysia by proposing a newly derived Fresh Fruit Bunch Index (FFBI). The impacts are then quantified financially in terms of opportunity losses and real Malaysian GDP value. This study also aims to forecast the Malaysian oil palm yields in the near future using the newly proposed FFBI time series model.

2. Materials and Methods

2.1. Study Area

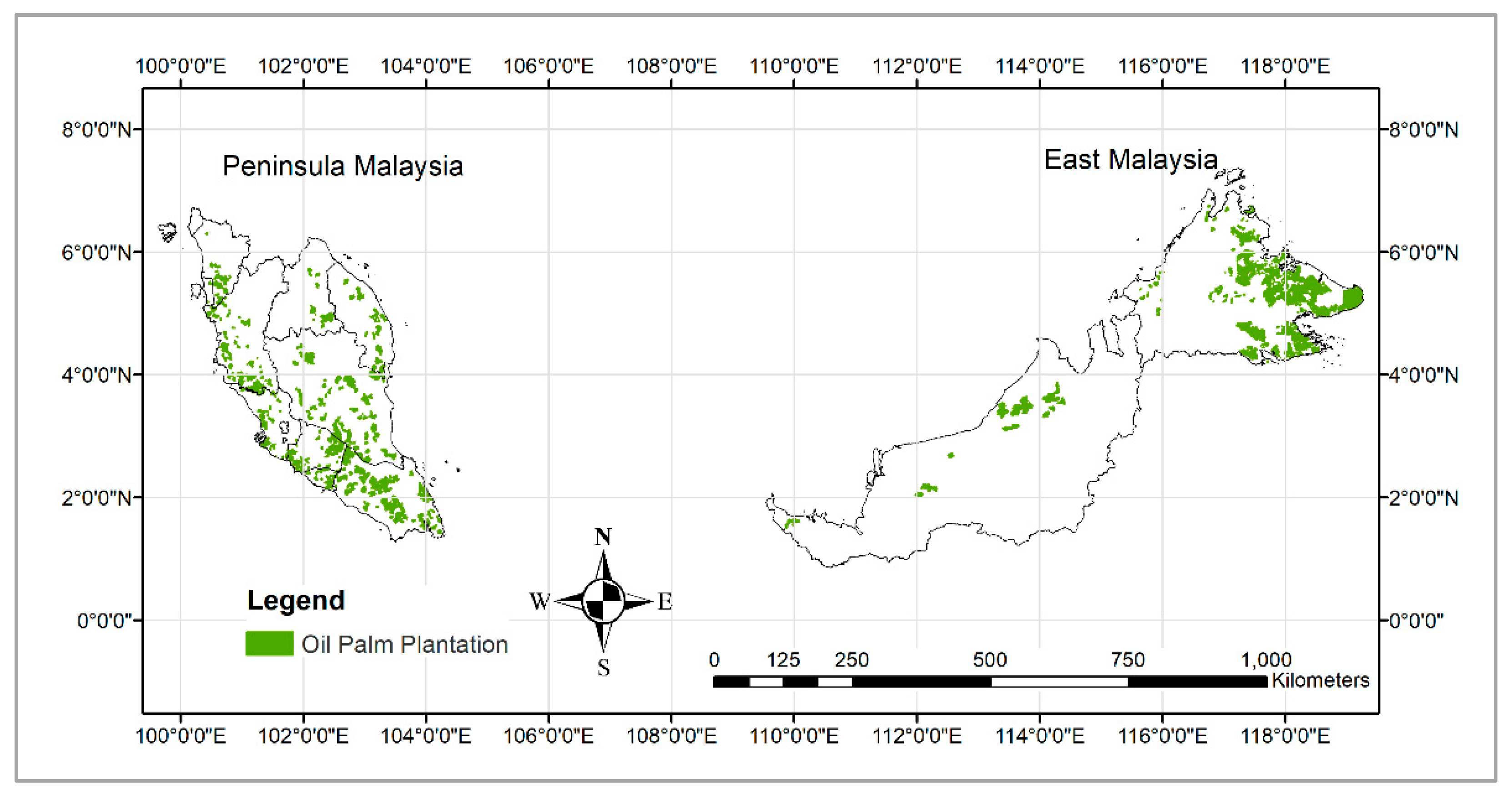

Located in Southeast Asia, Malaysia consists of two geological regions separated by the South China Sea. Peninsula Malaysia (or West Malaysia) shares a land border with Thailand to the north and Singapore to its south. Located on the northern part of the Borneo Island, East Malaysia borders Indonesia and surrounds the Sultanate of Brunei [30]. The total land area is 328,550 km2 [31]. In 2020, the total area planted with oil palm in Malaysia is 58,653 km2 (nearly 18% of the total land area) [7]. Figure 2 shows the location map of oil palm plantation areas in Malaysia.

2.2. The New Fresh Fruit Bunch Index (FFBI) Model

Fresh Fruit Bunch Index (FFBI) is created with the monthly Malaysian oil palm FFB yield data [5,6,7] (Appendix B) through a similar calculation method of ONI (Appendix D) which is based on the monthly sea surface temperatures (SST) tracked by the National Oceanic and Atmospheric Administration (NOAA) [18]. In this study, monthly oil palm FFB yields from January 1986 to July 2021 (total 427 data points) in Malaysia were used [5,6,7]. The national average FFB yield for each month was calculated on the month-to-month basis from 1986 to 2020 in Table 3.

FFBanomaly, the difference between FFB yield and average FFB yield (Table 3) at each corresponding month was calculated using Equation (1):

FFBanomaly = FFB − FFBaverage

The new FFBI (Appendix C) was then calculated by taking the 3-month running mean of FFBanomaly, as shown in Equation (2):

where FFBanomaly, i-1 and FFBanomaly, i+1 were the FFB anomalies one month before and after the month that was being calculated. Hence, from 427 points of FFB yields, a total of 425 points of FFBI was derived, from February 1986 to June 2021.

FFBIi = (FFBanomaly, i-1 + FFBanomaly, i + FFBanomaly, i+1)/3,

2.3. Correlation Test between Malaysian Oil Palm Yields and Oceanic Niño Index (ONI)

The relationships between FFB and FFBI with ONI were tested using correlation tests. Normality tests were conducted beforehand to determine whether parametric or non-parametric correlation tests should be used. If a given dataset has less than 2000 samples, the Shapiro-Wilk test is suggested rather than the Kolmogorov-Smirnov test. This paper used a dataset which has less than 2000 samples, and therefore, the Shapiro-Wilk test was used. If the p-value is greater than 0.05, then the dataset is considered to be normally distributed [33]. Based on the normality tests (Table 4), FFB and ONI data distribution were determined to be non-normally distributed, and FFBI data distribution was normally distributed. As such, non-parametric Spearman’s rho correlation test was used to investigate the relationship between the oil palm yields and ONI in a lag period from 0 to 18 months. A Spearman’s rho correlation is also referred as Spearman correlation or Spearman rank correlation. The strength of association between the variables tested is expressed in a single value between −1 and +1, which is a bivariate correlation analysis. A positive correlation coefficient indicates a positive relationship between the two variables (as values of one variable increase, values of the other variable also increase), while a negative correlation coefficient expresses a negative relationship (as values of one variable increase, values of the other variable decrease). A correlation coefficient with a value of zero indicates that no relationship exists between the variables. The Spearman correlation does not assume that the variables are normally distributed, hence being used in this study as not all the variables were normally distributed [34,35]. All of the tests were conducted using IBM SPSS Statistics version 26.0 [36].

2.4. Time Series Forecasting

FFB and FFBI time series forecasting models with ONI as its predictor were created using the Expert Modeler in IBM SPSS Statistics version 26.0 [36]. The FFBI time series model was also validated repeatedly using a 30-year moving time frame. Six FFBI time series models were created and validated using different block periods (1986–2015, 1987–2016, 1988–2017, 1989–2018, 1990–2019 and 1991–2020). Each model forecasted FFBI one year ahead of the respective block period to be compared and validated with the observed FFBI. Residual analyses for each model were also performed in which the 99% confidence intervals of the residuals’ median, standard deviation and variance were computed using BCa bootstrapping method in this study. Using monthly Malaysian FFB data points from February 1986 to June 2021 (N = 425), the final FFB and FFBI time series forecasting models were created to forecast for another 30 months from July 2021 until December 2023.

R-squared measures the proportion of the variable in the dependent variable explained by all of the independent variables in the model, while adjusted R-squared measures the proportion of variation explained by only those independent variables that really help in explaining the dependent variable. As such, the adjusted R-squared will decrease if independent variables that do not help in predicting the dependent variable are added to the model [37]. The adjusted R-squared (R2adj) was derived from the R-squared produced by the models using Equation (3):

where R2 is the R-squared of the models, N is the number of data points and K is the number of independent regressors [38].

To compare the FFB and FFBI time series models, residual analyses were conducted using IBM SPSS Statistics version 26.0. Residual between the predicted and observed data point was calculated [39,40]. Descriptive statistics of the residuals from both models were calculated for model comparison, including residuals’ skewness, range, median, standard deviation and variance. Shapiro-Wilk normality tests were also conducted for the residuals to determine whether the median or mean residuals should be referred for model prediction accuracy comparison. As the residuals from both models were determined to be non-normally distributed, the FFB and FFBI model’s median residuals were used for comparison assessment. The non-parametric inferential statistics of the bias corrected and accelerated (BCa) bootstrapping method was conducted with 2000 random samples (with replacement) to compute the 99% confidence intervals (CI) of the residuals’ median, standard deviation and variance.

2.5. Mann-Kendall Trend Test and Sen’s Slope

The Mann-Kendall trend test was used to evaluate the trends of FFBI during the occurrence of each El Niño events. Mann-Kendall test statistics (S) can be calculated using Equation (4):

where xi and xk are sequential data in the series and

The variance of S (Var(S)) is estimated as:

where tp defines the ties of the pth value, and q represents the number of the tied value. The standardized test static for the Mann-Kendall test (Z) can be calculated, as shown in Equation (7):

The sign of Z indicates the direction of the trend. The negative value of Z indicates a decreasing trend and vice versa. At the 5% significance level, the null hypothesis of no trend is rejected if the absolute value of Z is higher than 1.64 [41]. This study used the excel template developed by Finnish Meteorological Institute [42] to conduct the Mann-Kendall trend tests and Sen’s slope estimation for FFBI during El Niño events.

The Sen’s slope method was used for the estimation of the monthly change in FFBI from February 1986 to June 2021. The Sen’s slope is calculated as the median of all the slopes estimated between all the successive data points of FFBI time series as [41]:

where ∆FFBI is the change of FFBI in the change of time, ∆t between two subsequent FFBI data.

2.6. Opportunity Loss Modelling of El Niño Events

During or after the occurrence of an El Niño event in the study period, the first clump of continuous monthly negative FFBI was considered to be the oil palm yield losses triggered by El Niño. The oil palm FFB yield losses (FFBL) due to the observed El Niño event were computed by summing up the absolute magnitude of the negative FFB. As such, the opportunity loss caused by the El Niño event was calculated using Equation (9):

where OL is the opportunity loss caused by El Niño in the unit of USD, area is the oil palm matured area (Appendix K), OER is the oil extraction rate (Appendix K) to convert oil palm from fresh fruit bunch to crude palm oil (CPO) and price is the CPO price (Appendix J) [5,6,7].

OL = FFBL × Area × OER × Price,

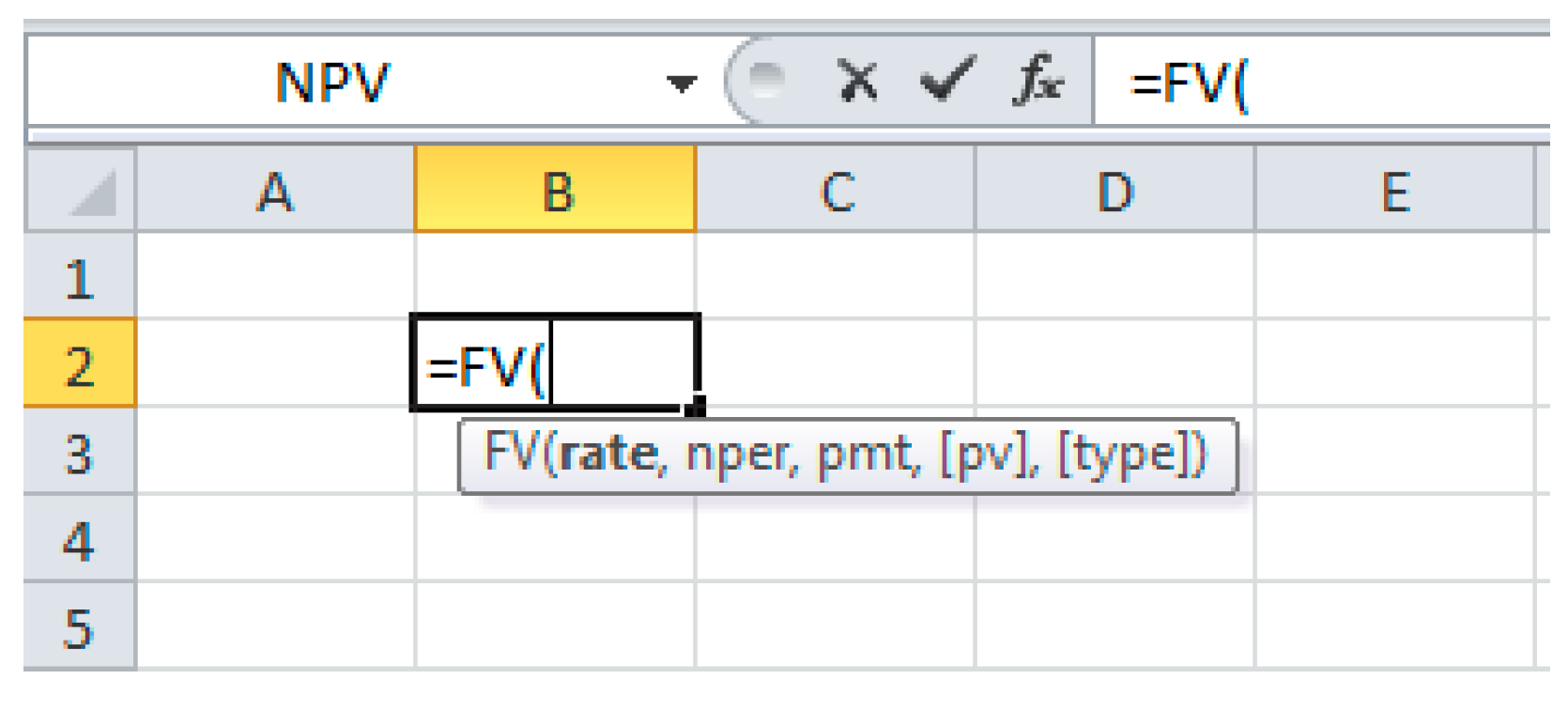

The opportunity losses for all El Niño events within the study period were projected to December 2021 for fair comparison using a hypothetical discount rate of 6%. This computation was done using FV function in Microsoft Excel software as shown in Figure 3,

where FV is the future value, rate is the discount rate per period, NPER is the total number of payment periods, PMT is the payment made for each period, PV is the present value and type is the representation of the timing of payment (1 for payment at the beginning of the period and 0 for payment at the end of the period).

3. Results

3.1. Predictive Ability of Fresh Fruit Bunch Index (FFBI) Model

3.1.1. Correlation with Oceanic Niño Index (ONI)

The newly proposed FFBI model (Appendix C) has an improved ability to model the impact of El Niño events on the oil palm production in Malaysia compared to FFB model. Based on the non-parametric Spearman’s rho correlation test (Table 5), FFBI has statistically significant correlations with ONI at lag periods from 2 to 16 months, with the highest correlation of −0.399 at 0.01 alpha level. On the other hand, the correlations of FFB and ONI are only significant at lag periods from 6 to 13 months, with the highest correlation of −0.217 at 0.01 alpha level.

3.1.2. Time Series Forecasting

Based on the statistical assessment of the FFB and FFBI time series model (Table 6), the FFBI model (Appendix F) has an adjusted R-squared of 0.9312, which is significantly higher than the FFB model (Appendix E) with adjusted R-squared of 0.8274 only. Compared to the FFB model with residual sum of squares (RSS) of 4.6876, the FFBI model has much lower RSS at 0.5459 only. The FFBI model also has a lower median residual (0.0051) than the FFB model (0.0077). Other than that, residual of the FFBI model has lower skewness, range, standard deviation and variance compared to the FFB model.

3.2. Production, Financial and Economical Loss in the Malaysian Oil Palm Industry due to El Niño

With the application of FFBI, oil palm FFB trends from January 1986 to June 2021 were studied. Based on the Mann Kendall’s (MK) trend test (Table 7), almost every El Niño event in the aforementioned period is accompanied by a significant decreasing trend of FFBI (at least 0.05 alpha level), except for 2002/03′s moderate El Niño and 2014/15′s weak El Niño. Those downward FFBI trends could be observed from 0 to 6 months after an El Niño event (Table 8).

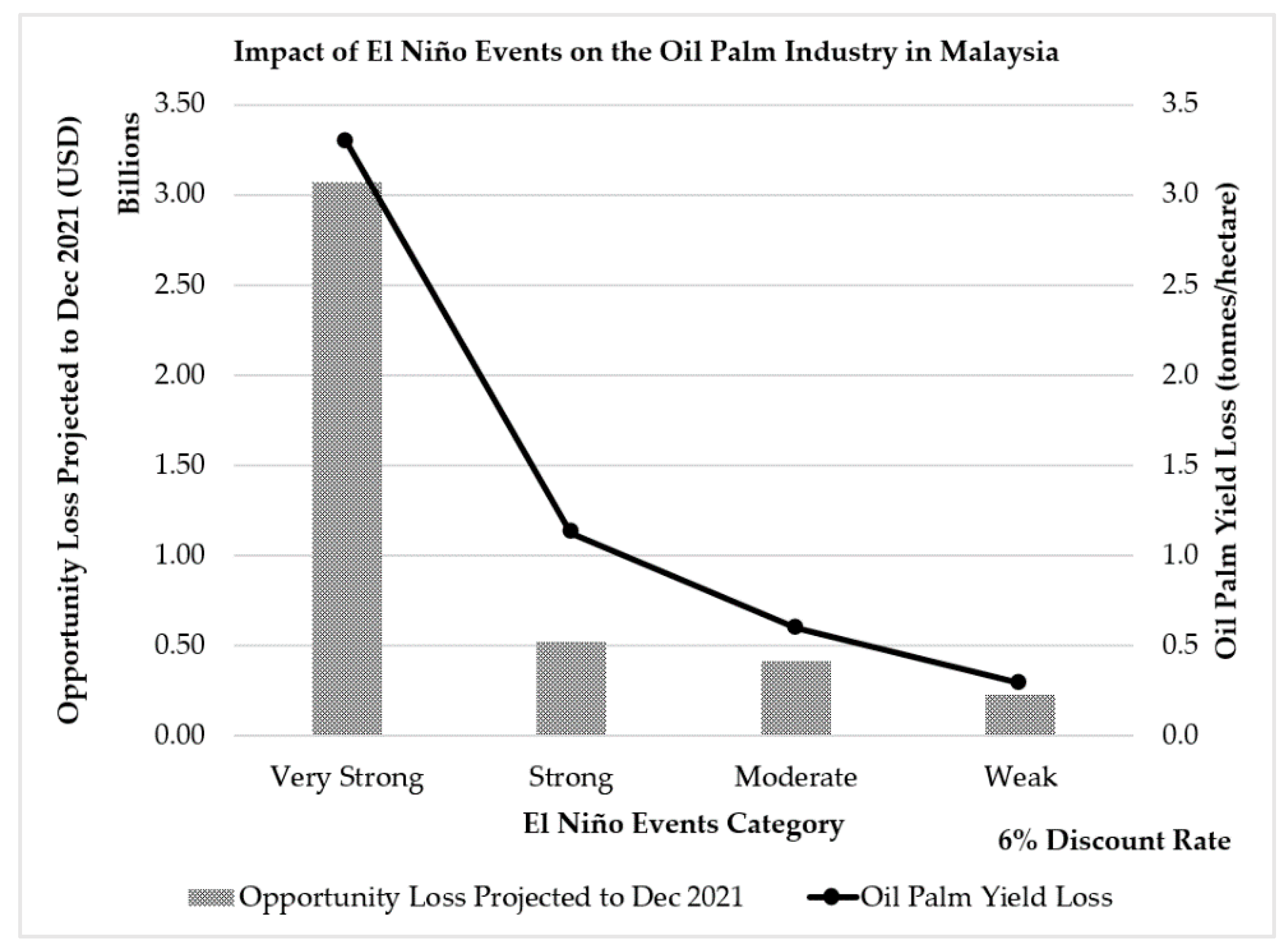

When the FFBI plummets below zero, oil palm production would suffer losses due to El Niño. Those losses could last between 4 to 25 months (Table 8) depending on the severity of the El Niño events, before recovering to normal productions. Both very strong El Niño events caused oil palm yield losses of about 3.0739 ton per hectare (t/ha) in 1997/98 and 3.5197 t/ha in 2015/16. Those losses equate to an average oil palm yield loss of 3.2968 t/ha in Malaysia, causing approximately 3.07 billion USD of opportunity losses when projected to December 2021 using a 6% discount rate (Table 9).

The oil palm production and opportunity losses decrease as the severity of El Niño events decrease (Figure 4). The oil palm yields were estimated to reduce by 1.1250 t/ha during a strong El Niño event, 0.5974 t/ha during a moderate El Niño event and about 0.2953 t/ha during a weak El Niño event on average. In financial terms, a strong El Niño event could cause opportunity losses of approximately 522 million USD, 416 million USD for a moderate El Niño event and 231 million USD for a weak El Niño event in Malaysia (Table 9).

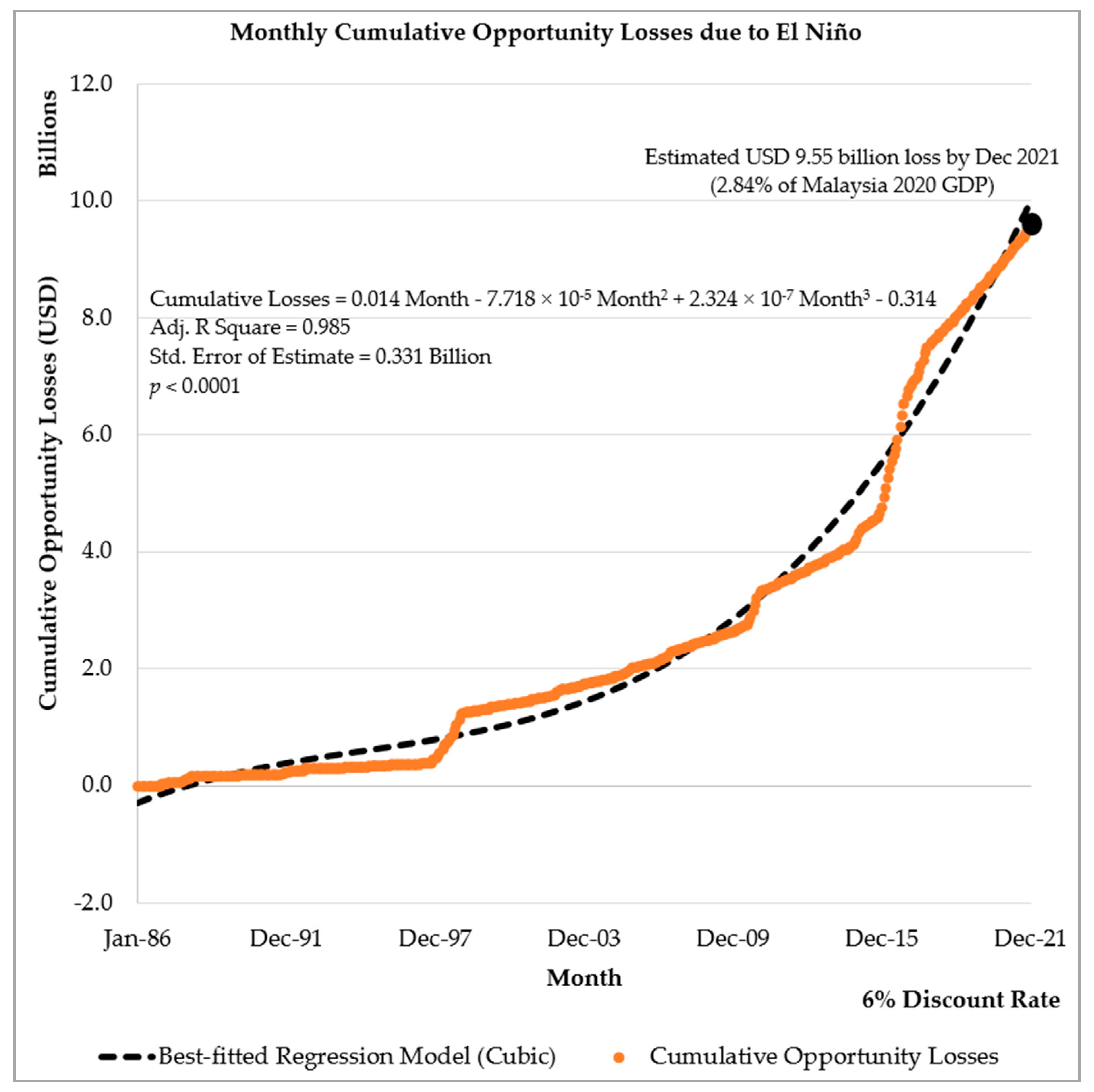

This study then accumulates the opportunity losses at a hypothetical 6% discount rate to show the collective impact of every El Niño event from January 1986 to June 2021 (except for 2018/19 weak El Niño) on the oil palm industry in Malaysia (Figure 5). The total combined loss is estimated to be 9.55 billion USD by the end of 2021, which is approximately 2.84% of Malaysia’s GDP in 2020 [11]. Using SPSS, the cumulative opportunity losses model was modelled with a cubic model with an adjusted R-squared of 0.985, standard error of estimate of 0.331 billion USD and significant at p-value less than 0.0001 (Figure 5).

4. Discussion

4.1. Predictive Ability of the New Fresh Fruit Bunch Index (FFBI)

Based on Spearman’s rho correlation tests (Table 5), both FFB and the proposed FFBI have negative correlations with ONI. This shows that when ONI increased during past El Niño events, water stress was induced in palm trees, causing oil palm production reduction in Malaysia [2,20,21,22,25]. The new FFBI has significantly higher correlation with ONI compared to FFB. By converting monthly FFB data into FFBI, the impact of El Niño on the monthly oil palm production in Malaysia could be modelled with higher precision.

The comparison between the FFB and FFBI time series model (Table 6) shows that FFBI model has better predictive ability than FFB model. Based on the residual analyses, both models have median residuals with 99% confidence intervals which span across zero, indicating their capabilities to produce a monthly oil palm production prediction with low error [40]. However, the FFBI time series model has a higher adjusted R-squared, lower RSS, median residual, residual skewness, residual range, residual standard deviation and residual variance than the FFB model. By having higher correlation with ONI and significantly better monthly oil palm yield forecasting ability, FFBI model is a better predictive modelling tool for the Malaysian oil palm industry stakeholders to better understand the impact of El Niño events. With the application of FFBI model, decision making processes could be enhanced so that appropriate measures could be taken to prepare for the adverse effects of El Niño on oil palm production in the future.

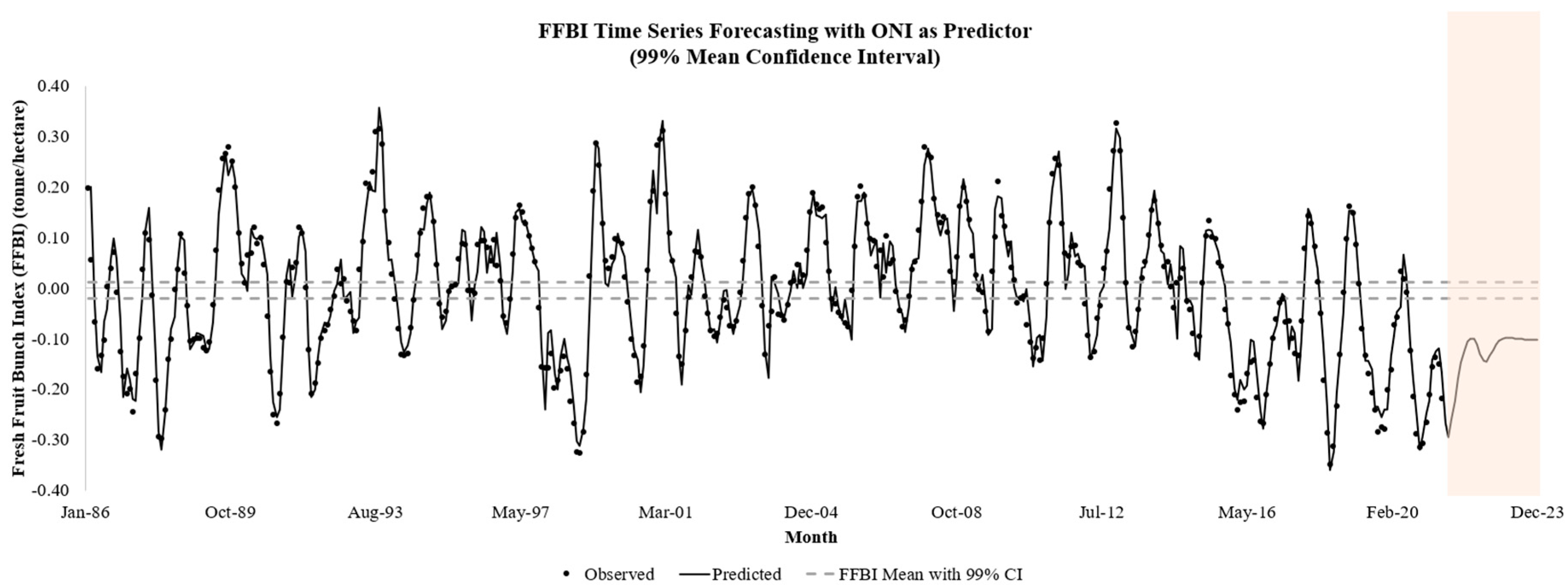

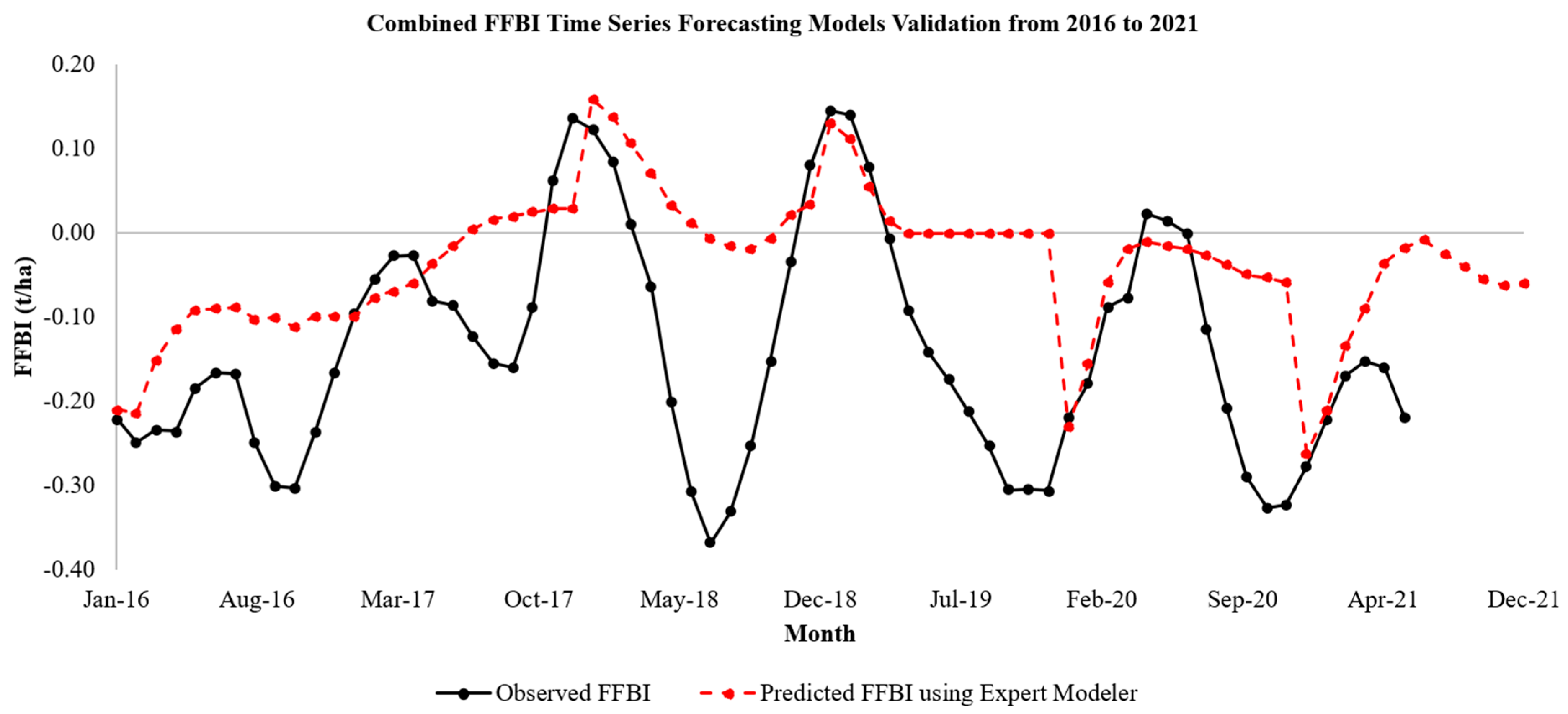

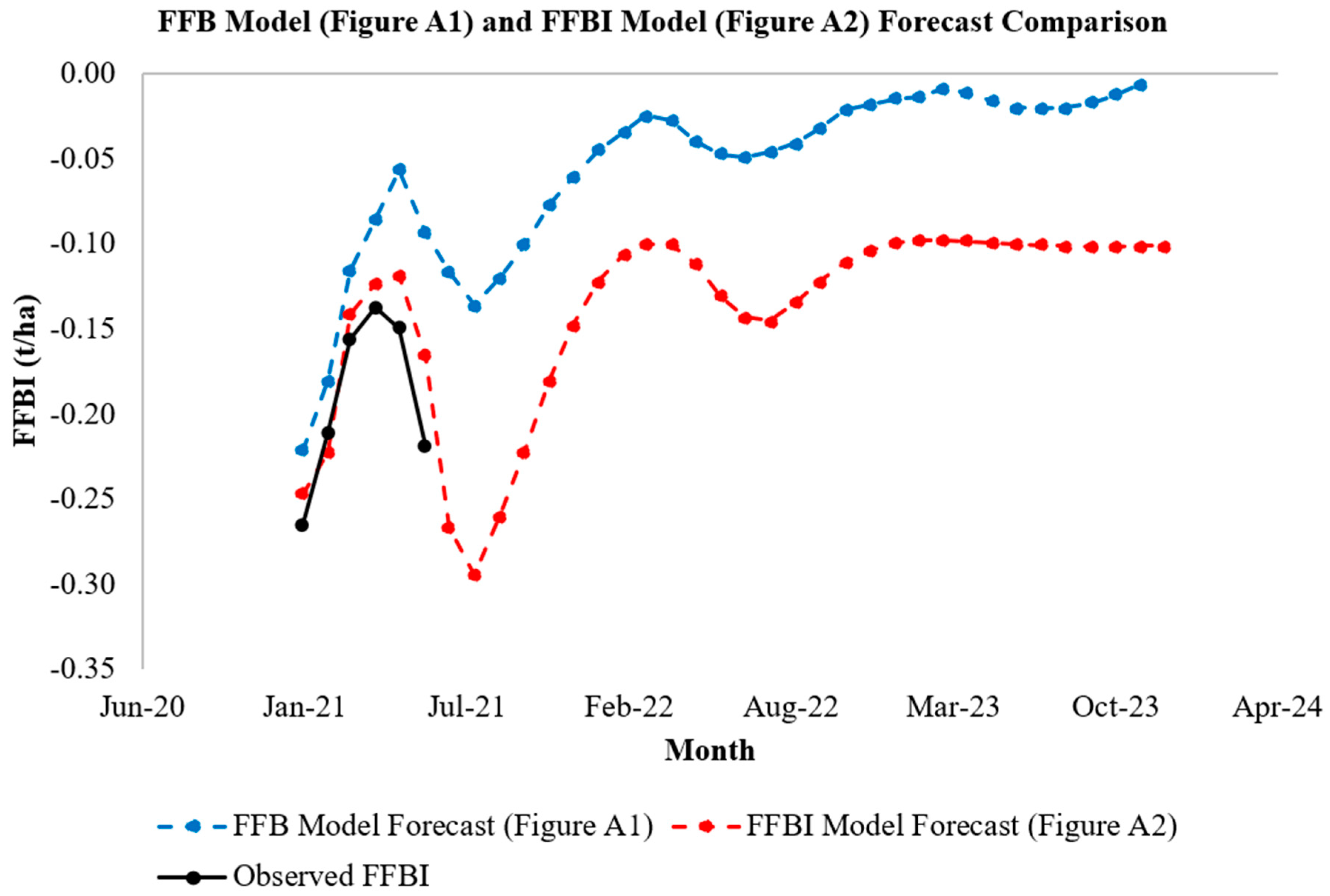

The validation tests using six different FFBI models in different time frames showed that the proposed FFBI model is consistent. The adjusted R-squared of all the validated models are consistent and stable, in the range of 0.916 to 0.9354 (Appendix G). The residuals of all the models have median residuals with 99% confidence intervals which span across zero, further supporting the forecasting ability and stability of the proposed FFBI model. Furthermore, the predicted FFBI produced by the validation models tend to follow the trend of real observed FFBI (derived from historical FFB [5,6,7], see Appendix H). The FFBI model also outperformed the FFB model as the forecasted FFBI (Appendix F) from 2021 to 2023 is closer to the observed FFBI from January 2021 to June 2021 (Appendix I).

4.2. Trends of Oil Palm Yields during El Niño Events

In the Spearman’s rho correlation tests (Table 5), FFBI shows a significant correlation with ONI with lag periods from 2 to 16 months. This is on par with other studies that reported lag periods from 3 to 24 months to witness oil palm production reduction in Malaysia due to El Niño events and drought [2,20,22,25,26,27,28,29]. Since there is no fixed way to explain the nature, the El Niño events could affect the oil palm yields after a period of time and are not constrained to a single fixed period. The FFBI model of this study suggests that the oil palm production could be affected after 2 to 16 months of the occurrence of El Niño events in Malaysia.

Using the FFBI model, trends of oil palm yield in Malaysia during each El Niño event from January 1986 to June 2021 were studied on an event-by-event basis. In general, oil palm yields started to decrease after 0 to 6 months of an El Niño event, according to the Mann Kendall’s trend tests (Table 7). The industry would suffer production losses when the oil palm yields continue to plummet, and this could last for 4 to 25 months depending on the severity of El Niño events (Table 8) before the oil palm yields would recover.

4.3. Impact of El Niño Events on the Malaysian Oil Palm Industry

As shown in Figure 4, very strong El Niño events have a significantly bigger impact on the Malaysian oil palm production compared to other categories of El Niño. Averaged oil palm reduction during very strong El Niño events is about 2.9 times more than the production loss in strong El Niño, 5.5 times more than the moderate El Niño and 11.2 times more than weak El Niño (Table 9). When a very strong El Niño happens, oil palm yields in Malaysia are expected to suffer production losses for about 21 months continuously. For other types of El Niño events, oil palm yields are expected to be negative in terms of FFBI for approximately 6 to 9 months. The total combined opportunity losses from the past 11 El Niño events in Malaysia since 1986 are estimated to be 9.55 billion USD when projected to December 2021. This equates to 2.84% of the Malaysia GDP in 2020 [11] (Figure 5). Undeniably, extreme temperature caused by El Niño is a major factor affecting the oil palm production in Malaysia.

However, the occurrence of El Niño event cannot be controlled. The adverse weather condition caused by El Niño cannot be remedied by concerted intervention [33]. To enhance performance of the oil palm industry in Malaysia, other underlying factors affecting oil palm production should be further investigated. These factors include labour shortage and ageing palm trees [1,43]. Based on the annual Malaysian oil palm FFB yields from 1986 to 2020 [5,6,7] (Appendix K), the FFB yields did not recover to the national average after the 2015/16 very strong El Niño. The Malaysian oil palm FFB yields continued to stay below the mean lower confidence limit (BCa bootstrapped 99% CI) continuously from 2017 to 2020, facing a downward trend, even though there was only a weak occurrence of El Niño in 2018/19 [18,19]. In addition, based on the FFBI validation models, the observed FFBI (derived from historical FFB) from 2016 to 2021 is found to be mostly below the predicted FFBI (Appendix I), showing the possibility that there might be other significant underlying factors affecting oil palm production in Malaysia.

Surely, El Niño would not be the reason to cause the current production downtrend in the Malaysian oil palm industry. One of the reasons might be labour shortage. Oil palm plantations struggle to hire foreign workers for the harvesting of oil palm, while locals shun the idea of working in plantations. The shortage of manpower became worse under the prolonged foreign labour hiring freeze due to the COVID-19 situation and caused more losses to the industry [44]. Another underlying factor is the ageing of palm trees due to the slow replanting process in Malaysia [45]. In 2020, about 35% of the oil palm plantations owned by a private plantation firm (IOI Corporation Berhad) in Malaysia were of prime age, while 37% already passed their prime production phase [46]. Replanting schemes are not attractive to plantation owners due to the lower profit margin of the oil palm sector in the recent years. Backlog of old oil palm trees slow down the improvement of crop yield in Malaysia [47]. According to the United States Department of Agriculture (USDA) [43], aged oil palm trees are to be replaced with new high yield varieties to increase the crop yield. However, many plantation owners are reluctant to replace aged trees in times of high palm oil prices in order to continue gaining profits. Researchers [8] also supported the idea that a proper replanting program is required to improve the oil palm yield in Malaysia. Based on the historical records, oil palm yields dropped during the 1997/98 very strong El Niño and successfully recovered about a year after. However, the oil palm yields maintained at low production since the 2015/16 very strong El Niño. It is possible that the aged palm trees suffered damage from the heat stress of recent very strong El Niño and failed to recover.

4.4. Global Applicability of FFBI

For the previous ten years, more than USD 50 billion has been invested in the Malaysian and Indonesian oil palm sectors [48]. In 2019, almost 88% of the world’s palm oil production comes from the top three palm oil producing countries, Indonesia, Malaysia and Thailand [14]. They are located in the same region (Southeast Asia) with the same climatic pattern [49,50,51]. Hence, the supply of palm oil in the global market will be heavily affected in the event of extreme weather such as El Niño event. Thus, the newly proposed FFBI can be utilized to model the threat of El Niño in the oil palm industry, so that these countries can brace themselves for the adverse effects of intense climate conditions on the oil palm yields in the industry.

5. Conclusions

This study proposes a new oil palm yield index, namely Fresh Fruit Bunch Index (FFBI) that is derived from the monthly oil palm FFB yields. It has shown improvement in the trend and oil palm yield modelling in Malaysia with respect to El Niño events. The FFBI shows a significantly higher correlation with ONI compared to FFB yields based on Spearman’s rho correlation tests at 0.01 alpha level. The FFBI time series model has also shown a significantly higher predictive accuracy when compared to the FFB model. The new FFBI model has an adjusted R-squared of 0.9312, which is significantly higher than the FFB model with adjusted R-squared of 0.8274 only. The FFBI model also has smaller errors based on residual analyses.

The proposed FFBI provides an improved method to model the impact of El Niño events in the Malaysian oil palm industry, as financial losses caused by El Niño events cannot be neglected. A very strong El Niño event is estimated to cause 3.07 billion USD of opportunity losses when projected to December 2021 using a 6% discount rate. The total combined opportunity losses of 13 past El Niño events, starting from 1986 (excluding 2018/19 weak El Niño) is approximately 9.55 billion USD, which is about 2.84% of Malaysia’s 2020 GDP.

The FFBI model reveals that the recent under yield situation of the Malaysian oil palm yield may continue in future. This study further shows that El Niño is not the sole factor affecting the Malaysian oil palm production. Hence, other underlying factors affecting Malaysian oil palm yields such as ageing oil palm trees should be further investigated for the implementation of preventive steps to preserve the sustainable competitive edge of the Malaysian oil palm industry in the international arena. Future work should incorporate Indonesian and Thailand monthly FFB dataset to study the possible global production impact as these countries (Indonesia, Malaysia and Thailand) in the same region produce around 88% of the global palm oil supply.

Author Contributions

Conceptualization, L.L. and Z.Y.; methodology, L.L. and J.F.K.; software, L.L. and J.F.K.; validation, L.L., W.L.T. and Z.Y.; formal analysis, L.L. and J.F.K.; investigation, L.L. E.Z.X.S. and J.F.K.; resources, J.F.K., L.L. and Z.Y.; data curation, L.L. and J.F.K.; writing—original draft preparation, J.F.K.; writing—review and editing, L.L., J.F.K., J.L.L. and Z.Y.; visualization, L.L. and J.F.K.; supervision, L.L., W.L.T. and Z.Y.; project administration, L.L. and Z.Y.; funding acquisition, L.L. and Z.Y. All authors have read and agreed to the published version of the manuscript.

Funding

The research was supported by Ministry of Higher Education (MoHE) through Fundamental Re-search Grant Scheme (FRGS/1/2021/WAB07/UTAR/02/1), Universiti Tunku Abdul Rahman (IPSR/RMC/UTARRF/2019-C2/L07) and partly supported by the Brunsfield Engineering Sdn. Bhd., Malaysia (Brunsfield 8013/0002 & 8126/0001).

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Oil palm data can be found in Palm Oil Registration & Licensing Authority (PORLA) reports “PORLA palm oil statistics” from 1986 to 1999 and Malaysian Palm Oil Board (MPOB) reports “Malaysian oil palm statistics” from 2000 to 2020 in MPOB libraries located in Kelana Jaya and Bangi, Malaysia. Recent oil palm data is available at <https://bepi.mpob.gov.my/index.php/en/> (accessed 17 August 2021). ONI data is available at <https://origin.cpc.ncep.noaa.gov/products/analysis_monitoring/ensostuff/ONI_v5.php> (accessed 25 October 2021).

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A

Table A1.

Annual productivity of crude palm oil (CPO) and crude palm kernel oil (CPKO) from 1975 to 2020 in Malaysia [5,6,7].

| Year | CPO Yield (t/ha) | CPKO Yield (t/ha) | Year | CPO Yield (t/ha) | CPKO Yield (t/ha) |

|---|---|---|---|---|---|

| 1975 | 3.66 | 0.17 | 2000 | 3.46 | 0.41 |

| 1976 | 3.48 | 0.16 | 2001 | 3.66 | 0.44 |

| 1977 | 3.54 | 0.18 | 2002 | 3.59 | 0.40 |

| 1978 | 2.95 | 0.17 | 2003 | 3.75 | 0.43 |

| 1979 | 3.65 | 0.21 | 2004 | 3.73 | 0.42 |

| 1980 | 3.78 | 0.22 | 2005 | 3.80 | 0.45 |

| 1981 | 3.76 | 0.22 | 2006 | 3.93 | 0.47 |

| 1982 | 3.83 | 0.28 | 2007 | 3.83 | 0.44 |

| 1983 | 3.43 | 0.29 | 2008 | 4.08 | 0.47 |

| 1984 | 4.25 | 0.32 | 2009 | 3.93 | 0.45 |

| 1985 | 4.33 | 0.35 | 2010 | 3.69 | 0.42 |

| 1986 | 4.41 | 0.36 | 2011 | 4.01 | 0.43 |

| 1987 | 3.39 | 0.34 | 2012 | 3.84 | 0.43 |

| 1988 | 3.47 | 0.34 | 2013 | 3.85 | 0.43 |

| 1989 | 3.88 | 0.38 | 2014 | 3.84 | 0.42 |

| 1990 | 3.64 | 0.41 | 2015 | 3.78 | 0.40 |

| 1991 | 3.48 | 0.37 | 2016 | 3.21 | 0.34 |

| 1992 | 3.43 | 0.37 | 2017 | 3.53 | 0.39 |

| 1993 | 3.78 | 0.42 | 2018 | 3.42 | 0.39 |

| 1994 | 3.43 | 0.41 | 2019 | 3.47 | 0.39 |

| 1995 | 3.50 | 0.41 | 2020 | 3.33 | 0.38 |

| 1996 | 3.55 | 0.41 | Average: | 3.66 | 0.36 |

| 1997 | 3.63 | 0.40 | |||

| 1998 | 3.02 | 0.36 | |||

| 1999 | 3.58 | 0.40 |

Appendix B

Table A2.

Monthly oil palm fresh fruit bunch (FFB) yield in tons per hectare from January 1986 to July 2021 in Malaysia [5,6,7].

| January | February | March | April | May | June | July | August | September | October | November | December | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1986 | 1.68 | 1.37 | 1.38 | 1.34 | 1.29 | 1.29 | 1.65 | 1.64 | 1.95 | 1.94 | 1.67 | 1.33 |

| 1987 | 1.09 | 1.04 | 1.08 | 1.20 | 1.20 | 1.49 | 1.64 | 1.87 | 2.05 | 1.78 | 1.47 | 1.17 |

| 1988 | 0.95 | 0.97 | 1.19 | 1.34 | 1.38 | 1.67 | 1.69 | 1.85 | 1.78 | 1.68 | 1.57 | 1.41 |

| 1989 | 1.19 | 1.09 | 1.20 | 1.26 | 1.43 | 1.61 | 1.81 | 2.05 | 2.14 | 2.02 | 2.02 | 1.68 |

| 1990 | 1.37 | 1.26 | 1.35 | 1.34 | 1.72 | 1.55 | 1.72 | 1.88 | 1.93 | 1.74 | 1.51 | 1.22 |

| 1991 | 0.99 | 0.97 | 1.25 | 1.41 | 1.59 | 1.43 | 1.73 | 1.88 | 1.98 | 1.88 | 1.49 | 1.23 |

| 1992 | 1.12 | 1.07 | 1.20 | 1.35 | 1.41 | 1.42 | 1.67 | 1.75 | 1.92 | 1.77 | 1.71 | 1.41 |

| 1993 | 1.21 | 1.17 | 1.20 | 1.66 | 1.63 | 1.73 | 1.86 | 1.99 | 2.31 | 2.06 | 1.83 | 1.53 |

| 1994 | 1.38 | 1.16 | 1.23 | 1.29 | 1.30 | 1.41 | 1.53 | 1.71 | 1.92 | 1.98 | 1.77 | 1.69 |

| 1995 | 1.55 | 1.29 | 1.39 | 1.38 | 1.35 | 1.50 | 1.64 | 1.73 | 1.87 | 1.83 | 1.82 | 1.58 |

| 1996 | 1.33 | 1.06 | 1.43 | 1.40 | 1.64 | 1.64 | 1.63 | 1.86 | 1.90 | 1.94 | 1.64 | 1.43 |

| 1997 | 1.23 | 1.12 | 1.42 | 1.58 | 1.63 | 1.68 | 1.77 | 1.82 | 1.95 | 1.88 | 1.67 | 1.30 |

| 1998 | 1.03 | 1.18 | 1.15 | 1.20 | 1.27 | 1.38 | 1.49 | 1.61 | 1.65 | 1.48 | 1.41 | 1.10 |

| 1999 | 0.98 | 1.05 | 1.29 | 1.65 | 1.85 | 1.76 | 1.75 | 1.76 | 1.88 | 1.89 | 1.76 | 1.61 |

| 2000 | 1.38 | 1.26 | 1.26 | 1.32 | 1.33 | 1.35 | 1.39 | 1.62 | 1.88 | 2.02 | 1.96 | 1.56 |

| 2001 | 1.80 | 1.51 | 1.46 | 1.51 | 1.57 | 1.48 | 1.43 | 1.57 | 1.78 | 1.81 | 1.70 | 1.52 |

| 2002 | 1.47 | 1.21 | 1.34 | 1.32 | 1.40 | 1.43 | 1.51 | 1.68 | 1.87 | 1.79 | 1.57 | 1.38 |

| 2003 | 1.29 | 1.12 | 1.40 | 1.56 | 1.67 | 1.73 | 1.83 | 1.82 | 1.83 | 1.66 | 1.46 | 1.62 |

| 2004 | 1.25 | 1.18 | 1.25 | 1.33 | 1.44 | 1.53 | 1.69 | 1.71 | 1.97 | 1.77 | 1.68 | 1.74 |

| 2005 | 1.50 | 1.31 | 1.52 | 1.56 | 1.61 | 1.50 | 1.62 | 1.70 | 1.82 | 1.75 | 1.61 | 1.40 |

| 2006 | 1.23 | 1.34 | 1.51 | 1.61 | 1.70 | 1.64 | 1.67 | 1.87 | 1.97 | 1.70 | 1.90 | 1.43 |

| 2007 | 1.45 | 1.25 | 1.30 | 1.35 | 1.43 | 1.39 | 1.62 | 1.83 | 1.89 | 1.85 | 1.95 | 1.68 |

| 2008 | 1.68 | 1.42 | 1.51 | 1.52 | 1.62 | 1.65 | 1.78 | 1.79 | 1.76 | 1.90 | 1.87 | 1.68 |

| 2009 | 1.52 | 1.30 | 1.42 | 1.39 | 1.48 | 1.52 | 1.60 | 1.63 | 1.74 | 2.14 | 1.77 | 1.69 |

| 2010 | 1.44 | 1.22 | 1.44 | 1.38 | 1.44 | 1.49 | 1.64 | 1.71 | 1.66 | 1.72 | 1.55 | 1.34 |

| 2011 | 1.15 | 1.20 | 1.51 | 1.60 | 1.78 | 1.79 | 1.79 | 1.69 | 1.96 | 1.95 | 1.68 | 1.59 |

| 2012 | 1.35 | 1.18 | 1.21 | 1.25 | 1.34 | 1.43 | 1.68 | 1.67 | 2.00 | 1.96 | 1.97 | 1.85 |

| 2013 | 1.63 | 1.32 | 1.30 | 1.33 | 1.35 | 1.37 | 1.65 | 1.74 | 1.90 | 1.93 | 1.83 | 1.67 |

| 2014 | 1.49 | 1.21 | 1.39 | 1.45 | 1.53 | 1.43 | 1.55 | 1.94 | 1.80 | 1.79 | 1.68 | 1.37 |

| 2015 | 1.15 | 1.07 | 1.33 | 1.55 | 1.64 | 1.61 | 1.68 | 1.89 | 1.81 | 1.84 | 1.57 | 1.34 |

| 2016 | 1.04 | 0.97 | 1.10 | 1.17 | 1.27 | 1.45 | 1.47 | 1.54 | 1.57 | 1.51 | 1.46 | 1.36 |

| 2017 | 1.20 | 1.13 | 1.32 | 1.38 | 1.45 | 1.37 | 1.61 | 1.61 | 1.62 | 1.78 | 1.75 | 1.67 |

| 2018 | 1.48 | 1.22 | 1.38 | 1.36 | 1.32 | 1.17 | 1.28 | 1.39 | 1.62 | 1.70 | 1.63 | 1.61 |

| 2019 | 1.52 | 1.34 | 1.42 | 1.42 | 1.40 | 1.34 | 1.49 | 1.55 | 1.57 | 1.57 | 1.35 | 1.22 |

| 2020 | 1.06 | 1.10 | 1.19 | 1.41 | 1.44 | 1.65 | 1.59 | 1.62 | 1.65 | 1.50 | 1.33 | 1.19 |

| 2021 | 1.03 | 0.97 | 1.20 | 1.28 | 1.32 | 1.35 | 1.30 |

Appendix C

Table A3.

Derived monthly Fresh Fruit Bunch Index (FFBI) in tons per hectare from February 1986 to June 2021 in Malaysia.

Table A3.

Derived monthly Fresh Fruit Bunch Index (FFBI) in tons per hectare from February 1986 to June 2021 in Malaysia.

| January | February | March | April | May | June | July | August | September | October | November | December | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1986 | NULL | 0.20 | 0.06 | −0.07 | −0.16 | −0.13 | −0.10 | 0.00 | 0.04 | 0.07 | −0.01 | −0.13 |

| 1987 | −0.17 | −0.21 | −0.20 | −0.24 | −0.17 | −0.10 | 0.04 | 0.11 | 0.10 | −0.01 | −0.18 | −0.29 |

| 1988 | −0.30 | −0.24 | −0.14 | −0.10 | 0.00 | 0.04 | 0.11 | 0.03 | −0.03 | −0.10 | −0.10 | −0.10 |

| 1989 | −0.10 | −0.12 | −0.12 | −0.11 | −0.03 | 0.07 | 0.19 | 0.26 | 0.27 | 0.28 | 0.25 | 0.20 |

| 1990 | 0.11 | 0.05 | 0.01 | 0.07 | 0.07 | 0.12 | 0.09 | 0.10 | 0.05 | −0.05 | −0.16 | −0.25 |

| 1991 | −0.27 | −0.21 | −0.10 | 0.01 | 0.01 | 0.04 | 0.05 | 0.12 | 0.11 | 0.00 | −0.12 | −0.21 |

| 1992 | −0.19 | −0.15 | −0.10 | −0.08 | −0.07 | −0.04 | −0.02 | 0.04 | 0.01 | 0.02 | −0.02 | −0.05 |

| 1993 | −0.06 | −0.08 | 0.04 | 0.09 | 0.21 | 0.20 | 0.23 | 0.31 | 0.32 | 0.29 | 0.15 | 0.09 |

| 1994 | 0.03 | −0.02 | −0.08 | −0.13 | −0.13 | −0.13 | −0.08 | −0.02 | 0.07 | 0.11 | 0.16 | 0.18 |

| 1995 | 0.18 | 0.13 | 0.05 | −0.03 | −0.06 | −0.05 | −0.01 | 0.00 | 0.01 | 0.06 | 0.09 | 0.09 |

| 1996 | 0.00 | 0.00 | −0.01 | 0.09 | 0.09 | 0.09 | 0.08 | 0.05 | 0.10 | 0.05 | 0.02 | −0.06 |

| 1997 | −0.07 | −0.02 | 0.07 | 0.14 | 0.16 | 0.15 | 0.13 | 0.10 | 0.08 | 0.05 | −0.04 | −0.16 |

| 1998 | −0.16 | −0.16 | −0.13 | −0.20 | −0.18 | −0.16 | −0.14 | −0.16 | −0.22 | −0.27 | −0.32 | −0.33 |

| 1999 | −0.28 | −0.17 | 0.02 | 0.19 | 0.29 | 0.24 | 0.13 | 0.05 | 0.04 | 0.06 | 0.10 | 0.09 |

| 2000 | 0.09 | 0.02 | −0.03 | −0.10 | −0.13 | −0.19 | −0.18 | −0.11 | 0.04 | 0.17 | 0.19 | 0.28 |

| 2001 | 0.30 | 0.31 | 0.19 | 0.11 | 0.05 | −0.05 | −0.14 | −0.15 | −0.08 | −0.02 | 0.02 | 0.07 |

| 2002 | 0.07 | 0.06 | −0.02 | −0.05 | −0.08 | −0.10 | −0.09 | −0.06 | −0.02 | −0.04 | −0.07 | −0.08 |

| 2003 | −0.06 | −0.01 | 0.05 | 0.14 | 0.19 | 0.20 | 0.16 | 0.08 | −0.03 | −0.13 | −0.07 | −0.05 |

| 2004 | 0.02 | −0.05 | −0.05 | −0.06 | −0.03 | 0.01 | 0.01 | 0.05 | 0.01 | 0.03 | 0.08 | 0.15 |

| 2005 | 0.19 | 0.17 | 0.16 | 0.16 | 0.09 | 0.03 | −0.02 | −0.03 | −0.05 | −0.05 | −0.07 | −0.08 |

| 2006 | 0.00 | 0.08 | 0.18 | 0.20 | 0.18 | 0.13 | 0.10 | 0.09 | 0.04 | 0.08 | 0.02 | 0.10 |

| 2007 | 0.05 | 0.06 | −0.01 | −0.04 | −0.08 | −0.06 | −0.02 | 0.04 | 0.05 | 0.12 | 0.17 | 0.28 |

| 2008 | 0.27 | 0.26 | 0.18 | 0.15 | 0.13 | 0.14 | 0.11 | 0.03 | 0.01 | 0.06 | 0.16 | 0.20 |

| 2009 | 0.17 | 0.14 | 0.06 | 0.03 | 0.00 | −0.01 | −0.05 | −0.09 | 0.03 | 0.10 | 0.21 | 0.14 |

| 2010 | 0.12 | 0.09 | 0.04 | 0.02 | −0.03 | −0.02 | −0.02 | −0.07 | −0.11 | −0.14 | −0.12 | −0.14 |

| 2011 | −0.10 | 0.01 | 0.13 | 0.23 | 0.26 | 0.24 | 0.13 | 0.07 | 0.06 | 0.08 | 0.09 | 0.05 |

| 2012 | 0.05 | −0.03 | −0.09 | −0.14 | −0.13 | −0.06 | −0.04 | 0.04 | 0.07 | 0.20 | 0.27 | 0.33 |

| 2013 | 0.27 | 0.14 | 0.01 | −0.08 | −0.12 | −0.09 | −0.04 | 0.02 | 0.05 | 0.11 | 0.16 | 0.17 |

| 2014 | 0.13 | 0.09 | 0.04 | 0.05 | 0.00 | −0.04 | 0.01 | 0.02 | 0.04 | −0.02 | −0.04 | −0.09 |

| 2015 | −0.13 | −0.09 | 0.01 | 0.10 | 0.13 | 0.10 | 0.10 | 0.05 | 0.04 | −0.04 | −0.07 | −0.17 |

| 2016 | −0.21 | −0.24 | −0.23 | −0.22 | −0.17 | −0.15 | −0.14 | −0.22 | −0.26 | −0.27 | −0.21 | −0.15 |

| 2017 | −0.10 | −0.06 | −0.03 | −0.02 | −0.07 | −0.07 | −0.10 | −0.13 | −0.13 | −0.06 | 0.08 | 0.14 |

| 2018 | 0.13 | 0.08 | 0.01 | −0.05 | −0.18 | −0.29 | −0.35 | −0.31 | −0.23 | −0.13 | −0.01 | 0.10 |

| 2019 | 0.16 | 0.15 | 0.09 | 0.01 | −0.08 | −0.13 | −0.17 | −0.21 | −0.24 | −0.28 | −0.27 | −0.28 |

| 2020 | −0.20 | −0.16 | −0.07 | −0.06 | 0.03 | 0.02 | −0.01 | −0.12 | −0.21 | −0.29 | −0.31 | −0.31 |

| 2021 | −0.26 | −0.21 | −0.16 | −0.14 | −0.15 | −0.22 | NULL |

Appendix D

Table A4.

Oceanic Niño Index (ONI) from January 1983 to June 2021 [18].

Table A4.

Oceanic Niño Index (ONI) from January 1983 to June 2021 [18].

| January | February | March | April | May | June | July | August | September | October | November | December | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1983 | 2.2 | 1.9 | 1.5 | 1.3 | 1.1 | 0.7 | 0.3 | −0.1 | −0.5 | −0.8 | −1.0 | −0.9 |

| 1984 | −0.6 | −0.4 | −0.3 | −0.4 | −0.5 | −0.4 | −0.3 | −0.2 | −0.2 | −0.6 | −0.9 | −1.1 |

| 1985 | −1.0 | −0.8 | −0.8 | −0.8 | −0.8 | −0.6 | −0.5 | −0.5 | −0.4 | −0.3 | −0.3 | −0.4 |

| 1986 | −0.5 | −0.5 | −0.3 | −0.2 | −0.1 | 0.0 | 0.2 | 0.4 | 0.7 | 0.9 | 1.1 | 1.2 |

| 1987 | 1.2 | 1.2 | 1.1 | 0.9 | 1.0 | 1.2 | 1.5 | 1.7 | 1.6 | 1.5 | 1.3 | 1.1 |

| 1988 | 0.8 | 0.5 | 0.1 | −0.3 | −0.9 | −1.3 | −1.3 | −1.1 | −1.2 | −1.5 | −1.8 | −1.8 |

| 1989 | −1.7 | −1.4 | −1.1 | −0.8 | −0.6 | −0.4 | −0.3 | −0.3 | −0.2 | −0.2 | −0.2 | −0.1 |

| 1990 | 0.1 | 0.2 | 0.3 | 0.3 | 0.3 | 0.3 | 0.3 | 0.4 | 0.4 | 0.3 | 0.4 | 0.4 |

| 1991 | 0.4 | 0.3 | 0.2 | 0.3 | 0.5 | 0.6 | 0.7 | 0.6 | 0.6 | 0.8 | 1.2 | 1.5 |

| 1992 | 1.7 | 1.6 | 1.5 | 1.3 | 1.1 | 0.7 | 0.4 | 0.1 | −0.1 | −0.2 | −0.3 | −0.1 |

| 1993 | 0.1 | 0.3 | 0.5 | 0.7 | 0.7 | 0.6 | 0.3 | 0.3 | 0.2 | 0.1 | 0.0 | 0.1 |

| 1994 | 0.1 | 0.1 | 0.2 | 0.3 | 0.4 | 0.4 | 0.4 | 0.4 | 0.6 | 0.7 | 1.0 | 1.1 |

| 1995 | 1.0 | 0.7 | 0.5 | 0.3 | 0.1 | 0.0 | −0.2 | −0.5 | −0.8 | −1.0 | −1.0 | −1.0 |

| 1996 | −0.9 | −0.8 | −0.6 | −0.4 | −0.3 | −0.3 | −0.3 | −0.3 | −0.4 | −0.4 | −0.4 | −0.5 |

| 1997 | −0.5 | −0.4 | −0.1 | 0.3 | 0.8 | 1.2 | 1.6 | 1.9 | 2.1 | 2.3 | 2.4 | 2.4 |

| 1998 | 2.2 | 1.9 | 1.4 | 1.0 | 0.5 | −0.1 | −0.8 | −1.1 | −1.3 | −1.4 | −1.5 | −1.6 |

| 1999 | −1.5 | −1.3 | −1.1 | −1.0 | −1.0 | −1.0 | −1.1 | −1.1 | −1.2 | −1.3 | −1.5 | −1.7 |

| 2000 | −1.7 | −1.4 | −1.1 | −0.8 | −0.7 | −0.6 | −0.6 | −0.5 | −0.5 | −0.6 | −0.7 | −0.7 |

| 2001 | −0.7 | −0.5 | −0.4 | −0.3 | −0.3 | −0.1 | −0.1 | −0.1 | −0.2 | −0.3 | −0.3 | −0.3 |

| 2002 | −0.1 | 0.0 | 0.1 | 0.2 | 0.4 | 0.7 | 0.8 | 0.9 | 1.0 | 1.2 | 1.3 | 1.1 |

| 2003 | 0.9 | 0.6 | 0.4 | 0.0 | −0.3 | −0.2 | 0.1 | 0.2 | 0.3 | 0.3 | 0.4 | 0.4 |

| 2004 | 0.4 | 0.3 | 0.2 | 0.2 | 0.2 | 0.3 | 0.5 | 0.6 | 0.7 | 0.7 | 0.7 | 0.7 |

| 2005 | 0.6 | 0.6 | 0.4 | 0.4 | 0.3 | 0.1 | −0.1 | −0.1 | −0.1 | −0.3 | −0.6 | −0.8 |

| 2006 | −0.9 | −0.8 | −0.6 | −0.4 | −0.1 | 0.0 | 0.1 | 0.3 | 0.5 | 0.8 | 0.9 | 0.9 |

| 2007 | 0.7 | 0.2 | −0.1 | −0.3 | −0.4 | −0.5 | −0.6 | −0.8 | −1.1 | −1.3 | −1.5 | −1.6 |

| 2008 | −1.6 | −1.5 | −1.3 | −1.0 | −0.8 | −0.6 | −0.4 | −0.2 | −0.2 | −0.4 | −0.6 | −0.7 |

| 2009 | −0.8 | −0.8 | −0.6 | −0.3 | 0.0 | 0.3 | 0.5 | 0.6 | 0.7 | 1.0 | 1.4 | 1.6 |

| 2010 | 1.5 | 1.2 | 0.8 | 0.4 | −0.2 | −0.7 | −1.0 | −1.3 | −1.6 | −1.6 | −1.6 | −1.6 |

| 2011 | −1.4 | −1.2 | −0.9 | −0.7 | −0.6 | −0.4 | −0.5 | −0.6 | −0.8 | −1.0 | −1.1 | −1.0 |

| 2012 | −0.9 | −0.7 | −0.6 | −0.5 | −0.3 | 0.0 | 0.2 | 0.4 | 0.4 | 0.3 | 0.1 | −0.2 |

| 2013 | −0.4 | −0.4 | −0.3 | −0.3 | −0.4 | −0.4 | −0.4 | −0.3 | −0.3 | −0.2 | −0.2 | −0.3 |

| 2014 | −0.4 | −0.5 | −0.3 | 0.0 | 0.2 | 0.2 | 0.0 | 0.1 | 0.2 | 0.5 | 0.6 | 0.7 |

| 2015 | 0.5 | 0.5 | 0.5 | 0.7 | 0.9 | 1.2 | 1.5 | 1.9 | 2.2 | 2.4 | 2.6 | 2.6 |

| 2016 | 2.5 | 2.1 | 1.6 | 0.9 | 0.4 | −0.1 | −0.4 | −0.5 | −0.6 | −0.7 | −0.7 | −0.6 |

| 2017 | −0.3 | −0.2 | 0.1 | 0.2 | 0.3 | 0.3 | 0.1 | −0.1 | −0.4 | −0.7 | −0.8 | −1.0 |

| 2018 | −0.9 | −0.9 | −0.7 | −0.5 | −0.2 | 0.0 | 0.1 | 0.2 | 0.5 | 0.8 | 0.9 | 0.8 |

| 2019 | 0.7 | 0.7 | 0.7 | 0.7 | 0.5 | 0.5 | 0.3 | 0.1 | 0.2 | 0.3 | 0.5 | 0.5 |

| 2020 | 0.5 | 0.5 | 0.4 | 0.2 | −0.1 | −0.3 | −0.4 | −0.6 | −0.9 | −1.2 | −1.3 | −1.2 |

| 2021 | −1.0 | −0.9 | −0.8 | −0.7 | −0.5 | −0.4 |

Appendix E

Figure A1.

FFB time series, ARIMA (2,0,2) (1,1,1) model with ONI as predictor (adjusted R-squared = 0.8274). Modelled period: February 1986 to June 2021 (N = 425). 30 months forecasted period: July 2021 to December 2023 (N = 30, highlighted area of Figure A1). Note: Dash lines represent BCa 99% confidence interval range of monthly oil palm yield in Malaysia. FFB model predicts monthly oil palm yield to fluctuate around the BCa 99% confidence interval range in next 30 months.

Figure A1.

FFB time series, ARIMA (2,0,2) (1,1,1) model with ONI as predictor (adjusted R-squared = 0.8274). Modelled period: February 1986 to June 2021 (N = 425). 30 months forecasted period: July 2021 to December 2023 (N = 30, highlighted area of Figure A1). Note: Dash lines represent BCa 99% confidence interval range of monthly oil palm yield in Malaysia. FFB model predicts monthly oil palm yield to fluctuate around the BCa 99% confidence interval range in next 30 months.

Appendix F

Figure A2.

The new FFBI time series, ARIMA (3,1,3) (0,0,1) model with ONI as predictor (adjusted R-squared = 0.9312). Modelled period: February 1986 to June 2021 (N = 425). 30 months forecasted period: July 2021 to December 2023 (N = 30, highlighted area of Figure A2). Note: Dash lines represent BCa 99% confidence interval range of monthly oil palm yield in Malaysia. Unlike FFB model (Figure A1), FFBI model revealed a future monthly under yield concern of Malaysian oil palm industry.

Figure A2.

The new FFBI time series, ARIMA (3,1,3) (0,0,1) model with ONI as predictor (adjusted R-squared = 0.9312). Modelled period: February 1986 to June 2021 (N = 425). 30 months forecasted period: July 2021 to December 2023 (N = 30, highlighted area of Figure A2). Note: Dash lines represent BCa 99% confidence interval range of monthly oil palm yield in Malaysia. Unlike FFB model (Figure A1), FFBI model revealed a future monthly under yield concern of Malaysian oil palm industry.

Appendix G

Table A5.

FFBI time series forecasting validation models’ summary with residual analyses using descriptive and inferential statistics at α = 0.01.

Table A5.

FFBI time series forecasting validation models’ summary with residual analyses using descriptive and inferential statistics at α = 0.01.

| Modelled Period | 1986–2015 | 1987–2016 | 1988–2017 | 1989–2018 | 1990–2019 | 1991–2020 |

|---|---|---|---|---|---|---|

| Model | ARIMA (1,1,5) (0,0,1) | ARIMA (0,0,4) (0,0,0) | ARIMA (3,1,3) (0,0,1) | ARIMA (0,0,4) (0,0,0) | ARIMA (0,0,4) (0,0,1) | ARIMA (3,1,3) (0,0,1) |

| R−Squared | 0.9285 | 0.9164 | 0.9281 | 0.9198 | 0.9238 | 0.9354 |

| Adjusted R−Squared | 0.9283 | 0.9162 | 0.9279 | 0.9196 | 0.9236 | 0.9352 |

| Residual Skewness | −0.5314 | −0.1992 | −0.7146 | −0.3753 | −0.5032 | −0.7131 |

| Residual Range | 0.2310 | 0.3372 | 0.2288 | 0.2741 | 0.2405 | 0.2265 |

| Residual Median | 0.0001 | −0.0002 | 0.0001 | 0.0020 | 0.0015 | 0.0036 |

| (BCa 99% CI) | [−0.0044, 0.0063] | [−0.0058, 0.0083] | [−0.0052, 0.0063] | [−0.0039, 0.0064] | [−0.0048, 0.0081] | [−0.0028, 0.0079] |

| Residual Standard Deviation | 0.0342 | 0.0375 | 0.0345 | 0.0374 | 0.0367 | 0.0343 |

| (BCa 99% CI) | [0.0304, 0.0382] | [0.0331, 0.043] | [0.0303, 0.0387] | [0.0333, 0.0415] | [0.0326, 0.0408] | [0.0305, 0.0382] |

| Residual Variance | 0.0012 | 0.0014 | 0.0012 | 0.0014 | 0.0013 | 0.0012 |

| (BCa 99% CI) | [0.0009, 0.0015] | [0.0011, 0.0018] | [0.0009, 0.0015] | [0.0011, 0.0017] | [0.0011, 0.0017] | [0.0009, 0.0015] |

Appendix H

Figure A3.

FFBI time series forecasting validation models (total of 6 models combined). Modelled period: moving 30 years starting from 1986 (N = 360) with 12 months forecasted period. Note: Predicted FFBI (Red dash line) from January 2016 to December 2016 are values predicted from 1986–2015 model and so on with a moving 30 years validation.

Figure A3.

FFBI time series forecasting validation models (total of 6 models combined). Modelled period: moving 30 years starting from 1986 (N = 360) with 12 months forecasted period. Note: Predicted FFBI (Red dash line) from January 2016 to December 2016 are values predicted from 1986–2015 model and so on with a moving 30 years validation.

Appendix I

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Appendix J

Table A6.

Monthly crude palm oil (CPO) price in Malaysian Ringgit (MYR) per ton from January 1986 to June 2021 [52].

Table A6.

Monthly crude palm oil (CPO) price in Malaysian Ringgit (MYR) per ton from January 1986 to June 2021 [52].

| January | February | March | April | May | June | July | August | September | October | November | December | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1986 | 637 | 476 | 653 | 553 | 589 | 573 | 504 | 448 | 504 | 723 | 718 | 712 |

| 1987 | 900 | 750 | 748 | 690 | 725 | 751 | 678 | 721 | 800 | 760 | 883 | 1093 |

| 1988 | 1068 | 895 | 906 | 916 | 1017 | 1220 | 1011 | 981 | 979 | 1073 | 985 | 967 |

| 1989 | 955 | 942 | 903 | 922 | 904 | 810 | 668 | 699 | 779 | 787 | 633 | 659 |

| 1990 | 696 | 683 | 695 | 705 | 700 | 710 | 701 | 708 | 707 | 752 | 863 | 896 |

| 1991 | 848 | 850 | 770 | 775 | 755 | 768 | 867 | 791 | 807 | 883 | 884 | 914 |

| 1992 | 888 | 891 | 905 | 848 | 848 | 859 | 826 | 841 | 868 | 917 | 938 | 953 |

| 1993 | 960 | 968 | 933 | 875 | 851 | 820 | 847 | 852 | 780 | 787 | 857 | 992 |

| 1994 | 970 | 943 | 974 | 1089 | 1107 | 1086 | 1185 | 1278 | 1404 | 1478 | 1647 | 1580 |

| 1995 | 1449 | 1551 | 1489 | 1311 | 1296 | 1345 | 1419 | 1321 | 1355 | 1417 | 1392 | 1354 |

| 1996 | 1185 | 1178 | 1214 | 1250 | 1188 | 1077 | 1099 | 1238 | 1142 | 1181 | 1207 | 1255 |

| 1997 | 1296 | 1264 | 1258 | 1281 | 1230 | 1157 | 1163 | 1305 | 1573 | 1709 | 1784 | 2075 |

| 1998 | 2392 | 2117 | 2145 | 2295 | 2292 | 2323 | 2428 | 2499 | 2234 | 2333 | 2302 | 2156 |

| 1999 | 1854 | 1563 | 1523 | 1586 | 1355 | 1232 | 988 | 1310 | 1239 | 1235 | 1245 | 1176 |

| 2000 | 1133 | 1040 | 1196 | 1149 | 1035 | 1030 | 1033 | 1003 | 901 | 852 | 822 | 804 |

| 2001 | 780 | 751 | 880 | 766 | 764 | 865 | 1236 | 1069 | 940 | 990 | 1097 | 1146 |

| 2002 | 1155 | 1150 | 1152 | 1204 | 1426 | 1355 | 1502 | 1470 | 1361 | 1510 | 1588 | 1644 |

| 2003 | 1619 | 1594 | 1433 | 1355 | 1416 | 1408 | 1280 | 1339 | 1460 | 1762 | 1737 | 1774 |

| 2004 | 1778 | 1947 | 1937 | 1888 | 1610 | 1550 | 1419 | 1515 | 1413 | 1438 | 1425 | 1387 |

| 2005 | 1274 | 1403 | 1461 | 1429 | 1412 | 1408 | 1377 | 1370 | 1460 | 1445 | 1391 | 1415 |

| 2006 | 1443 | 1507 | 1437 | 1481 | 1444 | 1491 | 1641 | 1578 | 1559 | 1661 | 1940 | 1995 |

| 2007 | 1900 | 1960 | 2070 | 2214 | 2581 | 2427 | 2608 | 2420 | 2644 | 2880 | 2930 | 3050 |

| 2008 | 3232 | 4005 | 3395 | 3395 | 3498 | 3598 | 3050 | 2620 | 2090 | 1515 | 1632 | 1695 |

| 2009 | 1779 | 1895 | 2000 | 2595 | 2560 | 2230 | 2189 | 2370 | 2105 | 2208 | 2472 | 2663 |

| 2010 | 2445 | 2595 | 2556 | 2558 | 2436 | 2373 | 2517 | 2570 | 2730 | 3061 | 3412 | 3788 |

| 2011 | 3809 | 3472 | 3326 | 3270 | 3393 | 3072 | 3096 | 3009 | 2905 | 2938 | 3018 | 3175 |

| 2012 | 3078 | 3270 | 3433 | 3471 | 3101 | 3020 | 2980 | 3019 | 2546 | 2496 | 2370 | 2438 |

| 2013 | 2557 | 2397 | 2378 | 2286 | 2397 | 2344 | 2236 | 2404 | 2320 | 2593 | 2654 | 2659 |

| 2014 | 2559 | 2800 | 2634 | 2623 | 2423 | 2426 | 2257 | 1929 | 2217 | 2306 | 2172 | 2266 |

| 2015 | 2146 | 2305 | 2165 | 2102 | 2216 | 2229 | 2120 | 1991 | 2375 | 2363 | 2344 | 2485 |

| 2016 | 2443 | 2548 | 2725 | 2593 | 2620 | 2353 | 2316 | 2526 | 2636 | 2763 | 3073 | 3109 |

| 2017 | 3029 | 2770 | 2646 | 2508 | 2499 | 2459 | 2675 | 2706 | 2695 | 2815 | 2603 | 2503 |

| 2018 | 2492 | 2559 | 2425 | 2362 | 2429 | 2326 | 2194 | 2248 | 2174 | 2150 | 2040 | 2121 |

| 2019 | 2299 | 2121 | 2106 | 2095 | 2069 | 1951 | 2070 | 2234 | 2135 | 2485 | 2744 | 3052 |

| 2020 | 2604 | 2319 | 2402 | 2088 | 2292 | 2297 | 2677 | 2738 | 2714 | 3011 | 3305 | 3600 |

| 2021 | 3490 | 3742 | 3612 | 3868 | 3919 | 3599 |

Appendix K

Table A7.

Annual oil palm matured area, oil extraction rate (OER) and fresh fruit bunch (FFB) yield from 1986 to 2020 in Malaysia [5,6,7].

| Year | Matured Area (ha) | OER (%) | FFB Yield (t/ha) |

|---|---|---|---|

| 1986 | 1,360,579 | 19.62 | 22.15 |

| 1987 | 1,373,147 | 19.87 | 17.10 |

| 1988 | 1,530,906 | 19.87 | 17.52 |

| 1989 | 1,672,096 | 19.78 | 19.57 |

| 1990 | 1,746,054 | 19.64 | 18.53 |

| 1991 | 1,826,267 | 19.47 | 17.85 |

| 1992 | 1,890,268 | 19.21 | 17.83 |

| 1993 | 2,020,516 | 18.67 | 20.26 |

| 1994 | 2,144,080 | 18.63 | 18.42 |

| 1995 | 2,243,065 | 18.51 | 18.93 |

| 1996 | 2,353,147 | 18.71 | 18.95 |

| 1997 | 2,513,183 | 19.03 | 19.10 |

| 1998 | 2,638,020 | 18.91 | 15.98 |

| 1999 | 2,856,701 | 18.60 | 19.26 |

| 2000 | 2,941,791 | 18.86 | 18.33 |

| 2001 | 3,005,267 | 19.22 | 19.14 |

| 2002 | 3,188,307 | 19.91 | 17.97 |

| 2003 | 3,303,133 | 19.75 | 18.99 |

| 2004 | 3,450,960 | 20.03 | 18.60 |

| 2005 | 3,631,440 | 20.15 | 18.88 |

| 2006 | 3,703,254 | 20.04 | 19.60 |

| 2007 | 3,764,389 | 20.13 | 19.03 |

| 2008 | 3,915,924 | 20.21 | 20.18 |

| 2009 | 4,075,702 | 20.49 | 19.20 |

| 2010 | 4,202,213 | 20.45 | 18.03 |

| 2011 | 4,281,837 | 20.35 | 19.69 |

| 2012 | 4,352,872 | 20.35 | 18.89 |

| 2013 | 4,526,089 | 20.25 | 19.02 |

| 2014 | 4,689,321 | 20.62 | 18.63 |

| 2015 | 4,859,397 | 20.46 | 18.48 |

| 2016 | 5,001,438 | 20.18 | 15.91 |

| 2017 | 5,110,713 | 19.72 | 17.89 |

| 2018 | 5,189,344 | 19.95 | 17.16 |

| 2019 | 5,216,822 | 20.21 | 17.19 |

| 2020 | 5,231,743 | 19.92 | 16.73 |

Annual FFB yields highlighted in red are the ones below the mean 99% confidence interval [18.02, 19.08]. All FFB yields below the mean confidence limit are associated with El Niño years, except for 2017 and after. Although there was a weak El Niño in 2018/19, the annual FFB yields never fall below the mean confidence limit due to weak El Niño based on the historical 35 years records.

References

- Mielke, T. Global supply, demand and price outlook of oils and fats in 2018/19. In Proceedings of the GLOBOIL, Mumbai, India, 28 September 2018. [Google Scholar]

- Oettli, P.; Behera, S.K.; Yamagata, T. Climate based predictability of oil palm tree yield in Malaysia. Sci. Rep. 2018, 8, 2271. [Google Scholar] [CrossRef] [Green Version]

- Malaysian Palm Oil Industry. Available online: http://www.palmoilworld.org/about_malaysian-industry.html (accessed on 17 August 2021).

- World Energy Council. Biofuels: Policies, Standards and Technologies; World Energy Council: London, UK, 2010. [Google Scholar]

- Palm Oil Registration & Licensing Authority (PORLA). PORLA Palm Oil Statistics; PORLA: Kelana Jaya, Malaysia, 1986–1999. [Google Scholar]

- Malaysian Palm Oil Board (MPOB). Malaysian Oil Palm Statistics; MPOB: Bangi, Malaysia, 2000–2020. [Google Scholar]

- Economics and Industry Development Division. Available online: https://bepi.mpob.gov.my/index.php/en/ (accessed on 17 August 2021).

- Wicke, B.; Sikkema, R.; Dornburg, V.; Junginger, M.; Faaij, A. Drivers of Land Use Changes and the Role of Palm Oil Production in Indonesia and Malaysia; Universiteit Utrecht Copernicus Institute: Utrecht, The Netherlands, 2008. [Google Scholar]

- Ling, A.H. Global palm oil trade—Prospects and outlook. In Proceedings of the Malaysian-China Business Forum, Kuala Lumpur, Malaysia, 4 March 2019. [Google Scholar]

- Barcelos, E.; Rios, S.D.A.; Cunha, R.N.V.; Lopes, R.; Motoike, S.Y.; Babiychuk, E.; Skirycz, A.; Kushnir, S. Oil palm natural diversity and the potential for yield improvement. Front. Plant. Sci. 2015, 6, 190. [Google Scholar] [CrossRef] [PubMed]

- World Development Indicators. Available online: https://databank.worldbank.org/reports.aspx?source=2&country=MYS# (accessed on 25 August 2021).

- Covert 1 US Dollar to Malaysian Ringgit. Available online: https://www.xe.com/currencyconverter/convert/?Amount=1&From=USD&To=MYR (accessed on 25 August 2021).

- Overview of the Malaysian Oil Palm Industry 2020. Available online: https://bepi.mpob.gov.my/images/overview/Overview_of_Industry_2020.pdf (accessed on 28 August 2021).

- Which Countries Produce the Most Palm Oil? Available online: https://www.statista.com/chart/23097/amount-of-palm-oil-produced-in-selected-countries/ (accessed on 25 October 2021).

- What is El Niño-Southern Oscillation (ENSO)? Available online: https://www.weather.gov/mhx/ensowhat (accessed on 17 August 2021).

- What are El Niño and La Niña? Available online: https://oceanservice.noaa.gov/facts/ninonina.html (accessed on 25 October 2021).

- El Niño. Available online: https://www.nationalgeographic.org/encyclopedia/el-nino/ (accessed on 25 October 2021).

- Cold & Warm Episodes by Season. Available online: https://origin.cpc.ncep.noaa.gov/products/analysis_monitoring/ensostuff/ONI_v5.php (accessed on 25 October 2021).

- El Niño and La Niña Years and Intensities. Available online: https://ggweather.com/enso/oni.htm (accessed on 17 August 2021).

- Shanmuganathan, S.; Narayanan, A. Modelling the climate change effects on Malaysia’s oil palm yield. In Proceedings of the 2012 IEEE Symposium on e-Learning, e-Management and e-Services (IS3e 2012), Kuala Lumpur, Malaysia, 21–24 October 2012. [Google Scholar]

- Tawang, A.; Tengku Ahmad, T.A.; Abdullah, M.Y. Stabilization of Upland Agriculture under El Nino Induced Climatic Risk: Impact Assessment and Mitigation Measures in Malaysia; United Nation: New York, NY, USA, 2001. [Google Scholar]

- Kamil, N.N.; Omar, S.F. Climate variability and its impact on the palm oil industry. Oil Palm Ind. Econ. J. 2016, 16, 18–30. [Google Scholar]

- Wójtowicz, M.; Wójtowicz, A. The effect of climate change on linolenic fatty acid in oilseed rape. Agronomy 2020, 10, 2003. [Google Scholar] [CrossRef]

- Sobko, O.; Stahl, A.; Hahn, V.; Zikeli, S.; Claupein, W.; Gruber, S. Environmental effects on soybean (Glyciune Max (L.) Merr) production in Central and South Germany. Agronomy 2020, 10, 1847. [Google Scholar] [CrossRef]

- Kamil, N.N.; Omar, S.F. The impact of El Niño and La Niña on Malaysian palm oil industry. Oil Palm Bull. 2017, 74, 1–6. [Google Scholar]

- Harun, M.H.; Mohammad, A.T.; Noor, M.R.M.; Din, A.K.; Latiff, J.; Sani, A.R.A.; Abdullah, R. Impact of El Niño occurrence on oil palm yield in Malaysia. Planter 2010, 86, 837–852. [Google Scholar]

- Shanmuganathan, S.; Narayanan, A.; Mohamed, M.; Ibrahim, R.; Khalid, H. A hybrid approach to modelling the climate change effects on Malaysia’s oil palm yield at the regional scale. In Recent Advances on Soft Computing and Data Mining; Herawan, T., Ghazali, R., Deris, M., Eds.; Springer: Basel, Switzerland, 2014; pp. 335–345. [Google Scholar]

- Puah, P.W.; Sidik, M.J. Impacts of rainfall, temperature and recent El Niños on fisheries and agricultural products in the west coast of Sabah [2000–2010]. Borneo Sci. 2011, 28, 73–85. [Google Scholar]

- Rahman, A.K.A.; Abdullah, R.; Balu, N.; Shariff, F.M. The impact of La Niña and El Niño events on crude palm oil prices: An econometric analysis. Oil Palm Ind. Econ. J. 2013, 13, 38–51. [Google Scholar]

- Malaysia. Available online: https://www.nationsonline.org/oneworld/malaysia.htm (accessed on 25 October 2021).

- Land Area (sq. km)—Malaysia. Available online: https://data.worldbank.org/indicator/AG.LND.TOTL.K2?locations=MY (accessed on 25 October 2021).

- GeoRSPO—RSPO Mapbuilder App. Available online: https://rspo.org/members/georspo (accessed on 25 October 2021).

- Ling, L.; Yusop, Z.; Yap, W.S.; Tan, W.L.; Chow, M.F.; Ling, J.L. A calibrated, watershed-specific SCS-CN method: Application to Wangjiaqiao watershed in the three gorges area. China. Water 2019, 12, 60. [Google Scholar] [CrossRef] [Green Version]

- Conduct and Interpret a Spearman Rank Correlation. Available online: https://www.statisticssolutions.com/free-resources/directory-of-statistical-analyses/spearman-rank-correlation/ (accessed on 27 August 2021).

- Artusi, R.; Verderio, P.; Marubini, E. Bravais-Pearson and Spearman correlation coefficients: Meaning, test of hypothesis and confidence interval. Int. J. Biol. Mark. 2002, 17, 148–151. [Google Scholar] [CrossRef]

- Downloading IBM SPSS Statistics 26. Available online: https://www.ibm.com/support/pages/downloading-ibm-spss-statistics-26 (accessed on 27 August 2021).

- Difference between Adjusted R-squared and R-squared. Available online: https://www.listendata.com/2014/08/adjusted-r-squared.html (accessed on 28 August 2021).

- Adjusted R2/Adjusted R-Squared: What is it Used for? Available online: https://www.statisticshowto.com/probability-and-statistics/statistics-definitions/adjusted-r2/ (accessed on 27 August 2021).

- Ling, L.; Yusop, Z.; Chow, M.F. Urban flood depth estimate with a new calibrated curve number runoff prediction model. IEEE Access 2020, 8, 10915–10923. [Google Scholar] [CrossRef]

- Ling, L.; Yusop, Z.; Ling, J.L. Statistical and Type II Error Assessment of a Runoff Predictive Model in Peninsula Malaysia. Mathematics 2021, 9, 812. [Google Scholar] [CrossRef]

- Ali, R.; Kuriqi, A.; Abubaker, S.; Kisi, O. Long-term trends and seasonality detection of the observed flow in Yangtze River using Mann-Kendall and Sen’s innovative trend method. Water 2019, 11, 1855. [Google Scholar] [CrossRef] [Green Version]

- MAKESENS-Application for Trend Calculation. Available online: https://en.ilmatieteenlaitos.fi/makesens (accessed on 20 June 2021).

- Foreign Agricultural Service (FAS). Commodity Intelligence Report—Malaysia: Stagnating Palm Oil Tields Impede Growth; United States Department of Agriculture (USDA): Washington, DC, USA, 2012. [Google Scholar]

- Malaysia’s Palm Oil Yield to Continue Declining on Labour Shortage. Available online: https://www.theedgemarkets.com/article/malaysias-palm-oil-yield-continue-declining-labour-shortage (accessed on 28 August 2021).

- Palm Oil Analyst Raises 2019 Malaysia Output Forecast to 20m Tonnes. Available online: https://www.thestar.com.my/business/business-news/2019/04/30/palm-oil-analyst-raises-2019-malaysia-output-forecast-to-20mil-tonnes (accessed on 28 August 2021).

- IOI Group Oil Palm Plantations Malaysia 2020 by Age. Available online: https://www.statista.com/statistics/1097997/ioi-group-oil-palm-plantations-in-malaysia-by-age/ (accessed on 28 August 2021).

- Organisation for Economic Co-operation and Development (OECD)/Food and Agriculture Organization (FAO). OECD-FAO Agricultural Outlook 2019–2028; OECD/FAO: Paris, France, 2019. [Google Scholar]

- Banks and Palm Oil. Available online: https://www.banktrack.org/campaign/banks_and_palm_oil (accessed on 25 October 2021).

- Indonesia. Available online: https://climateknowledgeportal.worldbank.org/country/indonesia/climate-data-historical (accessed on 25 October 2021).

- Climate—Thailand. Available online: https://www.climatestotravel.com/climate/thailand (accessed on 25 October 2021).

- Malaysia Information. Available online: https://www.malaysia.gov.my/portal/content/144 (accessed on 25 October 2021).

- Palm Oil. Available online: https://tradingeconomics.com/commodity/palm-oil (accessed on 25 October 2021).

Figure 1.

Market shares of 17 edible oils and fats produced internationally in: (a) 2018/19 and; (b) 1992/93. Created with data from [1].

Figure 1.

Market shares of 17 edible oils and fats produced internationally in: (a) 2018/19 and; (b) 1992/93. Created with data from [1].

Figure 2.

Location map of oil palm plantation areas in Malaysia. Created with data from [32].

Figure 2.

Location map of oil palm plantation areas in Malaysia. Created with data from [32].

Figure 3.

FV function in Microsoft Excel.

Figure 4.

Oil palm yield loss and opportunity loss due to El Niño according to category.

Figure 5.

Monthly cumulative opportunity losses in the Malaysian oil palm industry due to El Niño projected to December 2021.

Figure 5.

Monthly cumulative opportunity losses in the Malaysian oil palm industry due to El Niño projected to December 2021.

| Crop | Oil Yield (t/ha) |

|---|---|

| Palm Oil | 3.82 |

| Palm kernel | 0.45 |

| Palm + Palm kernel oil | 4.27 |

| Rapeseed | 0.69 |

| Sunflower | 0.52 |

| Groundnut | 0.45 |

| Coconut | 0.34 |

| Cottonseed | 0.19 |

| Soybean | 0.38 |

| Corn | 0.15 |

Table 2.

Categories of El Niño events occurred during the period of 1986 to 2021. Created with data from [19].

Table 2.

Categories of El Niño events occurred during the period of 1986 to 2021. Created with data from [19].

| Very Strong | Strong | Moderate | Weak |

|---|---|---|---|

| 1997/98 | 1987/88 | 1986/87 | 2004/05 |

| 2015/16 | 1991/92 | 1994/95 | 2006/07 |

| 2002/03 | 2014/15 | ||

| 2009/10 | 2018/19 |

Table 3.

Average FFB yield for each month from 1986 to 2020 in Malaysia. Created with data from [5,6,7].

| Month | Average FFB Yield (t/ha) |

|---|---|

| January | 1.3194 |

| February | 1.1903 |

| March | 1.3234 |

| April | 1.4049 |

| May | 1.4829 |

| June | 1.5109 |

| July | 1.6329 |

| August | 1.7420 |

| September | 1.8543 |

| October | 1.8146 |

| November | 1.6746 |

| December | 1.4743 |

FFB yields from January 2021 to July 2021 were not included in calculating these averages as data points in the full year of 2021 are still not available.

Table 4.

Shapiro-Wilk normality test results for FFB, FFBI and ONI.

| Variable | p-Value | Normality |

|---|---|---|

| FFB | 0.0103 (<0.05) | Non-normal |

| FFBI | 0.1922 (>0.05) | Normal |

| ONI | 0.0000 (<0.05) | Non-normal |

Table 5.

Spearman’s rho correlation between FFB and FFBI with ONI at lag periods from 0 to 18 months.

Table 5.

Spearman’s rho correlation between FFB and FFBI with ONI at lag periods from 0 to 18 months.

| Lag Period (Months) | FFB & ONI | FFBI & ONI | ||

|---|---|---|---|---|

| Spearman’s rho Coefficient | p-Value | Spearman’s rho Coefficient | p-Value | |

| 0 | −0.027 | 0.578 | −0.064 | 0.188 |

| 1 | −0.029 | 0.557 | −0.087 | 0.074 |

| 2 | −0.030 | 0.540 | −0.106 | 0.029 * |

| 3 | −0.034 | 0.479 | −0.125 | 0.010 ** |

| 4 | −0.049 | 0.317 | −0.154 | 0.001 ** |

| 5 | −0.079 | 0.104 | −0.197 | 0.000 ** |

| 6 | −0.120 | 0.013 * | −0.254 | 0.000 ** |

| 7 | −0.165 | 0.001 ** | −0.313 | 0.000 ** |

| 8 | −0.200 | 0.000 ** | −0.364 | 0.000 ** |

| 9 | −0.217 | 0.000 ** | −0.394 | 0.000 ** |

| 10 | −0.211 | 0.000 ** | −0.399 | 0.000 ** |

| 11 | −0.188 | 0.000 ** | −0.381 | 0.000 ** |

| 12 | −0.159 | 0.001 ** | −0.348 | 0.000 ** |

| 13 | −0.128 | 0.008 ** | −0.303 | 0.000 ** |

| 14 | −0.095 | 0.050 | −0.248 | 0.000 ** |

| 15 | −0.060 | 0.214 | −0.183 | 0.000 ** |

| 16 | −0.030 | 0.542 | −0.112 | 0.021 * |

| 17 | −0.007 | 0.878 | −0.039 | 0.424 |

| 18 | 0.009 | 0.849 | 0.023 | 0.642 |

* Correlation is significant at α = 0.05. ** Correlation is significant at α = 0.01. Lag period refers to the number of months FFB and FFBI are delayed corresponding to the ONI at that month.

Table 6.

FFB and FFBI time series forecasting models’ summary with residual analyses using descriptive and inferential statistics at α = 0.01.

Table 6.

FFB and FFBI time series forecasting models’ summary with residual analyses using descriptive and inferential statistics at α = 0.01.

| Dependent Variable | FFB (tons/Hectare) | New FFBI (tons/Hectare) |

|---|---|---|

| Predictor | ONI | ONI |

| Modelled Period | Feb 1986–Jun 2021 (N = 425) | Feb 1986–Jun 2021 (N = 425) |

| Forecasted Period | Jul 2021–Dec 2023 (N = 30) | Jul 2021–Dec 2023 (N = 30) |

| Model | ARIMA (2,0,2) (1,1,1) | ARIMA (3,1,3) (0,0,1) |

| Adjusted R-Squared | 0.8274 | 0.9312 |

| Residual Sum of Squares (RSS) | 4.6876 | 0.5459 |

| Residual Skewness | −0.6903 | −0.4162 |

| Residual Range | 0.7644 | 0.2790 |

| Residual Median | 0.0077 | 0.0051 |

| Residual Median (BCa 99% CI) | [−0.0076, 0.0258] | [−0.0001, 0.0096] |

| Residual Standard Deviation | 0.1067 | 0.0359 |

| Residual Standard Deviation (BCa 99% CI) | [0.0941, 0.1192] | [0.0320, 0.0396] |

| Residual Variance | 0.0114 | 0.0013 |

| Residual Variance (BCa 99% CI) | [0.0088, 0.0142] | [0.0010, 0.0016] |

Table 7.

Mann Kendall’s trend test and Sen’s Slope Test during each El Niño event from January 1986 to June 2021.

Table 7.

Mann Kendall’s trend test and Sen’s Slope Test during each El Niño event from January 1986 to June 2021.

| Category | El Niño Events | MK Trend of FFBI | Sen’s Slope |

|---|---|---|---|

| Very Strong | 1997/98 | Decreasing *** | −0.0348 |

| 2015/16 | Decreasing *** | −0.0438 | |

| Strong | 1987/88 | Decreasing ** | −0.0986 |

| 1991/92 | Decreasing * | −0.0970 | |

| Moderate | 1986/87 | Decreasing ** | −0.0479 |

| 1994/95 | Decreasing * | −0.0527 | |

| 2002/03 | No Trend | ||

| 2009/10 | Decreasing *** | −0.0379 | |

| Weak | 2004/05 | Decreasing *** | −0.0267 |

| 2006/07 | Decreasing * | −0.0360 | |

| 2014/15 | No Trend | ||

| 2018/19 | Decreasing *** | −0.0439 |

* Trend is significant at α = 0.05. ** Trend is significant at α = 0.01. *** Trend is significant at α = 0.001.

Table 8.

Oil palm yield loss and opportunity loss due to each El Niño event from January 1986 to June 2021.

Table 8.

Oil palm yield loss and opportunity loss due to each El Niño event from January 1986 to June 2021.

| Category | El Niño Events | Lag | Negative FFBI Period | Oil Palm Yield Loss | Opportunity Loss | Projected to December 2021 |

|---|---|---|---|---|---|---|

| (Months) | (Months) | (t/ha) | (USD) | (USD) | ||

| Very Strong | 1997/98 | 0 | 16 | 3.0739 | 799,512,628.04 | 3,118,809,718.44 |

| 2015/16 | 2 | 25 | 3.5197 | 2,223,629,847.24 | 3,026,040,134.75 | |

| Strong | 1987/88 | 4 | 8 | 1.2702 | 86,205,737.87 | 621,682,504.89 |

| 1991/92 | 3 | 9 | 0.9798 | 74,237,749.64 | 422,833,751.88 | |

| Moderate | 1986/87 | 1 | 8 | 1.2279 | 59,553,760.49 | 451,416,000.07 |

| 1994/95 | 3 | 4 | 0.1373 | 17,843,504.29 | 83,902,729.92 | |

| 2002/03 | 3 | 6 | 0.2844 | 68,135,456.56 | 206,588,187.64 | |

| 2009/10 | 4 | 9 | 0.7400 | 484,337,375.58 | 925,974,111.78 | |

| Weak | 2004/05 | 6 | 7 | 0.3016 | 74,053,854.49 | 189,770,606.98 |

| 2006/07 | 3 | 5 | 0.2035 | 89,253,638.73 | 208,552,751.05 | |

| 2014/15 | 0 | 5 | 0.3808 | 197,547,898.49 | 296,149,942.22 | |

| 2018/19 | 4 | 12 | 2.1576 | 1,308,607,860.03 | 1,481,072,202.50 |

USD = 4.2189178 as of 24 August 2021 [12]. Opportunity losses were projected using 6% discount rate. Opportunity loss for 2018/19 weak El Niño is excluded in the following analyses because the event has unexplained high production loss.

Table 9.

Averaged oil palm yield loss and opportunity loss due El Niño according to category.

| Category | Lag | Negative FFBI Period | Oil Palm Yield Loss | Opportunity Loss | Projected to December 2021 |

|---|---|---|---|---|---|

| (Months) | (Months) | (t/ha) | (USD) | (USD) | |

| Very Strong | 1.0 | 20.5 | 3.2968 | 1,511,571,237.64 | 3,072,424,926.59 |

| Strong | 3.5 | 8.5 | 1.1250 | 80,221,743.75 | 522,258,128.39 |

| Moderate | 2.8 | 6.8 | 0.5974 | 157,467,524.23 | 416,970,257.35 |

| Weak | 3.0 | 5.7 | 0.2953 | 120,285,130.57 | 231,491,100.09 |

USD = 4.2189178 as of 24 August 2021 [12]. Opportunity losses were projected using 6% discount rate.

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Khor, J.F.; Ling, L.; Yusop, Z.; Tan, W.L.; Ling, J.L.; Soo, E.Z.X. Impact of El Niño on Oil Palm Yield in Malaysia. Agronomy 2021, 11, 2189. https://doi.org/10.3390/agronomy11112189

AMA Style

Khor JF, Ling L, Yusop Z, Tan WL, Ling JL, Soo EZX. Impact of El Niño on Oil Palm Yield in Malaysia. Agronomy. 2021; 11(11):2189. https://doi.org/10.3390/agronomy11112189

Chicago/Turabian StyleKhor, Jen Feng, Lloyd Ling, Zulkifli Yusop, Wei Lun Tan, Joan Lucille Ling, and Eugene Zhen Xiang Soo. 2021. "Impact of El Niño on Oil Palm Yield in Malaysia" Agronomy 11, no. 11: 2189. https://doi.org/10.3390/agronomy11112189

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.