Abstract

This paper examines the impact of teamwork on sell-side analysts’ performance. Using a hand-collected sample of over 50,000 analyst research reports, we find that analyst teams issue more than 70% of annual earnings forecasts. In contrast, most research implicitly assumes that forecasts are issued by individual analysts. We document that analyst teams generate more accurate earnings forecasts than individual analysts and that the stock market reacts more strongly to forecast revisions issued by teams. Analyst teams also cover more firms, issue earnings forecasts more frequently, and issue less stale forecasts. Analysts working in teams are more likely to be voted as All-Star analysts in the future. Among analyst teams, we show that team size and team member ability are significantly associated with forecast accuracy. Moreover, using detailed analyst background information from LinkedIn, we find that forecast accuracy is positively associated with team diversity based on sell-side experience, educational background, and gender. Additional analyses suggest that analyst teams, especially more diverse ones, are more likely to issue cash-flow forecasts and use discounted cash-flow valuation models in their reports. These findings suggest that teamwork and team diversity play a crucial role in understanding sell-side analysts’ performance.

Similar content being viewed by others

Notes

We refer to the I/B/E/S analyst as the person whose name is associated with the forecast in I/B/E/S.

For instance, a lead analyst with the CFA designation can work with either CFA team members or non-CFA team members. We expect team member’s professional designations to impact team performance after controlling for the lead analyst’s professional designation.

As Investext does not cover all brokerages, we acknowledge that our sample may have a selection bias (similar to most other studies in this line of research).

P.Eng. refers to Professional Engineer, and P.Geo. refers to Professional Geologist.

The pattern in our data suggests that an analyst can work with different team members for different firms. Therefore we measure TEAM at the analyst-firm-year level.

Our inferences are similar using other measures. For example, we have considered the distinct number of educational major categories of each team or an HHI measure based on further splitting each major category into undergraduate, graduate, and doctoral levels (untabulated).

Drake, Joos, Pacelli, and Twedt (2019) show that bundled forecasts are less accurate, less bold, and less informative to investors than unbundled forecasts.

We winsorize all continuous variables at the top and bottom 1% tails. Inferences are robust to winsorizing at other cutoffs or no winsorizing.

The inferences remain similar if we use demeaned values of performance measures and analyst characteristics variables, following Bradley et al. (2017), or if we use unadjusted values of each variable and include firm-year fixed effects to control for systematic differences across firm-years.

Team size of one refers to individual forecasts.

Because we exclude firm-years that are only covered by individuals or teams, the 73% number should be interpreted as the lower bound for the prevalence of teamwork, considering that the percentage of teams is even higher in the excluded observations.

The percentage is lower than that of Drake et al. (2019), as we only consider one-year ahead earnings forecasts, whereas they also include forecasts with longer horizons.

The inferences remain unchanged using other clustering structures, such as at the firm or industry level.

Lag value of Accuracy is the analyst’s standardized forecast Accuracy for the same firm in the previous fiscal year.

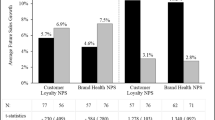

For example, the predicted value of Accuracy in Column 1 is 0.594 for individuals and 0.631 for analyst teams, suggesting that teams are 0.631/0.594–1 = 6.23% more accurate than individuals. Specially, the predicted value for individuals is the intercept 0.594, and the predicted value 0.631 for analyst teams is 0.594 + 0.037 × 1 = 0.631.

We obtain similar results (untabulated) if using the unadjusted value of forecast accuracy and control variables. In untabulated analyses, we also find that our findings are robust to controlling for whether team members other than the I/B/E/S analyst have ever appeared in I/B/E/S.

To further validate our measure of TEAM, which aims to captures whether analysts work with other people or just by themselves, we manually check 100 random cases of changes in TEAM over time. In 81 cases, we can collect the full employment history of team members, and in 71 cases (88%) the changes in TEAM correspond to the changes in team members’ employment status. This percentage should be interpreted as the lower bound of the accuracy of TEAM, because there might be reasons other than changes in employment status that affect whether a research associate works with the lead analyst.

Analysts with less experience and worse forecasting performance may be more likely to need help from others and thus work in teams. We control for analyst experience and previous-year forecast accuracy in the first-stage regression. As shown in Panel C of Table 3, our results do not support this argument.

The IMR is based on the probit estimate and it is calculated as the ratio of the standard normal probability density function divided by its cumulative probability.

In untabulated tests, we use each analyst’s covered firms without variation in TEAM as the control group. This sample is more balanced with respect to the number of treated and control observations. The results are similar to the findings in Panel B of Table 3.

In untabulated tests, we find that the effect of professional designations mainly comes from CFA, not CPA, P.Eng., or P.Geo. These results add to those reported by De Franco and Zhou (2009).

2.3% is calculated as the estimated coefficient 0.014 divided by sample mean 0.62 (0.014/0.62 = 2.3%).

Length is defined as the number of characters. Flesch Reading Ease = 206.8 – (1.015 × words per sentence) – (84.6 × syllables per word). Flesch Kincaid Index = (11.8 × syllables per word) + (0.39 × words per sentence) – 15.59. Fog = (words per sentence + percent of complex words) × 0.4.

Our inferences are robust to scaling by stock price, following Christie (1987).

Our inferences are unchanged if we exclude forecast revisions that experience concurrent earnings announcement in a three-day window. And our inferences (untabulated) are robust to measuring market reaction using intraday return following Keskek, Tse, and Tucker (2014).

The inferences remain similar if we employ an OLS model.

Similarly, no inferences are affected if we include the squared root of Broker Size as an additional control variable.

References

Adams, R., & Ferreira, D. (2010). Moderation in Groups: Evidence from Betting on Ice Break-ups in Alaska. The Review of Economic Studies, 33(3), 882–913.

Adams, R. B., Akyol, A. C., & Verwijmeren, P. (2018). Director skill sets. Journal of Financial Economics, 130(3), 641–662.

Alchian, A., & Demsetz, D. (1972). Production, information costs, and economic organization. American Economic Review, 62(5), 777–795.

Amason, A. C. (1996). Distinguishing the effects of functional and dysfunctional conflict on strategic decision making: Resolving a paradox for top management teams. The Academy of Management Journal, 39(1), 123–148.

Apesteguia, J., Azmat, G., & Iriberri, N. (2011). The impact of gender composition on team performance and decision making: Evidence from the field. Management Science, 58(1), 78–93.

Bae, K.-H., Stulz, R., & Tan, H. (2008). Do local analysts know more? A cross-country study of the performance of local analysts and foreign analysts. Journal of Financial Economics, 88(3), 581–606.

Becker, G., & Murphy, K. (1992). The division of labor, coordination costs, and knowledge. The Quarterly Journal of Economics, 107(4), 1137–1160.

Bedeian, A. G., & Mossholder, K. W. (2000). On the use of the coefficient of variation as a measure of diversity. Organizational Research Methods, 3(3), 285–297.

Bernile, G., Bhagwat, V., & Yonker, S. (2018). Board diversity, firm risk, and corporate policies. Journal of Financial Economics, 127(3), 588–612.

Blinder, A. S., & Morgan, J. (2005). Are two heads better than one? Monetary policy by committee. Journal of Money, Credit and Banking, 37(5), 789–811.

Boning, B., Ichniowski, C., & Shaw, K. (2007). Opportunity counts: Teams and the effectiveness of production incentives. Journal of Labor Economics, 25(4), 613–650.

Bowers, C. A., Pharmer, J. A., & Salas, E. (2000). When member homogeneity is needed in work teams: A meta-analysis. Small Group Research, 31(3), 305–327.

Bradley, D., Gokkaya, S., & Liu, X. (2017). Before an analyst becomes an analyst: Does industry experience matter? The Journal of Finance, 72(2), 751–792.

Bradshaw, M. T. (2004). How do analysts use their earnings forecasts in generating stock recommendations? The Accounting Review, 79(1), 25–50.

Bradshaw, M. T. (2011). Analysts’ forecasts: What do we know after decades of work? Working paper, Boston College.

Bradshaw, M., Ertimur, Y., & O'Brien, P. (2017). Financial analysts and their contribution to well-functioning capital markets. Foundations and Trends in Accounting, 11(3), 119–191.

Brightbill, K. (2018). Do analyst teams issue higher quality forecasts? Evidence from analyst reports. Working paper, University of Iowa.

Brown, L. D., & Hugon, A. (2009). Team earnings forecasting. Review of Accounting Studies, 14(4), 587–607.

Brown, L. D., Call, A. C., Clement, M. B., & Sharp, N. Y. (2015). Inside the ‘black box’ of sell-side financial analysts. Journal of Accounting Research, 53, 1–47.

Call, A. C., Chen, S., & Tong, Y. H. (2009). Are analysts’ earnings forecasts more accurate when accompanied by cash flow forecasts? Review of Accounting Studies, 14(2), 358–391.

Call, A. C., Chen, S., & Tong, Y. H. (2013). Are analysts’ cash flow forecasts Naïve extensions of their own earnings forecasts? Contemporary Accounting Research, 30(2), 438–465.

Christie, A. (1987). On cross-sectional analysis in accounting research. Journal of Accounting and Economics, 9, 231–258.

Clement, M. B. (1999). Analyst forecast accuracy: Do ability, resources, and portfolio complexity matter? Journal of Accounting and Economics, 27(3), 285–303.

Clement, M. B., & Tse, S. Y. (2003). Do Investors respond to analysts’ forecast revisions as if forecast accuracy is all that matters? The Accounting Review, 78(1), 227–249.

Clement, M. B., & Tse, S. Y. (2005). Financial analyst characteristics and herding behavior in forecasting. The Journal of Finance, 60(1), 307–341.

Clement, M. B., Koonce, L., & Lopez, T. J. (2007). The roles of task-specific forecasting experience and innate ability in understanding analyst forecasting performance. Journal of Accounting and Economics, 44(3), 378–398.

Cohen, L., Frazzini, A., & Malloy, C. (2010). Sell-Side School Ties. The Journal of Finance, 65(4), 1409–1437.

Cooper, D. J., & Kagel, J. H. (2005). Are two heads better than one? Team versus individual play in signaling games. The American Economic Review, 95(3), 477–509.

Dahlin, K. B., Weingart, L. R., & Hinds, P. J. (2005). Team diversity and information use. The Academy of Management Journal, 48(6), 1107–1123.

De Franco, G., & Zhou, Y. (2009). The performance of analysts with a CFA® designation: The role of human-capital and signaling theories. The Accounting Review, 84(2), 383–404.

De Franco, G., Hope, O.-K., Vyas, D., & Zhou, Y. (2015). Analyst report readability. Contemporary Accounting Research, 32, 76–104.

DeFond, M. L., & Hung, M. (2003). An empirical analysis of analysts’ cash flow forecasts. Journal of Accounting and Economics, 35(1), 73–100.

Demirakos, E. G., Strong, N. C., & Walker, M. (2010). Does valuation model choice affect target Price accuracy? European Accounting Review, 19(1), 35–72.

Díaz-García, C., González-Moreno, A., & Jose Sáez-Martínez, F. (2013). Gender diversity within R&D teams: Its impact on radicalness of innovation. Innovation, 15(2), 149–160.

Drake, M. S., Joos, P. R., Pacelli, J., & Twedt, B. J. (2019). Analyst forecast bundling. Forthcoming, Management Science.

Ertimur, Y., Sunder, J., & Sunder, S. V. (2007). Measure for measure: The relation between forecast accuracy and recommendation profitability of analysts. Journal of Accounting Research, 45, 567–606.

Gao, M., Ji, Y., & Rozenbaum, O. (2018). Do associate analysts matter? Working Paper, George Washington University and Hong Kong Polytechnic University.

Giannetti, M., & Zhao, M. (2019). Board ancestral diversity and firm-performance volatility. Journal of Financial and Quantitative Analysis, 54(3), 1117–1155.

Gleason, C. A., Johnson, B. W., & Li, H. (2013). Valuation model use and the Price target performance of sell-side equity analysts. Contemporary Accounting Research, 30, 80–115.

Green, C., Jegadeesh, N., & Tang, Y. (2009). Gender and job performance: Evidence from wall street. Financial Analysts Journal, 65(6), 65–78.

Groysberg, B., & Healy, P. M. (2013). Wall street research: Past, present, and future. Stanford Economics and Finance.

Groysberg, B., Healy, P. M., & Maber, D. A. (2011). What drives sell-side analyst compensation at high-status investment banks? Journal of Accounting Research, 49, 969–1000.

Guimerà, R., Uzzi, B., Spiro, J., & Amaral, L. A. (2005). Team assembly mechanisms determine collaboration network structure and team performance. Science 308(5722), 697 LP-702.

Hamilton, B., Nickerson, J. A., & Owan, H. (2003). Team incentives and worker heterogeneity: An empirical analysis of the impact of teams on productivity and participation. Journal of Political Economy, 111(3), 465–497.

Heckman, J. J. (1979). Sample selection Bias as a specification error. Econometrica, 47(1), 153–161.

Holmström, B. (1982). Moral Hazard in teams. Bell Journal of Economics, 13(2), 324–340.

Hoogendoorn, S., Oosterbeek, H., & van Praag, M. (2013). The impact of gender diversity on the performance of business teams: Evidence from a field experiment. Management Science, 59(7), 1514–1528.

Institutional Investor. (2014). The 2014 Rising Stars of Wall Street. https://www.institutionalinvestor.com/article/b14zblbkq2h2mb/the-2014-rising-stars-of-wall-street

Jacob, J., Lys, T. Z., & Neale, M. A. (1999). Expertise in forecasting performance of security analysts. Journal of Accounting and Economics, 28(1), 51–82.

Kahane, L., Longley, N., & Simmons, R. (2011). The effects of coworker heterogeneity on firm-level output: Assessing the impacts of cultural and language diversity in the National Hockey League. The Review of Economics and Statistics, 95(1), 302–314.

Keskek, S., Tse, S., & Tucker, J. W. (2014). Analyst information production and the timing of annual earnings forecasts. Review of Accounting Studies, 19, 1504–1531.

Kim, D., & Starks, L. T. (2016). Gender diversity on corporate boards: Do women contribute unique skills? American Economic Review, 106(5), 267–271.

Lazear, E. P. (1998). Globalization and the market for teammates. National Bureau of economic research working paper series no. 6579.

Li, N., & Wahid, A. S. (2018). Director tenure diversity and board monitoring effectiveness. Contemporary Accounting Research, 35, 1363–1394.

Li, C., Lin, A.-P., & Lu, H. (2018). Analyzing the analysts: The effects of technical and social skills on analyst careers. Working Paper.

Lorenz, J., Rauhut, H., Schweitzer, F., & Helbing, D. (2011). How social influence can undermine the wisdom of crowd effect. Proceedings of the National Academy of Sciences, 108(22), 9020–9025.

Malloy, C. J. (2005). The geography of equity analysis. The Journal of Finance, 60(2), 719–755.

Mikhail, M. B., Walther, B. R., & Willis, R. H. (1997). Do security analysts improve their performance with experience? Journal of Accounting Research, 35, 131–157.

Mohanram, P. S. (2014). Analysts' cash flow forecasts and the decline of the accruals anomaly. Contemporary Accounting Research, 31, 1143–1170.

O’Brien, P. C., & Tan, H. (2015). Geographic proximity and analyst coverage decisions: Evidence from IPOs. Journal of Accounting and Economics, 59(1), 41–59.

Page, S. E. (2007). The difference: How the power of diversity creates better groups, Firms, Schools, and Societies. Princeton, NJ: Princeton University Press.

Patel, S., & Sarkissian, S. (2017). To group or not to group? Evidence from mutual fund databases. Journal of Financial and Quantitative Analysis, 52(5), 1989–2021.

Polzer, J. T., Milton, L. P., & Swarm, W. B. (2002). Capitalizing on diversity: Interpersonal congruence in small work groups. Administrative Science Quarterly, 47(2), 296–324.

Stahl, G. K., Maznevski, M. L., Voigt, A., & Jonsen, K. (2010). Unraveling the effects of cultural diversity in teams: A meta-analysis of research on multicultural work groups. Journal of International Business Studies, 41(4), 690–709.

Tan, H., & Yu, C. (2019). Valuation uncertainty and analysts’ use of DCF models. Working paper, McGill University and York University.

Watson, W. E., Kumar, K., & Michaelsen, L. K. (1993). Cultural Diversity’s impact on interaction process and performance: Comparing homogeneous and diverse task groups. The Academy of Management Journal, 36(3), 590–602.

Wei, L. (2005). Brokers increasingly use teamwork. Dow Jones Newswires, (February 23).

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher’s note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Appendices

Appendix 1

Appendix 2: An Example of the Data-Collection Process

We search for the corresponding research report for each earnings forecast in our sample by matching the covered firm name, brokerage name, I/B/E/S analyst last name and first initial, and forecast issuance date. Then we manually extract the name of the authors of the report and their professional designations if available.

Example of Data-Collection Process

Figure 1 Presents a report issued by Wells Fargo on Dec 18, 2014. The covered firm is Genomic Health Inc. The authors include Tim Evans, who is the analyst listed in the I/B/E/S, and Luke Sergott. The corresponding forecast is treated as being issued by a team because there are two authors listed

Example of Data-Collection Process

Figure 2 Presents another report issued by the same analyst in May 2015. The covered firm is Myriad Genetics Inc. This forecast is treated as being issued by an individual analyst, as there is only one author listed. In fact, Luke Sergott joined another brokerage company, Evercore, in April 2015

Rights and permissions

About this article

Cite this article

Fang, B., Hope, OK. Analyst teams. Rev Account Stud 26, 425–467 (2021). https://doi.org/10.1007/s11142-020-09557-6

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11142-020-09557-6

Keywords

- Teamwork

- Analysts

- Earnings forecasts

- Diversity

- Market reactions to analyst revisions

- All-star analysts

- Cash-flow forecasts

- DCF models

- Sell-side

- Education

- Gender