STEPS in BUSINESS EXCELLENCE (SBEXC)

Volume 2, Issue 1, pp: 1-8

![]()

The Impact of Forensic Accounting Techniques in Detecting Financial Fraud

“Survey Study of The Opinions of Certified Accountants in Syria”

Saja Hashem 1,a*, Dr. Afraa Ali 1,b, Dr. Haider Haider 1,c

1 Department of Accounting, Faculty of Economics, Tishreen University, Syria.

E-mail: saja.hashem@tishreen.edu.sy a,*, afraa.ali@tishreen.edu.sy b, haider.haider@tishreen.edu.syc

* Correspondence Author

Received: 12 December 2023 | Revised: 11 January 2024 | Accepted: 07 February 2024 | Published: 07 May 2024

The purpose of this study was to investigate the impact of forensic accounting techniques used by certified accountants in detecting financial fraud in the companies they audit. The data was collected from primary sources based on a questionnaire distributed to (120) certified accountants who are practicing the profession for the year 2023 and are allowed to audit financial companies in Syria. The results showed a statistically significant impact of the forensic accounting techniques (financial ratio analysis – trend analysis – data mining – critical point audit – relative size theory) used by the certified accountant in detecting financial fraud in Syria. The ability of forensic accounting techniques reached 18.5% in detecting financial fraud according to the opinions of certified accountants in Syria. It also showed a positive and statistically significant effect of the forensic accounting techniques used by the certified accountant in detecting financial fraud in Syria after controlling years of experience. The percentage of explained variance increased from (18.5%) to (25.3%).

Keywords: Financial Fraud Detection, Forensic Accounting Techniques, Financial Ratio Analysis, Trend Analysis, Data Mining, Critical Point Auditing, Relative Size Theory.

Financial statement fraud is a topic that receives significant attention from the public, press, investors, financial community, and regulators due to prominent frauds that have been reported. Some companies provide incorrect financial information to manipulate the stock price, reduce the tax burden, and perceived financial risks (Rezaree, 2005). Previous corporate frauds have shown that tampering with financial information leads to a decline in confidence in companies’ financial statements (Özcan, 2019). Fraud and manipulation of financial information can have a negative impact on the efficiency and stability of the financial system. Therefore, it is crucial for authorities to implement effective policies that increase public and investor confidence. This text highlights the significance of forensic accounting and its practices in detecting financial information manipulation. The emergence and rise of forensic accounting can be attributed to the activities of illegal companies and the manipulation of financial information (Olukowade and Balogun, 2015; Grima et al., 2020).

Forensic accounting techniques aid companies and governments in detecting financial fraud. Forensic accountants focus on detecting manipulation of financial information, fraud, supporting litigation, and detecting tax evasion and bankruptcies. They use statistical and investigative methods, as well as traditional auditing techniques such as recalculation, sampling, and analytical procedures These techniques are influenced by auditing, which is credited with the development of forensic accounting. The U.S. General Accounting Office emphasises the importance of preventing and detecting fraud during statutory audits. International standard setters have increased auditors’ responsibility for fraud risk when conducting financial statement audits (Olukowade and Balogun, 2015). Professional skepticism is a crucial aspect of auditing and the forensic accounting process, lack of professional scepticism can lead to significant deficiencies in the audit process. The Securities and Exchange Commission (SEC) has stated that some of the services provided by audit firms fall within the scope of services provided by forensic accounting Therefore, the importance given to forensic accounting has increased significantly, and many audit firms have expanded their services to include forensic accounting practices (Grima et al., 2020). The International Standard on Auditing No. (ISA 240) represents a significant change in auditing practices. Auditors are now required to identify and evaluate the risks of material misstatement due to fraud in financial statements (Enyi, 2009). It is important to note that ordinary statutory auditing must include some elements of forensic investigation. The auditor’s responsibility is not only to prevent fraud but also to detect it (Olukowade and Balogun, 2015). Forensic accounting is taught at both undergraduate and graduate levels in the United States and Europe (Grima et al., 2020).

The objective of this research is to investigate the effectiveness of forensic accounting techniques employed by auditors (certified accountants in Syria) in detecting suspected fraudulent activities in financial statements. This study is particularly relevant in light of the findings of Price water house Coopers’ global survey on economic and fraud crimes in 2018, titled “Bringing Fraud Out from the Shadows: Shining a Light on Fraud in the Middle East.” In the Middle East, the percentage of companies exposed to fraud increased from 26% to 34% in the 24 months preceding the survey. Direct losses related to fraud were estimated to be between $100,000 to $50 million per case. Additionally, the survey revealed that 62% of internal fraud cases involved management. Given the increased risk of financial fraud, it is necessary to demonstrate the impact of forensic accounting techniques used by certified accountants in detecting financial fraud. This will help protect investments and support the national economy in the Syrian environment.

Numerous studies have investigated the effectiveness of forensic accounting techniques in detecting financial fraud. Some studies have found that techniques such as financial ratio analysis and trend analysis can be effective in detecting financial fraud (Eko et al., 2020; Eko, 2022). However, a recent study by Adebisi et al. (2022) found no correlation between the use of these techniques and the detection of financial fraud. Other studies have demonstrated that forensic accounting services aid in detecting financial fraud. For example, Abdulrahman et al. (2020), Rifani and Hasan (2022), and Jarallah and Al-Sayed (2022) found that forensic accounting helps identify fraud indicators during financial statement audits and enhances understanding of financial and accounting issues. Al Enazi et al. (2022) investigated the effectiveness of forensic accounting techniques in detecting financial fraud and the level of forensic accounting practice in the Kingdom of Saudi Arabia. It is important to enhance the practice of forensic accounting in the country. Alwan and Nemat (2023) conducted a study which demonstrated that forensic accounting techniques (such as data mining, the use of information technology, and diversity of the cognitive dimension), have a significant and positive effect on reducing earnings management practices in non-financial companies listed on the Palestine Stock Exchange. Additionally, Cusack and Ahokov (2016) recommended the adoption of financial ratio analysis technology as a basis for improving fraud detection programs in Australia.

The aim of this study is to evaluate the effectiveness of forensic accounting techniques in detecting financial fraud. Empirical evidence is provided regarding the impact of these techniques when used by certified accountants in Syria to detect corporate financial fraud.

Based on previous research (Eko et al., 2020; Adebisi et al., 2022), the following research hypotheses can be formulated:

H1: The use of forensic accounting techniques by certified accountants has a statistically significant effect on detecting financial fraud in Syria.

H2: After controlling for years of experience, the use of forensic accounting techniques by certified accountants has a statistically significant effect on detecting financial fraud in Syria.

Primary data was collected by distributing a questionnaire to (120) certified accountants who are accredited by the Accounting and Auditing Council and licensed to practice the profession of auditing for financial companies in Syria. The questionnaire was distributed in the following governorates: Damascus, Suwayda, Aleppo, Homs, Hama, Latakia and Tartous. Out of the (120) questionnaires distributed, (71) were returned and analyzed. Statistical tests were conducted using the Statistical Package for the Social Sciences (SPSS, V.25)

The Independent variable in this study is forensic accounting techniques, which include financial ratio analysis, trend analysis, data mining, critical points audit, and relative size theory.

The Dependent variable is financial fraud detection.

The concept of fraud in financial statements:

Financial statement fraud is when management of the companies intentionally misleads users of published financial statements, especially investors and creditors. These practices are considered illegal and unethical and are carried out through deliberate falsification of accounting records (transactions, balances, disclosure of financial statements and misapplication of international financial reporting standards). This type of fraud involves intent and deception by a team of perpetrators with a set of well-planned schemes. financial statement fraud mainly includes the following:

1- Falsifying accounting books, supporting documents, or commercial transactions or events, or other important information used to prepare financial statements.

2- Intentionally manipulation when applying or interpretation or implementation of accounting standards, principles, policies and methods used to measure economic events, business transactions and disclosures (Rezaee, 2005).

3- Provide incomplete disclosures regarding accounting standards, principles and practices and relevant financial information.

4-Using aggressive accounting methods by applying illegal profit management practices.

5- To get benefits of loopholes which are avilable of current accounting standards, which have become very detailed and easy to circumvent to hide their true financial performance and position (Anbalagan, 2014).

Fraud theory explains the reasons of engaging individual in financial fraud or any other type of fraud. This theory explains that there are three possible predection that push individuals to practice financial fraud(Albrecht et al. ,2014): the first one is perceived pressure, when senior managers may feel pressure to meet or exceed investors’ expectations(Albrecht et al. ,2014), where Shareholders anticipate the company’s performance and use financial statements to measure ite and compare it to their prior expectations, which in turn affects the market price of the company’s stock(Brennan and McGrath, 2007). In addition to the job security and financial compensation of managment depend on maintaining strong financial performance of the company and high its stock prices.

Fraud theory explains why an individual engages in financial or any other type of fraud. This theory shows that there are three possible expectations that lead individuals to engage in financial fraud (Albrecht et al., 2014). It also includes Auditing Standard SAS (99) (Hogan et al., 2008). The first one is perceived pressure: this occurs when senior managers feel pressure to meet or exceed investors’ expectations (Albrecht et al., 2014). Shareholders expect the company’s performance, and based on the published financial statements, they measure the company’s actual performance and make a comparison between the actual performance and the xpected one in advance, which in turn affects the market price of the company’s shares (Brennan and McGrath, 2007).

In addition, job security, managers’ continuity at work, and management’s financial compensation (bonuses) depends primarily on maintaining the company’s strong financial performance and high stock prices. However, it is important to avoid using fraudulent means to achieve this, and the possibility of committing fraud should not be considered a realistic possibility without considering facing the consequences (Albrecht et al., 2014). Thus, the motivation or pressure faced by fraud perpetrators is related to the expected negative consequences when a company’s true financial performance is revealed. The second is perceived opportunity, which is generated when an individual sees a favorable opportunity to commit fraud. He may consider initiating illegal actions. This theory is based on perceptions, that is, when pressures and opportunities are viewed as real, meaning that pressures and opportunities may not be real, but they are viewed as real. The third motive is logical justification, as fraud perpetrators often attempt to reconcile their unethical behavior with their core values by searching for excuses for their thoughts, intentions, and actions through logical justifications in order to present themselves as not violating their ethical standards (Albrecht et al. ,2014), as some research has identified six motives for fraud. The three additional motivations are competence, arrogance, and deterrence. Competence refers to a person’s ability to overcome a company’s internal controls. While arrogance refers to the superiority complex of the person committing the fraud and his belief that the company and external auditors are unable to detect it, while deterrence refers to the person ignoring the potential consequences of his actions as a result of his arrogance. Understanding these motivations (perceived pressure, perceived opportunity, justification, competence, arrogance, and deterrence) can be an aid to the forensic accountant in determining the type of person behind the fraud and what to look for during the investigation (Nigrini, 2020). Therefore, shareholders and boards of directors, when exercising their oversight role, aim to reduce the perception of fraud opportunities by implementing systems and controls, such as audit procedures, which are supposed to make it more difficult for fraudulent activities to continue. However, some individuals, especially high-powered executives, may believe that they are able to manipulate and control their environment.

Forensic Accounting Techniques:

Financial ratio analysis This approach involves performing ratio to evaluate financial data on a historical, industry, or benchmark basis. The purpose is to detect fraud by studying data patterns to identify potentially deceptive transactions (Oyedokun, 2022). In recent decades, orensic accountants have increasingly turned to analytical procedures due to their practicality and general benefits. The decision to use of analytical procedures depends on their effectiveness. of these procedures. Success in forensic accounting relies on identifying financial and non-financial measures that are connected to the manipulated financial information. The main steps involve developing expectations and comparing them tothe actual results to identify any discrepancies Data analysis and financial ratios can be useful in detecting fraud cases. Ratio analysis also enables auditors to compare data from two different years, allowing them to identify the reasons for any differences in the financial statements (Jain and Lamba, 2020).

Time series tests, specifically trend analysis, are crucial forensic accounting methods for detecting fraud The focus is on identifying unusual transactions. By comparing current transaction records those of the previous year, fraudulent transactions can be easily identified. This method is particularly useful in determining if the level of sales is increasing at the same rate as the level of bad debts in the business. Businesses can use trend analysis to compare sales data and bad debts over time. This can help to identify fraudulent sales transactions or manipulation of the system to improve turnover. It is important to use trend analysis over certain period to detect such fraudulent changes (Oyedokun, 2022).

Data mining is the process of identifying deviations, patterns, and correlations within large data sets to predict results. It can help in detecting fraud faster (Bassey, 2018) through data extraction, classification, compilation, regression analysis, and data retrieval. By using data mining techniques, patterns can be identified based on available historical data, providing a basis for future predictions (Jain and Lamba, 2020). Although this technology may be considered expensive for small and medium-sized companies, they can still benefit from it by using Microsoft Office programs. According to Nigrini’s study (2020), Access and Excel programs are useful for analyzing small and medium-sized cases.

The relative volume factor can be used to detect unusual transactions and fluctuations resulting from errors or fraud. The text describes the concept of the largest-to-second-largest ratio in a data set, which is used to identify anomalies in transactions, such as exceeding credit limits or violating company policies (Bassey, 2018).

Computer-aided auditing techniques involve the use of computers to automate auditing processes. This typically includes basic office software like spreadsheets, word processors, and text editors, as well as specialized auditing software such as ACL, Arbutus, and EAS. More advanced software packages that include statistical analysis may also be used. Computer-aided audit techniques assist auditors in performing various functions, including data queries, data segmentation, sample extraction, identification of missing sequences (missing values), statistical analysis, and identification of duplicate transactions. These techniques can also aid in the detection of fraud by conducting and creating analytical tests, data analysis reports, and continuous monitoring (Okafor and Obiora, 2022).

Model Specification: This section specifies the model used to examine the determinants of fraud detection in forensic accounting techniques.

FRD = f (DM, RAS, TRD, CPA, RSF)

It is stated econometrically as:

FRD = β0+β1 RAS +β2 DM +β3 TRD + β4 CPA + β5 RSF +ε

FRD = β0+β1RAS +β2DM +β3TRD + β4CPA + β5RSF + β6NYE +ε

Where:

FRD = Financial Fraud Detection )Umar et al., 2017)

DM = Data Mining (Eko, 2022).

RAS = Financial Ratio Analysis (Eko, 2022).

TRD = Trend Analysis (Eko, 2022).

CPA = Critical Point Audit (Ijeoma, 2015; Moses, 2019).

RSF = Relative Volume Factor (Ijeoma, 2015; Moses, 2019).

NYE = Number Of Years Of Experience.

ε = Random Error.

β1 – β6 = Unknown coefficients to be estimated

Reliability analysis: The reliability of the data was measured by calculating the Cronbach’s alpha coefficient for the experimental sample, which consisted of 24 certified accountants. Therefore, the reliability of the questionnaire was confirmed for the entire sample. The Cronbach’s alpha coefficient was found to be 77.8, which is considered acceptable according to Moses (2019). Table. 1 shows the measurement of the Cronbach’s alpha coefficient.

Table 1. Reliability Statistics

The variance inflation factor (VIF) test was used to evaluate the overlap in the relationship between independent variables. The results showed that all variables were weakly correlated with each other, with a maximum VIF of 1.954. It is similar to the tolerance level (Tol), and none of the variables reported a tolerance value of less than 0.05 (Mbasiti et al., 2021; Adebayo et al., 2022). Table. 2 shows the results test VIF and the Tolerance.

Table 2. Coefficientsa

Table. 3 shows the results of the skewness and skewness test for the data.

Table 3. Statistics

To verify the independence of the residuals, the Durbin-Waston test was conducted. The test yielded a value of 1.888, which is close to the expected value of 2, indicating that the residuals are independent. Table. 4 shows the results of the Durbin-Waston test.

Table 4. Model Summaryb

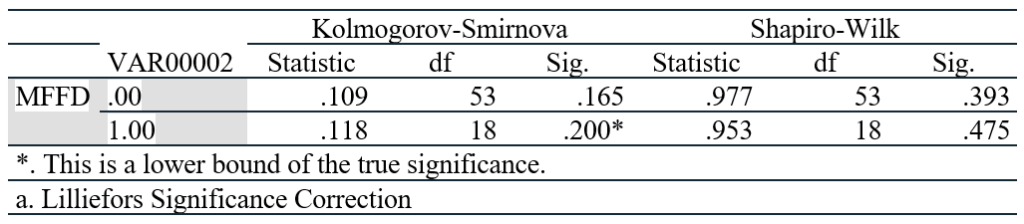

A test for homogeneity of variance was conducted, and the results are presented in Table 5,6. The p-value (>0.05) indicates that there is no heteroscedasticity.

Table 5. Tests of Normality

Table 6. Test of Homogeneity of Variance

The financial ratio analysis, trend analysis, critical points audit, and relative size factor were used as data mining techniques to test the multiple linear regression model.

FRD = β0+β1 RAS +β2 DM +β3 TRD + β4 CPA + β5 RSF +ε

The first hypothesis:

The use of forensic accounting techniques by certified accountants has a statistically significant effect on detecting financial fraud in Syria.

Table. 7 displays the determinant among the independent variables, including data mining techniques, financial ratio analysis, trend analysis, critical points audit, and relative size factor, and the dependent variable, financial fraud detection.

Table 7. Correlation Analysis

The Pearson correlation coefficient has a value of 0.43, indicating a positive and moderaterelationship between the independent and dependent variables. The R2 value is 0.185, meaning that 18.5% of the dependent variable can be explained by the independent variables.

Table. 8 presents the analysis of variance and coefficients for the initial multiple linear regression model, which examines the relationship between the independent variables and the dependent variable.

Table 8. ANOVAa

An F-test was conducted, and the result (0.019) indicates that H1, which states that there is a statistically significant effect of the forensic accounting techniques used by the certified accountant in detecting financial fraud in Syria, is accepted. Table. 9 provides further details.

Table 9. Model Specification

The certified accountant’s trend analysis technique has a positive and significant effect in detecting fraud (P=0.003). This indicates that these techniques do not have a significant effect. However, the P-values for the data mining technique, financial ratio analysis, critical point audit, and relative size factor are 0.801, 0.589, 0.723, and 0.242 respectively, which are higher than the threshold of (0.05).

It is evident from the above that, of the forensic accounting techniques employed by certified accountants in Syria to detect financial fraud in the companies they audit, only the trend analysis technique was significant – specifically, the regression model after controlling for the variable of years experience.

Akinbowale et al. (2020) state that forensic accounting is a recent development in developing countries due to the lack of professional accountants with sufficient skills to detect illegal activity within and outside the organization. Oyedokun (2022) adds that experience is one of the determinants of the use of forensic accounting techniques. A dummy variable was added to the research sample to represent the number of years of experience possessed by the chartered accountant. The sample included 49 chartered accountants with five years or more years of experience, as indicated by the dummy variable. The variable was assigned a value of 1 for those with experience and 0 for those without.

Table 10. The distribution of respondents according to years of experience

After adding a dummy variable, the multiple linear regression model was tested using data mining technique, financial ratio analysis, trend analysis, critical point audit, and relative size factor.

Table 11. Correlation Analysis

The Pearson correlation coefficient has a value of 0.503, indicating a positive and moderately intense relationship between the independent variables and the dependent variable.

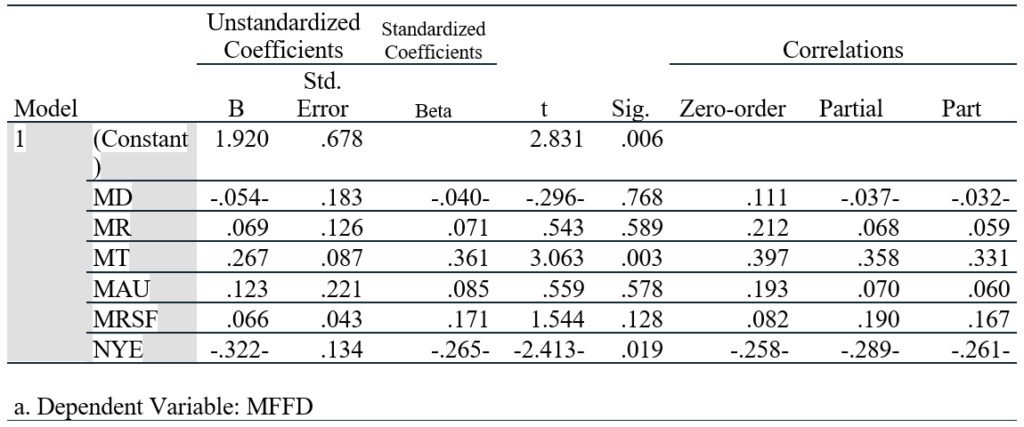

Table. 12 shows the analysis of variance and coefficients for the first multiple linear regression model between the independent variables and the dependent variable financial fraud detection among experienced people who have more than (5) Years of experience.

Table 12. ANOVAa

The regression model was found to be significant, with an F value of 3.607 (p<0.05) and an R2 value of 0.253, indicating that 25.3% of the dependent variable can be explained by the independent variables (Table. 13).

Table 13. Coefficientsa

The certified accountant’s trend analysis technique has a positive and significant effect in detecting fraud, with a P value of 0.003. However, the P-value for the data mining technique, financial ratio analysis, critical point audit, and relative size factor are 0.768, 0.589, 0.578, and 0.128, respectively, which are higher than the threshold of 0.05. Therefore, data mining techniques, financial ratio analysis, critical point auditing, and relative size factor have no significant impact on fraud detection.

The text highlights the use of forensic accounting techniques by experienced certified accountants in Syria to uncover the financial fraud in audited companies. The results indicate that the trend analysis technique was the most relied upon method for detecting fraud as experience increased.

The study examined the link between the use of forensic accounting techniques and fraud detection. The techniques used included ratio analysis, data mining , trending analysis, critical point audit, and relative volume factor. Primary data was collected through questionnaires distributed to certified accountants in Syria. Hypothesis testing was conducted using multiple regression test analysis. The study suggests that forensic accounting techniques, particularly trend analysis, have aided certified accountants in Syria in detecting financial fraud. Furthermore, the study found that certified accountants with more experience rely more heavily on trend analysis techniques. Therefore, it is recommended to increase support for certified accountants through scientific and practical qualification programs in the field of forensic accounting and its techniques. The Society of Certified Public Accountants in Syria, responsible for the accounting and auditing profession, should establish professional accounting rules that incorporate forensic accounting. Additionally, they should lay the groundwork for granting professional certificates that enable auditors to practice forensic accounting.

Cite: Hashem, S., Ali, A., & Haider, H. (2023). The Impact of Forensic Accounting Techniques in Detecting Financial Fraud “Survey Study of The Opinions of Certified Accountants in Syria.” STEPS in BUSINESS EXCELLENCE, 2(1), 1–8. https://doi.org/10.61706/SBEXC12003

Copyright: © 2023 by the authors. Licensee SSG, Dubai, UAE.

This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY-NC-ND 4.0) license (http://creativecommons.org/licenses/by-nc-nd/4.0/).

An independent academic publisher with an editorial team including many of the top researchers in the world. SSG publishes research, review, and case report articles in double-blind, peer-reviewed, open access scientific and academic journals.

Copyright © 2023 Scientific Steps International Publishing Services LLC (Dubai – United Arab Emirates)