Exploring Performance Determinants of China’s Cable Operators and OTT Service Providers in the Era of Digital Convergence—From the Perspective of an Industry Platform

Abstract

:1. Introduction

2. Literature Review

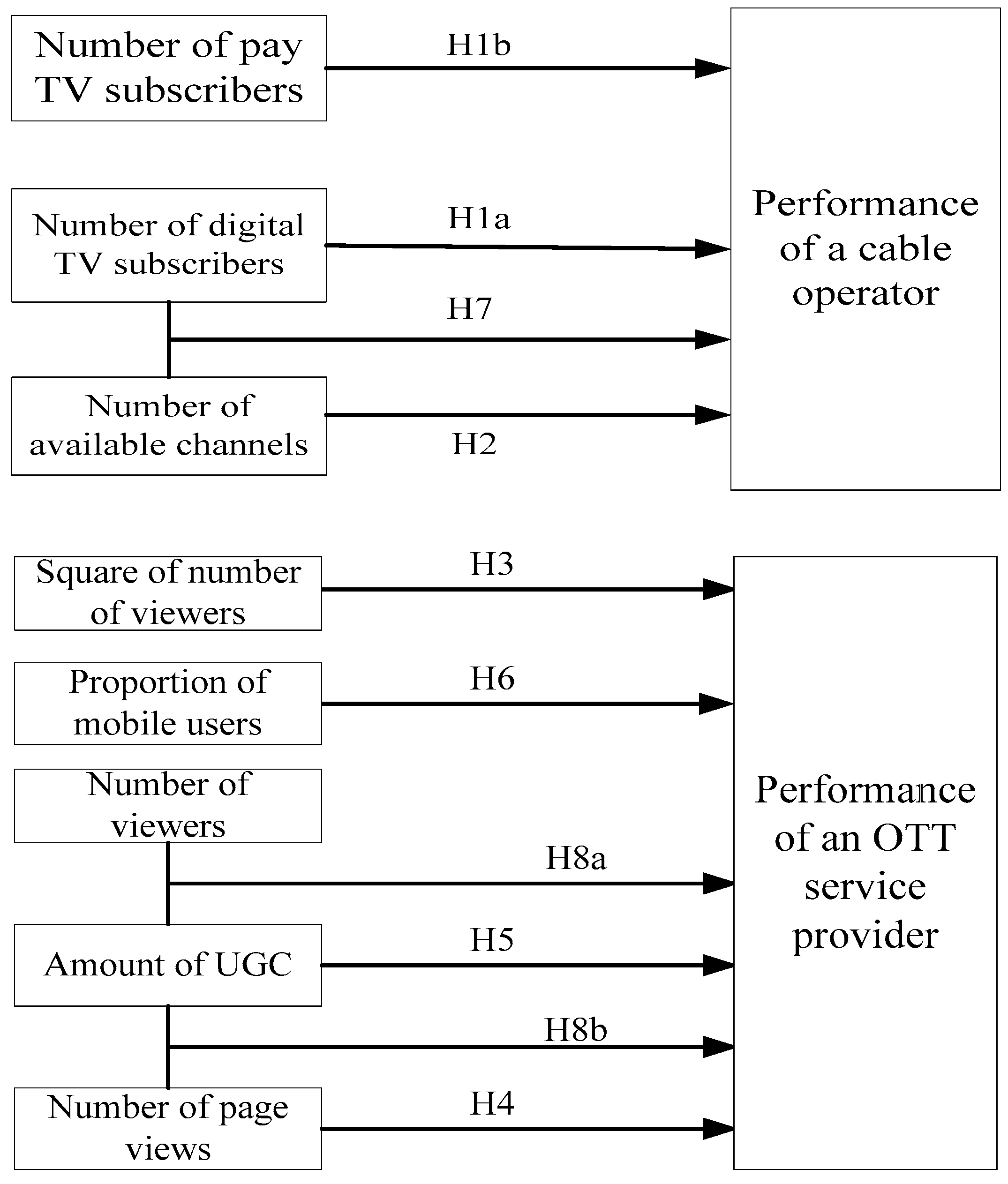

3. Hypotheses

3.1. Platform Participation and Engagement

3.2. Interaction between the Demand Side and the Supply Side

4. Analysis of China’s Cable Operators and OTT Service Providers

4.1. Cable Operators

4.1.1. Overview

4.1.2. Cable Operators as a Potential Industry Platform

4.2. OTT Service Providers

4.2.1. Overview

4.2.2. OTT Service Providers as a Potential Industry Platform

5. Empirical Analysis

5.1. Data and Variables

5.1.1. Cable Operators

5.1.2. OTT Service Providers

5.2. Methodology

5.3. Results

5.3.1. Cable Operators

5.3.2. OTT Service Providers

5.4. Discussion

6. Conclusions and Implications

Acknowledgments

Author Contributions

Conflicts of Interest

References

- Hacklin, F. Management of Convergence in Innovation: Strategies and Capabilities for Value Creation beyond Blurring Industry Boundaries; Physica-Verlag: Heidelberg, Germany, 2007. [Google Scholar]

- Wan, X.; Xuan, Y.; Lv, K. Measuring convergence of China’s ICT industry: An input–output analysis. Telecommun. Policy 2011, 35, 301–313. [Google Scholar] [CrossRef]

- Doyle, G. Digitization and changing windowing strategies in the television industry: Negotiating new windows on the world. Telev. New Media 2016, 17, 629–645. [Google Scholar] [CrossRef]

- Shin, J.; Park, Y.; Lee, D. Google TV or apple TV?—The reasons for smart TV failure and a user-centered strategy for the success of smart TV. Sustainability 2015, 7, 15955–15966. [Google Scholar] [CrossRef]

- D’Aveni, R.A.; Dagnino, G.B.; Smith, K.G. The age of temporary advantage. Strateg. Manag. J. 2010, 31, 1371–1385. [Google Scholar] [CrossRef]

- Den Hartigh, E.; Ortt, J.R.; van de Kaa, G.; Stolwijk, C.C.M. Platform control during battles for market dominance: The case of apple versus IBM in the early personal computer industry. Technovation 2016, 48–49, 4–12. [Google Scholar] [CrossRef]

- Gallagher, S.R. The battle of the blue laser DVDs: The significance of corporate strategy in standards battles. Technovation 2012, 32, 90–98. [Google Scholar] [CrossRef]

- Suarez, F.F. Battles for technological dominance: An integrative framework. Res. Policy 2004, 33, 271–286. [Google Scholar] [CrossRef]

- Cenamor, J.; Usero, B.; Fernández, Z. The role of complementary products on platform adoption: Evidence from the video console market. Technovation 2013, 33, 405–416. [Google Scholar] [CrossRef]

- Gawer, A.; Cusumano, M.A. Industry platforms and ecosystem innovation. J. Prod. Innov. Manag. 2014, 31, 417–433. [Google Scholar] [CrossRef]

- Thomas, L.W.; Autio, E.; Gann, D.M. Architectural leverage: Putting platforms in context. Acad. Manag. Perspect. 2014, 28, 198–219. [Google Scholar] [CrossRef]

- Wirtz, B.W. Reconfiguration of value chains in converging media and communications markets. Long Range Plan. 2001, 34, 489–506. [Google Scholar] [CrossRef]

- Funk, J.L. The emerging value network in the mobile phone industry: The case of Japan and its implications for the rest of the world. Telecommun. Policy 2009, 33, 4–18. [Google Scholar] [CrossRef]

- Evens, T. Platform leadership in online broadcasting markets. In Handbook of Social Media Management; Springer: Berlin/Heidelberg, Germany, 2013; pp. 477–491. [Google Scholar]

- Wu, I. Canada, South Korea, Netherlands and Sweden: Regulatory implications of the convergence of telecommunications, broadcasting and Internet services. Telecommun. Policy 2004, 28, 79–96. [Google Scholar] [CrossRef]

- Lin, T.T.C. Convergence and regulation of multi-screen television: The Singapore experience. Telecommun. Policy 2013, 37, 673–685. [Google Scholar] [CrossRef]

- Wu, R.W.S.; Leung, G.L.K. Implementation of three network convergence in China: A new institutional analysis. Telecommun. Policy 2012, 36, 955–965. [Google Scholar] [CrossRef]

- Curran, C.-S.; Bröring, S.; Leker, J. Anticipating converging industries using publicly available data. Technol. Forecast. Soc. Chang. 2010, 77, 385–395. [Google Scholar] [CrossRef]

- Yoo, Y.; Boland, R.J.; Lyytinen, K.; Majchrzak, A. Organizing for innovation in the digitized world. Organ. Sci. 2012, 23, 1398–1408. [Google Scholar] [CrossRef]

- Hacklin, F.; Battistini, B.; von Krogh, G. Strategic choices in converging industries. MIT Sloan Manag. Rev. 2013, 55, 65–73. [Google Scholar]

- Li, S.-C.S. Market competition and the media performance of Taiwan’s cable television industry. J. Media Econ. 2004, 17, 279–294. [Google Scholar] [CrossRef]

- Gawer, A.; Cusumano, M.A. How companies become platform leaders. MIT Sloan Manag. Rev. 2008, 49, 28–35. [Google Scholar]

- Wan, X.; Cenamor, J.; Parker, G.; Van Alstyne, M. Unraveling platform strategies: A review from an organizational ambidexterity perspective. Sustainability 2017, 9, 734. [Google Scholar] [CrossRef]

- Urgelles, A. The threat of ott for the pay TV market. In Current and Emerging Issues in the Audiovisual Industry; Medina, M., Herrero, M., Urgellés, A., Eds.; ISTE Ltd./John Wiley & Sons: Hoboken, NJ, USA, 2017. [Google Scholar]

- Srnicek, N. Platform Capitalism; John Wiley & Sons: Hoboken, NJ, USA, 2016. [Google Scholar]

- Tiwana, A.; Konsynski, B.; Bush, A.A. Research commentary: Platform evolution: Coevolution of platform architecture, governance, and environmental dynamics. Inf. Syst. Res. 2010, 21, 675–687. [Google Scholar] [CrossRef]

- Boudreau, K.J.; Hagiu, A. Platform rules: Multi-sided platforms as regulators. In Platforms, Markets and Innovation; Gawer, A., Ed.; Edward Elgar Publishing: Northampton, MA, USA, 2009; pp. 163–191. [Google Scholar]

- Sridhar, S.; Mantrala, M.K.; Naik, P.A.; Thorson, E. Dynamic marketing budgeting for platform firms: Theory, evidence, and application. J. Mark. Res. 2011, 48, 929–943. [Google Scholar] [CrossRef]

- Boudreau, K. Let a thousand flowers bloom? An early look at large numbers of software app developers and patterns of innovation. Organ. Sci. 2012, 23, 1409–1427. [Google Scholar] [CrossRef]

- Chaturvedi, A.R.; Dolk, D.R.; Drnevich, P.L. Design principles for virtual worlds. MIS Q. 2011, 35, 673–684. [Google Scholar] [CrossRef]

- Jeppesen, L.B.; Frederiksen, L. Why do users contribute to firm-hosted user communities? The case of computer-controlled music instruments. Organ. Sci. 2006, 17, 45–63. [Google Scholar] [CrossRef]

- Eisenmann, T.; Parker, G.; Van Alstyne, M. Strategies for two-sided markets. Harv. Bus. Rev. 2006, 84, 92–101. [Google Scholar]

- Roson, R. Two-sided markets a tentative survey. Rev. Netw. Econ. 2005, 4, 142–160. [Google Scholar] [CrossRef]

- Rysman, M. The economics of two-sided markets. J. Econ. Perspect. 2009, 23, 125–143. [Google Scholar] [CrossRef]

- Rochet, J.C.; Tirole, J. Platform competition in twotwoor two-sided. J. Eur. Econ. Assoc. 2003, 1, 990–1029. [Google Scholar] [CrossRef]

- Bhargava, H.K.; Choudhary, V. Economics of an information intermediary with aggregation benefits. Inf. Syst. Res. 2004, 15, 22–36. [Google Scholar] [CrossRef]

- Kauffman, R.J.; Hamid, M. Proprietary and open systems adoption in e-procurement. J. Manag. Inf. Syst. 2004, 21, 137–166. [Google Scholar] [CrossRef]

- Oestreicher-Singer, G.; Zalmanson, L. Content or community? A digital business strategy for content providers in the social age. MIS Q. 2013, 37, 591–616. [Google Scholar] [CrossRef]

- DaSilva, C.M.; Trkman, P. Business model: What it is and what it is not. Long Range Plan. 2014, 47, 379–389. [Google Scholar] [CrossRef]

- Song, M. A study of media business innovation of Korea telecom. Int. J. u- e-Serv. Sci. Technol. 2016, 9, 249–264. [Google Scholar] [CrossRef]

- Suarez, F.F.; Kirtley, J. Dethroning an established platform. MIT Sloan Manag. Rev. 2012, 53, 35–40. [Google Scholar]

- Eisenmann, T.; Parker, G.; Van Alstyne, M. Platform envelopment. Strateg. Manag. J. 2011, 32, 1270–1285. [Google Scholar] [CrossRef]

- Wan, X.; Hu, H.H.; Wu, C. A theoretical and empirical study on China’s transition to digital TV. Telecommun. Policy 2009, 33, 653–663. [Google Scholar]

- Slot, M. Changing user roles in ict developments; the case of digital television. Telemat. Inf. 2007, 24, 303–314. [Google Scholar] [CrossRef]

- Mayo, J.W.; Otsuka, Y. Demand, pricing, and regulation: Evidence from the cable TV industry. RAND J. Econ. 1991, 22, 396–410. [Google Scholar] [CrossRef]

- Otsuka, Y. A welfare analysis of local franchise and other types of regulation: Evidence from the cable TV industry. J. Regul. Econ. 1997, 11, 157–180. [Google Scholar] [CrossRef]

- Chipty, T. Vertical integration, market foreclosure, and consumer welfare in the cable television industry. Am. Econ. Rev. 2001, 91, 428–453. [Google Scholar] [CrossRef]

- Gupta, S.; Mela, C.F. What is a free customer worth? Armchair calculations of nonpaying customers’ value can lead to flawed strategies. Harv. Bus. Rev. 2008, 86, 102–109. [Google Scholar] [PubMed]

- Armstrong, M. Competition in two-sided Markets. RAND J. Econ. 2006, 37, 668–691. [Google Scholar] [CrossRef] [Green Version]

- Rochet, J.-C.; Tirole, J. Cooperation among competitors: Some economics of payment card associations. RAND J. Econ. 2002, 33, 549–570. [Google Scholar] [CrossRef]

- Kaiser, U.; Wright, J. Price structure in two-sided markets: Evidence from the magazine industry. Int. J. Ind. Organ. 2006, 24, 1–28. [Google Scholar] [CrossRef] [Green Version]

- Gal-or, E.; Geylani, T.; Yildirim, T.P. The impact of advertising on media bias. J. Mark. Res. 2012, 49, 92–99. [Google Scholar] [CrossRef]

- Afuah, A. Are network effects really all about size? The role of structure and conduct. Strateg. Manag. J. 2013, 34, 257–273. [Google Scholar] [CrossRef]

- Cusumano, M.A. Platform wars come to social media. Commun. ACM 2011, 54, 31–34. [Google Scholar] [CrossRef]

- Lai, L.S.L.; Turban, E. Groups formation and operations in the web 2.0 environment and social networks. Group Decis. Negotiat. 2008, 17, 387–402. [Google Scholar] [CrossRef]

- Hacklin, F.; Marxt, C.; Fahrni, F. Coevolutionary cycles of convergence: An extrapolation from the ICT industry. Technol. Forecast. Soc. Chang. 2009, 76, 723–736. [Google Scholar] [CrossRef]

- Liu, X. Platform Competition in the Online Video Industry: A Comparison between the United States and Chinese Markets. Master’s Thesis, Massachusetts Institute of Technology, Cambridge, CA, USA, 2013. [Google Scholar]

- Bogers, M.; Afuah, A.; Bastian, B. Users as innovators: A review, critique, and future research directions. J. Manag. 2010, 36, 857–875. [Google Scholar] [CrossRef]

- Pon, B.; Seppälä, T.; Kenney, M. One ring to unite them all: Convergence, the smartphone, and the cloud. J. Ind. Compet. Trade 2015, 15, 21–33. [Google Scholar] [CrossRef]

- Peitz, M.; Valletti, T.M. Content and advertising in the media: Pay-TV versus free-to-air. Int. J. Ind. Organ. 2008, 26, 949–965. [Google Scholar] [CrossRef]

- Gawer, A. Platforms, Markets and Innovation; Edward Elgar Publishing: Northampton, MA, USA, 2009.

- El Sawy, O.A. The is core IX: The 3 faces of is identity: Connection, immersion, and fusion. Commun. Assoc. Inf. Syst. 2003, 12, 588–598. [Google Scholar]

- China Internet Network Information Center. Research Report on Online Video Consumption by Chinese Netizens; CNNIC: Beijing, China, 2013.

- China Internet Network Information Center. The Statistical Report on China’s Internet Development; CNNIC: Beijing, China, 2017.

- Liu, C. Examining China’s triple-network convergence plan: Regulatory challenges and policy recommendations. Gov. Inf. Q. 2013, 30, 45–55. [Google Scholar] [CrossRef]

- Mangold, W.G.; Faulds, D.J. Social media: The new hybrid element of the promotion mix. Bus. Horiz. 2009, 52, 357–365. [Google Scholar] [CrossRef]

- Haridakis, P.; Hanson, G. Social interaction and co-viewing with YouTube: Blending mass communication reception and social connection. J. Broadcast. Electron. Media 2009, 53, 317–335. [Google Scholar] [CrossRef]

- Neter, J.; Wasserman, W.; Kutner, M.H. Applied Regression Models; Irwin: Homewood, IL, USA, 1989. [Google Scholar]

- Lanzolla, G.; Suarez, F.F. Closing the technology adoption–use divide the role of contiguous user bandwagon. J. Manag. 2012, 38, 836–859. [Google Scholar] [CrossRef]

- Adner, R.; Kapoor, R. Value creation in innovation ecosystems: How the structure of technological interdependence affects firm performance in new technology generations. Strateg. Manag. J. 2010, 31, 306–333. [Google Scholar] [CrossRef]

- Afuah, A. Mapping technological capabilities into product markets and competitive advantage: The case of cholesterol drugs. Strateg. Manag. J. 2002, 23, 171–179. [Google Scholar] [CrossRef]

- Strang, D. Adding social structure to diffusion models an event history framework. Sociol. Methods Res. 1991, 19, 324–353. [Google Scholar] [CrossRef]

- Van den Bulte, C.; Stremersch, S. Social contagion and income heterogeneity in new product diffusion: A meta-analytic test. Mark. Sci. 2004, 23, 530–544. [Google Scholar] [CrossRef]

- Beck, N.; Katz, J.N. What to do (and not to do) with time-series cross-section data. Am. Political Sci. Rev. 1995, 89, 634–647. [Google Scholar] [CrossRef]

- Logan, K. Hulu.com or NBC? Streaming video versus traditional TV. J. Advert. Res. 2011, 51, 276–287. [Google Scholar] [CrossRef]

- Kim, J. The institutionalization of youtube: From user-generated content to professionally generated content. Media Cult. Soc. 2012, 34, 53–67. [Google Scholar] [CrossRef]

- Zhang, J.; Liang, X.-J. Business ecosystem strategies of mobile network operators in the 3G era: The case of china mobile. Telecommun. Policy 2011, 35, 156–171. [Google Scholar] [CrossRef]

{kind=link}

| Cable Operators | OTT Service Providers | |

|---|---|---|

| Orientation | Both administrative and market orientation | Market orientation |

| Ownership and control right | State owned, and controlled by local governments | Most OTT service providers privately owned |

| Market structure | Fragmented in cities and counties, with disconnected networks | Dozens of OTT service providers; less than 20 with national influence |

| Content-related business | Content transmission, aggregation and value-added content services like VOD | Online content production, aggregation and broadcasting |

| Major source of revenues | Subscription fees, and revenues from value-added digital TV services | Advertising revenues |

| Mean | SD | Min | Max | 1 | 2 | 3 | 4 | 5 | 6 | Sources | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 1. LnDigcov | 14.47 | 0.98 | 11.08 | 16.49 | 1.00 | 1 | |||||

| 2. Ln Paycov | 11.65 | 2.12 | 3.91 | 14.91 | 0.68 | 1.00 | 1 | ||||

| 3. LnNumchan | 3.54 | 0.29 | 2.40 | 4.19 | 0.55 | 0.38 | 1.00 | 1 | |||

| 4. LnNetlen | 11.37 | 0.98 | 7.68 | 13.03 | 0.54 | 0.58 | 0.08 | 1.00 | 1 | ||

| 5. Ln View | 5.05 | 0.11 | 4.82 | 5.33 | 0.14 | −0.06 | 0.03 | 0.28 | 1.00 | 2 | |

| 6. Broadpen (%) | 30.02 | 15.55 | 7.02 | 79.09 | 0.69 | 0.46 | 0.58 | 0.33 | 0.17 | 1.00 | 3 |

| Mean | SD | Min | Max | 1 | 2 | 3 | 4 | 5 | 6 | |

|---|---|---|---|---|---|---|---|---|---|---|

| 1. LnCoverage | 8.79 | 0.69 | 7.17 | 10.25 | 1.00 | |||||

| 2. LnPV | 7.16 | 1.19 | 4.66 | 9.51 | 0.03 | 1.00 | ||||

| 3. UGC | 0.51 | 0.50 | 0.00 | 1.00 | 0.11 | 0.17 | 1.00 | |||

| 4. Mobile | 0.55 | 0.50 | 0.00 | 1.00 | 0.54 | −0.12 | −0.02 | 1.00 | ||

| 5. Age | 5.82 | 1.62 | 1 | 8 | 0.24 | 0.17 | 0.39 | 0.35 | 1.00 | |

| 6. Internetpen (%) | 42.06 | 3.09 | 38.30 | 45.80 | 0.52 | −0.04 | 0.09 | 0.69 | 0.41 | 1.00 |

| Model 1 | Model 2 | Model 3 | |

|---|---|---|---|

| Digcov | 0.208 *** (8.883) | −0.172 *** (−1.911) | |

| Paycov | 0.084 *** (6.407) | 0.092 *** (7.460) | |

| Numchan | 0.104 ** (2.220) | −1.568 *** (−4.166) | |

| Netlen | 0.064 (−1.197) | −0.060 (−1.197) | −0.038 (−0.877) |

| View | 0.147 * (−2.121) | −0.250 ** (−2.121) | −0.471 *** (−2.974) |

| Broadpen | 0.798 *** (6.194) | 0.263 *** (6.194) | 0.235 *** (5.071) |

| Numchan × Digcov | 0.113 *** (4.458) | ||

| Regional dummies | Yes | Yes | Yes |

| R2 adjusted | 0.942 | 0.961 | 0.963 |

| Redundant Fixed Effects Tests Cross-section F (Prob.) | 58.091 (0.000) | 36.016 (0.000) | 43.010 (0.000) |

| Period F (Prob.) | 3.458 (0.052) | 2.179 (0.060) | 2.034 (0.078) |

| Hausman test prob. | 0.001 | 0.001 | 0.000 |

| Model 4 | Model 5 | Model 6 | |

|---|---|---|---|

| Coverage2 | 0.095 *** (6.965) | 0.118 ** (3.690) | |

| PV | −0.227 *** (−4.622) | −0.198 ** (−2.667) | |

| UGC | 0.299 *** (13.347) | −4.486 *** (−3.248) | |

| Mobile | 0.561 *** (22.011) | 0.498 *** (15.203) | |

| UGC × Coverage | 0.516 ** (2.599) | ||

| UGC × PV | −0.048 (−0.500) | ||

| Age | 1.104 *** (11.498) | 0.870 *** (6.633) | 1.035 *** (5.054) |

| Internetpen | 0.333 ** (8.885) | 0.437 * (1.883) | −0.484 (−0.763) |

| Website Dummies | Yes | Yes | Yes |

| R2 adjusted | 0.586 | 0.896 | 0.898 |

| Redundant Fixed Effects Tests Cross-section F (Prob.) | 59.291 (0.000) | 30.266 (0.000) | 10.157 (0.000) |

| Period F (Prob.) | 7.218 (0.058) | 3.421 (0.082) | 2.917 (0.063) |

| Hausman test prob. | 0.000 | 0.000 | 0.000 |

© 2017 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Wan, X.; Cenamor, J.; Chen, J. Exploring Performance Determinants of China’s Cable Operators and OTT Service Providers in the Era of Digital Convergence—From the Perspective of an Industry Platform. Sustainability 2017, 9, 2247. https://doi.org/10.3390/su9122247

Wan X, Cenamor J, Chen J. Exploring Performance Determinants of China’s Cable Operators and OTT Service Providers in the Era of Digital Convergence—From the Perspective of an Industry Platform. Sustainability. 2017; 9(12):2247. https://doi.org/10.3390/su9122247

Chicago/Turabian StyleWan, Xing, Javier Cenamor, and Jing Chen. 2017. "Exploring Performance Determinants of China’s Cable Operators and OTT Service Providers in the Era of Digital Convergence—From the Perspective of an Industry Platform" Sustainability 9, no. 12: 2247. https://doi.org/10.3390/su9122247