Sustainability Performance Management Framework for Circular Economy Implementation in State-Owned Plantation Enterprises

Abstract

:1. Introduction

2. Literature Review

2.1. Circular Economy and the Concept of Sustainability

2.2. Balanced Scorecard

2.3. Triple Bottom Line

2.4. Sustainability Balanced Scorecard

3. Methodology

3.1. Framework Design Stages

3.1.1. Stakeholder Value Formulation Using SBSC Approach

3.1.2. Formulate Organizational Strategic Goals Based on Stakeholder Values

3.1.3. Validation

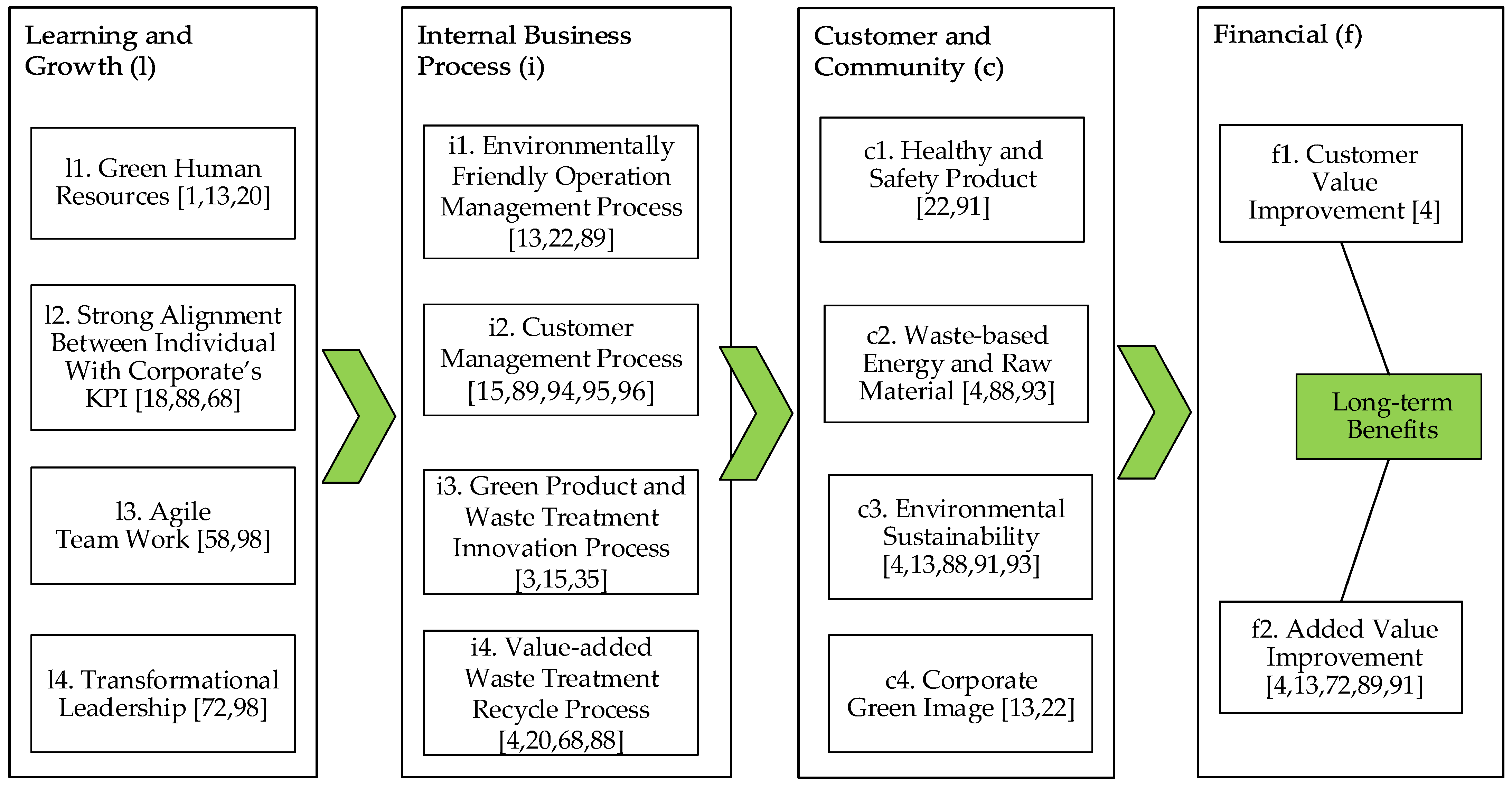

4. Results and Discussion

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Initial Framework | Interviews Results and Document Analysis | Code | Theme Strategic Goals | Validation |

|---|---|---|---|---|

| f1 | High product quality standards, for example: sugar products. | f11 | Customer value improvement | 100% |

| High product quality standards, for example: golden CPO. | f12 | |||

| f2 | Processing of PKS liquid waste into biogas | f21 | Added value Improvement | 100% |

| Processing molasses liquid waste into bioethanol | f22 | |||

| Palm kernel shell waste processed into briquettes | f23 | |||

| Processing forage waste and cakes into animal feed ingredients | f24 | |||

| Processing of solid and liquid waste into organic fertilizer | f25 | |||

| c1 | Do not use harmful additives | c11 | Healthy and Safety Product | 100% |

| Low glycaemic sugar products that are safe to use for diabetics | c12 | |||

| Golden CPO produced with an excellent production process. | c13 | |||

| c2 | Conversion of sugarcane shoots, oil palm meal, and palm oil mill sludge solids for animal feed | c21 | Waste-based Energy and Raw Material | 100% |

| Conversion of sugarcane bagasse, palm shell, and palm fibre for boiler fuel | c22 | |||

| Conversion of molasses for raw material for the manufacture of bioethanol | c23 | |||

| Conversion of sugarcane fronds, palm fronds, oil palm empty fruit bunches, palm oil effluent, and palm oil mill sludge solids to organic fertilizer for land | c24 | |||

| Palm shells are used as paving materials. | c25 | |||

| The wood from the land clearing will be used as smoked wood in the rubber factory. | c26 | |||

| Converting PKS liquid waste into biogas | c27 | |||

| c3 | Crop rotation, planting legumes, organic fertilization from liquid and solid waste from sugarcane, CPO, and PKO mills to maintain soil fertility. | c31 | environmental sustainability | 100% |

| Integrated pest control using natural predators and host plants | c32 | |||

| Planting perennials in watersheds to prevent erosion | c33 | |||

| c4 | Obtaining the proper green predicate from the Ministry of the Environment | c41 | Corporate Green Image | 100% |

| ISPO certification | c42 | |||

| RSPO certification | c43 | |||

| ISCC certification | c44 | |||

| UTZ certification | c45 | |||

| i1 | Implementation of standardization of quality control processes using ISO 9000:2015 | i11 | The environmentally friendly Operation management process | 100% |

| Implementation of environmental management standardization using ISO 14001 and proper | i12 | |||

| Implementation of ISPO certification to reduce greenhouse gas emissions | i13 | |||

| Implementation of RSPO certification for best practice control with social and environmental considerations | i14 | |||

| Implementation of ISCC certification for the concept of sustainability and greenhouse gas emissions | i15 | |||

| Compliance with renewable energy directive’s (RED) requirements in the European Union | i16 | |||

| i2 | Services to consumers of sugar sold to wholesalers, and buyers take it to the location so that it is more efficient and energy-efficient | i21 | Customer Management Process | 100% |

| Services for tobacco consumers are carried out through exports to other countries. | i22 | |||

| Services for consumers of CPO and sugar are carried out through direct selling, where consumers visit the product warehouse. | i23 | |||

| i3 | Process innovation for low glycaemic sugar | i31 | Green Product and Waste Treatment Innovation Process | 100% |

| The innovation of the waste treatment process is carried out, among others, through the manufacture of bioethanol using raw materials derived from sugarcane litter which previously used molasses as raw material. | i32 | |||

| Innovation of biogas products to obtain biogas with higher methane gas content | i33 | |||

| Waste treatment innovations are carried out, among others, through liquid waste containers in holding ponds that are channeled to palm oil fields using pumps. | i34 | |||

| Innovations in handling gas waste are carried out, among others, by making chimneys high above the ground and processing factory waste directly applied to the ground through ditches. | i35 | |||

| i4 | The success of processing sugarcane shoots and palm oil meal waste is used for animal feed. | i41 | Value-added waste treatment Recycle process | 100% |

| Successful treatment of waste bagasse for boiler fuel | i42 | |||

| The success of processing molasses waste for raw material for making bioethanol or selling it to other factories | i43 | |||

| The success of processing sugarcane litter for compost | i44 | |||

| The success of processing palm oil shell waste into briquettes using palm oil shell waste into briquettes | i45 | |||

| The success of processing waste from empty fruit bunches is used as raw material for paper pulp. | i46 | |||

| The success of processing palm oil waste into biogas | i47 | |||

| The success of processing palm oil waste into organic fertilizer | i48 | |||

| Successful treatment of waste hot steam from boilers for power generation | i49 | |||

| Utilization of waste from oil palm and rubber plantations in the form of plant roots and wood from land clearing, which will be sold directly | i410 | |||

| l1 | Increasing the competence of skilled human resources in managing environmentally friendly production processes | l11 | Green Human resources | 100% |

| Have a sustainability paradigm, and have the awareness to implement it | l12 | |||

| An employee that runs ISO 14001 is certified. | l13 | |||

| Employees run Occupational Health and Safety (K3), Reuse, Reduce and Recycle (3R), and ISO 14001 programs to protect the environment. | l14 | |||

| All employees are committed to achieving the highest predicate in managing the environment. | l15 | |||

| Internalization of organizational culture is carried out through a morning briefing to discuss the evaluation of past activities and the delivery of targets for the day. | l16 | |||

| l2 | The company’s and work unit’s sustainability and circular economic performance targets are aligned with individual KPIs so that employees’ work will be focused and aligned with the company’s vision of sustainability. | l21 | Strong Alignment between an individual with Corporate’s KPI | 100% |

| The unit operationalizes the company’s vision to care for the environment. | l22 | |||

| l3 | The existence of an investment committee consisting of various units to discuss the company’s budgeting that accommodates requests for budget allocations based on performance targets and unit potentials | l31 | Agile Teamwork | 100% |

| Building aggressive cross-organizational teamwork for organizational change, when some new policies or systems will be implemented | l32 | |||

| Forming teamwork to adopt certain technologies such as crowdfunding and e-farming that the company has implemented | l33 | |||

| Teamwork competence is one of the assessment elements considered for promotion. | l34 | |||

| l4 | The success of the leadership set targets in line with GM’s commitment to headquarters. This target was conveyed through a meeting of all factory employees and signed the agreement between GM, Supervisor, and the coordinator, cascading to each department. | l41 | Transformational leadership | 100% |

| The individual targets stated in the Work Target Agreement (KSK) are determined top-down by considering fairness for each unit and division following the directors’ targets. | l42 |

References

- Agrawala, S.; Singh, R.K.; Murtaza, Q. Outsourcing decisions in reverse logistics: Sustainable balanced scorecard and graph theoretic approach. J. Resour. Conserv. Recycl. 2016, 108, 41–53. [Google Scholar] [CrossRef]

- Amrina, E.; Ramadhani, C.; Vilsi, A.F. Fuzzy multi criteria approach for sustainable manufacturing evaluation in cement industry. Procedia CIRP 2016, 40, 619–624. [Google Scholar] [CrossRef] [Green Version]

- Baumgartner, R.J.; Rauter, R. Strategic perspectives of corporate sustainability management to develop a sustainable organization. J. Clean. Prod. 2017, 140, 81–92. [Google Scholar] [CrossRef]

- Dočekalová, M.P.; Kocmanová, A. Composite indicator for measuring corporate sustainability. Ecol. Indic. 2016, 61, 612–623. [Google Scholar] [CrossRef]

- Edgeman, R.; Eskildsen, J. Modeling and assessing sustainable enterprise excellence. Bus. Strateg. Environ. 2014, 23, 173–187. [Google Scholar] [CrossRef]

- Ahmed, M.D.; Sundaram, D. Sustainability modelling and reporting: From roadmap to implementation. J. Decis. Support Syst. 2012, 53, 611–624. [Google Scholar] [CrossRef]

- Figge, F.; Hahn, T.; Schaltegger, S.; Wagner, M. The sustainability balanced scorecard linking sustainability management to business strategy. Bus. Strateg. Environ. 2002, 11, 269–284. [Google Scholar] [CrossRef]

- Fulop, G.; Hernadi, B.; Jalali, M.; Kavaliauskiene, L.M.; Ferreira, F. Developing of sustainability balanced scorecard for the chemical industry: Preliminary evidence from a case analysis. Inz. Ekon.-Eng. Econ. 2014, 25, 341–349. [Google Scholar] [CrossRef] [Green Version]

- Journeault, M. The Integrated Scorecard in support of corporate sustainability strategies. J. Clean. Prod. 2016, 182, 214–229. [Google Scholar] [CrossRef]

- Junior, N.A.J.; Oliveira, M.C.; Helleno, A.L. Sustainability evaluation model for manufacturing sistems based on the correlation between triple bottom line dimensions and balanced scorecard perspectives. J. Clean. Prod. 2018, 190, 84–93. [Google Scholar] [CrossRef]

- Kalender, Z.T.; Vayvay, O. The fifth pillar of the balanced scorecard: Sustainability. Procedia Soc. Behav. Sci. 2016, 235, 76–83. [Google Scholar] [CrossRef]

- Nikolaou, I.E.; Tsalis, T.A. Development of a sustainable balanced scorecard framework. Ecol. Indic. 2013, 34, 76–86. [Google Scholar] [CrossRef]

- Elkington, J. Cannibals with Forks: The Triple Bottom Line of 21st Century Business; Capstone: Oxford, UK, 1997. [Google Scholar]

- Kaplan, R.S.; Norton, D.P. The Balanced Scorecard: Measures That Drive Performance; Harvard Business Review: Boston, MA, USA, 1992; pp. 71–79. [Google Scholar]

- Kaplan, R.S.; Norton, D. The Strategy-Focused Organization: How Balanced Scorecard Companies Thrive in the New Business Environment, 1st ed.; Harvard Business Review Press: Boston, MA, USA, 2000. [Google Scholar]

- Asiaei, K.; Jusoh, R. Using a robust performance measurement system to illuminate intellectual capital. Int. J. Account. Inf. Syst. 2017, 26, 1–19. [Google Scholar] [CrossRef]

- Bautista, S.; Enjolras, M.; Narvaez, P.; Camargo, M.; Morel, L. Biodiesel-triple bottom line (TBL): A new hierarchical sustainability assessment framework of principles criteria and indicators (PC dan I) for biodiesel production. Part II-validation. Ecol. Indic. 2016, 69, 803–817. [Google Scholar] [CrossRef]

- Campos, L.M.S.; Heizen, D.A.M.; Verdinelli, M.A.; Miguel, C. Environmental performance indicators: A study on ISO 14001 certified companies. J. Clean. Prod. 2015, 99, 286–296. [Google Scholar] [CrossRef]

- Chalmeta, R.; Palomero, S. Methodological proposal for business sustainability management by means of the Balanced Scorecard. J. Oper. Res. Soc. 2011, 62, 1344–1356. [Google Scholar] [CrossRef]

- Helleno, A.L.; Moraes, A.J.M.; Simon, A.T. Integrating sustainability indicators and lean manufacturing to assess manufacturing processes: Application case studies in Brazilian industry. J. Clean. Prod. 2017, 153, 405–416. [Google Scholar] [CrossRef]

- Hristov, I.; Chirico, A.; Appolloni, A. Sustainability value creation, survival, and growth of the company: A critical perspective in the Sustainability Balanced Scorecard (SBSC). J. Sustain. 2019, 11, 2119. [Google Scholar] [CrossRef] [Green Version]

- Hsu, C.-W.; Hu, A.H.; Chiou, C.-Y.; Chen, T.-C. Using the FDM and ANP to construct a sustainability balanced scorecard for the semiconductor industry. J. Clean. Prod. 2011, 38, 12881–12889. [Google Scholar] [CrossRef]

- Isaksson, R.B.; Garvare, R.; Johnson, M. The crippled bottom line—Measuring and managing sustainability. Int. J. Product. Perform. Manag. 2015, 64, 334–355. [Google Scholar] [CrossRef]

- Nouri, F.A.; Nikabadi, M.S. Developing the framework of sustainable service supply chain balanced scorecard (SSSC BSC). Int. J. Product. Perform. Manag. 2018, 68, 148–170. [Google Scholar] [CrossRef]

- Rimppi, H.; Uusitalo, V.; Väisänen, S.; Soukka, R. Sustainability criteria and indicators of bioenergy systems from steering, research and Finnish bioenergy business operators’ perspectives. Ecol. Indic. 2016, 66, 357–368. [Google Scholar] [CrossRef]

- Soriano, R.L.; Torres, M.J.; Chalmeta, R.R. Methodology for sustainability strategic planning and management. Ind. Manag. Data Syst. 2009, 110, 249–268. [Google Scholar] [CrossRef]

- Tai, X.; Xiao, W.; Tang, Y. A quantitative assessment of vulnerability using social-economic natural compound ecosystem framework in coal mining cities. J. Clean. Prod. 2020, 258, 120969. [Google Scholar] [CrossRef]

- Trisyulianti, E.; Suryadi, K.; Prihantoro, B. A conceptual framework of sustainability balanced scorecard for stated-own plantation enterprises. In Proceedings of the 7th International Conference on Frontiers of Industrial Engineering (ICFIE 2020), Singapore, 18–20 September 2020. [Google Scholar]

- Tsai, F.M.; Bui, T.D.; Tseng, M.L.; Wu, K.J.; Chiu, A.S.F. A performance assessment approach for integrated solid waste management using a sustainable balanced scorecard approach. J. Clean. Prod. 2019, 251, 119740. [Google Scholar] [CrossRef]

- Wilburn, K.; Wilburn, R. The double bottom line: Profit and social benefit. Bus. Horiz. 2014, 57, 11–20. [Google Scholar] [CrossRef]

- Korhonen, J.; Honkasalo, A.; Seppala, J. Circular Economy: The Concept and its Limitations. Ecol. Econ. 2018, 143, 37–46. [Google Scholar] [CrossRef]

- Wang, P.; Che, F.; Fan, S.; Gu, C. Ownership governance, institutional pressures and circular economy accounting information disclosure: An institutional theory and corporate governance theory perspective. Chin. Manag. Stud. 2014, 8, 487–501. [Google Scholar] [CrossRef]

- Zhijun, F.; Nailing, Y. Putting a circular economy into practice in China. Sustain. Sci. 2007, 2, 95–101. [Google Scholar] [CrossRef]

- Ma, S.; Hu, S.; Chen, D.; Zhu, B. A case study of a phosphorus chemical firm’s application of resource efficiency and eco-efficiency in industrial metabolism under circular economy. J. Clean. Prod. 2015, 87, 839–849. [Google Scholar] [CrossRef]

- Dajian, Z. Background, pattern and policy of China for developing circular economy. Chin. J. Popul. Resour. Environ. 2008, 6, 3–8. [Google Scholar] [CrossRef]

- Stahel, W.R.; Reday, G. The Potential for Substituting Manpower for Energy; European Communities: Brussels, Belgium, 1976. [Google Scholar]

- Stahel, W.R.; Reday, G. Jobs for Tomorrow, the Potential for Substituting Manpower for Energy; Vantage Press: New York, NY, USA, 1981. [Google Scholar]

- Pearce, D.W.; Turner, R.K. Economics of Natural Resources and the Environment; The Johns Hopkins University Press: Baltimore, MD, USA, 1990; pp. 35–42. [Google Scholar]

- Boulding, K.E. The Economics of the Coming Spaceship Earth. In Environmental Quality in a Growing Economy; Jarrett, H., Ed.; Johns Hopkins University Press: Baltimore, MD, USA, 1966; pp. 3–14. [Google Scholar]

- Su, Y.; Zhou, H. Promoting circular economy development a basic national policy. North. Econ. 2005, 1, 8–10. [Google Scholar]

- Kumar, V.; Sezersan, I.; Garza-Reyes, J.A.; Gonzalez, E.D.R.S.; Al-Shboul, M.A. Circular economy in the manufacturing sector: Benefits, opportunities and barriers. Manag. Decis. 2019, 57, 1067–1086. [Google Scholar] [CrossRef] [Green Version]

- Peters, G.P.; Weber, C.L.; Guan, D.; Hubacek, K. China’s growing CO2 emissions: A race between increasing consumption and efficiency gains. Environ. Sci. Technol. 2007, 41, 5939–5944. [Google Scholar] [CrossRef] [Green Version]

- Beckmann, A.; Sivarajah, U.; Irani, Z. Circular economy versus planetary limits: A Slovak forestry sector case study. J. Enterp. Inf. Manag. 2020, 34, 1673–1698. [Google Scholar] [CrossRef]

- Murray, A.; Skene, K.; Haynes, K. The circular economy: An interdisciplinary exploration of the concept and application in a global context. J. Bus. Ethics 2015, 140, 369–380. [Google Scholar] [CrossRef] [Green Version]

- Ellen MacArthur Foundation (EMF). Towards the Circular Economy: Economic and Business Rationale for an Accelerated Transition; Ellen MacArthur Foundation: Cowles, UK, 2013; p. 26. [Google Scholar]

- Zhu, Q.; Geng, Y.; Lai, K.H. Environmental supply chain cooperation and its effect on the circular economy practice-performance relationship among Chinese manufacturers. J. Ind. Ecol. 2011, 15, 405–419. [Google Scholar] [CrossRef]

- MacArthur, E. Towards a Circular Economy—Opportunities for the Consumer Goods Sector; Ellen MacArthur Foundation: Bristol, UK, 2013; Available online: www.ellenmacarthurfoundation.org/assets/downloads/publications/TCE_Report-2013.pdf (accessed on 25 October 2021).

- Feng, Z. Circular Economy Overview; People’s Publishing House: Beijing, China, 2004. (In Chinese) [Google Scholar]

- Ghisellini, P.; Cialani, C.; Ulgiati, S. A review on circular economy: The expected transition to a balanced interplay of environmental and economic systems. J. Clean. Prod. 2016, 114, 11–32. [Google Scholar] [CrossRef]

- Stahel, W.R. Circular economy. Nature 2016, 531, 435–438. [Google Scholar] [CrossRef] [Green Version]

- Ripanti, E.F.; Tjahjono, B. Unveiling the potentials of circular economy values in logistics and supply chain management. Int. J. Logist. Manag. 2019, 30, 723–742. [Google Scholar] [CrossRef] [Green Version]

- Jawahir, I.S.; Bradley, R. Technological Elements of Circular Economy and the Principles of 6R-Based Closed-loop Material Flow in Sustainable Manufacturing. Procedia CIRP 2016, 40, 103–108. [Google Scholar] [CrossRef] [Green Version]

- Winans, K.; Kendall, A.; Deng, H. The history and current applications of the circular economy concept. Renew. Sustain. Energy Rev. 2017, 68, 825–833. [Google Scholar] [CrossRef]

- De Vasconcelos, D.C.; Viana, F.L.E.; De Souza, A.L. Circular Economy and Sustainability in the Fresh Fruit Supply Chain: A Study across Brazil and the UK. Lat. Am. Bus. Rev. 2021, 22, 393–421. [Google Scholar] [CrossRef]

- Ferronato, N.; Rada, E.C.; Portillo, M.A.G.; Cioca, L.I.; Ragazzi, M.; Torretta, V. Introduction of the circular economy within developing regions: A comparative analysis of advantages and opportunities for waste valorization. J. Environ. Manag. 2019, 230, 366–378. [Google Scholar] [CrossRef]

- Geng, Y.; Fu, J.; Sarkis, J.; Xue, B. Towards a national circular economy indicator system in China: An evaluation and critical analysis. J. Clean. Prod. 2012, 23, 216–224. [Google Scholar] [CrossRef]

- Rada, E.C.; Cioca, L.I.; Ionescu, G. Energy recovery from Municipal Solid Waste in EU: Proposals to assess the management performance under a circular economy perspective. MATEC Web Conf. 2017, 121, 1–8. [Google Scholar] [CrossRef] [Green Version]

- Sehnem, S.; Jabbour, C.J.C.; Pereira, S.C.F.; Jabbour, A.B.L. Improving sustainable supply chains performance through operational excellence: Circular economy approach. Resour. Conserv. Recycl. 2019, 149, 236–248. [Google Scholar] [CrossRef]

- Su, C.; Urban, F. Circular economy for clean energy transitions: A new opportunity under the COVID-19 pandemic. Appl. Energy 2021, 288, 116666. [Google Scholar] [CrossRef]

- Su, B.; Heshmati, A.; Geng, Y.; Yu, X. A review of the circular economy in China: Moving from rethoric to implementation. J. Clean. Prod. 2013, 42, 215–277. [Google Scholar] [CrossRef]

- Stumpf, L.; Schoggl, J.; Baumgartner, R.J. Climbing up the circularity ladder?—A mixed-methods analysis of circular economy in business practice. J. Clean. Prod. 2021, 316, 128158. [Google Scholar] [CrossRef]

- Maldonado-Guzman, G.; Garza-Reyes, J.A.; Pinzón-Castro, Y. Eco-innovation and the circular economy in the automotive industry. Benchmarking Int. J. 2021, 28, 621–635. [Google Scholar] [CrossRef]

- Zaman, A.U.; Lehmann, S. The zero-waste index: A performance measurement tool for waste management systems in a “zero waste city”. J. Clean. Prod. 2013, 50, 123–132. [Google Scholar] [CrossRef]

- Golinska, P.; Kosacka, M.; Mierzwiak, R.; Werner-Lewandowska, K. Grey decision making as a tool for the classification of the sustainability level of remanufacturing companies. J. Clean. Prod. 2015, 105, 28–40. [Google Scholar] [CrossRef]

- Park, J.J.; Chertow, M. Establishing and testing the “reuse potential” indicator for managing waste as resources. J. Environ. Manag. 2014, 137, 45–53. [Google Scholar] [CrossRef]

- Kaplan, R.S. Conceptual foundations of the balanced scorecard. In Handbook of Management Accounting Research; Working Paper 10-074; Elsevier: Amsterdam, The Netherlands, 2010; Volume 3, pp. 1–36. [Google Scholar]

- Kaplan, R.S.; Norton, D. Alignment: Using the Balanced Scorecard to Create Corporate Synergies; HBS Press: Boston, MA, USA, 2006. [Google Scholar]

- Slaper, T. The triple bottom line: What is it and how does it work? Indiana University Kelley School of Business. Indiana Bus. Res. Cent. 2011, 86, 4–8. [Google Scholar]

- Govindan, K.; Seuring, S.; Zhu, Q.; Azevedo, S.G. Accelerating the transition towards sustainability dynamics into supply chain relationship management and governance structures. J. Clean. Prod. 2016, 112, 1813–1823. [Google Scholar] [CrossRef]

- Parnell, J.A. Strategic Management: Theory and Practice, 4th ed.; SAGE: Newcastle upon Tyne, UK, 1964. [Google Scholar]

- David, F.R. Strategic Management Concepts and Cases; Pearson: London, UK, 2011. [Google Scholar]

- Kaplan, R.S.; Norton, D. The Balanced Scorecard: Translating Strategy into Action; HBS Press: Boston, MA, USA, 1996. [Google Scholar]

- Ahmad, S.; Nisar, T. Green Human Resource Management: Policies and practices. Cogent Bus. Manag. 2015, 2, 1030817. [Google Scholar] [CrossRef]

- Senechal, O. Research directions for integrating the triple bottom line in maintenance dashboards. J. Clean. Prod. 2017, 142, 331–342. [Google Scholar] [CrossRef]

- Hansen, E.G.; Schaltegger, S. The sustainability balanced scorecard: A systematic review of architectures. J. Bus. Ethics 2014, 133, 193–221. [Google Scholar] [CrossRef]

- Zarte, M.; Pechman, A.; Nunes, I.L. Decision support systems for sustainable manufacturing surrounding the product and production life cycle, A literature review. J. Clean. Prod. 2019, 219, 336–349. [Google Scholar] [CrossRef]

- Jamaludin, N.F.; Hashim, H.; Muis, Z.A.; Zakaria, Z.Y.; Jusoh, M.; Yunus, A.; Murad, S.M.A. A sustainability performance assessment framework for palm oil mills. J. Clean. Prod. 2018, 174, 1679–1693. [Google Scholar] [CrossRef]

- Kumar, A.; Anbanandam, R. Assessment of environmental and social sustainability performance of the freight transportation industry: An index-based approach. Transp. Policy 2020. [Google Scholar] [CrossRef]

- Gohar, E.A.A. Sustainable Balanced Scorecard: A new approach to vision and implementation of a sustainable strategy in Egyptian travel agencies. Int. J. Tour. Hosp. Manag. 2019, 2, 98–126. [Google Scholar]

- Hansen, E.G.; Schaltegger, S. Sustainability balanced scorecards and their architectures: Irrelevant or misunderstood? . J. Bus. Ethics. 2017, 150, 937–952. [Google Scholar] [CrossRef] [Green Version]

- Huang, T.; Pepper, M.; Bowrey, G. Implementing a sustainability balanced scorecard to contribute to the process of organizational, Australasian Accounting. J. Legitimacy Assess. Bus. Financ. 2014, 8, 15–34. [Google Scholar]

- Lee, S.; Geuma, Y.; Lee, H.; Park, Y. Dynamic and multidimensional measurement of product-service system (PSS) sustainability: A triple bottom line (TBL) based sistem dynamics approach. J. Clean. Prod. 2012, 32, 173–182. [Google Scholar] [CrossRef]

- Lu, M.T.; Hsu, C.C.; Liou, J.J.H.; Loc, H.W. A hybrid MCDM and sustainability-balanced scorecard model to establish sustainable performance evaluation for international airports. J. Air Transp. Manag. 2018, 71, 9–19. [Google Scholar] [CrossRef]

- Petrini, M.; Pozzebon, M. Managing sustainability with the support of business intelligence: Integrating socio-environmental indicators and organizational context. J. Strateg. Inf. Syst. 2009, 18, 178–191. [Google Scholar] [CrossRef]

- Pislaru, M.; Herghiligiu, I.V.; Robu, I.B. Corporate sustainable performance assessment based on fuzzy logic. J. Clean. Prod. 2019, 223, 998–1013. [Google Scholar] [CrossRef]

- Wicher, P.; Zapletal, F.; Lenort, R. Sustainability performance assessment of industrial corporation using Fuzzy Analytic Network Process. J. Clean. Prod. 2019, 241, 118132. [Google Scholar] [CrossRef]

- Freeman, E. Stakeholder Management: Framework and Philosophy; Pitman: Boston, MA, USA, 1984. [Google Scholar]

- Munteanu, V.; Danaiata, D.; Hurbean, L.; Bergler, A. The value-based management approach: From the shareholder value to the stakeholder value. In Proceedings of the 6th International Management Conference, Approaches in Organizational Management, Bucharest, Romania, 15–16 November 2012. [Google Scholar]

- Freudenreich, B.; Freund, F.L.; Schaltegger, S. A stakeholder theory perspective on business models: Value creation for sustainability. J. Bus. Ethics 2019, 166, 3–18. [Google Scholar] [CrossRef]

- Bohari, A.A.M.; Skitmore, M.; Xia, B.; Teo, M.; Khalil, N. Key stakeholder values in encouraging green orientation of construction procurement. J. Clean. Prod. 2020, 20, 122246. [Google Scholar] [CrossRef]

- Chang, A.-Y.; Cheng, Y.-T. Analysis model of the sustainability development of manufacturing small and medium sized enterprises in Taiwan. J. Clean. Prod. 2019, 207, 458–473. [Google Scholar] [CrossRef]

- Kamali, M.; Hewage, K. Development of performance criteria for sustainability evaluation of modular versus conventional construction methods. Int. J. Clean. Prod. 2017, 142, 3592–3606. [Google Scholar] [CrossRef]

- Huang, A.; Badurdeen, F. Sustainable manufacturing performance evaluation: Integrating product and process metrics for systems level assessment. Procedia Manuf. 2017, 8, 563–570. [Google Scholar] [CrossRef]

- Franz, P.H.; Krichmer, M.; Rosemann, M. Value-Driven Business Process Management, Impact and Benefits; Accenture: Dublin, Ireland; Queensland University of Technology: Brisbane, Australia, 2012. [Google Scholar]

- Mohammadfam, I.; Kamalinia, M.; Momeni, M.; Golmohammadi, R.; Hamidi, Y.; Soltanian, A. Evaluation of the quality of occupational health and safety management systems based on key performance indicators in certified organizations. Saf. Health Work 2017, 8, 156–161. [Google Scholar] [CrossRef] [PubMed]

- Neely, A.; Gregory, M.; Platts, K. Performance measurement system design a literature review and research agenda. Int. J. Oper. Prod. Manag. 2005, 25, 1228–1263. [Google Scholar]

- Harmon, J.; Fairfield, K.D.; Wirtenberg, J. Missing an opportunity: HR leadership and sustainability. People Strategy 2010, 33, 16–21. [Google Scholar]

- Perkin, N.; Abraham, P. Building the Agile Business through Digital Transformation, 1st ed.; Kogan Page: New York, NY, USA, 2017. [Google Scholar]

- Yin, R.k. Case Study Research Design and Methods, 5th ed.; SAGE Publications Inc.: New York, NY, USA, 2014. [Google Scholar]

- Sladana, J. The Coding Manual for Qualitative Researchers, 2nd ed.; Sage: London, UK, 2013. [Google Scholar]

- Sekaran, U.; Bougie, R. Research Methods for Business—A Skill-Building Approach; John Wiley and Sons Ltd.: Hoboken, NJ, USA, 2016. [Google Scholar]

- Anthony Robert N. Planning and Control Systems: A Framework for Analysis; Division of Research, Graduate School of Business Administration, Harvard University: Boston, MA, USA, 1965. [Google Scholar]

| Authors | Reduce | Reuse | Recycling | Remanufacturing | Disposal | Additional Indicators |

|---|---|---|---|---|---|---|

| [31] | v | v | v | v | ||

| [41] | v | v | v | v | ||

| [42] | v | v | v | Close material loops | ||

| [54] | v | v | v | Renovation | ||

| [55] | v | v | ||||

| [56] | v | v | v | Added value | ||

| [52] | v | v | ||||

| [57] | v | |||||

| [58] | Knowledge, behavior, and culture | |||||

| [59] | v | v | ||||

| [60] | v | v | v | Integrated resource utilization | ||

| [61] | v | v | v | v | recover, redesign | |

| [62] | v | v | v | |||

| [63] | v | composting and landfill | ||||

| [64] | v | |||||

| [65] | v | |||||

| Propose | v | v | v | v | v | SBSC based on CE |

| BSC Perspectives | Strategic Goals | References |

|---|---|---|

| Financial perspective | The success of the company’s strategy implementation, measured from a financial point of view, is company profits. | [4,15,22,67,74,75,76] |

| Customer perspective | The successful implementation of the company’s strategy is measured from the customer’s point of view, namely in the form of customer satisfaction, customer retention, new customer acquisition, customer profitability, and market share in the target segment, which has a significant impact on strategic goals from a financial perspective. | [1,16,22,67] |

| Internal business process perspective | The successful implementation of the company’s strategy is measured from the point of view of internal business processes, namely in the form of innovation processes, operating processes, and after-sales services that have a significant impact on strategic goals from the customer perspective. | [15,22,67,72] |

| Learning and growth perspective | The success of the company’s strategy implementation, measured from the point of view of learning and growth, is in the form of increasing human capabilities, systems, and procedures of the company, which has a significant impact on strategic goals from the perspective of internal business processes. | [1,15,67,72] |

| Dimensions | Strategic Goals | References |

|---|---|---|

| Economy/ Profit | The company’s economic success for shareholders includes an increase in share value and profit. | [4,13,22,28] |

| Social/ People | The success of corporate social responsibility for the community includes a contribution to equal distribution of education, access to social resources, health and welfare, and improvement of quality of life. | [9,13,20,76] |

| Environment/ Planet | The success of the company’s environmental responsibility for the community includes environmental sustainability by monitoring air and water quality, energy consumption, natural resources, solid and toxic waste, and land use. | [13,20,22,68] |

| Author | Perspective/Dimension | |||||||

|---|---|---|---|---|---|---|---|---|

| BSC | TBL | Additional Perspective Contribution | ||||||

| Financial | Customer | Internal Business Process | Learning and Growth | Economy | Social | Environment | ||

| [4] | v | v | v | Corporate governance | ||||

| [5] | v | v | Innovation | |||||

| [7] | v | v | v | v | v | v | Non-Market | |

| [9] | v | v | v | v | v | Skill & capability | ||

| [12] | v | v | v | v | GRI indicators | |||

| [16] | v | v | v | v | v | v | v | Intellectual capital |

| [17] | v | v | v | Technology, politics. | ||||

| [18] | v | ISO 14001 | ||||||

| [19] | v | v | v | v | v | v | v | Technology |

| [20] | v | v | v | v | v | v | v | Lean manufacturing |

| [21] | v | v | v | Critical aspect | ||||

| [22] | v | v | v | Sustainability | ||||

| [23] | v | v | v | People, planet, and profit | ||||

| [24] | v | v | v | Supply chain dimension | ||||

| [25] | v | v | v | v | Bioenergy life cycle stage | |||

| [26] | v | v | v | v | Structure | |||

| [27] | v | v | Nature | |||||

| [28] | v | v | v | v | v | v | v | Agent of development |

| [29] | v | Financial inducement, stakeholder involvement, sustainable internal process | ||||||

| [30] | v | v | Profit and benefit social | |||||

| [76] | v | v | v | |||||

| [78] | v | v | ||||||

| [79] | v | v | v | v | v | v | v | |

| [80] | v | v | v | v | v | v | v | |

| [81] | v | v | v | v | v | v | v | |

| [82] | v | v | v | |||||

| [83] | v | v | v | v | v | v | ||

| [84] | v | v | v | |||||

| [85] | v | v | v | |||||

| [86] | v | v | v | |||||

| Propose | v | v | v | v | v | v | v | Circular Economy |

| Stakeholders | Stakeholder’s Value | References |

|---|---|---|

| Shareholders | Increase profits | [4,13,67,88,89,90,91] |

| Economic added value | [4] | |

| Customer | Customer value | [1,4,9,15,16,22,89,91] |

| Healthy and safe product quality | [22] | |

| Corporate image and reputation | [1,9,22] | |

| Continuous innovation | [1,3,15,76] | |

| Business partners | Profitable business contracts/enterprise alliances | [1,90] |

| Employee | Employee competence | [1,5,20,22,67,76,88,89,90,91] |

| Salary and benefit | [20] | |

| Community | Contribution to sustainability solutions (social and environmental) | [17,25,90] |

| Contribution to the circular economy | [19,54,56,57,92] |

| Strategic Goals | Question for Interview |

|---|---|

| Customer value improvement | How can product quality satisfy consumers? |

| Added value improvement | How does the company process waste products that generate added value? |

| Healthy and safe product | How do companies produce products that are healthy and safe for consumers? |

| Waste-based energy and raw material | How do companies use waste as an energy source? |

| How do companies use waste as raw material for other industries? | |

| Environmental sustainability | How does the company sustainably manage environmental sustainability? |

| Corporate green image | How to build an image that the company cares about the environment? |

| The environmentally friendly operation management process | How is operation process management carried out in an environmentally friendly manner? |

| Customer management process | How is the management of service to consumers? |

| Green product and waste treatment | How to carry out the innovation process to produce green products and waste treatment? |

| Value-added waste treatment recycle process | How to recycle waste treatment processes that provide added value? |

| Green human resources | How can a company have human resources who care and have competence for environmentally friendly production? |

| Strong alignment between an individual with corporate’s KPI | How do companies align KPIs on environmental management between companies and individuals? |

| Agile teamwork | How do companies build agile work teams? |

| Transformational leadership | What is the leader’s role in driving the achievement of individual and company targets? |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Trisyulianti, E.; Prihartono, B.; Andriani, M.; Suryadi, K. Sustainability Performance Management Framework for Circular Economy Implementation in State-Owned Plantation Enterprises. Sustainability 2022, 14, 482. https://doi.org/10.3390/su14010482

Trisyulianti E, Prihartono B, Andriani M, Suryadi K. Sustainability Performance Management Framework for Circular Economy Implementation in State-Owned Plantation Enterprises. Sustainability. 2022; 14(1):482. https://doi.org/10.3390/su14010482

Chicago/Turabian StyleTrisyulianti, Erlin, Budhi Prihartono, Made Andriani, and Kadarsah Suryadi. 2022. "Sustainability Performance Management Framework for Circular Economy Implementation in State-Owned Plantation Enterprises" Sustainability 14, no. 1: 482. https://doi.org/10.3390/su14010482