The Misunderstanding of China’s Investment, and a Clarification: “Faustian Bargain” or “Good Bargain”? On the OFDI Data of Central and Eastern Europe

and

and

Abstract

:1. Introduction: Good Bargain or Faustian Bargain?

2. Literature Review and Research Hypothesis

2.1. Economic Power from the Perspective of Realist Theory: The Source of China’s OFDI Power in CEE

2.2. The Logic of the Faustian Bargain: The Specific Mechanisms for China to Exert the Domination Effect of Economic Power

2.2.1. A Detrimental Race to the Bottom Produces the Shanghai Effect

2.2.2. Diffusion of Bad Governance—Diffusion of Corruption

3. Materials and Methods

3.1. Measurement of the Variables and Data Sources

3.2. Research Methods

3.2.1. Benchmark Model: Panel Model

3.2.2. Robustness Test: Regression Discontinuity Analysis of the Policy Shocks

4. Empirical Analysis: Results, Discussions and Limitations

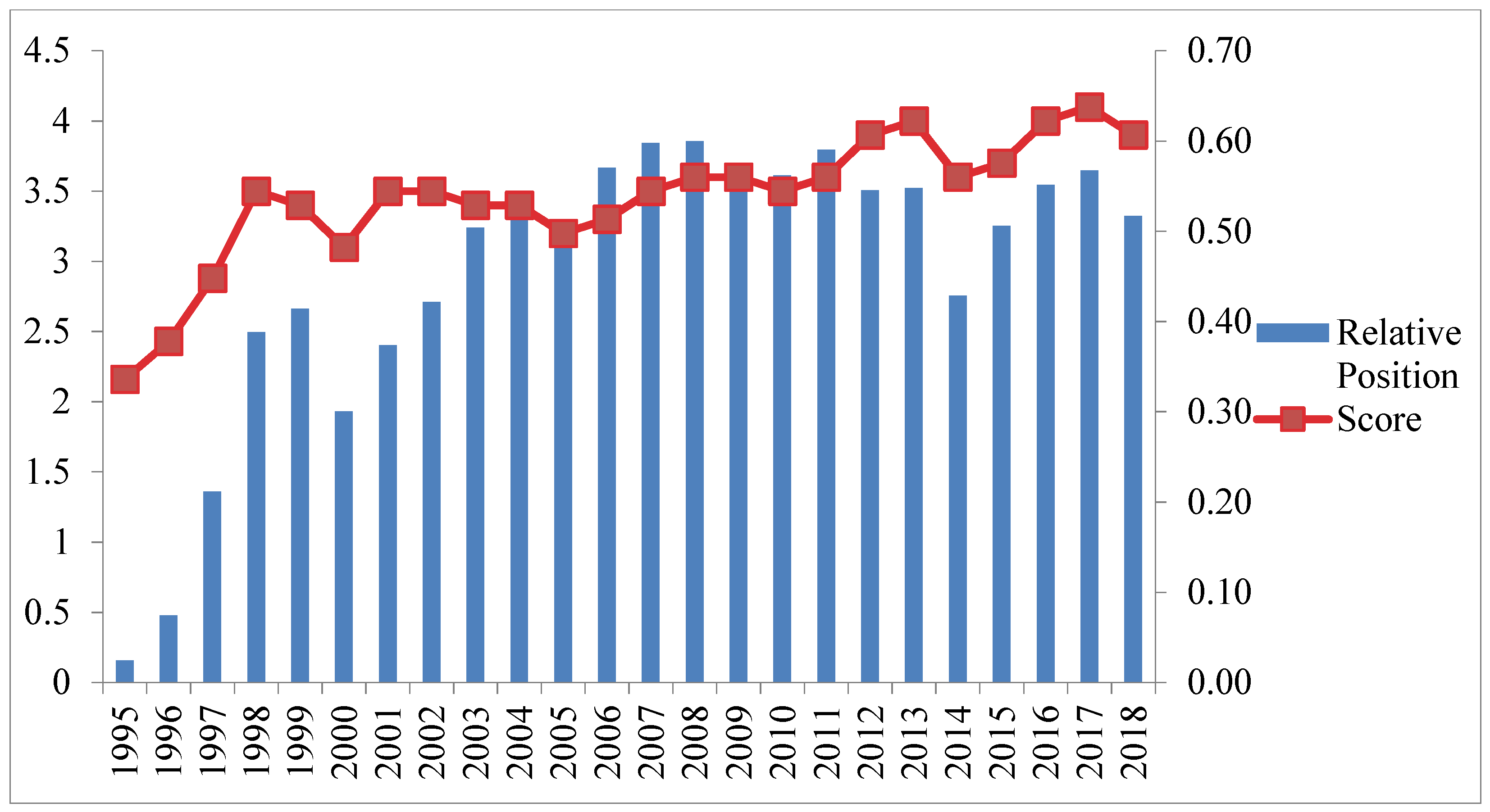

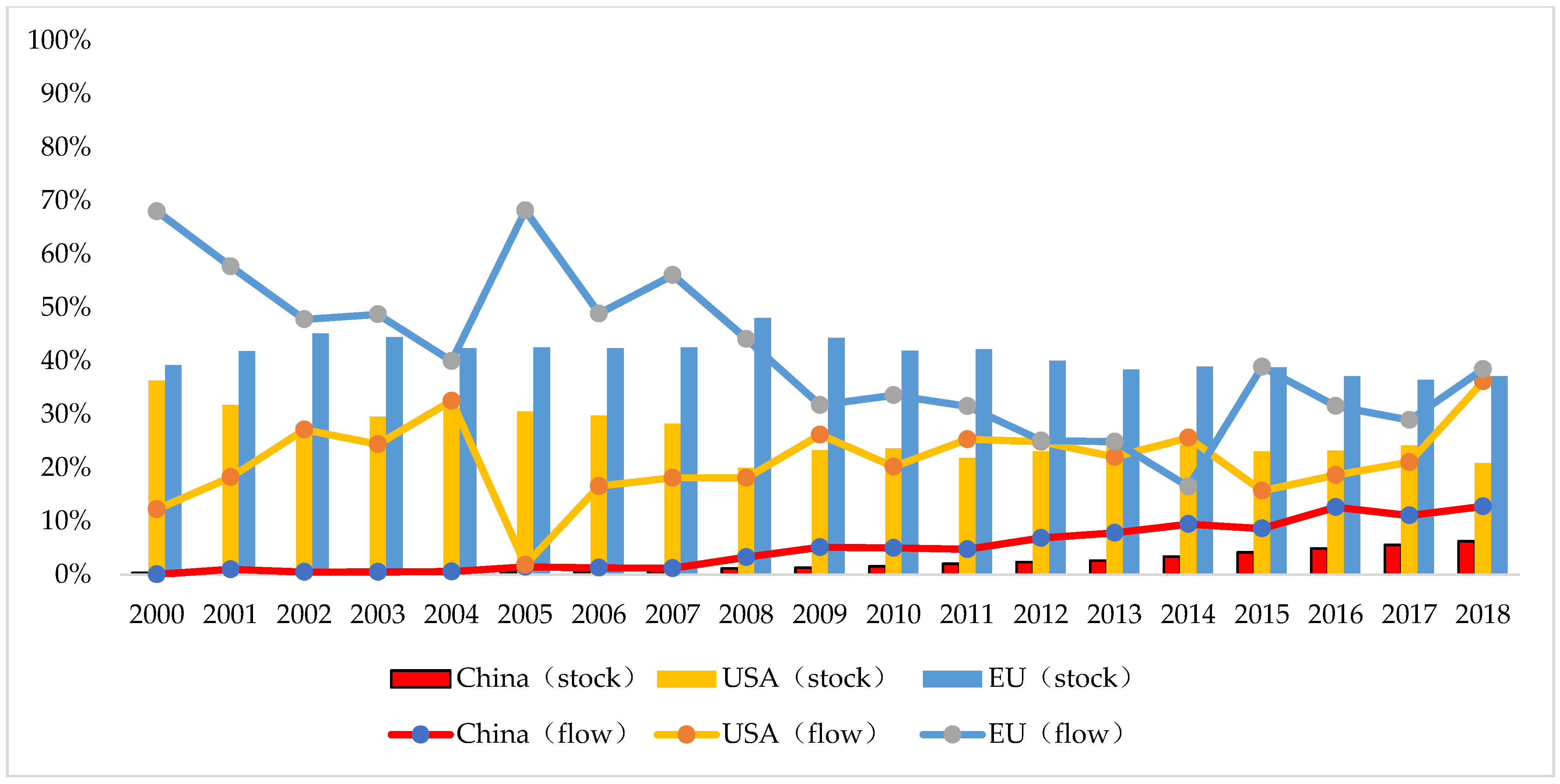

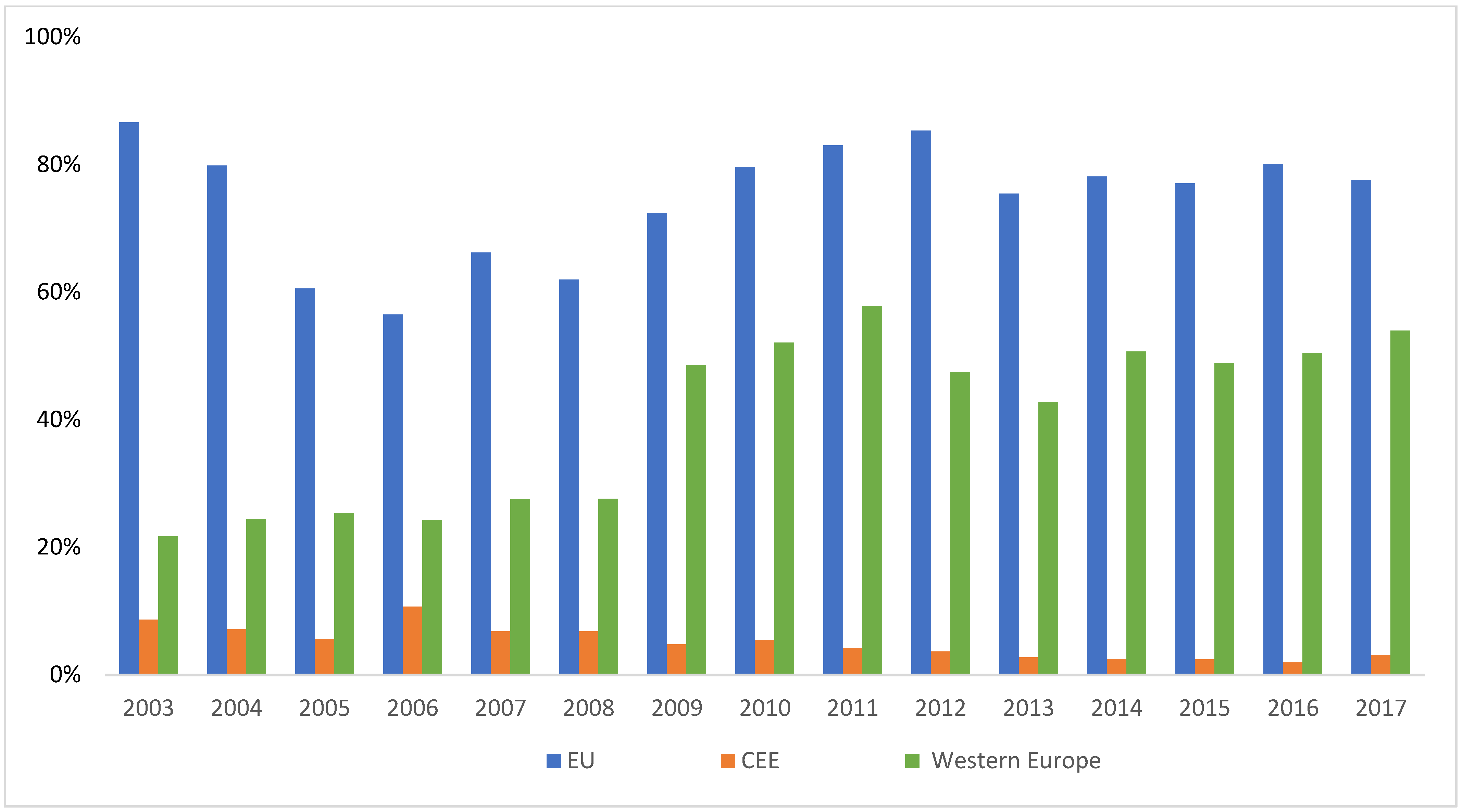

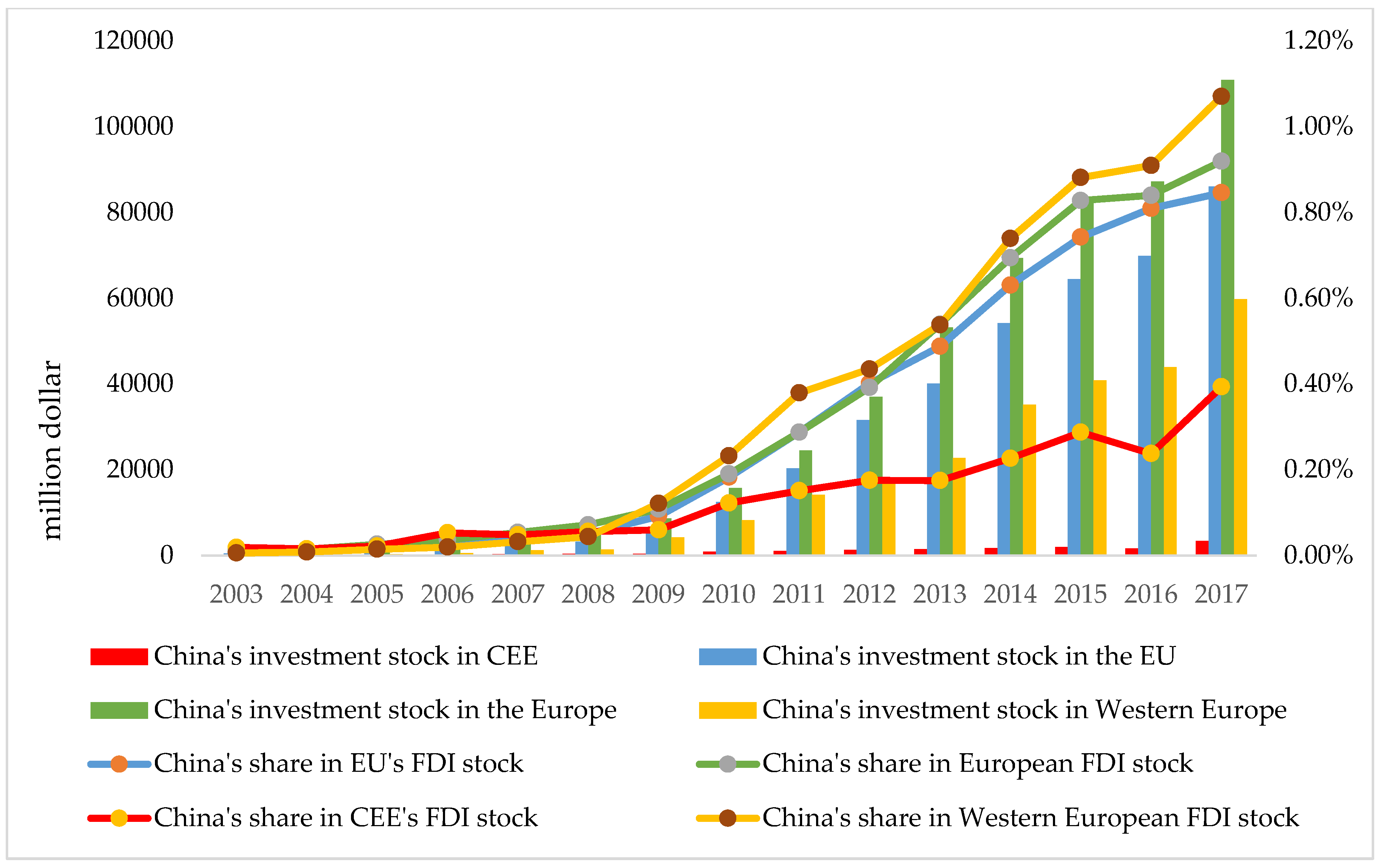

4.1. Descriptive Statistical Results: China’s Exagerrated Economic Power

4.2. Regression Model

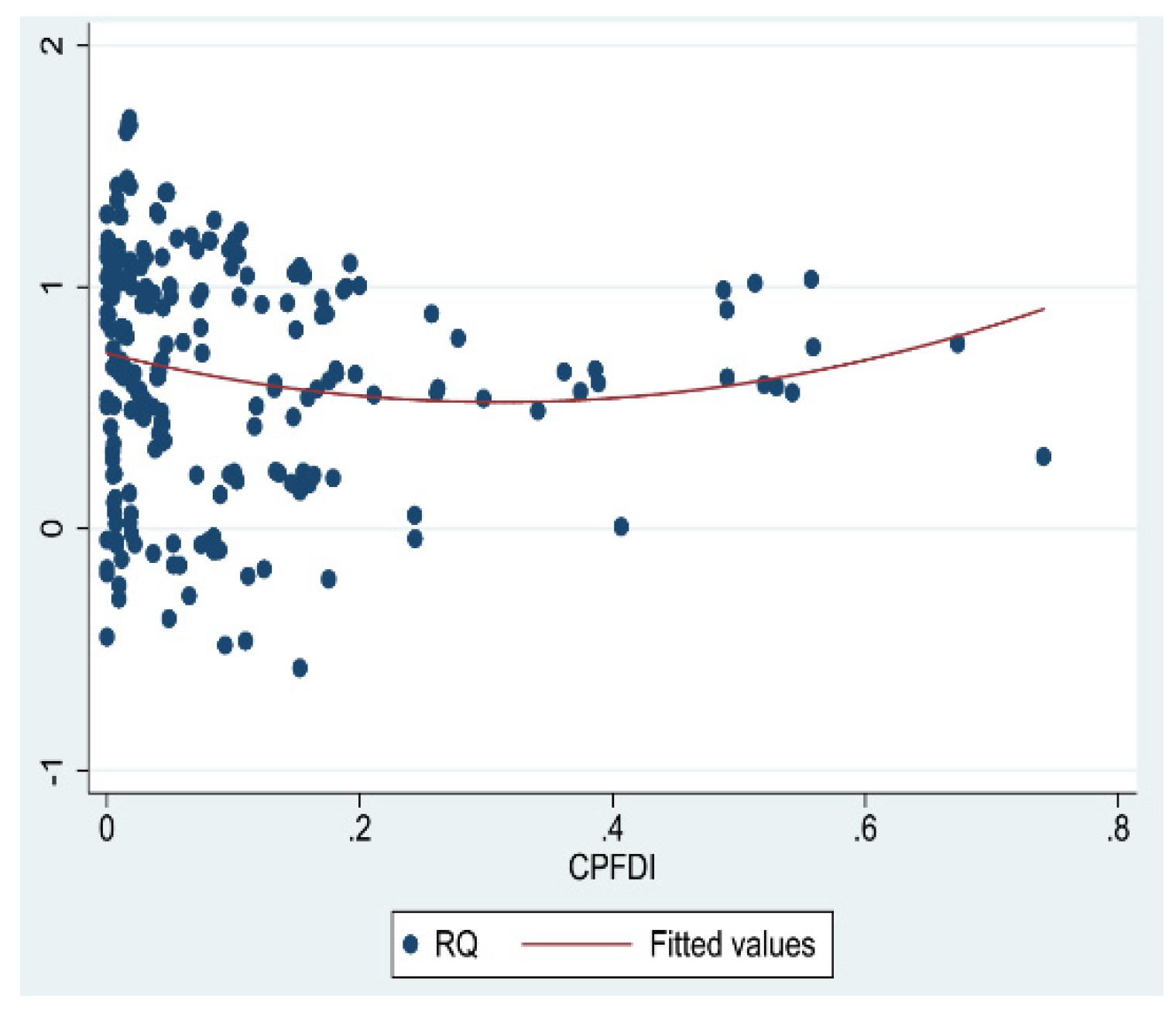

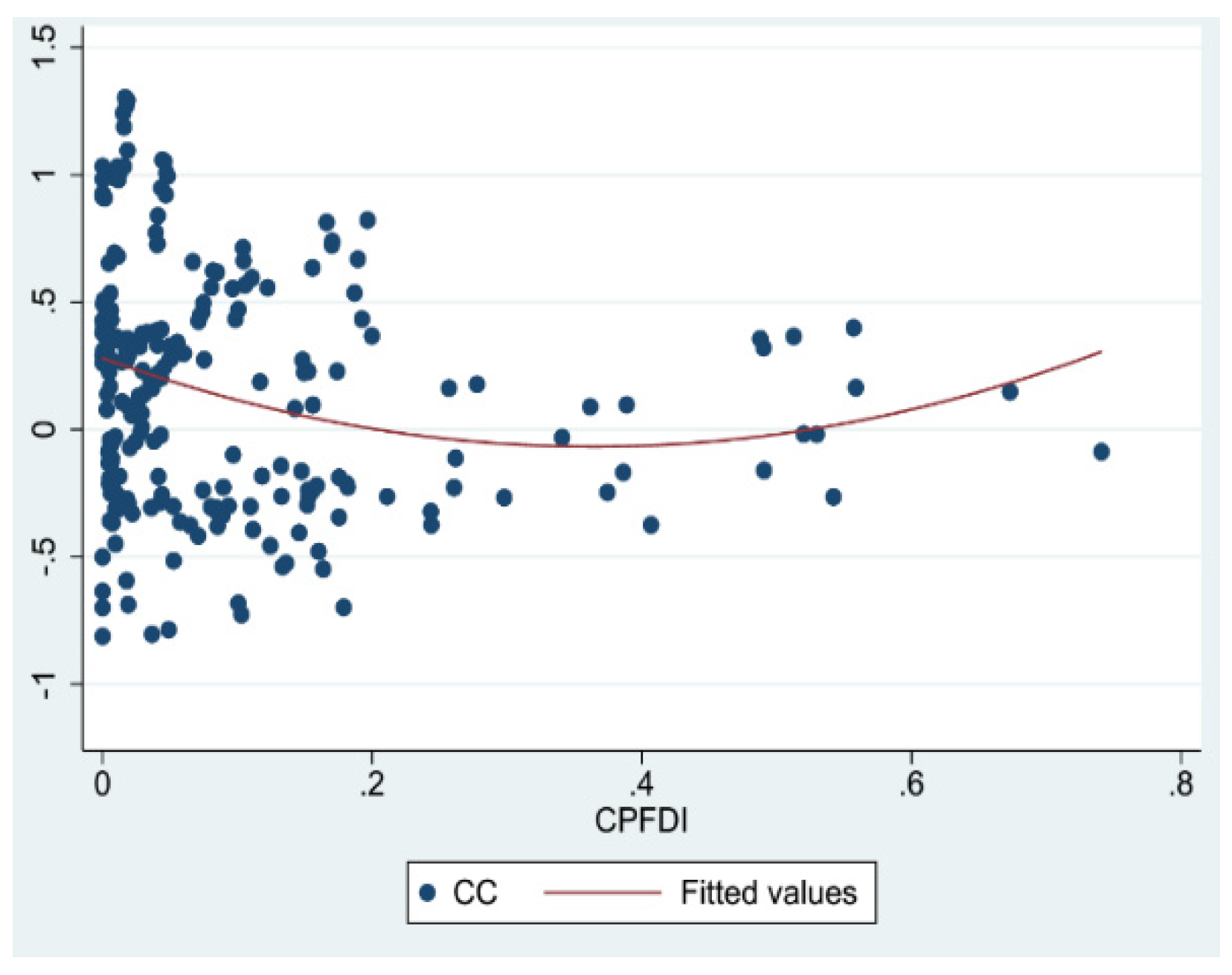

4.2.1. Benchmark Model: U-Shaped Effect

4.2.2. Robustness Test: Regression Discontinuity Model

5. Discussions and Conclusions

5.1. Discussion

5.2. Conclusions

5.3. Implication

5.4. Limits and Future Research

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Variable | Source | Reference |

|---|---|---|

| Regulatory Quality | The Worldwide Governance Indicators (WGI) of the World Bank | [72] |

| Control of Corruption | ||

| China OFDI Stock | China Foreign Direct Investment Statistics Bulletins, World Bank | [28] |

| Proportion of China OFDI Stock | ||

| Political Risk | Political Risk Services (PRS) Group | [95] |

| GDP per capita | The data bank of the World bank | [77] |

| Total Population | [78] | |

| Land Area | ||

| Urbanization | [26] | |

| Trade openness | [79,80] | |

| Education Levels | [96] |

Appendix B

| (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| Pool-RQ | Re-RQ | Fe-RQ | Pool-RQ | Re-RQ | Fe-RQ | |

| Ln (China’s OFDI stocks) squared | 0.003 | 0.000 | −0.000 | |||

| (0.003) | (0.002) | (0.002) | ||||

| Ln (China’s OFDI stocks) | −0.035 | −0.026 | −0.023 | |||

| (0.042) | (0.030) | (0.030) | ||||

| Share of China’s OFDI squared | 1.773 *** | 0.804 ** | 0.817 ** | |||

| (0.593) | (0.427) | (0.417) | ||||

| Share of Chinese investment | −0.910 *** | −0.778 *** | −0.638 *** | |||

| (0.328) | (0.238) | (0.232) | ||||

| Ln (GDP per capita) | 0.271 *** | 0.292 *** | 0.193 *** | 0.282 *** | 0.251 *** | 0.146 *** |

| (0.041) | (0.047) | (0.055) | (0.036) | (0.040) | (0.049) | |

| Ln (population) | −0.310 *** | −0.263 ** | −1.535 *** | −0.313 *** | −0.265 ** | −1.536 *** |

| (0.043) | (0.125) | (0.436) | (0.036) | (0.107) | (0.414) | |

| Ln (land area) | 0.369 *** | 0.373 ** | 4.763 | 0.374 *** | 0.326 ** | 2.624 |

| (0.048) | (0.160) | (3.606) | (0.045) | (0.139) | (3.462) | |

| Urbanization rate | 0.011 *** | 0.011 * | −0.004 | 0.012 *** | 0.015 *** | 0.005 |

| (0.002) | (0.006) | (0.008) | (0.002) | (0.005) | (0.007) | |

| Trade openness | −0.052 ** | −0.005 | 0.003 | −0.044 ** | −0.001 | 0.008 |

| (0.022) | (0.016) | (0.016) | (0.020) | (0.014) | (0.014) | |

| Education level | −0.127 | 0.341 *** | 0.518 *** | −0.217 * | 0.144 | 0.311 ** |

| (0.133) | (0.132) | (0.141) | (0.125) | (0.125) | (0.137) | |

| Political risk | 0.039 *** | 0.019 *** | 0.019 *** | 0.040 *** | 0.021 *** | 0.019 *** |

| (0.004) | (0.004) | (0.004) | (0.004) | (0.004) | (0.004) | |

| Constant term | −4.305 *** | −4.114 *** | −31.863 | −4.674 *** | −3.594 *** | −7.958 |

| (0.515) | (1.188) | (39.465) | (0.350) | (0.990) | (37.593) | |

| Obs. | 164 | 164 | 164 | 168 | 168 | 168 |

| R-squared | 0.844 *** | 0.768 *** | 0.393 *** | 0.852 *** | 0.796 *** | 0.406 *** |

Appendix C

| (7) | (8) | (9) | (10) | (11) | (12) | |

|---|---|---|---|---|---|---|

| Pool-RQ | Re-RQ | Fe-RQ | Pool-RQ | Re-RQ | Fe-RQ | |

| Ln (China’s OFDI stocks) squared | −0.004 | −0.011 *** | −0.012 *** | |||

| (0.004) | (0.003) | (0.004) | ||||

| Ln (China’s OFDI stocks) | 0.100 * | 0.180 *** | 0.187 *** | |||

| (0.060) | (0.055) | (0.057) | ||||

| Share of China’s OFDI squared | 2.537 *** | 0.736 * | 0.309 ** | |||

| (0.601) | (0.424) | (0.153) | ||||

| Share of Chinese investment | −1.441 *** | −0.431 ** | −0.435 ** | |||

| (0.344) | (0.242) | (0.221) | ||||

| Ln (GDP per capita) | 0.214 *** | 0.393 *** | 0.328 *** | 0.283 *** | 0.377 *** | 0.302 *** |

| (0.049) | (0.082) | (0.098) | (0.046) | (0.065) | (0.097) | |

| Ln(population) | −0.435 *** | −0.441 *** | −1.299 *** | −0.368 *** | −0.286 *** | −1.680 *** |

| (0.050) | (0.136) | (0.473) | (0.039) | (0.076) | (0.451) | |

| Ln (land area) | 0.443 *** | 0.564 *** | 3.127 | 0.420 *** | 0.371 *** | 4.714 |

| (0.051) | (0.176) | (3.242) | (0.048) | (0.099) | (3.129) | |

| Urbanization rate | 0.008 *** | −0.007 | −0.030 *** | 0.010 *** | 0.009 ** | −0.021 ** |

| (0.003) | (0.006) | (0.009) | (0.002) | (0.004) | (0.009) | |

| Trade openness | −0.032 | −0.011 | −0.006 | −0.036 | −0.013 | −0.004 |

| (0.024) | (0.015) | (0.015) | (0.023) | (0.016) | (0.015) | |

| Education level | −0.089 | 0.182 | 0.357 ** | −0.221 | 0.134 | 0.418 *** |

| (0.142) | (0.131) | (0.137) | (0.140) | (0.127) | (0.132) | |

| Political risk | 0.044 *** | 0.020 *** | 0.018 *** | 0.041 *** | 0.022 *** | 0.019 *** |

| (0.004) | (0.004) | (0.004) | (0.004) | (0.004) | (0.004) | |

| Constant term | −3.476 *** | −4.164 *** | −17.495 | −4.356 *** | −4.679 *** | −29.030 |

| (0.606) | (1.416) | (35.566) | (0.398) | (0.856) | (34.594) | |

| Obs. | 133 | 133 | 133 | 132 | 132 | 132 |

| R-squared | 0.865 *** | 0.696 *** | 0.418 *** | 0.867 *** | 0.824 *** | 0.402 *** |

Appendix D

| (13) | (14) | (15) | (16) | (17) | (18) | |

|---|---|---|---|---|---|---|

| Pool-CC | Re-CC | Fe-CC | Pool-CC | Re-CC | Fe-CC | |

| Ln (China’s OFDI stocks) squared | 0.002 | 0.001 | −0.000 | |||

| (0.004) | (0.002) | (0.002) | ||||

| Ln (China’s OFDI stocks) | −0.041 | −0.034 | −0.015 | |||

| (0.057) | (0.035) | (0.034) | ||||

| Share of China’s OFDI squared | 0.830 ** | 0.516 ** | 0.638 | |||

| (0.348) | (0.207) | (0.478) | ||||

| Share of Chinese investment | −0.568 *** | −0.316 ** | 0.036 | |||

| (0.219) | (0.159) | (0.166) | ||||

| Ln (GDP per capita) | 0.441 *** | 0.162 *** | −0.012 | 0.408 *** | 0.108 ** | −0.048 |

| (0.055) | (0.058) | (0.063) | (0.051) | (0.051) | (0.056) | |

| Ln(population) | −0.221 *** | −0.460 ** | −2.544 *** | −0.234 *** | −0.579 *** | −2.580 *** |

| (0.058) | (0.187) | (0.498) | (0.052) | (0.201) | (0.474) | |

| Ln (land area) | 0.245 *** | 0.453 * | 2.298 | 0.240 *** | 0.535 ** | 0.737 |

| (0.065) | (0.243) | (4.122) | (0.064) | (0.264) | (3.968) | |

| Urbanization rate | −0.002 | 0.001 | −0.011 | −0.002 | 0.004 | −0.003 |

| (0.003) | (0.007) | (0.009) | (0.003) | (0.007) | (0.008) | |

| Trade openness | −0.014 | 0.013 | 0.023 | −0.007 | 0.012 | 0.023 |

| (0.030) | (0.019) | (0.018) | (0.029) | (0.017) | (0.016) | |

| Education level | 0.553 *** | 0.247 | 0.366 ** | 0.536 *** | 0.023 | 0.147 |

| (0.181) | (0.160) | (0.161) | (0.178) | (0.156) | (0.157) | |

| Political risk | 0.031 *** | 0.019 *** | 0.019 *** | 0.034 *** | 0.020 *** | 0.019 *** |

| (0.005) | (0.005) | (0.005) | (0.005) | (0.004) | (0.005) | |

| Constant term | −5.479 *** | −0.589 | 13.341 | −5.193 *** | 0.540 | 31.246 |

| (0.702) | (1.745) | (45.106) | (0.500) | (1.828) | (43.083) | |

| Obs. | 164 | 164 | 164 | 168 | 168 | 168 |

| R-squared | 0.771 *** | 0.496 *** | 0.276 *** | 0.771 *** | 0.398 *** | 0.298 *** |

Appendix E

| (19) | (20) | (21) | (22) | (23) | (24) | |

|---|---|---|---|---|---|---|

| Pool-CC | Re-CC | Fe-CC | Pool-CC | Re-CC | Fe-CC | |

| Ln (China’s OFDI stocks) squared | −0.000 | −0.004 | −0.003 | |||

| (0.005) | (0.004) | (0.004) | ||||

| Ln (China’s OFDI stocks) | 0.044 | 0.075 | 0.029 | |||

| (0.080) | (0.066) | (0.065) | ||||

| Share of China’s OFDI squared | 0.254 *** | 0.523 ** | 0.259 | |||

| (0.095) | (0.261) | (0.289) | ||||

| Share of Chinese investment | −0.250 *** | −0.209 ** | −0.023 | |||

| (0.085) | (0.104) | (0.105) | ||||

| Ln (GDP per capita) | 0.537 *** | 0.435 *** | 0.186 | 0.578 *** | 0.397 *** | 0.167 |

| (0.065) | (0.101) | (0.112) | (0.064) | (0.105) | (0.111) | |

| Ln(population) | −0.330 *** | −0.487 *** | −2.970 *** | −0.246 *** | −0.577 *** | −3.051 *** |

| (0.066) | (0.170) | (0.541) | (0.055) | (0.201) | (0.519) | |

| Ln (land area) | 0.277 *** | 0.476 ** | −2.399 | 0.238 *** | 0.573 ** | −2.467 |

| (0.068) | (0.221) | (3.709) | (0.067) | (0.265) | (3.601) | |

| Urbanization rate | −0.005 | −0.004 | −0.010 | −0.003 | −0.000 | −0.005 |

| (0.003) | (0.008) | (0.010) | (0.003) | (0.009) | (0.010) | |

| Trade openness | 0.025 | 0.008 | 0.016 | 0.025 | 0.008 | 0.014 |

| (0.032) | (0.018) | (0.017) | (0.033) | (0.018) | (0.017) | |

| Education level | 0.728 *** | 0.167 | 0.222 | 0.729 *** | 0.171 | 0.158 |

| (0.190) | (0.158) | (0.157) | (0.197) | (0.155) | (0.152) | |

| Political risk | 0.022 *** | 0.013 *** | 0.008 * | 0.020 *** | 0.012 ** | 0.009 ** |

| (0.006) | (0.005) | (0.005) | (0.006) | (0.005) | (0.005) | |

| Constant term | −4.881 *** | −2.712 | 71.263 * | −5.840 *** | −1.921 | 73.163 * |

| (0.806) | (1.762) | (40.697) | (0.559) | (2.020) | (39.818) | |

| Obs. | 133 | 133 | 133 | 132 | 132 | 132 |

| R-squared | 0.811 *** | 0.698 *** | 0.327 *** | 0.803 *** | 0.598 *** | 0.346 *** |

References

- McCaleb, A.; Szunomár, Á. Chinese Foreign Direct Investment in Central and Eastern Europe: An Institutional Perspective. In Chinese Investment in Europe: Corporate Strategies and Labour Relations; Jan Drahokoupil, Ed.; European Trade Union Institute: Brussels, Belgium, 2017; pp. 121–140. [Google Scholar]

- Timsit, A. Chinese Investment in Europe Hit a 10-Year Low in 2020; Quartz: Minas Gerais, Brazil, 2021. [Google Scholar]

- Ames, E. Economic Policy in Eastern Europe from 1950 through 1956. Ann. Am. Acad. Pol. Soc. Sci. 1958, 317, 22–35. [Google Scholar] [CrossRef]

- Stanzel, A.; Kratz, A.; Szczudlik, J.; Pavlićević, D.; Doyon, J. China’s Investment in Influence: The Future of 16 + 1 Cooperation; European Council on Foreign Relations: London, UK, 2016. [Google Scholar]

- Pepe, J.M. China’s Inroads into Central, Estern, and South Eastern Europe: Regional and Global Implications for Germany and the EU; Social Science Open Access Repository: Berlin, Germany, 2017. [Google Scholar]

- Hanemann, T.; Rosen, D. China Invests in Europe; Rhodium Group: New York, NY, USA, 2012; pp. 1–96. [Google Scholar]

- Hanemann, T.; Huotari, M. Chinese FDI in Europe and Germany Preparing for a New Era of Chinese Capital Thilo Hanemann and Mikko Huotari; Mercator Institute for China Studies: Berlin, Germany, 2015. [Google Scholar]

- Malikane, C.; Chitambara, P. Foreign Direct Investment, Democracy and Economic Growth in Southern Africa. Afr. Dev. Rev. 2017, 29, 92–102. [Google Scholar] [CrossRef]

- Durham, J.B. Absorptive capacity and the effects of foreign direct investment and equity foreign portfolio investment on economic growth. Eur. Econ. Rev. 2004, 48, 285–306. [Google Scholar] [CrossRef]

- Zhang, K.H. How does foreign direct investment affect economic growth in China? Econ. Transit. 2001, 9, 679–693. [Google Scholar] [CrossRef]

- Forte, R.; Moura, R. The effects of foreign direct investment on the host country’s economic growth: Theory and empirical evidence. Singap. Econ. Rev. 2013, 58, 1350017. [Google Scholar] [CrossRef] [Green Version]

- Spisak, A. EU uneasy over China’s efforts to woo central and eastern European states. Financial Times, 8 May 2017. [Google Scholar]

- Lv, P.; Curran, L.; Spigarelli, F.; Barbieri, E. One country, many industries: Heterogeneity of Chinese OFDI motivations at meso level. China Econ. Rev. 2021, 69, 101672. [Google Scholar] [CrossRef]

- Hung, N.P. Development and Impact of Chinese Investment in EU. Creat. Knowl. Soc. 2016, 6, 1–14. [Google Scholar] [CrossRef] [Green Version]

- Tombeur, J. Chinese Outward Foreign Direct Investments in Europe: A Shift towards the European Periphery? Master’s Thesis, Ghent University, Ghent, Belgium, 2020. [Google Scholar]

- Meunier, S. A Tale of Two Ports: The Epic Story of Chinese Direct Investment in the Greek Port of Piraeus; Council for European Studies: New York, NY, USA, 2015; pp. 1–8. [Google Scholar]

- Götz, M. Pursuing FDI policy in the EU—Member States and their policy space. J. Econ. Polit. Econ. 2015, 2, 290–308. [Google Scholar]

- Xu, X. Chinese Investment in Central and Eastern European Countries—A Study of Motivations. Köz-Gazdaság 2019, 14, 68–76. [Google Scholar] [CrossRef]

- Garlick, J. China’s Economic Diplomacy in Central and Eastern Europe: A Case of Offensive Mercantilism? Eur. Asia Stud. 2019, 71, 1390–1414. [Google Scholar] [CrossRef]

- Meunier, S. A Faustian bargain or just a good bargain? Chinese foreign direct investment and politics in Europe. Asia Eur. J. 2014, 12, 143–158. [Google Scholar] [CrossRef]

- Turcsanyi, R.Q. Central European attitudes towards Chinese energy investments: The cases of Poland, Slovakia, and the Czech Republic. Energy Policy 2017, 101, 711–722. [Google Scholar] [CrossRef]

- Garcia-herrero, A.; Wolff, G.; Poitiers, N.; Felbermayr, G.; Langhammer, R.; Liu, W.-H.; Sandkamp, A. EU-China Trade and Investment Relations in Challenging Times, Study Requested by the INTA Committee; Social Science Research Network: Rochester, NY, USA, 2020. [Google Scholar]

- Dams, T.; Martin, X.; Kranenburg, V. China’s Soft Power in Europe Falling on Hard Times; Clingendael: Hague, The Netherland, 2021. [Google Scholar]

- European Commission. European Commission and HR/VP Contribution to the European Council: EU-China—A Strategic Outlook; European Commission: Brussels, Belgium, 2019. [Google Scholar]

- Kratz, A.; Oertel, J. Home Advantage: How China’s Protected Market Threatens Europe’s Economic Power; European Council on Foreign Relations: London, UK, 2021. [Google Scholar]

- VanHeuvelen, T. Recovering the missing middle: A mesocomparative analysis of within-group inequality, 1970–2011. Am. J. Sociol. 2018, 123, 1064–1116. [Google Scholar] [CrossRef]

- Isaksson, A.S.; Kotsadam, A. Racing to the bottom? Chinese development projects and trade union involvement in Africa. World Dev. 2018, 106, 284–298. [Google Scholar] [CrossRef]

- Kaczmarski, M.; Jakóbowski, J. Beijing’s Mistaken Offer: The ‘16 + 1’ and China’s Policy towards the European Union; Centre for Eastern Studies (OSW): Warszawa, Poland, 2017. [Google Scholar]

- Shambaugh, D. China’s Future, 1st ed.; Cambridge University Press: Cambridge, UK, 2016. [Google Scholar]

- Szunomar, A. Chinese Investment and Financial Engagement in Visegrad Countries Myth or Reality; Institute for World Economics-Centre for Economic and Regional Studies-Hungarian Academy of Sciences: Budapest, Hungary, 2014; ISBN 9789633016152. [Google Scholar]

- Jacoby, W. Different cases, different faces: Chinese investment in Central and Eastern Europe. Asia Eur. J. 2014, 12, 199–214. [Google Scholar] [CrossRef]

- Ramasamy, B.; Yeung, M. China’s outward foreign direct investment (OFDI) to developing countries: The case of Central and Eastern Europe (CEE). J. Asia Pac. Econ. 2020, 1–23. [Google Scholar] [CrossRef]

- Curran, L.; Lv, P.; Spigarelli, F. Chinese investment in the EU renewable energy sector: Motives, synergies and policy implications. Energy Policy 2017, 101, 670–682. [Google Scholar] [CrossRef]

- Godement, F.; Vasselier, A. China at the Gates: A New Power Audit of EU-China Relations; European Council on Foreign Relations: London, UK, 2017; ISBN 9781911544395. [Google Scholar]

- Barnett, M.N.; Finnemore, M. The politics, power, and pathologies of international organizations. Int. Organ. 1999, 53, 699–732. [Google Scholar] [CrossRef] [Green Version]

- Hasenclever, A.; Mayer, P.; Rittberger, V. Interests, power, knowledge: The study of international regimes. Mershon Int. Stud. Rev. 1996, 40, 177–228. [Google Scholar] [CrossRef]

- Keohane, R.O.; Nye, J.S. Reading 3.5 power and interdependence. In Conflict after the Cold War; Routledge: London, UK, 2017; pp. 167–174. [Google Scholar]

- Barnett, M.; Duvall, R. Power in International Politics; Cambridge University Press: Cambridge, UK, 2005; Volume 59, ISBN 0020818305050. [Google Scholar]

- Knorr, K. The Power of Nations: The Political Economy of International Relations. Polit. Sci. Q. 1975, 91, 569–571. [Google Scholar]

- Perroux, F. The domination effect and modern economic theory. Soc. Res. 1950, 17, 188–206. [Google Scholar]

- Richardson, N.R.; Kegley, C.W. Trade Dependence and Foreign Policy Compliance: A Longitudinal Analysis. Int. Stud. Q. 1980, 24, 191. [Google Scholar] [CrossRef]

- Papayoanou, P.A. Economic Interdependence and the Balance of Power. Int. Stud. Q. 1997, 41, 113–140. [Google Scholar] [CrossRef]

- Bandelj, N. Supraterritoriality, embeddedness, or both? Foreign direct investment in central and Eastern Europe. In Contemporary Studies in Economic and Financial Analysis; Emerald Group Publishing Limited: Bingley, UK, 2007. [Google Scholar]

- Kahler, M.; Kastner, S.L. Strategic uses of economic interdependence: Engagement policies on the Korean Peninsula and across the Taiwan strait. J. Peace Res. 2006, 43, 523–541. [Google Scholar] [CrossRef]

- Kowalski, B.; Nolan, P.; Gerrits, A. China’s foreign policy towards Central and Eastern Europe: The “16 + 1” format in the South–South cooperation perspective. Cases of the Czech Republic and Hungary. Camb. J. Eurasian Stud. 2017, 1, 1–16. [Google Scholar] [CrossRef]

- Yun, J.H.J.; Won, D.K.; Park, K.B. Entrepreneurial cyclical dynamics of open innovation. J. Evol. Econ. 2018, 28, 1151–1174. [Google Scholar] [CrossRef]

- Cooke, P. A ground-up “Quaternary” innovation strategy for South Korea using entrepreneurial ecosystem platforms. J. Open Innov. Technol. Mark. Complex. 2017, 3, 10. [Google Scholar] [CrossRef] [Green Version]

- Cooke, P. Three disruptive models of new spatial planning: “Attention”, “surveillance” or “sustainable” capitalisms? J. Open Innov. Technol. Mark. Complex. 2021, 7, 46. [Google Scholar] [CrossRef]

- Cooke, P. Silicon valley imperialists create new model villages as smart cities in their own image. J. Open Innov. Technol. Mark. Complex. 2020, 6, 24. [Google Scholar] [CrossRef] [Green Version]

- Cooke, P. World turned upside down: Entrepreneurial decline, its reluctant myths and troubling realities. J. Open Innov. Technol. Mark. Complex. 2019, 5, 22. [Google Scholar] [CrossRef] [Green Version]

- Yun, J.H.J. How do we conquer the growth limits of capitalism? Schumpeterian Dynamics of Open Innovation. J. Open Innov. Technol. Mark. Complex. 2015, 1, 1–20. [Google Scholar] [CrossRef] [Green Version]

- Adolph, C.; Quince, V.; Prakash, A. The Shanghai Effect: Do Exports to China Affect Labor Practices in Africa? World Dev. 2017, 89, 1–18. [Google Scholar] [CrossRef]

- Duttaray, M.; Dutt, A.K.; Mukhopadhyay, K. Foreign direct investment and economic growth in less developed countries: An empirical study of causality and mechanisms. Appl. Econ. 2008, 40, 1927–1939. [Google Scholar] [CrossRef]

- Vissak, T.; Roolaht, T. The Negative Impact of Foreign Direct Investment on the Estonian Economy. Probl. Econ. Transit. 2005, 48, 43–66. [Google Scholar]

- Hong, L. Does and How does FDI Promote the Economic Growth? Evidence from Dynamic Panel Data of Prefecture City in China. IERI Procedia 2014, 6, 57–62. [Google Scholar] [CrossRef] [Green Version]

- Barisitz, S.; Radzyner, A. The New Silk Road, part II: Implications for Europe. Focus Eur. Econ. Integr. Oesterreichische Natl. (Austrian Cent. Bank) 2017, 4, 70–81. [Google Scholar]

- Isaksson, A.S.; Kotsadam, A. Chinese aid and local corruption. J. Public Econ. 2018, 159, 146–159. [Google Scholar] [CrossRef]

- Davis, C.L.; Fuchs, A.; Johnson, K. State Control and the Effects of Foreign Relations on Bilateral Trade. J. Confl. Resolut. 2019, 63, 405–438. [Google Scholar] [CrossRef]

- Khan, M.A.; Khan, M.A.; Ali, K.; Popp, J.; Oláh, J. Natural resource rent and finance: The moderation role of institutions. Sustainability 2020, 12, 3897. [Google Scholar] [CrossRef]

- Bräutigam, D.; Xiaoyang, T. Economic statecraft in China’s new overseas special economic zones: Soft power, business or resource security? Int. Aff. 2012, 88, 799–816. [Google Scholar] [CrossRef] [Green Version]

- Pavlićević, D. ‘China threat’ and ‘China opportunity’: Politics of dreams and fears in China-Central and Eastern European relations. J. Contemp. China 2018, 27, 688–702. [Google Scholar] [CrossRef]

- Sen, A. Quality of life: India vs. China. In The New York Review of Books; Pratichi Trust: Kolkata, India, 2011; pp. 5–13. [Google Scholar]

- Nyíri, P. Chinese entrepreneurs in poor countries: A transnational “middleman minority” and its futures. Inter-Asia Cult. Stud. 2011, 12, 145–153. [Google Scholar] [CrossRef]

- Hao, J.; Li, C.; Yuan, R.; Ahmed, M.; Khan, M.A.; Oláh, J. The influence of the knowledge-based network structure hole on enterprise innovation performance: The threshold effect of R&D investment intensity. Sustainability 2020, 12, 6155. [Google Scholar] [CrossRef]

- Hauk, E.; Saez-Marti, M. On the cultural transmission of corruption. J. Econ. Theory 2002, 107, 311–335. [Google Scholar] [CrossRef] [Green Version]

- Zhou, X.; Liu, Y.; Ho, B. The cultural transmission of cooperative norms. Front. Psychol. 2015, 6, 1–10. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Bräutigam, D.A.; Knack, S. Foreign aid, institutions, and governance in sub-Saharan Africa. Econ. Dev. Cult. Chang. 2004, 52, 255–285. [Google Scholar] [CrossRef] [Green Version]

- Qamruzzaman, M.; Tayachi, T.; Mehta, A.M.; Ali, M. Do international capital flows, institutional quality matter for innovation output: The mediating role of economic policy uncertainty. J. Open Innov. Technol. Mark. Complex. 2021, 7, 141. [Google Scholar] [CrossRef]

- Parfenov, A.; Shamina, L.; Niu, J.; Yadykin, V. Transformation of distribution logistics management in the digitalization of the economy. J. Open Innov. Technol. Mark. Complex. 2021, 7, 58. [Google Scholar] [CrossRef]

- Chen, J.; Han, L.; Qu, G. Citizen innovation: Exploring the responsibility governance and cooperative mode of a “post-schumpeter” paradigm. J. Open Innov. Technol. Mark. Complex. 2020, 6, 172. [Google Scholar] [CrossRef]

- Ngo, Q.T.; Doan, N.P.; Thi Tran, T.H.; Nguyen, T.D. Technology adoption strategies in the supply chain: The case of vietnamese young small and medium-sized enterprises. J. Open Innov. Technol. Mark. Complex. 2020, 6, 37. [Google Scholar] [CrossRef]

- Liu, K.; Zhang, W. Is there an institutional preference for China’s OFDI?––A perspective of heterogeneous investment motivation. Macroecon. Res. 2018, 7. [Google Scholar] [CrossRef]

- Alfaro, L. Foreign Direct Investment and Growth: Does the Sector Matter? Harvard Business School: Harvard, MA, USA, 2017; Volume 53. [Google Scholar]

- Borensztein, E.; De Gregorio, J.; Lee, J.-W. How does foreign direct investment affect economic growth? J. Int. Econ. 1998, 45, 115–135. [Google Scholar] [CrossRef] [Green Version]

- Alfaro, L.; Johnson, M.S. Foreign Direct Investment and Growth. Evid. Impact Financ. Glob. 2013, 106, 299–309. [Google Scholar] [CrossRef]

- Jiang, G.H.; Jiang, D.C. Is the host country system important for China’s investment in developing countries? Manag. World 2012, 11, 45–46. [Google Scholar] [CrossRef]

- La Porta, R.; Lopez-de-Silanes, F.; Shleifer, A.; Vishny, R. The quality of government. J. Law Econ. Organ. 1999, 15, 222–279. [Google Scholar] [CrossRef]

- Gemmell, N. Economic Development and Structural Change: The Role of the Service Sector. J. Dev. Stud. 1982, 19, 37–66. [Google Scholar] [CrossRef]

- Mudiyanselage, M.M.R.; Epuran, G.; Tescasiu, B. Causal Links between Trade Openness and Foreign Direct Investment in Romania. J. Risk Financ. Manag. 2021, 14, 1–18. [Google Scholar]

- Liargovas, P.G.; Skandalis, K.S. Foreign Direct Investment and Trade Openness: The Case of Developing Economies. Soc. Indic. Res. 2012, 106, 323–331. [Google Scholar] [CrossRef]

- Al-Marhubi, F. The determinants of governance: A cross-country analysis. Contemp. Econ. Policy 2004, 22, 394–406. [Google Scholar] [CrossRef]

- Gelman, A. A statistician’s perspective on “mostly harmless econometrics: An empiricist’s companion”, by Joshua D. Angrist and Jorn-Steffen Pischke. Stata J. 2009, 9, 315–320. [Google Scholar] [CrossRef]

- Turcsányi, R. Central and Eastern Europe’s Courtship with China: Trojan horse within the EU? EU-Asia Glance 2014, 32, 21–22. [Google Scholar]

- Matura, T. China–CEE Trade, Investment and Politics. Eur. Asia Stud. 2019, 71, 388–407. [Google Scholar] [CrossRef]

- Clark, T.S.; Linzer, D.A. Should I Use Fixed or Random Effects? Polit. Sci. Res. Methods 2015, 3, 399–408. [Google Scholar] [CrossRef] [Green Version]

- Shen, L.; Koveos, P.; Zhu, X.; Wen, F.; Liao, J. Outward FDI and Entrepreneurship: The Case of China. Sustainability 2020, 12, 5234. [Google Scholar] [CrossRef]

- Te Velde, D.W.; United Nations Conference on Trade and Development. Foreign Direct Investment and Development an Historical Perspective; Overseas Development Institute: London, UK, 2006. [Google Scholar]

- Hasan, M.M.; Yajuan, L.; Khan, S. Promoting China’s Inclusive Finance Through Digital Financial Services. Glob. Bus. Rev. 2020, 1–23. [Google Scholar] [CrossRef]

- Hasan, M.M.; Popp, J.; Oláh, J. Current landscape and influence of big data on finance. J. Big Data 2020, 7, 21. [Google Scholar] [CrossRef]

- Gao, J.; Wang, H.; Shen, H. Task failure prediction in cloud data centers using deep learning. IEEE Trans. Serv. Comput. 2020. [Google Scholar] [CrossRef]

- Gao, J.; Wang, H.; Shen, H. Machine learning based workload prediction in cloud computing. In Proceedings of the 2020 29th International Conference on Computer Communications and Networks (ICCCN), Honolulu, HI, USA, 3–6 August 2020; pp. 1–9. [Google Scholar]

- Moran, T.H.; Oldenski, L. Foreign Direct Investment in the United States: Benefits, Suspicions, and Risks with Special Attention to FDI from China; Peterson Institute for International Economics: Washington, DC, USA, 2013. [Google Scholar]

- Burgoon, B.; Raess, D. Chinese investment and European labor: Should and do workers fear Chinese FDI? Asia Eur. J. 2014, 12, 179–197. [Google Scholar] [CrossRef]

- Wagner, R.H. Economic interdependence, bargaining power, and political influence. Int. Organ. 1988, 42, 461–483. [Google Scholar] [CrossRef]

- Lacroix, J.; Méon, P.G.; Sekkat, K. Democratic transitions can attract foreign direct investment: Effect, trajectories, and the role of political risk. J. Comp. Econ. 2021, 49, 340–357. [Google Scholar] [CrossRef]

- Hakhverdian, A.; Mayne, Q. Institutional trust, education, and corruption: A micro-macro interactive approach. J. Polit. 2012, 74, 739–750. [Google Scholar] [CrossRef] [Green Version]

| Variables | (1) | (2) | (3) | (4) | (5) | (6) |

|---|---|---|---|---|---|---|

| Pool-RQ | Re-RQ | Fe-RQ | Pool-RQ | Re-RQ | Fe-RQ | |

| Ln (China’s OFDI stocks) squared | 0.002 | 0.001 | 0.001 | |||

| (0.003) | (0.002) | (0.002) | ||||

| Ln (China’s OFDI stocks) | −0.061 | −0.040 | 0.008 | |||

| (0.042) | (0.029) | (0.029) | ||||

| Share of China’s OFDI squared | 0.497 ** | 0.846 ** | 0.841 ** | |||

| (0.193) | (0.407) | (0.412) | ||||

| Share of Chinese investment | −0.722 ** | −0.732 *** | −0.710 *** | |||

| (0.320) | (0.251) | (0.245) | ||||

| Ln (GDP per capita) | 0.503 *** | 0.291 *** | 0.196 *** | 0.290 *** | 0.252 *** | 0.159 *** |

| (0.038) | (0.042) | (0.050) | (0.032) | (0.036) | (0.044) | |

| Ln(population) | −0.286 *** | −0.251 ** | −1.529 *** | −0.143 *** | −0.147 | −0.478 |

| (0.041) | (0.121) | (0.434) | (0.045) | (0.122) | (0.466) | |

| Ln (land area) | 0.343 *** | 0.358 ** | −5.508 | 0.350 *** | 0.292 ** | 1.863 |

| (0.047) | (0.156) | (3.671) | (0.044) | (0.139) | (3.592) | |

| Urbanization rate | 0.012 *** | 0.011 ** | −0.005 | 0.014 *** | 0.019 *** | 0.012 * |

| (0.002) | (0.005) | (0.008) | (0.002) | (0.005) | (0.007) | |

| Trade openness | −0.046 ** | −0.022 | −0.017 | −0.030 | −0.010 | −0.005 |

| (0.021) | (0.015) | (0.015) | (0.019) | (0.013) | (0.012) | |

| Education level | −0.135 | 0.347 ** | 0.520 *** | −0.215 | 0.116 | 0.275 |

| (0.131) | (0.134) | (0.143) | (0.152) | (0.127) | (0.141) | |

| Political risk | 0.038 *** | 0.022 *** | 0.020 *** | 0.039 *** | 0.022 *** | 0.020 *** |

| (0.004) | (0.004) | (0.004) | (0.003) | (0.004) | (0.004) | |

| Constant term | −4.42 *** | −4.193 *** | −38.005 | −4.808 *** | −3.805 *** | −4.949 ** |

| (0.498) | (1.148) | (40.285) | (0.335) | (0.972) | (2.139) | |

| N | 185 | 185 | 185 | 196 | 196 | 196 |

| R−squared | 0.835 *** | 0.77 *** | 0.413 *** | 0.845 *** | 0.803 *** | 0.332 *** |

| Variables | (7) | (8) | (9) | (10) | (11) | (12) |

|---|---|---|---|---|---|---|

| Pool-CC | Re-CC | Fe-CC | Pool-CC | Re-CC | Fe-CC | |

| Ln (China’s OFDI stocks) squared | 0.002 | −0.002 | −0.003 | |||

| (0.004) | (0.002) | (0.002) | ||||

| Ln (China’s OFDI stocks) | −0.103 ** | −0.034 | 0.021 | |||

| (0.052) | (0.033) | (0.032) | ||||

| Share of China’s OFDI squared | 0.612 *** | 0.502 ** | 0.603 | |||

| (0.836) | (0.205) | (0.465) | ||||

| Share of Chinese investment | −0.945 *** | −0.650 ** | −0.418 | |||

| (0.358) | (0.272) | (0.363) | ||||

| Ln (GDP per capita) | 0.510 *** | 0.142 *** | −0.015 | 0.362 *** | 0.109 ** | 0.027 |

| (0.052) | (0.050) | (0.055) | (0.046) | (0.043) | (0.047) | |

| Ln(population) | −0.196 *** | −0.49 ** | −1.895 *** | −0.235 *** | −0.536 *** | −2.403 *** |

| (0.056) | (0.189) | (0.478) | (0.051) | (0.186) | (0.443) | |

| Ln (land area) | 0.236 *** | 0.489 ** | 2.919 | 0.241 | 0.486 ** | 1.279 |

| (0.064) | (0.246) | (4.042) | (0.063) | (0.244) | (3.907) | |

| Urbanization rate | −0.006 | 0.000 | −0.014 | 0.002 | 0.006 | −0.005 |

| (0.003) | (0.007) | (0.008) | (0.003) | (0.007) | (0.008) | |

| Trade openness | −0.012 | 0.013 | 0.022 | −0.003 | 0.002 | 0.004 |

| (0.029) | (0.017) | (0.016) | (0.027) | (0.015) | (0.015) | |

| Education level | 0.525 *** | 0.243 | 0.387 ** | 0.491 ** | 0.078 | 0.137 |

| (0.180) | (0.157) | (0.158) | (0.172) | (0.151) | (0.154) | |

| Political risk | 0.034 *** | 0.019 *** | 0.020 *** | 0.038 *** | 0.020 *** | 0.019 *** |

| (0.005) | (0.004) | (0.005) | (0.005) | (0.004) | (0.004) | |

| Constant term | −5.672 *** | −1.411 | 6.770 | −5.078 *** | −0.267 | 22.179 |

| (0.687) | (1.265) | (7.666) | (0.479) | (1.672) | (42.345) | |

| N | 185 | 185 | 185 | 194 | 194 | 194 |

| R−squared | 0.748 *** | 0.449 *** | 0.296 *** | 0.753 *** | 0.418 *** | 0.302 *** |

| LATE Coefficient | RD-RQ (13) | RD-RQ (14) | RD-CC (15) | RD-CC (16) | RD-CS (17) | RD-CS (18) | RD-CP (19) | RD-CP (20) |

|---|---|---|---|---|---|---|---|---|

| Algorithm 1: conventional | 0.009 | 0.090 | −0.030 | 0.002 | 0.014 | −0.143 | −0.001 | −0.005 |

| (0.975) | (0.491) | (0.869) | (0.986) | (0.99) | (0.785) | (0.926) | (0.689) | |

| Algorithm 2: bias−corrected | 0.035 | 0.145 | 0.005 | 0.138 | 0.154 | −0.047 | 0.01 | 0.002 |

| (0.898) | (0.271) | (0.976) | (0.143) | (0.885) | (0.929) | (0.510) | (0.896) | |

| Algorithm 3: Robust | 0.035 | 0.145 | 0.005 | 0.138 | 0.154 | −0.047 | 0.010 | 0.002 |

| (0.917) | (0.375) | (0.987) | (0.437) | (0.917) | (0.971) | (0.695) | (0.937) | |

| Control variables | NO | YES | NO | YES | NO | YES | NO | YES |

| Polynomial order (K) | 4 | 4 | 4 | 4 | 4 | 4 | 4 | 4 |

| N | 268 | 234 | 272 | 237 | 220 | 187 | 228 | 195 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Duan, C.; Zhou, Y.; Shen, D.; Lin, S.; Gong, W.; Popp, J.; Oláh, J. The Misunderstanding of China’s Investment, and a Clarification: “Faustian Bargain” or “Good Bargain”? On the OFDI Data of Central and Eastern Europe. Sustainability 2021, 13, 10281. https://doi.org/10.3390/su131810281

Duan C, Zhou Y, Shen D, Lin S, Gong W, Popp J, Oláh J. The Misunderstanding of China’s Investment, and a Clarification: “Faustian Bargain” or “Good Bargain”? On the OFDI Data of Central and Eastern Europe. Sustainability. 2021; 13(18):10281. https://doi.org/10.3390/su131810281

Chicago/Turabian StyleDuan, Cheche, Yicheng Zhou, Dehong Shen, Shengqiao Lin, Wei Gong, József Popp, and Judit Oláh. 2021. "The Misunderstanding of China’s Investment, and a Clarification: “Faustian Bargain” or “Good Bargain”? On the OFDI Data of Central and Eastern Europe" Sustainability 13, no. 18: 10281. https://doi.org/10.3390/su131810281