Research into the Mechanism for the Impact of Climate Change on Systemic Risk—A Case Study of China’s Small- and Medium-sized Commercial Banks

Abstract

:1. Introduction

2. Analysis of the Mechanism for the Effect of Climate Change on Changes in Financial Risks

2.1. Direct Impact of Climate Change on Changes in Financial Risks

2.2. Indirect Impact of Climate Change on Changes in Financial Risks

3. Measurement of Systemic Financial Risks and Climate Change

3.1. Measurement of Systemic Financial Risks Based on the Dynamic CoVaR Model

3.1.1. Introduction to Model

3.1.2. Data Selection and Processing

3.1.3. Status Variables

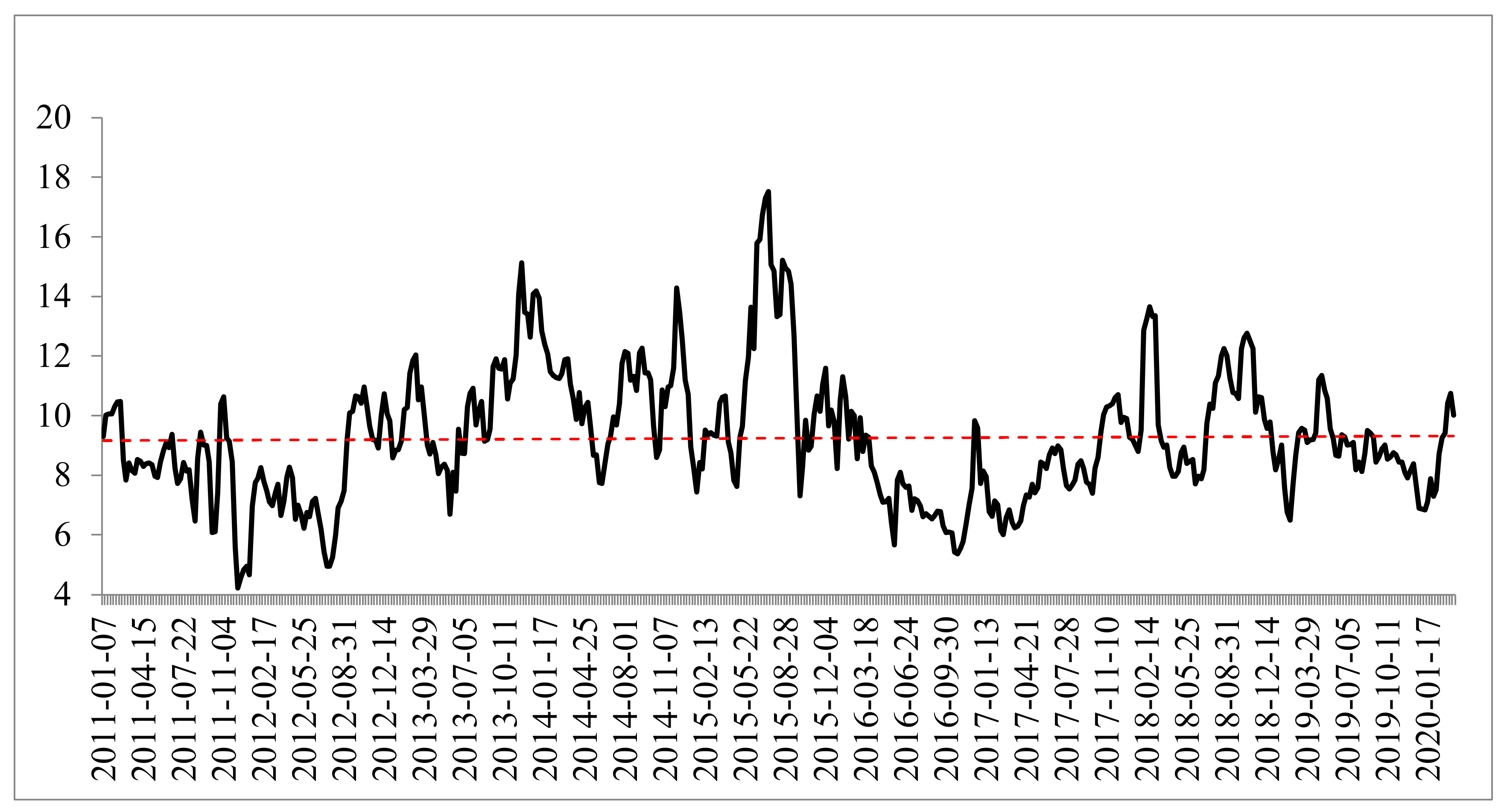

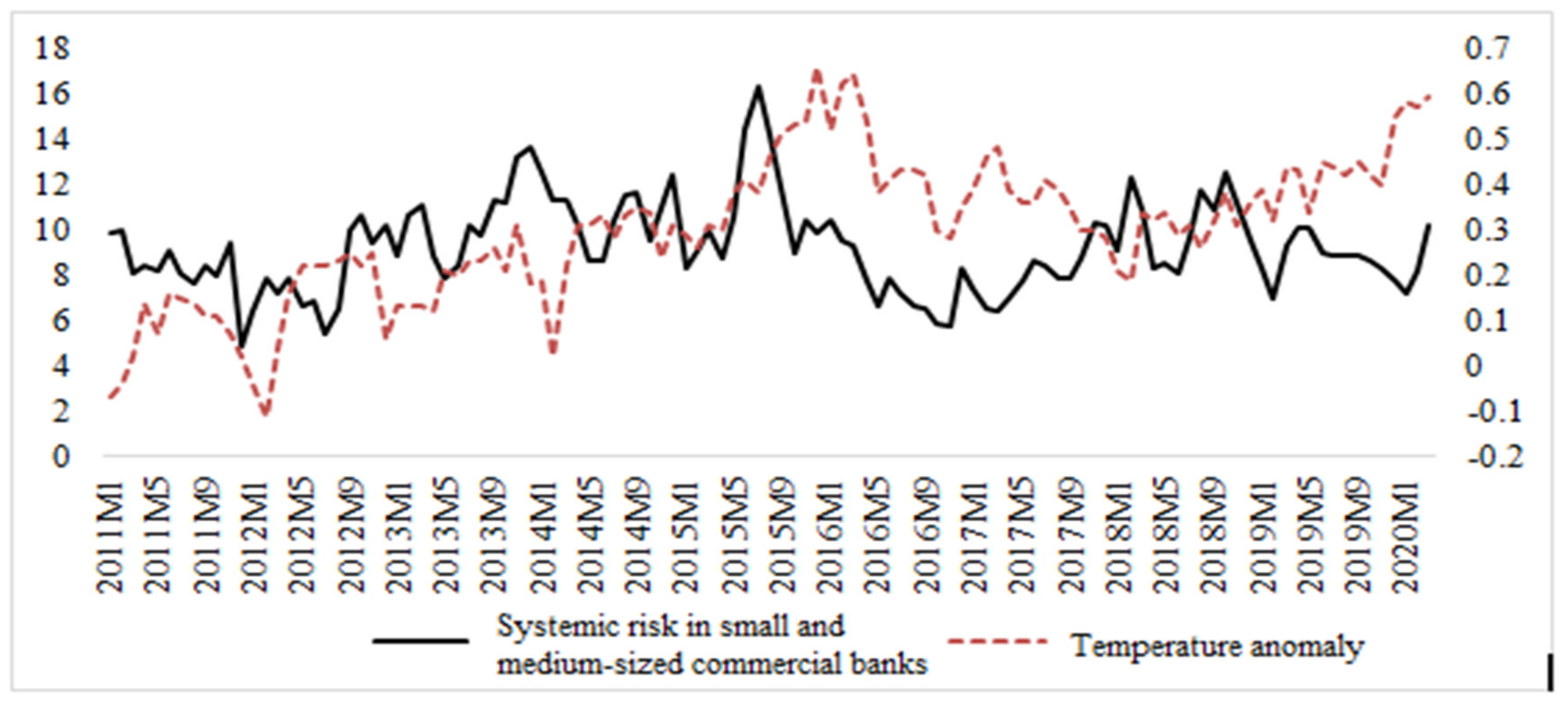

3.1.4. Empirical Results

3.2. Measurement of Risk caused by Climate Change

3.2.1. Selection of Indicators

3.2.2. Data Processing and Analysis

4. Assessment of the Impact of Climate Risk on Systemic Risk in Commercial Banks

4.1. Regression Model Based on the Single-Factor Impact of Climate

4.1.1. Creation of Inter-Series Cointegration

4.1.2. Error Correction Model

4.2. Building a Regression Model of Multiple-Factor Impact

4.2.1. Research Hypothesis

4.2.2. Model Building

4.2.3. Empirical Research and Result Analysis

5. Discussion

5.1. The Main Innovation of This Study

5.2. Countermeasure Suggestions for Banks and Government

6. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Battiston, S.; Mandel, A.; Monasterolo, I.; Schütze, F.; Visentin, G. A climate stress-test of the financial system. Nat. Clim. Chang. 2017, 7, 283–288. [Google Scholar] [CrossRef]

- Huntington, E.; Visher, S.S. Climatic Change: Their Nature and Causes; Yale University Press: New Haven, CO, USA, 1922; p. 2. Available online: https://www.questia.com/library/94928129/climatic-changes-their-nature-and-causes (accessed on 17 November 2020).

- Giusy, C.; Gianfranco, G.; Marco, S. Climate change and credit risk. J. Clean. Prod. 2020, 266, 1–10. [Google Scholar]

- Agassiz, L. Tudes Sur Les Glaciers; Privately Published; Neuch Tel: Paris, France, 1840. [Google Scholar]

- Hay, W.W.; Robert, M.D.; Christopher, N.W. The Late Cenozoic up lift climate change paradox. Int. J. Earth Sci. 2002, 91, 746–774. [Google Scholar] [CrossRef] [Green Version]

- Bernanke, B. A Letter to Sen. Bob Corke. Wall Str. J. 2009, 11, 18. [Google Scholar]

- Kaufman, G.G.; Kenneth, E.S. What Is Systemic Risk, and Do Bank Regulators Retard or Contribute to It? In The Independent Review; The Independent Institute: Oakland, CA, USA, 2003; pp. 371–391. Available online: https://law.stanford.edu/publications/what-is-systemic-risk-and-do-bank-regulators-retard-or-contribute-to-it/ (accessed on 17 November 2020).

- Dansgaard, W.; Johnsen, S.J.; Clausen, H.B.; Dahl-Jensen, D.; Gundestrup, N.S.; Hammer, C.U.; Hvidberg, C.S.; Steffensen, J.P.; Sveinbjörnsdottir, A.E.; Jouzel, J. Evidence for general instability of past climate from a 250 kyr ice core record. Nature 1993, 364, 218–220. [Google Scholar] [CrossRef]

- De Bandt, O.; Hattmann, P. Systemic Risk A Survey. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=258430 (accessed on 17 November 2020).

- Huntington, E. Climatic Variations and Economic Cycles, Geographical Review; Taylor & Francis, Ltd.: New York, NY, USA, 1916. [Google Scholar]

- Smaga, P. The Concept of Systemic Risk. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2477928 (accessed on 17 November 2020).

- Szpunar, P.J. Rola polityki makroostrożnościowej w zapobieganiu kryzysom finansowym. Narodowy Bank Polski. Departament Edukacji i Wydawnictw. 2012, 278. [Google Scholar] [CrossRef]

- Adrian, T.; Brunnermeier, M.K. CoVaR. Am. Econ. Rev. 2006, 106, 1705–1741. [Google Scholar] [CrossRef]

- Acharya, V.; Pedersen, L.; Philippon, T.; Richardson, M. Measuring Systemic Risk. Rev. Financ. Stud. 2017, 30, 2–47. [Google Scholar] [CrossRef]

- Brownlees, C.; Engle, R.F. SRISK: A Conditional Capital Shortfall Measure of Systemic Risk. Rev. Financ. Stud. 2017, 30, 48–79. [Google Scholar] [CrossRef]

- Aglietta, M.; Espagne, E. Climate and Finance Systemic Risks, more than an Analogy? The Climate Fragility Hypothesis. Available online: https://www.researchgate.net/profile/Etienne_Espagne/publication/305307236_Climate_and_Finance_Systemic_Risks_more_than_an_analogy_The_climate_fragility_hypothesis/links/57876ef808aea8b0f0c2bcd3.pdf (accessed on 7 November 2020).

- Batten, S.; Sowerbutts, R.; Tanaka, M. Let’s Talk About the Weather: The Impact of Climate Change on Central Banks. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2783753 (accessed on 7 November 2020).

- Dafermos, Y.; Nikolaidib, M.; Galanisc, G. Climate Change, Financial Stability and Monetary Policy. Ecol. Econ. 2018, 152, 219–234. [Google Scholar] [CrossRef]

- Bank of England. The impact of climate change on the UK insurance sector: A climate change adaptation report by the Prudential Regulation Authority. Available online: https://www.bankofengland.co.uk/-/media/boe/files/prudential-regulation/publication/impact-of-climate-change-on-the-uk-insurance-sector.pdf (accessed on 7 November 2020).

- FSB. Recommendations of the Task Force on Climate-related Financial Disclosures. June, 2017 [N/OL]. Available online: https://www.fsb-tcfd.org/wp-content/uploads/2017/06/FINAL-TCFD-Report-062817.pdf (accessed on 6 June 2019).

- Center for American Progress, Climate Change Threatens the Stability of the Financial System by Gregg Gelzinis and Graham Steele 2019. Available online: https://www.americanprogress.org/issues/economy/reports/2019/11/21/477190/climate-change-threatens-stability-financial-system/ (accessed on 21 November 2019).

- European Central Bank. The Financial Stability Review. Frankfurt, 2019. Available online: https://www.ecb.europa.eu/pub/financialstability/fsr/html/ecb.fsr201905~266e856634.en.html#toc1 (accessed on 16 March 2019).

- Economist Intelligence Unit. The Cost of Inaction: Recognising the Value at Risk from Climate; Chane: London, UK, 2015. [Google Scholar]

- Dowla, A. Climate Change and Microfinance. Bus. Strat. Dev. 2018. [Google Scholar] [CrossRef]

- Yao, L.; Tianyi, Z. Managing Financial Risks from Climate Change. Available online: https://www.citivelocity.com/citigps/managing-financial-risks-climate-change/ (accessed on 17 November 2020).

- Tianyin, S. Analysis on Sustainable Finance and Climate Risk. Financ. Perspect. J. 2020, 2, 24–31. [Google Scholar]

- Lin, T.; Jialin, G. Research on the Mechanism and Countermeasures of the Financial System for Risk from Climate Change. J. Financ. Dev. Res. 2020, 1, 13–20. [Google Scholar]

- Qiang, Z.; Han, Y.; Song, L. The Summary of Development in Global Climate Change and Its Influencing Factors. Adv. Earth Sci. 2005, 20, 47–60. [Google Scholar]

- Qin, D.H.; Chen, Z.L.; Luo, Y.; Ding, Y.H.; Dai, X.S.; Ren, J.W.; Zhai, P.M.; Zhang, X.Y.; Zhao, Z.C.; Zhang, D.E. Updated Understanding of Climate Change Sciences. Adv. Clim. Chang. Res. 2007, 3, 63–73. [Google Scholar]

- The National Climate Change Coordinating Group under the National Development and Reform Commission. Impacts of and Adaptation to Climate Change. In Initial National Communication on Climate Change of the People’s Republic of China; Planning Press: Beijing, China, 2004; pp. 23–35. [Google Scholar]

- Huang, C.; Liu, Q.; Hong, N. The Third National Assessment Report on Climate Change; Chinese Science Publishing & Media Ltd.: Beijing, China, 2015. [Google Scholar]

- Huo, Z.; Li, M.; Li, N.; Ma, Y. Impacts of Seasonal Climate Warming on Crop Diseases and Pests in China. Sci. Agric. Sin. 2012, 45, 2168–2179. [Google Scholar]

- Pan, G.; Gao, M.; Hu, G. Impacts of Climate Change on Agricultural Production in China. J. Agro Environ. Sci. 2011, 30, 1698–1706. [Google Scholar]

- Zhang, L.; Huo, Z.; Wang, L. Effects of Climate Change on the Occurrence of Crop Insect Pests in China. Chin. J. Ecol. 2012, 31, 1499–1507. [Google Scholar]

- Xu, S.; Song, G.; Li, D.; Yuan, N. Spatial-temporal Variation of Cultivated Land and Its Effects on Grain Production Capacity of Northeast Grain Main Production Area. Trans. Chin. Soc. Agric. Eng. 2012, 28, 1–9. [Google Scholar]

- Li, X.; Fu, H. Review of Foreign Theories about Risks in Financial System. Econ. Perspect. 1998, 1, 78–93. [Google Scholar]

- Ren, B. Empirical Research on the Impact of Money and Real Estate Bubble on Financial Risks. Ph.D. Thesis, Liaoning University, Shenyang, China, 2019. [Google Scholar]

- Ionescu, L. The Economics of the Carbon Tax: Environmental Performance, Sustainable Energy, and Green Financial Behavior. Geopolit. Hist. Intemational Relat. 2020, 12, 101–107. [Google Scholar]

- Pflugmann, F.; De Blasio, N. The Geopolitics of Renewable Hydrogen in Low Carbon Energy Markets. Geopolit. Hist. Intemational Relat. 2020, 12, 9–44. [Google Scholar]

- Ionescu, L. Pricing Carbon Pollution: Reducing Emissions or GDP Growth? Econ. Manag. Financ. Mark. 2020, 15, 37–43. [Google Scholar]

- Ionescu, L. Towards a Sustainable and Inclusive Low-Carbon Economy: Why Carbon Taxes, and Not Schemes of Emission Trading, Are a Cost-Effective Economic Instrument to Curb Greenhouse Gas Emissions. J. Self Govemance Manag. Econ. 2019, 7, 3541. [Google Scholar]

- Ionescu, L. Climate Policies, Carbon Pricing, and Pollution Tax: Do Carbon Taxes Really Lead to a Reduction in Emissions? Geopolit. Hist. Intemational Relat. 2019, 11, 92–97. [Google Scholar]

- Mao, J.; Zhang, H. Empirical Study on Systemic Financial Risk in China’s Banks Based on CCA Model. Macroeconomics 2015, 2, 33–52. [Google Scholar]

- Didier, J.; Wang, X. The Impact of Climate on Human Histories; Gold Wall Press: Beijing, China, 2014. [Google Scholar]

- Lamb, H.H.; Ingram, M.J. Report on the International Conference on “Climate and History”; Past & Present: Beijing, China, 1982. [Google Scholar]

- IPCC. Climate Change 2014: Synthesis Report; Contribution of Working Groups I, II and III to the Fifth Assessment Report of the Intergovernmental Panel on Climate Change; Pachauri, R.K., Meyer, L.A., Eds.; IPCC: Geneva, Switzerland, 2014; p. 44. [Google Scholar]

- Dietz, S.; Bowen, A.; Dixon, C.; Gradwell, P. Climate value at risk of global financial assets. Nat. Clim. Chang. 2016, 2, 676–679. [Google Scholar] [CrossRef] [Green Version]

- Federal Reserve Bank of New York. Superstorm Sandy: Update from Businesses in Affected Areas. 2014. Available online: https://www.newyorkfed.org/medialibrary/interactives/fall2013/fall2013/files/key-findingssandy.pdf (accessed on 20 July 2019).

- Klomp, J. Financial fragility and natural disasters: An empirical analysis. J. Financ. Stab. 2014, 13, 180–192. [Google Scholar] [CrossRef]

- Lambert, C.; Noth, F.; Schuewer, U. How Do Banks React to Increased Asset Risks? Evidence from Hurricane Katrina. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2022096 (accessed on 17 November 2020).

- Carney, M. Breaking the Tragedy of the Horizon–Climate Change and Financial Stability. Available online: http://www.bankofengland.co.uk/publications/Documents/speeches/2015/speech844.pdf (accessed on 2 July 2019).

- Adrian, T.; Brunnermeier, M.K. CoVaR; Working Paper; NBER: National Bureau of Economic Research: Cambridge, MA, USA, 2011. [Google Scholar] [CrossRef]

- Benoit, S.; Colliard, J.; Hurlin, C.; Pérignon, C. Where the Risks Lie: A Survey on Systemic Risk. Rev. Financ. 2017, 21, 109–152. [Google Scholar] [CrossRef]

- Agusman, A.; Cullen, G.S.; Gasbarro, D.; Monroe, G.S.; Zumwalt, J.K. Government intervention, bank ownership and risk-taking during the Indonesian financial crisis. Pac. Basin Financ. J. 2014, 5, 114–131. [Google Scholar] [CrossRef] [Green Version]

- Imai, M. Government Financial Institutions and Capital Allocation Efficiency in Japan. J. Bank. Financ. 2020, 7, 1–11. [Google Scholar] [CrossRef]

- Feng, L.; Fu, T.; Kutan, A.M. Can government intervention be both a curse and a blessing? Evidence from China’s finance sector. Int. Rev. Financ. Anal. 2019, 61, 71–81. [Google Scholar] [CrossRef]

- Yan, Y. Measurement of Systemic Risk in China’s Banking Sector Based on CoVaR. Stat. Decis. 2018, 6, 28–42. [Google Scholar]

- Jing, S. Research on the Influence of Internet Finance on the Systemic Risk of China’s Commercial Banks. Ph.D. Thesis, Shanxi University of Finance and Economics, Taiyuan, China, June 2019. [Google Scholar]

- Ren, G.; Chen, Y.; Liu, D. Definition and Trend Analysis of an Integrated Extreme Climatic Index. Clim. Environ. Res. 2010, 15, 56–72. [Google Scholar]

{kind=link}

{kind=link}

| Banks | |||||||

|---|---|---|---|---|---|---|---|

| China Minsheng Bank | 0.856345 (30.09) | 0.2563 | −0.1219 | 13.8702 | 0.6294 | −3.4297 | 6.0078 |

| Huaxia Bank | 0.685290 (28.14) | 8.0419 | 0.0316 | 8.3495 | 8.9260 | 0.8924 | −7.2788 |

| Bank of Beijing | 0.765317 (25.08) | −0.1324 | −0.4479 | 4.9239 | 0.2894 | −2.1921 | 0.4153 |

| Bank of Nanjing | 0.650929 (10.06) | −0.9238 | −0.1688 | 3.1751 | −3.0075 | −2.7424 | −7.8969 |

| Bank of Ningbo | 0.711595 (11.14) | 0.7706 | −0.1713 | 3.9613 | 1.0962 | −2.8082 | −3.9274 |

| Ping An Bank | 0.668712 (29.18) | 4.2248 | 0.1875 | 13.9360 | −0.2058 | −5.3534 | 6.6150 |

| Shanghai Pudong Development Bank | 0.723375 15.78) | 1.1720 | −0.3501 | 7.4879 | −0.6822 | −5.3691 | 13.1230 |

| Industrial Bank | 0.798520 (33.31) | 5.5964 | 0.4517 | 11.5811 | 6.6687 | −2.5132 | 0.5325 |

| China Merchants Bank | 0.757308 (30.24) | 0.5868 | −0.1320 | 3.7779 | 1.6247 | 0.5291 | −5.9086 |

| China CITIC Bank | 0.810208 (20.67) | 13.6422 | 0.1862 | 11.2629 | 13.2790 | −1.5200 | −11.3298 |

| China Everbright Bank | 0.774710 (28.55) | 9.0757 | 0.1234 | 9.4735 | 7.5043 | −1.8522 | −6.7870 |

| Banks | |||||||

|---|---|---|---|---|---|---|---|

| China Minsheng Bank | - | −1.1966 | −0.0518 | −1.0987 | −0.9090 | −0.3519 | 1.6229 |

| Huaxia Bank | - | −0.7739 | −0.1368 | −1.1132 | −0.2164 | −0.1428 | 1.0374 |

| Bank of Beijing | - | −0.7974 | −0.1307 | −0.7848 | −0.7721 | −0.2203 | 0.6553 |

| Bank of Nanjing | - | −0.2471 | −0.0778 | −0.8082 | −0.0720 | −0.2023 | 0.4323 |

| Bank of Ningbo | - | −1.2653 | −0.1016 | −1.2730 | −1.1757 | −0.3384 | 1.1455 |

| Ping An Bank | - | −0.9791 | −0.0801 | −1.6228 | −0.7318 | −0.1281 | 0.9631 |

| Shanghai Pudong Development Bank | - | −0.7994 | −0.0929 | −1.0020 | −0.5843 | −0.4944 | 0.8505 |

| Industrial Bank | - | −1.0974 | −0.1585 | −1.3098 | −0.8411 | −0.4610 | 1.2712 |

| China Merchants Bank | - | −1.0088 | −0.1553 | −1.1124 | −0.7291 | −0.3858 | 1.1022 |

| China CITIC Bank | - | −0.9109 | −0.0312 | −1.0315 | −0.6562 | −0.5171 | 1.8194 |

| China Everbright Bank | - | 0.1697 | −0.0970 | −1.1801 | 0.3483 | −0.1299 | −0.7992 |

| Variable | Test Form | t-Statistics | 10% Threshold | Prob * | Results |

|---|---|---|---|---|---|

| (c,t,0) | −4.020948 | −2.580908 | 0.0019 | Smooth | |

| DP | (c,t,0) | −2.629114 | −2.580908 | 0.0902 | Smooth |

| Coefficient | t-Statistics | p Value | R2 | DW Value | |

|---|---|---|---|---|---|

| Constant | 9.0372 | 1.906523 | 0.0983 | 0.24 | 0.5234 |

| Dp | 0.6229 | 1.817289 | 0.0652 |

| Residual | ADF Test Value | 10% Threshold | Results |

|---|---|---|---|

| ε( −Dp) | −4.0391 | −2.8879 | Smooth |

| Coefficient | t-Statistics | p Value | Adjustment to Long-Run Equilibrium | |

|---|---|---|---|---|

| Constant | −0.0041 | −2. 364135 | 0. 0196 | 0.2629 |

| D(Dp) | 0.8244 | 1.817289 | 0.0652 | |

| ECM(−1) | −0.2629 | −0.481435 | 0.6450 |

| DP | LDR | NPL | NIM | ||

|---|---|---|---|---|---|

| Mean | 9.2247 | 0.3010 | 0.7948 | 0.0122 | 0.0243 |

| Median | 8.8760 | 0.3100 | 0.7432 | 0.0141 | 0.0251 |

| Maximum | 16.3015 | 0.6600 | 0.9607 | 0.0173 | 0.0290 |

| Minimum | 4.8304 | −0.1100 | 0.6757 | 0.0055 | 0.0192 |

| Std. Dev. | 1.9991 | 0.1579 | 0.0944 | 0.0044 | 0.0029 |

| Skewness | 0.6383 | −0.1895 | 0.5480 | −0.3365 | −0.1970 |

| Kurtosis | 3.8311 | 2.9433 | 1.6649 | 1.4049 | 1.6743 |

| Observations | 111 | 111 | 111 | 111 | 111 |

| Variable | Test Form | t-Statistics | 10% Threshold | Prob * | Results |

|---|---|---|---|---|---|

| (c,t,0) | −4.0048 | −4.0436 | 0.0112 | Smooth | |

| DP | (c,0,0) | −2.6291 | −2.8879 | 0.0902 | Not smooth |

| D(DP) | (c,0,0) | −12.4167 | −2.8882 | 0.0000 | Smooth |

| LDR | (c,t,1) | −2.2407 | −3.4516 | 0.4622 | Not smooth |

| D(LDR) | (c,t,2) | −7.8801 | −3.4523 | 0.0000 | Smooth |

| NPL | (c,0,1) | −1.5993 | −2.8882 | 0.4795 | Not smooth |

| D(NPL) | (c,0,0) | −3.2312 | −2.8882 | 0.0208 | Smooth |

| NIM | (c,0,1) | −1.7209 | −2.8882 | 0.4180 | Not smooth |

| D(NIM) | (c,0,2) | −21.4569 | −2.8887 | 0.0000 | Smooth |

| Null Hypothesis | Trace Test | Null Hypothesis | Maximum Eigenvalue Test | ||||

|---|---|---|---|---|---|---|---|

| Statistics | Threshold (5%) | p Value | Statistics | Threshold (5%) | p Value | ||

| None * | 111.2557 | 95.7537 | 0.0028 | None * | 41.3392 | 40.0776 | 0.0358 |

| At most 1 * | 69.9165 | 69.8189 | 0.0491 | At most 1 | 25.2442 | 33.8769 | 0.3687 |

| At most 2 | 44.6723 | 47.8561 | 0.0966 | At most 2 | 19.2678 | 27.5843 | 0.3941 |

| At most 3 | 25.4045 | 29.7971 | 0.1475 | At most 3 | 14.3335 | 21.1316 | 0.3383 |

| At most 4 | 11.071 | 15.4947 | 0.2072 | At most 4 | 9.2030 | 14.2646 | 0.2697 |

| At most 5 | 1.8680 | 3.8415 | 0.1717 | At most 5 | 1.8680 | 3.8415 | 0.1717 |

| Variable | DP | LDR | NPL | NIM |

|---|---|---|---|---|

| R2 | 0.641 | 0.748 | 0.867 | 0.812 |

| VIF | 2.788 | 3.964 | 7.528 | 5.309 |

| Variable | Coefficient | Standard Deviation | t-Statistics | p Value |

|---|---|---|---|---|

| DP | 0.7274 | 2.0160 | 0.3608 | 0.7190 |

| LDR | −6.5623 | 4.0210 | −1.6320 | 0.1056 |

| NIM | −23.7898 | 152.5949 | −0.1559 | 0.8764 |

| NPL | 76.5610 | 118.2888 | 0.6472 | 0.5189 |

| ε | 13.8658 | 6.2878 | 2.2052 | 0.0296 |

| R-squared | 0.0363 | Mean dependent var | 9.2247 | |

| Adjusted R-squared | −0.0001 | S.D. dependent var | 1.9991 | |

| S.E. of regression | 1.9992 | Akaike info criterion | 4.2674 | |

| Sum squared resid | 423.6586 | Schwarz criterion | 4.3894 | |

| Log likelihood | −231.8388 | Hannan-Quinn criter. | 4.3169 | |

| F-statistic | 0.9970 | Durbin-Watson stat | 0.5451 | |

| Prob(F-statistic) | 0.4126 | |||

| F-Statistics | Prob.F | obs*R-Square | Prob.chi-Square |

|---|---|---|---|

| 3.792163 | 0.0064 | 13.89568 | 0.0076 |

| Variable | Coefficient | Standard Deviation | t-Statistics | p Value |

|---|---|---|---|---|

| ε | 13.3045 | 1.687277 | 7.885192 | 0.0000 |

| DP | 0.9027 | 0.417235 | 2.163685 | 0.0327 |

| LDR | −5.6124 | 0.680173 | −8.251482 | 0.0000 |

| NIM | −23.7731 | 47.19046 | −0.503770 | 0.6155 |

| NPL | 55.0378 | 31.47661 | 1.748531 | 0.0833 |

| Weighted Statistics | ||||

| R-squared | 0.7710 | Mean dependent var | 9.1596 | |

| AdjustedR-squared | 0.7623 | S.D. dependent var | 18.6795 | |

| S.E. of regression | 0.5254 | Akaike info criterion | 1.5950 | |

| Sum squared resid | 29.2712 | Schwarz criterion | 1.7170 | |

| Log likelihood | −83.5248 | Hannan-Quinn criter. | 1.6445 | |

| F-statistic | 89.2337 | Durbin-Watson stat | 0.9686 | |

| Prob(F-statistic) | 0.0000 | Weighted mean dep. | 9.2538 | |

| Unweighted Statistics | ||||

| R-squared | 0.0355 | Mean dependent var | 9.2247 | |

| Adjusted R-squared | −0.0009 | S.D. dependent var | 1.9991 | |

| S.E. of regression | 1.9999 | Sum squared resid | 423.9786 | |

| Durbin-Watson stat | 0.5442 | |||

| Variable | Mediator Variable | ||

|---|---|---|---|

| LDR | NPL | NIM | |

| DP | 0.8245 *** | 26.9530 *** | −26.6535 *** |

| Constant term | −0.3543 *** | −0.0276 | 0.9484 *** |

| Impact Path | Direct and Indirect Effect | BootSE | Interval Floor | Interval Ceiling |

|---|---|---|---|---|

| DP→ | −0.7776 | 0.5005 | −1.7698 | 0.2146 |

| DP→LDR→ | −3.1010 | 2.8845 | −9.0448 | 3.2072 |

| DP→NPL→ | 5.9292 | 2.0357 | 1.6650 | 10.0711 |

| DP→NIM→ | 16.7177 | 7.4589 | 11.3047 | 38.6391 |

| Hypothesis | Hypothesis Details | Results |

|---|---|---|

| H1 | Climate change would reduce the LDR of commercial banks and increase the systemic risk in the banking sector. | Not supported |

| H2 | Climate change would increase the NPL ratio of commercial banks and the systemic risk in the banking sector. | Supported |

| H3 | Climate change would narrow the NIM of commercial banks and increase the systemic risk in the banking sector. | Not supported |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Liu, Y.; Huang, C.; Zou, Z.; Chen, Q.; Chu, X. Research into the Mechanism for the Impact of Climate Change on Systemic Risk—A Case Study of China’s Small- and Medium-sized Commercial Banks. Sustainability 2020, 12, 9582. https://doi.org/10.3390/su12229582

Liu Y, Huang C, Zou Z, Chen Q, Chu X. Research into the Mechanism for the Impact of Climate Change on Systemic Risk—A Case Study of China’s Small- and Medium-sized Commercial Banks. Sustainability. 2020; 12(22):9582. https://doi.org/10.3390/su12229582

Chicago/Turabian StyleLiu, Yongping, Chunzhong Huang, Zongbao Zou, Qiao Chen, and Xuan Chu. 2020. "Research into the Mechanism for the Impact of Climate Change on Systemic Risk—A Case Study of China’s Small- and Medium-sized Commercial Banks" Sustainability 12, no. 22: 9582. https://doi.org/10.3390/su12229582