Data Valuation Model for Estimating Collateral Loans in Corporate Financial Transaction

1

Seoul Business School, aSSIST University, Seoul 03767, Republic of Korea

2

Department of Business Economics, Health and Social Care, The University of Applied Sciences and Arts of Southern Switzerland, 6928 Manno, Switzerland

*

Author to whom correspondence should be addressed.

J. Risk Financial Manag. 2023, 16(3), 206; https://doi.org/10.3390/jrfm16030206

Submission received: 17 January 2023

/

Revised: 1 March 2023

/

Accepted: 16 March 2023

/

Published: 22 March 2023

(This article belongs to the Special Issue Financial and Sustainability Reporting in a Digital Era)

Abstract

:The importance of data assets as intangible corporate assets is being emphasized as more business activities based on digital technology are being carried out. This study proposes the development of a data valuation model that can enable companies to use data assets as collateral for loans in financial transactions. To this end, a model was designed with a focus on the cost approach, which is less likely to involve arbitrariness and error among other valuation model approaches. Furthermore, a model simulation was conducted after securing transaction data of a Korean secondhand marketplace provider. Among the total costs of this marketplace provider, the cost of using data reflecting the ratio of data activities was derived, focusing on financial statements and tangible and intangible assets for the last five years. The data asset acquisition costs were derived, and the data replacement costs were calculated by reflecting the past price and wage growth rates. The results revealed that simulation companies could use a total of KRW 26.8 billion worth of data as collateral for a loan. Accordingly, the data valuation model developed in this study will contribute to reinforcing the value of corporate data assets and proposing a new means of corporate financing.

1. Introduction

With the rapid spread of personal media such as mobile and social media platforms, information in our daily lives is now being recorded as data. While data can be used for free in some cases, it is also purchased at a high price according to the needs of the buyer. It is for this reason that these data are recognized as intangible assets by big tech companies and companies pursuing digital transformation and are emerging as a critical driving force for creating corporate value (Sveiby 1997). Moreover, in the market, data is already recognized as a company’s means of production and has acquired the status of an asset as it is traded in accordance with the market economy system (Tsai et al. 2012). Therefore, as data is drawing attention as a new type of asset comparable to money, real estate, and intellectual property rights, the ‘data economy’ based on data distribution is growing rapidly (Reichman and Uhlir 2003).

According to Knowledge Sourcing Intelligence (Knowledge Sourcing Intelligence 2022), the global data broker market is expected to grow at a CAGR of 5.8%, from $232.6 billion in 2019 to $345.2 billion in 2026. Since the United States, the world’s largest data broker market, adopted an opt-out method early on, a data broker-centered data distribution market that freely collects and analyzes personal information was able to grow. Currently, more than 2500 private data broker companies are operating in the United States. China has established a government-led big data exchange to promote the rapid growth of the data industry and standardize technology, safety, and price. The UK promotes personal data transactions by determining the transfer of personal data to a third party through personal data storage and receiving monetary compensation for it (Pleger et al. 2021). Dawex is a global data marketplace platform that has data exchange technology and generates revenue through data transactions with its offices in Paris, Lyon, and Montreal (Dawex 2022). In the case of Korea, ten big data platforms were built to support the data distribution/transaction process under the leadership of the government. As a result, the data sales/brokerage service industry has grown at an average annual rate of 37% since 2018 (Korea Data Agency 2022).

Lately, companies have been directly acquiring related companies to secure data. Nike, for example, acquired Celect, an artificial intelligence development company, for personalized product recommendation and demand forecasting. Walmart acquired Aspectiva, a customer behavior analysis company, and McDonald’s also acquired Dynamic Yield, an Israeli startup specializing in menu-related data (Günther et al. 2017). Investment companies also highly value companies with excellent data collection and analysis capabilities (Miller and Mork 2013). For instance, Facebook’s Initial Public Offering in 2012 recorded the largest market value of $104 billion in history, clearly demonstrating that data is a company’s financial asset. In addition, in 2015, Caesars Entertainment in Las Vegas was sold based on the data asset value of the customer reward program, not real assets such as casino operating rights (KPMG International 2022).

Compared to other intangible assets, data is a non-rival good that can be shared infinitely without loss of value and has more diverse types than other intangible assets, and the more people use it, the more value can be realized (Wiencierz and Röttger 2017). In particular, data as an intangible asset is important in raising corporate finance such as other intangible assets, as its economic value increases. For this reason, financial companies are required to develop a loan evaluation system or financial product based on data intangible asset valuation to use data-collateralized loans as a realistic means of financing in the market (Araz et al. 2020; Subrahmanyam 2019). Accordingly, looking at previous studies on data valuation in the financial aspect, Reed (2007) suggested a data evaluation methodology for tax purposes, and King (2007) presented a methodology for a revenue-based approach.

The International Financial Reporting Standards (IFRS) and the International Valuation Standard Council (IVSC) can evaluate intangible assets as assets when they meet three criteria: identifiability, control of resources, and future economic benefits. However, since data may become tangible assets or intangible assets in some cases, if a company excludes usability simply for recording and storing purposes, it is evaluated as tangible assets (Salamudin et al. 2010). If the data is used for R&D and decision-making of a company, it can be evaluated as an intangible asset, and the value can be measured accordingly. In order to facilitate the transfer and transaction of various intangible assets (data, patents, brands, etc.), in-kind investment, technological finance (investment), litigation, and tax, the valuation of the value is actively conducted (Moody and Walsh 1999).

Recently, as artificial intelligence technology has been widely used in industrial sites, data among intangible assets is now changing from the recognition that it was a cost of a company in the past to a company’s asset. When comparing data with existing intangible assets, data is more diverse than other intangible assets, its capacity is incomparably larger, and it is highly utilized to derive effective business strategies. In addition, unlike other resources, it has a non-rivalry that can be shared with multiple departments and utilized at the same time, making it more highly regarded as an asset of a company in recent years (Reed 2007). AT&T, a U.S. telecommunications company, already had 2.7 billion dollars of data assets in its accounting books in 2011, with about 20% of European companies evaluating the data as assets of the company (KPMG International 2022). However, many companies’ data assets have not yet been reflected in their financial statements, or data valuations, such as data valuation methods, have been actively implemented.

A data value measurement model should be developed that reflects the differences between data assets and other intangible assets. Furthermore, a value measurement model is needed according to the purpose of using data of a company, and it is necessary to examine the factors affecting each model and its considerations. In particular, no matter how much data you have on important items, if the quality is not good, it is a big problem to use, and if it is not an essential item, it is not worth using even big data. In this regard, a 2015 Gartner study found that 40% of business projects fail due to data quality (Osinski et al. 2017). There is a need for criteria and methods to reasonably evaluate data value in consideration of these various factors.

Therefore, in this study, the following research questions could be asked. How can financial companies objectively perform data valuation for corporate loans? How should data collection and management be different for platform companies where data collection and management are critical? What is the best methodology for designing data valuation methods? Based on these research questions, this study attempted to develop a valuation model for data loan collateral based on the cost approach. A prior study on the data asset and intangible asset evaluation methodology was conducted first. Based on this, a data value evaluation model based on the cost approach methodology was designed. In addition, a model designed by collecting financial accounting and data-related data of actual companies was simulated.

The data business has a characteristic that the initial investment cost for data collection and management is high, and it takes a long time to secure profitability through commercialization. Hence, revitalizing financial support through activating data-collateralized loans can play an important role. In this respect, the data valuation model for collateral loans developed through this study will provide financial companies and data-based platform companies with specific guidelines for vitalizing data assets.

2. Previous Studies

2.1. Data Valuation and Mortgage

Collins et al. (1997) argued that the value of financial accounting information of companies engaged in industries requiring high technology differs from that of general companies. As Klock and Megna (2000) argued, intangible assets such as research and development costs, advertising costs, radio broadcast licenses, and the number of subscribers affect corporate value in the wireless communications industry. After all, when evaluating the value of high-tech companies for investing in R&D, human resources, and product development, their investment information on intangible assets plays a vital role (Amir and Lev 1996). According to Lönnqvist (2002) and Diefenbach (2006), intangible assets are ‘identifiable non-monetary assets with no physical substance’ and must be identifiable, controllable, and generate future economic benefits to meet the definition of an intangible asset. In addition, the recognition requirements are that possibility of an inflow of future economic benefits must be high and that the acquisition cost must be reliably measurable (Green and Ryan 2005).

Thus, investment banks and venture capitalists are highly interested in lending funds by collateralizing intangible assets owned by companies (Ganguli 2004). For example, in the United States, IP-backed loans are led by large private financial companies such as BoA, JP Morgan Chase, and Morgan Stanley (Heiden 2016). Since 1995, the Development Bank of Japan has provided IP-backed loans for IPs with legal rights. As China announced plans to expand financing for small and medium-sized enterprises in 2010, regional IP-backed loan systems were expanded. It promoted the universalization of financial services for intangible assets by promoting the establishment of various financial convergence systems such as IP-backed loans, securitization, and insurance in 2015 and strengthened its IP-backed loan business to support innovative small and medium-sized companies in 2019. As such, the need for a legal system and rational evaluation method for securing capital through selling or licensing intangible assets such as IP is strengthening worldwide (Amable et al. 2010).

In this respect, data is classified as a type of technology-related intangible asset (Saunders and Brynjolfsson 2016). Data is characterized by a wider variety of types generated than other intangible assets, an incomparably large capacity, and a very fast generation speed (Tsai et al. 2012). According to Chareonsuk and Chansa-ngavej (2010), considering data as information that has gone through software processing, the value of data increases according to the number of uses. In addition, unlike other resources, it is highly evaluated as an intangible asset of a company because it has non-rivalry that can be shared with various departments and used simultaneously (Green 2008).

Moreover, as data acquisition means, such as barcode technology, point-of-sale systems, mobile payment systems, and social networking services, have been diversified due to the innovative development of IT technology, data is accumulated in a certain form through a database, increasing value creation as an asset. As an example, in the UK, databases are copyrighted for 15 years from the time they are created and can act as assets if the rights of the database are proven (Reed 2007). Accordingly, research on the appropriate valuation methodology for database assets and the establishment of an evaluation basis for it is expanding (Lagrost et al. 2010).

Sengoku et al. (2021) defined and studied the Return of Byte using the concept of return on investment in relation to data valuation. Based on the data unit of 1 byte, they defined the Return of Byte, which measures the ratio of revenue generated by data compared to the cost required to store and manage data. If the Return of Byte is greater than 1, it means that the value of the data is greater than the cost of the data, and if it is less than 1, it means that the cost is greater than the value generated by the data. Shu (2016) suggested six characteristics for data to be valuable as an asset: ‘Information is shareable’, ‘The value of information increases with use’, ‘Depreciation of value over time depending on the type of data’, ‘The value of information increases with accuracy’, and ‘The value of information increases when combined with other information’, and ‘Appropriate amount of necessary data’. If each characteristic is interpreted in consideration of the mutual relationship, the value of data increases through the process of being shared and utilized, and the value decreases according to the type of data and the passage of time. In addition, they argued that if the data has high accuracy, it is possible to increase the value by linking it with other data.

Data can serve as collateral in the financial market through this asset valuation. Collateral is an important mechanism for reducing selective financing and reliably inform borrower’s quality (Stiglitz and Weiss 1981; Sharpe 1990; Boot and Thakor 1994). For this reason, data-collateralized loans refer to financial support for companies contributing to the creation of new markets and new industries by utilizing data-based business models (Rajan and Winton 1995). Corporate loans are executed with data assets and apps held by companies as collateral, and the characteristics of companies with business models that generate profits with core competencies in collecting, processing, and utilizing data without tangible assets such as real estate are taken into account (Sharpe 1990). Ultimately, the ability of such data to be collateralized becomes a vital financial resource that significantly influences a company’s investment and growth (Kiyotaki and Moore 1997).

2.2. Intangible Asset Valuation Models

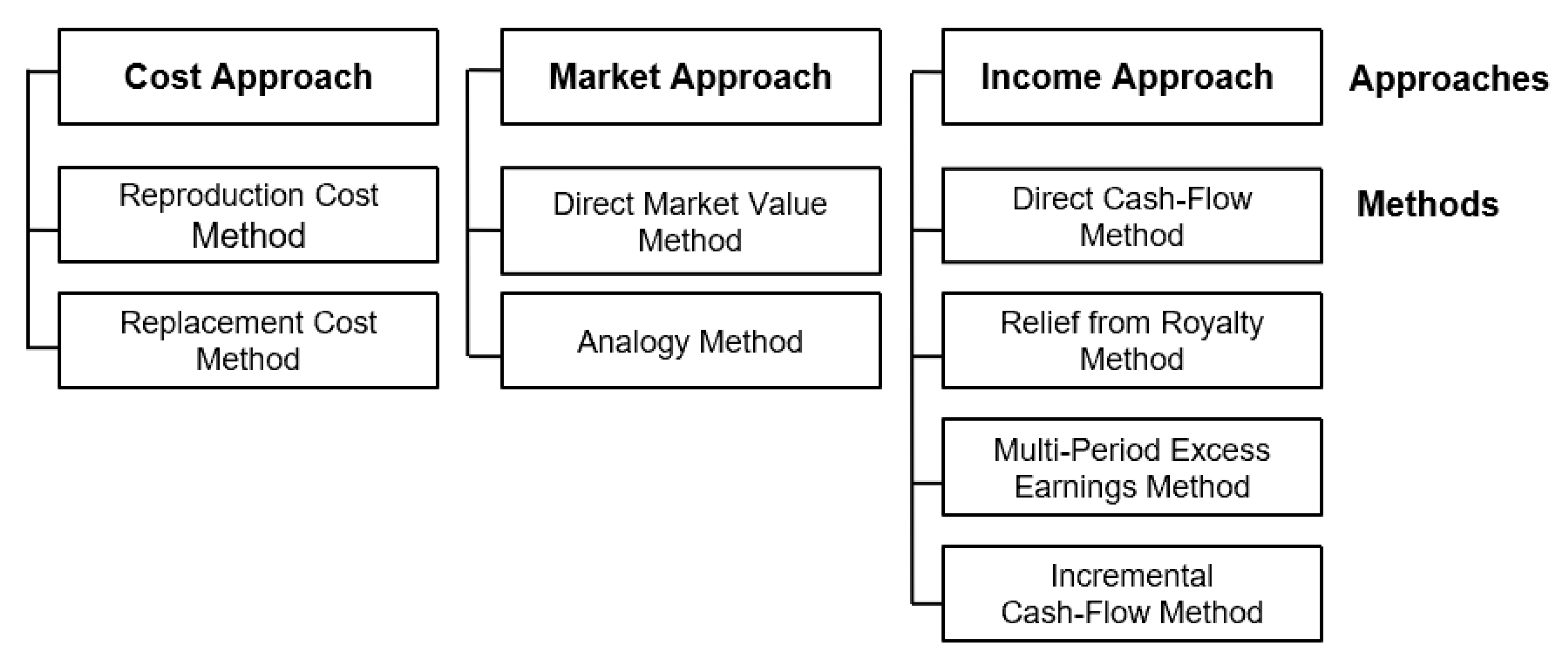

As shown in Figure 1, the most representative intangible asset valuation models include technology valuation and trademark valuation methods. In particular, technology valuation methods can be largely classified into cost approach, market approach, and income approach (Foster et al. 2003; Smith and Parr 2009).

First, the cost approach measures the value of goods by quantifying the cost of replacing an asset with another asset. A basic assumption of this approach is that the cost of new construction or purchase of real estate equals the value of ownership (Sharpe 1990; Smith and Parr 2009). Second, the market approach is based on the price paid as an indicator of the value of an asset. The basic principle is that supply and demand are in equilibrium under certain conditions in a competitive market (Foster et al. 2003). In particular, the direct market value method uses a direct deemed transaction price for the underlying asset. This method requires an active market for the product. In other words, the traded assets must be homogeneous, buyers and sellers can be found at any time, and prices must be publicly known (Wirtz 2012). Third, the basic theory of the income approach is that the value of an asset can be measured as the present value of the net economic benefits to be received over the life of the asset (Smith and Parr 2009; Wirtz 2012). Thus, the value of an asset is the result of its ability to generate cash flows and can be measured by the evaluation of these cash flows. Cash flows can appear in different ways and depend on the availability of assets.

Regarding data valuation methods, primary studies are on ‘data product’ valuation methods and ‘database’ valuation methods. First, the valuation methods of data products can be classified into cost-based, market-based, income-based, benefit monetization, and impact-based approaches (French 2004). The cost-based and market-based methods have the same perspective as the pricing method for tangible goods (Borkowski 2001). In other words, the price, one of the forms of value, is set based on the cost invested in producing the product or referring to competing products in the market. The market-based approach is a method that can be applied to markets with active transactions, but its disadvantage is the insufficient referenceable information to apply to the data product market with insufficient disclosed transaction information (Pagourtzi et al. 2003). The income, benefit, and impact criterion approach are a method that focuses on evaluating the additional value that data consumers can create through data products and is mainly applied to evaluate the financial benefits of public data such as census data (Venkatachalam 2004).

In the case of database asset valuation, three methodologies are representative. The first is the discounted cash flow method based on the income approach. The income approach is a method of replacing the net present value of future income expected to be obtained by technology with the value of technology, and the concept of income applied to the discounted cash flow method generally refers to increased cash flows over a certain period (Lipsey and Chrystal 2011). As shown in Equation(1), cash flows can be estimated by year within the economic life of the technology using an estimated income statement prepared based on the forecast of income and cost by technology, and the discount rate is determined using weighted average capital cost depending on the composition of capital, and the present value of the technology is obtained using the below formula (Ballester et al. 2003). Regardless of the development cost of the technology, this method focuses on the possibility of generating future income from the technology, viz., the future economic benefit, which includes future incomes, saved future cost, royalty relief, and increased corporate value due to competitive advantage. Equation (1) presents the discounted cash flow method based on the income approach.

: Value of technology, : Cash flow period t, : Discount rate (return on investment), : Economic life of technology.

Second, the cost approach is a method of measuring the future profit of an asset by calculating the number of resources required to obtain the same level of value as the value of the underlying asset (Rodov and Leliaert 2002). Normally, the estimation of asset value by the cost approach begins with estimating the cost required to obtain the same asset as the underlying asset, namely ‘the cost of reproduction new’, or the cost needed to acquire an asset with equivalent utility, namely ‘the cost of replacement’ (Madhani 2012). Equation (2) presents the cost approach based on expenses.

P: Cumulative price, C: Replacement cost, r: Year-on-year residual portion rate, n: Elapsed years.

Third, the market approach is a method of estimating the market value by analyzing recent sales or licensed similar technologies and then comparing and analyzing the technology subject to evaluation and technology transaction case information (Salamudin et al. 2010). Basically, it is possible only when there is a reliable transaction to grasp the flow of value form or trend in the market. The relief from royalty method is generally classified as the market approach, but it is also classified as the income approach because the estimated royalty income is capitalized and calculated as a valued amount. In the relief from royalty method, the value of the technology subject to evaluation is estimated based on the amount of royalty income, and the royalty income refers to the amount that would have occurred if the technology had been licensed in a fair transaction (Choi et al. 2000).

In general, the relief from royalty method utilizes the business sector or service to which the database asset subject to evaluation is applied. As shown in Equation (3), the final royalty value is calculated by deducting the corporate tax amount and converting the after-tax database asset royalty fee into the present value after multiplying the sales amount (St) generated by the business entity through future business activities during the economic life cycle (n) of the database asset by the database asset royalty rate (Osinski et al. 2017). Equation (3) shows the relief from the royalty method for the valuation of database assets.

Database asset value, : Sales volume at time t, Discount rate, Economic life of database assets, Database asset royalty rate, : Corporate tax amount at time t.

3. Building a Data Valuation Model

3.1. Valuation Method Based on the Cost Approach

The cost approach is based on the idea that future returns on an intangible asset can be measured by calculating the amount needed to obtain the same level of value as the value held by the intangible asset (Bhatt and Tang 1998). The cost approach is also based on the principle of substitution, which assumes that an investor will not pay more than the cost incurred to develop or acquire another asset with similar utility. In other words, after summing up the value of the physical and human resources invested in developing and forming the intangible asset to be evaluated, it is converted into present value (Shahab 2022).

Based on the overall development cost required to develop the intangible asset, it is calculated by deducting the value decrease during the elapsed period, taking into account the appropriate cost and opportunity cost related to technology. In particular, it can be used for immature technologies or technologies for which many substitutes are available. The characteristic of this evaluation method is that it can be a suitable method for the current data-based industry, where market growth potential is infinitely open and new types of convergent technology are emerging (Hendrik et al. 2013).

Regarding the valuation of intangible assets, existing studies have mainly focused on the income approach and market approach. However, both approaches have clear limitations. For example, the trading market of intangible assets is not very active for the market approach, and the income approach has a lot of room for evaluators’ subjectivity to be involved in estimating variables to predict future income. Therefore, in this study, financial evaluation is conducted based on the cost approach, which enables relatively objective evaluation through the existing financial statements.

Data valuation using a cost-based approach is conducted with a focus on the cost estimation required for data creation. The value of data is measured by summing up the costs invested in production, management, provision, and support for the data held by the company and converting past costs based on the current level. Operating expenses required for data creation were largely divided into direct and indirect costs, and different data operating ratios were applied in consideration of the characteristics of account titles (see Equation (4)). Equation (4) presents the data valuation method using the cost approach.

: Data asset value, : Total operating expense, : Data activity rate, : Data asset acquisition cost, : Data contribution.

The cost of data activity is the product of the rate associated with the data activity out of the total operating expense for each cost component. As for data activities, activities for companies to build databases were divided into five types such as data collection, storage, curation, analysis, and utilization. This classification is used to aggregate related operating expenses and assets. The total cost aggregation period is decided based on the income statement by comparing two of ‘the period between the start of the data business and the time of evaluation’ and ‘5 years from the time of evaluation’ and selecting the shorter one.

3.2. Data Definition and Calculation

Data collection was conducted in five types: ‘data collection’, ‘storage’, ‘curation’, ‘analysis’, and ‘utilization’. Data collection is an activity of storing data in a storage such as a data warehouse or cloud server and refers to activities such as application, device, development and operation or data purchase, scraping data collection, and application promotion for data collection.

Data storage is accumulating and continuously managing collected data in storage, and the main related activities are database, cloud server purchase and operation, and data security management. Data curation is an activity that meets the requirements necessary for the effective use of data through data quality management and data standard management. Data analysis is the activity of data exploration, transformation, and modeling to extract useful information from a business point of view and includes model development such as data mining, machine learning, deep learning, data statistical analysis, testing, etc.

Lastly, data utilization is an activity that combines data with business and includes data-based sales increase, added-value creation activities, and data-based internal operational efficiency improvement. According to the five types of data collection, storage, curation, analysis, and utilization, the direct cost (○) and indirect cost (△) of data operating assets and expense accounts are as follows (see Table 1).

Regarding the data cost calculation method by data activity asset and expense, sales and administrative expenses were classified by the criteria of McConnell (1990). Assets consist of tangible assets and intangible assets. For tangible assets, equipment, and intangible assets, software and assets acquired over the past five years were identified and classified as data activity assets based on the nature of each asset.

Sales and administrative expenses were divided into personnel expenses, other expenses related to personnel expenses, and direct costs. Regarding personnel expenses such as salary, retirement benefits, bonuses, and benefits for unused annual leave, data direct departments and indirect departments were divided based on the current organization chart, and the level of involvement in data activities by team was evaluated. In addition, based on the salary details of each team, the ratio of the data activity salary to the total employee’s salary was applied to the account amount each year. Regarding other expenses related to personnel expenses—employee benefits, travel expenses, transportation expenses, water and heat expenses, rent, education and training expenses, printing expenses, consumables, and property management expenses—the level of involvement in data activities by team was evaluated based on the current organizational chart, and considering the number of employees in each team, the ratio of the data activity man-hours to the total employee man-hours was applied to the account. In other words, the data activity ratio followed the calculation method in accordance with the definition of the data cost calculation method by identifying data activity assets and operating expense accounts.

The direct costs of sales and administrative expenses consist of communication expenses, commission fees, and advertising expenses. Data-related communication expenses, such as Amazon web services and cloud server hosting fees, were classified with details of communication expenses. In addition, data-related commission fees, such as server operation fees and software license purchase expenses, were classified with the details of commission fees. In addition, data-related advertising expenses, such as marketing and advertising expenses to secure users who are data contributors and mobile marketing platform Appsflyer fees, were classified with the details of advertising expenses (see Table 2).

4. Simulation Results

4.1. Selection of an Evaluation Targe and Collateral Set

Model verification was conducted on Korea’s representative third-largest used transaction platform company as ‘company A’. It is a second-hand trading app service in South Korea. Founded in 2011, it provided a platform service based on corporate transactions and started a used transaction app service for individual consumers in 2017. It handles used transactions of all products from clothes to food, cosmetics, used cars, electronic devices, home appliances, concert tickets, and e-cigarettes and is more convenient to use than existing used transaction sites because it is in the form of a smartphone app. It has used transaction data secured through the online used transaction service business. These used transaction data are managed and accumulated as important business resources, and necessary capital is sought by receiving loans or investments through data. Accordingly, the data valuation model designed by collecting data and accounting data from the past five years of this company was applied (see Table 3).

International Financial Reporting Standards (IFRS) are accounting standards issued by the International Accounting Standards Commission to enhance international uniformity in corporate accounting and financial statements. IFRS is a collective term for the International Accounting Standards Board (IBB) and Interpretations. The globalization of capital markets has led to an increase in the demand for reliable financial information on a single basis worldwide, and to meet this demand, the Board, an international accounting body operating independently of regulators, was created in 2001. IFRS is based on consolidated financial statements if there is a subsidiary, so all disclosure documents, including business reports, are prepared around consolidated financial statements. It also mandates or allows fair value measurements to be applied to financial assets, liabilities, tangible and intangible assets, and investment properties in order to provide meaningful investment information about the entity’s financial position and intrinsic value to investors in the capital market.

In Korea, all listed companies have been mandated to apply K-IFRS since 2011 in line with international accounting standards. Unlike before, when only individual financial statements were required to be disclosed due to the introduction of K-IFRS, it will be mandatory to disclose consolidated financial statements, and the evaluation method will be changed based on fair value, not on acquisition cost. In addition, the balance sheet is changed to a statement of financial position, the income statement is changed from the existing income statement to a comprehensive income statement that includes other comprehensive income on the balance sheet, and the retained earnings disposition statement is deleted. Allowance for bad debts shall be based on actual incurred losses rather than expected losses. The implementation of K-IFRS can reflect both the financial status and business performance of the company subject to consolidation, providing accurate financial information to investors.

Korean-listed companies and financial companies are required to use K-IFRS based on international accounting standards. Companies that are smaller in size and are not subject to external audits are required to use SME accounting standards. However, K-IFRS, currently used by listed companies, provides relatively more autonomy to account at the company’s discretion in situations where accounting principles are in place. In Korea, companies can use IFRS if they want to. IFRS is a principle-based accounting standard, not a regulatory-oriented accounting standard in the past K-GAAP. However, the use of general entity accounting standards was made possible, especially for smaller entities, because they might find it difficult to apply IFRS. General corporate accounting standards include excluding small companies from consolidated companies, recognizing amortization of goodwill, and allowing debt-bearing capital to be classified according to legal classification rather than the calculation of employee retirement liabilities based on actuarial assumptions. In this study, data analysis was conducted according to general corporate accounting standards in Korea as a study targeting unlisted startups.

As shown in Table 4, this study selected ‘company A’ as a simulation target to apply the designed data-based valuation model based on three evaluation items following the Korea Development Bank’s standards: data-based business model, marketability and growth potential, and data management capability. In the case of data-based business models, data-based industry specifications and business plans were evaluated based on the business plan preparation checklist. In the case of marketability and growth, the company was evaluated whether one or more of these three items were met based on Korea Development Bank’s standard as of December 2021 and whether it is listed on the stock market in accordance with the standard manual for technology credit evaluation, whether it has attracted more than 10 billion won in investment within the last three years, or whether it has received T3 or higher rating from designated TCB agencies.

Lastly, the data management capability is examined based on IS 8000-150 in data management and data governance and IS-IC 25010, 25,024 with data quality, 15 indicators, and 62 detailed indicators of the International Standard Index: Whether the company has its own data management organization composed of data scientists, whether it has security policies and backup systems for data management, whether it has work guidelines or manuals for efficient management and operation of data, and whether it conducts periodic inspections for data quality management and documents the inspection results.

In addition, as shown in Table 5, actual financial sector collateral was set up to confirm the actual utility of ‘company A’s data valuation. First, the rights of data and apps were registered in the copyright register, and a right of pledge agreement was signed. Next, the pledge was registered in the data and app copyright register. Afterward, the copyright registration was issued on the Internet to confirm the establishment of the pledge. Finally, after confirming the establishment of the pledge, a report on the right of pledge registration was made. Through this process, the possibility of data collateral of ‘company A’ was clearly confirmed.

4.2. Results

The data used for data valuation include these: company investor relations materials, recent 5-year financial statements, and list of tangible and intangible assets, which is the acquisition period and acquisition cost by asset, general ledger for data-related expense accounts, business plans presented by the company, and the latest organization chart of the company, the operational manual for each department and salary details, and research on the economic indicator of the Economist Intelligence Unit to calculate the current replacement cost.

Based on these data, the results of calculating the ratio of data activities by asset and expense of ‘Company A’, as shown in Table 6, are as follows. For tangible assets (equipment), the data contribution was calculated as 42.71% by aggregating the acquisition value of data operating assets. For intangible assets, the total acquisition value of data activity assets was aggregated. For personnel expenses with salaries and others, the ratio of data-related work salary to total employee salary was calculated as 44.96% based on the proportion of data activities by team. For other expenses related to personnel expenses with employee benefits and others, the ratio of data activity man-hours to the total employee man-hours was calculated as 43.71% based on the proportion of data activity work by team. For direct costs such as communication expenses, commission fees, and advertising expenses, the total expense of data activities was aggregated based on the details of the general ledger.

The calculation of the data activity MH by department and of the detailed data activity ratio of salary are as follows. The number of employees and the salary details for each team were confirmed to calculate the personnel expenses for data work based on the organization chart of June 2021, and the proportion of data activity work by team was identified through interviews with the company’s staff in charge. This study assumed that there is no difference in working hours. When calculating the personnel expenses for data work, one year’s personnel expenses for each team were estimated based on the salary in June 2021. The data-related personnel expenses were aggregated by applying the data activity work proportion to the personnel expenses of each team (see Table 7 and Table 8).

Regarding the acquisition value of data-related assets, this study reviewed tangible and intangible assets acquired from the second half of FY16 to the first half of FY21, the cost approach evaluation period, as shown in Table 9. In the case of tangible assets, the acquisition value of data-related tangible assets was aggregated, and the data contribution was applied. In the case of intangible assets, the total acquisition value related to data was aggregated. Regarding data activity expenses, the sales and administrative expenses incurred from the second half of FY16 to the first half of FY21, the cost approach evaluation period, were applied. Personnel expenses were divided into direct and indirect personnel expenses, and data MH ratio and data salary ratio were used. For expenses related to direct data activities, the total data-related expenses were aggregated through the data-related accounts, such as communication expenses, commission fees, and advertising expenses, in the general ledger from the second half of FY16 to the first half of FY21.

The current data replacement cost based on the company’s cost approach was calculated by reflecting economic indicators (inflation rate and wage increase rate) for each past year (see Table 10).

As a result of data value calculation during the evaluation period from the second half of FY16 to the first half of FY21, based on the evaluation criteria of the cost approach, it was calculated as KRW 26.8 billion. Of total tangible and intangible assets of about 2.8 billion won, data-related assets account for about 750 million won. Tangible assets, mainly business PCs, are approximately 180 million won by applying a data contribution of 42.71% to the acquisition value of equipment assets (approximately 420 million won) during the evaluation period. Intangible assets are software for data security management and fraud prevention, and the acquisition value of the software assets during the evaluation period was approximately 570 million won. Data-related expenses were tallied by checking the general ledger of data operating direct expense accounts, including communication expenses, commission fees, and advertising expenses). Regarding data operating-related personnel expenses, the ratio of data salary to employee salary (44.96%) was applied to salary, retirement benefits, bonuses, and benefits for unused annual leave. The ratio of data man-hours to employee man-hours (43.71%) was applied to indirect expenses related to personnel expenses: employee benefits, travel expenses, transportation expenses, water and heat expenses, rent, education and training expenses, printing expenses, consumables and property management expenses. In addition, the current data replacement cost based on the company’s cost approach was calculated by reflecting economic indicators (inflation rate and wage increase rate) for each past year (see Table 11).

5. Conclusions

5.1. Discussion and Implications

The study’s significance is that it designed a model that can evaluate the value of data and applied simulation results, especially for mortgage loans in the financial sector in the absence of a standardized framework for evaluating the value of intangible assets, such as software copyrights and data, as a type of corporate asset. Therefore, this study has the following implications; First, existing data valuation models are indirect value estimation methods with limitations in data utilization after turning the data into an asset specifically. However, this study designed a valuation model and simulated direct loan collateral setup to suggest the actual application of collateral valuation of financial institutions. In this process, the economic value inherent in the data was calculated using the company’s financial assets and operating expense accounts. In the end, evaluation data can be calculated by work connectivity through direct cost and indirect cost in achieving value evaluation for data assets. Therefore, it is crucial to structure the budget and execution of business activity expenses in all processes as data collection, storage, curation, analysis, and utilization, to clearly define data assets and efficiently evaluate their value.

Second, as the value of the data itself has increased not only in the data business sector but also in the manufacturing and service sectors and has become the source of corporate competitiveness, a realistic demand for companies to actively utilize the economic value of such intangible assets as collateral is arising. If a company provides data as collateral, the finance company should carefully manage the validity of the collateral so that it is not exposed to potential risks to its legal status during the loan period. In the case of mortgage loans, the data valuation model should reflect market conditions to narrow the gap with reality and increase reliability in consideration of the recoverability in the market. Furthermore, systematic management is required to avoid overestimating the value of data as collateral.

Third, the valuation of intangible assets should be evaluated using three approaches: the cost approach, the income approach, and the market approach. However, the conditions and various variables necessary for applying each approach must be determined based on the unique characteristics of the intangible asset. Depending on which approach should be applied in data valuation, the evaluation method can be selected in consideration of the evaluation purpose, target, and situation, and evaluation results can also vary. In other words, when evaluating data value, the value evaluation may vary depending on the approach to perform data evaluation and the model and parameters used. The result may also vary depending on the evaluation structure of each evaluation method and the estimated value of evaluation factors. Therefore, it is necessary to select an evaluation method that excludes subjective positions and ensures the rationality and objectivity of evaluation results.

Lastly, although corporate finance has shared corporate credit risk through tangible asset collateral represented by real estate, real estate market stagnation, and real estate collateral value decline are expected with the progress of the low birth rate and aging society. In this situation, data-collateralized loans are necessary from the viewpoints of the surrounding entities, companies whose core competitiveness is intangible assets, and financial companies seeking to strengthen industrial competitiveness and advance financial techniques by promoting new industries. It is essential to link the data assets owned by companies to the loan limit of financial companies to use them as a funding opportunity in a market environment where the quantitative and qualitative reinforcement of companies’ data assets is rapidly increasing. Therefore, it is crucial to have a data management and asset value enhancement system in consideration of data valuation, going beyond efforts just to accumulate data and use it as a business model. So far, many companies have focused on technical data management and system construction. However, they need to consider the financial value of data and apps as intangible assets and increase the protection and utilization of data assets through valuation. In this respect, it is possible to seek various approaches and strategic proposals for turning data into an asset and further consider preparing an institutional system to protect and manage data assets.

5.2. Research Limitations and Future Plans

Data-oriented companies can increase the utilization of retained data in the form of transfer/transaction, licensing, and others in addition to means of financial procurement through the proposed model by evaluating the economic value of data that is not highly utilized. In addition, they are expected to recognize the value of data and use it as reference information for decision-making. Nevertheless, this study’s data valuation method has several limitations.

First, this study was limited to data-based companies operating in Korea to verify the data value model, but it is required to expand and apply to various industries to generalize the study. Data-based companies typically have a high percentage of data operating. Therefore, securing the validity of the data value model proposed in this study is necessary by promoting research that compares and analyzes domestic and foreign general companies. Second, various models will need to be set up to evaluate the value of data, with basic value approaches, such as the income approach and the corporate value approach, or added value approaches, such as real options and the data transaction value approach in addition to the cost approach, considering the data evaluation target company’s data business types, marketability, new business promotion plans, and data sales. Lastly, since this study was conducted through the documents provided by the target company and the analytical review and inquiry thereof, differences could be found if close due diligence was performed. Due to the limitations in such data collection, it was impossible to compare and evaluate the data value reflecting the characteristics of each industry or them. A highly utilized data valuation model can be developed by continuously accumulating financial data of data-based companies and improving the model according to the purpose of valuation.

Author Contributions

Conceptualization, H.C.; methodology, H.C.; software, H.C.; validation, B.K.; formal analysis, H.C. and B.K; investigation, H.C. and B.K.; resources, H.C.; data curation, H.C.; writing–original draft preparation, H.C. and B.K.; writing–review and editing, B.K. and I.U.V.; visualization, B.K. and I.U.V.; supervision, B.K. and I.U.V.; project administration, B.K.; funding acquisition, H.C. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Not applicable.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Amable, Bruno, Jean-Bernard Chatelain, and Kirsten Ralf. 2010. Patents as collateral. Journal of Economic Dynamics and Control 34: 1092–104. [Google Scholar] [CrossRef]

- Amir, Eli, and Baruch Lev. 1996. Value-relevance of nonfinancial information: The wireless communications industry. Journal of Accounting and Economics 22: 3–30. [Google Scholar] [CrossRef]

- Araz, Ozgur M., Tsan-Ming Choi, David L. Olson, and F. Sibel Salman. 2020. Role of analytics for operational risk management in the era of big data. Decision Sciences 51: 1320–46. [Google Scholar] [CrossRef]

- Ballester, Marta, Manuel Garcia-Ayuso, and Joshua Livnat. 2003. The economic value of the R&D intangible asset. European Accounting Review 12: 605–33. [Google Scholar]

- Bhatt, Nitin, and Shui-Yan Tang. 1998. The problem of transaction costs in group-based microlending: An institutional perspective. World Development 26: 623–37. [Google Scholar] [CrossRef]

- Boot, Arnoud W. A., and Anjan V. Thakor. 1994. Moral hazard and secured lending in an infinitely repeated credit market game. International Economic Review 35: 899–920. [Google Scholar] [CrossRef]

- Borkowski, Susan C. 2001. Transfer pricing of intangible property: Harmony and discord across five countries. The International Journal of Accounting 36: 349–74. [Google Scholar] [CrossRef]

- Chareonsuk, Chaichan, and Chuvej Chansa-ngavej. 2010. Intangible asset management framework: An empirical evidence. Industrial Management & Data Systems 110: 1094–12. [Google Scholar]

- Choi, Won W., Sung S. Kwon, and Gerald J. Lobo. 2000. Market valuation of intangible assets. Journal of Business Research 49: 35–45. [Google Scholar] [CrossRef]

- Collins, Daniel W., Edward L. Maydew, and Ira S. Weiss. 1997. Changes in the value-relevance of earnings and book values over the past forty years. Journal of Accounting and Economics 24: 39–67. [Google Scholar] [CrossRef]

- Dawex. 2022. Available online: https://www.dawex.com/en/product/ (accessed on 30 August 2022).

- Diefenbach, Thomas. 2006. Intangible resources: A categorial system of knowledge and other intangible assets. Journal of Intellectual Capital 7: 406–20. [Google Scholar] [CrossRef] [Green Version]

- Foster, Benjamin P., Robin Fletcher, and William D. Stout. 2003. Valuing intangible assets. The CPA Journal 73: 50–54. [Google Scholar]

- French, Nick. 2004. The valuation of specialised property: A review of valuation methods. Journal of Property Investment & Finance 22: 533–41. [Google Scholar]

- Ganguli, Prabuddha. 2004. Patents and patent information in 1979 and 2004: A perspective from India. World Patent Information 26: 61–62. [Google Scholar] [CrossRef]

- Green, Annie. 2008. Intangible asset knowledge: The conjugality of business intelligence (BI) and business operational data. Vine 38: 184–91. [Google Scholar] [CrossRef]

- Green, Annie, and Julie J. C. H. Ryan. 2005. A framework of intangible valuation areas (FIVA): Aligning business strategy and intangible assets. Journal of Intellectual Capital 6: 43–52. [Google Scholar] [CrossRef] [Green Version]

- Günther, Wendy Arianne, Mohammad H. Rezazade Mehrizi, Marleen Huysman, and Frans Feldberg. 2017. Debating big data: A literature review on realizing value from big data. The Journal of Strategic Information Systems 26: 191–209. [Google Scholar] [CrossRef]

- Heiden, Bowman. 2016. The viability of FRAND: How the seminal landmark Microsoft ruling could impact the value of standard essential patents and the future of telecom standards. Telecommunications Policy 40: 870–87. [Google Scholar] [CrossRef]

- Hendrik, Bessembinder, William F. Maxwell, and Kumar Venkataraman. 2013. Trading activity and transaction costs in structured credit products. Financial Analysts Journal 69: 55–67. [Google Scholar]

- King, Kelvin. 2007. A Case Study in the Valuation of a Database. Journal of Database Marketing & Customer Strategy Management 14: 110–19. [Google Scholar]

- Kiyotaki, Nobuhiro, and John Moore. 1997. Credit cycles. Journal of Political Economy 105: 211–48. [Google Scholar] [CrossRef]

- Klock, Mark, and Pamela Megna. 2000. Measuring and valuing intangible capital in the wireless communications industry. The Quarterly Review of Economics and Finance 40: 519–32. [Google Scholar] [CrossRef]

- Knowledge Sourcing Intelligence. 2022. Available online: https://www.knowledge-sourcing.com/report/global-data-broker-market (accessed on 20 June 2022).

- Korea Data Agency. 2022. Available online: https://dataonair.or.kr (accessed on 12 September 2022).

- KPMG International. 2022. Available online: https://assets.kpmg/content/dam/kpmg/pdf/2015/08/data-new-driver-of-performance-v2.pdf (accessed on 12 September 2022).

- Lagrost, Céline, Donald Martin, Cyrille Dubois, and Serge Quazzotti. 2010. Intellectual property valuation: How to approach the selection of an appropriate valuation method. Journal of Intellectual Capital 11: 481–503. [Google Scholar] [CrossRef]

- Lipsey, Richard, and Alec Chrystal. 2011. Economics. London: Oxford University Press. [Google Scholar]

- Lönnqvist, Antti. 2002. Measurement of intangible assets–An analysis of key concepts. Frontiers of E-Business Research 27: 275–94. [Google Scholar]

- Madhani, Pankaj M. 2012. Intangible assets: Value drivers for competitive advantage. In Best Practices in Management Accounting. London: Palgrave Macmillan. [Google Scholar]

- McConnell, Kenneth E. 1990. Models for referendum data: The structure of discrete choice models for contingent valuation. Journal of Environmental Economics and Management 18: 19–34. [Google Scholar] [CrossRef]

- Miller, H. Gilbert, and Peter Mork. 2013. From data to decisions: A value chain for big data. It Professional 15: 57–59. [Google Scholar] [CrossRef]

- Moody, Daniel, and Peter Walsh. 1999. Measuring the value of information: An asset valuation approach. Paper presented at the Seventh European Conference on Information Systems (ECIS’99), Copenhagen Business School, Frederiksberg, Denmark, June 23–25; pp. 496–512. [Google Scholar]

- Osinski, Marilei, Paulo Mauricio Selig, Florinda Matos, and Darlan José Roman. 2017. Methods of evaluation of intangible assets and intellectual capital. Journal of Intellectual Capital 18: 470–85. [Google Scholar] [CrossRef]

- Pagourtzi, Elli, Vassilis Assimakopoulos, Thomas Hatzichristos, and Nick French. 2003. Real estate appraisal: A review of valuation methods. Journal of Property Investment & Finance 21: 383–401. [Google Scholar]

- Pleger, Lyn E., Katharina Guirguis, and Alexander Mertes. 2021. A Making public concerns tangible: An empirical study of German and UK citizens’ per-ception of data protection and data security. Computers in Human Behavior 122: 106830. [Google Scholar] [CrossRef]

- Rajan, Raghuram, and Andrew Winton. 1995. Covenants and collateral as incentives to monitor. The Journal of Finance 50: 1113–46. [Google Scholar] [CrossRef]

- Reed, David. 2007. Database valuation: Putting a price on your prime asset. Journal of Database Marketing & Customer Strategy Management 14: 104–9. [Google Scholar]

- Reichman, Jerome H., and Paul F. Uhlir. 2003. A contractually reconstructed research commons for scientific data in a highly protectionist intellectual property environment. Law and Contemporary Problems 66: 315–462. [Google Scholar]

- Rodov, Irena, and Philippe Leliaert. 2002. FiMIAM: Financial method of intangible assets measurement. Journal of Intellectual Capital 3: 323–36. [Google Scholar] [CrossRef]

- Salamudin, Norhana, Ridzwan Bakar, Muhd Kamil Ibrahim, and Faridah Haji Hassan. 2010. Intangible assets valuation in the Malaysian capital market. Journal of Intellectual Capital 11: 391–405. [Google Scholar] [CrossRef]

- Saunders, Adam, and Erik Brynjolfsson. 2016. Valuing information technology related intangible assets. Mis Quarterly 40: 83–110. [Google Scholar] [CrossRef]

- Sengoku, Shintaro, Toshihide Yoda, and Atsushi Seki. 2021. Assessment of pharmaceutical research and development productivity with a novel net present value-based project database. Drug Information Journal: DIJ/Drug Information Association 45: 175–85. [Google Scholar] [CrossRef]

- Shahab, Sina. 2022. Transaction costs in planning literature: A systematic review. Journal of Planning Literature 37: 403–14. [Google Scholar] [CrossRef]

- Sharpe, Steven A. 1990. Asymmetric information, bank lending, and implicit contracts: A stylized model of customer relationships. The Journal of Finance 45: 1069–87. [Google Scholar]

- Shu, Hong. 2016. Big data analytics: Six techniques. Geo-spatial Information Science 19: 119–28. [Google Scholar] [CrossRef] [Green Version]

- Smith, Gordon V., and Russell L. Parr. 2009. Intellectual Property: Valuation, Exploitation and Infringement Damages 2009 Cumulative Supplement. Hoboken: John Wiley & Sons. [Google Scholar]

- Stiglitz, Joseph E., and Andrew Weiss. 1981. Credit rationing in markets with imperfect information. The American Economic Review 71: 393–410. [Google Scholar]

- Subrahmanyam, Avanidhar. 2019. Big data in finance: Evidence and challenges. Borsa Istanbul Review 19: 283–87. [Google Scholar] [CrossRef]

- Sveiby, Karl Erik. 1997. The intangible assets monitor. Journal of Human Resource Costing & Accounting 2: 73–97. [Google Scholar]

- Tsai, Chih-Fong, Yu-Hsin Lu, and David C. Yen. 2012. Determinants of intangible assets value: The data mining approach. Knowledge-Based Systems 31: 67–77. [Google Scholar] [CrossRef]

- Venkatachalam, Lingappan. 2004. The contingent valuation method: A review. Environmental Impact Assessment Review 24: 89–124. [Google Scholar] [CrossRef]

- Wiencierz, Christian, and Ulrike Röttger. 2017. The use of big data in corporate communication. Corporate Communications: An International Journal 22: 258–72. [Google Scholar] [CrossRef]

- Wirtz, Harald. 2012. Valuation of intellectual property: A review of approaches and methods. International Journal of Business and Management 7: 40–48. [Google Scholar] [CrossRef] [Green Version]

Figure 1.

Valuation approaches and methods.

{kind=link}

Table 1.

Classification of direct and indirect costs in assets and expense accounts.

| Classification | Account Title | Classification Related to Data Activity | ||||

|---|---|---|---|---|---|---|

| Collection | Storage | Curation | Analysis | Utilization | ||

| Tangible assets | Equipment | ○ | ○ | ○ | ○ | - |

| Intangible assets | Software | ○ | ○ | ○ | ○ | ○ |

| Personnel expenses | Salary and others (1) | ○ | ○ | ○ | ○ | ○ |

| Other expenses related to personnel expenses | Employee benefits and others (2) | △ | △ | △ | △ | △ |

| Direct costs | Communication expenses | ○ | ○ | ○ | ○ | - |

| Commission fees | ○ | ○ | ○ | ○ | ○ | |

| Advertising expenses | ○ | △ | - | - | - | |

(1) Salary, retirement benefits, bonuses, benefits for unused annual leave. (2) Employee benefits, travel expenses, transportation expenses, water and heat expenses, rent, education and training expenses, printing expenses, consumables, and property management expenses.

Table 2.

Data cost calculation method by data operating asset and expense.

| Classification | Account Title | Data Cost Calculation Method | |

|---|---|---|---|

| Assets | Tangible assets | Equipment | Assets acquired over the past five years were identified and classified as data activity assets based on the nature of each asset. |

| Intangible assets | Software | ||

| Operating expenses (Sales and administrative expenses) | Personnel expenses | Salary and others | Data direct departments and indirect departments were divided, evaluating the level of involvement in data activities by team. Based on the salary details of each team, the ratio of the data activity salary to the total employee’s salary was applied to the account amount each year. |

| Other expenses related to personnel expenses | Employee benefits and others | The level of involvement in data activities by team was evaluated, and the ratio of the data activity man-hours to the total employee man-hours was applied to the account based on the number of employees in each team. | |

| Direct costs | Communication expenses | Data-related communication expenses, such as Amazon Web Services and CLOUD server hosting fees, were classified. | |

| Commission fees | Data-related commission fees, such as server operation fees and software license purchase expenses, were classified. | ||

| Advertising expenses | Data-related advertising expenses, such as marketing and advertising expenses to secure users who are data contributors and mobile marketing platform Appsflyer fees, were classified. | ||

Table 3.

The key financial statement of company A.

| Classification | FY 16 | FY 17 | FY 18 | FY 19 | FY 20 | FY21 1H |

|---|---|---|---|---|---|---|

| Sales | 2313 | 3528 | 7477 | 11,991 | 14,035 | 10,787 |

| Gross profit | 2313 | 3247 | 6255 | 10,053 | 12,262 | 6298 |

| Operating profit(loss) | 163 | 562 | 2073 | (2558) | (13,523) | (16,773) |

| Net profit(loss) | (206) | 261 | 1855 | (2509) | (13,170) | (16,662) |

| Total assets | 1076 | 5709 | 2164 | 5858 | 53,715 | 34,736 |

| Total liabilities | 4671 | 3474 | 1833 | 4215 | 7396 | 5079 |

| Total capital | (3595) | 2235 | 331 | 1643 | 46,319 | 29,657 |

Unit: KRW million.

Table 4.

Data-based enterprise checklist.

| Evaluation Items | Detailed Evaluation Items |

|---|---|

| Data-based business model (Both required) | Is its data-based industry clearly stated in the section of business purpose and type on its articles of incorporation, corporate registration certificate, and business registration certificate? |

| Does it have a plan for operating a data-based business in its business plan or mid- to long-term strategy? | |

| Marketability and growth potential (At least 1 out of 3) | Is it listed on the stock market (including KOSDAQ, excluding KONEX)? |

| Did it attract more than 10 billion won in investment (paid-in capital increase) within the last three years as of the date of loan counseling? | |

| Is its technology grade evaluated by designated TCB agencies higher than T3? | |

| Data management capability (All 5 required) | Does it have its own data management organization composed of data scientists? |

| Does it have security policies for data management? | |

| Does it have backup systems for data management? | |

| Does it have work guidelines or manuals for efficient management and operation of data? | |

| Does it conduct periodic inspections for data quality management and document the inspection results? |

Table 5.

Process to set collateral.

| Steps | Details |

|---|---|

| Step 1. Data and App registration (Registration of rights) | The rights of data and apps were registered in the copyright register. |

| Step 2. Right of pledge agreement | The pledge agreement was signed. |

| Step 3. Pledge registration (Registration of alteration of rights) | The pledge was registered in the data and app copyright register. |

| Step 4. Confirmation of pledge setting | The copyright registration was issued on the Internet. |

| Step 5. Report on right of pledge registration | After the confirmation of the pledge setting, a report on the pledge registration was made. |

Table 6.

Data activity ratio calculation method and result by asset and operating expense.

| Classification | Account Title | Data Activity Ratio Calculation Method | Data Activity Ratio Calculation Result | |

|---|---|---|---|---|

| Assets | Tangible assets | Equipment | The data contribution was calculated by aggregating the acquisition value of data activity assets. | Data contribution: 42.71% |

| Intangible assets | Software | The total acquisition value of data activity assets was aggregated. | Unapplied | |

| Operating expenses | Personnel expenses | Salary and others | The ratio of data-related work salary to total employee salary was calculated based on the proportion of data activities by team. | Ratio of data-related work salary to total employee salary: 44.96% |

| Other expenses related to personnel expenses | Employee benefits and others | The ratio of data activity man-hours to the total employee man-hours was calculated based on the proportion of data activity work by team. | Ratio of data activity man-hours to the total employee man-hours: 43.71% | |

| Direct costs | Communication expenses | The total expense of data activities was aggregated based on the details of the general ledger. | Unapplied | |

| Commission fees | ||||

| Advertising expenses | ||||

Table 7.

Details of data activity ratio calculation.

| Classification | Data Activity Man-Hour | Data Activity Salary (Unit: KRW Million) | ||||

|---|---|---|---|---|---|---|

| Employees by Department (1) | Employees for Data Work | MH Ratio (%) | Salary by Department | Salary for Data Work | Salary Ratio (%) | |

| Technical Support line | 61 | 41.4 | 68 | 3469 | 2431 | 70 |

| Directly under the CEO | 18 | - | - | 1282 | - | - |

| Customer | 22 | 15.8 | 72 | 1171 | 834 | 71 |

| Platform Business | 14 | - | - | 750 | - | - |

| Fashion and Life Biz | 9 | - | - | 314 | - | - |

| Digital Biz | 11 | - | - | 462 | - | - |

| Product | 11 | 5.5 | 50 | 870 | 435 | 50 |

| Creative Center | 17 | 8.5 | 50 | 779 | 390 | 50 |

| Ratio of data MH to employee MH | 163 | 71 | 43.71 | - | - | - |

| Ratio of data salary to employee salary | - | - | - | 9097 | 4090 | 44.96 |

(1) Data direct department: Technical Support line, Data indirect department: Directly under the CEO, Customer, Platform Business, Fashion and Life Biz, Digital Biz, Product, Creative Center.

Table 8.

Details of data activity ratio calculation for the equipment.

| Classification | FY 16 | FY 17 | FY 18 | FY 19 | FY 20 | FY21 1H | Total |

|---|---|---|---|---|---|---|---|

| Equipment | 10 | 19 | - | - | 269 | 117 | 415 |

| Data activity related equipment | 4 | 8 | - | - | 115 | 50 | 177 |

| Data activity ratio | 40 | 42.1 | - | - | 42.75 | 42.73 | 42.71 |

Unit: KRW million.

Table 9.

Results of data value calculation based on the cost approach before reflecting economic indicators.

Table 9.

Results of data value calculation based on the cost approach before reflecting economic indicators.

| Classification | Account Title | Data Operating by Account | Amount (Unit: KRW Million) | |

|---|---|---|---|---|

| Calculation Method | Applied Ratio (%) | |||

| Tangible assets | Equipment | Data contribution applied | 42.71 | 176 |

| Intangible assets | Software | Total acquisition value aggregated | Unapplied | 556 |

| Subtotal | 732 | |||

| Personnel expenses | Salary and others | Ratio of data salary to employee salary | 44.96 | 10,255 |

| Other expenses related to personnel expenses | Employee benefits and others | Ratio of data MH to employee MH | 43.71 | 1845 |

| Direct costs | Communication expenses | Aggregation of data operating expenses | Unapplied | 12,958 |

| Subtotal | 25,058 | |||

| Total | 25,790 | |||

Table 10.

Economic indicators.

| Classification | Applied Item | FY16 | FY17 | FY18 | FY19 | FY20 | FY21 1H |

|---|---|---|---|---|---|---|---|

| Wage increase rate | Personnel expenses | 3.8% | 2.7% | 5.1% | 3.3% | 0.7% | 3.3% |

| Inflation rate | Personnel expenses and others (1) | 1.0% | 1.9% | 1.5% | 0.4% | 0.5% | 1.5% |

(1) Assets, indirect costs related to personnel expenses, direct costs.

Table 11.

Result of data value calculation based on cost approach after reflecting economic indicators.

Table 11.

Result of data value calculation based on cost approach after reflecting economic indicators.

| Classification | Account Title | Amount (Unit: KRW Million) |

|---|---|---|

| Tangible assets | Equipment (Business PCs and others) | 181 |

| Intangible assets | Software (SW for data security management and fraud prevention) | 564 |

| Subtotal | 745 | |

| Personnel expenses | Salary, retirement benefits, bonuses, benefits for unused annual leave | 10,942 |

| Other expenses related to personnel expenses | Employee benefits, travel expenses, transportation expenses, water and heat expenses, rent, education and training expenses, printing expenses, consumables, property management expenses | 1889 |

| Direct cost | Communication expenses, commission fees, advertising expenses | 13,217 |

| Subtotal | 26,047 | |

| Total | 26,792 | |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Cheong, H.; Kim, B.; Vaquero, I.U. Data Valuation Model for Estimating Collateral Loans in Corporate Financial Transaction. J. Risk Financial Manag. 2023, 16, 206. https://doi.org/10.3390/jrfm16030206

AMA Style

Cheong H, Kim B, Vaquero IU. Data Valuation Model for Estimating Collateral Loans in Corporate Financial Transaction. Journal of Risk and Financial Management. 2023; 16(3):206. https://doi.org/10.3390/jrfm16030206

Chicago/Turabian StyleCheong, Hyongmook, Boyoung Kim, and Ivan Ureta Vaquero. 2023. "Data Valuation Model for Estimating Collateral Loans in Corporate Financial Transaction" Journal of Risk and Financial Management 16, no. 3: 206. https://doi.org/10.3390/jrfm16030206