Antecedents of Behavioural Intention to Adopt Internet Banking Using Structural Equation Modelling

1

Chitkara Business School, Chitkara University, Punjab 140401, India

2

Department of Insurance and Risk Management, Faculty of Economics, Management and Accountancy, University of Malta, MSD 2080 Msida, Malta

*

Author to whom correspondence should be addressed.

J. Risk Financial Manag. 2022, 15(4), 157; https://doi.org/10.3390/jrfm15040157

Submission received: 28 February 2022

/

Revised: 27 March 2022

/

Accepted: 28 March 2022

/

Published: 31 March 2022

(This article belongs to the Section Banking and Finance)

Abstract

:Technology is emerging as an as an important banking mode for customers, and although almost all the banks in India are offering Internet Banking, India faces problems related to the digital divide, e-frauds, and high rates of interest, amongst other things. This is causing concern in banks, which are trying to persuade people to adopt their online banking services. Therefore, the aim with this study is to determine the antecedents of behavioural intentions to adopt e-banking in an emerging economy such as India. We did this by administering a questionnaire with 34 questions and nine constructs to which participants responded using a Likert scale of 1 to 5, 1 being strongly disagree and 5 strongly agree. All constructs used in this questionnaire were adapted from literature related to the antecedents of behavioural intentions to adopt e-banking. We received 436 valid responses, which we analysed using Cronbach’s alpha, Confirmatory Factor Analysis, and Structural Equation Modelling. Results show that Performance Expectancy, Hedonic Motivation, Experience, Habit and Attitude, Perceived Website Usability, and Security and Reliability positively influence the intention to adopt Internet Banking, suggesting that policymakers and bankers should focus on improving website usability and hedonic enjoyment while focusing on Internet Banking performance, security, and dependability. In addition, Effort Expectations, Social Influence, Facilitating Conditions, and Trust resulted as not significant influencing factors of Internet Banking usage; Indians appear to find Internet Banking straightforward to use, perceive it as a breeze, and believe they are backed by solid support systems and organisational infrastructures. Moreover, trust is not a driving factor for Indians to adopt Internet Banking because they already perceive it as a trustworthy exercise.

1. Introduction

Technology has taken centre stage in behavioural research. Internet Banking (IB) services can be offered in several ways and have emerged as an important banking mode for customers (Nasri and Charfeddine 2012). Additionally, opening up the Indian economy to globalisation during the 1990s has facilitated the development of IB. Moreover, to implement various recommendations suggested by committees, the Indian government has stressed the importance of implementing IB in the banking sector (Srivastava 2007).

Banking is considered an information-intensive business in which information technology is playing a key role (Shih and Fang 2004). IB is an umbrella term for all those banking activities performed by customers either electronically or online without going through the hassle of reaching out to brick and mortar banks (Compeau and Higgins 1995; Banu et al. 2019). It encompasses the delivery of banking services via different channels such as the Internet, managed networks, personal computers, etc. (Daniel 1999). In addition, it allows the use of the Internet and the World Wide Web to allow customers to carry out financial activities in a virtual space (Shih and Fang 2006). IB is “a new type of information system that uses emerging techniques such as the Internet and the world wide web and has changed how customers perform various financial activities in a virtual space” (Shih and Fang 2006). Additionally, a virtual bank has been indicated as a “non-branch bank” that provides banking services through online channels (Liao et al. 1999). Employing the Internet in providing banking services adds to consumer value and power (Barrutia and Echebarria 2005).

IB extends traditional banking services by making banking services available at any time, providing ease of access, removing the inconvenience of queues, banking hours, reducing operating costs to banks, etc. (Khalfan et al. 2006). In addition, IB has been seen to provide banks with time and place advantage, reduced operating costs, and enhanced reach to customers (Rawashdeh 2015). Moreover, the service delivery from banks has improved by including technology and innovation (YuSheng and Ibrahim 2019).

However, although almost all the banks in India are offering IB, India is facing problems related to the digital divide, e-frauds, and high rates of interest, amongst other things. This is causing client apprehension and a concern for banks that are trying to persuade clients to adopt their online banking services and overcome any apprehension in the use of technology for banking transactions (Ingle and Pardeshi 2012).

In India, e-banking is still in its early phases of development. The banking industry has transformed due to competition and technological advancements (Smriti and Kumar 2021). In recent years, India’s Internet penetration rate has increased significantly. Between 2007 and 2021, it increased by 50% from 4% to 50%. This means that India’s population of 1.37 billion people has Internet connections, and the country is ranked second in the world for active Internet users (Basuroy 2022). On the other hand, roughly half of the population (i.e., 685,591,071) is still unconnected to the Internet, making India the country with the biggest number of unconnected persons (Ang 2020). According to another survey conducted by Statista (2021), roughly 68% of households own smartphones, yet only 14% use them for banking. As a result of this division, India is an intriguing case study in the context of Internet Banking.

Therefore, in this study, we investigate, lay out, and discuss our findings on the antecedents to behavioural intentions to adopt e-banking in an emerging economy such as India. Banks play an important role in the development of an economy especially an emerging economy such as India. A strong banking sector is the lifeline of any strong economy. Therefore, given this and the opportunities provided by e-banking, such a study is important both for banks and policymakers in their decision making on implementing a strategy for increasing the uptake by Indian people of e-banking services.

2. Related Literature

Various studies have explored the dimensions of customer behaviour for IB across different countries utilizing the Technology Acceptance Model (TAM) and the Technology Acceptance and Unified Theory of Acceptance and Use of Technology (UTAUT) models. The former is a customer-centred approach to measuring new technology uptake. Davis (1989) was seeking for a mechanism to predict and explain system utilisation to suppliers and IT managers at a time when computers were being brought into the workplace. When consumers are introduced with new technology, the model implies that a variety of factors influence their decision on how and when to utilise it. These include (1) PU (Perceived Utility)—“the degree to which a person believes that implementing a particular method would boost their job performance”. It refers to whether or not someone considers a piece of technology to be beneficial for the task at hand. (2) Perceived Ease-of-Use (PEOU), that is, “the degree to which a person believes that using a specific system would be devoid of effort”. If the technology is simple to use, the hurdles will be overcome. No one has a positive opinion of something if it is difficult to use and has a convoluted interface. (3) External factors such as social influence have a significant role in determining attitude. People will have the attitude and intention to use technology once items (1) and (2) mentioned above are in place. However, because everyone is different, perceptions may fluctuate depending on age and gender (Davis 1989). The TAM has been regularly explored and expanded, with the TAM 2 and TAM 3 being the two significant updates (Venkatesh and Davis 2000; Venkatesh 2000).

The latter model has been used by “many educational institutions and research organisations to answer one of the most important questions: What are users’ attitudes toward accepting ICT solutions?” It helps to investigate how performance expectancy (PE), effort expectancy (EE), social impact (SI), and facilitating factors influence (FC) technology acceptance (Venkatesh et al. 2003).

For example, Durkin et al. (2008), in their focus on e-banking as a self-service technology for providing IB, examined the demand for remote access to bank accounts. They found that banks need to strike a customer-centric balance between face-to-face relationship-managed activities and online enablement, and to recognise that this balance varies by client and product complexity. Cheng et al. (2006) look at how Hong Kong clients view and use IB. They created a theoretical model based on the TAM with the addition of a new concept, Perceived Web Security, and empirically examined its capacity to predict customers’ behavioural intentions towards IB adoption. Their findings back up the expanded TAM model and show that it is accurate in predicting customers’ intentions to use IB. Rodrigues et al. (2017) study the influence of gamification on intention to use. They suggest that gamification of banking leads to software design and development and influences the motivation of users to carry out online transactions. Moreover, they find a positive association between gamified banking experience to use, web design, information, and website characteristics.

Sharma et al. (2020) investigated the behavioural intention to adopt IB by individuals under the influence of user espoused cultural values in Fiji. According to their findings, levels of performance expectancy, effort expectancy, social influence, and facilitating environments all influence IB adoption positively. However perceived risk has a negative impact on IB usage intention. It was discovered that IB intention has a favourable impact on usage behaviour, which in turn has a beneficial impact on customer satisfaction. Moreover, they note that uncertainty avoidance also reduces the impact of performance expectancy and facilitating conditions of IB adoption intention. In addition, they continue by emphasising the role of cultural values in encouraging IB adoption. AlQudah (2014) applied the Technology Acceptance Model’s (TAM), which assists managers and decisionmakers to evaluate the success of the organisation’s technology implementation and persuade users to embrace the systems, to the Moodle system. The findings show that perceived ease of use is a more significant barrier to Moodle adoption.

A study of 798 online banking users in Iran by Dianat et al. (2019) looked at the interaction between Web design qualities (personalisation, structure, navigation, layout, search, and performance) and users’ personal characteristics on website usability and satisfaction, and it found that from the users’ standpoint, the design and usability of the evaluated websites were not sufficient. Web layout and performance were found to be the most important determinants of website usability, while personal variables such as gender, age, and previous Web usage experience had little effect. User happiness was likewise driven solely by Web design qualities (especially Web structure), not by the consumers’ personal traits. In addition, there was a link between website usability and user happiness. The findings implied that regardless of the personal qualities of their users, website designers should focus more on Web design elements (especially Web layout and structure) to improve website usability and happiness.

Alalwan et al. (2018) developed and tested a conceptual model that best describes the important aspects that influence Jordanian customers’ intents and adoption of IB. The proposed conceptual model was based on an expanded version of the UTAUT. This was expanded by including perceived danger as an external variable. Their findings demonstrated that PE, EF, hedonic motivation, price value, and perceived risk all have a significant impact on behavioural intention; however, social influence has no significant impact on behavioural intention. Wang et al. (2020) carried out research on cyber security in the Nigerian IB business. They included the biggest cyber security breaches that the industry has faced, as well as its cyber security capacity and practices. Their findings show that the Nigerian cybercrime business has progressed from low-tech cyber-enabled crimes to high-tech sophisticated breaches, with viruses, worms, and Trojan infections, electronic spam mailings, and hacking being the top three most common breaches. The note that although banking professionals have received acceptable management training in terms of cyber security practices, the lack of modern technologies to prevent and handle cyber security breaches, as well as a low degree of statutory compliance, appear to be the key contributors to the banks’ lower cyber security capabilities.

Arif et al. (2020) explore the impediments to IB adoption in Karachi, Pakistan. Their results highlighted a substantial positive association between value barrier, risk barrier, and image barrier. Only the traditional barrier had a negligible negative impact on IB usage. The image barrier has the greatest impact on IB usage, which is followed by the value and risk barriers. These barriers were more prominent in males.

A study by Yasin et al. (2020) focused on two main goals in Palestine: that is, (1) to determine the influence of the customer online brand experience (COBE) with online banking on the intention of customers to forward online company-generated content (CGC); and (2) to determine the role of online brand community engagement (OBCE) and brand community page perceived trust (BCP) as mediating variables between COBE and the intention to forward online CGC. Results highlighted that in the fast-growing Islamic banking market, COBE exerts a dual influence on intention to forward CGC. They find that COBE influences online Brand Community Engagement and customer behavioural outcomes, such as CGC forwarding intention. Furthermore, this research reveals that customers’ intention to advance online CGC is influenced by the perceived trust of the Facebook page, which mediates the relationship between Brand Engagement and intention to forward online CGC. Findings show the importance of trust and the quality of information provided and shared among community members and page administrators. These results are in line with the findings by Tang and Liu (2015), who note that people can easily participate in online activities thanks to social media, which removes the barrier for Internet users to generate and share information from anywhere at any time. However, they note that the expansion of user-generated content, on the one hand, presents new obstacles for online users in finding useful information, exacerbating the problem of information overload. The quality of user-generated content, on the other hand, might range from excellent to abuse or spam, posing a challenge of information credibility.

The goal of the study by Barrutia and Echebarria (2005) was to assess the impact of the Internet on the retail banking sector in Spain, taking into account two intertwined important constructs: customer power and consumer value. They developed a new conceptual framework, three fundamental propositions, and eleven hypotheses, and they compared and evaluated them in the context of Spain’s retail banking business. They show that the Internet has increased the customer value of retail banking customers using a multicase method and then investigated the reasons for this. Their research makes a three-fold contribution: (1) they define a new conceptual framework to understand the impact of the Internet on customer power and value; (2) they contrast the observations made in the most current literature on the subject in the context of Spain’s retail banking sector; (3) they show qualitatively that the drivers identified in strategy and marketing literature have an impact on consumer value, although not in the same way. However, they propose a differentiation consisting of two steps, that being driven by new players and a new competitive approach (the supply side) and that consumer power is driving the second transformation (the consumer side).

Jiménez and Díaz (2019) investigate the determinants that lead to the adoption of IB in Spain. Considering a sample size of 4300 observations, they find a positive relationship between a higher education level, gender, income level, employment status, use of ATMs, and frequency to operate for banking services.

Aboobucker and Bao (2018) studied the reasons that impede the acceptance of IB in Sri Lanka. Security and privacy, perceived trust, perceived risk, and online usability were the factors considered in this study. According to their findings, perceived trust and website usability are two potential impeding factors that IB clients are concerned about. Security and privacy, as well as perceived risk, were not found to be substantial influencing factors of concern when it comes to accepting Internet banking.

A study by Daneshgadeh and Yıldırım (2014) examined the factors that influence Turkish bank customers’ use of IB. An IB usage model (IBUM) was created and tested. The original proposed model included ten characteristics that influence Internet Banking usage: usefulness, simplicity of use, control, social influence, compatibility, risk, website features, alliance service, awareness of service, and personalisation. Results revealed that compatibility had the greatest impact on Internet Banking usage, which is followed by alliance service, usefulness, personalisation, and convenience of use. As a result, the original model was altered in order to discover the inter-relationships between components. The final IBUM was made up of seven components that can account for 65% of the variation in online banking usage. The final conclusions revealed that customers choose IB because it is convenient and easy to use. In addition, the compatibility of IB with customers’ life and work patterns has been identified as a key driver of IB usage.

In another study, Bauer and Hein (2006) revealed that perceived risk is a key factor responsible for obstructing the adoption of IB. They find older customers more hesitant to adopt IB irrespective of their risk tolerances. In addition, younger consumers become early adopters since they indicate higher risk tolerance levels.

3. Methodology

Drawing on the theory of technology adoption and IB adoption, this study is rooted in the UTAUT model suggested by Venkatesh et al. (2012). The model, as noted above, provides a unified view for validating technology acceptance models in different contexts. In addition, the studies by Venkatesh et al. (2003), Alalwan et al. (2018), and Venkatesh and Zhang (2010) mentioned above have supported the UTAUT as a comprehensive model for investigating consumer behaviour under the context of electronic banking.

3.1. Sample and Procedure

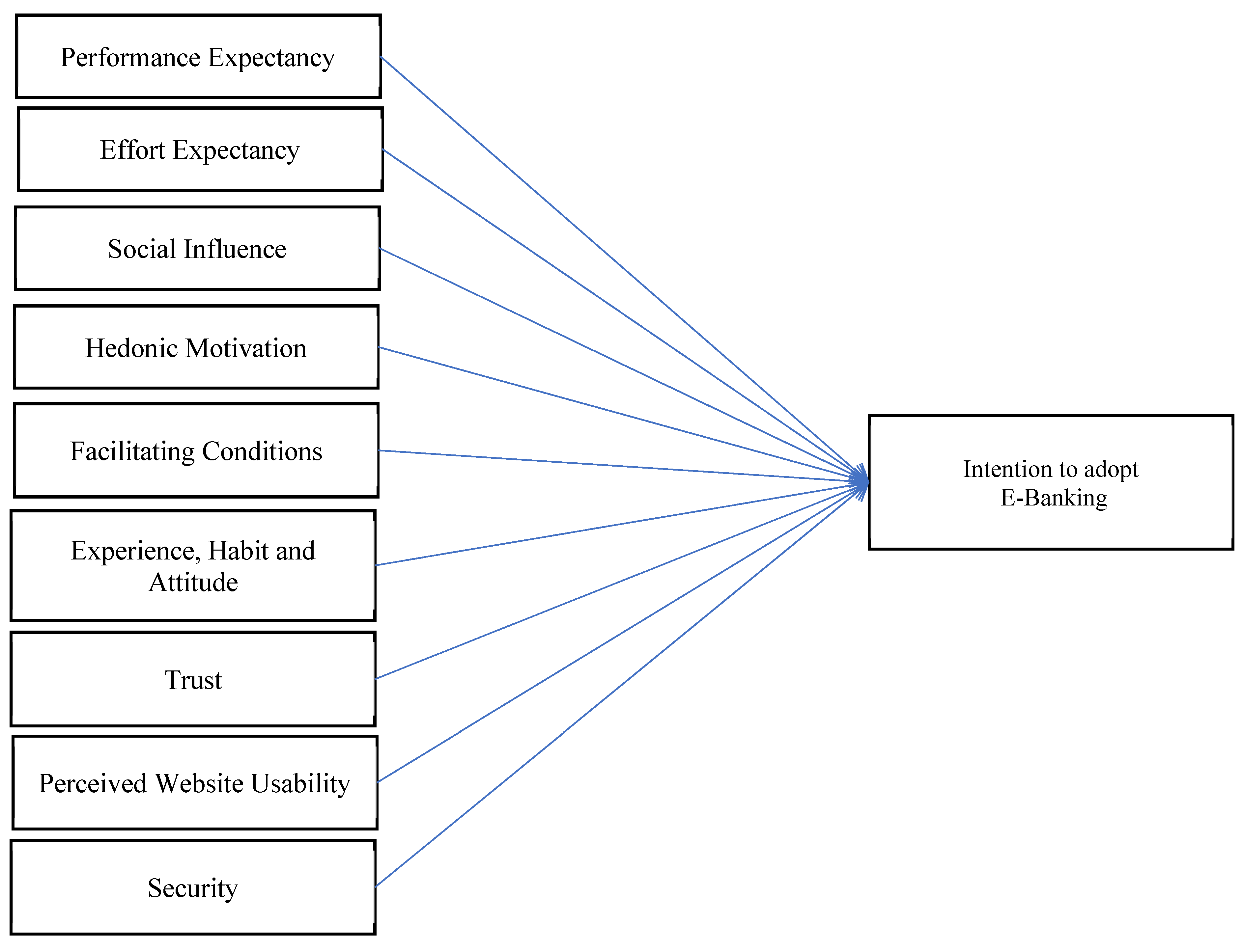

The study employed an experimental research design. The proposed antecedents to the behavioural intention to adopt e-banking are shown in Figure 1. For testing the instrument developed, we employed a 34 questions-based questionnaire, which we administered using a random sampling technique for data collection. The questionnaire was circulated among 700 prospective respondents, and we received 436 complete and valid responses eligible for final analysis. This provided us with a response rate of 62% and enabled us to generalise to the whole population, since the expected sample size to ensure 95% confidence is achieved with 384 complete questionnaires.

These responses were collected between June 2020 and December 2020. Therefore, the responses were better positioned to capture the respondents’ behavioural intentions during the pandemic. India has gone through many lockdowns, and the anxiety related to the pandemic might have influenced the behaviour and intentions towards IB. Although this can be seen as a limitation, we expected that the responses reflect and represent participants’ experiences on what most bank customers would prefer in order to adopt IB services especially during this period, since people had limited physical access to banks. We also expect this study to offer an opportunity to analyse how the shift in circumstances influences the adoption of technology and changes the dynamics of factors involved in IB usage.

All participants in this study were voluntary and were kept anonymous. Respondent’s responses to the questions in the questionnaire indicate the perception, opinion, and belief towards accepting and using IB

3.2. Measurement Model

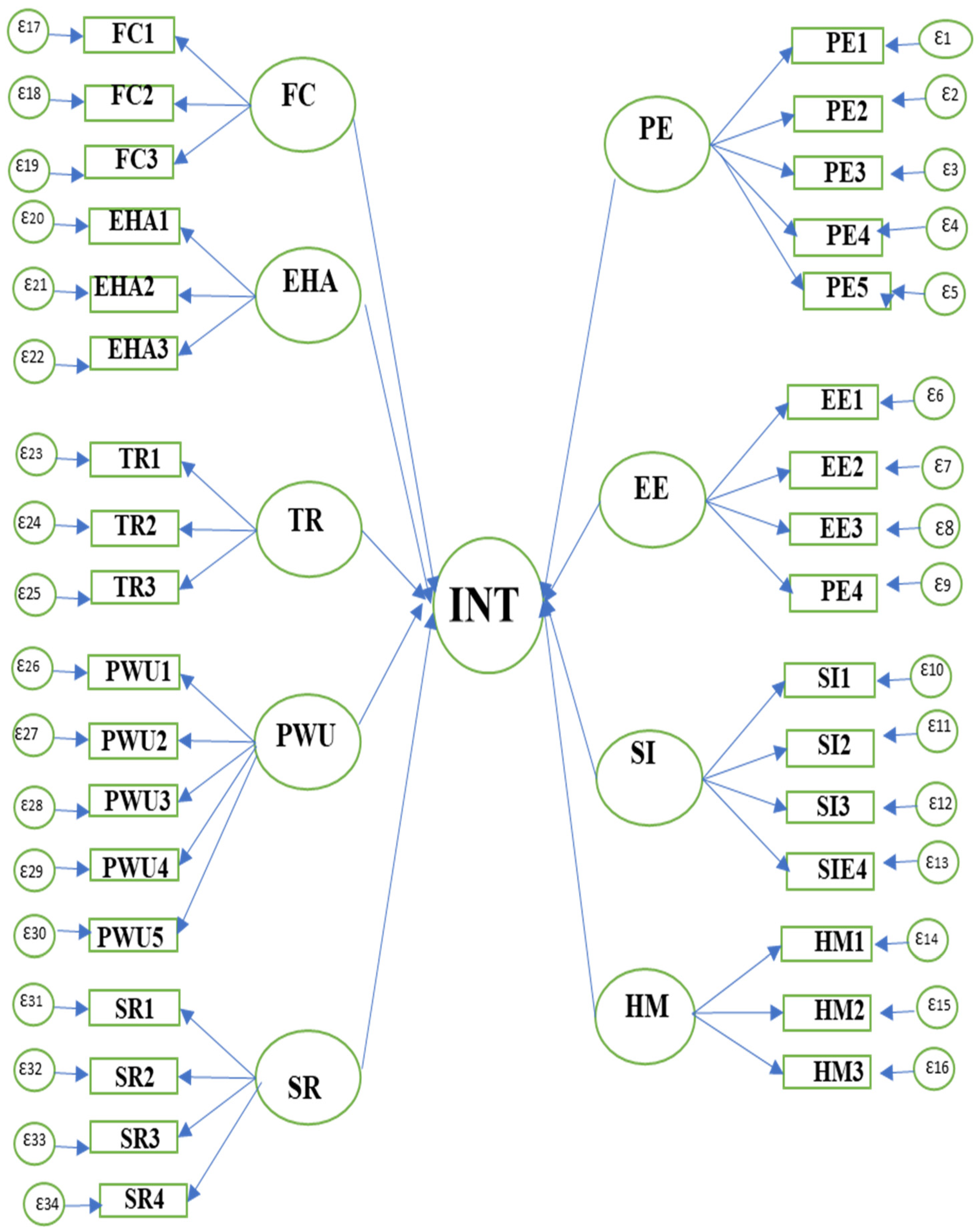

The measurement model used for the study is presented in Figure 2. All constructs are adapted from the literature provided above. Founding in the UTAUT model (Venkatesh et al. 2003; Venkatesh et al. 2012), and literature (as discussed in Section 2), a questionnaire with nine dimensions—Performance Expectancy (PE), Effort Expectancy (EE), Social Influence (SI), Hedonic Motivation (HM), Facilitating Conditions (FC), Experience, Habit and Attitude (EHA), Trust (TR), Perceived Website Usability (PWU), and Security and Reliability (SR)—has been used in the study. The list of sub-dimensions for each dimension is shown in Table 1. A five-point Likert scale is used in the questionnaire to quantify each construct’s items in the measurement model: 1 being strongly disagree and 5 being strongly agree. The questionnaire is self-administered by the authors using social networks and other communication means such as email, Zoom, Ms Teams, and the phone. A pilot test was carried out with 45 participants, and based on the results obtained from the pilot test, a few items were reviewed and modified.

3.3. Performance Expectancy

Performance Expectancy refers to how the customer perceives that using technology would benefit the carrying out of certain activities. It indicates the “extent to which the customer believes that using the system would increase the performance or output” (Davis 1989, p. 320). In addition, the perception of a system enhancing the performance (Davis et al. 1992) promotes the intention to use IB (Kapoor et al. 2015; Yu 2012; Lee 2009). Performance Efficiency leads to the acceptance or rejection of IB services.

Hypothesis 1 (H1).

Performance Expectancy influences the perceived intention to adopt IB positively.

3.4. Effort Expectancy

Effort Expectancy refers to how easy users would find it to adopt IB. If IB would be easy to use, the efforts involved in adopting IB would be low. Thus, the ease of adopting IB enhances the intentional adoption of IB. Mathieson (1991) suggests that lesser efforts would make the activity easy to carry out. Davis (1989) notes that perceived ease of use is how the customer would believe that using technology and systems would be. He notes that they need to perceive that it is easy and involves lesser effort. In addition, the service must be perceived as convenient to use and that the consumer can use it at no additional cost (Agarwal et al. 2009).

Hypothesis 2 (H2).

Effort Expectancy influences the perceived intention to adopt IB positively.

3.5. Social Influence

Social Influence refers to how the customer perceives that friends, family, and others in influential social circles should adopt IB. Fishbein et al. (1980) refer to social influence as “a person’s perception that most people who are important to him/her think s/he should or should not perform the behaviour in question”. Social influence indicates the social pressure from the individuals in the immediate circle, friends, and family. Studies such as those by Yu (2012) and Venkatesh and Zhang (2010), support the positive association between social influence and the adoption of IB.

Hypothesis 3 (H3).

Social Influence influences the perceived intention to adopt IB positively.

3.6. Hedonic Motivation

Hedonic Motivation refers to how customers feel enjoyment or pleasure while using technology. It has been indicated as having a significant role in technology adoption and acceptance (Brown and Venkatesh 2005). Hedonic Motivation indicates perceived enjoyment and influences technology adoption (Thong et al. 2006). Studies such as those by Venkatesh et al. (2012), Yang and Lee (2010), and Salimon et al. (2017) support the positive influence of Hedonic Motivation on the intention to adopt IB.

Hypothesis 4 (H4).

Hedonic Motivation influences the perceived intention to adopt IB positively.

3.7. Facilitating Conditions

Facilitating Conditions refers to how a person believes in support of the technical and organisational infrastructure (Venkatesh et al. 2003). Facilitating conditions require employing the latest technology to make use of IB. Having an advanced and updated system would facilitate the use of IB and positively influence the intention to use the services. Level of awareness (Smith 2006), knowledge and ease of using a computer (Wang et al. 2003), and easy access to a website (Gupta and Kamilla 2014) influence the adoption of IB. Having basic initial knowledge makes it comfortable to use the Internet for banking purposes and thus creates a conducive environment for individuals to adopt IB.

Hypothesis 5 (H5).

Facilitating Conditions influence the perceived intention to adopt IB positively.

3.8. Experience, Habit, and Attitude

Experience refers to the opportunity to use the technology, and habit indicates regular use of technology due to learning and change in behaviour (Limayem et al. 2007; Walker and Johnson 2005). Habits and experience of using IB are expected to positively influence the adoption of IB (Venkatesh et al. 2012). Attitude indicates feelings about performing an action or a target behaviour (Fishbein and Ajzen 1975; Walker and Johnson 2005). In addition, regular use is no indication of satisfied use (Walker and Johnson 2005). Habit changes the background of the accessible payment and reduces the obstacles or barriers in adopting IB.

Hypothesis 6 (H6).

Experience, Habit, and Attitude positively influence the perceived intention to adopt IB.

3.9. Trust

Trust is considered an important factor in explaining customers’ attitudes in the acceptance of IB (Suh and Han 2002). Low levels of trust hinder the adoption of IB, and lack of trust remains a barrier in the widespread adoption of IB (Yousafzai and Yani-de-Soriano 2012). Banks can build trust by providing Internet security, multiple authentication channels, and reliable transactions. Unfortunately, banks have not reached a point to achieve economies of scale via investments in security measures as the number of IB users in the Indian context is low. Studies such as Benamati et al. (2010), Suh and Han (2002), Wang et al. (2003), and Yousafzai and Yani-de-Soriano (2012) have supported the role of trust in influencing the adoption of IB.

Hypothesis 7 (H7).

Trust influences the perceived intention to adopt IB positively.

3.10. Perceived Website Usability

Perceived Website Usability refers to the extent to which a customer feels at ease, self-guiding, and free from mental hassle while using a website. Perceived Website Usability has been suggested to positively influence online banking. In addition, several studies by Abdullah et al. (2016), Alwan and Al-Zubi (2016), and Al-Sharafi et al. (2016) have indicated perceived ease of use to impact customer satisfaction. Perceived usability indirectly affects customer loyalty and leads to positive customer satisfaction (Casaló et al. 2008). Perceived usability of the website, its design, and content (Ling et al. 2016) have been suggested as a key driver for the adoption of IB.

Hypothesis 8 (H8).

Perceived Website Usability positively influences the intention to adopt IB.

3.11. Security and Reliability

Security refers to the lower probability of loss arising from fraud or a security breach while banking on the Internet (Lee 2009), therefore making IB more secure. It envelopes three root constructs: reliability, safety, and privacy (Ling et al. 2016; Polatoglu and Ekin 2001). Security enhances customer satisfaction, whereas Chiemeke et al. (2006) suggest that perceiving transactions security helps customers perceive the usefulness of IB. Subsequently, Költzsch (2006) noted that biometric technology enhances the authenticity of transactions and reduces the probability of fraud while establishing customer trust and facilitating banking. In addition, employing multi-factor authentication protects sensitive resources managed by services against attackers (Sinigaglia et al. 2020).

Hypothesis 9 (H9).

Security influences the perceived intention to adopt IB positively.

4. Analysis and Discussion

4.1. Sample

We received 437 valid responses, 55.73% of which were received from male participants and 44.26% of which were received from female participants. Most of the respondents (36.4%) were between the ages of 21 and 30 years. About 26% of respondents were below the age of 20 years, 15.8% of respondents were between the ages of 30 and 40 years, and 21.7% of respondents belonged to the age group of over 40 years. Nearly 50% of the respondents were coming from urban areas, 34.8% of the respondents were from a rural background, and approximately 8% of the respondents were from a semi-urban area (Table 2).

4.2. Reliability of Data

To test the reliability of data, we performed the Cronbach’s alpha for the whole questionnaire and analysed each of its dimensions. In addition, to determine the appropriateness of including each item in the questionnaire, McDonald’s omega and inter-item correlation for each construct were calculated and presented in Table 2. The constructs indicate no irregular behaviour of variability and central tendency. The observed mean value for all constructs ranges between 2.537 and 3.776 with a standard deviation between 0.061 and 0.478, which is indicative of reporting positive responses for most constructs considered. Additionally, Cronbach’s alpha value suggests a strong internal reliability. The values for Cronbach’s alpha resulted in a minimum of 0.730 and a maximum value of 0.868.

As indicated in Table 3, all latent constructs have shown adequate levels of composite reliability with a minimum value of 0.80. It can be observed that latent constructs PE and SI have higher values of CR. The AVE values for all latent constructs are greater than 0.50. Latent constructs, PE and PWU, have the highest AVE value, whereas SR and HM have the lowest values for AVE. In addition, the model is suitable with sufficient discriminant validity (see Table 4). Moreover, the factor loadings obtained indicate satisfactory loading of items on the latent variables.

4.3. Confirmatory Factor Analysis and Structural Equation Model

Then, we tested the measurement for the goodness of fit. The indices for the goodness of fit in the Confirmatory Factor Analysis (CFA) are presented in Table 5. Referring to the criteria followed by Kline (2005), the values obtained for different measures of goodness of fit suggest satisfactory results with GFI = 0.987, CFI = 0.900, TLI = 0.886, IFI = 0.902, NFI = 0.713, and RMSEA = 0.047.

Having established the instrument’s configuration from the literature and CFA, we apply the Structural Equation Modelling (SEM) to assess construct validity. The proposed measurement model (see Figure 1) includes all the items proposed by the literature and thus suggests nine constructs. Thus, the model has nine latent constructs: PE, defined by five items, EE, defined by four items), SI, defined by four items, Hedonic Motivation (HM), defined by three items, Facilitating Conditions (FC), defined by three items, Experience, Habit, and Attitude (EHA), defined by three items, Trust (TR), defined by three items, Perceive Website Usability (PWU), defined by five items, and Security and Reliability (SR), defined by four items. Thus, the model consists of 34 manifest variables or items and 34 error terms (from e01 to e34).

After specifying the model, the multivariate assumption is checked by estimating Mardia’s coefficient (see Table 5) (Bollen 1989). The model parameters are estimated through the ‘Maximum Likelihood (ML)’ procedure, as the ML procedure is considered an efficient and unbiased procedure if the assumption of multivariate normality is met. The results for Mardia’s coefficient indicate no red flags. Although the results for the Chi-square estimate are significant, the Chi-square estimate is inappropriate for large samples. Therefore, Levy et al. (2006) suggest analysing the absolute fit measures in addition to the Chi square (See Table 6). The main fit indices for the structural model lie within the threshold values such as GFI= 0.882, PGFI = 0.860, and RMSEA = 0.048 (see Table 7). Thus, the results suggest that the structural model fits data adequately.

After assessing the proposed measurement model for reliability and validity for measuring the latent variables and items through Confirmatory Factor Analysis, the structural model is assessed. The structural model fit indices indicate an adequate fit for the model. The path coefficients indicate the relationship strength between constructs (see Table 8). Referring to the hypothesis proposed in the study (see Section 2), we find that PE, HM, EHA, PWU, and SR have a positive influence on the ‘Intention to use online banking’. Therefore, our hypotheses H1, H4, H6, and H8 are supported. In contrast, the coefficient values for EE, SI, FC, and TR are not significant, and thus, our hypotheses H2, H3, H5, H7, and H9 are not supported (refer to Table 9).

These results demonstrate that customers and prospective customers would be encouraged to use and accept e-banking technology if it provided them with added value and an experience of satisfaction when using this technology. In addition, they need to perceive increasing marginal utility when using this technology, maybe by receiving some kind of award or discount for repeated use, in a way that people can experience satisfaction, value, and the urge to change their habits and attitude towards using technology. Policymakers and bank decisionmakers need to design interfaces and applications that are useable without much mental strain and that guarantee security and reliability.

It seems that Indian customers and prospective customers are not too concerned with what friends, family, and others in influential social circles do. Therefore, advertising and emphasis should not focus on peer influence. Nor are they concerned with matters of trust, convenience, or technical support. Maybe this is because trust, convenience, and technical support are already well provided.

5. Conclusions

The results show a covariate relationship between dimensions to IB and intention to adopt IB. The findings that PE, HM, EHA, PWU, and SR positively influence the intention to adopt IB, which suggests that policymakers and bankers should focus their attention on taking the necessary steps to enhance the website usability and hedonic pleasure while focusing on the performance and security and reliability of their services as key attributes of IB. Moreover, it is suggested that more attention should be placed on influencing the experience of customers/prospective customers and on understanding and influencing their habits and attitudes.

In addition, given that the results show that EE, SI, FC, and TR are not significant influencing factors of IB usage, it seems that Indians already find IB easy to use, perceive it as an effortless exercise, and believe that there are strong support systems and organisational infrastructures backing them. The adoption of IB by Indians is not influenced by society, friends, and family, and trust is not a motivating condition for such, since they already perceive it as a trustworthy exercise.

Banks are vital to the growth of any economy, especially a developing one such as India. Given the timing of this study, which took place during a pandemic, during which India passed through various lockdowns, giving them limited access to physical banking, the advantages of virtual banking and since, as noted above, India is an emerging economy and needs to grow its IB customer base, this study is vital for banks and policymakers alike, for their decision-making process on how to increase the number of Indians using e-banking services.

This study differs from others since it applies the UTAUT model on an emerging Asian country (India) at a time when the world is facing a pandemic, which is an unprecedented disruption of the norm and when people have to look for solutions to deliver and receive banking services with limited physical contact.

However, although this study is limited to India and the statements built around UTAUT, we believe that our findings can help bank decisionmakers and policymakers devise plans and strategies to enhance the use of IB by Indians.

Author Contributions

Conceptualisation, S.I. and K.S.; methodology, S.I. and S.G.; software, S.I. and S.G.; validation, S.G., S.I. and K.S.; formal analysis, S.I. and S.G.; investigation, S.G., S.I. and K.S.; resources, S.G., S.I. and K.S.; data curation, S.G., S.I. and K.S.; writing—original draft preparation, S.G., S.I. and K.S.; writing—review and editing, S.G., S.I. and K.S.; visualization, S.G., S.I. and K.S.; supervision, S.G.; project administration, S.G., S.I. and K.S. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

In India there is no requirement for prior ethical approval before contacting participants. Moreover, the participants are kept anonymous.

Informed Consent Statement

Informed consent was obtained from all subjects involved in the study.

Data Availability Statement

In this study, primary data have been collected by the authors through a field survey. The data supporting this study’s findings are available from the corresponding author upon reasonable request, and any shared data are absent.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Abdullah, Fazil, Rupert Ward, and Ejaz Ahmed. 2016. Investigating the influence of the most commonly used external variables of TAM on students’ Perceived Ease of Use (PEOU) and Perceived Usefulness (PU) of e-portfolios. Computers in Human Behavior 63: 75–90. [Google Scholar] [CrossRef]

- Aboobucker, Ilmudeen, and Yukun Bao. 2018. What obstruct customer acceptance of internet banking? Security and privacy, risk, trust and website usability and the role of moderators. The Journal of High Technology Management Research 29: 109–23. [Google Scholar] [CrossRef] [Green Version]

- Agarwal, Reeti, Sanjay Rastogi, and Ankit Mehrotra. 2009. Customers’ perspectives regarding e-banking in an emerging economy. Journal of Retailing and Consumer Services 16: 340–51. [Google Scholar] [CrossRef]

- Alalwan, Ali Abdallah, Yogesh K. Dwivedi, Nripendra P. Rana, and Raed Algharabat. 2018. Examining factors influencing Jordanian customers’ intentions and adoption of internet banking: Extending UTAUT2 with risk. Journal of Retailing and Consumer Services 40: 125–38. [Google Scholar] [CrossRef] [Green Version]

- AlQudah, Ayman Ahmed. 2014. Accepting Moodle by academic staff at the university of Jordan: Applying and extending tam in technical support factors. European Scientific Journal 10: 183–200. [Google Scholar]

- Al-Sharafi, A. Mohammed, R. Abdullah-Arshah, Qasim Alajmi, and A. T. Fadi Herzallah. 2016. Understanding online banking acceptance by jordanian customers: The effect of trust perceptions. Presented at 6th International Graduate Conference on Engineering, Science and Humanities (IGCESH), Universiti Teknologi Malaysia, Johor Bahru, Malaysia, August 15–17. [Google Scholar]

- Alwan, Hussein Ahmad, and Abdelhalim Issa Al-Zubi. 2016. Determinants of Internet Banking Adoption among Customers of Commercial Banks: An Empirical Study in the Jordanian Banking Sector. International Journal of Business and Management 11: 95. [Google Scholar] [CrossRef]

- Ang, Carmen. 2020. These Are the Countries Where Internet Access is Lowest. World Economic Forum. August 17. Available online: https://www.weforum.org/agenda/2020/08/internet-users-usage-countries-change-demographics/ (accessed on 12 December 2020).

- Arif, Imtiaz, Wajeeha Aslam, and Yujong Hwang. 2020. Barriers in adoption of internet banking: A structural equation modeling-Neural network approach. Technology in Society 61: 101231. [Google Scholar] [CrossRef]

- Banu, A. Meharaj, N. Shaik Mohamed, and Satyanarayana Parayitam. 2019. Online Banking and Customer Satisfaction: Evidence from India. Asia-Pacific Journal of Management Research and Innovation 15: 68–80. [Google Scholar] [CrossRef]

- Barrutia, José M., and Carmen Echebarria. 2005. The Internet and consumer power: The case of Spanish retail banking. Journal of Retailing and Consumer Services 12: 255–71. [Google Scholar] [CrossRef]

- Basuroy, Tanushree. 2022. Internet Penetration across India 2019, by State. Statista. Available online: https://www.statista.com/statistics/1115129/india-internet-penetration-by-state/ (accessed on 12 December 2020).

- Bauer, Keldon, and Scott E. Hein. 2006. The effect of heterogeneous risk on the early adoption of Internet banking technologies. Journal of Banking and Finance 30: 1713–25. [Google Scholar] [CrossRef]

- Benamati, John, Mark A. Serva, and Mark A. Fuller. 2010. The Productive Tension of Trust and Distrust: The Coexistence and Relative Role of Trust and Distrust in Online Banking. October 2010. Journal of Organizational Computing and Electronic Commerce 20: 328–46. [Google Scholar] [CrossRef]

- Bollen, Kenneth A. 1989. Structural Equations with Latent Variables. Hoboken: John Wiley & Sons. [Google Scholar] [CrossRef]

- Brown, Susan A., and Viswanath Venkatesh. 2005. Model of adoption of technology in households: A baseline model test and extension incorporating household life cycle. MIS Quarterly 29: 399–426. [Google Scholar] [CrossRef]

- Casaló, Luis V., Carlos Flavián, and Miguel Guinalíu. 2008. The Role of Satisfaction and Website Usability in Developing Customer Loyalty and Positive Word-of-Mouth in the e-Banking Services. International Journal of Bank Marketing 26: 399–417. [Google Scholar] [CrossRef]

- Cheng, T. C. Edwin, David Y. C. Lam, and Andy C. L. Yeung. 2006. Adoption of internet banking: An empirical study in Hong Kong. Decision Support Systems 42: 1558–72. [Google Scholar] [CrossRef] [Green Version]

- Chiemeke, S. C., A. E. Evwiekpaefe, and F. O. Chete. 2006. The adoption of Internet banking in Nigeria: An empirical investigation. Journal of Internet banking and Commerce 11: 1–10. [Google Scholar]

- Compeau, Deborah R., and Christopher A. Higgins. 1995. Computer self-efficacy: Development of a measure and initial test. MIS Quarterly 19: 189–211. [Google Scholar] [CrossRef] [Green Version]

- Daneshgadeh, Salva, and Sevgi Özkan Yıldırım. 2014. Empirical investigation of internet banking usage: The case of Turkey. Procedia Technology 16: 322–31. [Google Scholar] [CrossRef] [Green Version]

- Daniel, Elizabeth. 1999. Provision of electronic banking in the U.K. and the Republic of Ireland. International Journal of Bank Marketing 17: 72–83. [Google Scholar] [CrossRef]

- Davis, Fred D. 1989. Perceived usefulness, perceived ease of use, and user acceptance of information technology. MIS Quarterly 13: 319–40. [Google Scholar] [CrossRef] [Green Version]

- Davis, Fred D., Richard P. Bagozzi, and Paul R. Warshaw. 1992. Extrinsic and intrinsic motivation to use computers in the workplace 1. Journal of Applied Social Psychology 22: 1111–32. [Google Scholar] [CrossRef]

- Dianat, Iman, Pari Adeli, Mohammad Asgari Jafarabadi, and Mohammad Ali Karimi. 2019. User-centred web design, usability and user satisfaction: The case of online banking websites in Iran. Applied Ergonomics 81: 102892. [Google Scholar] [CrossRef] [PubMed]

- Durkin, Mark, Deirdre Jennings, Gwyneth Mulholland, and Stephen Worthington. 2008. Key influencers and inhibitors on adoption of the Internet for banking. Journal of Retailing and Consumer Services 15: 348–57. [Google Scholar] [CrossRef]

- Fishbein, Martin, and Icek Ajzen. 1975. Belief, Attitude, Intention, and Behavior: An Introduction to Theory and Research. Reading: Addison-Wesley. [Google Scholar]

- Fishbein, Martin, James Jaccard, Andrew R. Davidson, Icek Ajzen, and Barbara Loken. 1980. Predicting and understanding family planning behaviors. In Understanding Attitudes and Predicting Social Behavior. Hoboken: Prentice Hall. [Google Scholar]

- Gupta, Divya, and Usha Kamilla. 2014. Cyber Banking in India: A Cross-Sectional Analysis Using Structural Equation Model. IUP Journal of Bank Management 13: 47–63. [Google Scholar]

- Ingle, Arun, and Rajesdrasingh Pardeshi. 2012. Internet Banking in India: Challenges and Opportunities. IBMRD’s Journal of Management and Research 1: 13–18. [Google Scholar]

- Jiménez, José Ramón Zagalaz, and Inmaculada Aguiar Díaz. 2019. Educational level and Internet banking. Journal of Behavioral and Experimental Finance 22: 31–40. [Google Scholar] [CrossRef]

- Kapoor, Kawaljeet Kaur, Yogesh K. Dwivedi, and Michael D. Williams. 2015. Examining the role of three sets of innovation attributes for determining adoption of the interbank mobile payment service. Information Systems Frontiers 17: 1039–56. [Google Scholar] [CrossRef] [Green Version]

- Khalfan, Abdulwahed Mo Sh, Yaqoub S. Y. AlRefaei, and Majed Al-Hajery. 2006. Factors influencing the adoption of Internet banking in Oman: A descriptive case study analysis. International Journal of Financial Services Management 1: 155–72. [Google Scholar] [CrossRef]

- Kline, Rex B. 2005. Principles and Practice of Structural Equation Modelling, 2nd ed. New York: Guilford Press, ISBN 1593850751, 9781593850753. [Google Scholar]

- Költzsch, Gregor. 2006. Innovative methods to enhance transaction security of banking applications. Journal of Business Economics and Management 7: 243–49. [Google Scholar] [CrossRef] [Green Version]

- Lee, Ming-Chi. 2009. Factors influencing the adoption of internet banking: An integration of TAM and TPB with perceived risk and perceived benefit. Electronic Commerce Research and Applications 8: 130–41. [Google Scholar] [CrossRef]

- Levy, Kenneth N., Kevin B. Meehan, Kristen M. Kelly, Joseph S. Reynoso, Weber Michal, John F. Clarkin, and Otto F. Kernberg. 2006. Change in attachment patterns and reflective function in a randomized control trial of transference-focused psychotherapy for borderline personality disorder. Journal of Consulting and Clinical Psychology 74: 1027–40. [Google Scholar] [CrossRef] [PubMed]

- Liao, Shaoyi, Yuan Pu Shao, Huaiqing Wang, and Ada Chen. 1999. The adoption of virtual banking: An empirical study. International Journal of Information Management 19: 63–74. [Google Scholar] [CrossRef]

- Limayem, Moez, Sabine Gabriele Hirt, and Christy M. K. Cheung. 2007. How Habit Limits the Predictive Power of Intentions: The Case of I.S. Continuance. MIS Quarterly 31: 705–37. [Google Scholar] [CrossRef] [Green Version]

- Ling, Goh Mei, Yeo Sook Fern, Lim Kah Boon, and Tan Seng Huat. 2016. Understanding customer satisfaction of internet banking: A case study in Malacca. Procedia Economics and Finance 37: 80–85. [Google Scholar] [CrossRef] [Green Version]

- Mathieson, Kieran. 1991. Predicting user intention: Comparing the technology acceptance model with the theory of planned behaviour. Information Systems Research 2: 173–91. [Google Scholar] [CrossRef]

- Nasri, Wadie, and Lanouar Charfeddine. 2012. Factors affecting the adoption of Internet banking in Tunisia: An integration theory of acceptance model and theory of planned behaviour. The Journal of High Technology Management Research 23: 1–14. [Google Scholar] [CrossRef]

- Polatoglu, Vichuda Nui, and Serap Ekin. 2001. An empirical investigation of the Turkish consumers’ acceptance of Internet banking services. The International Journal of Bank Marketing 19: 156–65. [Google Scholar] [CrossRef]

- Rawashdeh, Awni. 2015. Factors affecting adoption of internet banking in Jordan: Chartered accountant’s perspective. International Journal of Bank Marketing 33: 510–29. [Google Scholar] [CrossRef]

- Rodrigues, Luís Filipe, Carlos J. Costa, and Abílio Oliveira. 2017. How does the web game design influence the behaviour of e-banking users? Computers in Human Behavior 74: 163–74. [Google Scholar] [CrossRef]

- Salimon, Maruf Gbadebo, Rushami Zien Bin Yusoff, and Sany Sanuri Mohd Mokhtar. 2017. The mediating role of hedonic motivation on the relationship between adoption of e-banking and its determinants. International Journal of Bank Marketing 35: 558–82. [Google Scholar] [CrossRef]

- Sharma, Rashmini, Gurmeet Singh, and Shavneet Sharma. 2020. Modelling internet banking adoption in Fiji: A developing country perspective. International Journal of Information Management 53: 102–16. [Google Scholar] [CrossRef]

- Shih, Ya-Yueh, and Kwoting Fang. 2004. The use of a decomposed theory of planned behaviour to study Internet banking in Taiwan. Internet Research-Electronic Networking Applications And Policy 14: 213–23. [Google Scholar] [CrossRef] [Green Version]

- Shih, Ya-Yueh, and Kwoting Fang. 2006. Effects of network quality attribute on customer adoption intentions of Internet banking. Total Quality Management 17: 61–77. [Google Scholar] [CrossRef]

- Sinigaglia, Federico, Roberto Carbone, Gabriele Costa, and Nicola Zannone. 2020. A survey on multi-factor authentication for online banking in the wild. Computers and Security 95: 101745. [Google Scholar] [CrossRef]

- Smith, Alan D. 2006. Exploring security and comfort issues associated with online banking. International Journal of Electronic Finance 1: 18–48. [Google Scholar] [CrossRef]

- Smriti, Ani, and Rajesh Kumar. 2021. Present status of e-banking in India: Challenges and opportunities. International Journal of Creative Research Thoughts (IJCRT). 9. Available online: www.ijcrt.org (accessed on 20 December 2021).

- Srivastava, Rajesh Kumar. 2007. Customer’s perception on usage of internet banking. Innovative Marketing 3: 67–77. [Google Scholar]

- Statista. 2021. Status of Online Banking in India 2020. Statista Research Department, July 12. Available online: https://www.statista.com/statistics/1249581/india-status-of-online-banking-adoptio/ (accessed on 20 December 2021).

- Suh, Bomil, and Ingoo Han. 2002. Effect of trust on customer acceptance of Internet banking. Electronic Commerce Research and Applications 1: 247–63. [Google Scholar] [CrossRef]

- Tang, Jiliang, and Huan Liu. 2015. Trust in social media. Synthesis Lectures on Information Security, Privacy, and Trust 10: 1–129. [Google Scholar] [CrossRef]

- Thong, James, Se-Joon Hong, and Kar Yan Tam. 2006. The effects of post-adoption beliefs on the expectation-confirmation model for information technology continuance. International Journal of Human-computer Studies 64: 799–810. [Google Scholar] [CrossRef]

- Venkatesh, Viswanath, and Fred D. Davis. 2000. A theoretical extension of the technology acceptance model: Four longitudinal field studies. Management Science 46: 186–204. [Google Scholar] [CrossRef] [Green Version]

- Venkatesh, Viswanath, and Xiaojun Zhang. 2010. Unified theory of acceptance and use of technology: U.S. vs. China. Journal of Global Information Technology Management 13: 5–27. [Google Scholar] [CrossRef]

- Venkatesh, Viswanath, James Y. L. Thong, and Xin Xu. 2012. Consumer acceptance and use of information technology: Extending the unified theory of acceptance and use of technology. MIS Quarterly 36: 157–78. [Google Scholar] [CrossRef] [Green Version]

- Venkatesh, Viswanath, Michael G. Morris, Gordon B. Davis, and Fred D. Davis. 2003. User acceptance of information technology: Toward a unified view. MIS Quarterly 27: 425–78. [Google Scholar] [CrossRef] [Green Version]

- Venkatesh, Viswanath. 2000. Determinants of perceived ease of use: Integrating control, intrinsic motivation, and emotion into the technology acceptance model. Information Systems Research 11: 342–65. [Google Scholar] [CrossRef] [Green Version]

- Walker, Rhett H., and Lester W. Johnson. 2005. Towards understanding attitudes of consumers who use internet banking services. Journal of Financial Services Marketing 10: 84–94. [Google Scholar] [CrossRef]

- Wang, Victoria, Harrison Nnaji, and Jeyong Jung. 2020. Internet banking in Nigeria: Cyber security breaches, practices and capability. International Journal of Law, Crime and Justice 62: 100415. [Google Scholar] [CrossRef]

- Wang, Yi-Shun, Yu-Min Wang, Hsin-Hui Lin, and Tzung-I. Tang. 2003. Determinants of user acceptance of Internet banking: An empirical study. International Journal of Service Industry Management 14: 501–19. [Google Scholar] [CrossRef]

- Yang, Kiseol, and Hyun-Joo Lee. 2010. Gender differences in using mobile data services: Utilitarian and hedonic value approaches. Journal of Research in Interactive Marketing 4: 142–56. [Google Scholar] [CrossRef]

- Yasin, Mahmoud, Francisco Liébana-Cabanillas, Lucia Porcu, and Rasem N. Kayed. 2020. The role of customer online brand experience in customers’ intention to forward online company-generated content: The case of the Islamic online banking sector in Palestine. Journal of Retailing and Consumer Services 52: 101902. [Google Scholar] [CrossRef]

- Yousafzai, Shumaila, and Mirella Yani-de-Soriano. 2012. Understanding customer-specific factors underpinning internet banking adoption. International Journal of Bank Marketing 30: 60–81. [Google Scholar] [CrossRef]

- Yu, Chian-Son. 2012. Factors affecting individuals to adopt mobile banking: Empirical evidence from the UTAUT model. Journal of Electronic Commerce Research 13: 104. [Google Scholar]

- YuSheng, Kong, and Masud Ibrahim. 2019. Service innovation, service delivery and customer satisfaction and loyalty in the banking sector of Ghana. International Journal of Bank Marketing 37: 1215–33. [Google Scholar] [CrossRef]

Figure 1.

Antecedents of behavioural intention to adopt e-banking (source: authors’ compilation).

Figure 2.

Measurement model (source: authors’ compilation).

{kind=link}

{kind=link}

Table 1.

List of latent constructs and items included in each latent construct.

| Latent Construct | Items/Sub Dimensions |

|---|---|

| Performance Expectancy (PE) | |

| Manage my money (PE1) | |

| Record my finances (PE2) | |

| No need to visit traditional banks (PE3) | |

| Save time paying bills (PE4) | |

| Feels improvement in the way of carrying transactions (PE5) | |

| Effort Expectancy (EE) | |

| Easy to use (EE1) | |

| The system is flexible to interact (EE2) | |

| Saves time and effort (EE3) | |

| Saves the cost of visiting branch office/Internet data is cheaper (EE4) | |

| Social Influence (SI) | |

| Friends suggest that I should use the service (SI1) | |

| Friends/family use IB (SI2) | |

| Co-workers support and suggest IB (SI3) | |

| Indicate that I am updated with technology (SI4) | |

| Hedonic Motivation (HM) | |

| It feels fun/pleasure with IB (HM1) | |

| More like gaming (HM2) | |

| It is child’s play (HM3) | |

| Facilitating Conditions (FC) | |

| Bank provides IB complementary (FC1) | |

| Have knowledge and awareness (FC2) | |

| Instructions are easy to read/understand (FC3) | |

| Experience, Habit and Attitude (EHA) | |

| Uses Internet for carrying out other financial transactions also (EHA1) | |

| I have been using IB for more than 1 year (EHA2) | |

| Experience of using IB suits my lifestyle (EHA3) | |

| Trust (TR) | |

| Bank protects my personal information and privacy (TR1) | |

| Transactions are secure, as the bank has enough anti-theft/fraud system in place (TR2) | |

| Account information is secure (TR3) | |

| Perceived Website Usability (PWU) | |

| Information on the website is easily available (PWU1) | |

| Visually appealing (PWU2) | |

| Steps are easily indicated (PWU3) | |

| Website labels are easy to understand (PWU4) | |

| Allows me to interact to receive tailored information (PWU5) | |

| Security and Reliability (SR) | |

| The probability of fraud or loss is low with my bank’s IB service (SR1) | |

| Uses advanced techniques to secure transactions (SR2) | |

| A true and fair description of products (SR3) | |

| The system generates the same response each time (SR4) |

Source: authors’ compilation.

Table 2.

Demographics.

| Demographic | Sample |

|---|---|

| Gender | Percentage (Number) |

| Male | 243 (55.73%) |

| Female | 193 (44.26%) |

| Age Group of Respondents | |

| Less than 20 years | 113 (25.92%) |

| Greater than 20 years and less than 30 years | 159 (36.47%) |

| Greater than 30 years and less than 40 years | 69 (15.83%) |

| Greater than 40 years | 95 (21.78%) |

| Regional Background | |

| Urban area | 221 (50%) |

| Rural area | 152 (34.8%) |

| Semi-urban area | 63 (8.25%) |

Source: authors’ compilation.

Table 3.

Internal reliability results.

| Latent Variable | Mean | Standard Deviation | McDonald’s Omega | Cronbach’s Alpha | Average Inter Item Correlation |

|---|---|---|---|---|---|

| PE | 3.072 | 0.478 | 0.813 | 0.811 | 0.463 |

| EE | 3.613 | 0.221 | 0.827 | 0.825 | 0.544 |

| SI | 2.585 | 0.125 | 0.807 | 0.804 | 0.508 |

| HM | 3.287 | 1.233 | 0.888 | 0.884 | 0.423 |

| FC | 2.537 | 0.061 | 0.751 | 0.733 | 0.486 |

| EHA | 3.093 | 0.337 | 0.776 | 0.773 | 0.410 |

| TR | 3.127 | 0.086 | 0.795 | 0.793 | 0.429 |

| PWU | 3.058 | 0.219 | 0.869 | 0.868 | 0.569 |

| SR | 3.776 | 0.144 | 0.738 | 0.730 | 0.402 |

| Complete Instrument | 3.080 | 0.448 | 0.775 | 0.770 | 0.157 |

Source: authors’ compilation.

Table 4.

Results for measurement model.

| Latent Variable | Items | Loading | CR | AVE |

|---|---|---|---|---|

| PE | PE1 | 0.979 | 0.9575 | −0.819 |

| PE2 | 0.960 | |||

| PE3 | 0.885 | |||

| PE4 | 0.785 | |||

| PE5 | 0.904 | |||

| EE | EE1 | 0.818 | 0.9126 | 0.7248 |

| EE2 | 0.758 | |||

| EE3 | 0.973 | |||

| EE4 | 0.842 | |||

| SI | SI1 | 0.977 | 0.9352 | 0.7846 |

| SI2 | 0.950 | |||

| SI3 | 0.808 | |||

| SI4 | 0.793 | |||

| HM | HM1 | 0.706 | 0.8015 | 0.574 |

| HM2 | 0.725 | |||

| HM3 | 0.837 | |||

| FC | FC1 | 0.723 | 0.8150 | 0.596 |

| FC2 | 0.734 | |||

| FC3 | 0.853 | |||

| EHA | EHA1 | 0.742 | 0.838 | 0.634 |

| EHA2 | 0.848 | |||

| EHA3 | 0.796 | |||

| TR | TR1 | 0.986 | 0.923 | 0.801 |

| TR2 | 0.868 | |||

| TR3 | 0.824 | |||

| PWU | PWU1 | 0.953 | 0.943 | 0.807 |

| PWU2 | 0.854 | |||

| PWU3 | 0.975 | |||

| PWU4 | 0.800 | |||

| SR | SR1 | 0.904 | 0.802 | 0.511 |

| SR2 | 0.724 | |||

| SR3 | 0.605 | |||

| SR4 | 0.583 |

Source: authors’ compilation.

Table 5.

Results of discriminant validity.

| PE | EE | SI | HM | FC | EHA | TR | PWU | SR | |

|---|---|---|---|---|---|---|---|---|---|

| PE | 0.904 | ||||||||

| EE | 0.030 | 0.851 | |||||||

| SI | −0.035 | 0.301 | 0.885 | ||||||

| HM | −0.004 | 0.004 | −0.011 | 0.757 | |||||

| FC | 0.018 | −0.004 | 0.015 | 0.026 | 0.772 | ||||

| EHA | −0.162 | −0.094 | −0.006 | −0.062 | 0.007 | 0.796 | |||

| TR | 0.053 | 0.109 | −0.023 | 0.002 | −0.026 | −0.013 | 0.894 | ||

| PWU | 0.216 | 0.054 | 0.028 | 0.133 | −0.036 | −0.189 | −0.087 | 0.898 | |

| SR | −0.296 | −0.029 | 0.022 | 0.102 | −0.027 | 0.164 | −0.033 | −0.069 | 0.714 |

Source: authors’ compilation.

Table 6.

Fit indices for the measurement model.

| Chi-Square Test | ||||

|---|---|---|---|---|

| Model | Chi Square | df | p-Value | |

| Baseline Model | 5200.874 | 561 | ||

| Factor Model | 953.719 | 490 | 0.0000 | |

| Fit Indices | ||||

| Index | Recommended level | Model values obtained | ||

| Bollen’s Incremental Fit Index (IFI) | >0.90 | 0.902 | ||

| Tucker–Lewis Index (TLI) | 0.886 | |||

| The Goodness of Fit Index (GFI) | 0.987 | |||

| Comparative Fit Index (CFI) | 0.900 | |||

| Parsimony Normed Fit Index (PNFI) | >0.70 | 0.713 | ||

| Root Mean Square Error of Approximation (RMSEA) | <0.60 | 0.047 | ||

| RMSEA 90% CI lower bound | 0.042 | |||

| RMSEA 90% CI upper bound | 0.051 | |||

| Hoelter’s critical N (α = 0.05) | >200 | 249.056 | ||

| Hoelter’s critical N (α = 0.01) | 259.639 | |||

Source: authors’ compilation.

Table 7.

Mardia’s coefficient results for multivariate normality.

| Mardia’s Coefficient | Coefficient | z-Statistic | χ2 Value | df | p-Value |

|---|---|---|---|---|---|

| Skewness | 129.253 | 9392.416 | 7140.000 | 0.0000 | |

| Kurtosis | 1293.983 | 14.767 | 0.0000 |

Source: authors’ compilation.

Table 8.

Model fit indices for structural model.

| Index | Value |

|---|---|

| χ2 (p-value) | 1001.491 (0.000) |

| Hoelter Critical N (CN) alpha = 0.05 | 242.720 |

| Hoelter Critical N (CN) alpha = 0.01 | 252.911 |

| Goodness of Fit Index (GFI) | 0.882 |

| Parsimony Goodness of Fit Index (GFI) | 0.860 |

| RMSEA | 0.048 |

| Upper 90% CI | 0.052 |

| Lower 90% CI | 0.043 |

| p-value RMSEA <= 0.05 | 0.799 |

Source: authors’ compilation.

Table 9.

Hypothesis testing results for the structural model (source: authors’ compilation).

| Hypothesis | Path | Coefficients | p-Value | Conclusion |

|---|---|---|---|---|

| H1 | PE→INT | 0.630 | 0.0000 | Supported |

| H2 | EE→INT | 0.144 | 0.068 | Not supported |

| H3 | SI→INT | 0.017 | 0.819 | Not supported |

| H4 | HM→INT | −0.281 | 0.004 | Supported |

| H5 | FC→INT | −0.012 | 0.883 | Not supported |

| H6 | EHA→INT | −0.393 | 0.000 | Supported |

| H7 | TRA→INT | 0.077 | 0.350 | Not supported |

| H8 | PWU→INT | 0.295 | 0.001 | Supported |

| H9 | SR→INT | 0.234 | 0.090 | Not supported |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Inder, S.; Sood, K.; Grima, S. Antecedents of Behavioural Intention to Adopt Internet Banking Using Structural Equation Modelling. J. Risk Financial Manag. 2022, 15, 157. https://doi.org/10.3390/jrfm15040157

AMA Style

Inder S, Sood K, Grima S. Antecedents of Behavioural Intention to Adopt Internet Banking Using Structural Equation Modelling. Journal of Risk and Financial Management. 2022; 15(4):157. https://doi.org/10.3390/jrfm15040157

Chicago/Turabian StyleInder, Shivani, Kiran Sood, and Simon Grima. 2022. "Antecedents of Behavioural Intention to Adopt Internet Banking Using Structural Equation Modelling" Journal of Risk and Financial Management 15, no. 4: 157. https://doi.org/10.3390/jrfm15040157