FinTechs, BigTechs and Banks—When Cooperation and When Competition?

Department of Banking and Financial Markets, Faculty of Finance, University of Economics in Katowice, ul. 1 Maja 50, 40-287 Katowice, Poland

J. Risk Financial Manag. 2021, 14(12), 614; https://doi.org/10.3390/jrfm14120614

Submission received: 30 October 2021

/

Revised: 7 December 2021

/

Accepted: 14 December 2021

/

Published: 18 December 2021

(This article belongs to the Special Issue FinTech and the Future of Finance)

Abstract

:While there is a fast-growing number of studies on FinTech, the relationships between technology companies and banks have received only limited attention in the research literature. Most of the studies on FinTech-bank interactions conducted so far address the questions: why banks collaborate with FinTechs (reasons) and how they do it (forms of cooperation), whereas this paper aims at clarifying when the most likely form of their interaction is cooperation and when competition. To cover this cognitive gap, the conceptual framework to help explain which factors affect the type of interactions between technology companies and banks is presented in this paper. Based on extensive literature review and using the market-based approach, the external factors of the market position of banks and technology companies were examined. It was found that this position and therefore the basic type of interaction depends on the adoption level of FinTechs and BigTechs in individual countries/regions. The adoption of FinTechs and BigTechs turned out to be higher in EMDEs and lower in AEs, which makes it more likely that in the first group of countries tech companies would tend to serve as banks’ competitors, whereas in the second group they would rather collaborate with banks or choose the coopetition strategy. When analyzing internal factors, the resource-based approach and a slightly modified IO theory were applied. In this part, the strategic tool which enables the assessment of the extent to which assets, skills, and features of FinTechs, BigTechs and banks are complementary (which gives the rationale for cooperation) or substitutable (which gives the rationale for competition) was proposed. This study is a critical analysis based on desk research, that contributes to the existing literature by (1) providing a narrow definition of FinTech representing the subjective/institutional approach, (2) considering separately FinTechs and BigTechs, and (3) proposing the strategic tool which helps to assess comparative advantages of banks, FinTechs and BigTechs, and thus makes it easier to choose the most appropriate type of their interaction.

1. Introduction

The emergence of Fintech has been one of the most relevant drivers of change in the financial services industry in recent years. According to the most common definition of Fintech in the literature, it is “technologically-enabled innovation in financial services that could result in new business models, applications, processes or products with an associated material effect on the provision of financial services” (FSB 2017a). This approach to define FinTech can be described as functional and broad as it may be applied to both traditional financial service providers and new entrants. However, using this approach, it is not possible to examine the consequences of expansion of technology companies into finance, including their possible interactions with incumbents.

Therefore, for the purposes of this paper, a narrow definition of FinTech representing the subjective or institutional approach will be proposed. According to this definition, FinTech is a separate sector of the financial services industry consisting of entities other than traditional financial service providers, which use cutting-edge technology to provide existing financial services more effectively and create new ones, that enables new value to be delivered to customers. This approach allows traditional financial service providers (banks and other financial institutions) to be excluded from the FinTech sector.

However, the sector of technology companies is not homogeneous. There is a consensus that FinTech sector includes young, small technology companies (often start-ups), focusing on developing innovative products and/or process in the financial services industry, with special emphasis on improving user experience (UX). Furthermore, a specific group of technology companies entering into finance has been distinguished recently, referred to as “BigTechs.” It is debated to what extent they can be included in the FinTech sector, since their key activities are not related to the provision of financial services but rather to cutting-edge technology, which is used by them in online sales of goods and services as well as in advertising (FSB 2019a). In contrast with FinTechs, BigTechs can be defined as large technology companies with high market capitalization, well-recognized brands and established market position, usually operating on a global or international scale, which offer mainly non-financial goods and services (both digital and traditional) via digital platforms. Their business model is based on three key elements, which reinforce each other: data analytics, network effects and linked activities (including offering financial services).

Although both FinTechs and BigTechs rely heavily on digital technology and represent technology-enabled innovation business model (but in fact very different), taking into account the significant differences between them, BigTechs and FinTechs should be considered separately. This distinction is justified as it has been assumed in the paper that the interactions of each of these groups with banks are different. The rationale behind this assumption is that companies concerned substantively differ in terms of their size, scale of activity, specific features and the extent to which their assets, skills, and features complement those of banks.

The literature on FinTech distinguishes three main streams of research. A number of studies, especially earlier ones, attempted to define the phenomenon known as FinTech (Arner et al. 2015; Jun and Yeo 2016; Zavolokina et al. 2016; Schueffel 2016; FSB 2017a; Harasim and Mitręga-Niestrój 2018), however, it has not yet led to the adoption of a broadly accepted and applied definition. The second discussed topic is the strengths and weaknesses of FinTechs and BigTechs and their most visible expansion areas (Dorfleitner et al. 2017; Claessens et al. 2018; Jagtiani and Lemieux 2018; Hau et al. 2019; BIS 2019; FSB 2019b; OECD 2020; Harasim 2021) as well as related competition issues (Fraile et al. 2018). And finally, as FinTechs and BigTechs operate in a highly regulated environment, such as the financial services industry, many studies address the regulatory arbitrage between incumbents and technology companies, as well as various risks posed by their expansion (Arner et al. 2015; Philippon 2016; Buchak et al. 2017; FSB 2017a; Braggion et al. 2018; BIS 2018; Padilla 2020).

To date relationships between technology companies and incumbents, and banks in particular, have received rather limited attention in the research literature. Bömer and Maxin (2018) correctly noted that these relations deserve attention due to special features of the financial services industry characterized by the increase in regulation requirements after the financial crisis of 2008, long-term relationships between banks and their clients based on trust and loyalty as well as fast technology development by the mid-2000s resulting in new products, processes, and business models.

Previous research primarily focused on cooperation between FinTechs and banks rather than competition from BigTechs or coopetition (which means cooperating with a competitor in a way that benefits both parties). The reasons behind the bank-FinTech collaboration and its benefits gained the greatest interest, as along with the types of the mutual interactions.

This study is a critical analysis based predominantly on desk research. An in-depth review of the literature has been allowed to assume that both external and internal factors influence the choice of a specific form of interaction. The adoption level of FinTechs and BigTechs across countries/regions has been considered the most important in the former case and the extent to which the resources, skills, and features of each group of technology companies and those of banks are complementary (or substitutable) in the case of the latter. As a consequence, two following research questions enhancing the understanding of interactions between FinTechs, BigTechs, and banks were posed:

- Which external factors impact the FinTech and BigTech adoption level across markets and how does it affect technology companies-banks collaborative space?

- How do complementarity and substitutability of assets, skills, and features of large banks, FinTechs, and BigTechs affect the forms of interactions between them?

In addition to identifying external and internal factors affecting the relationships between FinTechs, BigTechs, and banks, the ultimate objective of the paper is to propose a tool that may be helpful in choosing a specific form of interaction.

To achieve the objective pursued and address the research questions posed, both market-based and resource-based approach to gaining competitive advantage were used, as well as slightly modified IO theory. Although these approaches are well-known in the literature, a comprehensive approach using this perspective is relatively rare in the literature. Thus, this approach is original. Additionally, while the research conducted so far has made it possible to determine why banks collaborate with FinTechs (reasons) and how they do it (forms of cooperation) this paper attempts to answer a different question: when the most likely form of their interaction is cooperation and when it is competition or coopetition. Therefore, answering the research questions enabled the author to fill an important gap in the existing literature.

The remainder of the paper is organized as follows: after discussing the literature on banks-FinTechs collaboration (Section 2), Section 3 reviews external drivers of FinTech and BigTech adoption, their impact on market position of banks and technology companies as well as on general form of mutual interactions. Section 4 compares the assets, skills, and features of FinTechs, BigTechs, and banks using the proposed strategic tool to determine the most likely form of their interaction. Section 5 includes discussion on the outcomes and the last section concludes the paper.

2. Literature Review

Initially, the literature on the entry of FinTechs in the financial sector referred to them as “potential disruptors” and the prevailing view was that their expansion could cause dramatic changes in financial markets (Jakšič and Marinč 2015). A similar view was expressed by other researchers, including Lacasse et al. (2016), who emphasized that the products offered by FinTechs meet customer expectations in a better way or even exceed them. Stulz (2019) pointed out that both FinTechs and BigTechs benefit from uneven playing field—as they are less regulated than banks, the latter may lose their comparative advantage over them. Moreover, a number of surveys involving banks showed that they consider FinTechs as a severe threat that could put their business at risk (Bunea et al. 2016; EBA 2018).

A different viewpoint on this issue was represented by Burgmaier and Hüthing (2015) as well as Kalmykova and Ryabova (2016) who emphasized that it would be better for FinTechs and incumbents to cooperate than to compete. According to McWaters and Galaski (2017), even though FinTechs had successfully led innovation efforts and raised customer expectations via innovations, customers’ willingness to switch away from incumbents did not meet expectations, as the costs of switching and consumer inertia are high. Meanwhile, incumbents have been adapting to FinTech firms’ innovations.

Recently, a growing number of studies have examined the relationship between banks, FinTechs, and BigTechs, but most of them dealt with their possible general strategic responses (Stulz 2019; FSB 2019a; OECD 2020) as well as new business models, such as neo-bank (challenger bank), distributed bank, relegated bank (BIS 2018). Still, the literature examining the cooperation between banks and technology companies is relatively scarce. The existing studies on this subject can be broken down into two main streams. The first one concerns the premises/reasons for undertaking cooperation between banks and FinTechs along with its benefits, and the second—their scope, areas and the forms it can take.

Researchers focusing on the reasons for cooperation between banks and technology companies rather took banks’ perspective in terms of their innovation goals as well as the incumbent’s screening process (e.g., Corea 2015; Buchak et al. 2017; Bodek and Matinjan 2017; Maxin 2018). In contrast with this approach, Bömer and Maxin (2018) took FinTechs’ point of view and assumed that FinTechs require a bank to enter the market. At the same time, they can also strive for either increasing profits or developing new products. There is a growing body of evidence that both banks and technology companies benefit from cooperation. According to EBA (2018) study, banks with their expanded customer base have been effective distributors of FinTech products. In line with this, Brummer and Yadaw (2019) believe that the complementarity of FinTech products and services in relation to banking products and access to the customer base of banks enabled them to create innovative supply chains for FinTech products. Bömer and Maxin (2018), in turn, noted that because obtaining a license is very difficult and expensive task for start-ups, banks often allow FinTechs to create products that include licensed banking products (e.g., a current account).

The second stream of research focuses on the scope, areas and the forms of cooperation between banks and Fintechs. Brummer and Yadaw (2019) showed that incumbents may be involved in funding FinTech projects serving as incubators, putting young start-ups through their paces and offering pathways to partnership. Another multinational study conducted by Hornuf et al. (2018) revealed that the majority of banks choose non-aggressive strategies toward FinTechs. Using hand-collected data covering the largest banks in Canada, France, Germany, and the United Kingdom, they found that banks are significantly more likely to form alliances with FinTechs if they pursue a well-defined digital strategy and/or employ a Chief Digital Officer. They also discovered that large, listed universal banks are more prone to establishing alliances with FinTechs compared to smaller, unlisted, specialized banks. This is consistent with the results of EBA (2018) survey which revealed that the largest European banks also prefer to form partnerships with FinTechs; however, almost 3/4 of them have made capital investments in FinTechs through venture capital funds, or through setting up digital funds.

3. Results

3.1. External Drivers of Fintech Adoption—Cross-Country Differences

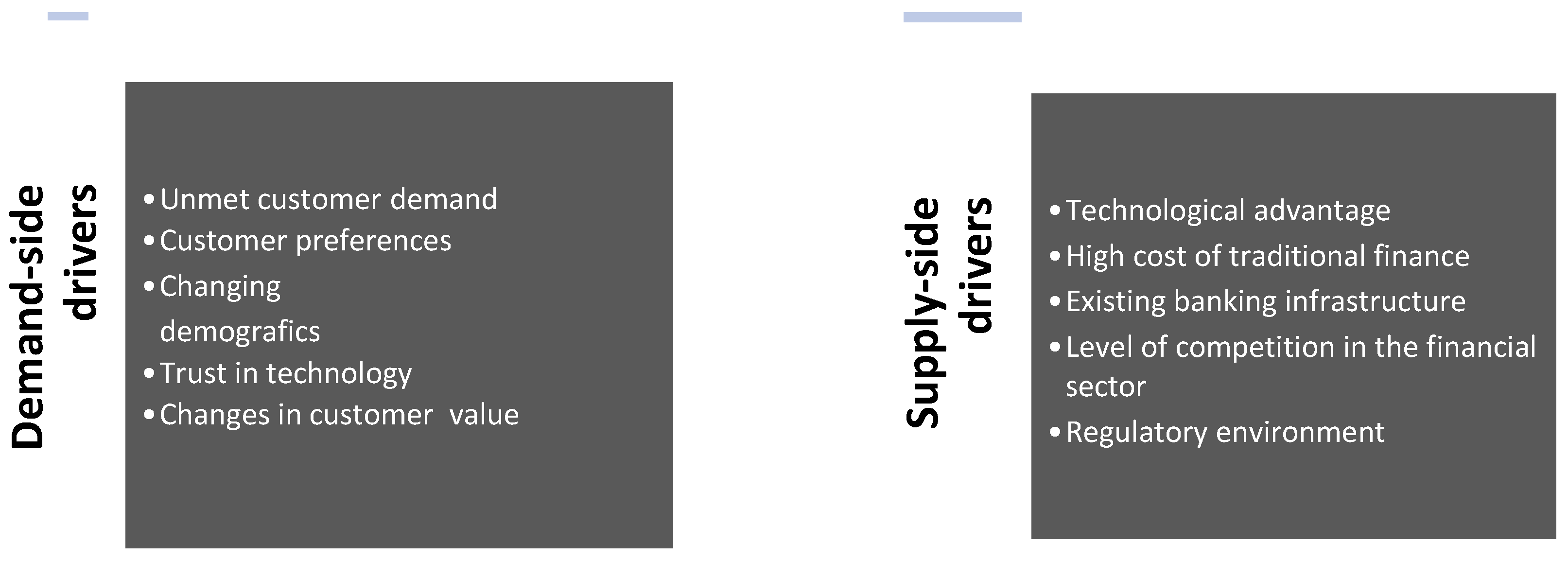

To answer the first research question, the desk research method was used. An in-depth analysis of the existing research results has allowed to split external factors which explain why FinTechs and BigTechs have grown more in some countries or regions, into supply-side and demand-side drivers. The most important of these drivers are shown in Figure 1.

There is evidence to suggest that unmet customer demand has been an important driver of Fintech adoption1 in many countries or even regions. Despite the fact that almost everywhere, including advanced economies (AEs), some consumers do not have access to financial services, this factor is of particular importance for the expansion of technology companies in emerging markets and developing economies (EMDEs). Various studies provided evidence that unmet demand is a likely key factor behind the rapid growth of mobile payments in Kenya, payments and money transfer services in India, Latin America, and Southeast Asia (Bech et al. 2018), as well as FinTech and BigTech credit in China (Hau et al. 2019), the United States (Jagtiani and Lemieux 2018; Tang 2019), and Argentina (Frost et al. 2019).

Demand-side drivers are also linked to changing demographics and related changes in customer value and preferences. A number of studies and surveys showed that the rate of FinTech and BigTech adoption is significantly higher in younger cohorts.2 A survey from EY (2017) confirmed that the use of FinTech products was the highest among young adults at an early stage of their career aged 25 to 34 years (48%) and 35 to 44 years (41%). Other EY study validated that FinTech usage is higher in regions or countries with a younger population, such as Asia, South Africa, India or Colombia (EY 2019). Over time, with younger cohorts entering the market, FinTech adoption will probably grow since these customers’ preferences and expectations differ significantly from those of the older generations. Nowadays, transaction security and even a price are no longer a priority—young consumers want to buy and pay immediately, so speed, convenience and enhanced user-friendliness are the most desirable features of transactions, including financial ones. This shift is supported by high trust in technology and tech firms among the youngest cohorts (Bain & Company and Research Now 2017). However, Nair (2019) claimed that overall trust in technology may decline due to scandals related to the misuse of personal data. Finally, it is worth noting that recent customer behavior, not only in finance, seems to be increasingly driven by ethical reasons. There is some evidence that some consumers are more likely to adopt FinTech products (e.g., P2P lending) as these are seen as more socially responsible and of greater social value than conventional banking (He et al. 2017; EY 2017; FSB 2019b).

The digital revolution has changed the demand for financial services and led the financial sector to become more customer-centric. However, on the supply side, it has left incumbents with obsolete technologies and an overextended branch network (OECD 2020). Saal et al. (2017) noted that as the financial services industry becomes increasingly contestable, decomposable, and reconfigurable, the capacity to innovate is a key success factor. The technological advantage of FinTechs and BigTechs over incumbents is undisputable, but there are also many other factors that influence the market position of tech companies.

While the market position of FinTechs and BigTechs in the financial services industry is generally not strong (except for China), there are some economies where technology firms have made significant inroads into finance. In general, the growing market power of tech companies and the wider adoption of their services has been observed in EMDEs (EY 2019; Frost 2020) with underdeveloped banking infrastructure but high mobile phone penetration. In these markets, the range of financial services they offer is wider and includes, apart from payment services, credit, insurance, and investment services. EMDEs with a strong demand for financial services, a low level of financial inclusion, a weak banking infrastructure, and low regulatory constraints create favorable conditions for the expansion of BigTechs. However, this does not explain the rapid development of BigTechs in AEs such as, e.g., the United States. There is some evidence that the wider adoption of some services provided in such economies by tech companies, namely lending services, could be explained by the relatively high cost of financial intermediation, which usually means that the banking sector is relatively uncompetitive and therefore more profitable (Bazot 2018; Frost 2020). That is the case, among others, of the United States, Australia, China or New Zealand. Claessens et al. (2018) found that the higher a country’s income and the less competitive the banking system become, the larger FinTech (and BigTech) credit activity is.

A very important supply-side driver of FinTechs’ and BigTechs’ market position is the regulatory framework. A growing number of studies showed that the regulatory environment can support or hinder FinTech and BigTech adoption. The results of studies confirming that volumes of some FinTech services or investments in FinTechs are higher in countries with less stringent (or more adequate) bank regulation would appear to be quite obvious (e.g., Navaretti et al. 2017; Claessens et al. 2018; Cambridge Centre for Alternative Finance—CCAF 2019). On the other hand, however, this means that the evidence from these studies did not support the common opinion that FinTech adoption is primarily driven by regulatory arbitrage.3 A detailed examination of the role of regulation was carried out by Rau (2017) and the outcome from his in-depth study suggested that countries with a higher quality of regulation, a stronger rule of law, control of corruption, ease of entry, and higher profitability of extant intermediaries have higher volumes of alternative finance. As shown in a BIS report (BIS 2019) the choice of policy tools concerning BigTechs’ entry into finance has been quite heterogeneous across jurisdictions: from strict restrictions on their entry in India (Indian e-commerce law), to granting them banking licenses in Korea, Hong Kong SAR, and Luxembourg. Since the evidence is scarce so far, more reliable conclusions should not be drawn until researchers have an adequate sample of FinTech service volumes across countries and over time (Frost 2020).

Most of the studies carried out mainly by large international organizations, such as the Financial Stability Board, Bank for International Settlements or OECD usually does not contain the results of empirical research allowing to determine the impact of individual factors on the forms of interaction between technology companies and banks. The few empirical research mainly concerns specific areas of activity of technology companies, e.g., payments (i.e., Kotkowski et al. 2020) or loans (i.e., Claessens et al. 2018). This is mainly due to the lack, incompleteness or incomparability of comprehensive data on FinTechs and BigTechs, which constitutes a significant barrier to development of quantitative research in this area. For the same reason, the few empirical studies that have been carried out are difficult to replicate as well as test their results. In addition, FinTechs and BigTechs were not distinguished and treated as one group of tech companies in the aforementioned studies.

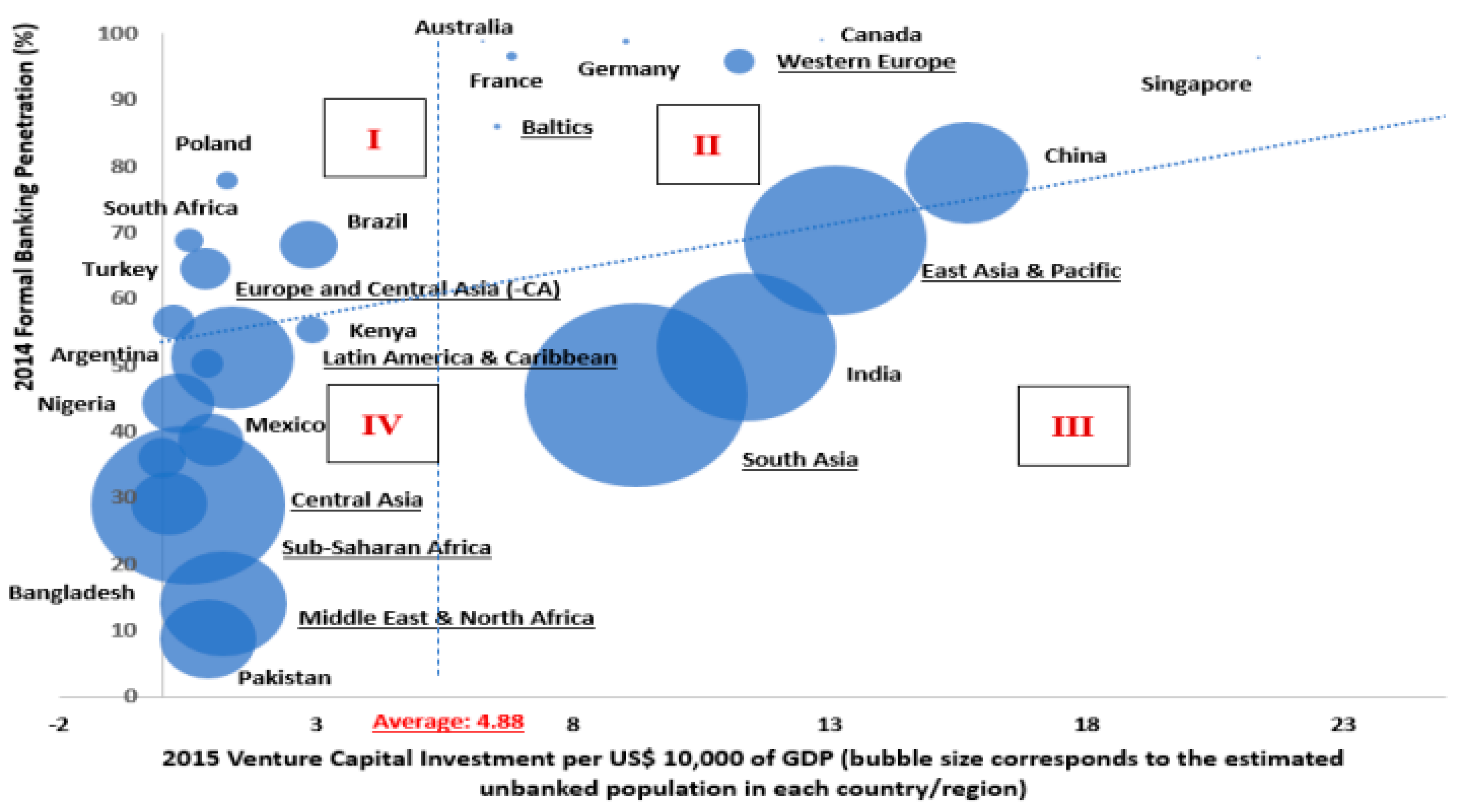

While the research cited so far has identified factors that affect the current position of technology companies by International Finance Corporation (a member of the World Bank Group) shows how selected factors can influence the potential market position of banks and technology companies and thus their forms of interactions. They found that the key challenges that have affected the digital transformation of financial services across countries and regions are: low level/penetration of formal financial services, low income and financial literacy levels, underdeveloped technology and venture capital ecosystems and weak infrastructure. As proxies for these four challenges they assumed formal banking penetration (representing the first two challenges, and displayed along the y-axis) and venture capital (VC) investment relative to GDP (representing the last two challenges, and displayed along the x-axis). The bubble sizes correspond to the estimated number of unbanked in each country. In the study the World Bank classification of countries by regions was applied. Taking the average venture capital penetration and the least-squares trend line for the interaction of the two variables as dividing lines, they get the four quadrants shown in Figure 2. The values for the US (quadrant II) are outside the shown scale, i.e., 50 for x-axis and 94% for y-axis.

In countries where the traditional banking sector is well established and has been providing reasonable services to the mass market (Quadrant I and II), banks will probably continue to play a dominant role in the market. In-sector competition in countries with bank dominance (Quadrant I) may foster technological innovations among banks (e.g., as in Poland), but innovation could also come from tech companies (although rather foreign than domestic ones). In countries with a stronger tech ecosystem (Quadrant II), BigTechs and some Fintechs will scale up, taking a market share from incumbents, while others will cooperate with banks. In markets where the banking sector has lagged and banks have left large segments of the market underserved (Quadrant III), tech companies (especially BigTechs) have a greater chance to gain a significant market share. Finally, in countries with underdeveloped technology ecosystems and weak banking infrastructure (Quadrant IV), telecoms companies tend to be the most significant market players in providing basic financial services (such as M-Pesa in Kenya for mobile payments). However, banks still have a chance to catch up with the competitors if they choose to strengthen their market position by adopting innovations. At the same time, they should move fast before telecoms firms corner the market (Saal et al. 2017). Although this study is very interesting and valuable, it ignores the impact of the regulatory environment on bank-FinTechs and BigTechs collaborative space, which can be of critical importance for their development and potential interactions.

3.2. Complementarity of Assets, Skills and Features of Banks and Technology Companies

In this section, modifying slightly the IO theory (Tirole 1988), it was assumed that the general reaction of new entrants (tech companies) and incumbents (banks) will depend on how much the assets/resources, skills and features of both these groups complement or substitute each other. If they are largely complementary, an incumbent may decide to accommodate the entry. In the opposite situation (when they are substitutable) it may try to prevent entry. In the first case, non-aggressive strategies, such as a commitment to remain small or form a partnership with the incumbent, are usually chosen by the entrant. In the second case, incumbents may prevent entry and decide to fight with new entrants by hampering access to their infrastructure or using bundling and tying strategies (OECD 2020). Indeed, the reaction of both sides also depends on underlying industry characteristics (Fudenberg and Tirole 1984; Vives 2008), and are specific to the size and the market position of both market participants.

In the existing literature, very few studies can be found that summarize the comparative advantages of banks and technology companies. In the one of them Petralia et al. (2019) comparing competitive advantages and disadvantages that banks face vis-à-vis FinTechs and BigTechs divided them into three primary categories: technology (which includes customer experience), size (cost of funding and network effects) and policy-based considerations (prudential regulation, data privacy/protection and political/lobby power). A similar approach has been applied in the FSB report on BigTech in finance (2019b) where comparative advantages of banks, BigTechs and FinTechs were also split into three categories but quite different. The first was: trust represented by such features/benefits as size, brand recognition and customer loyalty, the second: leverage containing investment capacity, low-cost funding, global customer base and network effects, and the last: performance containing cutting-edge technologies, cross-subsidization and limited regulatory burden. In both studies, the above-mentioned advantages were compared based on expert judgement, However, the comparison was limited only to determining whether the given advantage exists or not.

Those studies became an inspiration to create a more sophisticated tool for comparing the resources and skills of banks, FinTechs and BigTechs and then choosing the most appropriate form of interaction. The proposed tool significantly develops the previous proposals. In total, 27 features were identified and grouped into six primary categories: tangible and intangible assets, marketing assets, organizational skills and structure, others skills as well as experience and efficiency. Such a refinement of the tool makes it easier to use in practice. Each characteristic has been assessed with regard to the strength of its occurrence using a three-point scale where one plus means low intensity, two pluses—medium intensity and three—high intensity of occurrence.

In this paper the proposed tool was used to compare the assets, skills and features of large banks, BigTechs and FinTechs to determine the most likely general form of their interaction. As in the case of the previous studies, the assessment of particular assets and skills was made based on expert judgement.

Table 1 compares the assets/resources, skills and features of large banks, FinTechs and BigTechs. The greatest complementarity between resources, skills and features, and therefore the likelihood of forming a partnership, exists when one of the entities compared has advantages (+++) in the areas that are weak points of the other (+), and vice versa. On the other hand, the overlap between assets, skills, and features is supported by the choice of competition strategy.

The comparison of the assets, skills, and features of FinTechs and banks leads to the conclusion that they are largely complementary. The fundamental advantage of FinTechs is that they are operated as leaner, more agile, and more flexible businesses, and with their high-tech capabilities they may respond to changing customer expectations and preferences in a quicker and more flexible manner. They also have the ability to attract talented young people and create innovative solutions, which improve user experience. This means that they can meet consumer expectations in terms of speed and convenience better than incumbents, and moreover—they can do it at a low cost and using transparent pricing. On the other hand, a focused business model, the lack of an installed customer base, the comparative lack of reputation, the relatively small capital base, and the lack of experience in risk management and with regulatory frameworks are the main challenges that FinTechs need to overcome.

Despite the fact that nowadays it is very difficult to estimate the size and potential growth of the FinTech sector using traditional measures (i.e., number of companies, size of their assets) it can be assumed that they will not weaken incumbents’ market position in the near future. Taking into account the fact that FinTechs are generally small young start-ups, and their resources, skills, and features largely complement those of incumbents, especially banks, the likelihood of their choosing a cooperation strategy is greater than that of choosing competition. FinTechs can become a valuable intermediary between the bank and the customer by providing advanced technology solutions that allow financial services and the way they are delivered to be improved, making them more convenient and meeting customer preferences in a better way. On the other hand, banks, with their well-recognized brand, established reputation and market position, as well as an extensive customer base, can be attractive partners for FinTechs. FinTechs may, in turn, be able to obtain access to a broader customer base, as well as gain access to superior knowledge in risk management and in how to deal with financial regulation. Moreover, they can access funding from banks, which for some of them may be the opportunity to get a banking license more easily.

The comparison of the resources, skills, and features of large banks and BigTechs leads to a quite different conclusion, since both groups have many overlapping strengths, such as: a large installed customer base, abundant and superior customer information, powerful brands and an established reputation,4 a large capital base, considerable earnings, and almost unlimited access to cheap funding. Both banks and BigTechs can achieve economies of scale and scope. However, these will be larger in the case of BigTechs, which may additionally benefit from significant network effects achieved using consumer-facing platforms in the areas of e-commerce, on-line searches, and social media. Financial services fit well with other goods and services offered on the platform, which creates synergies giving digital platforms a strong competitive advantage over banks. At the same time, banks have a low ability to attract talented young staff, and with their legacy systems are prone to cyberattacks. However, compared to BigTechs, they have greater risk management skills, as well as knowledge and experience in dealing with regulations. Therefore, due to their size and mostly international scale of activity, as well as other advantages that to a large extent substitute those of incumbents, BigTechs will most probably become banks’ potential rivals.

It should be stressed that the comparison of resources, skills and features of BigTechs, FinTechs, and large banks only allows the most likely form of interaction between them to be determined. The extent to which a particular bank can generate value from a strategic interaction with a given FinTech or BigTech firm is an individual case depending on its capacity to create synergies between their specific assets, skills and features.

4. Discussion

Although many existing studies show the strengths and/or weaknesses of banks and technology companies (Górka 2018; BIS 2019; Stulz 2019; OECD 2020) to date, very few studies can be found in the literature that summarize comparative advantages of banks and technology companies. Two of them served as an inspiration to create a more sophisticated tool for comparing the resources, skills and features of banks, FinTechs and BigTechs and then choosing the most appropriate form of interaction. The proposed tool significantly develops the previous analysis carried out by Petralia et al. (2019) as well as by FSB (2019b). First, the advantages identified in earlier studies have been ordered and assigned to the respective types of resources and skills of the company using resource-based approach. Second, in order for each category to contain all relevant characteristics additional features were added. Third, in contrast to the previous proposals, the tool allows not only for determining whether a given advantage exists or not, but also enables the assessment to what extent the assets and skills of given companies are substitutable or complementary, making it easier to choose the most appropriate form of interaction.

Taking into consideration the differences between technology companies and banks, three basic forms of interaction are possible: competition, cooperation or coopetition. Considering the detailed results of the analysis into their comparative advantages, the most likely form of interaction between incumbents and tech companies seems to be: in the case of FinTechs—cooperation, in the case of BigTechs—competition, although in both cases coopetition is also possible.

The results obtained are in line with the findings of previous studies. The research carried out by Hornuf et al. (2018), which covered 400 banks from four countries (Canada, France, Germany, and the United Kingdom) revealed that most of banks choose non-aggressive strategies toward FinTechs. Bank-Fintech alliances most often take the form of product-related collaboration (54% of cases), however direct holdings are also chosen quite often, particularly by large banks in the UK and France. It must be stressed that in the latter case, banks prefer to purchase a minority stake in a Fintech firm instead of a full acquisition. The EBA (2018) survey has shown similar results. It revealed that the largest European banks also prefer to form partnerships with FinTechs; however, almost 3/4 of them have invested in FinTechs through venture capital funds, or through setting up digital funds. Moreover, 84% of the largest banks set up FinTech incubators/accelerators.

On the basis of the research conducted so far, one further conclusion can be drawn that the forms of bank-FinTech cooperation change over time what is often overlooked in the literature. Their typology was presented in Figure 3.

In the early stages of development, banks try to establish contacts with FinTechs by creating innovation labs and organizing hackathons. Then banks help FinTechs overcome the barriers they are facing at the beginning by setting up accelerators and incubators. In the subsequent stages, the form of cooperation becomes more structured and formalized. The most common is product-related cooperation, which is a comparatively less institutionalized form of alliance that offers little or no control over the product development process in a FinTech firm. Offering FinTech solutions potentially helps banks to maintain their customer base without having to develop new services or applications in-house, which could be very tough task as their legacy systems are barely compatible with the newest user-friendly applications. The largest banks relatively often invest directly in FinTechs, including their acquisition. Banks prefer to acquire small start-ups because as they grow, they become less and less attractive for banks. However, it should be emphasized that acquiring a FinTech firm may be a risky strategy since many FinTech solutions must be customized to end-user needs and regularly updated, which may be a difficult challenge for the bank after acquisition.

When it comes to BigTechs the conducted analysis showed that the most likely form of their interaction with banks is competition or coopetition. Since BigTechs have been offering financial services for a relatively short period of time, establishing how they interact with incumbents is more complicated. Research in this field is still scarce, nevertheless, more and more evidence suggests that in AEs they generally provide financial services in partnership with incumbents, whereas in EMDEs they tend to serve as competitors. This is also consistent with the conducted analysis of external drivers of their expansion. Their results indicate that the main drivers of BigTech expansion into finance in EMDEs are: a strong demand for financial services, a low level of financial inclusion, a weak banking infrastructure but high mobile phone penetration, and low regulatory constraints. According to FSB study the relatively higher concentration and larger expansion of BigTechs observed in EMDEs may also be explained by a better combination of falling average costs of meeting the demands of new customers, and increasing marginal gains from their acquisition in these economies (FSB 2019a).

In line with the results of the conducted analysis are also observed forms of interactions of BigTechs and banks in AEs. Based on its results in this group of countries the expansion of BigTechs can be explained by the relatively high cost of financial intermediation, (which usually means that the banking sector is relatively uncompetitive) as well as by the high country’s income which stimulates the demand for financial services. Moreover, consumers in these countries have higher expectations as to the quality of the services provided that create favorable conditions for the expansion of BigTechs. In AEs BigTechs usually provide financial services in partnership with incumbents rather than compete with them. This is confirmed by a European Banking Authority study carried out in Europe (where the scope of BigTechs expansion is smaller than e.g., in China or in the U.S.), which showed that existing payment institutions and electronic money institutions are more often partners of BigTech firms than their competitors (EBA 2019). Furthermore, the FSB research confirmed that BigTechs cooperate with licensed banks in order to gain funding for loans (originated and distributed by themselves) or to issue branded credit cards. The study also pointed out that BigTechs use their platforms to act as intermediaries between financial institutions and their clients, particularly in payments, loan initiation, and money market funds (FSB 2019a). However, it should be emphasized that even in doing so, BigTech firms still compete with incumbents, which indicates that in fact they follow a coopetition strategy.

What is often underestimated in the literature is the fact that BigTechs are important third-party service providers for financial institutions all over the world. This includes, for instance, cloud services (Amazon Web Services, Microsoft, Google and Ali Cloud in Asia), as well as specific tools using artificial intelligence and machine learning. As the FSB (2017b, 2019c) and Khan (2017) pointed out the activity of BigTechs as both suppliers to, and competitors with financial institutions raises a number of potential conflicts of interest and problems connected with market concentration, systemic risk, third-party dependencies, and other competition and regulatory issues related to their dominant market power in some markets. This specific feature of the interactions between BigTechs and incumbents seems to be mostly noticed by regulators and supervisors while it deserves the attention of the competition authorities as it may significantly affect the balance of power in the market.

It is worth pointing out that when it comes to FinTechs, especially start-ups, BigTechs generally use much more aggressive strategies. In recent years, BigTechs, both American and Chinese, have taken over many small innovative companies. The growing scale of this phenomenon has been drawn the attention of the regulatory authorities in the United States and China, who at the end of 2020, launched antitrust probes into tech giants (GAFA and Alibaba respectively) complaining that they hinder the development of innovation and restrict competition by buying startups in order to keep them from becoming competitors (Zhu et al. 2020). This type of BigTech strategic reaction is in line with the IO theory—as the resources and skills of FinTechs and BigTechs are largely substitutable, the latter try to prevent FinTechs from entering the market by taking them over.

5. Conclusions

The paper proposed a conceptual framework that helps to explain which factors affect the type of interactions between technology companies and banks. It is based on the assumption that, on the one hand, the market position of banks and technology companies, and thus the basic type of their mutual interactions, depends on external factors. The adoption level of FinTechs and BigTechs in individual countries/regions was considered as the most important factor. This level turned out to be greater in EMDEs with a strong demand for financial services, a low level of financial inclusion, a weak banking infrastructure, and low regulatory constraints, which create favorable conditions for the expansion of technology companies. In this group of countries, tech companies, and in particular BigTechs, tend to serve as competitors and their strategies versus incumbents can be aggressive. In contrast, in AEs, technology companies more often provide financial services in partnership with incumbents rather than compete with them. Additionally, BigTechs are there important third-party service providers for financial institutions. They provide them with a cloud computing services and AI/ML solutions; however, it should be stressed that this dependency raises a number of risks and potential conflicts of interest to be mitigated and solved not only internally but also by regulators and competition authorities.

On the other hand, it was assumed that the specific form of interaction between a given bank and a FinTech or a BigTech depends on to what extent their resources, skills, and features are complementary or substitutable. In order to assess this, a strategic tool was proposed. It enables the determination of both sides’ competitive advantages by comparing their tangible, intangible, and marketing assets, as well as features and skills related to their organization, level of effectiveness, risk management, and compliance skills. In this study, this tool was used to compare the resources, skills and features of large banks, BigTechs and FinTechs in order to determine the most likely form of their interaction. The comparison carried out using this tool has allowed drawing a few conclusions. Since assets, skills, and features of banks and FinTechs are largely complementary, it would be better for them to collaborate than to compete. By contrast, the comparison of the resources, skills, and features of large banks and BigTechs revealed that both groups have many overlapping strengths, which makes it more likely that they will compete with each other. When it comes to FinTechs and BigTechs whose resources are largely substitutable they will rather compete with each other (in the case of FinTechs with established market position) or BigTechs having greater market power will take over the smaller FinTechs thus eliminating potential competitors.

The paper provided a theoretical and methodological contribution to the existing literature. First, a narrow definition of FinTech representing the subjective or institutional approach, which makes it possible to clarify which entities can be included in the FinTech sector, was proposed. The proposed definition, can be useful not only for theoretical analysis, but also for conducting empirical research. Second, to make a separate analysis of both groups of technology companies possible, a definition of BigTech was also set out. The methodological contribution is threefold. First, in contrast to most of the previous studies concerning relationships between banks and technology companies, in which the latter were treated as one group referred to as FinTechs, in this paper, where possible, FinTechs and BigTechs has been considered separately. This distinction is justified since two companies substantively differ in terms of their size, scale of activity, specific features, and the extent to which their resources, skills and features are complementary to those of banks. Subsequently the type of interactions of each of these groups with banks is different. Second, both market-based and resource-based approach as well as a slightly modified IO theory have been used to determine when cooperation between banks and technology companies is more likely, and when they will rather compete with each other. A comprehensive approach using this perspective is relatively rare in the literature. And finally, there has been proposed a new strategic tool which helps to find comparative advantages of banks, FinTechs and BigTechs and thus makes it easier to choose the most appropriate type of interaction. The development of the conceptual framework presented creates new opportunities for future research on this topic.

As this paper was concerned rather with proposition building than theory testing, some limitations to the results exist. First, there is relatively little research on the factors influencing the degree of adoption of FinTechs and BigTechs in individual countries and regions to date. With the increase in their number, the knowledge about these factors as well as about the direction and strength of their impact on the adoption level of FinTechs and BigTechs, their market position and potential forms of their interactions will be greater and more established. Second, these external factors may change over time, which is not as much a limitation as a motivation for further research. Third, the combination of external factors in each country that belongs to AEs and EMDEs may be slightly different, which will undoubtedly affect the forms of interactions between banks and technology companies. Therefore, it would be welcomed to conduct research on this subject in individual countries.

The findings and limitations set the directions for further research. First of all, the conceptual framework and propositions should be further refined. It would also be interesting to use developed empirical data from particular countries that belong to AEs and EMDEs in the quantitative testing of earlier results. And finally, studies developing and refining the proposed strategic tool enabling the comparison of assets, skills, and features of banks, FinTechs and BigTechs would be welcomed.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Conflicts of Interest

The author declares no conflict of interest.

| 1 | The adoption rate is the pace at which a new technology is acquired and used by the public. This rate is usually represented by the number of people who start using a new technology or innovation during a specific period., Every two years since 2015, EY reports the level of FinTech adoption in the world. EY’s Global FinTech Adoption Index is the percentage of digitally active people who used at least two fintech services in the last six months. In 2019 the global FinTech adoption rate was 64% and emerging markets were leading the way. In both China and India, the adoption rate was 87%. Close behind were Russia and South Africa, both with 82% adoption. Among developed countries, the Netherlands, the UK and Ireland lead in adoption, reflecting in part the development of open banking in Europe (EY 2019). |

| 2 | However, J. Frost (2020) admitted that there may be some exceptions to the trend of greater adoption of Fintech by younger people. Namely in the US and the UK, where the majority of online marketplace borrowers (and in the UK also lenders—see Baeck et al. 2014) were from older cohorts. |

| 3 | However, other studies showed that certain Fintech activities, especially lending services (incl. P2P lending) could still be driven by this factor—for example, on the US mortgage market (Buchak et al. 2017), or in China (Braggion et al. 2018). |

| 4 | The reputation of banks was damaged during the recent financial crisis, while the reputation of some BigTechs has been negatively affected by misuse of customer data. |

References

- Arner, Douglas W., Janos Nathan Barberis, and Ross P. Buckley. 2015. The Evolution of Fintech: A New Post-Crisis Paradigm? University of New South Wales Law Research Series, Research Paper, No. 047; Sydney: University of New South Wales. [Google Scholar]

- Baeck, Peter, Liam Collins, and Bryan Zhang. 2014. Understanding Alternative Finance. The UK Alternative Finance Industry Report 2014. Nesta: University of Cambridge. [Google Scholar]

- Bain & Company, and Research Now. 2017. Evolving the Customer Experience in Banking. Available online: https://www.bain.com/insights/evolving-the-customer-experience-in banking/ (accessed on 5 October 2021).

- Bazot, Guillaume. 2018. Financial Intermediation Cost, Rents, and Productivity: An International Comparison. Working Papers 0141. Vienna: European Historical Economics Society (EHES). [Google Scholar]

- Bech, Morten, Umar Faruqui, Frederik Ougaard, and Cristina Picillo. 2018. Payments Are a-Changin’ But Cash Still Rules. BIS Quarterly Review. Basel: BIS, March, pp. 67–80. [Google Scholar]

- BIS. 2018. Sound Practices: Implications of Fintech Developments for Banks and Bank Supervisors. Basel: Basel Committee on Banking Supervision (BCBS), February. [Google Scholar]

- BIS. 2019. Big Tech in Finance: Opportunities and Risks. Annual Economic Report. Basel: BIS, pp. 55–79. [Google Scholar]

- Bodek, Mariusz C., and Julietta Matinjan. 2017. Innovation durch Corporate Incubation. In Innovationen und Innovationsmanagement in der Finanzbranche. Edited by Remigiusz Smolinski, Moritz Gerdes, Martin Siejka and Mariusz C. Bodek. Wiesbaden: Springer, pp. 117–44. [Google Scholar]

- Bömer, Max, and Hannes Maxin. 2018. Why Fintechs Cooperate with Banks—Evidence from Germany. Hannower Economic Papers 637: 1–31. [Google Scholar] [CrossRef] [Green Version]

- Braggion, Fabio, Alberto Manconi, and Haikun Zhu. 2018. Can Technology Undermine Macroprudential Regulation? Evidence from Peer-to-Peer Credit in China. CEPR Discussion Papers 12668. Washington, DC: CEPR. [Google Scholar]

- Brummer, Chris, and Yesha Yadaw. 2019. FinTech and the Innovation Trilemma. Georgetown Law Journal 235: 276–27. [Google Scholar]

- Buchak, Greg, Gregor Matvos, Tomasz Piskorski, and Amit Seru. 2017. FinTech, Regulatory Arbitrage, and the Rise of Shadow Banks. NBER Working Papers, No 23288. Washington, DC: NBER. [Google Scholar]

- Bunea, Sinziana, Benjamin Kogan, and David Stolin. 2016. Banks vs. fintech—At last, it’s official. Journal of Financial Transformation 44: 122–31. [Google Scholar]

- Burgmaier, Stefanie, and Stefanie Hüthing. 2015. Kampf oder Kooperation—Das Verhältnis von jungen Wil-den und etablierten Geldinstituten. In Multi- und Omni-Channel-Management in Banken und Sparkassen. Edited by Harald Brock and Ingo Bieberstein. Wiesbaden: Springer, pp. 101–14. [Google Scholar]

- CCAF. 2019. Shifting Paradigms: The 4th European Alternative Finance Benchmarking Report. April. Available online: https://www.jbs.cam.ac.uk/faculty-research/centres/alternative-finance/publications/shifting-paradigms/#.YX1jQlXP3IU (accessed on 28 September 2021).

- Claessens, Stijn, Jon Frost, Grant Turner, and Feng Zhu. 2018. Fintech Credit Markets around the World: Size, Drivers and Policy Issues. BIS Quarterly Review. Basel: BIS, September. [Google Scholar]

- Corea, Francesco. 2015. What Finance Can Learn from Biopharma Industry: A Transfer of Innovation Models. Expert Journal of Finance 2015: 45–53. [Google Scholar]

- Dorfleitner, Gregor, Lars Hornuf, Matthias Schmitt, and Martina Weber. 2017. FinTech in Germany. Berlin: Springer, ISBN 978-3-319-54665-0. [Google Scholar]

- EBA. 2018. Report on the Impact of FinTech on the Incumbents Credit Institutions Business Models. Paris: EBA, July. [Google Scholar]

- EBA. 2019. Report on the Impact of FinTech on Payment Institutions’ and e-Money Institutions, Business Models. Paris: EBA, July. [Google Scholar]

- EY. 2017. Global FinTech Adoption Index 2017. The Rapid Emergence of FinTech. London: EY. [Google Scholar]

- EY. 2019. Global FinTech Adoption Index 2019. As FinTech Becomes the Norm, You Need to Stand Out from the Crowd. London: EY. [Google Scholar]

- Fraile, Carmona Alberto, Lombardo Agustin González-Quel, Pastor Rafael Rivera, Quirós Carlota Tarín, García Juan Pablo Villar, Muñoz David Ramos, and Martín Luis Castejón. 2018. Competition Issues in the Area of Financial Technology (FinTech); Directorate-General for Internal Policies; Strasbourg: European Parliament, July.

- Frost, Jon. 2020. The Economic Forces Driving Fintech Adoption across Countries. BIS Working Papers, No. 838. Basel: BIS, February. [Google Scholar]

- Frost, Jon, Leonardo Gambacorta, Yi Huang, Shin Hyun Song, and Paolo Zbinden. 2019. BigTech and the Changing Structure of Financial Intermediation. BIS Working Papers, No. 779. Basel: BIS, April. [Google Scholar]

- FSB. 2017a. Financial Stability Implications from FinTech, Supervisory and Regulatory Issues that Merit Authorities’ Attention. Basel: FSB, June. [Google Scholar]

- FSB. 2017b. Artificial Intelligence and Machine Learning in Financial Services. Market Developments and Financial Stability Implications. Basel: FSB, November. [Google Scholar]

- FSB. 2019a. FinTech and Market Structure in Financial Services: Market Developments and Potential Financial Stability Implications. Basel: FSB, February. [Google Scholar]

- FSB. 2019b. BigTech in Finance. Market Development and Potential Stability Implications. Basel: FSB, December. [Google Scholar]

- FSB. 2019c. Third-Party Dependencies in Cloud Services. Considerations on Financial Stability Implications. Basel: FSB, December. [Google Scholar]

- Fudenberg, Drea, and Jean Tirole. 1984. The fat-cat effect, the puppy-dog ploy, and the lean and hungry look. American Economic Review 74: 61–66. [Google Scholar]

- Górka, Jakub. 2018. Banki, GAFAM, FinTech w gospodarce współdzielenia—Equilibrium współpracy i konkurencji. Prace Naukowe Uniwersytetu Ekonomicznego we Wrocławiu 531: 149–58. [Google Scholar] [CrossRef]

- Harasim, Janina. 2021. FinTechs, BigTechs and structural changes in capital markets. In The Digitalization of Financial Markets. The Socioeconomic Impact of Financial Technologies, 1st ed. Edited by Adam Marszk and Ewa Lechman. London: Routledge, part 2. pp. 81–100. [Google Scholar]

- Harasim, Janina, and Krystyna Mitręga-Niestrój. 2018. FinTech—dylematy definicyjne i determinanty rozwoju. Prace Naukowe Uniwersytetu Ekonomicznego we Wrocławiu 531: 169–79. [Google Scholar] [CrossRef]

- Hau, Harald, Yi Huang, Hongzhe Shan, and Zixia Sheng. 2019. How fintech enters China’s credit market. AEA Papers and Proceedings 109: 60–64. [Google Scholar] [CrossRef] [Green Version]

- He, Dong, Ross B. Leckov, Vikram Haksar, Griffoli Tomasso Mancini, Nigel Jenkinson, Mikari Kashima, Tanai Khiaonarong, Celine Rochon, and Hervé Tourpe. 2017. Fintech and Financial Services: Initial Considerations. Staff Discussion Notes. Washington, DC: IMF, June. [Google Scholar]

- Hornuf, Lars, Milan Klus, Todor S. Lohwasser, and Armin Schwienbacher. 2018. How Do Banks Interact with Fintechs? Forms of Alliances and Their Impact on Bank Value. CESifo Working Paper No. 7170, Category 14: Economics of Digitalization. Munich: CESifo GmbH. [Google Scholar]

- Jagtiani, Julapa, and Catharine Lemieux. 2018. Do fintech lenders penetrate areas thatare underserved by banks? Journal of Economics and Business 100: 43–54. [Google Scholar] [CrossRef] [Green Version]

- Jakšič, Marko, and Matej Marinč. 2015. The Future of Banking: The Role of Information Technology. Ljubljana: University of Ljubljana, p. 68. [Google Scholar]

- Jun, Jooyong, and Eunjung Yeo. 2016. Entry of FinTech Firms and Competition in the Retail Payments Market. Asia-Pacific Journal of Financial Studies 45: 159–84. [Google Scholar] [CrossRef]

- Kalmykova, Ekaterina, and Anna Ryabova. 2016. FinTech Market Development Perspectives. Les Ulis: EDP Sciences. [Google Scholar]

- Khan, Lina M. 2017. Amazon’s Antitrust Paradox. Yale Law Journal 126: 710–805. [Google Scholar]

- Kotkowski, Radosław, Krzysztof Maciejewski, and Piotr Maicki. 2020. PayTech—Innowacyjne rozwiązania płatnicze na rynku polskim. Warszawa: Narodowy Bank Polski. [Google Scholar]

- Lacasse, R. M., B. A. Lambert, N. Roy, J. Sylvain, and F. Nadeau. 2016. A Digital Tsunami: FinTech and Crowdfunding. Available online: http://fintechlab.ca/wp-content/uploads/2016/11/Digital-Tsunami-Site-Web.pdf (accessed on 8 October 2021).

- Maxin, Hannes. 2018. Corporate Venture Capital im Bankensektor: Eine Fallstudie. Zeitschrift für KMU und Entrepreneurship (ZfKE) 66: 71–89. [Google Scholar] [CrossRef] [Green Version]

- McWaters, Jesse, and Rob Galaski. 2017. Beyond Fintech: A Pragmatic Assessment of Disruptive Potential in Financial Services. World Economic Forum. August. Available online: https://www3.weforum.org/docs/Beyond_Fintech_-_A_Pragmatic_Assessment_of_Disruptive_Potential_in_Financial_Services.pdf (accessed on 8 October 2021).

- Nair, Sanjay. 2019. Trust in Tech is Wavering and Companies Must Act. Edelman Research. Available online: https://www.edelman.com/research/2019-trust-tech-wavering-companies-must-act (accessed on 12 October 2021).

- Navaretti, Giorgio B., Giacomo Calzolari, and Alberto F. Pozzolo. 2017. FinTech and Banks: Friends or Foes? Milano: European Economy: Banks, Regulation, and the Real Sector, December, pp. 9–30. [Google Scholar]

- OECD. 2020. Digital Disruption in Banking and Its Impact on Competition. Available online: http://www.oecd.org/daf/competition/digital-disruption-in-financial-markets.htm (accessed on 12 October 2021).

- Padilla, Jorge. 2020. BigTech “banks”, financial stability and regulation. Banquo de Espaňa, Financial Stability Review 38: 11–26. [Google Scholar]

- Petralia, Kathryn, Thomas Philippon, Tara Rice, and Nicolas Véron. 2019. Banking Disrupted? Financial Intermediation in an Era of Transformational Technology, Geneva Report 22. Available online: https://cepr.org/content/geneva-report-22-banking-disrupted-financial-intermediation-era-transformational-technology (accessed on 12 October 2021).

- Philippon, Thomas. 2016. The FinTech Opportunity. NBER Working Paper No. 22476. Available online: http://www.nber.org/papers/w22476 (accessed on 5 October 2021).

- Rau, Raghavendra. 2017. Law, Trust, and the Development of Crowdfunding. University of Cambridge Working Paper. June. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2989056 (accessed on 12 October 2021).

- Saal, Matthew, Susan Starnes, and Thomas Rehermann. 2017. Digital Financial Services: Challenges and Opportunities for Emerging Market Banks. EMCompass 42. License: CC BY-NC-ND 3.0 IGO. Washington, DC: International Finance Corporation, August, Available online: https://openknowledge.worldbank.org/handle/10986/30368 (accessed on 8 October 2021).

- Schueffel, Patrick. 2016. Taming the beast: A scientific definition of Fintech. Journal of Innovation Management 4: 32–54. [Google Scholar] [CrossRef]

- Stulz, René M. 2019. Fintech, bigtech, and the future of banks. Journal of Applied Corporate Finance 31: 86–97. [Google Scholar] [CrossRef]

- Tang, Huan. 2019. Peer-to-peer lenders versus banks: Substitutes or complements? Review of Financial Studies 32: 1900–38. [Google Scholar] [CrossRef]

- Tirole, Jean. 1988. The Theory of Industrial Organization. Cambridge, MA: MIT Press, ISBN 0-262-20071-6. [Google Scholar]

- Vives, Xavier. 2008. Information and Learning in Markets: The Impact of Market Microstructure. Princeton: Princeton University Press. [Google Scholar]

- Zavolokina, Liudmila, Mateusz Dolata, and Gerhard Schwabe. 2016. FinTech—What’s in a name? Paper prezented at Thirty Seventh International Conference on Information Systems, Dublin, Ireland, December 11–14. [Google Scholar]

- Zhu, Julie, Kane Wu, and Cheng Leng. 2020. China Launches Antitrust Probe into Tech Giant Alibaba. Reuters. Available online: https://www.reuters.com/article/us-china-antgroup/china-launches-antitrust-probe-into-tech-giant-alibaba-idUSKBN28Y05T (accessed on 15 October 2021).

Figure 1.

Drivers of FinTech and BigTech adoption across markets. Source: own elaboration based on Frost et al. (2019); OECD (2020); Frost (2020).

Figure 2.

The banking—fintech development space. Source: Saal et al. (2017).

Figure 2.

The banking—fintech development space. Source: Saal et al. (2017).

Figure 3.

Forms of bank-FinTechs interactions depending on the collaboration phase. Source: own elaboration.

Figure 3.

Forms of bank-FinTechs interactions depending on the collaboration phase. Source: own elaboration.

{kind=link}

{kind=link}

{kind=link}

Table 1.

Comparative advantages of large banks, FinTechs and BigTechs.

| Assets/Skills | Features | FinTechs | Banks | BigTechs |

|---|---|---|---|---|

| Tangible assets | Size (balance sheet) and reach | + | +++ | +++ |

| Cutting-edge technology | +++ | + +/+ | +++ | |

| Number of employees | + | +++ | ++ | |

| Branch network | - | +++ | - | |

| Intangible assets | Customer base/ability to exploit it | +/++ | +++/++ | +++/+++ |

| Customer trust and loyalty | + | +++ | ++ | |

| Brand recognition | + | +++ | +++ | |

| Ability to attract best talents | ++ | + | +++ | |

| Marketing assets | Wide and diversified range of products | + | +++ | ++ |

| Price level | ++ | +++ | + | |

| Price transparency | +++ | + | ++ | |

| User experience | +++ | +/++ | +++ | |

| Electronic channels | +++ | ++ | +++ | |

| Organizational skills and structure | Organizational complexity | + | +++ | ++ |

| Flexibility and agility | +++ | + | ++ | |

| Innovativeness | +++ | + | +++ | |

| Transaction security | ++ | +++ | ++ | |

| Customer data protection | ++ | +++ | + | |

| Others skills and experience | Risk assessment and management | + | +++ | + |

| Experience in compliance and regulation | + | +++ | + | |

| Experience beyond the financial industry | ++ | x | +++ | |

| Efficiency | Costs/revenues | + | +++ | + |

| Margins | + | +++ | + | |

| Access to cheap (low-cost) funding | + | +++ | ++ | |

| Investment capacity | + | +++ | +++ | |

| Cross-subsidization | x | ++ | +++ | |

| Economies of scale and scope | + | ++ | +++ | |

| Network effects | + | ++ | +++ |

+ low intensity; ++ medium intensity; +++ high intensity; x—not applicable. Source: own elaboration.

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Harasim, J. FinTechs, BigTechs and Banks—When Cooperation and When Competition? J. Risk Financial Manag. 2021, 14, 614. https://doi.org/10.3390/jrfm14120614

AMA Style

Harasim J. FinTechs, BigTechs and Banks—When Cooperation and When Competition? Journal of Risk and Financial Management. 2021; 14(12):614. https://doi.org/10.3390/jrfm14120614

Chicago/Turabian StyleHarasim, Janina. 2021. "FinTechs, BigTechs and Banks—When Cooperation and When Competition?" Journal of Risk and Financial Management 14, no. 12: 614. https://doi.org/10.3390/jrfm14120614