The Effects of Managerial Competency and Local Religiosity on Corporate Environmental Responsibility

1

School of Business and Technology Management, College of Business, Korea Advanced Institute of Science and Technology (KAIST), Daejeon 34141, Korea

2

Global Commercialization Center, Korea Advanced Institute of Science and Technology (KAIST), Daejeon 34141, Korea

3

Ingenium College of Convergence Studies, Hankuk University of Foreign Studies, Seoul 02450, Korea

*

Author to whom correspondence should be addressed.

Sustainability 2021, 13(11), 5857; https://doi.org/10.3390/su13115857

Submission received: 17 April 2021

/

Revised: 18 May 2021

/

Accepted: 19 May 2021

/

Published: 23 May 2021

Abstract

:This study investigates the influence of local religious beliefs to evaluate managerial motives towards corporate environmental engagement, considering the growing attention of the role of external factors in shaping corporate behavior. Using Newsweek’s green rankings of the largest publicly traded US firms by market capitalization from 2014–2016, we find that competent managers show a higher strategic preference for corporate environmental practices in firms located in low-Protestant or high-Catholic areas exhibiting higher risk and uncertainty, which tend to mitigate the negative effects of risky environments. We find that corporate environmental practices positively influence the sales of firms in high risk-taking states. This study provides significant contributions to the literature documenting the consequences of local religious risk-taking behavior and elaborates on the perceptions of competent managers on environmental management. The results provide valuable insights for practitioners and policymakers looking to incorporate environmental practices.

1. Introduction

The debate over the antecedents and the consequences of corporate environmental responsibility (CER) has drawn considerable interest among scholars and practitioners, suggesting profound changes in the way firms execute environmental practices. Numerous studies on the determinants and economic consequences of CER have not resulted in conclusive outcomes, resulting in a lag in the broader goal of incorporating corporate social and environmental considerations into corporate behavior [1,2]. The majority of the extant research exhibits some awareness regarding the motivations for CER practices through ethical practices and environmental sustainability. However, few studies have paid attention to the role of external factors in shaping corporate behaviors. Tsendsuren et al. [3] highlight the fact that the product market competition setting is a perfect stage for managers to strategically incorporate CER practices to gain advantage in the competitive market. Li et al. [4] show that a firm’s visibility in the news and media encourages managers to enhance corporate social and environmental practices. Similarly, cultural factors have also gained significant attention as important determinants of corporate behavior [5,6,7]. Numerous studies have recently highlighted the impact of local religious beliefs on economic attitudes, and thus how they shape corporate decisions [8,9]. Scholars argue that religiosity has a greater impact on managers’ personal values, consequently affecting their attitudes and decisions [10,11]. However, the effects of local culture on corporate environmental management decisions has to be established through a conclusive investigation [12].

The personal cognition of the decision-makers affects a firm’s CER practices, which depend on their values, philanthropy, and social concerns or their interests [13]. Moreover, competent managers possess superior knowledge and skills regarding technology, industry trends, and business environments. These attributes enable them to efficiently utilize the firm’s resources and generate a higher return on projects. Managerial competency is not only instrumental in defining corporate financial performance (CFP) outcomes but it also relates to the contemplation of the outcomes of activities to society and the environment while achieving superior performance [14]. Thus, managers decide according to their competency whether to allocate resources that account for environmental issues beyond their obligations and to maximize stakeholders’ wealth [15].

Local culture has a powerful effect on managerial decisions. Recent studies indicate that local religious risk-taking behavior affects managerial decision-making processes [16]. Managers are likely to conform to the norms of local culture, as social identity theory suggests that the value of sharing a common identity and having a sense of being in a particular group has a substantial influence on people’s behavior. Consistent with this perspective, a growing body of literature has empirically examined the influence of local religiosity, an important aspect of local culture, on a variety of corporate decisions such as corporate investments [12], earnings management [17,18], cash holding [7], tax avoidance [19], and bank risk-taking [6]. Surprisingly, scholars have overlooked the combined effect of local religiosity and managerial competency on the degree of a firm’s CER practices. This research analyzes the levels of local religiosity around organizations, and considers their corporate decisions and their incorporation of social and environmental considerations. We focus on risk-taking behaviors because prior studies provide strong and robust evidence of corporate behaviors due to the risk-taking attitudes of individuals. In particular, studies emphasize that Catholics exhibit less aversion to speculative risk compared to Protestants. Using Newsweek’s green rankings of the largest publicly traded US firms by market capitalization from 2014 to 2016, we examine the effects of the state-level Catholic to Protestant ratio (CPratio), that is, the proportion of Catholic to Protestant adherents in a particular state, on the firm’s CER performance measured by its green score, which is further examined in relation to managerial competency.

We find that both managerial competency and local religiosity are empirically important antecedents of CER practices [20,21]. However, we did not find a highly competent manager with a stronger preference for undertaking more CER strategies. Alternatively, the significant negative association between managerial competency and CER indicates that highly competent managers not only understand the cost of CER practices, which may destroy shareholders’ wealth, but also do not window dress for their own benefit [21]. Local religious risk-taking attitudes may not directly lead to higher CER practices, as there is no statistically significant relationship. Notably, local risk-taking attitudes positively moderate the manager’s consideration of CER undertakings; a competent manager practices more CER activities in organizations in areas with high levels of religiosity. Additional results indicate that a firm’s risk and CER activities challenge CFP; however, the effect of the interaction between CER and local religiosity reveals that CER positively moderates the negative impact of firm risk on CFP. Overall, our findings suggest that competent managers strategically promote value-enhancing CER practices, which results in an improvement in CFP. Our study utilizes the composition of local religious beliefs, an important aspect of local culture, to examine corporate behaviors toward CER practices and to document the role of managerial competency in the efficient execution of CER practices to improve firm performance.

A detailed literature review reveals that the major focus of analysis revolves around formal institutional factors in CER considerations [22,23], and studies on the role of religion on CER have been under-researched as cultural determinants of CER. Karolyi [24] argues that culture is a key factor influencing corporate decision-making in institutional settings. Stulz and Williamson [25] reveal that cultural variables have more significant explanatory power than institutional factors for investor right enforcement. Religion is the most important cultural variable in corporate decision-making. Recent studies use the CPratio as a proxy for analyzing religious risk-taking behavior of local populations. Following recent trends, we investigate the effect of local religion, which is one of the important measurable local cultural characteristics that determine the antecedents of CER. The religious variations in the Catholic to Protestant populations across the states in the U.S. allow us to identify the level of CER practices of firms with respect to local religious risk-taking attitudes. We find that competent managers understand the importance of addressing environmental issues, thereby improving corporate financial performance when their firms’ performance is challenged by local risk-taking behavior. Our findings extend existing studies on risk management and highlight the importance of the firms’ efforts to harmonize with local behavior. We highlight the strategic role of competent managers in creating value via strategic CER executions, which improves CFP in risky environments. Practitioners may find this useful for strategic CER practices that will create value for firms and will mitigate the negative effects of risky environments. The results also encourage policymakers to formulate policies and regulations to motivate the environment-friendly activities of managers that strengthen stakeholder relationships, thereby improving the financial performance of firms. This study contributes to the literature regarding strategic management and the growing literature on the effect of local religiosity on corporate behavior in CER practices. The remainder of this paper is organized as follows. Section 2 presents a literature review and develops the hypotheses, and Section 3 describes the data and empirical methodology. Section 4 provides the results and a discussion of our analysis, followed by the conclusions in Section 5. Lastly, Section 6 discusses the limitations of this study and suggests future extensions of this study.

2. Literature Review and Hypothesis Development

The causal drivers behind managers’ decisions on environment-friendly approaches may broadly be classified as either altruistic or strategic [5]. The strategic view suggests that CER creates a competitive advantage to differentiate firms from their rivals, which helps firms increase profitability, increase market shares, and sustain business [26,27]. This view recommends that firms increase their CER practices to attain scarce resources by gaining stakeholder support for future endeavors and investments of firms [28]. From an altruistic perspective, firms are willing to surrender a part of shareholders’ profits to fulfill social expectations, and avoid unethical profit by seeking a philanthropic approach for social contribution [5]. This approach may cover managers’ vested interest to engage in CER practices to increase their own compensation [29].

Previous studies found that investments in social and environmental practices improve corporate image, enhance brand reputation, and increase consumer satisfaction, thereby allowing the firm to enter into a newly evolving environment-friendly market [30,31]. However, corporate investment and organizational practices depend on the decision-making ability of CEOs, who have the primary responsibility of defining a firm’s strategic direction and goals [32,33,34]. The relevant literature reveals that an engagement in social and environmental practices results from the individual cognition of decision-makers, which depends on personal values, social concerns, philanthropy, or self-interest in accordance with their managerial competencies (MCs) [35,36].

MC refers to a manager’s decision-making ability to effectively transform a firm’s resources into revenue [37]; extant studies claim that this is as an important intangible asset of an enterprise. Competent managers possess superior knowledge, skills, and experience that they exhibit in strategic business operation roles, leading to a better financial performance and the ability to solve complex tasks, such as rescuing a firm from operational distress, financial crisis, product market competition, and industrial shocks [3,38]. Competent managers consider social responsibility practices as a strategic tool to display their ethical approach in addressing social demands under risk [21,39]. Therefore, we hypothesize that competent managers utilize CER as a strategic instrument to demonstrate their ethical approaches in business activities.

Hypothesis 1 (H1).

MC positively influences CER.

Religiosity is an ethical social norm that tends to ensure fair practice, empathy, and accountability toward social well-being and collective prosperity [40]. Recent studies have widely utilized religious risk-taking attitudes as an empirical variable to proxy cultural factors to study a firm’s corporate behaviors [41]. Hilary and Hui [12] documented that firms headquartered in less religious areas are more subject to risk. In the US, the Catholic and Protestant populations diverge in accordance with their risk-taking preferences. Kumar et al. [42] showed evidence that in states dominated by a higher CPratio, Catholics were associated with more risk tolerance and lower investor protection than Protestants. Du et al. [43] identified a strong association between religion and the level of law enforcement, which alternatively urges corporate firms to pay attention to CER. Prior studies indicate that local religious risk-taking behavior affects managerial decision-making processes [16]. Stulz and Williamson [25] argued that cultural forces affect individual preferences and beliefs. According to social identity theory, individuals opt to work and live in areas where they can align their culture and beliefs to feel comfortable. Hilary and Hui [12] argued that CEOs consistently prefer to work in organizations that have the same local culture. Managers are very likely to be influenced by social interactions that share the same identity within the local culture, indicating that their decision-making is integrated with the local culture surrounding the firms’ headquarters. Prior research has argued that local religiosity provides a social norm that leads to a consciousness of social responsibility, which strengthens CER [43,44]. These arguments underlie our hypothesis that local religiosity influences managerial decisions that satisfy stakeholders’ expectations regarding social and environmental considerations.

Hypothesis 2 (H2).

Local religiosity positively moderates the MC and CER relationship.

Despite the continued debate on the cost and benefits of CER efforts, there is an inconclusive causal relationship between CER and CFP [1,2]. Competent managers not only leverage economic returns on the risks associated with an activity but they also endorse stakeholders’ expectations in business execution to gain social legitimacy for a firm’s actions [14]. According to the positive revisionist approach, addressing environmental issues provides intangible benefits that facilitate market expansion [30,31,45]. Prior studies document that CER activities allow firms to obtain crucial resources, and, importantly, Cho and Lee [46] find that competent managers implement Corporate Social Responsibility (CSR) strategies more efficiently, contributing to an improved firm performance. A recent study considers religious risk-taking attitudes as an important measurable cultural factor in defining a firm’s corporate behavior [41]. Du et al. [43] suggested that managers embed local social norms into corporate strategies to strengthen CER practices that customers consider when making purchase decisions [47,48]. The literature suggests that customers reduce their price sensitivity for additional satisfaction that is derived from consuming eco-friendly products. This in turn rewards the firm for its environmental efforts [49,50]. Several studies provide evidence that firms are penalized when buyers sense environmental irresponsibility or unethical activities that solely seek profit maximization [47,48]. Accordingly, we hypothesize that CER induced by the local religious risk-taking attitudes will positively impact a firm’s CFP.

Hypothesis 3 (H3).

Local religiosity positively moderates the CER and CFP relationship.

3. Data and Methodology

3.1. Sample Construction

Our sample consists of Newsweek’s green rankings (https://www.newsweek.com/green-2014/top-green-companies-u.s.-2014 (accessed on 6 January 2019), https://www.newsweek.com/green-2015/top-green-companies-u.s.-2015 (accessed on 6 January 2019), and https://www.newsweek.com/green-2016/top-green-companies-us-2016 (accessed on 7 January 2019)), which publish the environmental performances of the 500 largest publicly traded firms by market capitalization in the US annually. TNewsweek has been publishing green scores of firms since 2009 through its Green Rankings assessments. The Newsweek methodology was modified in 2011, 2014, 2015, and 2017 to strengthen the evaluation criteria. Currently, green scores for the years 2014 to 2016 are publicly available. Therefore, we selected the publications from 2014–2016 to obtain a recent publicly available and relatively large sample. We used the managerial ability (the managerial ability score was retrieved from http://faculty.washington.edu/pdemerj/data.html (accessed on 19 February 2019)) scores from Demerjian et al. [37] as a proxy for managerial competency, which relates to the creation of revenue by efficiently employing the resources of the firm, relative to the firm’s rivals in the market. To generalize and improve the explanatory power of the variable, we constructed a managerial competency dummy, with one denoting those above the median value and zero otherwise. Demerjian et al. [37] used the data envelopment analysis (DEA) method to evaluate the firm’s relative efficiency among their rivals, which are the firms in the same Fama French 48 industry industries [51]. The DEA objective function is defined based on the input factors of firm efficiency, such as cost of goods and services, selling, general and administrative expense, R&D, etc. This generated a firm-level efficiency measure, ranging from one for the most efficient firm to zero for the least efficient firm. Then, this firm efficiency was regressed on several firm characteristics in order to obtain managerial ability. Following Wu et al. [20], we used a local concentration of the CPratio as a proxy for firm risk induced by the religious risk-taking attitudes of the state in which the firm was located. We retrieved the state-level religious and demographic data from the American Religion Data Archive (http://www.thearda.com/Archive/ChState.asp (accessed on 24 February 2019)) (ARDA) and the US Census Bureau (https://factfinder.census.gov/faces/nav/jsf/pages/index.xhtml (accessed on 4 March 2019)). We collected financial data from COMPUSTAT and extracted CEO- and board-level data from Execucomp and the Institutional Shareholder Service (ISS, Rockville, MD, USA), respectively for our sample of US firms. We dropped firms for which the “gvkey” or “ticker” identifiers were not available for extracting and merging data from other sources. We used Newsweek’s industry sector classification following a firm’s two-digit Global Industry Classification Standard (GICS) code. Following previous studies, we excluded financial (GICS code 40 and SIC codes between and 6000–6999), utility (GISC code 55 and SIC code between 4900–4999), and real estate (GISC code 60) firms due to their unique operating environments [52].

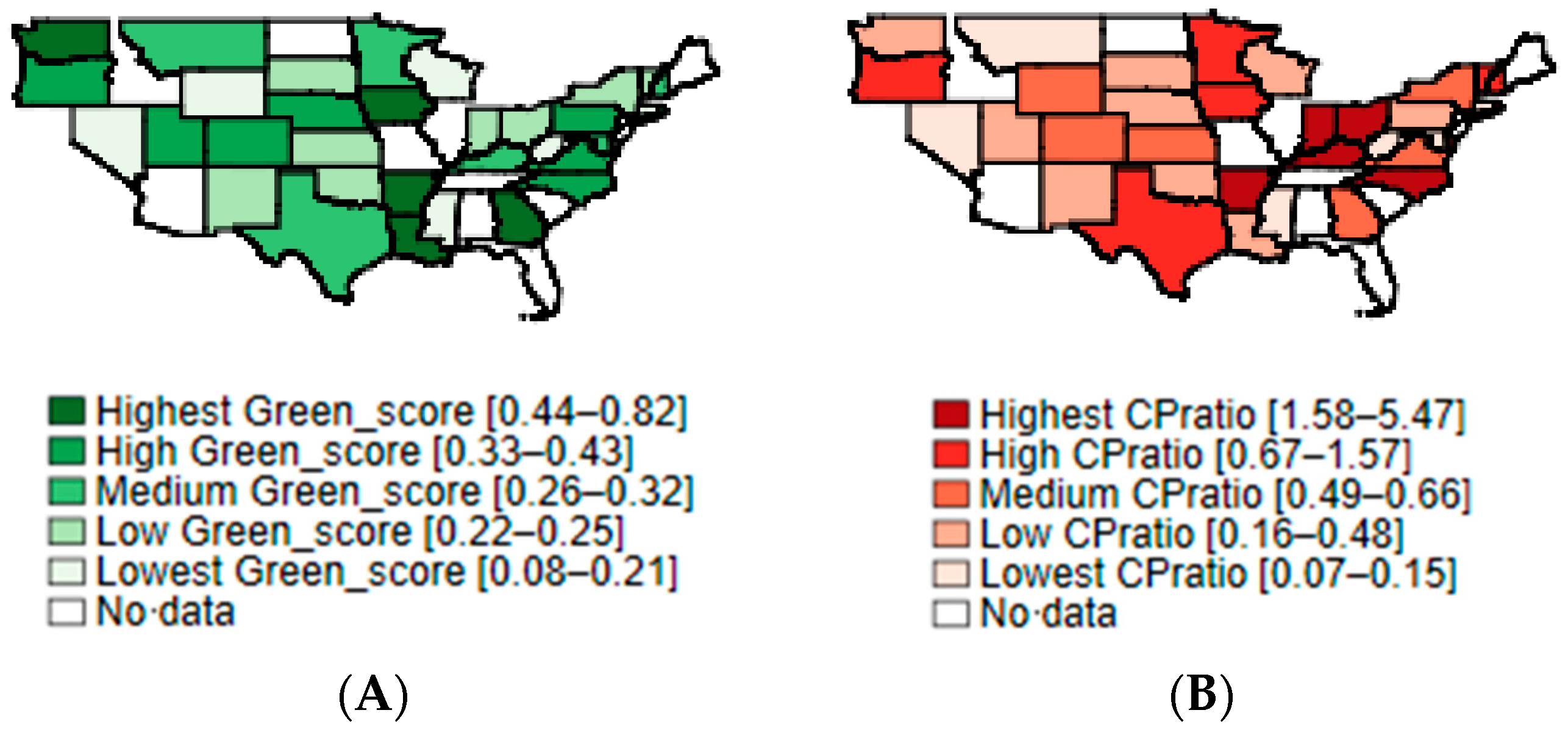

Panel (A) of Figure 1 presents the geographical distribution of the CER (Green_score) across the US. A greener shade indicates a higher state-level average CER. The green scores have reasonably high average values, indicating good green activities of the firms on average. Specifically, firms headquartered in the Washington, Iowa, Arkansas, Louisiana, Georgia, Oregon, Utah, Colorado, Nebraska, Texas, Minnesota, Kentucky, Pennsylvania, Virginia, North Carolina, and New Hampshire states seem to have relatively high CER practices.

Panel (B) of Figure 1 shows the geographical variations in state-level religious risk-taking behavior across the US. Apparently, the distribution of religiosity has a similar pattern to that of the Green_score illustrated in Panel (A). The CPratios have reasonably high average values, indicating, on average, high risk-taking behavior across the US. Firms headquartered in the Arkansas, Indiana, Ohio, Kentucky, North Carolina, Oregon, Texas, Minnesota, Iowa, Vermont, and New Hampshire states seem to have a relatively high CPratio. As expected, firms in high CPratio areas generally tend to engage in more CER activities.

3.2. Empirical Model

We employed Equation (1) to investigate the influence of managerial competency and local religious risk-taking attitudes (CPratio) on CER (Green_score and Green_rank) practices, extending the model in García-Sánchez et al. [53].

Then, we used Equation (2) to examine the impact of local religiosity and the firms’ CER practices on changes in the corporate financial performance (∆CFP) using ∆lnSALES which is, specifically, the difference between the natural logarithm of the ratio of the current and the previous year’s sales based on the model in Chang et al. [54].

Following previous studies, we included firm-level control variables including Firm_size (lnat), ROA, Leverage/assets, R&D/assets, standard deviation of cash flow (STD_CFO) from year t−2 to t, Dividend/assets, kz_index (Following Kim and Park [55], the Kaplan Zingales index is a linear combination of five accounting ratios after winsorizing the components at the bottom 1% and the top 99% level.), Capital_expenditures/assets, CEO_female, and CEO_duality [53,54]. We also controlled for CEOs older than 63 years old (CEO_older) as managers approaching retirement are more likely to be risk-averse and are less concerned about the firms’ long-term investments. Similarly, we controlled for Board_size and Board_independence to account for agency problems. We added state-level demographic characteristics, including local_seniors, median_income, median_house value, education, and population [56]. Finally, we controlled for year- and GICS sector-fixed effects to address unobserved time-invariant factors across the sectors. Appendix A provides the definitions and sources of each variable.

4. Results and Discussion

In Figure 1, geographical variations show that firms headquartered in Catholic-dominant states tend to be more environment-friendly and engage in more CER practices.

All the multivariate regressions show the variance inflation factor (VIF) statistics within the rule-of-thumb value of ten (VIF < 2.48), suggesting no multicollinearity concerns in our models. Similarly, F-statistics confirm the validity of the models in which the independent variables significantly describe the variation in the dependent variable. Appendix B presents the descriptive statistics.

Table 1 presents the regression results of Equation (1), with the CER as the dependent variable. Contrary to our expectation in Hypothesis 1, in Model (1), a negative correlation between managerial competency and CER with a strong statistical significance was observed, which indicates the lack of altruistic preference of competent managers for CER. This supports Chen and Ho’s [57] findings regarding managers’ perception of costly CER investment as having little or no financial benefit. The association between firm risk induced by local religious risk-taking attitudes and CER is not statistically significant, indicating that local religiosity may not directly impact CER undertakings. However, further results show that firm risk positively moderates the negative association between managerial competency and CER and complements Latan et al. [58] for environmental initiatives in response to potential benefits, which is consistent with Hypothesis 2. Overall, our findings indicate that competent managers perceive the value of CER and strategically utilize it when they sense any uncertainty or risk contesting firm performance. Our findings remain robust after employing alternative, dependent variables using the green rank (The green rank refers to the green score, which moves in the opposite direction such that a firm with the highest green score has the top rank one.) in Model (2) and lagged independent variables addressing possible reverse causality in Model (3) following Fernando et al. [59].

We further explored the relationship between firm risk and CER practices on CFP by employing Equation (2) and the results are presented in Table 2. In Model (1), we found that both CER and firm risk have a significant negative effect on ∆lnSALES, which indicates that local religious risk-taking attitudes and CER practices have a direct negative impact on CFP. Similarly, Sakunasingha et al. [60] show that a firm’s environment-friendly activities and profitability decline during a crisis. Managers ensure that the benefits outweigh the costs of CER investment to ensure survival, as scarce resources restrain managers and reduce the strength of an organization’s financial opportunities under risk [3,61]. Notably, the interaction term “CPratio × Green_score” has a positive effect on sales, consistent with Hypothesis 3, implying that CER practices help in mitigating local risks and contribute to CFP improvement. Our findings are consistent and robust with the lagged independent variable addressing possible reverse causality concerns in Model (2), following Fernando et al. [59]. The results suggest that CER practices are an essential tool for mitigating risk and improving sales in a risky business environment.

5. Conclusions

This study aimed to analyze the antecedents and consequences of environment-friendly corporate practices by exploring the joint effect of managerial competency and firm risk induced by local risk-taking attitudes on CER. Our results show that local religious risk-taking behavior is significantly associated with firms’ CER practices and mitigates the effect of local risk by improving stakeholder relationships. Notably, a firm’s risk motivates competent managers toward CER practices that they strategically incorporate in business practices to address stakeholders’ environmental concerns, which consequently results in a positive influence on the performance of the firm.

This study contributes to the literature on strategic management by documenting managerial competency to improve firm performance through the efficient execution of CER practices. It also complements the growing attention toward studies on the influence of external factors such as local religiosity on corporate behavior [8,9,10]. Similarly, practitioners may find this study valuable to strategically utilize CER practices to create value and mitigate the negative effects of a risky environment. Policymakers may find encouraging results from this work by formulating policies and regulations to encourage environment-friendly corporate activities.

6. Limitation and Future Studies

We acknowledge that the findings are subject to several limitations that may offer directions for future research. As is generally true with any empirical research, our results were subject to the availability of data. Two obvious threats to the validity of our results are (1) the truncated and (2) the longitudinal nature of the data. First, although we demonstrated the interaction of managerial competency and local religious risk-taking attitudes on corporate environment responsibility for publicly traded large-sized US firms, the exclusion of small-or medium-sized firms may have resulted in an incidental truncation issue since more capable managers can be hired by larger companies. Moreover, small-or medium-sized firms that may be governed by different sets of priorities in terms of corporate decisions may reflect a variance in CER affinity. In addition, and the relationships of our interest variables with the CER may be affected by policy, culture, regulation, and people’s attention, and thus an extension into other countries would allow us to control such omitted variables for CER activities. Second, even though our results show the role of managerial competency during our time period, i.e., three-years, it is possible that regionalisms accrued from a religion or increasing interests on the environmental issues have greatly improved the CER. We partially reduced such heterogeneity issues by controlling year- and sector- fixed effects, but the three years may not have been sufficient. Future research could be devoted to extending these results through additional countries, companies, and years of data.

Moreover, other external factors such as corporate governance, local demographics, culture, and market competition may also motivate CER practices. For instance, the CER is found to be affected by the compensation structure [29], firm visibility in the media [4], social capital [5], and product market competition [3]. More comprehensively, Gillan et al. [62] reviewed the financial economics based on previous studies focusing on various determinants such as market characteristics, boards and executives, ownership characteristics, firm risk, and firm performance and value on ESG and CSR in corporate finance. Therefore, future studies may consider these issues to provide robust results and establish a greater consensus on the study of religiosity, managerial competencies, and CER practices.

Our dataset is also not free from potential measurement errors and endogeneity issues, both of which may bring biased estimators. With respect to measurement errors, we utilized Newsweek’s green score data for CER, and Demerjian et al. [37] for managerial competency. The former may not be a serious issue since the measurement error of a dependent variable often causes inefficiency, but not bias. However, the latter can be an issue, but we considered the most commonly used measurement by academics. To control reverse causality where a firm that invests more on CER may hire more competent management, we used a lagged independent variable, following Fernando et al. [57], and the results are qualitatively the same with unlagged independent variables.

Author Contributions

This research work is an outcome of joint efforts of the four authors. Conceptualization, C.T. and P.L.Y.; methodology, C.T., P.L.Y., S.K., and S.H.; software, S.H.; validation, C.T., S.K., and S.H.; formal analysis, C.T. and P.L.Y.; investigation, C.T. and P.L.Y.; resources, S.H.; data curation, C.T., S.H., and P.L.Y.; writing—original draft preparation, C.T., and P.L.Y.; writing—review and editing, S.K., and P.L.Y.; visualization, S.K.; supervision, S.H. and P.L.Y.; project administration, S.H. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Not applicable.

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A. Variable Definitions and Data Sources

| Definition | Data Sources | |

| Dependent Variables | ||

| Green_Scoret | The weighted average of the eight fundamental indicators:

| NEWSWEEK |

| Green_Rank | Green Rank is 1 if the firm scores the highest Green Score in a year relative to all published firms | NEWSWEEK |

| ∆lnSALES | Sales change natural logarithm of current sales (SALEi,t) minus lagged sales (SALEi,t−1) | COMPUSTAT |

| Independent Variables | ||

| Managerial_competency | Dummy equals to one if the managerial competency is above the median value and zero otherwise | Demerjian et al. (2012) [37] |

| Managerial_competency_lagged | Managerial_competency i,t−1 | Demerjian et al. (2012) [37] |

| CPratio | Proportion of Catholic to Protestant adherents in which a firm is located | ARDA |

| CPratio_lagged | Lagged ratio of Catholic over Protestant (CPratioi,t−1)_ | ARDA |

| Green_score_lagged | Lagged green score (Green_Scorei,t−1) | NEWSWEEK |

| Firm-Level Control Variables | ||

| Firm_size (lnat) | Natural logarithm of total assets (ATi,t) | COMPUSTAT |

| ROAi,t | NIi,t/ATi,t | COMPUSTAT |

| Leverage/assetsi,t | (DLCi,t + DLTTi,t)/ATi,t | COMPUSTAT |

| R&D/assets | Research and development expense (XRDi,t) over ATi,t if XRDi,t is not missing and zero otherwise | COMPUSTAT |

| Standard deviation of CFO (STD_CFO) | Standard deviation of cash flow from CFOi,t-2 to CFOi,t where: Cash flow (CFO) is measured by income before extraordinary items (IBi,t) plus depreciation and amortization (DPi,t) scaled by ATi,t if DPi,t is not missing and IBi,t/ATi,t otherwise | COMPUSTAT |

| Dividend/assets | Common dividends (DVCi,t) plus preferred dividends (DVPi,t) scaled by ATi,t | COMPUSTAT |

| kz_indexi,t | Kaplan zingales index: kz_indexi,t = −1.001909 * CFOi,t + 0.2826389 * Tobin’s Qi,t + 3.139193 * Debt to total capitali,t − 39.3678 * Dividendi,t − 1.314759 * Cashholdingsi,t where:

| COMPUSTAT |

| Capital_expenditures/assets | Capital expenditure (CAPXi,t) minus sale of property (SPPEi,t) scaled by ATi,t if SPPEi,t is not missing and CAPXi,t/ATi,t otherwise | COMPUSTAT |

| Corporate Governance Control Variables | ||

| Board_independence | Number of outside directors scaled by the total number of the board directors | ISS |

| Board_size | Total number of directors on the board | ISS |

| CEO_female | Dummy equals to one if the CEO is female and zero otherwise | EXECUCOMP |

| CEO_older | Dummy equals to one if the CEO age is older than 63 and zero otherwise | EXECUCOMP |

| CEO_duality | Dummy equals to one if the CEO is also the chair of the board of directors and zero otherwise | EXECUCOMP |

| State-Level Demographic Control Variables Where a Firm is Located | ||

| Local_seniors | Proportion of people older than 65 years | U.S. CENSUS |

| Median_income | Median household income | U.S. CENSUS |

| Median_housevalue | Median house value | U.S. CENSUS |

| Education | Proportion of the population with college degrees | U.S. CENSUS |

| Population | Natural logarithm of population | U.S. CENSUS |

Appendix B. Descriptive Statistics

| Observations | Mean | Standard Deviation | Min | Max | |

| Dependent Variables | |||||

| Green_score | 1007 | 0.33 | 0.20 | 0.00 | 0.89 |

| Green_rank | 1007 | 241.43 | 143.36 | 1.00 | 500.00 |

| ∆lnSALES | 640 | 6.39 | 1.51 | −0.68 | 10.84 |

| Independent Variables | |||||

| CPratio | 975 | 1.38 | 1.26 | 0.07 | 5.49 |

| Firm-Level Control Variables | |||||

| Firm_size (lnat) | 1005 | 9.68 | 1.20 | −2.06 | 13.38 |

| ROA | 1005 | 0.06 | 0.20 | −5.22 | 0.35 |

| Leverage/assets | 1001 | 0.31 | 0.18 | 0.00 | 1.67 |

| R&D/assets | 1007 | 0.03 | 0.05 | 0.00 | 0.48 |

| Standard deviation of cash flow (STD_CFO) | 1003 | 0.36 | 2.71 | 0.00 | 78.63 |

| Dividend/assets | 1001 | 0.03 | 0.04 | 0.00 | 0.64 |

| kz_index | 838 | −9.54 | 15.62 | −105.32 | 5.49 |

| Capital_expenditures/assets | 1004 | 0.05 | 0.05 | −0.00 | 0.36 |

| State-Level Demographic Control Variables Where a Firm is Located | |||||

| Local_seniors | 975 | 0.14 | 0.02 | 0.11 | 0.19 |

| Median_income | 975 | 28,178.54 | 2891.68 | 22,067.00 | 41,160.00 |

| Median_house value | 975 | 242,046.46 | 94,708.03 | 123,800.00 | 520,600.00 |

| Education | 975 | 19.21 | 2.22 | 12.90 | 24.40 |

| Population | 975 | 16.33 | 0.81 | 13.33 | 17.49 |

| Board-Level Control Variables | |||||

| Board_size | 793 | 10.72 | 1.82 | 5.00 | 17.00 |

| Board_independence | 793 | 0.83 | 0.10 | 0.46 | 0.94 |

| CEO-Level Dummy Control Variables | |||||

| Managerial_competency | 938 | 0.09 | 0.20 | ||

| CEO_female | 1007 | 0.04 | 0.19 | ||

| CEO_older | 1007 | 0.20 | 0.40 | ||

| CEO_duality | 793 | 0.52 | 0.50 | ||

References

- Orlitzky, M.; Schmidt, F.L.; Rynes, S.L. Corporate Social and Financial Performance: A Meta-Analysis. Organ. Stud. 2003, 24, 403–441. [Google Scholar] [CrossRef]

- Busch, T.; Friede, G. The Robustness of the Corporate Social and Financial Performance Relation: A Second-Order Meta-Analysis. Corp. Soc. Responsib. Environ. Manag. 2018, 25, 583–608. [Google Scholar] [CrossRef] [Green Version]

- Tsendsuren, C.; Yadav, P.L.; Han, S.H.; Kim, H. Influence of Product Market Competition and Managerial Competency on Corporate Environmental Responsibility: Evidence from the US. J. Clean. Prod. 2021, 304, 127065. [Google Scholar] [CrossRef]

- Li, Z.F.; Liang, C.Y.C.; Tang, Z. CEO Social Media Presence and Insider Trading Behavior. SSRN Electron. J. 2020, 1–26. [Google Scholar] [CrossRef]

- Jha, A.; Cox, J. Corporate Social Responsibility and Social Capital. J. Bank. Financ. 2015, 60, 252–270. [Google Scholar] [CrossRef]

- Adhikari, B.K.; Agrawal, A. Does Local Religiosity Matter for Bank Risk-Taking? J. Corp. Financ. 2016, 38, 272–293. [Google Scholar] [CrossRef]

- Tsendsuren, C.; Yadav, P.L.; Han, S.H.; Mun, S. The Effect of Corporate Environmental Responsibility and Religiosity on Corporate Cash Holding Decisions and Profitability: Evidence from the United States’ Policies for Sustainable Development. Sustain. Dev. 2021, 1. [Google Scholar] [CrossRef]

- Agle, B.R.; Van Buren, H.J. God and Mammon: The Modern Relationship. Bus. Ethics Q. 1999, 9, 563–582. [Google Scholar] [CrossRef]

- Guiso, L.; Sapienza, P.; Zingales, L. Does Culture Affect Economic Outcomes? J. Econ. Perspect. 2006, 20, 23–48. [Google Scholar] [CrossRef] [Green Version]

- Brown, D.L.; Vetterlein, A.; Roemer-Mahler, A. Theorizing Transnational Corporations as Social Actors: An Analysis of Corporate Motivations. Bus. Polit. 2010, 12, 1–37. [Google Scholar] [CrossRef]

- Kwon, S.A.; Kim, S.; Lee, J.E. Analyzing the Determinants of Individual Action on Climate Change by Specifying the Roles of Six Values in South Korea. Sustainability 2019, 11, 1834. [Google Scholar] [CrossRef] [Green Version]

- Hilary, G.; Hui, K.W. Does Religion Matter in Corporate Decision Making in America? J. Financ. Econ. 2009, 93, 455–473. [Google Scholar] [CrossRef]

- Papagiannakis, G.; Lioukas, S. Values, Attitudes and Perceptions of Managers as Predictors of Corporate Environmental Responsiveness. J. Environ. Manag. 2012, 100, 41–51. [Google Scholar] [CrossRef] [PubMed]

- García-Sánchez, I.M.; Martínez-Ferrero, J. Chief Executive Officer Ability, Corporate Social Responsibility, and Financial Performance: The Moderating Role of the Environment. Bus. Strateg. Environ. 2018, 28, 542–555. [Google Scholar] [CrossRef]

- Attig, N.; Cleary, S. Managerial Practices and Corporate Social Responsibility. J. Bus. Ethics 2015, 131, 121–136. [Google Scholar] [CrossRef]

- Chatjuthamard-Kitsabunnarat, P.; Jiraporn, P.; Tong, S. Does Religious Piety Inspire Corporate Social Responsibility (CSR)? Evidence from Historical Religious Identification. Appl. Econ. Lett. 2014, 21, 1128–1133. [Google Scholar] [CrossRef]

- Grullon, G.; Kanatas, G.; Weston, J. Religion and Corporate (Mis)Behavior. Available SSRN 2009. [Google Scholar] [CrossRef] [Green Version]

- Dyreng, S.D.; Mayew, W.J.; Williams, C.D. Religious Social Norms and Corporate Financial Reporting. J. Bus. Financ. Account. 2012, 39, 845–875. [Google Scholar] [CrossRef]

- McGuire, S.T.; Omer, T.C.; Sharp, N.Y. The Impact of Religion on Financial Reporting Irregularities. Account. Rev. 2012, 87, 645–673. [Google Scholar] [CrossRef]

- Wu, D.; Lin, C.; Liu, S. Does Community Environment Matter to Corporate Social Responsibility? Financ. Res. Lett. 2016, 18, 127–135. [Google Scholar] [CrossRef]

- Chatjuthamard, P.; Jiraporn, P.; Tong, S.; Singh, M. Managerial Talent and Corporate Social Responsibility (CSR): How Do Talented Managers View Corporate Social Responsibility? Int. Rev. Financ. 2016, 16, 265–276. [Google Scholar] [CrossRef]

- Williamson, D.; Lynch-Wood, G.; Ramsay, J. Drivers of Environmental Behaviour in Manufacturing SMEs and the Implications for CSR. J. Bus. Ethics 2006, 67, 317–330. [Google Scholar] [CrossRef]

- Kim, H.; Park, K.; Ryu, D. Corporate Environmental Responsibility: A Legal Origins Perspective. J. Bus. Ethics 2017, 140, 381–402. [Google Scholar] [CrossRef]

- Karolyi, G.A. The Gravity of Culture for Finance. J. Corp. Financ. 2016, 41, 610–625. [Google Scholar] [CrossRef]

- Stulz, R.M.; Williamson, R. Culture, Openness, and Finance. J. Financ. Econ. 2003, 70, 313–349. [Google Scholar] [CrossRef] [Green Version]

- Greco, M.; Cricelli, L.; Grimaldi, M. A Strategic Management Framework of Tangible and Intangible Assets. Eur. Manag. J. 2013, 31, 55–66. [Google Scholar] [CrossRef]

- Yadav, P.L.; Han, S.H.; Kim, H. Sustaining Competitive Advantage through Corporate Environmental Performance. Bus. Strateg. Environ. 2017, 26, 345–357. [Google Scholar] [CrossRef]

- Luth, M.T.; Schepker, D.J. Antecedents of Corporate Social Performance: The Effects of Task Environment Managerial Discretion. Soc. Responsib. J. 2017, 13, 339–354. [Google Scholar] [CrossRef]

- Ikram, A.; Li, Z.F.; MacDonald, T. CEO Pay Sensitivity (Delta and Vega) and Corporate Social Responsibility. Sustainability 2020, 12, 7941. [Google Scholar] [CrossRef]

- Porter, M.E.; Linde, C. van der. Toward a New Conception of the Environment-Competitiveness Relationship. J. Econ. Perspect. 1995, 9, 97–118. [Google Scholar] [CrossRef]

- Ruf, B.M.; Muralidhar, K.; Brown, R.M.; Janney, J.J.; Paul, K. An Empirical Investigation of the Relationship between Change in Corporate Social Performance and Financial Performance: A Stakeholder Theory Perspective. J. Bus. Ethics 2001, 32, 143–156. [Google Scholar] [CrossRef]

- Porter, M.E. Competitive Advantage: Creating and Sustaining Superior Performance; NY Free Press: New York, NY, USA, 1985. [Google Scholar]

- Bertrand, M.; Schoar, A. Managing with Style: The Effect of Managers on Firm Policies. Q. J. Econ. 2003, 118, 1169–1208. [Google Scholar] [CrossRef] [Green Version]

- Leverty, J.T.; Grace, M.F. Dupes or Incompetents? An Examination of Management’s Impact on Firm Distress. J. Risk Insur. 2012, 79, 751–783. [Google Scholar] [CrossRef]

- Fisman, R.; Heal, D.; Nair, V. A Model of Corporate Philanthropy; Working Paper; Columbia University: New York, NY, USA, 2007; Available online: http://knowledge.wharton.upenn.edu/wp-content/uploads/2013/09/13311.pdf (accessed on 22 May 2021).

- Hubbard, T.D.; Christensen, D.M.; Graffin, S.D. Higher Highs and Lower Lows: The Role of Corporate Social Responsibility in CEO Dismissal. Strateg. Manag. J. 2017, 38, 2255–2265. [Google Scholar] [CrossRef]

- Demerjian, P.R.; Lev, B.; McVay, S.E. Quantifying Managerial Ability: A New Measure and Validity Tests. Manag. Sci. 2012, 58, 1229–1248. [Google Scholar] [CrossRef] [Green Version]

- Bagnoli, M.; Watts, S.G. Selling to Socially Responsible Consumers: Competition and the Private Provision of Public Goods. J. Econ. Manag. Strateg. 2003, 12, 419–445. [Google Scholar] [CrossRef]

- Quairel-Lanoizelee, F. Are Competition and Corporate Social Responsibility Compatible? The Myth of Sustainable Competitive Advantage. Soc. Bus. Rev. 2016, 11, 130–154. [Google Scholar] [CrossRef]

- Callen, J.L.; Fang, X. Religion and Stock Price Crash Risk. J. Financ. Quant. Anal. 2015, 50, 169–195. [Google Scholar] [CrossRef] [Green Version]

- Hu, H.; Lian, Y.; Zhou, W. Do Local Protestant Values Affect Corporate Cash Holdings? J. Bus. Ethics 2019, 154, 147–166. [Google Scholar] [CrossRef]

- Kumar, A.; Page, J.K.; Spalt, O.G. Religious Beliefs, Gambling Attitudes, and Financial Market Outcomes. J. Financ. Econ. 2011, 102, 671–708. [Google Scholar] [CrossRef] [Green Version]

- Du, X.; Jian, W.; Zeng, Q.; Du, Y. Corporate Environmental Responsibility in Polluting Industries: Does Religion Matter? J. Bus. Ethics 2014, 124, 485–507. [Google Scholar] [CrossRef] [Green Version]

- Fang, W.T.; Kaplan, U.; Chiang, Y.T.; Cheng, C.T. Is Religiosity Related to Environmentally-Protective Behaviors among Taiwanese Christians? A Structural Equation Modeling Study. Sustainability 2020, 12, 8999. [Google Scholar] [CrossRef]

- Lev, B.; Petrovits, C.; Radhakrishnan, S. Is Doing Good Good for You? How Corporate Charitable Contributions Enhance Revenue Growth. Strateg. Manag. J. 2010, 31, 182–200. [Google Scholar] [CrossRef]

- Cho, S.Y.; Lee, C. Managerial Efficiency, Corporate Social Performance, and Corporate Financial Performance. J. Bus. Ethics 2019, 158, 467–486. [Google Scholar] [CrossRef]

- Brown, T.J.; Dacin, P.A. The Company and the Product: Corporate Associations and Consumer Product Responses. J. Mark. 1997, 61, 68. [Google Scholar] [CrossRef] [Green Version]

- Luo, X.; Bhattacharya, C.B. Corporate Social Responsibility, Customer Satisfaction, and Market Value. J. Mark. 2006, 70, 1–18. [Google Scholar] [CrossRef]

- Yadav, P.L.; Han, S.H.; Kim, H. Manager’s Dilemma: Stockholders’ and Consumers’ Responses to Corporate Environmental Efforts. Sustainability 2017, 9, 1108. [Google Scholar] [CrossRef] [Green Version]

- Yadav, P.L.; Han, S.H.; Rho, J.J. Impact of Environmental Performance on Firm Value for Sustainable Investment: Evidence from Large US Firms. Bus. Strateg. Environ. 2016, 25, 402–420. [Google Scholar] [CrossRef]

- Fama, E.F.; French, K.R. Industry Costs of Equity. J. Financ. Econ. 1997, 43, 153–193. [Google Scholar] [CrossRef]

- Adhikari, B.K. Female Executives and corporate Cash Holdings. Appl. Econ. Lett. 2018, 25, 958–963. [Google Scholar] [CrossRef]

- García-Sánchez, I.M.; Hussain, N.; Martínez-Ferrero, J. An Empirical Analysis of the Complementarities and Substitutions between Effects of Ceo Ability and Corporate Governance on Socially Responsible Performance. J. Clean. Prod. 2019, 215, 1288–1300. [Google Scholar] [CrossRef]

- Chang, K.; Kim, I.; Li, Y. The Heterogeneous Impact of Corporate Social Responsibility Activities That Target Different Stakeholders. J. Bus. Ethics 2014, 125, 211–234. [Google Scholar] [CrossRef]

- Kim, J.; Park, J.L. How Do Financial Constraint and Distress Measures Compare? Invest. Manag. Financ. Innov. 2015, 12, 41–50. [Google Scholar]

- Ucar, E. Local Culture and Dividends. Financ. Manag. 2016, 45, 105–140. [Google Scholar] [CrossRef] [Green Version]

- Chen, C.M.; Ho, H. Who Pays You to Be Green? How Customers’ Environmental Practices Affect the Sales Benefits of Suppliers’ Environmental Practices. J. Oper. Manag. 2019, 65, 333–352. [Google Scholar] [CrossRef]

- Latan, H.; Chiappetta Jabbour, C.J.; Lopes de Sousa Jabbour, A.B.; Wamba, S.F.; Shahbaz, M. Effects of Environmental Strategy, Environmental Uncertainty and Top Management’s Commitment on Corporate Environmental Performance: The Role of Environmental Management Accounting. J. Clean. Prod. 2018, 180, 297–306. [Google Scholar] [CrossRef]

- Fernando, C.S.; Sharfman, M.P.; Uysal, V.B. Corporate Environmental Policy and Shareholder Value: Following the Smart Money. J. Financ. Quant. Anal. 2017, 52, 2023–2051. [Google Scholar] [CrossRef]

- Sakunasingha, B.; Jiraporn, P.; Uyar, A. Which CSR Activities Are More Consequential? Evidence from the Great Recession. Financ. Res. Lett. 2018, 27, 161–168. [Google Scholar] [CrossRef]

- Hart, O.D. The Market Mechanism as an Incentive Scheme. Bell J. Econ. 1983, 14, 366. [Google Scholar] [CrossRef]

- Gillan, S.L.; Koch, A.; Starks, L.T. Firms and Social Responsibility: A Review of ESG and CSR Research in Corporate Finance. J. Corp. Financ. 2021, 66, 101889. [Google Scholar] [CrossRef]

Figure 1.

Panel (A): State-level CER (Green_score) across the US, based on Newsweek’ green rankings 2016. Panel (B): State-level religious risk-taking (CPratio) across the United States based on ARDA data for 2016.

Figure 1.

Panel (A): State-level CER (Green_score) across the US, based on Newsweek’ green rankings 2016. Panel (B): State-level religious risk-taking (CPratio) across the United States based on ARDA data for 2016.

{kind=link}

Table 1.

Managerial competency and local religious risk-taking attitudes (CPratio) on corporate environmental responsibility (CER).

Table 1.

Managerial competency and local religious risk-taking attitudes (CPratio) on corporate environmental responsibility (CER).

| Dependent Variable: CER | |||

|---|---|---|---|

| (1) | (2) | (3) | |

| Green_Score | Green_Rank | Green_Score | |

| Managerial_competency | −0.1527 *** | 93.0707 ** | |

| (−2.80) | (2.47) | ||

| CPratio | 0.0132 | −12.0631 * | |

| (1.41) | (−1.86) | ||

| Managerial_competency × CPratio | 0.0708 ** | −34.6109 * | |

| (2.38) | (−1.68) | ||

| Managerial_competency_lagged | −0.1647 ** | ||

| (−2.56) | |||

| CPratio_lagged | 0.0106 | ||

| (0.91) | |||

| Managerial_competency_lagged × CPratio_lagged | 0.0720 ** | ||

| (2.12) | |||

| Firm_size (lnat) | 0.0461 *** | −34.9903 *** | 0.0529 *** |

| (6.31) | (−6.94) | (5.84) | |

| ROA | 0.1496 | −92.6416 | 0.0577 |

| (1.62) | (−1.45) | (0.56) | |

| Leverage/assets | 0.0493 | −39.5733 | 0.0925 |

| (1.04) | (−1.21) | (1.59) | |

| R&D/assets | 0.5023 ** | −359.2799 ** | 0.2167 |

| (2.38) | (−2.46) | (0.86) | |

| Standard deviation of cash flow (STD_CFO) | −0.0429 * | 32.0222 * | −0.0316 |

| (−1.66) | (1.80) | (−0.87) | |

| Dividend/assets | 0.8842 *** | −683.3069 *** | 1.2184 *** |

| (2.72) | (−3.04) | (3.18) | |

| kz_index | 0.0002 | −0.0504 | 0.0007 |

| (0.33) | (−0.11) | (0.92) | |

| Capital_expenditures/assets | −0.0226 | −34.9604 | 0.1013 |

| (−0.11) | (−0.24) | (0.35) | |

| Local_seniors | −0.8562 | 614.0931 | −0.0039 |

| (−1.48) | (1.54) | (−0.01) | |

| Median_income | 0.0000 | −0.0013 | 0.0000 |

| (0.45) | (−0.37) | (0.07) | |

| Median_housevalue | 0.0000 ** | −0.0002 ** | 0.0000 ** |

| (2.34) | (−1.97) | (2.47) | |

| Education | −0.0060 | 3.9591 | −0.0055 |

| (−0.87) | (0.83) | (−0.66) | |

| Population | −0.0100 | 4.0981 | −0.0091 |

| (−0.78) | (0.46) | (−0.56) | |

| CEO_female | −0.1393 *** | 100.5165*** | −0.1121 ** |

| (−3.89) | (4.06) | (−2.46) | |

| CEO_older | 0.0056 | −0.7591 | 0.0078 |

| (0.25) | (−0.05) | (0.27) | |

| CEO_duality | −0.0331** | 25.6535** | −0.0175 |

| (−2.14) | (2.41) | (−0.92) | |

| Board_size | 0.0194 *** | −13.8034 *** | 0.0175 *** |

| (4.49) | (−4.62) | (3.29) | |

| Board_indepdence | 0.2738 *** | −189.4556 *** | 0.2951 *** |

| (3.35) | (−3.35) | (2.87) | |

| Year and sector fixed effects | Yes | Yes | Yes |

| Constant | −0.3491 | 757.8986 *** | −0.5043 |

| Adjusted R2 | 0.3269 | 0.3392 | 0.3407 |

| F-statistics | 9.8649 *** | 10.5465 *** | 6.9464 *** |

| Number of observations | 622 | 622 | 372 |

*, **, and *** indicate the significance level of 10%, 5%, and 1% based on a two-sided t-test, respectively. The p-values are in parentheses.

Table 2.

Local religious risk-taking attitudes (CPratio) and corporate environmental responsibility (CER) on corporate financial performance (CFP).

Table 2.

Local religious risk-taking attitudes (CPratio) and corporate environmental responsibility (CER) on corporate financial performance (CFP).

| Dependent Variable: CFP | ||

|---|---|---|

| (1) | (2) | |

| ∆lnSALES | ∆lnSALES | |

| CPratio | −0.2157 ** | |

| (−2.20) | ||

| Green_score | −1.4762 *** | |

| (−3.54) | ||

| CPratio × Green_score | 0.3727 ** | |

| (1.99) | ||

| CPratio_lagged | −0.2502 * | |

| (−1.83) | ||

| Green_score_lagged | −1.9170 *** | |

| (−3.06) | ||

| CPratio_lagged × Green_score_lagged | 0.4731 * | |

| (1.77) | ||

| Controls same as Table 1 | Yes | Yes |

| Year and sector fixed effects | Yes | Yes |

| Constant | 4.8037 ** | 6.6230 * |

| Adjusted R2 | 0.5270 | 0.5257 |

| F-statistics | 18.7076 *** | 11.1054 *** |

| Number of observations | 414 | 225 |

*, **, and *** indicate the significance level of 10%, 5%, and 1% based on a two-sided t-test, respectively. The p-values are in parentheses.

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Tsendsuren, C.; Yadav, P.L.; Kim, S.; Han, S. The Effects of Managerial Competency and Local Religiosity on Corporate Environmental Responsibility. Sustainability 2021, 13, 5857. https://doi.org/10.3390/su13115857

AMA Style

Tsendsuren C, Yadav PL, Kim S, Han S. The Effects of Managerial Competency and Local Religiosity on Corporate Environmental Responsibility. Sustainability. 2021; 13(11):5857. https://doi.org/10.3390/su13115857

Chicago/Turabian StyleTsendsuren, Chuluunbat, Prayag Lal Yadav, Sangsoo Kim, and Seunghun Han. 2021. "The Effects of Managerial Competency and Local Religiosity on Corporate Environmental Responsibility" Sustainability 13, no. 11: 5857. https://doi.org/10.3390/su13115857

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.