Revisiting the Missing Link: An Ecological Theory of Money for a Regenerative Economy

1

CENSE—Center for Environmental and Sustainability Research, School of Science and Technology, NOVA University Lisbon, 2829-516 Caparica, Portugal

2

Centre for Ecology, Evolution and Environmental Change (cE3c), Faculty of Sciences, University of Lisbon, 1749-016 Lisboa, Portugal

*

Author to whom correspondence should be addressed.

Sustainability 2022, 14(7), 4309; https://doi.org/10.3390/su14074309

Submission received: 8 March 2022

/

Revised: 27 March 2022

/

Accepted: 1 April 2022

/

Published: 5 April 2022

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Abstract

:Money is critical for a regenerative future. Transforming it is an unavoidable social, political, and economic endeavor that must be a global priority if we are to prevent future financial crises, reduce economic inequality and adhere to our climate agreements and sustainability goals. For this transition to occur, we urgently need new economic and monetary paradigms that address the root causes of our current unsustainability, offer a new monetary ontology and design, and, more importantly, steer our monetary regime towards the regeneration of our social, economic and ecological landscapes. We need an ecological understanding of money grounded in Ecological Economics and an Ecological Value Theory that lays down the foundations for the conscious democratization, decentralization, and diversification of money. In this work, we revisit and update the missing link between money and sustainability by proposing new ontological avenues and reviewing the design elements and degenerative processes built into the existing system. We also contribute to the development and emergence of an Ecological Monetary Economics by systematizing the ongoing monetary transition toward sustainability and by offering a set of principles drawn from the regenerative economics literature for the conscious design of monetary ecosystems that contribute positively to solving our societal challenges of the 21st century.

1. Introduction

Much has been written in the aftermath of the 2008 global financial crisis (GFC) on the causes, the consequences, and the actors of this tremendous financial shock to our economies. Its sheer magnitude, cascading societal impact, and long-lasting ripples forced scholars and politicians to dig deeper than ever before for answers, while it opened up spaces for increasingly unorthodox ideas and debates to surface, namely in terms of money, banking, and finance [1]. It was a ‘landscape shock’ strong enough to crack open the monetary–banking–financial regime, leading to widespread niche innovations, such as complementary currencies, and the strengthening of alternative monetary theories, such as Modern Monetary Theory. It gave rise to social movements such as ‘Move Your Money’ campaigns, ‘Public Banking’ or ‘Slow Money’ [1].

Within the tsunami of articles and publications analyzing the events, the triggers, and the fragilities within the current monetary, banking, and international financial system (IMS hereafter), a rogue report authored by a group of transdisciplinary thinkers, stood out with a fresh and out-of-the-mainstream perspective on the financial crisis, monetary design and the central role of money in our current economies. “Money and Sustainability: The Missing Link”, published in 2013 [2], argued a simple yet radical idea: our monetary system lies at the center of the (un)sustainability of our current societies, and therefore, it cannot be, naively or intentionally, considered neutral, exogenous or innocuous to our economies. More adequately, it should be seen as part of an invisible matrix, solely questioned, that locks us into instability, inequality, and unsustainability [2,3,4]. This crucial link between money and sustainability, mostly absent in mainstream monetary thinking, is argued to be the critical missing part in neoclassical monetary theory and a key piece in the necessary transformation of our monetary system if we are to avert the “triple crunch”: another significant financial crisis, socioeconomic inequality and instability, and ecological disaster [5,6,7]. Undoubtedly, the responsibility for the current ecological and socioeconomic situation in the world cannot be solely attributed to our monetary system. However, Lietaer et al. [2] argue that in our increasingly monetized societies, where so much economic and political power has become dependent on how money is supplied, allocated, and (re)distributed, one cannot exclude it as an important explanatory variable.

Nevertheless, and until the GFC, there was apparent myopia, disregard, or discomfort, in approaching this linkage and challenging mainstream monetary thought in some of its working assumptions, such as the neutrality and the exogeneity of money, the single-currency hegemony, the privatization of money issuing or the necessary full liberalization of banking and finance. Although those assumptions and strongly held beliefs at the core of monetarism and monetary policy in OECD countries since the 1970s have been in the spotlight and under scrutiny, this is yet to translate into any significant or radical change [8,9,10]. In the past decade, we have missed a unique window of opportunity for collective and timely monetary transformation and the looming public-and-private debt crisis ahead [11], record-breaking inequality levels [12], together with the acceleration of ecological and social degradation [13,14] and the unique challenges posed by the COVID-19 pandemic to sustainability worldwide [15], make the missing link ever more relevant.

Adding to the reasons highlighted above, we would add three more for the importance of resurfacing the missing link and grounding a new ecological, monetary paradigm: (1) mainstream monetary theory is unable and incapable of understanding and integrating the complexity of monetary innovations booming after 2009; (2) alternative monetary economics, such as Modern Monetary Theory, is not addressing the fundamental degenerative processes within the monetary system; (3) a diverse, complex, and complementary monetary ecosystem requires an ecological perspective than can inspire and guide monetary designers and policy-makers.

As Romain Svartzman and colleagues summarize, we need to develop “a new monetary order embedded in a worldview that acknowledges the finiteness and incommensurable values of Earth’s life support systems” [16] (p. 109). As we step, willingly or not, into unorthodox monetary terrain, a new conceptual framework is needed. This is something that an ecology of money can offer and that we aim to enrich and continue with the present work. As Donella Meadows pointed out, the most effective leverage point to intervene in a system is at the core of its working paradigms and mindset [17]. This paper aims not only to revisit the missing link but mainly to continue the development of ecological monetary economics that contributes to the transformation urgently needed in our current monetary and banking system. In this respect, Section 1 summarizes the key ideas and arguments in the existing literature for a structural transformation within monetary theory and the links between money and society. Section 2 debates the next steps within the field of Ecological Economics regarding a theory of money, while in Section 3, we offer some insights and principles for a monetary transition pathway to a more resilient and regenerative ecosystem.

2. Methods

The core methodology for this work is a transdisciplinary literature review. Our starting point is Lietaer et al.’s groundbreaking report “Money and Sustainability: The Missing Link” [2]. We followed the trail of academic and grey literature that references it, focusing on those works that criticize, advance, or update the arguments and ideas gathered in the report. Moreover, we used Google Scholar, Academia, and ResearchGate as search engines for the following keywords: ecological monetary theory; monetary transition; money and sustainability; money and regeneration. Although wide-reaching and transdisciplinary, our research led us consistently to three leading scientific journals—Sustainability, Ecological Economics, and the International Journal of Complementary Currencies Research—and three economic think tanks—New Economics Foundation, International Movement for Monetary Reform, and the Financial Innovation Lab—that form the backbone of our theoretical approach.

The arguments presented have also benefited tremendously from the close interactions and conference discussions with the scientific community of the Network for Early Career Researchers in Sustainability Transitions (NEST) and the Research Association on Monetary Innovation and Community and Complementary Currency Systems (RAMICS).

3. Revisiting the Missing Link

“A fish will never create fire while immersed in water. We will never create sustainability while immersed in the present financial system. There is no tax, or interest rate, or disclosure requirement that can overcome the many ways the current money system blocks sustainability”, Prof. Dennis Meadows, in [2] (p. 6).

Monetary systems are as old as human societies, with debit and credit registries as old as writing, and the role of money in social and economic life is a long-debated theme within religions, philosophical debates, and political economy [18,19,20]. However, research has shown that the specific link between our monetary system and our societal sustainability is an underdeveloped and under-researched arena of knowledge [3,21]. Beyond loose ideas, scattered hypotheses, and unscientific claims, this fundamental link was only truly grounded in 2013 by Bernard Lietaer and colleagues in a report to the Club of Rome. This timely and politically powerful contribution ended up sharing with some of the works it references and builds upon—ironically, one must note—the historic complacency given to ideas and concepts perhaps too revolutionary for the economic paradigm and political status quo of their times. The report is scarcely cited in scientific articles—256 citations according to Google Scholar (consulted December 2021)—and mostly absent in publications from institutional monetary actors, particularly Central Banks. More surprisingly and striking, the ideas, arguments, and concepts presented and discussed in the report are still mostly ignored or absent in heterodox economics. This might not be surprising to economic historians as one can trace a line of alternative monetary ideas, questions, and hypotheses that significantly differ from the Aristotelian tradition that remain somewhat in the shadow or at the margins of mainstream monetary theory.

In G. Simmel, C.H. Douglas, N. Dodd, and G. Ingham, we trace the lineage of the philosophy and sociology of money [22]. In S. Gesell, A. Kitson, F. Soddy, N. Georgescu-Roegen, H. Daly, and R. Douthwaite, we can find the seeds of an ecology of money and the nexus between money, energy, and sustainability [2,3]. Those sociological and ecological streams found no fertile ground in the development of monetary economics in the 20th century [21]. Likewise, there is a similar absence within key ecological and sustainability literature about the role of money and the impact of the design of the monetary system, as the authors of the famous Club of Rome 1971 report “Limits to Growth” later recognized: “I did not think about the money system at all. I took it for granted as a neutral aspect of human society […]. I now understand that the prevailing financial system is incompatible with sustainability” [2] (p. 6). A striking example emerges from analyzing the United Nations’ 17 Sustainable Development Goals and its 169 targets from a monetary reform perspective. None directly targets or even mentions the necessary monetary system transformation. Even those that focus directly on banking and finance—such as targets 8.10, 10.5, 16.4, and 17.4—propose more regulation, expanded access to the same flawed system, or even suggest ‘debt sustainability’ management, not questioning where that debt came in the first place or the underlying mechanisms—like compound interest—that make it structurally unsustainable, unfair and highly damaging for developing countries [23,24]. Furthermore, part of the reason for this collective blindness to the money-sustainability nexus is because transforming monetary systems to meet sustainability, resilience, and stability is not about tweaking the capital requirements of banks, adjusting interest rates, or strengthening the role of Central Banks and other financial supervisors [10,25,26].

Monetary transition is an agenda that defies neoclassical economics beliefs, dismisses most macroeconomic and monetary modeling, and questions conventional policy goals—such as Gross Domestic Product growth. It is a convergence of sociopolitical movements challenging the full monetization of economic and social life, the systematic concentration and privatization of wealth, and the dependency on non-democratic, non-transparent banking and financial systems. Therefore, it is a fundamental and radical shift of power, beliefs, and, ultimately of economic paradigms [2,27]. Such a new monetary paradigm can only emerge from a systemic, complex, and transdisciplinary approach to money and economics, sprouting from seeds such as Kate Raworth’s “Doughnut Economics” [28], as much as the Ecological Economics literature and alternative monetary economics [29]. Only then can we fully uncover money’s deeply rooted symbols and embedded structures of power and build something truly new and integrated without falling into the traps set at every corner by conventional thinking.

Suppose we fail to address these structural flaws. In that case, the repetition of boom and bust cycles and the numbers of currency, banking, and financial crises will only continue to add up to what is already an impressive track record of 425 systemic crises in the four decades between 1970 and 2010 [30]. Moreover, we will do it at the expense of our societal well-being as much as our natural ecosystems’ resilience and sustainability, despite what might be our best interest, intentions, and international agreements. It is only logical then that “rethinking our money system is a necessary part of any solution [to face the challenges of today]” [2] (p. 193). Not only because of the embedded unsustainability of money but also due to the relationships between money, politics, and socioeconomic power in our modern societies. This necessary monetary apocalypse must include the deconstruction of persistent monetary blind spots (e.g., the monopoly of single-currency debt money), the unveiling of myths about the nature of money and its evolution (e.g., the myth of barter), the exploration of key structural flaws in monetary and banking theory, evidencing its nexus with political, economic and social power, and most importantly the connection with people and planet. A challenge not only to monetarism and (neo)Keynesianism but, more importantly, to Ecological Economics, a transdisciplinary field that, until very recently, did not have a sound monetary theory of its own [4,31,32]. This is of particular importance for two reasons: firstly because we urgently need new paradigms to understand complex economic systems that do not treat the biosphere and ecological impacts as externalities or market failures but that “explicitly recognize the interconnections and interdependence of the economic, biophysical and social worlds” [33]. Secondly, and as Joe Ament argues, without a sound monetary theory, “ecological economics risk importing flawed monetary theories and dualistic social/ecological ontologies, and accordingly, proposing inefficacious and contradictory policies” [31,32] (p. 2). Therefore, we need an ecological approach to money, and ecological economics needs a foundational theory of money.

3.1. An Ecological Ontology of Money

Revisiting the missing link between money and sustainability starts with revisiting money itself. Without delving too much into the history of money, perhaps because “[i]n truth, we can probably never discover the origins of money. Nor is this crucial for understanding the nature of the operation of modern monetary systems […]” [34] (p. 12); a definition of what money intrinsically is, opposed to what money does, is taken as the common starting point for a new alternative narrative among ecological and sociological thinkers [2,32]. However, given the plurality and diversity of manifestations, representations, and interpretations, crystalizing what money is has proven to be an immense and controversial challenge. Attempts to offer a unified “Reference Ontology of Money”—see [19,35,36]—remain as philosophical debates at the edge and somewhat distanced from current monetary thinking. Although there is a growing consensus within heterodox economists and other social scientists to see money not as a thing—a commodity or a neutral lubricant of economic activity—but rather as a social phenomenon—perhaps one of the most complex social institutions in our modern societies [22,37]—a new ontology of money with non-hierarchical dualisms between humans and nature is only now emerging and solidifying [31,32]. Lietaer et al. attempted to fill that gap with their ecological definition that follows the credit theory of money and tries to go further by honoring place and people at its core: “money is an agreement within a community to use something standardized as a medium of exchange” [2] (p. 120). This definition already allows us to broaden the scope of what we consider money and look into economic history with different lenses. However, in this paper, we will take a different stance. Firstly, because the notion of an agreement presupposes some degree of consent, consciousness, or intentionality by its users, we argue it might not always be the case, particularly with the dominant “national” currencies, as we will explore further on. Secondly, because it overstates the exchange function of money, specifically over the unit of account function, that is more overreaching and sounder from a sociological, anthropological, and ecological standpoint [18,38]. More than a social technology that shapes social relationships and institutionalizes value [39], money should be taken as a language that creates commensurability and comparability among the different goods and services [14,40]. Therefore, our transdisciplinary ecological ontology of money must go beyond the classical metalist notion of money as a thing or the chartalist concept of money as credit. Above all, money is the underlying economic language in our societies. The symbols, structure, unique design, and the specific uses of that “language” shape us individually in our behavior and beliefs, as much as collectively in our relationship with each other, with nature, and ultimately our choices and futures [3,41,42]. “Languages do matter for sustainability. In addition to being communication instruments, they can shape value systems about local nature.” [43]. In that sense, we support the claim that “[m]oney is not only endogenous from an economic standpoint but also from a social one […] and the existing monetary order seems incompatible with the emergence of a much-needed new ethics of human-nature relationships” [14] (p. 117). Therefore, building an ecological ontology of money must be more than just recognizing its intrinsic endogenous and social nature, or adding “ecological” words and concepts to the existing hegemonic dictionary. It must be a starting point to re-examine the invisible structures of money, its hidden value assumptions, and the starting point to offer new narratives and theories congruent with a systemic, holistic, and ecological view of money.

3.2. The Critique of the Current System: Structural Design and Detrimental Processes

In the convergence point between structural design and societal impact, the missing link between money and sustainability is fully revealed. Once again, Lietaer et al. play an essential role in synthesizing and crystalizing a wide range of century-old ideas: “Today’s monetary system combines a pro-cyclical money supply with de-regulated capital flows and uncontrolled speculative flows incentives. Furthermore, this money is created with built-in compound interest that makes growth obligatory and automatically renders the concentration of wealth. None of these features is an immutable law of nature. They are all conventions that can be systematically counter-balanced […]” [2] (p. 117). From this analysis, three fundamental building blocks of the IMS are stated: compound interest, single-currency hegemony, and privately created debt. These design elements lock us into unstable and unsustainable patterns by what the authors call the ‘five detrimental processes’: pro-cyclical nature of money creation; short-termism; compulsory growth; concentration of wealth; and devaluation of social capital [2] (p. 94). This systematization of the social and ecological critiques of the IMS is crucial to understanding the missing link and developing an EMT. Based on current developments and our critical assessment, a few modifications are proposed, particularly to the detrimental processes, i.e., the intrinsic working mechanisms built into the system that perpetuate the key design elements and accentuate the overall degenerative impact of the whole system. Firstly, we would add two more detrimental processes: on the one hand, monetary governance, or more specifically, the undemocratic, opaque, highly centralized, non-transparent, non-inclusive governance within our monetary institutions. Something that Lietaer et al. bring only at the end of their work and that we wish was given more centrality and visibility as it contributes to all other detrimental processes while disabling public debate, discouraging civic action, promoting myths and unnecessary complexity, and hindering collaborative solutions across the political and socioeconomic space [44,45]. The addition of monetary governance to the detrimental processes of the unsustainability of the IMS is made for three key reasons: (1) because money, as Nietzsche defined, is the ‘crowbar of power’, and any change to the architecture of the IMS is not only a political endeavor but more fundamentally a power negotiation. After all, the current dominant money exists “not by nature, but by law”; (2) to reinforce the relevance of the unique institutional arrangements, often negotiated in the context of wars between nations that created the present system [46]; and finally, because governance and agency directly influence the scale, the pace and the heading of any transition and is crucial for the impact of a currency as we will later on [44,47]. On the other hand, we would also add a detrimental process that is not referred to by Lietaer et al.: currency wars, i.e., the processes by which the IMS is able to push out, destroy, depreciate, integrate or limit other complementary or competitive monies. This is done by employing institutional conceptual discrimination—for example, what Central Banks define as money—legal instruments—what is officially recognized as legal tender by the state for the payments of taxes—and economic instruments such as transactional fees, exchange rates, and other depreciation tactics [48].

Secondly, in our analysis, we propose to re-classify the privatization of money issuance and allocation from a design feature to a detrimental process for two key reasons: (1) by itself, as an isolated design element, one cannot argue that private money is necessarily degenerative. Many forms of non-governmental money issuance and control can be regenerative, as we will see later on; (2) the privatization of money, specifically after the 1970s, has been a growing, incremental process with many stages, protagonists, and practices behind it. It has been a critical dynamic process in the loss of public monetary accountability and the mass misallocation of capital to destructive industries, particularly in the face of growing de-regulation and lack of financial control, that the famous offshore accounts are the most “visible” side [45].

Thirdly, we propose eliminating two detrimental processes: compulsory growth and short-termism. The latter is considered a result or a consequence of specific design elements—such as positive interest and future depreciation—not a distinctive process. Moreover, many aspects of what alternative authors criticize as short-termism are mainly determined by political cycles, cultural biases, and people’s time preferences beyond the monetary system’s design. Regarding the long-standing debate in terms of ‘compulsory growth’ and the ‘growth imperative’ following some recent contributions made by Arnsperger et al. [7], we fundamentally agree with the authors’ critique of the over-simplified, interest-focused initial formulations of the growth imperative. We stress that the overriding dynamics pushing for that impetus and need to grow the monetary base—namely the leakages to unproductive spheres and the high concentration of financial wealth—are already encapsulated within the “privatization & concentration of wealth” as well as within the “governance” processes.

These modifications to the initial analysis from Lietaer et al. allow us a more up-to-date and complete image of the already not-so-missing link. If taken together and considering the non-linear interaction between the five processes identified and the three core components of the IMS, the true ‘root of all evil’ is ultimately unveiled. Not the language or the social technology itself, but rather its structural design. Therefore, it is here that any initiative towards transforming our money system, and with it, our economic system and society, must start.

3.3. Establishing Priorities for Monetary Reform

Monetary reformists, as much as monetary innovators and radical thinkers, have been putting out different strategies and priorities for the transformation of our monetary system. Lietaer et al. sided and reinforced the ideas and voices arguing for deep structural reforms rather than cosmetic changes [25,26]. From the elements above in Figure 1, the priority for transformative action is clear-cut: to challenge the monetary ‘blind spot’ and core design fault of a single-currency hegemony by designing and implementing a diverse monetary ecosystem with multiple currency systems other than a monoculture of bank-debt money, are allowed to play a role. As mentioned by the authors: “The structural solution needed to give sustainability a chance, albeit totally unorthodox, is to diversify the available exchange media and the agents that create them. In short, in place of a monetary monoculture, we need a monetary ecosystem […]. This would provide greater structural diversity in both the media of exchange and the institutions creating them.” [2] (p. 88). Jérôme Blanc, Georgina Gomez and many other heterodox economists reinforce this claim by focusing on monetary diversity and plurality as the defining characteristic and the starting point for an alternative, more resilient, and sustainable monetary system [49,50,51]. These concepts are explored and developed mainly from a strong plurality perspective and not from the more common weak plurality—which only concerns different means of payments or market competition between the same types of currencies, following the Austrian school of thought [52]. Strong plurality extends that diversity to units of accounts and focuses on ‘unpacking complementarity’ and the different means of linking different types of endogenous money—substitutability, simultaneity, supplementarity, and autonomy [49]. Although we fundamentally agree and support strong monetary plurality, we argue that the rejection and critique of movements and initiatives towards more institutional reforms—such as the American Monetary Act and the Sovereign Money proposal in the UK [53]—and the oblivion of other squeezed alternatives—e.g., Move Your Money, Public, Ethical and Values-Based Banking—is detrimental for the overall transition of the monetary regime and perhaps reflects a lack of systemic approach to large-scale transition processes and a biased belief in niche diffusion and translation. As mentioned elsewhere [1], there is no single recipe for monetary reform and re-alignment, and there can hardly be a shared vision given the number, diversity, dispersion, and scale of alternatives. It is a technological, institutional, and socioecological multi-level and multi-actor dynamic that requires integrated strategies, working in symbioses to fully explore the cracks left open by the GFC landscape shock. This is something an ecological theory of money can offer, but only if it integrates this multi-arena, multi-stakeholder, multi-term holistic ecological gaze.

4. New Developments for Ecological Monetary Theory

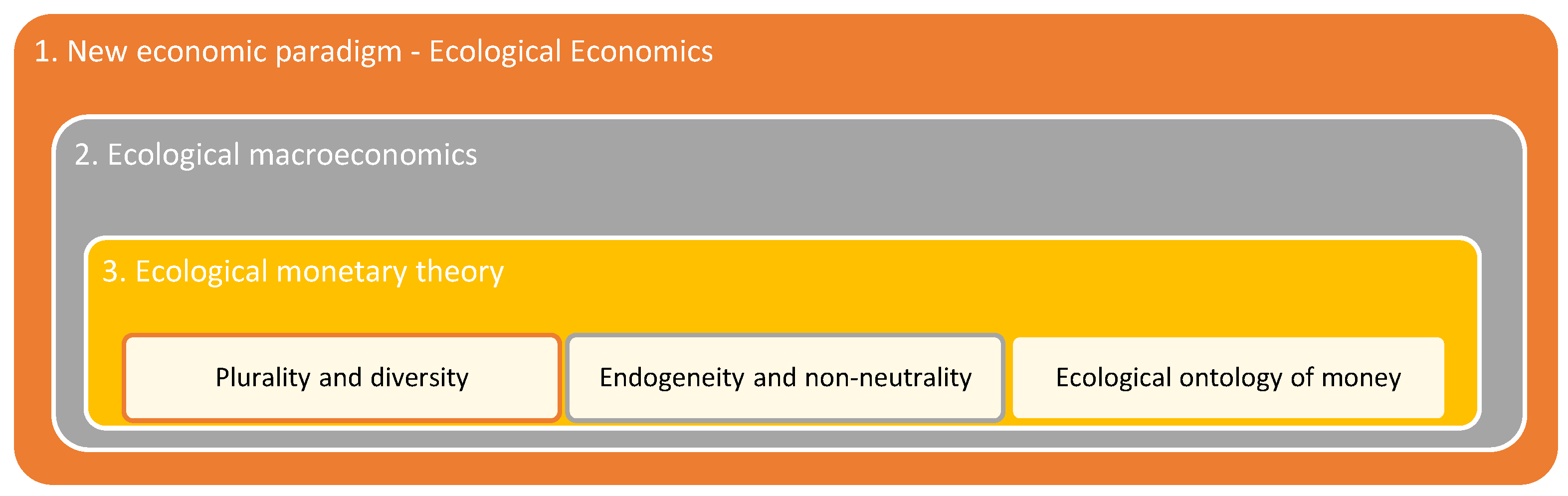

“Money and Sustainability: The Missing Link” is a report that makes its economic paradigm explicit and refers to ‘Ecological Economics’ as the working baseline for the concepts, ideas, and references presented. This is particularly relevant because it is, to our knowledge, the first explicit attempt at building an ecological monetary theory, which made evident the gaps, limits, and biases within ecological economics, namely regarding its monetary thought. Building a monetary theory out of a field of dispersed, not always coherent, and not yet mature ideas is a challenge in itself [54]. By the time Lietaer et al. were writing, Ecological Macroeconomics was still in its early stages of development and mainly was an ‘ecological add-on’ to post-Keynesian models [16,55,56]. EE value theory is an under-discussed and undervalued theme within the field [54,57,58]. Furthermore, as Louie Larue recently argued in his critical assessment of the ecology of money, the analogies and comparisons between the natural world and monetary ecosystems are “unlikely to hold”, and the transposition of critical concepts, such as efficiency and resilience, “still needs quite a lot of work to withstand scientific critique” [54] (p. 7). The ontological and epistemological foundations of an Ecological Monetary Theory (EMT hereafter) were only laid down recently by Joe Ament [32]. Based on his work as well as Lietaer’s contributions we envision a theoretical nested relationship for Ecological Monetary economics, as illustrated in Figure 2.

Beyond Ament’s [31,32] and Svartzman’s work [16], developments in ecological monetary economics, have shyly progressed since 2013, with ecological economists developing the macroeconomics dimension of EE—see for example [55,56]—and the three key concepts of the EMT highlighted in Figure 2. These developments allow us to envision a monetary theory that focuses not on the quantity of money but instead on the qualities of different monies: a monetary theory that embraces the necessary complexity of an ecosystem of currencies and unpacks its potential relationships—one that re-symbolizes the language of money coherently with an ecological paradigm. A monetary theory that sets concrete monetary goals and policies in tune with a sustainable and ecological economy. However, as we have pointed out earlier, ecological monetary economics is still far from standing on firm ground and proving itself a scientifically sound alternative. Adding to an ecological monetary ontology—discussed in point 1.1—and a solid critique of the current system—point 1.2—in our perspective, two elements are strongly needed: a transdisciplinary systems science value theory; and the transition theory that offers pathways and storylines of a new monetary future and how to get there.

4.1. An Ecological Theory of Value

“Value theory forms the bedrock of several economic paradigms” [57] (p. 1) and is probably the most critical theoretical piece needed to ‘finish the puzzle’ of Ecological Economics and place it “as a more effective interdisciplinary paradigm”. After all, value theory sits at the core of economic paradigms with profound implications in all ramifications of any school of economic thought, Ecological Economics being no exception [57,58,59]. An Ecological Theory of Value (EVT hereafter), sprouting from seeds such as the Energy Theory of Value [60], could be the fundamental ‘missing piece’ between Ecological Economics and an Ecological Monetary Theory, that the ‘Money and Sustainability: The Missing Link’ report, and most of the literature afterward, fails to address. Important debates that have fueled Ecological Economics, namely in the 1990s, around embodied energy, exergy, energy, and Energy Return on Energy Invested—see for example [61,62,63]—are scarcely mentioned. We are left without this key theoretical construct of the EMT. One that can challenge the classic—labor—and the neoclassic—utility—view of value, valuation, and money, with an embodied energy concept of value at its genesis. A benchmark concept of value and wealth that anchors monetary theory within the laws of thermodynamics and sets design principles for what Silvio Gesell called, more than a century ago, ‘a natural money system’. Such a grounding theory would also provide a clear framework for monetary and economic analysis: the Energy Return on Energy Invested.

An Ecological Value Theory is also a fundamental piece in the analysis, criticism, and offering of solutions regarding the degenerative design elements, particularly the ‘Debt’ and ‘Interest’ processes. Both have been extensively criticized by the ecological, de-growth, steady-state movements, not always with the scientific backing that an EVT could provide [7]. Two fundamental design principles emerge from the EVT literature: (1) no money system should carry positive interest. Interest should be 0 or negative; (2) no money system should be debt-based. Instead, we should design and implement currency systems backed by real assets, banking systems based on full reserve, or revert to mutual credit systems [64,65]. Finally, an EVT with energy and the Laws of Thermodynamics at its core could be the ideal starting point for new currency designs. Examples of this include what H. Odum’s proposed with the Emdollars, R. Douthwaite with his ‘ebcu’ [41], Kang with the Energy Coin [66], and many others have continued with energy-backed or energy-linked currencies [67].

4.2. A Monetary Socioecological Transition

Building an ecological theory of money is both an end goal and a more profound, longer, harder iterative process of questioning and transforming monetary paradigms and practices. And for such processes, a transition theory is of fundamental importance to better understand and frame ongoing dynamics and, more importantly, to anticipate, explore, and manage the opportunities, limitations, and conditions for steering this sociotechnical transition [68]. The literature on transition theory applied to the monetary-banking-financial sector is scarce. However, contributions have been made, for instance, regarding transitions within the UK banking systems [10], the principles for global transitions in money [69], systemic intrapreneurial transformations in finance and banking [70], the use of complementary currencies as a tool for a low carbon economy transition [71], as well as regarding the meta-transformation within the broader monetary-banking-financial system using Multi-level Perspective and Transition Management theory [1].

In this work, we want to build on these contributions while using the specific lenses of “Sustainability Transitions”, i.e., those processes, pathways, and actors that are involved in disruptive changes and transformations which are happening within the IMF towards a greener, more sustainable, regenerative system [10,71,72]. In particular, we are interested in understanding it mainly from an institutional and sociotechnical approach focusing on who is doing what within the IMF transition process and which level of influence can each actor–practice combination have in our monetary shift towards sustainability. Considering this and based on current trends in monetary innovation, practices, and theory, we identified and categorized three interdependent spheres that are emerging and co-developing, powered by three different socioeconomic-political dynamics. The first sphere, which we named “Green money”, includes the new awareness regarding the ecological and social footprint of money systems, making headlines in both alternative and mainstream academia and media [73,74]. It includes calculations of different payment systems’ energy and emissions footprints—Cash vs. Visa vs. Cryptocurrencies [75,76]—as much as different currencies themselves. It integrates new trends in sustainable and fair banking, both in the private sector [77] and within the realm of central banks—see the latest Glasgow Declaration from the Network for Greening the Financial Systems [78]. It pushes for social and ecological accountability and new standards in financial markets, stocks, and bonds [79]. It has led to the developments for the decarbonization of cryptocurrencies [80], the creation of ‘greener’ versions, such as Bitgreen—to face the critics regarding Bitcoin’s significant ecological footprint [81]—or the promotion of sustainable cryptocurrencies such as Moeda, IOTA or Solarcoin [67].

It is the logical first step to improve or upgrade the existing system in many cases. It is not revolutionary nor transformative but part of the squeezed-in transitioning processes [1,10]. Most of the dynamics, practices, and actions that we have categorized within this first sphere have a limited impact in steering the IMS towards sustainability, and they do not fundamentally address any of the three design blocks or the five detrimental processes identified above. It might even lead to socially detrimental banking strategies, such as the war on cash [82,83], which might have positive environmental impacts but have profound negative impacts on those more vulnerable to a cashless society. Moreover, it might contribute to “develop path-dependency through processes of optimization and incremental innovation” [47] (p. 605).

In a second sphere, we have a more profound process that looks beyond the mere “greening” of our money and payment systems and focuses on the goals and societal impacts of each monetary strategy and policy. We call it the “sustainable money” sphere. It includes recent movements lobbying for the European Central Bank and European Banks to align their monetary policy with the SDGs, the Paris Agreement, and our common climate goals [84,85]. It also includes the movements toward Public Banking in the USA [86] or UNEP’s vision of “Aligning the Financial System with Sustainable Development” [87]. It recognizes that monetary policy affects our world in very tangible ways and seeks coherence between social, environmental and climate goals with monetary goals. Four illustrative examples are: (1) the ‘Green Quantitative Easing’ campaign [88] and the ‘Green Scorecard’ for Central Banks, which ranks central banks’ climate performance, taking into account not only the footprint of their operation but, more importantly, the ecological impact of their investments choices and monetary policies [89,90]; (2) impact currencies and impact tokens designed to foster and accelerate the implementation and reach of the SDG’s [91]; (3) corporate and complementary currencies designed to promote and reward sustainable lifestyles and behaviors—such as Ecocoin, NU-Spaarpas or Torekes [92]; and finally, (4) developments in energy currencies, carbon currencies and emission reduction currency systems whose design and goal is targeting CO2 reductions and new standards of wealth and value anchored in nature [70,93]. The actors and actions within this second sphere still work mostly within the current monetary paradigm and its institutions, forcing its ‘reconfiguration’, ‘re-constellation’ and re-direction. It can be argued that these are transformative actions as they can potentially alter the configuration of the IMS regime in its design blocks—particularly regarding the single-currency hegemony and opaque governance. However, they have been limited by their scale, applicability, and other sociopolitical-economic constraints such as lack of proper funding, re-prioritization of goals, and monetary regime resistance to change [94,95]. The potential socioecological impact of sphere two actions is significantly higher than those of sphere one, particularly in the face of constant landscape pressures. Finally, our third sphere represents the radical shift an ecology of money embodies. It goes far beyond the footprint of money or its strategically designed goals. It is a sphere that includes the overall design of the system as a whole, its players, flows, relationships, and key assumptions. Therefore, it is not about incremental improvements (sphere one), nor reconfigurations within the existing regime (sphere two) but a different consciousness that informs a radical redesign and re-conceptualization of the whole IMS. It envisions a fundamentally different monetary architecture based on the EMT building blocks in Figure 2. The sphere of deeply transformative and revolutionary actions leads to profound socioecological impacts on our economies and societies. Due to its disruptive nature, and following the work of Daniel Wahl [96], we call it “regenerative money”. It includes new currency ecosystems in development, such as Seeds, which already embodies a whole-systems approach focused on regenerative actions—see Figure 3.

It also includes the principles behind the movements towards regenerative finance as stated by the Capital Institute [97] or Triodos Bank Regenerative Money Centre. It is a sphere characterized by new monetary actors, institutions, movements, and socioeconomic and political dynamics radically re-conceptualizing the monetary paradigm of the last 50 years. It works at the highest leverage point, and because of it, the implications and potential impacts are deeply transformative. Its holistic perspective addresses all building blocks and detrimental processes in Figure 1 and beyond.

To complement the ‘what’ is of crucial importance to know the ‘who’. Once again, we categorized three parallel dynamics according to the actors or institutions driving and governing each monetary development: people-powered money; sovereign money; and corporate money. The first one represents the niche innovations and bottom-up dynamics of groups and communities, specifically at the local and regional level, through the promotion and active support of community currencies, time banks, barter networks, and mutual credit systems. It is mostly a decentralized, heterogeneous, not-for-profit, exchange-focused, and resilience-building social dynamic [98]. This has been an abundant experimental, pioneering movement and field of monetary innovation in all three spheres, particularly in “green money” and “sustainable money” spheres [94,95]. However, its impact on the IMS regime or influence in the transition processes is residual [95,99]. The second dynamic is towards complementary Sovereign Money creation, or official acceptance, by the state either through the government (national or local level), the central bank, or a third independent institution. It has gained momentum since the GFC in two main streams: the adoption of municipal currencies at the local level, frequently in multi-stakeholder initiatives—see, for example, the case of REC in Barcelona; and the fast development by major central banks worldwide of CBDCs or ‘govcoins’, such as the E-krona in Sweden or the digital e-Yuan in China [100]. It represents the integration of new technological developments—such as Blockchain—into the existing centralized, not-for-profit, exchange, and unit-of-account public service system that aims to regain its monetary power. While in the municipal currencies stream, it is common to have social and ecological principles and goals fully embedded in the monetary design—see, for example [101]—regarding CBDCs, only a small fraction of ‘under research’, ‘pilot’ or ‘proof of concept’ CBDCs seem to be already integrating socioecological principles into their designs, placing the vast majority of CBDCs outside of our spheres and Municipal currencies within sphere 1 or 2. Lastly, we have the case of corporate currencies. A movement started decades ago with air miles, consumer loyalty points, and other benchmark cases such as the WIR in Switzerland, and that has been evolving since 2009 towards widespread use by businesses of global digital and cryptocurrencies [102]. Sardex, a B2B regional complementary currency [103], and Ven, a global digital ‘stablecoin’, provide two case studies of such developments since 2009. This decentralized, for-profit, all-purpose money dynamic has gained particular relevance for institutional monetary institutions given the potential impact of such global giant corporations—such as Facebook with ‘Diem’ and Amazon with ‘Amazon coins’—developing their internal currency.

This double-entry logic for the systematization of ongoing trends and innovation dynamics within the monetary system can help us to better frame and understand the underlying mechanisms and the impact of each actor–practice combination. It also allows us to identify arenas for future development—e.g., sustainable and regenerative CBDCs—and potential tipping points for systems change. Figure 4 and Figure 5 provide two graphical representations of the ongoing dynamics we have discussed. Figure 4 integrates “Climate Change” as an overarching concept for the climate and ecological landscape pressures forcing the IMS to change while identifying some trends with the highest potential impact to shake the system.

In Figure 5, we place the three spheres together with the three sociopolitical dynamics and provide some examples of currencies and projects that crystalize the essence of each cluster. While ‘Regenerative Money’ is still an emerging, challenging trend in its early stages, there are plenty of ‘Sustainable Money’ examples that can inspire and trigger a movement from Green and conventional money toward more impactful and transformative practices. It is also important to highlight that these are multi-actor ongoing live experiments that can and will transcend these subjective frontiers. Nevertheless, identifying the root, core intention, and consciousness of each transition movement is fundamental for understanding the larger-scale process and its steering towards a shared, desired future.

5. A Monetary Ecosystem beyond Sustainability

This systemic view of an ecosystem of currencies from different actors and serving different socioeconomic functions, together with a narrative of transformation and a transition theory, is a revolutionary step in monetary thinking, one where we must embrace complexity, non-equilibrium thermodynamics, and ecological network analysis if we aim to develop a new and coherent transdisciplinary monetary discipline. This is a non-linear leap, very often into uncharted territory, which we take not with a precise map, compass, and straight route but rather with a set of principles, some boundaries, and envisioned regenerative processes. Furthermore, for it to be transformative and not repeat patterns and mistakes from the past, it cannot be logically incremental nor focus on sustainability. Conventional sustainability and ‘sustainable-thoughtware’ are no longer enough [104]. We must embrace the highest leverage point in the system and aim for regeneration. Only then can we protect ourselves from single-focus solutions and the single-perfect-currency illusion. An economic–political mirage that has attracted so many into thinking that there is such thing as a perfect currency that will solve all our economic and societal problems. The Terra TRC by Bernard Lietaer, the mutual credit systems for Bendell and T. Greco [71], the EnergyCoin from Kang [66], or a Carbon Currency that will be the next ‘gold standard’ and root our entire economic system into the ‘real economy’ [93].

An ecological monetary system that goes beyond sustainability must thus be anchored in regenerative principles and processes. Based on the works of John Fullerton, Daniel Walh, Carol Sanford, among others, Patrick Huntjens proposes a new ‘Natural Social Contract’, based on eight fundamental principles for a regenerative economy [105]. Parallel to this, Brian Fath and colleagues propose ten principles and indicators for a regenerative economy coming from Energy Network Science [69]. Combining these different sources and applying them to monetary systems, while making a differentiation between design principles and regenerative processes, we propose that an ecological theory of money beyond sustainability should be based on the following design principles and regenerative processes (Figure 6):

The design elements and the regenerative processes shown above in Figure 6 serve as a map and compass to navigate the necessary transition and potential measures to assess the vitality and health of the ecosystem. It is essential to observe that they are equally important—no hierarchies or “steps” here—mutually beneficial and deeply interconnected. The principle of ‘diversity and connectivity’ has been already discussed above regarding strong monetary plurality, i.e., diversity of actors, mediums of payments, currencies, and units of accounts. Moreover, inhomogeneity by itself is not a necessary condition for a thriving, healthy system. Studies in Energy Network Analysis show that only diverse connectivity can guarantee resilience [69]. To complement and enrich this crucial design element, we need two more: to seek a balance between resilience and efficiency that guarantees that the system avoids excessive stagnation or brittleness and maintains itself within what Lietaer et al. called “The Window of Vitality” [2]. To strike that vital dynamic balance, we need a holistic view into the appropriate scale and relationship of the elements within the systems. This means fitting scale to form and function, primarily as a critical design protocol for each currency within the ecosystem and secondarily for managing the relationships between currencies. As one can easily infer from the lines above, these three principles are tightly connected and cannot be taken isolated as each one calibrates, complements, and enriches the others.

Regarding the processes that we believe fundamental for a metabolic systems, such as our monetary system, to be regenerative, four dynamics are unavoidable: robust, cross-scale circulation; participatory, empowered governance; symbiotic mutualism and reciprocity; collective learning and creative adaptation. “The circulation of money and information is particularly critical in socioeconomic networks, and these flows are always closely linked to networks and processes of energy” [69] (p. 16). Monetary circulation concerns much more than just the speed at which money changes hands—the money multiplier. It is about where that money is going—productive versus non-productive economy [106]—where are the bottlenecks and spaces of accumulation and concentration, where are the leaks in the system—such as offshores and “fiscal paradises” [45]—and the degree of mutualism and balance across scales and actors. A robust and regenerative metabolism must thus “continuously channel resources into self-feeding, self-renewing, self-sustaining internal processes” [69] (p. 18). Part of this process is intimately connected with seeking symbiotic or synergic relationships that are mutually beneficial. The degree to which an economy can foster collaborative dynamics and mutualism depends on factors beyond money. However, money can be designed to facilitate, promote and reinforce those flows and contribute effectively to a new regenerative economy. The extent to which each currency and the overall monetary ecosystem can integrate feedback learning loops and creatively respond and adapt to a continuously changing environment is perhaps the most crucial regenerative process and, at the same time, the one hardest to measure. Once again, Fath et al. proposed a composite list of indicators for collective learning, which can easily be transposed to monetary systems [69] (p. 19). Finally, we have empowered, participatory, accountable, transparent governance. Given the opaqueness of current existing national and global systems and the importance of these information, organization, and power processes—highlighted in Section 1—it is only natural that governance occupies a central role in any revolutionary movement towards regeneration. As Lietaer et al. conclude, “[monetary governance] may be the most crucial unresolved organizational question we need to deal with if we are serious about sustainability.” [2] (p. 191).

6. Conclusions

Transforming our concept of money and our understanding of monetary ecosystems is an unavoidable part of any process and pathway of economic and societal re-alignment with sustainability and regeneration. Moreover, the emergence of a new economic and monetary paradigm is a highly complex transition process for which we need new thoughtware to navigate appropriately.An ecological theory of money, such as Ament’s EMT, anchored and supported by an Ecological Value Theory and a Sustainable Transition theory, has the best chance to replace neoclassic monetary theory and provide the right lenses to acknowledge the language of money in all its symbols, forms, and mediums, and redesign our thriving monetary ecosystems to regenerate our social, economic and ecologic landscapes. A monetary ecology must avoid single-focused solutions and embrace complexity, interdependences, and complementarity. At its core, it must have a set of principles and working mechanisms distilled and adapted from the regenerative economics literature. The three design elements—appropriate scale and relationship; diversity and connectivity; balance between resilience and efficiency—together with the four regenerative processes—robust cross-scale circulation; participatory governance; symbiotic mutualism and collaboration; collective learning and creative adaptation—form the fundamental pillars for a new monetary paradigm that can steer our monies to face the ecological and social challenges of the XXI century.

Future research should increase our knowledge and understanding of complex monetary ecosystems and the interplay of relationships among those currency arenas. Furthermore, it could also shine some new light on the role of money in sustainability transitions and how to explore landscape shocks best to trigger transformations within the IMS. We missed the opportunity for deep reform after the landscape shock of the GFC in 2008. Let us not do the same with the COVID-19 shock and use this opportunity to bring about the monetary revolution the world urgently needs.

Author Contributions

F.M.A. is the main author of this work. R.S. and G.P.-L. had a critical role in critical analysis and regular review of the content. All authors have read and agreed to the published version of the manuscript.

Funding

The research that has led to this work has received funding from the Portuguese Ministry of Education and Science through Fundação para a Ciência e a Tecnologia (FCT) with the Ph.D. scholarship reference PD/BD/113934/2015. We would also thank Fundação para a Ciência e a Tecnologia for supporting the FCT investigator contract (IF/00940/2015). The APC was financially supported by CENSE—Center for Environmental and Sustainability Research, School of Science and Technology, NOVA University Lisbon who is financed by Fundação para a Ciência e a Tecnologia, I.P., Portugal (UIDB/04085/2020) and by the Centre for Ecology, Evolution and Environmental Change (cE3c), Faculty of Sciences, University of Lisbon who is financed by Fundação para a Ciência e a Tecnologia, I.P., Portugal (UIDB/00329/2020).

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Conflicts of Interest

The authors declare no conflict of interest. Moreover, the funders had no role in the design of the study; in the collection, analyses, or interpretation of data; in the writing of the manuscript, or in the decision to publish the results.

References

- Alves, F.M.; Kovasna, A.; Penha-Lopes, G. Alternative monetary narratives and experiments—Systematizing the necessary societal transition. J. Stud. Citizsh. Sustain. 2019, 4, 77–94. [Google Scholar]

- Lietaer, B.; Dunne, J. Rethinking Money: How New Currencies Turn Scarcity into Prosperity; Berret-Koehler Publishers, Inc.: San Francisco, CA, USA, 2013. [Google Scholar]

- Lietaer, B.; Arnsperger, C.; Goerner, S.; Brunnhuber, S. Money and Sustainability—The Missing Link; Triarchy Press: Bridport, UK, 2013. [Google Scholar]

- Hornborg, A. How to turn an ocean liner: A proposal for voluntary degrowth by redesigning money for sustainability, justice and resilience. J. Political Ecol. 2017, 24, 624–634. [Google Scholar] [CrossRef] [Green Version]

- Simms, A. Tackling the ‘triple crunch’ of financial crisis, climate change and soaring enery prices with a Green New Deal. In Triple Crunch—Joined-Up Solutions to Financial Chaos, Oil Decline and Climate Change to Transform the Economy; Potts, R., Ed.; New Economics Foundation: London, UK, 2009; pp. 3–6. [Google Scholar]

- Mellor, M. The Future of Money: From Financial Crisis to Public Resource; Pluto Press: London, UK, 2010. [Google Scholar]

- Arnsperger, C.; Bendell, J.; Slater, M. Monetary Adaptation to Planetary Emergency: Addressing the Monetary Growth Imperative; Institute for Leadership and Sustainability: Cumbria, UK, 2021; Unpublished. [Google Scholar]

- Turner, A. Between Debt and the Devil: Money, Credit and Fixing Global Finance; Princeton University Press: Princeton, NJ, USA, 2016. [Google Scholar]

- Hellwig, M. Twelve Years after the Financial Crisis—Too-big-to-fail is still with us. J. Financ. Regul. 2021, 7, 175–187. [Google Scholar] [CrossRef]

- Seyfang, G.; Gilbert-Squires, A. Move your money? Sustainability Transitions in Regimes and Practices in the UK Retail Banking Sector. Ecol. Econ. 2018, 156, 224–235. [Google Scholar] [CrossRef] [Green Version]

- OECD. OECD Data. Retrieved from OECD Data—Houselhold Debt. Available online: https://data.oecd.org/hha/household-debt.htm (accessed on 6 December 2021).

- de la Cuesta-González, M.; Ruaz, C.; Rodriguez-Fernandez, J. Rethinking the Income Inequality and Financial Development Nexus. A Study of Nine OECD Countries. Sustainability 2020, 12, 5449. [Google Scholar] [CrossRef]

- UNEP. Global Environmental Outlook 6; Cambridge University Press: Cambridge, UK, 2019. [Google Scholar]

- World Economic Forum. Global Risks Report, 16th ed.; WEF: Geneva, Switzerland, 2021. [Google Scholar]

- Ranjbari, M.; Esfandabadi, Z.S.; Zanetti, M.C.; Scagnelli, S.D.; Siebers Peer-Olaf Aghbashlo, M.; Peng, W.; Quatraro, F.; Tabatabaei, M. Three pillars of sustainability in the wake of COVID-19: A systematic review and future research agenda for sustainable development. J. Clean. Production. 2021, 297, 126660. [Google Scholar] [CrossRef]

- Svartzman, R.; Dron, D.; Espagne, E. From ecological macroeconomics to a theory of endogenous money for a finite planet. Ecol. Econ. 2019, 162, 108–120. [Google Scholar] [CrossRef]

- Meadows, D. Leverage Points—Places to Intervene in a System; Sustainability Institute: Hartland, VT, USA, 1999. [Google Scholar]

- Graeber, D. Debt: The First 5000 Years; Penguin: London, UK, 2012. [Google Scholar]

- Mäki, U. Reflections on the Ontology of Money. J. Soc. Ontol. 2020, 6, 245–263. [Google Scholar] [CrossRef]

- Fuller, E.W. A Source Book on Early Monetary Thought—Writings on Money before Adam Smith; Edward Elgar Publishing: Palo Alto, CA, USA, 2020. [Google Scholar]

- Aspinall, N.G.; Jones, S.R.; McNeill, E.; Werner, R.A.; Zalk, T. Sustainability and the financial system—Review of literature 2015. Br. Actuar. J. 2015, 23, 1–21. [Google Scholar] [CrossRef] [Green Version]

- Dodd, N. The Social Life of Money; Princeton University Press: Princeton, NJ, USA, 2014. [Google Scholar]

- Ajili, W. Do We Have to Rethink Sovereign Debt of Developing Countries? In Handbook of Research on Institutional, Economic, and Social Impacts of Globalization and Liberalization; Bayar, Y., Ed.; IGI Global: Bandırma, Turkey, 2021; pp. 337–355. [Google Scholar]

- Ibrahim Ari, M.K. Sustainable Financing for Sustainable Development: Understanding the Interrelations between Public Investment and Sovereign Debt. Sustainability 2018, 10, 3901. [Google Scholar]

- Duffie, D. Financial Regulatory Reform After the Crisis: An Assessment. ECB Forum on Central Banking; European Central Bank: Sintra, Portugal, 2016; pp. 1–70. [Google Scholar]

- Quaglia, L. Financial regulation and supervision in the European Union after the crises. J. Econ. Policy Reform 2013, 16, 17–30. [Google Scholar] [CrossRef]

- Fiscus, D. Life, Money, and the Deep Tangled Roots of Systemic Change for Sustainability. World Futures 2013, 69, 555–571. [Google Scholar] [CrossRef]

- Raworth, K. Doughnut Economics: Seven Ways to Think Like a 21st-Century Economist; Penguin Random House UK: London, UK, 2017. [Google Scholar]

- Arestis, P.; Sawyer, M. A Handbook of Alternative Monetary Economics; Edward Elgar Publishing Limited: Cheltenham, UK, 2017. [Google Scholar]

- Laevan, L.; Valencia, F. Systemic Banking Crises Database: An Update; Working Paper WF/12/163; IMF: Washington, DC, USA, 2012. [Google Scholar]

- Ament, J. Towards an Ecological Monetary Theory. Sustainability 2019, 11, 923. [Google Scholar] [CrossRef] [Green Version]

- Ament, J. Towards an Ecological Monetary Theory 2020. Available online: https://www.sciencedirect.com/science/article/abs/pii/S0921800919306962 (accessed on 16 December 2021).

- Erickson, J.G. The approach of ecological economics. Camb. J. Econ. 2005, 29, 207–222. [Google Scholar]

- Tymoigne, É.; Wray, L.R. Money: An alternative story. In A Handbook of Alternative Monetary Economics; Arestis, P., Sawyer, M., Eds.; Edward Elgar Publishing Limited: Cheltenham, UK, 2007; pp. 1–17. [Google Scholar]

- Glenda Amaral, T.P. Towards a Reference Ontology of Money: Monetary Objects, Currencies and Related Concepts. In 14th International Workshop on Value Modelling and Business Ontologies; VMBO: Brussels, Belgium, 2020. [Google Scholar]

- Searle, J.R. Money: Ontology and Deception. Camb. J. Econ. 2017, 41, 1453–1470. [Google Scholar] [CrossRef]

- Zelizer, V.A. The Social Meaning of Money: Pin Money, Paychecks, Poor Relief, and Other Currencies; Princeton University Press: Princeton, NJ, USA, 2017. [Google Scholar]

- Blanc, J.; Desmedt, L.; Le Maux, L.; Marques-Pereira, J.; Ahmed, P.O.; Theret, B. Monetary Plurality in Economic Theory. In Monetary Plurality in Local, Regional and Global Economies; Gómez, G.M., Ed.; Routledge: London, UK, 2018; pp. 18–46. [Google Scholar]

- Desan, C. The constitutional approach to money. In Money Talks: Explaining How Money Really Works; Bandelj, N., Wherry, F.F., Zelizer, V.A., Eds.; Princeton University Press: Princeton, NJ, USA, 2017; pp. 109–130. [Google Scholar]

- Aglietta, M.; Ahmed, O.P.; Ponsot, J. La Monnaie, Entre Dettes et Souveraineté; Odile Jacob: Paris, French, 2016. [Google Scholar]

- Douthwaite, R. The Ecology of Money; Green Books for the Schumacher Society: Bristol, UK, 1999. [Google Scholar]

- Kuzminski, A. The Ecology of Money: Debt, Growth and Sustainability; Lexington Books: Plymouth, UK, 2013. [Google Scholar]

- Inglis, D.; Pascual, U. On the links between nature’s values and language. People Nat. 2021, 1–17. [Google Scholar] [CrossRef]

- Brooks, S. How green is Your Money? Mapping the relationship between monetary systems and the environment. Int. J. Community Curr. Res. 2015, 19, 12–18. [Google Scholar]

- Bullough, O. Moneyland; Profile Books: London, UK, 2018. [Google Scholar]

- Ferguson, N. The Ascent of Money: A Financial History of the World; Penguin Press: New York, NY, USA, 2008. [Google Scholar]

- Loorbach, D.; Frantzeskaki, N.; Avelino, F. Sustainability Transtions Research: Transforming Science and Practice for Societal Change. Annu. Rev. Environ. Resour. 2017, 42, 599–626. [Google Scholar] [CrossRef]

- Amato, M.; Fantacci, L. Handbook of the History of Money and Currency; Springer: Singapore, 2020. [Google Scholar]

- Blanc, J. Unpacking Monetary Complementarity and Competition: A Conceptual Framework. Camb. J. Econ. 2017, 41, 239–257. [Google Scholar] [CrossRef]

- Gómez, G.M. Monetary Plurality in Local, Regional and Global Economies; Routledge: New York, NY, USA, 2019. [Google Scholar]

- Mouatt, S. The case for Monetary Diversity. Int. J. Community Curr. Res. 2010, 14, 17–28. [Google Scholar]

- Hayek, F.A. Denationalization of Money; Institute of Economic Affairs: London, UK, 1976. [Google Scholar]

- Dyson, B.; Hodgson, G.; van Lerven, F. Sovereign Money; Positive Money UK: London, UK, 2016. [Google Scholar]

- Larue, L. The Ecology of Money: A Critical Assessment. Ecol. Econ. 2020, 178, 106823. [Google Scholar] [CrossRef]

- Hardt, L.; O’Neill, D.W. Ecological Macroeconomic Models: Assessing Current Developments. Ecol. Econ. 2017, 134, 198–211. [Google Scholar] [CrossRef]

- Macchione Saes, B.; Ribeiro Romeiro, A. Ecological macroeconomics: A methodological review. Econ. Soc. 2018, 28, 365–392. [Google Scholar] [CrossRef] [Green Version]

- Pirgmaier, E. The value of value theory for ecological economics. Ecol. Econ. 2021, 179, 106790. [Google Scholar] [CrossRef]

- Douai, A. Value Theory in Ecological Economics: The Contribution of a Political Economy of Wealth. Environ. Values 2009, 18, 257–284. [Google Scholar] [CrossRef] [Green Version]

- Schumpeter, J.A. History of Economic Analysis; Routledge: London, UK, 1987. [Google Scholar]

- Berndt, E.R. From Technocracy to Net Energy Analysis: Engineers, Economists and Recurring Energy Theories of Value; Studies in Energy and the American Economy (MIT); Discussion paper N.11; Massachussets Institute of Technology: Cambridge, MA, USA, 1982. [Google Scholar]

- Contanza, R. Embodied energy and economic valuation. Science 1980, 210, 1219–1224. [Google Scholar] [CrossRef]

- Foster, J.B.; Holleman, H. The theory of unequal ecological exchange: A Marx-Odum dialectic. J. Peasant Stud. 2014, 41, 199–233. [Google Scholar] [CrossRef]

- Judson, D.H. The convergence of neo-Ricardian and embodied energy theories of value and Price. Ecol. Econ. 1989, 1, 261–281. [Google Scholar] [CrossRef]

- Renner, A.; Daly, H.; Mayumi, K. The dual nature of money: Why monetary systems matter for equitable bioeconomy. Environ. Econ. Policy Stud. 2021, 23, 749–760. [Google Scholar] [CrossRef]

- Karakatsanis, G. A Thermodynamic Theory of Money. Ecological Economics and Rio+20: Contributions and Challenges for a Green Economy; International Society for Ecological Economics: Rio de Janeiro, Brazil, 2012. [Google Scholar]

- Kang, J. Energy Coin: A Universal Digital Currency Based on Free Energy. Am. J. Mod. Energy 2020, 6, 95–100. [Google Scholar]

- Ryan-Collins, J.; Schusterand, L.; Greenham, T. Energizing Money—An Introduction to Energy Currencies and Accounting; New Economics Foundation: London, UK, 2012. [Google Scholar]

- Rotmans, J.; Loorbach, D. Complexity and Transition Management. J. Ind. Ecol. 2019, 13, 184–196. [Google Scholar] [CrossRef] [Green Version]

- Fath, B.D.; Fiscus, D.A.; Goerner, S.J.; Berea, A.; Ulanowicz, R.E. Measuring regenerative economics: 10 principles and measures undergirding systemic economic health. Glob. Transit. 2019, 1, 15–27. [Google Scholar] [CrossRef]

- Hascott, L. A Banker’s Guide to Transforming Finance; The Finance Innovation Lab: London, UK, 2020. [Google Scholar]

- Bendell, J.; Greco, T. Currencies of Transition—Transforming Money to Unleash Sustainability. In The Necessary Transition: The Journey towards the Sustainable Enterprise Economy; McIntosh, M., Ed.; Greenleaf Publishing Limited: London, UK, 2013; pp. 221–242. [Google Scholar]

- Markard, J.; Truffer, B. Sustainability transitions: An emerging field of research and its prospects. Res. Policy 2012, 41, 955–967. [Google Scholar] [CrossRef]

- Hanegraaf, R.; Jonker, N.; Mandley, S.; Miedema, J. Life Cycle Assessment of Cash Payments; DNB Working Paper n°610; SSRN: Amesterdam, The Netherlands, 2018. [Google Scholar]

- Sid, J.L.; Englesson, N. How Eco Friendly Is Our Money and Is There an Alternative. Netrogenic. 2017. Available online: https://papers.netrogenic.com/sid/eco-friendly-money.pdf (accessed on 5 January 2022).

- Shonfield, P. Carbon Footprint Assessment: Paper vs. Polymer £5 & £10 Bank Notes; Thinkstep: London, UK, 2017. [Google Scholar]

- Cleancoin. Cleancoins. Retrieved from Cleancoins. Available online: http://www.cleancoins.io/#/info (accessed on 6 December 2021).

- Caré, R. Sustainability in Banks: Emerging Trends. In Sustainable Banking: Issues and Challenges; Caré, R., Ed.; Palgrave Pivot: London, UK, 2018; pp. 93–130. [Google Scholar]

- NGFS. Press Releases. Retrieved from Networking for Greening the Financial Systems. Available online: https://www.ngfs.net/en/communique-de-presse/ngfs-publishes-ngfs-glasgow-declaration-and-continues-foster-climate-action-central-banks-and (accessed on 16 December 2021).

- TEG. EU Green Bond Standard: Usability Guide; EU Technical Group on Sustainable Finance: Brussels, Belgium, 2020; Available online: https://ec.europa.eu/info/business-economy-euro/banking-and-finance/sustainable-finance/european-green-bond-standard_en (accessed on 16 December 2021).

- Truby, J. Decarbonizing Bitcoin: Law and policy choices for reducing the energy consumption of Blockchain technologies and digital currencies. Energy Res. Soc. Sci. 2018, 44, 399–410. [Google Scholar] [CrossRef]

- Stoll, C.; Klaaßen, L.; Gallersdörfer, U. The Carbon Footprint of Bitcoin. Joule 2019, 3, 1647–1661. [Google Scholar] [CrossRef]

- Clarke, D. The Future of Cash: Protecting Access to Payments in the Digital Age; Positive Money UK: London, UK, 2018. [Google Scholar]

- Van Hove, L. On the War on Cash and its spoils. Int. J. Eletronic Bank. 2008, 1, 36–45. [Google Scholar] [CrossRef]

- Burcak Inel 2008, R. P. 2021. European Bank Practices in Implementing and Supporting the SDG’s. European Banking Federation and KPMG Spain. Available online: https://www.ebf.eu/wp-content/uploads/2021/06/European-bank-practices-in-supporting-and-implementing-the-UN-Sustainable-Development-Goals.pdf (accessed on 31 March 2022).

- ECB. Research & Publications. Retrieved from European Central Bank. Available online: https://www.ecb.europa.eu/pub/html/index.en.html#/search/sustainability/1 (accessed on 16 December 2021).

- Uğurlu, E.N.; Epstein, G. The Public Banking Movement in the United States: Networks, Agenda, Initiatives, and Challenges; Political Economy Research Institute: Amherst, MA, USA, 18 March 2021; pp. 1–46. [Google Scholar]

- UNEP. Aligning the Financial System with Sustainable Development: The Coming Financial Climate; United Nations Environment Programme: Nairobi, Kenya, 2015. [Google Scholar]

- Kedward, K.; Buller, A.; Ryan-Collins, J. Quantitative Easing and Nature Loss: Exploring Nature-Related Financial Risks and Impacts in the European Central Bank’s Corporate Bond Portfolio; Institute for Innovation and Public Purposes: London, UK, 2021. [Google Scholar]

- Barnes, M. Shadow banking: The next financial crisis? Co. Lawyer 2021, 42, 136–145. [Google Scholar]

- Jourdan, S.; Kalinowski, W. Aligning Monetary Policy with the EU’s Climate Targets; Veblen Institute for Economics Reforms & Positive Money Europe: Brussels, Belgium, 2019. [Google Scholar]

- Uzsoki, D.; Guerdat, P. Impact Tokens—A Blockchain-based Solution for Impact Investing; International Institute for Sustainable Development: Winnipeg, MB, Canada, 2019. [Google Scholar]

- Joachain, H.; Klopfert, F. Emerging Trends of Complementary Currencies Systems as Policy Instruments for Environmental Purposes: Changes Ahead? Int. J. Community Curr. Res. 2012, 16, 156–168. [Google Scholar]

- Seyfang, G. Carbon Currencies: A New Gold Standard for Sustainable Consumption? Centre for Social and Economic Research on the Global Environment 2009, 1, 1–16. [Google Scholar]

- Seyfang, G.; Longhurst, N. Growing green money? Mapping community currencies for sustainable development. Ecol. Econ. 2013, 86, 65–77. [Google Scholar] [CrossRef] [Green Version]

- Michel, A.; Hudon, M. Community currencies and sustainable development: A systematic review. Ecol. Econ. 2015, 116, 160–171. [Google Scholar] [CrossRef] [Green Version]

- Wahl, D. Designing Regenerative Cultures; Triarchy Press: Bridport, UK, 2016. [Google Scholar]

- Fullerton, J. Finance for a Regenerative World; Capital Institute: New York, NY, USA, 2018. [Google Scholar]

- CIA. People Powered Money—Designing, Developing & Delivering Community Currencies; New Economics Foundation: London, UK, 2015. [Google Scholar]

- Zeller, S. Economic Advantages of Community Currencies. J. Risk Financ. Manag. 2020, 13, 271. [Google Scholar] [CrossRef]

- Niepelt, D. Central Bank Digital Currency: Considerations, Projects, Outlook; Centre for Economic Policy Research: London, UK, 2021. [Google Scholar]

- Serra, F.L. Manual de Diseño de Monedas Locales de Iniciativa Municipal; ADER: La Palma, Spain, 2015. [Google Scholar]

- Davis, T. Corporates Using Crypto: Conducting Business with Digital Assets; Deloitte: London, UK, 2021. [Google Scholar]

- Motta, W.; Dini, P.; Sartori, L. Self-Funded Social Impact Investment: An Interdisciplinary Analysis of the Sardex Mutual Credit System. J. Soc. Entrep. 2017, 8, 149–164. [Google Scholar] [CrossRef]

- Gibbons, L.V. Regenerative—The New Sustainable? Sustainability 2020, 12, 5483. [Google Scholar] [CrossRef]

- Huntjens, P. (Ed.) Towards a Natural Social Contract. In Towards a Natural Social Contract—Transformative Social-Ecological Innovation for a Sustainable, Healthy and Just Society; Springer: Berlin/Heidelberg, Germany, 2021; pp. 27–79. [Google Scholar]

- Mazzucato, M. The Value of Everything—Making and Taking in the Modern Economy; Public Affairs: New York, NY, USA, 2018. [Google Scholar]

Figure 1.

Three design blocks, the five detrimental processes and their combined impact.

Figure 2.

The foundations and nested logic of an EMT.

Figure 3.

Seeds ecosystem design.

Figure 4.

Trends in monetary transition processes (Adapted from [1]).

Figure 4.

Trends in monetary transition processes (Adapted from [1]).

Figure 5.

Spheres, dynamics and respective scales of circulation and use.

Figure 6.

Design principles and regenerative processes of an EMT.

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Alves, F.M.; Santos, R.; Penha-Lopes, G. Revisiting the Missing Link: An Ecological Theory of Money for a Regenerative Economy. Sustainability 2022, 14, 4309. https://doi.org/10.3390/su14074309

AMA Style

Alves FM, Santos R, Penha-Lopes G. Revisiting the Missing Link: An Ecological Theory of Money for a Regenerative Economy. Sustainability. 2022; 14(7):4309. https://doi.org/10.3390/su14074309

Chicago/Turabian StyleAlves, Filipe Moreira, Rui Santos, and Gil Penha-Lopes. 2022. "Revisiting the Missing Link: An Ecological Theory of Money for a Regenerative Economy" Sustainability 14, no. 7: 4309. https://doi.org/10.3390/su14074309

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.