Abstract

The 15 short chapters that form this 2023 ammonia-for-energy roadmap provide a comprehensive assessment of the current worldwide ammonia landscape and the future opportunities and associated challenges facing the use of ammonia, not only in the part that it can play in terms of the future displacement of fossil-fuel reserves towards massive, long-term, carbon-free energy storage and heat and power provision, but also in its broader holistic impacts that touch all three components of the future global food-water-energy nexus.

Export citation and abstract BibTeX RIS

Original content from this work may be used under the terms of the Creative Commons Attribution 4.0 license. Any further distribution of this work must maintain attribution to the author(s) and the title of the work, journal citation and DOI.

1. The ammonia energy roadmap: renewable chemically energised water for a clean-air, fossil-free future

William I F David1,2

1ISIS Neutron and Muon Source, STFC Rutherford Appleton Laboratory, Harwell Science and Innovation Campus, Didcot OX11 0QX, United Kingdom

2Inorganic Chemistry Laboratory, University of Oxford, South Parks Road, Oxford OX1 3QR, United Kingdom

Email: bill.david@stfc.ac.uk

Overview

The 15 short sections that form this 2023 ammonia-for-energy roadmap provide a comprehensive assessment of the current worldwide ammonia energy landscape and the opportunities and associated challenges facing the use of ammonia, not only in the part that it can play in terms of the future displacement of fossil-fuel reserves towards massive, long-term, carbon-free energy storage and heat and power provision, but also in its broader holistic impacts that touch all three components of the future global food-water-energy nexus.

An energy roadmap that focusses on ammonia as chemically energised water produced from renewable sources represents a future direction that is distinctive in emphasis from both the all-electric scenario of batteries and the promise of a future hydrogen energy economy powered by hydrogen fuel cells.

For the past one hundred years, ammonia has been used as the principal feedstock for inorganic fertilisers and has been of fundamental importance in providing sufficient food to feed our planet [1, 2]. As the 21st century progresses, net-zero ammonia has the additional potential to make an equivalently significant impact through enabling the transition away from our global dependence on fossil fuels and contributing, in substantial part, to the reduction of greenhouse gas emissions. As an overlooked advantage that parallels the emergence of battery electric cars (BEVs) as zero-emission vehicles, today's ammonia is already in a positon to help eliminate harmful emissions and address health issues associated with poor air quality (see section 2).

It is important in outlining this future ammonia energy roadmap to recognise its role not only in the distributed delivery of fossil-free power but also in the worldwide provision of carbon-free energy reserves. With our awareness of the impact of CO2 emissions on global warming, what often comes first to mind are fuels such as petrol and diesel that power internal combustion engines (ICEs) and produce emissions. These fuels must be abandoned. Unfortunately, though it should not be so, the demise of the ICE is often conflated with this move away from fossil fuels. Noting that there are around two-billion ICEs on the planet (1.4-billion of which power light vehicles [3]), it would be imprudent to ignore this technology as we head for net-zero in 2050 and the opportunities it may bring for a just transition. Future low emissions for ICEs are discussed extensively in this article (sections 11–13).

The demise of the ICE is, however, the anticipated future paradigm, particularly in Europe [4]. Battery electric vehicles (BEVs) are seen to be the way forward for passenger cars but with only 26 million BEVs on the road today across the world and a potential 100 million by 2030, replacing 1.4 billion ICEs is well out of reach. Moreover, despite a decade of BEVs, no significant market penetration has been achieved into other ICE markets such as trucks, trains and ships [5].

The only other motive power technology under consideration at present is hydrogen fuel-cell transportation. This, however, is a technology, despite over a decade of development, which does not have a global impact; there are currently only ∼800 operating hydrogen refuelling stations worldwide [6] and the global number of hydrogen fuel-cell vehicles at the end of 2022 was ∼72 000 [7].

Despite, the long history of ammonia-fuelled ICEs [8], it is only recently that the notion of retrofitting internal combustion engines based around ammonia has begun to gain traction. 2020 global ammonia production was 182.6 Mt with the capacity to reach 224.6 Mt [9]. The 42 Mt spare capacity could power ∼35 million cars which is similar in magnitude to BEVs and 500× higher than hydrogen fuel-cell vehicles. The smart money should be on future battery-ammonia hybrids. Based upon the global ammonia infrastructure, direct-ammonia solid-oxide fuel cells offer an attractive alternative (see section 9).

ICEs are criticised because of their emissions. With ammonia combustion, there are zero CO2 emissions and no carbonaceous particulates. NOx emissions and ammonia slippage are seen as the Achilles heel of ammonia-fueled ICEs. Recent research (see section 10), however, has shown that a ∼70:30 blend of ammonia and cracked-ammonia performs with ppm levels of NOx emissions on a par with petrol and diesel engines. The technical challenge is to reduce these emissions to safe environmental ∼ppb levels; the technologies exist to achieve this level of excellent and safe air quality.

Figure 1 illustrates the striking difference between the distribution of fuel types for primary energy consumption and primary energy storage. While coal, oil and gas account for 82% of primary energy provision [10], the no-carbon energy options together amount to a significant 18% fraction which is set to grow substantially, particularly in the areas of wind and solar. This is not the case for primary energy storage and distribution which is currently dominated, at 97%, by fossil fuels. The remaining 3% (∼4.3 × 103 TWh yr−1) is currently provided by pumped hydroelectric energy storage (PHES) [11] which, with a timescale of hours and days, does not address longer term, interseasonal energy storage. Two other potential storage technologies, Li-ion batteries and ammonia, which both have existing infrastructures are included in figure 1. With year-on-year cumulative global Li-ion battery capacity of ∼1.5 TWh at the end of 2022 [12], a 24 h charge-discharge regime corresponds to ∼0.5 PWh year−1. This 2022 capacity is set to increase by an order of magnitude by 2030 when it will be equivalent in size to global PHES storage capacity. Notably, however, both PHES and battery energy storage are short-term, essentially intra-day solutions.

Figure 1. (left) The 2022 distribution of global primary energy consumption obtained from the 2023 Statistical Review [10]; (right) The 2022 distribution of primary energy storage: coal, oil and gas are energy storage technologies prior to their consumption. PHES is the only fossil-free technology that is currently operational. The battery and ammonia-based storage values were calculated based on the scale of the existing battery and ammonia infrastrucures and represent their respective potential global storage opportunities. The energy numbers in the pie charts are in units of PWh (1PWh = 103 TWh).

Download figure:

Standard image High-resolution imagePHES and battery intra-day energy storage solutions make a crucial but only partial contribution to a future energy infrastructure. The scale and function of a 2050 global carbon-free energy infrastructure must be commensurate and align with the principal aspects of existing fossil-fuel energy storage. This is particularly important in terms of fuel transportation and the provision of long-term storage that ranges from days and weeks up to interseasonal and multi-year durations.

While there are substantial challenges in the transportation of hydrogen as a fuel, it is considered to be a potential candidate for long-term renewable energy storage for electricity provision, using salt mines where available as an option [13]. The challenge, however, is that although the 2022 annual global production of hydrogen is ∼80 Mt, almost all the hydrogen is immediately used onsite for the refining of oil or the production of ammonia and methanol. The 2022 global hydrogen storage infrastructure is not commensurate with its ∼80 Mt production, consisting of (i) ∼800 hydrogen refuelling stations worldwide [6] (which equates to 12 000 tonnes H2 year−1), and (ii) liquid hydrogen production and storage of ∼127 000 tonnes year−1 [14]. Together, this equates to a 2022 global specifically hydrogen storage infrastructure corresponds to ∼0.005 PWh year−1. This is in strong contrast to the current ammonia infrastructure which has an equivalent energy storage of ∼1.2 PWh year−1.

The 2022 ammonia infrastructure is almost entirely based on natural gas. In 2019, global ammonia production resulted in ∼500 Mt yr−1 CO2 emissions, equivalent to ∼1.5% of global CO2 emissions [8]. As a comparative sense of scale, the UK and Germany respectively emit ∼340 Mt yr−1 and ∼630 Mt yr−1 of CO2. Decarbonisation of ammonia production is one of the major industry transitions that must be achieved in tackling global warming as we head for a carbon-free energy future.

From an infrastructure perspective, ammonia is the most realistic future carbon-free replacement for fossil fuels. However, the scale-up required over the next quarter century is particularly challenging in principal part because of the need to move to carbon-free ammonia production. The development of TW-scale electrolyser global capacity (section 4) represents the main challenge. The redefining of the Haber-Bosch process powered by intermittent renewable energy (section 5) must also be addressed. Electrochemical and photochemical ammonia production are currently distant opportunities to explore (section 6) and the opportunities offered by nuclear energy should be investigated.

Roadmap summary

- The roadmap begins with a description of the current status of the global ammonia infrastructure and the opportunity to address immediately the challenges of air quality and zero-emissions zones prior to tackling full-scale decarbonisation (section 2).

- Sections 3 and 4 discuss immediate future opportunities

- Existing ammonia production must move away from the two-stage route of steam reformation of methane (SMR) followed by the traditional Haber-Bosch process. Water electrolysis supplants SMR. Scale-up is a major challenge and all electrolysis options must be explored with due consideration of the supply of critical materials and recyclability (section 5).

- Future electrochemical and photochemical methods of ammonia synthesis are long-term research projects that have the potential to be transformative if scale-up can be achieved (section 6).

- Options are presented for modification of the Haber-Bosch process, which will only operate efficiently in the future if the issues associated with the intermittency and irregularity of renewable energy production are addressed (section 7).

- Ammonia storage, transportation and delivery are all well-established features of the existing global infrastructure; section 8 discusses an integrated global perspective.

- Ammonia and hydrogen are both carbon-free fuels for heat and power provision. However, recent research has shown that ammonia-hydrogen blends offer improved performance. Section 9 discusses the catalyst challenges of transforming ammonia to ammonia-hydrogen (and nitrogen) blends.

- Fuel cell emissions are benign for both ammonia and hydrogen fuels and make fuel cells an attractive technology for the provision of clean power at high efficiency. Section 10 discusses the different fuel cell options for ammonia and ammonia-hydrogen blended fuels. One intriguing options is the use of direct ammonia solid-oxide fuel cells (SOFCs). With efficiencies already above 65%, they offer economy of performance. Importantly, SOFCs can be run in reverse as solid-oxide electrolysers (SOECs) which means that they can be used as the chemical equivalent of the electrochemical charging and discharging of batteries.

- Chapter 11 discusses the retrofitting of existing internal combustion engines, boilers, furnaces and turbines to operate with optimal ammonia-hydrogen blends. While the use of fossil fuels in these technologies will be phased out in many countries in the mid-2030s, green ammonia-hydrogen blends provide the opportunity that the only emissions will be water and nitrogen.

- Sections 12 and 13 exemplify the use of existing engine technologies for maritime and aviation sectors. The maritime industry is familiar with the international transportation of ammonia and plan to have ships in the water by 2024/5. There is also significant interest in the aviation industry but it is unlikely to be an early adopter with first demonstrations anticipated ca. 2030.

- One of the most challenging hurdles to overcome is the public perception of ammonia energy technologies. Chapter 14 presents the issues that must be addressed.

- The final section looks at longer term opportunities and challenges on the journey to zero-emissions, both zero-carbon (CO2) and zero-nitrogen (NOx), that together address the twin issues of climate change and clean air.

Concluding remarks

The ammonia roadmap presented in the various contributions in this paper not only offers a different emphasis but, importantly, can also build upon two existing global-scale industries, the ammonia-for-fertiliser industry and the internal combustion engine (ICE). While fuel cells offer strong future opportunities, the retrofitting of ICEs to run on ammonia-hydrogen blends reuses existing engines, offers low-cost, low carbon footprint options, and enables the possibility of realising a just transition particularly for low-income countries. It is also worthy of note that carbon-free ammonia and PHES are respectively chemically and gravitationally energised water and bring strong renewable and sustainability credentials to a future green energy infrastructure.

This roadmap emphasises the importance of both zero-carbon and zero-nitrogen emissions targets that together address climate change and air quality. Adopting this holistic approach not only moves us away from fossil fuels but could also trigger research, development and the achievement of reducing NOx emissions from transportation and power provision to natural ppb levels.

Carbon-free ammonia, as well as being a renewable fuel, will also be the future feedstock for fossil-free synthetic fertilisers that will continue to improve crop yields which help feed a clean-air world. With an appropriate over-production of potable water, ammonia and water will the two key molecules at the centre of the future food-water-energy nexus.

Acknowledgments

In preparing this roadmap, I acknowledge all the authors for their specialist contributions which together articulate the challenges, opportunities and optimism for a future net-zero energy infrastructure where ammonia plays a central role. I would like to thank Trevor Brown, the Executive Director of the Ammonia Energy Association, for his encyclopaedic understanding of all things ammonia and his preparedness to share that knowledge. Closer to home, I would also like to thank all the members, past and present, of my Oxford/STFC research group, particularly Tom Wood and Josh Makepeace. Finally, I wish to acknowledge my colleagues in Sunborne Systems, particularly James Barth, Tom Wood and Mark Picciani for the journey that we have begun and the optimism that we retain for the role of ammonia in a future carbon-free energy infrastructure.

2. The 2023 global ammonia infrastructure

William I F David1,2

1ISIS Neutron and Muon Source, STFC Rutherford Appleton Laboratory, Harwell Science and Innovation Campus, Didcot OX11 0QX, United Kingdom

2Inorganic Chemistry Laboratory, University of Oxford, South Parks Road, Oxford OX1 3QR, United Kingdom

Email: bill.david@stfc.ac.uk

Status

Ammonia has a decades-long, globally established infrastructure of manufacture, transportation, bunkering, storage and utilization (figure 2(a)). The vast size and global reach of this infrastructure is commensurate with the fundamental importance of synthetic anhydrous ammonia for global food production. The 2020 global gross tonnage for the production of ammonia was 182.6 Mt yr−1 while the total production capacity was 224.6 Mt yr−1 [5] which leaves a potential 42.0 MT yr−1 excess for the development of an ammonia-based energy infrastructure. The 2020 ammonia production figures (in Mt) are listed, by region, in table 1.

Figure 2. (left) The international shipping routes for ammonia (2020) [6]; (right) ammonia storage facilities in Los Angeles (2012) the areas of the circles are proportional to the tonnage of the ammonia storage facilities.

Download figure:

Standard image High-resolution imageTable 1. 2020 gross capacity, actual production and excess capacity of production (Mt) of ammonia by global region [5].

| Region | Africa | Oceania | C&E Europe | C & S America | Middle East | North America | NE Asia | Russia C Asia | S Asia | SE Asia | W Europe | World |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Capacity | 10.2 | 2.3 | 15.2 | 9.8 | 20.5 | 24.4 | 76.1 | 23.4 | 19.3 | 12.5 | 11.3 | 224.6 |

| Production | 9.7 | 1.9 | 8.9 | 6.7 | 16.8 | 22.2 | 55.1 | 22.9 | 18.7 | 10.5 | 8,5 | 182.6 |

| Excess | 0.5 | 0.4 | 6.3 | 3.1 | 3.7 | 2.2 | 21.0 | 0.5 | 0.6 | 2.0 | 2.8 | 42.0 |

Ammonia synthesis, after cement and steel production, is the third most CO2-intensive global manufacturing industry. In line with its importance for the provision of food, its production is worldwide with the majority of ammonia being utilized within its country of production.

Consistent with its mature infrastructure, there are, today, significant anhydrous ammonia storage capabilities at the beginning and end of each trading route. For example, the map of Los Angeles (figure 2(b)) shows the ammonia storage facilities (cyan circles) in the city. These data date back to 2012 and were obtained from the US Environmental Protection Agency. While the majority of the facilities store less than 100 t NH3, principally for cold-storage facilities and ice rinks, the largest circle corresponds to ∼47 000 t storage capacity; the cumulative capacity in the hinterland of the Port of Los Angeles amounts to ∼120 000 t, corresponding to an lower heating value (LHV) energy equivalence of ∼630 GWh. The highlighted Chevron El Segundo Refinery with ∼30 000 t storage capacity is worthy of note as it is situated less than a kilometer from the runways at Los Angeles International Airport; its unrecognized presence is an indicator of the long-term safety record of these facilities in terms of storage and transportation.

The global maritime sector, with its long-term familiarity with ammonia, is the first industry sector to recognize and begin to address the utilization, safety and regulatory aspects of ammonia as a future substitute for fossil fuels (see section 11). The farming sector in the US Mid-West is already well-versed in the handling and utilization of ammonia and is likely to be another early adopter of the use of ammonia as a fuel as well as a fertilizer.

The highest density of ammonia storage facilities in the USA, and indeed globally, is in America's Heartland, the Mid-West of the United States where anhydrous ammonia is used almost entirely for direct injection as a fertilizer into the soil. Figure 3(a) shows the 2012 distribution of the 1095 anhydrous ammonia storage facilities in Iowa. The combined capacity of these facilities is 822 000 t.

Figure 3. (a) 2012 distribution of the 1095 ammonia storage facilities in Iowa (b) 2020 distribution of the 2205 gasoline stations in Iowa. (c) The log–log graph showing the size distribution of ammonia storage facilities in Iowa ranging from 100 000–3.4 tonnes. From left to right: 10 000–100 000 t (red) 12 facilities; 1000–10 000 t (yellow) 9 facilities; 100–1000 t (green) 668 facilities; 10–100 t (blue) 366 facilities; 3.4–10 t (purple) 40 facilities.

Download figure:

Standard image High-resolution imageEach of the 1095 Iowan ammonia storage facilities have their own stories [15]. Together, they represent the reality of the massive presence of ammonia in the American Mid-West and are, in the lives of Iowans, as equally established as their 2205 gasoline stations. The lack of awareness outside the American Heartlands of the everyday use of ammonia within these US States is testimony to the actuality of the long-term safe handling and use of ammonia.

Although regulations in the American Mid-West are in place for the transportation and storage of ammonia and its use as a fertilizer, issues of regulation and public perception of ammonia as an energy vector, power source and emissions-free fuel must be fully addressed over the upcoming years before ammonia can impact transportation in the US Mid-West (see section 14).

The physical properties of ammonia, in particular boiling point and room-temperature vapor pressure, are similar to liquid petroleum gas (LPG). LPG, often referred to as Autogas, is principally a combination of propane (C3H8) and butane (C4H10) with boiling points of −45 °C and −0 °C respectively at atmospheric pressure; ammonia boils at −33.3 °C. At 25 °C, the vapor pressure at the gas-liquid equilibrium of propane, butane and ammonia are approximately 9 bar, 4 bar and 10 bar respectively. Much of the infrastructure of current LPG forecourts can, in principle, be reused but it will take significant time to demonstrate, review and approve the regulatory and safety aspects associated with fuel dispensing and on-vehicle storage and use.

Status: the current role of hydrogen in the global ammonia infrastructure

For the past decades, the substantial majority of ammonia production has been based upon three collocated processes. The sequential chemical reactions, along with their individual durations, are:

The flow diagram detailing these three processes are explained and physically located in the annotated aerial view of the CF Fertilizer Ammonia Manufacturing Facility at Ince in NW England (figure 4). The raw materials in the production of ammonia are methane, water and air. Hydrogen is only briefly present, beginning its journey, for ∼15 s, in the SMR process (1 and 2 in figure 4) and then synthesized in the water-gas shift reaction (3 and 4) taking a further ∼3 min. Transferring the hydrogen ∼300 m to the ammonia synthesis reactor (9) takes ∼3 min after which it is reacted with nitrogen to form ammonia. The full synthesis loop takes of order 16 min after which the ammonia is refrigerated, (10), and finally stored (11), prior to transportation or fertilizer production. Hydrogen's journey from its production to the production of ammonia takes less than 30 min and travels ∼300 m. The raw materials for the production of ammonia are methane, water and air; hydrogen and nitrogen are brief transients.

Figure 4. Aerial view of the CF Fertilizer Ammonia Manufacturing Facility at Ince next to the River Mersey in the UK. The area of the ammonia production component at Ince is around 2.5 hectares. The numbers indicate the various stages in the synthesis of ammonia. The ammonia storage tank has a capacity of 10 000 t (which has an LHV energy equivalent to of 50 GWh).

Download figure:

Standard image High-resolution imageThe CO2 that is produced in the water-gas shift reaction is removed (5) prior to the Haber–Bosch process (9). In most existing ammonia production facilities, CO2 is either vented or used to produce urea. Given the massive global scale of ammonia production and the point source nature of its CO2 emissions, carbon capture is an important opportunity that is relatively straightforward to achieve and would result in a 500 Mt reduction (∼1.2% global) in CO2 emissions. This blue ammonia transition is important for existing ammonia plants. Future plants, however, should be carbon-free with only air and water used as the raw materials. This is discussed further in section 15.

Concluding remarks

In ammonia production, which is the principal industry in today's fossil-fuel based hydrogen economy, it is a paradox that hydrogen itself is only fleetingly present. It is incongruous that, while 182 Mt of ammonia are manufactured annually and ∼20 Mt yr−1 are transported across the oceans, hydrogen, in its eponymous economy, journeys a few hundred meters for less than half an hour. The durations and distances are similar in the refining of oil which together with ammonia accounts for ∼90% of the current usage of hydrogen. Although the 2023 annual production of hydrogen headlines at ∼80 Mt, the cumulative global yearly usage of hydrogen amounts to 134 000 t which represents only 0.17% of global hydrogen production. Hydrogen is widely promoted to be the green fuel of the future and is the eponym for the future green chemical revolution. However, the molecule with its own existing global infrastructure that has the most favorable credentials to eventually displace fossil fuels, for both storage, transportation and utilization, is ammonia.

Acknowledgments

The author wishes to thank Trevor Brown, Executive Director of the Ammonia Energy Association, for mining the databases of the US Environmental Protection Agency to retrieve information about the tonnage and very precise locations of anhydrous ammonia facilities across the United States. I also want to thank my daughter, Anna Di-Lieto, for producing the many extremely informative maps that articulate and reveal the magnitude of the prevalence of ammonia facilities across the United States. I also wish to thank Paul Sharp and Nicolas Cook, from CF Fertilisers UK, for explaining in detail the processes involved in the production of ammonia from natural gas, water and nitrogen and, in particular, to chart out the short lifetime and distance of travel of hydrogen before ammonia is stored, transported and used for fertilizer production.

3. Overview of current and future opportunities for low-carbon ammonia

Kevin H R Rouwenhorst1,2 and Rolf S Postma3

1Ammonia Energy Association, 77 Sands Street, 6th Floor, Brooklyn, NY 11201, United States of America

2Proton Ventures, Karel Doormanweg 5, 3115 JD Schiedam, The Netherlands

3Stamicarbon B.V., 6135 KW Sittard, The Netherlands

Email: krouwenhorst@ammoniaenergy.org and rolf.postma@stamicarbon.com

Status

Ammonia is currently almost exclusively produced from natural gas (72%) and coal (22%), following the Haber Bosch process, with heavy fuel oil and naphtha accounting for the remainder [16] This fossil-based ammonia is generally termed grey ammonia. Hydrogen production typically consumes around 95% of the total energy required for ammonia production [16]. The decarbonization of ammonia production is dominantly focused on decarbonizing hydrogen production.

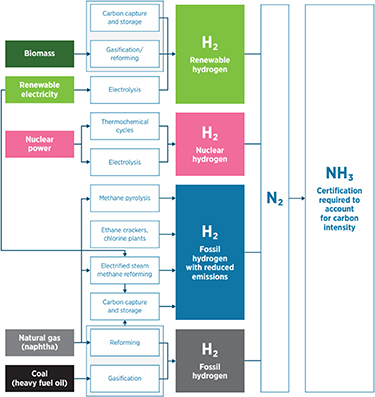

Decarbonization can be achieved (1) through carbon capture of emissions from fossil-based hydrogen production, or (2) through and net zero-carbon hydrogen production methods [17]. An overview of ammonia production pathways is shown in figure 5. The preferred method for decarbonization depends on local resources and incentives as well as the envisioned production capacity [18].

Figure 5. Production pathways of ammonia from various feedstocks. Reproduced with permission from [17]. © IRENA 2022.

Download figure:

Standard image High-resolution imageBlue ammonia is a term frequently used for ammonia produced from fossil fuels, where a significant part of the CO2 emissions are mitigated. It should be noted that the net CO2 emissions can vary depending on the carbon-capture rate in the process, e.g. capturing just the concentrated CO2 from the hydrogen production for the ammonia loop, or also the more dilute CO2 flue gas. Furthermore, the carbon intensity of the fossil feedstock prior to the ammonia synthesis plant should be considered, for example scope 2 and scope 3 emissions from natural gas extraction and transport.

Thus, the carbon intensity of the produced 'blue' ammonia can vary strongly. Therefore, color coding should not be taken as the sole indicator, but rather the carbon intensity and other sustainability indicators. Therefore, transparent frameworks for Life Cycle Assessment are required to certify the carbon intensity of the produced ammonia [17].

Green ammonia is the term used for ammonia that is produced from renewable energy sources, i.e. renewable ammonia, such as solar PV, wind or hydropower coupled with water electrolysis for renewable hydrogen production. Upon combining renewable hydrogen with atmospheric nitrogen and compressing the mixture to 100–450 bar, ammonia can be synthesized via the Haber–Bosch process. An alternative for zero-carbon electricity (and heat) is nuclear power, which is generally termed pink ammonia.

Another pathway for producing renewable ammonia is from circular biomass, biogas, and solid waste. As biomass contains carbon, it can be utilized to produce hydrogen together with CO and CO2 in a process analogues to fossil fuel-based route. This can be beneficial for renewable urea production, which requires carbon oxide as reactant. Biogas can be blended with natural gas in steam methane reformers (SMRs) and autothermal reformers (ATRs) in existing natural gas-based ammonia plants. Similarly, biomass and solid waste can be blended with coal in gasifiers in existing coal-based ammonia plants.

Current and future challenges

About two thirds of CO2 is typically captured in existing natural gas-based NH3 plants with SMRs. However, the remaining one third is in the flue gas at low concentrations and thus at high carbon capture cost. It should be noted that captured CO2 from NH3 plants is currently mainly used for producing urea (CO(NH2)2), which accounts for 55% of current NH3 usage [19]. This CO2 from urea is short cyclical and eventually emitted into the atmosphere upon urea usage, and does not result in a net CO2 emission reduction. For this, permanent CO2 sequestration via carbon capture and storage (CCS) is required. Furthermore, sector coupling with for instance steel production can allow for decreasing the net carbon footprint of the CO2 emitted during urea utilization. However, this raises the question how the CO2 emissions should be calculated and allocated.

Fossil feedstock for ammonia synthesis also has emissions upstream of the ammonia production plant, such as methane leakage during natural gas extraction. This means the supply chain to the ammonia plant must be decarbonized with best practice technologies and procedures.

Renewable ammonia plants are announced at locations with the best renewable resources. However, renewables such as solar and wind are fluctuating electricity sources, implying the ammonia plant must be oversized to meet the required production capacity and be able to operate highly flexibly. In general, electrolysis-based ammonia plants have a higher upfront cost than fossil-based ammonia plants. This is due to the electricity generation that needs to be built together with the ammonia plant, typically accounting for over half the investment required [17]. Alternatively, a power or hydrogen purchase agreement can be closed with a renewables developer which provides electricity for the ammonia plant. This shifts the electricity cost from a capital expenditure (CAPEX) to an operational expenditure for the ammonia plant operator.

The ideal locations for renewable ammonia plants must be identified, not only based on the optimal renewable electricity profile for the ammonia plant, but also on societal acceptance and favorable legislation. The availability of water is another issue that must be taken into account. Consequently, most renewable ammonia projects that have been announced ae located near the sea or a freshwater source.

Electrolysis-based ammonia plants will see a shift in production location from the traditionally fossil feedstock rich locations to more disperse renewables-optimal sites, which will allow certain regions to become self-sufficient in fertilizer production. The absence of carbon in the ammonia synthesis will require a shift from urea as most common fertilizer, or an available circular carbon source for urea.

Nuclear power (and heat) has its specific sets of challenges. Firstly, the electricity cost of existing nuclear power is typically too high to be utilized for electrolysis [20]. Furthermore, the perceived risk of nuclear power generation and nuclear waste production imply its introduction is not accepted in all locations. Lastly, current nuclear power plants typically have a capacity around 1 GW, while electrolysis capacity is typically orders of magnitude smaller, implying a size mismatch.

It is likely that trade of low carbon ammonia will initially be point-to-point, while a more global market will be established at a later stage. It remains uncertain whether a cost premium will be acceptable for low carbon ammonia and if so, how the premium will need to be determined.

Advances in science and technology to meet challenges

Fossil-based ammonia production, and specifically the hydrogen production, can be decarbonized along various pathways. Existing SMRs can recycle part of the hydrogen product to the burners, thereby decreasing the amount of CO2 produced in the flue gas. Alternatively, ATR can be utilized as a substitute for SMR, especially in large-scale plants [18]. ATR combines hydrogen production and natural gas combustion inside the reactor, implying all CO2 will be concentrated and can be easily removed. Novel technologies for natural gas processing include electrified steam methane reforming [19], e.g. the gas-fired heating is replaced by electric heating, and methane pyrolysis, where methane is split into hydrogen and solid carbon [20].

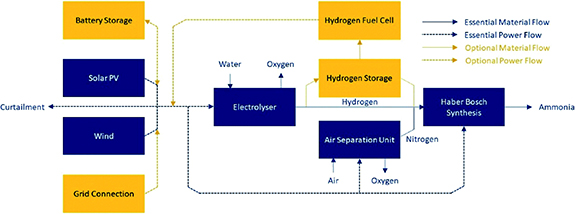

Fluctuations in renewable energy profiles can be accounted for with (1) energy storage buffers and/or ammonia or hydrogen storage, (2) firming with a stable electricity, and (3) more flexible ammonia synthesis loops [17], as shown in figure 6. The most economic design is often a compromise between these three strategies. Energy storage buffers include e.g. (flow) batteries to smoothen solar and wind peaks, ammonia storage tanks or hydrogen storage in high pressure vessels or salt caverns. Hydrogen storage can be combined with a hydrogen fuel cell for electricity generation [21] and stable electricity sources used for firming include the grid, nuclear, geothermal or hydropower. The latter was the electricity source used in the past for renewable ammonia production [22]. High temperature nuclear reactors offer a further option as heat may be utilized for steam electrolyzers, decreasing the electricity demand for hydrogen production. Flexible ammonia synthesis loops designed for renewable feedstock can operate down to 10%–30% ammonia outlet capacity [23, 24]. It should be noted, however, that a reduction in load factor of the ammonia synthesis loop results in a higher relative energy cost.

Figure 6. Conceptual diagram of renewable ammonia production including storage buffers. Reproduced from [21]. CC BY 3.0.

Download figure:

Standard image High-resolution imageHydrogen certification schemes are currently set up, based on established LifeCycle Assessment methodologies to estimate carbon intensity, as well as the Sustainable Development Goals. These schemes allow for harmonized trade between jurisdictions. Similar schemes are being developed for certifying ammonia, although these are not yet ready or widely accepted at the moment.

Concluding remarks

Decarbonization of ammonia production is possible with commercially available and proven technologies, such as CCS from hydrogen production, low carbon electricity coupled with water electrolysis, and biomass or waste gasification. Existing low carbon technologies should be implemented today where feasible. Innovative technologies can be implemented at a later stage.

Existing plants may require a combination of low carbon technologies to decarbonize. For example, an SMR-based plant can be decarbonized by replacing part of the natural gas feedstock with biogas, by capturing and storing the CO2 produced, and by replacing part of the hydrogen production with electrolysis. New-build plants can be designed for flexible load operation, to address the issue of fluctuating solar and wind resources, while storage buffers may still be required.

As ammonia takes off as a zero-carbon energy vector, renewable ammonia production in locations with the best solar and wind resources may scale-up to renewable energy hubs with tens of GW upstream solar and wind capacity. This is an order of magnitude bigger than the largest fossil-based ammonia production sites.

Acknowledgments

The authors acknowledge discussions with colleagues at the Ammonia Energy Association, Proton Ventures, and Stamicarbon B.V.

4. Green technologies: low temperature electrolysis (alkaline, PEM), high temperature electrolysis (SOEC), integrated H2, N2 production

John Bøgild Hansen

Topsoe, Haldor Topsøe Alle 1, 2800 Kgs. Lyngby, Denmark

Email: jbhenator@gmail.com

Status

Ammonia is carbon free and can be produced from air, water and renewable electricity by electrolysis. It is easily liquefied and its relatively high energy density of 3.53 MWh m−3 makes it an attractive energy vector for sustainable energy scenarios compared to the use of hydrogen.

Ammonia production via low temperature electrolysis for hydrogen manufacturing and cryogenic air separation for nitrogen supply was practiced worldwide before the advent of modern, natural gas based plants using steam reforming for ammonia synthesis gas production. Operating experience from such a plant based on alkaline electrolysis using hydropower is described in reference [25].

Norsk Hydro operated two plants at 160/165 MW capacity based on their own alkaline electrolyzer design. The Faradaic efficiency is given as 98% at start, degrading by 1% absolute every 4 years. Cell voltage also increased from 1.67 V/cell at the start to 1.8 V after 4 years. Overall energy consumption is stated to be 10 MWh Mt−1 ammonia, including power for air separation (1%) and Haber–Bosch synthesis (7.5%). The power required for the electrolyzer unit was 4.4 kWh Nm−3 H2 as DC power, e.g. ignoring transformer losses. In figure 7 are shown the mass and energy flows for an alkaline 1000 ton per day plant [26].

Figure 7. Overview of low temperature electrolysis based ammonia production. Reprinted from [26], with the permission of AIP Publishing.

Download figure:

Standard image High-resolution imageLow temperature PEM based electrolysis is an established technology that can also be used and is better suited for intermittent and low-load operation as will be required for direct coupling with wind or solar renewable power. PEM electrolyzers are also operating at higher current densities than alkaline so the footprint will be reduced [27, 28].

SOEC operates at 700 °C–850 °C and offers much better energy efficiency at 7.7–7.9 MWh ton−1 ammonia due to favorable thermodynamics and the fact that they use steam instead of liquid water. Part of the steam can be provided by utilization of the ammonia synthesis reaction heat [29, 30].

The nitrogen required for ammonia synthesis is manufactured by air separation. Cryogenic separation is the preferred choice for large capacities as they are energy efficient albeit very expensive. The nitrogen required for 1 ton of ammonia requires an energy input around 200 kWh [31]. Cryogenic plants do, however, not scale well at smaller capacities (scaling exponent close to 0.5). For smaller scale, decentralized plants pressure swing adsorption or membranes will be preferred but they are less energy efficient requiring 300–400 kWh per ton of ammonia for the nitrogen production [31].

Current and future challenges

Electrolysis for green ammonia production will, in the majority of cases, entail coupling to intermittent renewable power sources. This in turn puts an additional emphasis on bringing down the CAPEX. This can be accomplished by increasing the current density (A cm−2) provided that lifetime is not unduly compromised. Long lifetimes of many years have been demonstrated for classical alkaline electrolysis. The prospects for PEM-based systems looks encouraging. Degradation rates for SOECs have improved dramatically lately but challenges with, for instance, agglomeration of nickel in the fuel electrode remains. SOECs have, however, a wide temperature operation window, which can be used to counteract ageing [32, 33].

Robustness is as equally important as durability. This means resilience with respect to operational upsets resulting in off-design conditions with respect to electrical, temperature and/or mechanical stresses. Other aspects include resistance or mitigation of poisons in the feedstocks.

Minimizing cross-over of reactants, which represent a loss of Faradaic efficiency and limit the minimum operation point because explosion limits can be exceeded, is major challenge for alkaline electrolyzers and to some extent for PEM especially at higher pressures.

Mechanical compression of hydrogen is less efficient than electrochemical within the electrolyzers. As ammonia synthesis is operating at pressures preferably above 100 bar, it is beneficial to operate the electrolyzers at elevated pressure. Alkaline electrolysis has successfully been achieved at 30 bar g and PEM electrolysis at much higher pressure. Pressurized operation of SOEC is under development. For all three technologies elevated pressures means increased demands on durability.

From above discussion, it is evident that more than 90% of the energy input for an electrolysis-based ammonia plant is used for the production of hydrogen. Improvement in the Haber–Bosch synthesis would thus only have a minor impact, but for alkaline as well as PEM electrolysis there is room for improvement of efficiency by lowering the different internal resistance. However, for both technologies the possible improvements are limited by the fact that water in liquid form is used. Accordingly the heat of evaporation has to be supplied in the form of electricity to the stacks (approximately 0.5 kWh per Nm3 of hydrogen or 1/6 of the LHV). SOEC electrolyzers use steam, which can in part be provided by use of the reaction heat from the ammonia synthesis plant so that >99% efficiency (LHV basis) can be achieved and has been demonstrated in practice.

With respect to PEM electrolysis the most important challenge is to find and acceptable substitute for iridium as an active oxygen electrode.

Advances in science and technology to meet challenges

The challenges for all electrolyzer technologies are related to the trade-offs realized when trying to simultaneously optimize CAPEX, efficiency and durability.

For alkaline electrolyzers, the search for improved nickel electrode catalyst have intensified in order to increase surface area and activity so that both efficiency and current density can be improved.

For PEM electrolyzers, the most important problem to solve is to optimize the oxygen electrode, where only iridium, at present, can be used. Iridium is a very scarce noble metal with a yearly production of only around 10 metric tonnes per year [34, 35].

For SOECs, improved electrodes could be used to lower the operating temperatures further and also improve lifetime. Better morphology and new materials for both cathode and anode are relevant challenges.

The diaphragm is an important focus point for alkaline technology. Reduced thickness would improve efficiency. Another challenge would be to improve the PTl (porous transport layer) by, for instance, zero gap electrodes in order to improve mass transfer.

PEM electrolyzers use very expensive PTLs with platinum coated titanium. There is limited scope in reducing membrane thickness which are probably close to the optimum.

A better understanding of the mechanism(s) behind nickel agglomeration degrading SOEC performance would facilitate the search for solutions.

All electrolyzer technologies are sensitive to minute amounts of poisons or contaminants from the feedstock or construction materials including the raw materials for the stack. Efficient clean up materials will increase durability considerably and/or reduce balance of plant (BOP) costs.

Another common theme will be to increase cell and stack sizes leading to economy of scale savings in the BOP.

There are also room for improvements in manufacturing the stacks by automation and streamlining supply chains. Power supply units are expensive and incur efficiency losses.

Finally research into optimized and safe operating procedures is especially relevant given that intermittent operation and integration with downstream ammonia production will become of paramount importance.

Concluding remarks

Ammonia has emerged as an interesting energy vector in the transition to a sustainable carbon-free energy. IEA foresee in their net-zero carbon scenario for 2050 that 74 Mtonnes ammonia is used for electricity production and 250 Mtonnes for transport. IEA concludes that electrolysis becomes competitive with natural gas based production with CCUS at electricity prices in the range of USD 15–50 MWh−1 for ammonia, on the assumption of gas prices of USD 3–10 GJ−1 provided electrolysis CAPEX decrease by 50% and efficiency increases by 15%.

The targets are within reach to address the challenges discussed above. The scale and speed required for the deployment of electrolysis based green ammonia technology to take place is daunting and will require massive scientific, technological and financial innovations. An exemplar is the use of ammonia for shipping has attracted significant interest. If 30% of the forecasted demand for shipping fuels in 2050 was to be met by ammonia, an extra production capacity of 150 million tons per year would have to be installed. Approximately 400 GW of renewable power would be required to sustain this production if based on alkaline electrolysis with an energy consumption of 10 MWh MT−1 ammonia [36].

5. Redefining the Haber–Bosch process for green ammonia production

Laura Torrente-Murciano and Collin Smith

Department of Chemical Engineering and Biotechnology, University of Cambridge, Philippa Fawcett Drive, CB3 0AS Cambridge, United Kingdom

Status

The global ammonia production in 2022 is ∼180 million tons per year and is used primarily for fertilizer purposes, which, in turn, is reckoned to provide food for over 50% of the world's population. Currently, ammonia is produced through the Haber–Bosch process using fossil fuels as feedstock and energy source (mainly natural gas, but also coal and oil). This over-100-year-old technology, has been highly optimized and integrated, and is close to reaching its thermodynamic efficiency [37]. It is designed to operate continuously 24/7 and benefits from economy of scale with typical ammonia plants producing ∼2000–4000 tonnes of ammonia per day. However, it is only an optimization for extracting hydrogen and energy from fossil fuels. Industrial ammonia production today consumes ∼2% of the global energy demand and is responsible of ∼1.5%–2.0% of the overall CO2 emissions.

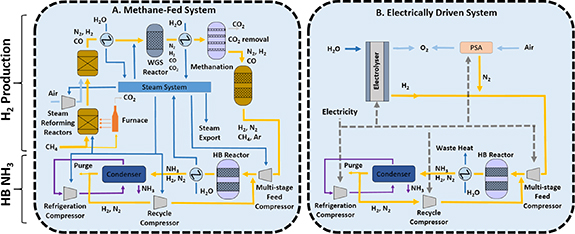

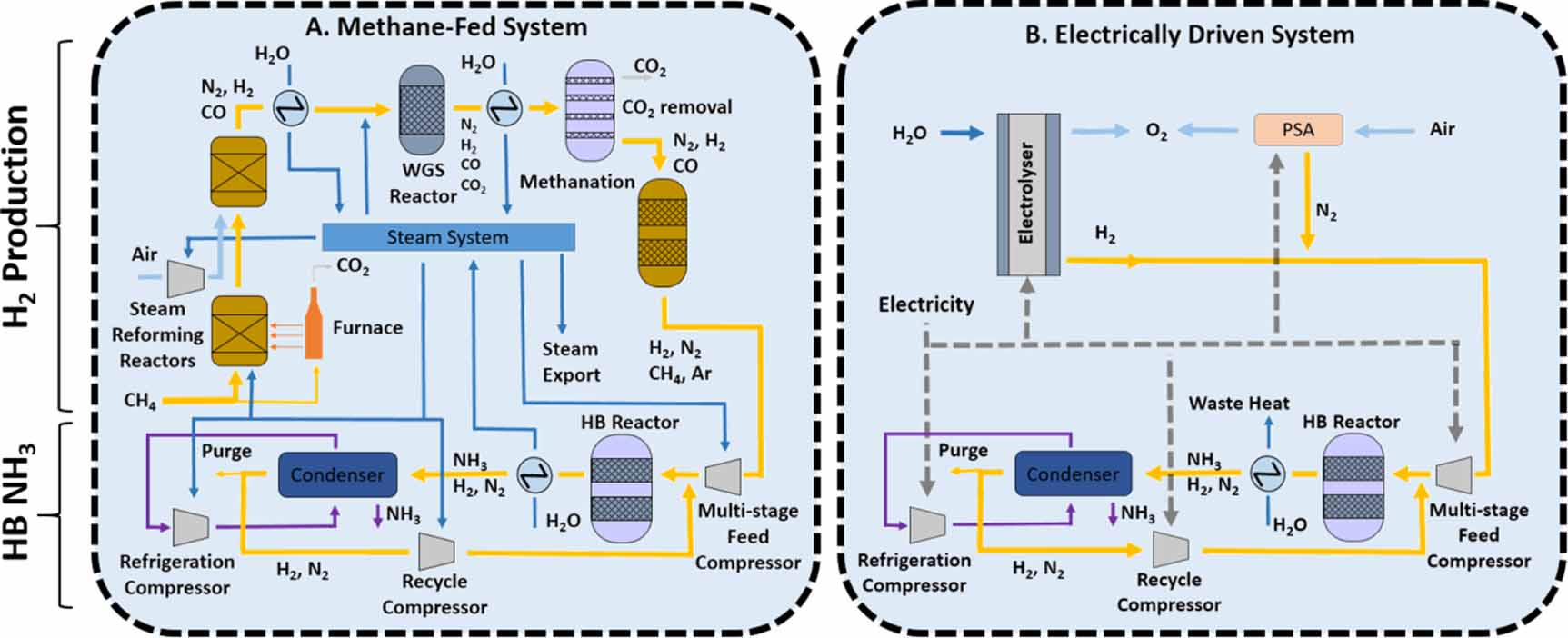

Currently, the thermo-chemical production of ammonia is the only feasible route for industrial ammonia production due to the high reaction rates and hydrogen utilization in comparison to electrochemical or plasma routes [38, 39]. However, its future relies on electrification, where the process will be exclusively powered by renewable energy using air and water as feedstocks. In the conventional Haber–Bosch process, hydrogen and heat are produced by steam-reforming of fossil fuels, followed by their use in the ammonia synthesis step (Haber–Bosch loop) (figure 8(A)). Electrification requires the decoupling of these two steps, with hydrogen being produced by the electrolysis of water using renewable energy (or alternative sustainable sources such as reforming of biogas) (figure 8(B)). This transformation opens up opportunities for the design of new processes, the re-development of the Haber–Bosch loop and the need for new optimization and integration strategies.

Figure 8. Schematic diagram of (A). A typical conventional methane-fed Haber Bosch process and (B). An electrically powered alternative. Hydrogen and ammonia production stages are separated for illustration purposes to identify similitudes and differences between both technologies. Yellow lines are process gas, dark blue lines are water/steam, light blue lines are air, purple lines are ammonia, and dashed lines are electricity. Reproduced from [37]. CC BY 3.0.

Download figure:

Standard image High-resolution imageThe successful development of green ammonia synthesis processes will deliver, in the short term, green fertilizers to provide food security in a sustainable manner. Equally important and with a potential higher impact, it will deliver a unique solution for the chemical long-term storage of renewable energy, mimicking the way that fossil fuels store energy but in a carbon-free molecule [40]. The high energy density of ammonia at mild conditions will trigger an international trading of renewable energy. It will also witness a multitude of uses of ammonia as a direct fuel to meet our transport and heating demands [41], and via its decomposition, as a source of ammonia-hydrogen fuel blends and pure hydrogen itself.

Current and future challenges

The production of green ammonia has been demonstrated at an industrial scale for more than a century. Indeed, the first industrial production of green ammonia was developed in Italy in 1921. Other green ammonia plants followed around Europe (e.g. Spain, France, Norway, Sweden) and around the World (e.g. Japan, Canada and USA) representing approx. 25% of the global ammonia production in 1930 (∼0.5 m tnNH3 out of the total annual global production of approx. 2 m tnNH3) [42]. In all the cases, hydrogen was produced by water splitting using alkaline electrolyzers powered by hydropower in relatively small units (∼300 tnNH3 per day). The onset of cheap and abundant natural gas, the technological development of hydrogen extraction from fossil fuels and the difficulties regarding scaling-up electrolyzers led to their closure by mid 1960 s, based on economic terms.

Current environmental pressures, the desire for energy independency as well as improvements in electrolyzer efficiency and cost reduction has re-initiated the interest in green ammonia production. However, the increase in ammonia demand creates a need to tap on renewable energy sources beyond hydropower. This is further exacerbated if green ammonia is to play a role as carbon-free energy vector in the future energy transitions where its production scale is expected to increase 5–10 times. Although hydropower still represents the largest proportion of renewable energy, we are currently witnessing fast developments in solar and wind sources due to their reduced cost, lower environmental impact and the larger array of suitable locations [22]. However, solar and energy power capacities are intermittent, strongly dependent to the location and distributed.

The production of 1000 tn d−1 of green ammonia requires 176.5 tn d−1 of green hydrogen. Assuming the bulk figures of the need of ∼60 MWh/tnH2 (using a typical commercial alkaline electrolyzer) and the land requirements of 0.50 MW/hectare when using solar energy and 0.06 MW/hectare when using wind energy and a typical capacity of 20% and 40% for solar and wind energy respectively [43], one can estimate the bulk land requirements for future green ammonia production. Thus, a green ammonia plant with a production capacity of 1000 tnNH3 d−1 will require a land extension in the order of at least 4400–18 400 hectares, equivalent to 4%–17% of the area of London or ∼6000–26 000 football pitches, when using solar and wind power respectively. It is important to note that this production capacity is less than half the average production capacity of a conventional ammonia plant.

Advances in science and technology to meet challenges

This analysis leads to three options:

- i.decentralized electricity production with transmission to centralized plants,

- ii.decentralized hydrogen production where a number of renewable energy installations produce hydrogen locally, transported (e.g. by pipelines) to a centralized ammonia production plant and

- iii.decentralized small-scale ammonia production with plants with small capacities.

The first option might consider electrified ammonia plants connected to the grid, assuming that the grid is sufficiently decarbonized. It requires large investments in grid infrastructure as well as ensuring that remote renewable energy installations have connection to the grid. An alternative is the use of private connections. The second option of decentralized hydrogen production will facilitate the deployment of green ammonia plants with large capacities (i.e. similar to the current ones) while the third option opens a wide range of opportunities for localized green ammonia production, eliminating the potentially elevated cost of transport for both, hydrogen and ammonia.

In all three cases, the economics are skewed by the current cost of renewable energy and electrolyzers [44]. Technological breakthroughs are urgently needed for more efficient hydrogen production with electrolyzers able to use low purity water (e.g. desalinated water) to avoid pressures on water accessibility [45]. In addition, decoupling the hydrogen and ammonia production steps requires new process integration strategies. Heat integration between different process steps are particularly relevant to maximize the overall energy efficiency. It is important to note that conventional heat integration approaches might fail in these enterprises as some of the process steps may not be co-located in space and/or time, as discussed above.

The lack of a continuous energy supply from renewables, in contrast to fossil-fuel based energy supply today, presents a number of challenges. For electrified ammonia plants connected to the grid (option i.), it will be translated in weather-dependent short-term variations of the electricity price. For decentralized hydrogen or ammonia production options (ii. and iii. above), it will rely on the use of energy buffers such as batteries and/or hydrogen storage to cope with short-term energy supply variations. The dependency on hydrogen buffers is further exacerbated by the challenges of coping with the seasonal variations of renewable energy which can account to >20% of the levelized ammonia cost [44].

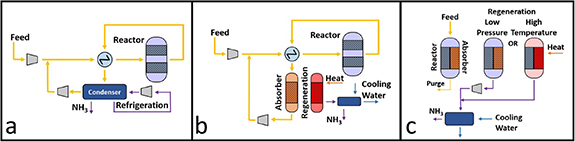

A highly attractive alternative to the options discussed above is the development of flexible ammonia synthesis technologies with ramping capabilities able to respond and align as much as possible to the renewable energy production profiles. The development of low temperature, non-noble metal based catalysts will certainly contribute towards this endeavor. However, greater impacts can be achieved when considering a holistic process development [46]. For example, replacing ammonia separation using condensation by absorption in the synthesis loop removes the need for high pressures (∼150 bar) of the current process, opening the door to mild pressure operation (∼20–30 bar) [47], directly enhancing its flexibility to ramp capacity (figure 9(b)). A more innovative approach is the integration of the ammonia synthesis and separation steps into a single-vessel recycle-less process [48, 49] (figure 9(c)). This inherently safe process is able to perfectly mimic the hydrogen production profile with no possibilities of leading to run-away reactions. This approach however, will lead to a low capital utilization.

Figure 9. (a) Conventional Haber–Bosch ammonia synthesis loop, (b) replacement of ammonia via condensation by absorption opening the door to mild pressure operation and (c) single-vessel recycles process where the synthesis and separation steps are integrated. Reproduced from [37]. CC BY 3.0.

Download figure:

Standard image High-resolution imageConcluding remarks

The synthesis of green ammonia exclusively powered by renewable energy and using air and water as feedstock has been technologically feasible since the onset of this industrial process. However, its economic feasibility away from subsidies and carbon credits relies on technological innovations able to minimize the detrimental effects of the intermittent nature of renewable energy. Amongst them, the development of nimble processes able to operate away from steady-state following the energy supply profile will be a paradigm shift in the chemical industry. Similarly, distributed small-scale modular ammonia production systems will transform the well-established economy-of-scale while avoiding the need of transport and providing cost control over market fluctuations. In all cases, novel optimization tools, safety and integration strategies are required to tailor the design and operation to location and needs. As a result, the successful development of green ammonia processes will not only lead the way for the electrification of the chemical industry on what is called Power-to-X but most importantly will enable the long-term storage and trading of renewable energy to open the door to a new green energy landscape.

Acknowledgments

The authors would like to thank the UK Engineering and Physical Science Research Council (EPSRC—Grant Number EP/X016757/1) and Breakthrough Energy for the Explorer grant Ammpot for funding.

6. Electrochemical & photochemical ammonia synthesis/electrochemical nitrate reduction

Douglas R MacFarlane1, Alexandr N Simonov1, Andrew Medford2, Marta Hatzell2

1School of Chemistry, Monash University, Clayton, Victoria 3800, Australia

2School of Chemical & Biomolecular Engineering, Georgia Institute of Technology, Atlanta, GA 30310, United States of America

Email: Douglas.macfarlane@monash.edu, alexandr.simonov@monash.edu, ajm@gatech.edu and marta.hatzell@me.gatech.edu

Status

Electrochemical reduction of N2 to ammonia is an attractive process that would ideally consume only N2, protons from the electrolyte and electrons at the cathode, while at the same time carrying out water oxidation at the anode. Thermodynamically, the N2 + 6H+ +6e−

2NH3 process occurs at a more positive potential than proton reduction (2H+ + 2e−

2NH3 process occurs at a more positive potential than proton reduction (2H+ + 2e−

H2), such that it should be possible without interference from hydrogen evolution. Hundreds of research reports have been devoted to this nitrogen reduction reaction (NRR), exploring a wide variety of electrocatalysts [50]. However, the overpotentials required are invariably sufficient that H2 production does occur. The Faradaic Efficiency (FE = the fraction of charge applied that results in ammonia) then becomes an important metric of the effectiveness of the electrocatalyst. Unfortunately, there are very few reports of FEs >50% and most are <20%. Even more challenging, the rates of the reaction per unit area, measured in mol(NH3) s−1 cm−2, are typically very small; so small that interference from other reducible N-compounds, including nitrates and NOx

gases, becomes a concern. In recent years the field has recognized the need to include quantitative 15N2 reduction experiments to verify the source of the nitrogen [51]. Tests with a small, fixed volume of nitrogen is another approach to prove the genuine nature of the NRR. The net result is that a number of the more substantial claims of success with aqueous NRR are being refuted [52] and the vast bulk of the reports are considered to be too low in yield rate to be practical [50], even if it can be shown that they do represent genuine NRR.

H2), such that it should be possible without interference from hydrogen evolution. Hundreds of research reports have been devoted to this nitrogen reduction reaction (NRR), exploring a wide variety of electrocatalysts [50]. However, the overpotentials required are invariably sufficient that H2 production does occur. The Faradaic Efficiency (FE = the fraction of charge applied that results in ammonia) then becomes an important metric of the effectiveness of the electrocatalyst. Unfortunately, there are very few reports of FEs >50% and most are <20%. Even more challenging, the rates of the reaction per unit area, measured in mol(NH3) s−1 cm−2, are typically very small; so small that interference from other reducible N-compounds, including nitrates and NOx

gases, becomes a concern. In recent years the field has recognized the need to include quantitative 15N2 reduction experiments to verify the source of the nitrogen [51]. Tests with a small, fixed volume of nitrogen is another approach to prove the genuine nature of the NRR. The net result is that a number of the more substantial claims of success with aqueous NRR are being refuted [52] and the vast bulk of the reports are considered to be too low in yield rate to be practical [50], even if it can be shown that they do represent genuine NRR.

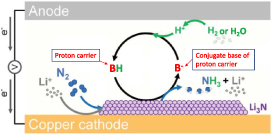

Electrochemical N2 reduction is not limited to aqueous media. A number of groups have investigated a lithium-mediated reaction (figure 10) that offers potential for a high-rate process [53–56]. The lithium cation acts effectively as a redox-catalyst in this process, being regenerated in each cycle.

Figure 10. Schematic of the Li-mediated nitrogen reduction process. From [55]. Reprinted with permission from AAAS.

Download figure:

Standard image High-resolution imageRecent advances [55, 57] have brought the FE of this approach to nearly 100% and rates to values (ca 0.5 μmol s−1 cm−2) close to the U.S. Department of Energy targets for NRR (90% FE and ca 1 μmol s−1 cm−2). Another important feature demonstrated in these recent reports is the ability of the process to cycle on and off as required. The downside of this approach is the overall energy efficiency, which is limited to around 25% by the lithium mediator. Improvements will no doubt emerge from investigations of alternate mediators.

High temperature electrochemical cells are also under development for ammonia production, based on hydrogen oxidation as the anode process. A range of reports have presented solid oxide electrolyte cells for ammonia electrosynthesis under such conditions [58]. Once again, the yield rates reported are low to the extent that the genuine nature of the process remains questionable.

An alternative possible approach is direct photocatalytic ammonia synthesis from N2 and H2O, but the ammonia yields demonstrated are significantly below electrochemical NRR. Nevertheless, research on photocatalytic ammonia synthesis is rapidly growing and it is critical for this field also to adopt rigorous protocols to eliminate false positives.

Finally, an indirect pathway to ammonia has been suggested that involves plasma-assisted N2 oxidation to oxidized forms of nitrogen (NOx ), followed by the selective electroreduction of the latter to NH3 [59]. While the second electrochemical step of this approach is clearly feasible and is well established [60, 61], energy-efficient N2 to NOx conversion is yet to be achieved.

Current and future challenges

Although non-aqueous solvents are capable of dissolving much higher amounts of N2 than water, the achievable concentrations are still challengingly low. To overcome this, recent reports have moved to moderately elevated N2 pressures around 15 bar. Notably, such pressures are required to liquify ammonia at ambient conditions and can be expected to be present in other parts of the system. Nonetheless, there remains an important to goal to reduce the operating pressure to ambient, in order to simply the technology of these cells.

The electrochemical reduction of oxidized forms of nitrogen (NOx RR) [62–64], mentioned above, derived from plasma-assisted N2 oxidation [59] holds promise. Moreover, nitrate and NOx gases are common pollutants in groundwater and the atmosphere, and electrochemical NOx reduction has been studied to treat waste streams for more than half of a century [60, 61]. Nonetheless, challenges remain if the resulting ammonia is to be used as an energy carrier. First, since the nitrate is present in an aqueous setting, hydrogen evolution is a competing reaction, and its suppression is largely accomplished through tuning the pH to alkaline conditions. However, design of catalyst and microenvironments to suppress hydrogen production is desirable, potentially through electrolyte engineering [65]. Even more promising is design of effective NOx RR catalysts that enable the process at potentials where H2 evolution is not possible [64]. Another challenge is that nitrate found in waste streams is often accompanied by contaminants, which can poison the catalyst; pretreatment processes will be required. Design of durable and stable catalysts is thus an important direction in the field of NOx RR [66], focusing on low-cost materials, as well as low catalyst loadings [67]. On the systems level, since nitrate is present at dilute concentrations both in nature and in the plasma N2 oxidation process, identifying the minimum concentration necessary for efficient reduction remains a critical discussion.

An alternative involves direct photocatalysis of the NRR or NOx RR; this could allow direct harnessing of solar resources that are plentiful in areas where ammonia is currently scarce (figure 11) [68, 69]. The challenge here is that both upstream and downstream separations are likely required to deliver concentrated ammonia from a low-yield process, potentially negating the low-cost advantages of photocatalysis over electrocatalysis. This scale-up challenge is particularly pertinent if ammonia is to be used as an energy carrier, since large volumes and high purity will be required. However, for agricultural applications solar-to-ammonia efficiencies below 1% may be practical if low-concentration ammonia can be directly utilized [69].

Figure 11. Comparison of global distribution of solar energy, farmlands, and Haber–Bosch plants. The average daily solar flux (top) compared to the location of Haber–Bosch plants (black dots) and distribution of farmland (bottom). Reprinted from [69], Copyright 2019, with permission from Elsevier.

Download figure:

Standard image High-resolution imageAdvances in science and technology to meet challenges

Requiring substantially higher energy inputs than the Green H2 + HB route, the major remaining issue in the alternative routes to ammonia, either through electrochemical N2 reduction or N2 oxidation + NOx electro/photoreduction, is energy efficiency; this is especially true of the latter. However, the rapidly falling price of renewable electricity, especially in dedicated installations, will have an impact on the significance of this energy input-cost. Technoeconomic analyses are being carried out by a number of groups to understand the energy versus capital cost factors in both cases. It is likely that the outcome in terms of overall cost competitiveness versus traditional ammonia production will express a strong regional component, reflecting the balance of renewables available and the relative value of the ammonia or fertilizers produced.

Establishing molecular-scale insights into the active sites and reaction mechanisms are instrumental to the discovery of practical processes for ammonia synthesis. Towards this end, the use of advanced in situ and operando spectroscopies along with predictive theoretical models can provide valuable insights. Similarly, advanced quantum mechanical modelling and molecular dynamics simulations enable a deeper understanding of molecular-level events. In other words, funding bodies must not underestimate the significance of pure fundamental research, which is the only pathway to innovation and new technologies that will support energy futures. Translation of fundamental concepts to the practical domain will require closer integration between process, reactor, and catalyst design, supported by detailed technoeconomic studies that can help identify quantitative performance targets and operational conditions under different use cases and economic scenarios. The resulting practical insights will help guide the development of testing conditions and performance metrics for process evaluation and can help move renewable ammonia synthesis out of the lab and into the field.

Concluding remarks

Sustainable N2 activation processes based on either electrochemical or photochemical energy input clearly hold the promise of producing ammonia and fertilizers at a distributed scale, finding application in the first instance in the agricultural sector. Efforts to commercialize these technologies are underway in a number of start-up companies [70]. Economies of scale and further significant developments in energy cost in the future will ultimately determine the conditions under which these technologies become attractive versus a Green H2 + Haber Bosch process. Direct cost comparisons are likely to only represent part of this calculus since security of supply has also become a major factor in many regions. Ultimately, we expect that a variety of (photo)electrochemical and other processes for electrifying ammonia synthesis will play a role, with the viability of various options being determined by the wide geographical variations in energy cost, feedstock supply, and ammonia demand. Nevertheless, future development and implementation of these new technologies and any planned mitigation steps must be supported by rigorous assessment of their potential to impact the, already significantly affected, natural N-cycle in the global eco-system [71].

Acknowledgments

The material based upon work by A J M was supported by the National Science Foundation under Grant No. 1943707. D R M and A N S acknowledge the financial support from ARC (FT200100317; DP200101878).

7. Ammonia storage, transportation and delivery: an integrated global perspective

René Bañares-Alcántara and Nicholas Salmon

Department of Engineering Science, Oxford University, Oxford OX1 3PJ, United Kingdom

Email: rene.banares@eng.ox.ac.uk and nicholas.salmon@worc.ox.ac.uk

Introduction

The promise of ammonia as an energy source primarily originates from the ease with which it can be stored and transported compared to hydrogen. The two most important physical properties which enable this behavior are its density (in the liquid state, it holds around 120 kg m−3 of hydrogen, whereas liquid hydrogen holds only 71 kg m−3)—and its boiling point (−33 °C at atmospheric pressure, as opposed to −252 °C for hydrogen) [72]. Therefore, compared to hydrogen, it is much easier to get ammonia into the liquid state, to hold it in the liquid state, and to transport it in that state.

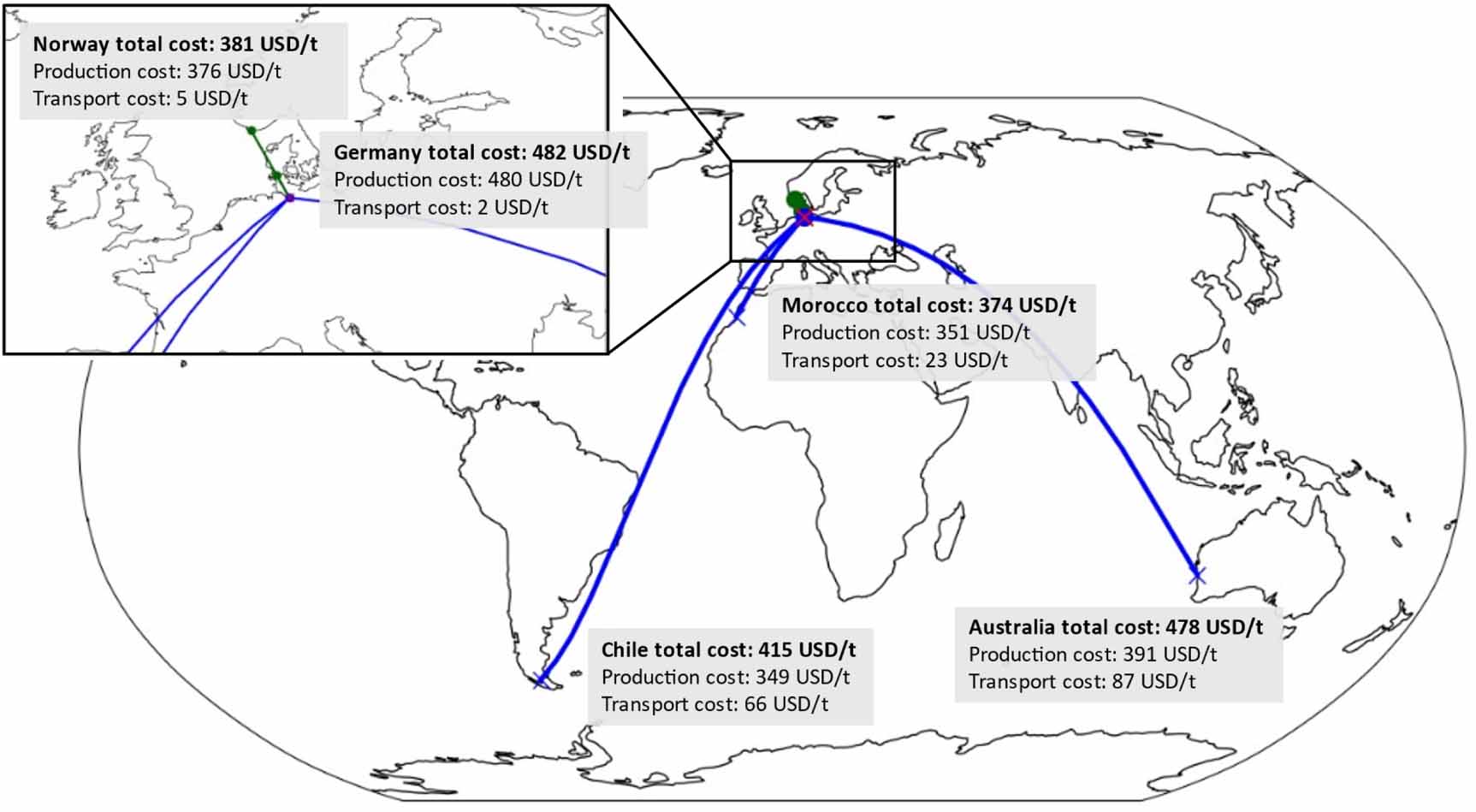

Despite these favorable properties, the transport costs of ammonia exceed those of conventional fossil fuels—on an energy density basis, it holds only 3.5 kWh l−1, which does not compare favorably to crude oil or its derivatives (between 9 and 11 kWh l−1) or even liquid natural gas (6.5 kWh l−1) [72]. Therefore, while ammonia may in many cases be preferable compared to hydrogen as a vector for renewable energy, the problem of ammonia supply chains is a significantly more expensive one than that encountered using conventional fuels only. Even though production costs tend to dominate in comparison to transport costs, the supply chain is still deterministic of the best ammonia production site to fulfil a certain demand, because over medium distances (∼5000 km), the transport cost may exceed the difference in production costs between two prospective supply locations (see figure 12).

Figure 12. Examples of production and transport costs from potential major suppliers to Hamburg (shown with a red cross), estimated using cost projections for 2030. Blue lines represent marine transport; green corresponds to pipelines. Transport is shown on great circle lines for clarity, but true marine distances are used in shipping cost estimates. Production costs are sourced from [73], with the method updated to use 2030 costs. Transport costs are estimated using the method from [74].

Download figure:

Standard image High-resolution imageFigure 12 demonstrates this principle, comparing five production sites and the associated cost of transport to Germany. Local production is not affordable, with costs even higher than when ammonia is imported a very large distance from Australia. However, it is equally inappropriate to simply select the cheapest production site in Chile, because the transport costs are excessive. Regional production in either Norway or Morocco with short distance transport has a total cost that is around 10% cheaper than imports from Chile.

For that reason, selection of the cheapest transport and storage properties in isolation is to oversimplify a complex problem. Determining the optimal solution for the location of ammonia production facilities, or the design of energy systems more broadly, must factor both local production costs as well as supply chain costs. This will change the nature of global energy trade. Historically, the abundance of fossil-based energy dense fuels created economic incentives for large scale production in low-cost hubs (e.g. the Middle East and the US Gulf Coast), since even very long-range transport of these fuels did not translate into high costs. Moving into the future, transport of chemical fuels will remain a critical requirement for energy system stability, and ammonia will be able to plug some of the gaps left by fossil fuels [75]; however, production will be more distributed, and transport will be more regional, rather than intercontinental, to avoid the very high transport costs which would otherwise accrue in hub-based production [74, 76].

This section has two purposes: firstly, to describe the engineering considerations required for ammonia transport, and secondly to discuss how these and other factors impact the economic case for ammonia export, as opposed to alternative forms of energy storage or production.

Engineering considerations for ammonia transport and storage

Ammonia storage will typically be required at three points in the supply chain: at the production site, at a transit port, and at the usage site. In general, this can be achieved in tanks similar to those widely deployed in the chemicals and energy sectors. A refrigeration unit should be included in order to prevent boil-off that will otherwise occur due to ambient heat transfer. This simple tank design is in stark contrast to the storage of liquid hydrogen, which has historically used gas spheres, which must be very well-insulated to prevent excessive boil-off. Due to the technical challenges of constructing these spheres, they are fairly small in volume; the largest liquid hydrogen sphere in the world holds less than 4% of the hydrogen that can be contained in a large ammonia tank [77, 78]. Ammonia tanks are already used at large scale in the fertilizer industry, and technological development is not required to facilitate the use of these tanks for energy storage.

The role of these tanks in the supply chain varies according to the end-use application of ammonia, and the means of transport under consideration. However, in general, the tank/s at the supply site should be used as buffer(s) to smooth out the variable operation of the green ammonia production facility, which will typically ramp down during periods of low renewable energy production, particularly if the local resource is highly seasonal. Because ammonia storage is reasonably cheap, it will generally be more economical to significantly oversize the tank at the supply site and absorb all variations in the operation of the comparatively expensive ammonia synthesis unit (rather than modulating down otherwise affordable production in periods when the tank is full). Downstream tanks at ports are then required to enable ships to be fully loaded and unloaded at the supply and demand ports respectively.

The only economic mechanism for large scale ammonia transport over land is by pipeline; while road and rail transport are both technically possible, their labor intensity results in very high costs. By contrast, ammonia can be transported in low-cost carbon steel pipelines because it is non-corrosive. These pipelines are already in wide use, particularly in the USA, where over 4500 km have been installed [79]. Having been delivered to ports, ammonia will then be transported via gas carrier; these carriers are already in wide use today, and many more existing ships can be converted to ammonia transport because it has a similar density and boiling point to LPG. Again, this compares favorably to shipping liquid hydrogen, for which commercial scale shipping does not exist. There is a wide range in ammonia ship sizes available, up to a maximum transport capacity of around 80 000 t of ammonia per ship. Very small-scale ships may use a semi-pressurized, semi-refrigerated vessel to keep ammonia in the liquid state, but in general fully refrigerated tanks at atmospheric pressure will be more affordable at export scale. In order for the delivered ammonia to be carbon neutral, the gas carrier itself will need to use some of the ammonia onboard as a fuel; this would cannibalize about 1% of the fuel onboard for a 10 000 km journey, which is roughly the distance from Shanghai to LA [74].