Abstract

This study contributes to the aid-development literature by examining the role of host country factors in conditioning the investment effect of foreign aid, covering a panel of six South Asian countries over the period 1990–2019. The study uses second-generation panel unit root, cointegration, and causality methods to control for endogeneity, cross-section dependency, and structural breaks. The study further applies the panel autoregressive distributed lag (ARDL) method of Pooled Mean Group (PMG) and the Common Correlated Effect Pooled Mean Group (CCEPMG) to estimate the long and short-run effects. The study results suggest that in the long run, foreign aid reduces or crowds out domestic investment directly but promotes domestic investment from the complementarity between aid and trade, human and financial development, and FDI. The causality result provides evidence of bi-directional causality between the two, supporting the crowding-out effect.

Similar content being viewed by others

Introduction

Developing countries consistently face resource constraints and depend heavily on foreign capital inflows such as FDI, FPI, remittances, and foreign aid to bridge the investment-savings gap. While the importance of FDI and remittance inflow has increased, the role of foreign aid has recently declined (OECD 2019). Nonetheless, foreign aid is still critical in achieving Sustainable Development Goals (SDGs) for low-income countries as there is a need for a considerable amount of resources (UN 2021). Like other low-income countries, South Asian countries are the major recipients of foreign aid, and aid is vital for bridging the savings-investment gap, promoting trade and human development, and economic growth.

The theoretical literature suggests that foreign aid can promote economic growth by augmenting domestic capital, promoting trade, transferring technology, improving infrastructure, transparency, and accountability, and removing foreign exchange constraints in the recipient country (Burnside and Dollar 2000; Adamu 2013; Juselius et al. 2014; Arndt et al. 2015; Orji et al. 2019). However, empirical studies provide little support for theoretical predictions, leading to skepticism about the effectiveness of aid in promoting economic development (Mekasha and Tarp 2019). At the extreme, some studies find that aid is more harmful to growth than beneficial as it encourages consumption and corruption, reduces investment, and erodes the balance of payment (Gong and Heng-Fu 2001; Liew et al. 2012). The ineffectiveness of aid has called for a change in how aid is provided, the conditions attached, and the institution involved in the aid implementation program (Mayo 2009; Asongu 2013; Moyer and Hedden 2020).

While most debates focused on aid-growth linkage, limited research has been devoted to the effectiveness of aid in promoting investment despite investment being the major channel through which aid promotes economic growth. The limited studies on aid-investment linkage also do not provide any conclusive evidence. While studies (Gong and Heng-Fu 2001; Economides et al. 2008; Uneze 2010; Herzer and Grimm 2012) find that aid crowds out or reduces domestic investment, only a few studies (Dollar and Easterly 1999; Orji et al. 2019) find the crowding-in or complementary effect. Others (Dollar and Easterly 1999; Djankov et al. 2008; Herzer and Grimm 2012; Nowak-Lehmann and Gross 2021) recognize the role of favorable conditioning factors such as trade openness, quality institutions, good governance, and infrastructure facilities in promoting investment. Despite all these studies, there is no consensus on the conditional factors. More importantly, the role of conditional factors is examined in the context of the growth effect, not the investment effect. Moreover, the conditional/channel factors identified for a particular region or country may not be effective for other regions or countries. Therefore, there is a need for further studies to examine the role of conditioning factors covering different regions/countries.

This study focuses on South Asia, as this region has received significant foreign aid. Aid flow toward South Asia increased from a meager $5 billion in 1990 to $15 billion in 2010 and further to $17 billion in 2020. Despite receiving significant aid, this region has been less focused on the empirical literature. Additionally, studies on South Asia mainly focused on the growth effect rather than the investment impact of aid, assuming aid complements investment automatically. Therefore, this study fills this research gap and aims to extend aid-conditional literature by examining the role of six conditioning factors/ channels in the interplay between aid and investment in South Asia.

This study contributes to the aid development literature in many ways. First, this study re-examines the impact of aid in promoting domestic investment covering South Asia, as this issue has been ignored in the empirical literature. Second, the study examines the role of six conditioning factors: financial development, trade, FDI, human development, government expenditure, and external debt in the interplay between aid and investment. Identifying favorable conditioning factors is vital for increasing aid effectiveness. Third, the study addresses the methodological drawbacks of previous studies by accounting for cross-section dependency and structural breaks neglected in past studies. Fourth, the direction of causality is ascertained to formulate effective policy intervention.

The paper is structured as follows: the “Literature survey” section deals with the theoretical and empirical literature. The “Trends, composition, and importance of foreign aid” section presents the trends and importance of foreign aid inflows for South Asia. The “Data, methodology, and model specifications” section concentrates on data, methodology, and model specifications. A discussion of the results is provided in the “Results analysis” section. The conclusion and policy implications are presented in the final section “Conclusion and policy implications”.

Literature survey

Theoretical considerations

Theoretically, it is argued that foreign aid complements domestic savings and promotes investment by bridging the saving-investment gap (Papanek 1973; UNCTAD 1999). It can relax foreign exchange constraints, help import critical capital goods vital for domestic industry, and boost domestic investment (Sachs 2005; Abuzeid 2009). Others (Chatterjee et al. 2003; Chatterjee and Turnovsky 2005) point out that aid increases public investment by complementing government expenditure in infrastructure and social development. More importantly, sectoral aid such as educational, health, research, and developmental aid may increase the productivity of private investment by generating positive externalities (Calderon and Serven 2004). In addition, developing countries, particularly low-income countries, face debt overhang, which may hamper investment. Foreign aid may promote investment by removing the debt overhang problem (Herzer and Grimm 2012). Further, Guillaumont and Chauvet (2001) and Collier and Dehn (2013) advocate that foreign aid helps low-income countries to overcome adverse shocks (trade, climate, exchange rate) and may promote investment. Herzer and Morrissey (2013) argue that foreign aid promotes domestic investment by reducing the tax burden and increasing the net return of investment. Some studies have concluded that the positive impact of foreign aid on growth and investment is not automatic and depends on many domestic factors such as good institutions, economic policies, including trade and fiscal policies, availability of infrastructure and human capital, and financial development (Burnside and Dollar 2000; Mbaku 2004; McGillivray et al. 2006, Wagner 2014).

Notwithstanding the theoretical prediction of a positive impact on domestic investment, some studies (Easterly 2003; Economides et al. 2008) argue that foreign aid may deter investment by promoting corruption, consumption, and rent-seeking activities. Others (Herzer and Morrisey 2013; Rajan and Subramanaiam 2011) argue that aid may reduce investment by reducing exports by appreciating exchange rate and increasing volatility. Therefore, the contributions within the theoretical literature show the ambiguity of the relationship between aid and investment and should be assessed by empirical evidence

Previous studies

There are numerous studies on the link between foreign aid and economic development, and results are mixed. Early studies (Bauer 1970) show that aid has no growth effect, and aid results in promoting corruption, bad governance, and higher poverty in the recipient country. In contrast, studies (Burnside and Dollar 2000; Hansen and Tarp 2001; Dalgaard et al. 2004; Kargbo and Sen 2014) find that aid promotes growth by increasing domestic savings and investment and removing foreign exchange constraints. Some other studies find that aid has no direct effect but many indirect effects that promote growth (Burnside and Dollar 2000; McGillivray et al. 2006).

Like aid-growth literature, the results of the aid-investment nexus are inconclusive. Early studies (Bauer 1970; Mosley et al. 1987) found a negative impact of foreign aid on investment. Mosley et al. (1987) examine the effects of foreign aid on private investment covering eight less-developed countries from 1960–1980 using time-series analysis. The study finds that 1% of foreign aid inflows crowds out private investment by 0.37%. Further, Snyder (1996) examined the same issue by covering 36 developing countries from 1977 to 1991 and found that aid reduces domestic investment as it is used for unproductive purposes. On the other hand, Mahdavi (1990) finds a weak relationship between aid and private investment since aid mainly promotes consumption and government spending rather than productive investment. However, early studies ignored the endogeneity and heterogeneity problem, and therefore, the robustness of the results is questionable.

Werker et al. (2009) examine the pattern of aid expenditure for 88 non-oil-producing Muslim countries from 1960–2003. Using the panel fixed effect and 2SLS method, the study finds that aid impact on investment and savings depends on how the aid is used. Further, the study finds that a 1% increase in foreign aid increases household consumption by 0.67% and imports by 1% of GDP. Additionally, aid substitutes domestic savings one-for-one with no significant impact on investment. Using 18 developing countries from 1970 to 1999 and the panel cointegration and causality method, Herzer and Grimm (2012) find that aid crowds out private investment by financing public investment. However, the conclusion of this study is not reliable since it is based on a bi-variate framework and ignores other relevant variables. Uneze (2010) examines the differential impact of multilateral and bilateral aid covering 14 West African countries. Using 4-year averages and the panel fixed effect method, the study finds that only multilateral aid positively affects private investment. Based on the results, the study advocates increasing coordination between aid-receiving countries and donors to boost aid effectiveness. However, this study suffers from the problem of endogeneity and cross-section effect.

Most studies on the relationship between aid and investment are cross-country in nature, and only a few country-specific studies are conducted. Sothan (2018) examines the impact of foreign aid on growth and investment in Cambodia from 1980 to 2014. Using the ARDL model, the study finds that aid has a positive short-run effect on capital formation but a negative impact in the long run. The results of this study suggest that long-run dependency on aid is harmful to the economy. In contrast, a study on Nigeria by Orji et al. (2019) show that aid positively contributes to domestic capital formation. The causality results reveal a bi-directional causality between the two, thus supporting the crowding-in hypothesis.

Like other regions, most studies in South Asia examined the growth impact without evaluating the link between aid and investment. However, a few studies also examined the effect of aid on poverty, FDI, human development, and trade competitiveness (Bhavan 2014; Das and Sethi 2019; Paul and Srinivasan 2019; Sharma and Kautish 2021; Sardar et al. 2022). Bhavan (2014) examined the role of foreign aid in attracting FDI. Using the panel fixed effect model, the study finds that social and infrastructure aid promotes FDI. Similarly, Sardar et al. (2022) find that aid for trade promotes human development by augmenting trade and investment in South Asia.

The above literature suggests that the investment impact of aid is heterogeneous and varies from country to country and region to region depending on the period of study, sample countries, and methodology applied. Further, most studies examined the direct impact and ignored the channel effect. A survey by Meksha and Tarp (2019) suggests that the direct impact of aid is limited, but the indirect impact is significant, subject to the availability of favorable country-specific factors. Therefore, this study fills this gap and extends the conditional literature by examining the role of conditioning factors in the interplay between aid and investment covering South Asia.

Trends, composition, and importance of foreign aid

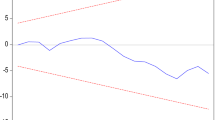

Table 1 shows the trends in Official Development Assistance (ODA) or foreign aid from 1980–2019. Foreign aid increased from $34 billion in 1980 to more than $100 billion in 2005 to $167 billion in 2019. Over the past 40 years, $3.3 trillion (in current prices) of foreign aid flowed to developing countries, but one-third of total aid flew to Africa. The distribution of aid by income level suggests that the middle-income (MICs) countries received relatively higher aid compared to the lower-middle (LMICs) and the lower-income countries (LICs)Footnote 1.

Regarding regional distribution, the central receiver of foreign aid has been Sub-Saharan Africa, followed by MENA and South Asia. The growth in foreign aid for Sub-Saharan Africa and MENA has been more than seven times and 3.3 times, respectively, for the same period (see Fig. 1). There has been approximately three-fold growth in the foreign aid received by South Asia countries.

Source: World Development Indicators, World Bank. The figure illustrates foreign aid received in various regions as percentage of total foreign aid in those years.

Country-wise aid inflows in South Asia suggest that aid flow has increased to Bangladesh, Nepal, and Pakistan and declined in Sri Lanka and IndiaFootnote 2. Bangladesh is the highest receiver of foreign aid, followed by India and Pakistan. The Maldives received the lowest aid in South Asia (see Table 1).

Composition of foreign aid

Having analyzed the trends in aid inflows, this section presents the composition of aid flows to South Asia as aid composition significantly impacts the development outcomes. Table 2 shows the aid composition to South Asia between 2005 to 2019. South Asian countries received the majority of aid in the form of economic and social infrastructure, which is considered more productive. The composition of aid indicates that Bangladesh and India received the most aid in terms of economic infrastructure. In contrast, Nepal, Pakistan, and Sri Lanka have received the largest aid in social infrastructure. The Maldives has received the most evenly distributed aid among all the categories.

Importance of foreign aid

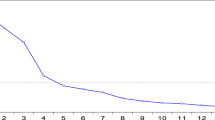

The importance of foreign aid is measured by expressing foreign aid as a ratio of gross fixed capital (GFC) and is presented in Fig. 2. The overall trend shows a declining trend for all the countries over time, suggesting that foreign aid as a source of foreign capital has decreased significantly recently. For example, in the early 1990s, aid as a ratio of GFC was 60% for Nepal; now, it has declined to 15% post-2010.

Source: World Bank Development Indicators and OECD, International Development Statistics online. The figure illustrates foreign aid received in India, Pakistan, Bangladesh, Sri Lanka, Nepal and Maldives as percentage of their gross fixed capital formation.

Similarly, aid as a ratio of GFC was more than 30% for the Maldives; now, it has declined to below 10% in the post-2010s period. The trend also shows that foreign aid is more important for small countries like Nepal, Bangladesh, and the Maldives than India and Pakistan and remains critical for them.

Data, methodology, and model specifications

Data

The data set used for the empirical analysis is collected from the World Development Indicator (WDI) of the World Bank and IMF outlook for six South Asian countries from 1990–2019. Table 3 lists variables, definitions, sources, and expected signs.

Methodology

A dynamic panel model is appropriate since our panel consists of 6 countries for 32 years. Therefore, the study follows a multi-step procedure to unravel the dynamic link between foreign aid and domestic investment. First, stationary properties of the variables are examined using a second-generation panel unit root with and without structural breaks. Second, the cointegration test was applied to establish a long-run relationship among the variables accounting for structural breaks. Given that we have a mix of I(0) and (1) variables, in the third step, the study applies the Pool Mean Group estimators in the ARDL framework to derive the long and short-run impact of foreign aid on investment. For robustness check, the study applies the Common Correlated Effect Pooled Mean Group (CCEPMG) estimators accounting for cross-sectional effects and structural breaks. In the final step, the study uses a dynamic heterogenous panel causality test to establish the causal link between aid and investment.

Panel stationarity test

This study applies the CADF panel unit root test as it is robust to cross-section dependency (Pesaran 2007). The augmented ADF regression model is mentioned below:

Where \(\bar Yt\) is the cross-sectional mean, p is the optimal lag order, and D is the difference operator. The presence of the unit root is tested by using the null, β = 0 by setting alternative βi < 0 for some i. The individual t-ratio is then averaged to calculate the CIPS:

Panel unit root test with structural breaks

In addition to the CIPS unit root test, the study uses the Karavias and Tzavalis (2014) unit root or (KT) test to account for possible structural breaks. This test accounts for the cross-sectional and heteroskedasticity effect and allows a break with intercept or intercept with linear trends. Consider the null hypothesis of a random walk against the alternative hypothesis of a stationary series with breaks in intercepts and linear trend at time b:

where δ is the autoregressive parameter, σ1i, and σ2i are the fixed effect model before and after the break, βi is the drift, and under H0, β1,i, and β2,i are the trend coefficients under H1. I(.) implies the indicator function. Assuming the breaks are unknown, Karavias and Tzavalis (2014) propose the following statistics for the unit root test:

Panel cointegration test

The error correction version of the panel cointegration (Westerlund 2007) method is used to establish the long-run relationship among variables. This test accounts for cross-section dependency and heterogeneity in short and long-run relationships. The model is written as:

Where δ is the error correction term and should be significantly negative. The cointegration test assumes the error correction term equals zero (δi = 0 for all). However, the alternative hypothesis depends on the assumption of the error term. For instance, the group means test (Ga and Gt) assumes cointegration for some countries, and the panel test (Pa and Pt) assumes the panel is cointegrated.

Panel cointegration with structural breaks

To account for structure breaks, the study applies the Westerlund and Edgerton (2008) test, which is robust to cross-sectional effect and structural breaks in both slope and intercept. Two-panel statistics, namely, Zϕ (N) and Zτ (N), were developed based on LM-based test statistics with the null of no-cointegration.

Panel auto-regressive distributed (ARDL) model

In the third step, the study applies the panel ARDL model to estimate short-run and long-run coefficients, which is appropriate for this study as we have a long panel with a mix of I (0) and I (1) variables. The ARDL framework of Eq. (14) can be written as:

where D is the difference operator, m is the lag order, β1–β7 are long-run coefficients, δ1–δ6 are short-run coefficients, and eit is the error term. The error correction framework of Eq. (6) is formulated as:

where θ is the coefficient of error correction term and should be significantly negative to confirm cointegration, the magnitude of the coefficient measures the speed of adjustment to the long-run equilibrium. To estimate the panel ARDL model (Eq. (6)), the pooled mean group (PMG) technique proposed by Pesaran et al. (1999) is used. This method allows short-run coefficients, intercept, and error terms to vary across countries but assumes the long-run coefficients to be homogenous. The Hausman test is applied to validate the slope homogeneity.

Panel causality test

Like the unit root and cointegration test, the first-generation causality test does not count the cross-section effect. However, second-generation causality tests like Dumitrescu and Hurlin (2012) and Juodis et al. (2021) consider this problem. This study uses Juodis et al. (2021), given its superiority over Dumitrescu and Hurlin’s (2012) method, as it corrects the “Nickel Bias” of the pooled estimator by using the Half Panel Jackknife (HPJ) approach. The causality test is carried out using the following model:

where the parameter \(\alpha _{0,i}\) represents the individual fixed effect, \(\gamma _{k,i}\) are the heterogeneous autoregressive parameters, \(\rho _{ik}\) are heterogeneous feedback coefficients. Assuming homogenous lags for both \(Y_{i,t},\) \(X_{i,t}\), granger causality from Xi,t to Yi,t is tested using the null hypothesis: H0: ρki = 0 for all i and k.

And the alternative: Ha: ρki ≠ 0 for some i and k.

The pooled estimator \(\{ {\rho _{ki}}\}_{i = 1}^N\) are subject to Nickel Bias corrections and form the basis of a Wald test for Granger causality. As N. T → ∞ with N/T → u2 ϵ [0, ∞], the standard Wald statistics computed as:

where \({\hat{{{J}}}} = \left( {{{{{NT}}}}} \right)^{ - 1}\mathop {\sum}\nolimits_{{{{i}}}}^1 {{{{{X}}}}_{{{{i}}}}^{^\prime} {{{{M}}}}_{{{{{z}}}}_{{{{i}}}}}X_i}\), Zi,t = (1, уi,t − 1, …, уi,t − p)′ and \(M_{z_i} = I_T - Z_i\left( {Z_i^{^\prime} Z_i} \right)^{ - 1}Z_i^{^\prime}\)

Model specifications

Three main investment theories are used in the literature to explain investment behavior: Keynesian, accelerator, and neoclassical or flexible theory. The Keynesian theory predicts that a fall in interest rate increases the opportunity cost of capital and increases investment. Therefore, the Keynesian theory emphasizes the role of interest rate in investment decisions and ignores the other significant factors. The accelerator theory, on the other hand, assumes that the level of investment depends on the level of output (Knox 1952). The rate of investment growth depends on the growth rate of GDP. The flexible accelerator theory was developed by Lucas (1967) and further by Fry (1993). This theory assumes that the desired capital stock depends on the user cost of capital and output level. So, the desired capital stock (K*) depends on the level of output (Q) and the cost of capital (r) as given below:

where λ is the adjustment coefficient between desired and past investment rates, σ is the elasticity of substitution between capital and labor. Therefore, the investment rate can be written as follows:

Substituting Eq. (10) into Eq. (11), we can re-write investment equation as:

Assuming constant elasticity of substitution and adding an error term, our investment equation is expressed as:

The study uses the flexible accelerator model (Eq. (13)) but augmented it by adding other relevant variables by considering the specific conditions of developing countries. The following model is used to examine the aid impact on investment:

where DINV is the domestic investment rate, G is the year-lagged growth rate, AID is aid inflows, DC is Bank credit to the domestic sector, REXC is the real exchange rate, LR is real bank lending rate, TD is the total trade, INT is the interaction term presenting channel effect, δt is the time specific constant and uit residual term.

Besides growth rate, user capital, and aid, several other independent variables are included to avoid the omission bias problem. These are financial development, real exchange rate, and trade development. The real lending rate represents the cost of capital and is considered an important determinant of investment in the developing country. The expected sign of the user capital (lending rate) is negative since a rise in lending rate increases the cost of capital and reduces investment (Fry 1993). The model also includes a lagged GDP growth (G) rate to capture the expected demand effect, and the coefficient of the lagged GDP growth rate should be positive (Fry 1993). The exchange rate also affects investment since developing countries import a larger share of capital goods for investment activities. However, the impact of the real exchange rate (REXC) on investment is ambiguous, as an increase in the real exchange rate (depreciation) would reduce investment by increasing the price of imported goods (Fry 1993). In contrast, an appreciating real exchange rate (decrease in the real exchange rate) would stimulate investment by making imports cheaper (Serven and Solimano 1992).

Further, financial development (FD) is another factor that influences investment in developing countries by supplying credit (Levine 2005). Financial development is expected to stimulate domestic investment by pooling savings and mobilizing credit to investors (Levine 2005). We use bank credit (DC) as the proxy for financial development, which is more reliable and relevant for developing countries. Trade (exports + imports) is also expected to encourage higher investment as higher trade boosts economic growth by increasing demand for domestic goods. So, the investment may positively respond to the rise in trade through a size effect. Finally, as discussed in the theoretical section, foreign aid may stimulate investment by bridging the savings-investment gap, reducing the burden of debt overhang, promoting public investment in education, health, and infrastructure, reducing the tax burden on investors and stabilizing macroeconomic factors (Démurger 2001; Calderon and Serven 2004; McGillivray et al. 2006; Wagner 2014). While the coefficient β2 measures the direct long-run impact of aid (unconditional) on domestic investment, the indirect impact or net effect (conditional) is measured by using the following equation:

The sign of the net effect \(\left( {\beta _2 + \beta _7} \right)\) indicates whether the channel effect is complementary (if positive) or substitutive (if negative). Following the previous literature, we considered six conditional variables: financial development, trade, human development, external debt, FDI, and government expenditure. Accordingly, six interaction terms (AID*FD, AID*TD, AID*HUM, AID*EXD, AID*FDI, and AID*GEXP) are added to the model (Eq. (14)) to estimate the net effects of aid.

The justification for including these conditional variables is that a rise in financial development may increase aid effectiveness by facilitating better aid management (Nkusu and Sayek 2004). There may exist complementarity between aid for trade and investment as aid for trade promotes trade by improving trade infrastructure and trade facilitation, which encourages higher investment (Calì and Velde 2011). The theoretical prediction of AID and human capital interaction term is positive as foreign aid for education, health, and skill development promotes human capital development and boosts the productivity of private investment. Other studies (Wang and Balasubramanyam 2011; Bhavan 2014) suggest complementarity between aid and FDI as aid promotes institutions, human capital, and infrastructure crucial for attracting higher FDI. Therefore, aid may promote domestic investment via promoting higher FDI. The availability of infrastructure removes the Dutch disease effect and improves aid effectiveness (Adam and Bevan 2006). There is a conflicting view on the nexus between aid and foreign debt. Easterly (2003) argues that if foreign aid is mainly used to repay foreign debt, it may decrease the effectiveness of foreign aid in augmenting investment. On the other hand, Omotola and Hassan (2009) argue that if foreign aid is used to repay external debt, it would reduce debt services costs, provide debt relief, save limited foreign exchange, and engender increased savings and investment.

Results analysis

Panel stationarity test

The empirical analysis starts with a cross-section dependence test (Pesaran 2007), and the results are presented in Table 4. It is clear that, except for the lagged growth rate, all variables show the presence of cross-section dependency. Therefore, the CIPS unit root test is appropriate. Results presented in Table 4 indicate that most of the series I (1) except G and FDI. Although the CIPS test accounts for the cross-section effect, it does not accommodate structural breaks in series. Therefore, we use the Karavias and Tzavalis (2014) unit root test, and the results are presented in Table 4. Results indicate that in addition to G and FDI, other variables such as REXC and DC are also I(0) series. Therefore, the variables under investigation are a mix of I (1) and I (0) series.

Panel cointegration test

Having established the order of the integration of the variables, the study applies a cointegration test to establish the long-run stable relationship among variables. The null of no-cointegration is examined using four cointegration tests proposed by Westerlund (2007) using two specifications: constant and constant with the trend. The results are provided in Table 5. It is observed from the results that out of four-panel tests, three tests have rejected the null of no cointegration in favor of the long-run relationship among the variables. In addition to the Westerlund (2007) cointegration test, we also applied Westerlund and Edgerton (2008) test to account for structural breaks. Results are presented in Table 5. Both Zϕ(N) and Zτ(N) test statistics provide cointegration evidence even after allowing for structural breaks in level and the slope.

Contribution of foreign aid to domestic investment

After checking the long-run relationship, we proceed to estimate the contribution of foreign aid to investment using PMG estimators. As many as seven specifications were estimated and the results are presented in Table 6. Column 2 presents the direct impact of foreign aid, and Columns 3–7 present the net effects. The results from Table 6 indicate that the Error correction term is negative and significant, implying that the model converges into a long-run relationship. The coefficient of ECT is −0.13, suggesting a correction of 13% for the discrepancy of the estimation.

The estimated results suggest that the long-run coefficient of foreign aid is negative and significant, indicating that foreign aid depresses domestic investment in South Asian countries. More precisely, in the long run, a 1% rise in foreign aid as a ratio of GDP decreases domestic investment by 0.78% as a ratio of GDP. The results support the hypothesis that, in the long run, foreign aid crowds out or substitutes domestic investment in South Asia. As discussed in the literature, foreign aid may crowds-out domestic investment as it encourages current consumption, unproductive government expenditure, higher corruption, rent-seeking behavior, reduces accountability, and weakens governance (Easterly 2003; Economides et al. 2008; Munemo 2011; Herzer and Grimm 2012; Herzer and Morrissey 2013). The result is in line with previous findings for other regions (Easterly 2003; Herzer and Grimm 2012; Herzer and Morrissey 2013) but contrasts with the conclusions of Snyder (1996), Dollar and Easterly (1999), and Orji et al. (2019). Despite receiving significant aid in the form of economic and social infrastructure, the direct investment impact of aid is found to be negative. This implies ineffective aid utilization, and weak management system in South Asia. So, there is a need for strengthening aid management system by improving governance and reducing corruption to increase the aid effectiveness.

The net effects are calculated using Eq. (15) to assess the complementarity or substitutability between the aid and the conditioning factor, and the results are presented in Table 6 (columns 3–7). For example, the net effect of the interaction term of Aid and financial development ((AID*DC) is calculated as 0.27 ([−1.21] + [0.052 × 30.4]), where the mean value of the financial development is 30.4, the unconditional effect of AID is −1.21 and the conditional coefficient of the interaction term is 0.052. The positive net impact indicates that aid promotes investment from the complementarity between aid and financial development. Aid for financial development promotes financial development and boosts domestic investment, as financial development is crucial for channeling capital for investment activities and managing aid better (Nkusu and Sayek 2004). Therefore, a rise in financial development will increase the effectiveness of aid in promoting investment in South Asia. The net effect of other conditioning factors such as external debt, FDI, Trade, government expenditure, and human development are calculated as −0.26, 0.19, 1.1, −0.35, and 0.43, respectively. Therefore, the net effect of the interaction between aid and FDI, Trade, and human development is positive, suggesting that aid boosts domestic investment from the complementarity between aid and these conditioning factors in South Asia. The complementarity between aid and FDI is also noted in the literature (Sunesen et al. 2008). This is because aid promotes institutions, human development, and infrastructure, and this, in turn, attracts more FDI. Further, FDI is found to complement domestic investment and the co-moments of aid, and FDI, therefore, positively contributes to capital formation (Sunesen et al. 2008). Aid for trade promotes trade in various ways, and a rise in trade increases domestic investment through the demand effect (OECD 2011). Foreign aid also complements domestic investment through human development as aid effectiveness increases with the availability of quality human capital. Moreover, aid for human development like education, health, and infrastructure boosts investment and economic growth by promoting human development (Sardar et al. 2022).

On the other hand, the net effect on domestic investment is negative from the complementarity between aid and external debt. This implies that if aid is used to finance external debt, its effectiveness in augmenting investment declines (Easterly 2003). Reducing external debt is beneficial as higher external debt increases debt service, consumes limited foreign exchanges, and hinders imports of critical capital goods (Omotola and Hassan 2009). Similarly, the net effect on domestic investment is negative from the complementarity between aid and government expenditure, indicating that a rise in aid increases unproductive government expenditure that crowds out domestic investment (Herzer and Grimm 2012).

Overall, the empirical results suggest that foreign aid, in general, crowds out domestic investment in South Asia. At the same time, foreign aid complements domestic investment through conditioning factors like trade, finance, FDI, and human development. The short-run coefficients indicate that foreign aid and financial development complements investment while lagged growth and real interest rate reduces investment. The short-run impact of trade is insignificant.

The results further indicate that the coefficient of other explanatory variables is significant and, as expected, except for the coefficient of real lending rate. Contrary to expectation, the coefficient of lending rate is positive and significant, indicating that a rise in lending promotes higher investment in South Asia. This may be because the financial sector is heavily controlled in South Asia, and interest rate is administered in most cases. In this condition, the rise in the real lending rate would increase the supply of credit to finance, thereby promoting investment (McKinnon 1973; Shaw 1973; Fry 1993). Further, a higher real interest rate positively impacts investment by promoting higher savings and outweighing the negative impact of investment (Shrestha and Chowdhury 2007). The effect of the lagged growth rate is positive and significant, supporting the flexible accelerator hypothesis. Trade has also been found to promote investment as expected. One percent rise in trade as a ratio of GDP stimulates investments by 0.06% as a ratio of GDP. Further, financial development has a positive impact on domestic investment, indicating that the development of the financial sector is critical for the availability of credit required for financing investment activities (Bontempi et al. 2010). The coefficient of the real exchange rate is negative, implying that depreciation of the real exchange rate reduces domestic investment in South Asia by making imports costlier (Serven and Solimano 1992).

Robustness check using CCEPMG

The CD test presented in Table 4 suggests the presence of a cross-section effect in series. The PMG estimators become biased and inconsistent when cross-section effects are present. As Chudik and Pesaran (2015) indicated, the CCEPMG estimators should be applied as they accommodate the cross-section effect by adding cross-sectional averages and lags. Further, this method is very useful when there is a structural break in the series (Baltagi 2015). Like the PMG model, the CCEPMG assumes symmetric long-run coefficients but allows short-term heterogeneity. The Hausman test is used to test the slope homogeneity. The results are presented in Table 7.

The Hausman test suggests that CCEPMG estimators are consistent and should be preferred. The CD test indicates that the model is free of cross-section effects. The ECT term is negative and significant, indicating that deviation from the long run is corrected. The estimated results suggest that the coefficient of foreign aid is negative and significant, meaning that foreign aid depresses domestic investment in South Asian countries, as found in PMG. Now, we examine the net effect of various conditioning factors. The net effect of conditioning factors such as financial development, external debt, FDI, Trade, government expenditure, and human development are calculated as 0.46, −0.19, 0.46, 0.63, −0.18, and 0.09, respectively. The following conclusions are derived from Table 7. The net effect on domestic investment is positive from the complementarity between aid and (1) financial development, (2) FDI, (3) Trade, and (4) human capital. The net effect on domestic investment is negative from the complementarity between aid and (1) external debt and (2) government expenditure. The results are in line with PMG estimators The control variables are found to be significant and have expected signs except real interest rate. The short-run results indicate that foreign aid and financial development complements investment while lagged growth and real interest rate negatively affect investment. The short-run impact of trade and the real exchange rate is insignificant.

Overall, the study finds that foreign aid reduces domestic investment directly but complements domestic investment through conditioning factors like trade, FDI, finance, and human capital but substitutes through conditioning factors like external debt and government expenditure.

Panel causality between foreign aid and domestic investment

After estimating the long-run impact of foreign aid on domestic investment, in the final step, the study applies the panel causality test (Juodis et al. 2021, Granger non-causality) to examine the direction of causality between the two. The results are presented in Table 8. The causality result suggests evidence of a bi-directional or mutual feedback relationship between the two. Given that aid has a direct negative impact on investment, the causality results indicate that foreign aid reduces domestic investment and vice versa. The results, therefore, support the crowding-out hypothesis.

Conclusion and policy implications

This study aims to extend the aid-conditional literature by examining different conditioning factors in promoting domestic investment in South Asia, covering panel data from 1990 to 2019. This study is relevant as this aspect has been ignored in the South Asia region. For this purpose, the study uses second-generation unit root, cointegration, and causality to consider the problem of endogeneity, cross-section effect, and structural breaks. Cointegration results suggest the presence of a long-run stable relationship among variables. The long-run coefficients derived from ARDL estimation of PMG and CCEPMG method suggest that aid reduces domestic investment directly. However, the net effect from the complementarity between aid and conditioning factors indicates that foreign aid complements domestic investment through trade, FDI, and financial and human development. On the other hand, foreign aid substitutes domestic investment through conditioning factors like external debt and government expenditure. In addition, the causality results suggest that foreign aid crowds out domestic investment in South Asia.

The findings of this study have few policy implications. First, there is a need for a review of aid policy linking with national developmental requirements. There is a need for structural change in implementing mechanisms/institutions in South Asia to increase aid effectiveness. Second, from the channel effect, it is clear that the complementarity between trade, human capital, FDI, and financial development should be enhanced to increase the investment impact of aid. Third, since foreign aid is mainly channeled through the government, the government should use it effectively for investment activities such as infrastructure and human capital development, trade development, and institution buildup to increase the effectiveness of foreign aid and reduce the direct negative impact. Fourth, since aid promotes investment through FDI, aid and FDI policies should be interlinked. Reducing external debt has a beneficial impact on capital formation as it has a substantive negative effect.

South Asian countries face multiple challenges to increase the conditioning factors that are beneficial for aid effectiveness. To promote human capital development, there is a need to step up public investment in education, health, skill development, and infrastructure development. Creating a conducive environment for private sector investment in education, health, and infrastructure is also vital. Developing the financial sector is also another challenge. The financial sector in South Asia is mainly dominated by the banking sector, and developing an active capital market is essential to increase the effectiveness of foreign capital, including aid and FDI, in economic development. This will reduce/neutralize the crowding-out effect of public investment. Further, opening the external sector is vital as trade promotes resource efficiency and investment.

Data availability

The data generated during and/or analyzed during the current study have been provided in the data set.

Notes

Since 2018, LICs have received higher aid than LMICs.

The graduation of Sri Lanka to middle-income country and domestic violence since 2007 has resulted in reduction in foreign aid patriculaly from traditional donors. The decline in foreign aid to India due its graduation to middle-income country and a policy shift since 2004 for not accepting certain types of aid like disaster and humanitarian aid. Aid flows to Bangladesh have increased in recent times due to aid finance to mega projects undertaken in sectors like power and communications.

References

Abuzeid F (2009) Foreign aid and the big push theory: lessons from Sub-Saharan Africa. Stanf J Int Relat 11(1):16–23

Adamu PA (2013) The impact of foreign aid on economic growth in ECOWAS countries: a simultaneous-equation model. WIDER Working Paper No. 2013:143

Adam C, Bevan D (2006) Aid and the supply side: public investment, export performance and Dutch disease in low-income countries. World Bank Econ Rev 20:261–290

Arndt C, Jones S, Tarp F (2015) Assessing foreign aid’s long-run contribution to growth and development. World Dev 69(C):6–18

Asongu S (2013) On the effectiveness of foreign aid in institutional quality. Eur Econ Lett 2(1):12–19

Baltagi B (2015) Estimation of heterogeneous panels with structural breaks. Center for Policy Research, NY p 213

Bauer P (1970) Dissent on foreign aid. In: Meier G (ed) Leading issues in economic development. Oxford University Press, Oxford

Bhavan T (2014) Effectiveness of foreign aid in facilitating foreign direct investment: evidence from four South Asian countries. Asian Econ Financ Rev 4(12):1770–1783

Bontempi ME, Golinelli R, Parigi G (2010) Why demand uncertainty curbs investment: evidence from a panel of Italian manufacturing firms. J Macroecon 32(1):218–238

Burnside C, Dollar D (2000) Aid, policies and growth. Am Econ Rev 90:847–868

Calderon CA, Serven L (2004) The effects of infrastructure development on growth and income distribution. Ann Econ Financ 15(2). https://doi.org/10.1596/1813-9450-3400

Calì M, Velde W (2011) Does aid for trade really improve trade performance? World Dev 39(C):725–740

Chatterjee S, Sakoulis G, Turnovsky S (2003) Unilateral capital transfers, public investment, and economic growth. Eur Econ Rev 47:1077–1103

Chatterjee S, Turnovsky S (2005) Financing public investments through foreign aid: consequences for economic growth and welfare. Rev Int Econ 13:20–44

Chudik A, Pesaran M (2015) Common correlated effects estimation of heterogeneous dynamic panel data models with weakly exogenous regressors. J Econ 188(2):393–420

Collier P, Dehn J (2013) Aid shocks and growth. World Bank Policy Research Working Paper, Washinton, DC

Dalgaard CJ, Hansen H, Tarp F (2004) On the empirics of foreign aid and growth. Econ J 114(496):F191–F216

Das A, Sethi N (2019) Effect of foreign direct investment, remittances, and foreign aid on economic growth: evidence from two emerging South Asian economies. J Public Aff 20(7):e2043

Démurger S (2001) Infrastructure development and economic growth: an explanation for regional disparities in China? J Comp Econ 29(1):95–117

Dumitrescu EI, Hurlin C (2012) Testing for Granger non-causality in heterogeneous panels. Econ Model 29:1450–1460

Dollar D, Easterly W (1999) The search for the key: aid, investment and policies in Africa. Policy Research Working Paper Series, 2070, World Bank. https://doi.org/10.1596/1813-9450-2070

Djankov S, Montalvo JG, Reynal-Querol M (2008) The curse of aid. J Econ Growth 13(3):169–194

Easterly W (2003) Can foreign aid buy growth? J Econ Perspect 17(3):23–48

Economides G, Kalyvitis S, Philippopoulos A (2008) Does foreign aid distort incentives and hurt growth? Theory and evidence from 75 aid-recipient countries. Public Choice 134(3/4):463–488

Fry MJ (1993) Foreign direct investment in a macroeconomic framework: finance, efficiency, incentives, and distortions. Policy Research Working Paper Series 1141, The World Bank

Gong L, Heng-Fu Z (2001) Foreign aid reduces labor supply and capital accumulation. Rev Dev Econ 5(1):105–118

Guillaumont P, Chauvet L (2001) Aid and performance: a reassessment. J Dev Stud 37(6):66–92

Hansen H, Tarp F (2001) Aid and growth regressions. J Dev Econ 64(2):547–570

Herzer D, Grimm M (2012) Does foreign aid increase private investment? Evidence from panel cointegration. Appl Econ 44(20):2537–2550

Herzer D, Morrissey O (2013) Foreign aid and domestic output in the long run. Rev World Econ 149(4):723–748

Juodis A, Karavias Y, Sarafidis V (2021) A homogeneous approach to testing for Granger non-causality in heterogeneous panels. Empir Econ 60(4):93–112

Juselius K, Moller NF, Tarp F (2014) The long-run impact of foreign aid in 36 African countries: insights from multivariate time series analysis. Oxf Bull Econ Stat 52(2):169–210

Kargbo PM, Sen K (2014) Aid categories that foster pro-poor growth: the case of Sierra Leone. Afr Dev Rev 26(2):416–429

Karavias Y, Tzavalis E (2014) Testing for unit roots in short panels allowing for a structural break. Comput Stat Data Anal 76(C):391–407

Knox A (1952) The acceleration principle and the theory of investment: a survey. Economica 19(75):269–297

Levine R (2005) Finance and growth: theory and evidence. In: Aghion A, Durlauf S (eds) Handbook of economic growth, vol 1. Elsevier Science, The Netherlands, pp 865–934

Liew CY, Mohamed MR, Mzee SS (2012) The impact of foreign aid on the economic growth of East African countries. J Econ Sustain Dev 3(12):129–188

Lucas RE (1967) Optimal investment policy and the flexible accelerator. Int Econ Rev 8(1):78–85

Mayo D (2009) Dead aid: why aid is not working and how there is a better way for Africa. Farrar, Straus and Giroux, NY

Mahdavi S (1990) The effects of foreign resource inflows on the composition of aggregate expenditure in developing countries: a seemingly unrelated model. Kyklos 43:111–137

Mbaku JM (2004) NEPAD and prospects for development in Africa. Int Stud 41(4):387–409

McKinnon R (1973) Money and capital in economic development. Brookings Institute, Washington, DC

McGillivray M, Feeny S, Hermes N, Lensink R (2006) Controversies over the impact of development aid: it works; it doesn’t; it can, but that depends …. J Int Dev 18(7):1031–1050

Meksha T, Tarp F (2019) A meta analysis of aid effectiveness: revisiting the evidence. Politics Gov 7(2):5–28

Mosley P, Hudson J, Horrell S (1987) Aid, the public sector and the market in less developed countries. Econ J 97(387):616–641

Moyer J, Hedden S (2020) Are we on the right path to achieve the Sustainable development goals? World Dev 127:104749

Munemo J (2011) Foreign aid and export diversification in developing countries. J Int Trade Econ Dev 20(3):339–355

Nowak-Lehmann F, Gross E (2021) Aid effectiveness: when aid spurs investment. App Econ Anal 29:189–207

Nkusu M, Sayek, S (2004) Local financial development and the aid-growth relationship. IMF Working Paper No. 238

Omotola S, Hassan S (2009) Foreign aid, debt relief and Africa’s development: problems and prospects. S Afr J Int Aff 16(1):87–102

Orji A, Ogbuabor JE, Anthony-Orji O et al. (2019) Analysis of capital formation and foreign aid nexus in Nigeria. Int J Emerg Mark 14(2):266–280

OECD (2011) Trade for growth and poverty reduction: how to aid for trade can help. OECD, Paris. https://doi.org/10.1787/9789264098978-en

OECD (2019) The Global Outlook on financing for sustainable development 2019. OECD, Paris

Papanek G (1973) Aid, foreign private investment, savings, and growth in less developed countries. J Pol Econ 81(1):120–130

Paul A, Srinivasan P (2019) Impact of foreign aid on economic growth and poverty alleviation in India. Empir Econ Lett 18(9):957–968

Pesaran M, Shin Y, Smith R (1999) Pooled mean group estimation of dynamic heterogeneous panels. J Am Stat Assoc 94(446):621–634

Pesaran HM (2007) A simple panel unit root test in pressure of cross-section dependence. J Appl Econ 22:265–312

Rajan R, Subramanaiam A (2011) Aid, Dutch disease and manufacturing growth. J Dev Econ 94(1):106–118

Sachs J (2005) The end of poverty: economic possibilities for our time. Penguin, New York

Sardar S, Khan D, Khan A, Magda R (2022) The influence of aid for trade on human development in South Asia. Sustainability 14:12169

Serven L, Solimano A (1992) Private investment and macroeconomic adjustment: a survey. World Bank Res Obs 7(1):95–114

Shaw E (1973) Financial deepening in economic development. Oxford University, New York

Sharma R, Kautish P (2021) Aid-growth association and role of economic policies: new evidence from South and Southeast Asian countries. Glob Bus Rev 22(3):735–752

Shrestha M, Chowdhury K (2007) Testing financial liberalisation hypothesis with ARDL modelling approach. App Fin Eco 17:1529–1540

Sothan S (2018) Foreign aid and economic growth: evidence from Cambodia. J Int Trade Econ Dev 27(2):168–183

Sunesen P, Rytter E, Selaya P, et al. (2008) Does foreign aid increases foreign direct investment. Discussion Paper, University of Copenhagen

Snyder DW (1996) Foreign aid and private investment in developing economies. J Int Dev 8(6):735–745

Uneze E (2010) Testing the impact of foreign aid on domestic private investment in West Africa. Afr Rev Money Financ Bank 59–84

UNCTAD (1999) Trade and development report, 1999. United Nations, Geneva

UN (2021) Financing for sustainable development report. United Nations, NY

Wang C, Balasubramanyam V (2011) Aid and foreign direct investment in Vietnam. J Econ Integr 26(4):721–739

Wagner J (2014) Optimising foreign aid to developing countries: a study of aid, economic freedom, and growth. Honors Project, Grand Valley State University

Werker E, Ahmed F, Cohen C (2009) How foreign aid is spent: evidence from a natural experiment. Am Econ J Macroecon 1(2):225–244

Westerlund J (2007) Testing for error correction in panel data. Oxf Bull Econ Stat 69(6):709–748

Westerlund J, Edgerton D (2008) A simple test for cointegration in dependent panels with structural breaks. Oxf Bull Econ Stat 70:665–704

Author information

Authors and Affiliations

Contributions

RD and DG contributed to the conceptualization and analysis of data for the paper. TK contributed to the collection and interpretation of the data for the paper. RD critically reviewed it for important intellectual content. DG and TK contributed to the writing of the first draft of the paper All authors who contributed to the manuscript read and approved the submitted version.

Corresponding author

Ethics declarations

Competing interests

The authors declare no competing interests.

Ethical approval

Ethical approval was not required as the study did not involve human participants.

Informed consent

Informed consent was not required as the study did not involve human participants.

Additional information

Publisher’s note Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Supplementary information

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article’s Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Dash, R.K., Gupta, D.J. & Khandelwal, T. Revisited the role of foreign aid in capital formation: experience of South Asian countries. Humanit Soc Sci Commun 11, 323 (2024). https://doi.org/10.1057/s41599-024-02709-y

Received:

Accepted:

Published:

DOI: https://doi.org/10.1057/s41599-024-02709-y