Abstract

This study has developed a new method to valuate intellectual property for pledge financing. First, based on interval theory and the relevant calculation rules, the income interval model is and then used to calculate the interval values of intellectual property. Second, based on the change structure of risk indicators, the AHP and set-valued statistics are utilized to calculate the risk adjustment coefficient. Third, the point value of intellectual property is calculated with its values at an interval scale and risk adjustment coefficient. The values of intellectual property at an interval scale provide the two parties negotiating pledge financing with a reference range of loan amounts. The risk adjustment coefficient becomes a crucial indicator for measuring value evaluation risk. The point value of intellectual property specifies how much the bank loan amount can deviate from the values of intellectual property at an interval scale. The method creates a multi-indicator system to valuate intellectual property for pledge financing, which lowers the risk of intellectual property pledge financing to a significant extent and facilitates its operation. Moreover, the method has been proven to be efficient in practice.

Similar content being viewed by others

Introduction

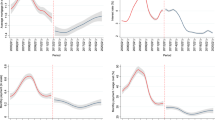

The accumulation and spillover of intellectual capital underpins sustainable economic development. The intellectual property, capital and labor of an economy work together to produce increasing returns to scale, improve marginal productivity, and promote economic development (Romer, 1986). Enterprises can also create technical barriers by building intellectual property to make a fortune (Wang et al., 2014). Currently, small- and medium-sized tech companies across the globe, major creators of intellectual property, have become the major driving force for innovation and have played an irreplaceable role in stimulating the economic development of the world. However, most small- and medium-sized tech startups are capital guzzlers that require considerable investment, thus facing high risk. As a result, they are having trouble raising funds from conventional financing channels, and intellectual property pledge financing is designed to address this issue (Bo et al., 2021). An increasing number of small- and medium-sized tech companies are attempting to raise funds with their intellectual property assets. Therefore, intellectual property pledge financing has become a significant way for these companies to acquire financial support. However, to conduct intellectual property pledge financing, we need effective methods to valuate intellectual property (Vuong et al., 2021). Furthermore, such methods must be developed on the basis of well-established theories. As an intangible asset, intellectual property is valuable in different ways than tangible assets. Specifically, intellectual property is innovative, proprietary and incommensurable. Therefore, the labor theory of value and cost-of-production theory cannot explain the formation of intellectual property value (Boisot, 1998). The market method and the cost method are also inapplicable to intellectual property valuation (AlGhamdi and Durugbo, 2021). An intellectual property asset, as a production factor, must be provided as a commodity or service together with its physical carrier to generate utility for consumers. The value of an intellectual property asset varies with the utility it provides consumers. Therefore, marginal utility theory can explain the formation of intellectual property value. Products derived from intellectual property create a competitive advantage, the future income of which is the source of value of intellectual property. Utility and scarcity are the theoretical basis for valuating intellectual property (Boisot 1998; Hidalgo, 2015). The income method for asset valuation is founded on the theory. Despite its prevailing application in intellectual property valuation, this method is limited (AlGhamdi and Durugbo, 2021) in that intellectual property valuation is subject to the influence of different appraisers, changes in objective situations and the power balance between the two parties engaged in pledge financing. This allows the indicators of the income method to fluctuate in certain intervals. In response, we have developed the income interval analysis, which extends the traditional income method by taking intervals into consideration. Then, to make valuation less risky and provide the two parties engaged in pledge financing with a base point of transaction, the AHP and set-valued statistics are combined to calculate the risk adjustment coefficient. Finally, the point value of intellectual property is calculated with the values at an interval scale estimated by the income interval analysis and the risk adjustment coefficient. The intellectual property valuation method has also been tested in practice. China has made great efforts to promote intellectual property pledge financing, which has led to an upsurge of studies on intellectual property valuation methods and their widespread application. Intellectual property pledge financing is thus thriving in China. The total amount of pledge financing rose from 93.17 billion yuan in 2015 to 218 billion yuan in 2020, representing an average annual growth rate of 17.2% (see Fig. 1). This has overcome the financing challenges confronting small- and medium-sized tech companies. With sufficient financial support, a large number of Chinese tech companies have flourished, pushing China’s innovation to higher levels. The number of approved invention patents also saw a surge from 93,000 in 2008 to 530,000 in 2020. Therefore, effective intellectual property valuation has played a vital role in promoting the development of intellectual property pledge financing. The intellectual property valuation method developed in this paper, subject to little influence of social and economic systems and culture, among other factors, is universally applicable and can be generalized to a wide range of scenarios.

Pledged financing amount Data released by the State Intellectual Property Office of China, the growth rate is calculated by the author.

Literature review

Intellectual property pledge financing evaluation is a professional service in which an institution evaluates the value of an intellectual property asset and prepares an evaluation report to provide a reference for the pledger to make financing decisions. The market method, cost method and income method are the most commonly used methods for the evaluation of intellectual property pledge financing (Lagrost et al., 2010; Svishchova, 2022). The market method determines the value of an intellectual property asset by comparing the actual amount paid for a similar asset in a similar market. This method should be used in scenarios where an active market and all data of the comparable asset are available (AlGhamdi and Durugbo, 2021). The intellectual property trading market in developing countries is neither active nor well established. Moreover, every intellectual property asset is original, novel and unique in itself. The owner of an intellectual property asset has a monopoly over it, and any other, even if having made the same technology achievements through independent research and development, will not be deemed the owner of the intellectual property asset. Therefore, it is extremely difficult to obtain transaction data to conduct valuation via the market method. Moreover, the actual amount paid for an intellectual property asset is often kept confidential. The limitations of the market method and the features of intellectual property have conspired to restrict the application of this method in intellectual property valuation. This approach is primarily effective in evaluating the value of right-of-use intangible assets and that of assets with similar features (Lagrost et al., 2010; Svishchova, 2022). The cost method is used to valuate intellectual property assets by aggregating the expenditures incurred after considering different kinds of obsolescence factors. The cost of development of an intellectual property asset is readily available. However, valuating an intellectual property asset at its cost reveals the socially necessary labor time for creating the asset but neglects the value it can possibly generate in the future. Investment in intellectual property creation is usually high risk but brings huge rewards. In other words, intellectual property generates far more or far less income than cost. The cost method is most suitable for determining the minimum trading value (Parr, 2018; Svishchova, 2022). The income method calculates the future income that can possibly be generated to determine the present value of the asset in question. This method is the most popular tool to valuate intellectual property in that it makes scientific calculations (Loyarte et al., 2018; Lagrost et al., 2010). However, this approach is also limited: it is difficult to predict the future income most intellectual property assets can possibly generate. The discounted rate can be affected by many risk factors. Calculations vary considerably with changes in indicators; consequently, improvement is required to make this method more effective in practice.

It is difficult to valuate intellectual property scientifically. In response, many scholars have attempted to improve the income method, including measuring the expected rate of return against the expected excess return and calculating the expected income and discounted rate with the income share percentage (Ma et al., 2019; Yuan et al., 2012). As more scholars have become committed to studying the evaluation of intellectual property, approaches other than the market method, the cost method and the income method have been developed. These approaches combine qualitative and quantitative tools to valuate intellectual property. Delphi is a frequently used qualitative method, but to quantify expert evaluations, we must resort to the AHP. By structuring and systemizing the valuation of intellectual property, the AHP enables both qualitative evaluation and quantitative calculation of intellectual property value (Subramanian and Ramanathan, 2012). The AHP is a simple, flexible and practical tool to manage multi-criteria decision-making by evaluating both qualitative and quantitative factors (Satty, 2008). The AHP can be used in many scenarios together with other methods, such as TOPSIS, Delphi and fuzzy comprehensive evaluation. Intellectual property is unique, and its valuation is subject to the influence of its distinctive features and various other factors, thus entailing high risks (Zyoud and Fuchs-Hanusch, 2017; Huang et al., 2022; Lyu et al., 2020). Based on theoretical research and a review of existing methods, we propose to combine income interval analysis with the risk adjustment coefficient to valuate intellectual property. In this way, an indicator system composed of the interval scale, risk adjustment coefficient and point value of intellectual property is formed, and this multi-indicator system can lower the risk of evaluation. Intellectual property pledge evaluation differs from transaction evaluation in that meeting the risk control requirements of financial institutions facilitates transactions. The intellectual property pledge financing evaluation method developed in this paper speaks to the distinctive feature of pledge financing by exerting effective risk control.

This paper enriches relevant theories by clarifying the status of utility theory and interval theory as the theoretical foundation for intellectual property pledge financing valuation. The labor theory of value, the cost-of-production theory of value and the marginal utility theory of value are major economic theories explaining value formation (Boisot, 1998). Intellectual property is original, proprietary and incommensurable; therefore, it cannot be measured against the socially necessary labor time. Consequently, the labor theory of value cannot explain the formation of intellectual property value. The cost-of-production theory of value is more effective in deciphering the value formation of tangible assets that can be produced repeatedly. In contrast, intellectual property, a crystallization of human wisdom, occurs only once. Moreover, it is difficult to determine the cost of intellectual property. Therefore, the cost-of-production theory of value is not suitable for valuating intellectual property. The value of intellectual capital resides in the future income that the competitive advantage of its commercialization can possibly generate. The value of intellectual property is judged by its utility and scarcity, and it is reasonable to valuate intellectual property pledge financing based on the utility theory of value and interval theory. This paper is innovative in the following three aspects. First, we optimized the income method. Specifically, we conducted income interval analysis based on the utility theory of value, interval theory and calculation rules of intervals. This approach is designed in accordance with the distinctive features of intellectual property pledge financing to fulfill relevant risk control requirements and proved effective in practice. Second, we combined the AHP with set-valued statistics. The AHP, a multi-criteria decision-making tool involving both qualitative and quantitative analysis, works perfectly with flexible set-valued statistics. We have developed a typical way to calculate the risk adjustment coefficient and have managed to determine the point value of intellectual property. Third, we have established a valuation system composed of interval values, risk adjustment coefficient and point value to valuate intellectual property pledge financing, which overcomes the limitations of valuating intellectual property against a single indicator. It has been found in practice that valuating intellectual property based on a multi-indicator system serves the parties engaged in intellectual property pledge financing better.

Theoretical and methodological basis

Interval theory and income interval analysis

The income method estimates the expected future income and remaining useful life of intellectual property and then discounts the probable future income to the value in the present day using a discounted rate.

where V is the value of intellectual property, Rt is the expected income of intellectual property in year t, r is the expected discounted rate of intellectual property, t is the expected remaining useful life of intellectual property.

At present, the income method produces only accurate point estimates of various indicators or the closest estimates to the true values of these indicators but fails to specify the margin of error. However, valuation is a kind of consultation, and the valuation of intellectual property varies with the professional competence of different appraisers. In addition, the value of intellectual property will change with economic and legal variations. Therefore, it is reasonable to assume that interval estimates allowing for a certain margin of error rather than accurate point estimates should be adopted for the indicators of the income method. First, the expected income Rt is not the historical data of income but the part of income earned using intellectual property in the expected income increments. Intellectual property is only valuable when it is offered with a physical carrier, but it is difficult to draw a clear line between the two. As a result, adopting the interval estimates of income contributed by intellectual property allows for changes in influence factors, thus being more agreeable with the features of valuation. Then, the expected discounted rate r is a type of return on investment, which comprises the risk-free rate of return often represented by the bank interest rate or treasury note rate and the rate of return to investment that carries risk as well as inflation. The discounted rate varies with macroeconomic changes and industry progress. Therefore, assigning the discounted rate to a specific range is consistent with reality. Finally, the expected useful life t refers to the remaining useful years of intellectual property calculated from the time when the valuation is done, and it is dependent on the economic life of intellectual property. This indicates that t of intellectual property should not be smaller than the term of the loan, and its value should be able to cover the loan amount to protect the creditor’s rights. However, we can only estimate the maximum useful years of intellectual property. Therefore, it is reasonable to assign the expected useful life of intellectual property to a specific range. The analysis above leads us to the following formula for calculating the income interval:

where [V−, V+] stands for the value interval of intellectual property. \([R_t^ - ,R_t^ + ]\) represents the expected income interval of intellectual property in year t. [r−, r+] refers to the interval of the expected discounted rate of intellectual property in year t. [t−, t+] is the interval of the expected useful life of intellectual property.

Calculation rules of interval values

The utility theory of value and interval theory lay a solid theoretical foundation for income interval analysis. The calculation rules of interval values serve as the basis for income interval analysis to make calculations (Moore et al., 2009). These calculation rules are rarely used in asset valuation. This paper innovates by employing these calculation rules to valuate intellectual property pledge financing. Detailed calculation rules are presented as follows.

The interval of binary numbers is in the form of \(\left[ {\bar{A}} \right] = \left[ {a^ - ,a^ + } \right]\), \(\left[ {\bar{B}} \right] = \left[ {b^ - ,b^ + } \right]\). The calculation rules of the binary numbers are detailed as follows:

Addition:\(\left[ {\bar{A}} \right] + \left[ {\bar{B}} \right] = \left[ {a^ - + b^ - ,a^ + + b^ + } \right],a \ge 0,b \ge 0.\)

Subtraction: \(\left[ {\bar{A}} \right] - \left[ {\bar{B}} \right] = \left[ {a^ - - b^ - ,a^ + - b^ + } \right],a \ge 0,b \ge 0.\)

Multiplication:\(\left[ {\bar{A}} \right] \times \left[ {\bar{B}} \right] = \left[ {a^ - ,a^ + } \right] \times \left[ {b^ - ,b^ + } \right],a \ge 0,b \ge 0.\)

Division:\(\frac{{\left[ {\bar{A}} \right]}}{{\left[ {\bar{B}} \right]}} = \frac{{\left[ {a^ - ,a^ + } \right]}}{{\left[ {b^ - ,b^ + } \right]}} = \left[ {\frac{{a^ - }}{{b^ + }},\frac{{a^ + }}{{b^ - }}} \right],a \ge 0,b > 0.\)

Exponentiation:\(\left[ {\bar{A}} \right]^n = \left[ {a^ - ,a^ + } \right]^n = \left[ {\left( {a^ - } \right)^n,\left( {a^ + } \right)^n} \right],a \ge 0,b \ge 0.\)

Average calculating operation: supposing\(\left[ {\bar{A}_1} \right] = \left[ {a_1^ - ,a_1^ + } \right],\left[ {\bar{A}_2} \right] = \left[ {a_2^ - ,a_2^ + } \right],{\rm{L}} ,\left[ {\bar{A}_n} \right] = \left[ {a_n^ - ,a_n^ + } \right],a \ge 0,b \ge 0.\) the formula \(Ave\left[ {\bar{A}_1} \right] = \left[ {\frac{{a_1^ - + a_2^ - + {\rm{L}} + a_n^ - }}{n},\frac{{a_1^ + + a_2^ + + {\rm{L}} + a_n^ + }}{n}} \right].\) returns the average.

Set-valued statistics

Set-valued statistics incorporate point estimates into the interval of estimates (Sun et al., 2001; Wang, 1985). During valuation, experts are invited to estimate the interval of intellectual property values. Suppose the kth expert assigns the value of intellectual property \(\left[ {\mathop {\mu }\nolimits_{i1}^{\left( 1 \right)} ,\mathop {\mu }\nolimits_{i2}^{\left( 2 \right)} } \right]\mathop {{,\mu }}\nolimits_{i1}^{\left( 1 \right)} ,\mathop {\mu }\nolimits_{i2}^{\left( 2 \right)} \ge 0\) in interval i. n experts assign the value of intellectual property in n intervals, thereby forming a set-valued statistical series \(\left[ {\mathop {\mu }\nolimits_{i1}^{\left( 1 \right)} ,\mathop {\mu }\nolimits_{i2}^{\left( 1 \right)} } \right],\left[ {\mathop {\mu }\nolimits_{i1}^{\left( 1 \right)} ,\mathop {\mu }\nolimits_{i2}^{\left( 1 \right)} } \right],\left[ {\mathop {\mu }\nolimits_{i1}^{\left( 2 \right)} ,\mathop {\mu }\nolimits_{i2}^{\left( 2 \right)} } \right],\left[ {\mathop {\mu }\nolimits_{i1}^{\left( 3 \right)} ,\mathop {\mu }\nolimits_{i2}^{\left( 3 \right)} } \right], {\rm{L}} ,\left[ {\mathop {\mu }\nolimits_{i1}^{\left( k \right)} ,\mathop {\mu }\nolimits_{i2}^{\left( k \right)} } \right], {\rm{L}} ,\left[ {\mathop {\mu }\nolimits_{i1}^{\left( n \right)} ,\mathop {\mu }\nolimits_{i2}^{\left( n \right)} } \right]\). These subsets are distributed in a certain pattern on the value axis, which can be described by expression (3):

where \(\mathop {\chi }\nolimits_{\left[ {\mathop {\mu }\nolimits_{i1}^{\left( k \right)} ,\mathop {\mu }\nolimits_{i2}^{\left( k \right)} } \right]} = \left\{ {\begin{array}{*{20}{c}} {1,\mathop {\mu }\nolimits_{i1}^{\left( k \right)} \le \mu _i\mathop {{ \le \mu }}\nolimits_{i2}^{\left( k \right)} } \\ {0,else\begin{array}{*{20}{c}} {\begin{array}{*{20}{c}} {} & {} \end{array}} & {} & {} \end{array}} \end{array}} \right.\)

\(\overline {\rm X} (\mathop {\mu }\nolimits_i )\) is the drop shadow function. The estimated weight of indicator i \(\bar{\mu }_i\) is calculated in expression (4).

max and min are the maximum and minimum values of μi, which can be obtained based on expressions (5) and (6):

Expressions (5) and (6) lead to expression (7).

The confidence interval bi of \(\bar{\mu }_i\) of indicator i can be utilized to determine whether expert evaluations are consistent and \(\bar{\mu }_i\) is accurate. bi can be calculated with expression (8).

gi can be calculated using expression (9).

Expression (8) indicates that a larger gi will result in a smaller bi, suggesting consistency in expert evaluations. bi is usually preset to 0.9 for intellectual property valuation. If bi does not reach the preset value, experts have to continuously adjust the interval values they give until bi equals 0.9.

The AHP

The AHP is a systematic analysis method that combines qualitative analysis and quantitative analysis and is widely employed in asset valuation (Zyoud and Fuchs-Hanusch, 2017; Huang et al., 2022; Lyu et al., 2020). Intellectual property valuation is both subjective and professional, and the involvement of enough experts is necessary. To obtain more robust evaluations, it is important to analyze the indicator-specific factors influencing intellectual property value and paint a full picture of intellectual property value for experts to help them make accurate quantitative evaluations. The AHP is a powerful tool to tackle unquantifiable multi-criteria problems that attempt to achieve multiple objectives (Saaty, 2008; Subramanian and Ramanathan, 2012). In this paper, we combined the AHP with set-valued statistics to double adjust the weights of risk indicators calculated by the AHP and then calculate the risk adjustment coefficient. The seamless combination of the AHP managing multi-objective decision-making based on both qualitative analysis and quantitative analysis with flexible set-valued statistics has fulfilled the requirements of various parties involved in intellectual property pledge financing on risk control.

Application of the new valuation method

Procedures

The new method evaluates intellectual property pledge financing in three steps: first, establish an indicator system and calculate the preliminary interval values of intellectual property based on income interval analysis. Second, based on the change structure of risk indicators affecting intellectual property value, use the AHP and set-valued statistics to calculate the risk adjustment coefficient of intellectual property value. Third, calculate the point value of intellectual property value based on the preliminary interval values and risk adjustment coefficient (see Fig. 2).

It intuitively describes the process and steps of the value assessment of intellectual property pledge financing, and indicates that several aspects of the work constitute a step as a whole in the scope of the virtual box.

Case study

XTX Technology Co., Ltd. (hereinafter referred to as XTX Technology) in Nanjing specializes in the research and development of copying machines, printers and other consumables. According to Baiten, a patent service provider in China, as of 2020, 43 patents have been granted to XTX Technology. Moreover, several toners independently developed by XTX Technology have been identified as high-tech products in Jiangsu Province. However, as production scales up, more money is put into research and development. To obtain funds, on November 11, 2021, XTX Technology pledged a patented technology (No: ZLNJ027) with the Bank of China to apply for a loan. Zhongtian Assets Appraisal is responsible for valuating the patent as an independent third party, and the valuation is done via the income method. The income method involves the following indicators. Expected income Rt: Rt is measured against the technical contribution of the patent to the sales of related products. Sales of related products increased from 8.7 million yuan in 2016 to 11.1036 million yuan in 2021, representing an annual growth rate of ~5%. Approximately 7% of the sales are attributable to the patent. In other words, the sales generated by the patent also rose from 609,000 yuan in 2016 to 777,200 yuan in 2021. Sales are expected to grow at approximately 5% from 2022 to 2028, and the technical contribution of the patent remains at 7%. Therefore, the sales attributable to the patent will gradually increase from 816,100 yuan in 2022 to 1.0937 million yuan in 2028. Expected discounted rate r: discounted rate = risk-free treasury note rate + industry risk rate + inflation rate. The 5-year treasury note rate is 5.32%, and the sum of the industry risk rate and inflation rate is ~4%. Therefore, the discounted rate of the patent is approximately 9.32%. Expected useful life t: under patent law, the term of invention patents is 15 years. Considering the changing market environment and technological advances, the economic life of the patent is expected to be ~7 years.

The indicator system of intellectual property valuation

First, after studying recent cases, policies, papers and monographs in relation to intellectual property valuation and consulting with professionals, we have chosen several indicators that influence intellectual property value on the basis of the Intellectual Property Evaluation Manual published by China Technology Exchange (CTEX). Second, more indicators will not necessarily lead to more accurate evaluations. On the one hand, experts will be distracted by too many indicators; on the other hand, with so many indicators, it is more likely that some may be incompressible to experts, making it difficult for the experts to arrive at sound evaluations. Based on the theoretical basis and features of the method for intellectual property valuation, experts are invited to rate the intellectual property on a 1–9 Saaty scale. The weight of each indicator is then calculated using yaahp, which is taken as the score of the indicator, and finally, the indicators are ranked by score and those with higher scores are selected. Third, since intellectual property valuation is inevitably subject to the influence of subjective factors, the indicators that are chosen may overlap in logic terms. In response, experts are invited to remove indicators with unclear definitions and logically overlapping ones. Eleven high-ranking indicators survived the two tests. The 11 indicators, with normalized scores, form the indicator system for the intellectual property valuation case study in this paper (see Table 1).

Preliminary interval of intellectual property values

First, appraisers from Zhongtian Assets Appraisal prepared a detailed report on the pledged patent of XTX Technology. The report expounded on the discounted rate, expected income and expected useful life of the patent, among other indicators, and presented preliminary calculation results. Second, Zhongtian Assets Appraisal invited five experts to valuate the patent of XTX Technology, who then calculated the indicators in Table 1 based on the detailed information and preliminary calculation results of these indicators in the report. Third, consider the calculation results of [r−, r+] of expert 1. Given the weights of various indicators in Table 1, expert 1 first determined the lower limit of the interval of indicators P1-P11 based on the information and preliminary calculation results in the report, then multiplied the weight by the lower limit of each indicator, and finally summed the products of these indicators. The sum is the lower limit r− in [r−, r+], which is 8.12. The upper limit r+ is calculated via the same method, and the result is 10.33. [r−, r+] equals [8.12, 10.33]. The calculation results of [r−, r+] for all 11 indicators are listed in Table 2. Other experts calculated [r−, r+] in the same way. Corresponding results are reported in Table 3. Fourth, [t−, t+] and [R−, R+] are calculated with the same method as [r−, r+]. The calculation results are presented in Tables 3 and 4. With the calculation results of various indicators available, [V−, V+] is calculated based on expression (2). The results are reported in Table 4.

Calculate [t−, t+] = [6.1, 7.1] and [R−, R+] in reference to the calculation formula of [r−, r+]: \(\left[ {r^ - ,r^ + } \right] = \left[ {\frac{{8.12 + 8.21 + 8.22 + 8.29 + 8.27}}{5},\frac{{10.33 + 10.42 + 10.43 + 10.45 + 10.51}}{5}} \right] = \left[ {8.22,10.43} \right]\). Experts are invited to predict the income that intellectual property can possibly generate in the future [6, 7] years. Predictions are detailed in Table 4.

Consider the [V−, V+] calculated by expert 1 with the income interval analysis.

With t = 6,

With t = 7,

The final calculation results of [V−, V+] of expert 1 are:

\(\left[ {V^ - ,V^ + } \right]_1 = \frac{{\left[ {V^ - ,V^ + } \right]_6 + \left[ {V^ - ,V^ + } \right]_7}}{2} = \frac{{\left[ {391.4123,422.6362} \right] + \left[ {445.8396,485.9123} \right]}}{2} = \frac{{\left[ {837.2518,908.5485} \right]}}{2} = \left[ {418.6259,454.2742} \right]\)\(\left[ {V^ - ,V^ + } \right]\) of the other four experts can be calculated in the same way, and the calculation results are reported in Table 4. The preliminary value interval of intellectual property can be determined by averaging the calculation results of the five experts.

\(\begin{array}{l}\left[ {V^ - ,V^ + } \right]_0 = \frac{{\left[ {V^ - ,V^ + } \right]_1 + \left[ {V^ - ,V^ + } \right]_2 + \left[ {V^ - ,V^ + } \right]_3 + \left[ {V^ - ,V^ + } \right]_4 + \left[ {V^ - ,V^ + } \right]_5}}{5}\\ = \frac{{\left[ {418.6259,454.2742} \right] + \left[ {419.1508,454.7012} \right] + \left[ {419.8964,455.5277} \right] + \left[ {419.2773,454.3643} \right] + \left[ {419.213,454.5574} \right]}}{5}\\ = \left[ {419.2327,454.6850} \right]\end{array}\)

Weights of indicators calculated by the AHP

Risk change structure model of intellectual property value components

The preliminary value interval of intellectual property may still be biased. This can mainly be ascribed to changes in the value components of intellectual property and the cognitive limitations of experts. To lower the risk, a change structure of risk indicators is identified, where weights of the intellectual value components are calculated by the AHP to measure the influence of changes in these components on the intellectual value. On this basis, set-valued statistics are used to calculate the risk adjustment coefficient, as shown in Fig. 3.

The content and composition level of intellectual property value assessment risk are described intuitively, and the scope of the virtual box specifically explains the content of the value change risk of the upper level.

Weighting and consistency testing

Based on Fig. 3, experts measured the influence of indicators at level C on those at level A with a 1–9 Saaty scale and then compared and quantified this influence. On this basis, the judgment matrix A–C is developed.

The indicator value of C1 is calculated with the square foot method: \(\mathop {N}\nolimits_1 = \root {3} \of {{1 \times 2 \times 3}} = 1.82\). The indicator values of C2 and C3 are calculated in the same way: \(\mathop {N}\nolimits_2 = \root {3} \of {{2 \times 1 \times \frac{1}{2}}} = 1\) and \(\mathop {N}\nolimits_3 = \root {3} \of {{\frac{1}{3} \times \frac{1}{2} \times 1}} = 0.55.\)The weights are normalized: \(W = (C1,C2,C3) = (0.5390,0.2972,0.1638).\)The eigenvectors of matrices A-C are calculated: \(E = (C1,C2,C3) = (1.62482,0.8943,0.492063).\)The largest Eigen value \(\mathop {\lambda }\nolimits_{\max } = 3.0092\) conforms to the matrix in question. CI is calculated: \(CI = 0.0046.\) As demonstrated in Table 5, \(RI = 0.58\). Then, we have \(CR = \frac{{CI}}{{RI}} = \frac{{0.0046}}{{0.58}} = 0.0079\) and \(CR \le 0.1.\)This indicates that the indicator weights are consistent. The weights of the three judgment matrices are calculated with the same method, as reported in Tables 6, 7, and 8. The combined weights are calculated with the criterion layer weights and the plan layer weights (see Table 9).

A consistency check is performed on the total order of the hierarchy. \(C\bar{R} = \frac{{\mathop {\sum}\limits_i {CI_iw_i} }}{{\mathop {\sum}\limits_i {RI_iw_i} }} = \frac{{0.0046 \times 1 + 0.0103 \times 0.5390 + 0.0048 \times 0.2972 + 0.0092 \times 0.1638}}{{0.58 \times 1 + 0.90 \times 0.5390 + 0.90 \times 0.2972 + 0.58 \times 0.1638}} = \frac{{0.01308522}}{{1.427584}} = 0.0092\)\(C\bar{R} < 0.1\), demonstrating that the hierarchy total order passed the consistency test and verifying the credibility of the weights of risk indicators affecting intellectual property value.

A multi-indicator valuation system for intellectual property pledge financing

Intellectual property pledge financing is designed to obtain bank loans rather than sell an intellectual property asset. Therefore, on the enterprises’ part, the key to valuating intellectual property is to obtain enough bank loans to meet their capital needs, and they are willing to exchange their intellectual property for a bank loan of less value. Moreover, under the current financial system in China, banks, with money in hand, have a large say in whether to grant a loan. To make intellectual property pledge financing happen, it is important to help banks maximize interests and fulfill their risk control requirements. Simply simulating market transactions where appraisers act as impartial evaluators of intellectual property value, although seemingly objective and fair, actually runs counter to the realities and real intentions of intellectual property pledge financing. Such valuation is one-sided. Therefore, it is necessary to incorporate the risk control requirements of banks into intellectual property valuation. To do so, experts are invited to assign a value within [0, 1] to each risk indicator. The value manifests experts’ confidence in the accuracy of the weight being assigned to each indicator. For instance, if an expert assigns 0.8 to P11, the chance that the weight of P11 (0.0517) is accurate stands at 80%. Then, the risk-free weight of P11 can be calculated accordingly: 0.0517 × 0.8 = 0.04136. Experts are asked to place their confidence in the accuracy of the weight within a range of estimates. Set-valued statistics are employed to calculate the upper and lower limits of the range. Taking P11, \(\bar{\mu }_i\), gi and bi are calculated with set-valued statistics based on the following expressions. Specifically, \(\bar{\mu }_i\) is calculated based on expression (7).

gi is calculated based on expression (9).

According to expression (8), we have \(\mathop {b}\nolimits_i = \frac{1}{{1 + 0.0008}} = 0.999\). \(\mathop {b}\nolimits_i \ge 0.9\) suggests that experts’ evaluations are consistent and \(\bar{\mu }_i = 0.945\) is accurate. The \(\bar{\mu }_i\), gi, and bi values of all other plan layer indicators are calculated in the same way (see Table 10).

The risk adjustment coefficient of intellectual property valuation AC can be calculated with the weight \(W\) and \(\bar{\mu }_i\) values in Table 10: \(AC = \frac{{0.0517 \times 0.945 + 0.1494 \times 0.862 + {\rm{L}} + 0.0898 \times 0.894 + 0.0345 \times 0.875}}{{0.0517 + 0.1494 + {\rm{L}} + 0.894 + 0.875}} = 0.8864\). The preliminary value interval [V−, V+] is \(\left[ {V^ - ,V^ + } \right]_0 = \left[ {419.2327,454.6850} \right]\), in which 4.192327 million yuan is the lower limit of \(\left[ {V^ - ,V^ + } \right]_0\) or the smallest expected income the intellectual property can possibly generate in the future. As the expected income grows from 4.192327 million yuan to 4.54685 million yuan, risk increases accordingly, and 4.54685 million yuan is associated with the highest risk. The risk adjustment coefficient AC measures the probability of the expected income rising from 4.192327 million yuan to 4.54685 million yuan, or rising by 354,523 (454.6850–419.2327) yuan. In this case, AC = 0.8864 means that the probability the expected income rises by 354,523 (454.6850–419.2327) yuan is 0.8864. Furthermore, the point value of intellectual property can be calculated based on the preliminary interval values and risk adjustment coefficient: \(V_F = \left[ {V^ - ,V^ + } \right]_0 \times AC = 419.2327 + (454.6850 - 419.2327) \times 0.8864 = 450.6576\), which is 4.506576 million yuan. The point value, interval values and risk adjustment coefficient calculated by the method developed in this paper form an indicator system for intellectual property valuation, which paints a fuller picture for parties involved in pledge financing. In addition, with more comprehensive analysis, it can greatly lower the risk of pledge financing and facilitate its operation.

Conclusions

In the case of XTX Technology, its patent pledged is valued in [4.192327, 4.54685] million yuan, which serves as a reference for both parties to pledge financing to make decisions. Pledge financing performed by small- and medium-sized tech companies is different from conventional transactions in that these companies attempt to obtain sufficient funds from banks by pledging their intellectual property assets rather than securing a good deal. Therefore, as long as these tech companies can obtain sufficient funds, they are satisfied with any loan amount within the interval [4.192327, 4.54685] million yuan. Banks usually try to maximize the profits of a loan on the one hand and minimize the risk on the other, especially the cumulative risk of multiple loans. The two parties will negotiate the pledge financing around [4.192327, 4.54685] million yuan. However, in reality, banks have the upper hand in the credit market, and they usually determine the loan amount by adding to the lower limit of 4.192327 million yuan. The risk adjustment coefficient serves as an important basis for banks to decide on the amount they will add to the lower limit. A larger risk adjustment coefficient suggests more accurate intellectual property valuation. Consequently, banks are willing to add more to the lower limit of 4.192327 million yuan and grant a loan worth as much as 4.506576 million yuan, which is the point value of intellectual property. The interval values, risk adjustment coefficient and point value of intellectual property enable banks to consider granting a loan from many respects, thereby reducing the risk to a considerable extent and facilitating the operation of pledge financing. Intellectual property is difficult to quantify, resulting in ambiguous and arbitrary valuation. The valuation method of intellectual property in this paper is founded on sound theories and offers a simple but practical tool to make accurate evaluations. Finally, as demonstrated by the case study, Zhongtian Asset Appraisal has made a satisfactory valuation of intellectual property using this method. The method is universally applicable and can be used in the intellectual property pledge financing of small- and medium-sized tech companies around the world.

Limitations and inspirations for future research

Only a limited number of experts are involved in the study. Zhongtian Asset Appraisal only invites experts who are conversant with intellectual property valuation theories, certified by the China Appraisal Society and involved in at least two asset valuation missions, limiting the number of qualified experts. To overcome this limitation, expert opinions can be collected in the form of scales, and then reliability analysis, validity analysis and factor analysis can be conducted with SPSS to establish a valuation indicator system. Studies on the AHP have found ways to make it more objective. However, we did not make full use of the objective AHP in the research. More efforts will be put into reducing biased expert evaluation with the objective AHP in our future studies.

Data availability

The datasets analyzed during the current study are available in the Dataverse repository: https://dataverse.harvard.edu/privateurl.xhtml?token=a42afa12-37c4-4d0b-9e58-1d809be71dbe.

References

AlGhamdi MS, Durugbo CM (2021) Strategies for managing intellectual property value: a systematic review. Word Pat Inform 67:102080. https://doi.org/10.1016/j.wpi.2021.102080

Bo F, Xuan Y, Junwen F (2021) Study on the value evaluation of intellectual property pledge financing. Can Soc Sci 17(3):113–122. https://doi.org/10.3968/12167

Boisot MH (1998) Knowledge assets: securing competitive advantage in the information economy. OUP Oxford, London

Hidalgo C (2015) Why information grows: the evolution of order, from atoms to economies. Basic Books, New York

Huang Z, Li J, Yue H (2022) Study on comprehensive evaluation based on AHP-MADM model for patent value of balanced vehicle. Axioms 11(9):481. https://doi.org/10.3390/axioms11090481

Lagrost C, Martin D, Dubois C, Quazzotti S (2010) Intellectual property valuation: how to approach the selection of an appropriate valuation method. J Intellect Cap. https://doi.org/10.1108/14691931011085641

Loyarte E, Garcia-Olaizola I, Marcos G, Moral M, Gurrutxaga N, Florez-Esnal J, Azua I (2018) Model for calculating the intellectual capital of research centres. J Intellect Cap. https://doi.org/10.1108/JIC-01-2017-0021

Lyu HM, Sun WJ, Shen SL, Zhou AN (2020) Risk assessment using a new consulting process in fuzzy AHP. J Constr Eng M 146(3):04019112, https://ascelibrary.org/doi/abs/10.1061/(ASCE)CO.1943-7862.0001757

Ma SC, Feng L, Yin Y, Wang JP (2019) Research on petroleum patent valuation based on value capture theory. Word Pat Inform 56:29–38. https://doi.org/10.1016/j.wpi.2018.10.004

Moore RE, Kearfott RB, Cloud MJ (2009) Introduction to interval analysis. Soc Ind Appl Math, Philadelphia

Parr RL (2018) Intellectual property: valuation, exploitation, and infringement damages. John Wiley & Sons, New York

Romer PM (1986) Increasing returns and long-run growth. J Polit Econ 94(5):1002–1037. https://doi.org/10.1086/261420

Saaty TL (2008) Relative measurement and its generalization in decision making: why pairwise comparisons are central in mathematics for the measurement of intangible factors the analytic hierarchy/network process // international symposium on chinese spoken language processing. https://doi.org/10.1007/BF03191825

Subramanian N, Ramanathan R (2012) A review of applications of analytic hierarchy process in operations management. Int J Prod Econ 138(2):215–241. https://doi.org/10.1016/j.ijpe.2012.03.036

Sun YF, Chen SQ, Wu JP, Liu YQ, Zhang C, Ma Q (2001) Fuzzy neural network expert system based on set-value statistics and its application. Fuzzy Syst Math (2):97–101 (in Chinese). https://kns.cnki.net/kcms2/article/abstract?v=fKv7BsF2ndxzQx0tzssCx3bu4QHBOD0WocFqv62wdxWgnqjCKLZYtBHk5D5vy1XSSDXFJlhwZf9n79rl_yTHCxx72hM1ADRVhIheAbFhExEBk1Z6EmNOvQ==&uniplatform=NZKPT

Svishchova N (2022) Development of the combined approach to the valuation of intellectual property objects. Technol Audit Prod Reserv 1(4):63. https://doi.org/10.15587/2706-5448.2022.253472

Vuong QH, Nguyen HTT, Pham TH, Ho MT, Nguyen MH (2021) Assessing the ideological homogeneity in entrepreneurial finance research by highly cited publications. Hum Soc Sci Commun 8(1):1–11. https://doi.org/10.1057/s41599-021-00788-9

Wang PZ (1985) Fuzzy sets and random set drop shadows. Beijing Normal University Press, Bei Jing

Wang Z, Wang N, Liang H (2014) Knowledge sharing, intellectual capital and firm performance. Manage Decis. https://doi.org/10.1108/MD-02-2013-0064

Yuan ZM, Li HY, Sun HL, Wang H (2012) Valuation of intellectual property pledge financing: a study of revenue sharing rate. Sci Res 30(06):856-864+840. https://doi.org/10.16192/j.cnki.1003-2053.2012.06.002. in Chinese

Zyoud SH, Fuchs-Hanusch D (2017) A bibliometric-based survey on AHP and TOPSIS techniques. Expert Syst Appl 78:158–181. https://doi.org/10.1016/j.eswa.2017.02.016

Acknowledgements

This research is supported by the Anhui Province Social Science Innovation Development research project (grant no.2020CX099), 2021 University discipline (Professional) Top Talent academic support Project (grant no. Smbjrc202102), and the Scientific Foundation of Anhui Polytechnic University for introducing talents (grant no. 2021YQQ054).

Author information

Authors and Affiliations

Contributions

RS’s contribution included Conceptualization, Formal analysis, methodology and writing-original draft; ML’s contribution included validation and software; YHF’s data curation and supervision; CY’s data curation and supervision. All authors have read and agreed to the published version of the manuscript.

Corresponding authors

Ethics declarations

Competing interests

The authors declare no competing interests.

Ethical approval

This article does not contain any studies with human participants performed by any of the authors. All research methods followed ethical guidelines, and all data are used with permission.

Informed consent

This article does not contain any studies with human participants performed by any of the authors.

Additional information

Publisher’s note Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Supplementary information

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons license, and indicate if changes were made. The images or other third party material in this article are included in the article’s Creative Commons license, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons license and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this license, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Su, R., Li, M., Fang, Y. et al. Valuation method of intellectual property pledge financing based on income interval analysis and risk adjustment coefficient. Humanit Soc Sci Commun 10, 501 (2023). https://doi.org/10.1057/s41599-023-01897-3

Received:

Accepted:

Published:

DOI: https://doi.org/10.1057/s41599-023-01897-3