Abstract

When a widespread funding shock hits the banking system, banks may engage in strategic behaviour to deal with funding shortages by a pre-emptive disposal of assets. Alternatively, they may adopt a more cautious strategy to mitigate price reactions, thereby distributing the assets sales into smaller portions over time. We model banks’ optimal behaviour using standard optimisation techniques and show that an equilibrium always exits in a stylised setting. A numerical analysis to approximate the equilibrium supplements the theoretical part. The implementation delivers two liquidity measures for the German banking system: the Systemic Liquidity Buffer and the Systemic Liquidity Shortfall. These measures are more informative about systemic liquidity risk than regulatory liquidity measures, such as the LCR, because they model adverse, nonlinear price dynamics in a more realistic way. Our approach is applied to different stress scenarios.

Similar content being viewed by others

Introduction

Financial crises have gone hand in hand with liquidity crises, particularly with a dry-up of liquidity in the banking system. For example, the great financial crisis (GFC) of 2007/2008 was characterised by simultaneous and widespread dislocation in funding markets [1].Footnote 1 As a consequence of the GFC, policymakers have introduced new liquidity management ratios, such as the Liquidity Coverage Requirement (LCR), which regulate the level and composition of liquid assets and financial liabilities for a single bank [4, 5]. The LCR is based on-balance sheet positions weighted by fixed liquidity weights. It is a static concept, which does not properly reflect changes in market prices and liquidity risk in different macroeconomic environments.Footnote 2 While the LCR is an important step to improve banks’ resilience to liquidity shocks, it does not address shortfalls caused by systemic liquidity risk [8].

Systemic liquidity risk occurs when multiple financial institutions experience liquidity shortages at the same time, which has the potential to destabilise the whole financial system [9]. For example, this situation can be characterised by banks over-relying on short-term wholesale funding and investing in the same assets in (potentially) illiquid markets. Systemic liquidity risk depends primarily on the endogenous response of market participants to extreme events [10]. In such a setting, strategic interactions between market participants play an important role when the outcome of one market participant depends upon the actions of other market participants. The interaction between funding liquidity risk (i.e. the possibility an institution becomes unable to meet its obligations when due) and market liquidity risk (which relates to the inability of trading at fair prices with immediacy) is a classical situation, where strategic interaction between market participants can lead to a coordination failure [11, 12]. Bank runs and distress sales of assets is one example.

The paper addresses the research question of how to measure the resilience of the banking system to a systemic liquidity shock when focusing on banks’ strategic interactions. This is an important question as established liquidity requirements in banking regulation, such as the LCR, do not consider strategic interactions as a source of endogenous systemic liquidity risk. Consequently, the LCR might reflect a too optimistic view in terms of the resilience of the banking system to systemic liquidity shocks.

We study the interaction between funding and market liquidity risk both theoretically and empirically. The key contributions of this study are twofold. First, we develop a novel theoretical model to analyse strategic interaction between banks via adverse price dynamics in distress asset sales triggered by a system-wide funding shock. Second, our empirical analysis makes use of granular regulatory data for German banks, which facilitate to pinpoint the resilience of the German banking system to a systemic liquidity shock.

In our theoretical framework, we take a widespread bank run as given, in which all banks simultaneously face liquidity outflows for a specified period, say 5 or 30 days, as banks’ counterparties withdraw cash and do not rollover credit. In our model, this exogenous funding shock brings about an endogenous change in the market value of banks’ security holdings as imminent cash outflows force banks to offload securities if their initial cash reserves are insufficient to service their liabilities. Banks have two objectives: First, they stay liquid at any point by selling securities if necessary. Second, they minimise losses on the market value of their securities by considering their impact and the impact of other banks’ sales on the market price. This gives rise to a coordination problem in terms of the timing and volume of sale.

Two forces then drive endogenous price dynamics: If banks expect the market price of securities to fall because other banks will sell securities to deal with funding shortages, they may dispose of them as early as possible to minimise losses in market value. Banks are cautious, however, not to single-handedly accelerate a price drop with their sales. They can therefore prefer to divide sales into small portions and extend them over a longer period. Hence, large banks tend to act more cautiously than those with little influence over the market price.

To summarise the impact of the funding shock and the induced change in the market liquidity of securities, we introduce the Systemic Liquidity Buffer (SLB) and the Systemic Liquidity Shortfall (SLS). The SLB is the difference between the liquidity inflows from distress asset sales and the liquidity outflows from on-balance and contingent liabilities. This buffer measures how vulnerable the system is to liquidity risk: Low or even negative values indicate that the system does not have enough liquid assets to withstand a system-wide bank run. While some institutions in the system may have sufficient liquidity, other institutions may not be able to meet their financial obligations. The SLS is the amount of liquidity the system would need to ensure that all institutions withstand the funding shock.

We apply the theoretical framework to derive the SLB and SLS of the German banking system. First, we examine the evolution of systemic liquidity risk over time from September 2000 to March 2023. To this end, we compare the excess liquidity of the German banking system according to established regulatory requirements, such as the LCR, with the SLB. Before the most intense period of the GFC in September 2008, this regulatory excess liquidity was positive and rising steadily, showing no sign of possible liquidity risks in the banking system. In contrast, the SLB reached its lowest and negative level in mid-2007, pointing to a vulnerability of the system to liquidity risk, which was prevalent at that time. The divergence between the two measures before the crisis stems from the impact of distress sales on security prices triggered by banks’ excessive short-term wholesale funding: Established regulatory requirements for liquidity implicitly assume that each bank can sell a particular security at the current market price less any fixed percentage (haircut). However, this static view may underestimate the sharp downwards price pressures banks collectively exert in a liquidity crisis. This latter effect is captured by the SLB.

Furthermore, the current evolution of the SLB provides insight into the (side) effects monetary policy has on systemic liquidity risk. With an expansion of unconventional monetary policy measures employed by the Eurosystem in response to the COVID-19 pandemic in March 2020, the SLB increased significantly and converged with the LCR.Footnote 3 As a stricter monetary policy was implemented from September 2022 onwards, the SLB experienced a decline and diverged from the LCR. These fluctuations in the SLB can be attributed to the accumulation and reduction of banks’ cash reserves. As a consequence of the expansion of unconventional monetary policy measures, banks had increased their cash reserves. With the reversal of monetary policy, cash reserves have recently started to fall again. High cash reserves relative to short-term funding limits contagion effects via distress asset sales as banks are able to settle obligations from existing reserves without selling assets.

Second, we examine the distribution of liquidity risk in the cross section. In a run on the banking system that takes 5 days, the SLS is about EUR 31 bn, attributable to commercial banks. Moreover, the SLB illustrates the consequences of a fire sale spiral: Comparing the stock of liquid assets valued at the end of the stress episode at depressed market prices relative to the value of the liquid assets before the run reveals an overall loss in the market value of EUR 55 bn. This loss is significant as it accounts for 8% of banks’ aggregate Tier 1 capital.

Third, we study the impact of rollover risk in the US dollar, the most important foreign currency for internationally active German banks, on liquidity in the banking system. Fourth, we examine the interaction of interest rate risk and liquidity risk. In this application, banks are faced with a repricing of banks’ liquid securities due to an upwards shift in the yield curve immediately before they face a run on their debt.

Related literature. Systemic liquidity risk has been studied extensively recently. One strand of literature focuses on (system-wide) bank runs [14,15,16], but take asset prices largely as exogenous. Another strand of literature highlights the amplification mechanism between asset prices and margin or balance sheet constraints. For example, Brunnermeier and Pedersen [17] analyse the interaction between funding liquidity and market liquidity to generate liquidity spirals, where shocks to institutions net worth lead to binding margin constraints and fire sales. The resulting increase in volatility brings about a spike in margins and haircuts forcing financial intermediaries to deliver further. Focusing more on empirical findings, Macchiavelli and Zhou [18] show that dealers’ funding liquidity affects their liquidity position in securities markets. Other studies analyse the effects of fire sales on banking systems in a mark to market environment when banks deleverage to their targets [19, 20]. These studies analyse how lower asset prices tighten balance sheet constraints, causing asset distress sales, which further depress asset prices. Unlike these models, our model assumes another amplification channel: In a liquidity crisis, where asset prices are expected to fall, banks have an incentive to sell ahead of competing banks to secure favourable prices. This amplification channel has been studied by other papers and our work complements this literature. For example, Bernardo and Welch [21] model a run on a financial market, in which each risk-neutral investor fears having to liquidate assets after a run, but before prices can recover back to fundamental values. Oehmke [22] examines disorderly liquidations of repo collateral, including a “rush for the exits” selling strategy. Finally, Morris and Shin [23] propose a model, where traders with short horizons and privately known loss limits interact in a market for a risky asset. When the price falls close to the loss limits of the short horizon traders, selling of the risky asset by any trader increases the incentives for others to sell. In contrast to existing models, our approach combines this amplification channel with banks’ funding structure: Banks’ excessive reliance on short-term (wholesale) funding amplifies downwards pressures on prices in a liquidity crisis, which drive banks to “front-run” competing banks by selling before them.

The plan of the paper is as follows. In “Theoretical model” section introduces the theoretical model and provides the economic intuition behind the approach. In “Implementation” section explains how we calibrate this model for numerical analysis. In “Applications” section discusses four empirical applications of this approach to the German banking system. In “Conclusions” section concludes.

Theoretical model

First, we formally define the SLB and explain its concept to capture systemic liquidity risk. Then, we describe the model to compute distress prices for liquid securities.

The Systemic Liquidity Buffer

The SLB is the remaining balance of liquid assets at a bank after a stress period of liquidity withdrawals lasting for a specified period T, say 5 or 30 days.Footnote 4 This remaining liquidity balance takes into account the price impact of asset sales, including those by the bank concerned and other banks, along with their strategic interactions.

We define the SLB for bank i as

where \(c_{i,T+1}\) includes the initial stock of cash \(c_{i,1}\) plus the cumulative sum of net liquidity, i.e. proceeds \(v_{i,t}\) from security sales at simulated distress prices minus outflows \(l_{i,t}\) from liabilities and contingent liabilities. \(a_{i,T+1}\) denotes the remaining security portfolio, evaluated at prevailing distress prices after the stress period has ended. While \(c_{i,T+1}\) includes actual cash flows, \(a_{i,T+1}\) is a hypothetical cash flow. Here, we ask how much cash the bank could generate if it sold the remaining portfolio.

The SLB indicates that the bank is prone to liquidity risk if it is minor or even negative. Similar to established excess liquidity requirements, such as the LCR, the SLB demands banks to hold enough liquid assets (i.e. cash or liquid securities) to cover expected liquidity outflows in a specific stress scenario over a certain period.Footnote 5 However, in contrast to the LCR, the SLB considers adverse price dynamics for securities and strategic interaction as a source of endogenous systemic liquidity risk.

By aggregating the SLB across all banks, we obtain an indicator of the banking system’s resilience to liquidity risk.

where N denotes the total number of banks in the system.

We also introduce the Systemic Liquidity Shortfall (SLS),

including only those banks with insufficient liquidity in a crisis. In this way, banks with sufficiently large liquidity positions do not offset illiquid banks. While the SLB measures the value of liquid assets available in the system after the funding shock, the SLS is informative about the level of liquidity needed in the banking system to ensure that all banks withstand a liquidity shock.

An optimisation model endogenously determines banks’ security sales and the resulting distress prices of liquid securities.Footnote 6 The model reflects the liquidity management of individual banks and is characterized by strategic interaction. We assume an exogenous shock to funding liquidity, where all banks simultaneously face liquidity outflows from liabilities and contingent liabilities over a certain period T. Banks’ counterparties withdraw cash and do not roll over credit. We model an endogenous shock to market liquidity based on the exogenous funding shock. We assume two objectives characterise banks’ decision-making. First, they aim to stay liquid at any point by drawing on existing cash reserves and generating cash through sales of securities. Second, they aim to minimise the market value declines of securities by considering the price impact of their and other banks’ strategies. Assuming that banks take into account the projected liquidity outflows of other banks and their decision-making, the constellation described above leads to a coordination problem among banks in terms of the timing and the volume of sale of liquid securities. The model determines banks’ optimal selling strategies in a Nash equilibrium to derive the distress prices.

Modelling distress prices

After having explained the concept of the SLB, we now formulate the underlying model.

Price impact ratio

The total volume of sales by the entire banking system invokes a price reaction on asset markets. Let \(p_{k,t}\) denote the market price of asset k at time t. The gross return of an asset class k is denoted as \(R_{t,t+1}^{k}:= p_{k,t+1}/p_{k,t}\). A widely used empirical measure of market liquidity suggested by Amihud [24] considers the (absolute value of the) price change per nominal amount traded in the market. If even small trading volumes are associated with large price changes, the Amihud measure is large and indicates illiquid markets. We consider a modified version of the Amihud measure in our model. We restrict attention to falling prices in the stress episode, i.e. \(R_{t,t+1}^k < 1\), and assume the constant relationship

between returns and the trading volume.Footnote 7\(V_{t,t+1}^k\) denotes the trading volume for asset class k measured at market prices at time \(t+1\). Rearranging Eq. 4, for a given price impact ratio \(\lambda _k\) we obtain the relative price decline between the two periods t and \(t+1\):

Note that while \(\lambda _k\) is constant the simulated price decline, \(R_{t,t+1}^k\) varies depending on the total sales volume \(V_{t,t+1}^k\) (measured by market prices at time \(t + 1\)). Total sales in asset class k in period t are then given by \(V_{t,t+1}^k = \sum _{i=1}^N v_{i,k,t},\) in which \(v_{i,k,t}\) denotes the sales volume of bank i in asset k at time t. Bank’s sales volume is determined endogenously by our optimisation model.

Optimisation model

We formulate the bank’s liquidity management for the above-described shock scenario in a stylised version and consider two banks (\(i =1, 2\)), two periods \((t = 1, 2)\) and one asset class \((k=1)\) for this purpose. While this simplified version is sufficient to explain the model’s main features, extending it to N banks and T periods is straightforward. We assume that in the optimisation problem below, bank 1 takes sales of bank 2 as given. Regarding the sales volumes \(v_{1,t}\) for \(t=1,2\), the optimisation problem for bank 1 is then

and additional constraints

We assume positive initial values \(a_{i,1}\) and \(c_{i,1}\) for assets and cash for both banks \(i =1, 2\). The objective function minimises bank 1’s losses in market value on its holdings of liquid securities \(a_{1,t}\). The two transition equations show the evolution of cash holdings \(c_{1,t}\) and the market value of the asset \(a_{1,t}\) that bank 1 has. They reflect that assets are sold to raise cash so that the bank can service its liabilities. Doing so a price reduction of the assets is caused. The variable \(l_{i,t}\) denotes outflows from deposits and other forms of debt. The first inequality constraint is a non-negativity constraints on the sales volumes. The second constraint ensures that the bank serves its liquidity providers. The third constraint is an upper bound to the sales volume which results from the availability of assets and the reduction in market prices.

In the remainder of this section, we rely on two assumptions.

Assumption 2.1

-

(a)

\(\lambda = \left( R_{t,t+1}-1\right) /V_t\) is strictly negative, i.e. \(\lambda < 0\),

-

(b)

\(l_{i,1} - c_{i,1} > l_{i,2}\) for \(i= 1, 2\).

The first assumption says that we focus on falling prices in the stress episode. The latter assumption considers that banks’ liabilities net of liquid funds follow a monotonic decreasing pattern over time. The assumed liability profile should be consistent with the actual conditions since banks’ short-term liabilities usually exceed their long-term liabilities (see also Fig. 2a, b). The second assumption is helpful for technical reasons. In such a setting, it can be proved that at least one equilibrium always exists.Footnote 8 Before discussing possible equilibria, we state the following result.

Theorem 2.1

Let

Then, under Assumption 2.1, the optimal solution to problem (6), denoted by \(\left( v_{1,1}^*,v_{1,2}^*\right)\), is given by

-

1.

Just-in-time: \(v_{1,1}^* = l_{1,1}-c_{1,1}\), \(v_{1,2}^* = l_{1,2}\) if \(d_{1,1} ( v_{2,1},v_{2,2} ) < l_{1,1} - c_{1,1}\),

-

2.

Smoothing: \(v_{1,1}^* = d_{11} ( v_{2,1},v_{2,2} ), v_{1,2}^* = d_{1, 2} ( v_{2,1},v_{2,2} )\), if \(l_{1,1} - c_{1,1} \le d_{1,1} ( v_{2,1},v_{2,2} ) < l_{1,1} + l_{1,2} - c_{1,1}\),

-

3.

Front-Servicing: \(v_{1,1}^* = l_{1,1} + l_{1,2} - c_{1,1}\), \(v_{1,2}^* = 0\), if \(l_{1,1} + l_{1,2} - c_{1,1} \le d_{1,1} ( v_{2,1},v_{2,2} )\) and \(\frac{a_{1,1}}{1-\lambda a_{1,1}} \ge v_{2,2}\),

-

4.

Distress-Sale: \(v_{1,1}^* = \left( \frac{a_{1,1}}{1-\lambda a_{1,1}}\right) \left( 1+\lambda v_{2,1}\right)\), \(v_{1,2}^* = 0\), if \(l_{1,1} + l_{1,2} - c_{1,1} \le d_{1,1} ( v_{2,1},v_{2,2} )\) and \(\frac{a_{1,1}}{1-\lambda a_{1,1}} < v_{2,2}\).

The strategies ensure that bank 1 can raise sufficient cash and simultaneously minimises market losses of its securities. The four strategies are ordered based on how early and to what extent securities are sold. Aware of its influence on the market price, bank 1 wants to divide the sale into small portions in the just-in-time strategy, but the need to meet liquidity constraints force a higher level of sales in period 1. Consequently, bank 1 sells the exact amount of securities that covers the outflows in each period. In the Smoothing strategy, bank 1 anticipates sales by bank 2 in period 2. To secure a more favourable price, bank 1 sells a portion of its holdings in period 1, exceeding the liquidity withdrawals. This price impact by bank 2 in period 2 is more dominant in the Front-Servicing strategy, where bank 1 already sells an amount equal to the total liquidity needed in period 1 and does not make a sale after that. In the distress sale strategy, the price impact by bank 2 completely dominates bank 1’s decision-making, as bank 1 sells the maximum amount available in the first period.

A key variable in the theorem is \(d_{1,1}\). It determines the decision of bank 1, which of the four possible strategies are optimal. Note that the optimal strategy for bank 1 in period 1 in the Smoothing strategy coincides with the variable \(d_{1,1}\). We refer to Appendix 1.1 for more detailed explanations regarding the intuition of the expressions for each of the four cases and to Krüger et al. [25] for the proof of Theorem 2.1. A symmetric version of the theorem holds for bank 2, given that bank 1 has decided on its strategy.

The strategic interaction created through the bank’s influence on the price impact of the asset means that the problem takes the form of a 2-period game in pure strategies under complete information, in which banks choose selling strategies to minimise their losses in the market value of its portfolio and to meet liquidity outflows. Next, we show that Nash equilibria in this set-up always exists so that the individually optimal selling strategies are mutually compatible and banks avoid becoming illiquid.

Theorem 2.2

Under Assumption 2.1, a Nash equilibrium exists. In other words, for each initial parameter setting \(w=(a_{1,1}, a_{2,1}, c_{1,1}, c_{2,1}, l_{1,1}, l_{1,2}, l_{2,1}, l_{2,2}, \lambda )\), a combination of strategies \(( v_{1,1}, v_{1,2} )\) for bank 1 and \(( v_{2,1}, v_{2,2} )\) for bank 2 exists such that simultaneously the following two statements hold:

-

1.

The strategy vector \(( v_{1,1}, v_{1,2} )\) of bank 1 is an optimal solution to the optimisation problem w.r.t. the strategy \(( v_{2,1}, v_{2,2} )\) of bank 2.

-

2.

The strategy vector \(( v_{2,1}, v_{2,2} )\) of bank 2 is an optimal solution to the optimisation problem w.r.t. the strategy \(( v_{1,1}, v_{1,2} )\) of bank 1.

We refer to Krüger et al. [25] for the proof.Footnote 9

Two opposing incentives determine banks’ optimal strategy in this model. On the one hand, banks will individually strive to sell their assets as quickly as possible to be ahead of competing banks and secure favourable prices. On the other hand, they will try to divide the sale into small portions so as not to accelerate the price drop single-handedly. Hence, large banks tend to act more cautiously than those with little influence over the market price. A banking system in which the portfolio of assets and the liabilities of one bank are much more extensive relative to those of the other bank tends to reach a Nash equilibrium, where the large bank chooses just-in-time or Smoothing and the small bank chooses Front-Servicing or Distress-Sale.

Implementation

First, we introduce a generalised model, which can be used for numerical analyses of the German banking system. Then, we describe the regulatory and market data of net outflows, liquid assets and cash. Finally, we discuss the assumptions of the numerical analyses.

Generalised problem

To perform numerical analyses of the German banking system using regulatory and market data, we need to expand the model considering N banks, K asset classes and T days. In this set-up, a bank i has to decide on the sales volume of its assets \(a_{i,k,t}\) for each asset class \(k=1, \ldots K\) and in each point in time \(t = 1, \ldots , T\). In order to simplify the problem, we will consider a pro rata approach to asset sales and assume that the sales volume of bank i in asset class k at day t is given by

The variable \(\omega _{i,t}\) describes the fraction, which bank i spreads equally across asset classes at day t. The decisions to be made by bank i are captured by the strategy vector \(\omega _{t} = \left( \omega _{i,1}, \ldots , \omega _{i,t}, \ldots , \omega _{i,T}\right)\). The gross return per asset class k is denoted as

Combining Eqs. 7 and 8, we obtain

Taking into account Eq. 9, the optimisation problem for the implementation model for bank i isFootnote 10

The bank must choose a strategy that ensures its liquidity until \(T+1\) (L). The liquid funds evolve according to (C). The available cash in period \(t+1\) is given by previous cash holdings \(c_{i,t}\) less net liquidity outflows. Moreover, the bank may decide to liquidate a share of its asset portfolio to restore or to increase liquidity. These shares are bounded between zero and one (B). The market value of an asset in period \(t+1\) is the remaining stock of assets after liquidation in period t, evaluated at market prices implied by \(R_{t,t+1}^k\), as specified in condition (V). The cash position \(c_{i,T+1}\) and the market value of the entire portfolio \(a_{i,T+1} = \sum _{k=1}^{K} a_{i,k,T+1}\) are then used to compute the Systemic Liquidity Buffer, see (1).

Due to its complexity, finding a closed-form solution to the optimisation problem goes beyond the scope of this paper. To reach a satisfactory solution, we develop a heuristic approach that iteratively determines each bank’s optimal strategy conditional on the strategies of the other banks. Details are laid out in Appendix 1.2.

Data

Net outflows, liquid assets and cash

Data on net outflows, the initial stock of liquid assets and cash are obtained from the common reporting framework (COREP), which includes two different data sets: (1) the Liquidity Coverage Requirement (LCR) and (2) the Additional Monitoring Metrics for Liquidity (AMM). The LCR data set is used to compare the SLB with the LCR excess liquidity over time (see “How does the SLB differ from liquidity requirements in banking regulation?” section).Footnote 11 The AMM data set is the basis for our analyses assessing the banking system’s resilience to liquidity risks in the short run (see “How resilient is the banking system in the short run?” section).

German banks report both data sets on a monthly basis. Generally, we use reporting information at the banking group level.Footnote 12 For banks not part of a banking group, we use reporting information at the solo level. Furthermore, we consider the unique properties of the banking associations’ liquidity management into account. As the savings and cooperative banks are integrated into a central cash management controlled by their respective central institutions, it is not reasonable to model them as independently acting players in a systemic liquidity crisis. Thus, we assume that savings banks coordinate with their regional head bank (Landesbank), and cooperative banks coordinate with their respective central institute, so that each association would act like a single banking group when selling securities.

We aggregate banks’ reported liquid assets into five classes: government bonds, uncovered bonds, covered bonds, shares and asset-backed securities.Footnote 13 We assume that these classes properly reflect differences in liquidity in times of stress, and we assign different price impact ratios to each class. Further details regarding their computation can be found below. For each asset class, market values are reported, which we use as initial values when modelling distress sale losses.

We determine the daily net outflows for each bank based on outflows from funding obligations net of inflows from non-fungible assets (e.g. inflows from interest income). In the LCR data set, outflows are based on bank’s liabilities, which are weighted depending on their rollover risk and run risk.Footnote 14

We obtain outflows for the AMM data set according to their contractual obligations. For deposits, banks provide contractual and so-called behavioural outflows in their AMM data reports. These behavioural outflows take banks’ estimates of actual business dynamics of deposit outflows into account and reflect the experience that they are a lot stickier than their contractual maturities suggest.Footnote 15 We assume liabilities become due according to their contractual maturity during the funding shock period, except for deposits, where we take behavioural outflows. For robustness checks, we deviate from the baseline case and examine results when the contractual deposit outflows are used instead, see Appendix 1.3.

The AMM data set provides a granular breakdown of banks’ maturities of obligations. In particular, inflows and outflows are reported daily for the first seven days. To ensure that the stress scenario is sufficiently severe, we restrict daily net outflows to be floored by zero, i.e. inflows from non-fungible assets cannot overcompensate outflows from payment obligations.Footnote 16

The LCR data set refers to a period of 30 calendar days for the net outflows, and the German Liquidity Directive refers to a period of one month, respectively. As no more detailed breakdown by maturity is provided, the daily net outflows for each bank are calculated based on the simplifying assumption of uniformly distributed outflows over the referred period.Footnote 17

Price impact ratio

A vital parameter of the empirical model is the price impact ratio \(\lambda\). Since our price impact ratio is a constant value in the empirical model, it is reasonable to determine \(\lambda\) for each asset in the most conservative way possible.

We calculate the daily associations between the aggregated trading volume and the trading volume weighted average price decline across all securities that belong to a particular asset class k over a specific observation period. We select the average or minimum value among the calculated daily associations and assign it to the price impact ratio \(\lambda _k\). Table 1 includes an illustrative example of the calculation for \(\lambda _k\) and lists the price impact ratios for each asset class type calculated. For (corporate) bonds the ratio amounts to \(-\)0.015 per billion USD, which lies in the lower range of other empirical estimates for this type of securities (i.e. the value used in our model is more conservative and results in a larger price drop) [27,28,29].

For government bonds (which make up by far the largest part of banks’ portfolio of liquid assets), we use MTS dataFootnote 18 on daily bond prices and turnovers and calculate the average price impact ratio for government bonds during the period from the beginning of May to the end of June 2012, which was just prior to the ECB president Mario Draghi’s famous speech on 31 July 2012 at UKTI’s Global Investment Conference over the irreversibility of the Euro and ECB’s preparedness to do “whatever it takes”. During this turbulent European Sovereign debt crisis, spreads of 10-year Italian bonds over the corresponding German government bonds interest rate have been the largest in recent history. Based on this stress period, we select the average value among the calculated daily associations between the aggregated trading volume and the trading volume weighted average price decline and assign it to the price impact ratio \(\lambda _k\). In Appendix 1.3, we check the simulation results if we use the minimum value among the calculated daily associations (which reflects the most significant negative daily price impact).

The trading volume and price data for corporate bonds and covered bonds not traded on a centralised exchange are captured based on data from the TRACE reporting system with Bloomberg’s TACT analysis and valuation function. The sample covers the period from June 2016 to August 2016. As this period does not reflect a period of market stress, we select the minimum value among the calculated daily associations and assign it to the price impact ratio \(\lambda _k\).

In principle, the calculation for \(\lambda _k\) follows the concept of the Amihud-Ratio, which is defined as the average daily association between a unit of trading volume (measured in USD) and the relative price change for an individual security over a certain period, e.g. 1 year.Footnote 19

Discussion of the assumptions of the numerical analyses

Our numerical analyses makes three specific assumptions. First, we disregard the role of the central bank as a lender of last resort, as we want to test the banking system’s resilience to a widespread funding shock without assistance from the central bank. Consequently, we assume banks do not have access to central bank funding. In particular, repo transactions vis-à-vis the central bank are excluded.Footnote 20 This assumption is guided by the macroprudential, i.e. preventive focus of our liquidity metrics. They are supposed to pick up liquidity risks that do not anticipate lender of last resort activities in the spirit of Bagehot [30], as addressing those liquidity risks in a timely manner would ideally make central bank intervention less likely and necessary.Footnote 21 Second, we assume that banks cannot rely on interbank credit as a potential funding source during episodes of stress. In particular, banks cannot offset the cash outflows through the interbank repo market. Banks depend on outright asset sales as a short-term funding source to service their liabilities in such a scenario.Footnote 22 Third, we assume banks restrict asset sales to securities designated as liquid assets according to the Capital Requirements Regulation (CRR), i.e. high-quality liquid assets (HQLA), which are eligible for the LCR. We are thus following the underlying concept of the LCR where banks should build up a buffer of HQLA that can be used in times of stress. Adopting such a regulatory perspective allows us to readily compare the results produced by our model with the LCR.

Applications

We use the SLB to address four policy issues. First, we contrast the SLB with established liquidity requirements in banking regulation over time, including the LCR. Second, we examine the SLB and SLS in the cross section for a severe funding shock over 5 days. We supplement the baseline funding shock with two alternative shock scenarios covering the German banks’ US dollar business, and suddenly rising interest rates in the banking system.

How does the SLB differ from liquidity requirements in banking regulation?

This exercise aims to present a long-run view of the SLB compared with established liquidity requirements.Footnote 23

Time series analysis from 2000 to 2017

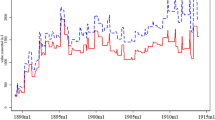

As banks’ liquidity was regulated nationally in the German liquidity regulation until 2017, we use data from the German liquidity regulation to investigate systemic liquidity risk for the period from 2000 to 2017.

Figure 1(a) presents the evolution of the aggregated SLB across all banks in Germany and the aggregated excess liquidity according to the national liquidity regulation from 2000 to 2017. Notably, both indicators are constructed in a similar manner: They equal the sum of stock of cash and liquid securities less of net outflows. The only difference is the measurement of liquid securities. While simulated distress prices for the SLB measure liquid securities, the German liquidity regulation assigns current market prices to liquid securities (i.e. no haircuts are assigned, which is equivalent to \(\lambda _k=0\)). We make three observations.

-

(i)

The SLB is lower than the aggregate excess liquidity throughout. Hence, considering the impact of potential distress sales, systemic liquidity is lower than the aggregate of the individual liquidity measures. This is plausible given that the German liquidity regulation does not consider reducing the actual market price for most types of liquid assets.

-

(ii)

The SLB falls below zero in the second quarter of 2006 and reached its low point in the second quarter of 2007, while the aggregate excess liquidity continues to rise. Therefore, ahead of the most intense period of the GFC in September 2008, the SLB indicates that the banking system is vulnerable to liquidity risk. The reason for the diverging patterns of the SLB and the aggregate excess liquidity is that the banking system increased its short-term funding on a large scale in the run-up to the crisis from June 2003 to June 2007, resulting in an increase of net outflows of nearly 65% to EUR 763 bn. Notably, an increase in net outflows has a twofold effect on the SLB: Net outflows are directly deducted from the SLB (as for the aggregate excess liquidity), and, in addition, an increase in net outflows results in lower prices of liquid assets once banks start selling assets to raise cash, which depresses the SLB further. The latter effect is not reflected by the German liquidity regulation. In this sense, the SLB has the potential to serve as an early warning indicator of systemic liquidity risk induced by excessive short-term refinancing in the banking system.

-

(iii)

In 2008, both measures of liquidity risk decreased since the GFC. German banks drastically reduced their interbank borrowing and hoarded liquidity. These effects result in substantially lower net outflows and a more prominent cash position, which increases both the SLB and aggregate excess liquidity.

The Systemic Liquidity Buffer (SLB) over time (in EUR bn). This figure shows the SLB over time as discussed in “How does the SLB differ from liquidity requirements in banking regulation?” section from 2000 to 2023. In addition, we depict the aggregate excess liquidity (liquid assets—net outflows) derived from regulatory requirements. The excess liquidity is derived from a German liquidity measure from 2000 to 2017 in Fig. 1(a), and from the liquidity coverage ratio (LCR) in Fig. 1(b). In either case, the net outflows underlying the SLB and the excess liquidity coincide, but the two approaches differ in the valuation of liquid assets, as the SLB takes distress sales into account

Net liquidity outflows across maturities (as a percentage of liquid assets, June 2020). This figure shows the aggregate net outflow (liquidity outflow–liquidity inflow) of the German banking system in June 2020, as a percentage of liquid assets (blue). The net outflow is sorted into four maturity buckets, spanning 30 calendar days in total. The net outflow is based on contractual maturities, and similarly to the liquidity coverage ratio (LCR), net outflows are restricted to be non-negative, so that a net inflow is not allowed. In addition, the figure displays the net outflow when contractual outflows from deposits are replaced by behavioural outflows from deposits (red). These behavioural outflows are reported by banks. Furthermore, this adjusted net outflow adds contingent outflows from committed credit and liquidity facilities, denoted as credit lines. Panel (a) shows overall positions (all currencies), while Panel (b) reports positions only in US dollars

Time series analysis from 2018 to 2022

In Germany, the LCR replaced the German liquidity regulation in 2018 and related a liquidity buffer to a net liquidity outflow over a 30-calendar-day period.Footnote 24 We adopt an analogous approach to compare the aggregated SLB with the aggregated excess liquidity according to the LCR. As the LCR assigns haircuts for many types of securities (in contrast to the former German liquidity regulation), we include a third indicator as a benchmark, which does not allow for market risk (i.e. no haircuts are assigned, which is equivalent to \(\lambda _k=0\)). The three measures differ only in the valuation of liquid securities.

We depict the evolution of the indicators since 2018 in Fig. 1(b). We make three observations.

-

(i)

As the excess liquidity requirement according to the LCR and the SLB are larger than zero, both measures indicate sufficient liquidity in the system to withstand the underlying funding shock. For most of the period under review, the SLB is, however, lower than the excess liquidity. Again, this is plausible given that for the aggregate excess liquidity according to the LCR, the reduction of the actual market price is very small for most securities that banks hold for liquidity management. Government bonds account for more than two-thirds of all securities designated as HQLA. Most government bonds receive a weight of 100% and are thus measured at their current market price.Footnote 25 Thus, each bank individually assumes that government bonds, say, can be sold at the current market price, but this assumption may neglect the downwards price pressure exerted by banks collectively. In contrast, the SLB takes the effect of distress sales on market prices into account, resulting in a reduction of up to 35% during the observation period.

-

(ii)

Over time the difference between the aggregate excess liquidity and the SLB has decreased, and has even temporarily disappeared after the outbreak of the COVID-19 pandemic in 2020 and 2021. The reason why the gap has narrowed is that most banks have built up large central bank funds (cash reserves) following the introduction of extraordinary monetary policy measures in the euro area, such as the such as Targeted Longer-Term Refinancing Operations (TLTRO-III) and the Pandemic Emergency Longer-Term Refinancing Operations (PELTROs). Accordingly, in June 2020, cash reserves accounted for 58% of aggregate HQLA. Cash reserves are taken into account equally in both the SLB and the LCR framework. As they form such a large part of banks’ liquid assets, the need to liquidate other assets in times of stress is relatively low. Thus, a large share of cash reserves causes the level of both indicators to converge.

-

(iii)

As a stricter monetary policy was implemented from September 2022 onwards, the SLB experienced a decline and diverged from the LCR. These fluctuations in the SLB can be attributed to the accumulation and reduction of banks’ cash reserves. With the reversal of monetary policy, cash reserves have recently started to fall again. Lower cash reserves relative to short-term funding amplify contagion effects via distress asset sales as more banks are forced to sell assets to settle obligations.

The Bridge between LCR and \({SLB}\)

As shown in Table 2, the difference between the SLB and the LCR excess liquidity is mainly driven by the different valuations of government bonds. Table 2 provides a comparative calculation between the LCR excess liquidity and the SLB to illustrate the differences between the two measures. The calculation is done for December 2019 and December 2021 because the difference between the two measures has decreased significantly during the outbreak of the COVID-19 pandemic. While for government bonds, the LCR haircut is zero or very small, their simulated distress sale loss is immense. As government bonds account for the bulk of banks’ liquid securities (roughly two-thirds), their large total selling volume drives the relatively large price drop experienced by sovereign bonds. Notably, for uncovered bonds, shares and ABS, the losses due to distress sales are lower than the LCR haircut. While the (absolute) price impact ratios for uncovered bonds, shares and ABS are relatively high, their stock of securities held by banks is relatively low. Consequently, the simulated selling volume is relatively low, and so is the downwards pressure on market prices.Footnote 26 These observations regarding the haircuts reveal an interesting point regarding our model: The haircuts computed for the SLB are not necessarily more conservative than the LCR haircuts, but instead they are dynamic and reflect the characteristics of a particular stress situation.Footnote 27

How resilient is the banking system in the short run?

We examine the impact of a severe funding shock over 5 days on the SLB and SLS in the cross section, broken down by bank groups according to their business model. As a robustness check, we run the baseline funding shock with different values for \(\lambda _k\) and net outflows, detailed in Appendix 1.3. The baseline funding shock is supplemented with two alternative shock scenarios covering the German banks’ US dollar business, and suddenly rising interest rates in the banking system.

Baseline funding shock

Panel (a) of Fig. 2 shows predicted net outflows from the German banking system under the baseline scenario. Outflows account for more than 20% of liquid assets in this horizon of 5 days. Note the significant difference between net outflows according to contractual maturities (blue) and net outflows adjusted to incorporate behavioural outflows from deposits (red). Taking these behavioural outflows into account, we obtain a scenario that may resemble a breakdown of wholesale funding markets.

In Panel A of Table 3, we explore the cross-sectional distribution of liquidity risk for March 2023, by evaluating the SLB and the SLS for several institutions according to their business model. We learn that there is substantial heterogeneity in the cross section: While there is no shortfall among cooperative and savings banks, commercial banks have a shortfall of about EUR 31 bn.Footnote 28 Overall, the SLS is helpful in assessing the liquidity needs of the banking system and also helps to find potentially vulnerable institutions within the system.

In addition, we consider the loss in market value that banks experience during the funding shock. Here, we compare the stock of liquid assets valued at the end of the stress episode at possibly depressed market prices relative to the value of the liquid assets before the run on the banking system started. There is an overall loss in the market value of EUR 55 bn in this period. While this loss is 3% of liquid assets, it is significant for most banks in terms of Tier 1 capital. The loss is also relevant for systemically important institutions, which suffer a loss of 9% of their Tier 1 capital.

For robustness checks, we deviate from the baseline case and examine results with different values for \(\lambda _k\) and when contractual deposit outflows are used instead, see Appendix 1.3.

Furthermore, in Fig. 3, we depict the evolution of the gross returns by asset class to illustrate the dynamics of the simulated downwards price spiral. Note that we adopt the pro rata assumption in our model, so that asset sales are distributed across the whole portfolio of the banks. Therefore, we observe a price impact for all types of assets. Figure 3 shows a sharp price fall over the first two days, then a flattening. This is because most banks, in particular smaller institutions, engage in distress sales, in which they sell their stock of liquid assets as early as possible. The cumulative price declines vary between 3% and 10%. In addition to stocks, government bonds suffer the most significant decline, despite having the most minor (absolute) price impact ratio. Significantly, the price impact across asset classes depends on the commonality and level of banks’ security holdings. As government bonds account for the bulk of banks’ liquid securities (roughly two-thirds), their large total selling volume drives the relatively large price drop experienced by sovereign bonds.Footnote 29

The gross returns for liquid assets according to the Systemic Liquidity Buffer (SLB). This figure shows the gross returns \(R_{t,t+1}\) attached to several types of assets classes over the course of the scenario horizon for the funding shock in March 2023. See also “Theoretical model” section for a definition of the gross return

US Dollar funding shock

The US dollar business plays an important role for internationally active banks, and funding of European institutions in this currency has tended to be vulnerable in times of market-wide distress.Footnote 30 Therefore, we reapply the baseline funding shock outlined above, which is limited to liquid assets and net outflows in the US dollar.

Panel (b) of Fig. 2 shows the net outflows in US dollars across maturity bands, as a percentage of liquid assets in US dollars. Note that in contrast to the case in which we consider all maturities, adjusted net outflows now exceed the net outflows with contractual outflows. There are two reasons for this result. First, banks do not maintain sizeable retail business in US dollars. Consequently, there is not much impact from replacing contractual outflows from deposits with behavioural outflows. Second, the adjusted net outflow also incorporates contingent outflows from credit lines, pushing the adjusted outflow over the net outflow without contingent outflows. This figure also highlights that banks may be vulnerable to liquidity shocks in certain currencies, as in this case, the system faces net outflows over 5 days which exceed liquid assets in that currency.

The results of this exercise are presented in Panel B of Table 3. Notably, the overall SLS is large relative to the SLS in the baseline case, which includes all currencies. The shortfall of USD 71 bn is primarily due to a shortfall in systemically important institutions. These institutions dominate the US dollar business conducted by German banks. As this shortfall is mostly concentrated on systemically important institutions, these findings may suggest that the German banking system is vulnerable to a funding shock in US dollars.Footnote 31

Combined interest rate and funding shock

We examine the interaction between interest rate and liquidity risk. We combine the baseline funding shock studied above with an exogenous interest rate shock, which shifts the yield curve upwards. In this way, we add another risk channel that impacts the banking system’s resilience. In addition to the exogenous increase in outflows on banks’ liability side and the endogenous distress sales by banks to restore liquidity, there is a new effect: Rising interest rates lower the present value of banks’ assets immediately. Most importantly, from a liquidity management perspective, the market value of fixed-income securities decreases. In this sense, the asset valuation channel opens up in two ways, an instantaneous repricing effect and a distress sale effect that materialises throughout the stress horizon.Footnote 32

We start by describing the interest rate shock that affects the market value of the bond portfolio. Using data from the Bundesbank’s Securities Holdings Statistics (SHS), we obtain a sample of the government bonds that German banks held in March 2018.Footnote 33 We accompany these securities with market data from Thomson Reuters Datastream, including the modified duration.Footnote 34 According to the modified duration, an overnight increase in interest rates of 100 basis points is associated with an average loss in the market value of 8.5% and a median loss of 6%. We view this measure of the sensitivity of banks’ bond holdings to changes in interest rates as a guideline in this exercise: We examine a scenario in which a rise in interest rates results in an instantaneous loss in the market value of banks’ bonds of 10%. Given the information from the sample described above, this loss is larger and more widespread, as we adopt this drop in the value of bonds to the entire portfolio, including government and other types of bonds.

In Panel C of Table 3, we present the combined interest rate and funding shock results. The initial shock of 10% corresponds to a market value loss of about EUR 62 bn, while the distressed sales result in a loss in the market value of about EUR 46 bn. The total shortfall in the system remains almost unchanged, but the losses in market value on banks’ securities increase substantially relative to the baseline funding shock, from EUR 55 bn to EUR 108 bn. Accordingly, the loss as a share in aggregate Tier 1 capital increases from 8% to 16%. Hence, in this exercise, the additional interest rate shock increases the level of market value losses, but does not change the dynamics of the funding shock significantly, as the shortfall in the combined scenario (Panel C) does not change much relative to the baseline scenario (Panel A).

Conclusions

This paper measures systemic liquidity risk by analysing banks’ strategic interaction via adverse price dynamics. The model tests the banking system’s resilience to an exogenous funding shock. It gauges the collective impact of a funding liquidity shock and distress sales on financial institutions, illustrating how strategic bank behaviour can further amplify price declines. In addition, we propose two indicators termed SLB and SLS. The first metric measures the resilience of the banking system to such a funding shock scenario with distress sales, and the latter metric measures the aggregate liquidity need in such an extreme event. Both measures are expressed in nominal terms and are therefore easy to interpret.

We demonstrate the practicality of our framework with four examples: First, we compare the SLB with established regulatory liquidity measures over time, including the LCR. Then, we compute the impact in the cross section. We supplement the baseline funding shock with two alternative shock scenarios covering the German banks’s US dollar business and suddenly rising interest rates in the banking system.

This framework is helpful for policymakers in the context of macroprudential surveillance. Like the SLB, the (microprudential) LCR assumes a stress event where funding suddenly evaporates, and banks face projected outflows over a specified time. However, the LCR assigns fixed liquidity weights (haircuts) to securities designated as HQLA, whereas the SLB assigns distress prices that vary over time depending on system-level factors, particularly the aggregated short-term funding in the banking system. The higher the aggregated short-term funding, the lower the simulated distress prices for securities according to the model underlying the SLB. In this respect, the SLB is more sensitive than the LCR to changes in the aggregated short-term funding. It has the potential to provide early warning of mounting vulnerabilities in the banking system caused by excessive short-term borrowing. The SLB signalled an increase in systemic liquidity risks ahead of the GFC 2007–08 by a decline in the corresponding liquidity buffers.

In addition, established regulatory indicators might be too optimistic regarding systemic liquidity because they do not account for distress sales. For example, the LCR applies a haircut of zero to most government bonds eligible for refinancing at the central bank. While from a microprudential point of view, a liquidity risk weight of zero for these safe and liquid securities is meaningful, from a macroprudential view, such an approach may underestimate systemic liquidity risk at times. In a financial crisis, the market liquidity of government bonds can deteriorate suddenly. Likewise, refinancing eligibility at the central bank may be restrained (as was the case for Greek government bonds during the European Sovereign debt crisis in 2012). In this respect, our contribution is to provide an indicator that signals systemic liquidity stress in time. Finding suitable macroprudential instruments to deal with the identified systemic liquidity risks is beyond the scope of this paper and is left for future research.Footnote 35

When working with complex strategic interactions between multiple decision-makers, we must make simplifying assumptions. For example, we assume banks’ liquidity outflows are exogenous and certain over the stress period. In reality, banks’ future outflows are endogenous depending on the state of the financial system (e.g. market liquidity) and uncertain to other banks. A large volume of sales conducted by one bank would signal liquidity problems to other banks and may lead to an increased withdrawal of deposits from the selling bank. In such a setting, the game would transform into a signalling game where funding liquidity and market liquidity would mutually reinforce each other. Furthermore, we take a narrow view of the banks’ strategies. We assume that banks sell securities to maintain liquidity but do not become buyers in these markets. Therefore, the above scenario assumes that funds leave the German banking system entirely and are shifted to other banking systems. Such a setting does not consider a reallocation of funds within the German banking system, which may have a stabilising effect. In times of stress, investors may shift funds that they have provided to some institutions to other institutions that are perceived as high-quality banks [41].

At the same time, this setting does not consider adverse effects stemming from predatory trading, which may amplify price declines in a liquidity crisis [42]. We also assume that banks sell their securities in proportion to their actual holdings (pro rata) but do not follow a pecking order. While there is empirical evidence that banks tend to sell securities in such a way in a crisis event [43], this certainly leaves room for future research.

Another area for improving the current framework is to integrate the interactions between banks and other sectors of the financial system or the real economy. Ignoring the common asset holdings between banks and the non-banks financial sector can significantly underestimate losses in distressed sales [44]. In this vein, other financial intermediaries, such as insurance companies or mutual funds, often played a key role during past liquidity crises [45]. The same applies to the role of the central bank. In a liquidity crisis, central banks may provide emergency liquidity assistance as lenders of last resort. Integrating such crisis responses by the central bank in the model would allow an ex ante policy evaluation.

Notes

Beyond banks’ liquidity situation, the COVID-19 crisis also affected banks’ capital buffers. For details, see [13].

The choice of T depends on various factors. It is advisable to set the stress period at 30 days if one intends to compare the SLB with the LCR. For measuring very short-term liquidity risks, it may be sensible to choose a shorter time frame, say 5 days.

This allows us to quickly compare the SLB with established liquidity requirements in banking regulation, see “Applications” section.

All other variables of the SLB are exogenous. Initial stock of cash, quantities of liquid securities and outflows are readily available from reports for regulatory liquidity measures. See “Implementation” section for more details.

Since \(\lambda _k\) is assumed to be a constant, it is reasonable to determine the parameter in the most conservative way possible for the empirical model. For more details refer to “Data” section.

Besides the consequences for the proof of the existence of an equilibrium, the Assumption 2.1 (b) has two other implications. It implies \(l_{i,1} > c_{i, 1}\). Consequently, the bank is faced with illiquidity risk already in period 1. Furthermore, the restriction \(v_{1,1} \ge 0\) in the optimisation problem (6) becomes redundant as it already follows from \(v_{1,1} > l_{1,1} - c_{1,1}\).

As banks’ objective functions are not quasi-concave, we cannot refer to established existence theorems. The non-quasiconcavity of the objective function makes the proof of the existence of the Nash equilibrium more complex. However, the chosen objective function simplifies the empirical implementation since it builds on a modified version of a widely used empirical measure of market liquidity suggested by Amihud [24], which can be easily calibrated based on market data (see also “Implementation” section).

Reports by the German Liquidity Directive complements the LCR data to conduct a long-term study before 2018.

The implicit assumption is that liquidity can quickly be transferred within the same banking group in a stressful period. The assumption could be substantial for large international banks, which conduct worldwide business operations across several jurisdictions. See, for example, the FSB policy document [26] on the ongoing regulatory discussion regarding complexities associated with liquidity in resolution for global systemically important banks.

The reported instrument breakdown for the German Liquidity Directive differs. We construct the following asset classes using the national liquidity regulation: bonds, covered bonds, money market papers, equities and collateral eligible for refinancing at central banks.

For instance, it is typically assumed that retail deposits are more stable than deposits of other commercial banks in a stress period and hence attract a smaller weight. An analogous approach applies to the inflows a bank expects, such as repayments on interest and principal made by non-financial customers.

Deposits include sight deposits held by retail investors, some of which are subject to deposit insurance and are, therefore, less run-prone.

In contrast, according to the LCR the amount of inflows that can offset outflows is capped at 75% of total expected cash outflows. This requires that a bank maintains a minimum amount of stock of HQLA equal to 25% of the total cash outflows.

We confirmed the robustness of our results by a distribution of net outflows over 30 days skewed to the right, where most outflows occur during the first few days of financial stress.

MTS is one of Europe’s leading electronic fixed-income trading markets and a significant fraction of Italian government bonds is said to be traded via this market. Italy was one of the countries most affected by the European Sovereign debt crisis.

Due to high computational effort and insufficient data granularity that prevents us from applying price impact ratios on an individual security basis, we have to aggregate assets and assign common price impact ratios to each asset class. The choice to aggregate assets implies that all assets within one class correlate equally to one. This assumption tends to overestimate the simulated distress sale losses. However, the imprecision should not be very large. First, banks’ largest security class is “government bonds”, which primarily consists of only one asset, namely “Bundesanleihen” (Bunds). Second, in times of severe market liquidity stress, downwards price pressure is often exerted simultaneously on different securities, i.e. correlations are usually high in a liquidity crisis.

Having said that, we do not wholly disregard central banks. Banks’ reserves with the central bank have become an important part of banks’ liquidity buffers. As central banks worldwide have adopted extraordinary monetary policy measures in recent years, their decisions and actions have implications for the data we use in our paper applications (see “Applications” section).

Additionally, distinguishing between liquidity and solvency problems might be challenging in a crisis (see, for example, Thakor [31]).

In Germany, the majority of all repo transactions are traded on the interbank repo market [32, 33]). Some large non-bank financial intermediaries, such as investment funds and insurances, also have access to the repo market and could provide short-term liquidity to the banking system through the repo channel. We leave it for future research to incorporate private repo markets in the analyses.

Liquidity regulation requires banks to hold a certain amount of liquid assets to cover their expected net outflows in case of a stress scenario over a certain period, say one month or 30 days. Haircuts (or discounts to account for market risk) are assigned to liquid assets depending on how easily an asset can be expected to raise cash at short notice. The haircuts vary from 0% to 100%. The net outflows are the difference between cash outflows and cash inflows a bank faces. Outflows are derived from the bank’s liabilities and weighted depending on their rollover risk and run risk.

After the GFC, liquidity requirements for banks were substantially revised and harmonised, resulting in the Basel III regulatory standard. The LCR was introduced into European law for the first time by the CRR. For details on further regulatory reforms, such as the CRR II and the CRR III, and their impact on banks, see Neisen and Schulte-Mattler [34, 35] and [36].

Equivalently, they are subject to a haircut of 0% if their risk weight for credit risk is also 0% under the Basel Capital Adequacy Rules.

As the stock of covered bonds has almost halved between December 2019 to December 2021, the simulated selling volume and the downwards pressure on market prices has reduced respectively. This explains why the losses due to distress sales are higher than the LCR haircut in December 2019, but lower in December 2021.

We are aware that our model does not capture the entire financial system. Rather it represents the sales of the banking system during a liquidity crisis. The price drops for covered and sovereign bonds should be quite accurate given the large holdings of the banking system in these segments. The share of government bonds held by German banks in the amount of all German government bonds outstanding has been around 15% for the past decade and recently declined to 12%. As this market share is not negligible, considerable price reactions are to be expected if many banks were to sell government bonds at the same time. The price movements determined for the other asset classes with smaller portfolios held by banks might be slightly upwardly biased. Nevertheless, since the volumes of securities that need to be sold properly reflect the banks’ funding needs in a crisis scenario, our statements regarding the strategic interaction of banks and the numeric results should represent good proxies.

In addition, we examine the SLB when contractual deposit outflows are used. In this case, the scenario becomes even more severe and the SLB aggregated across all banks becomes negative (EUR \(-\)1.200 bn). This result shows that the treatment of deposit outflows can greatly impact any liquidity analysis.

It is necessary to add, however, that in a crisis, government bonds may be subject to flight-to-liquidity effects as a result of increased demand by institutional investors, which could dampen the price declines shown here if these effects are not fully captured in the price impact parameter [37, 38].

For an overview of the role of the US dollar and risks from US dollar funding in the international financial system after the GFC, see report by the BIS [39].

Note that a simplification had to be considered. The analysis assumes that banks only use liquid assets in US dollars to deal with the funding shock. In practice, banks can issue additional debt in euros, and then transform these funds into US dollars by using FX swaps. Similarly, they can use existing Euro cash to buy US dollars on the spot market. Incorporating these features into the model requires additional assumptions on the nature of the EUR/USD swap market or the evolution of the EUR/USD spot rate. We leave these extensions for future work.

Notice that this combined shock is adopted in a pure ad hoc fashion. We do not claim that rising interest rates may cause a run on the banking system or vice versa. Furthermore, we neither model the effect of a rise in interest rates on the value or composition of banks’ liabilities, nor consider income-related effects on capital.

We focus on bond issuances by the following countries: Austria, Germany, Spain, France, Greece, Great Britain, Italy, Portugal and the US.

In June 2020, systemically relevant institutions held government bonds with a market value of EUR 256 bn. Smaller institutions (less significant institutions) had a bond portfolio with a market value of EUR 197 bn.

From the policy perspective, the question arises of whether regulators should consider a (possibly time-varying) add-on to the current regulatory measures such as the LCR or whether other complementary instruments are needed to address systemic liquidity risk adequately [40]. This issue is currently being discussed in different regulatory forums [8].

In our applications introduced below, one abort criterion is always satisfied during the iteration process. Our simulations have demonstrated that the more complex the application becomes in terms of a longer shock period or a larger number of banks, the more likely it is that the first criterion is not fulfilled, but the second criterion is.

One might argue that the chosen assumption reflects a non-realistic extreme scenario. Another possible alternative could be to allow illiquid banks more time to liquidate their assets, e.g. for illiquid banks their optimisation problem should be applied without the non-negative constraints. It would ensure that these banks can still minimise losses during the distress sale spiral (and therefore would act according to the interests of the banks’ investors). However, this alternative may eventually lead to stark, perverse effects on the SLB. Specifically, illiquid banks would “contribute” to a higher SLB than liquid banks. In other words, the space of feasible selling strategies for liquid banks is bound by constraints which induce those banks to sell securities earlier in the distress sale spiral than they otherwise would and exacerbate the market price decline. Instead, the behavioural assumption we choose ensures that illiquid banks will tend to decrease the SLB relative to liquid banks further.

References

International Monetary Fund. 2011. How to Address the Systemic Part of Liquidity Risk. Global Financial Stability Report, Chapter 2.

Gatev, E., T. Schuermann, and P.E. Strahan. 2007. How do banks manage liquidity risk? Evidence from the equity and deposit markets in the fall of 1988. In The risks of financial institutions. Ch. 3, ed. M. Carey and R.M. Stulz, 105–132. University of Chicago Press.

Correa, R., H. Sapriza, and A. Zlate. 2016. Liquidity shocks, dollar funding costs, and the bank lending channel during the European sovereign debt crisis. September.

Basel Committee on Banking Supervision. 2013. Basel III: The liquidity coverage ratio and liquidity risk monitoring tools. vol. January 2013.

Fischer, R., and H. Schulte-Mattler. 2023. Kommentar zu Kreditwesengesetz, VO (EU) Nr. 575/2013 (CRR) und Ausführungsvorschriften. C.H.BECK, 2023.

European Central Bank. 2019. ECB Sensitivity analysis of Liquidity Risk - Stress Test 2019. Banking Supervision - Methodological note.

Cont, R., A. Kotlicki, and L. Valderrama. 2020. Liquidity at risk: Joint stress testing of solvency and liquidity. IMF Working Paper WP/20/82.

European Central Bank Task Force on Systemic Liquidity. 2018. Systemic liquidity concept, measurement and macroprudential instruments. Occasional Paper Series, vol. 214/October 2018.

Barnhill, T., and L. Schumacher. 2011. Modeling Correlated Systemic Liquidity and Solvency Risks in a Financial Environment with Incomplete Information. IMF Working Paper, vol. 11/263.

Brunnermeier, M., G. Gorton, and A. Krishnamurthy. 2014. Liquidity mismatch measurement. In Risk Topography: Systemic Risk and Macro Modeling. Ch. 7, ed. M. Brunnermeier and A. Krishnamurthy, 99–112. University of Chicago Press.

Drehmann, M., and K. Nikolaou. 2009. Funding Liquidity Risk: Definition and Measurement. ECB Working Paper Series, vol. March, No. 1024.

Nikolaou, K. 2009. Liquidity (Risk) Concepts: Definitions and Interactions. ECB Working Paper Series, vol. February, No. 1008.

Neisen, M., and H. Schulte-Mattler. 2021. The effectiveness of IFRS 9 transitional provisions in limiting the potential impact of COVID-19 on banks. Journal of Banking Regulation 22(4): 342.

Gertler, M., N. Kiyotaki, and A. Prestipino. 2020. A macroeconomic model with financial panics. Review of Economic Studies 87: 240–288.

Uhlig, H. 2010. A model of a systemic bank run. Journal of Monetary Economics 57: 78–96.

Diamond, D.W., and P.H. Dybvig. 1983. Bank runs, deposit insurance, and liquidity. Journal of Political Economy 91(3): 401–419.

Brunnermeier, M.K., and L.H. Pedersen. 2009. Market liquidity and funding liquidity. Review of Financial Studies 22(6): 2201–2238.

Macchiavelli, M., and X. Zhou. 2022. Funding liquidity and market liquidity: The broker–dealer perspective. Management Science 68(5): 3379–3398.

Greenwood, R., A. Landier, and D. Thesmar. 2015. Vulnerable banks. Journal of Financial Economics 115: 471–485.

Cifuentes, R., G. Ferrucci, and H.S. Shin. 2005. Liquidity risk and contagion. Journal of the European Economic Association 3(2/3): 556–566.

Bernardo, A., and I. Welch. 2004. Liquidity and financial market runs. Quarterly Journal of Economics 119: 135–158.

Oehmke, M. 2014. Liquidating illiquid collateral. Journal of Economic Theory 149: 183–210.

Morris, S., and H.S. Shin. 2004. Liquidity black holes. Review of Finance 8: 1–18.

Amihud, Y. 2002. Illiquidity and stock returns: Cross-section and time-series effects. Journal of Financial Markets 5(1): 31–56.

Krüger, U., C. Roling, L. Silbermann, and L.-H. Wong. 2022. Bank’s strategic interaction, adverse price dynamics and systemic liquidity risk. Bundesbank Discussion Paper No. 6/2022.

Financial Stability Board. 2018. Funding strategy elements of an implementable resolution plan. FSB Policy Document.

Feldhütter, P. 2012. The same bond at different prices: Identifying search frictions and selling pressures. Review of Financial Studies 25: 1155–1206.

Dick-Nielsen, J., P. Feldhütter, and D. Lando. 2012. Corporate bond liquidity before and after the onset of the subprime crisis. The Journal of Financial Stability 103: 471–492.

Ellul, A., C. Jotikasthira, and C. Lundblad. 2011. Regulatory pressure and fire sales in the corporate bond market. Journal of Financial Economics 101: 596–620.

Bagehot, W. 1873. Lombard Street, a Description of the Money Market. Henry S. King.

Thakor, A.V. 2015. The financial crisis of 2007–2009: Why did it happen and what did we learn? The Review of Corporate Finance Studies 4(2): 155–205.

ECB. 2017. Financial stability review. Financial Stability Review, November.

ICMA. 2021. European repo market survey. European Repo Market Survey, vol. Number 40, March.

Neisen, M., and H. Schulte-Mattler. 2022. CRR III implementation: Impact on capital requirements, performance and business models of European banks. Journal of Risk Management in Financial Institutions 15(4): 338.

Neisen, M., and H. Schulte-Mattler. 2020. A comprehensive synopsis of the first European step towards implementing Basel IV (Part I). Journal of Risk Management in Financial Institutions 13(2): 114.

Neisen, M., and H. Schulte-Mattler. 2020. A comprehensive synopsis of the first European step towards implementing Basel IV (Part II). Journal of Risk Management in Financial Institutions 13(3): 224.

Santis, R.A.D. 2014. The euro area sovereign debt crisis: Identifying flight-to-liquidity and the spillover mechanisms. Journal of Empirical Finance 26: 150–170.

Beber, A., M.W. Brandt, and K.A. Kavajecz. 2008. Flight-to-quality or flight-to-liquidity? Evidence from the Euro-area bond market. The Review of Financial Studies 22(3): 925–957.

Bank For International Settlements. 2020. US dollar funding: an international perspective. CGFS Papers, No 65, June.

European Systemic Risk Board. 2014. The ESRB handbook on operationalising macro-prudential policy in the banking sector.

Pérignon, C., D. Thesmar, and G. Vuillemey. 2018. Wholesale funding dry-ups. Journal of Financial Economics 73(2): 575–617.

Brunnermeier, M.K., and L.H. Pedersen. 2005. Predatory trading. Journal of Finance 60(4): 1825.

Van den End, J.W., and M. Tabbae. 2012. When liquidity risk becomes a systemic issue: Empirical evidence of bank behaviour. The Journal of Financial Stability 8: 107–120.

Caccioli, F., G. Ferrara, and A. Ramadiah. 2021. Modelling fire sale contagion across banks and non-banks. Bank of England Staff Working Paper

Deutsche Bundesbank. 2020. Financial Stability Review. October.

Acknowledgments

The authors thank Valeriya Arnold, Sabrina Baier, Marvin Borsch, Markus Brunnermeier, Sébastien Dereeper, Gerardo Ferrara, Alexandros Gilch, David Guio Rodriguez, Natalie Kessler, Henry Penikas, Alexander Schmidt, Hermann Schulte-Mattler, Simon Schwab, participants of the World Finance Banking Symposium 2022 in Miami organised by the Florida International University, participants of the 10th International Conference “Financial Engineering and Banking Society” in 2021, organised by the Université de Lille, participants of the 37th Symposium on Money, Banking and Finance in 2021 organised by the Banque de France, participants of the Joint CNB/ECB/ESRB Workshop “Sources of structural systemic risk in the financial system: identification and measurement” 2019 in Prague, participants of the CCBS Workshop “Managing liquidity and funding risk” 2019 at the Bank of England in London, participants of the CCBS Workshop “Systemic risk assessment: identification and monitoring” 2019 at the Bank of England in London and seminar participants at the Bundesbank for helpful comments. The article represents the authors’ personal opinions and does not necessarily reflect the views of the Deutsche Bundesbank or its staff. On behalf of all authors, the corresponding author states that there is no conflict of interest.

Funding

Open Access funding enabled and organized by Projekt DEAL.

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note