Abstract

This paper uses a Markov regime-switching model to assess the vulnerability of a series of Central and Eastern European countries (ie Czech Republic, Hungary, Slovak Republic) and two CIS countries (ie, Russia and Ukraine) during the period 1993–2004. For the new EU member states in Central and Eastern Europe, the results of our model show that the majority of crises in those countries can be explained by inconsistencies in the domestic policy mix and by the deterioration of macroeconomic fundamentals, as emphasised by first-generation crises models, while for the CIS countries analysed, financial vulnerability type indicators were the most relevant, that is, indicators connected with the second- and third-generation of crisis model better explain the vulnerability of these countries. Additionally, the set of indicators chosen by our model is rather heterogeneous, supporting the superiority of a country-by-country approach.

Similar content being viewed by others

Notes

The IMF's EWS is described in Berg et al. (1999).

As explained later in the paper, from the group of Central and Eastern European countries we excluded Poland, because of data availability. Other countries from the region (ie, the Baltics, Belarus, and Bulgaria) were excluded due to the lack of open crisis during the period of data availability.

For a comprehensive review of the theoretical literature for the first- and second-generation crises models, see Blackburn and Sola (1993), Flood and Marion (1999) and Jeanne (2000).

What triggers the jump between multiple equilibria remains largely unexplained. Possible explanations are contagion effects or herding behaviour in the presence of imperfect information, see Masson (1999).

Kaminsky and Reinhart (1996, 1999) pioneered the empirical work on twin crises. They found empirical evidence that banking crises tend to precede currency crises, but the causal link is not unidirectional since the currency crisis deepens the banking crisis.

For an extensive survey of the empirical literature, see for example Kaminsky et al. (1998) and Abiad (2003).

Kaminsky (1998) presents a method to combine individual indicators into a composite indicator.

In addition to the studies mentioned, Alvarez-Plata and Schrooten (2003), Jeanne and Masson (2000) and Fratzscher (1999) use Markov-switching models with constant transition probabilities to model the switches between multiple equilibria leading to currency crises.

At a cut-off probability of 50%, the model correctly calls 65% of pre-crisis periods, whereby 27% of total alarm signals are false.

The model correctly calls approximately 70% of pre-crisis periods at a cut-off probability of 40%.

Diebold et al. (1993) extended the baseline Hamilton (1989) regime-switching model to allow for time-varying transition probabilities.

Here, it is assumed that the indicators that influence the crisis probability neither worsen nor improve during this period.

Results not presented here, but available from the authors upon request.

Each indicator is standardised to be zero mean and unit variance.

Results not presented here, but available from the authors upon request.

At the beginning of 1997, the estimations for current account deficit to GDP for the whole of 1997 were around 10%, far exceeding the expected inflows of long-term non-debt capital.

Gibson and Tsakalaatos (2004: 577).

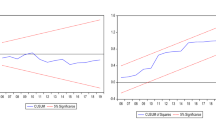

The rate of devaluation in the crawling band regime decreased continuously, from 0.060% of daily devaluation in March 1995 to 0.00654% of daily devaluation in April 2001.

The first base rate increase took place in May, while the second was at the end of November. In both cases, the increase of the base interest rate was 300 basis points.

The estimated costs of the removal of non-performing loans are about 105 billion Slovak crowns (about 12% of the nominal GDP in 1999).

After the break-up of Czechoslovakia and the following monetary separation, both countries pegged their currencies to baskets with relatively narrow oscillation bands (±0.5% from central parity).

During May 2002, the central bank decided to increase interest rates to cool down excessive demand pressures.

The goodness-of-fit values differ somewhat ranging between 88% in Russia to 69% in Hungary for all observations. The results are most homogeneous for calling the tranquil periods, that is, above 80% success rate for all countries.

References

Abiad, A . 2003: Early warning systems: A survey and a regime-switching approach. IMF Working Paper 03/32.

Alvarez-Plata, P and Schrooten, M . 2003: The Argentinean currency crisis: A Markov-switching model estimation. DIW Discussion Paper 348.

Arias, G and Erlandsson, UG . 2004: Regime switching as an alternative early warning system of currency crises – an application to South-East Asia. Department of Economics, Lund University, Scandinavian Working Papers in Economics 11.

Arvai, Z and Vincze, J . 2000: Financial crises in transition countries: Model and facts. National Bank of Hungary, Working Paper 2000/6.

Bakanova, M, Vinhas de Souza, LV, Kolesnikova, I and Abramov, I . 2004: Transition and growth in belarus. In: Ofer, G and Pomfret, R (eds). The economic prospects of the CIS: sources of long-term growth. Edward Elgar Publishing: UK. pp. 57–75.

Berg, A, Borensztein, E, Milesi-Ferretti, GM and Pattillo, C . 1999: Anticipating balance of payments crises: The role of early warning systems. IMF Occasional Paper 186.

Berg, A and Pattillo, C . 1999a: Are currency crises predictable? A test. IMF Staff Papers 46 (2): 107–138.

Berg, A and Pattillo, C . 1999b: Predicting currency crises: The indicators approach and an alternative. Journal of International Money and Finance 18: 561–586.

Blackburn, K and Sola, M . 1993: Speculative currency attacks and balance of payment crises. Journal of Economic Surveys 7 (2): 119–144.

Brüggemann, A and Linne, T . 1999: How good are leading indicators for currency and banking crises in Central and Eastern Europe? An empirical test. IWH Discussion Paper 95.

Brüggemann, A and Linne, T . 2002: Die Bestimmung des Risikopotenzials von Finanzkrisen anhand eines Frühwarnindikatorensystems: Eine Untersuchung der EU-Beitrittskandidatenländer und ausgewählter Staaten Mittel- und Osteuropas Schriften des Instituts für Wirtschaftsforschung Halle, Vol. 13, Nomos Verlagsgesellschaft, Baden-Baden.

Chang, R and Velasco, A . 1998: Financial Crises in Emerging Markets: A Canonical Model. NBER Working Paper 6606.

Corsetti, G, Pesenti, P and Roubini, N . 1998: Paper tigers? A model of the Asian crisis. Internet Version November 2004.

Diebold, FX, Lee, J-H and Weinbach, GC . 1993: Regime switching with time-varying transition probabilities. Federal Reserve Bank of Philadelphia, Working Paper 93-12.

Dooley, MP . 1997: A model of crises in emerging markets. NBER Working Paper 6300.

Eichengreen, B, Rose, AK and Wyplosz, C . 1995: Exchange market mayhem: The antecedents and aftermath of speculative attacks. Economic Policy 21: 249–312.

Esanov, A, Merkl, C and Vinhas de Souza, L . 2005: Monetary policy rules for Russia. Journal of Comparative Economics 33 (3): 484–499.

Flood, R and Garber, P . 1984: Collapsing exchange rate regimes: Some linear examples. Journal of International Economics 17: 1–13.

Flood, R and Marion, N . 1999: Perspectives on the recent currency crisis literature. International Journal of Finance and Economics 4 (1): 1–26.

Frankel, JA and Rose, AK . 1996: Currency crashes in emerging markets: An empirical treatment. Journal of International Economics 41: 351–366.

Fratzscher, M . 1999: What causes currency crises: sunspots, contagion or fundamentals? EIU Working Paper 99/39.

Gibson, H and Tsakalaatos, E . 2004: Capital flows and speculative attacks in prospective EU member states. Economics of Transition 12 (3): 559–586.

Goldfajn, I and Valdés, RO . 1997: Capital flows and the twin crises: The role of liquidity. IMF Working Paper 97/87.

Hamilton, JD . 1989: A new approach to the economic analysis of nonstationary time series and the business cycle. Econometrica 57: 357–384.

Hamilton, JD . 1994: Time series analysis. Princeton University Press: New Jersey.

Jeanne, O . 2000: Currency crises: A perspective on recent theoretical developments. Special Papers in International Economics, Department of Economics, Princeton University, Princeton, New Jersey.

Jeanne, O and Masson, P . 2000: Currency crises, sunspots and markov-switching regimes. Journal of International Economics 50 (2): 327–350.

Kaminsky, GL . 1998: Currency and banking crises: The early warnings of distress, Board of Governors of the Federal Reserve System, International Finance Discussion Papers 629.

Kaminsky, GL, Lizondo, S and Reinhart, CM . 1998: Leading indicators of currency crises. IMF Staff Papers 45 (1): 1–48.

Kaminsky, GL and Reinhart, CM . 1996: The twin crises: The causes of banking and balance-of-payments problems. Board of Governors of the Federal Reserve System, International Finance Discussion Papers 544.

Kaminsky, GL and Reinhart, CM . 1999: The twin crises: The causes of banking and balance-of-payments problems. The American Economic Review 89 (3): 473–500.

Krugman, P . 1979: A model of balance-of-payments crises. Journal of Money, Credit and Banking 11 (3): 311–325.

Krugman, P . 1996: Are currency crises self-fulfilling? NBER macroeconomics annual. The MIT Press: Cambridge, pp. 345–406.

Krugman, P . 1998: What happened to Asia? November 2004.

Martinez-Peria, MS . 2002: A regime-switching approach to the study of speculative attacks: A Focus on EMS crises. Empirical Economics 27 (2): 299–334.

Masson, P . 1999: Multiple equilibria, contagion, and the emerging market crises. IMF Working Paper 99/164.

McKinnon, RI and Pill, H . 1997: Credible economic liberalizations and overborrowing. The American Economic Review 87 (2): 189–193.

Obstfeld, M . 1986: Rational and self-fulfilling balance-of-payment crises. The American Economic Review 76 (1): 72–81.

Obstfeld, M . 1994: The logic of currency crises. NBER Working Paper 4640.

Obstfeld, M . 1996: Models of currency crises with self-fulfilling features. European Economic Review 40: 1037–1047.

Radelet, S and Sachs, J . 1998: The onset of the east Asian financial crisis Harvard Institute for International Development, November 2004.

Rosenberg, MR . 1998: Currency crises in emerging markets: A guide to speculative-attack models and early warning systems. Merrill Lynch, International Fixed Income Research: New York.

Salant, S and Henderson, D . 1978: Market anticipation of government policy and the price of gold. Journal of Political Economy 86: 627–648.

Vinhas de Souza, LM and Havrylyshyn, O . 2006: Return to growth in CIS countries and the macroeconomic framework. Springer: Germany (forthcoming).

Vinhas de Souza, LM, Schweickert, R, Movchan, V, Bilan, O and Burakovsky, I . 2005: Now so near, and yet still so far: Economic relations between Ukraine and the European Union. Institute for World Economics, Kiel Discussion Paper 419. Kiel.

Author information

Authors and Affiliations

Additional information

The views expressed here are exclusively those of the authors and do not necessarily reflect the official views of their institutions. All usual disclaimers apply.

Rights and permissions

About this article

Cite this article

Kittelmann, K., Tirpak, M., Schweickert, R. et al. From Transition Crises to Macroeconomic Stability? Lessons from a Crises Early Warning System for Eastern European and CIS Countries. Comp Econ Stud 48, 410–434 (2006). https://doi.org/10.1057/palgrave.ces.8100162

Published:

Issue Date:

DOI: https://doi.org/10.1057/palgrave.ces.8100162