Abstract

In this paper, we introduce a bivariate extension of three-parameter generalized crack distribution for modelling loss data. Some basic properties such as the conditional distribution and the measures of association are discussed, and a method of parameter estimation is offered. A simulation-based approach to compute bivariate value-at-risk under the model is also discussed. The proposed model and estimation method are illustrated with a model fitting exercise on a real catastrophic loss data set.

Similar content being viewed by others

Notes

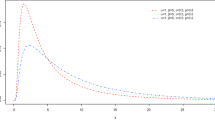

A brief review on the Birnbaum–Saunders, Gaussian crack and generalized crack distributions are given in Sect. 2.

Here we drop the parameters in the expressions for the sake of notational ease.

The computation of the coefficient of upper tail dependence is given in Appendix.

If \(F(x_1, \cdots ,x_d)\) is partially increasing on \(\mathbf {R}^d_+ /(0,\cdots ,0)\) and \(\text{ E }(X_i) < \infty\), for \(i = 1, \cdots , d\). More details can be found on Cousin & Bernardino (2013). Note that the BVGCR models satisfies the regularity conditions provided that the second raw moment of the base distribution exists.

Relying on the fact that the sample median is more robust than the sample mean, one may consider an alternative definition of multivariate VaR based on the conditional median. We do not pursue such approach in this paper since the theoretical properties of the alternative definition are yet to be studied.

Data source: public.emdat.be.

We use the R-function ‘decompose’ for the decomposition of time series.

This issue is expected to be alleviated if the size of simulations is increased with a larger computational cost.

References

Bae, T., & Chen, J. (2017). On heavy-tailed crack distribution for loss severity modeling. International Journal of Statistics and Probability, 6, 92–110.

Bingham, N. H., Goldie, C. M., & Teugels, J. L. (1987). Regular Variation. Cambridge University Press.

Birnbaum, Z. W., & Saunders, S. C. (1969). Estimation for a family of life distributions with applications to fatigue. Journal of Applied Probability, 6, 328–347.

Birnbaum, Z. W., & Saunders, S. C. (1969). A new family of life distributions. Journal of Applied Probability, 6, 319–327.

Cousin, A., & Bernardino, E. D. (2013). On multivariate extensions of value-at-risk. Journal of Multivariate Analysis, 119, 32–46.

Daniels, H. E. (1950). Rank correlation and population models. Journal of the Royal Statistical Society: Series B (Methodological), 12, 171–181.

Dempster, A., Laird, N., & Rubin, D. (1977). Maximum likelihood from in complete data via the EM algorithm. Journal of the Royal Statistical Society: Series B (Methodological), 39, 1–38.

Diáz-Garciá, J. A., & Leiva-Sánchez, V. (2005). A new family of life distributions based on the elliptically contoured distributions. Journal of Statistical Planning and Inference, 128, 445–457.

Durbin, J., & Stuart, A. (1951). Inversions and rank correlation coefficients. Journal of the Royal Statistical Society: Series B (Methodological), 13, 303–309.

Embrechts, P., Klüppelberg, C., & Mikosch, T. (1997). Modelling Extremal Events for Insurance and Finance. Berlin: Springer-Verlag.

Embrechts, P., & Puccetti, G. (2006). Bounds for functions of dependent risks. Finance and Stochastics, 10, 341–352.

Fredricks, G. A., & Nelson, R. B. (2007). On the relationship between spearman’s rho and kendall’s tau for pairs of continuous random variables. Journal of Statistical Planning and Inference, 137, 2143–2150.

Gupta, R., & Kirmani, S. N. V. A. (1990). The role of weighted distribution in stochastic modeling. Communications in Statistics-Theory and Methods, 19, 3147–3162.

Nappo, G., & Spizzichino, F. (2009). Kendall distributions and level sets in bivariate exchangeable survival models. Information Sciences, 179, 2878–2890.

Schreyer, M., Paulin, R., & Trutschnig, W. (2017). On the exact region determined by kendall’s \(\tau\) and spearman’s \(\rho\). Journal of the Royal Statistical Society: Series B (Methodological), 79, 613–633.

Volodin, I., & Dzhungurova, O. (2000). On limit distributions emerging in the generalized birnbaum-saunders model. Journal of Mathematical Sciences, 99, 1348–1366.

Acknowledgements

The authors are grateful to the anonymous reviewers for valuable comments and suggestions. T. Bae is supported by the Discovery Development Grant program (DDG-2019-06064) of the Natural Science and Engineering Research Council of Canada (NSERC).

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

The authors declare that they have no conflict of interest.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Appendix

Appendix

1.1 Proof of Proposition 1

For notational convenience, we drop parameters in the argument of functions, and write \(\bar{G}(\cdot ) = 1 - G(\cdot )\) and \(b(t_i) = \alpha _i^{-1}\left( \sqrt{\beta _i/t_i}- \sqrt{t_i/\beta _i}\right) ,\, i = 1, 2\).

By (10), the joint distribution of \((T_1, T_2)\) having \(\text {BVGCR}(\varvec{\alpha },\varvec{\beta },\varvec{p};g)\) is

and the marginal density of \(T_i, \, i =1, 2\), is

where \(p_1 = p_{11}+p_{12}\), \(p_2 = p_{11}+p_{21}\), \(q_i = 1-p_i\), \(i =1,2\). By expanding the integrand in (12) using these expressions and taking the double integration, we have

where, for each \(i = 1,2\),

That is, the evaluation of the double integral in (12) reduces to that of the following two integrals: \(\int _0^{\infty } H(t)f_{IS}(t) dt\) and \(\int _0^{\infty } H(t)f_{LB}(t) dt\). Due to the expression \(F_{IS}(t) = 1- G(b(t)) + H(t)\) and

and changing the order of integrations, we obtain

Similarly, due to the expression \(F_{LB}(t) = 1- G(b(t)) - H(t)\), we obtain

Combining these results and some simplifications give the expression (13).

1.2 Proof of Proposition 2

As in the proof of Proposition 1, expanding the integrand in (14) using the joint cdf and pdf of the BVGCR and taking double integrals give

With the results derived in the proof of Proposition 1, i.e., \(\text{ E }[F_{S_i}(S_i)] = \text{ E }[F_{V_i}(V_i)] = 1/2\), \(\eta _i = 1/2 + 2 \gamma _i\), and \(\zeta _i = 1/2 - 2 \gamma _i\) for each \(i = 1,2\), and after some simplification, the above integral can be expressed as

which gives the desired expression (15) for Kendall’s tau.

1.3 Calculation of the coefficient of upper tail dependence

The following gives the calculation of coefficient of upper tail dependence under the GVGCR distribution. Specifically, the upper tail dependence is measured by the coefficient \(\lambda\) defined as

where \(F_1(\cdot )\) and \(F_2(\cdot )\) are the marginal cdfs of \(T_1\) and \(T_2\), respectively. By the expressions (5) and (6), the numerator in (20) can be written as follows:

where \(b_i(t) = \alpha _i^{-1}\left( \sqrt{\beta _i/t}-\sqrt{t/\beta _i}\right)\), \(i = 1, 2\). Direct applications of L’hopital’s rule give

where \(q_1 = 1- p_1 = p_{21} + p_{22}\) and \(q_2 = 1- p_2 = p_{12} + p_{22}\). Using these and \(\lim _{u\rightarrow 1}G(b_i(F^{-1}_i(u))) = \lim _{u\rightarrow 1}H(F^{-1}_i(u)) = 0\), we can easily show

Rights and permissions

About this article

Cite this article

Bae, T., Choi, Y.H. A bivariate extension of three-parameter generalized crack distribution for loss severity modelling. J. Korean Stat. Soc. 51, 378–402 (2022). https://doi.org/10.1007/s42952-021-00144-2

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s42952-021-00144-2