Abstract

A negative correlation between forecast errors of the price level and real output is evidence that prices are countercyclical and so evidence for the dominance of supply shocks. We examine the correlation between the forecast errors of real GDP and its deflator for six OECD countries. With the exceptions of the United Kingdom and the United States, previous research used errors from an Index of Industrial Production and the Consumer Price Index. Using real GDP and the GDP deflator, the patterns of correlations over forecast horizons for Canada, France, Italy, and Japan do not match closely with that of either the UK or the US. Using a longer sample than previous studies we find evidence that the correlations are greater and often positive after 1981 indicating diminished dominance of supply shocks. This decrease is associated with decreases in both the relative frequency and relative size of the negative products of the forecast errors.

Similar content being viewed by others

Notes

Mills (1927 and 1946) and Burns and Mitchell (1946) found evidence that the prices of many commodities tended to rise during expansions and fall during recessions. Kydland and Prescott (1990) and Cooley and Ohanian (1991) find a positive correlation between detrended values of price and output. Rottemberg (1996) and Davis and Kanago (2002) look at the correlation between forecast errors but only at a horizon of one.

The corresponding author will provide a spreadsheet with the products of the forecast errors for all horizons and all countries upon request.

A reviewer suggested also looking at 2008 as a breakpoint because at about that time central banks moved policy rates towards and kept them at or near the zero lower bound for some time. However, given quarterly data a break at a date this close to the end of the sample leaves a small number of forecast errors for computing correlations. If the sample used to make forecasts begins in 2008, the number of forecast errors diminishes as the time horizon rises as errors at longer forecast horizons would not be available at the start of the sample.

References

Burns, A. F., & Mitchell, W. C. (1946). Measuring Business Cycles. National Bureau of Economic Research.

Cassou, S. P., & Vázquez, J. (2014). Small-scale New Keynesian Model Features that Can Reproduce Lead, Lag And Persistence Patterns. The BE Journal of Macroeconomics, 14(1), 267–300.

Cooley, T. F., & Ohanian, L. E. (1991). The Cyclical Behavior of Prices. Journal of Monetary Economics, 28(1), 25–60.

Davis, G. K., & Kanago, B. E. (2002). The Contemporaneous Correlation Between Price Shocks and Output Shocks. Applied Economics, 34(18), 2333–2339.

Davis, G. K., & Kanago, B. E. (2008). The Cyclical Behavior of Prices and Relative Prices. Economic Inquiry, 46(4), 576–586.

Den Haan, W. J. (2000). The Comovement Between Output and Prices. Journal of Monetary Economics, 46(1), 3–30.

Den Haan, W. J., & Sumner, S. W. (2004). The Comovement Between Real Activity and Prices in The G7. European Economic Review, 48(6), 1333–1347.

Hall, T. E. (1995). Price Cyclicality in the Natural Rate-Nominal Demand Shock Model. Journal of Macroeconomics, 17(2), 257–272.

Judd, J. P., & Bharat, T. (1995). The Cyclical Behavior of Prices: Interpreting the Evidence. Journal of Money, Credit, and Banking, 27(3), 789–797.

Kydland, F. E., & Prescott, E. C. (1990). Business Cycles: Real Facts and a Monetary Myth. Federal Reserve Bank of Minneapolis Quarterly Review, 14(2), 3–18.

María-Dolores, R., & Vázquez, J. (2008). The New Keynesian Monetary Model: Does it Show the Comovement Between GDP and Inflation In The US? Journal of Economic Dynamics and Control, 32(5), 1466–1488.

Mills, F. C. (1927). The Behavior of Prices. National Bureau of Economic Research.

Mills, F. C. (1946). Price-Quantity Interactions in the Business Cycle. National Bureau of Economic Research.

Rotemberg, J. J. (1996). Prices, Output, and Hours: An Empirical Analysis Based on a Sticky Price Model. Journal of Monetary Economics, 37(3), 505–533.

Schreft, S. L. (1990). Credit Controls: 1980. FRB Richmond Economic Review, 76(6), 25–55.

Stock, J. H., & Watson, M. W. (2002). Has the Business Cycle Changed and Why? NBER Macroeconomics Annual, 17, 159–218.

Summers, P. M. (2005). What Caused the Great Moderation? Some Cross-Country Evidence. Economic Review-Federal Reserve Bank of Kansas City, 90(3), 5.

Vázquez, J. (2002). The Co-Movement Between Output and Prices in the EU15 Countries: An Empirical Investigation. Applied Economics Letters, 9(14), 957–966.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

The author declares he has no conflict of interest.

Human Participants or Animals

The author declares that this study did not involve participation of human participants or animals.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Appendix: A Results for Bivariate VAR Models

Appendix: A Results for Bivariate VAR Models

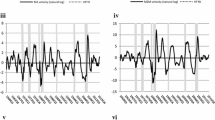

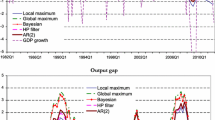

See Figs.

Correlations from bivariate VAR for Canada

19,

Correlations from bivariate VAR model for France

20,

Correlations from bivariate VAR model for Italy

21,

Correlations from bivariate VAR model for Japan

22,

Correlations from bivariate VAR model for UK

23,

Correlations from bivariate VAR model for US

24.

Rights and permissions

Springer Nature or its licensor (e.g. a society or other partner) holds exclusive rights to this article under a publishing agreement with the author(s) or other rightsholder(s); author self-archiving of the accepted manuscript version of this article is solely governed by the terms of such publishing agreement and applicable law.

About this article

Cite this article

Kanago, B. The Comovement Between Forecast Errors for Real GDP and Its Deflator in Six OECD Countries: Did Supply Shocks Become Less Dominant During the Great Moderation?. J Bus Cycle Res 19, 149–169 (2023). https://doi.org/10.1007/s41549-023-00086-0

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s41549-023-00086-0