Abstract

Purpose of Review

Climate change poses a threat to European forests and threatens their capacity to deliver ecosystem services. Innovation is often considered critical to increasing resilience in wood-based value chains. However, the knowledge about types of innovation processes and how they enhance resilience, if at all, is largely dispersed. In this conceptual paper, we refer to examples from the forestry, bioeconomy, adaptation, and innovation literature to develop an overview of innovation pathways along the wood value chain. Thereafter, we evaluate the extent to which they enhance or compromise resilience to climate change and how they do so.

Recent Findings

We differentiate between forest and value chain resilience and assume that innovation positively influences both types of resilience via three resilience drivers: diversifying the product portfolio, making operations more efficient, or making the processes more flexible. Our literature review revealed nine innovation pathways along the value chain.

Summary

The pathways rarely connect forest management and the processing industry. Consequently, a mismatch was identified between the innovation pathways and resilience drivers applied to increase diversification at the beginning of the value chain (in forest management) and those applied to increase efficiency towards the end of the value chain (in the processing industry). Considering this mismatch, we stress that it is critical to reconsider the term innovation as a silver bullet and to increase the awareness of resilience drivers and innovation pathways, as well as reconsider ways to combine them optimally. We recommend engaging in open innovation activities to cooperatively draft innovation strategies across the entire wood value chain and intercept pathways by making processes more flexible.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

Introduction

European forests are critical to the European environment, economy, and society [1]. Climate change poses a growing threat to European forests due to the increasing frequency and severity of heat waves, extended periods of drought, storms, wildfires, and other natural disturbances that affect forests on an increasingly large scale. As a result, forest ecosystem dynamics, forest resilience, and tree species suitability are being altered at best and most likely negatively impacted [2]. As climate change continues, forest managers have to cope with both short-term and long-term impacts on the stability of forests and their capacity to deliver ecosystem services [3•]. As an indication, extreme disturbance events occurring over the last decade [4] have challenged the forest-based sector by causing unpredictable wood flows and reduced wood quality [5].

The concept of resilience has been assigned multiple forms of significance in different disciplines. In the forest sciences, [6••] recognizes a hierarchy of concepts in which engineering resilience refers to the ability of a system to recover after a disturbance [7]; ecological resilience corresponds to the ability of the system to persist, absorbing changes and disturbances and avoiding shifts to alternative states [8]; and socio-ecological resilience addresses the capacity to adapt and reorganize interconnected natural and human systems in response to unexpected shocks or gradual changes [9]. Thus, the term resilience is generally defined as encompassing these concepts and refers to the capacity of a system to absorb disturbances and to recover and reorganize, retaining essentially the same structure, identity, and functions [10,11,12]. This definition includes three components that should be applied to enhance a forest’s (and potentially the value chain’s) capacity to cope with (climate change-induced) disturbances and uncertainties [13••]: resistance, resilience (corresponding to the abovementioned engineering resilience), and adaptive capacity. In this regard, resistance is the ability of an ecosystem to resist external stress, resilience is the ability of an ecosystem to return to its original state after a disturbance, and adaptive capacity relates to the ability of an ecosystem to adapt to climate change and other global changes.

Although some research has been performed on how to enhance the capacity of specific forest ecosystems to cope with climate change (e.g. [3, 14]), few efforts have been made to specifically investigate relationships between adaptive management and the associated value chains. Depending on the type of forest disturbance that occurs, wood-based value chains can be affected by the over- and undersupply of wood, and the wood value chain can shift from applications with higher value (e.g. sawn wood) to those of lower value (e.g. wood for energy production) [15,16,17].

Regarding forest-sector value chains, we can recognise nature- and human-driven subsystems as being connected by ecosystem services that interact with one another. The nature-driven system supplies ecosystem services to the human-driven subsystem, but the human-driven subsystem strongly influences the development of the nature-driven subsystem through policy and management [18]. Thus, the resistance, resilience, and adaptive capacity of a forest rely on the maintenance or improvement of such ecosystem services or their associated value chains. In this context, we define value chain resilience as the ability to deliver and increase the value of ecosystem services as demanded by the human-driven subsystem throughout the value chain, while simultaneously being able to absorb disturbances, and recover and reorganize, retaining essentially the same structure, identity, and functions.

Innovation is seen as a silver bullet that can enhance value chain resilience and is often mentioned in academic papers (e.g. [19,20,21,22]). As an indication, a political vision introduced in the New European Forest Strategy suggests that innovation and new product development have the potential to shift the composition of value chain structure, enabling it to respond to changes in societal demand [23] and to those related to climate change. This vision, which is becoming steadily more broadly accepted, encourages those working in the forest-based sector to develop new management strategies, explore new markets, and develop new business models [24].

It is unclear how much and in which ways, if at all, innovation enhances value chain resilience. Innovation itself is a broad term. If we define innovation as broadly as the authors of [25, 26] do, the term refers to the “generation, acceptance, and implementation of new ideas, processes, products or services”; hence, it would include any climate change adaptation strategy beyond those used in the current operational forest or industry practice.

According to [27••], resilience in ‘low-certain value chains’, which are subject to risks due to unpredictable environmental factors, can be improved by strengthening structural variety (i.e. diversification), parametric redundancy (i.e. efficiency), and process flexibility. First, strengthened structural variety can be enhanced by diversifying the product portfolio and supplier–consumer relationships, while minimising the number of intersections between different suppliers and consumers (e.g. by avoiding sourcing from the same suppliers). Second, value chain processes must become more efficient to reduce parametric redundancy and to ensure that natural, social, human, manufactured, and financing capital are optimally allocated [27••]. Nevertheless, maintaining some redundancy could support resilience, since part of the system that fails can be easily replaced by another [28]. And finally, to strengthen process and resource flexibility, we need to allow resources to be exchanged upstream and downstream of the value chain, and specifically by establishing flexible workstations and decentralised control principles supported by track-and-trace mechanisms. This makes it possible to select short-term stabilisation measures based on a clear understanding of the available capacities and inventories [27••].

In the forest-based sector, it has been argued that diversification in forest management for wood could strengthen engineering resilience and ecological resilience, especially when targeting forests that are evenly aged and contain single species [29,30,31]. This, in turn, could increase the capacity of these forests to cope with climate change-induced disturbances [32, 33]. Expanding forest product portfolios beyond wood production can also contribute to forest income heterogeneity and stability. Job opportunities may be created as new customers and markets are reached [29, 30, 34, 35]. Thereby, diversification will contribute more prominently to ‘inclusive growth’ [36]. Within the value chain, diversifying procurement strategies and processing different types of wood could also lead to more stability [15,16,17].

Regarding efficiency, the pressure on forest resources is decreased when interactions between nature- and human-driven subsystems ensure the optimal allocation of capital [37]. However, increasing the efficiency of the wood harvest could be a dangerous goal. In the past, the advocacy for even-aged pure forests that are easy to be managed led to damage that is not only caused by climatic changes, but also to less resistant and resilient forest structures, which suffer from a low adaptive capacity [38, 39]. Efficiency-enhancing innovations also require a large number of investments to be made in the physical and social infrastructures of forests (e.g. transportation routes, forest partnerships, and knowledge sharing) [40].

To increase the resource flexibility in the forest and the process flexibility in the value chain, resources should be exchanged upstream and downstream and new industry connections should be formed [37]. By optimally shifting wood from higher-value applications to lower-value applications, employment opportunities, export income, and other indicators for economic resilience can improve [41, 42]. In addition, the need for resource flexibility has become evident due to more blurred industrial boundaries and the fact that chemical, energy, and forest-based industries often use the same feedstocks and develop products for the same markets [43].

In the present work, we set out to define innovation pathways that the forest-based sector is adopting or has been recommended to follow by the scientific literature. Thereafter, we assessed various innovation pathways and analogous resilience drivers (diversification, efficiency, and flexibility) along the wood value chain in order to evaluate how much they enhance or compromise (forest and value chain) resilience to climate change and how they do so.

The remainder of this paper is structured as follows: We describe our methodological approach and study design in Sect. 2, present our analytical results in Sect. 3, and discuss these results in light of previous research and the policy implications of the study in Sect. 4. Finally, a short conclusion is provided.

Methods

To determine innovation pathways in the forest-based sector and assess how they contribute or compromise resilience, we must first have a clear overview of the wood value chain (Fig. 1).

In this study, we identified relevant peer-reviewed research articles, limiting the search to articles written in the English language, published between January 2013 and December 2022 in international scientific journals, and indexed in the Scopus abstract and citation database. We performed the same queries in the ScienceDirect database and on the Web of Science platform, which provides access to multiple databases, enabling us to identify additional papers. We set up a recordkeeping and reporting system according to the widely accepted Preferred Reporting Items for Systematic Review and Meta-Analysis Statement (PRISMA) and describe the literature review process and exclusion criteria in a flow diagram [46] (Fig. 2).

Graphical representation of the literature screening process used for the review performed in this study (n = number of papers)

We first conducted a systematic literature review (Fig. 2) to identify innovation pathways.Footnote 1 In total, 89 papers were identified as relevant data sources which enabled us to preliminarily define innovation pathways along the wood value chain. To cluster the themes found in the literature and identify the pathways, we first assigned each paper a position along the value chain. Thereafter, we applied an iterative coding process with multiple rounds to detect similarities and differences among the themes derived from the literature.

Subsequently, a second literature review was carried out as described above by using keywords related to innovation pathways and climate adaptation.Footnote 2 As a result, 37 additional papers were identified that were further used in the analysis. These selected scientific papers were read in detail, continuously referring to the selected three drivers of value chain resilience (diversification, flexibility, and efficiency) in order to determine whether a paper referred to resilience to climate change or to another form of resilience. Finally, not all papers used to classify a pathway were used to describe that pathway in the results section.

Results

Overview of the literature, the pathways, and their resilience drivers

In total, 125 papers were used to define and analyse the innovation pathways, 71 of which referred to climate change (Fig. 3). The analysis of these papers enabled the identification of nine innovation pathways along the value chain (Fig. 4): Innovations supporting mixed structure-rich forestry (1), technology-driven silvicultural innovations (2), innovations strengthening forest recreation (3), innovative payment or ecosystem services (PES) schemes (4), innovations extending the product portfolio beyond wood (5), innovations supporting co-management and joint forest ownership (6), innovations supporting circularity (7), innovations extending the product portfolio with high-value products (8), and innovative approaches to sales and marketing (9). A more in-depth analysis of the literature in each pathway is described in Sects. 3.2–3.10. The literature used to define and analyse each pathway is summarised in the supplementary materials.

Scientific articles used to categorise and analyse the innovation pathways

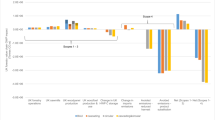

Innovation pathways, indicating their locations along the value chain and their contributions to resilience

Innovations supporting mixed structure-rich forestry

The sample of scientific literature that enabled us to develop this innovation pathway consists of 25 papers, 23 of which were directly related to climate change resilience, while 21 mentioned diversification as a resilience driver. In addition, one paper referred to more flexibility, as the harvest timing in structure-rich forestry can be more flexible [47] (Fig. 3). In this sample, twelve papers build on ecological modelling and forest simulation, seven are literature reviews, five report results of dendrological measurements or other measures in a stand, one consists of stakeholder interviews, and one applies an analytical framework to assess resilience.

The application of mixed structure-rich forestry can be implemented at the beginning of the value chain. In this work, we interpret a mixed forest as a forest dominated by more than one single tree species, which sometimes corresponds to a mixture of broad-leaved and coniferous species and that could include an understorey of shrubs and bushes [39]. Mixed forests often show a heterogeneous structure, where different cohorts and size classes co-exist ensuring regeneration capacity and habitat diversity. The management of mixed forests predominantly emphasises tree species that are well-adapted to the current growing conditions and a changing climate. Mixed forestry also includes dynamic forestry practices, which involve, for instance, successional species rotation and harvest practices.

More stringent silvicultural interventions might be needed to maintain a defined mixture over the whole rotation time [48]. Several tree species may coexist in mature old-growth forests, which show more resilience to warming trends [49]. However, more dominant forest species can tend to suppress others (e.g. due to a long history of selecting fast-growing species and continuous thinning), especially in the early stages of stand development, and gap opening might be required [31, 50]. For example, in a mixture of Norway Spruce and European Beech, the spruce continuously outcompetes (i.e. height) the beech [33]. In addition, birch colonises forest gaps, subsequently increasing soil functioning and biodiversity, but its rapid height growth might also affect the vitality of other forest species [51], especially when the forest is not allowed to grow for long enough until birch is again replaced by other shade-tolerant species.

Although the species diversity and the structural complexity of mixed forests does not always guarantee enhanced resilience, a mixed forest tends to be more resilient under certain conditions. Mixed structure-rich forests made up of a variety of tree species adapted to local environmental conditions or to ongoing climate change are more resilient to disturbances than homogeneous forests due to the complementary ecological performance of species and early stages of tree growth, which support regeneration. The species mixture or uneven-aged structures might enhance the recovery speed, enabling the forest to reach a pre-disturbance state after a severe disturbance [14], while the integration of tree species with rare functional traits could enhance the adaptive capacity of a forest, thus maintaining forest resilience under strongly altered conditions [13••]. Thus, these mixed forests tend to ensure a good spread of risk to climate change and disturbances and promote potential synergies between species [32, 33]. For example, increasing the variability to European Beech stands [52] and Norway Spruce stands [47, 53] increases the resilience of these stands to climate change, while Silver Fir forests benefits from species mixing during drought [54]. Adding broad-leaved species to conifer stands helps them to become more resistant to windthrow and pests [47, 55]. Tree species mixing can also improve the growing conditions of trees, irrespective of disturbances [56]. For example, [57] found that beech trees in mixed stands grew taller and used nutrients more efficiently than mono-specific stands, while [58] found that incorporating a nitrogen-fixing species (e.g. Anadenanthera peregrina) into plantations increased eucalyptus growth there. Other studies have shown that the stem shape and wood quality in the Sessile and Common Oak are improved when stand mixing increases (e.g. by adding European Beech, Hornbeam, or limetree) [59, 60]. Lastly, [61] found that mixing and carefully managing non-native tree species may have climate adaptation benefits. Regarding the introduction of non-native tree species (e.g. introduced Blackwood in Portugal [62]), these should be carefully managed, since introducing non-native species from distant regions could also introduce non-native pests such as fungi and microorganisms and disrupt local food webs [61]. Alternatively, assisted gene flow from populations currently located in gradients, including the projected future climatic conditions, may increase the resilience of mixed forests to climate change [63].

Favouring mixed, structure-rich forests might enhance the forest’s economic resistance [64] and increase the value chain resilience associated to these forests, as they are more flexible to market demand [65], although careful management and interventions are needed. Diversification increases timber returns and reduces timber volume losses experienced under negative environmental conditions such as drought [14, 66] assessed innovative silvicultural strategies linked to resilience and found that shifting from a clear-fell system to continuous cover forestry in Central-European forests enhanced economic resilience. [67] found that adding Douglas Fir to a predominantly spruce forest and adapting the rotation periods compensated for the adverse economic effects of climate change. [68] found a higher production potential for mixed stands in a context of climate change as compared to monospecific mountain forests in Central Europe. [69] found that adding Silver Fir to beech forests increased their ability to adapt to climate change and secured profit. Finally, regarding Southern European forests, [70] found that a mixture of Sweet Chestnut and Truffle Holm Oak had higher socio-ecological resilience. Therefore, the literature reviews show that mixed stands tend to buffer the adverse economic consequences of climate change, although they do not completely mitigate them, as has been observed in some cases (Southeast Germany [71]). Sometimes an insurance premium is offered following a diversifying innovation. However, higher returns may not be enhanced by this practice, as a certain extent of efficiency is lost [64].

Technology-driven silviculture innovations

Eight scientific papers laid the foundation to classify this innovation pathway, comprising four literature reviews, one study based on interviews, one case study, and two mixed-method approaches. Half of these papers refer to climate change resilience, and six of these argued that resilience is driven by efficiency. Out of these six, three also argued for flexibility as a resilience driver (Fig. 3). Based on this sample, this pathway encompasses technological solutions that enhance efficiency in value chains in the forest-based sector. Examples from the analysed papers include the use of satellite technologies and remote sensing to simplify the process of creating a forest inventory [72] and to more effectively respond to disturbances [73]. The use of digital technologies can also enhance people’s recreational experiences in forests [40, 74].

Innovations in this pathway can optimise supply chain management and enable the forest-based sector to respond more quickly to changes in demand. However, these are also characterised by innovations that could be knowledge- and material-intensive. As a result, such innovations may be too costly for small-scale forest owners. For example, this shortcoming applies to costs associated with complementing a ground-level forest inventory with forest measurements to collect data with remote sensing (e.g. assessing the carbon storage of large forested areas or large-scale forest disturbances) [72]. Similarly, in Northern Europe, cut-to-length systems or mechanised planting rely heavily on the ability to make real-time measurements by using onboard computers and sensors in harvesters. Such harvesting systems reduce administrative tasks, wood waste, and discrepancies in stock data, but are expensive [75]. Similar conclusions regarding high costs were reached for recreation-enhancing digital solutions [40, 74].

Innovations in this pathway are also sometimes associated with strengthened forest resilience. Digital solutions can streamline forest operations, and the collected data can be used to accurately respond to rapidly changing environmental conditions [72]. As an indication, drone technology is being increasingly used to detect and map the spread of pests, diseases, wildfire outbreaks, and damage to forest infrastructure. These solutions thus contribute to the development of early warning systems and the coordination of forest management efforts [73, 76]. In addition, forest inventory data may be used in forestry along with more citizen monitoring, rightly shifting the power to the population [76], for example, by improving forest fire disturbance responses and fire prevention management by providing the local population with digital solutions [77]. However, in some cases, digitisation has not improved resilience. Historically, forest administrations have advocated homogenisation and rationalisation of forestry, favouring even-aged stands consisting of low tree diversity, which are easy to manage and require little machinery [38].

Innovations strengthening forest recreation

The third innovation pathway includes modifications related to forest tourism, recreation, and the experience economy. The sample of scientific literature consists of 16 papers, five of which refer to climate change resilience. The methods applied vary: Five survey approaches (one in combination with interviews), five interviews, two choice experiments, one modelling approach, one literature review, one governance analysis, and one exploratory study. Eleven papers addressed diversification as the value chain resilience driver (Fig. 3). A few examples mentioned in the papers include mountain bike tourism [78, 79], tourism related to the collection of forest products [80], and forestry workshops [81].

No evidence was found in the sample of papers that diversifying forest systems by strengthening recreational systems directly enhances forest resilience. However, forest-based recreation is often found to be indirectly linked to the appreciation of a forest, which depends heavily on its diversity [82, 83]. Forest preference studies conclude that people appreciate mature forests that have good visibility, some undergrowth, and a green field layer with no obviously visible signs of forest management [84, 85]. In contrast, intensive wood production, short rotation cycles, and large size management units negatively affect forest attractiveness, decreasing the suitability of a forest for recreation [86]. The “naturalness” of an area, meanwhile, might reduce the accessibility and thus negatively affect recreation [87]. However, a forest that is optimal for recreation does not necessarily provide optimal risk diversification. While functional diversification serves as a buffer against uncertainty, it could also result in a completely different forest portfolio compared to the one which is optimally diversified for recreation [39].

Innovations strengthening forest recreation might diversify the product portfolio, but a forest owner typically only receives minimal benefits from allowing recreation on their land, and recreation-oriented management practices could reduce profits from timber production [85, 86] examined private landowners’ preferences in Finland and found that many forest owners are willing to protect their land and benefit from the recreational fees received as compensation for use. The idea that forests are publicly owned and the frequent assertion of everyman’s rights make it difficult to integrate commercial innovations into recreational services, as citizens are unaccustomed to paying for them [88]. Payments for parking spaces near recreation areas, however, have proved to be an important source of income.

Creative approaches applied in combination with payments for ecosystem services schemes to enhance consumers’ experiences would be potentially useful in the future, but institutional support for the development of such businesses is lacking [89]. Collaborative deliberation and communication processes are needed to teach forest managers how they can support and carry out such processes [90]. In addition, maintaining good relationships between entrepreneurs and private forest owners, as well as combining their interests, is vital for sustaining nature tourism activities [91]. For example, without community cooperation, mountain biking trails in Switzerland and Austria would not exist and would not provide additional income or garner government funding [79, 92].

Innovative payment for forest ecosystem services (PES) schemes

Twelve papers were analysed to determine and describe the fifth innovation pathway. Out of these twelve papers, nine referred to climate change resilience. Seven papers addressed diversification as a value chain resilience driver (Fig. 3). The methodologies applied included four case studies, two economic valuation methods, two interviews (one in combination with a survey), one literature review, and one mixed method approach.

Many forms of payments for ecosystem services exist, and these can be differentiated by whether they include direct payments or indirect payments. Some examples include schemes related to regulating and supporting ecosystem services, such as habitat improvement and soil conservation [93], carbon sequestration [94], or water tariffs paying forest owners to manage their forests in order to improve water quality and quantity [95]. Other examples include cultural ecosystem services, such as payment schemes that enhance recreation. For example, [96] described a system in Trentino where the tourism tax is used to maintain the landscape values. This system was set up after a large storm severely damaged the landscape. Alternatively, some payment schemes combine the above-mentioned ecosystem services, including those for provisioning, for example, by offering payments for targeted livestock grazing to reduce wildfire risks and boost biodiversity, water quality, and scenic beauty [97] or to meet other goals, such as increasing wood production or conservation [85, 98]. Some encourage the production of mushroom colonies on dead wood to improve biodiversity and forest microclimates [99].

Diversification by implementing payments for ecosystem service schemes can potentially enhance forest and value chain resilience, particularly in light of climate change. These examples lead to forest diversification and indirectly strengthen the forest’s ecological quality and, thereby, its resilience to cope with disturbances [19]. In addition, implementing payments for ecosystem service schemes could strengthen the economic value of the forest-based sector by reducing the financial imbalance caused by climate change [19, 20].

Innovations extending the product portfolio beyond wood

The fifth innovation pathway includes innovations that extend the product portfolio in the forest management part of the value chain beyond wood production. Fourteen papers served as a basis for developing and analysing this pathway, half of which referred to climate change resilience. Eleven stressed the importance of diversification to improve resilience, one of which also referred to increased (cost) efficiency by offering hunting as a product [100] (Fig. 3). The applied methodologies include six exploratory literature reviews, two interview approaches, two surveys, two case studies, one economic assessment, and one combined legal and spatial assessment. A few examples from this sample of literature include introducing by-products into the market, such as wild mushrooms, commercialising edible fruits, or including forest farming and silvo-pastoral systems. In addition, alternative forms of income such as woodland burials [101] or income from wind power [102] were considered.

Although alternative forest products have more potential to enhance value chain resilience than is presently recognised [29, 30, 103], their potential to strengthen forest resilience is scarcely documented in the academic literature. [30] conducted a review of recent European advances in modelling integrated multifunctional forest systems, including both wood and non-wood products. In almost all cases, wood and NWFPs could be synergistically produced and create additional income for forest owners. For example, managing Mediterranean pine stands was unprofitable without the additional income from the sale of mushrooms and pine nuts [104,105,106]. In some cases, promoting NWFPs did not provide forest owners with additional income, as, for example, in the joint production of timber and mushrooms in Norway spruce stands [107]. In other cases, harvesting NWFPs had a negative impact on timber quality or yield; resin and sap tapping conflicts with timber production [30]. Sometimes this additional income is equivalent to a working income: The income earned per hour worked may not be attractive to forest owner, as the assumed cost per working hour may be too high to enable the forest owner to earn a profit [108]. Furthermore, in Serbia, NWFPs can be exported at an increased price, but the profit is not earned by the right people due to the high fees charged by intermediaries [109, 110]. Similarly, [111] stated that the economic viability of chestnuts should be supported by policy and driven by the private sector [112].

Integrating NWFP production into forest management may involve interventions (e.g. using forest-thinning regimes to enhance mushroom or berry production) [36], selecting specific tree species (e.g. cherries, nuts, or other fruit trees) [30], or implementing forest farming systems (e.g. the Portuguese Montado system with cork production and grazing) [97]. In some situations, extending the product portfolio while offering recreational possibilities makes management more feasible, as is the case regarding game-oriented forest management and other non-wood services [100] or growing and selling Christmas trees [35].

Innovations supporting co-management or joint forest ownership

The sample of papers in this pathway consists of 18 papers, only six of which referred to climate change resilience. The effects of forest ownership on climate resilience have not been studied in detail or were deemed to be insufficiently correlated. Nevertheless, six papers mention diversification, and seven papers underline flexibility as an important resilience driver (Fig. 3). Out of these 18 scientific papers, four are case studies, five are surveys, one is a qualitative data analysis, four are interviews, three are literature reviews, and one is a policy mapping.

The term joint forest ownership refers to management approaches involving multiple parties in decision-making and management processes. These approaches generate income through the production of goods and services, but also provide social returns for the partners, comprising participatory forestry and community-owned forest management. Co-management is defined as cooperation among forest owners with larger forest holdings to increase the efficiency of the forest operations, e.g. by sharing equipment or supporting synergies in the production and marketing of wood products. Although a more mixed property structure correlates with resilience, this does not mean that single owners miss out on chances to strengthen their resilience.

Cooperation positively correlates with strengthened forest and value chain resilience and climate adaptation goals. Co-owners or stakeholders may differ in terms of their gender, age, education, or other individual characteristics that tend to be associated with multifunctional forest values and diverse management strategies [113,114,115] found evidence indicating that social and community enterprises in Britain generate more diverse benefits, such as conservation and increasing social benefits for the community or a larger population. Similarly, [116] found that woodland social enterprises are diverse and consider different forms of income than just the income from wood. In Sweden, [117] also noted that people who knew more about climate adaptation were more likely to apply more climate adaptation practices.

Several studies have shown that corporations continually find new ways to innovate, increase their assets, and mobilise wood while taking a stronger competitive position in the market [40, 118, 119]. Individuals that are convinced of the value of a forest to a larger group of stakeholders, such as a community, drive innovation [120]. For example, [120] found that community forests in England share financial responsibility, increase the number of income streams, and have many volunteers. [121] found that co-management practices in Finland increase financial stability. Forest cooperatives in Greece have found win–win situations that meet sustainability goals and increase demand [122]. Similarly, in Spain ‘socio-ecological resilience’ to forest fires is strengthened by including additional stakeholders, and especially bottom-up initiatives [123].

Innovations supporting circularity

The seventh innovation pathway encompasses all innovations related to cascading wood use, ranging from higher value applications (e.g. sawn wood) to lower value applications (e.g. fuelwood), and the use of process waste. Eleven papers were used to analyse this pathway, merely four of which refer to climate change resilience (Fig. 3). Methodologically the sample is varied: two Delphi studies, four literature reviews, three case studies, and one mass flow analysis. From analysing the papers, it becomes clear that innovations supporting circularity potentially enhance resilience by driving efficiency (8 papers) and diversification (4 papers). Examples include the use of by-products from the sawmill industry as raw material for the pulp industry [124], the integration of a biorefinery concept in existing pulp and paper operations, and the production of energy from forest waste [125, 126] or the enhancement of the potential to recover solid wood for other applications [127].

By enhancing efficiency and diversification, this innovation pathway strengthens value chain resilience. Most of the literature on circular economy and biorefinery development places a focus on the mitigation aspect of climate change, but little evidence was found that this innovation results in higher forest resilience. The large amounts of wood damaged as a result of climate change-related disturbances, however, could easily be utilised in lower value applications. In addition, primary and secondary producers further downstream in the value chain can become more independent if they diversify their procurement strategies and source wood from other sources along the value chain instead of directly from the forest, thus reducing the pressure on the standing trees [15,16,17].

Cascading wood use is considered a robust but conservative transformation pathway. [126] found that most biorefinery projects in Finland and Sweden displayed merely incremental differences in terms of their dominant business logic and technology paradigms. However, the authors emphasised that the perception of wood availability could be a limiting innovation along this pathway. Furthermore, in order to avoid dependency on fossil fuels, the total production site in the processing industry must be optimised [125]. This finding contrasts with that of [128], who suggest that the volume of the fibre sludge side stream (commercially used as a dust-binding agent) is too high to be fully utilised by producers and cannot be used for higher-value applications. Similarly, bark and other tree residues (e.g. foliage) still remain a largely underexploited resource [129].

Innovations extending the product portfolio with high-value products

The process of extending the product portfolio with high-value products differs in sawmills and pulp mills. The wood needed for high-quality applications in pulp mills is of lower quality than the wood needed in sawmills. Therefore, this pathway complements the seventh innovation pathway. The sample used to determine and analyse this innovation pathway consists of 24 papers. It is the only pathway in which diversification (addressed in 15 papers), efficiency (addressed in seven papers), and flexibility (addressed in three papers) come together (Fig. 3). The analysed papers apply the following research methods: nine literature reviews, two interviews (one with observations at seminars and workshops), three case studies, one forest sector model application, one LCA, one wood quality measurements, two Delphi studies, one focus groups, one willingness-to-pay approach, one trade flow analysis, and one questionnaire. Examples include wooden (multi-storage) construction [130, 131], wood textiles [23], furniture [42], sustainable packaging solutions [132, 133], design products [132], the use of wood in the automotive industry [134], and the use of bark phytochemicals as bulk chemicals in the food, pharmaceutical, and cosmetic industries [129].

For high-value applications, higher-quality wood is needed in many cases [37, 135]. This resource does not need to harmonise with the higher availability of low-quality wood due to increased forest disturbance [37, 135] listed desirable wood properties for optimal processing in higher-value applications: Wood used for conventional sawn wood, panels, and plywood needs to have strength, stiffness, and a high density. This requires trees to be more uniform, have an improved trunk form and less juvenile wood; at the same time, the wood must have a small microfibril angle and a high lignin content. The desired properties of wood used for paper, paperboard, and packaging production are broader, as the wood can be enhanced by adding cellulosic nanomaterials in the form of fillers and coatings to meet high quality standards, such as increased sheet smoothness and strength. This requires the wood to have a higher cellulose to lignin and hemicellulose ratio. Lignin is more easily removed from softwood than from hardwood; however, the lignin in hardwood species has a higher quality. In addition, using wood in some higher-value applications requires using specific fractionation and effective purification processes that are technologically demanding and often not cost-effective [23, 136].

When these processes are implemented and high-quality wood is available, increases in employment opportunities and export income from high-value products are seen, strengthening value chain resilience. In Sweden, for example, the value of joinery and furniture is 15–20 times higher than that of sawn timber. The added value of wood in the building industry is about 1.5 times higher (also in Sweden) [42]. Similarly, many possibilities exist to capitalise on lignin production for a large number of applications [137], and the willingness of consumers to pay for wood fibres in textiles is growing steadily [138]. Creating wood products by using higher-value applications also strengthens forest company branding and opens up new supply markets [132].

Innovative approaches to sales and marketing

The last innovation pathway centres around organisational adaptations made to diversify marketing and sales channels, such as using sustainability labels, trans-shipment points, and biomass trade-centres, hosting wood auctions, or launching forest e-shops. This pathway builds on five papers, none of which refer to climate change. Nevertheless, they do refer to strengthened resilience through flexibility (three papers) and efficiency (four papers) (Fig. 3). The applied methods include two literature reviews, one expert interviews, one application of an analytical framework, and one application of the expanded business model canvas.

Innovations along this pathway enable forest firms to respond more rapidly to changing consumer demands and market opportunities, as well as to find international consumers for products [139,140,141] which might become more available as the result of disturbances. For example, [40] examined an e-shop in Finland and the use of high-quality wood auctions in Slovenia. The e-shop is run by a forest owner association (FOA) that tries to offer new marketing channels based on social media by using Google as a marketing channel to offer the forest owner group benefits. By using the internet as a delivery channel, the easy access to products and services is safeguarded, and these can be quickly adapted to meet customers’ demands. Furthermore, a new type of nationwide partnership has been established where financial benefits can be derived from joint marketing and niche product production to avoid competing with the same kind of forest products. In this regard, [21] suggested that eco-labels and certification can be considered as essential for sustainable product development in forest sector. The business model of Slovenian high-quality wood auctions offers private forest owners a chance to sell high-quality wood from their forests for a price that is higher than ordinary prices. This increases the forest owners’ motivation to become active in areas of forest management, education, and investments in research and development [40].

[142] examined drivers, organisational resources, and innovations in the transition of the Finnish forest-based sector to a circular bioeconomy. They found that it is essential for teams with diverse knowledge to develop communication and marketing skills. This aspect has been proven difficult for smaller companies, as they often do not have the resources to develop such skills. The challenges that were identified include the frequent need to find new markets and the lack of validity for traditionally marketing traditional products. In addition, different customers often need marketing messages specifically tailored for their needs.

Discussion

Innovation has been claimed by many authors and researchers to positively contribute to climate adaptation in forest-based value chains (e.g. [19,20,21,22]). However, knowledge regarding the kind of innovation pathways and how these enhance resilience, if at all, is widely dispersed. This conceptual paper was written to increase the understanding of such innovation pathways along wood value chains and to evaluate the extent to which they enhance or compromise resilience to climate change in the forest-based sector.

Based on the results of two subsequent literature reviews, we were able to identify nine innovation pathways along the wood value chain (Fig. 4). Taking a deeper look, we saw that innovation mostly contributes positively to resilience to climate change, but it can also compromise resilience under certain circumstances. We analysed this by asking three questions: Where does innovation occur along the wood value chain? Which form of resilience does it contribute to (i.e. value chain [143] or forest resilience [144])? And which value chain resilience driver is attached to the innovation (efficiency, flexibility, or diversification) [27••]?

Our findings indicate that innovation that supports resilience takes on different forms at the beginning of the value chain (in forest management) than at the end of the value chain (in the processing industry). In the forest management part of the value chain, innovation is dominated by the resilience driver diversification. In contrast, efficiency as a resilience driver dominates in the primary and secondary processing parts of the value chain. The two drivers might not complement one another, because diversification increases complexity rather than simplicity and, by extension, reduces efficiency. Pathway 2 (technology-driven silvicultural innovations) is the only pathway positioned in the forest management part of the value chain that are based on an efficiency resilience driver (whereas the other pathways are based on diversification). This innovation pathway also includes cases of innovations that have compromised resilience, for example, when new digital technologies or harvest operations require easy-to-measure forest structures which can be managed straightforwardly by using high amounts of mechanization. According to [38], this is also reflected by the fact that forest managers have historically advocated for the homogenisation and rationalisation of forestry, suggesting that even-aged, pure forests are optimal. At present, we can see the consequences of such systems in some European regions, where the enormous damages are not only caused by climatic changes, but also by less resistant and less resilient forest structures that suffer from a low adaptive capacity [145, 146].

As depicted in Fig. 3, innovation rarely links forest management and the processing industry. Three pathways can be implemented in multiple parts of the value chain: pathway 6 (innovations towards co-management and joint forest ownership), pathway 7 (innovations towards circularity), and pathway 9 (innovative approaches to sales and marketing). The latter (pathway 9) could be implemented throughout the value chain. In addition, these pathways (pathway 6, 7, and 9) can be combined with a broader set of innovations along the value chain and can subsequently increase the amount of control industries have over the wood value chain, strengthening their connections with suppliers or customers [40].

In some cases, combining various innovation pathways is reported to lead to synergies related to forest and value chain resilience. Fostering forest resilience by creating a mixed and structure-rich forest (pathway 1) is considered to be particularly appropriate for recreational purposes (pathway 3) [82, 84, 85]. Such a forest has also been shown to positively influence the ability of innovations to extend the product portfolio beyond wood (pathway 5) [30, 35, 100]. Likewise, some authors reported that the high financial costs and technological demand hindering pathway 2 (technology-driven silvicultural innovations) could be resolved if forest owners joined forces with others, as suggested in pathway 6 (innovations supporting co-management and joint forest ownership) [40, 118, 119]. Furthermore, pathways 7 and 8 should be strategically combined, and wood should first be used in higher-value applications before it is downcycled to low-value applications [37]. Lastly, combining pathways 4 (innovative PES-schemes) and 9 (innovative approaches to sales and marketing) could intensify the positive contribution of all other innovation pathways for forest management, potentially increasing the ability of these forests to adapt to climate change.

In other cases, combining various pathways could result in conflicts, in the same way that forest functions might conflict. For example, conflicts were noted between wood production and recreation [85, 86], between wood production and carbon sequestration [147], and between wood production and nature conservation goals [82]. Such trade-offs are also expected to result in conflicts downstream in the value chain, because the primary and secondary production sectors prefer to have a constant supply of softwood at reasonable prices. Another potential trade-off is underlined by the fact that processing wood further in higher-value applications (pathway 8) does not harmonise with the higher availability of low-quality wood due to increased forest disturbance, but it does harmonise with cascading wood to lower-value applications (pathway 7).

Two solutions are presented to overcome the mismatch between diversification and efficiency drivers as described above, as well as to foster synergies and minimise conflicts. First, it is possible to strengthen flexibility by using innovations that support co-management and joint forest ownership (pathway 6), those that support circularity (pathway 7), or that extend the product portfolio with high-value products (pathway 8), or to take innovative approaches toward sales and marketing (pathway 9). Second, our analysis of the innovation pathways enabled us to identify two important common and interconnected drivers: taking an inter- and multidisciplinary participatory approach and engaging in open innovation activities. In particular, other researchers have found that exhibiting openness towards cross-sectoral relations [40, 41, 148,149,150] and civil society [79, 128, 142, 150] is especially critical. Other critical factors identified include having sufficient technological resources, human skills [151], integrating and coordinating policies [152], increasing environmental awareness [153], and setting voluntary climate change targets [154].

Regarding the reliability and validity of the results, some limitations associated with systematic literature reviews should be considered when weighing our study outcomes. Most importantly, the lack of scientific publications that address certain aspects of climate adaptation does not necessarily imply that these aspects do not exist. This study involved the detection and analysis of 126 relevant papers with a European scope. In the future, it would be of interest to examine experiences made in this topical area outside of Europe.

Conclusions

In this study, we determined nine innovation pathways and analogous resilience drivers along the wood value chain. We then assessed the extent to which the associated innovations are known to enhance or compromise resilience to climate change in the forest-based sector. An important outcome of the study was that we could recognize the role of innovation drivers with respect to value chain resilience: These drivers increase diversification, efficiency, and/or flexibility (Fig. 3).

Our results show that a mismatch exists between innovation pathways and resilience drivers at the beginning of the value chain in forest management and towards the end of the value chain in the processing industry. Indeed, innovation rarely links forest management and the processing industry. Moreover, innovation pathways used in forest management to strengthen resilience also support diversification, whereas those used in the processing industry support efficiency. The trade-off between diversification and efficiency has led to conflicts in the past: The rationalisation of efficient forestry suggests that even-aged, pure forests that are easy to manage are optimal, but these are not resistant or resilient to natural disturbances exacerbated by climate change.

This conceptual work linking resilience to innovation has consequences for future research on this topic. To overcome the mismatch between diversification and efficiency drivers, as well as to foster synergies and minimise conflicts, we recommend integrating forest and wood value chain research. In this regard, an increased awareness of resilience drivers and the analogous innovation pathways, as well as of the possibility to optimally combine them, is needed. At the same time, communication between forest management and the processing industry needs to be improved. Along these lines, we recommend engaging in open innovation activities to cooperatively draft innovation strategies across the wood value chain, thereby facilitating joint work among forest owners, managers, transportation companies, primary processing industries, and secondary processing industries.

Future researchers could look at the direction of the effects, which requires further consideration: Intercepting such innovation pathways could increase the resilience of forests to climate change, but we need to know more about how climate change is driving such pathways. Lastly, our work focuses on the wood value chain. It would also be good to consider first resilience and second innovation in other primary production-based value chains, such as those for cork, eucalyptus, or resin.

Notes

2 separate search terms: Forest* AND Innovation* (1) and Wood AND Innovation.

15 separate search terms: forest* AND (“Climate adaptation’’ OR “climate resilience’’) AND (1) “Community ownership’’ (2) “non-wood forest product’’ (3) “forest farming’’ (4) recreation (5) “payment for ecosystem services’’ (6) “wood cascading’’ (7) bioenergy (8) technolog* (9) marketing (10) certification (11) construction (12) “wood fiber’’ (13) Packag* (14) “Climate-smart forestry’’ (15) “

mixed forestry’’.

References

Papers of particular interest, published recently, have been highlighted as: • Of importance •• Of major importance

European Commission. New EU Forest Strategy for 2030. European Union; 2021.

Seidl R, et al. Forest disturbances under climate change. Nat Clim Change. 2017;7(6):395–402. https://doi.org/10.1038/nclimate3303.

• Sousa-Silva R, et al. Adapting forest management to climate change in Europe: Linking perceptions to adaptive responses. Forest Policy Econ. 2018;90:22–30. https://doi.org/10.1016/j.forpol.2018.01.004. This paper surveyed forest owners throughout Europe and found that little climate change adaptation innovations are taken. Consequently, it underlines an important research gap, that the presented paper aims to contribute to.

Lorenz R, Stalhandske Z, Fischer EM. Detection of a climate change signal in extreme heat, heat stress, and cold in Europe from observations. Geophys Res Lett. 2019;46(14):8363–74. https://doi.org/10.1029/2019GL082062.

Hetemäki L, Hurmekoski E. Forest products markets under change: review and research implications. Curr Forestry Rep. 2016;2(3):177–88. https://doi.org/10.1007/s40725-016-0042-z.

•• Nikinmaa L, et al. Reviewing the use of resilience concepts in forest sciences. Curr Forestry Rep. 2020;6(2):61–80. https://doi.org/10.1007/s40725-020-00110-x. This paper defines and elaborates on the concept of resilience in the forest-based sector. One of the key premises of this paper.

Holling, ‘Engineering Resilience versus Ecological Resilience. In: Schulze, P.E., Ed., Engineering within Ecological Constraints’, Washington DC: National Academy Press, 1996, pp. 31–43.

Scheffer M, Carpenter SR, Dakos V, van Nes EH. Generic indicators of ecological resilience: inferring the chance of a critical transition. Annu Rev Ecol Evol Syst. 2015;46(1):145–67. https://doi.org/10.1146/annurev-ecolsys-112414-054242.

Biggs R, Schlüter M, and Schoon ML, Eds., Principles for Building Resilience: Sustaining Ecosystem Services in Social-Ecological Systems, 1st ed. Cambridge University Press. 2015. https://doi.org/10.1017/CBO9781316014240

Folke C, et al. Regime shifts, resilience, and biodiversity in ecosystem management. Annu Rev Ecol Evol Syst. 2004;35(1):557–81. https://doi.org/10.1146/annurev.ecolsys.35.021103.105711.

Walker RM. Innovation and organisational performance: evidence and a research agenda. SSRN J. 2004. https://doi.org/10.2139/ssrn.1306909.

UNISDR, WMO, ‘UN System Task Team on the Post-2015 UN Development Agenda, Disaster risk and resilience, Thematic Think Piece’. 2012.

•• Larsen JB et al. (2022) Closer-to-nature forest management. S. l.: European Forest Institute. This paper defines and elaborates on the concept of resilience, resistance and adaptive capacity in the forest-based sector.

Knoke T, Paul C, Gosling E, Jarisch I, Mohr J, Seidl R. Assessing the economic resilience of different management systems to severe forest disturbance. Environ Resource Econ. 2023;84(2):343–81. https://doi.org/10.1007/s10640-022-00719-5.

Mantau U. Wood flow analysis: Quantification of resource potentials, cascades and carbon effects. Biomass Bioenerg. 2015;79:28–38. https://doi.org/10.1016/j.biombioe.2014.08.013.

Schwarzbauer P, Weinfurter S, Stern T, Koch S. Economic crises: Impacts on the forest-based sector and wood-based energy use in Austria. Forest Policy Econ. 2013;27:13–22. https://doi.org/10.1016/j.forpol.2012.11.004.

Suominen T, Kunttu J, Jasinevičius G, Tuomasjukka D, Lindner M. Trade-offs in sustainability impacts of introducing cascade use of wood. Scand J For Res. 2017;32(7):588–97. https://doi.org/10.1080/02827581.2017.1342859.

Nassl M, Löffler J. Ecosystem services in coupled social–ecological systems: Closing the cycle of service provision and societal feedback. Ambio. 2015;44(8):737–49. https://doi.org/10.1007/s13280-015-0651-y.

Maier C, Hebermehl W, Grossmann CM, Loft L, Mann C, Hernández-Morcillo M. Innovations for securing forest ecosystem service provision in Europe – A systematic literature review. Ecosyst Serv. 2021;52:101374. https://doi.org/10.1016/j.ecoser.2021.101374.

Mann C, Loft L, Hernández-Morcillo M. Assessing forest governance innovations in Europe: Needs, challenges and ways forward for sustainable forest ecosystem service provision. Ecosyst Serv. 2021;52:101384. https://doi.org/10.1016/j.ecoser.2021.101384.

Hyytiä A. Sustainable development—international framework—overview and analysis in the context of forests and forest products—competitiveness and policy. For Prod J. 2022;72(s1):1–4. https://doi.org/10.13073/FPJ-D-20-00053.

Toivonen R, Vihemäki H, Toppinen A. Policy narratives on wooden multi-storey construction and implications for technology innovation system governance. Forest Policy Econ. 2021;125:102409. https://doi.org/10.1016/j.forpol.2021.102409.

Hurmekoski E, Lovrić M, Lovrić N, Hetemäki L, Winkel G. Frontiers of the forest-based bioeconomy – A European Delphi study. Forest Policy Econ. 2019;102:86–99. https://doi.org/10.1016/j.forpol.2019.03.008.

Näyhä A. Transition in the Finnish forest-based sector: Company perspectives on the bioeconomy, circular economy and sustainability. J Clean Prod. 2019;209:1294–306. https://doi.org/10.1016/j.jclepro.2018.10.260.

Thompson JD, Zald MN, and W. R. Scott. Organizations in Action: Social Science Bases of Administrative Theory, 1st ed. Routledge, 2017. https://doi.org/10.4324/9781315125930.

Thompson JD. ‘Organizations in Action: Social Science Bases of Administrative Theory. U’, niversity of Illinois at Urbana-Champaign’s Academy for Entrepreneurial Leadership Historical Research Reference in Entrepreneurship., 1967. [Online]. Available: Available at SSRN: https://ssrn.com/abstract=1496215.

•• Ivanov D, Dolgui A. Low-Certainty-Need (LCN) supply chains: a new perspective in managing disruption risks and resilience. Int J Prod Res. 2019;57(15–16):5119–36. https://doi.org/10.1080/00207543.2018.1521025. This paper brings forward a new approach to manage supply chains resilience in a so-called 'uncertain world' Following Ivanov & Dolgui (2019), in this paper we assume that innovations can positively influence resilience via three strategies: diversifying the product portfolio, making operations more efficient, or making the processes more flexible.

Standish RJ, et al. Resilience in ecology: Abstraction, distraction, or where the action is? Biol Cons. 2014;177:43–51. https://doi.org/10.1016/j.biocon.2014.06.008.

Martinez de Arano I, Maltoni S, Picardo A, Mutke S, and European Forest Institute. ‘Non-wood forest products for people, nature and the green economy. Recommendations for policy priorities in Europe. A white paper based on lessons learned from around the Mediterranean.’ Eur Forest Inst, Knowl Action. 2021. https://doi.org/10.36333/k2a05.

Miina J, Kurttila M, Calama R, de-Miguel S, Pukkala T. Modelling non-timber forest products for forest management planning in europe. Curr Forestry Rep. 2020;6(4):309–22. https://doi.org/10.1007/s40725-020-00130-7.

Pretzsch H, Zenner EK. Toward managing mixed-species stands: from parametrization to prescription. For Ecosyst. 2017;4(1):19. https://doi.org/10.1186/s40663-017-0105-z.

Ledermann T, et al. Effects of silvicultural adaptation measures on carbon stock of austrian forests. Forests. 2022;13(4):565. https://doi.org/10.3390/f13040565.

Pretzsch H, Poschenrieder W, Uhl E, Brazaitis G, Makrickiene E, Calama R. Silvicultural prescriptions for mixed-species forest stands. A European review and perspective. Eur J Forest Res. 2021;140(5):1267–94. https://doi.org/10.1007/s10342-021-01388-7.

Tome M et al. ‘Resource and management – Novel management concepts to boost product diversity and secure higher product flows’, in Non-wood forest Can Tell Us: Seeing the forest around the trees, in What science can tell us, no. N10. Joensuu: European Forest Institute, 2019.

Weiss E. Corradini, and Živojinović, ‘new values of non-wood forest products.’ Forests. 2020;11(2):165. https://doi.org/10.3390/f11020165.

Prokofieva I, Lovric M, Pettenella D, Weiß G, Wolfslehner B, and Wong J. ‘What is the potential contribution of non-wood forest products to the European forest-based bioeconomy?’, Towards Sustain Eur Forest-Based Bioecon. 2017;132.

Sikkema R, Dallemand JF, Matos CT, van der Velde M, San-Miguel-Ayanz J. How can the ambitious goals for the EU’s future bioeconomy be supported by sustainable and efficient wood sourcing practices? Scand J For Res. 2017;32(7):551–8. https://doi.org/10.1080/02827581.2016.1240228.

Siiskonen H. The conflict between traditional and scientific forest management in 20th century Finland. For Ecol Manage. 2007;249(1–2):125–33. https://doi.org/10.1016/j.foreco.2007.03.018.

Clapp RA. The resource cycle in forestry and fishing. Can Geogr. 2008;42(2):129–44. https://doi.org/10.1111/j.1541-0064.1998.tb01560.x.

Kajanus M, et al. What can we learn from business models in the European forest sector: Exploring the key elements of new business model designs. Forest Policy Econ. 2019;99:145–56. https://doi.org/10.1016/j.forpol.2018.04.005.

Näyhä A, Pesonen H-L. Strategic change in the forest industry towards the biorefining business. Technol Forecast Soc Chang. 2014;81:259–71. https://doi.org/10.1016/j.techfore.2013.04.014.

Sandberg D, Vasiri M, Trischler J, Öhman M. The role of the wood mechanical industry in the Swedish forest industry cluster. Scand J For Res. 2014;29(4):352–9. https://doi.org/10.1080/02827581.2014.932005.

Jonsson BG, Svensson J, Mikusiński G, Manton M, Angelstam P. European Union’s last intact forest landscapes are at a value chain crossroad between multiple use and intensified wood production. Forests. 2019;10(7):564. https://doi.org/10.3390/f10070564.

Rueda. Activities along the wood value chain. 2022. [Online]. Available: https://resonateforest.org

• Wolfslehner B, Linser S, and Pülzl H. Forest bioeconomy: a new scope for sustainability indicators. in From Science to Policy / European Forest Institute, no. 4. Joensuu: EFI, 2016. This paper delineated the value chain of wood products and all activities along it.

Moher D. Preferred reporting items for systematic reviews and meta-analyses: the PRISMA statement. Ann Intern Med. 2009;151(4):264. https://doi.org/10.7326/0003-4819-151-4-200908180-00135.

Neuner S, et al. Survival of Norway spruce remains higher in mixed stands under a dryer and warmer climate. Glob Change Biol. 2015;21(2):935–46. https://doi.org/10.1111/gcb.12751.

Pretzsch H. Facilitation and competition reduction in tree species mixtures in Central Europe: Consequences for growth modeling and forest management. Ecol Model. 2022;464:109812. https://doi.org/10.1016/j.ecolmodel.2021.109812.

Colangelo M, et al. Mediterranean old-growth forests exhibit resistance to climate warming. Sci Total Environ. 2021;801:149684. https://doi.org/10.1016/j.scitotenv.2021.149684.

Zamora-Pereira JC, Yousefpour R, Cailleret M, Bugmann H, Hanewinkel M. Magnitude and timing of density reduction are key for the resilience to severe drought in conifer-broadleaf mixed forests in Central Europe. Ann For Sci. 2021;78(3):68. https://doi.org/10.1007/s13595-021-01085-w.

Dubois H, Verkasalo E, Claessens H. Potential of Birch (Betula pendula Roth and B. pubescens Ehrh.) for forestry and forest-based industry sector within the changing climatic and socio-economic context of western Europe. Forests. 2020;11(3):336. https://doi.org/10.3390/f11030336.

Antonucci S, Santopuoli G, Marchetti M, Tognetti R, Chiavetta U, Garfì V. What is known about the management of European beech forests facing climate change? A review. Curr Forestry Rep. 2021;7(4):321–33. https://doi.org/10.1007/s40725-021-00149-4.

Honkaniemi J, Rammer W, Seidl R. Norway spruce at the trailing edge: the effect of landscape configuration and composition on climate resilience. Landscape Ecol. 2020;35(3):591–606. https://doi.org/10.1007/s10980-019-00964-y.

Vitali V, Forrester DI, Bauhus J. Know your neighbours: drought response of norway spruce, silver fir and douglas fir in mixed forests depends on species identity and diversity of tree neighbourhoods. Ecosystems. 2018;21(6):1215–29. https://doi.org/10.1007/s10021-017-0214-0.

Griess VC, Knoke T. Growth performance, windthrow, and insects: meta-analyses of parameters influencing performance of mixed-species stands in boreal and northern temperate biomes. Can J For Res. 2011;41(6):1141–59. https://doi.org/10.1139/x11-042.

Messier C et al. ‘For the sake of resilience and multifunctionality, let’s diversify planted forests!’ Conserv Lett. 2022;15(1). https://doi.org/10.1111/conl.12829.

Schmidt M, Veldkamp E, Corre MD. Tree species diversity effects on productivity, soil nutrient availability and nutrient response efficiency in a temperate deciduous forest. For Ecol Manage. 2015;338:114–23. https://doi.org/10.1016/j.foreco.2014.11.021.

Bristow M, Vanclay JK, Brooks L, Hunt M. Growth and species interactions of Eucalyptus pellita in a mixed and monoculture plantation in the humid tropics of north Queensland. For Ecol Manage. 2006;233(2–3):285–94. https://doi.org/10.1016/j.foreco.2006.05.019.

Attocchi G and Skovsgaard JP. ‘Crown radius of pedunculate oak ( Quercus robur L.) depending on stem size, stand density and site productivity’, Scandinavian J Forest Res. 2015;1–15. https://doi.org/10.1080/02827581.2014.1001782.

Brzeziecki B, Andrzejczyk T, Żybura H. Natural regeneration of trees in the Białowieża Forest. Sylwan. 2018;162(11):883–96.

Pötzelsberger E, Spiecker H, Neophytou C, Mohren F, Gazda A, Hasenauer H. Growing non-native trees in European forests brings benefits and opportunities but also has its risks and limits. Curr Forestry Rep. 2020;6(4):339–53. https://doi.org/10.1007/s40725-020-00129-0.

Martins C, Monteiro S, Knapic S, Dias A. Assessment of bending properties of sawn and glulam Blackwood in Portugal. Forests. 2020;11(4):418. https://doi.org/10.3390/f11040418.

Aitken SN, Bemmels JB. Time to get moving: assisted gene flow of forest trees. Evol Appl. 2016;9(1):271–90. https://doi.org/10.1111/eva.12293.

Friedrich S, Paul C, Brandl S, Biber P, Messerer K, Knoke T. Economic impact of growth effects in mixed stands of Norway spruce and European beech – A simulation based study. Forest Policy Econ. 2019;104:65–80. https://doi.org/10.1016/j.forpol.2019.04.003.

Almeida I, Rösch C, and Saha S. ‘Converting monospecific into mixed forests: stakeholders’ views on ecosystem services in the Black Forest Region’, E&S. 2021;26(4):art28. https://doi.org/10.5751/ES-12723-260428.

Brèteau-Amores S, Fortin M, Andrés-Domenech P, Bréda N. Is diversification a suitable option to reduce drought-induced risk of forest dieback? An economic approach focused on carbon accounting. Environ Model Assess. 2022;27(2):295–309. https://doi.org/10.1007/s10666-022-09821-w.

Fuchs JM, Bodelschwingh HV, Lange A, Paul C, Husmann K. Quantifying the consequences of disturbances on wood revenues with Impulse Response Functions. Forest Policy Econ. 2022;140:102738. https://doi.org/10.1016/j.forpol.2022.102738.

Vacek Z, et al. Mixed vs. monospecific mountain forests in response to climate change: structural and growth perspectives of Norway spruce and European beech. Forest Ecol Manag. 2021;488:119019. https://doi.org/10.1016/j.foreco.2021.119019.

Baumbach L, Niamir A, Hickler T, Yousefpour R. Regional adaptation of European beech (Fagus sylvatica) to drought in Central European conditions considering environmental suitability and economic implications. Reg Environ Change. 2019;19(4):1159–74. https://doi.org/10.1007/s10113-019-01472-0.

Aumeeruddy-Thomas Y, Therville C, Lemarchand C, Lauriac A, Richard F. ‘Resilience of sweet chestnut and truffle holm-oak rural forests in languedoc-roussillon, france: roles of social-ecological legacies domestication, and innovations.’ E&S. 2012;17(2):art12. https://doi.org/10.5751/ES-04750-170212.

Paul C, Brandl S, Friedrich S, Falk W, Härtl F, Knoke T. Climate change and mixed forests: how do altered survival probabilities impact economically desirable species proportions of Norway spruce and European beech? Ann For Sci. 2019;76(1):14. https://doi.org/10.1007/s13595-018-0793-8.

Näyhä A, Pelli P, Hetemäki L. Services in the forest-based sector – unexplored futures. Foresight. 2015;17(4):378–98. https://doi.org/10.1108/FS-08-2013-0034.

Nitoslawski SA, Wong‐Stevens K, Steenberg JWN, Witherspoon K, Nesbitt L, and Konijnendijk van den Bosch CC. ‘The Digital Forest: Mapping a Decade of Knowledge on Technological Applications for Forest Ecosystems’, Earth’s Fut. 2021 9(8). https://doi.org/10.1029/2021EF002123.

Kankaanhuhta V, Packalen T, Väätäinen K. Digital transformation of forest services in finland—a case study for improving business processes. Forests. 2021;12(6):781. https://doi.org/10.3390/f12060781.

Ersson B, Laine T, Saksa T. Mechanized Tree Planting in Sweden and Finland: Current State and Key Factors for Future Growth. Forests. 2018;9(7):370. https://doi.org/10.3390/f9070370.

Calders K, Jonckheere I, Nightingale J, Vastaranta M. Remote sensing technology applications in forestry and REDD+. Forests. 2020;11(2):188. https://doi.org/10.3390/f11020188.

Xanthopoulos G, et al. ‘Innovative action for forest fire prevention in Kythira island Greece, through mobilization and cooperation of the population: methodology and challenges.’ Sustainability. 2022;14(2):594. https://doi.org/10.3390/su14020594.

Pröbstl-Haider U, Lund-Durlacher D, Antonschmidt H, Hödl C. Mountain bike tourism in Austria and the Alpine region – towards a sustainable model for multi-stakeholder product development. J Sustain Tour. 2018;26(4):567–82. https://doi.org/10.1080/09669582.2017.1361428.

Wilkes-Allemann J, Ludvig A. The role of social innovation in negotiations about recreational infrastructure in forests – A mountain-bike case study in Switzerland. Forest Policy Econ. 2019;100:227–35. https://doi.org/10.1016/j.forpol.2019.01.002.

Copena D, Pérez-Neira D, Macías Vázquez A, Simón X. Community forest and mushrooms: Collective action initiatives in rural areas of Galicia. Forest Policy Econ. 2022;135:102660. https://doi.org/10.1016/j.forpol.2021.102660.

Wong JLG and Wiersum FK. ‘A spotlight on NWFPs in Europe’, in Non-wood forest Can Tell Us: Seeing the forest around the trees, in What science can tell us, no. N10. Joensuu: European Forest Institute, 2019.

Margaryan L. Nature as a commercial setting: the case of nature-based tourism providers in Sweden. Curr Issue Tour. 2018;21(16):1893–911. https://doi.org/10.1080/13683500.2016.1232378.

Tyrväinen L, Silvennoinen H, Hallikainen V. Effect of the season and forest management on the visual quality of the nature-based tourism environment: a case from Finnish Lapland. Scand J For Res. 2017;32(4):349–59. https://doi.org/10.1080/02827581.2016.1241892.

Ciesielski M, Stereńczak K. What do we expect from forests? The European view of public demands. J Environ Manage. 2018;209:139–51. https://doi.org/10.1016/j.jenvman.2017.12.032.

Tyrväinen L, Mäntymaa E, Juutinen A, Kurttila M, Ovaskainen V. Private landowners’ preferences for trading forest landscape and recreational values: A choice experiment application in Kuusamo, Finland. Land Use Policy. 2021;107:104478. https://doi.org/10.1016/j.landusepol.2020.104478.

Juutinen A, Kosenius A-K, Ovaskainen V, Tolvanen A, Tyrväinen L. Heterogeneous preferences for recreation-oriented management in commercial forests: the role of citizens’ socioeconomic characteristics and recreational profiles. J Environ Planning Manage. 2017;60(3):399–418. https://doi.org/10.1080/09640568.2016.1159546.

Schirpke U, Scolozzi R, Da Re R, Masiero M, Pellegrino D, Marino D. Recreational ecosystem services in protected areas: A survey of visitors to Natura 2000 sites in Italy. J Outdoor Recreat Tour. 2018;21:39–50. https://doi.org/10.1016/j.jort.2018.01.003.

Muttilainen H, Hallikainen V, Miina J, Vornanen J, Vanhanen H. Forest owners’ perspectives concerning non-timber forest products, everyman’s rights, and organic certification of forests in Eastern Finland. Small-scale Forestry. 2022. https://doi.org/10.1007/s11842-022-09528-6.

Živojinović I, Weiss G, Wilding M, Wong JLG, Ludvig A. Experiencing forest products – An innovation trend by rural entrepreneurs. Land Use Policy. 2020;94:104506. https://doi.org/10.1016/j.landusepol.2020.104506.

Mäntymaa E, Tyrväinen L, Juutinen A, Kurttila M. Importance of forest landscape quality for companies operating in nature tourism areas. Land Use Policy. 2021;107:104095. https://doi.org/10.1016/j.landusepol.2019.104095.

Matilainen A, Lähdesmäki M. Nature-based tourism in private forests: Stakeholder management balancing the interests of entrepreneurs and forest owners? J Rural Stud. 2014;35:70–9. https://doi.org/10.1016/j.jrurstud.2014.04.007.

Wilkes-Allemann J, Ludvig A, Hogl K. Innovation development in forest ecosystem services: A comparative mountain bike trail study from Austria and Switzerland. Forest Policy Econ. 2020;115:102158. https://doi.org/10.1016/j.forpol.2020.102158.

Gatto P, Defrancesco E, Mozzato D, Pettenella D. Are non-industrial private forest owners willing to deliver regulation ecosystem services? Insights from an alpine case. Eur J Forest Res. 2019;138(4):639–51. https://doi.org/10.1007/s10342-019-01195-1.

Pache R-G, Abrudan IV, Niţă M-D. ‘Economic valuation of carbon storage and sequestration in Retezat National Park Romania.’ Forests. 2020;12(1):43. https://doi.org/10.3390/f12010043.

Ovando P, Beguería S, Campos P. Carbon sequestration or water yield? The effect of payments for ecosystem services on forest management decisions in Mediterranean forests. Water Resources Econ. 2019;28:100119. https://doi.org/10.1016/j.wre.2018.04.002.

Bussola F, et al. Piloting a more inclusive governance innovation strategy for forest ecosystem services management in Primiero, Italy. Ecosyst Serv. 2021;52:101380. https://doi.org/10.1016/j.ecoser.2021.101380.

Varela E, et al. Unravelling opportunities, synergies, and barriers for enhancing silvopastoralism in the Mediterranean. Land Use Policy. 2022;118:106140. https://doi.org/10.1016/j.landusepol.2022.106140.

Mäntymaa E, Juutinen A, Tyrväinen L, Karhu J, Kurttila M. Participation and compensation claims in voluntary forest landscape conservation: The case of the Ruka-Kuusamo tourism area, Finland. JFE. 2018;33:14–24. https://doi.org/10.1016/j.jfe.2018.09.003.

Pavlík M, Halaj D. Production and investment evaluation of oyster mushroom cultivation on the waste dendromass: a case study on aspen wood in Slovakia. Scand J For Res. 2019;34(4):313–8. https://doi.org/10.1080/02827581.2019.1584639.

Ikonen P, et al. Grounds for improving the implementation of game-oriented forest management – A double sampling survey of Finnish forest owners and professionals. Forest Policy Econ. 2020;119:102266. https://doi.org/10.1016/j.forpol.2020.102266.

Clayden A, Dixon K. Woodland burial: Memorial arboretum versus natural native woodland? Mortality. 2007;12(3):240–60. https://doi.org/10.1080/13576270701430700.

Bunzel K, Bovet J, Thrän D, Eichhorn M. Hidden outlaws in the forest? A legal and spatial analysis of onshore wind energy in Germany. Energy Res Soc Sci. 2019;55:14–25. https://doi.org/10.1016/j.erss.2019.04.009.