Abstract

We develop a novel empirical test of racial bias based on comparisons between forward-looking, expectations-based credit scores and backward-looking, repayment-history-based credit scores. We then test for racial bias using confidential-access data from the Kauffman Firm Survey. Businesses founded by disadvantaged minorities have much lower average business credit scores, but these scores show no evidence of racial bias. If anything, forward-looking credit-score models under-predict the rate of payment delinquency among minority-owned businesses.

Similar content being viewed by others

Notes

Entry into entrepreneurship is positively related to increases in personal wealth, e.g., via bequest (Cagetti and de Nardi, 2006; Hurst and Lusardi, 2004) or external change in taxation rate (Nanda (2008), and with increased access to bank financing through deregulation and loosening of branching restrictions (Black and Strahan 2002).

For more information about the KFS survey design and methodology, please see Ballou et al. (2008). A public use dataset is available for download from the Kauffman Foundation’s website and a more detailed confidential dataset is available to researchers through a data enclave provided by the National Opinion Research Center (NORC). For more details about how to access these data see http://www1.kauffman.org/kfs.

We adopt the Robb and Robinson (2012) definition of outside debt, which includes business loans, personal loans from banks for the business, business credit cards, and business lines of credit. That is, our measure of outside debt includes bank debt that is issued to either the founder or the business itself. We do this to address the fact that in many instances banks require personal guarantees or collateral for business loans, which effectively blurs the distinction between the owner’s personal financial balance sheet and that of the firm. See Robb and Robinson (2012) for more details.

Outside equity includes venture capital, angel financing, and equity stakes owned by governments or other firms.

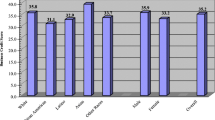

We also considered whether minority borrowers were more likely to be more than 30 days late (Paydex below 50) or less likely to pay on time (Paydex over 80) than would be suggested by the CCS score but found no evidence of this. Results are available upon request.

References

Adelino, M., Ma, S. and Robinson, D. (2017) Firm age, investment opportunities and job creation. Journal of Finance 72, forthcoming.

Ballou, J., Barton, T., DesRoches, D., Potter, F., Reedy, E., Robb, A., Shane, S., Zhao, Z. (2008). Kauffman firm survey: results from the baseline and first follow-up surveys. Kauffman Foundation.

Bates, T. (1991). Commercial bank financing of white and Black-owned small business startups. Quarterly Review of Economics and Business, 31, 64–80.

Bates, T., & Lofstrom, M. (2013). African Americans’ pursuit of self-employment. Small Business Economics, 40, 73–86.

Bates, T., & Robb, A. (2013). Greater access to capital is needed to unleash the local economic development potential of minority-owned businesses. Economic Development Quarterly, 27, 250–259.

Bates, T., & Robb, A. (2016). Impacts of owner race and geographic context on access to small-business financing. Economic Development Quarterly, 30, 159–170.

Berger, A., & Frame, W. (2007). Small business credit scoring and credit availability. Journal of Small Business Management, 45, 5–22.

Berger, A., Frame, W., & Miller, N. (2005). Credit scoring and the availability, price, and risk of small business credit. Journal of Money, Credit, and Banking, 37, 191–222.

Bertrand, M., & Mullainathan, S. (2004). Are Emily and Greg more employable than Lakisha and Jamal? A field experiment on labor market discrimination. American Economic Review, 94, 991–1013.

Black, S., & Strahan, P. (2002). Entrepreneurship and bank credit availability. Journal of Finance, 57, 2807–2833.

Blanchflower, D., Levine, P., & Zimmerman, D. (2003). Discrimination in the small business credit market. Review of Economics and Statistics, 85, 930–943.

Braunstein, Sandra F. (2010). Credit scoring: testimony before the subcommittee on financial institutions and consumer credit, the committee on financial services. US House of Representatives, March 24, 2010.

Cagetti, M., & de Nardi, M. (2006). Entrepreneurship, frictions and wealth. Journal of Political Economy, 114, 835–870.

Capon, N. (1982). Credit scoring systems: A critical analysis. Journal of Marketing, 46, 82–91.

Cavalluzzo, K., & Wolken, J. (2005). Small business loan turndowns, personal wealth and discrimination. Journal of Business, 78, 2153–2177.

Cavalluzzo, K., Cavalluzzo, L., & Wolken, J. (2002). Competition, small business financing, and discrimination: Evidence from a new survey. Journal of Business, 75, 641–679.

Fairlie, R. (1999). The absence of the African American owned business: An analysis of the dynamics of self-employment. Journal of Labor Economics, 17, 80–108.

Fairlie, R., & Robb, A. (2008). Race and entrepreneurial success: Minority-, Asian-, and White-owned businesses in the United States. Cambridge: MIT Press.

Fairlie, R., and Woodruff, C. (2009). Mexican-American entrepreneurship. Working Paper, University of California.

Fairlie, R., Robb, A. and Robinson, D. (2016). Black and White: racial differences in access to capital for startups. Working Paper, Duke University and University of California, Santa Cruz.

Frame, W., Padhi, M., & Woolsey, L. (2004). The effect of credit scoring on small business lending in low and moderate income areas. Financial Review, 33, 813–825.

Haltiwanger, J., Jarmin, R. and Miranda, J. (2009). Jobs created from business startups in the united states. Kauffman Foundation, Working Paper.

Haltiwanger, J., Jarmin, R. and Miranda, J. (2010). Who creates jobs? small vs. large vs. young. National Bureau of Economic Research Working Paper, 16300.

Hu Y., Liu L., Ondrich J., and Yinger, J. (2011). The racial and gender interest rate gap in small business lending. Working paper, Syracuse University.

Hurst, E., & Lusardi, A. (2004). Liquidity constraints, household wealth, and entrepreneurship. Journal of Political Economy, 112, 319–347.

Kane, T., (2010). The importance of startups in job creation and job destruction. Working paper.

Lofstrom, M., and Wang, C. (2008). Hispanic self-employment: a dynamic analysis of business ownership. Working paper, Public Policy Institute of California.

Mijid, N., & Bernasek, A. (2013). Decomposing racial and ethnic differences in small business lending: Evidence of discrimination. Review of Social Economy, 1–31.

Nanda, R., (2008). Cost of external finance and selection into entrepreneurship. Cambridge: Harvard Business School Working Paper 08-047.

Puri, M., & Zarutskie, R. (2012). On the life-cycle dynamics of venture-capital and non-venture-capital financed firms. Journal of Finance, 67, 2247–2293.

Robb, A., & Robinson, D. (2012). The capital structure decisions of new firms. Review of Financial Studies, 1, 1.

Acknowledgements

This research was supported under grant SBAHQ-12-Q-0044 from the Small Business Administration. Certain data included herein are derived from the Kauffman Firm Survey release 6.0. Any opinions, findings, and conclusions or recommendations expressed in this material are those of the author(s) and do not necessarily reflect the views of the Ewing Marion Kauffman Foundation. The authors wish to thank Tim Bates, Bill Bradford, Rob Seamans, and workshop participants at the Kauffman-sponsored MBE sessions at the 2016 AEA meetings and the 2016 AoM meetings. Jonathan Zandberg provided expert research assistance.

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Robb, A., Robinson, D.T. Testing for racial bias in business credit scores. Small Bus Econ 50, 429–443 (2018). https://doi.org/10.1007/s11187-017-9878-2

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11187-017-9878-2