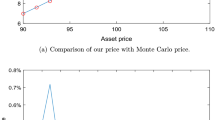

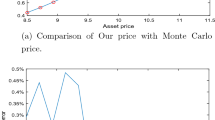

Abstract

We present a generalization of Cochrane and Saá-Requejo’s good-deal bounds which allows to include in a flexible way the implications of a given stochastic discount factor model. Furthermore, a useful application to stochastic volatility models of option pricing is provided where closed-form solutions for the bounds are obtained. A calibration exercise demonstrates that our benchmark good-deal pricing results in much tighter bounds. Finally, a discussion of methodological and economic issues is also provided.

Similar content being viewed by others

References

Andersen T.G., Benzoni L., Lund J. (2001) An empirical investigation of continuous-time equity returns models. Journal of Finance 57: 1239–1284

Benzoni, L. (2000). Pricing options under stochastic volatility: An empirical investigation. Working paper, University of Minnesota.

Bernardo A.E., Ledoit O. (2000) Gain, loss, and asset pricing. Journal of Political Economy 108: 144–172

Björk T., Slinko I. (2006) Towards a general theory of good deal bounds. Review of Finance 10: 221–260

Cerny A. (2003) Generalized sharpe ratios and asset prices in incomplete markets. European Finance Review 7: 191–233

Cochrane, J. H., & Saá-Requejo, J. (1999). Good-deal option price bounds with stochastic volatility and stochastic interest rate. Working paper, University of Chicago.

Cochrane J.H., Saá-Requejo J. (2000) Beyond arbitrage: Good-deal asset price bounds in incomplete markets. Journal of Political Economy 108: 79–119

Eraker B., Johannes M.S., Polson N.G. (2003) The impact of jumps on volatility and returns. Journal of Finance 58: 1269–1300

Hansen L.P., Jagannathan R. (1991) Implications of security market data for models of dynamic economies. Journal of Political Economy 99: 225–262

Hansen L.P., Jagannathan R. (1997) Assessing specification errors in stochastic discount factor models. Journal of Finance 52: 557–590

Henderson V., Hobson D., Howison S., Kluge T. (2005) A comparison of option prices under different pricing measures in a stochastic volatility model with correlation. Review of Derivatives Research 8: 5–25

Jaschke S., Küchler U. (2001) Coherent risk measures and good-deal bounds. Finance and Stochastics 5: 181–200

Pan J. (2002) The jump-risk premia implicit in options: Evidence from an integrated time-series study. Journal of Financial Economics 63: 3–50

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Bondarenko, O., Longarela, I.R. A general framework for the derivation of asset price bounds: an application to stochastic volatility option models. Rev Deriv Res 12, 81–107 (2009). https://doi.org/10.1007/s11147-009-9032-7

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11147-009-9032-7

Keywords

- Option pricing

- Incomplete markets

- Good-deal bounds

- Benchmark stochastic discount factor

- Stochastic volatility model

- Continuous time