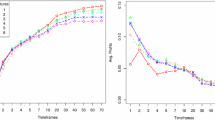

Abstract

Financially motivated kernels based on EURUSD currency data are constructed from limit order book volumes, commonly used technical analysis methods and canonical market microstructure models—the latter in the form of Fisher kernels. These kernels are used through their incorporation into support vector machines (SVM) to predict the direction of price movement for the currency over multiple time horizons. Multiple kernel learning is used to replicate the signal combination process that trading rules embody when they aggregate multiple sources of financial information. Significant outperformance relative to both the individual SVM and benchmarks is found, along with an indication of which features are the most informative for financial prediction tasks. An average accuracy of 55% is achieved when classifying the direction of price movement into one of three categories for a 200 s predictive time horizon.

Similar content being viewed by others

References

Alp O. S., Buyukbebeci E., Cekic A. I., Ozkurt F. Y., Taylan P., Weber G. W. (2011) CMARS and GAM & CQP—modern optimization methods applied to international credit default prediction. Journal of Computational and Applied Mathematics 235(16): 4639–4651

Appel, G. (2005). Technical analysis: Power tools for active investors. Financial Times.

Bach, F. R., Lanckriet, G. R. G., & Jordan, M. I. (2004). Multiple kernel learning, conic duality, and the smo algorithm. In ICML ’04: Proceedings of the twenty-first international conference on Machine learning, p. 6. ACM, New York, NY, USA. doi:10.1145/1015330.1015424.

BIS. (2007). Triennial central bank survey of foreign exchange and derivatives market activity in 2007. http://www.bis.org/publ/rpfxf07t.htm .

Blum A. L., Langley P. (1997) Selection of relevant features and examples in machine learning. Artificial Intelligence 97(1–2): 245–271

Bollinger J. A. (2001) Bollinger on Bollinger Bands. McGraw-Hill, New York

Cao L. (2003) Support vector machines experts for time series forecasting. Neurocomputing 51: 321–339

Chalup, S. K., & Mitschele, A. (2008). Kernel methods in finance. In Handbook on information technology in finance (pp. 655–687). Berlin: Springer.

Cortes, C., & Vapnik, V. (1995) Support vector networks. In Machine learning (pp. 273–297).

Cristianini N., Shawe-Taylor J. (2000) An introduction to support vector machines and other kernel-based learning methods. Cambridge University Press, New York, NY, USA

Dittmar, R., Neely, C. J., & Weller, P. (1996). Is technical analysis in the foreign exchange market profitable? A genetic programming approach. CEPR Discussion Papers 1480, C.E.P.R. Discussion Papers.

Easley D., O’Hara M. (1992) Time and the process of security price adjustment. Journal of Finance 47(2): 576–605

Easley, D., Engle, R. F., O’Hara, M., & Wu, L. (2002). Time-varying arrival rates of informed and uninformed trades. Technical report, EconWPA.

Engle R., Russell J. (1998) Autoregressive conditional duration: A new model for irregularly spaced transaction data. Econometrica 66: 1127–1162

Faith C. (2007) Way of the Turtle. McGraw-Hill Professional, New York

Fletcher, T., Redpath, F., & D’Alessandro, J. (2009). Machine learning in FX carry basket prediction. In Proceedings of the international conference of financial engineering (Vol. 2, pp. 1371–1375).

Fletcher, T., Hussain, Z., & Shawe-Taylor, J. (2010). Multiple kernel learning on the limit order book. In JMLR Proceedings (Vol. 11, pp. 167–174).

Gehler, P., & Nowozin, S. (2008). Infinite kernel learning.

Gestel, T. V., Suykens, J. A. K., Baestaens, D. E., Lambrechts, A., Lanckriet, G., Vandaele, B., Moor, B. D., & Vandewalle, J. (2001). Financial time series prediction using least squares support vector machines within the evidence framework. IEEE Transactions on Neural Networks, 12, 809–821.

Hasbrouk J. (2006) Empirical market microstructure: The institutions, economics, and econometrics of securities trading. Oxford University Press, Oxford, USA

Hazarika N., Taylor J. G. (2002) Predicting bonds using the linear relevance vector machine, chap. 17. Springer, Berlin, pp 145–155

Huang, S. C., & Wu, T. K. (2006). Wavelet-based relevance vector machines for stock index forecasting. In International joint conference on neural networks (IJCNN) (pp. 603–609).

Huang S. C., Wu T. K. (2008) Combining wavelet-based feature extractions with relevance vector machines for stock index forecasting. Expert Systems 25: 133–149

Huang W., Nakamori Y., Wang S. Y. (2005) Forecasting stock market movement direction with support vector machine. Computers & Operations Research 32(10): 2513–2522

Jaakkola, T., & Haussler, D. (1998). Exploiting generative models in discriminative classifiers. In Advances in neural information processing systems (Vol. 11, pp. 487–493). Cambridge: MIT Press.

Jondeau, E., Perilla, A., & Rockinger, G. M. (2008). Optimal liquidation strategies in illiquid markets. SSRN eLibrary.

Kaufman P. (2005) The new trading systems and methods. Wiley, New York

Kim K. (2003) Financial time series forecasting using support vector machines. Neurocomputing 55: 307–319

Kuan C. M., Liu T. (1995) Forecasting exchange rates using feedforward and recurrent neural networks. Journal of Applied Econometrics 10(4): 347–364

Lagarias J.C., Reeds J.A., Wright M.H., Wright P.E. (1998) Convergence properties of the nelder–mead simplex method in low dimensions. SIAM Journal on Optimization 9: 112–147. doi:10.1137/S1052623496303470

Lancaster T. (1992) The econometric analysis of transition data. Cambridge University Press, Cambridge

Lanckriet G.R.G., De Bie T., Cristianini N., Jordan M.I., Noble W.S. (2004) Astatistical framework for genomic data fusion. Bioinformatics 20(16): 2626–2635. doi:10.1093/bioinformatics/bth294

LeBaron, B. (1996). Technical trading rule profitability and foreign exchange intervention. NBER Working Papers 5505, National Bureau of Economic Research, Inc.

Linnainmaa, J., & Rosu, I. (2008). Time series determinants of liquidity in a limit order market. SSRN eLibrary.

Lo, A., MacKinlay, A., & Zhang, J. (1997). Econometric models of limit-order executions. SSRN eLibrary.

Lui Y. H., Mole D. (1998) The use of fundamental and technical analyses by foreign exchange dealers: Hong kong evidence. Journal of International Money and Finance 17(3): 535–545

Luss, R., & d’Aspremont, A. (2009). Predicting abnormal returns from news using text classification.

Mainardi F., Gorenflo R., Scalas E. (2004) A fractional generalization of the poisson processes. Vietnam Journal of Mathematics 32: 53–64

Mainardi F., Raberto M., Gorenflo R., Scalas E. (2000) Fractional calculus and continuous-time finance II: The waiting-time distribution. Physica A: Statistical Mechanics and its Applications 287: 468

Marney, C. (2010). Building robust FX trading systems. FX Trader Magazine.

Neely, C. J. (1998). Technical analysis and the profitability of U.S. foreign exchange intervention. Review (Jul), pp. 3–17.

Neely, C. J., & Weller, P. A. (2001). Intraday technical trading in the foreign exchange market. Working Papers 1999-016, Federal Reserve Bank of St. Louis.

Neely C. J., Weller P. A., Ulrich J. M. (2009) The adaptive markets hypothesis: Evidence from the foreign exchange market. Journal of Financial and Quantitative Analysis 44(02): 467–488

Özöğür-Akyüz, S., & Weber, G. W. (2009). Modelling of kernel machines by infinite and semi-infinite programming. In A. Halim Hakim, P. Vasant, & N. Barsoum (Eds.), American Institute of Physics Conference Series (vol. 1159, pp. 306–313).

Özöğür-Akyüz S., Weber G. W. (2010) On numerical optimization theory of infinite kernel learning. Journal of Global Optimization 48: 215–239

Parlour C., Seppi D. (2008) Limit order markets: A survey. In: Boot A., Thakor A. (eds) Handbook of financial intermediation and banking, chap. 3. Elsevier Science, Amsterdam, The Netherlands, pp 61–96

Perez-cruz F., Afonso-rodriguez J., Giner J. (2003) Estimating garch models using support vector machines. Quantitative Finance 3(3): 163–172

Politi M., Scalas E. (2007) Activity spectrum from waiting-time distribution. Physica A: Statistical Mechanics and its Applications 383(1): 43

Politi M., Scalas E. (2008) Fitting the empirical distribution of intertrade durations. Physica A: Statistical Mechanics and its Applications 387(8-9): 2025

Rakotomamonjy A., Bach F., Canu S., Grandvalet Y. (2008) SimpleMKL. Journal of Machine Learning Research 9: 2491–2521

Rydberg T., Shephard N. (2000) A modelling framework for the prices and times of trades made on the New York stock exchange. Cambridge University Press, Cambridge

Shadbolt, J., Taylor, J. G. (eds) (2002) Neural networks and the financial markets: Predicting, combining and portfolio optimisation. Springer, London, UK

Tay F., Cao L. (2001) Application of support vector machines in financial time series forecasting. Omega 29: 309–317

Tay F., Cao L. (2002) Modified support vector machines in financial time series forecasting. Neurocomputing 48: 847–861

Taylan P., Weber G. W., Beck A. (2007) New approaches to regression by generalized additive models and continuous optimization for modern applications in finance, science and technology. Optimization 56(5–6): 675–698

Tino, P. Nikolaev, N., & Yao, X. (2005). Volatility forecasting with sparse bayesian kernel models. In Proceedings of the 4th International Conference on Computational Intelligence in Economics and Finance, Salt Lake City, UT (pp. 1150–1153).

Ullrich, C., Seese, D., & Chalup, S. (2007). Foreign exchange trading with support vector machines. In Advances in data analysis (pp. 539–546). Berlin: Springer.

Walczak S. (2001) An empirical analysis of data requirements for financial forecasting with neural networks. Journal of Management Information Systems 17(4): 203–222

Wang L., Zhu J. (2010) Financial market forecasting using a two-step kernel learning method for the support vector regression. Annals of Operation Research 174: 103–120

Wilder J. W. (1978) New Concepts in Technical Trading Systems. Trend Research, McLeansville, NC

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Fletcher, T., Shawe-Taylor, J. Multiple Kernel Learning with Fisher Kernels for High Frequency Currency Prediction. Comput Econ 42, 217–240 (2013). https://doi.org/10.1007/s10614-012-9317-z

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10614-012-9317-z