Abstract

Improved implementations of previously suggested methods for constructing bootstrap prediction intervals for the self-exciting threshold autoregressive model are presented. The simulation results are compared with those reported by Li (2011). It is found that better estimates of actual coverage rates are obtained using the improved version of the methods.

Similar content being viewed by others

Notes

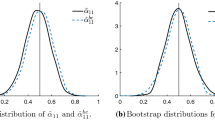

The impact may be not so large here, as the sample averages of the residuals from regressions without the constant are close to zero. E.g., for the cases reported in the three panels of Fig. 1, the means of residual sample averages calculated over 1,000 Monte Carlo replications are \(-\)0.029, \(-\)0.031, and \(-\)0.031, respectively. The corresponding standard deviations are equal to 0.085, 0.087, and 0.092.

The stationarity correction seems relevant as it was required relatively often for specific DGPs. For example, for the cases studied in Fig. 4, the means and the standard deviations (in parentheses) of the frequency of application of the bias correction was equal to 6.3 % (9.7 %) for \(\beta _{11}=0.2\), 19.25 % (13.15 %) for \(\beta _{11}=0.8\), and 13.75 % (13.9 %) for \(\beta _{11}=1.0.\)

References

Alonso AM, Peña D, Romo J (2006) Introducing model uncertainty by moving blocks bootstrap. Stat Pap 47(2):167–179

Clements MP, Kim JH (2007) Bootstrap prediction intervals for autoregressive time series. Comput Stat Data Anal 51(7):3580–3594

Clements MP, Taylor N (2001) Bootstrapping prediction intervals for autoregressive models. Int J Forecast 17(2):247–267

De Gooijer JG, Hyndman RJ (2006) 25 years of time series forecasting. Int J Forecast 22(3):443–473

Kapetanios G (2000) Small sample properties of the conditional least squares estimator in SETAR models. Econ Lett 69(3):267–276

Kilian L (1998) Small-sample confidence intervals for impulse response functions. Rev Econ Stat 80(2):218–230

Kim JH (2001) Bootstrap-after-bootstrap prediction intervals for autoregressive models. J Bus Econ Stat 19(1):117–128

Li J (2011) Bootstrap prediction intervals for SETAR models. Int J Forecast 27(2):320–332

Lütkepohl H (2013) Reducing confidence bands for simulated impulse responses. Stat Pap 54(4):1131–1145

Stine RA (1987) Estimating properties of autoregressive forecasts. J Am Stat Assoc 82(400):1072– 1078

Staszewska-Bystrova A (2011) Bootstrap prediction bands for forecast paths from vector autoregressive models. J Forecast 30(8):721–735

Thombs LA, Schucany WR (1990) Bootstrap prediction intervals for autoregression. J Am Stat Assoc 85(410):486–492

Acknowledgments

Support from the MNiSW/DAAD PPP Grant (56268818) and the National Science Center, Poland (NCN) through MAESTRO 4: DEC–2013/08/A/HS4/00612 are gratefully acknowledged.

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Staszewska-Bystrova, A., Winker, P. Improved bootstrap prediction intervals for SETAR models. Stat Papers 57, 89–98 (2016). https://doi.org/10.1007/s00362-014-0643-1

Received:

Revised:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s00362-014-0643-1